UK Monthly Commentary

May 2017

Valuation Advisory

UK Commentary

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 2

Finance

US Federal Reserve rate at 1%

UK Base Rate at 0.25%

5-Year Swap Rate 0.79% (Beginning April 0.80%).

10-Year Rate 1.15% (Beginning April 1.13%).

LIBOR at 0.33

Bank lending, 65% LTV maximum, margins range from

150 basis points plus, depending on asset, borrower and

LTV, expanding group of lenders and range of loan terms

including development finance. Mezzanine funding

available

European Banking Market Greek Government funding and

debt repayment – discussions continue. IMF consider a

significant debt “write down” needed to enable Greek

economy to survive and grow in the Euro. Frances’

President Macron aims to lead Eurozone towards

becoming a unitary state.

Economic view

The FTSE 100 index at 7,522.03 up from 7,283 at the

beginning of April. This compares to 6,242 this time last

year.

Inflation RPIX (excluding mortgage interest payments) at

3.4% as of March 2017. CPI at 2.3% in the year to March

2017, unchanged from February.

Earnings for employees in Great Britain in nominal terms

increased by 2.3% including bonuses and by 2.2%

excluding bonuses, compared with a year earlier.

Retail Sales increased by 1.7% compared with March

2016 and decreased by 1.8% compared with February

2017; decreases are seen across the four main store

types.

Services Sector (78.8% of GDP), in the 3 months to

February 2017, services output increased by 0.5%

compared with the 3 months ending November 2016. In

the 3 months to February 2017, services output increased

by 2.5% compared with the same period a year ago. The

trade deficit in goods and services widened to £3.7bn in

February 2017, from a revised deficit of £3.0bn in January

2017. In the 3 months to February 2017, the deficit on

trade in goods and services narrowed to £8.5bn.

Manufacturing Output soars to three-year high. PMI rose to

57.3 in April, up from a four-month low of 54.2 in March

2017

Unemployment Rate was 4.7%, down from 5.1% for a year

earlier. There were 1.56mn unemployed people, 45,000

fewer than for September to November 2016 and 141,000

fewer than for a year earlier.

Annual House Price growth slowest in nearly four years.

House prices show second consecutive monthly decline in

April. Annual house price growth dips to 2.6%.

GDP forecast for 2017 at 1.8% and at 1.4% in 2018.

UK Commentary

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 3

Property view

IPD Total Returns for all Property in the 12 months to

March 2017 3.81% (February 2017 2.68%)

IPD Total Returns for the sectors in the 12 months to

March 2017 were: Offices 1.44% (February 2017 0.60%),

Industrial 9.44% (February 2017 7.45%), Retail 2.30%

(February 2017 1.35%).

Rental growth (monthly rates) up 0.08% (Offices down -

0.02%, Industrial up 0.41% and Retail down -0.01%)

Investment Volumes £15,404mn year to date April 2017.

(Compared to £17,288mn in 2016).

Sentiment

Prices steady supported by rental growth as yields

flattening out. Shortage of product. Demand competitive

for quality assets across UK especially in South East

London, attracting “safe haven” and of trophy investment.

Buyers from Sovereign Wealth Funds, Asia Pacific,

Germany, US, Middle East also UK private/”opportunity”

fund/investors property companies, UK institutions. Yields

stabilised. IPD all property equivalent yield at the end of

March 2017 is 6.18%.

International

US Economic activity in the manufacturing sector

expanded in April and the overall economy grew for the

95th consecutive month. The April manufacturing PMI

registered 54.8 percent, a decrease from the March

reading of 57.2 percent. GDP 2017 forecast at 2.1% and

2018 forecast at 2.6%. The US Economy grew 2.0%

(y-o-y) in Q4 2016.

Brent Crude at $51.6 a barrel

In the Eurozone GDP growth forecast at 1.7% in 2017 and

1.5% in 2018. Across the EU, GDP is forecast to expand

by 1.8% in 2017 and 1.6% in 2018.

Unemployment in the Eurozone at 9.5% in March 2017

(15.515mn people), stable compared to February 2017 and

down from 10.2 % in March 2016. Unemployment rate at

23.5% in Greece (youth 48.0%), 18.2% in Spain (youth

40.5%). Eurozone youth unemployment was 19.4% in

March 2017. Czech Republic unemployment rate at 3.2%,

Germany 3.9%.

Asia GDP growth forecast for 2017 at 4.6%. Malaysia:

GDP 2017 forecast at 4.5%; Vietnam: 2017 forecast at

6.7%; Singapore: GDP growth forecast at 2.7% in 2017;

South Korea: GDP growth forecast at 2.3% in 2017.

UK Commentary

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 4

South Korea: Q1 upside surprise masks underlying

weakness. The Korean economy expanded by 0.9% q/q

on a seasonally adjusted chain-linked basis in Q1, beating

all expectations. A pick-up in exports encouraged much

stronger private investment, while construction also held

up. Underlying concerns remain, especially with the pace

of private consumption, and policy is expected to remain

accommodative as external factors weigh on activity.

Japan: BoJ 2% inflation target, an improved outlook for

exports led the BoJ to upgrade its GDP growth forecasts to

1.4% for 2017.

China: 2017 GDP growth forecast raised to 6.5%. Solid

economic growth is still key government objective. China’s

economic growth picked up in the quarter of the year,

reflecting stronger investment and exports as well as

restocking in industry.

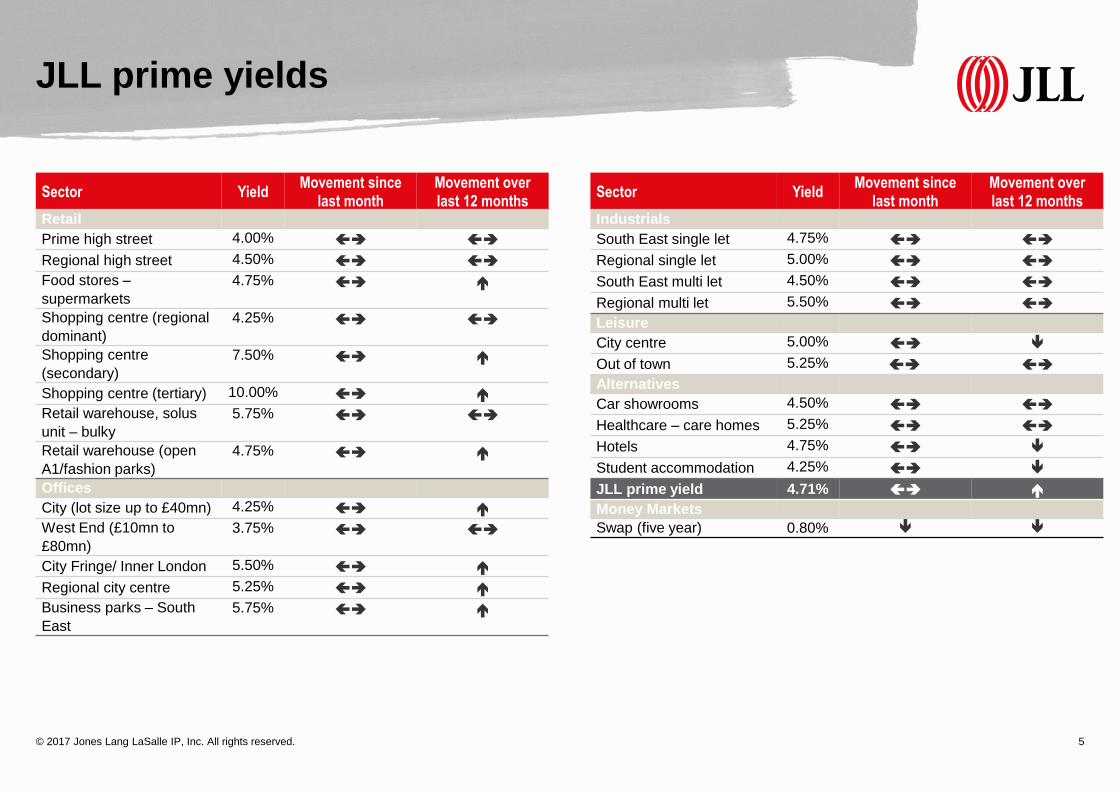

JLL prime yields

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 5

Sector YieldMovement since

last monthMovement over last 12 months

Retail

Prime high street 4.00%

Regional high street 4.50%

Food stores –

supermarkets

4.75%

Shopping centre (regional

dominant)

4.25%

Shopping centre

(secondary)

7.50%

Shopping centre (tertiary) 10.00%

Retail warehouse, solus

unit – bulky

5.75%

Retail warehouse (open

A1/fashion parks)

4.75%

Offices

City (lot size up to £40mn) 4.25%

West End (£10mn to

£80mn)

3.75%

City Fringe/ Inner London 5.50%

Regional city centre 5.25%

Business parks – South

East

5.75%

Sector YieldMovement since

last monthMovement over last 12 months

Industrials

South East single let 4.75%

Regional single let 5.00%

South East multi let 4.50%

Regional multi let 5.50%

Leisure

City centre 5.00%

Out of town 5.25%

Alternatives

Car showrooms 4.50%

Healthcare – care homes 5.25%

Hotels 4.75%

Student accommodation 4.25%

JLL prime yield 4.71%

Money Markets

Swap (five year) 0.80%

JLL prime yields

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 6

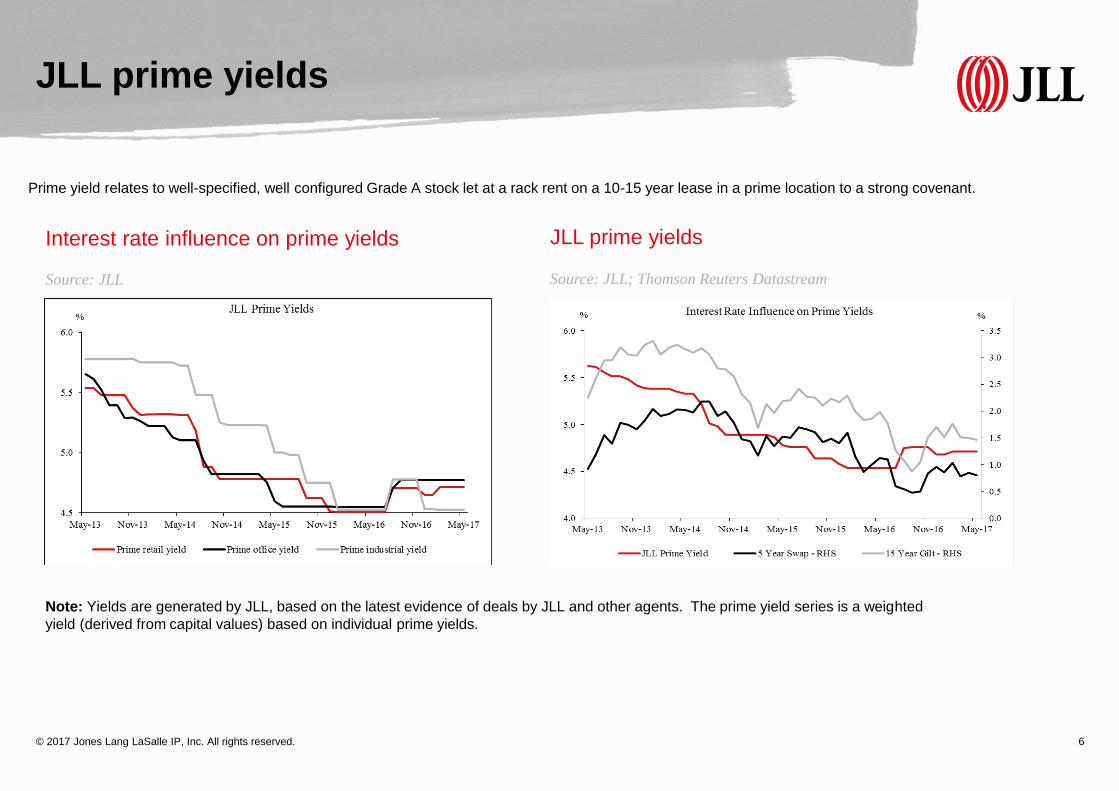

Prime yield relates to well-specified, well configured Grade A stock let at a rack rent on a 10-15 year lease in a prime location to a strong covenant.

Interest rate influence on prime yields

Source: JLL

JLL prime yields

Source: JLL; Thomson Reuters Datastream

Note: Yields are generated by JLL, based on the latest evidence of deals by JLL and other agents. The prime yield series is a weighted

yield (derived from capital values) based on individual prime yields.

JLL prime yields

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 7

The JLL Prime Yield remained unchanged through April, at

4.71%.

Investment turnover in the City and Docklands stands at

£3.25bn across 43 transactions, marginally up from the

£2.76bn that traded this time last year, although this year’s

figure has been somewhat inflated by the £1.15bn sale of The

Leadenhall Building in March. The total turnover for April was

£663.20mn across 8 transactions, considerably below that of

April 2016 which saw turnover of £1.25bn across 15

transactions. April this year saw only 3 deals transaction over

£20mn compared with 9 during April 2016. Key deals include

(i) Cannon Place, 78 Cannon Street, EC4 – bought by Deka,

a German Institution, for £485mn, reflecting a net initial yield

of 4.44% and a capital value of £1,206 psf. (ii) 22 Shand

Street Estate, SE1 – bought by Southwark Council for

£42.20mn, reflecting a net initial yield of 3.95% and a cap val

of £752 psf.

In the West End, year to date investment volumes stand at

£2,275mn across 32 transactions. The overwhelming demand

has come from Hong Kong and Chinese purchasers who

account for around 41% of total volumes. UK purchasers saw

a resurgence in April, accounting for 60% of volumes, up from

just 15% in Q1. There were 4 transactions in April totalling

£490mn, up from £200mn in March. Key deals include: (i) 13-

17 Fitzroy Street, W1 – sold off-market by Arup to the

Workspace Group for £98.5mn, at a NIY of 4.6% and £1,063

psf CV.

(ii) 8 Fitzroy Street, W1 –purchased off-market by Arup from

Derwent London. The price of c.£197mn reflects a NIY of

3.40% and CV of £1,332 psf. (iii) 3 St James’s Square, W1 –

sold by WELPUT to Joint Treasure, a Hong Kong family

office, for £135mn, at a NIY of 3.96% and a CV of £2,609 psf.

The South East investment market has experienced a

relatively slow start to the year with circa £400mn transacted.

With limited new stock on the market, much of this figure is

made up of hangover deals from 2016 and off market

transactions. Local authorities continue to be active in the

market, favouring well-let secure investments and acquiring

both inside and out of borough. In many cases the councils

have been outbidding overseas investors, as they benefit

from relatively low cost of capital. Authorities accounted for

circa 20% of acquisitions over the quarter. Key deals include

(i) Lucidus House, Watford – bought by M&G from British

Streel for £16.5mn at NIY of 6.75%. (ii) Academy Place,

Brentford – purchased by Threadneedle Investments for

£12M at a NIY of 7.00%. (iii) Queensbury, Brighton – also

purchased by Threadneedle Investments for £12.6mn at a

NIY of 6.5%.

In the high street investment market, we see a lot of

department stores coming to the market after disappointing

trading results. Department stores with strong fundamentals

and alternative uses are well received but those with limited

JLL prime yields

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. 8

other uses are struggling somewhat. Key deals include: (i) House of

Frazier, Chichester – acquired by Savills IM from Henderson Global

Investors for £13.4mn, reflecting 5.25% NIY.

In the shopping centre investment market, we are seeing increased

levels of market activity compared to 2016. Key deals include: (i)

Southside, Wandsworth – Delancey’s 50% stake sold to Invesco for

£150mn at 4.38% NIY. (ii) Arndale Centre, Eastbourne – sold by L&G to

Norinchukin Bank (Japan) for £100mn, at NIY of 5.75%.

In the industrial market, there was £1.4bn traded in Q1, 16% above Q4.

Sentiment is generally positive, but subdued stock levels are a

constraint. The relatively long leases available compared to other asset

classes continue to attract investors. Despite the lack of product in the

market, notable transactions during April included: (i) Centennial Park,

Elstree – JLL acted for the vendor, achieving a price of £28mn (4.75%

NIY), ahead of £22.4mn quote (6% NIY). (ii) Prologis, Middlewitch –

bought by Cabot for £13.35mn at 6.35% NIY.

The semi-annual De Montfort report on commercial property lending was

released at the end of April. Key points from the report include: (i)

Overall UK commercial property loan book grew by 0.5% y-o-y at end-

2016, despite uncertainty caused by EU referendum. (ii) £44.5bn new

loan originations completed in 2016, including £21.4bn in H1 and

£23.1bn in H2. This is 17% down on 2015. (iii) UK Banks & Building

Societies and Other Non-bank Lenders recorded higher loan book in

2016 than 2015, all other groups saw a reduction in total loan books.

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. The information contained in this document is proprietary to JLL and shall be used solely for the purposes of evaluating this proposal. All such documentation and

information remains the property of JLL and shall be kept confidential. Reproduction of any part of this document is authorized only to the extent necessary for its evaluation. It is not to be shown to any third party without the

prior written authorization of JLL. All information contained herein is from sources deemed reliable; however, no representation or warranty is made as to the accuracy thereof.

Jll.co.uk

Contacts

9

London | Hugo [email protected] | 020 7087 5859

North West | Tim Luckman [email protected] | 0161 828 6426

North East | Simon [email protected] | 0113 235 5241

Midlands | James [email protected] | 0121 214 9902

South West | Daniel Bishop [email protected] | 0117 930 5991

Scotland | Niall [email protected] | 0141 567 6647

Recommended