Unprofitable Affiliates and Income Shifting Behavior

Lisa De Simone

Stanford Graduate School of Business

Kenneth J. Klassen

University of Waterloo

Jeri K. Seidman

University of Texas at Austin

August 2014

Income shifting from high-tax to low-tax jurisdictions is commonly considered as a primary

method of reducing worldwide tax burdens of multinational firms. Extant research generally

makes the high- and low-tax distinctions using statutory or aggregated effective tax rates.

However, current losses also affect the marginal tax rates of affiliates. In the absence of

carryback or carryforward provisions, an unprofitable affiliate has a marginal tax rate of zero.

Thus, an unprofitable affiliate can temporarily alter the income shifting incentives and strategy of

a multinational firm. We alter prior estimation approaches to allow for the inclusion of loss

affiliates and test whether the unexplained income of unprofitable affiliates and their associated

profitable affiliates is correlated with tax-related factors. Results suggest that multinational firms

with an unprofitable affiliate use tax-motivated shift-to-loss transfer pricing strategies.

Keywords: transfer pricing, income shifting, losses

______________________________________________________________________________

The authors appreciate helpful discussions with Jennifer Blouin and Leslie Robinson, as well as

comments from Mary Barth, Daniel Collins, Cristi Gleason, Jost Heckemeyer, Daniel Lynch, Ed

Maydew, Edmund Outslay, Kathy Petroni, Richard Sansing, Casey Schwab, Bridget Stomberg,

Erin Towery, Benjamin Whipple, and workshop participants at Michigan State University, the

University of Georgia, the University of Iowa, the Stanford Graduate School of Business, the

EIASM 4th

Workshop on Current Research in Taxation, the Tax Policy and the Activities of

Multinational Firms Conference at Eberhard Karls Universität Tübingen, and the 2014 Stanford

Accounting Summer Camp. The authors are thankful for financial support from the McCombs

Research Excellence Fund and the McCombs Supply Chain Management Center of Excellence.

1

1. INTRODUCTION

The accounting, finance, and economics literatures investigate income tax reduction

through cross-border income shifting. Prior research finds that firms undertake a strategy of

shifting income out of high-tax jurisdictions into low-tax jurisdictions, thus reporting lower

profit in high-tax affiliates and higher profit in low-tax affiliates.1 In a multinational firm with

only profitable affiliates, this shifting strategy results in tax savings equal to the dollars of

income shifted times the rate differential between the high-tax and low-tax affiliates, net of any

costs.

Prior research generally determines relative tax rate groupings using either the statutory

tax rate of the jurisdiction or an aggregated effective tax rate. These methods mask an alternative

tax-saving recipient of shifted income: an unprofitable affiliate. Ignoring the potential benefit of

a loss carryback or carryforward, an unprofitable affiliate becomes an extremely low-tax affiliate

because it has a marginal tax rate of zero. A firm may shift income from a profitable affiliate into

an unprofitable affiliate, reporting lower profit in the profitable affiliate and a smaller loss in the

unprofitable affiliate. Thus, shifting income into unprofitable affiliates often results in higher tax

savings than the “traditional” transfer pricing strategy because the savings are equal to the dollars

of income shifted times the rate of the profitable affiliate.

However, this alternative shift-to-loss strategy is not costless. Efficient transfer pricing

strategies can be expensive to put in place and, for this reason, are often set over a multi-year

period. In contrast, affiliate losses are relatively transitory as the affiliate will either return to

profitability or cease operations.2 Adjusting the income shifting regime to take advantage of an

1 See for example, Collins, Kemsley and Lang (1998); Klassen, Lang and Wolfson (1993); Desai and Dharmapala

(2006); Huizinga and Laeven (2008); Weichenrieder (2009); Klasssen and Laplante (2012); Dharmapala and Riedel

(2013); Dharmapala (2014); and Dyreng and Markle (2014). 2 It is possible for a multinational to continue to operate an affiliate with structural losses due to strategic or other

reasons. In general, however, one would expect this to be rare.

2

unprofitable affiliate may necessitate costly tax planning, such as re-characterizing the nature of

significant transactions or reorganizing the global supply chain structure. Each of these requires

creation of supporting documentation, procurement of additional professional services/advice,

and/or a reduction in the probability of sustaining a position upon audit. Whether the tax savings

from using an unprofitable affiliate as an alternative recipient of shifted income outweigh the

adjustment costs necessary to change from the traditional strategy is an empirical question,

especially if losses are expected to be transitory or unexpectedly arise in an affiliate.

Our paper uses affiliate-level data on multinational firms to explore responses to the

income shifting incentives generated by unprofitable affiliates. We follow Claessens and Laeven

(2004) and measure profitability as return on assets plus one, which allows us to include

unprofitable affiliates in the traditional logged Cobb Douglas profit prediction model. On a

sample that includes both profitable and unprofitable affiliates, we estimate a model which

specifies affiliate profitability as a function of labor; assets; productivity; macroeconomic,

industry-level, and firm-level shocks; and tax-related factors.

We study whether the unexplained profitability of affiliates varies with tax factors related

to the shift-to-loss strategy, such as the adjustment costs and the potential tax savings of such a

strategy. Results show that the profit of unprofitable affiliates is due at least in part to tax-

motivated shift-to-loss behavior. We document that the statutory tax rate of unprofitable

affiliates affects the unexplained profit of both unprofitable affiliates and their associated

profitable affiliates. Consistent with prior literature using profitable affiliates, we estimate that a

one standard deviation increase in the statutory tax rate of profitable affiliates is associated with

a 4.8 percentage decrease in profitability reported by the average profitable affiliate. In contrast,

we estimate that a one standard deviation increase in the statutory tax rate of unprofitable

affiliates is associated with a 6.6 percent increase in profitability reported by the average

3

unprofitable affiliate, and a 3.9 percent decrease in the profitability reported by the average

profitable affiliate. We also provide evidence that suggests that corporate taxpayers respond to

transfer pricing risk and jurisdictional scrutiny of reported losses, and that the profit shifted by

profitable affiliates to their unprofitable affiliates is proportional to their relative economic

activity. Overall, our study provides evidence that shifting income to an unprofitable affiliate is

an important transfer pricing consideration for multinational firms.

This paper is in the spirit of Gramlich, Limpaphayom, and Rhee (2004) (hereafter GLR)

and Onji and Vera (2010), who both study income shifting among keiretsu members in Japan.

Both papers document a lower incidence of losses in affiliated members relative to unaffiliated

members. These results suggest that affiliated groups band together to save keiretsu-level income

taxes by shifting taxable profit into unprofitable members.3 We contribute to this stream of

research by using a cross-border setting to test whether the unexplained profit reported by

unprofitable affiliates varies with the expected benefits, costs and risks of a shift-to-loss strategy.

The cross-border setting allows us to exploit variation in tax rates and heterogeneous affiliate tax

characteristics. Importantly, we are the first to use a cross-border sample in tests of tax-motivated

shift-to-loss income shifting and thus are the first to document that the presence of loss affiliates

affects the unexplained profitability of affiliated firms.

This study informs policy makers and public economists who, in light of increased

multinational income shifting and the recent economic downturn, are debating how to curb tax

base erosion and profit shifting (Saint-Amans and Russo, 2013). By focusing on temporary

changes to the multinational corporation’s income shifting incentives, our research provides

3 This result is also consistent with risk sharing to the extent the risk sharing manifests in profitable affiliates shifting

income into unprofitable affiliates rather than profitable affiliates tolerating the losses of unprofitable affiliates. Kim

and Yi (2006) provide evidence of earnings management in affiliated Korean firms (“chaebols”), which is consistent

with risk-sharing-motivated income shifting.

4

valuable insight into the costs of temporarily altering transfer prices and the size of inframarginal

effects induced by larger tax rate changes. Our evidence that firms will respond to temporary tax-

minimizing opportunities contributes to policy maker analyses of altering tax policies targeted at

multinational corporations, such as repatriation tax holidays, temporary tax incentives for foreign

direct investors, or patent boxes.

Our results also inform policy makers regarding the semi-elasticity of reported income

with respect to changes in statutory tax rates. Our paper suggests that, by using samples of

profitable affiliates only, previous estimates of the magnitudes of income shifting in response to

tax rate changes should be considered a lower bound. Some shifting by profitable affiliates goes

to unprofitable affiliates, rather than to low-tax profitable affiliates, and by omitting this sample

of unprofitable affiliates, the estimates include the muted effect to tax rate changes for these

affiliates. In addition, our analysis is helpful for policy analyses that involve large changes or

differences in statutory tax rates, and our estimates for unprofitable affiliates provide a lower

bound of the effect size for these analyses, as described more fully below.

This study also suggests that the jurisdictions that benefit from profit shifting and those

that are injured by profit shifting are not obvious. Although low-tax jurisdictions generally

benefit from multinational income shifting, our results suggest that low-tax jurisdictions also lose

expected tax revenues during periods of economic decline. During such periods, affiliated groups

could shift income to unprofitable affiliates instead of to affiliates located in low-tax

jurisdictions, or even shift income out of profitable affiliates located in low-tax jurisdictions into

unprofitable affiliates. Further, previous research demonstrates income shifting from high-tax

jurisdictions to low-tax jurisdictions, which suggests that high-tax revenue authorities should

5

focus their audit efforts on transactions with related parties in low-tax jurisdictions.4 Our results

suggest that revenue authorities should also be concerned about affiliates shifting income out of

their jurisdiction into unprofitable affiliates, regardless of the tax rate in the unprofitable

affiliate’s jurisdiction.

Our results also inform researchers. First, researchers should consider the impact of this

alternative tax-minimizing transfer pricing strategy in their studies of the “standard” tax-

motivated transfer pricing strategy. Many income shifting studies use aggregated affiliate profits

and losses (i.e., consolidated financial statement data), which confounds the two types of income

shifting strategies by combining a number of potentially-conflicting transfer pricing incentives.5

Other income shifting studies restrict their sample to profitable affiliates.6 The removal of

unprofitable affiliates does not fully address the concern, though, because the effect of shifting to

unprofitable affiliates is also reflected in lower profitability of profitable affiliates. Further,

estimates of tax policy changes on income shifting behavior may be understated by the exclusion

of loss affiliates from the sample. Second, our study provides evidence on the trade-offs firms

make in their transfer pricing decisions. The cost of establishing a tax-efficient supply chain

cannot be easily estimated. However, evidence regarding the expected tax benefit required to

entice firms to alter their transfer pricing to a shift-to-loss strategy provides indirect evidence on

the cost, which may be useful to researchers interested in cross-sectional variation in the use of

various income-shifting strategies. Finally, this study deepens our understanding of the income

shifting practices of multinational firms. Examining a new and economically significant income

4 For example, Collins et al. (1998), Clausing (2006, 2009), and Klassen and Laplante (2012).

5 For example, high-tax profitable affiliates have an incentive to shift income out of their jurisdictions while high-tax

unprofitable affiliates may be recipients of shifted income. Low-tax profitable affiliates are likely to receive shifted

income, but in the presence of an unprofitable affiliate, they may also shift income out to the unprofitable affiliate. 6 For example, Power and Silverstein (2007), Blouin, Robinson and Seidman (2013), De Simone (2014), Markle

(2012).

6

shifting setting helps answer the call to research in Shackelford and Shevlin (2001) to increase

our ability to explain and predict income-shifting strategies beyond mere documentation.

The paper proceeds as follows. The next section provides institutional background on

how multinationals shift income as well as an overview of the literature on both cross-border

income shifting behavior and the effect of losses on firm behavior. The third section develops

our three hypotheses. Section 4 outlines the regressions and describes the data and variables we

use to test our hypotheses. Section 5 details results and Section 6 concludes.

2. BACKGROUND AND RELATED LITERATURE

2a. Income Shifting Background

The most effective income shifting strategies employ two components in concert with

each other—an operational decision and an accounting decision. The operational decision entails

tax-efficiently structuring the firm’s global supply chain such that the affiliated parties to major

intercompany transactions are strategically located. As such, multinationals often locate high-

return assets and activities in low-tax jurisdictions and relatively low-return activities in high-tax

jurisdictions.7

Further, multinationals have incentives to choose prices for these intercompany

transactions that optimizes the worldwide tax burden of the firm; this represents the accounting

decision component. Transfer pricing guidelines for income tax reporting are established by the

OECD, and have been adopted in some form by most European countries. These regulations

prescribe that for the purposes of calculating taxable income, any intercompany prices for goods,

services and intangibles should be those that would have been realized if the parties were

7 Examples of high-return activities include the research and development of unique intangibles. Examples of low-

return activities include contract manufacturing and limited-risk distribution.

7

unrelated, known as the “arm’s length principle” (OECD, 2010). However, these arm’s length

prices can be difficult to observe, especially for services, unique intangibles, and unusual or

unfinished products (PWC, 2006). This inability to always find exact market price matches for

intercompany transactions leaves multinational entities some discretion in setting transfer prices.

Further, although many multinationals strive to appropriately price a transaction during the

course of the year, they can also make so-called “topside adjustments” to these prices after the

financial books have been closed but prior to the filing of the tax return.8 Thus, the accounting

decision for how and when to set the transfer price of an intercompany transaction is flexible and

relatively nimble when compared to the operational decision.

When a multinational firm realizes an affiliate will likely earn a loss, the multinational

has a number of options to consider. First, the affiliate could simply report the loss as earned. If

its jurisdiction allows loss carryback and it was profitable during the allowed carryback period,

the reported loss will generate an immediate refund. If its jurisdiction does not allow loss

carryback (or if it was not profitable during the allowed carryback period) but does allow loss

carryforward, the reported loss will generate tax savings in the future if the affiliate returns to

profitability. If the jurisdiction of the reported loss does not allow loss carryback or loss

carryforward, the reported loss generates no tax benefit for the multinational firm. Thus, both the

adjustment costs and the benefits are lowest under this option.

Second, the multinational firm can undertake real activities to minimize the loss at the

affiliate.9 For example, the multinational could move research and development activities to a

more profitable affiliate or, as a more extreme example, move a physical factory from one

8 Because we rely on affiliate financial statement information, we are unable to measure the impact of these topside

adjustments. However, topside adjustments bias against our tests detecting income shifting behavior. 9 We assume that the aggregate level of the multinational’s activities was optimal but that its allocation of these

activities to affiliates was not. Thus, in our setting, activities are moved rather than decreased.

8

jurisdiction to another. This option likely entails significant adjustment costs and will result in a

less tax-efficient structure in the future, assuming the unprofitable affiliate returns to

profitability.

Finally, the multinational can adjust transfer prices to minimize the reported loss.

Because transfer prices have some inherent flexibility, a multinational could potentially reduce

taxes using a traditional strategy when all affiliates are profitable, but change to a shift-to-loss

strategy when losses occur in some affiliates. This is the behavior we aim to study.

The inherent flexibility in transfer prices arises because market prices for intercompany

transactions can be difficult to observe. Firms generally construct a range of prices based on

inexact “comparables,” or companies with a similar business profile. Most countries accept any

price within the range generated using such methods, and as such, firms often choose the most

tax-favored endpoint of the range.

For example, firms with a high-tax affiliate that is purchasing services from a low-tax

affiliate will choose a price at the high end of the range to minimize profits in the relatively high-

tax jurisdiction and maximize profits in the relatively low-tax jurisdiction. If the high-tax affiliate

instead earns a loss, it has several options. First, and most commonly, the firm can choose a

transfer price at the other end of the range to minimize the reported loss. Second, the firm can

adjust its search for independent comparable transactions in order to expand the range to include

a new, more favorable endpoint. Finally, if necessary, the firm can identify risks borne by the

unprofitable affiliate that resulted in the loss (e.g., foreign currency exchange or product failure

risk), or other previously uncompensated transactions that the affiliate is party to, and

compensate the affiliate for that previously un-priced contribution. However, this last option

potentially sets a precedent for less tax-favored outcomes in profitable years.

9

2b. Related Literature

Accounting, finance, and economics literatures abound with evidence that firms reduce

income taxes by shifting taxable income from relatively higher-tax jurisdictions to lower-tax

jurisdictions. Grubert and Mutti (1991) exploit the relation between profitability and the tax rate

as a measure of income shifting and variants of their research design are often used in the

literature. For example, Klassen, Lang, and Wolfson (1993) use a similar methodology to study

changes in income shifting behavior in response to tax rate changes, while Hines and Rice (1994)

employ the research design to study the use of tax havens. The approach of Hines and Rice has

become common as a general model of multinational income shifting (Dharmapala, 2014).

Alternative methods for studying tax-motivated income shifting behavior have also been

developed. Jacob (1996) considers the volume of intrafirm trade as a measure of income shifting

flexibility and shows that tax savings are related to the volume of intrafirm trade. Clausing

(2006) finds that the price of intrafirm transactions and the trading partners’ tax rates are strongly

related in a manner consistent with tax-motivated transfer pricing. Overesch (2006) uses

intercompany accounts receivable (A/R) to indirectly measure intrafirm prices and shows that the

intercompany A/R of foreign-owned German subsidiaries with a loss carryforward is less

sensitive to the tax rate differential (between the foreign parent and the German subsidiary) than

is the intercompany A/R of foreign-owned German subsidiaries without a loss carryforward.

Bernard, Jensen, and Schott (2008) find that the prices that U.S. exporters charge arm’s-length

customers are significantly higher than the prices that they charge related-parties, and that this

price wedge is greater for goods sent to countries with lower corporate tax rates or to countries

with higher import tariffs.

While there is ample evidence of tax-motivated income shifting by multinational firms,

the literature has largely focused on the benefit of shifting income from higher-tax affiliates to

10

lower-tax affiliates and ignored the benefit of shifting income from a profitable affiliate to an

unprofitable affiliate.10

Because the presence of an unprofitable affiliate can alter the income

shifting incentives of relatively low-tax profitable affiliates, this omission may have a profound

effect on measurement of income shifting. Although Klassen, Lang, and Wolfson (1993) discuss

the difficulty in measuring the tax incentives of unprofitable firms and the potential confounding

effect losses have on tax-motivated income shifting behavior, to our knowledge, only GLR and

Onji and Vera (2010) attempt to test the effect of unprofitable affiliates.11

Both GLR and Onji and Vera (2010) find that members of Japanese keiretsu groups

(member firms) appear to alter their transfer pricing behaviors in the presence of loss members.

Although these results support loss-related income shifting, their data sets do not allow the

variation in tax rates necessary to directly study the relation between tax rates and profitability.

Further, the costs and benefits of shifting income between keiretsu members will differ from

those associated with foreign affiliates in a commonly-controlled group.

While the tax-motivated income shifting literature has largely ignored the impact of

losses on cross-jurisdictional income shifting, the effect of losses on other types of tax

minimizing behavior has been studied. For example, Mackie-Mason (1990) finds that firms with

loss carryforwards are significantly less likely to issue debt than firms without loss carryforwards

and Edgerton (2010) shows that firms with loss carryforwards elect bonus depreciation less

frequently than fully taxable firms. In addition, De Simone et al. (2014) provide evidence that

10

Much of the tax-motivated income shifting research excludes unprofitable foreign affiliates or unprofitable

foreign groups from analysis. However, this does not always address the problem because the effect of unprofitable

affiliates should be reflected in the profitability of profitable affiliates, which often remain in the sample.

Additionally, research that is only able to measure aggregated foreign versus domestic income, rather than that of

specific affiliates, treats the income-shifting incentives of unprofitable affiliates the same as those of profitable

affiliates. 11

Overesch (2006) and Overesch (2009) both tangentially discuss the potential effects of losses on tax-motivated

income shifting but neither explicitly investigates the impact of losses on inferences. While the literature on risk-

sharing (for example, Chang and Hong, 2000; Khanna and Yafeh, 2005; and Kim and Yi, 2006) inherently studies

the effects of unprofitable affiliates on affiliated groups, it primarily does so from a non-tax angle.

11

firms are less likely to be tax aggressive if they have significant loss carryforwards. These

studies suggest that the tax shield provided by additional deductions or aggressive exclusions is

less desirable for firms with tax losses than for firms without tax losses. Our work differs from

these studies because we posit that losses alter the tax planning strategy rather than simply

lessening the tax planning incentives. In that sense, our approach is more like Erickson et al.

(2012) and Maydew (1997) who find evidence of tax-motivated inter-temporal loss shifting.

We connect these two lines of literature by more directly studying the impact of losses on

cross-jurisdictional tax-motivated income shifting behavior. To do so, we develop a method to

estimate the expected income of unprofitable affiliates. We then examine the relation between

unexplained profits earned by unprofitable affiliates and the costs and benefits of employing a

shift-to-loss strategy.

3. MODEL AND HYPOTHESIS DEVELOPMENT

3a. Model

In a multinational group comprised exclusively of profitable affiliates, the traditional

strategy of shifting income from high-tax affiliates to low-tax affiliates reduces worldwide taxes.

This paper suggests that the presence of unprofitable affiliates temporarily confounds these

traditional income shifting incentives both by providing high-tax profitable affiliates additional,

potentially tax-minimizing recipients of shifted income and by altering the incentives of lower-

tax affiliates. Essentially, unprofitable affiliates face a reduced marginal tax rate, potentially

zero. Low-tax affiliates continue to have an incentive to receive shifted income but now also

have potential zero-tax recipients to whom they can shift income.

Hines and Rice (1994) develop a model in which each affiliate in a corporate group

reports a pre-tax profit, i, that is the sum of the pre-tax profit from the economic activity in the

12

affiliate, i, the amount of profit shifted into or out of the affiliate, i, and the cost of any

shifting, a 2 ´yi

2 ri. i would be positive for low tax-rate affiliates and negative for high tax

affiliates. Algebraically, this is represented as follows:

pi= r

i+y

i-a

2

yi

2

ri

(1)

This approach is in the spirit of the “all parties, all taxes, all costs” framework of Scholes,

Wilson and Wolfson (1992) in that it attempts to separately identify the benefits and the costs

associated with shifting income to an affiliate. In equilibrium, the firm maximizes overall profit,

the sum of after-local-tax profits of all its affiliates. They assume profits will not face repatriation

taxes and that total profits shifted among affiliates is constrained to be less than or equal to zero.

Because Hines and Rice (1994) estimate their model at the jurisdiction level, aggregating

the affiliates of all U.S. companies in the jurisdiction, they do not estimate the income shifted by

a particular affiliate. Huizinga and Laeven (2008), however, use this same model to estimate the

equilibrium shifting at the affiliate level. Huizinga and Laeven (2008) show that the equilibrium

profits shifted to or from jurisdiction i is

yi =ri

a 1-t i( )´

rk1-t k( )

t k -t i( )k¹i

å

rk 1-t k( )k=1

n

å

(2)

where i is tax rate in jurisdiction i. The fraction of the jurisdiction’s income that is shifted is

based on the cost parameter, a, the jurisdiction’s tax rate,, and the weighted average of the

difference in the jurisdiction’s tax rate relative to each of the other jurisdiction’s tax rates.

The model does not distinguish between profitable and loss affiliates, that is whether i is

positive or negative; however, since the tax rate is typically the statutory tax rate and a negative

13

value of i would yield a negative weight, empirical estimates based on this model employ

profitable affiliates only (e.g., Huizinga and Laeven, 2008). To analyze the change in equilibrium

income shifting if the affiliate in country j has losses, we examine the effect of a discrete

decrease in the tax rate for affiliate j.12

That is, we assume losses will lower the net present value

of taxes paid by the affiliate. To address the challenges that the above model faces in the

presence of a loss affiliate, we make two changes to the cost of shifting. First, we replace pre-tax

profit, i, as the driver of the cost of income shifting with Ki, where Ki represents economic

activities such as capital or labor. This is consistent with recent proposals from the OECD that

suggest that it is economic activity in the jurisdiction that is the standard of how much profit is

reasonable in that jurisdiction. Second, we model the cost of shifting as not tax deductible,

consistent with an alternative specification considered by Huizinga and Laeven (2008).13

With

these two changes, the equilibrium shifting for the affiliate in country i becomes the following:

yi=Ki

a´

Kk

tk

-ti( )

k¹ j

å

Kk

k

å (3)

If the affiliate in jurisdiction j suffers a loss, we assume that the loss affects the expected

present value of the tax rate for this affiliate, which we denote tj

L. We assume the affiliate’s

capital, and therefore its cost of shifting, are unaffected by the losses. The resulting change in

equilibrium shifting at the unprofitable affiliate that results from the loss is as follows:

y j

L -y j

P =K j

a´ t j -t j

L( ) (4)

12

Throughout the remainder of this section, if an affiliate has a loss, we denote the loss affiliate as being in

jurisdiction j. 13

In footnote 5, the authors state that the specification in which costs are not tax deductible, as in equation (3) here,

obtains quantitatively similar results to their main specification. Non-deductible costs of income shifting include

centrally borne compliance costs (not charged out to the affiliate) as well as potential penalties.

14

where the shifting superscripts denote a loss, L, or profit, P. This difference is positive, leading

to the expectation that the amount shifted and reported profits will be higher in a loss affiliate as

the loss reduced its tax rate. This is a very intuitive result.

Huizinga and Laeven (2008) demonstrate that the optimal shifting takes into account not

only the tax rate and cost of shifting of the affiliate in jurisdiction j, but also the tax rates and

costs of shifting of the firm’s affiliates in other jurisdictions as well. Thus, the income shifting of

profitable affiliates will change in response to the change in tax rate created by a loss. Taking the

difference in equation (3) for the firm’s affiliate in another country Z, where Z is not the loss

affiliate’s country (i = Z, Z ≠ j), yields the following:

yZ

j=L -yZ

j=P =KZ

a´K j t j

L -t j( )Kk

k

å

=K j

a´ t j

L -t j( ) ´KZ

Kkk

å

(5)

As intuition suggests, this difference will be negative whenever a loss lowers the tax rate in

jurisdiction j, i.e. when j > tj

L. It is also worthy of note that only the tax rate of the loss

affiliate j matters; there is no effect of the tax rates of other affiliates on income shifting

strategies of profitable affiliates in the presence of an unprofitable affiliate.

The Appendix provides numerical examples of the effect of a loss affiliate on income

shifting. Given an assumed cost structure of income shifting (costs are quadratic, a = 10), these

examples demonstrate that the introduction of an unprofitable affiliate increases shifting into the

unprofitable affiliate. That is, looking down the Cases in the Appendix, the amount of income

shifted into the loss affiliate, j, increases when it has losses, as operationalized by a reduction in

tax rate j.

15

3b. Hypothesis Development

The equilibrium changes in shifting outlined in equations (4) and (5) incorporate the cost

of shifting through the parameter a. These adjustment costs may include uncertain costs, such as

those associated with the increased likelihood of an audit due to inconsistent transfer prices, as

well as certain costs, such as commissioning a new transfer pricing study. Additionally, if losses

are transitory, adjustment costs include both costs to alter income shifting behavior in this year

and costs to revert back to a previously established income shifting strategy in the near future. As

adjustment costs increase—that is, as a increases—the equilibrium change in profit shifting that

results from becoming an unprofitable affiliate decreases. Algebraically, it is straightforward to

show that the derivatives of equations (4) and (5) with respect to the cost parameter a are

negative and positive, respectively. Thus, we expect that relatively higher adjustment costs

mitigate changes in income shifting behavior brought about by the presence of an unprofitable

affiliate.

H1: The magnitude of the unexplained profit is negatively associated with

adjustment costs to achieve income shifting to the unprofitable affiliate.

Next, we outline two hypotheses regarding the benefit of using the unprofitable affiliate’s

loss by having it receive shifted income. Equation (4) models the equilibrium change in income

shifting for the unprofitable affiliate as increasing in the change in tax rate due to a loss. Given

extant research documenting the sensitivity of profits to tax rates, intuitively we expect larger

changes in the marginal tax rate faced by a newly unprofitable affiliate to create larger incentives

for the firm to significantly alter its income shifting for that affiliate.

If t jL is a constant, e.g., zero, affiliates with higher marginal tax rates prior to becoming

unprofitable experience larger changes in marginal tax rates than affiliates in relatively low-tax

16

jurisdictions.14

Consistent with this logic, equation (4) (equation (5)) is increasing (decreasing) in

the tax rate j, which predicts that a higher statutory tax rate in the loss affiliate’s jurisdiction

amplifies the adjustment to reported profits.

H2: The magnitude of the unexplained profit is positively associated with

the statutory tax rate in the loss affiliate’s country.

Next we consider situations where t jL is not a constant. Equation (4) specifies the income

shifting adjustment as a function of the difference between the regular tax rate in the jurisdiction,

j, and the net present value of the tax rate faced by profits shifted to the loss affiliate, t jL; that is,

how large is the j – t jL.15

We consider three ways that a loss may have value to the group,

leading to a non-zero t jL: tax scrutiny, loss carryback, and loss carryforward. First, if losses are

more carefully scrutinized by tax authorities in a jurisdiction, losses will be less valuable to the

controlled group. Because these costs are specific to the loss affiliates, rather than being a

country or group level cost, we consider them to relate to the value of the loss, rather than as a

cost of shifting; i.e., part of parameter a. Second, if carryback is allowed and the affiliate was

profitable during the carryback period, the availability of a carryback refund increases the value

of the loss. Finally, if carryforward is allowed and the affiliate is expected to be profitable in the

near future, the affiliate will be able to recover some value of the loss in the form of future

income savings. We expect to observe less shifting into the loss affiliate (out of the profitable

affiliate) when the loss has higher expected value to the affiliated group.

14

A tax rate under loss of zero is consistent with either affiliates in jurisdictions that do not allow consolidation, loss

carryback or loss carryforward, or with affiliates that do not have fact patterns that will provide a benefit when these

provisions are allowed (i.e., no profitable affiliate with the same direct parent in the jurisdiction, losses during the

carryback period and expected losses during the carryforward period). We relax this assumption in H3. 15

Equation (5) specifies the opposite equation: tj

L -tj. We outline our third hypothesis with respect to equation (4)

but it applies to equation (5) equally but in the opposite direction.

17

H3: The magnitude of the unexplained profit is negatively associated with

the value of the loss.

Finally, we consider one additional aspect of the impact an unprofitable affiliate has on

the income shifting of profitable affiliates within the group. Shifting profit into an unprofitable

affiliate will result in both the profitable affiliate reporting lower profit and the unprofitable

affiliate reporting a smaller loss.16

Thus, the additional income reported in the loss affiliate, as

defined in equation (4) is shifted from the profitable jurisdictions in proportion to their economic

activity, the last factor in equation (5).17

Our final hypothesis considers this direct effect of an

unprofitable affiliate on the change in income shifting behavior of profitable affiliates.

H4: The magnitude of the unexplained profit shifting for profitable affiliates associated

with an unprofitable affiliate is in proportion to their relative economic activity.

4. DATA AND RESEARCH DESIGN

4a. Profit Prediction Model

To estimate their models, Hines and Rice (1994) and Huizinga and Laeven (2008) apply

the Cobb-Douglas production function to estimate the profits associated with the economic

activity in the jurisdiction.

ueALKcLwQ 432

31 (6)

16

In a multinational group with multiple profitable affiliates, it is unclear which profitable affiliates will shift

income to the unprofitable affiliate(s). Regardless of whether the profit shifting is shared across multiple profitable

affiliates or concentrated in only one affiliate, tests may not be powerful enough to discern the decrease in profit. We

test for the effect of a shift-to-loss strategy in both profitable and unprofitable affiliates but acknowledge that

because we can only identify the recipient and not the donor of shifted income, tests in the profitable sample are

expected to have lower power. 17

The Appendix shows that the change in income shifted into affiliate j is drawn from all profitable affiliates when

affiliate j is in a loss position (Case 2 in the Appendix), and the amount of change is in proportion to their relative

capital. In the example, affiliate Z is one third the size of affiliate i, and the change in dollars of income shifted is

also one third as large.

18

where is the profit before shifting as in equation (1). Applying log transformations to both

sides of equation (6) and incorporating equilibrium income shifting, as specified in Section 3a,

yields the following estimation equation:

log pi =b1 +b2 log Ki +b3 log Li +b4 log Ai +b5 ti +ui (7)

where Ki is jurisdiction capital, Li is jurisdiction labor, A is a measure of productivity, and i is

jurisdiction tax rate (or a broader measure of tax incentive for the affiliate; e.g., C in Huizinga

and Laeven, 2008).18

The model above is commonly used in the income shifting literature.

However, it is not conducive to a study of unprofitable affiliates because of its log specification.

Claessens and Laeven (2004) avoid this limitation by specifying i as return on assets

(ROA) plus one. We employ this approach, scaling the Cobb-Douglas production function in

equation (6) by assets and adding one to the dependent variable before taking logs.19

This

specification allows us to estimate a version of equation (7) on a sample that includes both

profitable and unprofitable European affiliates. Specifically, we specify the below regression to

estimate profit:

ln(i + 1) = β0 + β1*ln(Capital) + β2*ln(Labor) + β3*Productivity + β4*TaxRate

+ β5*Shock + β6*VSP + β7*VSP*Shock + β8*Loss + β9*Loss*Shock (8)

We estimate this model on a sample of European affiliates. All variables are from the

Amadeus database unless otherwise noted. Profit, i, is ROA, computed as EBIT divided by total

assets (TOAS); Capital is tangible fixed assets reported on the balance sheet (TFAS); Labor is

18

Variation in explained profit that is associated with the tax rate of the foreign affiliate is attributed to either

income shifting or implicit taxes. A negative coefficient on i suggests that higher rate leads to lower profitability.

This result is attributed to income shifting—firms report less taxable profit in higher tax jurisdictions and more

taxable profit in lower tax jurisdictions to minimize income taxes. A positive coefficient on i suggests that higher

rate leads to higher profitability and is attributed to implicit taxes; under perfect competition, total costs should

equalize so that jurisdictions with higher (lower) tax will have lower (higher) non-tax costs resulting in higher

(lower) i. 19

Scaling pi in equation (6) by assets results in ROA on the left-hand-side of the equation. Scaling the right-hand-

side of equation (6) by assets changes the exponent on Ki from β2 to (β2 – 1).

19

compensation expense reported on the income statement (STAF); Productivity is defined as

either SectorGDP (a country-year-sector measure of gross value added from Eurostat, where

sector is one of six major industry groups) or IndustryROA (median ROA by two-digit NACE

industry-country-year, calculated using all affiliated and independent firms); and TaxRate is the

country-year statutory tax rate (STR). The Shock variables are included in the model because the

Cobb-Douglas production function assumes all factors of production and coefficients are

positive. To realize a pre-tax loss, some element of the affiliate or its environment must provide

the negative influence. We include four variables to allow for such influence. These variables are

GDP, MktShare, MktSize and Age. GDP is the percent change in country-year GDP per

capita; GDP is as reported by the European Commission. MktShare is affiliate sales scaled by

MktSize in year t less affiliate sales scaled by MktSize in year t-1. MktSize is the country-

industry-year sum of all affiliate and standalone sales in year t less the sum in year t-1, scaled by

1,000,000. Age is year t less the first year the affiliate appears in the Amadeus database.

We consider affiliates with very small levels of profit separately from both unprofitable

and profitable affiliates for two reasons. First, affiliates reporting a small profit may be

unprofitable if not for a shift-to-loss income shifting strategy. Consistent with this, Onji and Vera

(2010) find that discontinuity in the probability distribution of affiliate profits occurs in a small

range of ROS near zero. To acknowledge this possibility, we include a two indicator variables:

VSP equals one if EBIT is greater than zero but less than 1.5% of net sales and Loss equals one if

EBIT is less than zero. This approach also captures the fact that some jurisdictions impose a

minimum profitability constraint on controlled foreign affiliates, which is discussed in more

detail in Section 4c. All measures are calculated at the affiliate-year, firm-year, or country-

industry-year level using Bureau van Dijk’s Amadeus database. We obtain country-year GDP

information from the European Commission website.

20

4b. Sample

The Amadeus database contains financial and operating information on independent and

affiliated European firms. We use unconsolidated company information from Amadeus over the

period 2003 to 2012 for all tests. Our sample selection is detailed in Table 1.

(insert Table 1 around here)

Table 1 outlines that we limit our sample to controlled groups with at least one foreign

affiliate with greater than 50 percent total (direct and indirect) ownership. We require that both

the parent and this foreign affiliate be located in Europe, where Amadeus includes more detailed

information, and that the affiliate not be missing earnings before interest and taxes (Amadeus

variable EBIT). These selection criteria yield a beginning sample of 222,461 affiliate-year

observations.

To remain in the sample, we require an industry classification (NACE) code because we

expect that profitability varies by industry and so include fixed effects in our regression. We

exclude affiliated groups in banking and insurance industries because their profitability is less

easily estimated using assets and compensation. We further require that the consolidated group

be profitable, reporting a return on sales (∑PLBT/∑REV) of at least three percent, because

consolidated losses create incentives to change the income shifting strategy that are unrelated to

our research question (Stock, 2013).20

For the purposes of estimation, we require tangible fixed

assets (TFAS) and total assets (TOAS), compensation expense (STAF), and a return on assets plus

one (EBIT/TOAS + 1) greater than zero. Countries missing at least one measure of productivity

are dropped from the sample. Country-specific measures are included in certain specifications so

20

We calculate consolidated return on sales for the affiliates in our sample, rather than use the consolidated figures

available in Amadeus, so ensure that we appropriately measure the incentives and ability of the affiliates in our

sample to achieve a shift-to-loss strategy. This approach also acknowledges that we do not have data for all affiliates

in the corporate groups.

21

observations in countries with fewer than 50 observations are dropped from the sample. Our final

sample consists of 41,199 affiliate-years representing 1,991 unique controlled groups.

In tests of our four hypotheses, outlined below, we separately estimate regressions on a

sample of 6,692 unprofitable affiliate-years and a sample of 23,602 affiliate-years that earn a

return on sales of at least 1.5 percent. For purposes of these tests, observations with very small

profit are not included in either sample.

4c. Tests of the Costs and Benefits of Shifting Income to an Unprofitable Affiliate

We hypothesize that as the benefit (cost) to the affiliated group of shifting into an

unprofitable affiliate increases (decreases), income shifting behavior is further altered and the

unprofitable affiliate reports a smaller loss. H1 focuses on the adjustment costs to change from a

standard transfer pricing strategy to a shift-to-loss strategy, H2 on the tax savings achieved by a

shift-to-loss strategy, H3 on the value of the loss if left with the unprofitable affiliate, and H4 on

which profitable affiliates provide the profit in the shift-to-loss strategy. Because these benefits

and costs simultaneously impact income shifting decisions, we test the hypotheses together when

they are directed at the same subset of affiliates.

The profit prediction model is presented in Section 4a. The residual from this model

becomes the dependent variable in tests of our four hypotheses. Because certain hypotheses

apply only to one group of affiliates and because variable definitions need to differ between the

two groups of affiliates, we estimate separate models for unprofitable and profitable affiliates. It

is conceptually possible to combine equations (8), (9) and (10) into a single regression. We

believe using residuals from the income prediction model to estimate our hypotheses in a second-

stage regression is a preferable approach to a single-stage regression for several reasons. First the

incentives that affect the two types of affiliates are different, as described below for equation (9)

versus equation (10). Thus, by estimating our model in two stages we can use measures tailored

22

to our hypotheses for profitable versus unprofitable affiliate income shifting incentives more

parsimoniously than in a single-stage regression with numerous interactions. Secondly, by

estimating the equations separately, the correlations of the independent variables used in each

equation do not affect the coefficient estimates. While none of the correlations exceed 0.26 in

absolute value (not tabulated), we believe that the equations are conceptually different, and thus

their coefficients should be estimated individually. Finally, to incorporate the independent

variables from equations (9) and (10) into the single regression would require interactions with

Loss and VSP indicator variables, plus potentially additional “main effect” variables. Such a

regression creates concerns about multicollinearity, even though individual variables are not

highly correlated.21

To test our hypotheses, we estimate the following two models, for unprofitable affiliates

and profitable affiliates, respectively:

Residit = β0 + 1*AdjCostsFt + 2*TaxSavingsit + 3*LossValueit + FE (9)

Residit = β0 + 1*AdjCostsFt + 2*TaxSavingsFt + 3*LossValueFt + 4*Rel_Activityit + FE (10)

where Resid is the residual from equation (8). Subscript i denotes an affiliate-level variable while

subscript F denotes an affiliated-group-level variable.

We predict that higher adjustment costs reduce shift-to-loss behavior, thus reducing

unexplained profit (increasing unexplained loss). Our proxy for adjustment costs captures the

level of transfer pricing risk for a firm. We obtain a jurisdiction-year measure, TP_Riskit, from

the EY Transfer Pricing Global Reference Guides from 2003 to 2013. In these biannual guides,

EY transfer pricing professionals rate transfer pricing risk by country as non-existent, low,

21

While we believe that it is preferable to estimate and describe the model using the three equations, in untabulated

results, we also estimate a single-stage model. Some of the variance inflation factors for the single-stage model

exceed 100, suggesting severe multicollinearity. However, interpretations of results are unchanged. Because the

interpretation of results is similar across models, we present the two-stage model for ease of discussion.

23

medium or high. We convert these ratings to a scale from zero to four, where zero represents the

least risk and four represents the most risk.22

Finally, because the transfer pricing risk of

affiliated trading partners affects the pricing decision as well as the transfer pricing risk of the

affiliate’s home jurisdiction, our variable, Max_TP_RiskFt, is an affiliated-group-year variable

equal to the transfer pricing risk experienced by the affiliate with the highest statutory tax rate

within the group that year. Higher transfer pricing risk should discourage firms from adopting a

shift-to-loss strategy more than lower transfer pricing risk. Thus, H1 predicts a negative

(positive) coefficient on Max_TP_RiskFt when equation (9) (equation (10)) is estimated on the

unprofitable (profitable) sample.

We include the loss jurisdiction’s statutory tax rate to test H2. For unprofitable affiliates,

we use STRit, the affiliate’s statutory tax rate, which captures j – t jL under the assumption that

the LossValue proxies described below capture cross-sectional differences in t jL. For profitable

affiliates, we include the statutory rate of the loss affiliate within the group (LSTRit). If a

corporate group has more than one loss affiliate, the model suggests that the statutory rates are

weighted by economic activity to yield LSTRFt; we alternatively weight by capital or labor.

Equation (4) (Equation (5)) predicts a positive (negative) coefficient on loss affiliate statutory tax

rates when estimating the regression on a sample of unprofitable (profitable) affiliates.

Higher benefits to the loss should induce smaller changes in income shifting behavior.

Thus, the value of the loss serves as a mitigating device similar to adjustment costs. H3 predicts

that a higher value of the loss reduces shift-to-loss behavior, thus reducing unexplained profit

(reducing unexplained loss) in unprofitable affiliates (profitable affiliates). The value of the loss

is a function of a number of variables, including whether Net Operating Loss Carryback (CB) or

22

Factors of transfer pricing risk include the risk of tax audit, the risk that transfer pricing will be considered as part

of the tax audit, and the risk that transfer pricing will be challenged as a result of the tax audit.

24

Carryforward (CF) is allowed, the period of the CB or CF, and the recent profit history and

expected future profitability of the unprofitable affiliate.

We use two proxies for the value of the loss. The first is the value of the loss to the

unprofitable affiliate itself. In the spirit of simulated marginal tax rates (Shevlin, 1990; and

Graham 1996), CB/CF_Valueit equals one if the unprofitable affiliate was profitable during its

allowable CB period in excess of the current period loss, equals 0.91 if CF is allowed and the

cumulative profits over the carry-back period, if any, through one year following the current year

exceeds zero, and equals 0.83 if CF is allowed and the cumulative profits through two years

following the current year exceeds zero.23

CB/CF_Valueit equals zero when the following three

conditions hold: carryback or carryforward is not allowed, carryback will not generate an

immediate refund due to persistent losses, and the carryforward will not be used within two

years, assuming perfect foresight. When a profitable affiliate is associated with more than one

unprofitable affiliate, we alternatively weight CB/CF_Valueit by capital or labor to generate

CB/CF_ValueFt. H3 predicts a negative (positive) coefficient on CB/CF_Value when equation

(9) (equation (10)) is estimate on the sample of unprofitable (profitable) affiliates.

We also consider whether the jurisdiction allows an affiliate to report a loss or gives

special scrutiny to reported losses. Based on anecdotal evidence from transfer pricing

practitioners, some jurisdictions claim that arm’s length transfer prices should not result in an

affiliate loss because if unrelated firms entered into transactions at a loss they would go out of

business. We use the country summaries in the EY Transfer Pricing Global Reference Guides

23

Our variable definition assumes perfect foresight for two years (only) and a discount rate of 10%. To calculate this

variable, we hand collect current loss carryforward and carryback rules for each jurisdiction in our sample, if

available, and assume that the rules in historical periods were similar. The loss carryforward and carryback periods

for the jurisdictions in our sample vary greatly. In our sample, 34 of the 40 jurisdictions do not allow loss carryback

and only two allow carryback of two years or more. Three of the jurisdictions do not allow loss carryforward, 14

allow loss carryforward of three to five years, seven allow loss carryforward of six to 15 years, and 16 allow infinite

loss carryforward.

25

from 2003 to 2013 to identify jurisdictions that practitioners claim will give more scrutiny to a

firm’s transfer pricing if an affiliate earns a loss in their jurisdiction and set Loss_Scrutinyit equal

to one for these jurisdiction-years.24

When a profitable affiliate is associated with more than one

unprofitable affiliate, we size weight Loss_Scrutinyit to generate Loss_ScrutinyFt . Because high

loss scrutiny provides an additional incentive to shift income into unprofitable affiliates to

minimize the loss, we predict a positive (negative) coefficient on Loss_Scrutiny for coefficients

estimated on the unprofitable sample (profitable sample.)

Finally, we test whether profitable affiliates provide profit to unprofitable affiliates at a

rate proportionate to their relative economic activity, as predicted by equation (5). We define

Rel_Activityit as either 1) the profitable affiliate’s total assets divided by the total assets of the

affiliated group or 2) the profitable affiliate’s total compensation expense divided by the total

compensation expense of the affiliated group. Rel_Activityit is included only in equation (10). H4

predicts a negative coefficient on Rel_Activityit because shifting to an unprofitable affiliate will

result in negative unexplained profit.

5. RESULTS

5a. Summary Statistics

Table 2 presents summary statistics by country. The number of affiliate-years by country

varies from 102 in Ireland to 5,999 in Italy. We also provide averages over the sample period

2003-2012 of key inputs to our country-year proxies. Average statutory tax rates vary by country

from a low of 10 percent in Serbia and Bosnia and Herzegovina to a high of 34 percent in Italy

24

Countries cited in the 2013 Guide for having a higher risk of transfer pricing audit if an affiliate reports a low

margin or loss include: Belgium, Denmark, France, Germany, Hungary, Norway, Poland and the United Kingdom.

Other examples of higher scrutiny of losses include Portugal’s rejection of loss-makers from the set of comparable

benchmark firms used to substantiate intercompany prices and Belgium’s lack of any statute of limitation in the case

of a tax loss.

26

and Belgium. Countries with the highest transfer pricing risk on average over the sample period

include Austria, Germany, Denmark, Finland, France, Croatia, Italy, the Netherlands, Norway

and Slovenia, while the lowest risk country as reported by EY practitioners is Slovakia. Most

countries do not allow a carryback and the maximum average carryback period is three years

(France). All sample countries except Estonia allow a carryforward of at least five years. The

jurisdictions that scrutinize losses the most on average over the sample period are Germany and

Croatia, whereas many countries including Austria, Spain, and Italy do not scrutinize losses

according to practitioners.

Table 3 presents summary statistics for sample affiliate-years. As expected given our

sample selection, sample affiliates report a positive ROA on average. Approximately 19 percent

of the affiliate-year observations report a negative EBIT (Loss=1) while another 7.4% report 0 <

ROS ≤ 1.5% (VSP=1). The average affiliate in our sample faces a statutory tax rate of 28.4%.

While the average affiliate is located in a jurisdiction with relatively high overall transfer pricing

risk (2.76 on average, out of 4), only 29.5% of affiliates face specific scrutiny of losses.

(insert Table 3 around here)

Panels B, C, and D present descriptive statistics for affiliates experiencing a loss, very

small profit, and profit respectively. Comparing the panels in Table 3, the average unprofitable

firm is smaller at both the mean and median than the average profitable firm based on Total

Assets, Capital, Labor and Sales.

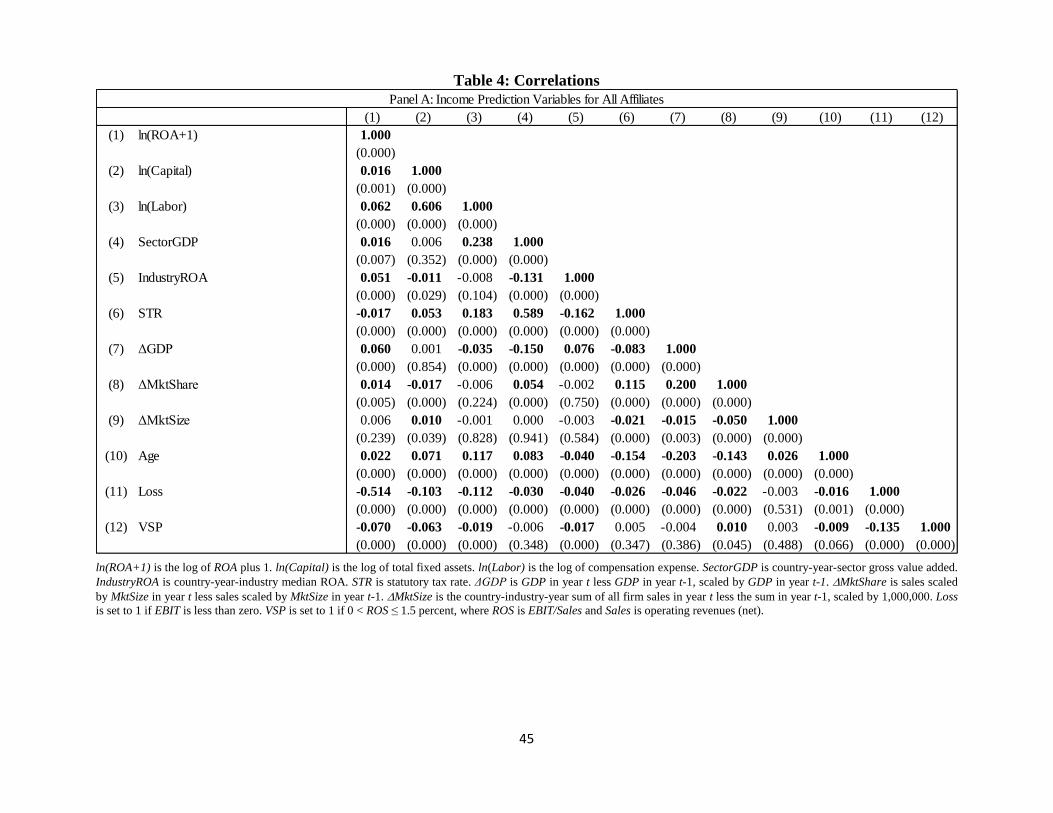

Table 4 presents correlations between our tax-motivated shift-to-loss variables. Panel A

presents correlations between variables included in the profit prediction model. Panels B and C

present correlations between variables included in the residual income hypotheses tests for the

sample of unprofitable and profitable firms, respectively. In all three panels, we find many

statistically significant correlations, but most generate a small coefficient. However, the

27

correlation between ln(Capital) and ln(Labor) is positive and statistically significant at 0.606;

though concerning, this is in line with prior literature.25

Additionally, the correlation between

SectorGDP and STR is positive and statistically significant with a coefficient of 0.589, again

similar to correlations reported in prior literature and nearly identical to the correlation between

the more-commonly-used jurisdictional-level GDP and STR in our sample.

In untabulated tests, we also examine the correlations between the first stage and second

stage variables. STRit is positively correlated with LSTRFt with a coefficient of 0.53 in the sample

of affiliates reporting return on sales of at least 1.5%. The coefficients on all other statistically

significant correlations are less than 0.26, with most being much closer to zero.

(insert Table 4 around here)

5b. Profit Prediction Model

We first estimate the profit prediction model to provide baseline information. Table 5

presents the results of estimating equation (8), which specifies profitability as a function of

capital, labor, productivity, taxes, and economic shock variables. Column (1) proxies for

Productivity using SectorGDP; Column (2) defines Productivity as IndustryROA.

(insert Table 5 around here)

Unlike the traditional Cobb-Douglas-based function of profits estimated in the income

shifting literature, we expect a negative coefficient on capital because we deflate both sides by

assets before taking logs and the Cobb-Douglas exponent on capital is generally assumed to be

less than one. Consistent with this expectation, we find a negative coefficient on Capital. As

expected, Labor are Productivity are positively related to profitability. Consistent with prior

income-shifting literature, STR is negatively related to profitability. Our models obtain R2

statistics of almost 30 percent, suggesting a relatively good fit.

25

For example, Huizinga and Laeven (2008) report a correlation of 0.84 between Capital and Labor.

28

5c. Costs and Benefits of Shifting Income to an Unprofitable Affiliate (H1 through H4)

To test the costs and benefits of shifting income to an unprofitable affiliate, we estimate

whether unexplained income (loss) is associated with the costs and benefits of a shift-to-loss

strategy. Table 6 presents results of estimating equation (9), which specifies profitability as a

function of tax-related variables (costs of adjusting to a shift-to-loss strategy, potential tax

savings from a shift-to-loss strategy, and the value of the loss if not shifted away) on the sample

of unprofitable affiliates (Loss=1). EY professionals’ opinions regarding the transfer pricing risk

in the various jurisdictions of the affiliate group (Max_TP_Risk) proxy for the costs of adjusting

to a shift-to-loss strategy. STR proxies for potential tax savings. We proxy for the value of the

loss to the firm using CB/CF_Value and Loss_Scrutiny.

(insert Table 6 around here)

Column (1) of Table 6 presents results using the residual from Column (1) of Table 5,

where SectorGDP is the proxy for Productivity; the dependent variable in Column (2) is residual

profit using IndustryROA as the proxy for Productivity. Unsupportive of H1, we find

insignificant coefficients on Max_TP_RiskFt in both columns of Table 6. This test fails to show

that transfer pricing risk is a significant determinant of use of a shift-to-loss strategy. Consistent

with H2, we find a positive coefficient on STRit in Column (2), which suggests that unprofitable

affiliates in high tax rate jurisdictions report higher unexplained profit (smaller unexplained loss)

than unprofitable affiliates in low tax rate jurisdictions when unexplained profit (loss) is

estimated using IndustryROA as the proxy for Productivity. Together with results from the first

stage and defining Productivity as IndustryROA to minimize multicollinearily concerns, we

estimate that a one standard deviation increase in the statutory tax rate of unprofitable affiliates is

associated with a 6.6 percentage increase in reported profitability. Table 5 allows us to estimate

the change in reported profitability for a profitable affiliate for comparison purposes; a one

29

standard deviation increase in the statutory tax rate of the average profitable sample affiliate is

associated with 4.8 percentage decrease in reported profitability.26

The estimate for unprofitable affiliates provides insight into the change in profits that

results from a large discrete change in tax rates within a single country, or large differences in

tax rates across countries (e.g., from the entering of a tax haven). Because the estimates involve

affiliates that, if profitable, would face a tax rates equal to the statutory tax rate but now face a

tax rate that is much lower (controlling for CB/CF_Value), the estimates do not represent a

marginal effect inherent in extant methods (i.e., those based on Hines and Rice, 1994, and

summarized in Dharmapala, 2014). However, because the losses are expected to be temporary,

the shifting is expected to be muted relative to a permanent change in tax rates to zero. Thus, the

estimates provide a lower bound on the income change that is introduced by a large difference in

tax rates across affiliates.

Results on CB/CF_Valueit are contrary to predictions generated by H3. We predict that

unprofitable affiliates will report a larger loss where the carryback/carryforward value of the loss

is higher but in fact we find that unprofitable affiliates report a smaller unexplained profit (loss)

in these situations. This relation may result from CB/CF_Value being negatively correlated with

the persistence of the loss, and extant research shows more persistent losses being larger, on

average (Joos and Plesko, 2005). Finally, consistent with H3, we find that unprofitable affiliates

in jurisdictions with higher loss scrutiny report larger unexplained profit (smaller unexplained

losses) when unexplained profit (loss) is estimated using SectorGDP as the proxy for

26

Using a one percent change in STR and the average value of the dependent variable, the semi-elasticity for

profitable affiliates equals 0.80 percent, which is exactly consistent with the average semi-elasticity reported by

Heckemeyer and Overesch (2013). The semi-elasticity computed in this manner for unprofitable affiliates is -0.82

percent. These calculations provide support that our approach for including unprofitable affiliates in the sample (i.e.,

adding a constant to ROA) does not bias estimated coefficients.

30

Productivity. We estimate that a one standard deviation increase in Loss_Scrutinyit is associated

with a 13.0 percentage increase in ROA for the average unprofitable affiliate the sample.

Table 7 presents results of estimating equation (10) on the sample of profitable affiliates

(Loss=0 and VSP=0). As before, EY professionals’ opinions regarding the jurisdiction’s transfer

pricing risk (MAX_TP_RISK) proxy for the costs of adjusting to a shift-to-loss strategy. LSTRFt,

the weighted average statutory tax rate of the associated unprofitable affiliates, proxies for

potential tax savings. We proxy for the value of the loss to the firm using weighted average

values for CB/CF_ValueFt and Loss_ScrutinyFt. Finally, Rel_Activity proxies for the ability of

profitable firms to contribute profit to unprofitable affiliates.

(insert Table 7 around here)

Columns (1) and (2) of Table 7 present results using the residual from Column (1) of

Table 5, where SectorGDP is the proxy for Productivity. The dependent variable in Columns (3)

and (4) is residual profit using IndustryROA as the proxy for Productivity. Consistent with H1,

we find significantly positive coefficients on Max_TP_RiskFt in all columns of Table 7. Using

Column (4), we estimate that a one standard deviation increase in the maximum transfer pricing

risk faced by affiliates in the same group-year is associated with a 4.4 percent increase in ROA

as reported by the average profitable sample affiliate. This indicates that transfer pricing risk is a

significant determinant of profitable affiliates using a shift-to-loss strategy.

Consistent with H2, we find significantly negative coefficients on LSTRFt in all columns.

This result suggests that profitable affiliates associated with unprofitable affiliates in higher-tax

jurisdictions report smaller unexplained profit than profitable affiliates associated with

unprofitable affiliates in lower-tax jurisdictions. Again using Column (1), we estimate that a one

standard deviation increase in the weighted average statutory tax rates of unprofitable affiliates

31

in the same group-year is associated with a 3.9 percentage decrease in the ROA reported by the

average profitable sample affiliate.

Results on CB/CF_ValueFt and Loss_ScrutinyFt .are contrary to predictions. We find that

the value of the loss if left with the unprofitable affiliate does not affect the reported profit (loss)

of associated profitable affiliates. Additionally, the loss scrutiny of the unprofitable affiliates is

associated with higher unexplained profit in profitable affiliates, contrary to predictions

generated by H3. Finally, consistent with H4, we find that profitable affiliates contribute profit to

unprofitable affiliates proportional to their relative activity. Using the coefficient reported in

Column (4), we estimate that a one standard deviation increase in relative capital is associated

with a 5.3 percentage decrease in ROA reported by the average profitable affiliate in the sample.

Overall, results in Tables 6 and 7 suggest that a number of tax-related factors affect the

use of a shift-to-loss income shifting strategy.27

We consistently find that the statutory tax rate of

unprofitable affiliates affects the unexplained profit (loss) reported by both profitable and

unprofitable affiliates, consistent with our second hypothesis. We also document that the profit

shifted out of profitable affiliates is proportionate to their relative activity, consistent with

predictions. Additionally, we find evidence that adjustment costs necessary to achieve a shift-to-

loss strategy affect the unexplained profit of profitable affiliates as predicted. While we find

inconsistent evidence regarding the value of an unshifted loss on unexplained profit (loss), our

results confirm that income tax minimization through a shift-to-loss strategy contributes to the

reported profit (loss) of both unprofitable affiliates and their associated profitable counterparts.

27

In untabulated results we also estimate a single-stage model. We note that some of the variance inflation factors

for the single-stage model exceed 100, suggesting severe multicollinearity. However, interpretations of results are

unchanged. Among unprofitable affiliates, we continue to find support for H2 and mixed support for H3. Among

profitable affiliates, we continue to find support for H1, H2 and H4, though support for H1 and H2 is more sensitive

to the definition of Productivity and Rel_Activity in the single-stage model than in the two-stage model.

32

6. CONCLUSION

Our paper studies a tax-motivated income shifting strategy that exploits losses earned by

unprofitable affiliates of a multinational group. By shifting income from profitable affiliates to

unprofitable affiliates, multinational corporations can reduce their worldwide tax burden.

However, there are potentially significant costs associated with adjusting away from a

traditional, multi-year income shifting strategy that shifts income out of high-tax jurisdictions

and into low-tax jurisdiction. Additionally, carryback and carryforward rules and affiliate-

specific circumstances could yield valuable tax benefits of reporting the loss in the unprofitable

affiliate. We therefore examine how the adjustment costs, potential tax savings, value of the

unshifted loss, and ability of profitable affiliates to contribute profits impact unexplained profits

earned by both the unprofitable affiliates of a multinational group and their associated profitable

affiliates. We also study which profitable affiliates contribute profit to unprofitable affiliates. The

role of losses in transfer pricing behavior has not been thoroughly studied in prior work.

We find consistent support for two of our four hypotheses: the potential tax savings and

the ability of profitable affiliates to contributed profits both affect unexplained profit (loss) as

predicted. We also find support for the hypothesis that costs of adjusting away from a

“traditional” income shifting strategy to a shift-to-loss strategy affects the unexplained profit

(loss) reported by profitable affiliates but no support for an effect on unprofitable affiliates.

Finally, we find results inconsistent with expectations regarding the effect of the value of an

unshifted loss on reported profit (loss). Overall, our results suggest that shift-to-loss transfer

pricing behavior is at least partially tax motivated.

33

References

Altman, E. I., 1968. “Financial Ratios, Discriminant Analysis and the Prediction of Corporate

Bankruptcy,” Journal of Finance 23(4): 589-609.

Bernard, A. B., J. B. Jensen, and P. K. Schott, 2008. “Transfer Pricing by U.S.-Based

Multinational Firms,” Tuck School of Business Working Paper No. 2006-33 and US Census

Bureau Center for Economic Studies Paper No. CES-WP- 08-29.

Blouin, J. L., L. A. Robinson and J. K. Seidman, 2013. “Conflicting Transfer Pricing Incentives

and the Role of Coordination,” University of Pennsylvania, Dartmouth College and

University of Texas at Austin working paper.

Chang, S. J., and J. Hong, 2000. “Economic Performance of Group-Affiliated Companies in

Korea: Intragroup Resource Sharing and Internal Business Transactions,” The Academy of

Management Journal 43(3): 429-448.

Clausing, K. A., 2003. “Tax-motivated Transfer Pricing and U.S. Intrafirm Trade Prices,”

Journal of Public Economics 87(9-10): 2207-2223.

Clausing, K.A., 2006. “International Tax Avoidance and U.S. International Trade,” National Tax

Journal 59(2): 269-287.

Clausing, K. A., 2009. “Multinational Firm Tax Avoidance and Tax Policy,” National Tax

Journal 62(4): 703-725.

Collins, J., D. Kemsley, and M. Lang, 1998. “Cross-Jurisdictional Income Shifting and Earnings

Valuation,” Journal of Accounting Research 36(2): 209-229.

Desai, M.A., and D. Dharmapala, 2006. “Corporate Tax Avoidance and High-Powered

Incentives,” Journal of Financial Economics 79: 145-179.

De Simone, L., 2014. “Does a Common Set of Accounting Standards Affect Tax-motivated

Income Shifting for Multinational Firms?” Stanford University working paper.

De Simone, L., J. R. Robinson and B. Stomberg, 2014. “Distilling the Reserve for Uncertain Tax

Positions: The Revealing Case of Black Liquor,” Review of Accounting Studies 19(1): 456-

472.

Dharmapala, D., 2014. “What Do We Know about Base Erosion and Profit Shifting? A Review

of the Empirical Literature,” University of Illinois working paper.

Dharmapala, D., and N. Riedel, 2013. “Earnings Shocks and Tax-Motivated Income-Shifting:

Evidence from European Multinationals,” Journal of Public Economics 97: 95-107.

34