Embed Size (px)

Citation preview

Canada Banking Sector –Government Policies – Risk and

Threats

By: Paul Young, CPA, CGA

Disclaimer

• This presentation is one opinion of the banking sector in Canada

Paul Young - Presenter

Bio

• CPA/CGA

• 25 years of experience in Academia, Industry and Financial solutions

• Youtube Channel -https://www.youtube.com/channel/UCAArky1bAXPSuV2NLtUnyLg

Agenda

• What is the Bank Act

• What does the Bank Act regulate

• What is Basel Reporting

• Do Canadian Banks follow Basel Reporting

• Accounting Rules

• Liberal Party proposed changes

• Banking Sector Analysis

• Issues facing the Banking Sector

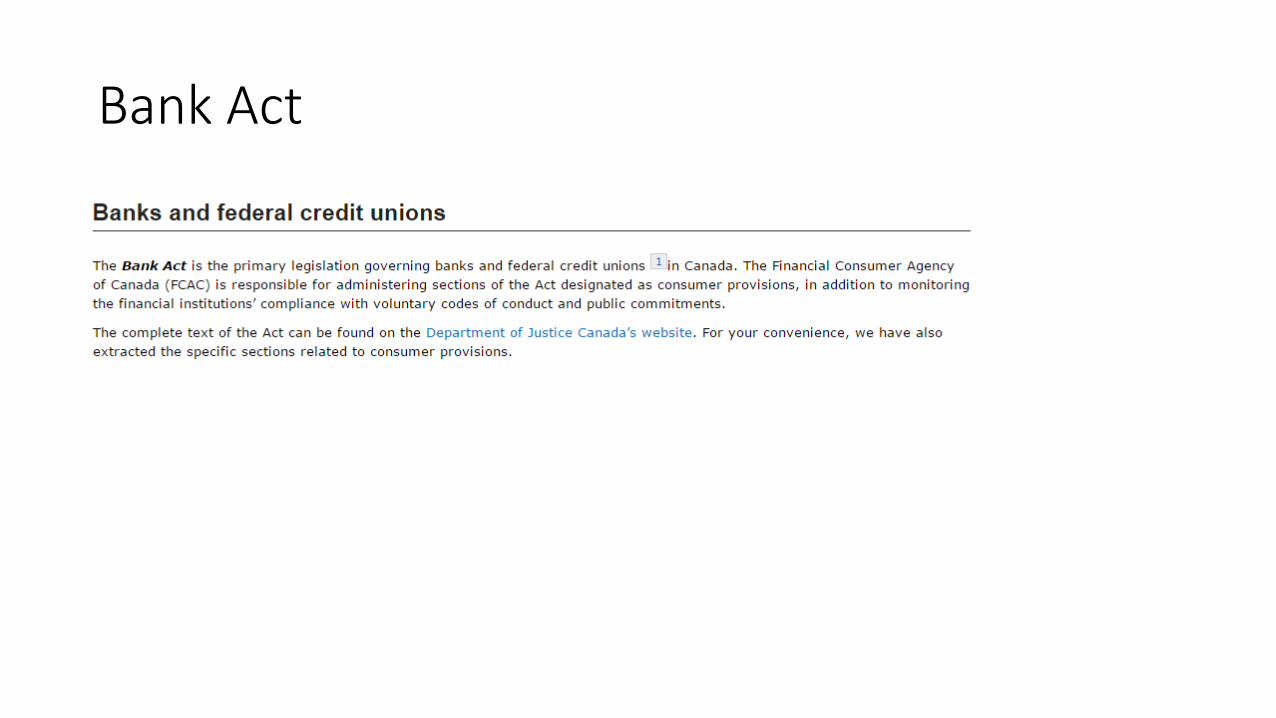

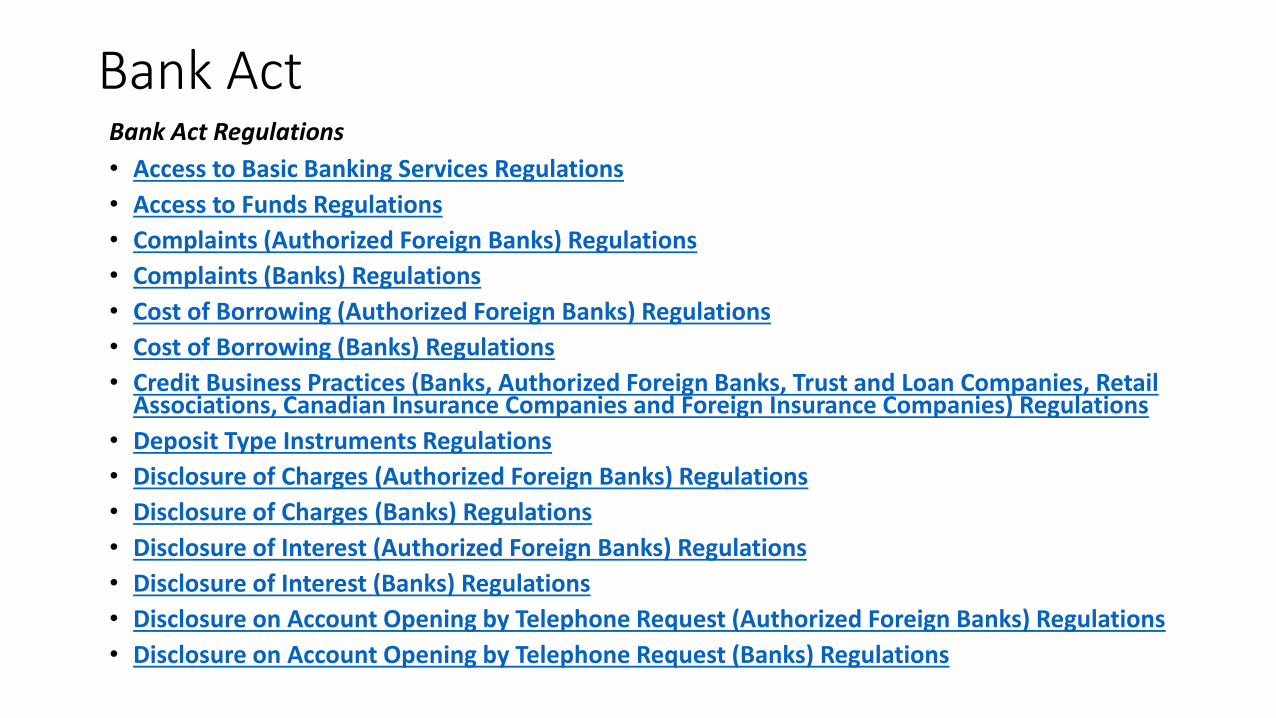

Bank Act

Bank ActBank Act Regulations

• Access to Basic Banking Services Regulations

• Access to Funds Regulations

• Complaints (Authorized Foreign Banks) Regulations

• Complaints (Banks) Regulations

• Cost of Borrowing (Authorized Foreign Banks) Regulations

• Cost of Borrowing (Banks) Regulations

• Credit Business Practices (Banks, Authorized Foreign Banks, Trust and Loan Companies, Retail Associations, Canadian Insurance Companies and Foreign Insurance Companies) Regulations

• Deposit Type Instruments Regulations

• Disclosure of Charges (Authorized Foreign Banks) Regulations

• Disclosure of Charges (Banks) Regulations

• Disclosure of Interest (Authorized Foreign Banks) Regulations

• Disclosure of Interest (Banks) Regulations

• Disclosure on Account Opening by Telephone Request (Authorized Foreign Banks) Regulations

• Disclosure on Account Opening by Telephone Request (Banks) Regulations

Bank ActBank Act Regulations

• Electronic Documents (Banks) Regulations

• Mortgage Insurance Disclosure (Banks, Authorized Foreign Banks, Trust and Loan Companies, Retail Associations, Canadian Insurance Companies and Canadian Societies) Regulations

• Negative Option Billing Regulations

• Notice of Branch Closure (Banks) Regulations

• Notices of Deposit Restrictions (Authorized Foreign Banks) Regulations

• Notices of Uninsured Deposits Regulations (Banks)

• Prepaid Payment Products Regulations

• Prescribed Deposits (Authorized Foreign Banks) Regulations

• Prescribed Deposits (Banks without Deposit Insurance) Regulations

• Prescribed Products Regulations

• Principal Protected Notes Regulations

• Prospectus (Federal Credit Unions) Regulations

• Public Accountability Statements (Banks, Insurance Companies, Trust and Loan Companies) Regulations

• Registered Products Regulations

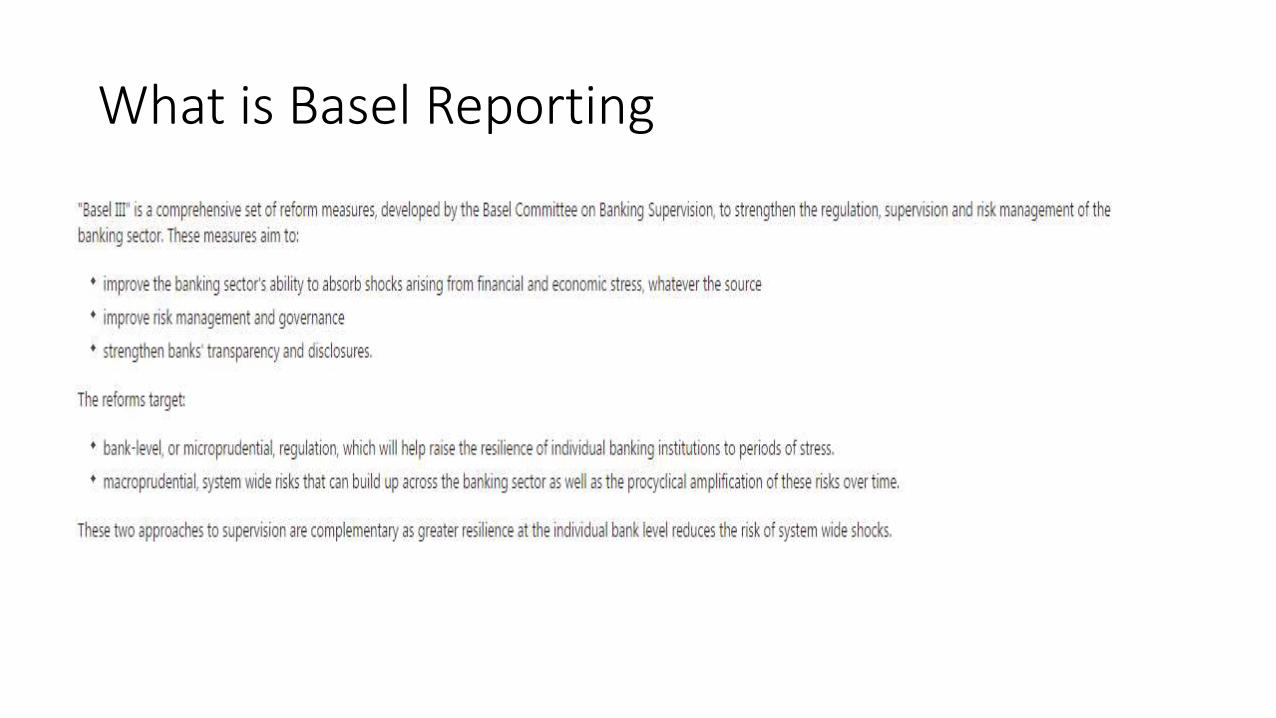

What is Basel Reporting

Do Canadian Banks file Basel Reporting• Basel III is a framework that sets out global regulatory rules for bank capital

and liquidity. These rules were originally published in December 2010 in response to the global financial crisis and are subject to ongoing review and updates.

• The phase-in of Basel III capital rules began in 2013. Canada implemented these changes in January 2013, well ahead of many other countries and well ahead of the Basel III timeline. The phase-in of Basel III’s liquidity rules began in 2015.

• Basel III was developed and agreed to by members of the Basel Committee on Banking Supervision. This is a longstanding committee of the Bank for International Settlements (BIS) that is mandated to review and develop banking guidelines and supervisory standards at a global level.

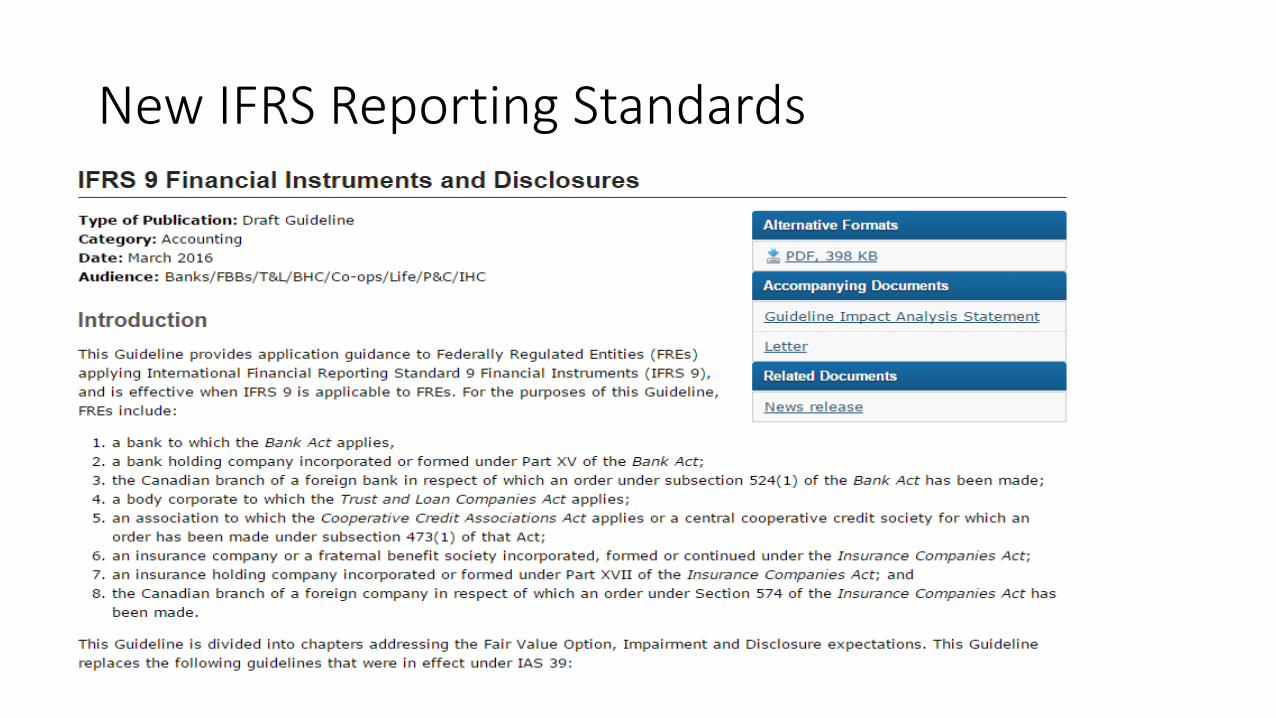

New IFRS Reporting Standards

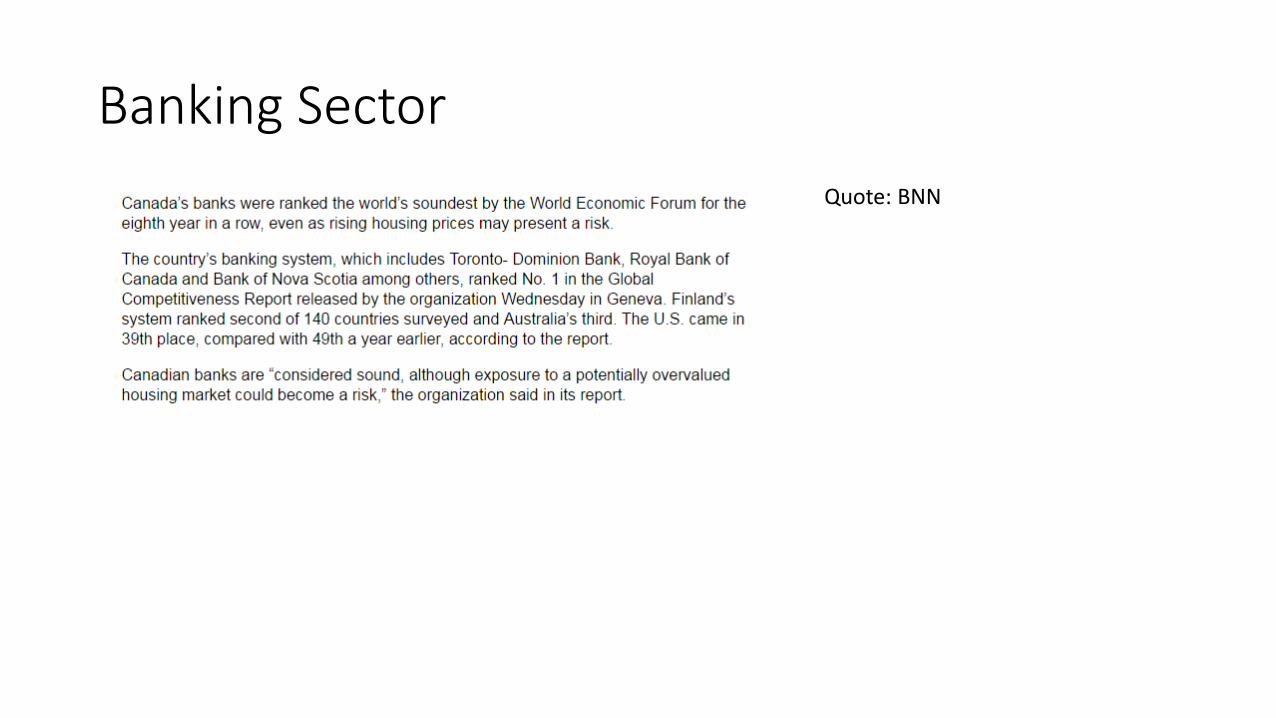

Banking Sector

Quote: BNN

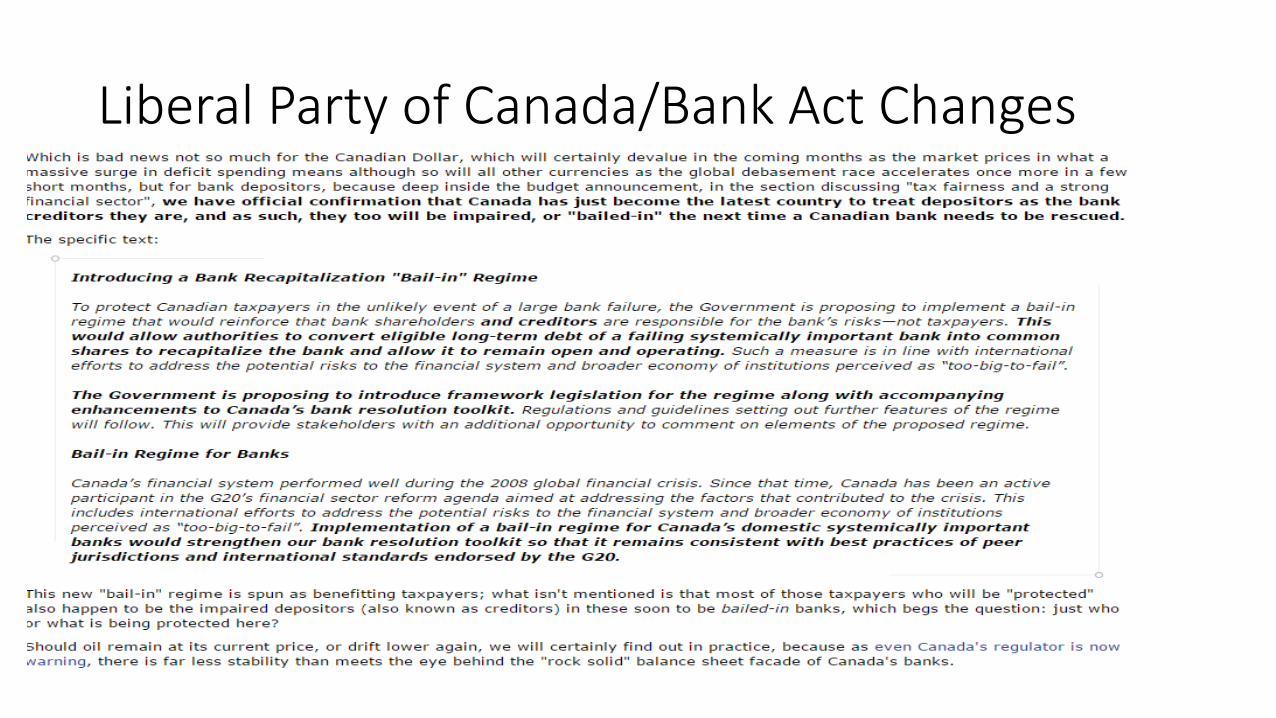

Liberal Party of Canada/Bank Act Changes

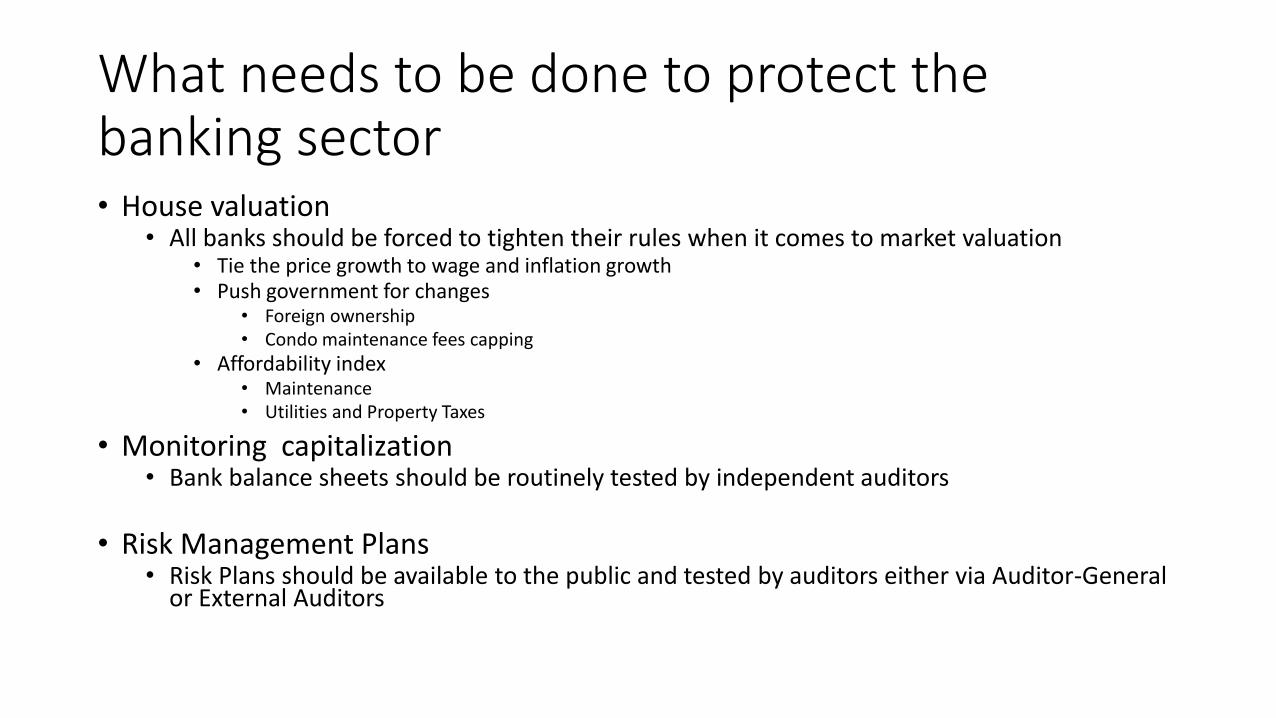

What needs to be done to protect the banking sector• House valuation

• All banks should be forced to tighten their rules when it comes to market valuation• Tie the price growth to wage and inflation growth• Push government for changes

• Foreign ownership• Condo maintenance fees capping

• Affordability index• Maintenance• Utilities and Property Taxes

• Monitoring capitalization• Bank balance sheets should be routinely tested by independent auditors

• Risk Management Plans• Risk Plans should be available to the public and tested by auditors either via Auditor-General

or External Auditors