Embed Size (px)

Citation preview

1

CHAPTER FIVECHAPTER FIVEMeasuring And Evaluating Measuring And Evaluating

The Performance Of The Performance Of Banks And Their Principal Banks And Their Principal

CompetitorsCompetitors

2

Determining the Bank’s Long-Determining the Bank’s Long-range Objectivesrange Objectives

A fair evaluation of any bank’s performance should start by evaluating whether it has been able to achieve its objectives.

3

Maximizing the Value of the Maximizing the Value of the FirmFirm

If the stock of a bank fails to rise in value, current investors will start to sell the stocks and the bank may face difficulty in raising new capital for future growth.

Performance based classification of banks

Category Position

A Best Performer

B Moderate performer

C Average Performer

D Below Average performer

E Losing and Bad performer

CAMELS RATINGS

The components of a bank's condition that are assessed

(C) Capital adequacy, (A) Asset quality, (M) Management Capability, (E) Earnings, (L) Liquidity and (S) Sensitivity to Market Risk

6

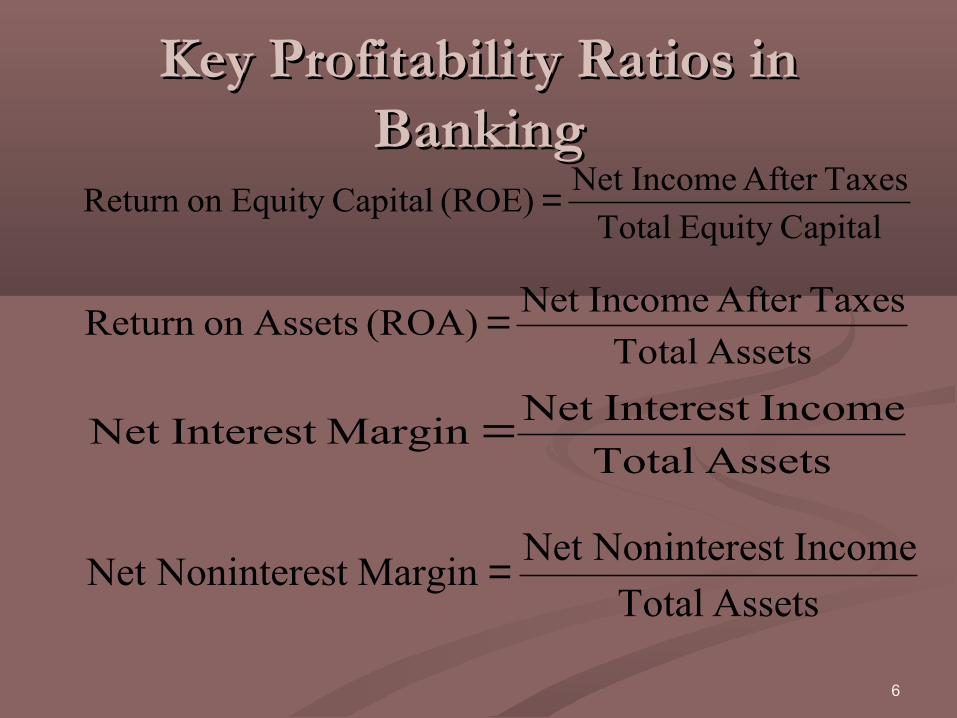

Key Profitability Ratios in Key Profitability Ratios in BankingBanking

CapitalEquity Total

TaxesAfter IncomeNet (ROE) CapitalEquity on Return =

Assets Total

TaxesAfter IncomeNet (ROA) Assetson Return =

Assets Total

IncomeInterest Net Margin Interest Net =

Assets Total

Incomet NoninteresNet Margin t NoninteresNet =

7

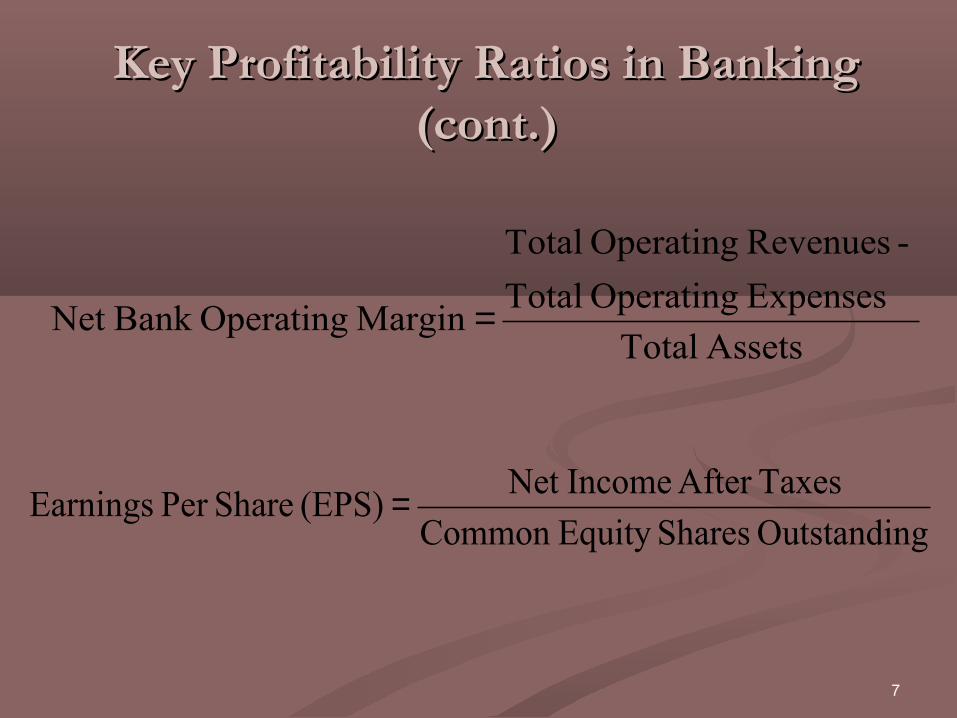

Key Profitability Ratios in Banking Key Profitability Ratios in Banking (cont.)(cont.)

Assets Total

Expenses Operating Total

- Revenues Operating Total

Margin OperatingBank Net =

gOutstandin SharesEquity Common

TaxesAfter IncomeNet (EPS) SharePer Earnings =

8

Bank RisksBank Risks

Credit RiskCredit RiskLiquidity RiskLiquidity RiskMarket RiskMarket Risk Interest Rate RiskInterest Rate RiskEarnings RiskEarnings RiskCapital RiskCapital Risk

9

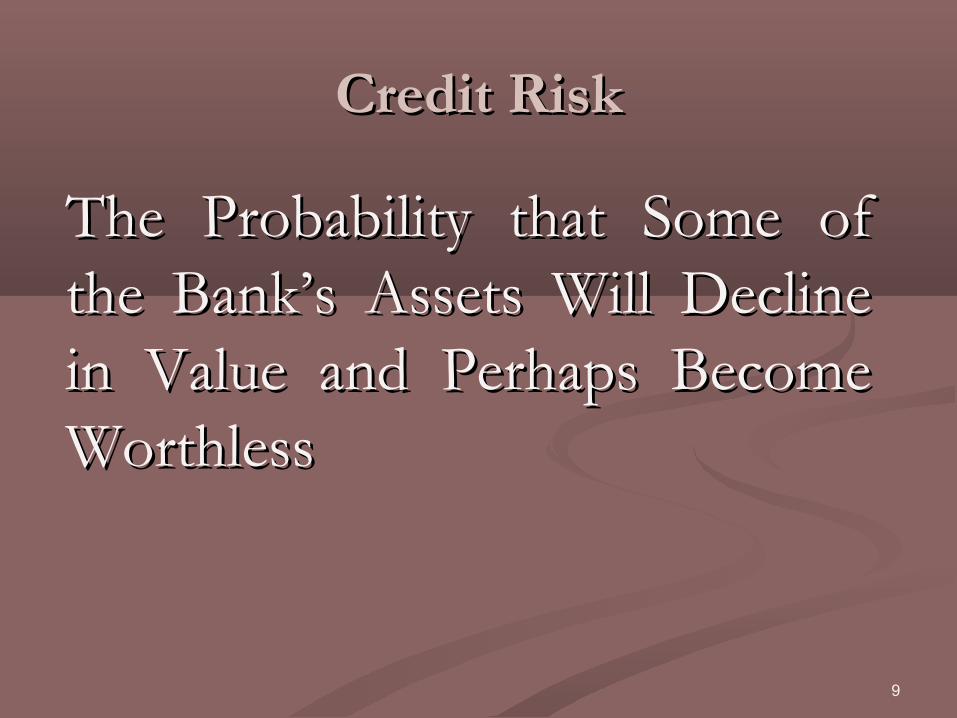

Credit RiskCredit Risk

The Probability that Some of The Probability that Some of the Bank’s Assets Will Decline the Bank’s Assets Will Decline in Value and Perhaps Become in Value and Perhaps Become WorthlessWorthless

10

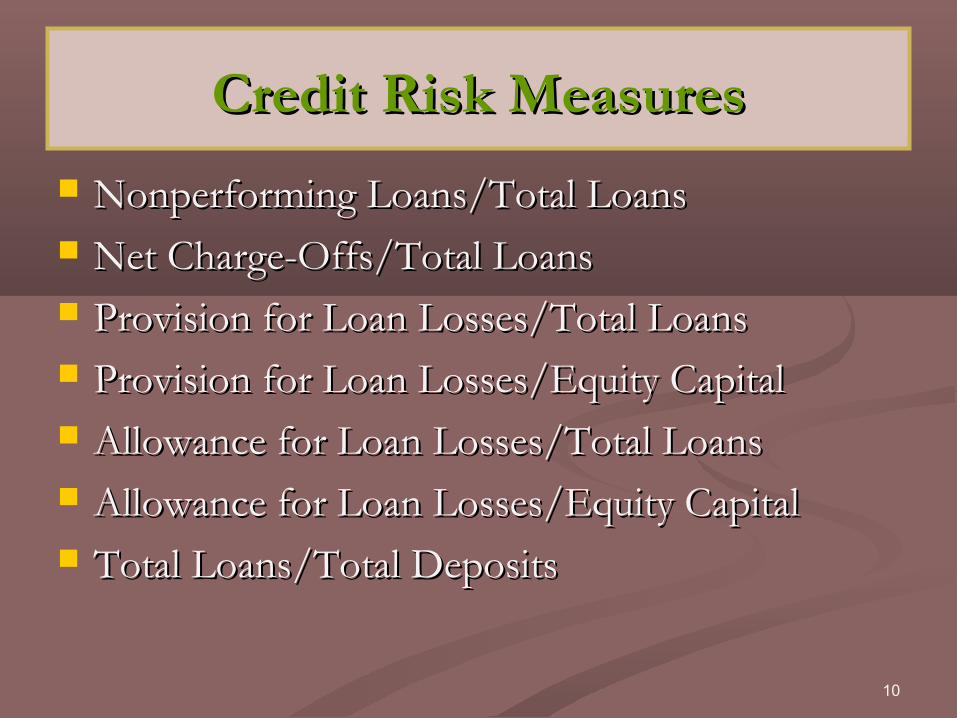

Credit Risk MeasuresCredit Risk Measures

Nonperforming Loans/Total LoansNonperforming Loans/Total Loans Net Charge-Offs/Total LoansNet Charge-Offs/Total Loans Provision for Loan Losses/Total LoansProvision for Loan Losses/Total Loans Provision for Loan Losses/Equity CapitalProvision for Loan Losses/Equity Capital Allowance for Loan Losses/Total LoansAllowance for Loan Losses/Total Loans Allowance for Loan Losses/Equity CapitalAllowance for Loan Losses/Equity Capital Total Loans/Total DepositsTotal Loans/Total Deposits

11

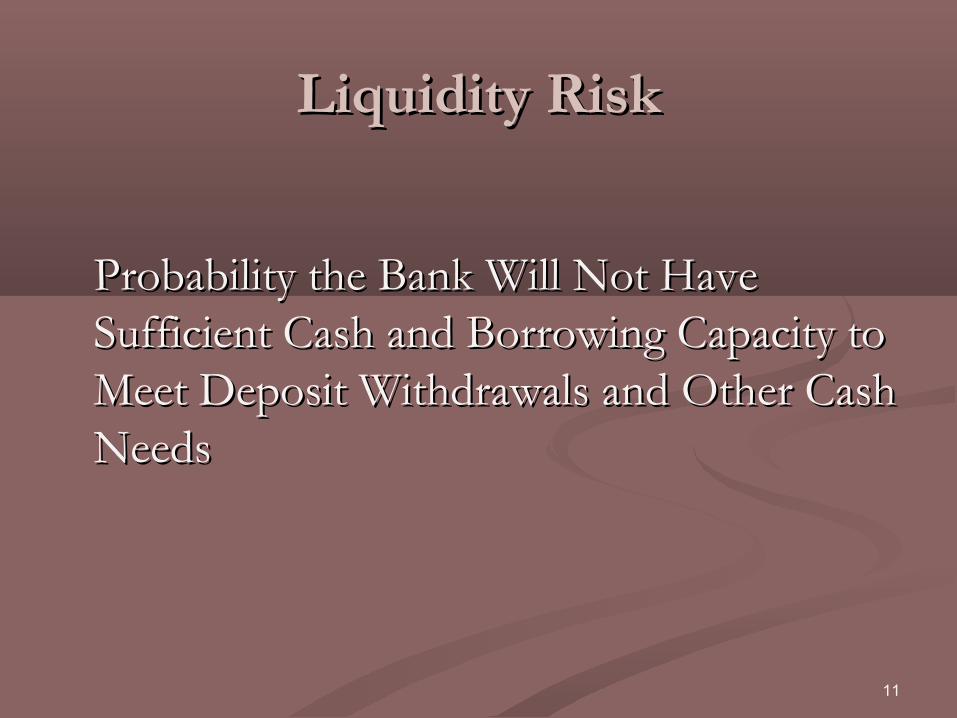

Liquidity RiskLiquidity Risk

Probability the Bank Will Not Have Probability the Bank Will Not Have Sufficient Cash and Borrowing Capacity to Sufficient Cash and Borrowing Capacity to Meet Deposit Withdrawals and Other Cash Meet Deposit Withdrawals and Other Cash NeedsNeeds

12

Liquidity Risk MeasuresLiquidity Risk Measures

Purchased Funds/Total AssetsPurchased Funds/Total Assets Net Loans/Total AssetsNet Loans/Total Assets Cash and Due from Banks/Total AssetsCash and Due from Banks/Total Assets Cash and Government Securities/Total Cash and Government Securities/Total

AssetsAssets

13

Market RiskMarket Risk

Probability of the Market Value Probability of the Market Value of the Bank’s Investment of the Bank’s Investment Portfolio Declining in Value Portfolio Declining in Value Due to a Rise in Interest RatesDue to a Rise in Interest Rates

14

Market Risk MeasuresMarket Risk Measures

Book-Value of Assets/ Market Value of Book-Value of Assets/ Market Value of AssetsAssets

Book-Value of Equity/ Market Value of Book-Value of Equity/ Market Value of EquityEquity

Book-Value of Bonds/Market Value of Book-Value of Bonds/Market Value of BondsBonds

Market Value of Preferred Stock and Market Value of Preferred Stock and Common StockCommon Stock

15

Interest Rate RiskInterest Rate Risk

The Danger that Shifting Interest The Danger that Shifting Interest Rates May Adversely Affect a Rates May Adversely Affect a Bank’s Net Income, the Value of Bank’s Net Income, the Value of its Assets or Equityits Assets or Equity

16

Interest Rate Risk MeasuresInterest Rate Risk Measures

Interest Sensitive Interest Sensitive Assets/Interest Sensitive Assets/Interest Sensitive LiabilitiesLiabilities

Uninsured Deposits/Total Uninsured Deposits/Total DepositsDeposits

17

Earnings RiskEarnings Risk

The Risk to the Bank’s Bottom The Risk to the Bank’s Bottom Line – Its Net Income After All Line – Its Net Income After All ExpensesExpenses

18

Earnings Risk MeasuresEarnings Risk Measures

Standard Deviation of Net IncomeStandard Deviation of Net IncomeStandard Deviation of ROEStandard Deviation of ROEStandard Deviation of ROAStandard Deviation of ROA

19

Capital RiskCapital Risk

Probability of the Value of the Probability of the Value of the Bank’s Assets Declining Below the Bank’s Assets Declining Below the Level of its Total Liabilities. The Level of its Total Liabilities. The Probability of the Bank’s Long Run Probability of the Bank’s Long Run SurvivalSurvival

20

Capital Risk MeasuresCapital Risk Measures

Stock Price/Earnings Per ShareStock Price/Earnings Per ShareEquity Capital/Total AssetsEquity Capital/Total AssetsPurchased Funds/Total Purchased Funds/Total

LiabilitiesLiabilitiesEquity Capital/Risk AssetsEquity Capital/Risk Assets

Indicators of successful banks

Indicators of Problem banks

Dealing with failed banks

The three ways as follows; Liquidation Merger Nationalization