Embed Size (px)

Citation preview

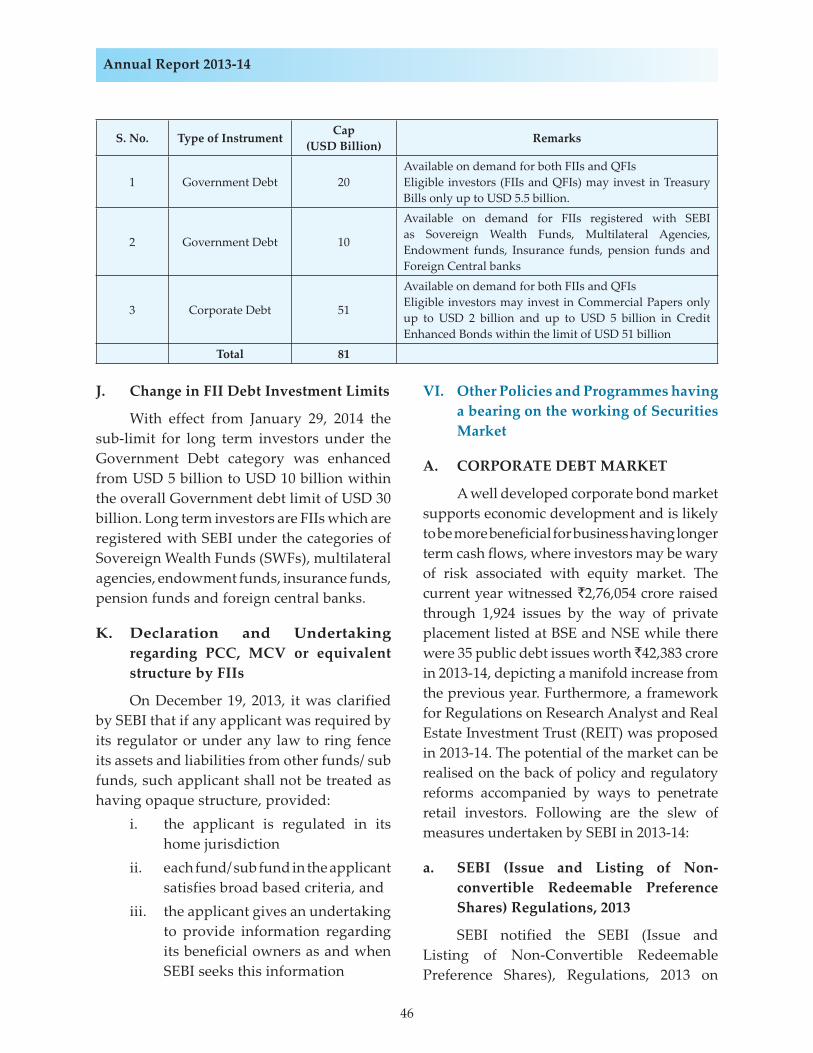

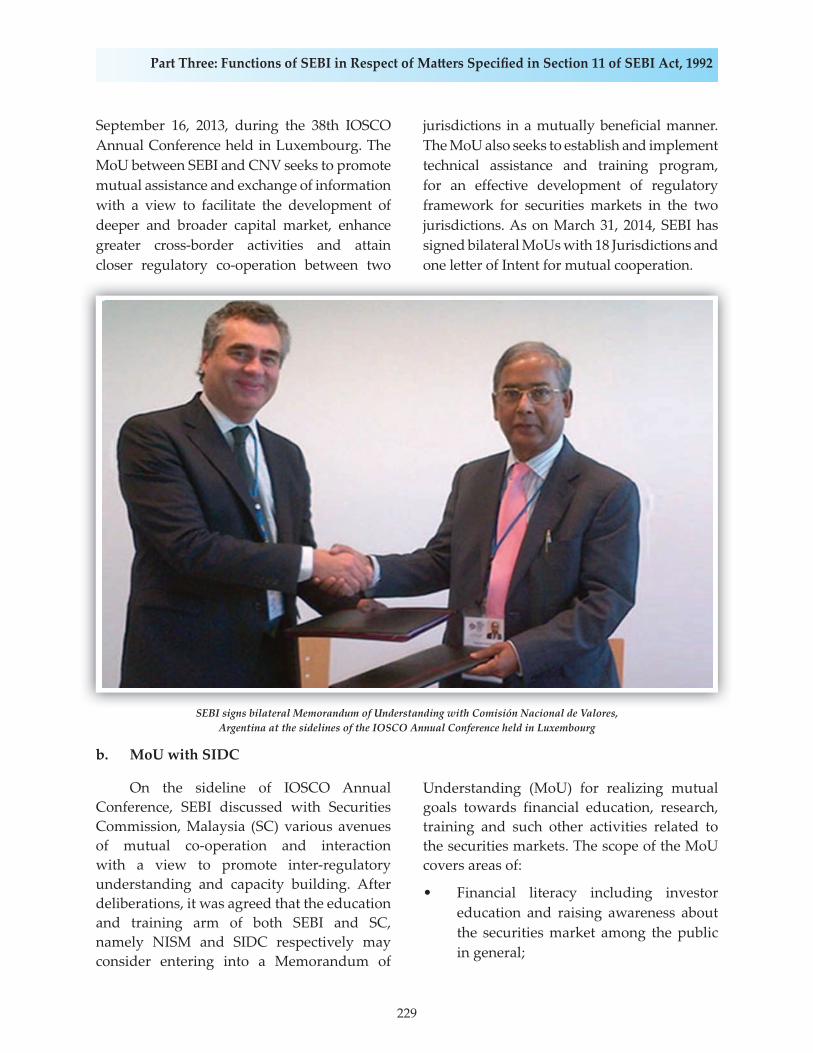

This Report is in conformity with the format as per the Securitiesand Exchange Board of India (Annual Report) Rules, 1994,

notifi ed in Offi cial Gaze� e on April 7, 1994

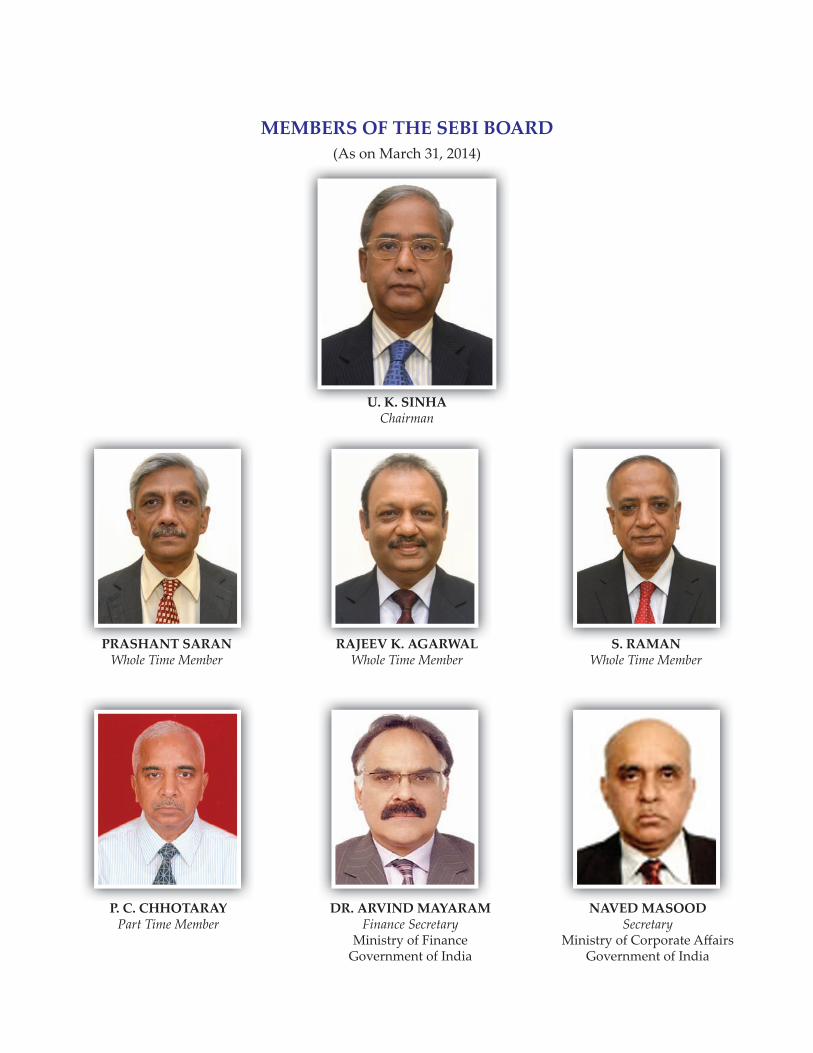

MEMBERS OF THE BOARD(As on March 31, 2014)

Appointed under Section 4(1) (a) of the SEBI Act, 1992 (15 of 1992)

U. K. SINHACHAIRMAN

Appointed under Section 4(1) (d) of the SEBI Act, 1992 (15 of 1992) PRASHANT SARANWHOLE TIME MEMBER

RAJEEV K. AGARWALWHOLE TIME MEMBER

S. RAMANWHOLE TIME MEMBER

P. C. CHHOTARAYPART TIME MEMBER

Nominated under Section 4(1) (b) of the SEBI Act, 1992 (15 of 1992)

DR. ARVIND MAYARAMFinance SecretaryMinistry of FinanceGovernment of India

NAVED MASOODSecretaryMinistry of Corporate Aff airsGovernment of India

MEMBERS OF THE SEBI BOARD(As on March 31, 2014)

U. K. SINHAChairman

PRASHANT SARANWhole Time Member

RAJEEV K. AGARWALWhole Time Member

S. RAMANWhole Time Member

P. C. CHHOTARAYPart Time Member

DR. ARVIND MAYARAMFinance Secretary

Ministry of FinanceGovernment of India

NAVED MASOODSecretary

Ministry of Corporate Aff airsGovernment of India

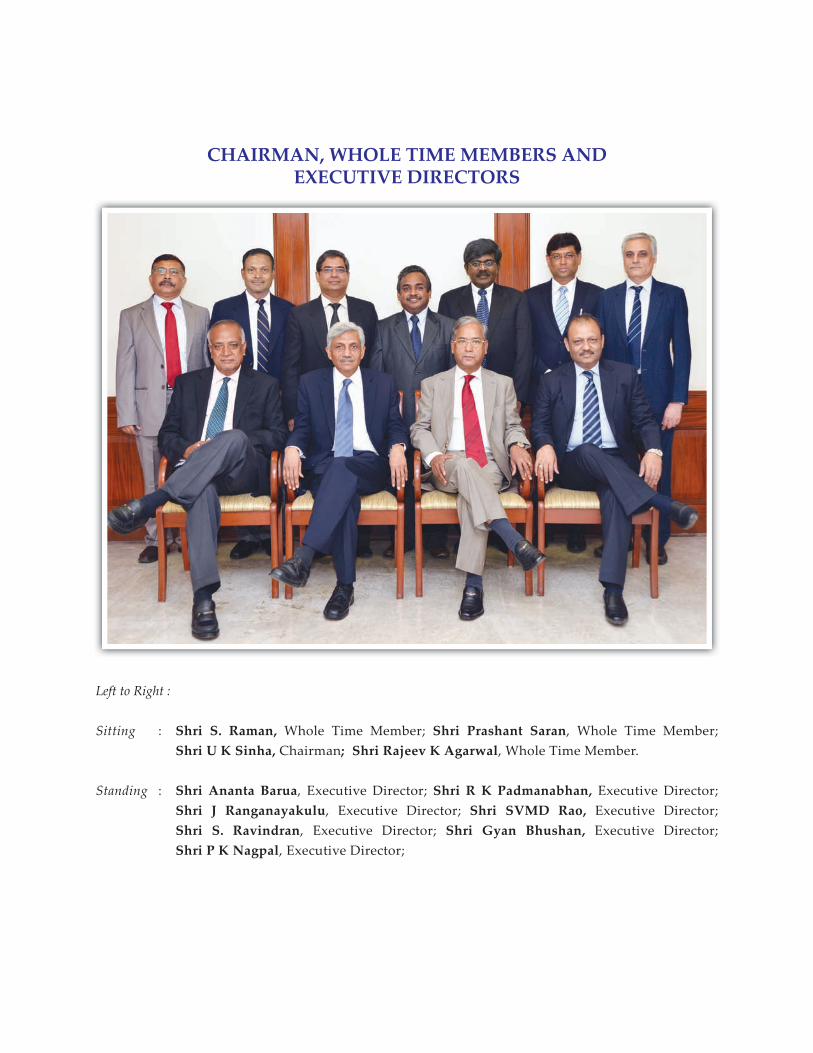

CHAIRMAN, WHOLE TIME MEMBERS AND EXECUTIVE DIRECTORS

Left to Right :

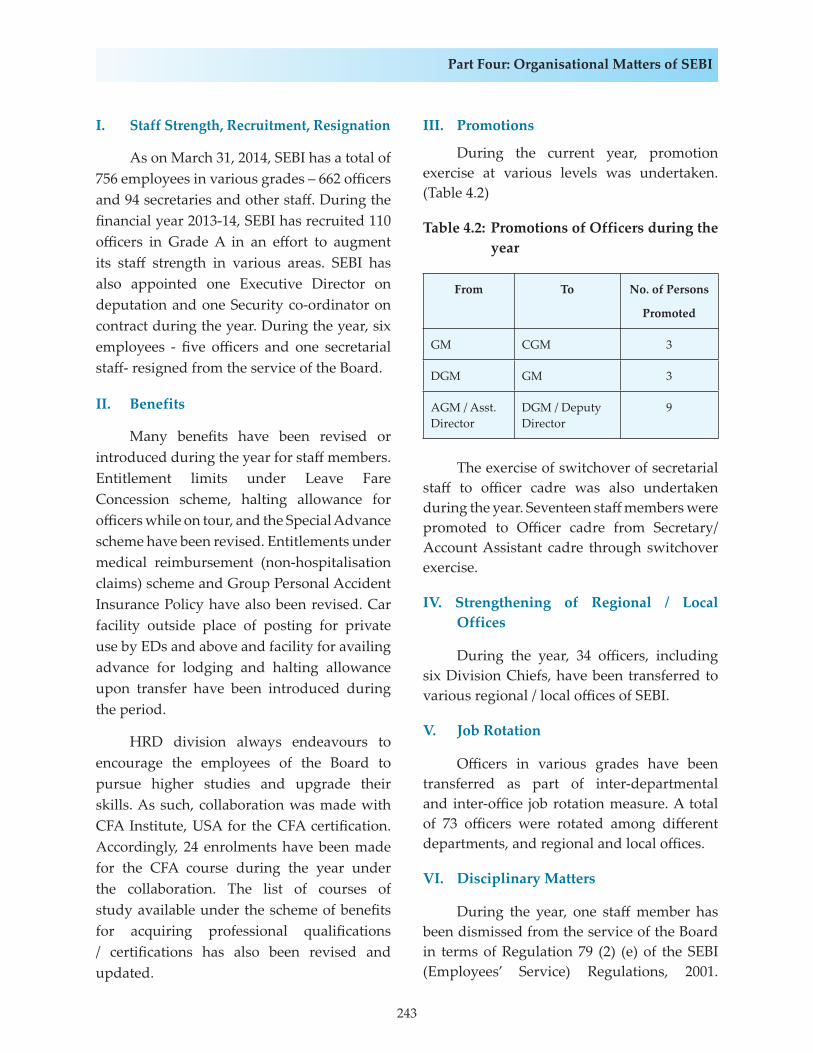

Sitting : Shri S. Raman, Whole Time Member; Shri Prashant Saran, Whole Time Member; Shri U K Sinha, Chairman; Shri Rajeev K Agarwal, Whole Time Member.

Standing : Shri Ananta Barua, Executive Director; Shri R K Padmanabhan, Executive Director; Shri J Ranganayakulu, Executive Director; Shri SVMD Rao, Executive Director; Shri S. Ravindran, Executive Director; Shri Gyan Bhushan, Executive Director; Shri P K Nagpal, Executive Director;

i

CONTENTS

List of Boxes ...............................................................................................................................................vi

List of Tables ............................................................................................................................................ vii

List of Charts ..............................................................................................................................................xi

Abbreviations ...........................................................................................................................................xii

PART ONE: POLICIES AND PROGRAMMES

1. REVIEW OF THE GENERAL MACRO-ECONOMIC ENVIRONMENT AND THE INVESTMENT CLIMATE .............................................................................................................. 1

2. REVIEW OF POLICIES AND PROGRAMMES

I. Primary Securities Market ................................................................................................... 13

II. Secondary Securities Market............................................................................................... 20

III. Mutual Funds ........................................................................................................................ 36

IV. Intermediaries Associated with Securities Market .......................................................... 38

V. Foreign Institutional Investment ........................................................................................ 43

VI. Other Policies and Programmes having a bearing on the working of Securities Market .................................................................................................................. 46

VII. Assessment and Prospects .................................................................................................. 51

PART TWO: REVIEW OF WORKING AND OPERATIONS OF THE SECURITIES AND EXCHANGE BOARD OF INDIA IN THE SECURITIES MARKET

1. PRIMARY SECURITIES MARKET

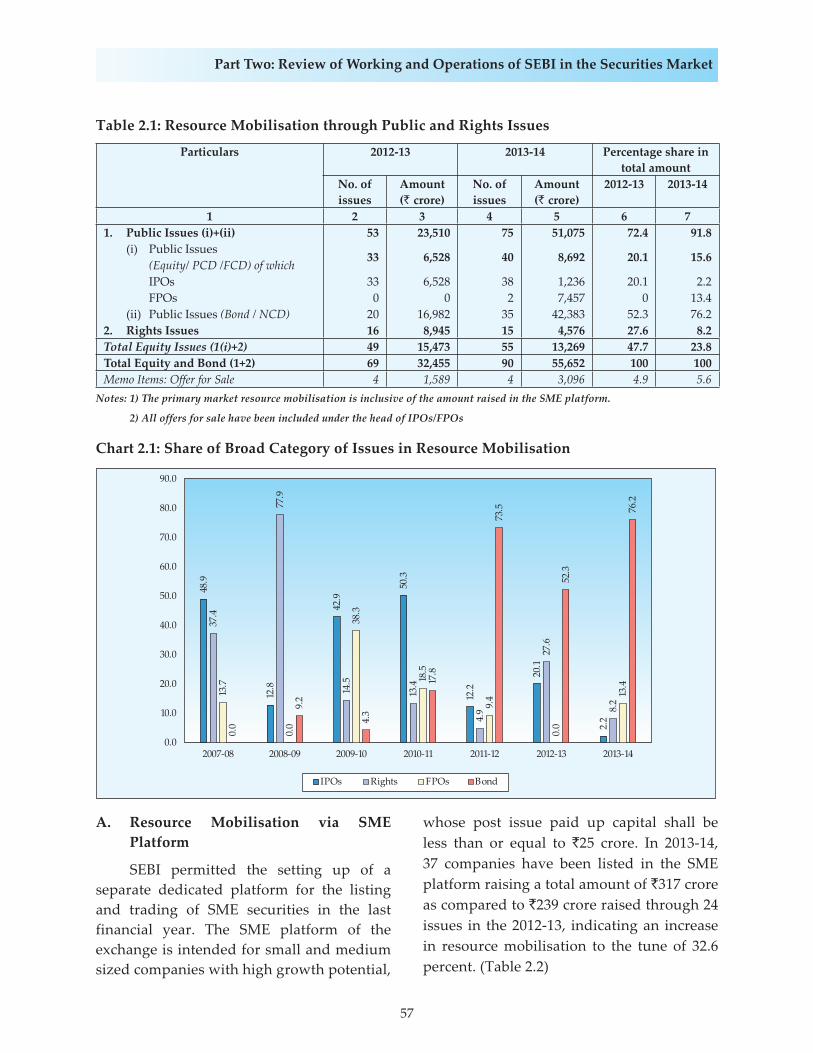

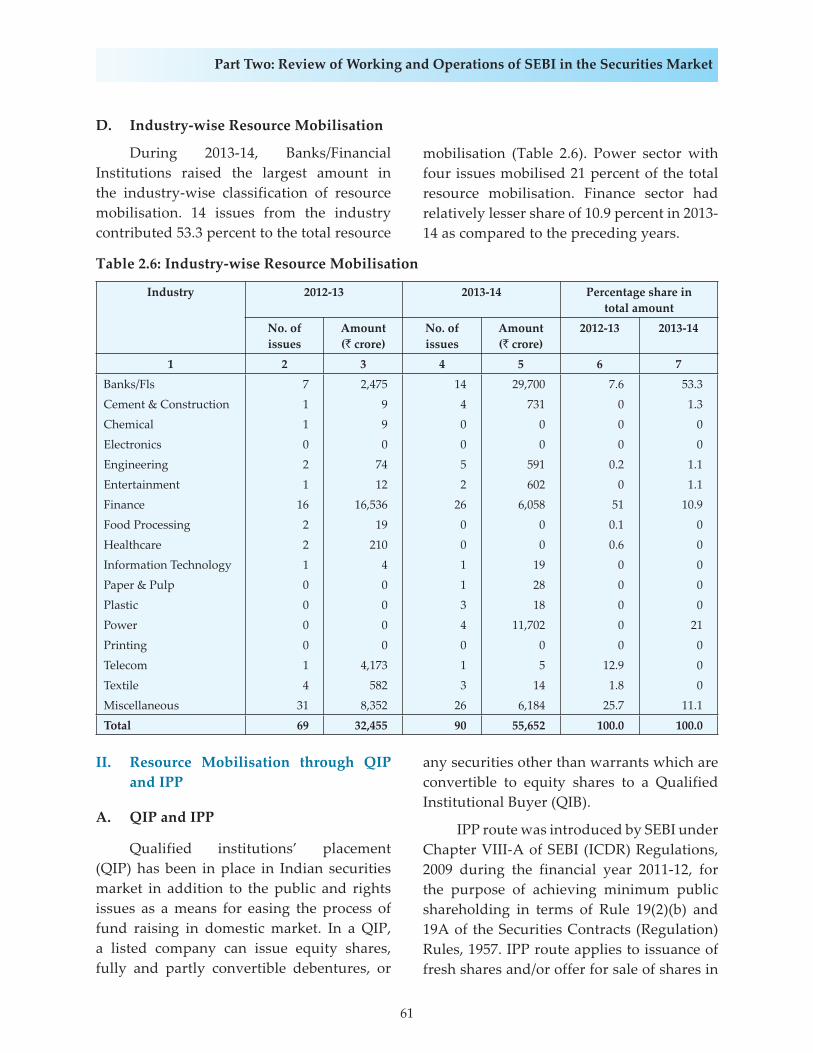

I. Resource Mobilisation through Public and Rights Issues .............................................. 56

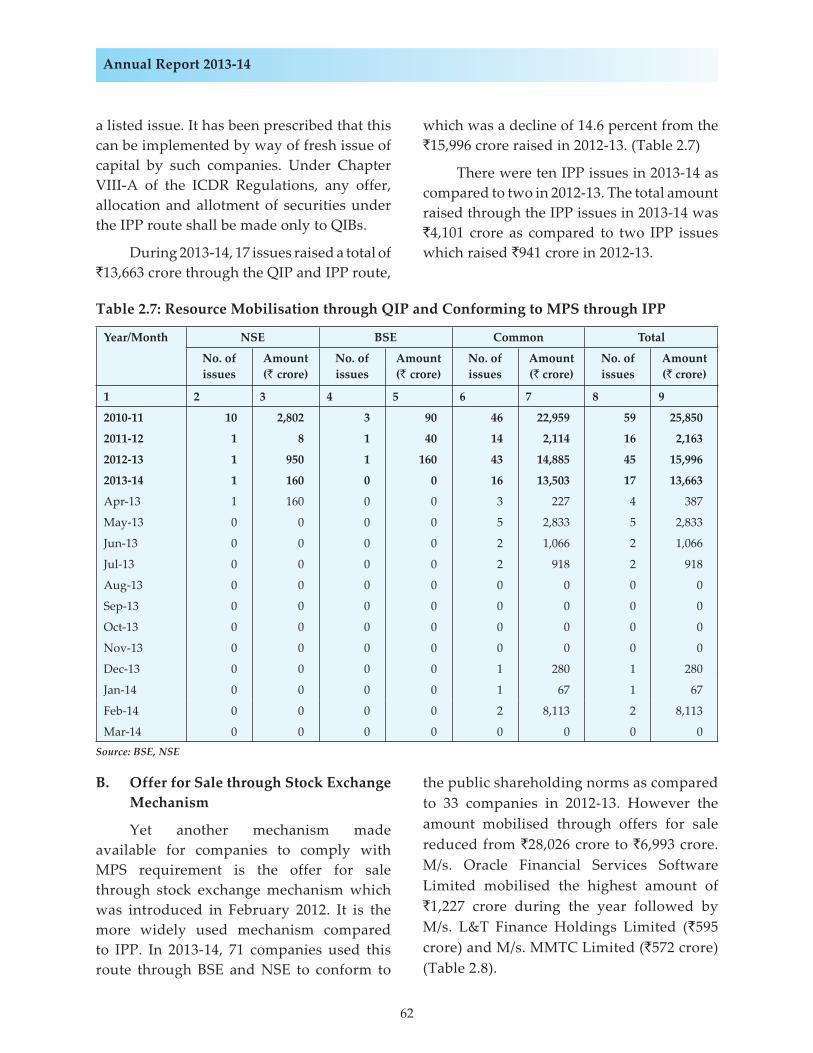

II. Resource Mobilisation through QIP and IPP ................................................................... 61

III. Resource Mobilisation through Preferential Allotment .................................................. 63

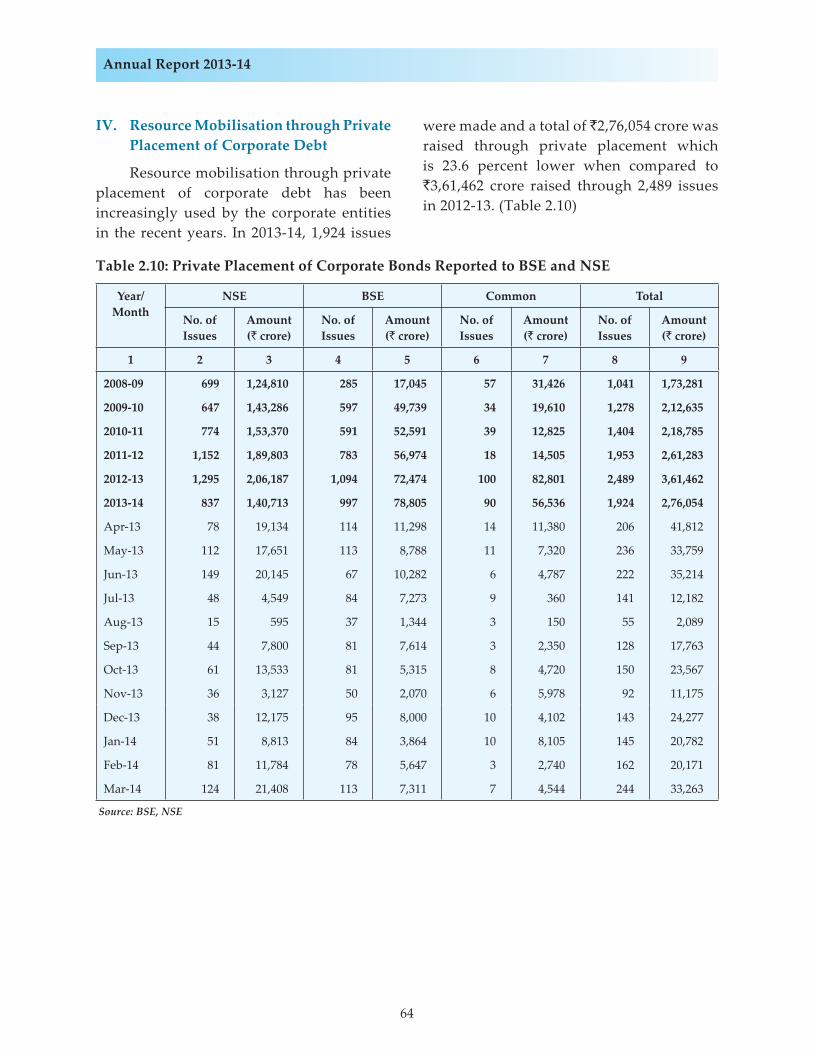

IV. Resource Mobilisation through Private Placement in Corporate Debt ........................ 64

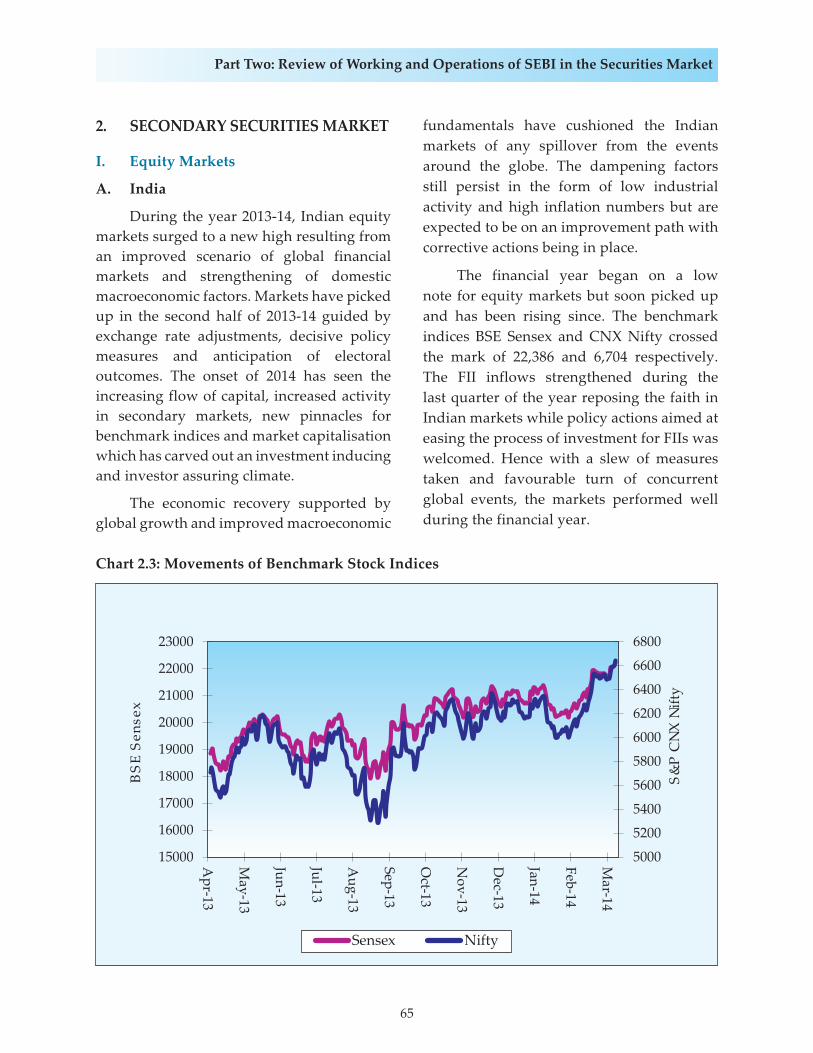

2. SECONDARY SECURITIES MARKET

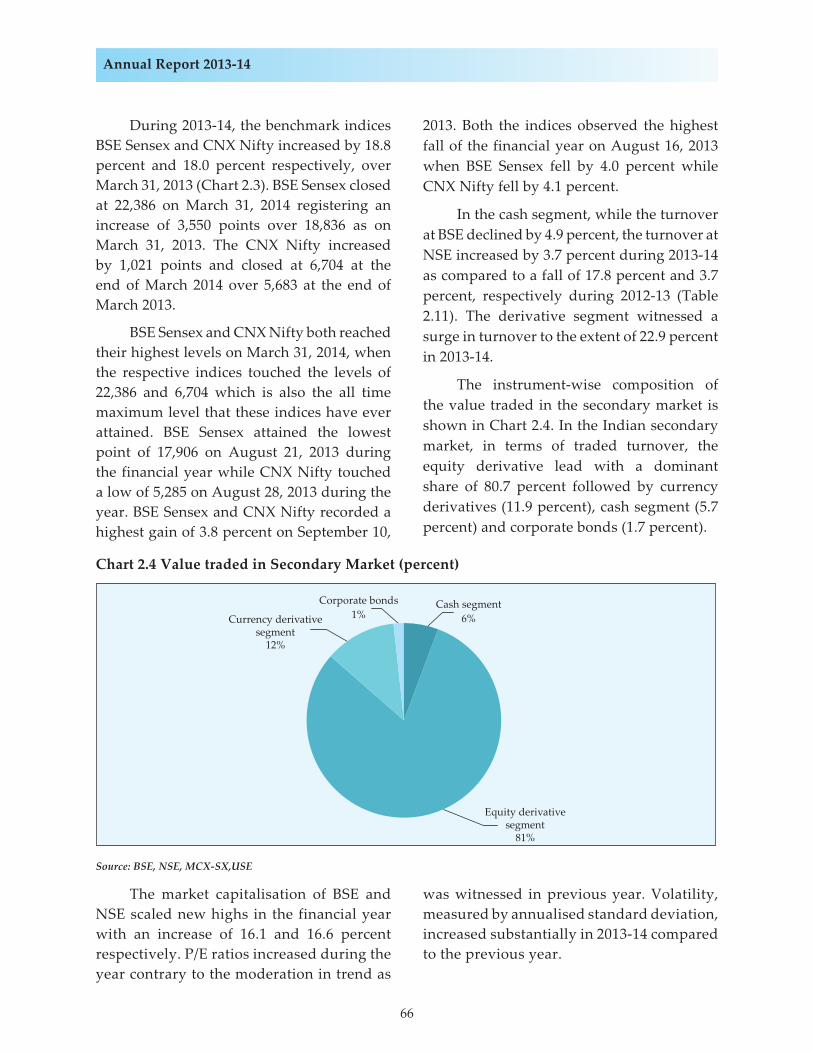

I. Equity Market ....................................................................................................................... 65

II. Performance of Major Stock Indices and Sectoral Indices .............................................. 69

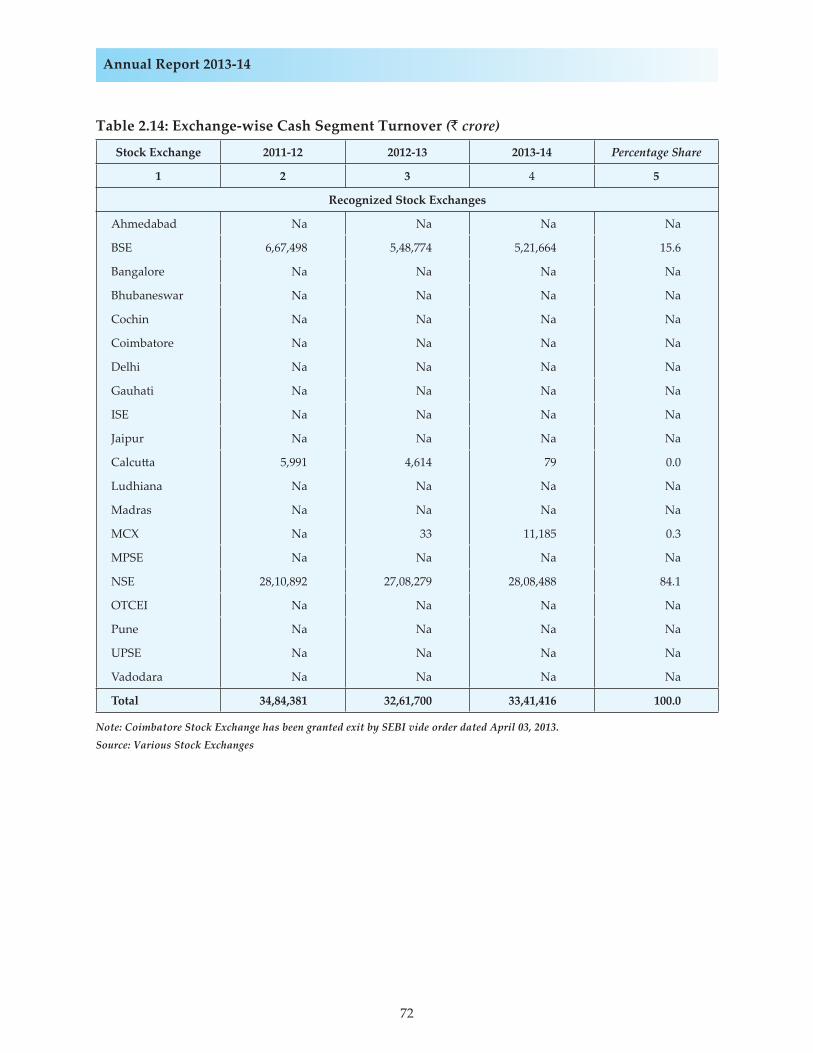

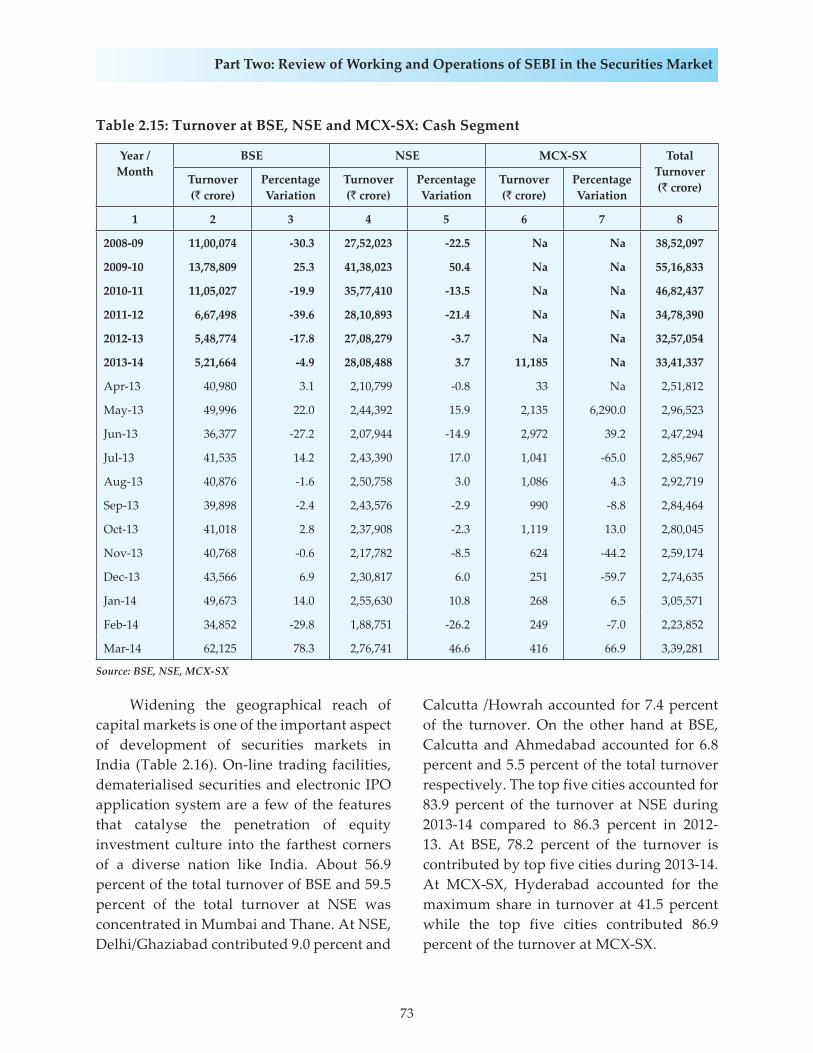

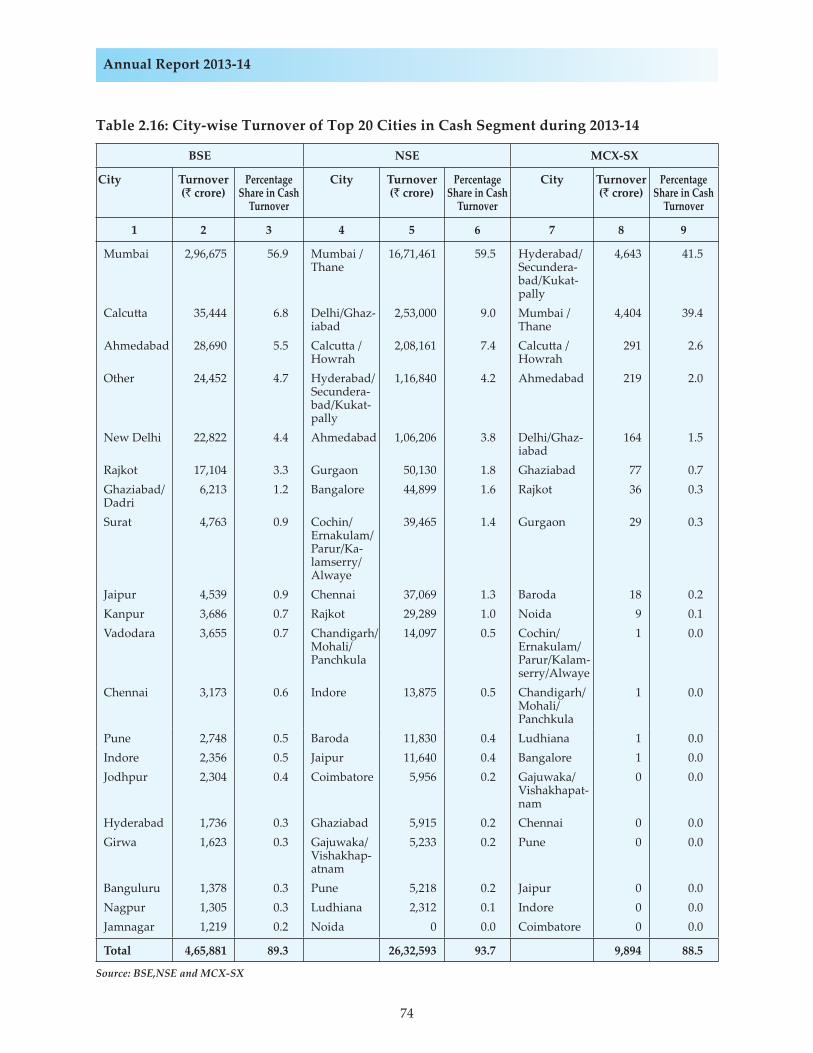

III. Turnover in Indian Stock Market ....................................................................................... 71

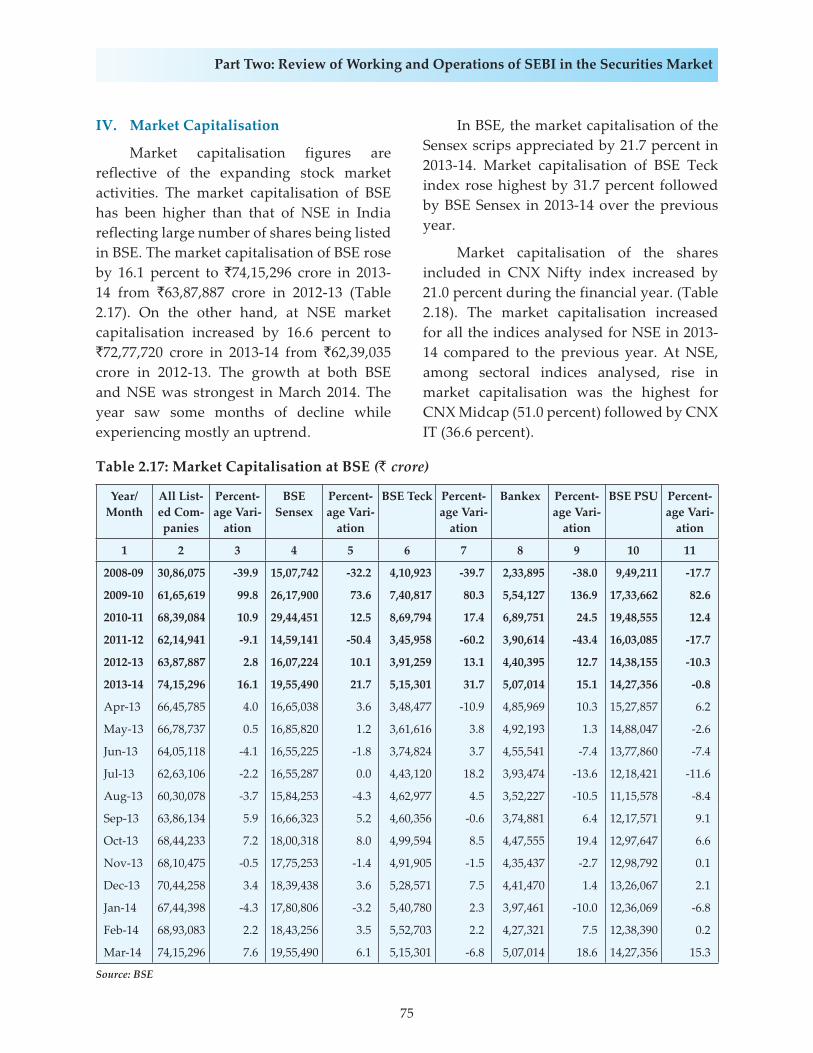

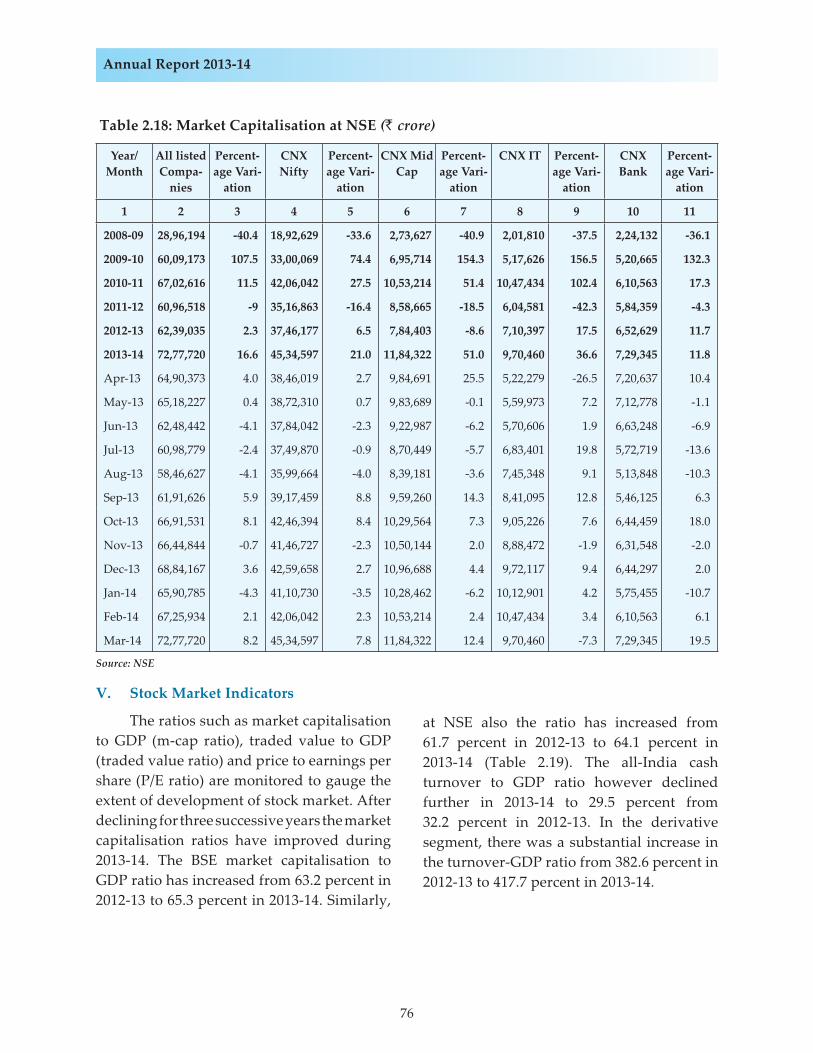

IV. Market Capitalisation .......................................................................................................... 75

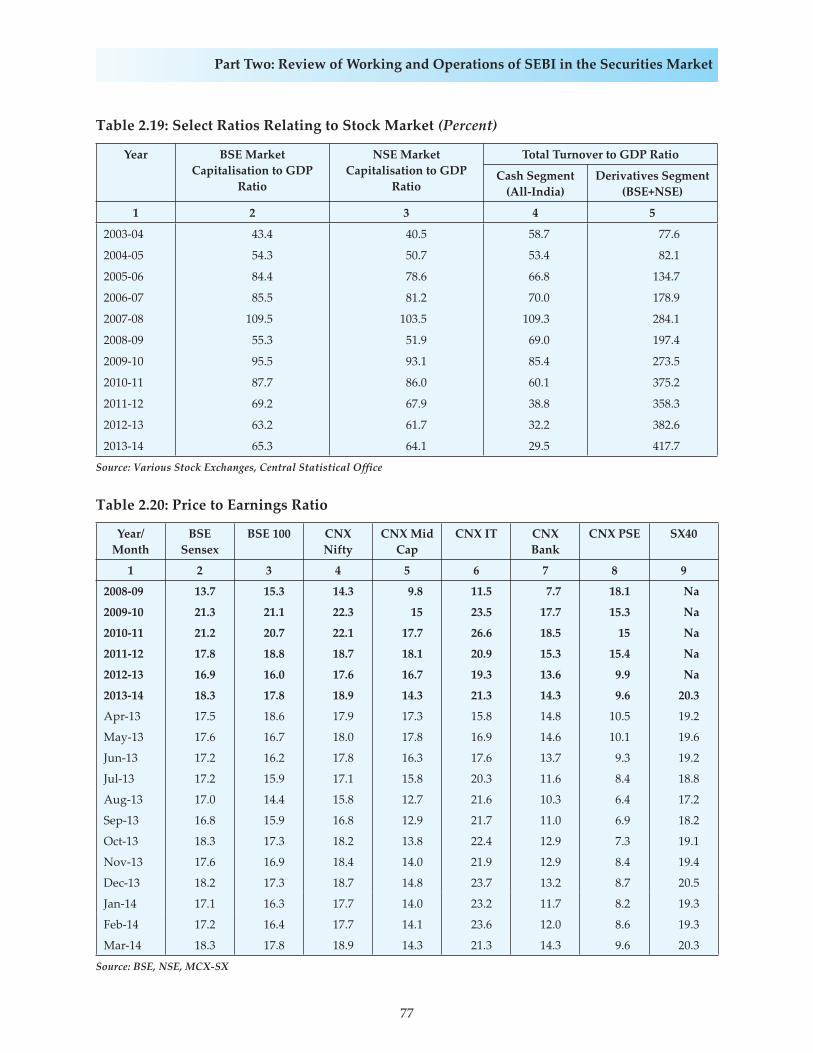

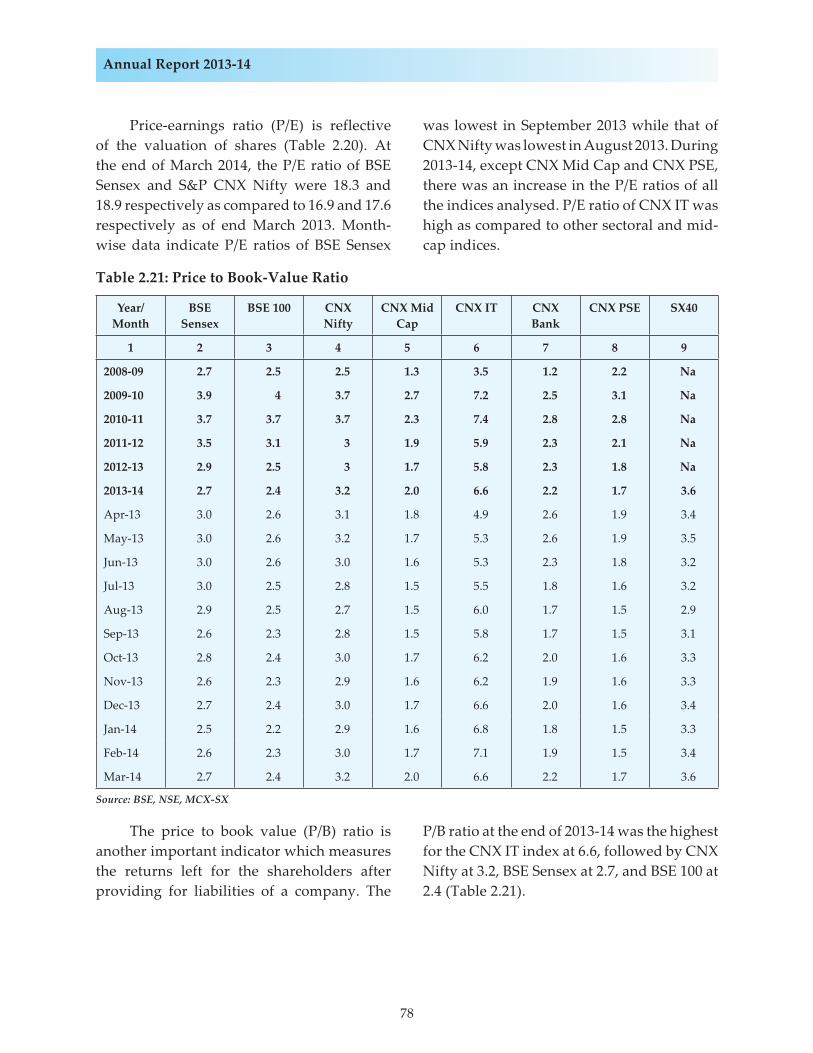

V. Stock Market Indicators ....................................................................................................... 76

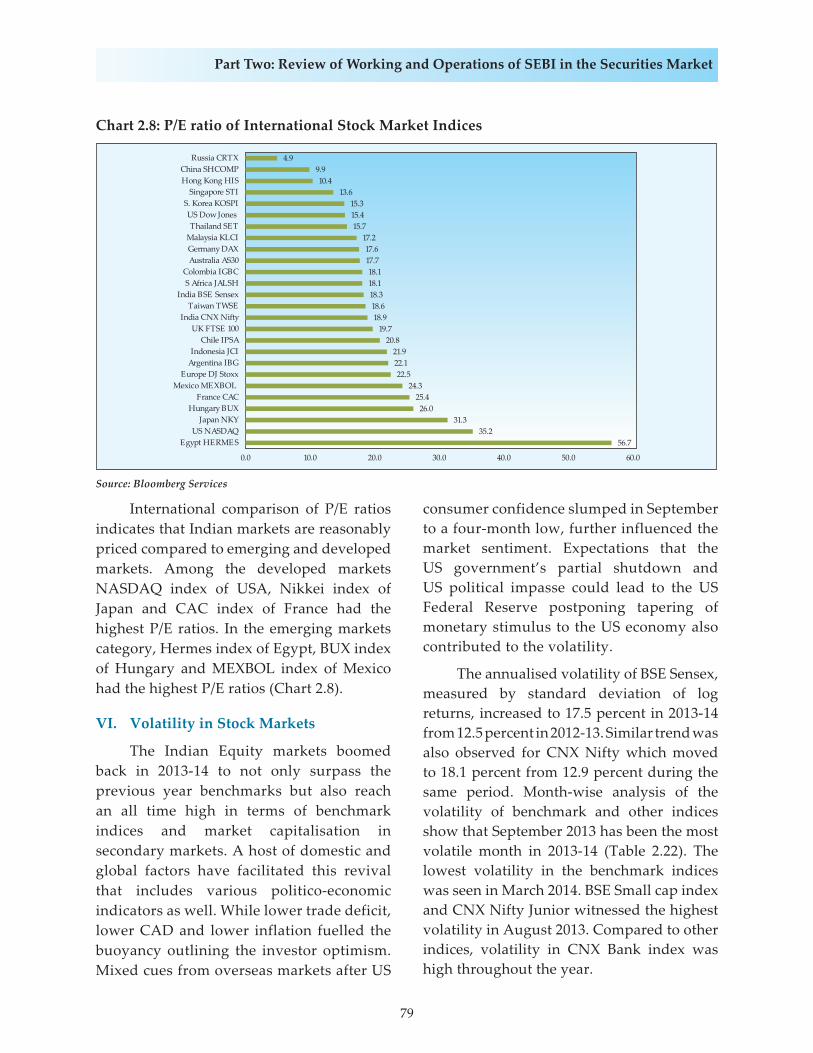

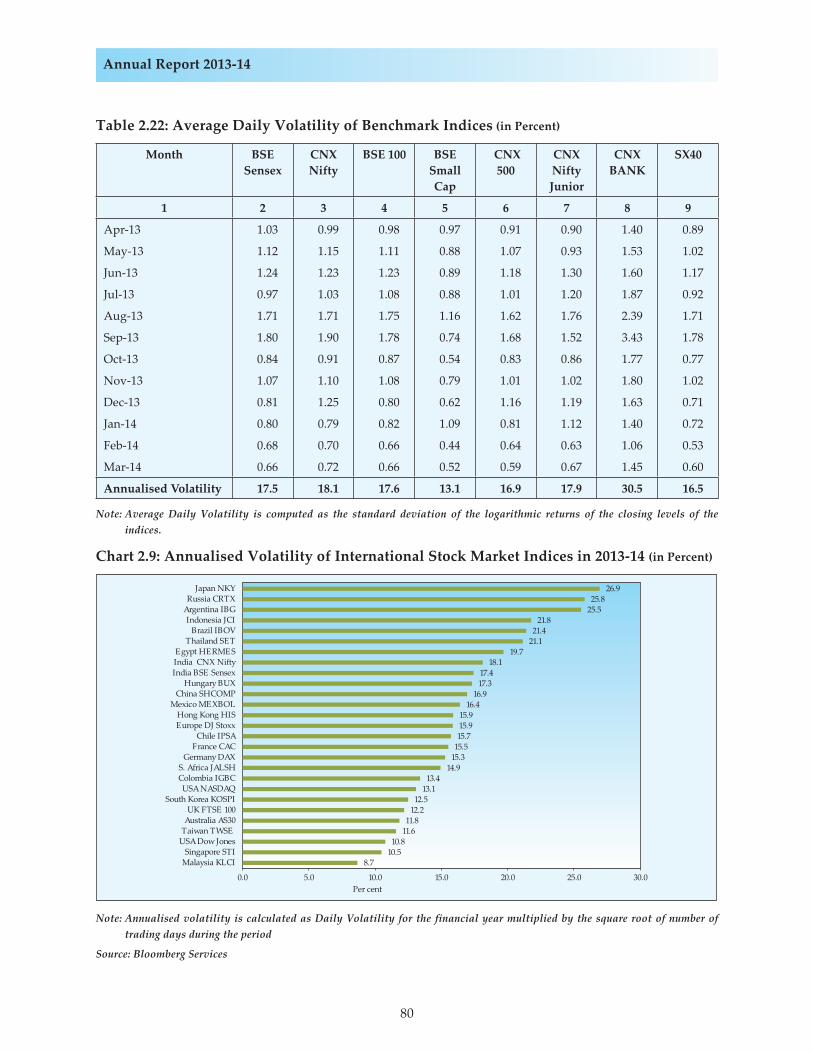

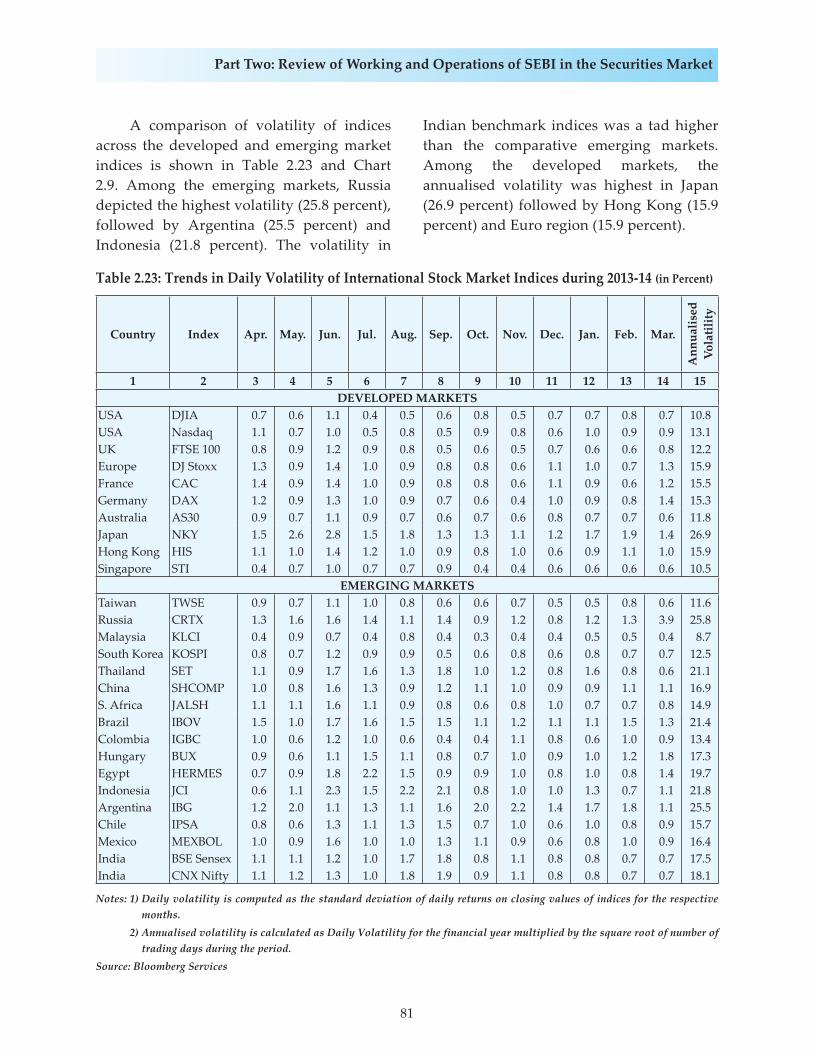

VI. Volatility in Stock Markets .................................................................................................. 79

VII. Trading Frequency ............................................................................................................... 82

Page No.

ii

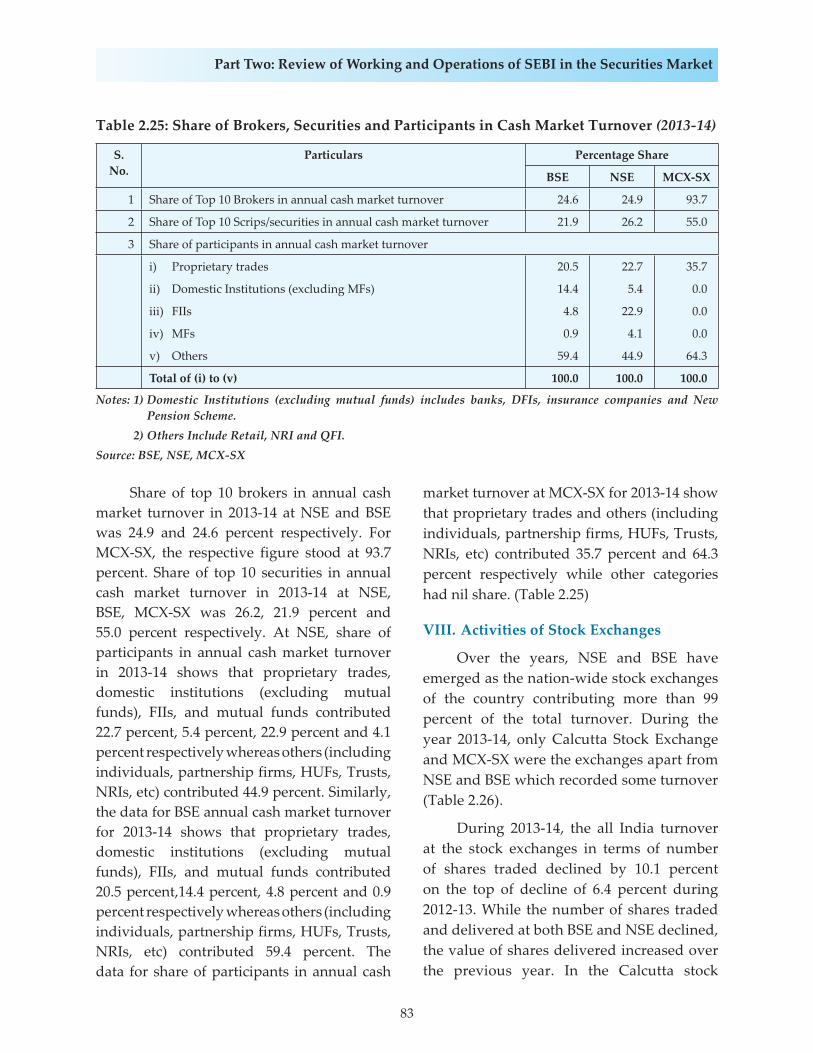

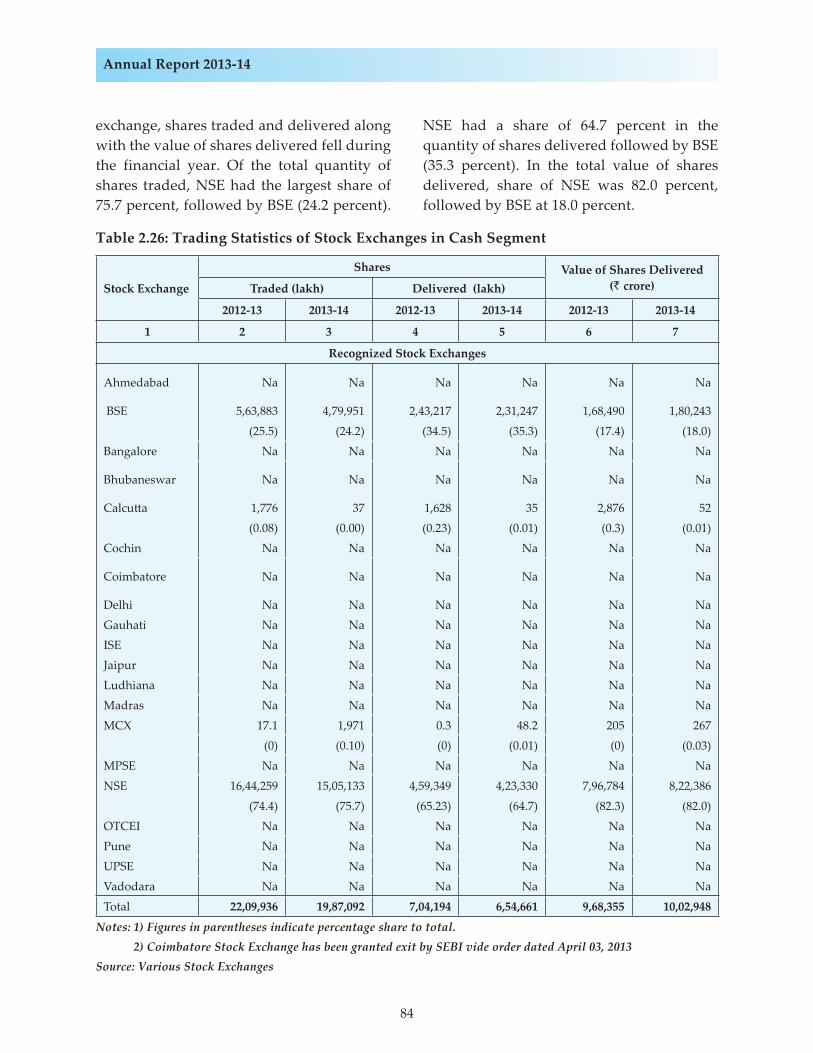

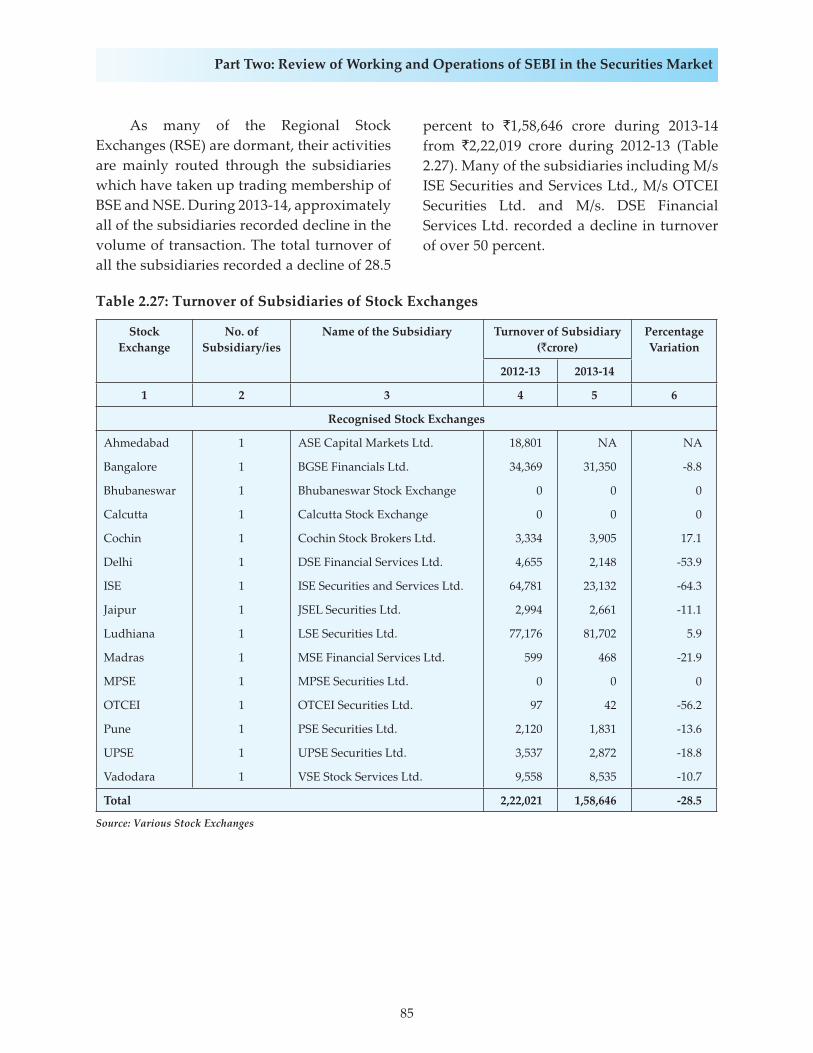

VIII. Activities of Stock Exchanges ............................................................................................. 83

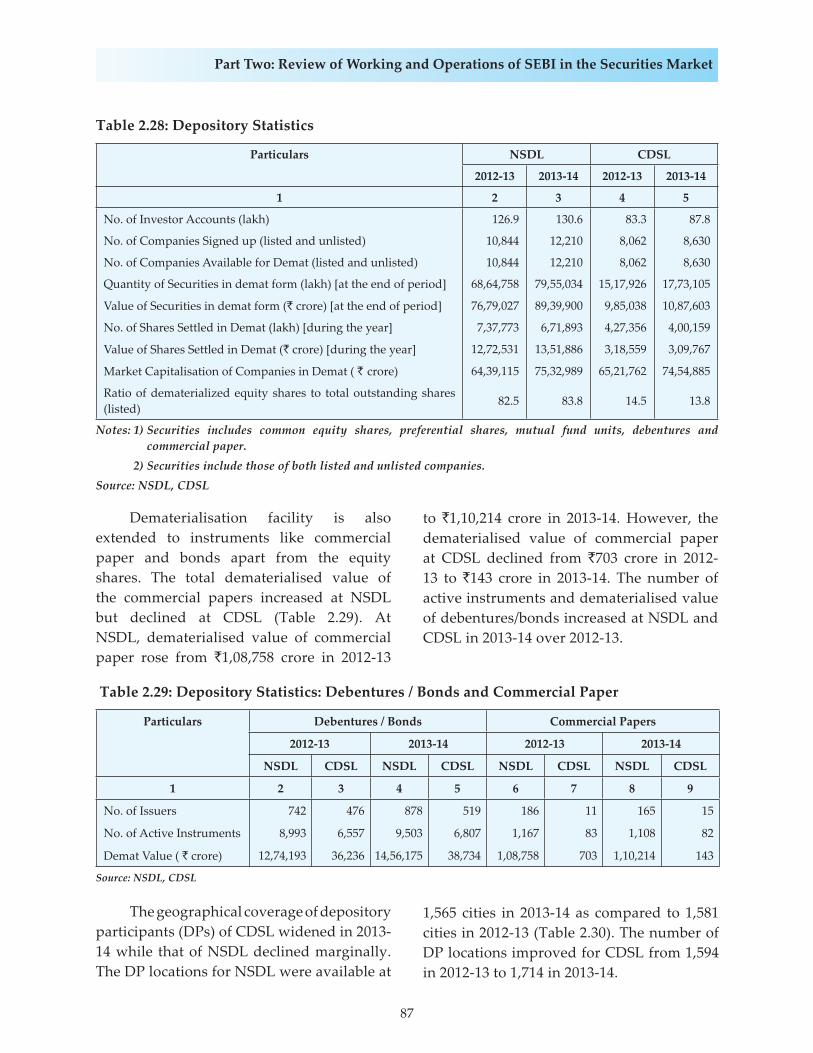

IX. Dematerialisation ................................................................................................................. 86

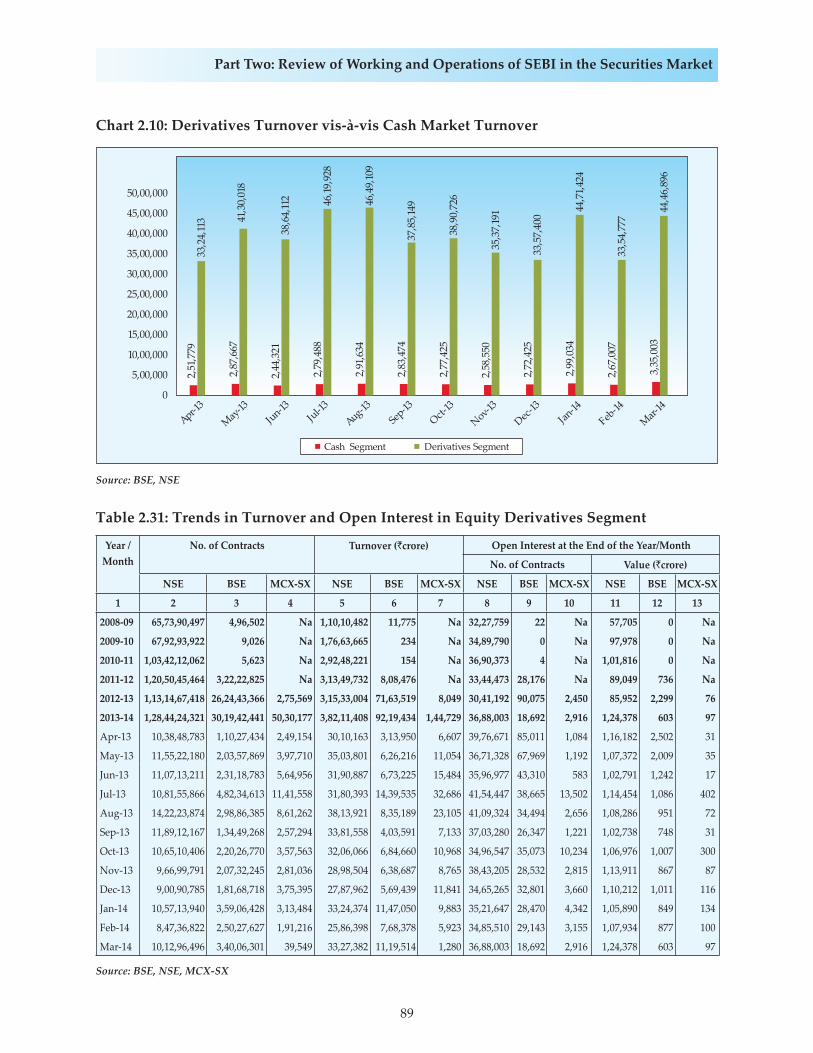

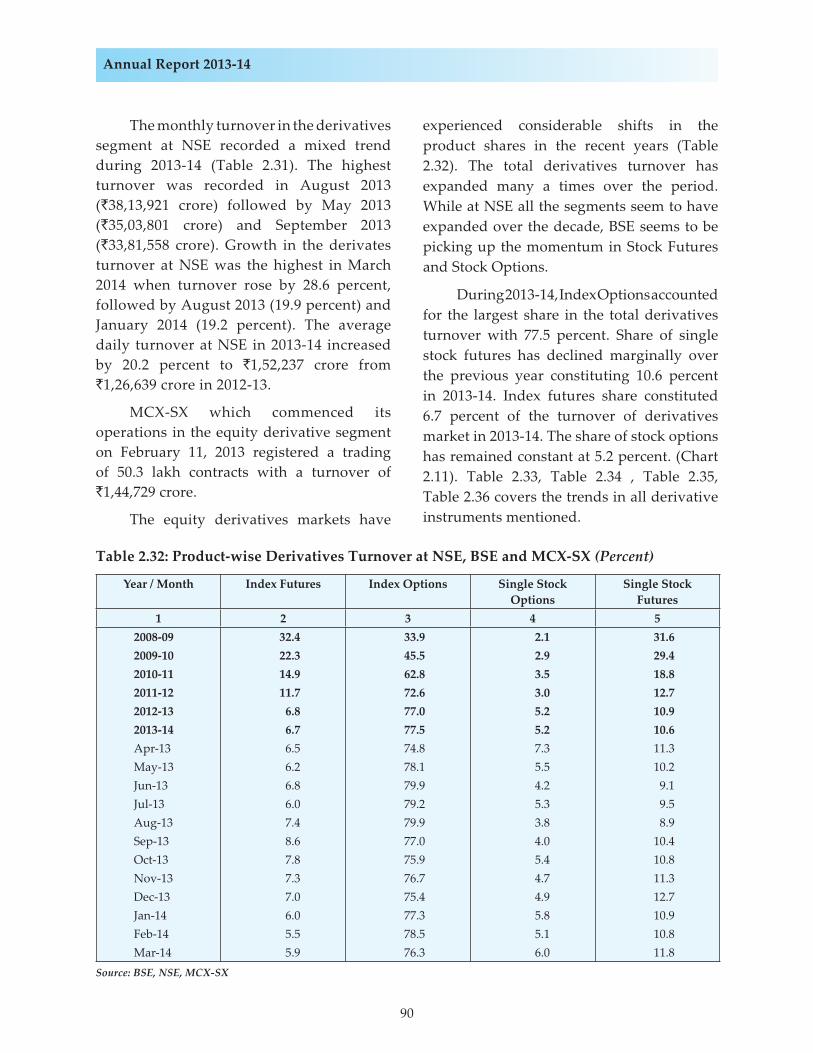

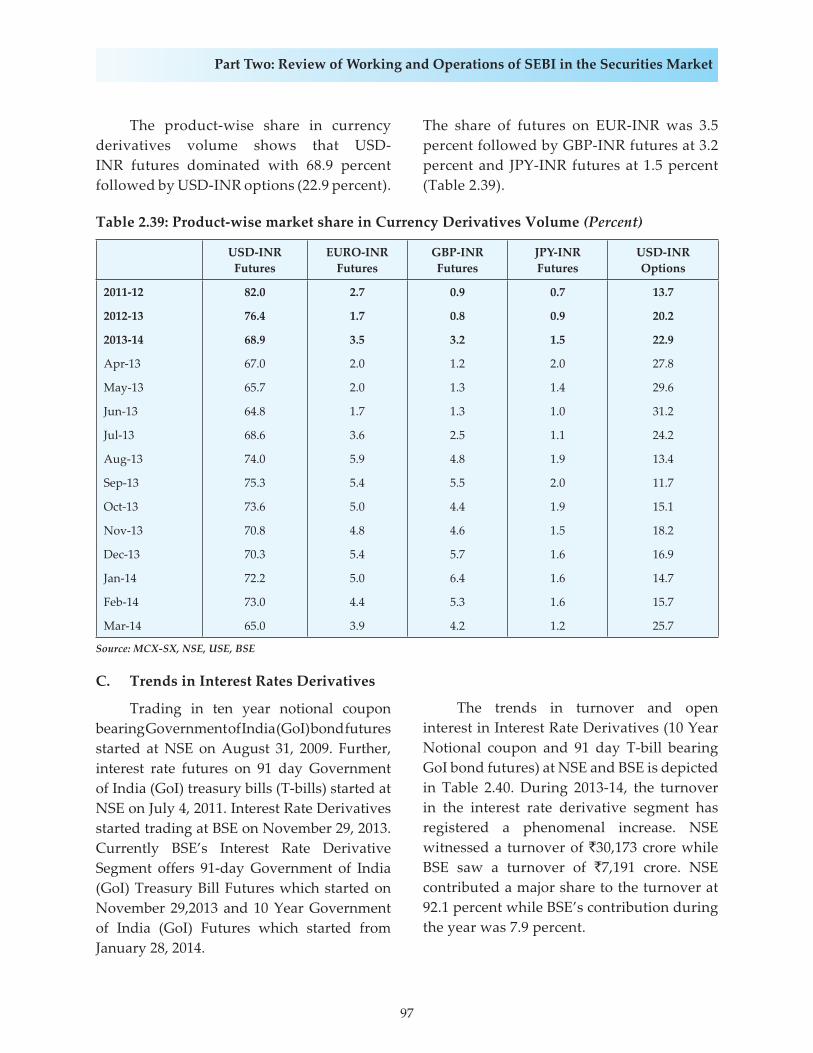

X. Derivatives Segment ............................................................................................................ 88

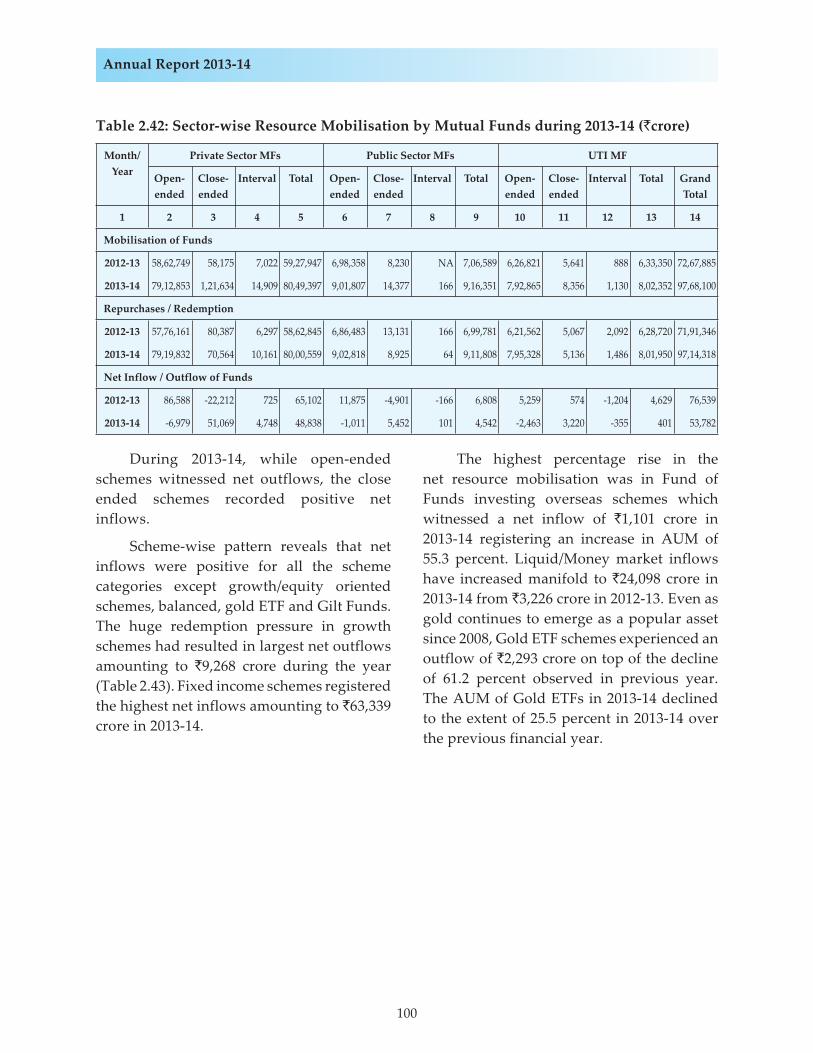

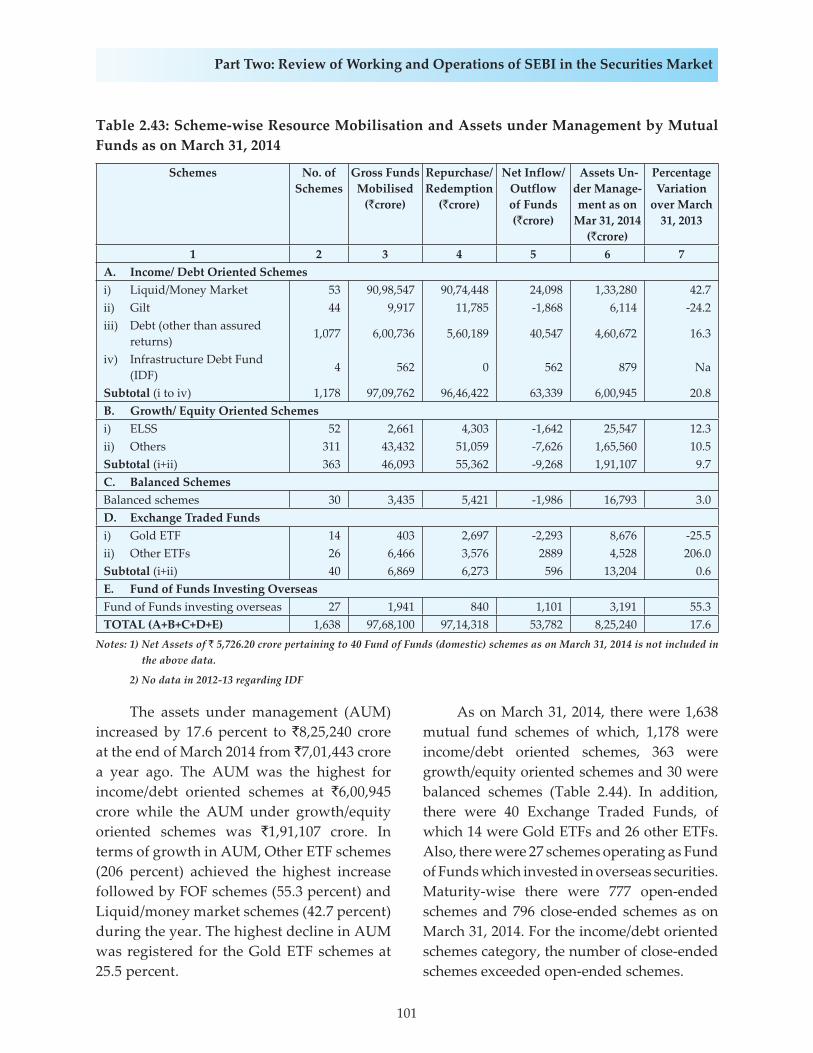

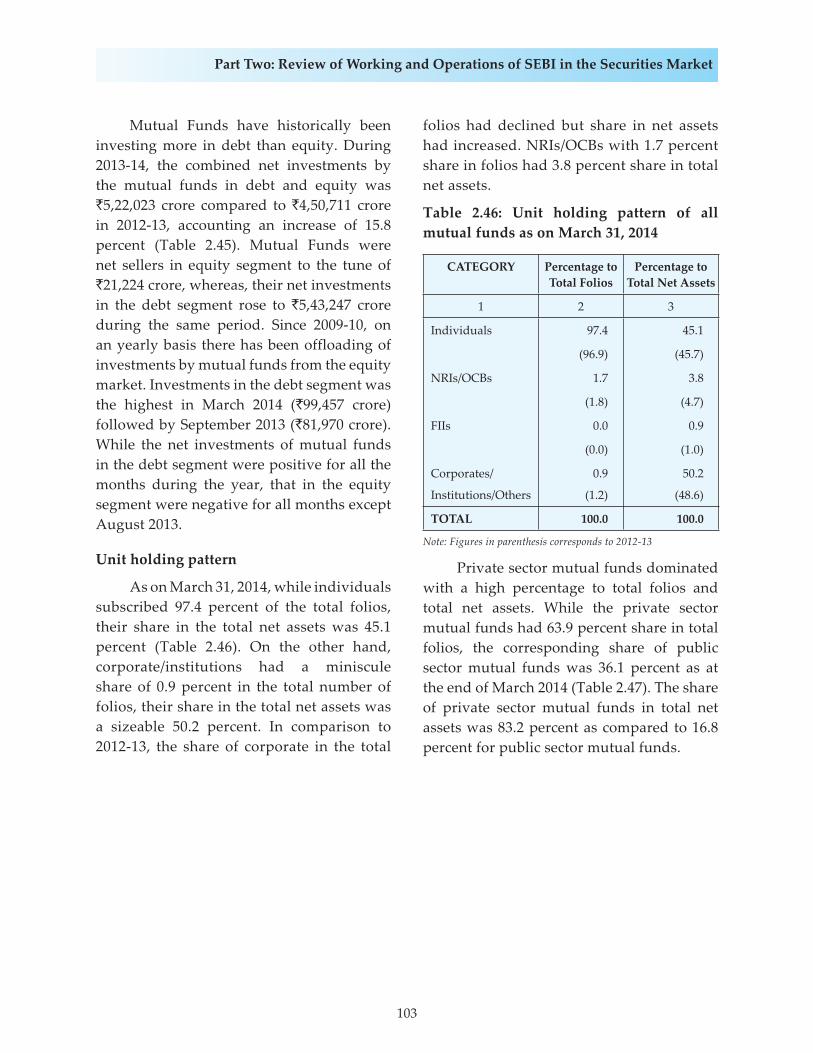

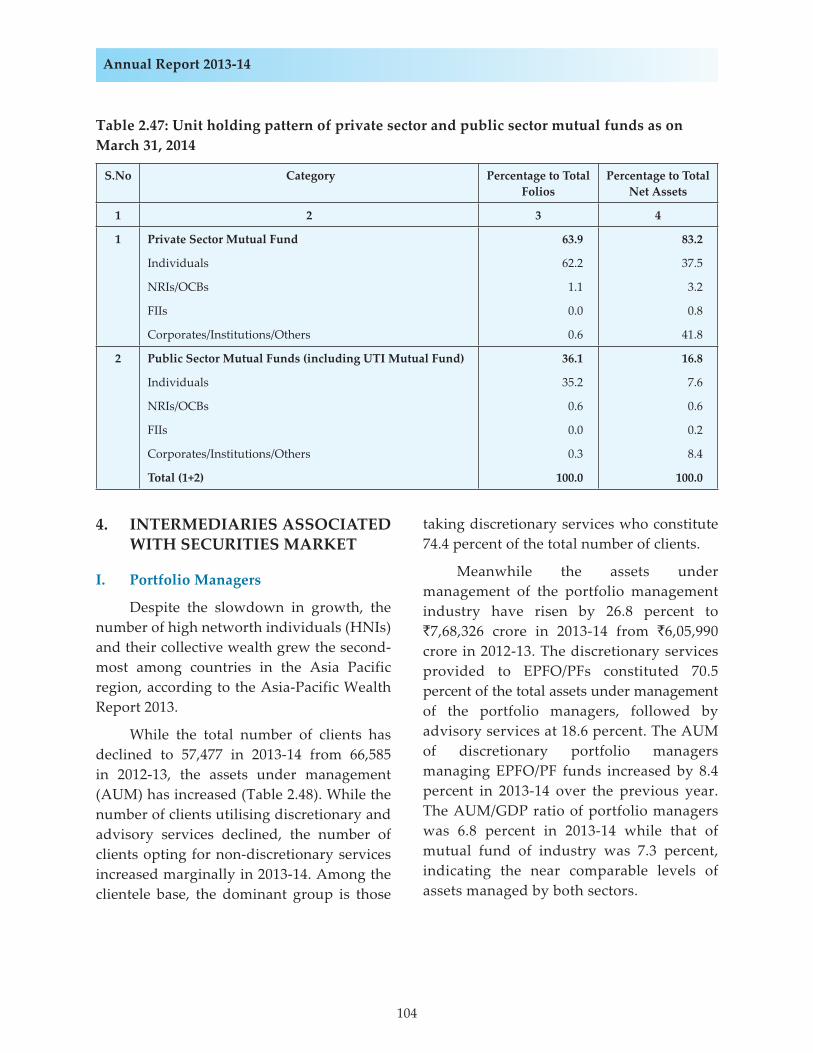

3. MUTUAL FUNDS .......................................................................................................................... 98

4. INTERMEDIARIES ASSOCIATED WITH SECURITIES MARKET.. ............................... 104

I. Portfolio Managers ............................................................................................................. 104

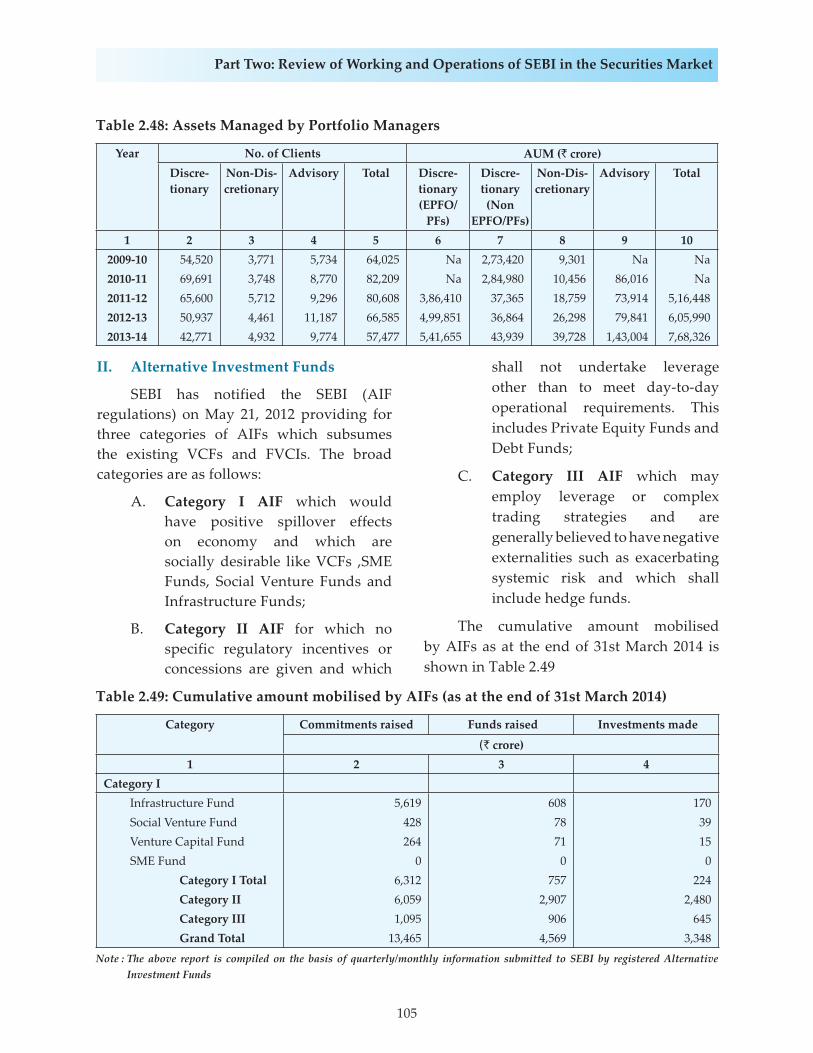

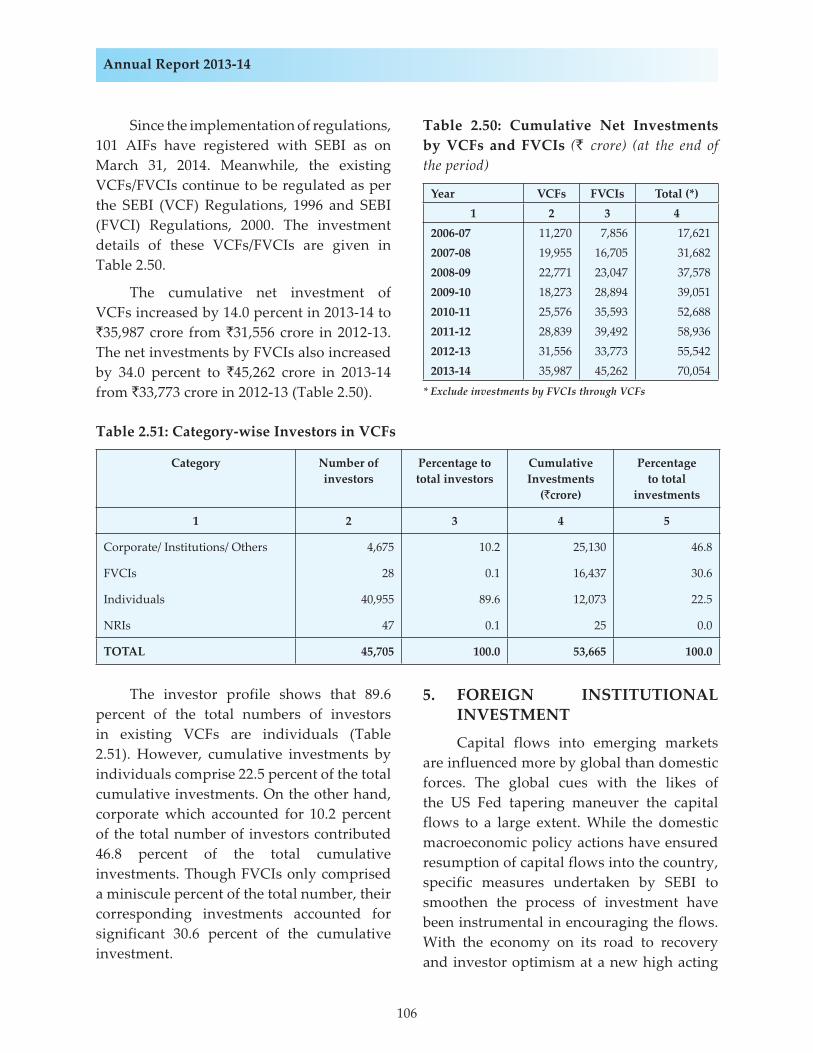

II. Alternative Investment Funds .......................................................................................... 105

5. FOREIGN INSTITUTIONAL INVESTMENT ....................................................................... 106

6. OTHER ACTIVITIES HAVING A BEARING ON THE WORKING OF SECURITIES MARKET ........................................................................................................................................ 112

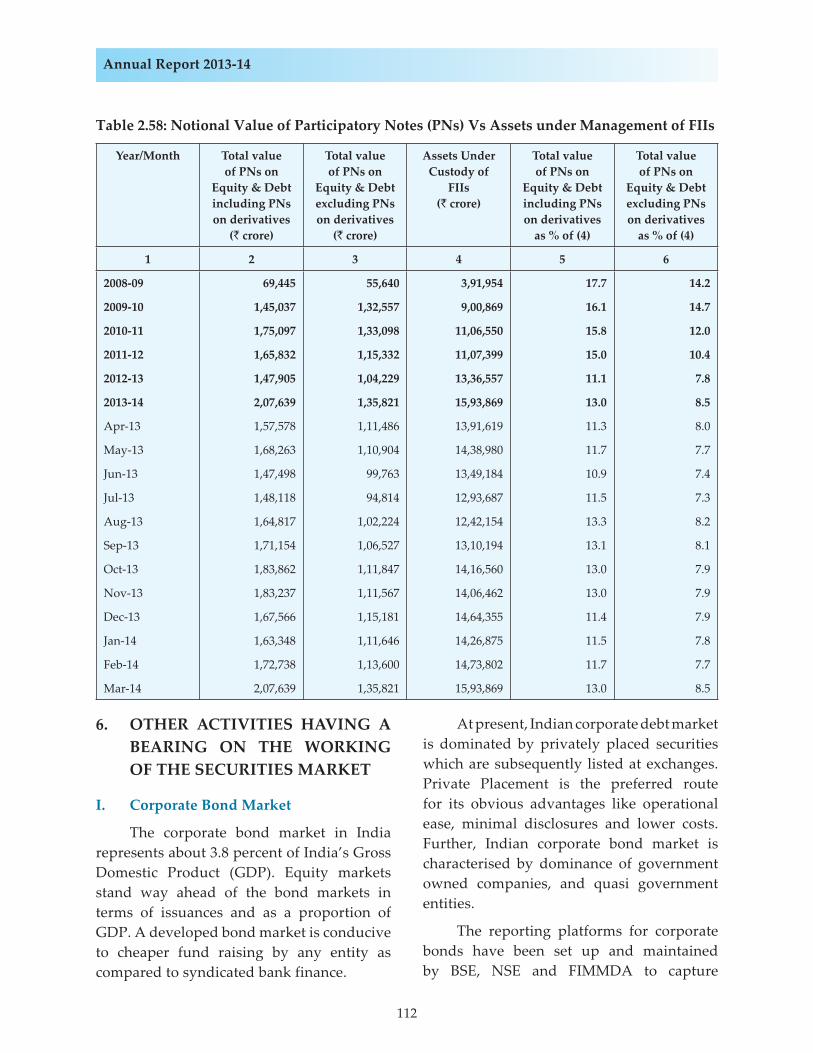

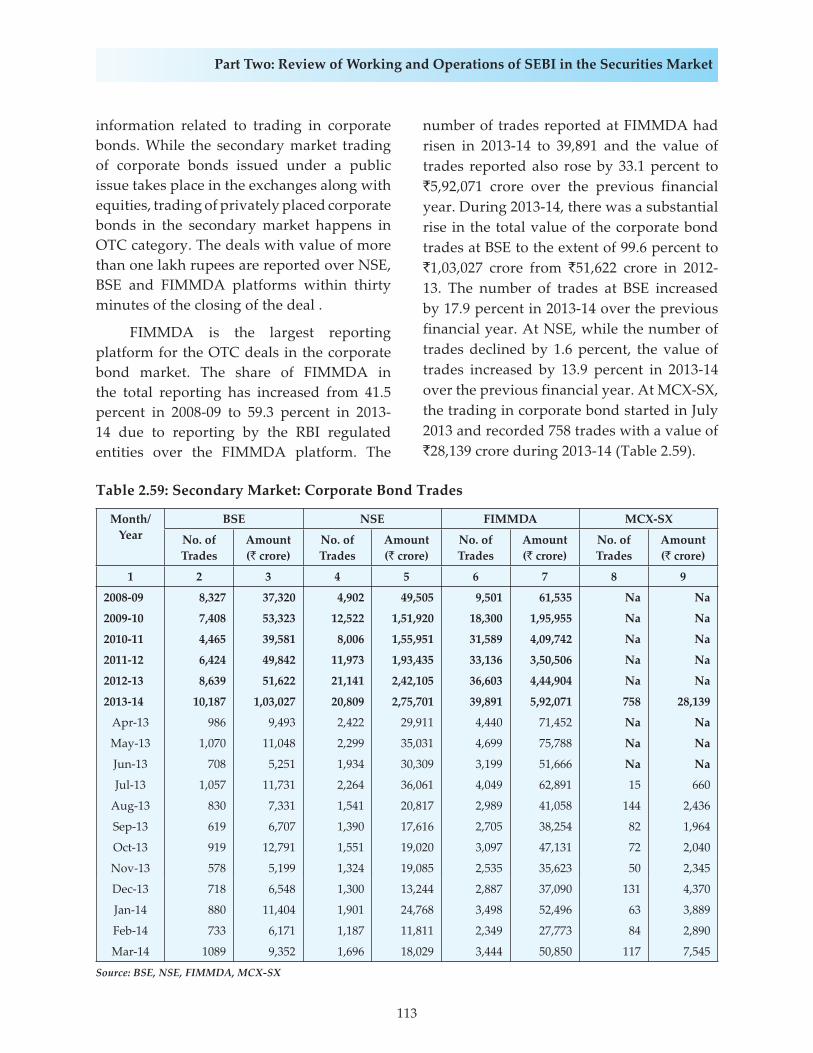

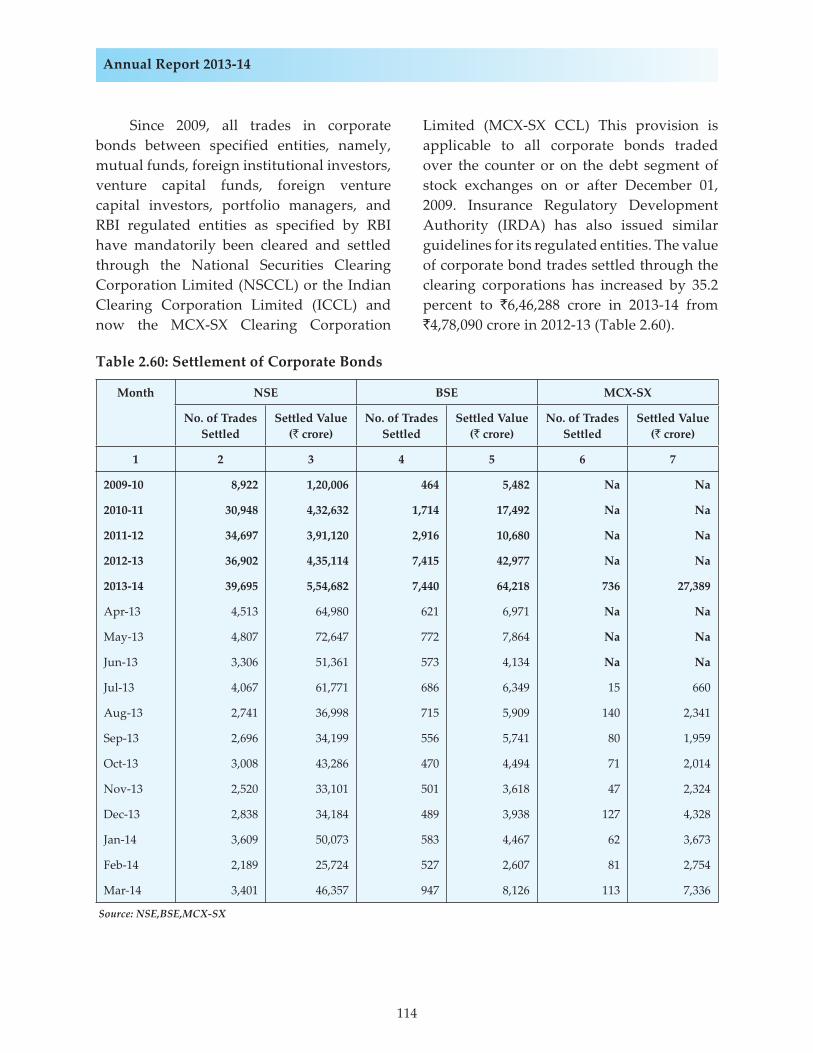

I. Corporate Bond Market ..................................................................................................... 112

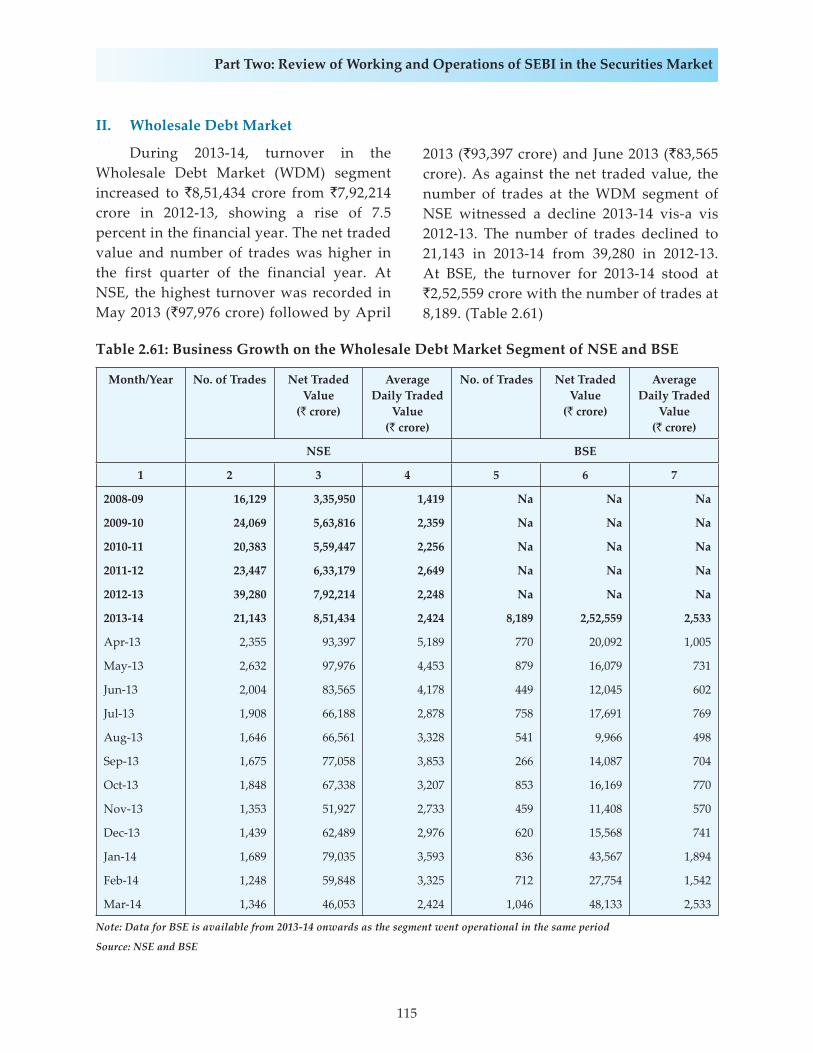

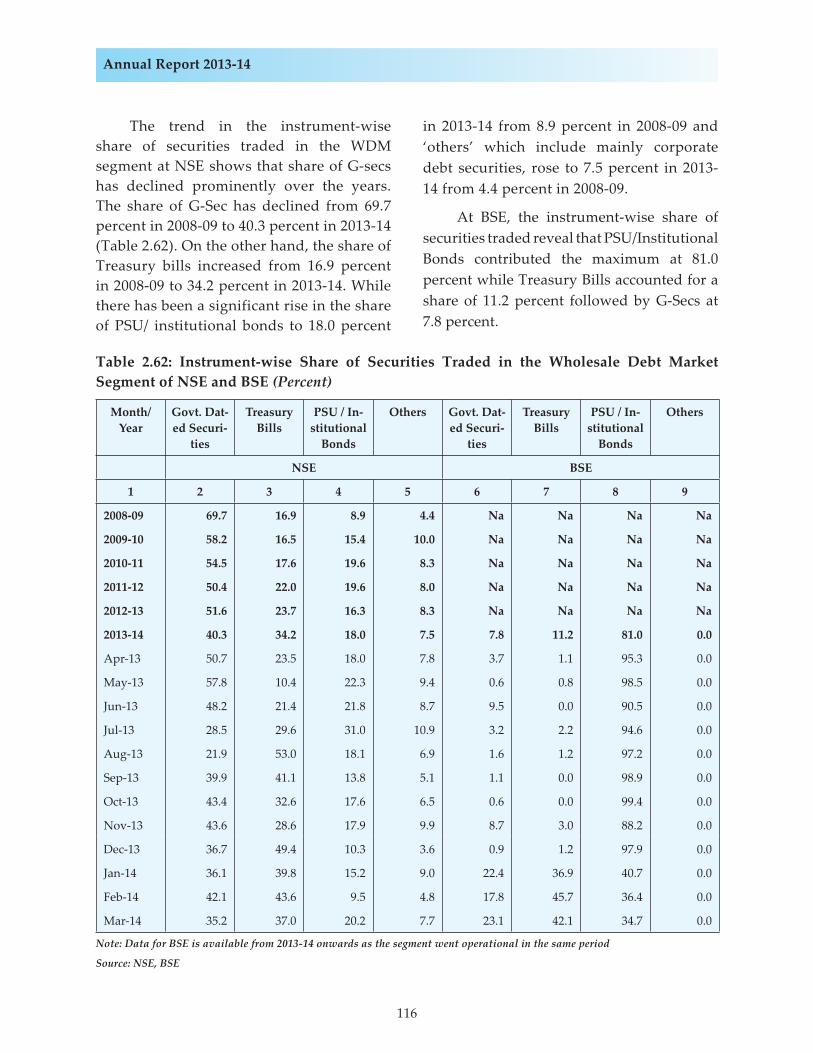

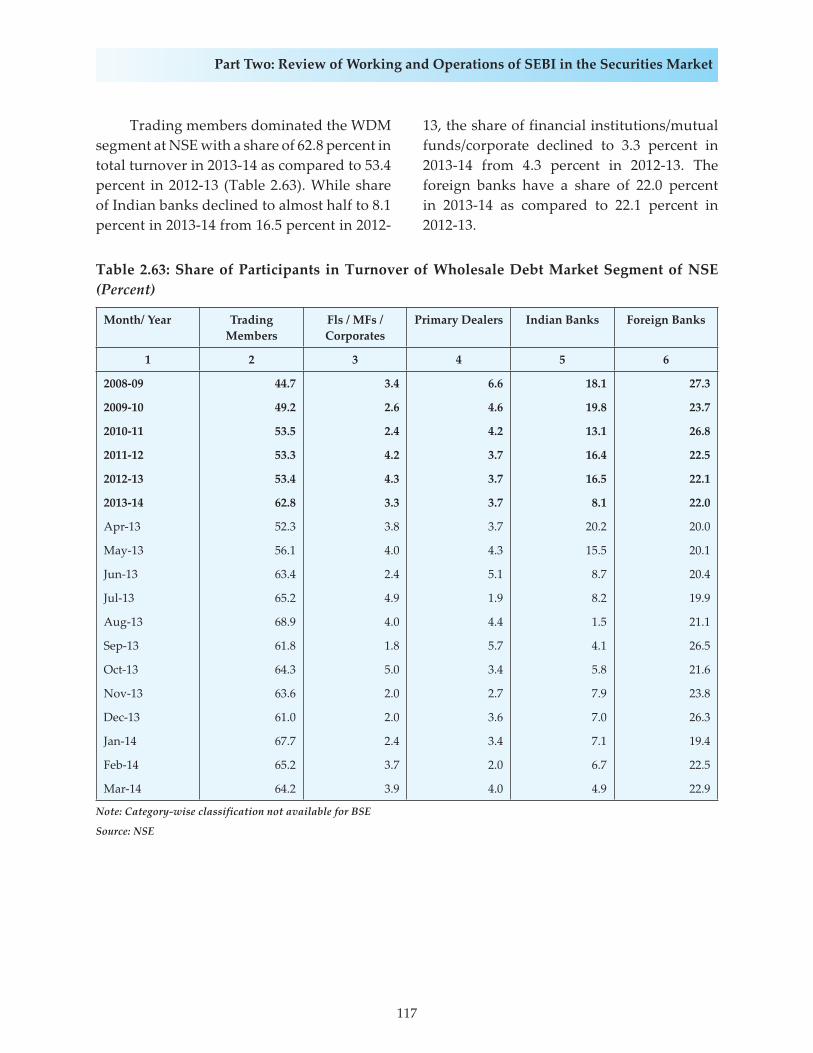

II. Wholesale Debt Market ..................................................................................................... 115

PART THREE: FUNCTIONS OF SEBI IN RESPECT OF MATTERS SPECIFIED IN SECTION 11 OF SEBI ACT, 1992

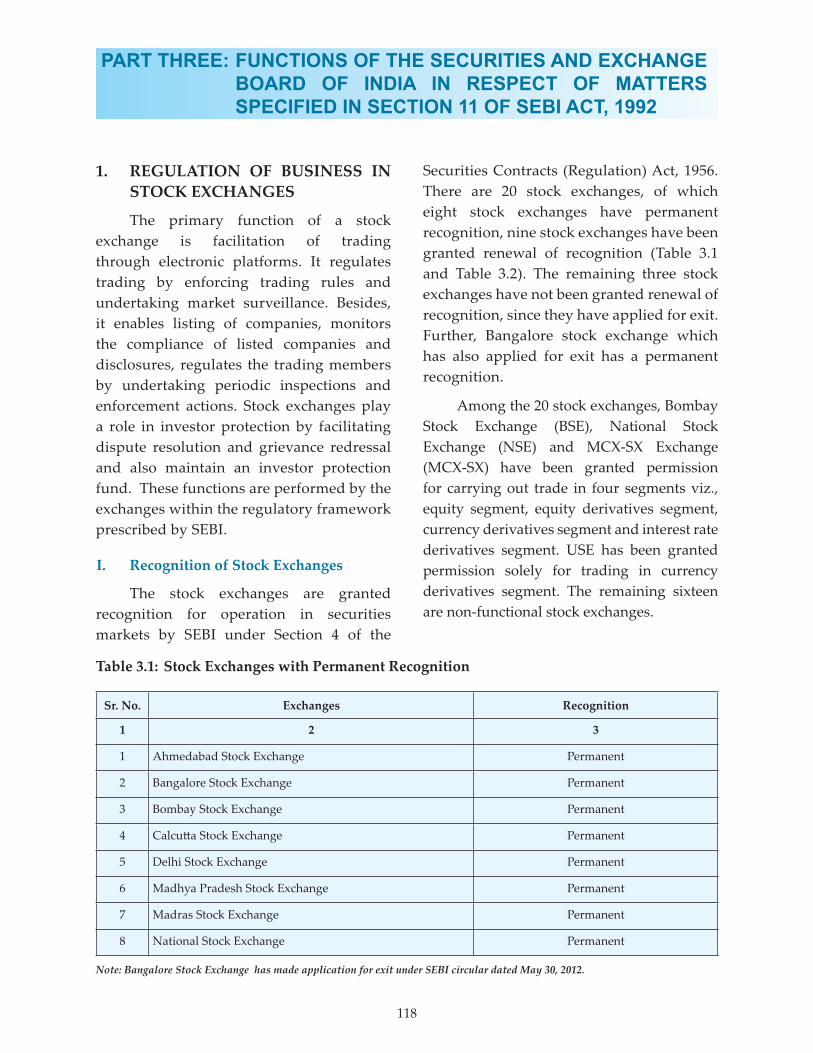

1. REGULATION OF BUSINESS IN STOCK EXCHANGES .................................................. 118

I. Recognition of Stock Exchanges ....................................................................................... 118

II. Trading and Settlement Practices at Stock Exchanges .................................................. 119

III. Memorandum of Understanding (MoU) between Stock Exchanges .......................... 120

IV. Steps taken by SEBI to ring-fence MCX-SX .................................................................... 120

V. Exit of Stock Exchange ....................................................................................................... 121

VI. Measures adopted for Regulation of Stock Exchanges ................................................. 122

2. REGISTRATION AND REGULATION OF WORKING OF INTERMEDIARIES ASSOCIATED WITH THE SECURITIES MARKET ............................................................ 122

I. Streamlining the Process of Initial / Permanent Registration of Intermediaries ....... 123

II. Measures for Regulation of Intermediaries .................................................................... 124

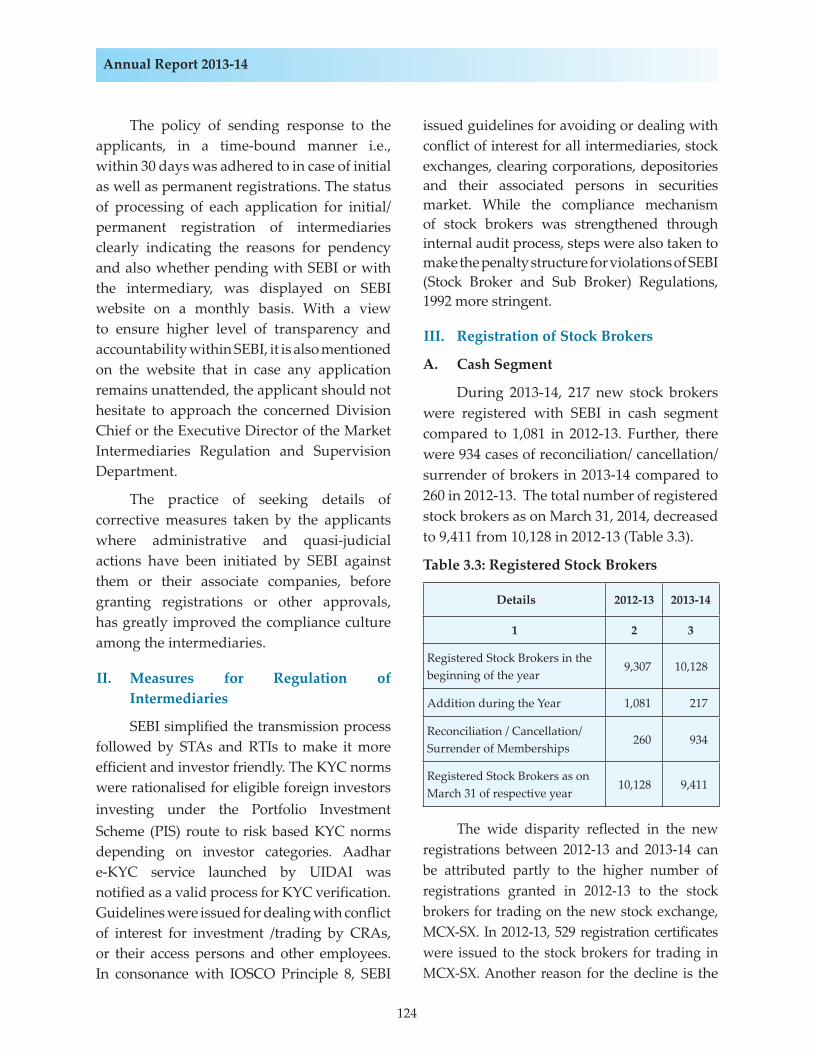

III. Registration of Stock Brokers ............................................................................................ 124

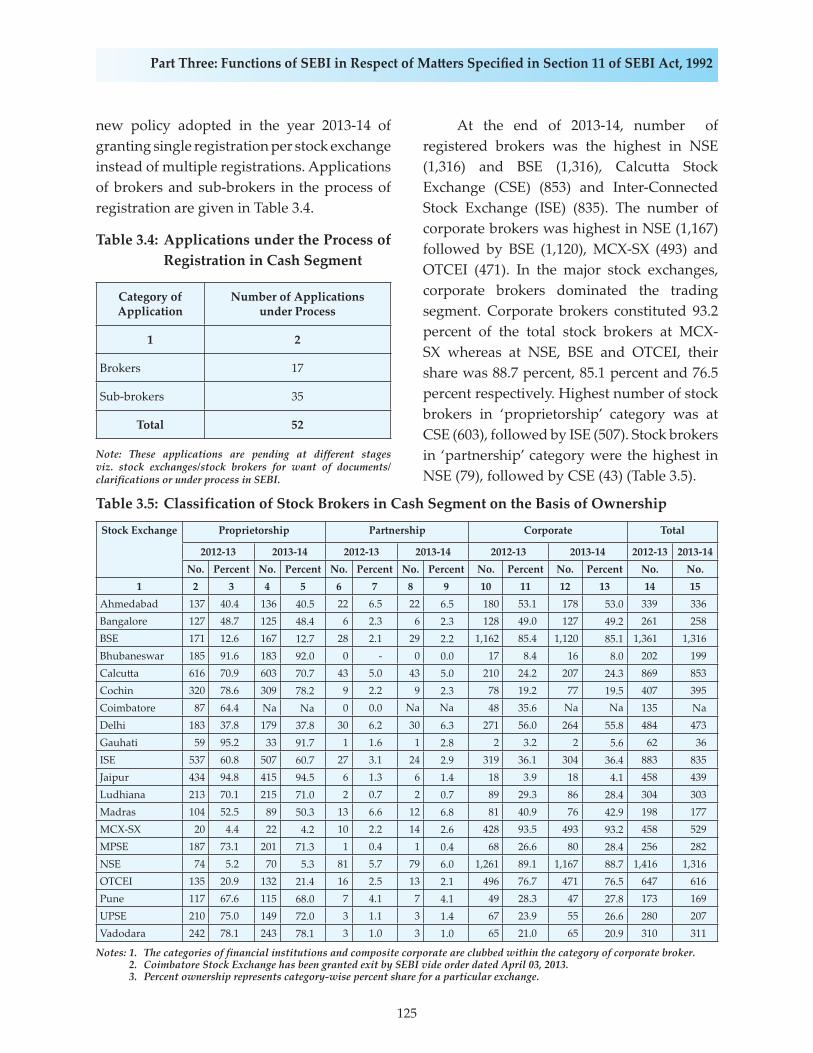

IV. Registration of Sub-brokers .............................................................................................. 127

V. Registration of Other Intermediaries ............................................................................... 128

VI. Registration of Foreign Institutional Investors, Sub-Accounts and Custodians ....... 129

VII. Registration of Venture Capital Funds and Alternative Investment Funds .............. 130

VIII. Registration of Portfolio Managers and Investment Advisers ..................................... 133

CONTENTS

Page No.

iii

3. REGISTRATION AND REGULATION OF WORKING OF COLLECTIVE INVESTMENT SCHEMES INCLUDING MUTUAL FUNDS ............................................ 134

I. Registration of Collective Investment Schemes ............................................................. 134

II. Inspection of Collective Investment Schemes ................................................................ 134

III. Regulatory actions against Collective Investment Schemes ........................................ 134

IV. Registration and Regulation of Mutual Funds............................................................... 139

4. PROMOTION AND REGULATION OF SELF REGULATORY ORGANISATIONS .... 140

5. FRAUDULENT AND UNFAIR TRADE PRACTICES .......................................................... 140 I. Types of fraudulent and unfair trade practices .............................................................. 140

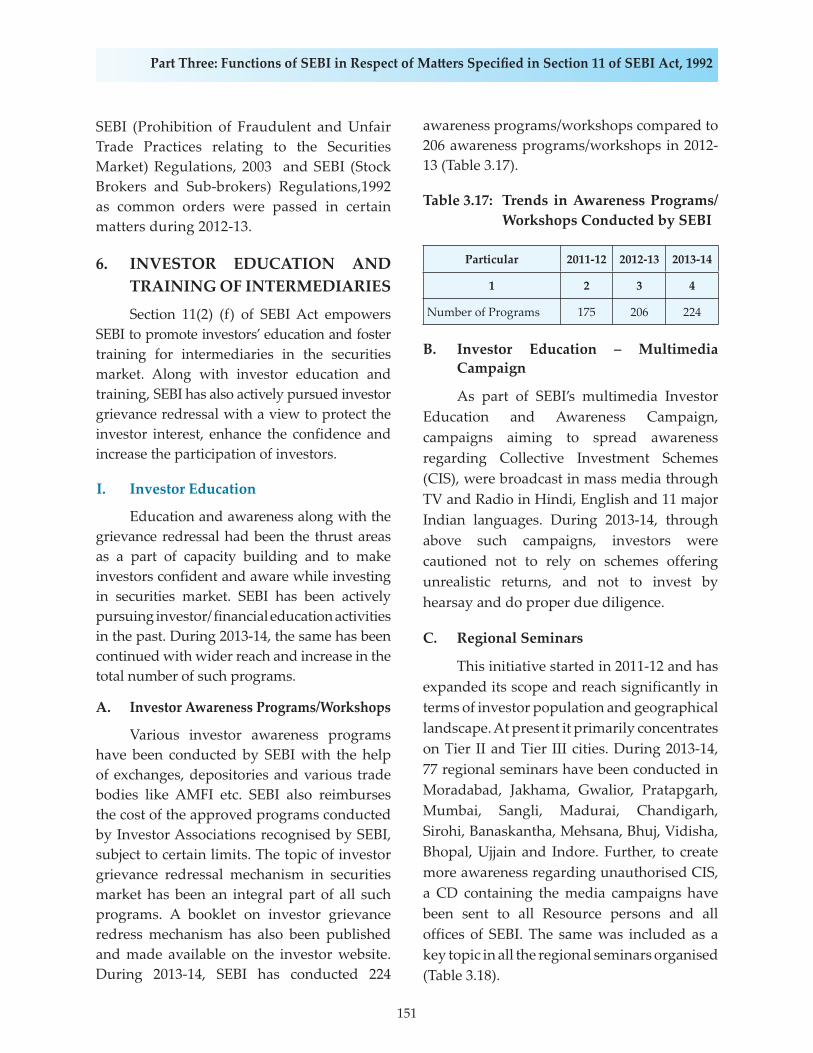

II. Fraudulent and unfair trade practices cases during 2013-14 ....................................... 141

III. Steps taken to prevent the occurrence of fraudulent and unfair trade practices ...... 150

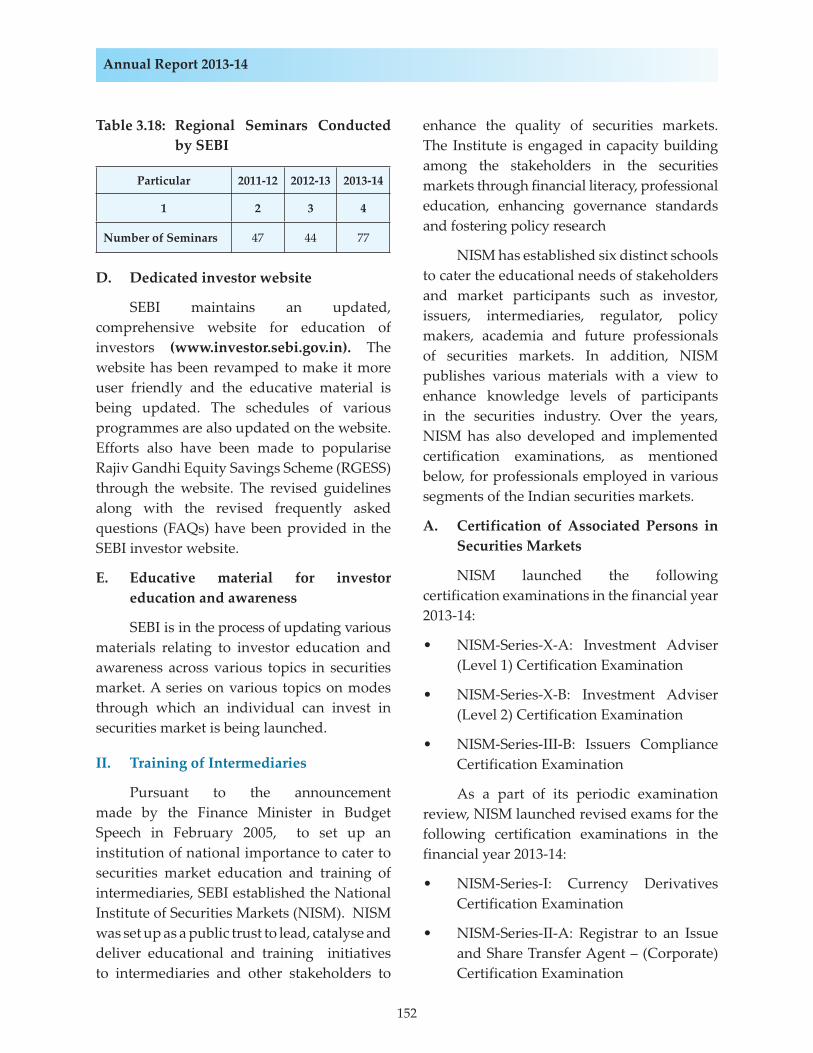

6. INVESTOR EDUCATION AND TRAINING OF INTERMEDIARIES ............................ 151

I. Investor Education ............................................................................................................. 151

II. Training of Intermediaries ................................................................................................. 152

III. Financial Education ............................................................................................................ 154

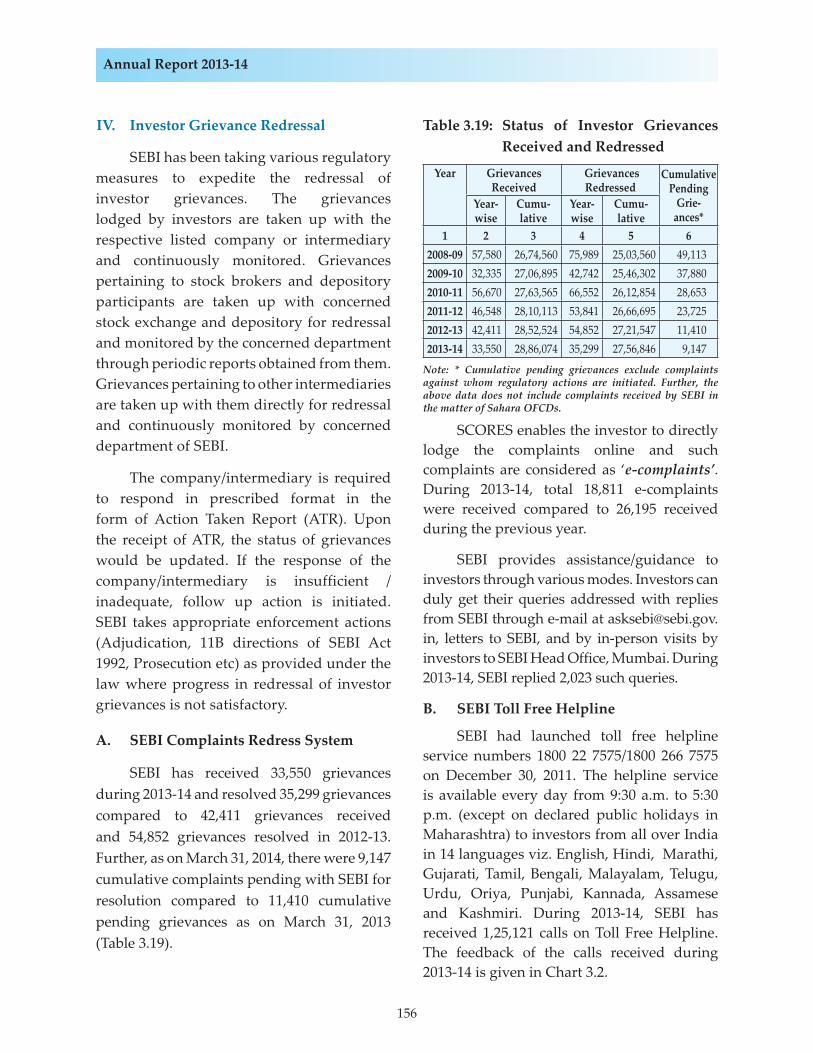

IV. Investor Grievance Redressal ........................................................................................... 156

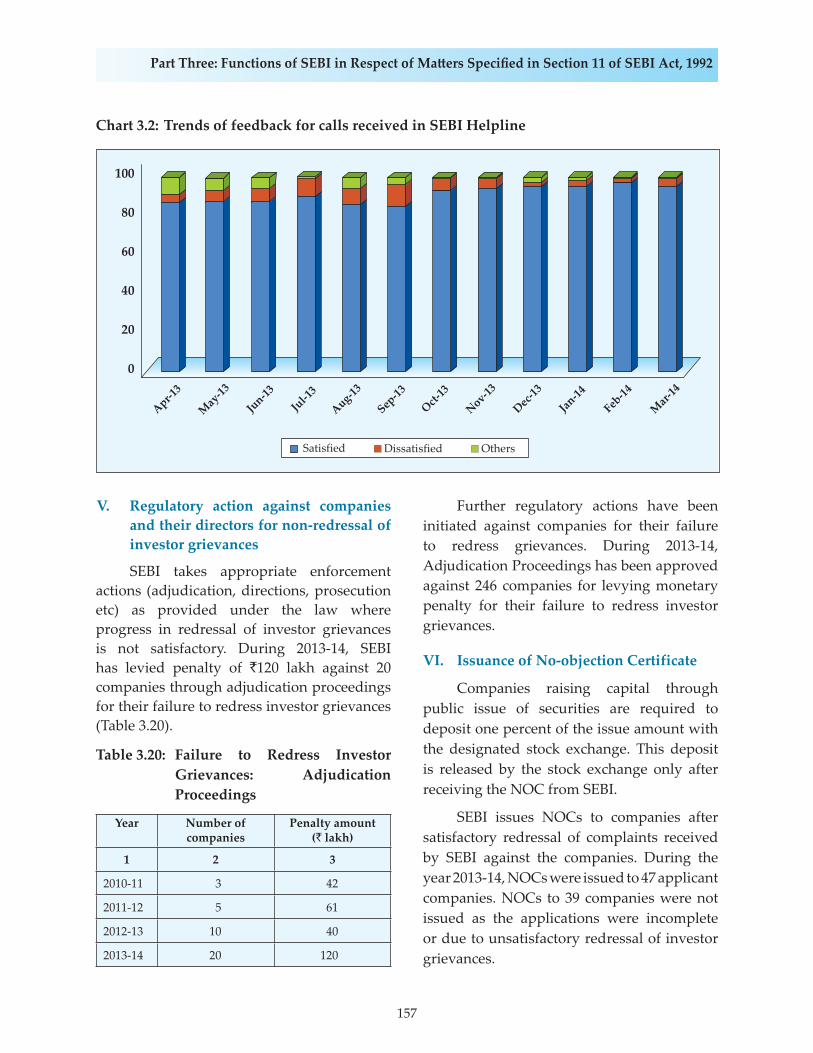

V. Regulatory action against companies and their directors for non-redressal of investor grievances ............................................................................................................. 157

VI. Issuance of No-objection Certificate ................................................................................ 157

7. PROHIBITION OF INSIDER TRADING ............................................................................... 158

I. Types of Insider trading practices .................................................................................... 158

II. Insider trading cases during 2013-14 ............................................................................... 158

III. Steps initiated to curb Insider Trading practices ........................................................... 164

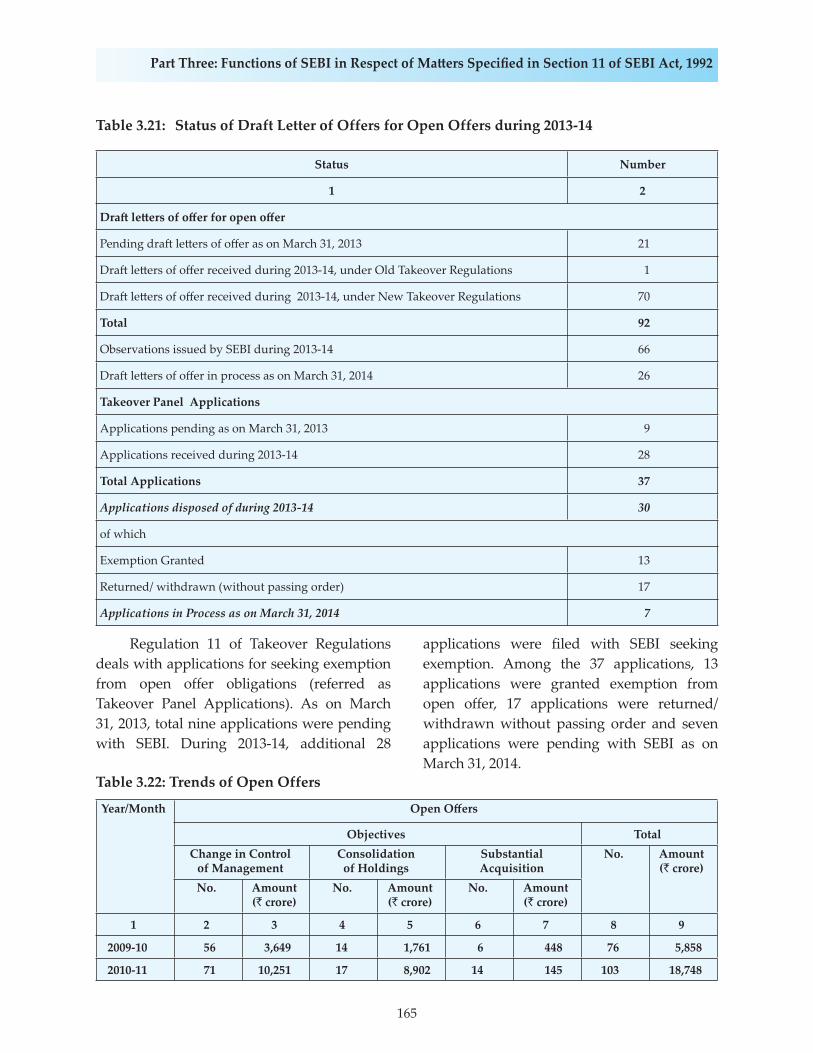

8. SUBSTANTIAL ACQUISITION OF SHARES AND TAKEOVERS .................................. 164

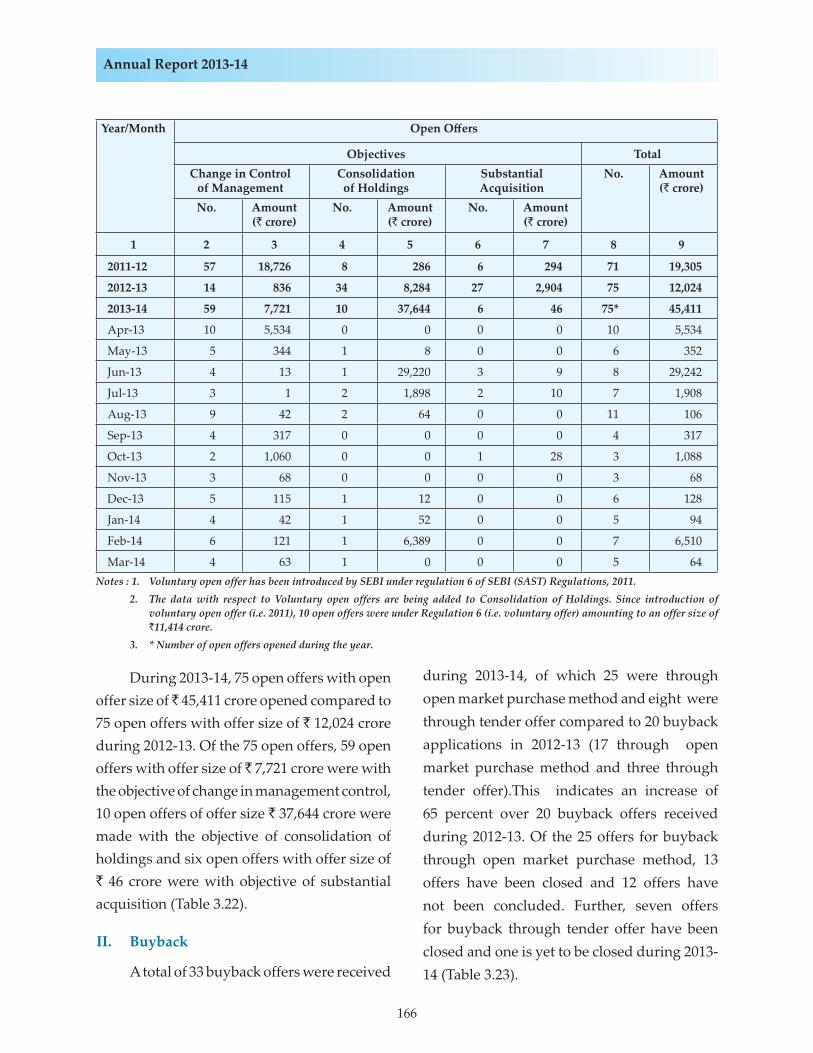

I. Open Offer ........................................................................................................................... 164

II. Buyback ................................................................................................................................ 166

9. INFORMATION CALLED FROM, INSPECTION UNDERTAKEN, INQUIRIES AND AUDIT OF STOCK EXCHANGES AND INTERMEDIARIES AND SELF REGULATING ORGANISATIONS CONDUCTED BY SEBI ............................................ 167

I. Inspection of Stock Exchanges, Depositories and Clearing Corporations ................. 167

II. Inspection of Market Intermediaries……..………..………..………..………..… ......... 168

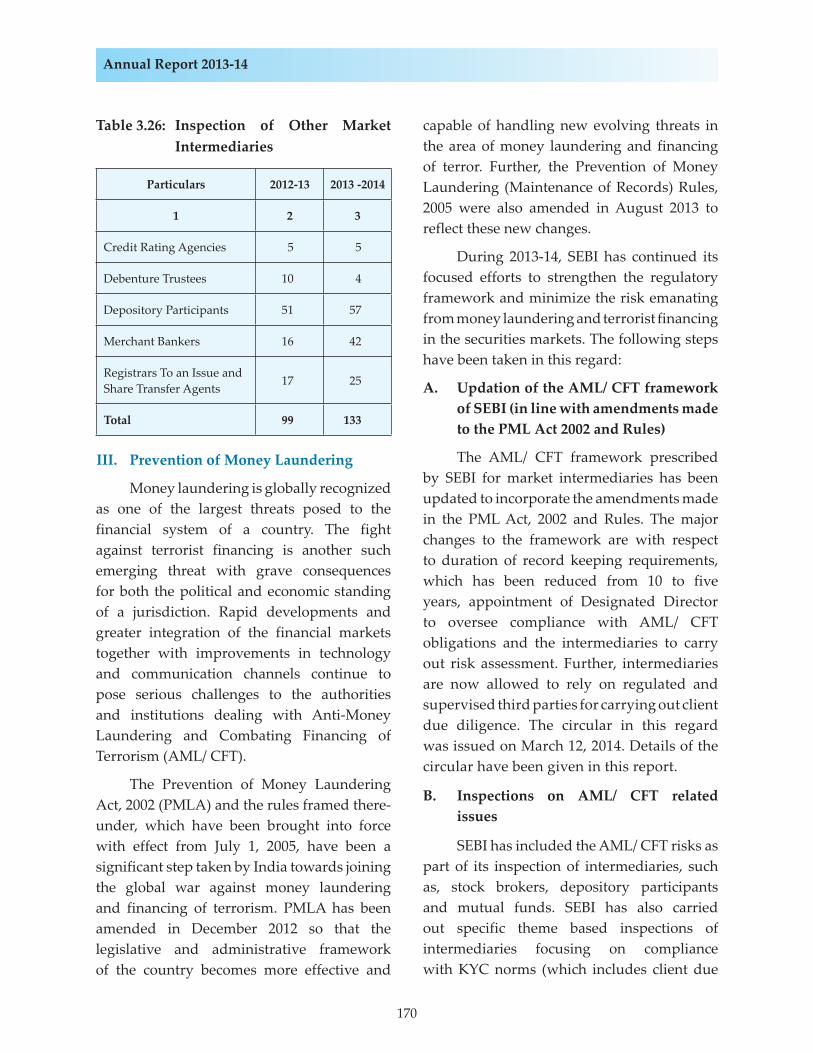

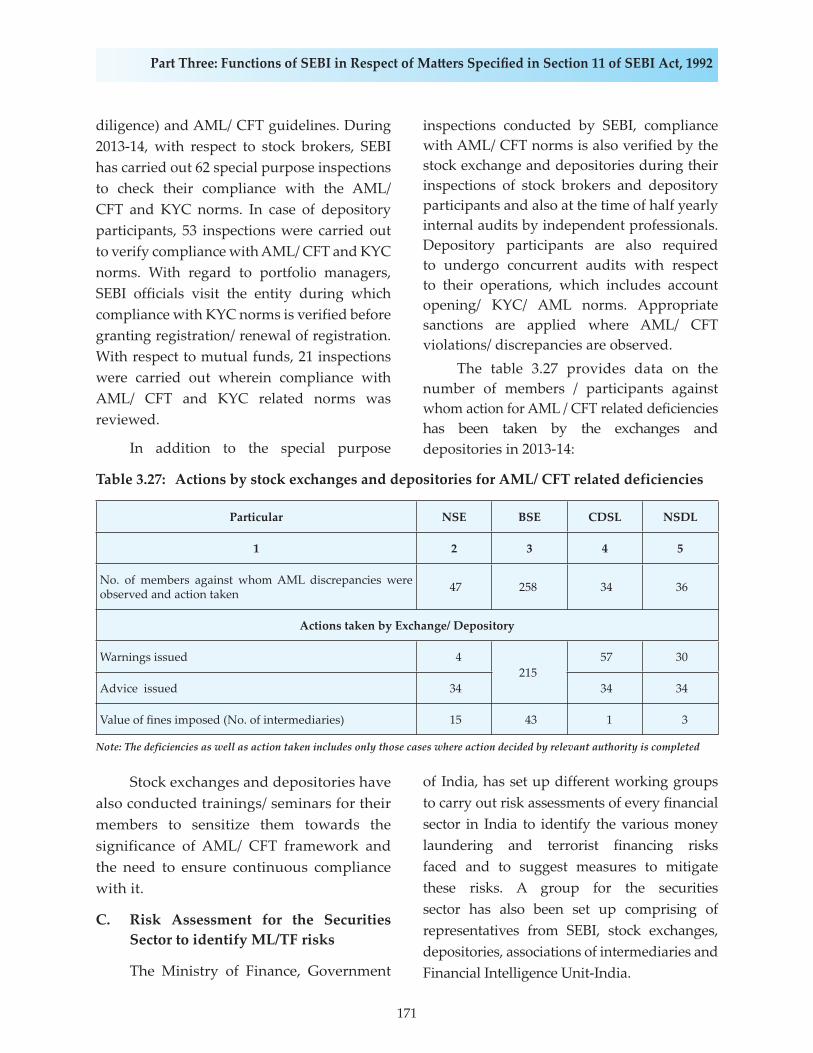

III. Prevention of Money Laundering .................................................................................... 170

CONTENTS

Page No.

iv

10. DELEGATED POWERS AND FUNCTIONS .......................................................................... 172

11. FEES AND OTHER CHARGES................................................................................................. 173

12. RESEARCH AND STUDIES ...................................................................................................... 175

I. Research Activities ............................................................................................................. 175

II. Systemic Stability Unit ...................................................................................................... 175

III. Academic Interactions ....................................................................................................... 176

IV. International Research Conference .................................................................................. 176

V. New Research Initiatives ................................................................................................... 176

13. OTHER FUNCTIONS ................................................................................................................. 177

I. Surveillance ......................................................................................................................... 177

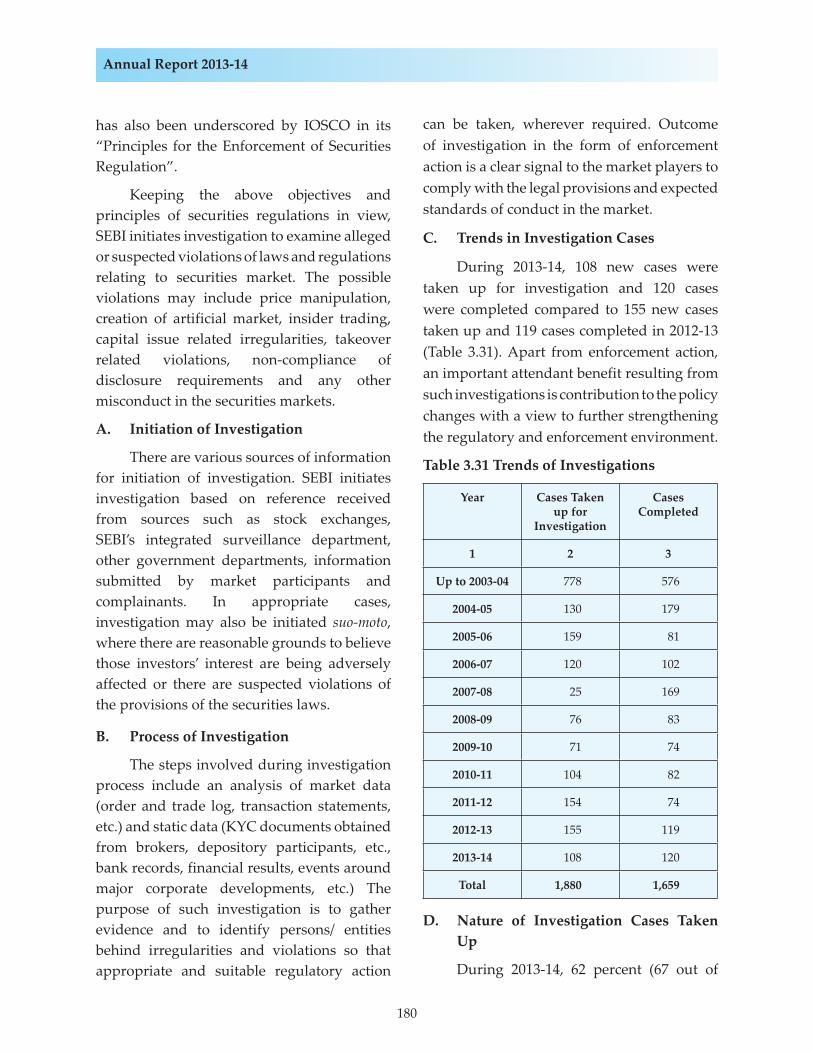

II. Investigation ........................................................................................................................ 179

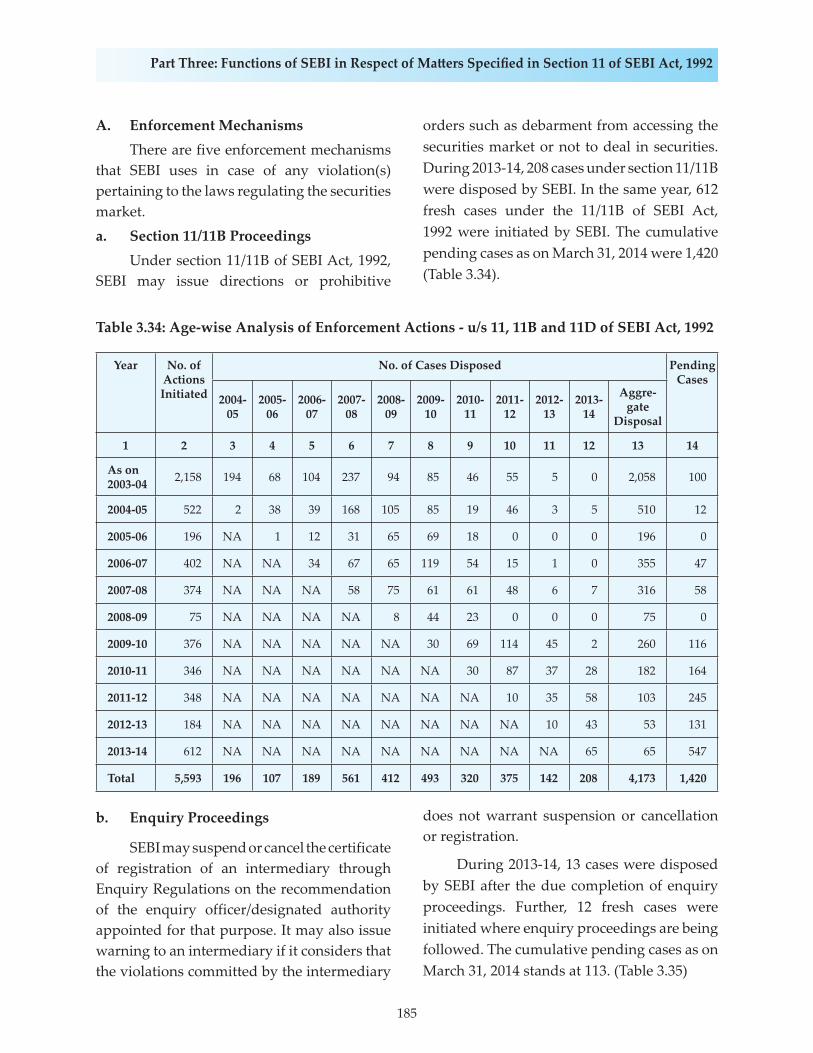

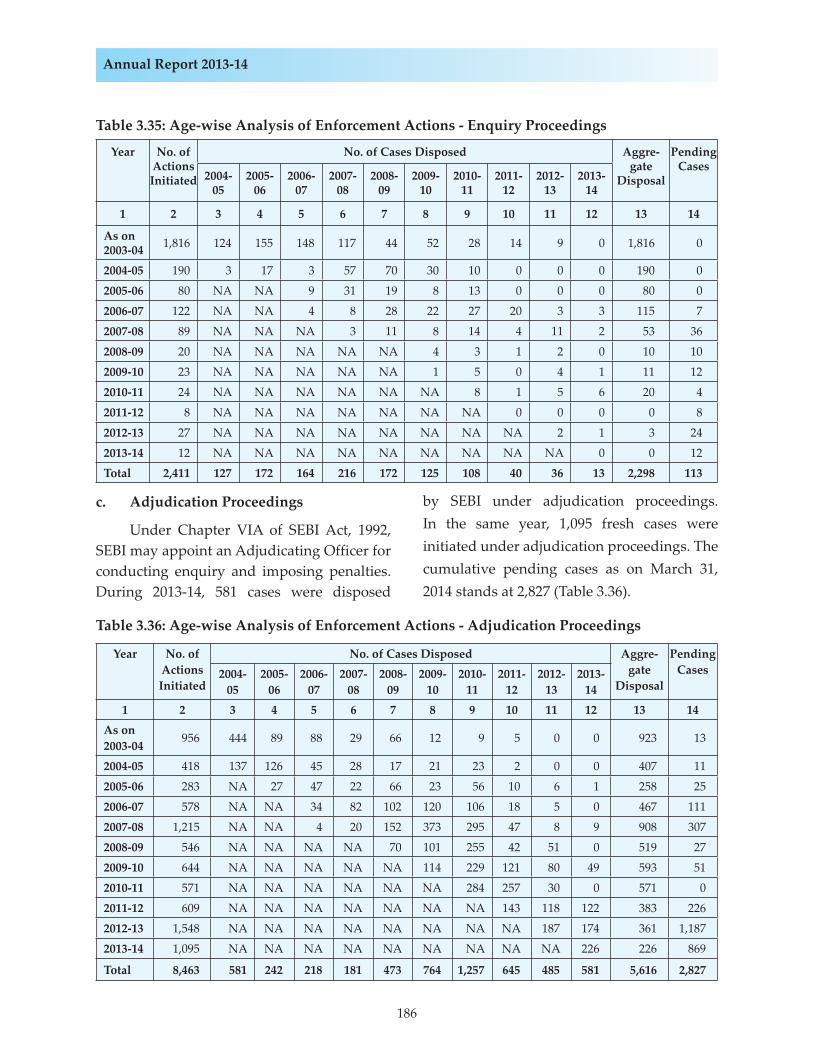

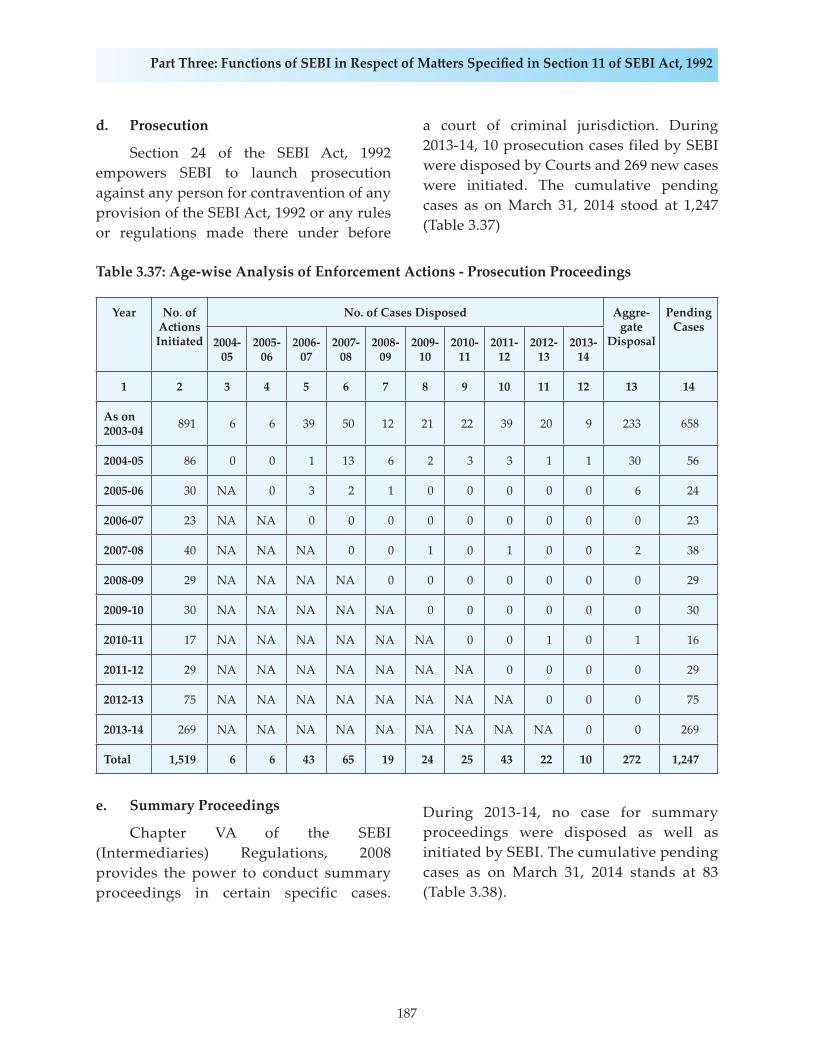

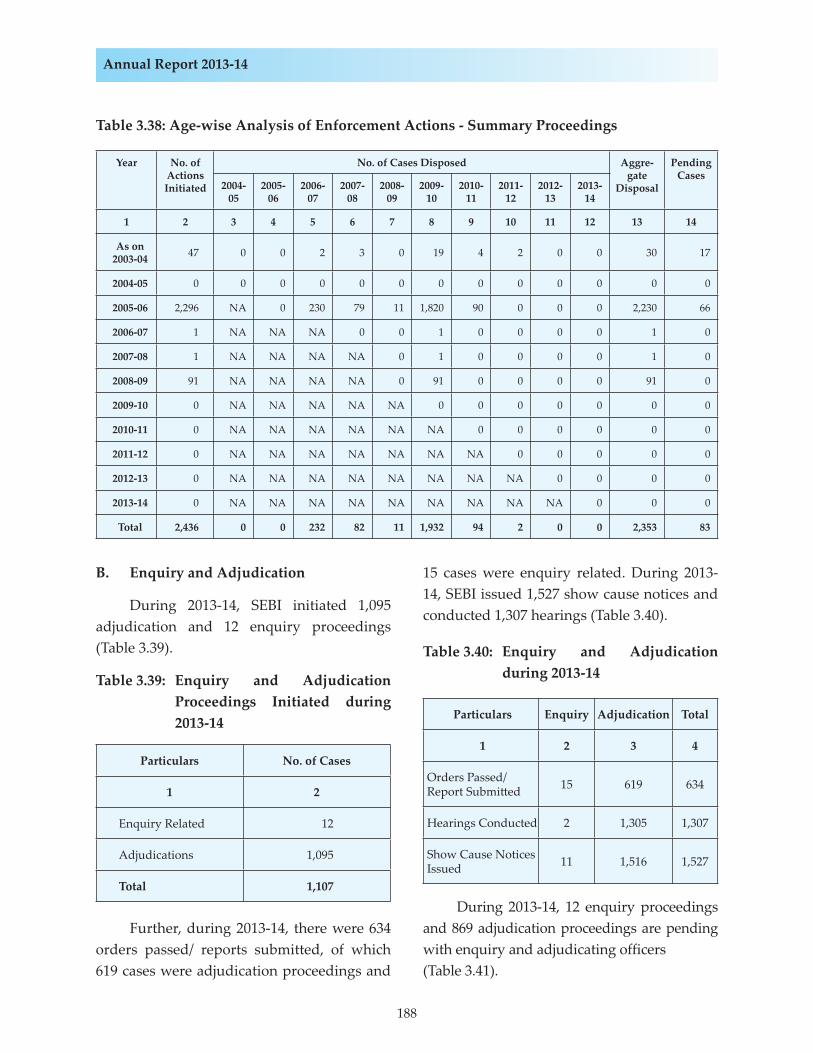

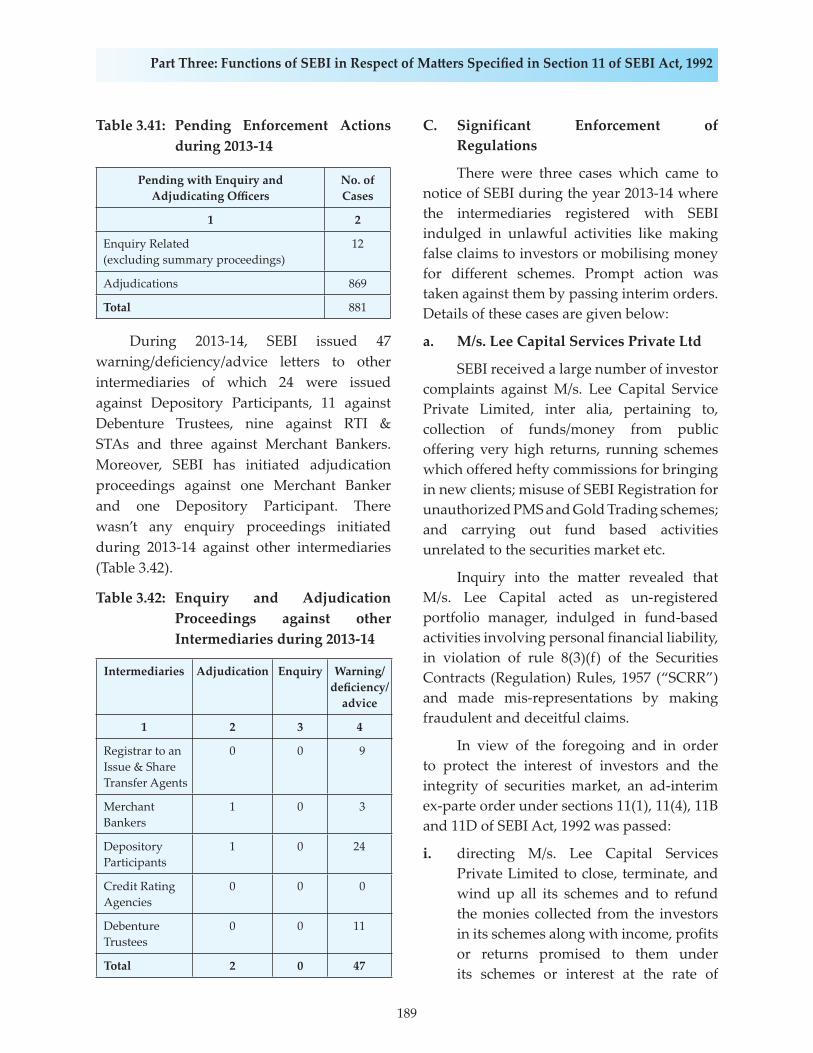

III. Enforcement of Regulations .............................................................................................. 184

IV. Prosecution .......................................................................................................................... 191

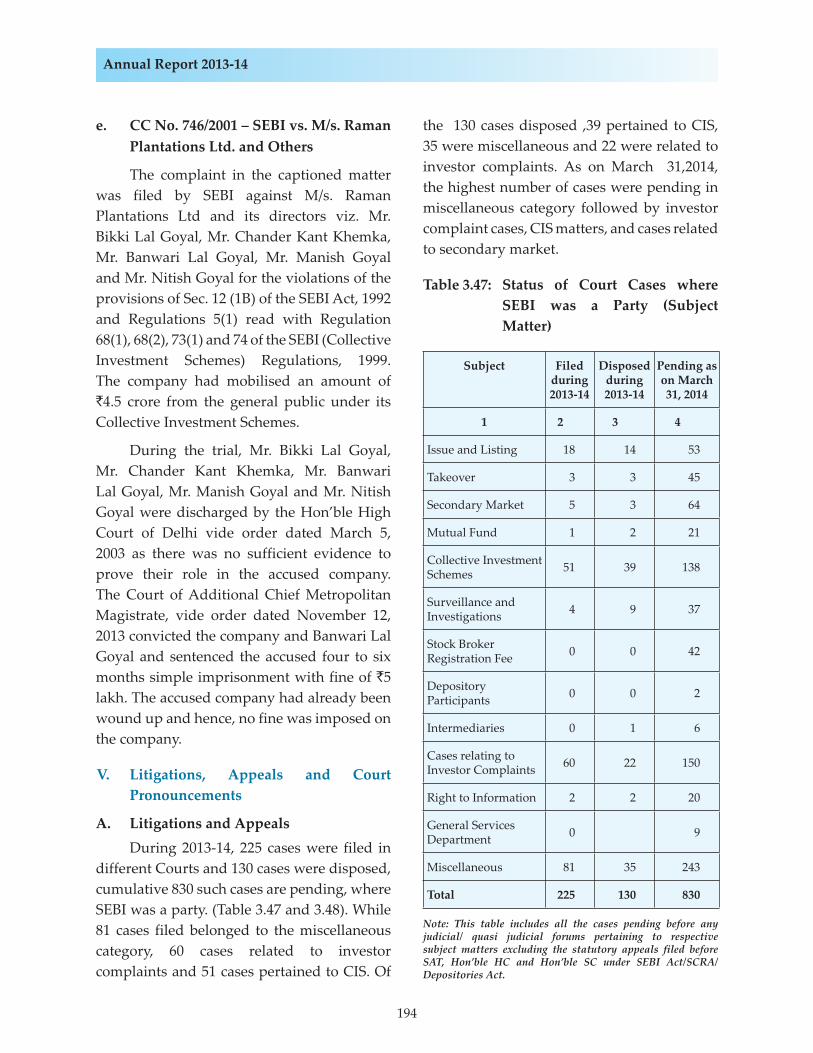

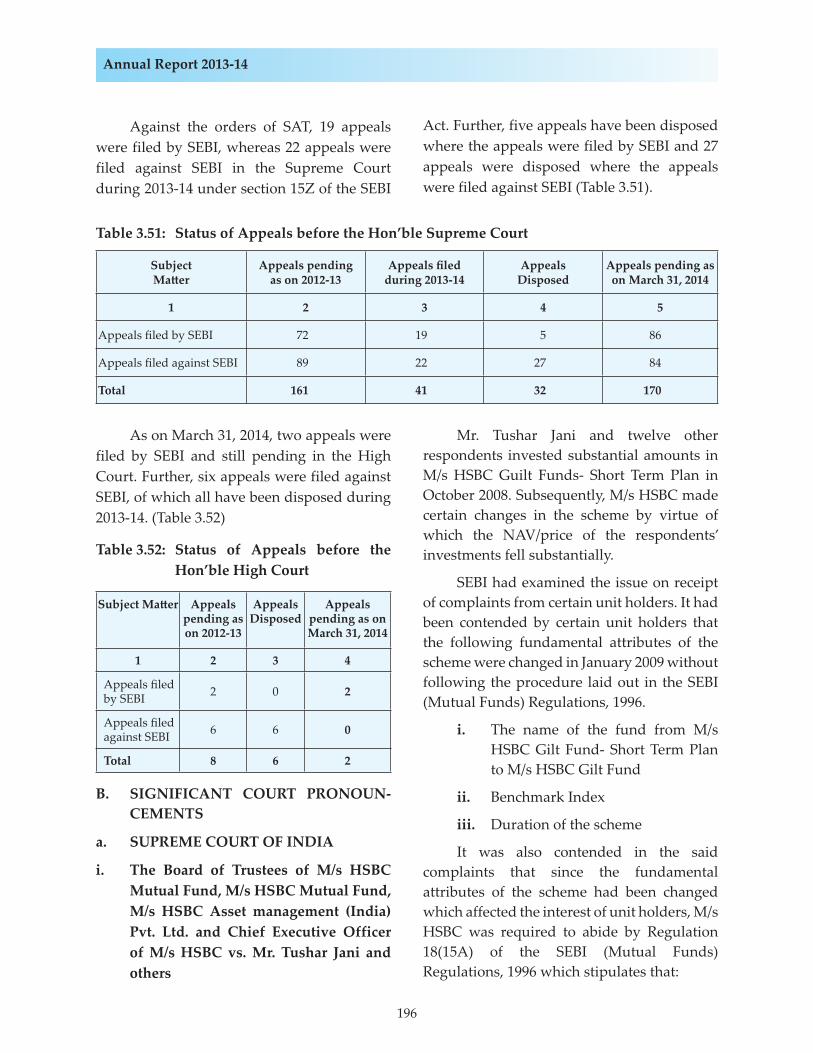

V. Litigations, Appeals and Court Pronouncements ......................................................... 194

VI. Consent and Compounding ............................................................................................. 211

VII. The Recovery Proceedings ................................................................................................ 212

VIII. Regulatory Changes ........................................................................................................... 213

IX. Right To Information Act, 2005......................................................................................... 221

X. Parliament Questions ......................................................................................................... 223

XI International Co-operation ............................................................................................... 224

XII. National Institute of Securities Markets .......................................................................... 237

PART FOUR: ORGANISATIONAL MATTERS OF SEBI

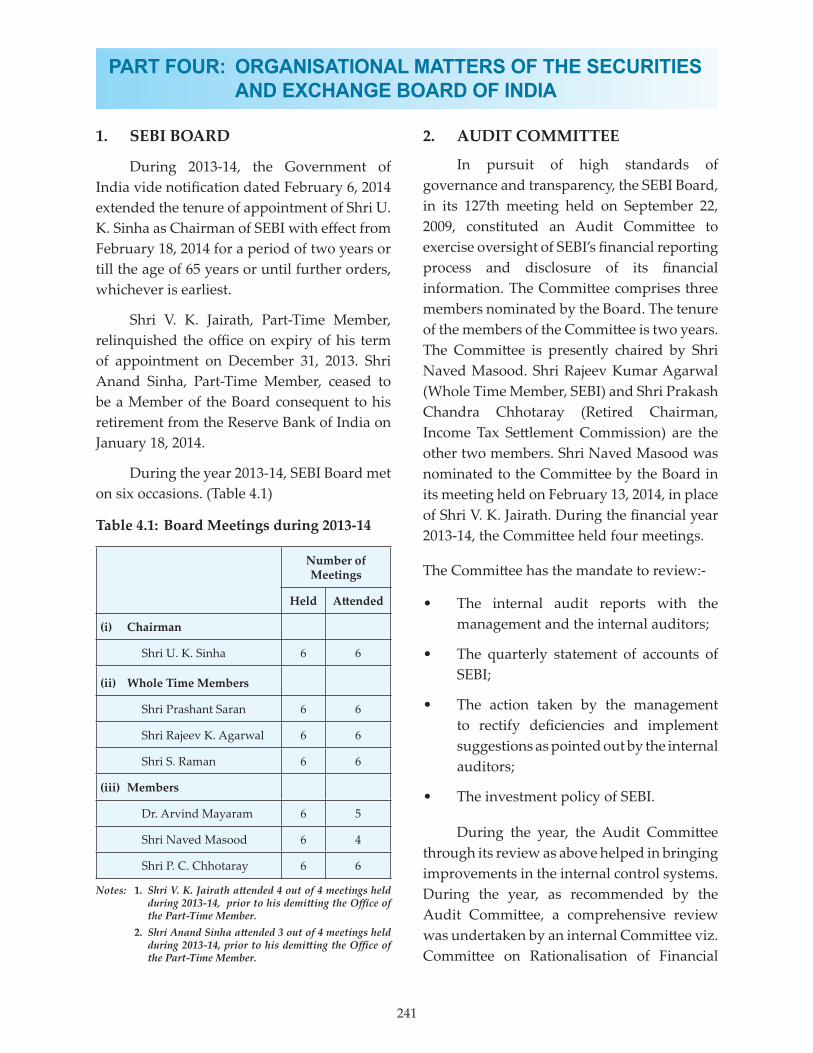

1. SEBI BOARD ................................................................................................................................. 241

2. AUDIT COMMITTEE ................................................................................................................. 241

3. ORGANISATION RESTRUCTURING CELL AND PROJECT MANAGEMENT OFFICE ........................................................................................................................................... 242

4. HUMAN RESOURCES ............................................................................................................... 242

I. Staff Strength, Recruitment, Resignation ........................................................................ 243

II. Benefits ................................................................................................................................. 243

III. Promotions .......................................................................................................................... 243

IV. Strengthening of Regional/Local Offices ........................................................................ 243

CONTENTS

Page No.

v

V. Job Rotation ......................................................................................................................... 243

VI. Disciplinary Matters ........................................................................................................... 243

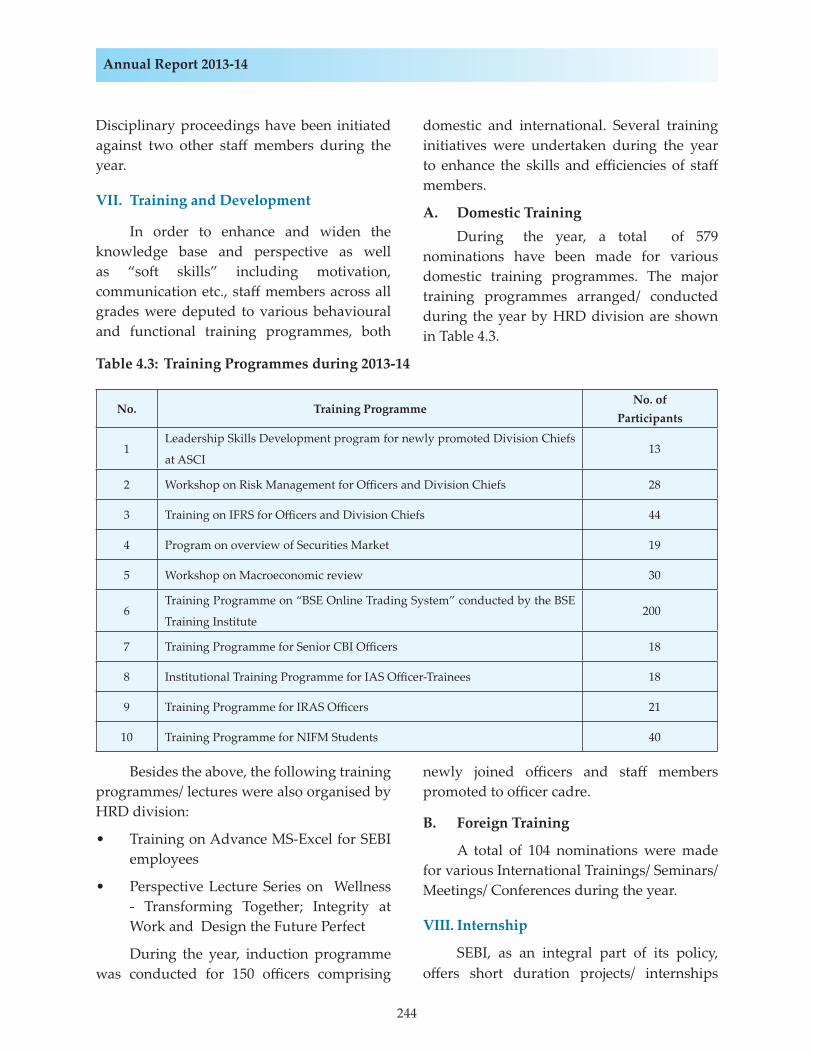

VII. Training and Development ............................................................................................... 244

VIII. Internship............................................................................................................................. 244

IX. Extracurricular activities within SEBI ............................................................................. 245

X. Initiatives in the realm of corporate social responsibility ............................................ 245

XI. Scheme for recognizing and rewarding academic excellence of children of employees ............................................................................................................................ 245

5. PROMOTION OF OFFICIAL LANGUAGE ........................................................................... 245

I. Bilingualisation ................................................................................................................... 245

II. Rajbhasha Competitions .................................................................................................... 245

III. Aaj Ka Shabd ...................................................................................................................... 245

IV. Hindi Noting and Hindi Quotes ..................................................................................... 246

V. Incentive Schemes .............................................................................................................. 246

VI. Hindi Workshops ............................................................................................................... 246

VII. Rajbhasha Meetings and Seminars .................................................................................. 246

VIII. Investor Website and SCORES ........................................................................................ 246

IX. Regional Offices .................................................................................................................. 246

6. LOCAL OFFICES…….…….…….…….…….…….…….…….…….…….…….…................... 246

7. FACILITIES MANAGEMENT…….…….…….…….…….…….…….…….……. .................. 247

8. VIGILANCE CELL…….…….…….…….…….…….…….…….…….…….…….... ................. 247

9. INFORMATION TECHNOLOGY ............................................................................................ 247

I. Implementation of unified communication and up-gradation of SEBI Network ..... 247

II. Disaster Recovery Drill ...................................................................................................... 248

III. Software for Investigation Department ........................................................................... 248

IV. Connectivity to local offices .............................................................................................. 248

V. CIS Complaint System ....................................................................................................... 248

VI. System for managing Resource Persons ......................................................................... 248

VII. Software development for Recovery Division ............................................................... 248

VIII. Implementation of Centralised Biometric Attendance System ................................... 248

CHRONOLOGY OF MAJOR POLICY INITIATIVES BY SEBI ................................................. 249

CONTENTS

Page No.

vi

LIST OF BOXES

Box No. Name Page No.

1.1 Compliance with Minimum Public Shareholding Requirement ...........................................16

1.2 Powers conferred on SEBI vide the Securities Laws (Amendment) Ordinance, 2014 ........19

1.3 Institutional Trading Platform.....................................................................................................21

1.4 Exchange Traded Cash Settled Interest Rate Futures (IRF) on 10 year Government of India Security ...........................................................................................................................................22

1.5 Monetary relief from Investor Protection Fund (IPF) for investors .......................................24

1.6 International Research Conference on HFT, Algo and Co-location .......................................25

1.7 Principles of Financial Market Infrastructures (PFMIs) ..........................................................27

1.8 Third Meeting of the International Advisory Board of SEBI ..................................................35

1.9 Standardization and Simplification of Procedures for Transmission of Securities .............39

1.10 Foreign Portfolio Investor (FPI) Regime ....................................................................................43

2.1 Testing of software used in or related to trading and risk management ..............................86

3.1 Standard Operating Procedure (SOP) for stock exchanges for suspension and revocation of trading of shares of listed entities for non-compliance of certain listing conditions ....122

3.2 Simplification of Registration Requirements for Stock Brokers ...........................................123

3.3 SEBI (Alternative Investment Funds) Regulations, 2012 .......................................................130

3.4 SEBI (Investment Advisers) Regulations, 2013 .......................................................................133

3.5 IOSCO’s Asia-Pacific Regional Committee Meeting, New Delhi .........................................226

3.6 Conference on Investor Protection in Capital Markets .........................................................231

3.7 Asian Roundtable and SEBI-OECD Conference on Corporate Governance in Mumbai - February, 2014 ...........................................................................................................234

vii

LIST OF TABLES

Table No. Name Page No.

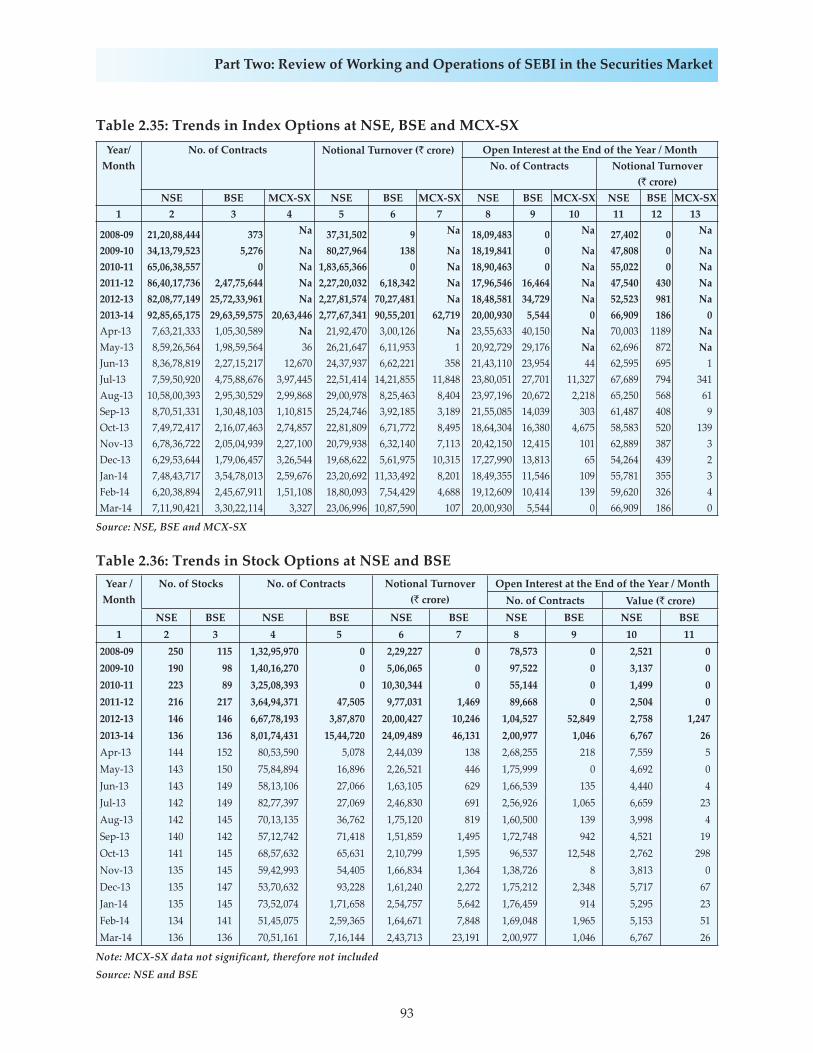

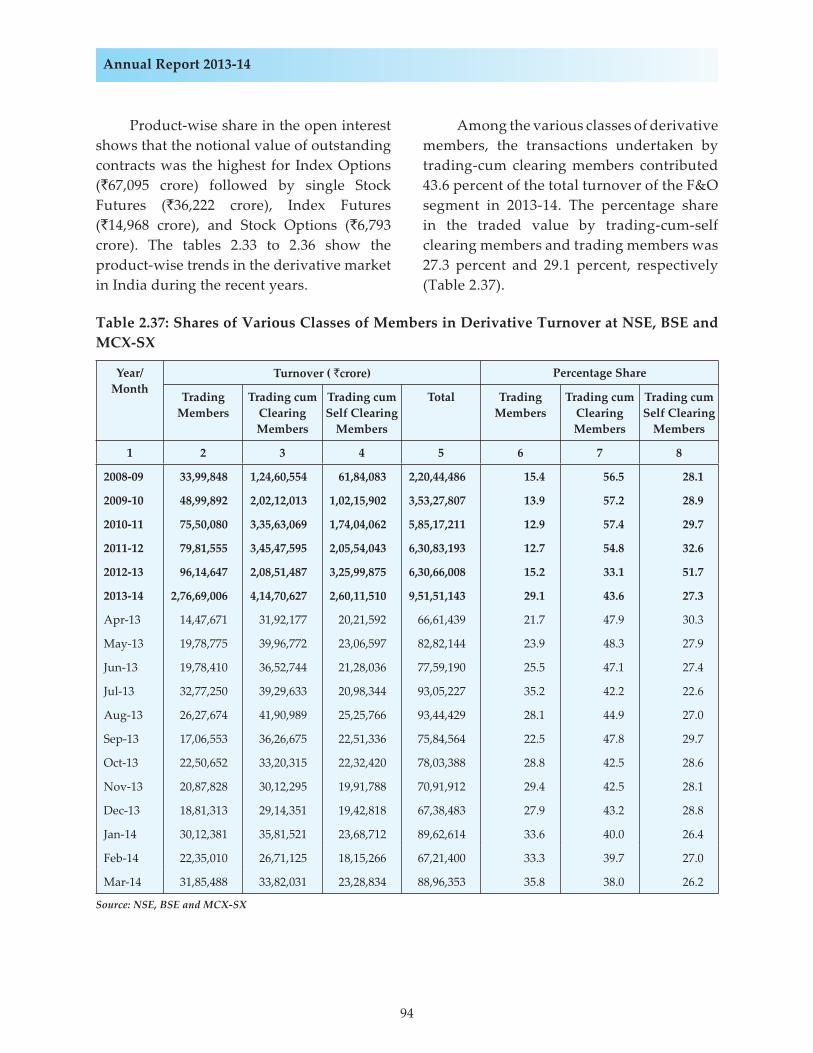

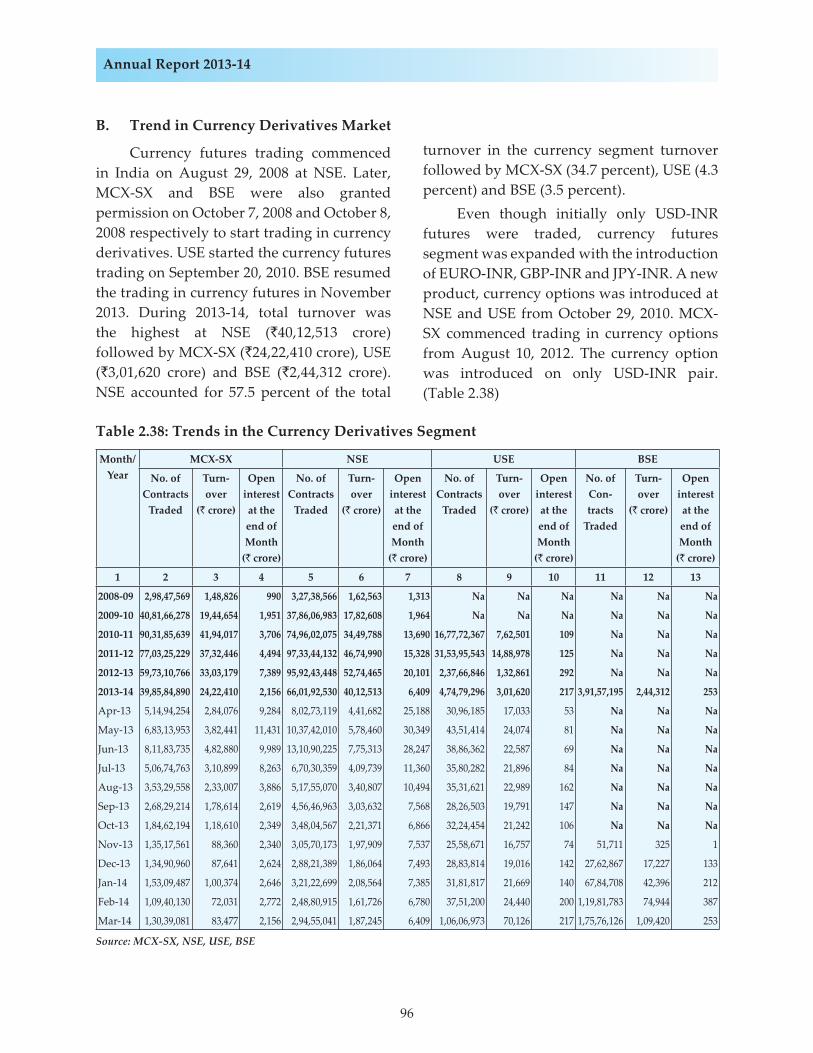

1.1 National Income (at 2004-05 prices) ...................................................................................31.2 GDP (at Factor Cost) by Economic Activity (at 2004-05 prices) .....................................4 1.3 Index of Industrial Production (Base: 2004-05=100) .........................................................4 1.4 Gross Domestic Savings and Investment ..........................................................................7 1.5a Demat Statistics ...................................................................................................................12 1.5b Number of Listed Companies ...........................................................................................12 1.6 Growth of Turnover in Various Segments in Indian Stock Market .............................12 1.7 Value of Assets of Foreign Investors reported by custodians .......................................12 2.1 Resource Mobilisation through Public and Rights Issues .............................................57 2.2 SME Platform .......................................................................................................................58 2.3 Sector-wise Resource Mobilisation ...................................................................................58 2.4 Size-wise Resource Mobilisation ......................................................................................59 2.5 Mega Issues in 2013-14 .......................................................................................................60 2.6 Industry-wise Resource Mobilisation ..............................................................................61 2.7 Resource Mobilisation through QIP and Conforming to MPS through IPP ..............62 2.8 Offer for Sale through Stock Exchange Mechanism to conform to MPS ....................63 2.9 Resource Mobilisation through Preferential Allotment ................................................63 2.10 Private Placement of Corporate Bonds Reported to BSE and NSE..............................64 2.11 Major Indicators of Indian Stock Markets .......................................................................67 2.12 Major Stock Indices and their Percentage Variation ......................................................69 2.13 Sectoral Stock Indices and their Returns .........................................................................70 2.14 Exchange-wise Cash Segment Turnover .........................................................................72 2.15 Turnover at BSE ,NSE and MCX-SX: Cash Segment ......................................................73 2.16 City-wise Turnover of Top 20 Cities in Cash Segment during 2013-14 .......................74 2.17 Market Capitalisation at BSE .............................................................................................75 2.18 Market Capitalisation at NSE ............................................................................................76 2.19 Select Ratios Relating to Stock Market .............................................................................77 2.20 Price to Earnings Ratio .......................................................................................................77 2.21 Price to Book-Value Ratio ...................................................................................................78 2.22 Average Daily Volatility of Benchmark Indices ..............................................................80 2.23 Trends in Daily Volatility of International Stock Market Indices during 2013-14 .....81 2.24 Trading Frequency of Listed Stocks .................................................................................82 2.25 Share of Brokers, Securities and Participants in Cash Market Turnover ....................83 2.26 Trading Statistics of Stock Exchanges in the Cash Segment .........................................84 2.27 Turnover of Subsidiaries of Stock Exchanges .................................................................85 2.28 Depository Statistics ...........................................................................................................87

viii

2.29 Depository Statistics: Debenture/Bonds and Commercial Paper .................................872.30 Cities According to Number of DP Locations: Geographical Spread .........................88 2.31 Trends in Turnover and Open Interest in Equity Derivatives Segment ......................89 2.32 Product-wise Derivatives Turnover at NSE, BSE and MCX-SX ...................................90 2.33 Trends in Index Futures at NSE, BSE and MCX-SX .......................................................91 2.34 Trends in Single Stock Futures at NSE, BSE and MCX-SX ............................................92 2.35 Trends in Index Options at NSE, BSE and MCX-SX ......................................................93 2.36 Trends in Stock Options at NSE and BSE ........................................................................932.37 Shares of Various Classes of Members in Derivatives Turnover at NSE, BSE and MCX-SX ........................................................................................................................942.38 Trends in the Currency Derivatives Segment .................................................................96 2.39 Product-wise Market Share in Currency Derivatives Volume .....................................972.40 Trends in Interest Rate Derivatives at NSE and BSE......................................................98 2.41 Mobilisation of Resources by Mutual Funds ..................................................................99 2.42 Sector-wise Resource Mobilisation by Mutual Funds during 2013-14 ......................100 2.43 Scheme-wise Resource Mobilisation and Assets under Management by Mutual Funds as on March 31, 2014 .............................................................................................1012.44 Number of Schemes by Investment Objective as on March 31, 2014 ........................102 2.45 Trends in Transactions on Stock Exchanges by Mutual Funds ..................................102 2.46 Unit holding pattern of all mutual funds as on March 31, 2014 ................................103 2.47 Unit holding pattern of private and public sector mutual funds as on March 31, 2014 ...................................................................................................................104 2.48 Assets Managed by Portfolio Managers ........................................................................105 2.49 Cumulative amount mobilised by AIFs (as at the end of 31st March 2014) .............105 2.50 Cumulative Net Investments by VCFs and FVCIs .......................................................106 2.51 Category-wise Investors in VCFs ...................................................................................106 2.52 Investment by Foreign Institutional lnvestors ..............................................................107 2.53 Investments by Foreign Institutional lnvestors (Equity & Debt) ...............................108 2.54 QFI Investments during 2013-14 .....................................................................................109 2.55 Allocation of Debt Investment limits to FIIs and Sub-accounts during 2013-14 .....109 2.56 Debt Utilisation Status as on March 31, 2014 ................................................................110 2.57 Notional Value of Open Interest of Foreign Institutional investors in Derivatives during 2013-14 ..............................................................................................1112.58 Notional Value of Participatory Notes (PNs) Vs Assets Under Management of FIIs ..................................................................................................................................1122.59 Secondary Market: Corporate Bond Trades ..................................................................113

LIST OF TABLES

Table No. Name Page No.

ix

2.60 Settlement of Corporate Bonds .......................................................................................114 2.61 Business Growth on the Wholesale Debt Market Segment of NSE and BSE ...........115 2.62 Instrument-wise Share of Securities Traded in Wholesale Debt Market Segment of NSE and BSE .................................................................................................1162.63 Share of Participants in Turnover of Wholesale Debt Market Segment of NSE ......1173.1 Stock Exchanges with Permanent Recognition .............................................................118 3.2 Renewal of Recognition Granted to Stock Exchanges during 2013-14 ......................1193.3 Registered Stock Brokers .................................................................................................124 3.4 Applications under the Process of Registration in Cash Segment .............................125 3.5 Classification of Stock Brokers in Cash Segment on the Basis of Ownership ..........125 3.6 Number of Registered Members in Equity Derivatives Segment ..............................126 3.7 Number of Registered Members in Currency Derivatives Segment .........................126 3.8 Applications under the Process of Registration in Derivative Segment ...................127 3.9 Registered Sub-Brokers ....................................................................................................127 3.10 Registered Intermediaries other than Stock Brokers and Sub-Brokers .....................128 3.11 Process of Registration of other Intermediaries............................................................129 3.12 Number of Registered FIIs, Sub-accounts and Custodians ........................................129 3.13 Status of Registration of FII, Sub-accounts and Custodians during 2013-14 ...........130 3.14 Registered Venture Capital Funds and Alternative Investment Funds ....................130 3.15 Registered Portfolio Managers and Investment Advisers ..........................................133 3.16 Mutual Funds Registered with SEBI ..............................................................................139 3.17 Trends in Awareness Programs/ Workshops Conducted by SEBI .............................151 3.18 Regional Seminars Conducted by SEBI .........................................................................152 3.19 Status of Investor Grievances Received and Redressed ..............................................156 3.20 Failure to Redress Investor Grievances: Adjudication Proceedings ..........................157 3.21 Status of Draft Letter of Offers for Open Offers during 2013-14 ................................165 3.22 Trends of Open Offers ......................................................................................................165 3.23 Buyback cases during 2013-14 .........................................................................................167 3.24 Inspection of Stock Brokers/Sub-brokers .......................................................................169 3.25 Inspections by Stock Exchanges ......................................................................................169 3.26 Inspection of other Market Intermediaries ....................................................................170 3.27 Actions by stock exchanges and depositories for AML/ CFT related deficiencies ..171 3.28 Fees and other Charges ....................................................................................................174 3.29 Major Market Movement during 2013-14 ......................................................................178 3.30 Surveillance Actions during 2013-14 ..............................................................................179 3.31 Trends of Investigations ...................................................................................................180

LIST OF TABLES

Table No. Name Page No.

x

3.32 Category-wise Nature of Investigation ..........................................................................181 3.33 Type of Regulatory actions taken during 2013-14 ........................................................183 3.34 Age-wise Analysis of Enforcement Actions - u/s 11, 11B and 11D of SEBI Act, 1992 ....................................................................................................................185 3.35 Age-wise Analysis of Enforcement Actions - Enquiry Proceedings ..........................186 3.36 Age-wise Analysis of Enforcement Actions - Adjudication Proceedings .................186 3.37 Age-wise Analysis of Enforcement Actions - Prosecution Proceedings ...................187 3.38 Age-wise Analysis of Enforcement Actions Summary Proceedings .........................188 3.39 Enquiry and Adjudication Proceedings Initiated during 2013-14 .............................188 3.40 Enquiry and Adjudication during 2013-14 ....................................................................188 3.41 Pending Enforcement Actions as on March 31, 2014 ...................................................189 3.42 Enquiry and Adjudication Proceedings against other Intermediaries during 2013-14 ................................................................................................................................1893.43 Prosecutions Launched ....................................................................................................191 3.44 Region-wise Data on Prosecution Cases as on March 31, 2014 ..................................191 3.45 Nature of Prosecutions Launched as on March 31, 2014.............................................191 3.46 Number of Prosecution Cases decided by the Courts as on March 31, 2014 ...........192 3.47 Status of Court Cases where SEBI was a Party (Subject Matter) ................................194 3.48 Status of Court Cases where SEBI was a Party (Judicial Forum) ...............................195 3.49 Status of Appeals before the Securities Appellate Tribunal ........................................195 3.50 Disposals of Appeals by Securities Appellate Tribunal ...............................................195 3.51 Status of Appeals before the Hon’ble Supreme Court .................................................196 3.52 Status of Appeals before the Hon’ble High Court .......................................................196 3.53 Receipt and Disposal of applications under Consent and Compounding Process .......211 3.54 Consent Applications filed with SEBI during 2013-14 ................................................212 3.55 Compounding Applications filed by the accused in criminal courts during 2013-14 ................................................................................................................................2123.56 Details of Recovery Proceedings .....................................................................................213 3.57 Trends in RTI applications and First Appeal to SEBI ..................................................223 3.58 Trends in Appeals before Central Information Commission .....................................223 3.59 Parliament Queries Received and replied by SEBI during 2013-14 ...........................223 3.60 Data on Various References Received and Responded to during 2013-14 ...............224 3.61 Trends in Regulatory Assistance made and received by SEBI ...................................235 4.1 Board Meetings during 2013-14 ......................................................................................241 4.2 Promotions of Officers during the year .........................................................................243 4.3 Training Programmes during 2013-14 ...........................................................................244

LIST OF TABLES

Table No. Name Page No.

xi

LIST OF CHARTS

Chart No. Name Page No.

1.1 Share of Components of GDP (at Factor Cost) .................................................................. 5

2.1 Share of Broad Category of Issues in Resource Mobilisation ........................................ 57

2.2 Sector-wise Resource Mobilisation .................................................................................... 59

2.3 Movement of Benchmark Stock Market Indices .............................................................. 65

2.4 Value traded in Secondary Market (percent) ................................................................... 66

2.5 Year-on-Year Returns of International Indices ................................................................. 68

2.6 Movement of Sectoral Indices of BSE ................................................................................ 70

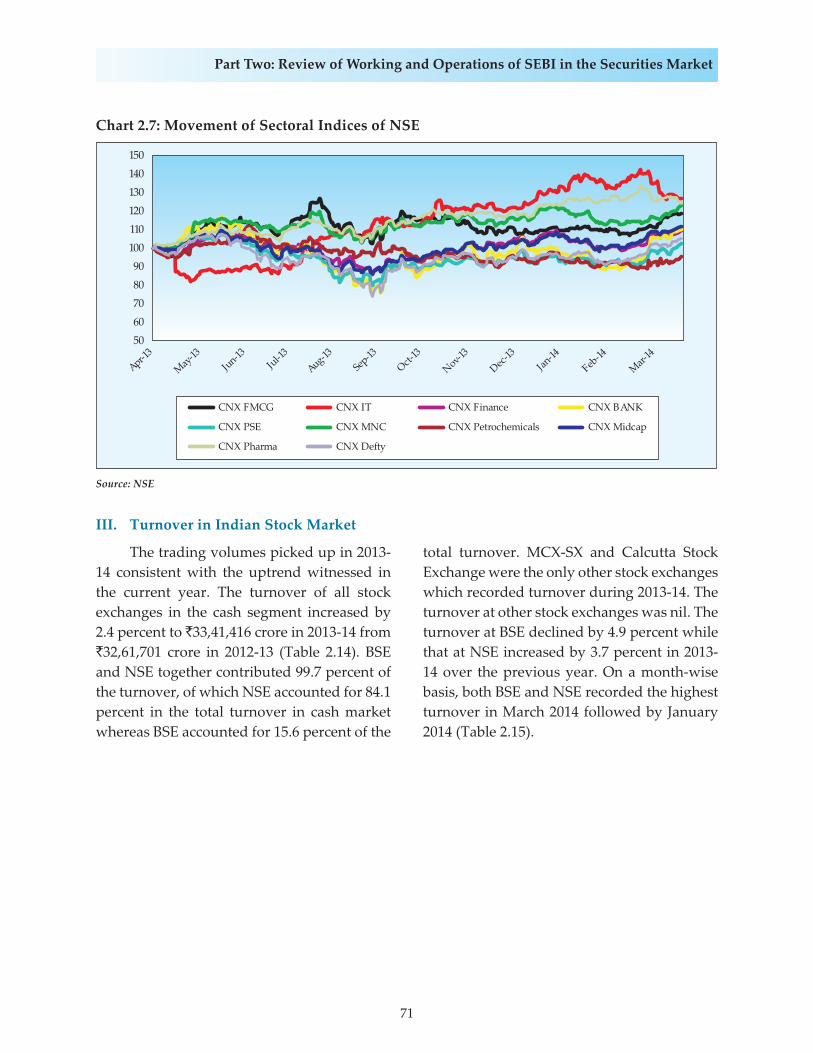

2.7 Movement of Sectoral Indices of NSE ............................................................................... 71

2.8 P/E Ratio of International Stock Market Indices .............................................................. 79

2.9 Annualised Volatility of International Stock Market Indices in 2013-14 ..................... 80

2.10 Derivatives Turnover vis-à-vis Cash Market Turnover .................................................. 89

2.11 Product-wise Share in Equity Derivatives Turnover at NSE and BSE ......................... 91

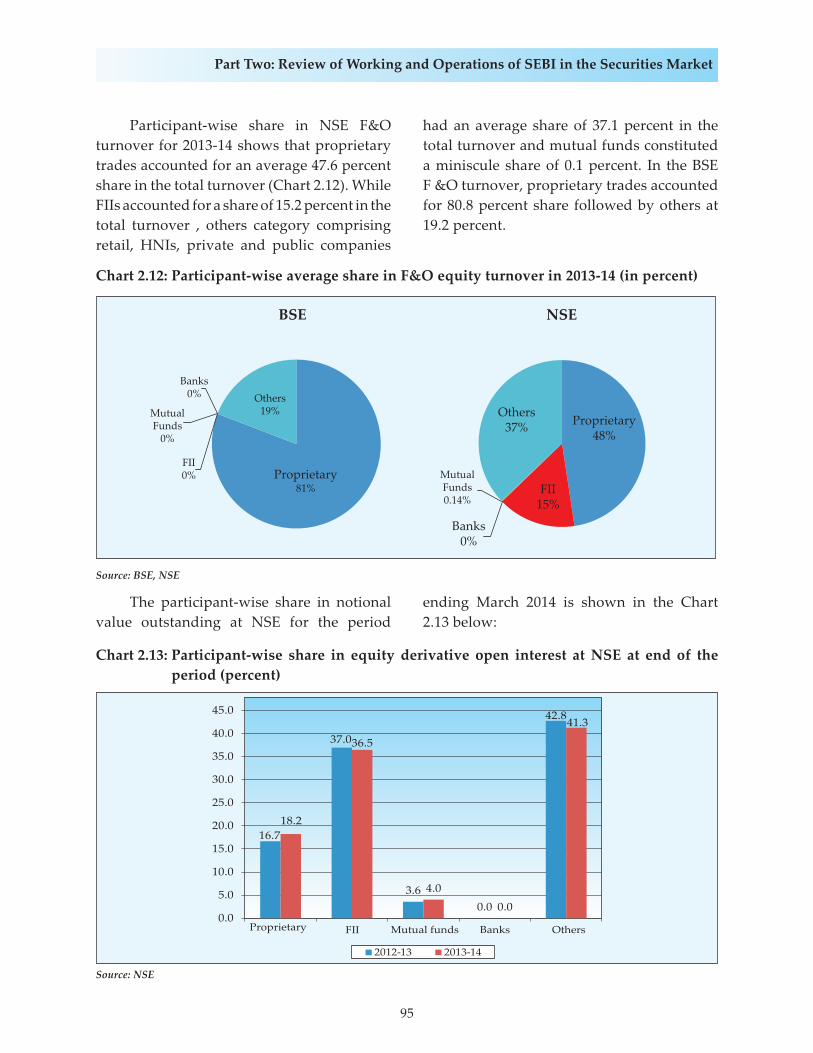

2.12 Participant-wise average share in F&O equity turnover in 2013-14 ............................. 95

2.13 Participant-wise share in equity derivative open interest at NSE at end of

the period .............................................................................................................................. 95

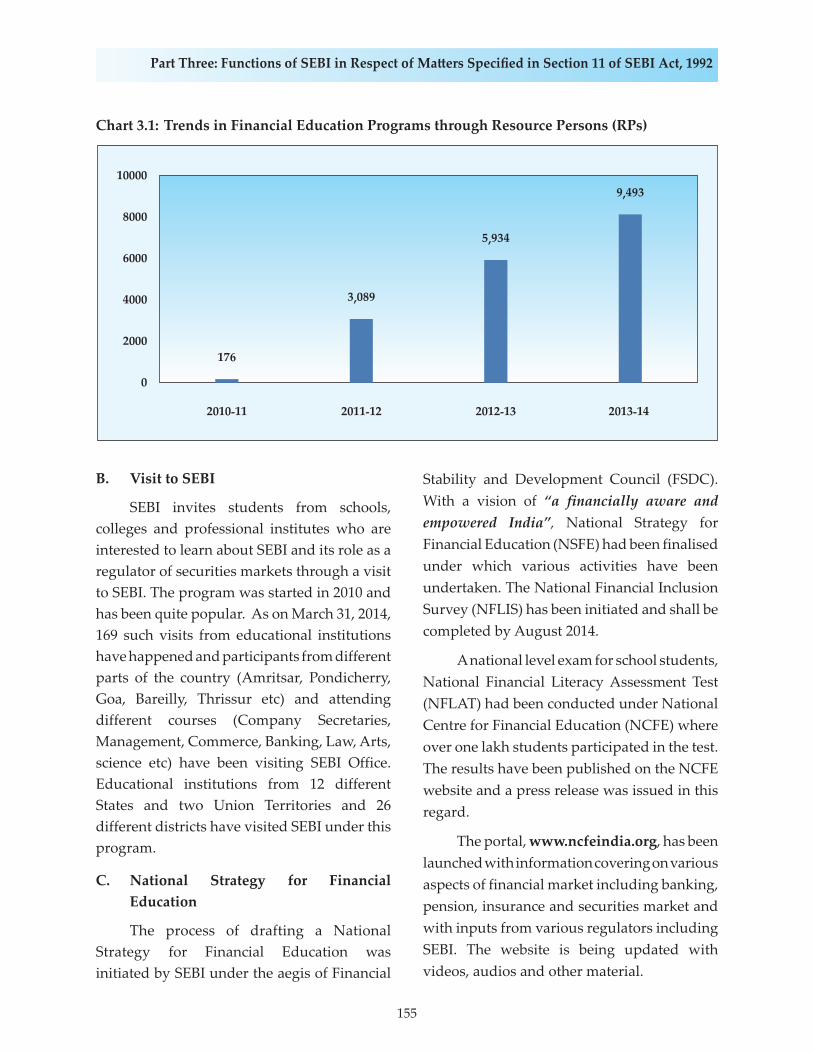

3.1 Trends in Financial Education Programs through Resource Persons ........................ 155

3.2 Trends of feedback for calls received in SEBI Helpline ................................................ 157

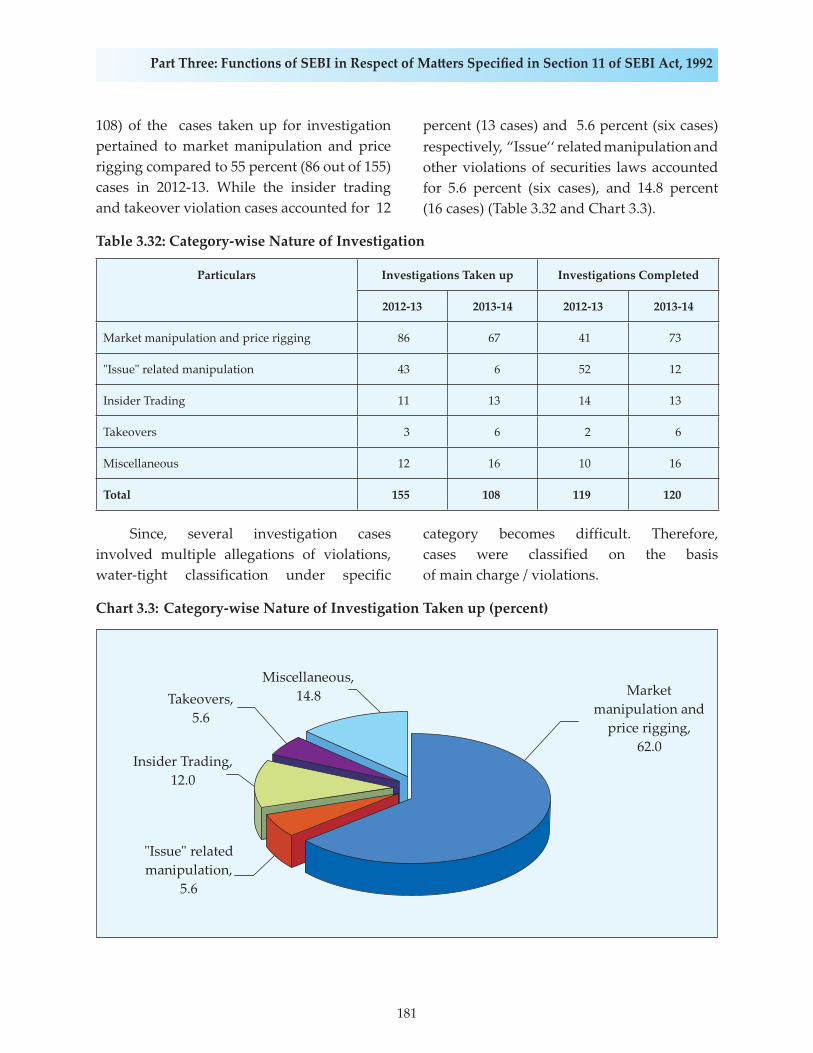

3.3 Category-wise Nature of Investigation Taken up ......................................................... 181

3.4 Category-wise Nature of Investigation Cases Completed ........................................... 182

3.5 Percentage share of type of Regulatory actions taken during 2013-14 ...................... 183

This Report can also be accessed on internet – http://www.sebi.gov.in

Conventions used in this Report` : RupeesLakh : Hundred thousandCrore : Ten millionMillion : Ten lakhBillion : Thousand million/hundred croreNA : Not AvailableNa : Not Applicable p.a. : Per annum

Differences in total are due to rounding off and sometimes they may not exactly add up to hundred per cent.

Source of Charts and Boxes where not mentioned, is SEBI.

xii

AAUM Average Assets Under ManagementADR American Depository ReceiptAGM Assistant General ManagerAIBI Association of Investment Bankers of IndiaAIF(s) Alternative Investment Fund(s)AMC(s) Asset Management Company/CompaniesAMFI Association of Mutual Funds in IndiaAML Anti-Money LaunderingAPs Authorised PersonsASCI Administrative Staff College of IndiaASJ Additional Sessions JudgeATR(s) Action Taken Report(s)AUC Assets Under CustodyAUM Assets Under ManagementBO Beneficial OwnerBSE Bombay Stock ExchangeCAD Current Account DeficitCBDT Central Board of Direct TaxesCBI Central Bureau of InvestigationCBLO Collateralized Borrowing and Lending ObligationCBOE Chicago Board Options ExchangeCBSE Central Board of Secondary EducationCC Clearing CorporationCCI Competition Commission of IndiaCCP Central Counter PartyCD(s) Certificate of Deposit(s)CDS Credit Default SwapsCDSL Central Depository Services (India) LimitedCFA Charted Financial AnalystCFERM Certificate in Financial Engineering and Risk ManagementCFT Countering Financing of TerrorismCGM Chief General ManagerCIC Central Information CommissionCIIA Certificate in International Investment AnalystCIS Collective Investment SchemesCISA Certified Information Systems AuditorCISM Certified Information Security ManagerCISO Chief Information Security OfficerCISSP Certified Information Systems Security Professional

ABBREVIATIONS

xiii

CM Clearing MemberCMB Cash Management BillsCoBoSAC Corporate Bonds and Securitization Advisory CommitteeCP(s) Commercial Paper(s)CPE Continuing Professional EducationCPI Consumer Price IndexCPSS Committee on Payments and Settlement SystemsCRA(s) Credit Rating Agency/AgenciesCRFR Committee on Rationalisation of Financial ResourcesCRR Cash Reserve RatioCSE Calcutta Stock ExchangeCSL Certificate in Securities LawCSO Central Statistical OfficeDC(s) Division Chief(s)DDPs Designated Depository ParticipantsDFIs Development Finance InstitutionsDGM Deputy General ManagerDIP Disclosure and Investor ProtectionDIS Delivery Instruction SlipsDISA Post Qualification Certification in Information Systems AuditDJIA Dow Jones Industrial AverageDLP Data Leakage ProtectionDMA Direct Market AccessDMS Document Management SystemDP(s) Depository Participant(s)DR Disaster RecoveryDRG Development Research GroupDRS Disaster Recovery SiteDSRC Depository System Review CommitteeDT(s) Debenture Trustee(s)DVP Delivery vs. PaymentDWBIS Data Warehousing and Business Intelligence SystemECL Eastern Coalfields LimitedECR Export Credit RefinanceED Executive Director/Enforcement DirectorateEDCE Equity Derivative Certification ExaminationEFD Enforcement DepartmentEGM Extraordinary General MeetingEOB Electronic Order Book

ABBREVIATIONS

xiv

EPFO Employee Provident Fund OrganisationETF Enforcement Task ForceETF(s) Exchange Traded Fund(s)F&O Futures and OptionsFAQ(s) Frequently Asked Question(s)FATF Financial Action Task ForceFCCB(s) Foreign Currency Convertible Bond(s)FCD Fully Convertible DebenturesFDI Foreign Direct InvestmentFEMA Foreign Exchange Management ActFEW Financial Education WebsiteFI(s) Financial Institution(s)FIA Futures Industry AssociationFII(s) Foreign Institutional Investor(s)FIMMDA Fixed Income Money Market and Derivatives Association of IndiaFINRA Financial Industry Regulatory AuthorityFLIS Financial Literacy and Inclusion SurveyFMC Forward Markets CommissionFMI Financial Market InfrastructureFMP(s) Fixed Maturity Plan(s)FPI Foreign Portfolio InvestorFPO(s) Further Public Offering(s)/Follow-on Public OfferFRRB Financial Reporting Review BoardFRTI Financial Regulators Training InitiativeFSAP Financial Sector Assessment ProgrammeFSB Financial Stability BoardFSDC Financial Stability and Development CouncilFSR Financial Stability ReportFSRB FATF-Style Regional BodyFSS Financial Supervisory Service, South KoreaFTIL Financial Technologies (India) LtdFUTP Fraudulent and Unfair Trade PracticesFVCI(s) Foreign Venture Capital Investor(s)FY Financial YearGAAP(s) Generally Accepted Accounting Principle(s)GDCF Gross Domestic Capital FormationGDP Gross Domestic ProductGDR(s) Global Depository Receipt(s)GDS Gross Domestic Savings/Gold Deposit Scheme

ABBREVIATIONS

xv

GETF(s) Gold Exchange Traded Fund(s)GID General Information DocumentGM General ManagerGNI Gross National IncomeGoI Government of IndiaGSE Gauhati Stock ExchangeG-Sec Government SecuritiesHFC(s) Housing Finance Company/CompaniesHFT High Frequency TradingHNIs High Net Worth IndividualsHRD Human Resource DevelopmentHSD High Speed DieselHUF Hindu Undivided FamilyIA Investment AdvisersIAD Investor Awareness DivisionIAFE International Association of Financial EngineersIAIS International Association of Insurance SupervisorsIASB International Accounting Standards BoardIBC India Business CentreIBT Internet Based TradingICAI Institute of Chartered Accountants of IndiaICAI-FRRB Financial Reporting Review Board of the Institute of Chartered Accountants

of IndiaICCL Indian Clearing Corporation LimitedICDR Issue of Capital and Disclosure RequirementsICLS Indian Corporate Law SeviceICSI The Institute of Company Secretaries of IndiaICWAI The Institute of Cost and Work Accountants of IndiaIDF Infrastructure Debt FundIDR(s) Indian Depository Receipt(s)IEFJ International Economics and Finance JournalIFC Infrastructure Finance CompaniesIFRSs International Financial Reporting StandardsIGRC Investor Grievance Redressal CommitteeIIP Index of Industrial ProductionIMD Investment Management DepartmentIMF International Monetary FundIMSS Integrated Market Surveillance SystemINR Indian RupeeIOSCO International Organisation of Securities Commissions

ABBREVIATIONS

xvi

IPC Indian Penal CodeIPEF Investor Protection and Education FundIPF Investor Protection FundIPO Initial Public OfferIPP Institutional Placement ProgrammeIPS Intrusion Detection and Prevention SystemIPV In-Person VerificationIRAS Indian Railway Accounts ServiceIRDA Insurance Regulatory and Development AuthorityIRF Interest Rate FuturesIRM Information Rights ManagementIRS Indian Revenue ServiceISD Integrated Surveillance DepartmentISE Inter-Connected Stock ExchangeISIN International Securities Identification NumberIT Information TechnologyITD Information Technology DepartmentITeS Information Technology Enabled ServicesITF Implementation Task ForceITP Institutional Trading PlatformJF Joint ForumJPY Japanese YenJSE Jaipur Stock ExchangeKIM Key Information MemorandumKRA KYC Registration AgencyKYC Know Your ClientL&T Larsen & ToubroLAF Liquidity Adjustment FacilityLES(s) Liquidity Enhancement Scheme(s)LLP Limited Liability PartnershipLSE Ludhiana Stock ExchangeLTP Last Traded PriceMB(s) Merchant Banker(s)MCA Ministry of Corporate AffairsMCR Monthly Cumulative ReportMCV Multi-class share VehiclesMCX Multi-Commodity Exchange of India LtdMCX-SX MCX Stock ExchangeMCX-SX CCL MCX-SX Clearing Corporation Limited

ABBREVIATIONS

xvii

ABBREVIATIONS

MD Managing DirectorMF(s) Mutual Fund(s)MFAC Advisory Committee on Mutual FundsMII(s) Market Infrastructure Institution(s)MMoU Multilateral Memorandum of UnderstandingMMTC Minerals and Metals Trading Corporation of IndiaMoF Ministry of FinanceMoU Memorandum of UnderstandingMPS Minimum Public ShareholdingMPSE Madhya Pradesh Stock Exchange LimitedMSE Madras Stock ExchangeMSF Marginal Standing FacilityMWPL Market Wide Position LimitNAV Net Asset ValueNBFCs Non-Banking Financial CompaniesNCAER National Council of Applied Economic ResearchNCD Non Convertible DebentureNCFE National Centre for Financial EducationNDP Net Domestic ProductNDUs Non Disposal UndertakingsNFLAT National Financial Literacy Assessment TestNFLIS National Financial Inclusion SurveyNGO Non-Government OrganisationNHB National Housing BankNHPC National Hydroelectric Power CorporationNIFM National Institute of Financial ManagementNII(s) Non-Institutional Investor(s)NISM National Institute of Securities MarketsNNI Net National IncomeNoC No Objection CertificateNRI Non-Resident IndianNRO Northern Regional OfficeNSCCL National Securities Clearing Corporation LimitedNSDL National Securities Depository LimitedNSE National Stock ExchangeNSEL National Spot Exchange LtdNSFE National Strategy for Financial EducationNSMD Network for Securities Markets DataNTPC National Thermal Power Corporation

xviii

ABBREVIATIONS

OCB Overseas Corporate BodyOCRES Online CPE Registration and Enrolment SystemODI(s) Offshore Derivative Instrument(s)OECD Organisation for Economic Co-operation and DevelopmentOFCD(s) Optionally Fully Convertible Debenture(s)OFS Offer for SaleOIAE Office of Investor Assistance and EducationOMOs Open Market OperationsOTC Over the CounterOTCEI Over the Counter Exchange of IndiaP.A. Per AnnumP/B Ratio Price to Book-Value RatioP/E Ratio Price to Earnings RatioPAN Permanent Account NumberPCC Protected Cell CompaniesPCD Partly Convertible DebenturePCI Press Council of IndiaPE Private EquityPF(s) Provident Fund(s)PFI Public Financial InstitutionPFMIs Principles of Financial Market InfrastructuresPFRDA Pension Fund Regulatory and Development AuthorityPFUTP Prohibition of Fraudulent and Unfair Trade PracticesPGCSM Post Graduate Certificate in Securities MarketsPGPSM Post Graduate Programme in Securities MarketsPID Public Interest DirectorsPIS Portfolio Investment SchemePIT Prohibition of Insider TradingPMAC Primary Market Advisory CommitteePMLA Prevention of Money Laundering ActPN Participatory NotesPSE Pune Stock ExchangePSUs Public Sector Undertaking(s)PTM Proprietary Trading MemberQARC Qualified Audit Review CommitteeQDP Qualified Depository ParticipantQE Quantitative EasingQFI(s) Qualified Foreign Investor(s)QIB(s) Qualified Institutional Buyer(s)

xix

QIP(s) Qualified Institutions’ Placement(s)RAIN Registrars Association of IndiaRBI Reserve Bank of IndiaRCG Regional Committee GroupRDDBFI Recovery of Debts due to Banks and Financial InstitutionsRE Revised EstimateREER Real Effective Exchange RateREIT Real Estate Investment TrustRFQ Request for QuoteRGESS Rajiv Gandhi Equity Savings SchemeRHP Red Herring ProspectusRII Retail Individual InvestorsRMRC Risk Management Review CommitteeRP(s) Resource Person(s)RRD Regulatory Research DivisionRSE(s) Regional Stock Exchange(s)RTI Right to InformationRTI/STA(s) Registrar to an Issue and Share Transfer Agent(s)SA(s) Sub Account(s)SAARC South Asian Association for Regional Co-operationSARFAESI Securitization and Reconstruction of Financial Assets and Enforcement of

Security Interest ActSAST Substantial Acquisition of Shares and TakeoversSAT Securities Appellate TribunalSC(R)A Securities Contracts (Regulation) ActSCG School for Corporate GovernanceSCI School for Certification of IntermediariesSCM Self Clearing MemberSCN Show Cause NoticeSCODA SEBI Committee on Disclosures and Accounting StandardsSCORES SEBI Complaints Redress SystemSCRR Securities Contracts (Regulation) RulesSCSB(s) Self Certified Syndicate Bank(s)SDIs Securitised Debt InstrumentsSEBI Securities and Exchange Board of IndiaSEC Securities and Exchange CommissionSECC Stock Exchanges and Clearing CorporationsSGF Settlement Guarantee FundSHA Shareholders’ Agreement

ABBREVIATIONS

xx

SICCE Securities Intermediaries Compliance (Non-Fund) Certification ExaminationSID Scheme Information DocumentSIDD Separately Identifiable Department or DivisionSIEFL School for Investor Education and Financial LiteracySLB Securities Lending and BorrowingSLR Statutory Liquidity RatioSMAC Secondary Market Advisory CommitteeSME Small and Medium EnterprisesSMS Short Message ServicesSOP Standard Operating ProcedureSPV(s) Special Purpose Vehicle(s)SRO(s) Self Regulatory Organisation(s)SRSS School for Regulatory Studies and SupervisionSSE School for Securities EducationSSIR School for Securities Information and ResearchSTT Securities Transaction TaxSTWT Securities Trading using Wireless TechnologySWFs Sovereign Wealth FundsTAC Technical Advisory CommitteeT-Bills Treasury BillsTC Technical CommitteeTER Total Expense RatioTM Trading MemberUAT User Acceptance TestUIDAI Unique Identification Authority of IndiaUIN Unique Identity NumberUK United KingdomUPSE Uttar Pradesh Stock Exchange LimitedUSA United States of AmericaUSD United States DollarUSE United Stock ExchangeUTI Unit Trust of IndiaVaR Value at RiskVCF(s) Venture Capital Fund(s)VPN Virtual Private NetworkWDM Wholesale Debt MarketWFE World Federation of ExchangesWPI Wholesale Price IndexWTM Whole Time Member

ABBREVIATIONS

PART ONE: POLICIES AND PROGRAMMES

The Annual Report of the Securities and Exchange Board of India (SEBI) for 2013-14 reviews significant developments in securities markets in the backdrop of an unprecedented spell of financial turbulence transmitted by the tapering concerns, and the subsequent restoration of normalcy in macro-economic fundamentals. Indian economy and financial markets came under acute stress by the turmoil in the global financial markets generated by the US Federal Reserve announcements on tapering. However with a swift and decisive policy response, India was able to minimise the fallout on the real economy and maintained financial stability.

SEBI Annual Report for 2013-14 articulates the policies and programmes embarked during the financial year while ensuring to fulfill its stated objective to strengthen the Indian regulatory framework of capital markets. This report has been prepared as per the format prescribed by the Securities and Exchange Board of India (Annual Report) Rules, 1994. SEBI continued to pursue its endeavour to achieve the three statutory objectives viz. (a) protection of the interests of investors in securities, (b) promotion of the development of the securities market and (c) regulation of the securities market.

In 2013-14, SEBI continued to channelise its efforts to achieve these objectives by reviewing its policies, implementing fresh initiatives, disciplining the market through a variety of appropriate enforcement actions, facilitating redressal of grievances of investors and nurturing a security culture for the orderly and expansive growth of capital market. The major policy issues are discussed in public domain through discussion papers to ensure transparency, efficiency, fairness, safety and integrity of the capital market. The various

quasi-judicial orders passed by the Board during the year are also posted on the website.

In line with the stated objectives, this Report provides the manner in which SEBI discharged its responsibilities and exercised its powers during the year in furtherance of the objectives enshrined in (a) the Securities and Exchange Board of India Act, 1992, (b) the Securities Contracts (Regulation) Act, 1956 (c) the Depositories Act, 1996 and (d) the relevant provisions of the Companies Act, and newly enacted Companies Act, 2013. It also covers the global developments relevant to the Indian securities market.

1. REVIEW OF THE GENERAL ECONOMIC ENVIRONMENT AND THE INVESTMENT CLIMATE

After the recovery of global economic conditions in late 2012-13, the current financial year unfolded an unprecedented stress to Indian economy and markets. The tightening of global liquidity increased external pressures and heightened the focus on India’s macroeconomic imbalances viz., high inflation, large current account and fiscal deficits and structural weaknesses particularly supply bottlenecks in infrastructure, power and mining. The impact of US Federal Reserve’s May 2013 announcement on Indian financial markets was one of the most severe amongst emerging markets with the rupee depreciation weighing on the stock market, foreign outflows from the debt market further aggravating the forex markets and impacting yields as also the equity market. Thus, the global developments since May 2013 have brought to the fore not just the stress in the financial markets and asset prices, but also their impact on other macroeconomic parameters, including growth, public finances

1

2

Annual Report 2013-14

and inflation, as also financial stability. In the wake of intense exchange rate pressures, stabilisation of the economy by restoring exchange rate stability was the foremost task. A series of exceptional monetary policy actions were taken to tighten interest rates to siphon off liquidity, to restrain the current account deficit (CAD) and to improve its financing. With the resultant improved stability in the foreign exchange market, exceptional liquidity and monetary measures were normalised.

Having built the buffers in the interim, Indian economy and markets withstood the December 2013 tapering announcement better than its emerging market peers. In spite of the recent improvements in statistics, country faces a challenging macro-economic situation with growth slowing down, persistent inflation and lingering structural bottlenecks.

The growth concerns remain dominant for Indian economy with GDP growth recording below 5 percent for seven successive quarters and index of industrial production (IIP) growth stagnating for two successive years. Even though the agriculture output and export performance strengthened, industrial growth continues to stagnate. The leading indicators of the services sector exhibited a mixed picture. During the year, growth picked up in emerging markets, but the momentum appeared to be weaker than

in the advanced economies mainly due to less favourable external environment and country specific concerns like high inflation and wide current account deficit producing weak investor sentiments for emerging markets.

I. Growth

The Indian economy, which witnessed a slowdown after a robust growth of over 8 percent in 2010-11, troughed to a decadal low rate of 4.5 percent in 2012-13 and the provisional estimate stood at a marginal high of 4.7 percent in 2013-14. As per the provisional estimates of Central Statistical Office (CSO), Gross Domestic Product (GDP) at factor cost at constant (2004-05) prices in the year 2013-14 is ̀ 57,41,791 crore, as against the first revised estimate of GDP for the year 2012-13 of `54,82,111 crore (Table 1.1).

In 2013-14, the overall growth is expected to improve on the back of a reviving agriculture sector, with a growth rate of 4.7 percent as compared to 1.4 percent in 2012-13. However, Industry which recorded a growth of 0.9 percent continues to dampen further over the previous year. Service sector continued to maintain its momentum over the previous two years with a growth of 6.2 percent in 2013-14. However, sub-sectors trade, hotels, transport and communication recorded a sluggish growth of 3.0 percent in 2013-14.

3

Part One: Policies and Programmes

II. Agriculture

The post-monsoon rainfall and favourable progress of Rabi crops sown in the current financial year is expected to boost growth prospects in agriculture sector remarkably by 4.7 percent in 2013-14 from that of 1.4 percent seen in 2012-13. The production of food grains is expected to rise by 5.6 percent in 2013-14, unlike the previous year when the production grew at 2.8 percent (Table 1.2). However, unseasonal rains and the possible effects of El Nino in various parts of the country, makes the sector prone to uncertainties for future harvests. In this context, the ability of agriculture sector to

meet increased food demand and mounting input prices poses a challenge.

Although share of agriculture in the GDP accounts for approximately 14 percent since last three years, but it is still the main source of livelihood for majority of the rural population. The agricultural growth had accelerated significantly during 11th five year plan with an average growth rate of 3.7 percent as opposed to the achievement of 2.4 percent in the 10th five year plan. With new structural changes taking place within the sector, the 12th five year plan (2012-17) maintained the growth target for agriculture at 4.0 percent.

Table 1.1: National Income (at 2004-05 prices)(` crore)

Item 2011-12 2012-13 2013-14(2nd Revised

Estimate)( 1st Revised

Estimate)(Provisional

Estimate)1 2 3 4

A. Estimates at Aggregate Level 1. National Product 1.1 Gross National Income (GNI) at factor cost 52,01,163 54,16,659 56,73,857

(6.9) (4.1) (4.7) 1.2 Net National Income (NNI) at factor cost 45,73,328 47,28,776 49,20,183

(6.5) (3.4) (4.0) 2. Domestic Product 2.1 Gross Domestic Product (GDP) at factor cost 52,47,530 54,82,111 57,41,791

(6.7) (4.5) (4.7) 2.2 Net Domestic Product (NDP) at factor cost 4,619,695 47,94,228 49,88,116

(6.2) (3.8) (4.0)B. Estimates at Per Capita Level 1. Population (million) 1,202 1,217 1,233

(1.3) (1.2) (1.3)

2. Per Capita NNI at factor cost (`) 38,048 38,856 39,904(5.1) (2.1) (2.7)

3. Per Capita GDP at factor cost (`) 43,657 45,046 46,568(4.9) (3.2) (3.4)

Notes: 1. Figures in the parentheses are percentage change over the previous year. 2. Growth rates in 2011-12 are based on growth calculated over 3rd revised estimates of 2010-11.Source: Central Statistical Office

4

Annual Report 2013-14

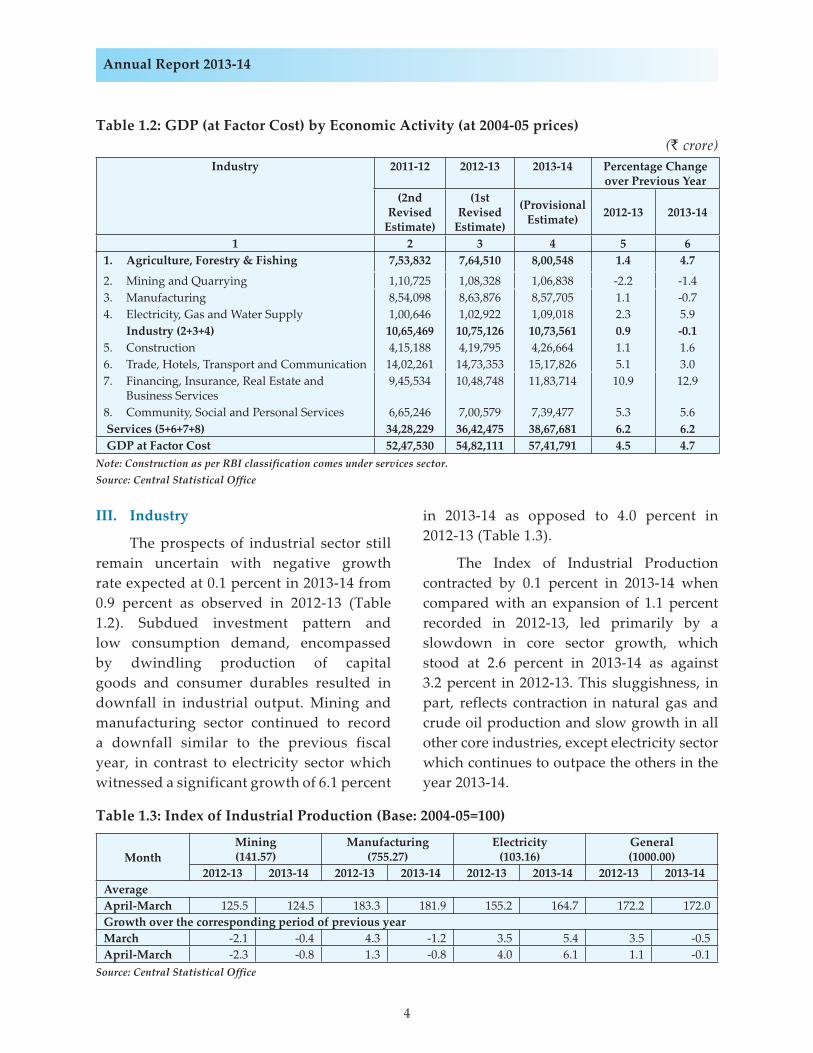

III. Industry

The prospects of industrial sector still remain uncertain with negative growth rate expected at 0.1 percent in 2013-14 from 0.9 percent as observed in 2012-13 (Table 1.2). Subdued investment pattern and low consumption demand, encompassed by dwindling production of capital goods and consumer durables resulted in downfall in industrial output. Mining and manufacturing sector continued to record a downfall similar to the previous fiscal year, in contrast to electricity sector which witnessed a significant growth of 6.1 percent

in 2013-14 as opposed to 4.0 percent in 2012-13 (Table 1.3).

The Index of Industrial Production contracted by 0.1 percent in 2013-14 when compared with an expansion of 1.1 percent recorded in 2012-13, led primarily by a slowdown in core sector growth, which stood at 2.6 percent in 2013-14 as against 3.2 percent in 2012-13. This sluggishness, in part, reflects contraction in natural gas and crude oil production and slow growth in all other core industries, except electricity sector which continues to outpace the others in the year 2013-14.

Table 1.2: GDP (at Factor Cost) by Economic Activity (at 2004-05 prices)(` crore)

Industry 2011-12 2012-13 2013-14 Percentage Change over Previous Year

(2nd Revised

Estimate)

(1st Revised

Estimate)

(Provisional Estimate) 2012-13 2013-14

1 2 3 4 5 61. Agriculture, Forestry & Fishing 7,53,832 7,64,510 8,00,548 1.4 4.7

2. Mining and Quarrying 1,10,725 1,08,328 1,06,838 -2.2 -1.43. Manufacturing 8,54,098 8,63,876 8,57,705 1.1 -0.74. Electricity, Gas and Water Supply 1,00,646 1,02,922 1,09,018 2.3 5.9 Industry (2+3+4) 10,65,469 10,75,126 10,73,561 0.9 -0.15. Construction 4,15,188 4,19,795 4,26,664 1.1 1.66. Trade, Hotels, Transport and Communication 14,02,261 14,73,353 15,17,826 5.1 3.07. Financing, Insurance, Real Estate and

Business Services9,45,534 10,48,748 11,83,714 10.9 12.9

8. Community, Social and Personal Services 6,65,246 7,00,579 7,39,477 5.3 5.6 Services (5+6+7+8) 34,28,229 36,42,475 38,67,681 6.2 6.2 GDP at Factor Cost 52,47,530 54,82,111 57,41,791 4.5 4.7

Note: Construction as per RBI classification comes under services sector.Source: Central Statistical Office

Table 1.3: Index of Industrial Production (Base: 2004-05=100)

MonthMining(141.57)

Manufacturing(755.27)

Electricity(103.16)

General(1000.00)

2012-13 2013-14 2012-13 2013-14 2012-13 2013-14 2012-13 2013-14AverageApril-March 125.5 124.5 183.3 181.9 155.2 164.7 172.2 172.0Growth over the corresponding period of previous yearMarch -2.1 -0.4 4.3 -1.2 3.5 5.4 3.5 -0.5April-March -2.3 -0.8 1.3 -0.8 4.0 6.1 1.1 -0.1

Source: Central Statistical Office

5

Part One: Policies and Programmes

Mining sector, partly accountable for the overall contraction in industrial output, recorded a decline of 0.8 percent in 2013-14 as against a decline of 2.3 percent in 2012-13. The sector with 14.1 percent weight in IIP continues to exhibit weak activity as compared to other sectors of the IIP on account of regulatory and environmental concerns (Table 1.3).

Manufacturing sector, which accounts for a significant 75.5 percent weight in IIP, witnessed 0.8 percent contraction in the output in the current year as compared to 1.3 percent growth in 2012-13, highlighting the weak domestic growth impulses. In 2013-14, the number of sub-sectors of the manufacturing sector displaying contraction rose to 10 out of 22, including industries like radio, TV and communication equipment, rubber and plastics, fabricated metal products and motor vehicles. In terms of Use-based classification, pace of growth of intermediate goods output rose to 3.0 percent in 2013-14 from 1.6 percent in

2012-13. The contraction recorded in production of capital goods, a barometer of demand, eased to 3.7 percent 2013-14, from 6.0 percent in the previous financial year. In order to capture a better share in GDP, it is indispensable to increase manufacturing sector growth to 12-14 percent over the years amidst global competitiveness and sustainable environment, as perceived in the National Manufacturing Policy.

The growth of electricity generation improved to a robust 11.5 percent in February 2014 as compared to previous months of the fiscal, led primarily by a pickup in growth of thermal as well as hydro electricity generation. On the whole, the sector posted an improved growth of 6.1 percent in 2013-14 as compared to 4.0 percent growth in 2012-13, continuing to outpace the other two sectors in the current financial year. However, the availability of electricity supply still remains an area of concern, particularly in rural areas where the per capita consumption of electricity is mere 8 units per month.

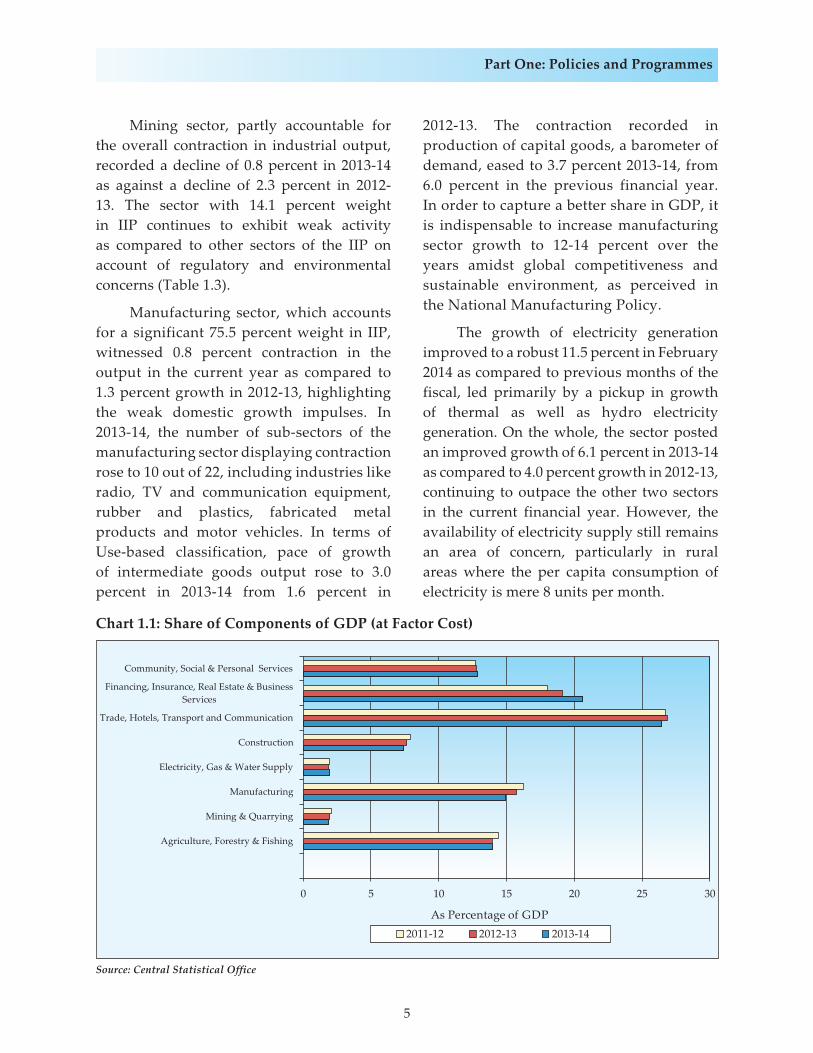

Chart 1.1: Share of Components of GDP (at Factor Cost)

Source: Central Statistical Office

6

Annual Report 2013-14

IV. Services

Services sector has been a major contributor to India’s GDP and growth with a rising share of 67.3 percent in the GDP in 2013-14 as against 66.4 percent in 2012-13. The sector, however, is expected to grow at 6.2 percent in 2013-14, similar to growth observed in 2012-13 but much higher than the other two sectors of the economy.

The sector with high growth potential was largely hampered due to a tad increase of 3.0 percent observed in ‘Trade, Hotels, Transport and Communication’ sub -sector, as compared to 5.1 percent recorded in 2012-13. Weak consumer confidence has impacted the sale of passenger cars, commercial vehicles and three wheelers. Nonetheless, the reduction in excise duty on passenger vehicles and two wheelers, as announced in the interim budget for 2014-15, is expected to augur well for the sector.

‘Financing, Insurance, Real Estate and Business Services’ sub-sector has further increased its share in GDP from 19.1 percent in 2012-13 to 20.3 percent in the current year. The sub-sector continues to outperform the other three sub-sectors while recording a growth rate of 12.9 percent in 2013-14 as compared to 10.9 percent observed in 2012-13. Construction sub sector, with 7.4 percent weight in GDP, is expected to grow at 1.6 percent in 2013-14 as against 1.1 percent recorded in the previous financial year.

‘Community, Social and Personal Services’ sub-sector, which contributes 13.1 percent share in GDP, is estimated to grow at 5.6 percent in the current year, slightly higher than the growth rate of 5.3 percent achieved in 2012-13. India’s services sector has emerged as a prominent sector over a decade in terms of its contribution to national and states incomes, FDI inflows and employment.

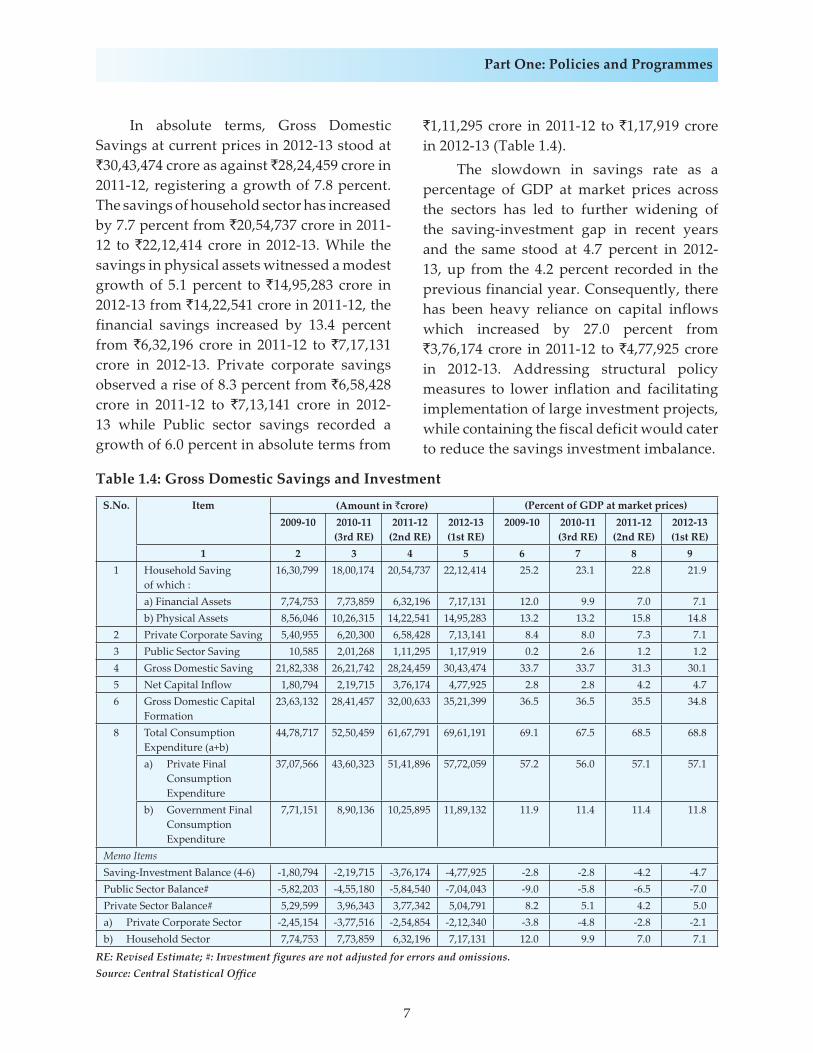

V. Savings and Investments

As per the update of Central Statistical Office (CSO), India’s Gross Domestic Savings as a percentage of GDP at market prices is reflecting a downward trend since 2009-10, sliding further to 30.1 percent in 2012-13 from 31.3 percent in 2011-12. The decrease came primarily on the back of reduced Private corporate savings from 7.3 percent in 2011-12 to 7.1 percent in 2012-13 accompanied by Household savings in physical assets moving from 15.8 percent in 2011-12 to 14.8 percent in 2012-13, which may be attributed to inflationary pressures experienced by the economy for most of the year. The mobilisation of financial savings impacted by low deposit rates in the face of high inflation saw a modest increase of 7.1 percent (as a percentage of GDP at market prices) in 2012-13 from 7.0 percent in 2011-12, while Public sector savings as a percentage of GDP at market prices stood at 1.2 percent in 2012-13 as well as in 2011-12. The investment too has seen a dwindling trend, declining to 34.8 percent in 2012-13 from 35.5 percent in 2011-12 and the peak of 36.5 percent recorded in 2009-10 and 2010-11.

The expenditure side of GDP at market prices indicates that the aggregate demand of the Indian economy during the year continued to remain weak even as net exports remained strong. Private final consumption expenditure, a principal component of GDP at market prices, decelerated from 17.9 percent in 2011-12 to 12.3 percent in 2012-13 in absolute terms on account of low agricultural production and insistent high consumer price inflation. On the contrary, the growth rate of government final consumption expenditure increased marginally from 15.3 percent in 2011-12 to 15.9 percent in 2012-13 due to fiscal consolidation.

7

Part One: Policies and Programmes

In absolute terms, Gross Domestic Savings at current prices in 2012-13 stood at `30,43,474 crore as against `28,24,459 crore in 2011-12, registering a growth of 7.8 percent. The savings of household sector has increased by 7.7 percent from `20,54,737 crore in 2011-12 to `22,12,414 crore in 2012-13. While the savings in physical assets witnessed a modest growth of 5.1 percent to `14,95,283 crore in 2012-13 from `14,22,541 crore in 2011-12, the financial savings increased by 13.4 percent from `6,32,196 crore in 2011-12 to `7,17,131 crore in 2012-13. Private corporate savings observed a rise of 8.3 percent from `6,58,428 crore in 2011-12 to `7,13,141 crore in 2012-13 while Public sector savings recorded a growth of 6.0 percent in absolute terms from

`1,11,295 crore in 2011-12 to `1,17,919 crore in 2012-13 (Table 1.4). The slowdown in savings rate as a percentage of GDP at market prices across the sectors has led to further widening of the saving-investment gap in recent years and the same stood at 4.7 percent in 2012-13, up from the 4.2 percent recorded in the previous financial year. Consequently, there has been heavy reliance on capital inflows which increased by 27.0 percent from `3,76,174 crore in 2011-12 to `4,77,925 crore in 2012-13. Addressing structural policy measures to lower inflation and facilitating implementation of large investment projects, while containing the fiscal deficit would cater to reduce the savings investment imbalance.

Table 1.4: Gross Domestic Savings and Investment

S.No. Item (Amount in `crore) (Percent of GDP at market prices)2009-10 2010-11

(3rd RE)2011-12

(2nd RE)2012-13 (1st RE)

2009-10 2010-11(3rd RE)

2011-12 (2nd RE)

2012-13 (1st RE)

1 2 3 4 5 6 7 8 91 Household Saving

of which :16,30,799 18,00,174 20,54,737 22,12,414 25.2 23.1 22.8 21.9

a) Financial Assets 7,74,753 7,73,859 6,32,196 7,17,131 12.0 9.9 7.0 7.1b) Physical Assets 8,56,046 10,26,315 14,22,541 14,95,283 13.2 13.2 15.8 14.8

2 Private Corporate Saving 5,40,955 6,20,300 6,58,428 7,13,141 8.4 8.0 7.3 7.13 Public Sector Saving 10,585 2,01,268 1,11,295 1,17,919 0.2 2.6 1.2 1.24 Gross Domestic Saving 21,82,338 26,21,742 28,24,459 30,43,474 33.7 33.7 31.3 30.15 Net Capital Inflow 1,80,794 2,19,715 3,76,174 4,77,925 2.8 2.8 4.2 4.76 Gross Domestic Capital

Formation23,63,132 28,41,457 32,00,633 35,21,399 36.5 36.5 35.5 34.8

8 Total Consumption Expenditure (a+b)

44,78,717 52,50,459 61,67,791 69,61,191 69.1 67.5 68.5 68.8

a) Private Final Consumption Expenditure

37,07,566 43,60,323 51,41,896 57,72,059 57.2 56.0 57.1 57.1

b) Government Final Consumption Expenditure

7,71,151 8,90,136 10,25,895 11,89,132 11.9 11.4 11.4 11.8

Memo ItemsSaving-Investment Balance (4-6) -1,80,794 -2,19,715 -3,76,174 -4,77,925 -2.8 -2.8 -4.2 -4.7Public Sector Balance# -5,82,203 -4,55,180 -5,84,540 -7,04,043 -9.0 -5.8 -6.5 -7.0Private Sector Balance# 5,29,599 3,96,343 3,77,342 5,04,791 8.2 5.1 4.2 5.0a) Private Corporate Sector -2,45,154 -3,77,516 -2,54,854 -2,12,340 -3.8 -4.8 -2.8 -2.1b) Household Sector 7,74,753 7,73,859 6,32,196 7,17,131 12.0 9.9 7.0 7.1

RE: Revised Estimate; #: Investment figures are not adjusted for errors and omissions.Source: Central Statistical Office

8

Annual Report 2013-14

VI. Current Account Deficit

The year 2013-14 for Indian economy reflected concerns with the current account deficit and it’s financing in the early months. However, circumstances improved and external risk mitigated in second half of the year. The narrowing of CAD followed a lower trade deficit due to the higher exports helped by a depreciating rupee as well as moderation in imports, by curbing the import demand arising from gold and other non-essential imports through tariff hikes and administrative measures and to boost capital flows through liberalisation and special schemes.

India’s Current Account Deficit (CAD) was USD 32.4 billion in 2013-14 (1.7 percent of GDP), much lower than USD 87.8 billion (4.7 percent of GDP) recorded in 2012-13 on account of narrowing trade deficit and rising net invisibles receipts. In Q4 of 2013-14, CAD stood at USD 1.2 billion (0.2 percent of GDP) compared to USD 4.2 billion (0.9 percent of GDP) during Q3 of 2013-14, which is much lower than USD 31.9 billion, a historic high of 6.5 percent of GDP, during Q3 of 2012-13. There has been a significant deceleration in valuables with curbs on gold imports and this is expected to positively impact household financial savings and help restrain CAD.

In Indian context, sustaining CAD to a comfortable level is not only desired but indispensable too as it would reduce economy’s dependence on volatile foreign capital inflows such as portfolio investments to fund current account deficit. This leads to a balanced situation funded through foreign direct investment that is highly stable.

In addition to containing the current account deficit, efforts have also been made to make the Indian economy more resilient by building buffers. Foreign exchange reserves

have been replenished by mobilising USD 34 billion by way of non-resident Indian (NRI) deposits and bank borrowings in the international market. India’s foreign exchange reserves, which stood at USD 303.7 billion as on March 28, 2014, are comfortable in terms of various reserve adequacy criteria. While India may still be vulnerable to debt outflows on account of disorderly exit from quantitative easing by major central banks, this risk has been mitigated due to the containment of the current account deficit, reduction in the stock of the volatile component of capital flows, and an increase in foreign exchange reserves.

VII. Fiscal Deficit

As the elevated fiscal deficit posed a major challenge to the economy, several measures for fiscal consolidation were adopted such as phased reduction of diesel subsidies. The fiscal performance in 2012-13 was better as the actual gross fiscal deficit declined to 4.9 percent of GDP in 2012-13 as against the budgeted level of 5.1 percent. For 2013-14, gross fiscal deficit stood at 4.5 percent of GDP. It has been budgeted at a further reduced level of 4.1 percent for 2014-15.

VIII. Liquidity

After tighter liquidity conditions observed in 2012-13, the Q1 of 2013-14 witnessed considerably improved scenario with liquidity deficit staying within the comfort zone together with a decline in deposit rate of SCBs, following a reduction in the repo rate. However, to restore stability in the foreign exchange market grounded by capital outflows subsequent to the announcement of tapering of US quantitative easing programme, exceptional liquidity measures were undertaken to tighten the

9

Part One: Policies and Programmes

monetary and liquidity conditions. Hike in Marginal Standing Facility (MSF) rate and Cash Reserve Ratio (CRR) requirement, cap on daily Liquidity Adjustment Facility (LAF) borrowing and weekly auctions of cash management bills (CMBs) were some of the measures carried to drain out liquidity from the economy.

Moderation of exchange rate pressures from September 2013 onwards and evolving macroeconomic situations significantly eased the tight liquidity conditions of Q2 witnessing ongoing normalisation in exceptional monetary measures. However, liquidity conditions altered during the last quarter of 2013-14 as it started with monetary tightening in the first half of February 2014 owing to frictional pressures primarily on account of government cash balances and a rise in currency in circulation. The situation was eased later due to injection of additional liquidity through term repos and forex swaps.