Embed Size (px)

Citation preview

A Project Of Strategic Financial Management

On Maximizing Return by minimizing the Risk

Askari Bank

&

Muslim Commercial BankSubmitted to

Sir Rais Ahmad

By:

Avinash Advani-6356

1. Acknowledgment

2. Abstract

3. Introduction

4. Calculation of Askari And MCB band

5. Individual Analysis

6. Business Portfolio Analysis

7. Conclusion

8. References

Sir Rais Ahmed

First of all we would like to thank Almighty GOD who enabled me to work on this report. Then, we would like to show gratitude to my Teacher Sir Rais Ahmed who guided me in every phrase and help me out to prepare this report and also want to thank all of my friends and group members who support me to complete this report on time.

Sir Rais Ahmed we tried our level best to fulfill the requirement of course Strategic finance and management , throughout during this report we learned how we can Analysis company & also we come to know the standard format & steps.We hope this report fulfill the requirements of course Strategic finance and management

Sincerely,Avinash-6356Nazia-6526

Stock return volatilities are related to firms' financial status.

Financially constrained firms are more volatile, In the stock

market and financial markets, volatility refers to the standard

deviation of a financial instrument within a given time frame.

Volatility is thus used to quantify the risk of the financial

instrument over the given time period. In finance, volatility is

calculated over a given time period and then expressed in

annualized terms as a percentage.

The Return on stock and risk very effected the whole market

of stock which is very valuable for stock market there are

many companies which are registered in stock exchange and

they analysis about their return, risk, and beta.

•Asker Bank was incorporated on October 09, 1991 as a Public

Limited Company and is listed on the Karachi, Lahore and

Islamabad Stock Exchange.

•It started its operations from April 01, 1992. The bank was

declared as “Best Bank in Pakistan” in2001 in Global Finance

•Askari Bank Limited has expanded into a nation wide presence

of over a 100 branches, comprising commercial and Islamic

banking branches, connected online and supported by a

network of Automated Teller Machines (ATMs).

Askari Commercial Bank Limited was the first bank in Pakistan to

offer Internet banking Services and B2B e-commerce (Business to

Business electronic Commerce)solutions for merchants looking to

purchase on credit. They believe that balanced growths the key to

survive in the today’s global banking environment

Vision:

“To be the Bank of first choice”

•MCB Bank Ltd formerly known as Muslim Commercial Bank Limited was

incorporated by the Adamjee Group on July 9, 1947, under the Indian

Companies Act, VII of 1913 as a limited company

•The bank was established with a view to provide banking facilities to the

business community of the sub-continent. The bank was nationalized in 1974

during the government of Zulfikar Ali Bhutto.MCB earned Revenue of PKR

31.787 billion and Net Income of PKR 15.266 billion in 2007.

MCB is the fourth largest bank of Pakistan. Its wide network include fully

facilitated branches all over Pakistan. It covers 125 cities, comprising of

978 branches out of which 262 have the ATM machines

MCB has been awarded as a Euro money Award 2008 for the " Best

Bank in Asia". In 2006 MCB yet again received the esteemed Euro

money Award for the "Best Bank in Pakistan”. It is the only bank to

receive the Euro money Award for Excellence for the sixth time in

the past seven years

MCB Continues to shine as once again Asia Money declares MCB as

"The Best Domestic Commercial Bank in Pakistan" for the year 2004

and 2005

MCB Bank’s team of committed

professionals is dedicated to maintaining

long term customer relationships through

outstanding service and convenience

The future is uncertain.

Investors do not know with certainty

whether the economy will be growing

rapidly or be in recession.

Investors do not know what rate of

return their investments will yield.

A measure of variability or dispersion of a

quantity, given as the average squared

deviation of individual observations from

the mean value in a distribution. Its

square root is the standard deviation.

A measure of the volatility of return,

computed as an average squared

deviation of return from the mean value.

Risk reflects the chance that the actual

return on an investment may be different

than the expected return.

If investors accept the idea that

investment risk is defined by a loss of

capital and/or underperformance

relative to expectations, it makes

defining low risk and high-risk investments

substantially easier.

•Portfolio is a group of financial assets such as shares, stocks,

bonds, debt instruments, mutual funds, cash equivalents, etc. A

portfolio is planned to stabilize the risk of non-performance of

various pools of investment.

•It is a generally accepted principle that a portfolio is designed

according to the investor's risk tolerance, time frame and

investment objectives

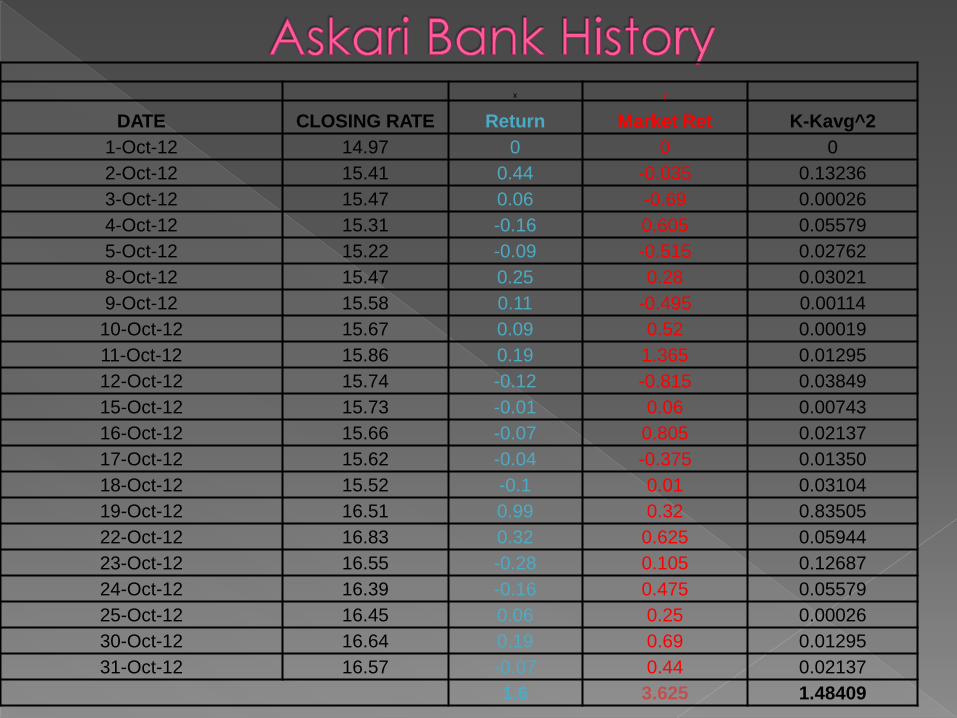

x y

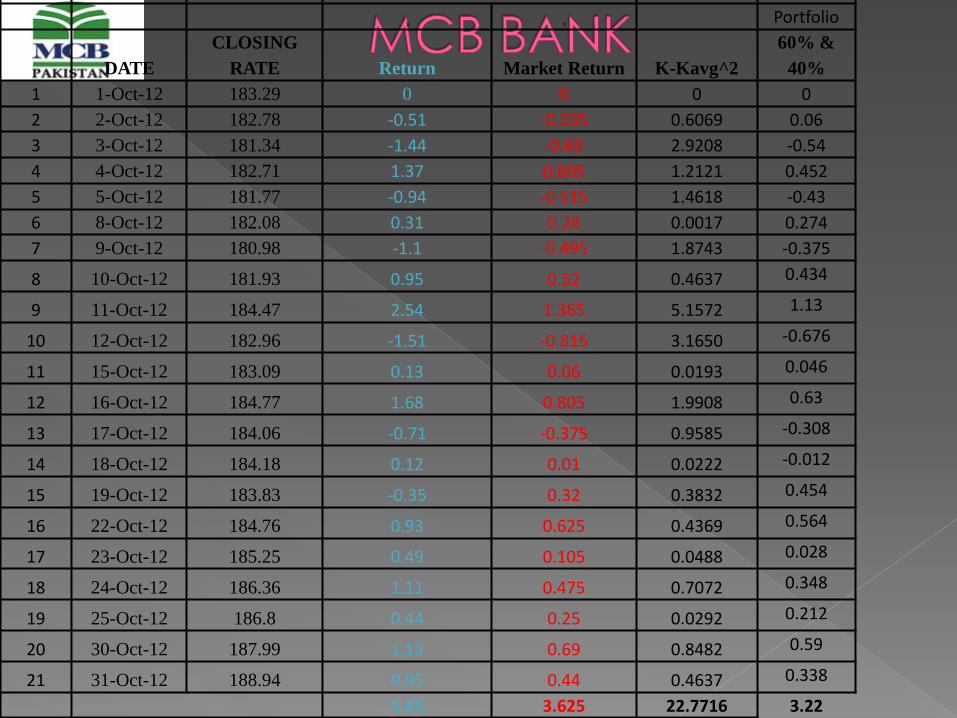

DATE CLOSING RATE Return Market Ret K-Kavg^2

1-Oct-12 14.97 0 0 0

2-Oct-12 15.41 0.44 -0.035 0.13236

3-Oct-12 15.47 0.06 -0.69 0.00026

4-Oct-12 15.31 -0.16 0.605 0.05579

5-Oct-12 15.22 -0.09 -0.515 0.02762

8-Oct-12 15.47 0.25 0.28 0.03021

9-Oct-12 15.58 0.11 -0.495 0.00114

10-Oct-12 15.67 0.09 0.52 0.00019

11-Oct-12 15.86 0.19 1.365 0.01295

12-Oct-12 15.74 -0.12 -0.815 0.03849

15-Oct-12 15.73 -0.01 0.06 0.00743

16-Oct-12 15.66 -0.07 0.805 0.02137

17-Oct-12 15.62 -0.04 -0.375 0.01350

18-Oct-12 15.52 -0.1 0.01 0.03104

19-Oct-12 16.51 0.99 0.32 0.83505

22-Oct-12 16.83 0.32 0.625 0.05944

23-Oct-12 16.55 -0.28 0.105 0.12687

24-Oct-12 16.39 -0.16 0.475 0.05579

25-Oct-12 16.45 0.06 0.25 0.00026

30-Oct-12 16.64 0.19 0.69 0.01295

31-Oct-12 16.57 -0.07 0.44 0.02137

1.6 3.625 1.48409

Kavg/K

bar

0.076

19

Total Return = 1.6

Variance 0.07420451

S.Deviation 0.27240505

CV 3.5753163

Beta Askari 0.341016

Calculations:

Total Return is on X and Y is on Market return so total return divide by total number

1.6/21 = 0.07619

Variance = K-Kavg^2/n-1

1.48409/21-1 = 0.07420451

Standard deviation is σ “sigma” of variance = 0.27240505

Coefficient of variance = Sigma/Kavg = 3.5753163

Beta = n(XY)-(x)(Y) / n(xy)^2-(X)^2

Or

=slope of X and Y = 0.341016

X YPortfolio

DATE

CLOSING

RATE Return Market Return K-Kavg^2

60% &

40%

1 1-Oct-12 183.29 0 0 0 0

2 2-Oct-12 182.78 -0.51 -0.035 0.6069 0.06

3 3-Oct-12 181.34 -1.44 -0.69 2.9208 -0.54

4 4-Oct-12 182.71 1.37 0.605 1.2121 0.452

5 5-Oct-12 181.77 -0.94 -0.515 1.4618 -0.43

6 8-Oct-12 182.08 0.31 0.28 0.0017 0.274

7 9-Oct-12 180.98 -1.1 -0.495 1.8743 -0.375

8 10-Oct-12 181.93 0.95 0.52 0.4637 0.434

9 11-Oct-12 184.47 2.54 1.365 5.1572 1.13

10 12-Oct-12 182.96 -1.51 -0.815 3.1650 -0.676

11 15-Oct-12 183.09 0.13 0.06 0.0193 0.046

12 16-Oct-12 184.77 1.68 0.805 1.9908 0.63

13 17-Oct-12 184.06 -0.71 -0.375 0.9585 -0.308

14 18-Oct-12 184.18 0.12 0.01 0.0222 -0.012

15 19-Oct-12 183.83 -0.35 0.32 0.3832 0.454

16 22-Oct-12 184.76 0.93 0.625 0.4369 0.564

17 23-Oct-12 185.25 0.49 0.105 0.0488 0.028

18 24-Oct-12 186.36 1.11 0.475 0.7072 0.348

19 25-Oct-12 186.8 0.44 0.25 0.0292 0.212

20 30-Oct-12 187.99 1.19 0.69 0.8482 0.59

21 31-Oct-12 188.94 0.95 0.44 0.4637 0.338

5.65 3.625 22.7716 3.22

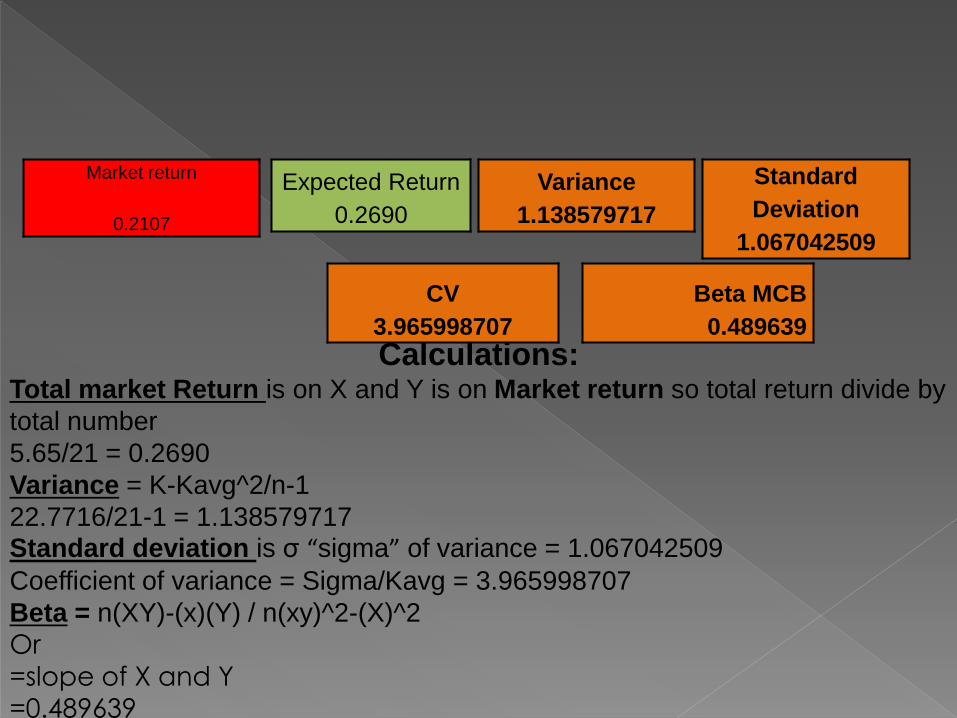

Market return

0.2107

Expected Return

0.2690

Variance

1.138579717

Standard

Deviation

1.067042509

CV

3.965998707

Beta MCB

0.489639

Calculations:Total market Return is on X and Y is on Market return so total return divide by

total number

5.65/21 = 0.2690

Variance = K-Kavg^2/n-1

22.7716/21-1 = 1.138579717Standard deviation is σ “sigma” of variance = 1.067042509

Coefficient of variance = Sigma/Kavg = 3.965998707

Beta = n(XY)-(x)(Y) / n(xy)^2-(X)^2

Or

=slope of X and Y=0.489639

Total return of askari bank and MCB both

must be plus after this we have to divide

with two then result will come

Market return

0.2107

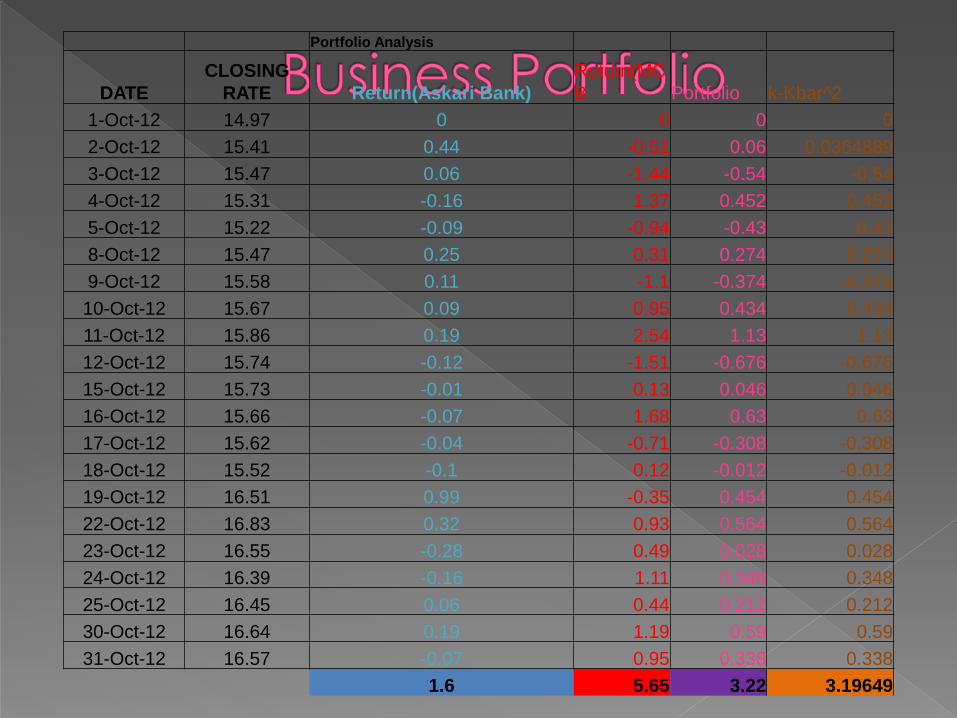

Portfolio Analysis

DATE

CLOSING

RATE Return(Askari Bank)

Return(MC

B Portfolio k-Kbar^2

1-Oct-12 14.97 0 0 0 0

2-Oct-12 15.41 0.44 -0.51 0.06 0.0364889

3-Oct-12 15.47 0.06 -1.44 -0.54 -0.54

4-Oct-12 15.31 -0.16 1.37 0.452 0.452

5-Oct-12 15.22 -0.09 -0.94 -0.43 -0.43

8-Oct-12 15.47 0.25 0.31 0.274 0.274

9-Oct-12 15.58 0.11 -1.1 -0.374 -0.374

10-Oct-12 15.67 0.09 0.95 0.434 0.434

11-Oct-12 15.86 0.19 2.54 1.13 1.13

12-Oct-12 15.74 -0.12 -1.51 -0.676 -0.676

15-Oct-12 15.73 -0.01 0.13 0.046 0.046

16-Oct-12 15.66 -0.07 1.68 0.63 0.63

17-Oct-12 15.62 -0.04 -0.71 -0.308 -0.308

18-Oct-12 15.52 -0.1 0.12 -0.012 -0.012

19-Oct-12 16.51 0.99 -0.35 0.454 0.454

22-Oct-12 16.83 0.32 0.93 0.564 0.564

23-Oct-12 16.55 -0.28 0.49 0.028 0.028

24-Oct-12 16.39 -0.16 1.11 0.348 0.348

25-Oct-12 16.45 0.06 0.44 0.212 0.212

30-Oct-12 16.64 0.19 1.19 0.59 0.59

31-Oct-12 16.57 -0.07 0.95 0.338 0.338

1.6 5.65 3.22 3.19649

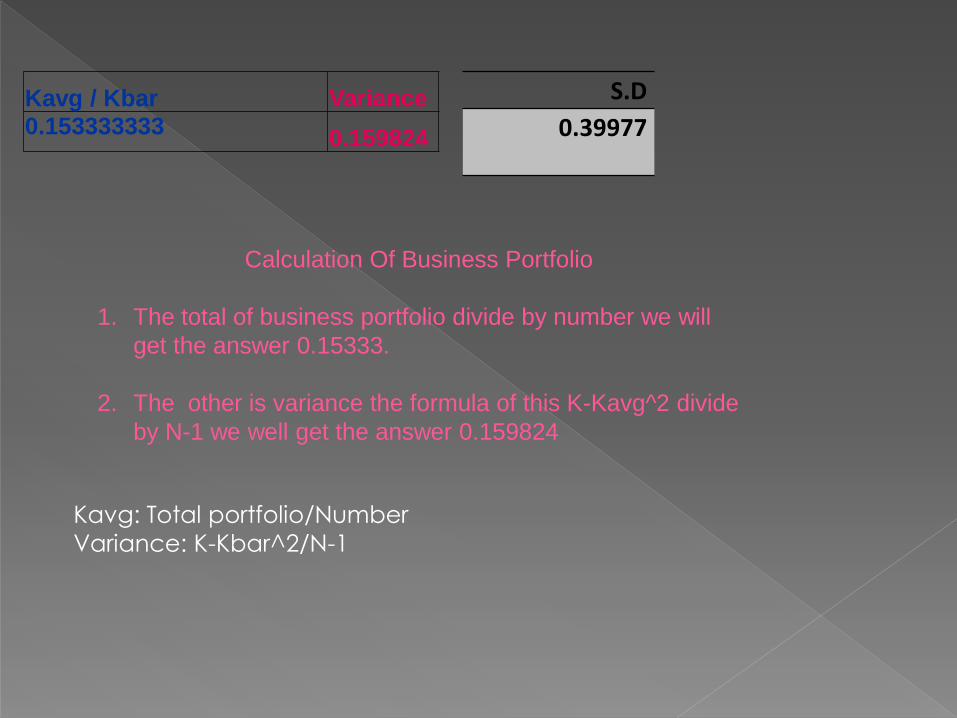

Kavg / Kbar Variance0.153333333

0.159824

Calculation Of Business Portfolio

1. The total of business portfolio divide by number we will

get the answer 0.15333.

2. The other is variance the formula of this K-Kavg^2 divide

by N-1 we well get the answer 0.159824

Kavg: Total portfolio/Number

Variance: K-Kbar^2/N-1

S.D

0.39977

Askari Bank Return is 0.07619

MCB Return is 0.2690

So when we compare these both result

then MCB gives us high return on stock and askari gives us lower return

Standard deviation of Askari or risk is 0.27240505

Standard deviation of MCB is 1.067042509

The Aksari risk is 0.27240 and MCB risk is 1.06704

It means that higher return higher risk of MCB and Aksari is lower

return lower risk so if I am risk taker I will go for MCB

Systematic risk is overall market risk as applied to a particular

stock. It cannot be diversified against in a portfolio.

Depending on its volatility compared to the benchmark, a

stock will have a beta of greater or less than 1. The higher the

beta, the more volatile the stock; the lower the beta, the less

volatile.

In this chapter we learn about the total return on stock and their risk. For example if company A gives us 0.9 return on stock and Company B gives us 0.7 on stock then its return is less than company A so we prefer the company A because its gives us high return on stock A and 0.9 is greater than 0.7 so its conceptual that we go for stock A.

The related terms "threat" and "hazard" are often used to mean something that could cause harm.

When we talk about Risk, lower risk is better than high risk but in this risk there are two types of risk

1. Risk Taker 2. Risk Aversion

If a company gives us high return and its risk is also high and if we are risk taker then we go for it because we are expecting the more return but also as well as we are risk taker.

A risk management technique that seeks to eliminate any possibility of risk through hazard prevention, or the discontinuation of activities determined to entail any level of risk. Often used in extreme situations where the risk exposure creates an extraordinary liability potential.

Business portfolio

We are not invest only single company we invest different companies because every individual company gives us dissimilar return and their risk is also dissimilar

So in this chapter it included about the return on stock, market return, risk, and business portfolio and how to calculate them.

:http://www.investorwords.com/19201/risk_avoidance.html#ixzz2EeJATzXn

http://www.investopedia.com/terms/r/riskreturntradeoff.asp

http://riskandreturn.net/

http://www.accessecon.com