Embed Size (px)

Citation preview

White Paper May 2014

Freddie McMahon - Director, Strategy and Innovation

Money Launderers Playing the Long Game

Anti-Money Laundering and Combating the Financing of Terrorism

Anomaly42.com2

Overview

Money Laundering is Big Business page 3

US$ is the Primary Currency for Money Laundering page 3

US Authorities Crackdown on European Banks page 4

AML / CFT Defences Costs are Spiralling page 5

Does Traditional AML / CFT Automation Really Work? page 6

Money Launderers Playing the Long Game page 7

Countering the Money Launderers page 8

Evidence Insights and Sanitised Case Study page 10

Remember Your AML / CFT Exposurespage 12

Benefits of KYC EDD Automationpage 12

Summarypage 12

Anomaly42.com3

Money Laundering is Big Business

Between US$1.44 trillioni to US$3.59 trillion is being laundered every year. Money laundering is big business, dwarfing other markets like Big Data, which is valued at US$30 billion a yearii.

The message is clear.

Major money laundering players are successfully bypassing the controls of financial institutions, especially banks.

It is time to think differently about AML / CFTiii.

US$ is the Primary Currency for Money Laundering

US$ is the primary currency for money launderingiv.

Why is this important? This means every US$ wire payment transaction involving transfers between any countries around the world needs to include a bank that is resident in the USA. Therefore, the USA, in particular New York , is the central hub for US$ wire payment data being routed from an originator (firm or individual) to a beneficiary (firm or individual).

US Regulators are at the vanguard of tackling this multi trillion dollar issue.

4

Greece (6.39)Switzerland (5.76)

Luxembourg (6.24)

Germany (5.79)

Austria (5.79)

US Authorities Crackdown on European Banks

Significant money laundering wire payment journeys involve countries that are actually known for sound financial stability, low rates of perceived corruption and strong political and judicial institutions. Europe is one of these jurisdictions. For instance, Greece (6.39), Luxembourg (6.24), Austria (5.79), Germany (5.79), and Switzerland (5.76) appear at a high level in the 2013 Basle AML Indexv. However, this index may not adequately represent the way sophisticated money launderers use other European countries such as Cyprus, UK, France, Holland and Latvia to bypass current AML / CFT safeguards.

As a consequence, American authorities are accelerating a crackdown primarily focused on banks based in New York that has caused upheaval among European banksvi. This is being led by four authorities: the US Treasury, the Justice Department, the Manhattan District Attorney and the New York State Department of Financial Services (NYSDFS).

Countries appearing at

a high level in the 2013

Basle AML Index

Currently, BNP Paribas, the leading French Bank, is facing up to a US$10 billionvii fine related to AML / CFT sanction violations. Other French banks being investigated include Societe Generaleviii which has set a total provision of US$700m as of December 2013 for potential litigation; and Credit Agricole set aside €1.1bn for potential litigation on 31 December, 2012 and did not reveal how much it had set aside for probable litigation in 2013.

Over the past five years, Barclays PLC, ABN Amro (now part of Royal Bank of Scotland Group), ING Group, Credit Suisse AG, Standard Chartered, and HSBC have collectively paid more than $5 billion in fines to settle charges by U.S. authorities regarding AML / CFT violations and sanctions against Iran, Libya, Sudan or Cuba.

It should be remembered these provisions and fines are for specific AML / CFT violations. We believe there are significant other AML / CFT exposures that have now started to be examined by the authorities. It is important to understand that wire payment transactions show the payment life cycle of all the banks involved, so as one bank is investigated evidence is gained by the authorities of other banks involved.

Anomaly42.com5

“13,000 employees will have been added since the beginning of 2012 through the end of 2014 to support our regulatory, compliance and control effort (Risk, Compliance, Legal, Finance, Technology, Oversight and Control, and Audit) across the entire firm. 8,000 of our employees across our lines of business will be dedicated solely to building and maintaining an industry-leading Anti-Money Laundering (AML) program.”

AML / CFT Defences Costs are Spiralling

Though Banks spend upwards towards US$10bn every year tackling AML / CFT using First Level Defence (automation) and Second Level Defence (human intervention) a recent survey showed Know Your Customer (KYC) continues to be an area of concern, with 70 percent of respondents stating that they had been subject to a regulatory visit focusing on this areaix.

A powerful signal to the way AML / CFT costs are spiralling out of control can be found in the 2014 Letter to Shareholders by Jamie Dimon, Chairman and Chief Executive Officer of JP Morgan Chasex when he stated:

- Jamie Dimon

- Jamie Dimon

The statement went on to say the number of people involved with addressing these issues:

The question is whether this investment is aimed properly at addressing the way money launderers are playing the long game.

“The bad news was bad. The most painful, difficult and nerve-wracking experience that I have ever dealt with professionally was trying to resolve the legal issues we had this past year with multiple government agencies and regulators as we tried to get many large and risky legal issues behind us.”

Anomaly42.com6

Does Traditional AML / CFT Automation Really Work?

Our experience shows that traditional AML / CFT Automation, including sanctions, often generates 5% to 11% wire payment exceptions that are addressed through human intervention, with less than 1% becoming forensic cases for subsequent investigations. However, our work has also indicated that major money laundry players are just as familiar with these checks, especially sanctions lists that are in the public domain. Therefore, it is not a surprise that current AML / CFT Automation is inadequate to safeguard the interests of a bank and meet the demands of regulators and other authorities.

A 2014 publication, The Report Questions Global Fight against Money Laundering and Terrorism believes international regulation is at a crossroads. Peter Reuter, a policy researcher specializing in illegal markets, and co-author of the report states,

“The science of risk analysis is poorly developed for money laundering, and it is currently impossible to judge relative risk on an objective and systematic basis.”xi

- Peter Reuter

Anomaly42.com7

They tend to create firms in sectors related to international trade like energy and transportation.

They like to set up shell firms that can be confused with legitimate trading brands.

They target bank offices located in jurisdictions that are SWIFT members and are an easier touch for CDD.

They invest in or buy, banks that are SWIFT members.

They have access to the same publicly sourced data that identifies very high risk AML / CFT countries.

They tend to create shell firms with specialist companies in concentrated areas within targeted ‘lower’ AML / CFT risk jurisdictions to get economies of scale

They often use 5+ degrees of separation between the originator and beneficiary for US$ money transfers to be under the radar of banks controls in the USA.

Money Launderers Playing the Long Game

Based on our experience of the evidence gathered, the following behaviours and methods are being deployed by major money launderers that are designed to bypass the controls of financial institutions, in particular banks:

They access the same open data for sanctions and PEPS as the banks: for example banks based in the USA need to apply the US Treasury OFACxii list.

They seem aware of banks AML / CFT automation rules such as looking for transactional patterns over specific time periods.

They set up firms that remain ‘clean’ (dormant) for 3+ years.

They use ‘clean’ firms to establish bank accounts in other jurisdictions.

They tend to set up or take over LLP and LP firms using firms in other countries. They tend to use a network of shell firms across multiple jurisdictions, including LLP and LP firms.

They use multiple shell firms to own another firm to avoid triggering ownership thresholds.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Anomaly42.com8

Countering the Money Launderers

Understandably, financial firms are increasingly dissatisfied with their current automated monitoring capabilities to counter the behaviours of money launderers. Despite increasing pressure from regulatory authorities and the threat of billion dollar fines and the growing discontent from shareholders, financial firms’ controls are struggling to contain AML / CFT risks.

The primary barrier to automation that can strengthen AML / CFT controls and reduce the compliance overheads are twofold:

1. Data Complexity

Wire payment data is complex. SWIFT has over 300 different Message Types each with their own record format. Within a Message Type there is a combination of structured (normalised data); semi-structured data (tags; concatenated strings of recognisable data such as date and money combined); and unstructured data (free format text that contains content such as beneficiary address, reason for payment).

Similar complexities are applicable to CHIPS and FedWire transactions. Because of these complications, wire payment files need to be deconstructed and reconstructed into a format for automated data and decision processing.

To counter money laundering requires Enhanced Due Diligence (EDD)xiii, which requires publicly sourced data that comes in many varieties of formats. Public source data is complex. When it comes to enhanced due diligence, the data is often available in the public domain or through nominal charges from government bodies such as the UK Companies House, but this data needs to be collected, connected and correlated with the appropriate wire payment transactions to turn the data into a coherent picture and hence identify anomalies and high risks cases.

Anomaly42.com9

The output from the AI Agent is a leader board of wire payment transactions in the sequence of aggregated risk weightings. These leader boards are represented by risk bands with the highest band expecting to have 90% probability of accuracy with the remaining 10% highlighting KYC issues.

The highest risks transactions are represented through multiple mediums including: a) leader boards for each risk threshold; b) dynamic visualisation showing the flow of money for a transaction from originator to beneficiary including all the banks involved; c) forensic case for high risk transactions for further investigations and the gathering of additional evidence.

Apply the above on historical data to identify money laundering anomalies that may have bypassed the bank’s controls and not been reported as suspicious activities.

Set-up a 3rd Level Defence to monitor transactions that complements a bank’s First level Defence (traditional AML / CFT automation) and Second Level Defence (human intervention).

2. Algorithms

AML / CFT algorithms are complex as they need to cope with the complex data outlined and the behavioural patterns of the money launderers that are continually changing.

Our thought leadership has approached tackling money laundering in a new way. The first step involves being laser focused on a narrow and deep aspect of money laundering that involves the SWIFT Message Type 103 and the associated CHIPS and FedWire transactions. This involves money transfer originators and beneficiaries that are non- banks – the heartland of the money launderers.

By using our Anomaly42 Smart Data Platform we are able to:

Deconstruct and reconstruct SWIFTxiv

MT103xv which is a single wire payment involving non-financial firms; in addition it includes the relevant CHIPSxvi and FedWirexvii transactions.

Apply the science of risk weighting analysis on an objective and systematic basis using tables derived from public sourced data and government bodies to automate finding money laundering exposures hidden deep with the wire payment data. This automation is processed by an Artificial Intelligence (AI) Agent, which is a combination of artificial intelligence and algorithms specific to MT103. An AI Agent is likened to a subject matter expert whose IQ increases over times through controlled evolutionary improvements.

Anomaly42.com10

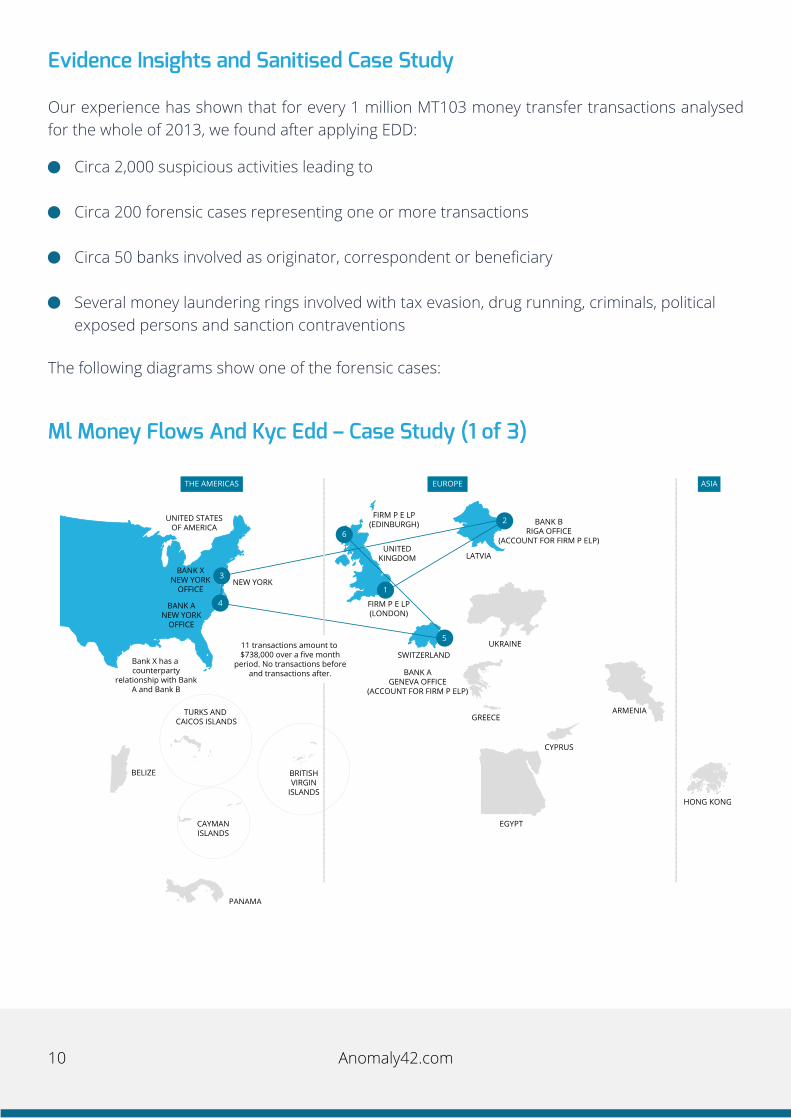

Evidence Insights and Sanitised Case Study

Our experience has shown that for every 1 million MT103 money transfer transactions analysed for the whole of 2013, we found after applying EDD:

Ml Money Flows And Kyc Edd – Case Study (1 of 3)

The following diagrams show one of the forensic cases:

Circa 2,000 suspicious activities leading to

Circa 200 forensic cases representing one or more transactions

Circa 50 banks involved as originator, correspondent or beneficiary

Several money laundering rings involved with tax evasion, drug running, criminals, political exposed persons and sanction contraventions

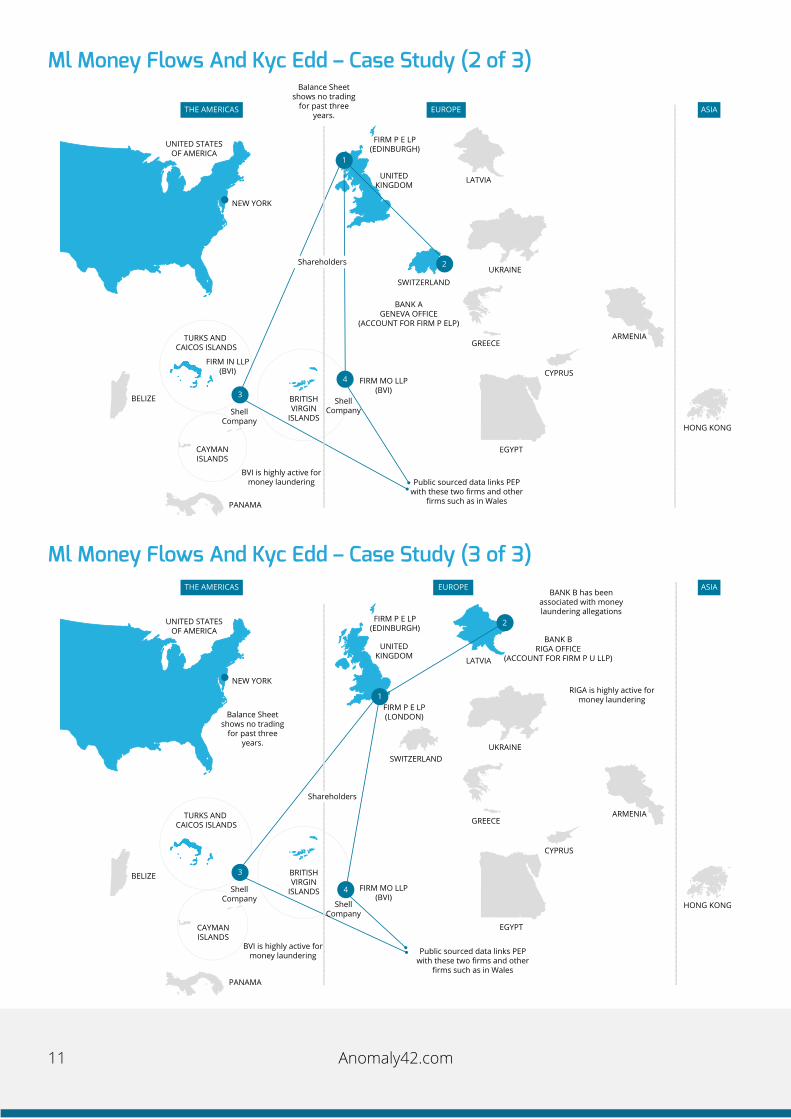

Anomaly42.com11

Ml Money Flows And Kyc Edd – Case Study (3 of 3)

Ml Money Flows And Kyc Edd – Case Study (2 of 3)

Anomaly42.com12

Benefits of KYC EDD Automation

The benefits of automating KYC EDD for MT103 and equivalent are as follows:

From a longer term perspective KYC EDD also provides the customer insights that go well beyond the conventions of CRM for stimulating new market and revenue growth.

Remember Your AML / CFT Exposures

As regulatory authorities use advanced technologies and techniques to find AML / CFT exposures, each money laundering transaction names every bank involved. This level of market transparency is starting to emerge meaning that there is no hiding place for any exposed transactions from the past. It is now simply a matter of time. This is the time to take action to find any systemic weaknesses deep into the past wired payments transacted.

Summary

Countering money laundering needs rethinking. A shift towards “Living KYC” with enhanced due diligence needs to become the modus operandi for firms involved with international money transfer transactions. By using Know Your Customer, data has a dual purpose for:

Protect the integrity and trust of the brand for all stakeholders.

Better assurance against regulator investigations, fines and the threat of criminal exposures to employees.

Reduce the costs of compliance and supervision

1

2

3

Driving down costs and risks, whilst protecting the brand from contamination. Growing market and revenues, whilst amplifying brand trust and integrity.

Anomaly42.com13

References

i The IMF believes the money laundered every year equates to

2% to 5% World GDP. Source: https://www.imf.org/external/np/

speeches/1998/021098.htm The CIA Fact Book 2014 states

that the 2013 World GDP is valued at US$71.83 trillion. Source:

https://www.cia.gov/library/publications/the-world-factbook/

index.html

ii Big Data Vendor Revenue and Market Forecast 2013-2017;

Author: Jeff Kelly; February 12, 2014

iii AML / CFT Anti-Money Laundering and Combating the

Financing of Terrorism

iv Source: Woodrow International Center for Scholars: “It’s All

About the Money”, May 2012

v The Basel AML Index 2013 report by the Basel Institute on

Governance

vi Wall Street Journal, “BNP Paribas Facing $2 Billion in Fines over

Sanctions Violations; Internal Probe Found Bank Breached U.S.

Sanctions against Iran” 30th April 2014 Source: http://tinyurl.

com/pmvu36d/

vii Source: BBC “BNP Paribas ‘$10bn’ US fine unreasonable, says

France “ - www.bbc.co.uk/news/business-27676000

viii Source: 6th May 2014 Too big to jail? No bank above the law,

says US Attorney General; Criminal charges could be filed within

weeks following tax evasion probes of European banks http://

tinyurl.com/m33xwfn/

ix KPMG Global Anti-Money Laundering Survey 2014

x Jamie Dimon, Chairman and Chief Executive Officer: Dear

Shareholders Letter January 2014 http://tinyurl.com/luwu6fs/

xi GLOBAL SURVEILLANCE OF DIRTY MONEY: ASSESSING

ASSESSMENTS OF REGIMES TO CONTROL MONEY-LAUNDERING

AND COMBAT THE FINANCING OF TERRORISM; 30 January 2014

http://tinyurl.com/ll4m66z/

xii USA Office of Foreign Asset Control list covering targeted

countries, individuals etc.

xiii Source: FATF: Methodology for assessing technical compliance

with the FATF recommendations and effectiveness of AML /

CFT systems. Enhanced Due Diligence (EDD) determines that a

beneficiary who is a legal person or a legal arrangement presents

a higher risk, it should be required to take enhanced measures

which should include reasonable measures to identify and verify

the identity of the beneficial owner of the beneficiary, at the time

of pay-out.

xiv SWIFT Society for Worldwide Interbank Financial

Telecommunication

xv A swift MT103 is a message to a customer showing the credit

transfer for a single payment.

xvi CHIPS is the largest private-sector U.S.-dollar funds-transfer

system in the world. In 2012, CHIPS cleared and settled an

average of $1.5 trillion in cross-border and domestic payments

daily.

xvii FEDWIRE Formally known as the Federal Reserve Wire

Network, FedWire is a real-time gross settlement funds transfer

system operated by the United States Federal Reserve Banks

that enables financial institutions to electronically transfer funds

between its participants. In conjunction with the privately held

Clearing House Interbank Payments System (CHIPS), FedWire

is the primary United States network for large-value or time-

critical domestic and international payments, and it is designed

to be highly resilient and redundant. The average daily value

of transfers over the FedWire Funds Service in 2007 was

approximately $2.7 trillion, and the daily average number of

payments was about 537,000.[2] 2009 figures show a value of

631 trillion dollars in transfers originated in FedWire.