Embed Size (px)

Citation preview

The “Checklist” > 2a. Estimation: Flexible Probabilities > Historical

Historical estimation with Flexible Probabilities

• Topic: non-parametric estimation of the invariants distribution and itsfeatures

• We generalize to the Flexible Probabilities the estimation approachbased on the Historical distribution

• We show how to generalize to the Flexible Probabilities othernon-parametric or semi-parametric approaches

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Canonical historical estimationThe historical scenarios with uniform probabilities {εt, pt ≡ 1

t}tt=1 define

the historical distribution, whose pdf and cdf read respectively

• Historical pdf

fHistε (x) ≡ 1

t

∑tt=1δ

(εt)(x) (2a.22)

• Historical cdfFHistε (x) ≡ 1

t

∑tt=1 1εt≤x (2a.27)

Glivenko-Cantelli theorem

“ lim ” t→∞ fHistε = fε (2a.23)

More formally

supx|FHistε (x)− Fε (x) | → 0 almost surely (2a.28)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Canonical historical estimationThe historical scenarios with uniform probabilities {εt, pt ≡ 1

t}tt=1 define

the historical distribution, whose pdf and cdf read respectively

• Historical pdf

fHistε (x) ≡ 1

t

∑tt=1δ

(εt)(x) (2a.22)

• Historical cdfFHistε (x) ≡ 1

t

∑tt=1 1εt≤x (2a.27)

Glivenko-Cantelli theorem

“ lim ” t→∞ fHistε = fε (2a.23)

More formally

supx|FHistε (x)− Fε (x) | → 0 almost surely (2a.28)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

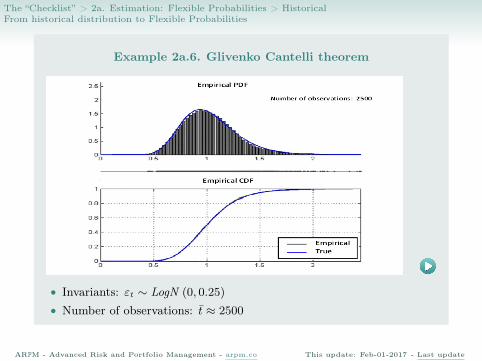

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Example 2a.6. Glivenko Cantelli theorem

• Invariants: εt ∼ LogN (0, 0.25)

• Number of observations: t ≈ 2500

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Generalization with Flexible Probabilities

The historical scenarios with Flexible Probabilities {εt, pt}tt=1 define theHistorical with Flexible Probabilities (HFP) distribution, whose pdf and cdfread respectively

• HFP pdffHFPε (x) ≡

∑tt=1 ptδ

(εt)(x) (2a.24)

• HFP cdfFHFPε (x) ≡

∑tt=1 pt1εt≤x (2a.26)

Generalized Glivenko-Cantelli theorem

“ lim ”ens(p)→∞ fHFPε = fε (2a.25)

where ens(p) is the Effective Number of Scenarios (2a.21).

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Generalization with Flexible Probabilities

The historical scenarios with Flexible Probabilities {εt, pt}tt=1 define theHistorical with Flexible Probabilities (HFP) distribution, whose pdf and cdfread respectively

• HFP pdffHFPε (x) ≡

∑tt=1 ptδ

(εt)(x) (2a.24)

• HFP cdfFHFPε (x) ≡

∑tt=1 pt1εt≤x (2a.26)

Generalized Glivenko-Cantelli theorem

“ lim ”ens(p)→∞ fHFPε = fε (2a.25)

where ens(p) is the Effective Number of Scenarios (2a.21).

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

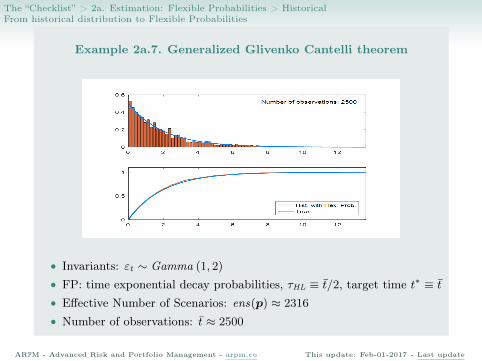

Example 2a.7. Generalized Glivenko Cantelli theorem

• Invariants: εt ∼ Gamma (1, 2)

• FP: time exponential decay probabilities, τHL ≡ t/2, target time t∗ ≡ t• Effective Number of Scenarios: ens(p) ≈ 2316

• Number of observations: t ≈ 2500

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Extracting Properties

A generic property θε ≡ S{εt} reads

θε = gS[fε] (2a.29)

for some functional gS.

How to estimate the properties of fε?

Historical with Flexible Probabilities (HFP) estimate

θHFP

ε ≡ SHFP{ε} (2a.33)

fHFPε ≈

ens(p)→∞fε

gS

y ygS

θHFP

ε ≈ens(p)→∞

θε

(2a.35)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalFrom historical distribution to Flexible Probabilities

Extracting Properties

A generic property θε ≡ S{εt} reads

θε = gS[fε] (2a.29)

for some functional gS.

How to estimate the properties of fε?

Historical with Flexible Probabilities (HFP) estimate

θHFP

ε ≡ SHFP{ε} (2a.33)

fHFPε ≈

ens(p)→∞fε

gS

y ygS

θHFP

ε ≈ens(p)→∞

θε

(2a.35)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

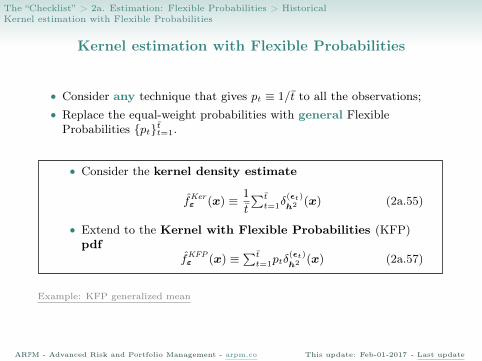

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalKernel estimation with Flexible Probabilities

Kernel estimation with Flexible Probabilities

• Consider any technique that gives pt ≡ 1/t to all the observations;• Replace the equal-weight probabilities with general FlexibleProbabilities {pt}tt=1.

• Consider the kernel density estimate

fKerε (x) ≡ 1

t

∑tt=1δ

(εt)

h2 (x) (2a.55)

• Extend to the Kernel with Flexible Probabilities (KFP)pdf

fKFPε (x) ≡

∑tt=1ptδ

(εt)

h2 (x) (2a.57)

Example: KFP generalized mean

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update

The “Checklist” > 2a. Estimation: Flexible Probabilities > HistoricalKernel estimation with Flexible Probabilities

Kernel estimation with Flexible Probabilities

• Consider any technique that gives pt ≡ 1/t to all the observations;• Replace the equal-weight probabilities with general FlexibleProbabilities {pt}tt=1.

• Consider the kernel density estimate

fKerε (x) ≡ 1

t

∑tt=1δ

(εt)

h2 (x) (2a.55)

• Extend to the Kernel with Flexible Probabilities (KFP)pdf

fKFPε (x) ≡

∑tt=1ptδ

(εt)

h2 (x) (2a.57)

Example: KFP generalized mean

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Feb-01-2017 - Last update