Embed Size (px)

Citation preview

Are you ready for the new reality?

What is really going to happen to the health insurance market?

The Fine Print

Copyright

No part of this presentation may be reproduced or transmitted in any form without the written permission of the author.

Disclaimer

This presentation was diligently researched and compiled with the intent to provide information for persons wishing to learn about the landscape

of health insurance reform and the opportunities they present. Throughout the making of this consumer presentation , every effort has been

made to ensure the highest amount of accuracy and effectiveness for the techniques suggested by the author. The presentation may contain

contextual as well as typographical mistakes.

No information provided in this presentation constitutes a warranty of any kind; nor shall readers of this presentation rely solely on any such

information or advice. All content, products, and services are not to be considered as legal, medical, or professional advice and are to be used

for personal use and information purposes only. This presentation makes no warranties or guarantees express or implied, as to the results

provided by the strategies, techniques, and advice presented in this presentation. The publishers of this presentation expressly disclaim any

liability arising from any strategies, techniques, and advice presented in this presentation.

The purpose of this consumer presentation is to educate and guide. Neither the publisher nor the author warrant that the information contained

within this consumer presentation is free of omissions or errors and is fully complete. Furthermore, neither the publisher nor the author shall

have responsibility or liability to any entity or person as a result of any damage or loss alleged to be caused or caused indirectly or directly by

this presentation.

Safe Harbor Notice

Certain statements in this presentation relate to future results that are forward-looking statements as defined in the Private Securities Litigation

Reform Act of 1995. This presentation contains statements involving risks and uncertainties, including statements relating market opportunity

and future business prospects. Actual results may differ materially and presentation results should not be considered as an indication of future

performance. Factors that could cause actual results to differ are not included.

Eric Johnson Founder, Comedy CE.com

Director of Education,

Health Partners America

Josh Hilgers President,

Health Partners America

As seen in:

• Employee Benefits Adviser

• Benefits Selling Magazine

• Leader’s Edge

• CDHC Solutions

Agenda

Future of small group insurance

Exchanges 101

Options employers are likely to pursue

Confusion around government subsidies available through private

exchanges

Current approach of most industry “experts”

Definition of Small Group

It’s changing January 1, 2014

PPACA Section 1304(b)

Source: Patient Protection and Affordable Care Act

1-100

PPACA Section 1304(b)

Source: Patient Protection and Affordable Care Act

1-50

Small Group Premiums

Cost Sharing Limits

Essential Benefits

Modified Adjusted Community Rating

Cost Sharing Limits

First renewal on or after January 1, 2014

3 types of cost-sharing limits are required:

1. Actuarial value requirements (metallic levels)

2. Out-of-pocket limits

3. Deductible limits

Actuarial Value

Source: PPACA Section 1302(d)

90% 80% 70% 60%

“Metallic” Plans

Copyright 2013, Health Partners America. All Rights Reserved. No duplication, in whole or in part, permitted without expressed written consent.

Cost Sharing Subsidies: Actuarial Value Increased

(but not in the group market)

Source: http://www.kff.org/healthreform/upload/7962-02.pdf

Out of Pocket Limit

Under the ACA, out-of-pocket limits for health plans are subject to the

limit that currently applies to health savings account qualified health

plans.

In 2014, the limits are expected to be:

$6,350 for single coverage and

$12,500 for family coverage

OOP Limit Will Make HSAs More Attractive

This may require a reduction in OOP

exposure for some copay plans

The family limit on copay plans will

be reduced from 3x to 2x

This requirement should result in a

bigger price separation between

HSA-qualified plans and traditional

copay plans since HSAs already

meet the OOP max requirement,

which will lead to higher HSA

enrollment.

Cost Sharing Subsidies: OOP Max Reduced

(but not in the group market)

Source: http://www.kff.org/healthreform/upload/7962-02.pdf

250% 20%

Deductible Limits

$2,000 single / $4,000 family deductible maximum

Applies to small group market only

Source: http://housedocs.house.gov/energycommerce/ppacacon.pdf

Deductible Limits

Higher deductible allowed with FSA, HRA, or HSA

Source: http://housedocs.house.gov/energycommerce/ppacacon.pdf

No longer applies – HHS is not going to allow a plan design with

higher deductibles offset by contributions to tax-advantaged

accounts to comply with the deductible max provision.

Deductible Limits

Deductible limit cannot impact actuarial value of bronze level plan.

Source: http://housedocs.house.gov/energycommerce/ppacacon.pdf

Is it even possible to design a plan that will meet the requirements?

Deductible Limits

Higher Deductibles Permitted if…

“a plan may exceed the annual deductible limit

if it cannot reasonably reach a given level of

coverage (metal tier) without doing so.”

Source: http://www.gpo.gov/fdsys/pkg/FR-2013-02-25/pdf/2013-04084.pdf

Copyright 2013, Health Partners America. All Rights Reserved. No duplication, in whole or in part, permitted without expressed written consent.

Source: http://www.kff.org/kaiserpolls/upload/8321-F.pdf

Welcomed Relief

Essential Benefits

First renewal on or after January 1, 2014

What are essential benefits?

Essential Benefits = Mandates

Copyright 2013, Health Partners America. All Rights Reserved. No duplication, in whole or in part, permitted without expressed written consent.

What are essential benefits?

Copyright 2013, Health Partners America. All Rights Reserved. No duplication, in whole or in part, permitted without expressed written consent.

Include Pediatric Dental & Vision

Copyright 2013, Health Partners America. All Rights Reserved. No duplication, in whole or in part, permitted without expressed written consent.

Modified Adjusted Community Rating

First renewal on or after January 1, 2014

What is modified community rating?

In contrast with community rating, in which an insurer evaluates the risk

factors of an entire market area (not those of any one individual person)

when determining insurance premiums, modified community rating

allows for premium variation based on individual risk factors, with some

limitations.

This concept helps maintain price fairness among high-risk individuals

and the rest of the population as costs are spread across a group of

people.

Source: http://www.bcbsm.com/content/microsites/health-care-reform/en/reform-alerts/cms-issues-proposed-rule-modified-community-rating.html

State-Specific Example – Texas

Small group rating is a two step process in Texas.

1. Actuaries rate based on case characteristics

• Group size (20% variation allowed)

• Industry (15% variation allowed)

• Age mix of group

• Gender mix of group

• Location

2. Underwriters rate based on risk characteristics

• Medical conditions

• Longevity with carrier

• Other risk characteristics

• “Rate up” of 67% allowed year one and 15% at renewal time

Note: These rules do not currently apply to the individual market in Texas.

How are the rules changing?

New “Modified Adjusted Community Rating” Requirements

1. Actuaries rate based on case characteristics

• Group size (20% variation allowed)

• Industry (15% variation allowed)

• Age mix of group

• Gender mix of group

• Location

2. Underwriters rate based on risk characteristics

• Medical conditions

• Longevity with carrier

• Other risk characteristics

• “Rate up” of 67% allowed year one and 15% at renewal time

Note: These rules will apply to plans in the small group and individual markets.

3 to 1 basis

lifestyle choices

Premium Variations only allowed for:

Age (3 to 1)

(Most states are currently 5 to 1 or more)

Premium Variations only allowed for:

Age (3 to 1)

Tobacco use (1.5 to 1)

• Any type of tobacco • 4 days per week or more • Excludes use for religious purposes • Does not have to be applied evenly

across age bands

Premium Variations only allowed for:

Age (3 to 1)

Tobacco use (1.5 to 1)

Family composition

Can rate for all adults over age 21 + the 3 oldest children under age 21

Premium Variations only allowed for:

Age (3 to 1)

Tobacco use (1.5 to 1)

Family composition

Geographic Regions to be

defined by the states

Up to 7 regions

Premium Variations only allowed for:

Age (3 to 1)

Tobacco use (1.5 to 1)

Family composition

Geographic Regions

Wellness discounts

(up to 50%)

• Up to 30% discount • Additional 20% if participating in

tobacco cessation program

Premium Variations only allowed for:

Age (3 to 1)

Tobacco use (1.5 to 1)

Family composition

Geographic Regions

Wellness discounts (up to 50%)

Cannot rate based on health

or gender

Add it up…

"Well you can take a swag at it by adding up the values:

4% premium taxes

4-11% product increase

25% rating rules increase for healthiest groups

Add another 12% for just the regular trend increase

So you get 25-50% rate increase in the small group market."

–Anonymous Carrier Executive

Regulatory Burden on Employers

Copyright 2013, Health Partners America. All Rights Reserved. No duplication, in whole or in part, permitted without expressed written consent.

Things are Changing

Offering group health benefits could soon repel employees.

2013 Federal Poverty Guidelines

Household Size 100% 133% 150% 200% 300% 400%

1 $11,490 $15,282 $17,235 $22,980 $34,470 $45,960

2 $15,510 $20,628 $23,265 $31,020 $46,530 $62,040

3 $19,530 $25,975 $29,295 $39,060 $58,590 $78,120

4 $23,550 $31,322 $35,325 $47,100 $70,650 $94,200

5 $27,570 $36,668 $41,355 $55,140 $82,710 $110,280

6 $31,590 $42,015 $47,385 $63,180 $94,770 $126,360

7 $35,610 $47,361 $53,415 $71,220 $106,830 $142,440

8 $39,630 $52,708 $59,445 $79,260 $118,890 $158,520

Each extra person $4,020 $5,347 $6,030 $8,040 $12,060 $16,080

48 Contiguous States and DC

Source: http://www.familiesusa.org/resources/tools-for-advocates/guides/federal-poverty-guidelines.html

Premium & Cost Sharing Illustration – Single

Source: http://publications.milliman.com/publications/healthreform/pdfs/ten-critical-considerations.pdf

2011 Survey: 30% of Employers will drop coverage

An Example

Family of 4 making $55k a year

• Single Premium: $5,400 ($450 per month)

• Family Premium: $14,556 ($1,213 per month)

Employer

Contribution

Employee

Contribution

Government

Contribution

Minimum ER

contribution

(9.5% W-2) $175 $14,381 $0

Income: $55k EO: $5,400 EF: $14,556

Employer

Contribution

Employee

Contribution

Government

Contribution

Minimum ER

contribution

(9.5% W-2) $175 $14,381 $0

50% of single $2,700 $11,856 $0

Income: $55k EO: $5,400 EF: $14,556

Employer

Contribution

Employee

Contribution

Government

Contribution

Minimum ER

contribution

(9.5% W-2) $175 $14,381 $0

50% of single $2,700 $11,856 $0

100% of single $5,400 $9,156 $0

Income: $55k EO: $5,400 EF: $14,556

Employer

Contribution

Employee

Contribution

Government

Contribution

Minimum ER

contribution

(9.5% W-2) $175 $14,381 $0

50% of single $2,700 $11,856 $0

100% of single $5,400 $9,156 $0

50% of family $7,278 $7,278 $0

Income: $55k EO: $5,400 EF: $14,556

Employer

Contribution

Employee

Contribution

Government

Contribution

Minimum ER

contribution

(9.5% W-2) $175 $14,381 $0

50% of single $2,700 $11,856 $0

100% of single $5,400 $9,156 $0

50% of family $7,278 $7,278 $0

No group

coverage $0/2k $4,135 $10,421

Income: $55k EO: $5,400 EF: $14,556

Bottom Line

Small group is getting more expensive

• Small group undefined

• Cost sharing increased

• Rating changing

Regulations are burdensome

Value to employees is decreasing

• Subsidies cannot be accessed if employer offers insurance

Employers must choose who to protect

Who do you save –

your higher paid workers or

your lower paid workers?

101 EXCHANGES

Private Exchange Public Exchange

Single

Carrier

Group

Multi Carrier

Group,

employer

chooses

carrier

Multi Carrier

Group,

consumer

chooses

carrier

Small Group SHOP Exchange

Single Carrier Group

ABC Health Plan 1

ABC Health Plan 2

ABC Health Plan 3

ABC Health Plan 4

ABC Health Plan 5

ABC Health Plan 6

ABC Health Plan 7

ABC Health Plan 8

Single Carrier Group

Multi Carrier Group,

employer chooses carrier

ABC Health Plan 1

ABC Health Plan 2

XYZ Health Plan 1

XYZ Health Plan 2

XYZ Health Plan 3

ACME Health Plan 1

ACME Health Plan 2

Vandalay Health Plan 8

Single Carrier Group

Multi Carrier Group,

employer chooses carrier

ABC Health Plan 1

ABC Health Plan 2

XYZ Health Plan 1

XYZ Health Plan 2

XYZ Health Plan 3

ACME Health Plan 1

ACME Health Plan 2

Vandalay Health Plan 8

Multi Carrier Group,

consumer chooses carrier

Private Exchange Public Exchange

Single

Carrier

Group

Multi Carrier

Group,

employer

chooses

carrier

Multi Carrier

Group,

consumer

chooses

carrier

Small Group SHOP Exchange

Single Carrier

Individual

Multi Carrier

Individual

Individual

State/Federal Exchange

(FFE in SC)

Single Carrier,

based on zip code

ABC Health Plan 1

ABC Health Plan 2

ABC Health Plan 3

ABC Health Plan 4

ABC Health Plan 5

ABC Health Plan 6

ABC Health Plan 7

ABC Health Plan 8

Single Carrier,

based on zip code

Multi Carrier,

Based on zip code

ABC Health Plan 1

ABC Health Plan 2

XYZ Health Plan 1

XYZ Health Plan 2

XYZ Health Plan 3

ACME Health Plan 1

ACME Health Plan 2

Vandalay Health Plan 8

Pending state-level guidance

regarding Web Based Entities

(WBE)

Single Carrier,

based on zip code

Multi Carrier,

Based on zip code

Qualified Health Plans

(QHP)

for that state

Private Exchange Public Exchange

Single

Carrier

Group

Multi Carrier

Group,

employer

chooses

carrier

Multi Carrier

Group,

consumer

chooses

carrier

Small Group SHOP Exchange

Single Carrier

Individual

Multi Carrier

Individual

Individual

State/Federal Exchange

(FFE in SC) We

b B

as

ed

En

titi

es

(W

BE

)

Options Employers may pursue

* Limited Data Available

Government

subsidies

Exchange

Involvement

Reimbursement/

Spending

Accounts

Employer

Sponsored Plan

Options

Offer nothing

ACA Implications

Private Exchange

with Individual

Products

Private Exchange with

Individual Products

and Cafeteria Plan

Private Exchange with

Individual Products

and Group Products

Private Exchange with

Individual Products,

Group Products, and

Cafeteria Plan

Available to EEs

making less than

400% FPL

Available to EEs

making less than 400%

FPL

Available to EEs making

less than 400% FPL

Available to EEs making

less than 400% FPL – if

group health doesn’t

meet requirements

Not offered Not offered

Cafeteria plan

ER contributions an

option

Employer sponsored

products: health,

dental, vision, life, DI,

accident, CI

Cafeteria plan

Employer sponsored

products: health, dental,

vision, life, DI, accident, CI

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

exchange

HPA exchange

branded for ER,

Agency or

Organization

HPA exchange branded

for ER, Agency or

Organization.

Specific instructions,

forms, links for TPA

offerings

HPA exchange branded

for ER, Agency or

Organization.

Links to Bswift for group

offerings

HPA exchange branded for

ER, Agency or

Organization.

Specific instructions, forms,

links for TPA offerings.

Links to Bswift for group

offerings

None None

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

None

Available to EEs making

less than 400% FPL – if

group health doesn’t meet

requirements

If group health is option, no

penalty if it meets requirements

Employer Option >

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

If group health is option, no

penalty if it meets requirements

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

subsidies

Exchange

Involvement

Reimbursement/

Spending

Accounts

Employer

Sponsored Plan

Options

Offer nothing

ACA Implications

Private Exchange

with Individual

Products

Private Exchange with

Individual Products

and Cafeteria Plan

Private Exchange with

Individual Products

and Group Products

Private Exchange with

Individual Products,

Group Products, and

Cafeteria Plan

Available to EEs

making less than

400% FPL

Available to EEs

making less than 400%

FPL

Available to EEs making

less than 400% FPL

Available to EEs making

less than 400% FPL – if

group health doesn’t

meet requirements

Not offered Not offered

Cafeteria plan

ER contributions an

option

Employer sponsored

products: health,

dental, vision, life, DI,

accident, CI

Cafeteria plan

Employer sponsored

products: health, dental,

vision, life, DI, accident, CI

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

exchange

HPA exchange

branded for ER,

Agency or

Organization

HPA exchange branded

for ER, Agency or

Organization.

Specific instructions,

forms, links for TPA

offerings

HPA exchange branded

for ER, Agency or

Organization.

Links to Bswift for group

offerings

HPA exchange branded for

ER, Agency or

Organization.

Specific instructions, forms,

links for TPA offerings.

Links to Bswift for group

offerings

None None

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

None

Available to EEs making

less than 400% FPL – if

group health doesn’t meet

requirements

If group health is option, no

penalty if it meets requirements

Employer Option >

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

If group health is option, no

penalty if it meets requirements

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

subsidies

Exchange

Involvement

Reimbursement/

Spending

Accounts

Employer

Sponsored Plan

Options

Offer nothing

ACA Implications

Private Exchange

with Individual

Products

Private Exchange with

Individual Products

and Cafeteria Plan

Private Exchange with

Individual Products

and Group Products

Private Exchange with

Individual Products,

Group Products, and

Cafeteria Plan

Available to EEs

making less than

400% FPL

Available to EEs

making less than 400%

FPL

Available to EEs making

less than 400% FPL

Available to EEs making

less than 400% FPL – if

group health doesn’t

meet requirements

Not offered Not offered

Cafeteria plan

ER contributions an

option

Employer sponsored

products: health,

dental, vision, life, DI,

accident, CI

Cafeteria plan

Employer sponsored

products: health, dental,

vision, life, DI, accident, CI

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

exchange

HPA exchange

branded for ER,

Agency or

Organization

HPA exchange branded

for ER, Agency or

Organization.

Specific instructions,

forms, links for TPA

offerings

HPA exchange branded

for ER, Agency or

Organization.

Links to Bswift for group

offerings

HPA exchange branded for

ER, Agency or

Organization.

Specific instructions, forms,

links for TPA offerings.

Links to Bswift for group

offerings

None None

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

None

Available to EEs making

less than 400% FPL – if

group health doesn’t meet

requirements

If group health is option, no

penalty if it meets requirements

Employer Option >

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

If group health is option, no

penalty if it meets requirements

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

subsidies

Exchange

Involvement

Reimbursement/

Spending

Accounts

Employer

Sponsored Plan

Options

Offer nothing

ACA Implications

Private Exchange

with Individual

Products

Private Exchange with

Individual Products

and Cafeteria Plan

Private Exchange with

Individual Products

and Group Products

Private Exchange with

Individual Products,

Group Products, and

Cafeteria Plan

Available to EEs

making less than

400% FPL

Available to EEs

making less than 400%

FPL

Available to EEs making

less than 400% FPL

Available to EEs making

less than 400% FPL – if

group health doesn’t

meet requirements

Not offered Not offered

Cafeteria plan

ER contributions an

option

Employer sponsored

products: health,

dental, vision, life, DI,

accident, CI

Cafeteria plan

Employer sponsored

products: health, dental,

vision, life, DI, accident, CI

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

exchange

HPA exchange

branded for ER,

Agency or

Organization

HPA exchange branded

for ER, Agency or

Organization.

Specific instructions,

forms, links for TPA

offerings

HPA exchange branded

for ER, Agency or

Organization.

Links to Bswift for group

offerings

HPA exchange branded for

ER, Agency or

Organization.

Specific instructions, forms,

links for TPA offerings.

Links to Bswift for group

offerings

None None

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

None

Available to EEs making

less than 400% FPL – if

group health doesn’t meet

requirements

If group health is option, no

penalty if it meets requirements

Employer Option >

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

If group health is option, no

penalty if it meets requirements

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

subsidies

Exchange

Involvement

Reimbursement/

Spending

Accounts

Employer

Sponsored Plan

Options

Offer nothing

ACA Implications

Private Exchange

with Individual

Products

Private Exchange with

Individual Products

and Cafeteria Plan

Private Exchange with

Individual Products

and Group Products

Private Exchange with

Individual Products,

Group Products, and

Cafeteria Plan

Available to EEs

making less than

400% FPL

Available to EEs

making less than 400%

FPL

Available to EEs making

less than 400% FPL

Available to EEs making

less than 400% FPL – if

group health doesn’t

meet requirements

Not offered Not offered

Cafeteria plan

ER contributions an

option

Employer sponsored

products: health,

dental, vision, life, DI,

accident, CI

Cafeteria plan

Employer sponsored

products: health, dental,

vision, life, DI, accident, CI

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

exchange

HPA exchange

branded for ER,

Agency or

Organization

HPA exchange branded

for ER, Agency or

Organization.

Specific instructions,

forms, links for TPA

offerings

HPA exchange branded

for ER, Agency or

Organization.

Links to Bswift for group

offerings

HPA exchange branded for

ER, Agency or

Organization.

Specific instructions, forms,

links for TPA offerings.

Links to Bswift for group

offerings

None None

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

None

Available to EEs making

less than 400% FPL – if

group health doesn’t meet

requirements

If group health is option, no

penalty if it meets requirements

Employer Option >

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

If group health is option, no

penalty if it meets requirements

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

subsidies

Exchange

Involvement

Reimbursement/

Spending

Accounts

Employer

Sponsored Plan

Options

Offer nothing

ACA Implications

Private Exchange

with Individual

Products

Private Exchange with

Individual Products

and Cafeteria Plan

Private Exchange with

Individual Products

and Group Products

Private Exchange with

Individual Products,

Group Products, and

Cafeteria Plan

Available to EEs

making less than

400% FPL

Available to EEs

making less than 400%

FPL

Available to EEs making

less than 400% FPL

Available to EEs making

less than 400% FPL – if

group health doesn’t

meet requirements

Not offered Not offered

Cafeteria plan

ER contributions an

option

Employer sponsored

products: health,

dental, vision, life, DI,

accident, CI

Cafeteria plan

Employer sponsored

products: health, dental,

vision, life, DI, accident, CI

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Government

exchange

HPA exchange

branded for ER,

Agency or

Organization

HPA exchange branded

for ER, Agency or

Organization.

Specific instructions,

forms, links for TPA

offerings

HPA exchange branded

for ER, Agency or

Organization.

Links to Bswift for group

offerings

HPA exchange branded for

ER, Agency or

Organization.

Specific instructions, forms,

links for TPA offerings.

Links to Bswift for group

offerings

None None

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

None

Available to EEs making

less than 400% FPL – if

group health doesn’t meet

requirements

If group health is option, no

penalty if it meets requirements

Employer Option >

Ind. MM premium

reimbursement –

HRA/PRA

OOP med expenses –

FSA/HSA/DCA

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

If group health is option, no

penalty if it meets requirements

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

< 50 FTE – No penalty

> 50 FTE Penalty of

$2k per full time EE

minus first 30

Impact on Employers

Employer under 50 FTE:

Financial

Admin./Regs.

Other

Employer with 50+ FTEs:

Financial

Admin./Regs.

Other

Current insurance costs, projected insurance costs, waived

employees, and income levels will drive insurance decisions:

2014 Adjusted Pre Reform Cost

Waived Employees & Inflation

Baseline Insurance, Compensation Cost, & Hours

Retain Insurance No Insurance

Key Employee Groups

Large

Exchange

Subsidy

Eligibles

Expanded

Medicaid

Small

Exchange

Subsidy

Eligibles

No

Exchange

Subsidy

Eligibles

Health

Reform

Impact

Pay or Play Summary:

Executive Summary – Employer Impact

Below displays the impact walk through for xyz company

based on the points in time & assumptions discussed:

$485,000

$628,000

$745,000 $745,000

$206,000

Baseline BL Inflated BL Adjusted Retain Insurance No Insurance

Employer Cost

2011 Baseline Plus Inflation Plus Waived Retain Insurance No Insurance

Case Study courtesy

of Eide Bailly

$234,000 $303,000

$365,000 $365,000

$515,000

Baseline BL Inflated BL Adjusted Retain Insurance No Insurance

Employee Cost

2011 Baseline Plus Inflation Plus Waived Retain Insurance No Insurance

Pay or Play Summary:

Executive Summary – Employee Impact

Below displays the impacts to xyz company’s employees

based on the points in time & assumptions discussed:

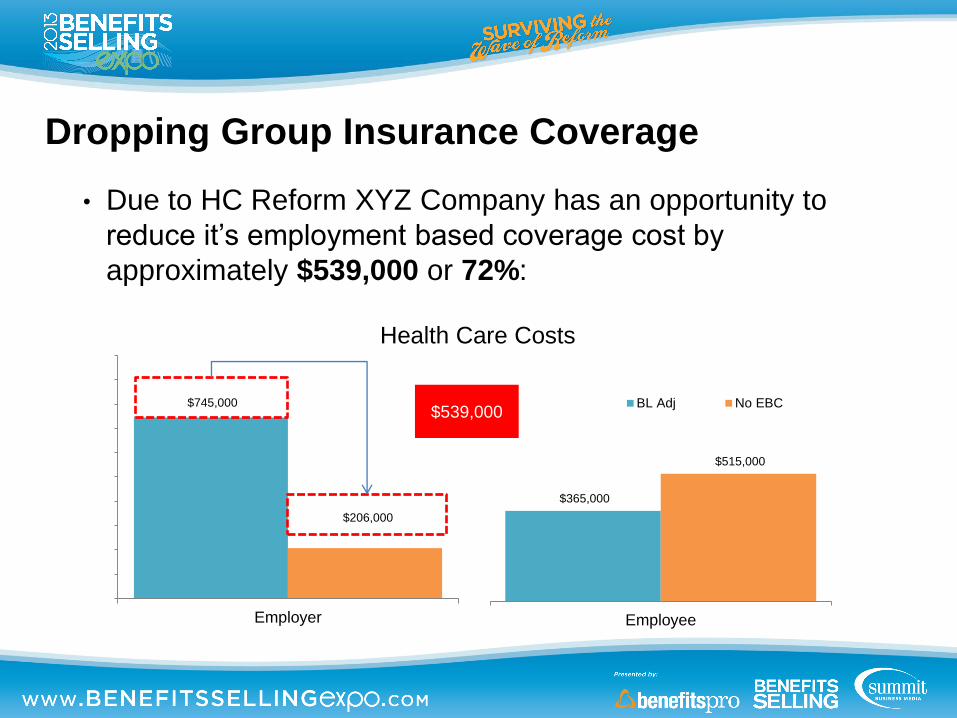

Dropping Group Insurance Coverage

$365,000

$515,000

Employee

Health Care Costs

BL Adj No EBC $745,000

$206,000

Employer

• Due to HC Reform XYZ Company has an opportunity to

reduce it’s employment based coverage cost by

approximately $539,000 or 72%:

$539,000

Defined Contribution Plan

• Impact to a company and employees of changing health

insurance to a defined contribution plan $389,000 or 52%:

$365,000 $365,000

Employee

Health Care Costs

BL Adj Adj DCP

$745,000

$356,000

Employer

$389,000

Defined Contribution Plan

• By going to a defined contribution plan, an employer

can gain better control and make employees whole in a

health reform environment:

BL Adj, $745,000

No EBC, 206,000

Adj DCP, $356,000

Employer

Employer health care cost

• Assumes $150,000 is placed in a pre-tax

defined contribution plan

• Employees can access either public or

private exchanges

• $389,000 savings while making

employees whole (same benefit as 2014

pre reform)

Impact on Employees

Individual premiums are also going up – BUT:

Deductible options can keep premiums lower

Subsidies will offset for many (63-68% of all Americans)

Alternative coverage options exist (ex. STM)

Employees under 400% FPL:

Financial

Admin./Regs.

Other

Employees 400% to 600% (approx) FPL:

Financial

Admin./Regs.

Other

Impact on Employees

Variables

Inputs Net savings after tax penalty

Family status Family of 4

Household income $100,000

Annual cost for Bronze Plan $12,000

Government subsidy $0

Net cost after subsidy $12,000

Hii 12 month STM annual cost $3,600

Annual savings for STM $8,400

Tax penalty in 2014 (1%) $0 $8,400

Above $98,000

(4x FPL in 2016)

this family would likely

have to pay more than

8% of its income for a

bronze insurance plan

and would therefore

be exempt from the

mandate.

Exemption if Premium Exceeds 8% of MAGI

Impact on Employees

Variables

Inputs Net savings after tax penalty

Family status Family of 4

Household income $100,000

Annual cost for Bronze Plan $12,000

Government subsidy $0

Net cost after subsidy $12,000

Hii 12 month STM annual cost $3,600

Annual savings for STM $8,400

Tax penalty in 2014 (1%) $0 $8,400

Variables

Inputs Net savings after tax penalty

Family status Family of 4

Household income $300,000

Annual cost for Bronze Plan $12,000

Government subsidy $0

Net cost after subsidy $12,000

Hii 12 month STM annual cost $3,600

Annual savings for STM $8,400

Tax penalty in 2014 (1%) $3,000 $5,400

Tax penalty in 2015 (2%) $6,000 $2,400

Tax penalty in 2016 (2.5%) $7,500 $900

Impact on Broker

Revenues changing but still there

Shift in roll to provide more strategy to Employers of using alternative

benefit structures to attract and retain employees

Private Exchange Broker Blueprint webinar models this out

Insurance Broker:

Financial

Admin./Regs.

Other

Common Question

Will the federal Subsidies be available through

Private Exchanges?

Lots of Articles about HHS Guidance

Game-Changing Decision by HHS

Government Subsidies through Private Exchanges

Cindy Gillespie, a former advisor to Mitt Romney:

"the bottom line of this new model is that consumers never have to go

near the state or federally-facilitated exchange website to buy a product

and access the refundable tax credit. All of the information transfers

between the private broker site and the ACA exchange and the

insurance carriers are invisible to the consumer."

HPA’s Private Exchange Broker Blueprint

An Exchange is not just a website – it is the whole fulfillment process

2 ways to facilitate government subsidies

1. Qualify as a WBE

2. Have subsidy calculator on exchange site, when prospect enters

information call center expert makes call and walks them through

the enrollment process on the appropriate government exchange

(state or federal)

For up to date info

Favorite Resources

Carrier Resources

Reform Reference Material

What We Are Reading

HPA Resources

Press Releases

Q&A