HEFFNER &ASSOCIATESELDER LAW

Mark B. Heffner, Esq. , CELAHeffner & Associates

615 Jefferson BoulevardWarwick, Rhode Island

www.hefflaw.com

Planning for Incapacity:Wellness at Brown!

HEFFNER &ASSOCIATESELDER LAW

Disclaimer•Materials are for general education and should not be substituted for consultation with a competent estate planning attorney in your state•Materials presented from the perspective of Rhode Island•Rules and practice vary significantly from state to state and are subject to change

HEFFNER &ASSOCIATESELDER LAW

Lifetime Planning: Health Care DecisionmakingAdvance Directive

Durable Power of Attorney for Health Care

Living Will

Selection of Agent

Selection of Successor Agent

HEFFNER &ASSOCIATESELDER LAW

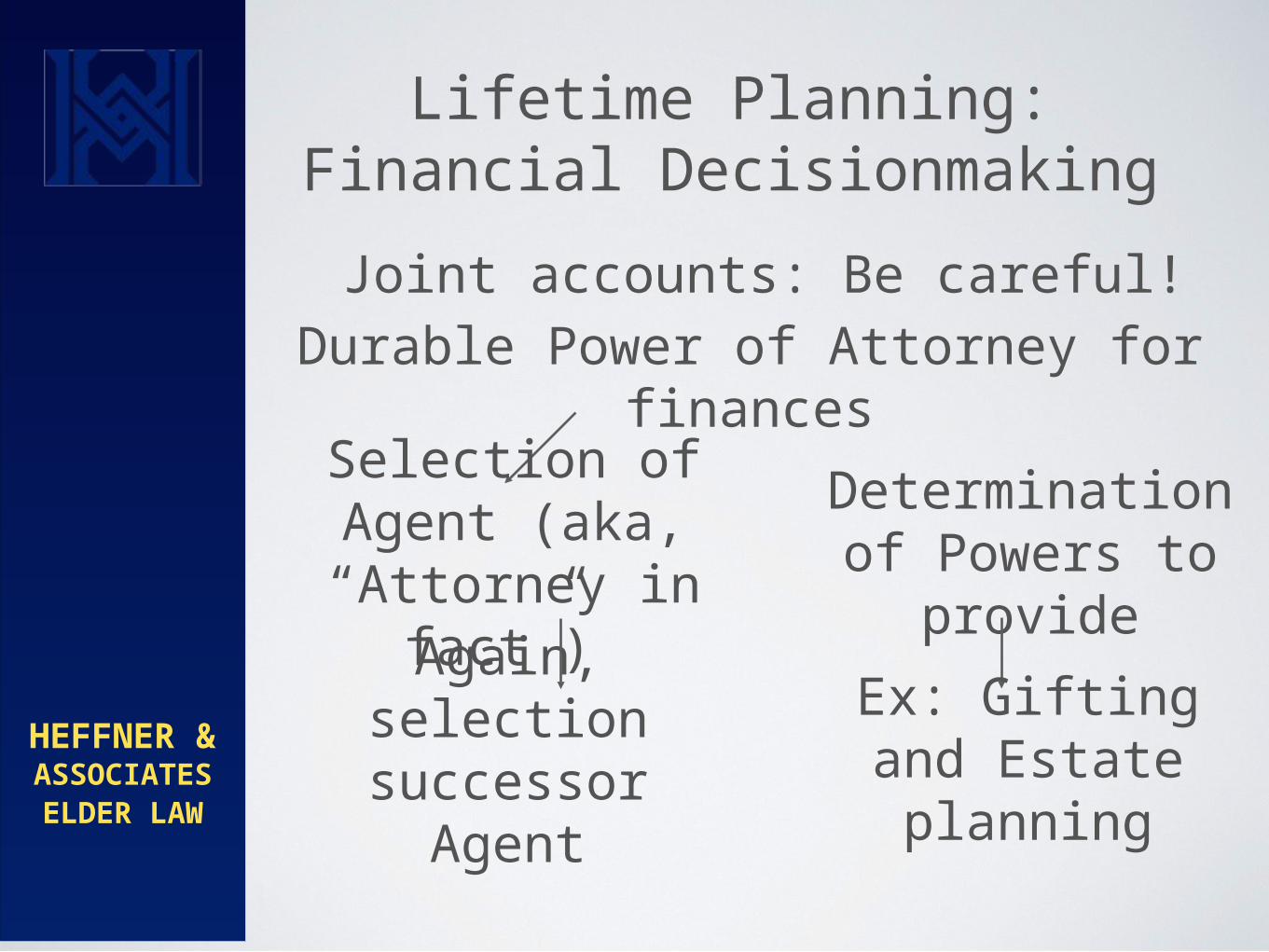

Lifetime Planning: Financial Decisionmaking

Joint accounts: Be careful!Durable Power of Attorney for

financesDetermination of Powers to

provideAgain, selection successor Agent

Selection of Agent (aka, “Attorney in

fact”)

Ex: Gifting and Estate planning

HEFFNER &ASSOCIATESELDER LAW

Lifetime Planning: Financial Decisionmaking

Revocable Trust, aka, “Living Trust”Avoids/Reduces “Push-Back” of

Institutions with use of Durable Power of Attorney

Selection of Trustee & successor Trustee critical

Provide no protection for assets for nursing home cost

Instead, would need Irrevocable Trust

HEFFNER &ASSOCIATESELDER LAW

Planning for post-deathWill—requires probate

Selection of Executor—same person generally as agent under financial

DPOARevocable Trust—if “funded” will avoid probate for those assets

Note: Need to check beneficiary designations (IRAs, life insurance, annuities), joint titling, as general “trump” Will or Trust provisions

HEFFNER &ASSOCIATESELDER LAW

What happens if long-term care needed?

Medicare--limited long term care (LTC) coverage 20 days full

payment, up to 80 additional days with co-pay ($164/day)

Medicare LTC coverage initially applicable if individual has a three

day prior hospital admission & continues to require skilled care

After that….

HEFFNER &ASSOCIATESELDER LAW

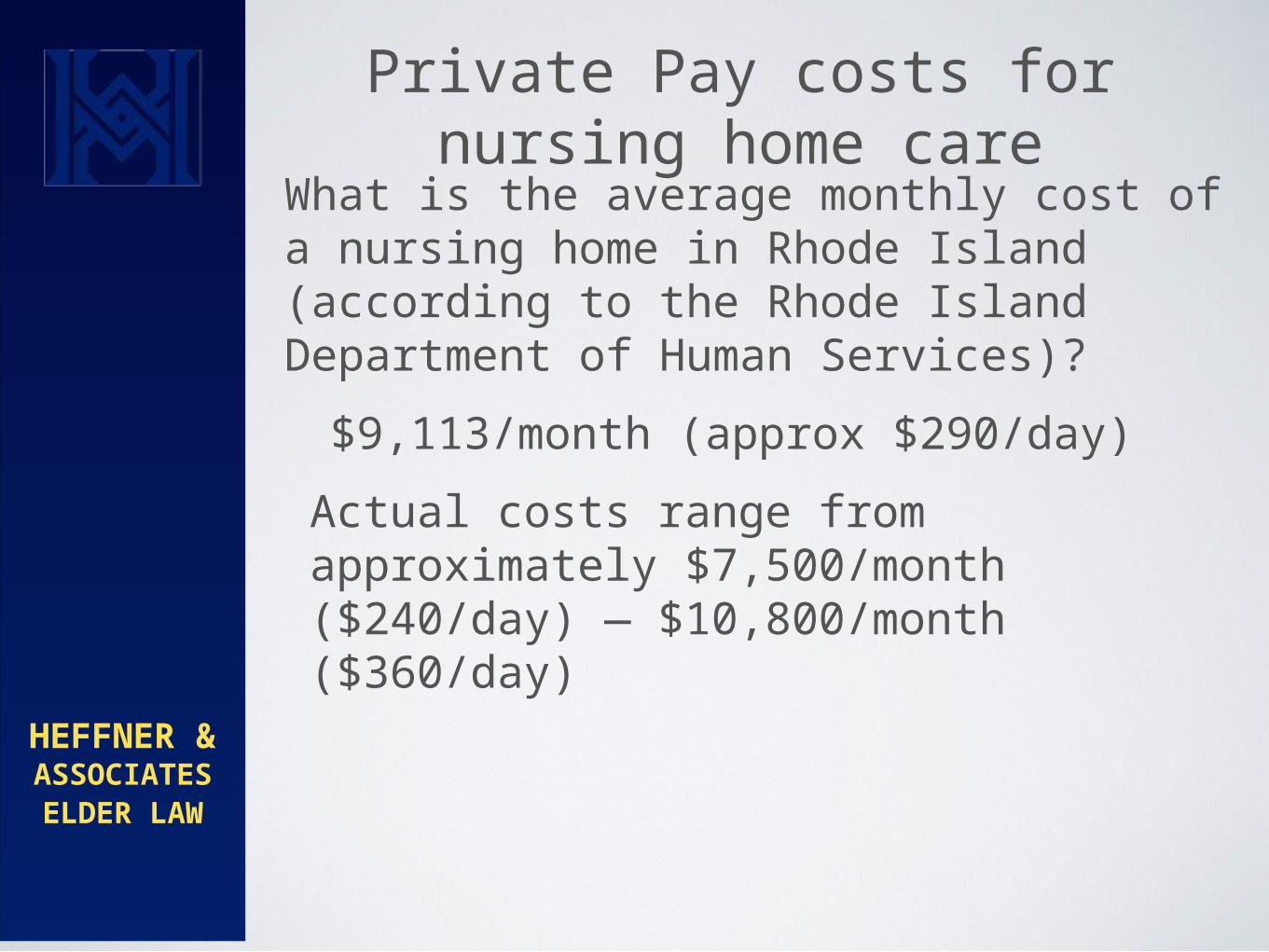

Private Pay costs for nursing home care

What is the average monthly cost of a nursing home in Rhode Island (according to the Rhode Island Department of Human Services)?

$9,113/month (approx $290/day)Actual costs range from approximately $7,500/month ($240/day) — $10,800/month ($360/day)

HEFFNER &ASSOCIATESELDER LAW

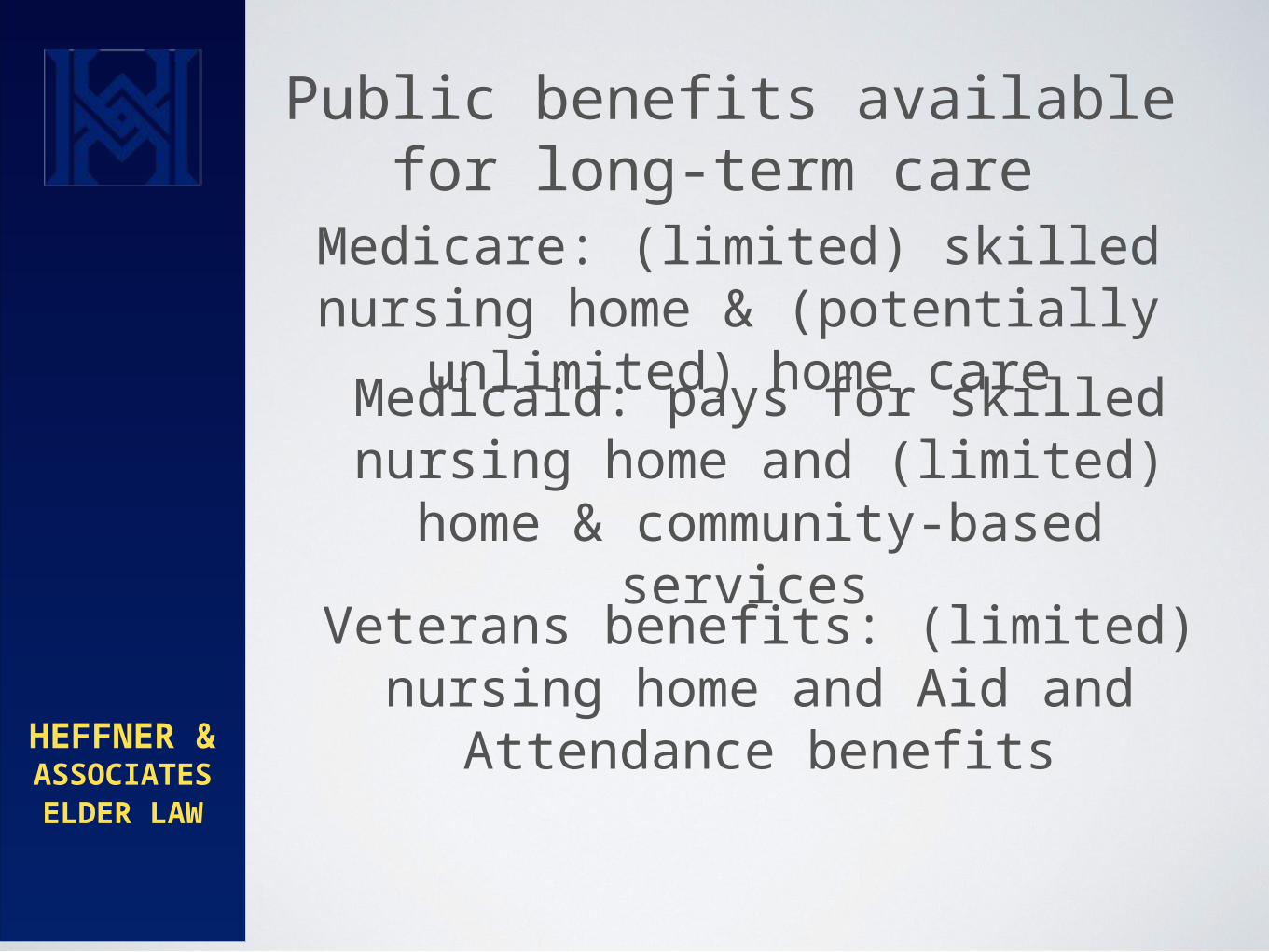

Public benefits available for long-term care

Medicare: (limited) skilled nursing home & (potentially unlimited)

home careMedicaid: pays for skilled nursing

home and (limited) home & community-based services

Veterans benefits: (limited) nursing home and Aid and Attendance

benefits

HEFFNER &ASSOCIATESELDER LAW

What is Medicaid?•It is not Medicare!

•Medicaid: in addition to general criteria (age, blind, disabled) & needing a level of care, must also fall within financial criteria (assets, income, transfer restrictions)

•Medicare: insurance model; no asset or income qualification requirements

•Substantial state to state variations

HEFFNER &ASSOCIATESELDER LAW

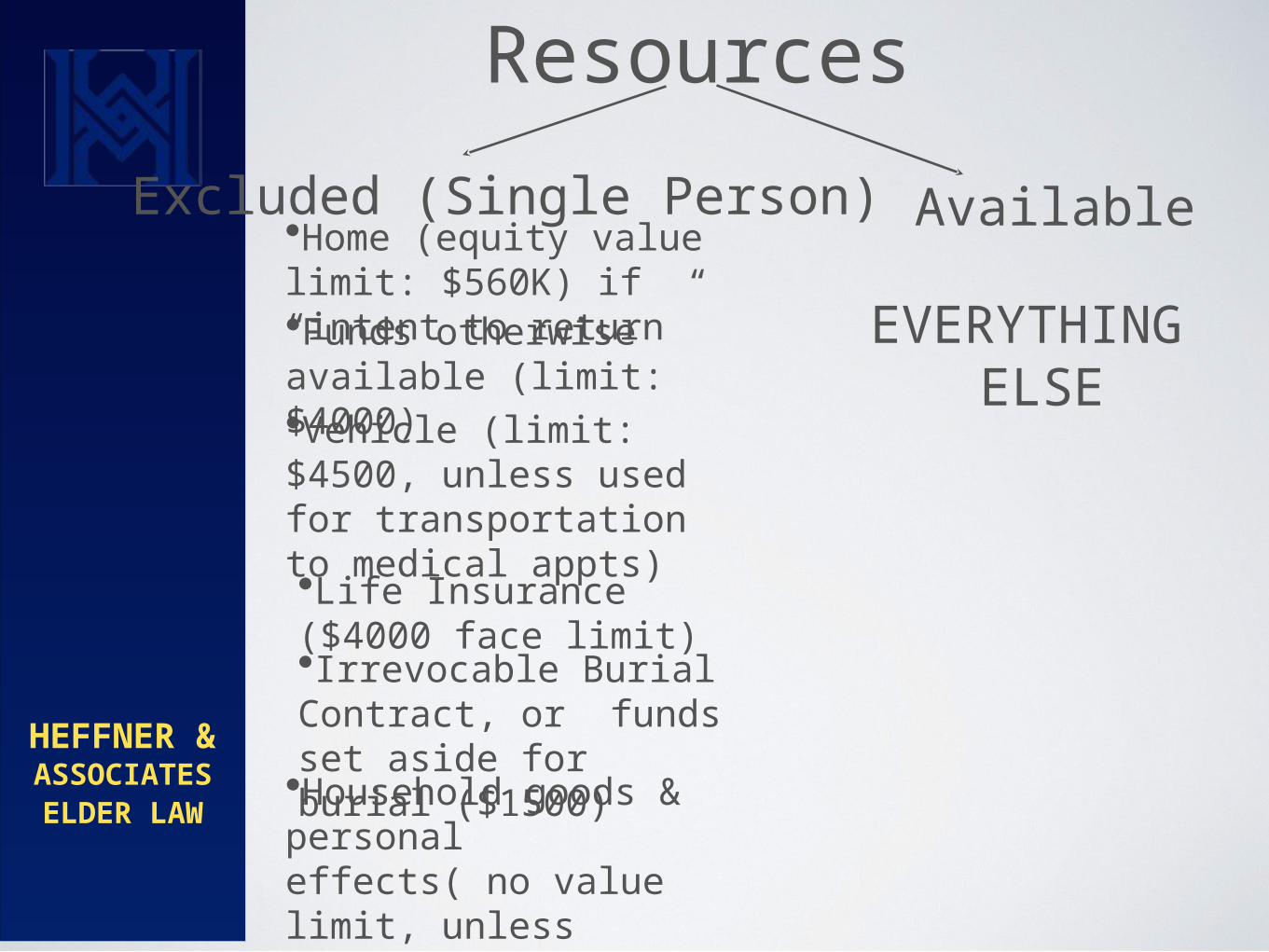

Resources

Excluded (Single Person)•Home (equity value limit: $560K) if “intent to return”

•Household goods & personal effects( no value limit, unless exceptional)

•Vehicle (limit: $4500, unless used for transportation to medical appts)•Life Insurance ($4000 face limit)•Irrevocable Burial Contract, or funds set aside for burial ($1500)

•Funds otherwise available (limit: $4000)

Available

EVERYTHING ELSE

HEFFNER &ASSOCIATESELDER LAW

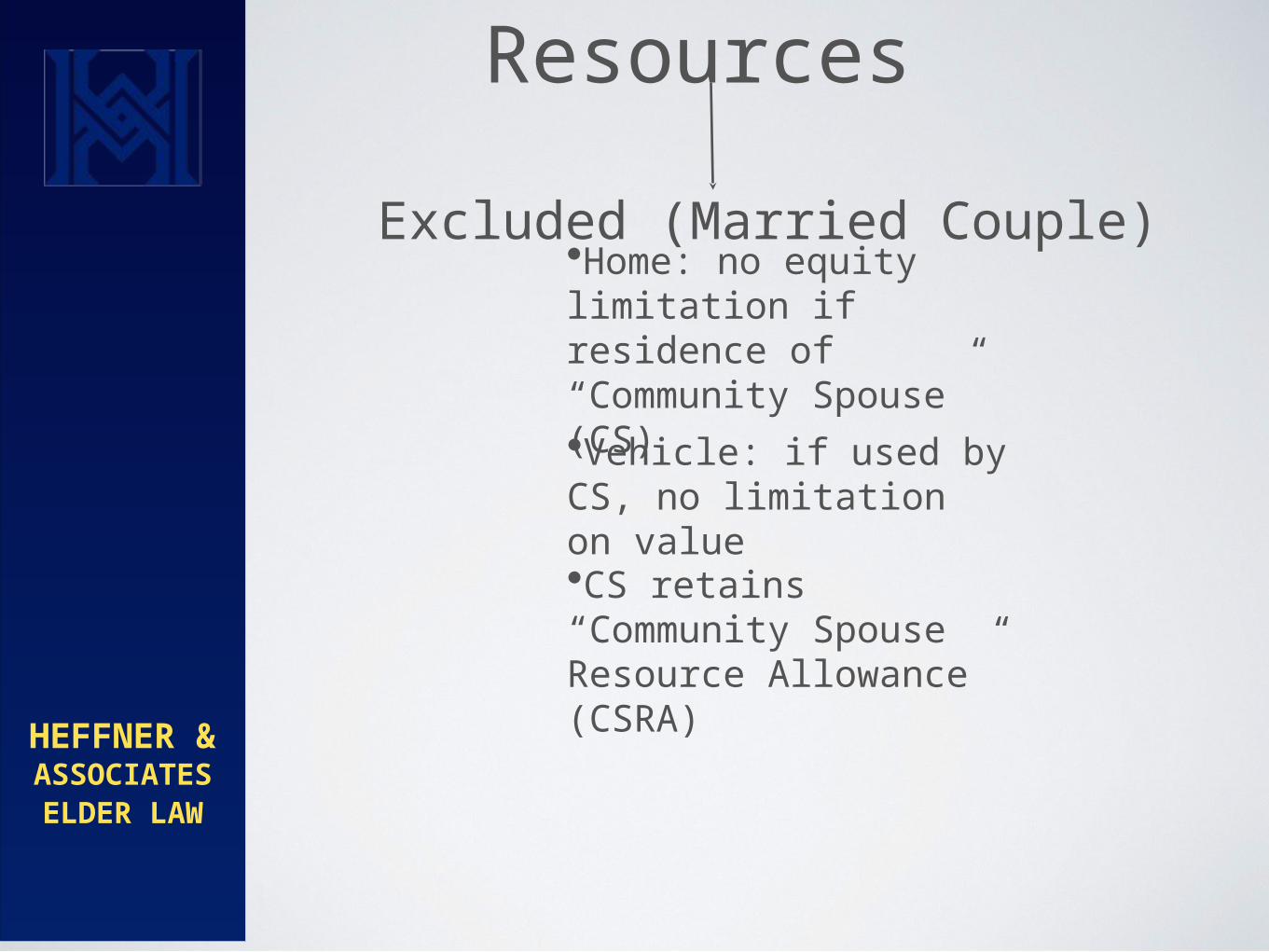

Resources

Excluded (Married Couple)•Home: no equity limitation if residence of “Community Spouse” (CS) •Vehicle: if used by CS, no limitation on value•CS retains “Community Spouse Resource Allowance” (CSRA)

HEFFNER &ASSOCIATESELDER LAW

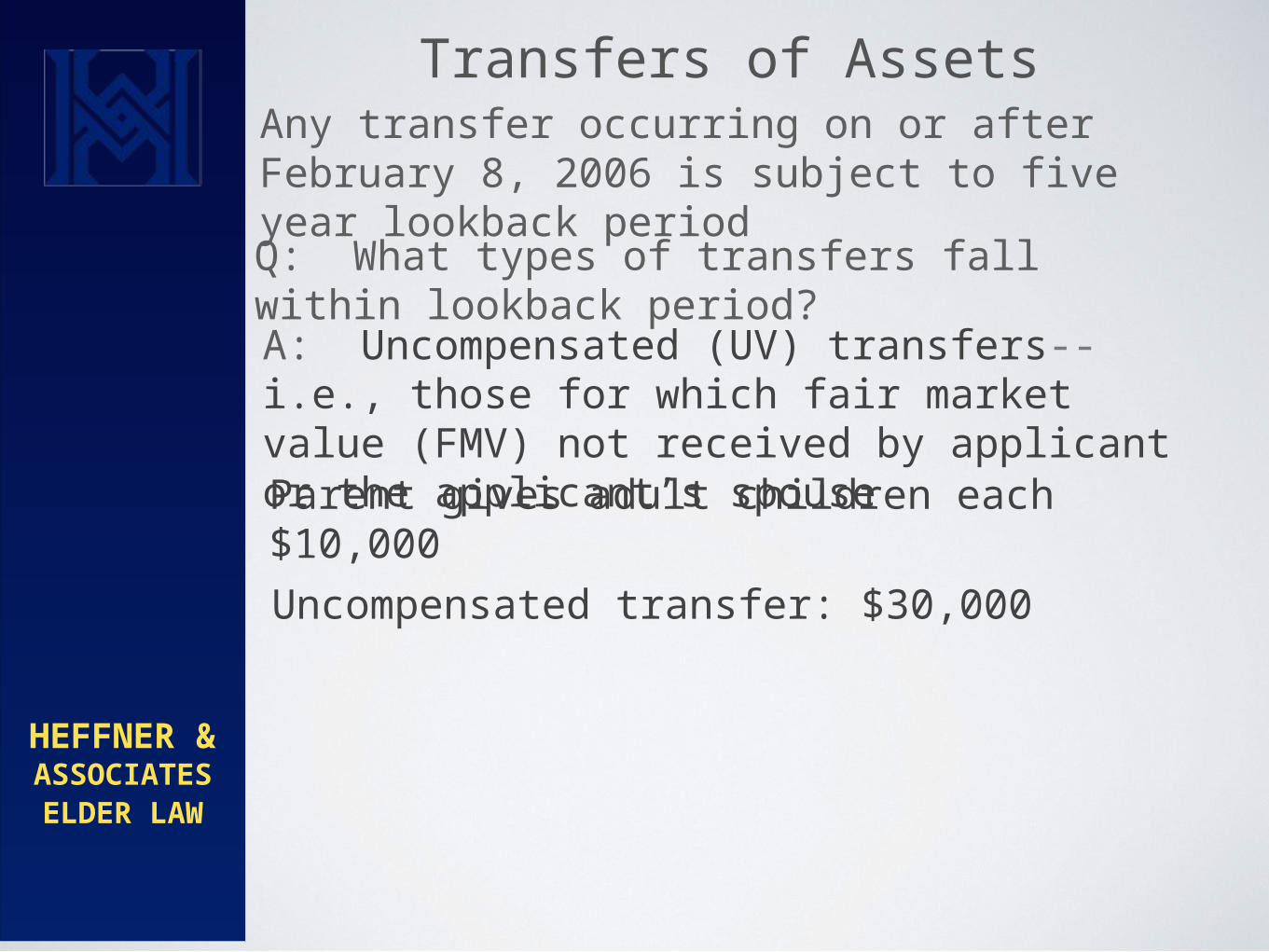

Transfers of AssetsAny transfer occurring on or after February 8, 2006 is subject to five year lookback periodQ: What types of transfers fall within lookback period?A: Uncompensated (UV) transfers--i.e., those for which fair market value (FMV) not received by applicant or the applicant’s spouse Parent gives adult children each $10,000 Uncompensated transfer: $30,000

HEFFNER &ASSOCIATESELDER LAW

Medicaid Planning TechniquesHighly individualized—one size definitely does not fit all!

• Spenddowns—debts, taxes, burial contracts. • Specialized annuities—married couples only

“Crisis planning” techniques include:

• “Reverse half a loaf” planning• Many more opportunities exist for married couples; however still “never too late” for single individuals

HEFFNER &ASSOCIATESELDER LAW

Medicaid Planning TechniquesNon-crisis, or “pre-crisis” planning techniques include:• Make transfers, incur five year lookback

period• Transfers—must be mindful of tax implications, creditors—grantor Irrevocable Trusts useful device. • Durable Powers of Attorney with estate and Medicaid planning authority provided to agent

• Again, highly individualized as to what techniques to use & timing of use of techniques

HEFFNER &ASSOCIATESELDER LAW

How to get startedArrange for consultation with competent elder attorneyPreparation: provide elder law attorney with individual family, financial and health informationInitial meeting should be at least an hourExpect fee for initial consultation

HEFFNER &ASSOCIATESELDER LAW

National Elder Law Foundationwww.nelf.org

Locating competent elder law attorneyCertified Elder Law Attorney

Provides interactive state map of Certified Elder Law Attorneys (CELA)

in each state

HEFFNER &ASSOCIATESELDER LAW

Mark B. Heffner, Esq. , CELAHeffner & Associates

615 Jefferson BoulevardWarwick, Rhode Island

www.hefflaw.com

Recommended