Embed Size (px)

Citation preview

Hyundai Card Hyundai Card is...Hyundai Card Investor Presentation 1H13

DisclaimerThese presentation materials have been prepared by Hyundai Card Co., Ltd. (“HCC or the Company”), solely for the use at this presentation and havenot been independently verified. No representations or warranties, express or implied, are made as to, and no reliance should be placed on, theaccuracy, fairness or completeness of the information presented or contained in this presentation. Neither the Company nor any of its affiliates,advisers or representatives accepts any responsibility whatsoever for any loss or damage arising from any information presented or contained in thispresentation. The information presented or contained in this presentation is current as of the date hereof and is subject to change without notice andits accuracy is not guaranteed. Neither the Company nor any of its affiliates, advisers or representatives make any undertaking to update any suchits accuracy is not guaranteed. Neither the Company nor any of its affiliates, advisers or representatives make any undertaking to update any suchinformation subsequent to the date hereof. This presentation should not be construed as legal, tax, investment or other advice.

Certain information and statements made in this presentation contain “forward-looking statements.” Such forward-looking statements canbe identified by the use of forward-looking terminology such as “anticipate,” “believe,” “considering,” “depends,” “estimate,” “expect,” “intend,” “plan,”“planning,”“planned,” “project,”“trend,” and similar expressions. All forward-looking statements are the Company’s current expectation of futureevents and are subject to a number of factors that could cause actual results to differ materially from those described in the forward-lookingstatements. Caution should be taken with respect to such statements and you should not place undue reliance on any such forward-lookingstatements.

Certain industry and market data in this presentation was obtained from various trade associations, and the Company have not verified such data withindependent sources. Accordingly, the Company make no representations as to the accuracy or completeness of that data, and such data involves risksand uncertainties and is subject to change based on various factors.

This presentation does not constitute an offer or invitation to purchase or subscribe for any shares or other securities of the Company and neither anypart of this presentation nor any information or statement contained therein shall form the basis of or be relied upon in connection with any contract orcommitment whatsoever. Any decision to purchase shares in any offering of shares of the Company should be made solely on the basis of theinformation contained in the offering document which may be published or distributed in due course in connection with any offering of shares of theCompany, if any.

The contents of this presentation may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in wholeor in part, for any purpose.

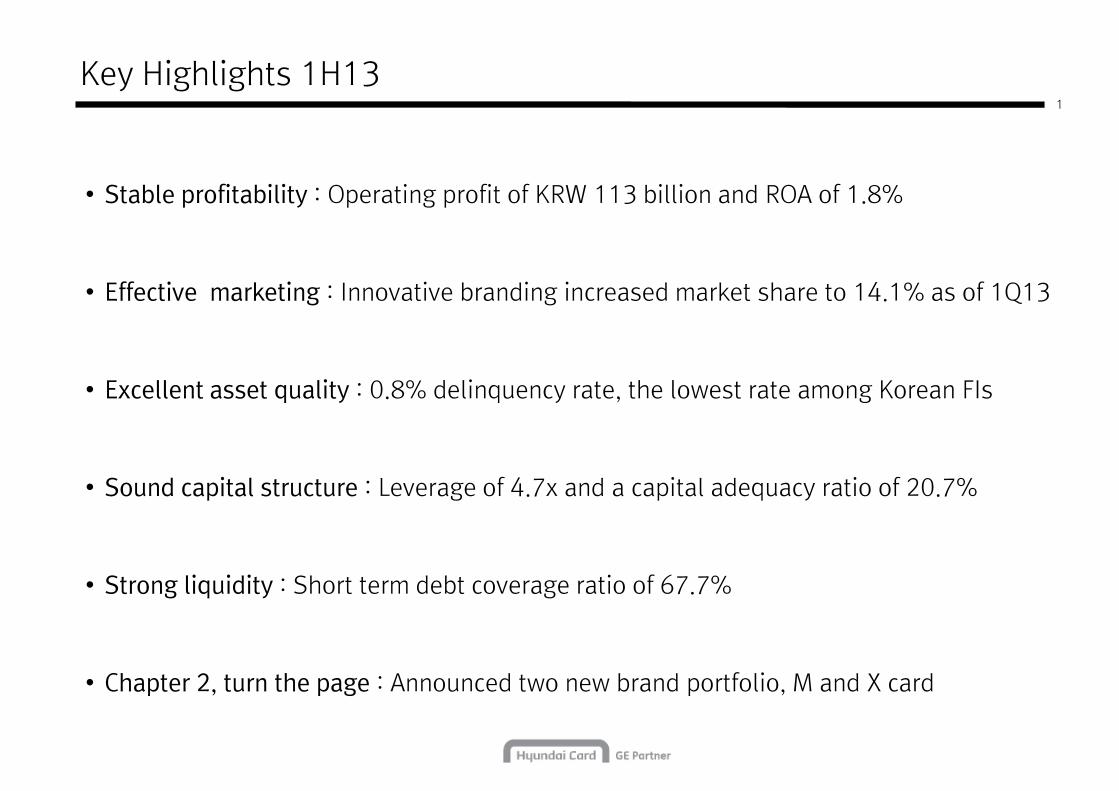

• Stable profitability : Operating profit of KRW 113 billion and ROA of 1.8%

1

Key Highlights 1H13

• Effective marketing : Innovative branding increased market share to 14.1% as of 1Q13

• Excellent asset quality : 0.8% delinquency rate, the lowest rate among Korean FIs

• Sound capital structure : Leverage of 4.7x and a capital adequacy ratio of 20.7%

• Strong liquidity : Short term debt coverage ratio of 67.7%

• Chapter 2, turn the page : Announced two new brand portfolio, M and X card

2

Resilient GDP Growth and Increasing Credit Card Usage

GDP Growth Rate & Unemployment Rate

GDP Growth Rate Unemployment Rate

Credit Card Spending & Usage Rate

Credit Card Spending (KRW Tn)

� Despite of slower GDP growth, unemployment rate has been stabilized

� Credit card usage takes up high portion of total private consumption

Credit card spending / Total private consumption

279.3 303.9

350.7

390.2

451.2

49.7%52.8%

56.8%59.6%

66.3%

6.1%

3.6%

3.5% 3.5%

3.0%3.2% 3.1%

Source: Bank of Korea, Unemployment Rate at the end of period Source: Credit Finance Association

2008 2009 2010 2011 2012

0.2%

2.0% 1.9%

2009 2010 2011 2012 1H13

3

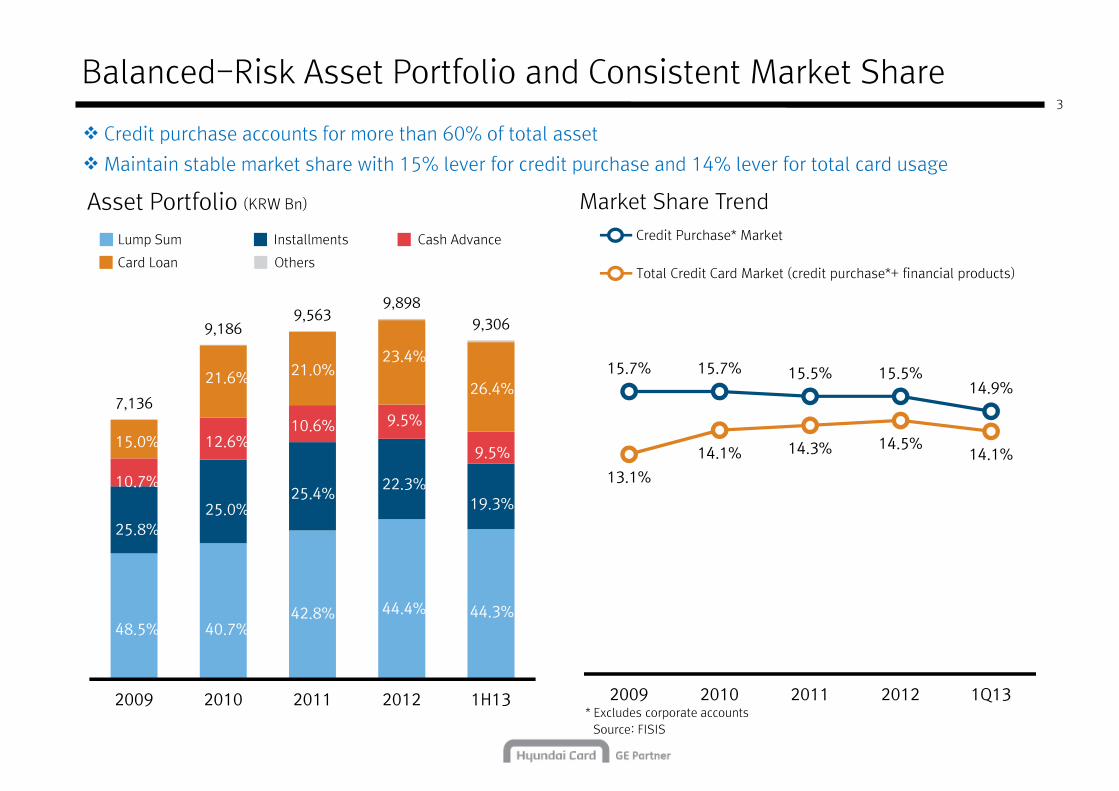

Balanced-Risk Asset Portfolio and Consistent Market Share

Asset Portfolio (KRW Bn) Market Share Trend

Lump Sum Installments Cash Advance

Card Loan Others

Credit Purchase* Market

� Credit purchase accounts for more than 60% of total asset

� Maintain stable market share with 15% lever for credit purchase and 14% lever for total card usage

Card Loan OthersTotal Credit Card Market (credit purchase*+ financial products)

7,136

9,1869,563

9,898

9,306

25.8%

10.7%

15.0%

25.0%

12.6%

21.6%

25.4%

10.6%

21.0%

22.3%

9.5%

23.4%

19.3%

9.5%

26.4%15.7% 15.7% 15.5% 15.5%

14.9%

13.1%

14.1% 14.3% 14.5%14.1%

* Excludes corporate accountsSource: FISIS

2009 2010 2011 2012 1H13

48.5%

25.8%

40.7%42.8% 44.4% 44.3%

2009 2010 2011 2012 1Q13

4

Good Profitability Underscores Strong Fundamentals

2010 2011 2012 1H12 1H13 YoY

Income Statement (KRW Bn) Return on Equity & Return on Assets

ROE ROA

17.6%

Key Highlights

Operating Revenues 2,337 2,408 2,526 1,234 1,308 6.0%

(Excluding FX effect) 2,260 2,370 2,460 1,217 1,237 1.7%

Operating expenses 1,966 2,084 2,292 1,113 1,195 7.4%

(Excluding FX effect) 1,890 2,045 2,227 1,096 1,125 2.6%

15.1%17.6%

12.6%9.0% 7.4%

3.5% 3.5%2.6% 2.0% 1.8%

2009 2010 2011 2012 1H13

Key Highlights

� Operating income was down YoY due to:

- Reduced profitability as a result of regulatory changes

- Increase in bad debt expense due to economy slowdown

� Maintained stable market share and number of card holders

Bad debt expense 185 200 203 98 115 16.9%

Operating income 371 324 233 121 113 -6.9%

Net Income 278 239 191 106 83 -21.5%

5

Excellent Asset Quality and Conservative Reserve Policy

30+ Day Delinquency Rate (%) Total Reserve VS Regulatory Requirement (KRW Bn)

Regulatory Requirement Reserve under Accounting Principles

� 30+ Delinquency rate has been slightly increased due to the slowdown in the macro economy

� Maintained conservative reserve policy which is always higher than regulatory requirement

Supplemental Reserve Total Reserve/ Regulatory Requirement

0.3% 0.4%

0.6%0.7%

0.8%

363 366 378

544

123.9% 127.7%

199.1%

157.1% 155.2%

551

2009 2010 2011 2012 1H13

114 148 190

346 355

142189 174

181

185

204

2009 2010 2011 2012 1H13

6

Leverage and Capital Adequacy Soundly Managed

Leverage Trend (KRW Bn) Capital Adequacy Ratio (KRW Bn)

Total Assets / Total Shareholders' Equity Adjusted Capital CAR

� Leverage was controlled below FSS regulation of 6X

� Capital adequacy ratio has been well controlling above the regulatory guideline of 8%

Total Assets

7,291

10,417 10,848

11,251 10,755

4.9x

6.0x

5.4x5.1x

4.7x

Total Assets / Total Shareholders' Equity

22.5%18.7% 19.6% 18.7%

20.7%

Total Assets

2009 2010 2011 2012 1H13

1,699 1,843 1,845 1,801

1,869

2009 2010 2011 2012 1H13

• Maintain the proportions of ABS and CP

under 20% and 10%, respectively

7

Well Diversified, Stable Funding Portfolio

Funding Portfolio by Product Funding Principles

ABS ABS ABS ABS 13.6%13.6%13.6%13.6%

• Maintain the average maturity ratio of

liability-to-asset at over 100%

• Contingency plans under regular review

1H13 Achievement

Bonds Bonds Bonds Bonds 83.0%83.0%83.0%83.0%

Loans Loans Loans Loans 3.4%3.4%3.4%3.4%

13.6%13.6%13.6%13.6%

• Enhance long-term funding : short-term • Funding Balance : KRW 6,586Bn

• Long-term funding : 66.3%

• Enhance long-term funding : short-term

coverage 67.7%

• Stabilize funding portfolio : CP portion less

than 5%

8

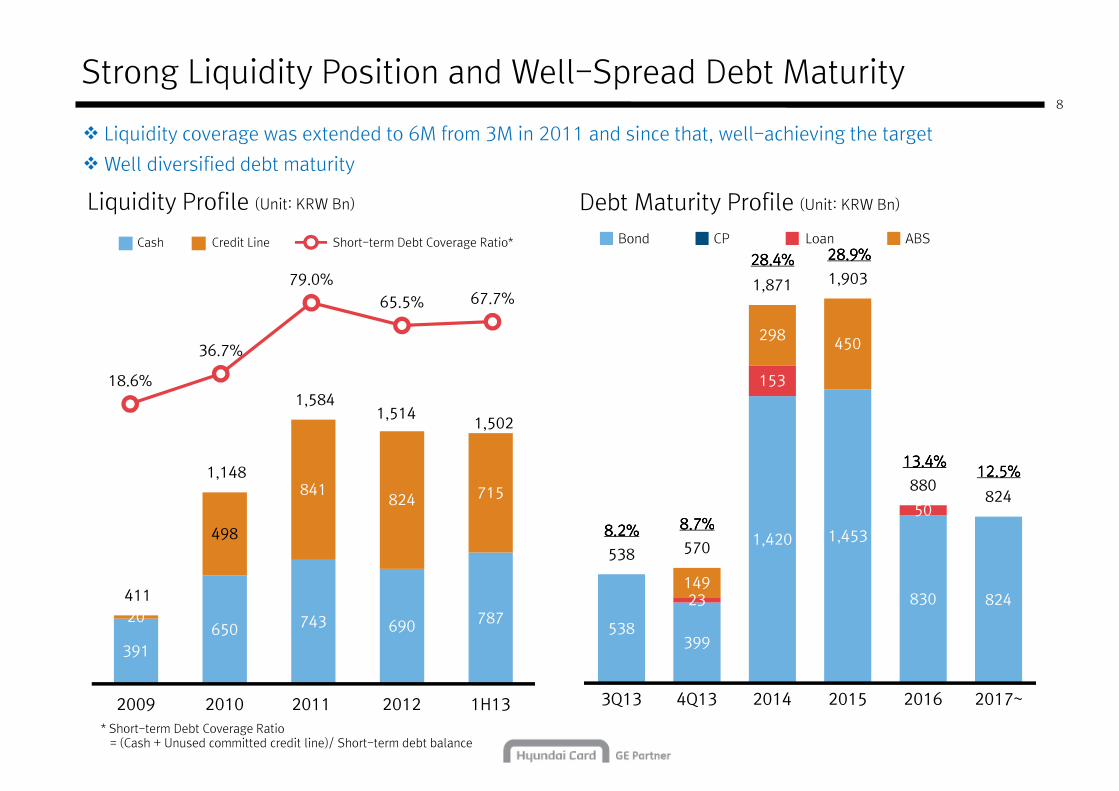

Strong Liquidity Position and Well-Spread Debt Maturity

Liquidity Profile (Unit: KRW Bn) Debt Maturity Profile (Unit: KRW Bn)

Credit LineCash Short-term Debt Coverage Ratio* CP LoanBond ABS

28.4%28.4%28.4%28.4% 28.9%28.9%28.9%28.9%

� Liquidity coverage was extended to 6M from 3M in 2011 and since that, well-achieving the target

� Well diversified debt maturity

498

841824 715

1,148

1,584 1,514

1,502

18.6%

36.7%

79.0%

65.5% 67.7%

153

50

298450

8.2%8.2%8.2%8.2% 8.7%8.7%8.7%8.7%

28.4%28.4%28.4%28.4%

13.4%13.4%13.4%13.4%12.5%12.5%12.5%12.5%

1,871 1,903

880824

* Short-term Debt Coverage Ratio= (Cash + Unused committed credit line)/ Short-term debt balance

391

650 743 690 787 20

498

411

2009 2010 2011 2012 1H13

538399

1,420 1,453

830 82423149

8.2%8.2%8.2%8.2% 8.7%8.7%8.7%8.7%

538 570

3Q13 4Q13 2014 2015 2016 2017~

Hyundai Card Hyundai Card Company OverviewHyundai Card Investor Presentation 1H13

I. Who is Hyundai Card?

9

The Premier Korean Credit Card Company

• Industry leader across key quality metrics- Excellent asset quality with the industry’s lowest delinquency rate of only 0.8%

- Strong customer loyalty with high card usage per customer

• Marketing innovations differentiate brand and drive growth- Strategic marketing program with Hyundai Motor Group

- Leadership position in super premium segment

• Seven-year-long partnership between two global leaders:

Hyundai Motor Group and GE Capital - Strong governance with GE Capital's active involvement in management & daily operations- Strong governance with GE Capital's active involvement in management & daily operations

- Joint promotions with Hyundai Motor Group

• Strong credit profile based on robust fundamentals- International – Fitch: BBB / S&P: BBB

- Domestic – AA+

- Innovative “Point Programs”

- Stable & solid operational base

- Extensive sales network

Shareholder Financial & Operational Support

Relationship with Shareholders GE Capital’s Financial Support

2013201320132013 - Total Investment to date : U$544mm(As of 2Q13 end)

10

- GE Capital increases paid in capital by KRW 165bn

- 2006 ~ 2008Exercising of Warrants(Additional equity investment)

- GE Capital provides U$200mm back-up credit-line

54.0%- Extensive sales network

- Powerful financing arm

- Effective marketing tool

- Most successful joint venture

- Sole consumer finance window in Korea

2010201020102010

2008200820082008

2006200620062006

2012201220122012 - Total Investment to date : U$725mm

- GE Capital acquires KRW 313bn equity interest in HCC

- Establishment of joint venturewith GE Capital43.3% - Advanced knowledge of risk

management

- Financial support

- Active involvement in management and daily operations

2005200520052005

- GE Capital purchases KRW 200bn subordinated bond

11

Management Strategy

• Continuous product and service innovation and profit improvement to

overcome regulatory changes and intensifying market competition

• Enhance customer value through spending stimulation and increasing

customer loyalty

• Achieve sustainable growth through prioritizing risk management and

a strong capital structure

12

Committed to Transparent Corporate Governance

Board of DirectorsBoard of DirectorsBoard of DirectorsBoard of Directors

• HMC 5 : GECC 4 : Outside directors 3

• GECC has veto rights

Risk Control CommitteeRisk Control CommitteeRisk Control CommitteeRisk Control Committee

• Member : 5 from HMC, 5 from GECC

• Frequency : Monthly

• Function

-Determination of risk indicator levels and appropriate course of actions in

Executive Finance CommitteeExecutive Finance CommitteeExecutive Finance CommitteeExecutive Finance Committee

• Member : 4 from HMC, 3 from GECC

• Frequency : Monthly

• Function

-Approval of various operating expenses, Capex, business and

Compliance Review BoardCompliance Review BoardCompliance Review BoardCompliance Review Board

• Member : 9 from HMC, 7 from GECC

• Frequency : Quarterly

• Function

-Formulation and execution of compliance strategy, schemes, and and appropriate course of actions in

respect thereofexpenses, Capex, business and funding plans

compliance strategy, schemes, and improvements

• C-Suite executives: Vice President, Deputy CFO, Deputy CRO, Deputy CMO, Controller

• Working level : GE employees also involved in day-to-day operations

• Transfer of advanced knowledge in various functions through best practice sharing program

GEPresence

13

Business Area Features

Product Overview & Market Share

Market Share Trend

Total Credit Card Market (credit purchase*+ financial products)

Credit Purchase* Market

Credit Purchase

Lump sum• Single-payment purchases

• Repaid on a monthly billing cycle

Installment• Multiple-payment purchases

• Payment period of 2-12 months

Card loan• Unsecured loans to cardholders

11.8%

12.8%

13.8%

15.7% 15.7% 15.5% 15.5%14.9%

10.1%

11.2%

13.1%

14.1% 14.3% 14.5%14.1%

Financial Products

Card loan• 3 – 36 month maturity

Cash advance• Cash withdrawal

• Lump sum or installment payback

* Excludes corporate accountsSource: FISIS

8.8%

10.1%

2006 2007 2008 2009 2010 2011 2012 1Q13

II. Premium Brand & Marketing

14

One of Korea’s Most Well Recognized & Respected Brands

Strong Brand Drives Higher Customer Loyalty Innovative Branding Activities

Strategy:

Innovative Experience

- Liquid metal card plates

- British Rock Sound Identity - Pop-up stores

- Super event series

Emotional Emotional Emotional Emotional CommunicationCommunicationCommunicationCommunication

• Customizable card materials & design

• Music platform promoting independent artists

Innovative Experience

Classic Dynamic

*88.1% (Source: TNS RI Research 2011)

• Restaurant review Smartphone application

• ‘Pop-up stores’ in style-focused locations

Result:

- Well respected, trendsetting image with high customer awareness*

- Higher customer loyalty & spending, evidenced through average card usage per customer

15

Chapter 2 : For the Next New 10 years

Two Track Brand Portfolio Two Key Benefit

Point • Simple Card Product- Simplify Product portfolio

Cash Back

- Simplify Product portfolio- Concentrate on saving Point

• Differentiated Service - Selecting card product by usage amount (M1~M3)

Cash Back• Discount through cash-back system

- Cash-back from every merchandizes

• Differentated Service- Selecting card product by usage amount (X1~X2)

III. Macro & Industry Environment

16

Korea’s Macro Environment

GDP Growth Rate & Consumer Price Index

GDP Growth Rate Consumer Price Index

Credit Card Spending & Usage Rate

Credit Card Spending (KRW Tn)

Credit card spending / Total private consumption66.3%

279.3 303.9

350.7

390.2

451.2

49.7%52.8%

56.8%59.6%

66.3%

6.1%

3.6%

2.8% 3.0%

4.0%

2.2%

1.3%

Source: Bank of Korea Source: Credit Finance Association

2008 2009 2010 2011 2012

0.2%

2.0% 1.9%

2009 2010 2011 2012 1H13

Korean Credit Card Market Features17

• Conservative lending environment - Low usage of revolving credit card products, as full payment of monthly balance

preferredpreferred

• Strong credit infrastructure - Well developed credit bureau system provides a quantitative customer credit score

based on all previous credit history

• Cash-less society - Ubiquitous acceptance of credit cards, high popularity of online shopping, and tax

incentives for credit card use

• Strict government oversight- Regulations governing new origination practices and customer cash advance limits

18

Korea Credit Card Industry: Then & Now

Combined Asset portfolio Total Asset Quality (30+ Day Delinquency Rate)

Credit Purchase Financial Products

Combined Capital Adequacy Ratio Regulatory & Infrastructure Changes:

- Credit bureau system established

35.1%65.2%

64.9%34.8%

2003 1Q13

28.3%

2.1%

2003 1Q13

Source: FSS

- Credit bureau system established

- Marketing regulations restricting new originations

- Companies must maintain capital adequacy ratio of above 8%

- Leverage limit of 6x (Dec. 2012)

-5.5%

26.7%

2003 1Q13

IV. Asset Portfolio & Performance

19

Balanced Asset Portfolio of Credit and Financial Products

Asset Portfolio (Unit: KRW Bn)

Lump Sum Installments Cash Advance

Card Loan Others

9,1869,563

9,898

9,306

3,508

4,507

5,618

7,136

9,186 9,306

28.9%

12.6%

14.5%

25.8%

10.7%

15.0%

25.0%

12.6%

21.6%

25.4%

10.6%

21.0%

12.3%

13.5%

7.9%

22.3%

9.5%

23.4%

19.3%

9.5%

26.4%

2006200620062006 2007200720072007 2008200820082008 2009200920092009 2010201020102010 2011201120112011 2012201220122012 1H131H131H131H13

44.0%

48.5% 40.7%42.8%

50.6%

23.5%

58.5%

19.0%11.9%

44.4% 44.3%

Best in Class Risk Management

Strong governance for risk monitoring Examples of pre-emptive risk management

Category Recent actions taken• Risk Control Committee (RCC)

– Decision making for most supreme risk– Review portfolio risk performance

20

Cash Advance

Lowered cash advance limits for lower credit quality customers

Card LoanTightened underwriting policy for heavy debtors

• Systematic New Product Risk Analysis

- Two-stage RCC approval process - Pre-launch new product introduction and credit

review point assessment

• Risk Appetite Management

– Establish guidelines for portfolio / asset quality – Determine risk management strategy per product

Credit Purchase

Tightened underwriting policy for revolving products and new originations

• Portfolio Quality Review

– Monitoring of main risk indices– Follow-up on effects of credit policy changes

• Stress Test & Contingency Planning

– Scenario analysis based on economic forecasting– Prepare action plans per contingency stage

Historical Asset Quality

30+ Day Delinquency Rate (%)

21

2.2%

0.4%

0.7%

0.4%0.6%

0.7%0.8%

0.4%0.3%

0.4%

2006200620062006 2007200720072007 2008200820082008 2009200920092009 2010201020102010 2011201120112011 2012201220122012 1H131H131H131H13

22

Historical Reserve & FSS Requirement Coverage Ratio

Total Reserve VS Regulatory Requirement (KRW Bn)

Regulatory Requirement Reserve under Accounting Principles Supplemental Reserve Total Reserve/ Regulatory Requirement

178.1%200.4% 199.1%

204

363 366

178.1%

143.3%123.9% 127.7%

157.1% 155.2%

378

544 551

K-GAAP K-IFRS

89 52

94 114 148 190

346 355

158 104 135

142 189 174 181 185

2009200920092009 2010201020102010 2011201120112011 201220122012201220082008200820082006200620062006 2007200720072007 1H131H131H131H13

Sustainable Growth Based on Strong Fundamentals

2008 2009 2010 2011 2012 1H12 1H13 YoY

Income Statement (KRW Bn)

23

KKKK----IFRSIFRSIFRSIFRSKKKK----GAAPGAAPGAAPGAAP

Operating Revenues 1,594 1,841 2,337 2,408 2,526 1,234 1,308 6.0%

(excl. FX effect) 1,444 1,795 2,260 2,370 2,460 1,217 1,237 1.7%

Operating Expenses 1,337 1,555 1,966 2,084 2,292 1,113 1,195 7.4%

(excl. FX effect) 1,186 1,509 1,890 2,045 2,227 1,096 1,125 2.6%

Card expenses 506 730 863 924 1,044 530 520 -1.9%

Interest expenses 187 221 319 357 343 173 157 -9.4%

SG&A Expenses 367 398 484 538 610 280 296 5.4%

PPOP 357 441 570 525 436 221 228 3.0%

Bad Debt expenses 103 113 185 200 203 98 115 16.9%

Provision for unused Credit Line

-3 42 14 1 0 2 0 -

Operating Income 258 286 371 324 233 121 113 -6.9%

ROA 3.9% 3.5% 3.5% 2.6% 2.0% 2.2% 1.8%

ROE 16.7% 15.1% 17.6% 12.6% 9.0% 10.2% 7.4%

Income before Tax 272 295 371 324 233 121 114 -6.4%

Net Income 202 213 278 239 191 106 83 -21.5%

V. Capitalization, Funding & Liquidity

Capital Adequacy Ratio (Unit: KRW Bn)

24

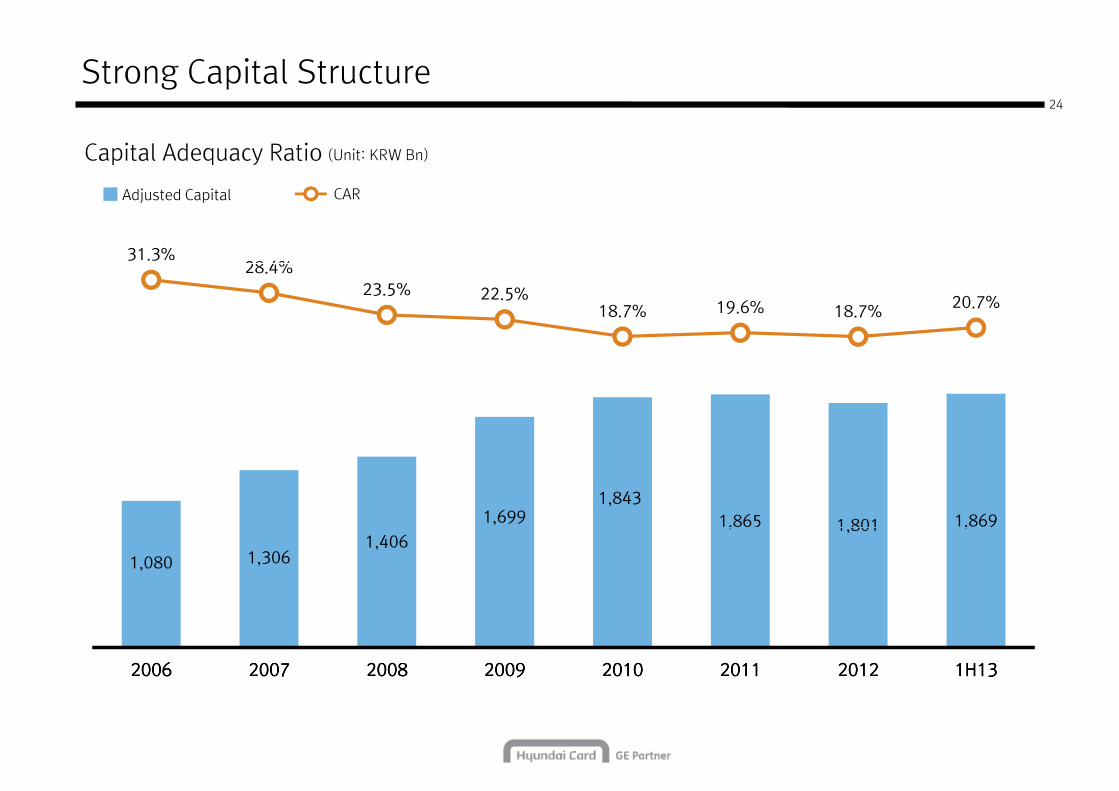

Strong Capital Structure

Adjusted Capital CAR

31.3%28.4%

1,699 1,843

1,865 1,801 1,869

28.4%23.5% 22.5%

18.7% 19.6% 18.7% 20.7%

1,080 1,306 1,406

1,865 1,801 1,869

2006200620062006 2007200720072007 2008200820082008 2009200920092009 2010201020102010 2011201120112011 2012201220122012 1H131H131H131H13

Well Controlled Leverage

Leverage Trend

Total Assets / Total Shareholders' Equity Managed Borrowings / Total Shareholders' Equity

25

12.3x12.3x

4.1x4.1x

4.6x 4.9x

6.0x5.4x

5.1x4.7x

11.3x

4.4x

2.6x 2.6x3.2x

3.5x

4.4x

3.5x3.2x

2.9x

2005200520052005 2006200620062006 2007200720072007 2008200820082008 2009200920092009 2010201020102010 2011201120112011 2012201220122012 1H131H131H131H13

Diversification of Funding Portfolio over Time

Managed Borrowings (KRW Bn)

26

Bond-domestic Bond-overseas ABS-domestic ABS-overseas Bank loans CP

2,199

2,933

3,980

5,165

7,197 7,067 7,073 6,586

80.2%

12.7%1.9%

14.8% 10.1%

14.1%

8.3%

7.7%

11.0%6.4%

11.0%

73.2%

4.6%

9.2%

10.1%

83.6%

6.9%

6.3%

4.9%

82.7%

13.6%

3.4%

%%%% of LT of LT of LT of LT FundingFundingFundingFunding 50.5%50.5%50.5%50.5% 62.6%62.6%62.6%62.6% 63.1%63.1%63.1%63.1% 57.3%57.3%57.3%57.3% 56.5%56.5%56.5%56.5% 71.6%71.6%71.6%71.6% 67.3%67.3%67.3%67.3% 66.3%66.3%66.3%66.3%

2,199

2006200620062006 2007200720072007 2008200820082008 2009200920092009 2010201020102010 2011201120112011 2012201220122012 1H131H131H131H13

59.4%

15.9%9.3%

47.3%

19.5%

14.8%

13.6%

49.6%

15.1%

61.8%

27

Substantial Improvement in Liquidity Position

Liquidity Profile (KRW Bn)

Credit LineCash Short-term Debt Coverage Ratio* 79.0%

65.5% 67.7%

498

841824 715

1,148

1,5841,514 1,50213.1%

27.3%32.7%

18.6%

36.7%

* Short-term Debt Coverage Ratio= (Cash + Unused committed credit line)/ Short-term debt balance

143 149360 391

650 743 690787

150

120 20

143

299

480411

2006 2007 2008 2009 2010 2011 2012 1H13

Investor Relations Contacts

Jungsang Kim, Head of Investor RelationsPhone +82 2 2167 [email protected]

Minchul Seo, Deputy General Manager of Investor RelationsPhone +82 2 2167 [email protected]

Suh ye Choi, Manager of Investor RelationsPhone +82 2 2167 7541

Justin Lee, Manager of Investor RelationsPhone +82 2 2167 8082

http://ir.hyundaicard.com/

Phone +82 2 2167 [email protected]

Phone +82 2 2167 [email protected]

Jay Moon, Assistant Manager of Investor RelationsPhone +82 2 2167 [email protected]

Hyunyoung Jang, Assistant Manager of Investor RelationsPhone +82 2 2167 [email protected]