Embed Size (px)

Citation preview

The Time Value of Money

TOPIC 3

Learning Objectives

1. Define the time value of money

2. The significance of time value of money in financial management

3. Define and understand the conceptual and calculation of future and present value in cash flows

4. Define the meaning of compounding and discounting

5. Work with annuities and perpetuities

2 WRMAS

TIME VALUE OF MONEY

3

Basic Principle : A dollar received today is worth more than a dollar received in the future.

• This is due to opportunity costs. The opportunity cost of receiving $1 in the future is the interest we could have earned if we had received the $1 sooner.

• Example

Invest RM1 today at a 6% annual interest rate. At the end of the year you will get $1.06.

SO You can say:

1. The future value of RM1 today is $1.06 given a 6% interest rate a year. OR WE CAN SAY

2. The present value of the $1.06 you expect to receive in one year is only $1 today.

WRMAS

4

Translate $1 today into its equivalent in the future (compounding) – Future Value

Translate $1 in the future into its equivalent today (discounting)- Present Value

Today

?

Future

?

Today Future

WRMAS

SIGNIFICANCE OF TIME VALUE OF MONEY

• This concept is so important in understanding financial management.

• We must take this time value of money into consideration when we are making financial decisions.

• It can be used to compare investment alternatives and to solve problems involving loans, mortgages, leases, savings, and annuities.

5 WRMAS

COMPOUND INTEREST AND FUTURE VALUE

• Future value is the value at a given future date of an amount placed on deposit today and earning interest at a specified rate.

• Compound interest is interest paid on an investment during the first period is added to the principal; then, during the second period, interest is earned on the new sum (that includes the principal and interest earned so far). (Process of determining FV)

• Principal is the amount of money on which interest is paid.

WRMAS 5-6

5-7

Simple Interest

• Interest is earned only on principal.

• Example: Compute simple interest on $100 invested at 6% per year for 3 years.

– 1st year interest is $6.00

– 2nd year interest is $6.00

– 3rd year interest is $6.00

– Total interest earned: $18.00

8

Compound Interest and Future Value

Example:

Compute compound interest on $100 invested at 6% for 3 years with annual compounding.

1st year interest is $6.00 Principal is $106.00

2nd year interest is $6.36 Principal is $112.36

3rd year interest is $6.74 Principal is $119.11

Total interest earned: $19.10

WRMAS

The Equation for Future Value

• We use the following notation for the various inputs:

– FVn = future value at the end of period n

– PV = initial principal, or present value

– r = annual rate of interest paid. (Note: On financial calculators, I is typically used to represent this rate.)

– n = number of periods (typically years) that the money is left on deposit

OR

FVn = PV (1+r)n FVn = PV (FVIFr,n)

WRMAS 9

Future Value Example Example: What will be the FV of $100 in 2 years at interest rate of

6%?

Manually Table

FV2= $100 (1+.06)2 FV2= PV(FVIF6%,2)

= $100 (1.06)2 = $100 (1.1236)

= $112.36 = $112.36

Exercise Jane Farber places $800 in a savings account paying 6% interest compounded annually. She wants to know how much money will be in the account at the end of 5 years.

10

SAME ANSWER!

WRMAS

11

Future Value

Changing I, N and PV

• Future Value can be increased or decreased by changing: Increasing number of years of compounding

(n)

Increasing the interest or discount rate (i)

Increasing the original investment (PV)

WRMAS

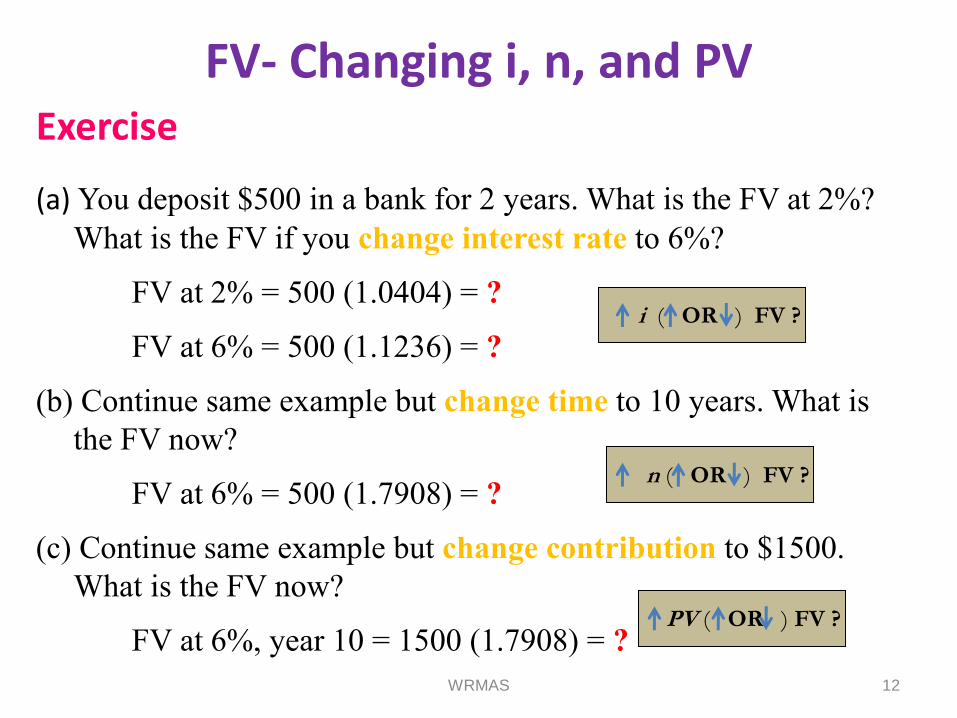

FV- Changing i, n, and PV Exercise

(a) You deposit $500 in a bank for 2 years. What is the FV at 2%?

What is the FV if you change interest rate to 6%?

FV at 2% = 500 (1.0404) = ?

FV at 6% = 500 (1.1236) = ?

(b) Continue same example but change time to 10 years. What is

the FV now?

FV at 6% = 500 (1.7908) = ?

(c) Continue same example but change contribution to $1500.

What is the FV now?

FV at 6%, year 10 = 1500 (1.7908) = ?

i ( OR ) FV ?

n ( OR ) FV ?

PV ( OR ) FV ?

WRMAS 12

Future Value Relationship

WRMAS

We can increase the FV by: 1. Increasing the number of years for which money is invested;

and/or 2. Investing at a higher interest rate.

13

Example 1 At what annual rate would the following have to be invested ; $500 to grow to $1183.70 in 10 years. 1183.70 = 500 (FVIFi,,10) 1183.70/500 = FVIFi,10 2.3674 = FVIFi,10 (refer to FVIF table) 2.3674 = 9% Example 2 How many years will the following take? $100 to grow to $672.75 if invested at 10% compounded annually. $672.75 = $100 (FVIF10%,n) 672.75/100 = FVIF10%,n 6.7275 = FVIF10%,n (refer to FVIF table) 6.7275 = 20 years

FV- Finding I and n

14 WRMAS

Exercise-Finding i and n

a) How many years will the following take :

i. $100 to grow to $298.60 if invested at 20% compounded annually

ii. $550 to grow to $1,044.05 if invested at 6% compounded annually

b) At what annual rate would the following have to be invested :

i. $200 to grow to $497.65 in 5 years

ii. $180 to grow to $485.93 in 6 years

15 WRMAS

DISCOUNT INTEREST AND PRESENT VALUE

Present value reflects the current value of a future payment or receipt.

How much do I have to invest today to have some amount in the future?

Finding Present Values (PVs) = discounting Example You need RM400 to buy textbook next year. Earn 7% on your money. How much do you have to put today?

16 WRMAS

Formula of Present Value (PV):

or

Where;

FVn = the future value of the investment at the end of n years

n = number of years until payment is received

i = the interest rate

PV = the present value of the future sum of money

FVIF = Future value interest factor or the compound sum $1

[ 1/(1+i)n ] is also known as discounting factor

PV = FVn (PVIFi,n)

PRESENT VALUE

PV = FVn

(1+i )n

17 WRMAS

Present Value

18

Example :

What is the PV of $800 to be received 10 years from today if our discount rate is 10%.

Manually

PV = 800/(1.10)10

= $308.43

Table

PV = $800 (PVIF 10%,10yrs)

= $800 (0.3855)

= $308.40

SAME ANSWER!

WRMAS

Exercise 1 (finding PV) Pam Valenti wishes to find the present value of $1,700 that will be received 8 years from now. Pam’s opportunity cost is 8%. Exercise 2 (changing i) Find the PV of $10,000 to be received 10 years from today if our discount rate is: a) 5% b) 10% c) 20% Exercise 3 (finding n) How many years will it take for your initial investment of RM7,752 to grow to RM20,000 with a 9% interest ?

Present Value Exercise

19

i ( OR ) PV ?

n ( OR ) PV ?

WRMAS

WRMAS 20

Present Value Relationship

PV is lower if: 1. Time period is longer; and/or 2. Interest rate is higher.

ANNUITY

21

An annuity is a series of equal payments for a specified numbers of years. These cash flows can be inflows of returns earned on investments or outflows of funds invested to earn future returns.

There are 2 types of annuities*:

- An ordinary annuity is an annuity for which the cash flow

occurs at the end of each period (much more frequently in

finance)

- An annuity due is an annuity for which the cash flow occurs

at the beginning of each period.

Note: An annuity due will always be greater than an ordinary annuity because interest will compound for an additional period.

WRMAS

Ordinary Annuity-PV a) Present Value of Annuity (PVA)

• Pensions, insurance obligations, and interest owed on bonds are all annuities. To compare these three types of investments we need to know the present value (PV) of each.

Formula:

or

PVAn = PMT [1-(1+i)-n] i

PVAn = PMT (PVIFAi,n)

22 WRMAS

b) Future Value of Annuity (FVA) • Depositing or investing an equal sum of money at the end of

each year for a certain number of years and allowing it to grow.

Formula

or

FVAn = PMT (1+ i)n -1 i

FVAn = PMT (FVIFAi,n)

23 WRMAS

Ordinary Annuity-FV

FV of Annuity: Changing PMT, N & r 1. What will $5,000 deposited annually for 50 years be worth

at 7%? – FV= $2,032,644 – Contribution = 250,000 (= 5000*50)

2. Change PMT = $6,000 for 50 years at 7% – FV = 2,439,173 – Contribution= $300,000 (= 6000*50)

3. Change time = 60 years, $6,000 at 7% – FV = $4,881,122 – Contribution = 360,000 (= 6000*60)

4. Change r = 9%, 60 years, $6,000 – FV = $11,668,753 – Contribution = $360,000 (= 6000*60)

24

ANNUITY DUE • Remember-Annuity due is ordinary annuities in which all

payments have been shifted forward by one time period.

a) Future Value of Annuity Due (FVAD):

b) Present Value of Annuity Due (PVAD) formula:

FVADn = PMT (FVIFAi,n) (1+i)

25 WRMAS

PVADn = PMT (PVIFAi,n) (1+i)

Earlier, we examined this “ordinary” annuity:

Using an interest rate of 5%, we find that:

• The FVA (at 3) is $2,818.50

• The PVA (at 0) is $2,106.00

HOW ABOUT ANNUITY DUE?

• FVAD5 (annuity due) = PMT{[(1 + r)n – 1]/r}* (1 + r)

= 500(5.637)(1.06)

= $2,987.61

• PVAD0 = $2,818.80

26

0 1 2 3 …….……5

500 500 500

WRMAS

Exercise 1 Fran Abrams wishes to determine how much money she will have at the end of 5 years if he chooses annuity A that earns 7% annually and deposit $1,000 per year. Exercise 1 Branden Co., a small producer of plastic toys, wants to determine the most it should pay to purchase a particular annuity. The annuity consists a cash flows of $700 at the end of each year for 5 years. The required return is 8%. Exercise 3 Determine the answers for exercise 1 and 2 on annuity due.

Annuity Exercise

27 WRMAS

28

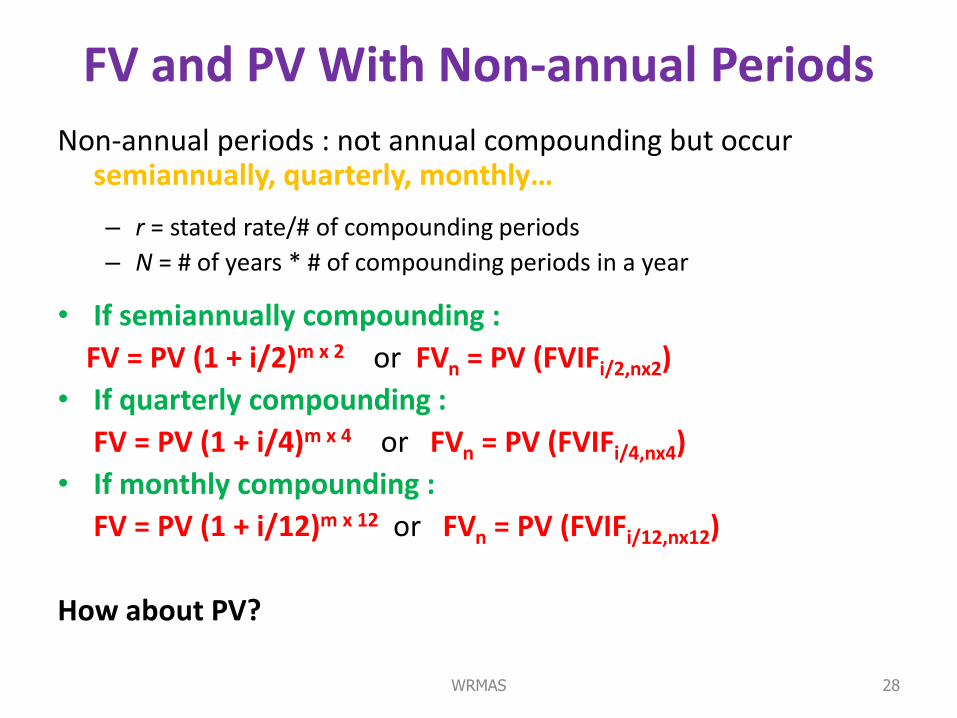

FV and PV With Non-annual Periods

Non-annual periods : not annual compounding but occur semiannually, quarterly, monthly…

– r = stated rate/# of compounding periods

– N = # of years * # of compounding periods in a year

• If semiannually compounding :

FV = PV (1 + i/2)m x 2 or FVn = PV (FVIFi/2,nx2)

• If quarterly compounding :

FV = PV (1 + i/4)m x 4 or FVn = PV (FVIFi/4,nx4)

• If monthly compounding : FV = PV (1 + i/12)m x 12 or FVn = PV (FVIFi/12,nx12)

How about PV?

WRMAS

Example 1: If you deposit $100 in an account earning 6% with semiannually compounding, how much would you have in the account after 5 years?

Manually Table FV5 = PV (1 + i/2)m x 2 FV5 = PV (FVIFi/2, nx2 )

= 100 (1 + 0.03 )10 = 100 (FVIF 3%,10)

= 100 (1.3439) = $134.39 = 100 (1.3439) = $134.39

Example 2: If you deposit $1,000 in an account earning 12% with quarterly compounding, how much would you have in the account after 5 years?

Manually Table FV5 = PV (1 + i/4)m x 4 FV5 = PV (FVIFi/4, nx4 )

= 1000 (1 + 0.03)20 = 1000 (FVIF 3%,20) = 1000 (1.8061) = $1806.11 = 1000 (1.8061) =$1806.11

Compound Interest With Non-annual Periods

29 WRMAS

Exercise-Non Annual Exercise 1 How much would you have today, if RM1,000 is being discounted at 18% semiannually for 10 years. Exercise 2 Calculate the PV of a sum of money, if RM40,000 is discounted back quarterly at 24% per annum for 10 years. Exercise 3 Paul makes a single deposit today of $400. The deposit will be invested at an interest rate of 12% per year compounded monthly. What will be the value of Paul’s account at the end of 2 years? Exercise 4

Consider a 10-year mutual fund in which payments of $100 are made at the beginning of each month. What is the amount today if the annual rate of interest is 5%?

WRMAS 30

Quoted Vs. Effective Rate • We cannot compare rates with different compounding periods.

5% compounded annually is not the same as 5% compounded quarterly.

• To make the rates comparable, we must calculate their equivalent rate at some common compounding period by using effective annual rate (EAR).

• In general, the effective rate > quoted rate whenever compounding occurs more than once per year.

WRMAS 31

Example 1 RM1 invested at 1% per month will grow to RM1.126825 (=RM1.00(1.01)12) in 1 year. Thus even though the interest rate may be quoted as 12% compounded monthly, the EAR is:

EAR = (1 + .12/12)12 – 1 = 12.6825% Example 2 Fred Moreno wishes to find the effective annual rate associated with an 8% quoted rate (r = 0.08) when interest is compounded (1) annually (m = 1); (2) semiannually (m = 2); and (3) quarterly (m = 4).

Quoted Vs. Effective Rate

WRMAS 32

PERPETUITY • A perpetuity is an annuity that continues forever.

• The present value of a perpetuity is

PV = PP

i

PV = present value of the perpetuity

PP = constant dollar amount provided by the perpetuity

i = annuity interest (or discount rate)

Example

What is the present value of $2,000 perpetuity discounted back to the present at 10% interest rate?

= 2000/.10 = $20,000

33 WRMAS

Exercise

What is the Present Value of the following :

- A $100 perpetuity discounted back to the present at 12%

- A $95 perpetuity discounted back to the present at 5%

Perpetuity Exercise

34

i ( OR ) P? $ ( OR ) PV ?

WRMAS

WRMAS 35