Embed Size (px)

Citation preview

March 13, 2017

Report #9Lithium in NWT and Québec, Frac Sand in British Columbia

Booming Frac Sand Markets Golden for 92 ResourcesWhile continuing to focus and advance its flagship Hidden Lake Lithium Pro-ject near Yellowknife in the Northwest Territories, 92 Resources Corp. today announced its plans to start mapping, sampling and drilling its Golden Frac Sand Property near Golden in British Columbia, Canada.

92 Resources also announced today that it has expanded its Golden Frac Sand Property by almost 300%, adding 2,404 hectares to the original 808 hectares Zim Frac Property. The company believes that significant value can be unlocked to in-crease shareholder value as the property represents a significantly undervalued asset given its potential to host a large, high quality frac sand deposit.

Given the company’s relatively small market capitalization of around $6 million CAD, it is easy to see the savvy reasoning behind this.

A few weeks ago, ASX-listed Heemskirk Consolidated Ltd. was the subject of a

>$42 million AUD takeover bid from Sydney-based Taurus Resources Fund No. 2via its newly created private Canadian subsidiary Northern Silica Corp. Heemskirk is the owner of the Moberly Silica Mine, which covers a portion of the Mount Wilson Formation.

92 Resources’ Golden Frac Sand Property is not only adjacent and contiguous with Heemskirk’s quarry-style mine but also covers some 18 km strike length of the favourable Mount Wilson Formation, which hosts high purity, white quartzite with a high friability. Adrian Lamoureux (President and CEO of 92 Resources) commented today:

“Domestic or western Canadian Frac Sand deposit with suitable quality would benefit from more advantageous transportation and exchange rate costs over foreign competitors. We believe these to be important factors in the recent takeover of the neighboring Moberly Silica Sand Mine, which is slated for production in 3rd quarter of 2017.“

Company Details

92 Resources Corp.#1400 – 1111 West Georgia StreetVancouver, BC, Canada V6E 4M6Phone: +1 778 945 2950 Email: [email protected] www.92resources.com

Shares Issued & Outstanding: 45,171,623

Canadian Symbol (TSX.V): NTYCurrent Price: $0.13 CAD (03/10/2017)Market Capitalization: $6 Million CAD

German Symbol / WKN: R9G2 / A11575Current Price: €0.086 EUR (03/10/2017)Market Capitalization: €4 Million EUR

Chart Canada (TSX.V)

Chart Germany (Tradegate)

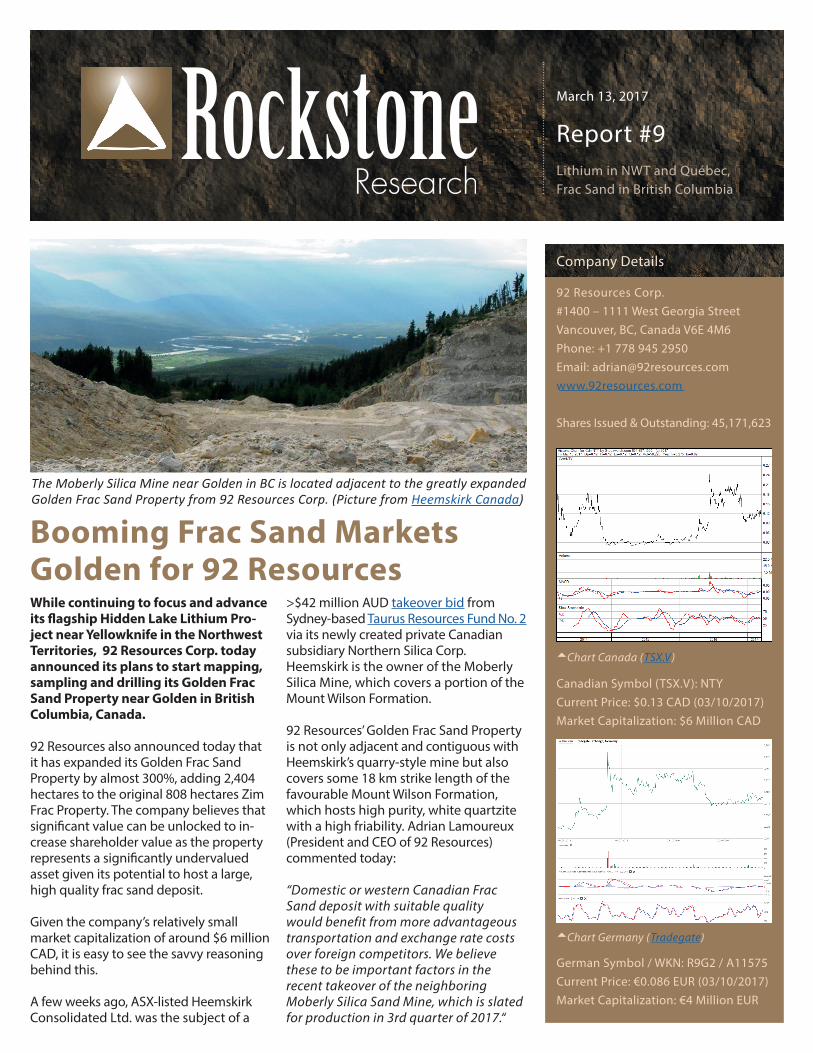

The Moberly Silica Mine near Golden in BC is located adjacent to the greatly expandedGolden Frac Sand Property from 92 Resources Corp. (Picture from Heemskirk Canada)

2

rac sand has become a >$5 billion dollar industry in North America, surpassing the total

value of many other minerals traded worldwide.

In 2015, total US frac sand production was estimated at 67 million t (USGS) at prices ranging from $70-$84 USD/t.

Prices are forecasted to increase significantly over the next years as oil and gas producers are using more frac sand per well than anyone ever imagined, which is propelling this oilfield services sub-sector to the forefront of the oil and gas industry in a quite urgent way.

A majority of Canadian frac sand is imported from the US given the very high quality of Wisconsin Sand. The “gold standard” of frac sand is known as “Northern White” and most Canadian companies haul it some 3,000 km or more from the upper midwest US to the big shale plays in northern BC and Alberta, adding between $50-$150/t for transportation plus significant exchange rate costs.

With oil prices and rig counts down significantly, Canadian companies are looking for ways to cut costs. To improve their independence from the US market, domestic frac sand source must get identified and developed, ideally near Canada’s large shale gas basins in British Columbia, Alberta or Saskatchewan.

By 2020, the Horn River and Montney Basins in northeastern British Columbia are projected to produce around 6 bil-lion cubic feet of natural gas per day and

meeting somewhere between 25-33% of Canada’s demand. Those 2 fields alone may host as much as 300 trillion cubic feet of gas. To get the gas, producers must shoot tonnes of water and sand down a well while fracking fluids split open rocks to release trapped oil and gas. The sand wedges into cracks and keeps them open so that the hydrocar-bons can be pumped out. This process puts an immense pressure on the tiny grains of sand, the reason why the indus-try has high specifications for this sand. The sand grains have to be round as if they are angular they will crush on the pressure and cause inefficiencies.

According to Brandon Dobell (2016), an oil and gas analyst at William Blair, overall sand usage should rise even if oil prices stay within a range of $40-$60/barrel, because drillers are now using 2-3 times more sand per well than they did 3 years ago.

The larger volumes of sand used per well have partly offset the drop in demand of frac sand, owing to the recent downturn in the price of oil.

Between 2,000-3,000 t of frac sand are now routinely pumped into new and refracked wells, with wells in some parts of Texas consuming up to 8,000 t, Dobell said, adding that the largest well he has seen required 15,000 t – enough to fill up a 1.5 mile (2.4 km) long train of rail cars.

“If sand is sand, then what matters is a facility on a rail that allows you to ship 100 railcars at once and beat me by $20 to $40 a ton in costs,” Dobell said. “The market is still very focused on costs.”

According to Kent Harrington:

“Regardless of the sand drillers chose, overall demand is down in 2015, but its use per well has been steadily increasing. Wells currently use 4.2 million pounds of frac sand, but that’s expected to eventually double if current trends continue.

In 2012, the average well in the Eagle Ford received less than 1,000 pounds for every foot that snaked down into the ground, according to energy consulting firm Wood Mackenzie. By 2013, that number was 1,200 pounds. And last year it climbed to over 1,500 pounds. A study revealed that this extra sand can triple output.”

Some operators in North Dakota’s Bakken shale play are using >3,000 pounds of frac sand per foot. As Joseph Cafariello of Energy & Capital once said:

“If oil is black gold, then ‘frac sand’ is gold dust. The fracking boom in America could not advance nor even exist without frac sand or its synthetic imitations. The mining, processing, shipping and transloading of frac sand has become a whole new gold rush unto itself.”

Report #9 | 92 Resources Corp.

F

Close-up view of typical frac sand (on the right) and ordinary sand of similar grain size (on the left). Notice how the frac sand has a more uniform grain size, nicely rounded grain shapes, and a uniform composition. It is also a very tough material that can resist compressive forces of up to several tons per square inch. Grains in this image are about 0.5 mm in size. (Source: Geology.com)

3

The Moberly Mine has been producing industrial mineral products for over 30 years, whereas operations are currently being redeveloped in order to continue production of high quality frac sands, glass sands and other high purity silica sands later this year.

With capital costs of around $27 million USD, a nameplate production output capacity of 300,000 t frac sand per year is planned by Heemskirk, with first produc-tion expected in June 2017. An expansion to 600,000 t/year is planned at additional capital costs of $15 million USD. The plant has a flexible design to adapt to changes in product requirements and utilises energy efficient technology. It is located on the Trans-Canada Highway and the Canadian Pacific Rail Mainline, providing customers with logistical flex-ibility for delivery as being in 12 h truck-ing distance to targeted market areas which extend from northeast British Columbia (Horn River Basin) to southern Saskatchewan (Bakken Basin).

Thanks to well-rounded sand grains with a high purity of 99% SiO2, industry experts have confirmed that Moberly’s frac sand can compete against US frac sands in wells below 2,500 m.

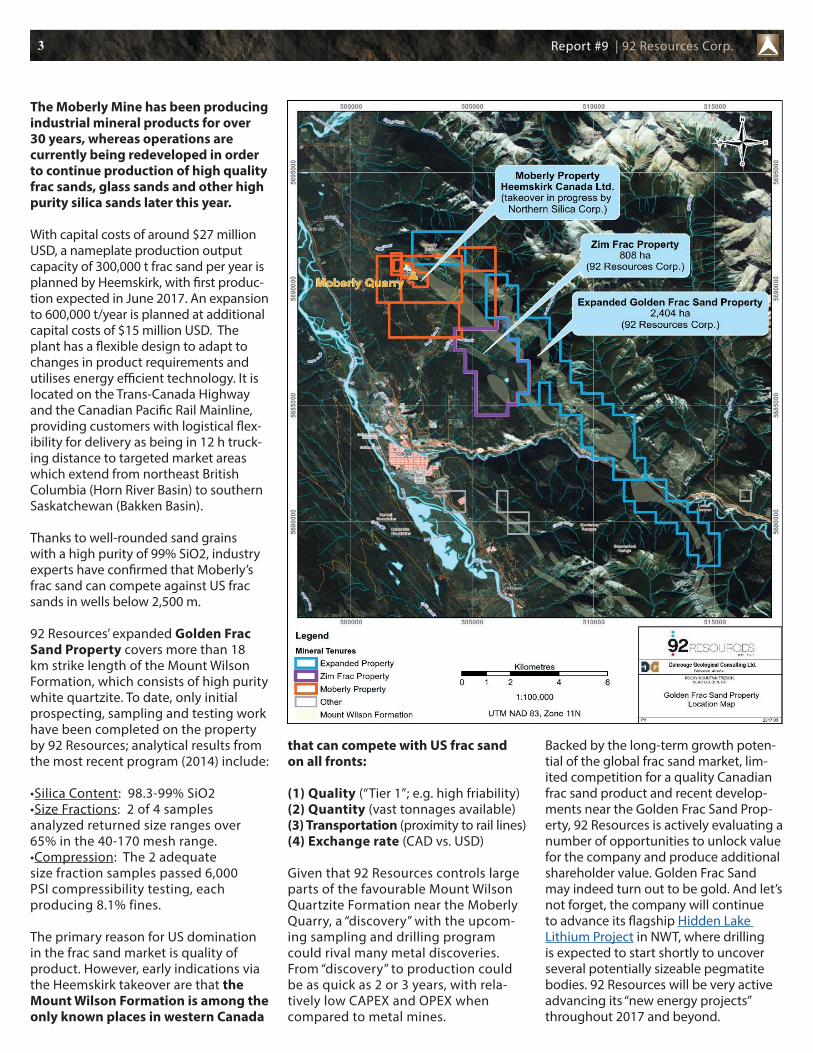

92 Resources’ expanded Golden Frac Sand Property covers more than 18 km strike length of the Mount Wilson Formation, which consists of high purity white quartzite. To date, only initial prospecting, sampling and testing work have been completed on the property by 92 Resources; analytical results from the most recent program (2014) include:

•Silica Content: 98.3-99% SiO2•Size Fractions: 2 of 4 samples analyzed returned size ranges over 65% in the 40-170 mesh range.•Compression: The 2 adequate size fraction samples passed 6,000 PSI compressibility testing, each producing 8.1% fines.

The primary reason for US domination in the frac sand market is quality of product. However, early indications via the Heemskirk takeover are that the Mount Wilson Formation is among the only known places in western Canada

that can compete with US frac sand on all fronts:

(1) Quality (“Tier 1”; e.g. high friability)(2) Quantity (vast tonnages available)(3) Transportation (proximity to rail lines)(4) Exchange rate (CAD vs. USD)

Given that 92 Resources controls large parts of the favourable Mount Wilson Quartzite Formation near the Moberly Quarry, a “discovery” with the upcom-ing sampling and drilling program could rival many metal discoveries. From “discovery” to production could be as quick as 2 or 3 years, with rela-tively low CAPEX and OPEX when compared to metal mines.

Backed by the long-term growth poten-tial of the global frac sand market, lim-ited competition for a quality Canadian frac sand product and recent develop-ments near the Golden Frac Sand Prop-erty, 92 Resources is actively evaluating a number of opportunities to unlock value for the company and produce additional shareholder value. Golden Frac Sand may indeed turn out to be gold. And let’s not forget, the company will continue to advance its flagship Hidden Lake Lithium Project in NWT, where drilling is expected to start shortly to uncover several potentially sizeable pegmatite bodies. 92 Resources will be very active advancing its “new energy projects” throughout 2017 and beyond.

Report #9 | 92 Resources Corp.

4 Report #9 | 92 Resources Corp.

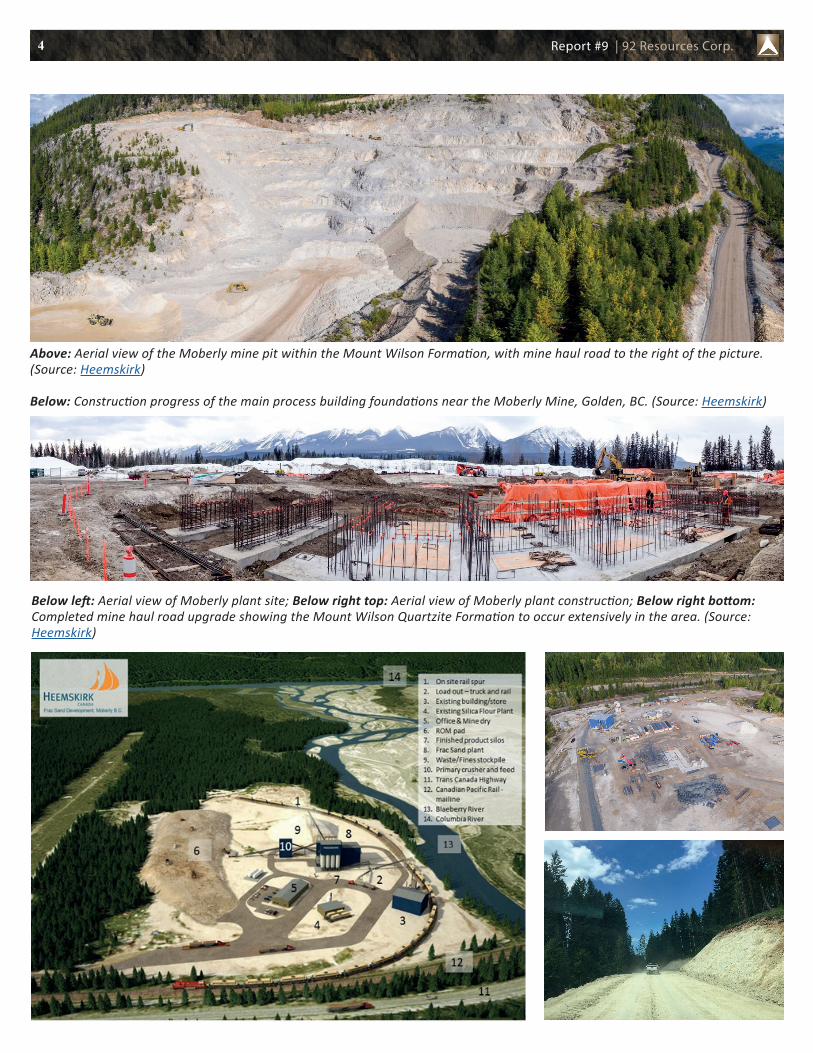

Above: Aerial view of the Moberly mine pit within the Mount Wilson Formation, with mine haul road to the right of the picture. (Source: Heemskirk)

Below: Construction progress of the main process building foundations near the Moberly Mine, Golden, BC. (Source: Heemskirk)

Below left: Aerial view of Moberly plant site; Below right top: Aerial view of Moberly plant construction; Below right bottom: Completed mine haul road upgrade showing the Mount Wilson Quartzite Formation to occur extensively in the area. (Source: Heemskirk)

5

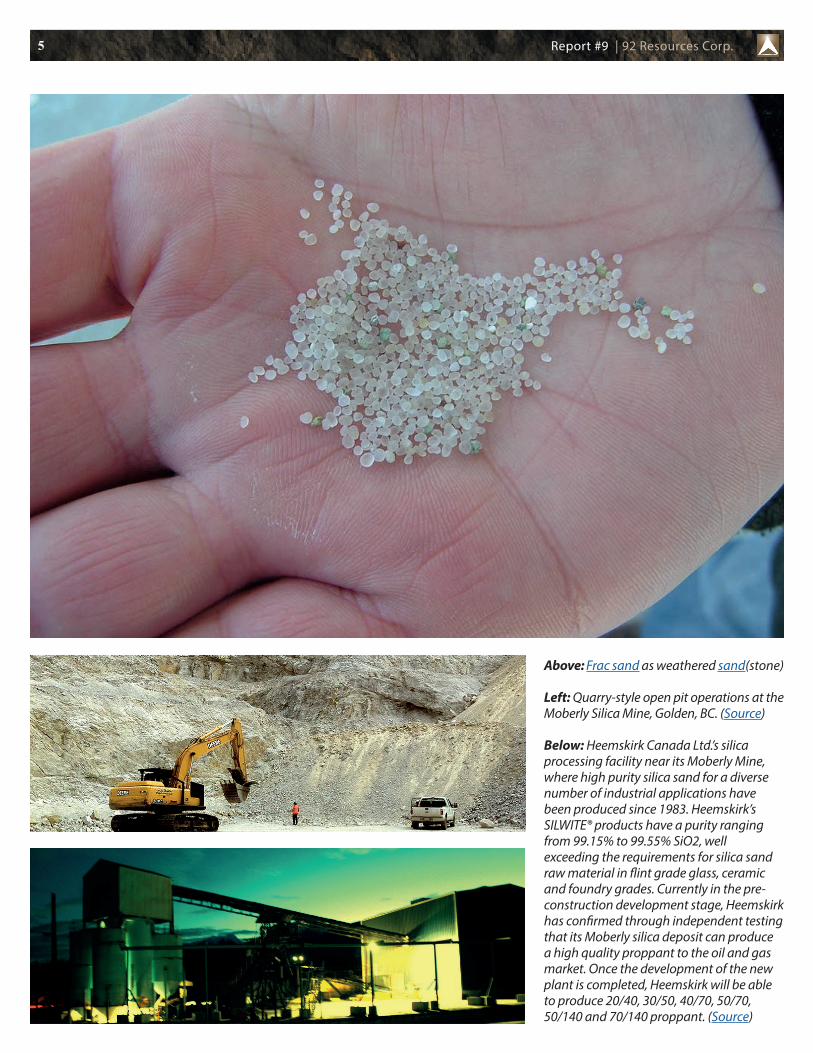

Above: Frac sand as weathered sand(stone)

Left: Quarry-style open pit operations at the Moberly Silica Mine, Golden, BC. (Source)

Below: Heemskirk Canada Ltd.’s silica processing facility near its Moberly Mine, where high purity silica sand for a diverse number of industrial applications have been produced since 1983. Heemskirk’s SILWITE® products have a purity ranging from 99.15% to 99.55% SiO2, well exceeding the requirements for silica sand raw material in flint grade glass, ceramic and foundry grades. Currently in the pre-construction development stage, Heemskirk has confirmed through independent testing that its Moberly silica deposit can produce a high quality proppant to the oil and gas market. Once the development of the new plant is completed, Heemskirk will be able to produce 20/40, 30/50, 40/70, 50/70, 50/140 and 70/140 proppant. (Source)

Report #9 | 92 Resources Corp.

6 Report #9 | 92 Resources Corp.

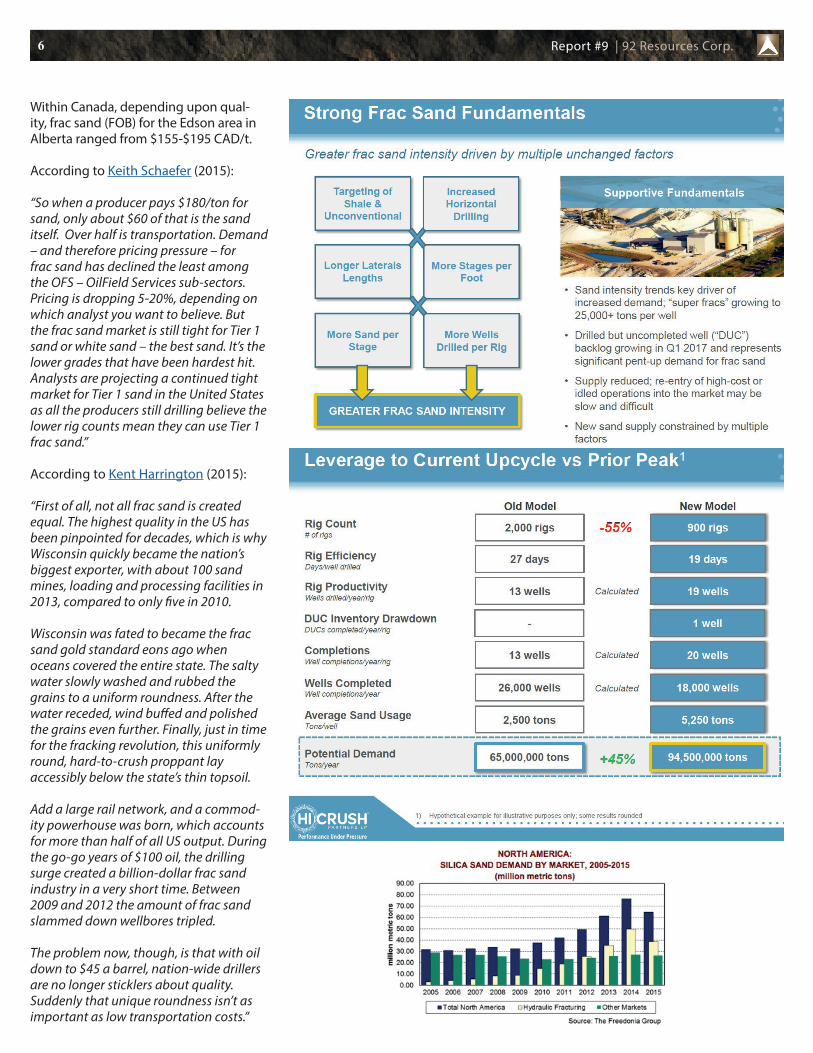

Within Canada, depending upon qual-ity, frac sand (FOB) for the Edson area in Alberta ranged from $155-$195 CAD/t.

According to Keith Schaefer (2015):

“So when a producer pays $180/ton for sand, only about $60 of that is the sand itself. Over half is transportation. Demand – and therefore pricing pressure – for frac sand has declined the least among the OFS – OilField Services sub-sectors. Pricing is dropping 5-20%, depending on which analyst you want to believe. But the frac sand market is still tight for Tier 1 sand or white sand – the best sand. It’s the lower grades that have been hardest hit. Analysts are projecting a continued tight market for Tier 1 sand in the United States as all the producers still drilling believe the lower rig counts mean they can use Tier 1 frac sand.”

According to Kent Harrington (2015):

“First of all, not all frac sand is created equal. The highest quality in the US has been pinpointed for decades, which is why Wisconsin quickly became the nation’s biggest exporter, with about 100 sand mines, loading and processing facilities in 2013, compared to only five in 2010.

Wisconsin was fated to became the frac sand gold standard eons ago when oceans covered the entire state. The salty water slowly washed and rubbed the grains to a uniform roundness. After the water receded, wind buffed and polished the grains even further. Finally, just in time for the fracking revolution, this uniformly round, hard-to-crush proppant lay accessibly below the state’s thin topsoil.

Add a large rail network, and a commod-ity powerhouse was born, which accounts for more than half of all US output. During the go-go years of $100 oil, the drilling surge created a billion-dollar frac sand industry in a very short time. Between 2009 and 2012 the amount of frac sand slammed down wellbores tripled.

The problem now, though, is that with oil down to $45 a barrel, nation-wide drillers are no longer sticklers about quality. Suddenly that unique roundness isn’t as important as low transportation costs.”

7 Report #9 | 92 Resources Corp.

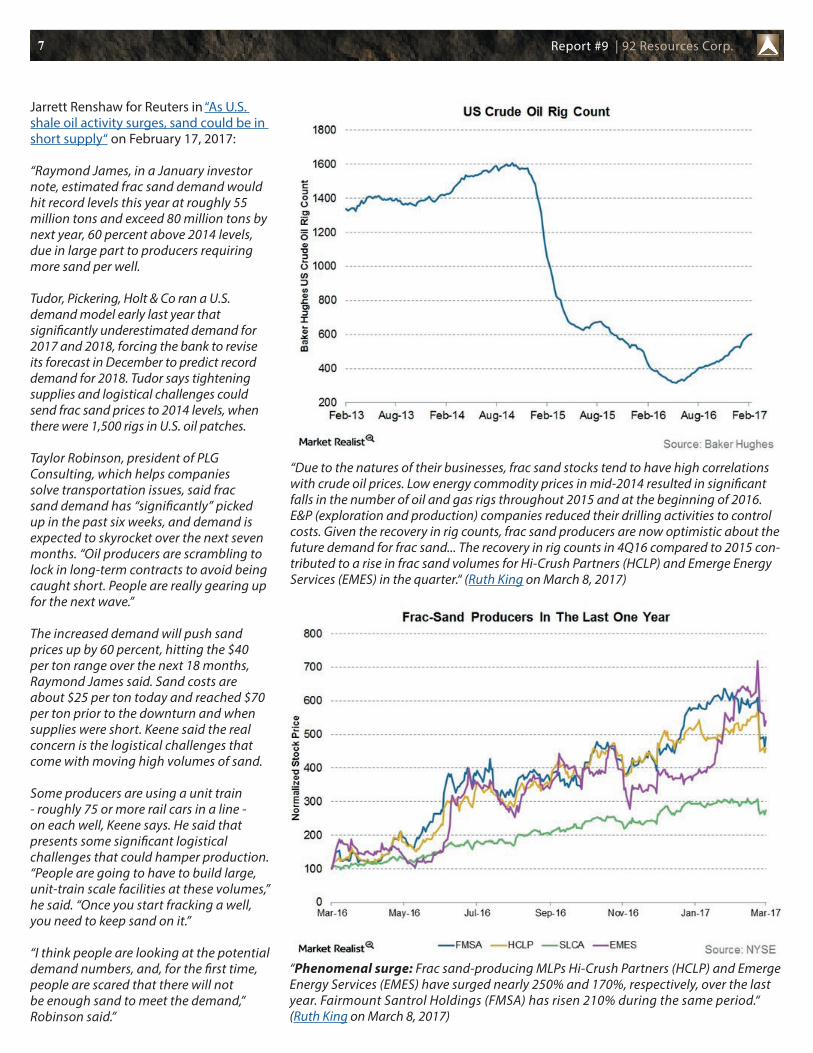

“Phenomenal surge: Frac sand-producing MLPs Hi-Crush Partners (HCLP) and Emerge Energy Services (EMES) have surged nearly 250% and 170%, respectively, over the last year. Fairmount Santrol Holdings (FMSA) has risen 210% during the same period.“ (Ruth King on March 8, 2017)

“Due to the natures of their businesses, frac sand stocks tend to have high correlations with crude oil prices. Low energy commodity prices in mid-2014 resulted in significant falls in the number of oil and gas rigs throughout 2015 and at the beginning of 2016. E&P (exploration and production) companies reduced their drilling activities to control costs. Given the recovery in rig counts, frac sand producers are now optimistic about the future demand for frac sand... The recovery in rig counts in 4Q16 compared to 2015 con-tributed to a rise in frac sand volumes for Hi-Crush Partners (HCLP) and Emerge Energy Services (EMES) in the quarter.“ (Ruth King on March 8, 2017)

Jarrett Renshaw for Reuters in “As U.S. shale oil activity surges, sand could be in short supply“ on February 17, 2017:

“Raymond James, in a January investor note, estimated frac sand demand would hit record levels this year at roughly 55 million tons and exceed 80 million tons by next year, 60 percent above 2014 levels, due in large part to producers requiring more sand per well.

Tudor, Pickering, Holt & Co ran a U.S. demand model early last year that significantly underestimated demand for 2017 and 2018, forcing the bank to revise its forecast in December to predict record demand for 2018. Tudor says tightening supplies and logistical challenges could send frac sand prices to 2014 levels, when there were 1,500 rigs in U.S. oil patches.

Taylor Robinson, president of PLG Consulting, which helps companies solve transportation issues, said frac sand demand has “significantly” picked up in the past six weeks, and demand is expected to skyrocket over the next seven months. “Oil producers are scrambling to lock in long-term contracts to avoid being caught short. People are really gearing up for the next wave.”

The increased demand will push sand prices up by 60 percent, hitting the $40 per ton range over the next 18 months, Raymond James said. Sand costs are about $25 per ton today and reached $70 per ton prior to the downturn and when supplies were short. Keene said the real concern is the logistical challenges that come with moving high volumes of sand.

Some producers are using a unit train - roughly 75 or more rail cars in a line - on each well, Keene says. He said that presents some significant logistical challenges that could hamper production. “People are going to have to build large, unit-train scale facilities at these volumes,” he said. “Once you start fracking a well, you need to keep sand on it.”

“I think people are looking at the potential demand numbers, and, for the first time, people are scared that there will not be enough sand to meet the demand,” Robinson said.”

8

Click on chart (or here) for updated version (15 min. delayed)

Previous Coverage

Report #8: “High Lithium Grades and Astounding Size Potential Sampling Suggests“ (November 28, 2016)

Report #7: “High-Grade Lithium and Tantalum confirmed by Channel Sampling“ (November 8, 2016)

Report #6: “Crews mobilized for next phase of exploration on the Hidden Lake Lithium Property in NWT“ (August 16, 2016)

Report #5: “92 Resources snags hard-rock lithium property in Quebec“ (July 26, 2016)

Report #4: “Why 92 Resources looks ready for the next upswing“ (June 20, 2016)

Report #3: “Extremely high-grade lithium assays from surface“ (June 7, 2016)

Report #2: “Untapping Canada‘s Hidden Lithium Treasuries“ (March 1, 2016)

Report #1: “92 Resources on the case for Hard Rock Lithium“ (April 11, 2016)

Corporate Presentation: March 2017Corporate Factsheet: March 2017Website: www.92resources.com

Further Reading:

“Company plans pegmatite drill program outside Yellowknife near Hidden Lake“ (by Guy Quenneville for CBC News on January 25, 2017)

“Canada: a key mining player despite local challenges“ (January 2017 edition of the Materials World Magazine by the Institute of Materials, Minerals and Mining (IOM3) domiciled in London, UK)

Report #9 | 92 Resources Corp.

9

Disclaimer and Information on Forward Looking StatementsAll statements in this report, other than statements of historical fact should be con-sidered forward-looking statements. Much of this report is comprised of statements of pro-jection. Statements in this report that are for-ward looking include that frac sand, lithium and commodity prices are expected to per-form well in future; that 92 Resources Corp. (“NTY”) or its partner(s) can and will start work programs on its properties; that explor-ation has or will discover a mineable deposit; that the company can raise sufficient funds for exploration or development; that any of the mentioned mineralization indications or estimates are valid or economic; that drilling will start shortly on NTY’s Hidden Lake Prop-erty in NWT to potentially discover sizeable pegmatites under shallow overburden; that the frac sand property may represent a significantly undervalued asset given its potential to host a large, high-quality frac sand deposit; that there could be savvy reas-ing behind NTY’s aggressive land staking/aquisitions; that the company can unlock or produce any shareholder value with its frac sand property in BC. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those antici-pated in these forward-looking statements. Risks and uncertainties respecting mineral exploration and mining companies are generally disclosed in the annual financial or other filing documents of 92 Resources Corp. and similar companies as filed with the relevant securities commissions, and should be reviewed by any reader of this report. In addition, with respect to 92 Resources Corp., a number of risks relate to any statement of projection or forward statements, including among other risks: the receipt of all neces-sary approvals and permits; the ability to conclude a transaction to start or continue exploration; uncertainty of future lithium and commodity prices, capital expenditures and other costs; financings and addition-al capital requirements for exploration, development, construction, and operating of a mine; the receipt in a timely fashion of further permitting for its legislative, political, social or economic developments in the jurisdictions in which 92 Resources Corp. carries on business; operating or technical difficulties in connection with mining or development activities; the ability to keep key employees, joint-venture partner(s), and operations financed. There can be no assur-ance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements.

Accordingly, readers should not place undue reliance on forward-looking informa-tion. Rockstone and the author of this report do not undertake any obligation to update any statements made in this report.Disclosure of Interest and Advisory CautionsNothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report is paid by Zimtu Capital Corp., a TSX Venture Exchange listed investment company. Part of the author’s responsibilities at Zimtu is to research and report on companies in which Zimtu has an investment. So while the author of this report is not paid directly by 92 Resources, the author’s employer Zimtu will benefit from appreciation of 92 Resources’ stock price. In addition, the author owns equity of 92 Resources Corp. and would also benefit from volume and price appreciation of its stock. 92 Resources Corp. may have one or more common directors with Zimtu Capital Corp. Overall, multiple conflicts of interests exist. Therefore, the information provided herewithin should not be construed as a financial analysis but rather as advertisement. The author’s views and opinions regarding the companies featured in reports are his own views and are based on information that he has researched independently and has received, which the author assumes to be reliable. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. 92 Resources Corp. has not reviewed all the content prior to publication and may not agree with statements made herein. Lastly, the author does not guarantee that any of the companies mentioned will perform as expected, and any comparisons made to other companies may not be valid or come into effect. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is educational and general in nature.

Author Profile & Contact

Stephan Bogner (Dipl. Kfm., FH)Rockstone Research 8050 Zurich, SwitzerlandPhone: +41-44-5862323Email: [email protected]

Stephan Bogner studied at the International School of Management (Dortmund, Germany), the European Business School (London, UK) and the University of Queensland (Brisbane,

Australia). Under supervision of Prof. Dr. Hans J. Bocker, Stephan completed his diploma thesis (“Gold In A Macroeconomic Context With Special Consideration Of The Price Formation Process”) in 2002.

Bogner then marketed and translated into German Ferdinand Lips‘ bestseller (“Gold Wars“). After working in Dubai for 5 years, he now lives in Switzerland and is the CEO of Elementum International AG specialized in storage of gold and silver bullion in a high-security vaulting facility within the St. Gotthard Mountain Massif in central Switzerland.

Rockstone is specialized in capital markets and publicly listed companies. The focus is set on exploration, development and production of resource deposits as well as commodity and currency markets.

Through the publication of general geological basic knowledge, the individual reports receive a background in order for the reader to be inspired to conduct further due diligence. All reports are made accessible free of charge, whereas it is always to be construed as non-binding educational research and is addressed solely to a readership that is knowledgeable about the risks, experienced with stock markets, and acting on one’s own responsibility.

For more information and sign-up for free newsletter, please visit:

www.rockstone-research.com

Report #9 | 92 Resources Corp.