Embed Size (px)

Citation preview

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Capital Adequacy – The Basel-II Overview

Module D: Balance Sheet Management

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

CAIIB – SUPER NOTES

Bank Financial Management: Capital Adequacy – The Basel-II Overview

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Contents

Coverage:

1. Introduction

2. Basel II – Revised

Framework

3. Scope of Application

4. Pillar 1: Minimum Capital

Requirements

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

INTRODUCTION

1.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Introduction

• BCBS released the “International Convergence of Capital

Measurement and Capital Standards: A Revised Framework”

on June 26, 2004

• Updated in Nov 2005 to include trading activities and the

treatment of double default effects

• Apply to ‘internationally active’ banks

• In Europe it is applicable to all banks

• In European Union it is also applicable to financial institutions

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

BASEL II – REVISED FRAMEWORK

2.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

The Revised Framework

• Adoption of stronger risk management practices by Banks

• Greater use of assessment of Risk provided by Bank’s internal systems as

inputs to capital calculations

• Demands capital allocation for operational risk

• National regulators are free to set higher standards

• Provides incentives for banks to invest and increase the sophistication of

their internal risk management capabilities in order to gain reductions in

capital

• Aligns regulatory capital with Bank’s risk profiles

• Recognizes the role of home country supervisors in implementation

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

The Three Pillars

• Consists of three mutually reinforcing pillars:

– Minimum Capital Requirements

– Supervisory Review of Capital Adequacy

– Market Discipline

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

The Three Pillars

Pillar I: Minimum Capital Requirement

Pillar I: Minimum Capital Requirement

Capital for Credit Risk

•Standardised Approach

•Internal Rating Based Approaches

•Foundation Approach

•Advanced Approach

Capital for Credit Risk

•Standardised Approach

•Internal Rating Based Approaches

•Foundation Approach

•Advanced Approach

Capital for Market Risk

•Standardised Method

•Maturity Method

•Duration Method

Capital for Market Risk

•Standardised Method

•Maturity Method

•Duration Method

Capital for Operational Risk

•Basic Indicator Approach

•Standardised Approach

•Advanced Measurement Approach

Capital for Operational Risk

•Basic Indicator Approach

•Standardised Approach

•Advanced Measurement Approach

Pillar II: Supervisory Review

Pillar II: Supervisory Review

Evaluate Risk Assessment Evaluate Risk Assessment

Ensure soundness and integrity of Bank’s internal processes to assess the adequacy of capital

Ensure soundness and integrity of Bank’s internal processes to assess the adequacy of capital

Ensure maintenance of minimum capital with PCA for

shortfall

Ensure maintenance of minimum capital with PCA for

shortfall

Prescribe differential capital, where necessary i.e., where the

internal processes are slack

Prescribe differential capital, where necessary i.e., where the

internal processes are slack

Pillar III: Market Discipline

Pillar III: Market Discipline

Enhanced Disclosures Enhanced Disclosures

Core disclosures and Supplementary Disclosures

Core disclosures and Supplementary Disclosures

Disclosure Frequency: Half Yearly

Disclosure Frequency: Half Yearly

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

SCOPE OF APPLICATION

3.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Scope of Application

• All Commercial Banks (except Local Area Banks and Regional

Rural Banks)

• At solo level (global position) as well as consolidated level

• Group companies engaged in insurance business and

businesses not pertaining to financial services may be

excluded

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Applicable Approaches

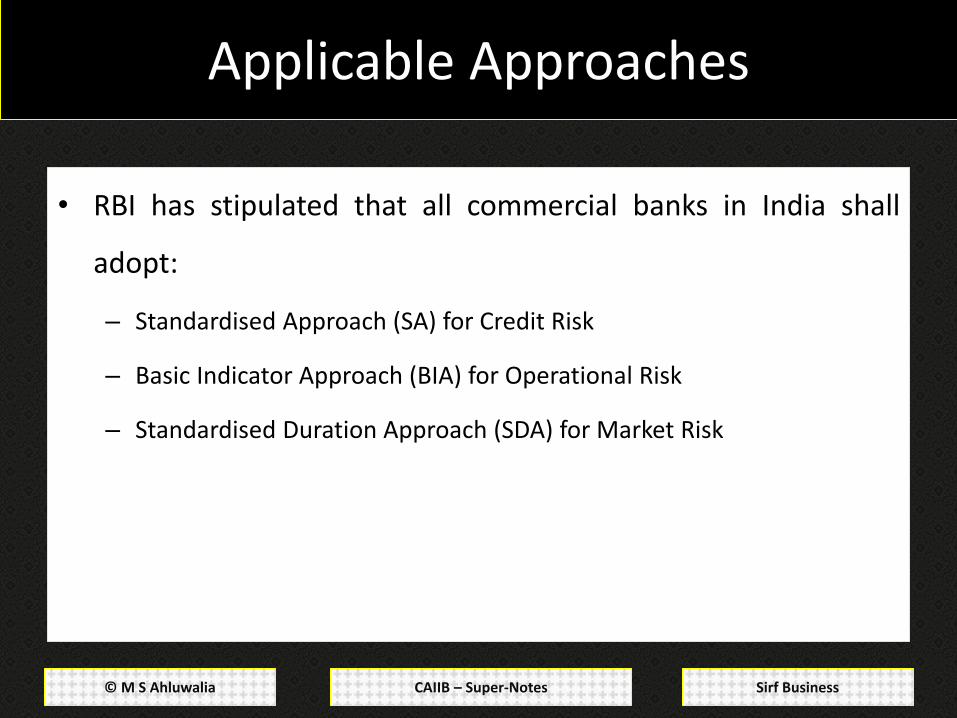

• RBI has stipulated that all commercial banks in India shall

adopt:

– Standardised Approach (SA) for Credit Risk

– Basic Indicator Approach (BIA) for Operational Risk

– Standardised Duration Approach (SDA) for Market Risk

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

MINIMUM CAPITAL REQUIREMENTS

4.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

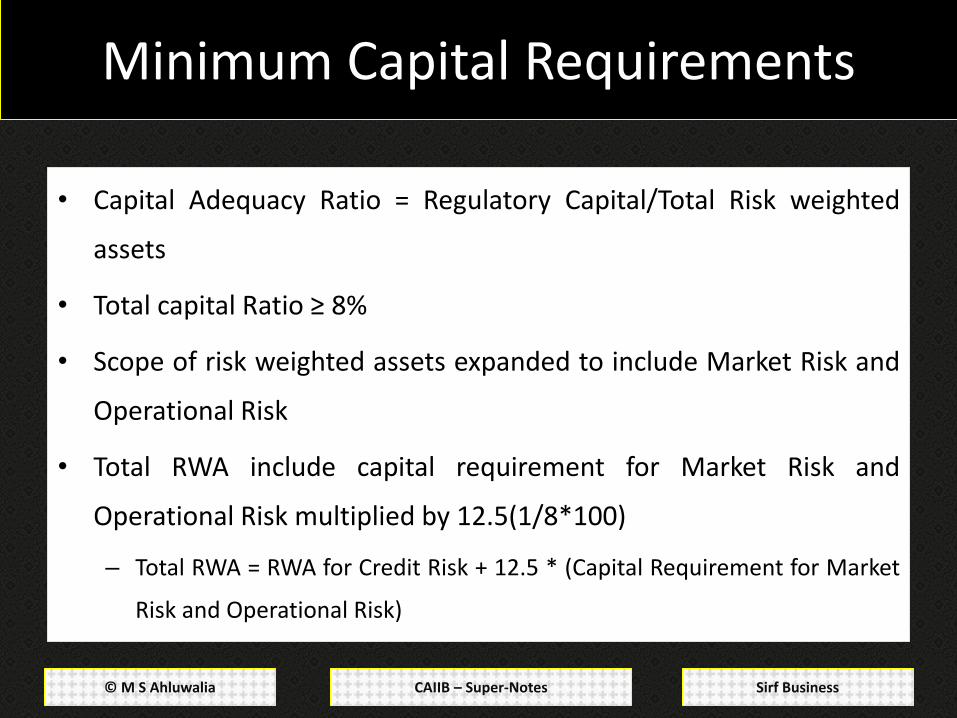

Minimum Capital Requirements

• Capital Adequacy Ratio = Regulatory Capital/Total Risk weighted

assets

• Total capital Ratio ≥ 8%

• Scope of risk weighted assets expanded to include Market Risk and

Operational Risk

• Total RWA include capital requirement for Market Risk and

Operational Risk multiplied by 12.5(1/8*100)

– Total RWA = RWA for Credit Risk + 12.5 * (Capital Requirement for Market

Risk and Operational Risk)

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Capital – The Three Tiers

Tier I or Core Capital

Tier II or Supplemental

Capital

Tier III Capital

• Paid up Capital

• Free Reserves

• Unallocated surpluses

• Less specified deductions

• Subordinated debt of more than 5 years maturity

• Loan loss reserves

• Revaluation reserves

• Investment fluctuation reserves

• Limited life preference shares

• Short Term subordinated debt (maturity < 2 yrs)

• Limited to 250% of bank’s Tier I capital required to support market risk

• Presently not allowed by RBI

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Do you have any questions or queries or some feedback to give?

Just mark an email to [email protected]

CAIIB – Super-Notes © M S Ahluwalia Sirf Business For more Super-Notes: Click Here

M S Ahluwalia, amongst other things, is a visual artist, blogger,

blog designer and of course an MBA and Banker from New

Delhi, India.

To know more about him you may visit his blog-site: Estudiante De La Vida