Embed Size (px)

Citation preview

BDC 101

CHAPTER 1

FINANCIAL ACCOUNTING 1

INTRODUCTION TO ACCOUNTING

SCHOOL OF ACCOUNTING & FINANCEFACULTY OF BUSINESS AND MANAGEMENT

PREPARED BY:NORAL HIDAYAH ALWINUR AMALINA BINTI BORHAN

Slide 2 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

LEARNING OUTCOMES

At the end of this chapter, students will be able to:

Define the meaning and functions of accounting

Identify the users of the financial information and the reasons for relying in it

Identify the roles and responsibilities of the regulatory bodies

Identify the various accounting concepts

Slide 3 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

TOPIC OUTLINES

1.1 Definition of Accounting1.1.1 The Different Between Accounting and Bookkeeping

1.2 The Importance of Accounting

1.3 Users of Accounting Information1.3.1 Internal Users1.3.2 External Users

1.4 Types of Accounting

1.5 Types Of Business

1.6 Accounting Bodies

1.7 Accounting Concepts

Slide 4 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

INTRODUCTION

What do you think of when you read or hear the word, ‘accounting’?

Figure 1

Slide 5 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

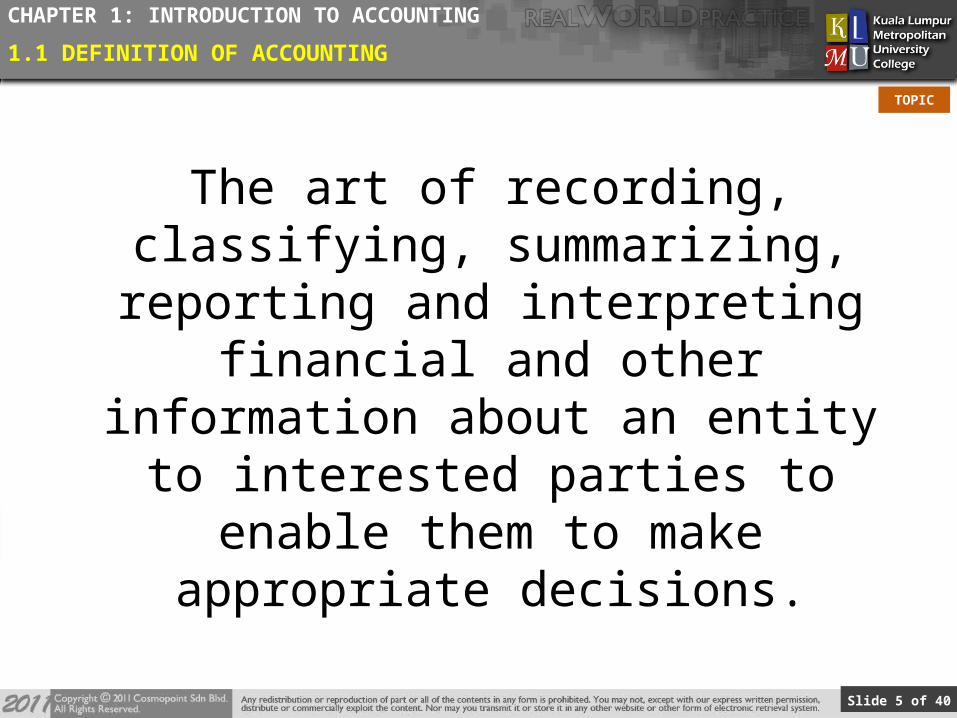

1.1 DEFINITION OF ACCOUNTING

The art of recording, classifying, summarizing, reporting and

interpreting financial and other information about an entity to

interested parties to enable them to make appropriate decisions.

Slide 6 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

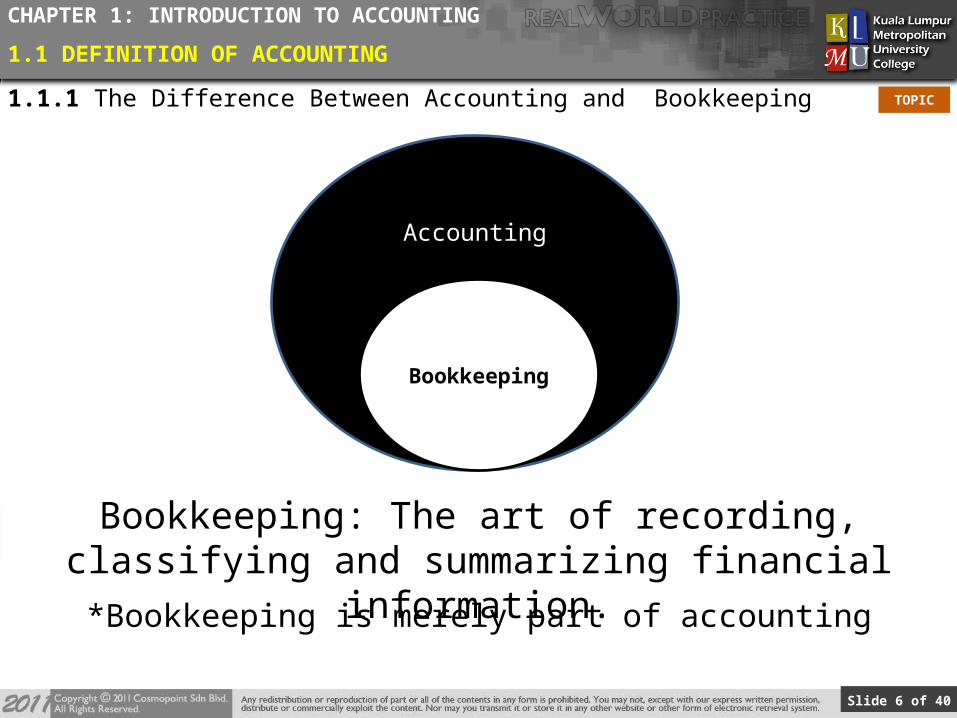

1.1.1 The Difference Between Accounting and Bookkeeping

Accounting

Bookkeeping: The art of recording, classifying and summarizing financial

information.*Bookkeeping is merely part of accounting

Bookkeeping

1.1 DEFINITION OF ACCOUNTING

Slide 7 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Provide management and owner with information on the profitability and financial position of the business.

Enable management to plan short-term and long-term business activities.

Enable the organization to comply with the statutory requirements of state and federal government.

1.2 THE IMPORTANCE OF ACCOUNTING

Slide 8 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

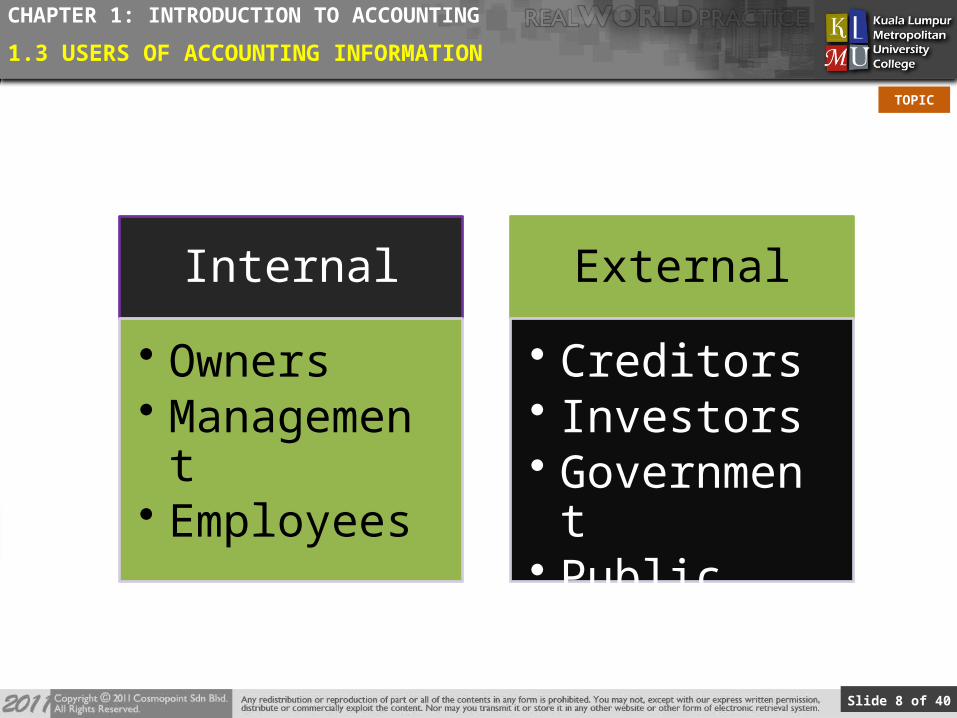

Internal

• Owners• Management• Employees

External

• Creditors• Investors• Government• Public

1.3 USERS OF ACCOUNTING INFORMATION

Slide 9 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.3 USERS OF ACCOUNTING INFORMATION

1.3.1 Internal Users

• Need accounting information as they are interested in the profits earned from their investment as well as financial stability and growth of their businesses

Owners

Slide 10 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.3 USERS OF ACCOUNTING INFORMATION

1.3.1 Internal Users

• Need accounting information to make decisions on various aspects of business for eg. production, finance and marketing.

Management

Slide 11 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.3 USERS OF ACCOUNTING INFORMATION

1.3.1 Internal Users

• Need accounting information as they are interested in the business’s ability to progress and expand

Employees

Slide 12 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.3 USERS OF ACCOUNTING INFORMATION

1.3.2 External Users

• Need acctg information as they need to determine whether business able to pay debt or not.Creditors

Slide 13 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.3 USERS OF ACCOUNTING INFORMATION

1.3.2 External Users

• Need acctg information as they are interested in the biz’s performance for the year.

• Also want to evaluate how efficiently and profitably mgt has used the resources entrusted to them.

Investors

Slide 14 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

• IRB is the taxing authority and therefore interested in the acctg statements and report of biz.Govt

1.3 USERS OF ACCOUNTING INFORMATION

1.3.2 External Users

Slide 15 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

• Mostly consumers of the products and services.• Interested in the establishment of good accounting

control as a means of reducing cost of production, selling and distribution, and hence the reduction of the prices of the goods they purchase.

The Public

1.3 USERS OF ACCOUNTING INFORMATION

1.3.2 External Users

Slide 16 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

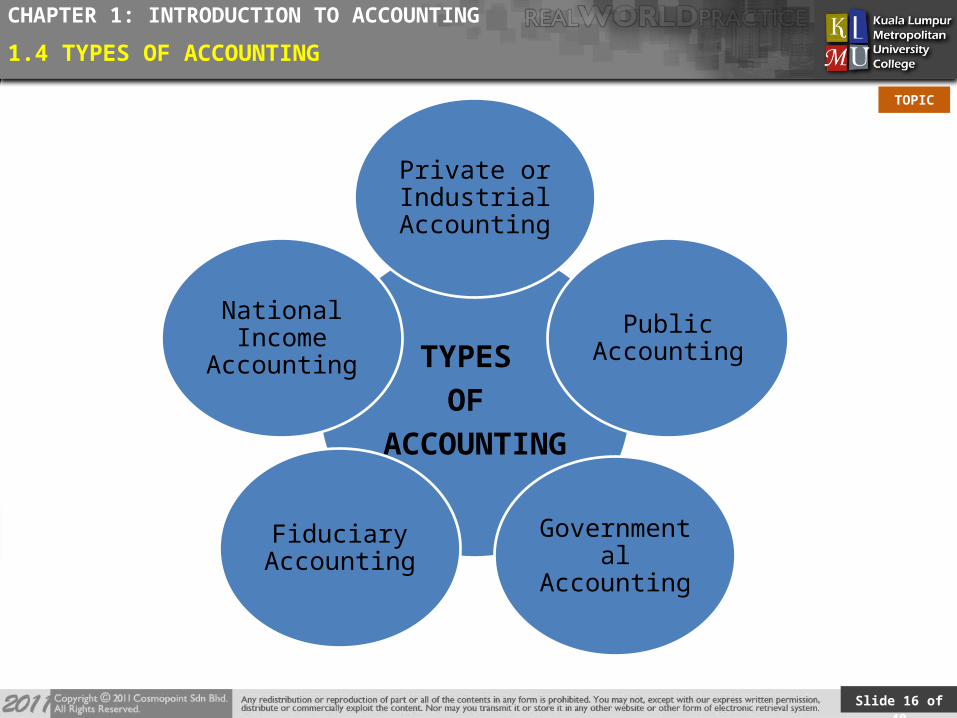

1.4 TYPES OF ACCOUNTING

TYPES

OF

ACCOUNTING

Private or Industrial

Accounting

Public Accounting

Governmental Accounting

Fiduciary Accounting

National Income

Accounting

Slide 17 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.4 TYPES OF ACCOUNTING

Refers to accounting activity that is limited only to a single firm.

A private accountant provides his skills and services to a single employer and receives salary on an employer-employee basis.

The term ‘private’ is applied to the accountant and the accounting service he renders.

The term is used when an employer-employee type of relationship exists even though the employer is some case is a public corporation.

Private or Industrial Accounting

Slide 18 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.4 TYPES OF ACCOUNTING

Refers to the accounting service offered by a public accountant to the general public.

When a practitioner-client relationship exists, the accountant is referred to as a public accountant.

Public accounting is considered to be more professional than private accounting.

Both certified and non certified public accountants can provide public accounting services.

Certified accountants can be single practitioners or by partnership ranging in size from two to hundreds of members. The scope of these accounting firms can include local, national and international clientele.

Eg. PriceWaterhouseCoopers (PwC)

Public Accounting

Slide 19 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.4 TYPES OF ACCOUNTING

Refers to accounting for a branch or unit of government at any level, may it be federal, state, or local.

Governmental accounting is very similar to conventional accounting methods.

Both the governmental and conventional accounting methods use the double-entry system of accounting and journals and ledgers.

The objective of government accounting units is to give service rather than make profits. Since profit motive cannot be used as a measure of efficiency in government units, other control measures must be developed.

To enhance control, special funds accounting is used.

Governmental Accounting

Slide 20 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.4 TYPES OF ACCOUNTING

Fiduciary accounting lies in the notion of trust. This type of accounting is done by a trustee, administrator, executor,

or anyone in a position of trust. His work is to keep the records and prepares the reports. This may be authorized by or under the jurisdiction of a court of law. The fiduciary accountant should seek out and control all property

subject to the estate or trust

Fiduciary Accounting

Slide 21 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

1.4 TYPES OF ACCOUNTING

National income accounting uses the economic or social concept in establishing accounting rather than the usual business entity concept.

The national income accounting is responsible in providing the public an estimate of the nation's annual purchasing power.

The GNP or the gross national product is a related term, which refers to the total market value of all the goods and services produced by a country within a given period of time, usually a calendar year.

National Income Accounting

Slide 22 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

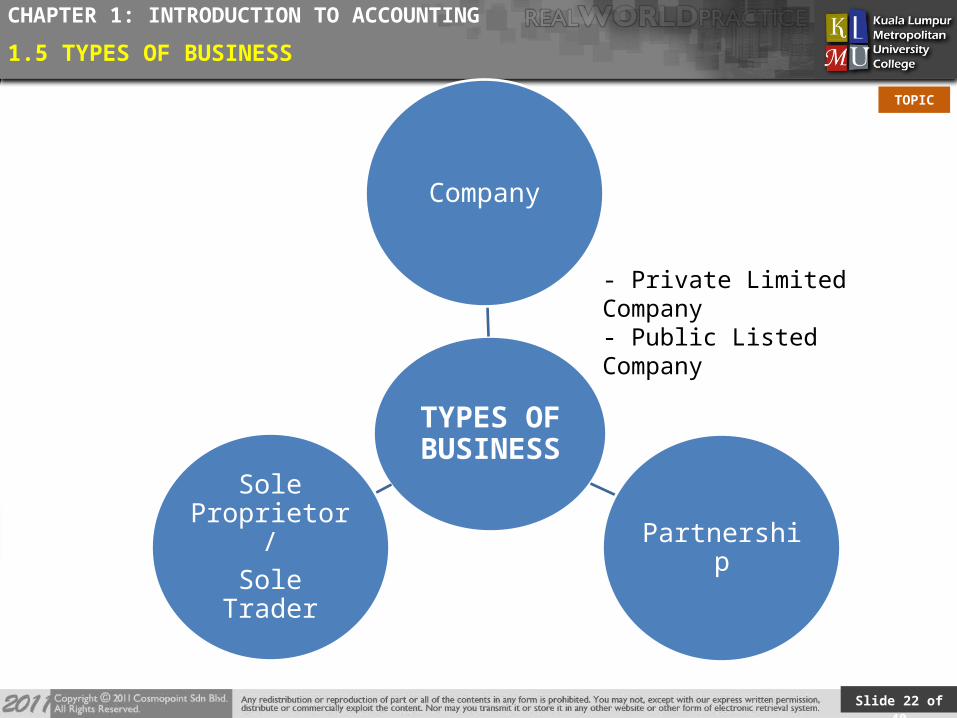

- Private Limited Company- Public Listed Company

1.5 TYPES OF BUSINESS

TYPES OF BUSINESS

Sole Proprietor/

Sole TraderPartnership

Company

Slide 23 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Owned by one individual only The person and his business is "one" legally The name of the owner may be used for business. Usually it start with a small amount of capital. All profits will go to the owner but he/she has unlimited liability if

business fails. The life span of the business depends upon the age of the owner

(dissolve upon the death) or how efficiently he/she manages the business

No legal obligation to audit the book of accounts Eg: Kedai Gunting Ahmad

Sole Proprietorship/Sole Trader

1.5 TYPES OF BUSINESS

Figure 2

Slide 24 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

A partnership is carried out by two or more partners but NOT exceeding 20 persons. (In professional business, such as legal firms, architect and accounting firms, the members could number up to 50 persons)

A written agreement (Letter of Agreement) is necessary stating the terms and conditions of conducting the business without harming the interest of either party.

Profits/loss are shared either equally or as per the terms given in the written legal agreement.

Business liabilities are unlimited (may involve personal assets of all partners of the company)

Partnership

1.5 TYPES OF BUSINESS

Figure 3

Slide 25 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

With the Limited Liability Partnerships Act, partners can profit from limited liability and reap tax advantages.

No legal obligation to audit the book of accounts The life span of the partnership business depends on the life span of

the partners (if any of the partners passes away or is declared a bankrupt, the business is automatically dissolved, unless there is an agreement)

For eg : Klinik Abu dan rakan-rakan

Partnership

1.5 TYPES OF BUSINESS

Slide 26 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Unlike a sole trader or a partnership concern, a Company is legally a separate entity.

Governed under Companies Act 1965.

Must have at least two members.

The members of the company will appoint the

Board of Directors who will manage and run

the business

Company

1.5 TYPES OF BUSINESS

Figure 4

Slide 27 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Members are known as ‘shareholders’

Each shareholder has an authorized shareholding which defines the limit of the shareholder liability.

The liabilities are limited to the total shares contributed to the company’s capital (personal assets are not affected)

Has to maintain proper records and legally

obligated to audit the book of accounts.

Company

1.5 TYPES OF BUSINESS

Slide 28 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

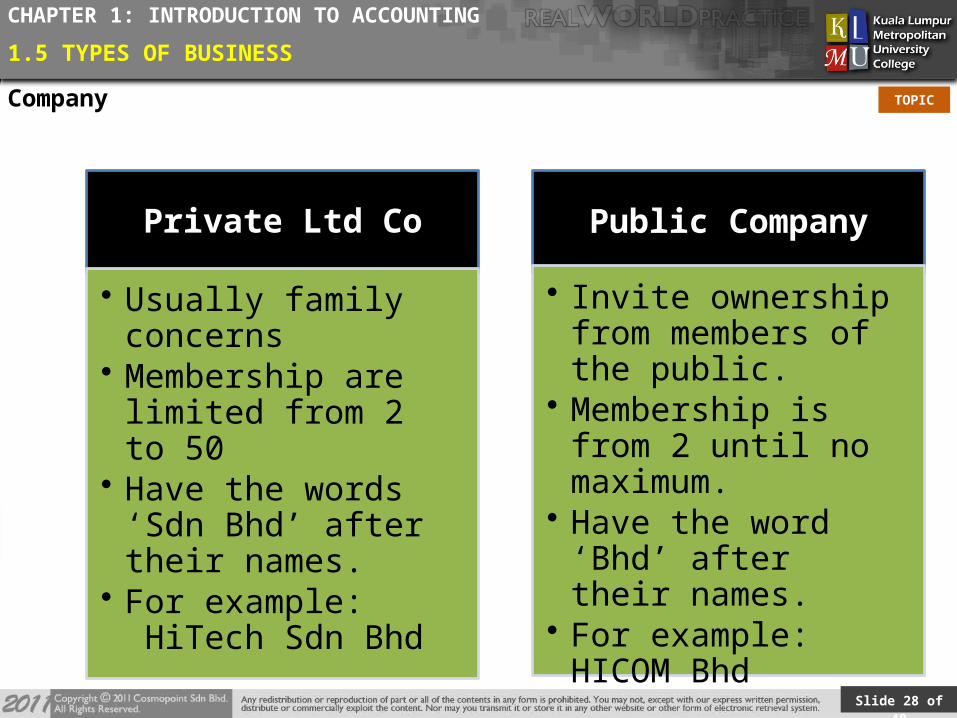

Private Ltd Co

• Usually family concerns

• Membership are limited from 2 to 50

• Have the words ‘Sdn Bhd’ after their names.

• For example: HiTech Sdn Bhd

Public Company

• Invite ownership from members of the public.

• Membership is from 2 until no maximum.

• Have the word ‘Bhd’ after their names.

• For example: HICOM Bhd

Company

1.5 TYPES OF BUSINESS

Slide 29 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Malaysian Accounting Standard Board (MASB)

Malaysian Institute of Accountants (MIA)

Malaysian Institute of Certified Public Accountants (MICPA)

1.6: ACCOUNTING BODIES

*Tutorial 1

Explain the roles and responsibilities of all accounting bodies listed above. Please submit in writing.

Due date: 20 February 2013 (In class)

Slide 30 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Separate Entity Concept

Going Concern Concept

Historical Cost Concept

Duality Concept

Periodicity Concept

1.7: ACCOUNTING CONCEPTS

Slide 31 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Money Measurement Concept

Accrual Concept

Realization Concept

Consistency Concept

Materiality Concept

Prudence Concept

1.7: ACCOUNTING CONCEPTS

Slide 32 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Business is a separate entity from its owner. The idea here is that personal transactions of owner must be kept

separate from business For eg. payment of electricity bill of owner’s house cannot be charged

as business expenses. If owner is taking assets from the business, it must be recorded as

‘drawings’.

Separate Entity Concept

1.7: ACCOUNTING CONCEPTS

Slide 33 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Holding to the assumption that business will remain in existence for the foreseeable future.

Going Concern Concept

1.7: ACCOUNTING CONCEPTS

Slide 34 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Assets must be stated at COST PRICE in the balance sheet and not the current market or liquidation value of the assets

Historical Cost Concept

1.7: ACCOUNTING CONCEPTS

Slide 35 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Also known as ‘double entry’ concept. Every business transaction recorded has double/dual effect on the

position of business. For example, when asset is bought on credit, the asset account will

increase (debit asset) and simultaneously liability will also increase (credit liability).

Duality Concept

1.7: ACCOUNTING CONCEPTS

Slide 36 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Based on the going concern concept, business enterprise is assumed to cover a long period of time.

This period is divided into units of equal length which is called ‘accounting period’.

The common accounting period is 12 months or one year.

Periodicity Concept

1.7: ACCOUNTING CONCEPTS

Slide 37 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

This concept simply states that only those transactions that can be expressed in money values (currencies) can be recorded in the books of accounts.

Money Measurement Concept

1.7: ACCOUNTING CONCEPTS

Slide 38 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

All income and expenses must be recorded in the appropriate statement at the appropriate time.

I.e., all income and expenses for a particular accounting period will be recorded in full regardless whether they are really received or paid by cash.

Payment for future period must be carried forward as prepayment and not charged in the current profit statement.

…recognizing economic events regardless of when cash transactions occur…

Accrual Concept

1.7: ACCOUNTING CONCEPTS

Slide 39 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

‘Realization’ only occurs when a sale is made to customer. This means that sale on credit can be recorded as revenue without

having to wait for the payment.

Realization Concept

1.7: ACCOUNTING CONCEPTS

Slide 40 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

Methods of accounting must be consistent from year to year. For eg. If business adopts the straight line method of depreciation this

current period, it must be continuously used to the next accounting periods to ensure acctg reports are comparable from time to time.

Consistency Concept

1.7: ACCOUNTING CONCEPTS

Slide 41 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

An amount is considered material if it has significant effect upon the income or financial position of a business.

Whether it is material or not, it depends on the circumstances surrounding a business transaction.

For eg. A new motor vehicle must be depreciated over its useful life because it has a material amount. But the paper clips may not be depreciated even though it has useful life because it has a very small or no effect at all to the financial statements.

Materiality Concept

1.7: ACCOUNTING CONCEPTS

Slide 42 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

A business usually face with a risk of uncertainty as the business cannot predict what will happen in the future.

As a result, a business tends to take a conservative view point and this will reflect in preparing the accounting reports.

In relation to accounting reports, the accountant will choose the one that results in a lower profit, a lower assets value and a higher liability value.

Prudence Concept

1.7: ACCOUNTING CONCEPTS

Slide 43 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

THE ENDCLASS ASSIGNMENT…

Please click the arrow

Slide 44 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

SUMMARY

Accounting is the art of recording, classifying, summarizing, reporting and interpreting financial and other information about an entity for decision making.

Bookkeeping is the art of recording, classifying and summarizing financial information.

There are 2 types of users, internal and external. There are 5 types of accounting. 3 types of businesses consist of Sole proprietorship, partnership and company. There are 11 accounting concepts applicable.

Slide 45 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

NEXT SESSION PREVIEW

CHAPTER 2ACCOUNTING EQUATION & DOUBLE ENTRY SYSTEM

Slide 46 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

REFERENCES

Business Accounting I, 11th Edition Frank Wood and Alan Sangster, ISBN 13: 978-0-273-71212-1, FT Prentice Hall, Harlow © 2008

Slide 47 of 40

TOPIC

CHAPTER 1: INTRODUCTION TO ACCOUNTING

APPENDIX

Figure Source

Figure 1 http://censemaking.files.wordpress.com/2011/06/modern-thinker-by-lumaxart.jpg

Figure 2 http://www.referenceforbusiness.com/photos/sole-proprietorship-355.jpg

Figure 3 http://population-based-intervention.wikispaces.com/file/view/partners.jpg/306127206/partners.jpg

Figure 4 http://gamma.com.my/images/company_01.jpg