Embed Size (px)

Citation preview

Addamjeee Insurance Comppany L

St

imited

rugglin

d (AICL

g to gea

Friday, J

L)

ar mom

July 04, 2014

AHCML

mentum

4

L

m

Friday, July 04, 2014

AHCML

AICL: Upgrading to BUY with Price Objective of PKR 63.25

We have upgraded our stance to BUY from HOLD with changed PO from PKR46.00 to PKR63.25, up 37pc, for Adamjee Insurance Company Limited.

Analysis

Adamjee Insurance continues to witness stagnation in its underwriting business despite the fact the industry depicted a growth of 16% (CAGR) during the last decade or so. Despite that the company was able to retain its position in terms of market share, AICL currently ranked 2nd after EFU General Insurance.

Non‐life Insurance industry is comprised of 39 insurance companies (22 listed and 14 non‐listed) and 3 General Takaful operators (non‐listed). The 3 large insurers (EFU General, Adamjee Insurance and Jubilee Insurance) had a combined total market share of 50% in 2013 while the remaining 50% is distributed among the remaining 35 insurers.

Fire and Property Damage (FPD) segment remains the major business segment for the company, however more than 80% of the FPD business is being passed on to the reinsurers in this segment. Motor insurance remains the second biggest segment where the net retention is approximately 90% in this segment.

Furthermore, the market value of the company’s invested portfolio contributes significantly to its Fair‐value, and much of the value of invested portfolio is derived from the investments in associates (Nishat Group, mainly MCB Bank).

Therefore, we foresee higher dividend income from associates and higher capital gains emanating from the company’s invested portfolio may remain the price source of profitability for the company in the long run. AICL offers Potential upside of 33% at current price; which requires us to assign a ‘BUY’ rating for the stock.

AICL: Company Profile

Adamjee Insurance Company Limited (AICL) was incorporated as a Public Limited Company on September 28, 1960 and is listed on all three stock exchange of Pakistan. The Company is involved in the business of general insurance. The head office is located in Karachi and it operates a network of branches all across Pakistan and two in UAE.

The Company commenced operations with a paid‐up capital of Rupees 2.5 million, which has grown phenomenally in the past five decades to Rupees 3.5 billion, as on 31 December 2013. A strong asset base, significant paid‐up capital, substantial reserves, balanced portfolio mix along with steady growth in gross premium account gives Adamjee Insurance a well deserved competitive edge within the insurance industry. The company is broadly involved in underwriting the following classes of

Brief Snapshot

KATS Code AICL

Bloomberg Code AICL:PA

Reuters Code ADIN.KA

Sector Non Life

Insurance Paid‐up Capital (PKR mn) 3,500.00

O/S shares (mn) 350.00

Free Float % 70%

Mkt. Cap. (PKR bn) 16.65

Mkt. Cap. (US$ bn) 0.17

Volume mn (Jul 03'14) 0.43

Price (Jul 03'14) 47.58

Target Price 63.25

Potential Upside 33%

Recommendation BUY

3M 6M 12M

Avg. Rate 47.69 44.79 61.38

High 52.90 52.90 108.99

Low 42.50 36.85 36.36

Avg. Vol. (mn) 2.21 3.45 2.34

Rel. % ‐1.67% 24.75% ‐40.84%

Friday, July 04, 2014

AHCML

businesses:

Fire and Property Engineering Health Marine Motor Miscellaneous business

AICL acquiring 5.4pc stake in Security General Insurance Company

Adamjee Insurance intends to acquire 3.6 million ordinary shares of Rs10 each of SGIC, at a maximum price of PKR95 per share, however the book value per share of the company, as per the latest annual accounts, stands at PKR 116.00. Additionally the market value of company’s investment portfolio stands at PKR 15,728mn translating into a per share value of PKR 231.10 as on July 3, 2014.

The deal bodes favourably for the AICL; however, it may be assumed that such an acquisition may not be purely from the core business point of view but more related to strategic cross holdings as both the companies are part of the Nishat Group.

Valuation

We have arrived at a SOP based value of PKR63.25per share; which includes DCF based fair value of its core operations (insurance business) of PKR14.38 and a portfolio value of PKR48.87. Furthermore, we have applied a 25pc discount on the market price of quoted equity investments (excluding companies under coverage‐for which we have used our model based fair values) and investments in Government securities and in unquoted companies (associates) have been taken at carrying value in the balance sheet thereby arriving at the appropriate value of company’s invested portfolio.

Assumptions

We have used WACC (21.25%) for discounting the cash flows of the company. We have assumed that 50% of the Gross Written to be recorded as Premiums Earned in the current year and the remainder in following year. Loss & Loss Adjustment Expense (LAE) Ratio is assumed at 70% while the Loss Paid in Cash assumed at 95% of the Loss Expense. Reinsurance share have been assumed at 40% of the Gross Written Premium.

“A DCF based fair value of its core operations (insurance business) of PKR14 and a portfolio value of PKR49”

“Applying a 25% discount on the market price of quoted equity investments in the portfolio”

“MCB, HUBC, NML, UBL, NBP, FFBL, FFC, OGDC, POL, PPL & DGKC are taken on our model based fair values”

“Loss & Loss Adjustment Expense (LAE) Ratio is assumed at 70% while the Loss Paid in Cash assumed at 95% of the Loss Expense”

Friday, July 04, 2014

AHCML

IGI Insurance Company ‐ Discounted Cash Flow Statement

2014E 2015F 2016F 2017F 2018F

Underwriting Income: 16,413 2,005 2,066 2,128 2,192

Tax on Underwriting Income: ‐5,744 ‐702 ‐723 ‐745 ‐767

Cash Flow from Underwriting Activities 388,974 397,602 409,610 421,980 434,724

Cash Flow from Operations 501,296 407,375 438,039 449,091 462,443

Capex: ‐32,487 ‐141,884 ‐146,041 ‐150,329 ‐154,753

Cash Flow from Investing: ‐32,487 ‐141,884 ‐146,041 ‐150,329 ‐154,753

Total Free Cash Flow: 468,810 265,491 291,998 298,762 307,690

WACC: 21.25% 21.25% 21.25% 21.25% 21.25%

PV of after tax Cash Flows 426,215 199,072 180,484 152,585 129,368

Terminal Growth Rate 4%

Terminal Value 777,624

ENTERPRISE VALUE 1,865,347

Deduct: Net Debt ‐3,163,786

INTRINSIC VALUE 5,029,133

Per Share Value 14.38

Portfolio Value 48.87

Sum of the Parts Value 63.25

AHCML estimates

Friday, July 04, 2014

AHCML

Industry overview: Non‐life Insurance

Non‐life Insurance industry is comprised of 39 insurance companies (22 listed and 14 non‐listed) and 3 General Takaful operators (non‐listed). Gross Written Premium (GWP) stands at PKR 61.89bn during the FY13 for both Insurance and Takaful companies (Insurance 59.86bn, Takaful 2.02bn). Since 2000, the number of non‐life insurers in Pakistan has not been increasing and in fact nearly 24 non‐life insurers have exited the market by 2009, either voluntarily or due to regulatory actions owing to severe non‐compliances (industry sources). According to the Herfindahl–Hirschman Index, given the small size of the market, the existence of 39 non‐life insurers as of 2013, appears to be inefficient. The public insurance company, NICL, has 10.5% of the market share, which has been relatively stable for the past 5 years. Private insurers control the remaining 89.5% of the market. Of these private insurers, the 3 large insurers (EFU General, Adamjee Insurance and Jubilee Insurance) have a combined total market share of 50% in 2013. This share, for the top three has remained, on an average, over 50% in the last 5 years. The other 50% of private market share is distributed among the other 35 active non‐life private insurers. Consequently, the non‐life insurance sector is considered quite over‐competitive with certain aggressive pricing techniques and low profit margins.

Insurance Sector (2013) Gross Premium

(PKR: mn) Insurance Penetration

InsuranceDensity PKR

InsuranceDensity US$

Life Insurance Sector 107,340 0.41% 570.96 5.73

(excluding family Takaful)

Non‐Life Insurance Sector 59,863 0.23% 318.42 3.19

(excluding general Takaful)

Family Takaful Sector 5,127 0.02% 27.27 0.27

General Takaful Sector 2,030 0.01% 10.8 0.11

Life Insurance Sector 112,468 0.43% 27.27 0.27

(including family Takaful)

Non‐Life Insurance Sector 61,893 0.24% 27.27 0.27

(including general Takaful)

Total 174,361 0.67% 927.45 9.3

*GDP 2013‐14 (MP) Current Basic Prices: PKR 26,001,895 million *Population 2013: 188.00million

Non‐life Insurance industry (including Takaful) grew at a pace of 16% (CAGR) in the last decade (2004‐2013). Despite that a declining growth rate trend of GWP is a bone of contention for the whole industry as the rate dropped from 42% in 2005 to 5% in 2012 and 9% in 2013 (source: industry).

“Growth rate has declined from 42pc in 2005‐06 to 9pc in 2013”

“3 classes of business make up over 74% of the total premium written for non‐life business”

“Lack of product innovation and ineffective product marketing remain the culprits of market expansion”

2

“‘Fire and Propclass of businethe insurance bMotor segmenmarket share i

“60% of the mcaptured by to2013”

“Bottom 25% ohardly able to the market sha

perty’ is the laress capturing 3business follownt, comprising in 2011”

arket share waop 4 companies

of the compancapture only 1are”

rgest 4% of wed by of 26%

as s in

ies is 1% of

Non‐Life In

Typically non‐classes of bus(iii) Motor. Infor non‐life bureduced in reyears, the groinflation; henof the non‐life

0

10

20

30

40

50

60

70

GWP in PKR

Billion

1%5%

surance Bus

‐life business issiness are founn 2013 these 3usiness. Howecent years, indowth rate in nce despite an e industry’s pre

2003

2004

2005

Non‐Li

27%

20%

Cl

siness Class‐

s short term wnd to be (i) Fir3 classes makever, in real terdicating a stagon‐life premiuaverage growtemium is facin

2006

2007

2008

ife Insurance In

ass‐wise indus(GWP

‐wise

with 12 month re & Property, up over 74% rms, the total pnant non‐life ium has not beth rate of apprng stagnation.

2008

2009

2010

ndustry: Perfor

33%

14%

try segmentatiP‐2013)

Friday, J

contracts in pl(ii) Marine & of the total prpremium writtnsurance marken able to maroximately 9%

2011

2012

2013

rmance

ion

Fire &

Mari

Moto

Liabl

Accid

Misc

July 04, 2014

AHCML

lace. The majoTransport, andremium writtenten has actuallyket. Over last 5atch the rate o, the real value

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Growth Rate

& Property

ne & Transport

or

ity

dent & Health

ellaneous

4

L

or d n y 5 of e

2

“‘Fire and Propclass of businethe insurance bMotor segmenmarket share i

“60% of the mcaptured by to2013”

“Bottom 25pc hardly able to the market sha

perty’ is the laress capturing 3business follownt, comprising in 2011”

arket share waop 4 companies

of the compancapture only 1are”

rgest 4% of wed by of 26%

as s in

nies is 1pc of

Market Sha

Non‐life insurof the markethe market shmarket shareshared amonmarket shareand National share. It is alacompanies, ar

3%

37%

are: Oligopo

rance industry t being capturhare is capturee is distributedg 29 companie in non‐life inInsurance Comarming to obsere not able to

11%

oly with limit

depicts an oligred by a few med by top 4 cod among top 1ies. AICL rankensurance followmpany Limited erve that the bmake up to 1%

22%

11%

Marke(20

ted pricing p

gopolistic marmajor insurancmpanies. Addi10 companies ed 2nd in the wed by Jubileboth capturin

bottom 10 com% of market sha

16%

t Share013)

Friday, J

power

ket structure wce companies;ng further, abwhile the remFY13, capturie General Insung approximatempanies collectare in the indu

EFU General InCompany

Adamjee InsuraLimited

Jubilee GeneraLimited

National InsuraLimited

IGI Insurance Li

Others

July 04, 2014

AHCML

with larger par; about 60% oout 76% of themaining 24% iing 16% of theurance Limitedely 22% markeively, out of 39ustry.

surance

ance Company

l Insurance

ance Company

imited

4

L

rt of e s e d et 9

s

“AICL ranked 2companies inscapturing only

“Gross Writtengrowing as thecontinuously emanagement c

“Share of eachslightly changeyears”

2nd in the 39 urance sector y 16pc market s

n Premium is ne company experiences change”

h segment in Ged over the las

by share”

not

GWP has st 5

Adamjee In

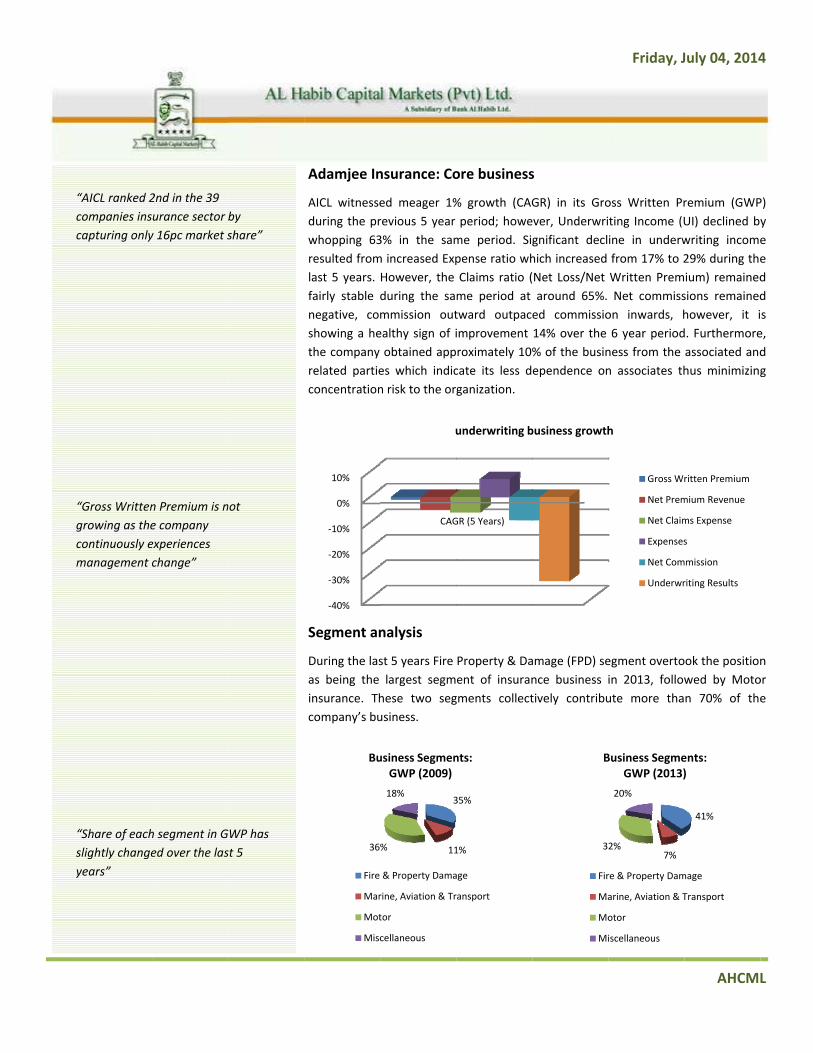

AICL witnesseduring the prwhopping 63resulted fromlast 5 years. fairly stable dnegative, comshowing a hethe company related partieconcentration

Segment an

During the lasas being the insurance. Thcompany’s bu

‐40%

‐30%

‐20%

‐10%

0%

10%

36

Bu

Fire

Mar

Mot

Misc

nsurance: Co

ed meager 1%revious 5 year 3% in the samm increased ExpHowever, the during the sammission outealthy sign of iobtained appes which indicn risk to the or

nalysis

st 5 years Fire largest segm

hese two segusiness.

CAG

u

3

11%

18%

usiness SegmenGWP (2009)

& Property Dama

rine, Aviation & Tr

tor

cellaneous

ore business

% growth (CAGperiod; howe

me period. Sigpense ratio whClaims ratio (me period at tward outpacimprovement roximately 10%cate its less dganization.

Property & Daent of insurangments collect

GR (5 Years)

underwriting b

35%

1%

nts:

age

ransport

s

GR) in its Groever, Underwrignificant declhich increased Net Loss/Net around 65%. ed commissio14% over the % of the businependence on

amage (FPD) sence business itively contribu

business growth

3

B

Fir

Ma

Mo

Mi

Friday, J

oss Written Prting Income (Uine in underwfrom 17% to 2Written PremNet commiss

on inwards, h6 year periodness from the n associates th

egment overtoin 2013, followute more tha

h

Gross Wr

Net Prem

Net Claim

Expenses

Net Com

Underwr

7%2%

20%

Business SegmeGWP (2013)

re & Property Dam

arine, Aviation & T

otor

iscellaneous

July 04, 2014

AHCML

remium (GWPUI) declined bywriting income29% during theium) remainedsions remainedhowever, it id. Furthermoreassociated andhus minimizing

ok the positionwed by Moton 70% of the

ritten Premium

mium Revenue

ms Expense

s

mmission

riting Results

41%

ents: )

mage

Transport

4

L

P) y e e d d s e, d g

n or e

o

st

i

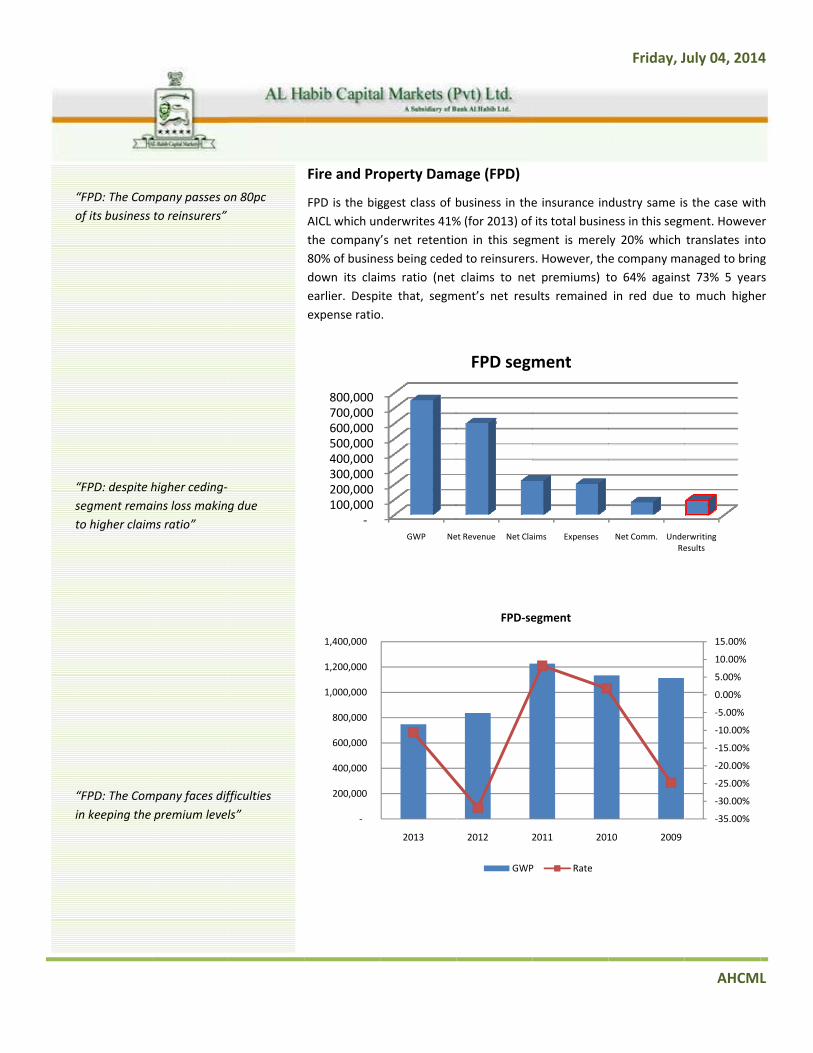

“FPD: The Comof its business

“FPD: despite hsegment remato higher claim

“FPD: The Comin keeping the

mpany passes oto reinsurers”

higher ceding‐ains loss makingms ratio”

mpany faces difpremium level

on 80pc

g due

fficulties ls”

Fire and Pro

FPD is the bigAICL which unthe company80% of businedown its claiearlier. Despiexpense ratio

‐

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

‐100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000

operty Dam

ggest class of bnderwrites 41%’s net retentioess being cedems ratio (net ite that, segm.

2013

GWP Ne

age (FPD)

business in the% (for 2013) of on in this segmd to reinsurersclaims to net

ment’s net resu

2012 2

FPD‐se

GWP

et Revenue Net Cla

FPD segm

e insurance inits total businment is merels. However, tht premiums) tults remained

2011 201

egment

P Rate

aims Expenses

ment

Friday, J

dustry same isess in this segmly 20% which e company mato 64% againsin red due to

10 2009

Net Comm. UndeRe

July 04, 2014

AHCML

s the case withment. Howevetranslates intoanaged to bringst 73% 5 yearo much highe

‐35.00%

‐30.00%

‐25.00%

‐20.00%

‐15.00%

‐10.00%

‐5.00%

0.00%

5.00%

10.00%

15.00%

erwriting esults

4

L

h er o g rs er

o

dr

o

“MAT: The Comof its business

“MAT: A highlydue to prudentretention”

“Motor: The Coof the business

mpany passes to reinsurers

y profitable segt policy in cedin

ompany retains with itself”

on 20%

gment ng and

ns 90%

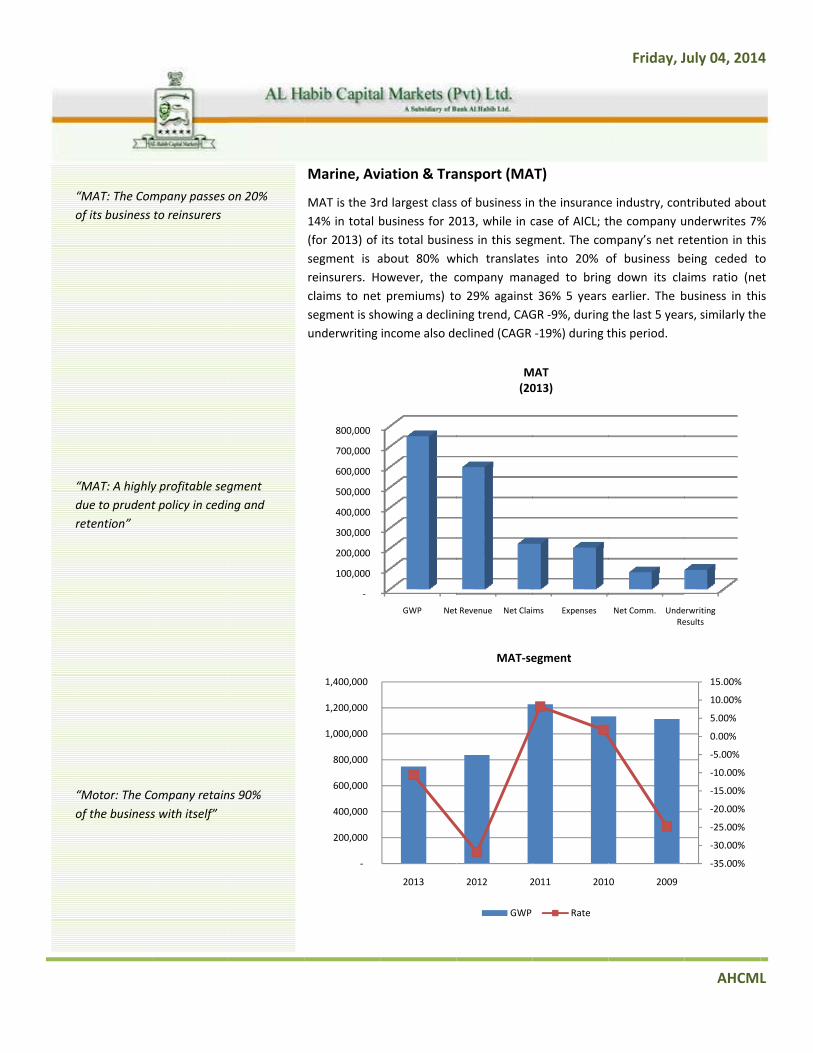

Marine, Av

MAT is the 3r14% in total b(for 2013) of segment is areinsurers. Hclaims to netsegment is shunderwriting

‐

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

‐

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

viation & Tra

rd largest classbusiness for 20its total businabout 80% wowever, the ct premiums) toowing a declinincome also de

GWP Net

2013

ansport (MA

s of business in013, while in cess in this seghich translatecompany mano 29% againstning trend, CAGeclined (CAGR

t Revenue Net Clai

M(20

2012 2

MAT‐se

GWP

AT)

n the insurancecase of AICL; tgment. The comes into 20% onaged to bringt 36% 5 years GR ‐9%, during‐19%) during t

ms Expenses

MAT013)

2011 201

egment

Rate

Friday, J

e industry, conthe company umpany’s net reof business bg down its claearlier. The b the last 5 yeathis period.

Net Comm. UndeRe

0 2009

July 04, 2014

AHCML

ntributed abouunderwrites 7%etention in thieing ceded toaims ratio (nebusiness in thirs, similarly the

erwriting esults

‐35.00%

‐30.00%

‐25.00%

‐20.00%

‐15.00%

‐10.00%

‐5.00%

0.00%

5.00%

10.00%

15.00%

4

L

ut % s o et s e

s

s

t

“Motor: declinhelping compasegment profit

“Motor: segmestagnation”

“Misc: The Comthe business w

ning claims ratiany to keep thitable”

ent also faced

mpany retains with itself”

ios is

with

59% of

Motor

Motor insuracontributed ahas underwritnet retentionbeing ceded treaches up‐tohighest net cremain in redThe profitabilother businesMotor segmethe insurance

500,00

1,000,00

1,500,00

2,000,00

‐

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

ance is the 2rbout 27% in totten 32% (for 2n in this segmeto reinsurers. o 58% making claims in termd as it continuelity in this segss segments. Tent stands at 2e company.

‐

00

00

00

00

GWP

2013

rd largest clasotal business fo2013) of its totent is about 8The company’a segment has of volume. e to hold on tgment depicts The underwrit28% in FY13 wh

Net Revenue Net C

Mo(20

2012

Motor‐

GWP

ss of businessor 2013, while tal business in 89% which tran’s claims ratio aving the 2nd Company’s neto its higher nea consoling piting income tohich is second

Claims Expenses

otor013)

2011 20

segment

P Rate

Friday, J

s in the insurin case of AICLthis segment. nslates into 11(net claims tohighest net clet commissionet retention inicture as compo gross writtenmost profitab

Net Comm. UndR

10 2009

July 04, 2014

AHCML

rance industryL; the companyThe company’1% of busineso net premiumlaims ratio and is expected on this segmentpared to a fewn premium foble segment fo

erwriting Results

‐30.00%

‐20.00%

‐10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

4

L

y, y s s

m) d o t. w or or

pr

s

“Misc: Claims rtrend during th

“Misc: despite premiums the remains depreexpense ratio”

“Misc: segmenstagnation”

ratio on the dehe last 5 years

high written underwriting iessed due to hig”

nt also faced w

eclining ”

income gher

with

Miscellaneo

Miscellaneouindustry, contcompany has The companyof business bepremium) camthan the comcommission ibetween cedeto remain subhere that thcompany’s les

500,00

1,000,00

1,500,00

2,000,00

‐

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

ous

s insurance segtributed aboutalso underwri

y’s net retentioeing ceded to me down to 43mpany’s aggregs expected toent and the rebdued keepinge segment’s sser focus on t

‐

00

00

00

00

GWP

2013

gment is the 3t 20% in total bitten 20% (for on in this segmreinsurers. The3% from 55% fgate claims rato remain meaninsures. The pg in view the hgrowth is shohis segment.

Net Revenue Net C

Miscel(20

2012 2

Misc‐se

GWP

rd largest classbusiness for 202013) of its toent is about 59e company’s cive years earlieio i.e. 64%. In ningless as therofitability in thistorical resulowing a decl

Claims Expenses

laneous013)

2011 201

egment

Rate

Friday, J

s of business in013, while in caotal business in9% which tranclaims ratio (neer which is signthis segment e business is this segment ists. It is pertineining trend w

Net Comm. UndeR

10 2009

July 04, 2014

AHCML

n the insurancease of AICL; then this segmentslates into 41%et claims to nenificantly lowecompany’s neequally shareds also expectedent to mentionwhich indicate

erwriting esults

‐30.00%

‐20.00%

‐10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

4

L

e e t. % et er et d d n s

f

“Portfolio valuthe fair value o

“MCB value cofair value of th

“BUY with 33p

ue constitutes 7of the company

onstitutes 32pche company”

pc upside poten

75pc of y”

c of the

ntial”

Portfolio Va

Equity portfoheld in the associates). Tquoted equitsecurities‐for Government carrying valucompany’s inv

It is pertinentholdings as pThe value of portfolio, conchange in MCchange in MC

Recommen

AICL is tradin33pc, which r

38%

alue: Gems

lio has been oquoted equityTherefore, we ty investmentswhich we havsecurities and e in the balanvested portfoli

t to note thatortfolio value MCB bank remntributing aboCB bank’s fair vCB bank’s value

ndation: BUY

ng at PKR 47.5equires us to a

55%5%

and Pearls

objectively valuy investment have applieds of both AFSve used our min unquoted cnce sheet theio.

the fair valueconstitutes momains the majoout 32pc in covalue may havee will change A

Y

8 on July 3, 2assign a ‘BUY’ r

6%5%

Top 5‐ Portf(Based on m

ue; consideringportfolio (bo

d a 25% discoS and associatmodel based facompanies (asereby arriving

e of AICL is higore than 75pcor value driverompany’s fair e a significant AICL’s fair value

014 closing, orating for the s

41%

folio Holdingsmarket value)

Friday, J

g the illiquidityoth AFS and iunt on the mtes (excludingir value), and sociates) haveat the approp

ghly sensitive of the compar for the compvalue. So animpact on AICe by 1.80pc.

offering a potestock.

MCB Bank

United Ba

MCB CashOptimizer

MCB Dyna

Fauji FertiLimited

Others

July 04, 2014

AHCML

y of the shareinvestments inmarket price og certain listedinvestments ine been taken apriate value o

to its portfolioany’s fair valuepany’s investedy fundamentaL’s value, a 5p

ential upside o

k Limited

nk Limited

h Management r Fund

amic Cash Fund

lizer Company

4

L

es n of d n at of

o e. d al c

of

Friday, July 04, 2014

AHCML

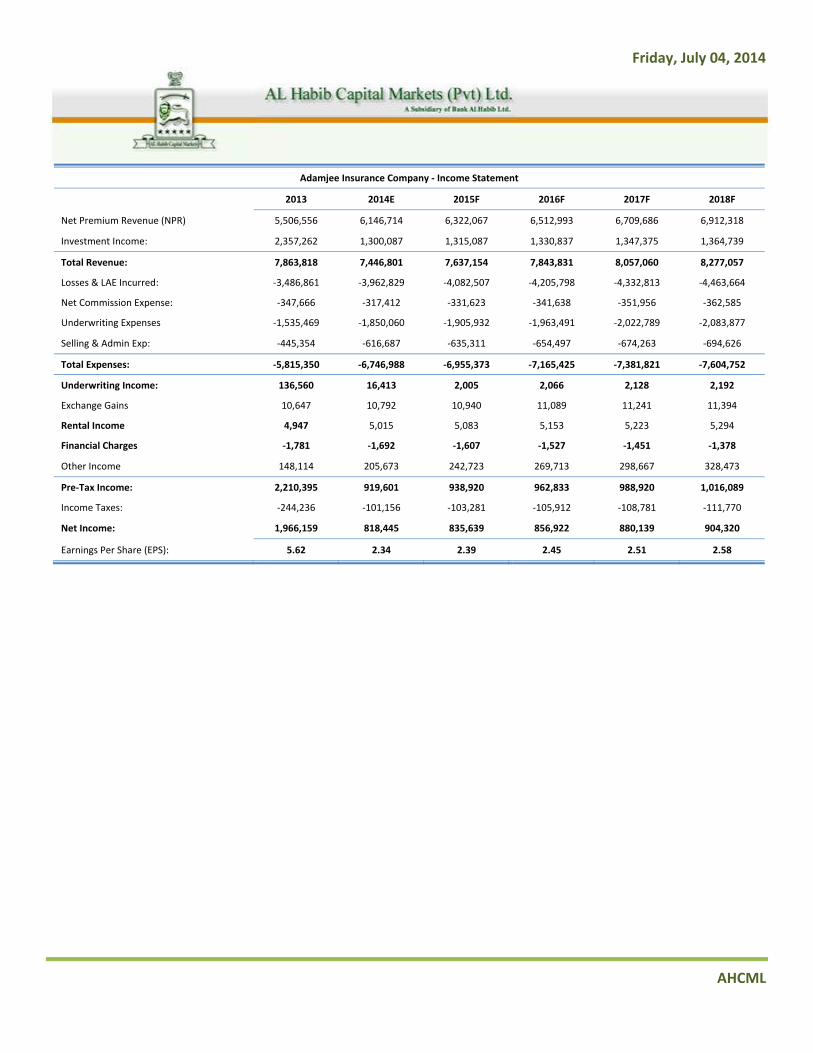

Adamjee Insurance Company ‐ Income Statement

2013 2014E 2015F 2016F 2017F 2018F

Net Premium Revenue (NPR) 5,506,556 6,146,714 6,322,067 6,512,993 6,709,686 6,912,318

Investment Income: 2,357,262 1,300,087 1,315,087 1,330,837 1,347,375 1,364,739

Total Revenue: 7,863,818 7,446,801 7,637,154 7,843,831 8,057,060 8,277,057

Losses & LAE Incurred: ‐3,486,861 ‐3,962,829 ‐4,082,507 ‐4,205,798 ‐4,332,813 ‐4,463,664

Net Commission Expense: ‐347,666 ‐317,412 ‐331,623 ‐341,638 ‐351,956 ‐362,585

Underwriting Expenses ‐1,535,469 ‐1,850,060 ‐1,905,932 ‐1,963,491 ‐2,022,789 ‐2,083,877

Selling & Admin Exp: ‐445,354 ‐616,687 ‐635,311 ‐654,497 ‐674,263 ‐694,626

Total Expenses: ‐5,815,350 ‐6,746,988 ‐6,955,373 ‐7,165,425 ‐7,381,821 ‐7,604,752

Underwriting Income: 136,560 16,413 2,005 2,066 2,128 2,192

Exchange Gains 10,647 10,792 10,940 11,089 11,241 11,394

Rental Income 4,947 5,015 5,083 5,153 5,223 5,294

Financial Charges ‐1,781 ‐1,692 ‐1,607 ‐1,527 ‐1,451 ‐1,378

Other Income 148,114 205,673 242,723 269,713 298,667 328,473

Pre‐Tax Income: 2,210,395 919,601 938,920 962,833 988,920 1,016,089

Income Taxes: ‐244,236 ‐101,156 ‐103,281 ‐105,912 ‐108,781 ‐111,770

Net Income: 1,966,159 818,445 835,639 856,922 880,139 904,320

Earnings Per Share (EPS): 5.62 2.34 2.39 2.45 2.51 2.58

Friday, July 04, 2014

AHCML

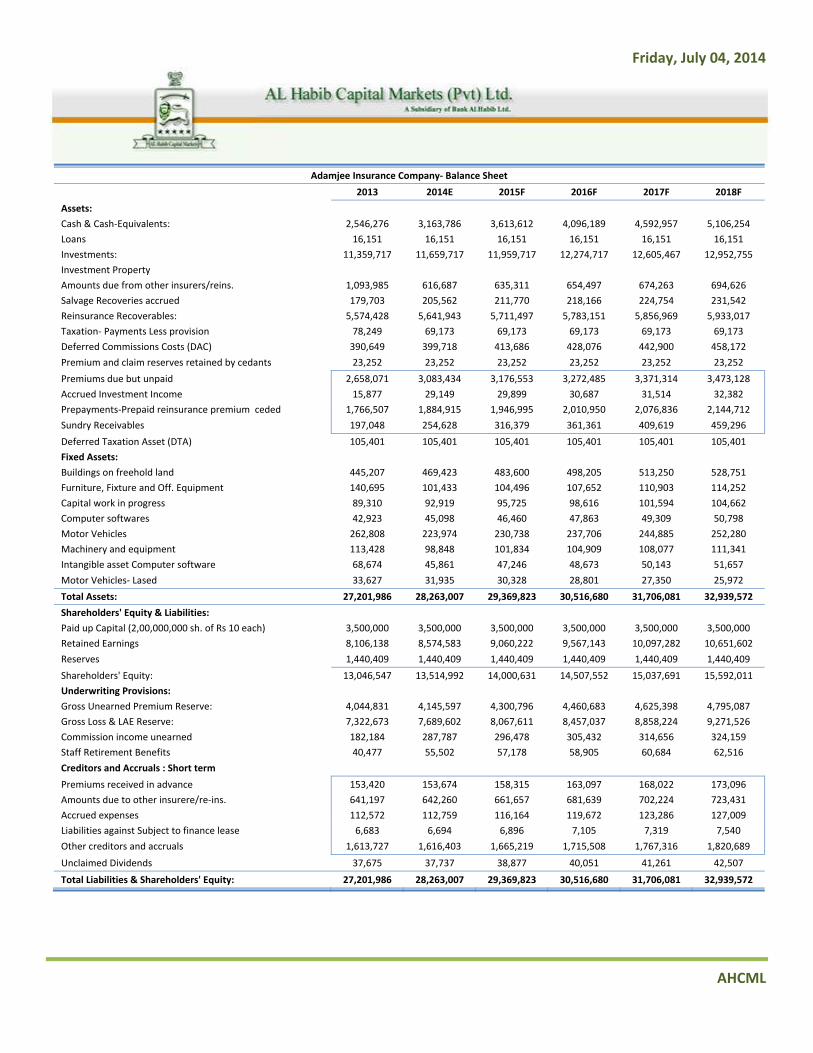

Adamjee Insurance Company‐ Balance Sheet

2013 2014E 2015F 2016F 2017F 2018F

Assets:

Cash & Cash‐Equivalents: 2,546,276 3,163,786 3,613,612 4,096,189 4,592,957 5,106,254

Loans 16,151 16,151 16,151 16,151 16,151 16,151

Investments: 11,359,717 11,659,717 11,959,717 12,274,717 12,605,467 12,952,755

Investment Property

Amounts due from other insurers/reins. 1,093,985 616,687 635,311 654,497 674,263 694,626

Salvage Recoveries accrued 179,703 205,562 211,770 218,166 224,754 231,542

Reinsurance Recoverables: 5,574,428 5,641,943 5,711,497 5,783,151 5,856,969 5,933,017

Taxation‐ Payments Less provision 78,249 69,173 69,173 69,173 69,173 69,173

Deferred Commissions Costs (DAC) 390,649 399,718 413,686 428,076 442,900 458,172

Premium and claim reserves retained by cedants 23,252 23,252 23,252 23,252 23,252 23,252

Premiums due but unpaid 2,658,071 3,083,434 3,176,553 3,272,485 3,371,314 3,473,128

Accrued Investment Income 15,877 29,149 29,899 30,687 31,514 32,382

Prepayments‐Prepaid reinsurance premium ceded 1,766,507 1,884,915 1,946,995 2,010,950 2,076,836 2,144,712

Sundry Receivables 197,048 254,628 316,379 361,361 409,619 459,296

Deferred Taxation Asset (DTA) 105,401 105,401 105,401 105,401 105,401 105,401

Fixed Assets:

Buildings on freehold land 445,207 469,423 483,600 498,205 513,250 528,751

Furniture, Fixture and Off. Equipment 140,695 101,433 104,496 107,652 110,903 114,252

Capital work in progress 89,310 92,919 95,725 98,616 101,594 104,662

Computer softwares 42,923 45,098 46,460 47,863 49,309 50,798

Motor Vehicles 262,808 223,974 230,738 237,706 244,885 252,280

Machinery and equipment 113,428 98,848 101,834 104,909 108,077 111,341

Intangible asset Computer software 68,674 45,861 47,246 48,673 50,143 51,657

Motor Vehicles‐ Lased 33,627 31,935 30,328 28,801 27,350 25,972

Total Assets: 27,201,986 28,263,007 29,369,823 30,516,680 31,706,081 32,939,572

Shareholders' Equity & Liabilities:

Paid up Capital (2,00,000,000 sh. of Rs 10 each) 3,500,000 3,500,000 3,500,000 3,500,000 3,500,000 3,500,000

Retained Earnings 8,106,138 8,574,583 9,060,222 9,567,143 10,097,282 10,651,602

Reserves 1,440,409 1,440,409 1,440,409 1,440,409 1,440,409 1,440,409

Shareholders' Equity: 13,046,547 13,514,992 14,000,631 14,507,552 15,037,691 15,592,011

Underwriting Provisions:

Gross Unearned Premium Reserve: 4,044,831 4,145,597 4,300,796 4,460,683 4,625,398 4,795,087

Gross Loss & LAE Reserve: 7,322,673 7,689,602 8,067,611 8,457,037 8,858,224 9,271,526

Commission income unearned 182,184 287,787 296,478 305,432 314,656 324,159

Staff Retirement Benefits 40,477 55,502 57,178 58,905 60,684 62,516

Creditors and Accruals : Short term

Premiums received in advance 153,420 153,674 158,315 163,097 168,022 173,096

Amounts due to other insurere/re‐ins. 641,197 642,260 661,657 681,639 702,224 723,431

Accrued expenses 112,572 112,759 116,164 119,672 123,286 127,009

Liabilities against Subject to finance lease 6,683 6,694 6,896 7,105 7,319 7,540

Other creditors and accruals 1,613,727 1,616,403 1,665,219 1,715,508 1,767,316 1,820,689

Unclaimed Dividends 37,675 37,737 38,877 40,051 41,261 42,507

Total Liabilities & Shareholders' Equity: 27,201,986 28,263,007 29,369,823 30,516,680 31,706,081 32,939,572

Friday, July 04, 2014

AHCML

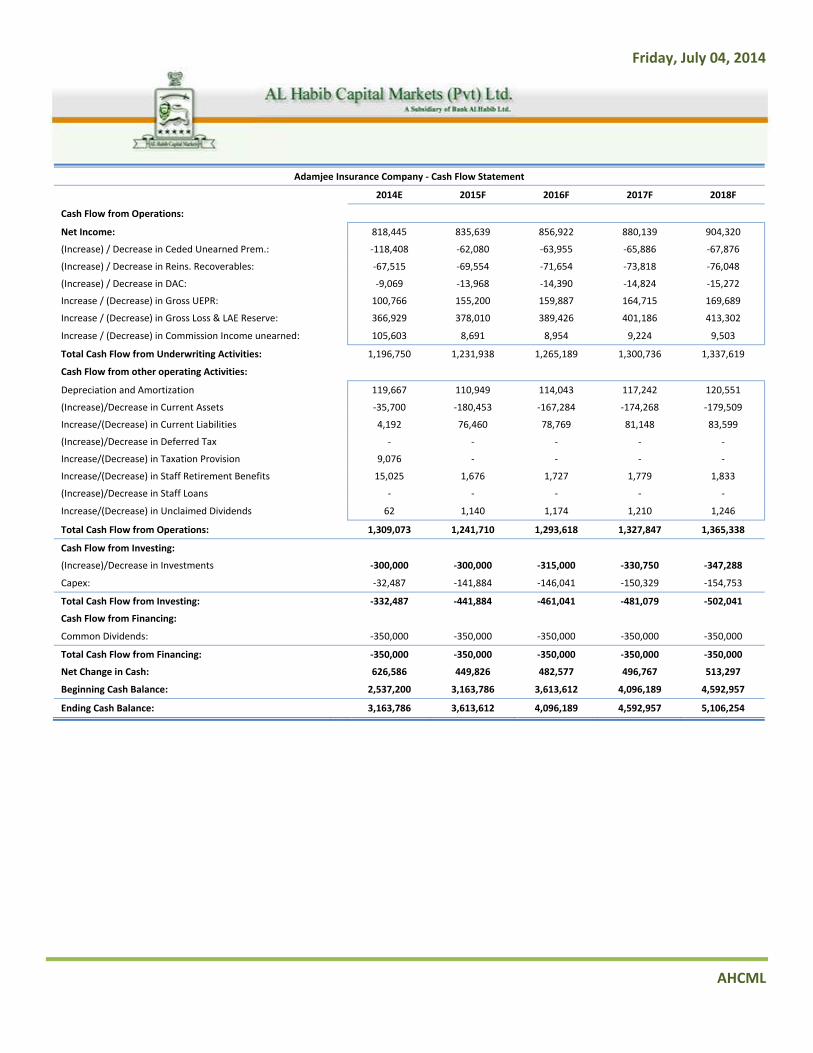

Adamjee Insurance Company ‐ Cash Flow Statement

2014E 2015F 2016F 2017F 2018F

Cash Flow from Operations:

Net Income: 818,445 835,639 856,922 880,139 904,320

(Increase) / Decrease in Ceded Unearned Prem.: ‐118,408 ‐62,080 ‐63,955 ‐65,886 ‐67,876

(Increase) / Decrease in Reins. Recoverables: ‐67,515 ‐69,554 ‐71,654 ‐73,818 ‐76,048

(Increase) / Decrease in DAC: ‐9,069 ‐13,968 ‐14,390 ‐14,824 ‐15,272

Increase / (Decrease) in Gross UEPR: 100,766 155,200 159,887 164,715 169,689

Increase / (Decrease) in Gross Loss & LAE Reserve: 366,929 378,010 389,426 401,186 413,302

Increase / (Decrease) in Commission Income unearned: 105,603 8,691 8,954 9,224 9,503

Total Cash Flow from Underwriting Activities: 1,196,750 1,231,938 1,265,189 1,300,736 1,337,619

Cash Flow from other operating Activities:

Depreciation and Amortization 119,667 110,949 114,043 117,242 120,551

(Increase)/Decrease in Current Assets ‐35,700 ‐180,453 ‐167,284 ‐174,268 ‐179,509

Increase/(Decrease) in Current Liabilities 4,192 76,460 78,769 81,148 83,599

(Increase)/Decrease in Deferred Tax ‐ ‐ ‐ ‐ ‐

Increase/(Decrease) in Taxation Provision 9,076 ‐ ‐ ‐ ‐

Increase/(Decrease) in Staff Retirement Benefits 15,025 1,676 1,727 1,779 1,833

(Increase)/Decrease in Staff Loans ‐ ‐ ‐ ‐ ‐

Increase/(Decrease) in Unclaimed Dividends 62 1,140 1,174 1,210 1,246

Total Cash Flow from Operations: 1,309,073 1,241,710 1,293,618 1,327,847 1,365,338

Cash Flow from Investing:

(Increase)/Decrease in Investments ‐300,000 ‐300,000 ‐315,000 ‐330,750 ‐347,288

Capex: ‐32,487 ‐141,884 ‐146,041 ‐150,329 ‐154,753

Total Cash Flow from Investing: ‐332,487 ‐441,884 ‐461,041 ‐481,079 ‐502,041

Cash Flow from Financing:

Common Dividends: ‐350,000 ‐350,000 ‐350,000 ‐350,000 ‐350,000

Total Cash Flow from Financing: ‐350,000 ‐350,000 ‐350,000 ‐350,000 ‐350,000

Net Change in Cash: 626,586 449,826 482,577 496,767 513,297

Beginning Cash Balance: 2,537,200 3,163,786 3,613,612 4,096,189 4,592,957

Ending Cash Balance: 3,163,786 3,613,612 4,096,189 4,592,957 5,106,254

Friday, July 04, 2014

AHCML

Disclaimer All rights reserved. The information presented in this report is compiled from sources we believed to be reliable in preparation of this report. However, we do not accept any responsibility for its accuracy and completeness. This report is not intended to be an offer or solicitation to buy or sell any security. AL Habib Capital Markets (Pvt.) Ltd. and its employees may or may not have a position in or with respect to the securities mentioned in this report. In particular, the report takes no account of investment objectives, financial situation & particular needs of investors who should seek further professional advice or rely upon their own judgment before making any investment.

Muhammad Ali Khan Senior Investment Analyst [email protected]

Abdul Samad Supervising Officer [email protected]

Head Office: GF‐01, Techno City, Hasrat Mohani Road, Karachi Ph: +92 21 32270808‐13 Fax: +92 21 32270519

Stock Office: Room No. 16 Ground Floor, New Stock Exchange Bldg., Stock Exchange Road, Karachi Ph: +92 21 32460867‐ 32460869