Embed Size (px)

Citation preview

MONGOLIA

2

GDP growth contributions (supply side)

3

• The economy grew by 5.3% in the

first half of 2017, recovering strongly

from only 1.2% growth in 2016.

• Services lifted GDP by 4.3 percentage

points, and agriculture by 1.0 point.

• Coal production soared, with coal

exports increasing by more than

fourfold.

• However, mining as a whole slumped

as copper concentrate production

languished, causing the larger

industry sector to subtract marginally

from growth. -10%

-5%

0%

5%

10%

15%

20%

I II III IV I II III IV I II III IV I II III IV I II

2013 2014 2015 2016 2017

Agriculture Industry, constructionServices Net taxes on productsGDP

Sources: National Statistical Office. 2017. Monthly Statistical Bulletin.

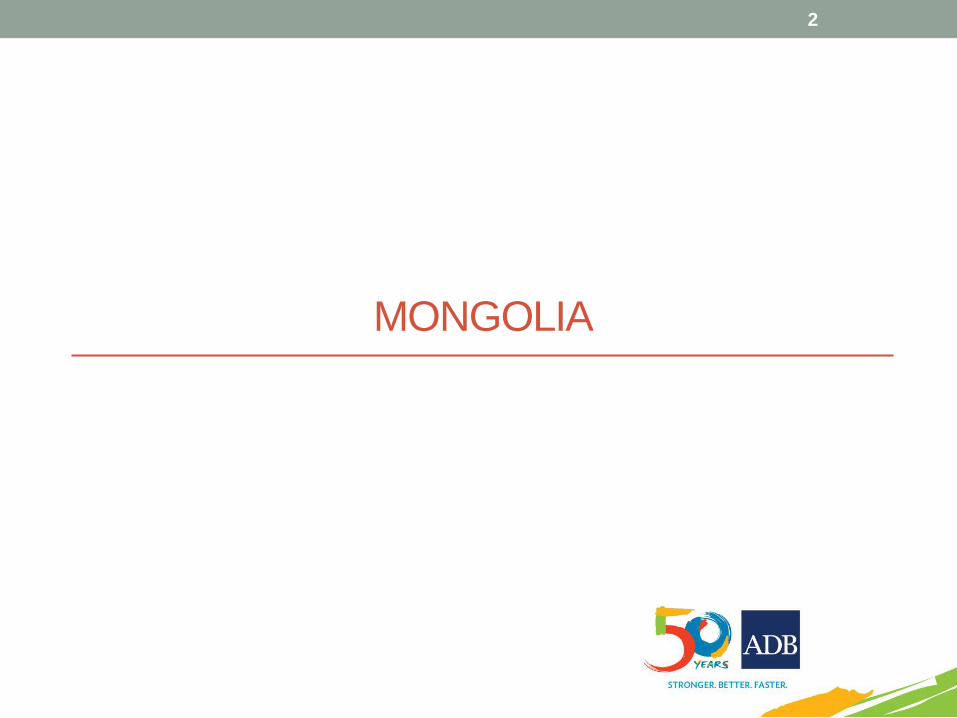

Coking coal prices unstable

4

Demand side contributions

5

• Investment, mainly into mining,

contributed 13.2 percentage

points to growth, and consumption

added 1.6 points.

• Net exports subtracted 9.6 points

as imports rose by 37.4% in

tandem with mining investment.

-40%

-20%

0%

20%

40%

I II III IV I II III IV I II III IV I II III IV I II

2013 2014 2015 2016 2017

Household consumption*** Government consumption

Gross fixed capital formation Changes in inventories****

Net exports GDP

Sources: National Statistical Office. 2017. Monthly Statistical Bulletin.

Inflation picks up but modest

• Inflation averaged 3.0% in the first half of the year as

togrog depreciation by 24.8% last year began to affect

prices.

• In June, the Bank of Mongolia, the central bank, lowered

its policy rate by 2.0 percentage points to 12.0% as terms

of trade improved and short-term external debt pressures

eased.

6

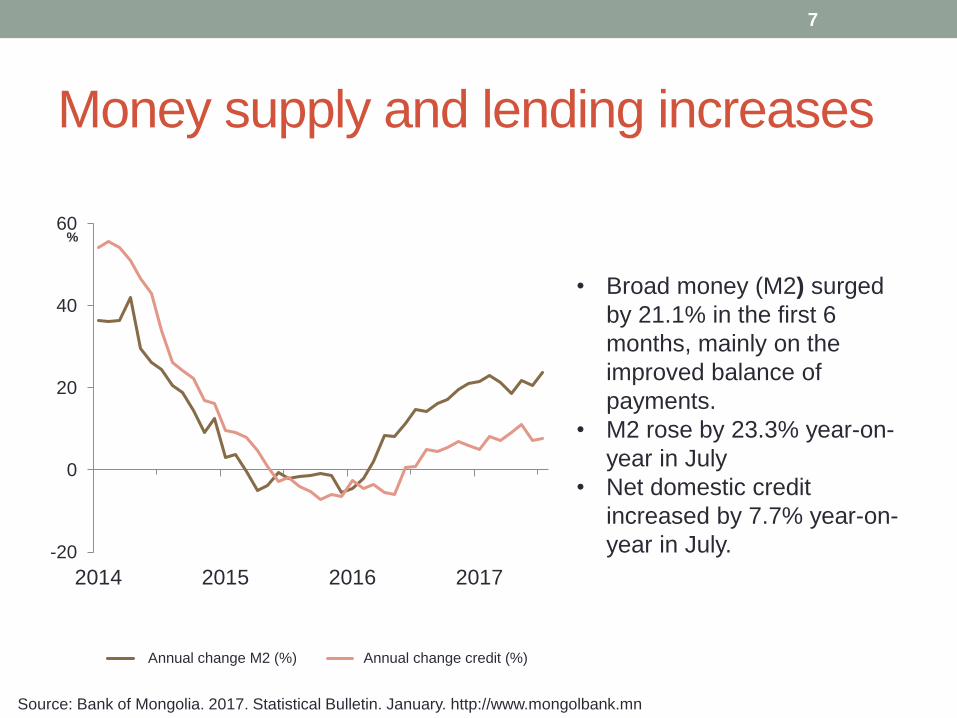

Money supply and lending increases

7

Source: Bank of Mongolia. 2017. Statistical Bulletin. January. http://www.mongolbank.mn

• Broad money (M2) surged

by 21.1% in the first 6

months, mainly on the

improved balance of

payments.

• M2 rose by 23.3% year-on-

year in July

• Net domestic credit

increased by 7.7% year-on-

year in July.-20

0

20

40

60

2014 2015 2016 2017

%

Annual change M2 (%) Annual change credit (%)

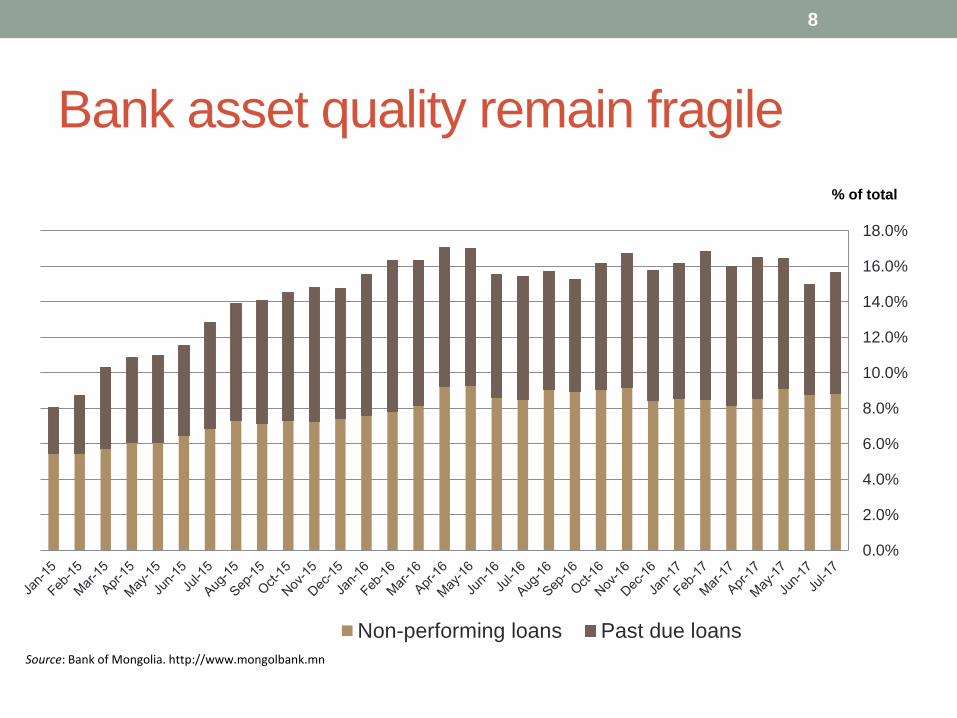

Bank asset quality remain fragile

8

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Non-performing loans Past due loans

% of total

Source: Bank of Mongolia. http://www.mongolbank.mn

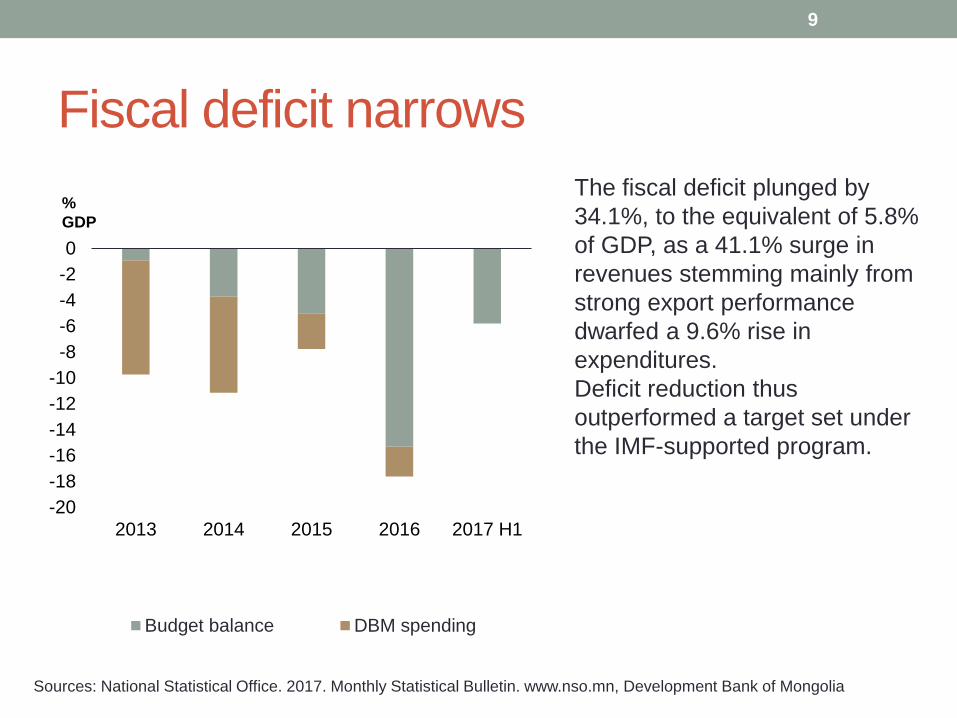

Fiscal deficit narrows

9

• The fiscal deficit plunged by

34.1%, to the equivalent of 5.8%

of GDP, as a 41.1% surge in

revenues stemming mainly from

strong export performance

dwarfed a 9.6% rise in

expenditures.

• Deficit reduction thus

outperformed a target set under

the IMF-supported program.

Sources: National Statistical Office. 2017. Monthly Statistical Bulletin. www.nso.mn, Development Bank of Mongolia

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

2013 2014 2015 2016 2017 H1

Budget balance DBM spending

%

GDP

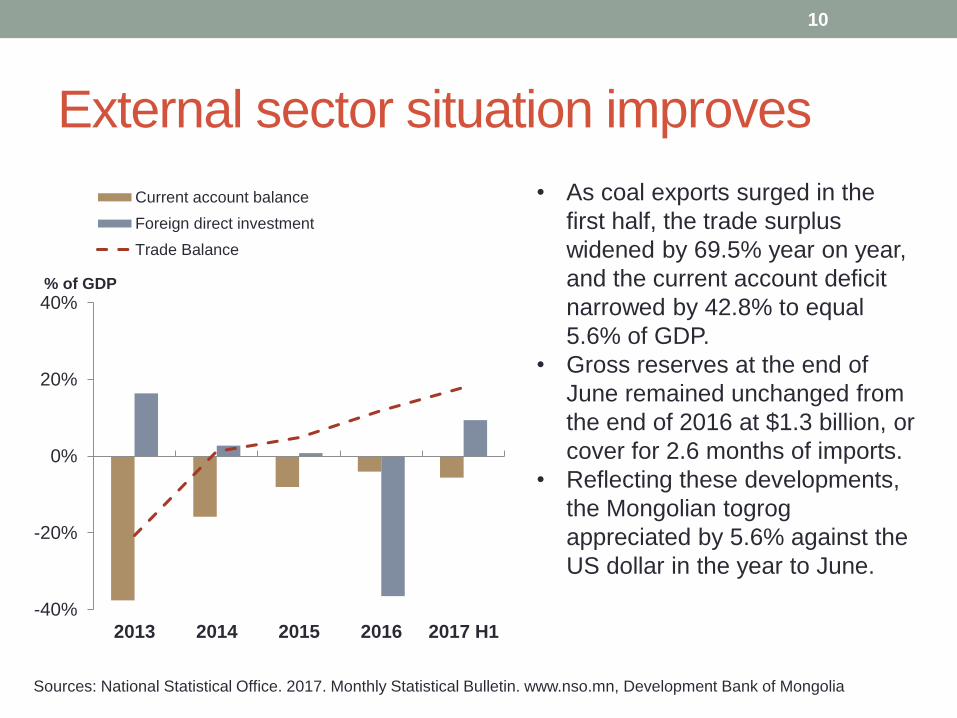

External sector situation improves

10

• As coal exports surged in the

first half, the trade surplus

widened by 69.5% year on year,

and the current account deficit

narrowed by 42.8% to equal

5.6% of GDP.

• Gross reserves at the end of

June remained unchanged from

the end of 2016 at $1.3 billion, or

cover for 2.6 months of imports.

• Reflecting these developments,

the Mongolian togrog

appreciated by 5.6% against the

US dollar in the year to June.

Sources: National Statistical Office. 2017. Monthly Statistical Bulletin. www.nso.mn, Development Bank of Mongolia

-40%

-20%

0%

20%

40%

2013 2014 2015 2016 2017 H1

% of GDP

Current account balance

Foreign direct investment

Trade Balance

Forecast

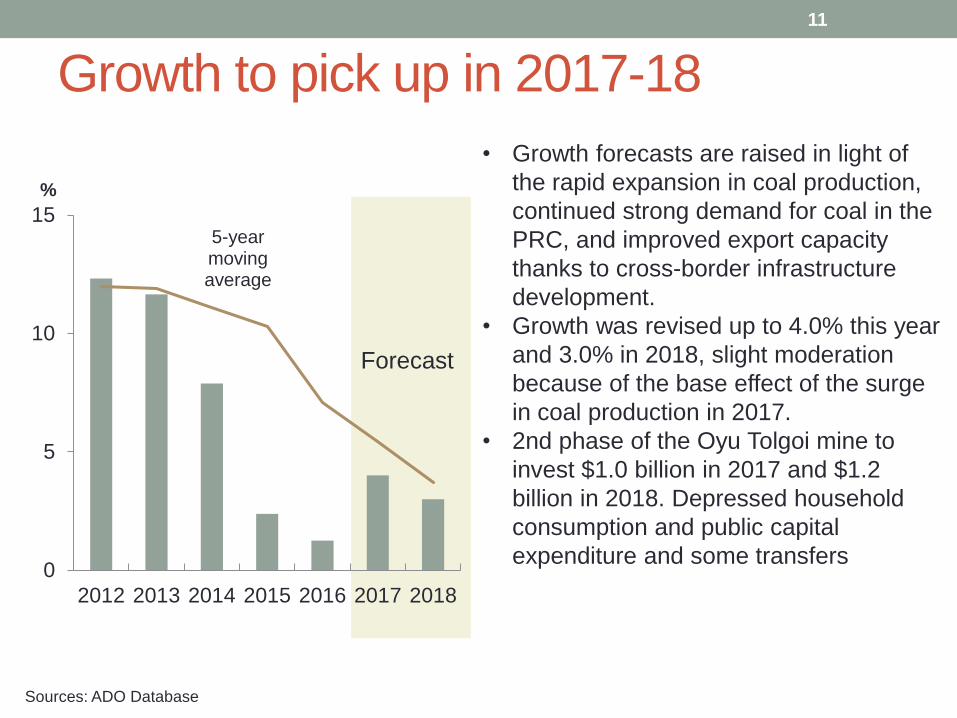

Growth to pick up in 2017-18

11

• Growth forecasts are raised in light of

the rapid expansion in coal production,

continued strong demand for coal in the

PRC, and improved export capacity

thanks to cross-border infrastructure

development.

• Growth was revised up to 4.0% this year

and 3.0% in 2018, slight moderation

because of the base effect of the surge

in coal production in 2017.

• 2nd phase of the Oyu Tolgoi mine to

invest $1.0 billion in 2017 and $1.2

billion in 2018. Depressed household

consumption and public capital

expenditure and some transfers

5-year moving average

0

5

10

15

2012 2013 2014 2015 2016 2017 2018

%

Sources: ADO Database

Forecast

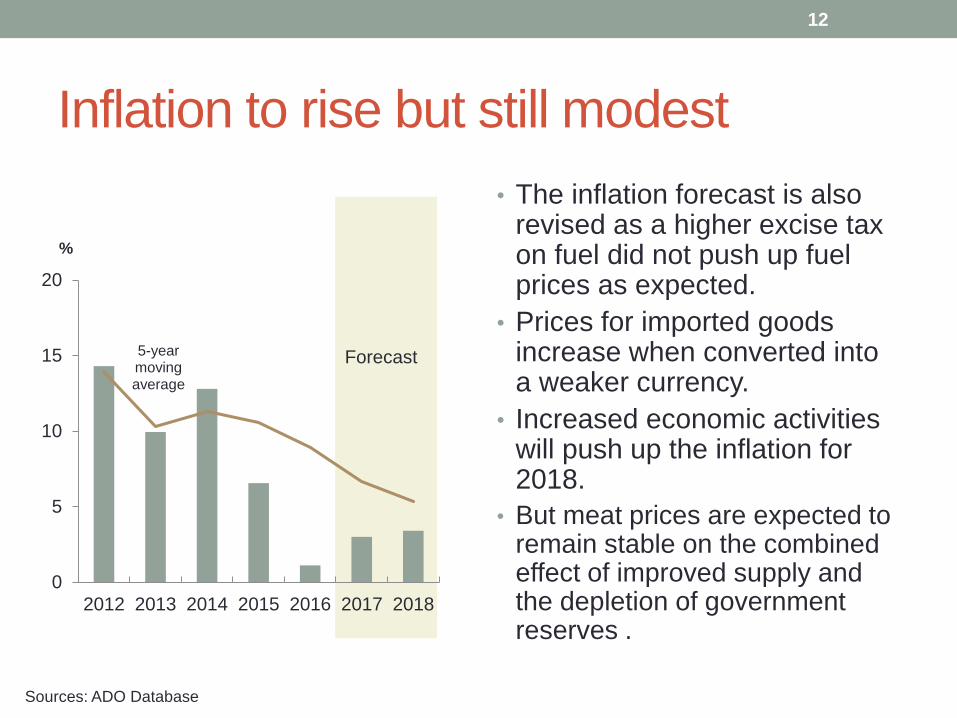

Inflation to rise but still modest

12

5-year moving average

0

5

10

15

20

2012 2013 2014 2015 2016 2017 2018

%

Sources: ADO Database

• The inflation forecast is also revised as a higher excise tax on fuel did not push up fuel prices as expected.

• Prices for imported goods increase when converted into a weaker currency.

• Increased economic activities will push up the inflation for 2018.

• But meat prices are expected to remain stable on the combined effect of improved supply and the depletion of government reserves .

Forecast

Current account deficit to increase with

capital imports

• The current account deficit was revised up to 6.4% of GDP in 2017 on strong mining related imports and widen further to 8.9% in 2018 as imports continue to expand while exports stabilize.

• The expected pickup in foreign direct investment will ease pressure on the balance of payments.

13

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

2013 2014 2015 2016 2017 2018%GDP

Sources: ADO Database

Risks remain

• Downside risks to the baseline forecasts include the economy’s vulnerability to commodity price swings and prevailing drought that may affect crop and livestock production;

• Political instability has caused some uncertainty around stabilization program;

• Upside risks are stronger growth in the PRC, shocks affecting its domestic coal supply, and rising copper prices;

• The same factors could undermine forecasts for inflation and the current account balance.

14

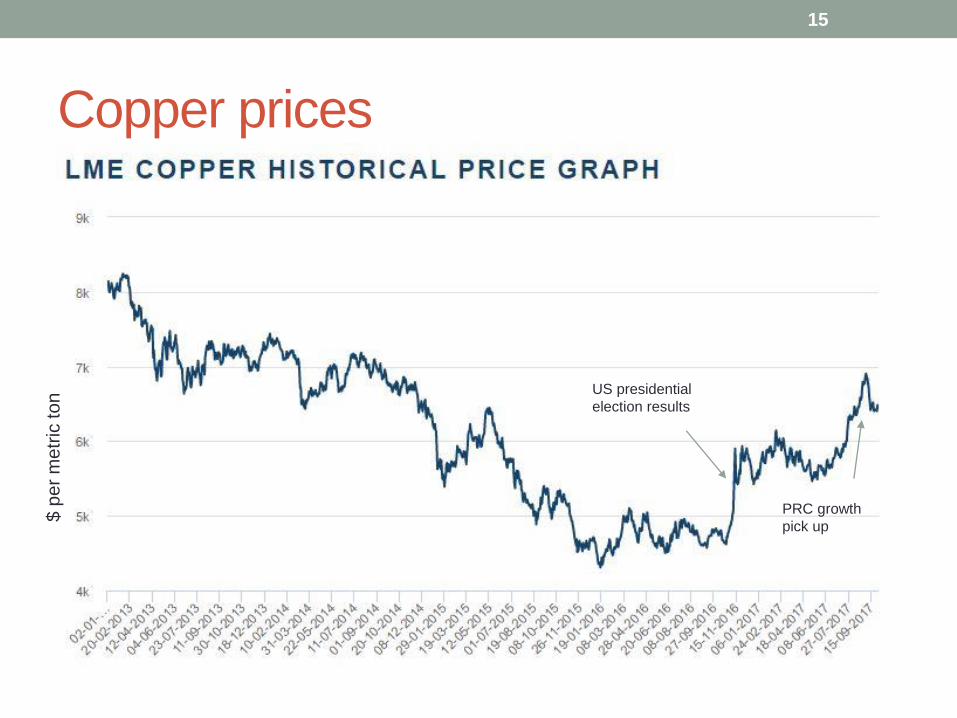

Copper prices

15

US presidential

election results

PRC growth

pick up

$ p

er

me

tric

to

n

PEOPLE’S REPUBLIC OF CHINA

16

Rebalancing progress amid controlled growth moderation

17

4

6

8

10

12

Q1 2015 Q3 Q1 2016 Q3 Q1 2017

%

Economic growth

Gross domestic product

Industrial sector value added

Retail sales

0

5

10

15

20

25

30

Jan2015 Jul Jan2016 Jul Jan2017 Aug

ytd, yoy %

Growth of fixed asset investment

Manufacturing Real Estate

0

2

4

6

8

10

2012 2013 2014 2015 2016 2017H1

Percentage points

Supply-side contributions to growth

Services

Industry

Agriculture

Gross domestic product

-3

0

3

6

9

2012 2013 2014 2015 2016 2017H1

Percentage points

Demand-side contributions to growth

Net exports

Investment

Consumption

Gross domestic product

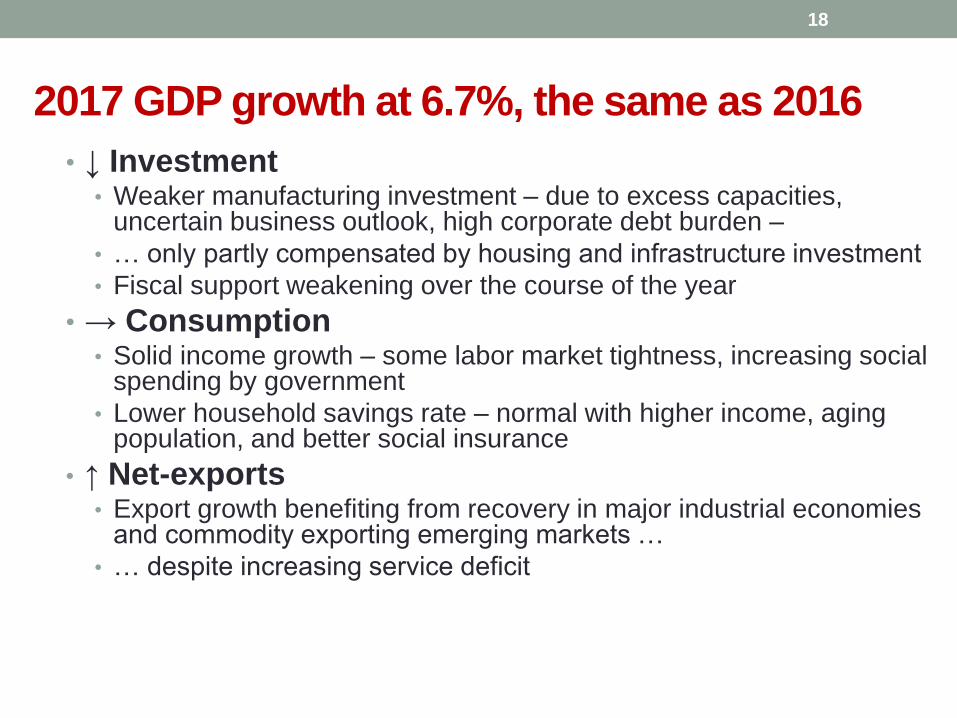

2017 GDP growth at 6.7%, the same as 2016

• ↓ Investment• Weaker manufacturing investment – due to excess capacities,

uncertain business outlook, high corporate debt burden –

• … only partly compensated by housing and infrastructure investment

• Fiscal support weakening over the course of the year

• → Consumption• Solid income growth – some labor market tightness, increasing social

spending by government

• Lower household savings rate – normal with higher income, aging population, and better social insurance

• ↑ Net-exports• Export growth benefiting from recovery in major industrial economies

and commodity exporting emerging markets …

• … despite increasing service deficit

18

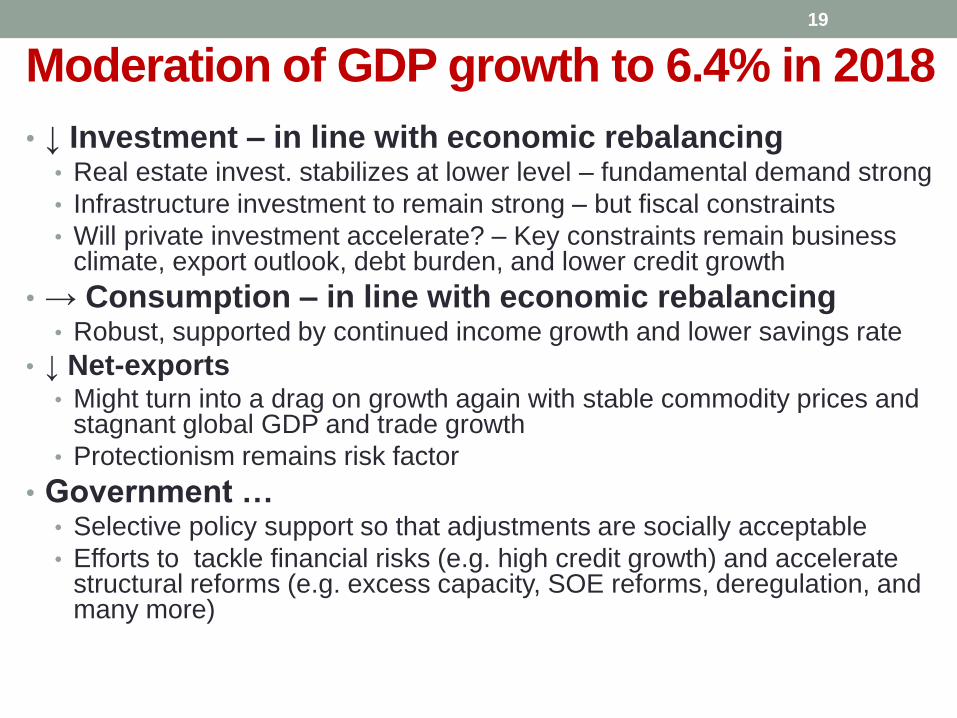

Moderation of GDP growth to 6.4% in 2018

• ↓ Investment – in line with economic rebalancing • Real estate invest. stabilizes at lower level – fundamental demand strong

• Infrastructure investment to remain strong – but fiscal constraints

• Will private investment accelerate? – Key constraints remain business climate, export outlook, debt burden, and lower credit growth

• → Consumption – in line with economic rebalancing• Robust, supported by continued income growth and lower savings rate

• ↓ Net-exports• Might turn into a drag on growth again with stable commodity prices and

stagnant global GDP and trade growth

• Protectionism remains risk factor

• Government … • Selective policy support so that adjustments are socially acceptable

• Efforts to tackle financial risks (e.g. high credit growth) and accelerate structural reforms (e.g. excess capacity, SOE reforms, deregulation, and many more)

19