Year End Review November 3, 2011

Tim Guertin President and CEO

Varian’s Growth – The Last 5 Years

0

500

1000

1500

2000

2500

3000

3500

2006 2007 2008 2009 2010 2011

Net OrdersRevenuesOps Earnings

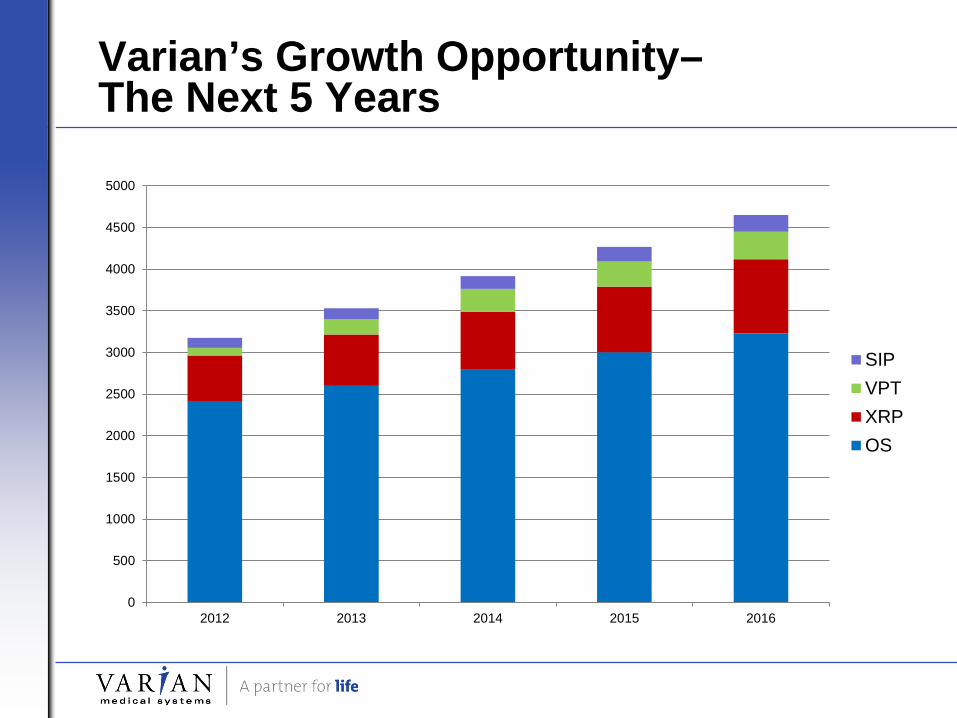

Varian’s Growth Opportunity– The Next 5 Years

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2012 2013 2014 2015 2016

SIPVPTXRPOS

Fiscal 2012 Outlook (As of end of Fourth Quarter, Fiscal 2011)

Fiscal Year 2012

Revenues growth estimated at ~ 9% to 11%

EPS estimated at ~ $3.92 to $4.02

First Quarter, FY2012

Revenues growth estimated at ~ 8% to 9%

EPS estimated at ~ $0.74 to $0.75

Varian updates its outlook once per quarter when it reports financial results. The outlook is for Continuing Operations.

Agenda

FY2011 Financial Review Elisha Finney- SrVP and CFO

X-Ray Products Robert Kluge- SrVP/President X-ray Products

Emerging Businesses Lester Boeh – VP, Emerging Businesses

Oncology Systems Dow Wilson – Executive VP/COO

Q&A

FY2011 Financial Review Elisha Finney – Sr.VP and CFO

VMS FY11 Profile

Orders: $2.9 B

Sales: $2.6 B

EPS: $3.44

Operating Earnings % 23%

Employees: 5,707

NYSE Symbol: VAR

Note: The results exclude discontinued operations.

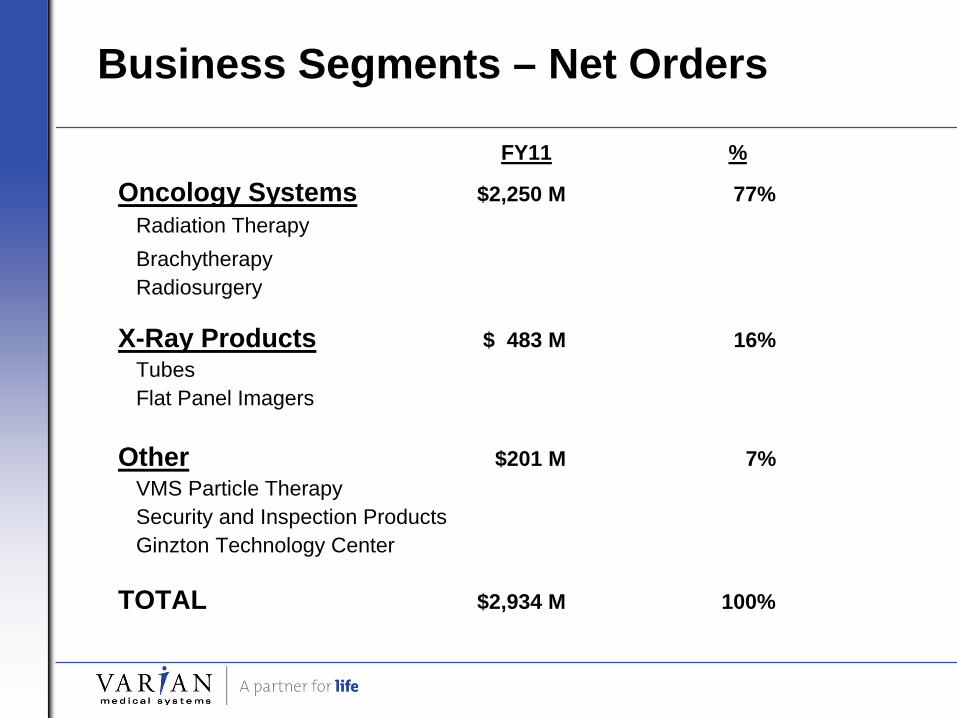

Business Segments – Net Orders

FY11 %

Oncology Systems $2,250 M 77% Radiation Therapy Brachytherapy Radiosurgery

X-Ray Products $ 483 M 16% Tubes Flat Panel Imagers Other $201 M 7% VMS Particle Therapy Security and Inspection Products Ginzton Technology Center TOTAL $2,934 M 100%

Oncology Systems

Q4 FY11 Q4 FY11 YTD

Net Orders 717 9% 2,249 8%

Revenues 549 7% 2,022 9%

Gross Margin 45% 2 pts 45% Flat

R&D 29 113

SG&A 78 297

Op Earnings 139 10% 507 10%

ROS 25% 1 pt 25% Flat

Headcount 4,088

Note: Dollars in millions.

X-Ray Products

Q4 FY11 Q4 FY11 YTD

Net Orders 126 13% 483 15%

Revenues 119 11% 469 16%

Gross Margin 41% Flat 41% 1 pt

R&D 8 26

SG&A 11 49

Op Earnings 30 7% 118 18%

ROS 25% (1 pt) 25% Flat

Headcount 776

Note: Dollars in millions.

Fourth Quarter 2011 Results

VMS OS XRP Other

Net Orders

968 25% 717 9% 126 13% 124 1534%

Revenues 719 10% 549 7% 119 11% 51 53%

Gross Margin 42% 45% 41% 10%

R&D 44

SG&A 97

Op Earnings 160 22% ROS (+ 7%)

Interest Income 0.1

EPS $0.95 (116M diluted shares) Note: (1) Dollars in millions, except per share amounts. (2) The operating results for the Other segment and Total VMS exclude discontinued operations.

FY11 Results

VMS OS XRP Other

Net Orders (1)

2,934 15% 2,249 8% 483 15% 201 227%

Revenues 2,597 10% 2,022 9% 469 16% 106 16%

Gross Margin 44% 45% 41% 24%

R&D 171

SG&A 377

Op Earnings 588 23% ROS (+ 10%)

Interest Income 0.3

EPS $3.44 (119M diluted shares) Note: (1) Q4 FY10 YTD net orders for Total VMS and the Other segment excludes $62M for the cancellation of a proton therapy order. (2) Including the proton order cancellation in the year ago period,Q4 FY11 YTD net orders would be up 18% for Total VMS and up $202M for the Other segment. (3) Dollars in millions, except per share amounts. (4) The operating results for the Other segment and Total VMS exclude discontinued operations.

Backlog $2,530M (As of 09/30/11)

0

500

1000

1500

2000

2500

3000

FY 2008 FY 2009 FY 2010 FY 2011

Q1Q2Q3Q4

Q4 FY11 Balance Sheet / Cash Flow

Conservative balance sheet $564M cash and cash equivalents $19M short-term investment $198M total debt $1,244M stockholders’ equity

*DSO 80 days - down 2 days from year ago quarter - down 1 days from prior quarter

Cash Flow $146M cash flow from operations $181M from short-term borrowings Spent $267M to repurchase 4.8M shares in Q411 including an accelerated buyback of 3.8M shares

*Days Sales Outstanding

X-Ray Products Robert Kluge – Sr. VP and President X-Ray Products

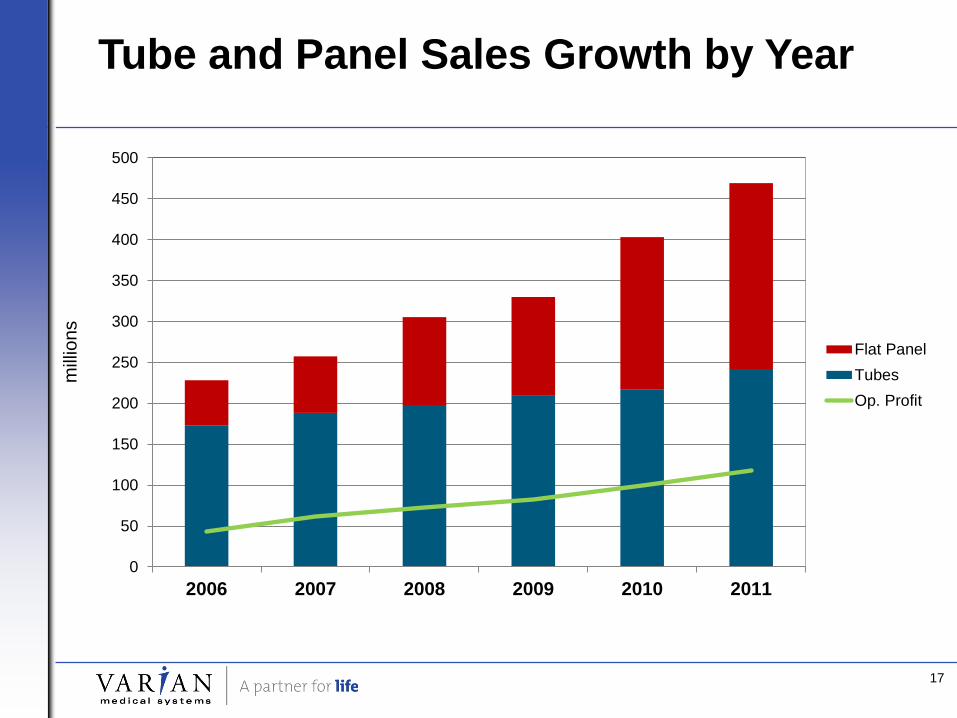

Tube and Panel Sales Growth by Year m

illio

ns

0

50

100

150

200

250

300

350

400

450

500

2006 2007 2008 2009 2010 2011

Flat PanelTubesOp. Profit

17

X-Ray Product Growth Drivers

Industry Conversion Transition to Digital Imaging DR and CR Imaging is replacing Film

Varian is well positioned from a Technology and Product

Cost Perspective New X-ray Tube Opportunities to Support Digital Imaging

Varian is by far the STRONGEST Independent Supplier

18

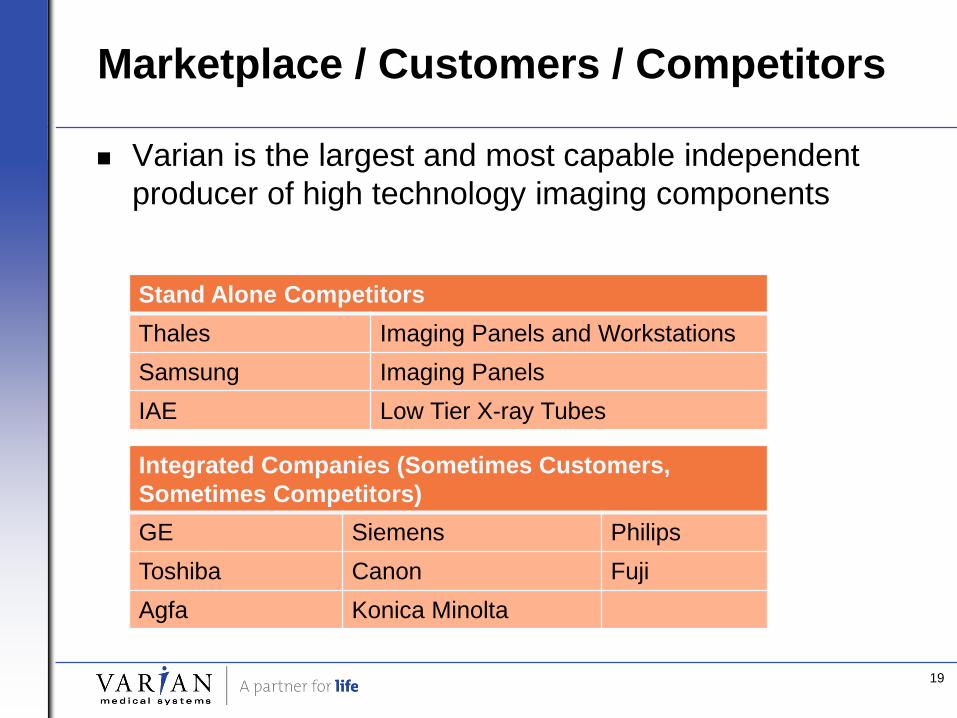

Marketplace / Customers / Competitors

Varian is the largest and most capable independent producer of high technology imaging components

Stand Alone Competitors Thales Imaging Panels and Workstations Samsung Imaging Panels IAE Low Tier X-ray Tubes

Integrated Companies (Sometimes Customers, Sometimes Competitors) GE Siemens Philips Toshiba Canon Fuji Agfa Konica Minolta

19

XRP FY 11 Highlights

Sales Growth High Tier CT X-ray Tubes continued to grow

Mammo tubes grew (added a major OEM customer)

Radiographic Imaging Panels grew rapidly

Varian - largest and most capable supplier of high tier imaging components

20

XRP FY 11 Highlights

New Products … FY11 was a year of Product Development New High Tier CT tubes

New Mammography tubes to support advanced applications

New Generation Radiographic Panel (including wireless)

Next Generation Cone Beam Imaging Panel

Mammography Imaging Panel

21

New X-Ray Tube Solutions -

PaxPower™ - M 1500 Mammography Tube Designed for advanced mammographic applications Space efficient Ultra high performance

PaxPower™ - FP 1000 CT Tube More Uniform Image Over Entire Field Beam Optimized for Flat Panel Detectors High Heat Dissipation/Lighter Weight

PaxPower™ - FP 2250/5300 Special Procedures Tube Space efficient for interventional angiography in OR, ambulatory

surgery or EP Lab

22

Flat Panel Detectors

Dynamic Panels Cardiology Angiography, DSA Cone Beam CT Surgical C-Arms Oncology

IGRT / Patient Positioning

Dynamic Panels 2020+

1313 4030E 4030CB

3030+

2520E / 2520V

2520D

23

New Mammography Detector

High resolution 83 µm pixel matrix

Environmentally stable amorphous silicon (aSi)

Variable frame rate for advanced applications

Panel to edge proximity for chest wall visualization

3024M

24

New 4336 Wireless Panel

“CR” cassette-size FPD

Designed for Portable DR

Light weight: 3.8kgs.

High Resolution: 3.6 lp/mm

PaxScan 4336 Wireless Panel

25

New Flat Panel Detectors

Designed for large field of view Cardiology, Angiography, DSA Cone Beam CT High resolution: 3.6 lp/mm

PaxScan 4343 Dynamic Panel

26

XRP Outlook

FY12 looks strong … New Products should support growth Family of Diagnostic X-ray Tube to enhance Flat Panel Imager

Performance

First entry into Mammo Panel Market

New High Tier Fluoro Panel

New Wireless RAD Imager

New High Tier RAD imager (Tomo & Dual Energy Capability)

27

Emerging Businesses Lester Boeh – Vice President

Security & Inspection Products

Security & Inspection Products

Market leading provider of high-energy security imaging Components: Linear accelerators, detectors, software, service

Systems: IntellX

Customers include all major systems integrators Components: Rapiscan, Smiths, AS&E, several regional players

Systems: US Customs & Border Protection, Rapiscan

End-users include customs and defense departments

~$100M annual business Market Drivers: Terrorism, Global Instability, Tax Revenue

80% of VAR’s security business is ex-US

Varian Strengths

Fast, automated materials discrimination Identify the most material classes within containers quickly and

reliably – organic, inorganic, metals, and high-density materials Recent expansion into mobile platforms

Lower priced, compact and reliable x-ray sources to enable low-cost, high performance, mobile platforms

Varian’s R&D and infrastructure investments IP: more than 50 active imaging and security patents

Global support and distribution network

Security & Inspection Products FY-11 Highlights

$21M award from US Customs for IntellX3 Cargo screening systems

Successfully completed all vendor testing on next

generation system

Demonstrated expanded material discrimination

capability by identifying material type in thin materials

Deployed dual-view imaging systems in the Middle

East for a high-throughput car scanner (100 cars/hour)

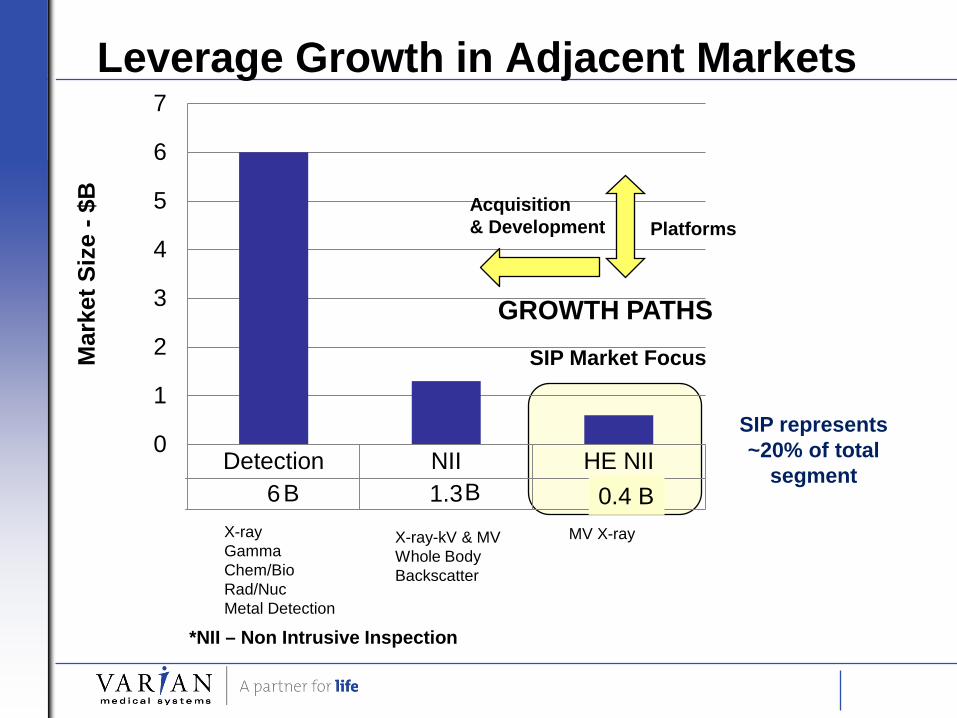

Leverage Growth in Adjacent Markets

X-ray Gamma Chem/Bio Rad/Nuc Metal Detection

X-ray-kV & MV Whole Body Backscatter

MV X-ray

SIP Market Focus

SIP represents ~20% of total

segment B B B

Detection NII HE NIISeries1 6 1.3 0.6

0

1

2

3

4

5

6

7M

arke

t Siz

e - $

B

GROWTH PATHS

Acquisition & Development Platforms

0.4 B

*NII – Non Intrusive Inspection

Going Smaller and Portable

Mi6 Cx1

First Generation MX1 Next Gen. in Development 20 Units Shipped Highest Volume

Expanding Market Opportunity Through Lower Price Point and Smaller Package

Cx1: $250K Mi6: $675K

Smaller Is What’s Big

Smaller, lower cost, mobile, “source in a box” ($250K vs. $400K)

Lower cost platform, good throughput, high energy performance: Higher unit potential at borders, temporary checkpoints, and defense

Rapiscan Portal

Improved Material Discrimination Performance

Identify Material Types behind objects

Identify Material

Types as a function

of density

Particle Therapy

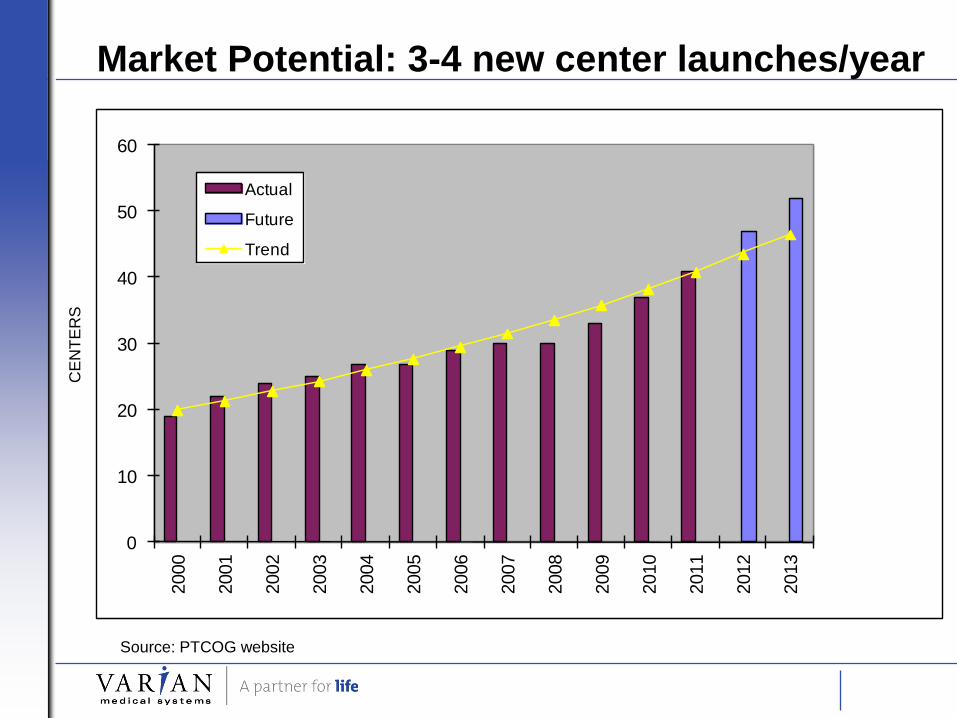

Market Potential: 3-4 new center launches/year

0

10

20

30

40

50

60

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Actual

Future

Trend

CE

NTE

RS

Source: PTCOG website

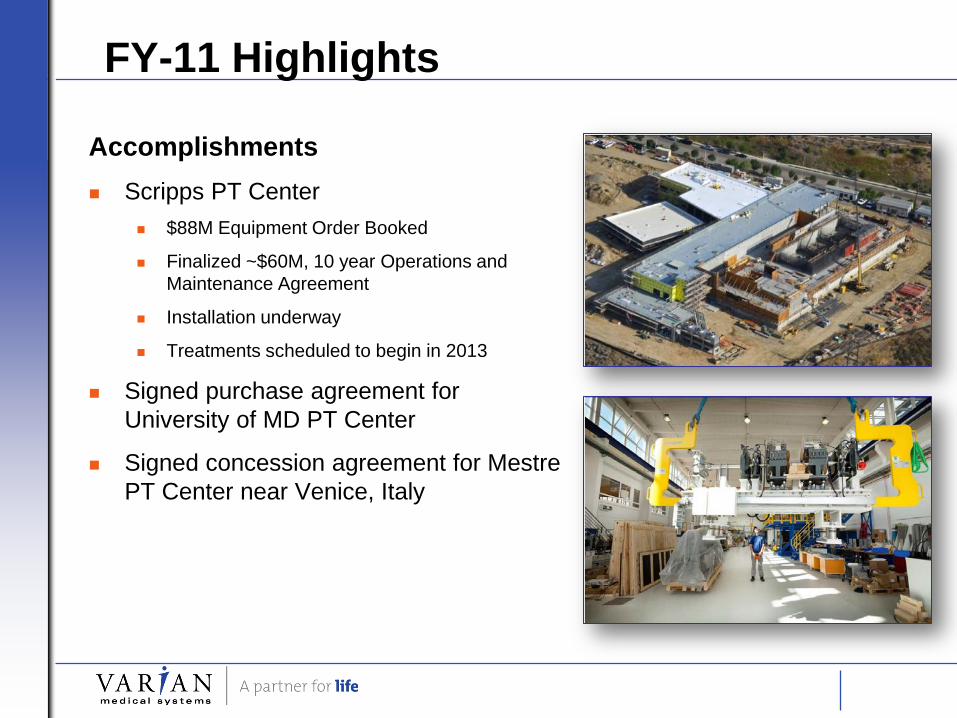

FY-11 Highlights

Accomplishments Scripps PT Center

$88M Equipment Order Booked

Finalized ~$60M, 10 year Operations and Maintenance Agreement

Installation underway

Treatments scheduled to begin in 2013

Signed purchase agreement for University of MD PT Center

Signed concession agreement for Mestre PT Center near Venice, Italy

FY-11 Highlights

Accomplishments First cyclotron completed, tested & shipped

Second cyclotron in the assembly phase

FDA 510(k) in Jan. ‘11, CE since FY-09

Gantry test facility constructed

Making progress on implementing RT workflow capabilities into PT In-room imaging

Patient motion management

Clinical workflow

New industrial design Consistent with TrueBeam family

Common User Interface

Cyclotron Installation Oct 28, 2011

Cyclotron Installation Oct 28, 2011

Addressing Market Needs

Solutions Provider Survey and focus group results indicate:

A strong desire for an integrated solution from a single provider

Advanced treatment delivery is required for success now and in the future Beyond Intensity Modulated Proton Therapy

(IMPT)

Image Guidance

Motion management

Ability to adopt and integrate future capabilities is critical

Varian has tremendous experience in advanced technology development and delivery in cancer therapy

R&D activities targeted at two objectives Superior Quality of Care

Reducing integral dose and treatment margins

Advanced imaging and motion management capabilities

Improved user environment

Making Proton Therapy economically viable $50M, 2-Room System

Improved Clinical Worlkfow, Higher throughput

Material and process development

ProBeam Roadmap

Oncology Systems Dow Wilson – Exec. VP, Chief Operation Officer

Innovation

Globalization

Services

Oncology Systems

FY2011 Varian Highlights

• Orders grew 8% in FY2011, outgrowing the market by 3% • NA grew 5%, outpaced the NA market by 3% • Int’l grew 11%, outpaced the Int’l market by 4%

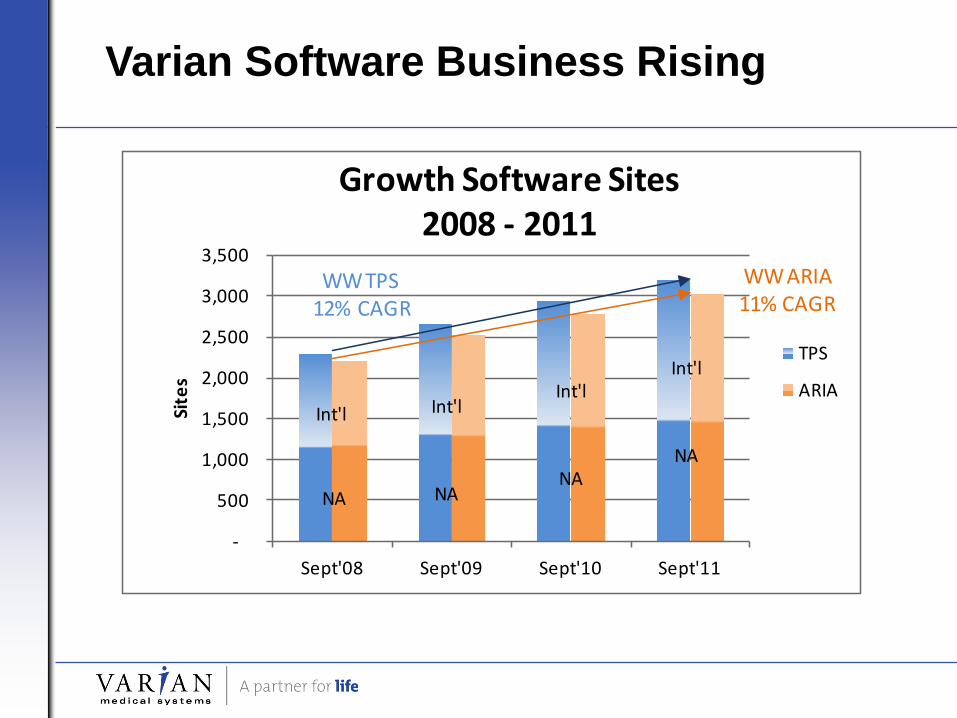

• Software sites grew by double digits from 2008 – 2011

• Eclipse Treatment Planning - 12% • ARIA Oncology Informatics - 11%

• Service grew in mid-teens

• Leveraged growing installed base

~380 orders

~145 installs

~70% of USA orders

~ 40% of WW orders

TrueBeam 1.5 launched

TrueBeam… Lots of Big Wins

>2000 orders

>$300M booked Gated RapidArc

launched

Est. >20,000 patients treated

RapidArc… Going Strong

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Sept'08 Sept'09 Sept'10 Sept'11

Site

sGrowth Software Sites

2008 - 2011

TPS

ARIA

WW TPS12% CAGR

WW ARIA 11% CAGR

Int'l

NA

Int'l

NA

Int'l

NA

Int'l

NA

Varian Software Business Rising

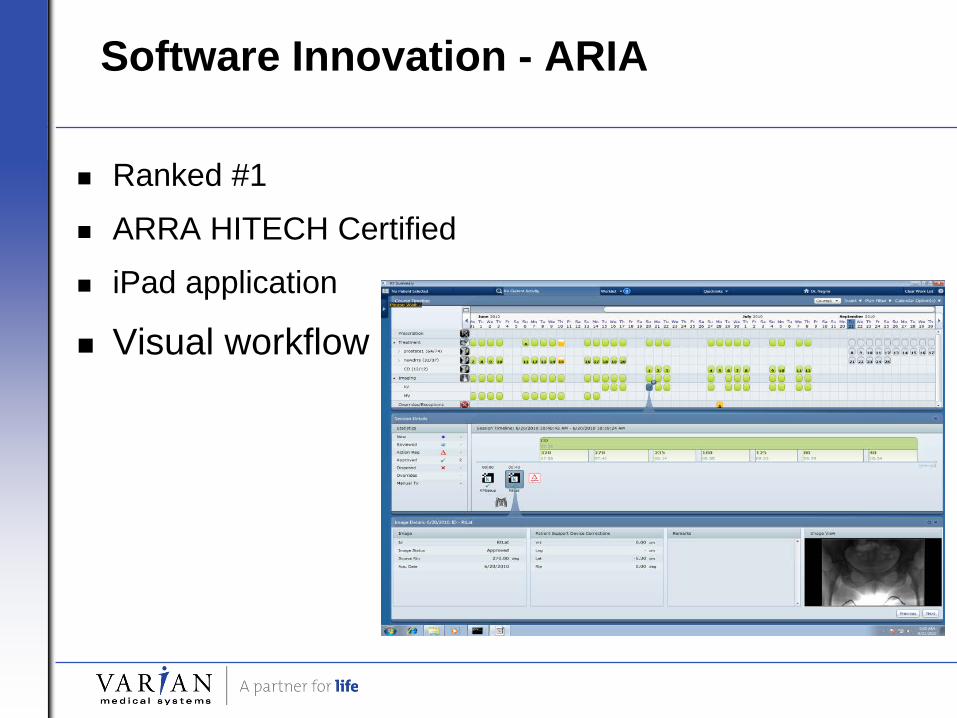

Software Innovation - ARIA

Ranked #1

ARRA HITECH Certified

iPad application

Visual workflow

Software Innovation – Eclipse

• Faster, easier planning

Varian Linac Base Expanding

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Sept'08 Sept'09 Sept'10 Sept'11

Lina

csGrowth Linac Installed Base

2008 - 2011WW Linac Base

5% CAGR

Int'l Int'l Int'l Int'l

NA NA NANA

• Int’l markets growing fastest; developed markets replacing, upgrading units • Expanding base is platform for growth in service and software

Clinical Needs Driving Product Portfolio

2005 2011

Clinac LE

Clinac EX Clinac IX

Trilogy

TrueBeam STX

Clinac LE

Clinac CX

Clinac IX

Trilogy

NTX

TrueBeam

Unique

Clinac EX

~$1M

~$3M Needs Radiosurgery capability Faster dose delivery Motion management Image guidance Better workflow Better patient experience Greater access Lower cost/treatment

Includes RapidArc capability

The Next 5 Years

Disease site solutions • Lung

• Liver

• Prostate

• Breast

Lung Cancer - #1 Killer

Lung cancer common and still deadly.

Five-year survival stands at ~15%.

Lung Cancer Men Women Diagnosed WW 1 million 500,000 Mortality WW 950,000 400,000

Source: GLOBOCAN 2008, IARC (International Agency for Research on Cancer), World Health Organization

Lung Radiosurgery Encouraging

Two studies show promise of radiosurgery in patients with early stage lung cancer: Study of potentially operable stage I NSCLC demonstrates tumor control comparable to surgery, while SBRT for inoperable centrally-located lung tumors yields promising results

How We Will Treat Lung Cancer

TrueBeam radiosurgery Gated RapidArc

Real time, triggered imaging

High Intensity Mode dose rate

Calypso?

Simulated treatment image with fiducials

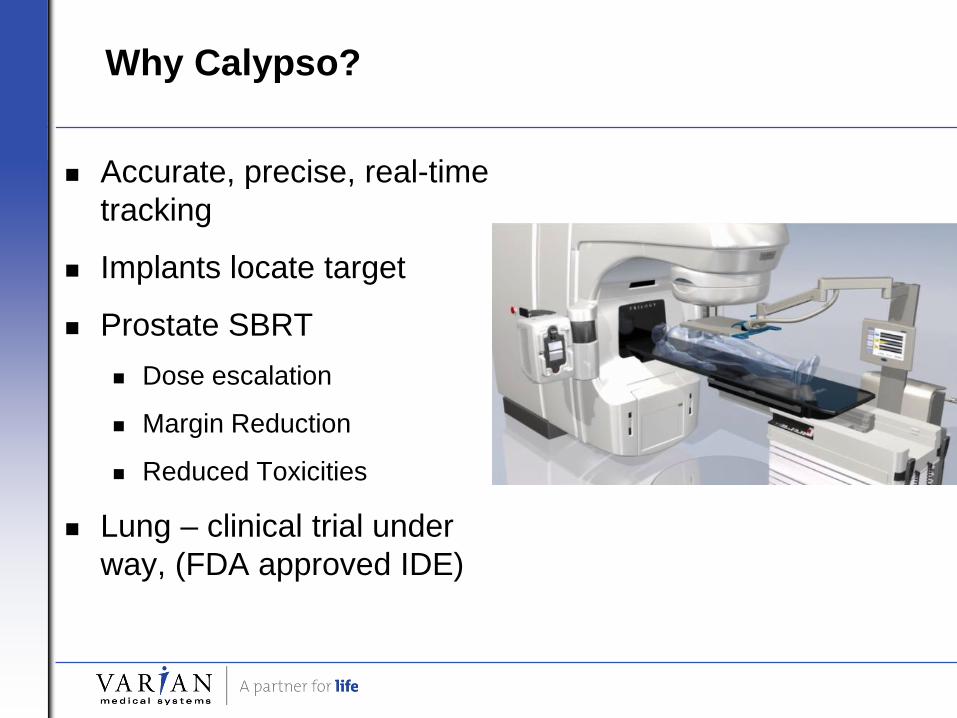

Why Calypso?

Accurate, precise, real-time tracking

Implants locate target

Prostate SBRT Dose escalation

Margin Reduction

Reduced Toxicities

Lung – clinical trial under way, (FDA approved IDE)

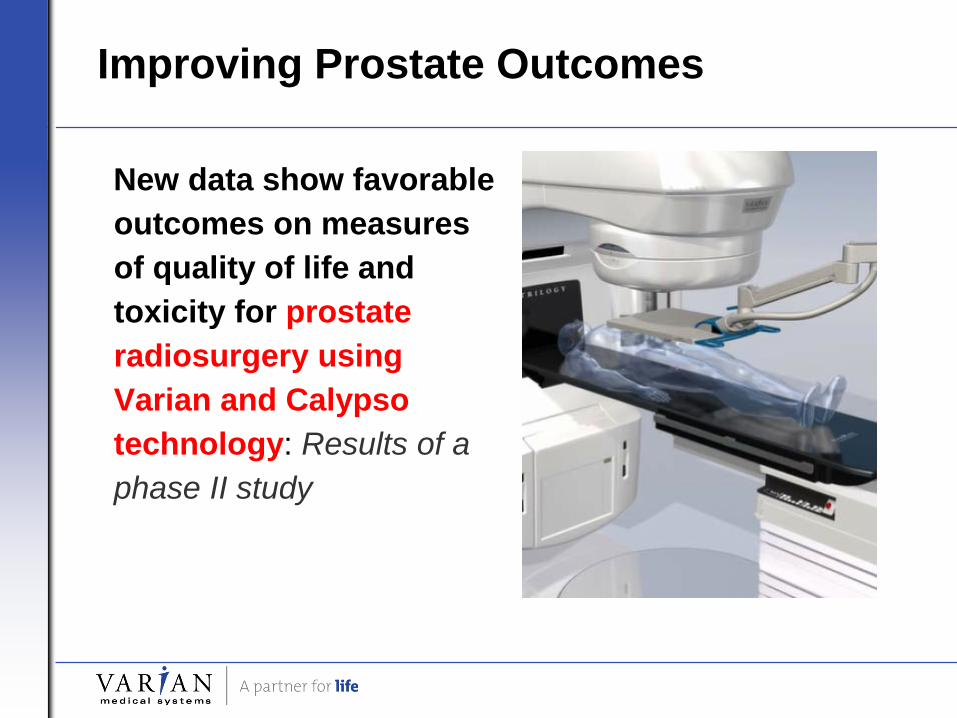

Improving Prostate Outcomes

New data show favorable outcomes on measures of quality of life and toxicity for prostate radiosurgery using Varian and Calypso technology: Results of a phase II study

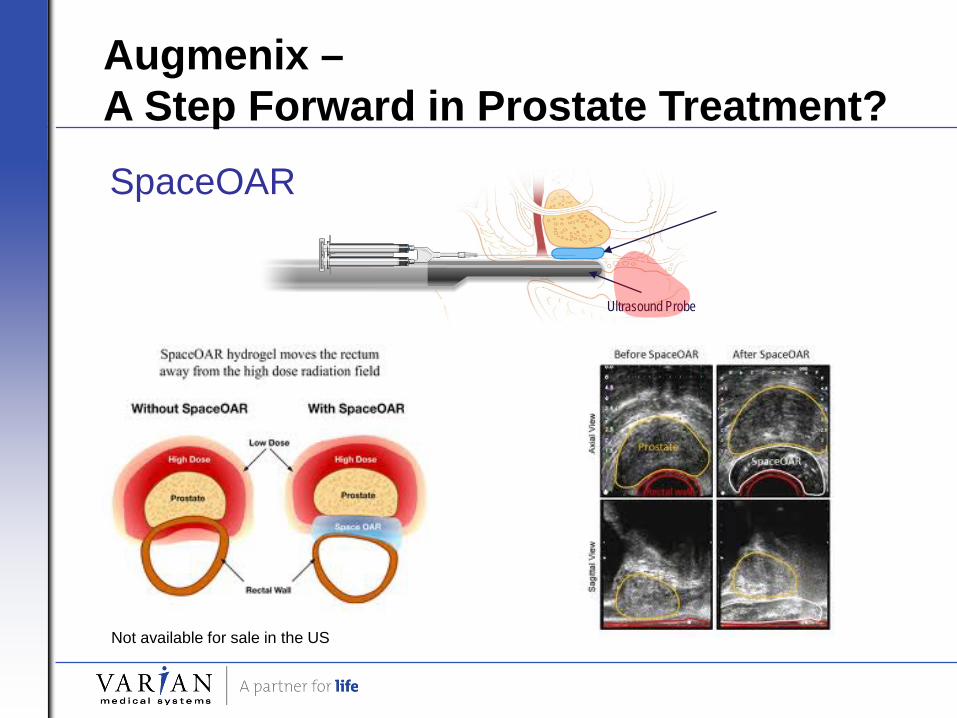

Ultrasound Probe

Augmenix – A Step Forward in Prostate Treatment? SpaceOAR

Not available for sale in the US

Pivotal™ Treatment Solution For Breast

Improved heart and lung sparing*

*Journal of Clinical Oncology, Vol 25, No 16 (June 1), 2007: pp. 2236-2242 © 2007 American Society of Clinical Oncology. DOI: 10.1200/JCO.2006.09.1041 Phase I-II Trial of Prone Accelerated Intensity Modulated Radiation Therapy to the Breast to Optimally Spare Normal Tissue

Prone Breast Treatment Technique

Tumor shift away from chest wall

Supine position Prone position

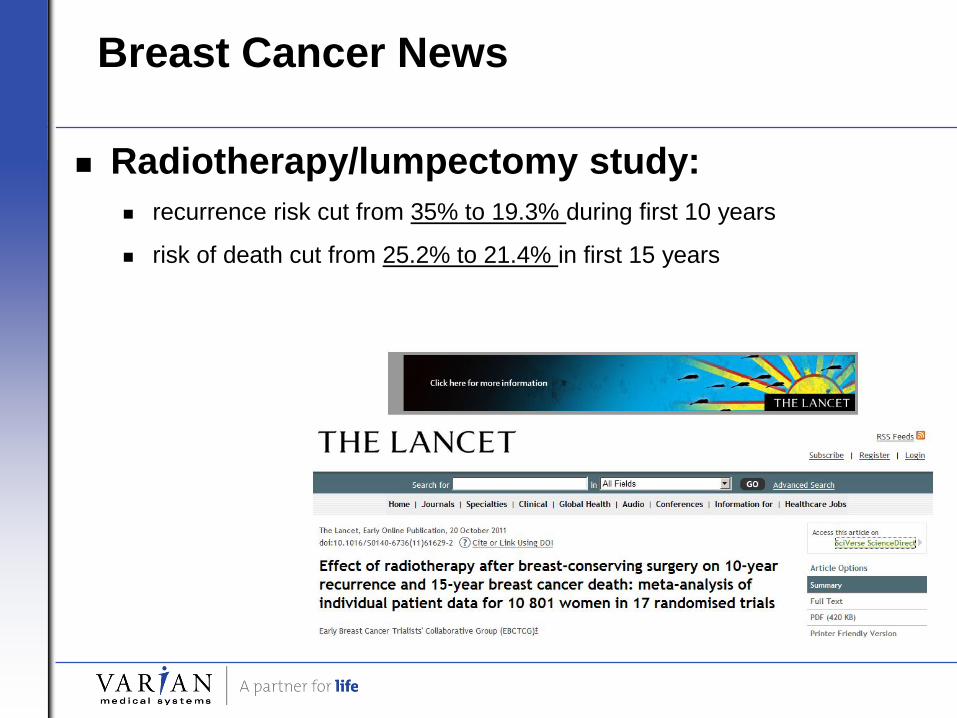

Breast Cancer News

Radiotherapy/lumpectomy study: recurrence risk cut from 35% to 19.3% during first 10 years

risk of death cut from 25.2% to 21.4% in first 15 years

Varian Medical Systems

65

Global Availability of Radiation Therapy

Number of Radiotherapy Machines per Million People 65 Yrs & Older

Source: IAEA and World Health Organization

Radiotherapy Machines per Million People

65 Yrs & Older

no machines

between 21 and 30

between 41 and 75

Over 75

between 31 and 40

between 1 and 20

10,000 more accelerators

The World Needs

Varian Oncology is Global Today

0

500

1000

1500

2000

2500

2006 2007 2008 2009 2010 2011

North America

International

$ Millions Net Orders

International

54% of FY11 orders

Building On Our Global Footprint

Q4 Orders from 50 countries

Service in 100 countries

Major training facilities US Switzerland China India Japan

Leveraging Customer Support Services

Growth Drivers Expanding installed base Richer product mix ....

premium pricing Extended Warranty Options Software Service Agreements Professional Services Services Sales Team

Productivity Drivers Faster installs SmartConnect Technology Continuous design

enhancements

$552M

FY2010 FY2011

Net Orders

$655M

How We Will Grow Service

* IMV data

• PremierAssurance™ customizable support contracts

• SmartConnect™ remote service technology for faster response

• Broader reach with >2000 services employees worldwide

•Superior reliability

Keys to Growing Service

Software Innovation

Expanding Install Base

Goal:

$1 Billion by 2015

Questions and Answers

Year End Review November 3, 2011

Thank you

Recommended