1-1

McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

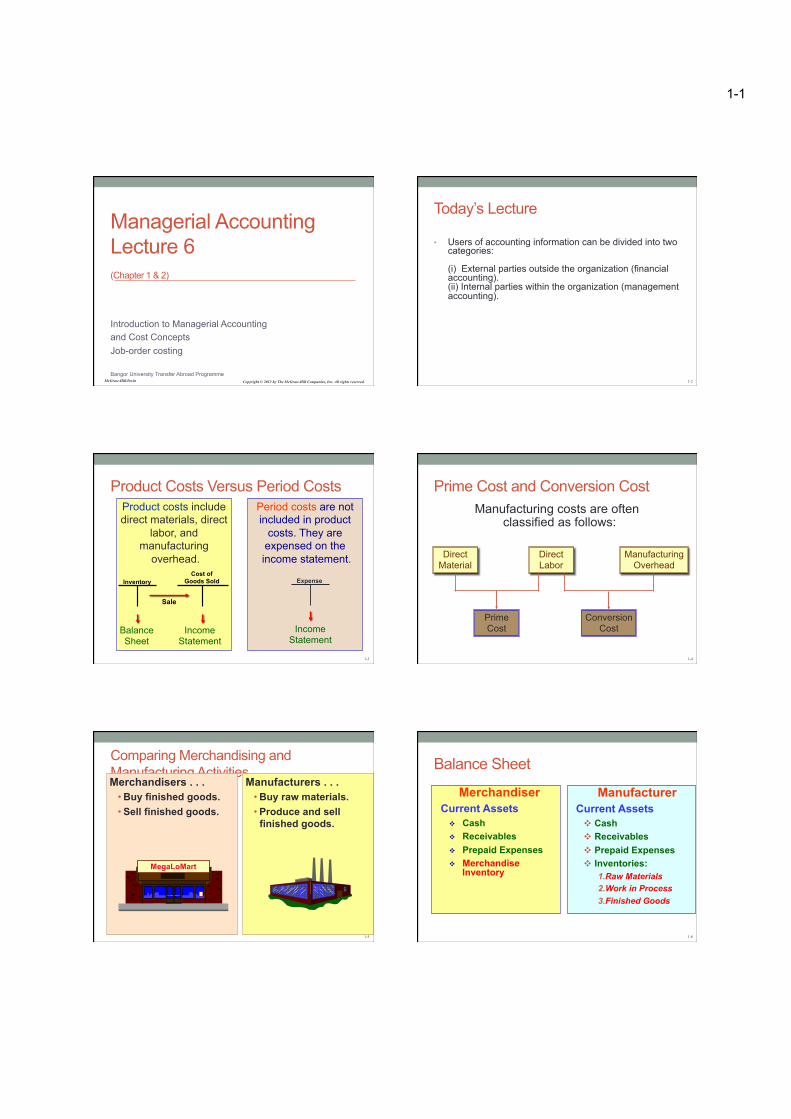

Managerial Accounting Lecture 6 (Chapter 1 & 2)

Introduction to Managerial Accounting and Cost Concepts Job-order costing Bangor University Transfer Abroad Programme

1-2

Today’s Lecture • Users of accounting information can be divided into two

categories: (i) External parties outside the organization (financial accounting). (ii) Internal parties within the organization (management accounting).

1-3

Product Costs Versus Period Costs

Inventory Cost of

Goods Sold

Balance Sheet

Income Statement

Sale

Product costs include direct materials, direct

labor, and manufacturing

overhead.

Period costs are not included in product

costs. They are expensed on the income statement.

Expense

Income Statement

1-4

Prime Cost and Conversion Cost

Direct Material

Direct Labor

Manufacturing Overhead

Prime Cost

Conversion Cost

Manufacturing costs are often classified as follows:

1-5

Comparing Merchandising and Manufacturing Activities Merchandisers . . .

• Buy finished goods. • Sell finished goods.

Manufacturers . . . • Buy raw materials. • Produce and sell

finished goods.

MegaLoMart

1-6

Balance Sheet

Merchandiser Current Assets

v Cash v Receivables v Prepaid Expenses v Merchandise

Inventory

Manufacturer Current Assets Cash Receivables Prepaid Expenses Inventories:

1. Raw Materials 2. Work in Process 3. Finished Goods

1-2

1-7

Merchandiser Current Assets

v Cash v Receivables v Prepaid Expenses v Merchandise

Inventory

Manufacturer Current Assets Cash Receivables Prepaid Expenses Inventories:

1. Raw Materials 2. Work in Process 3. Finished Goods

Balance Sheet

Partially complete products – some material, labor, or

overhead has been added.

Completed products awaiting sale.

Materials waiting to be processed.

1-8

The Income Statement Cost of goods sold for manufacturers

differs only slightly from cost of goods sold for merchandisers.

Manufacturing CompanyCost of goods sold: Beg. finished goods inv. 14,200$ + Cost of goods manufactured 234,150 Goods available for sale 248,350$ - Ending finished goods inventory (12,100) = Cost of goods sold 236,250$

Merchandising CompanyCost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goods sold 236,250$

1-9

Inventory Flows

Beginning balance

Additions to inventory + = Ending

balance

Withdrawals from

inventory +

1-10

Schedule of Cost of Goods Manufactured

Calculates the cost of raw material, direct labor and

manufacturing overhead used in production.

Calculates the manufacturing costs associated with goods that were finished during the

period.

1-11

Manufacturing WorkRaw Materials Costs In Process

Beginning raw materials inventory

+ Raw materials purchased

= Raw materials available for use in production

– Ending raw materials inventory

= Raw materials used in production

As items are removed from raw materials inventory and placed into the production

process, they are called direct materials.

Schedule of Cost of Goods Manufactured

1-12

Manufacturing WorkRaw Materials Costs In Process

Beginning raw Direct materials materials inventory + Direct labor

+ Raw materials + Mfg. overhead purchased = Total manufacturing

= Raw materials costs available for use in production

– Ending raw materials inventory

= Raw materials used in production

Conversion costs are costs

incurred to convert the

direct material into a finished

product.

As items are removed from raw materials inventory and placed into

the production process, they are called direct materials.

Schedule of Cost of Goods Manufactured

1-3

1-13

Manufacturing WorkRaw Materials Costs In Process

Beginning raw Direct materials Beginning work in materials inventory + Direct labor process inventory

+ Raw materials + Mfg. overhead + Total manufacturing purchased = Total manufacturing costs

= Raw materials costs = Total work in available for use process for the in production period

– Ending raw materials – Ending work in inventory process inventory

= Raw materials used = Cost of goods in production manufactured.

All manufacturing costs incurred during the period are added to the

beginning balance of work in process.

Schedule of Cost of Goods Manufactured

1-14

Manufacturing WorkRaw Materials Costs In Process

Beginning raw Direct materials Beginning work in materials inventory + Direct labor process inventory

+ Raw materials + Mfg. overhead + Total manufacturing purchased = Total manufacturing costs

= Raw materials costs = Total work in available for use process for the in production period

– Ending raw materials – Ending work in inventory process inventory

= Raw materials used = Cost of goods in production manufactured.

Costs associated with the goods that are completed during the period are

transferred to finished goods inventory.

Schedule of Cost of Goods Manufactured

1-15

WorkIn Process Finished Goods

Beginning work in Beginning finished process inventory goods inventory

+ Manufacturing costs + Cost of goods for the period manufactured

= Total work in process = Cost of goods for the period available for sale

– Ending work in - Ending finished process inventory goods inventory

= Cost of goods Cost of goods manufactured sold

Cost of Goods Sold

1-16

Manufacturing Cost Flows

Selling and Administrative

Period Costs

Finished Goods

Cost of Goods Sold

Selling and Administrative

Manufacturing Overhead

Work in Process

Direct Labor

Balance Sheet Costs Inventories

Income Statement Expenses Material Purchases Raw Materials

1-17

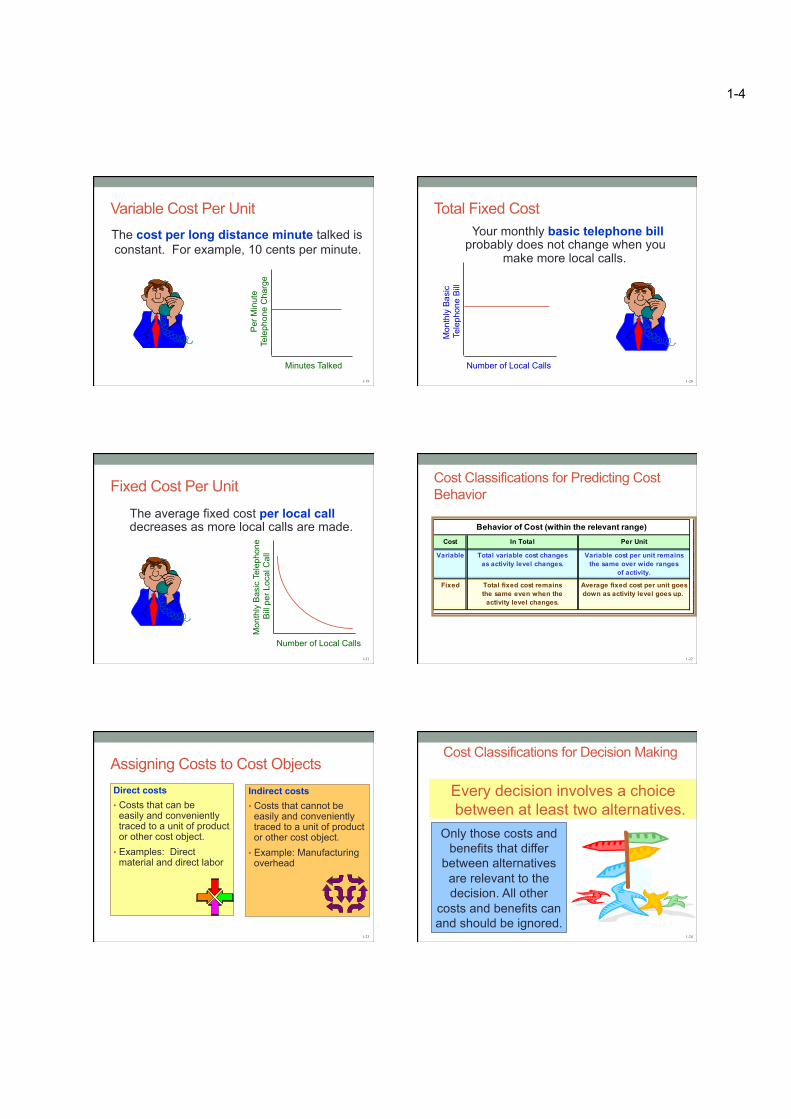

Cost Classifications for Predicting Cost Behavior

How a cost will react to changes in the level of

business activity. v Total variable costs

change when activity changes.

v Total fixed costs remain unchanged when activity changes.

1-18

Total Variable Cost

Your total long distance telephone bill is based on how many minutes you talk.

Minutes Talked

Tota

l Lon

g D

ista

nce

Tele

phon

e B

ill

1-4

1-19

Variable Cost Per Unit

Minutes Talked

Per

Min

ute

Tele

phon

e C

harg

e

The cost per long distance minute talked is constant. For example, 10 cents per minute.

1-20

Total Fixed Cost Your monthly basic telephone bill probably does not change when you

make more local calls.

Number of Local Calls

Mon

thly

Bas

ic

Tele

phon

e B

ill

1-21

Fixed Cost Per Unit

Number of Local Calls

Mon

thly

Bas

ic T

elep

hone

B

ill p

er L

ocal

Cal

l

The average fixed cost per local call decreases as more local calls are made.

1-22

Cost Classifications for Predicting Cost Behavior

Behavior of Cost (within the relevant range)Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remainsas activity level changes. the same over wide ranges

of activity.

Fixed Total fixed cost remains Average fixed cost per unit goesthe same even when the down as activity level goes up.

activity level changes.

1-23

Assigning Costs to Cost Objects Direct costs • Costs that can be

easily and conveniently traced to a unit of product or other cost object.

• Examples: Direct material and direct labor

Indirect costs • Costs that cannot be

easily and conveniently traced to a unit of product or other cost object.

• Example: Manufacturing overhead

1-24

Cost Classifications for Decision Making

Every decision involves a choice between at least two alternatives.

Only those costs and benefits that differ

between alternatives are relevant to the decision. All other

costs and benefits can and should be ignored.

1-5

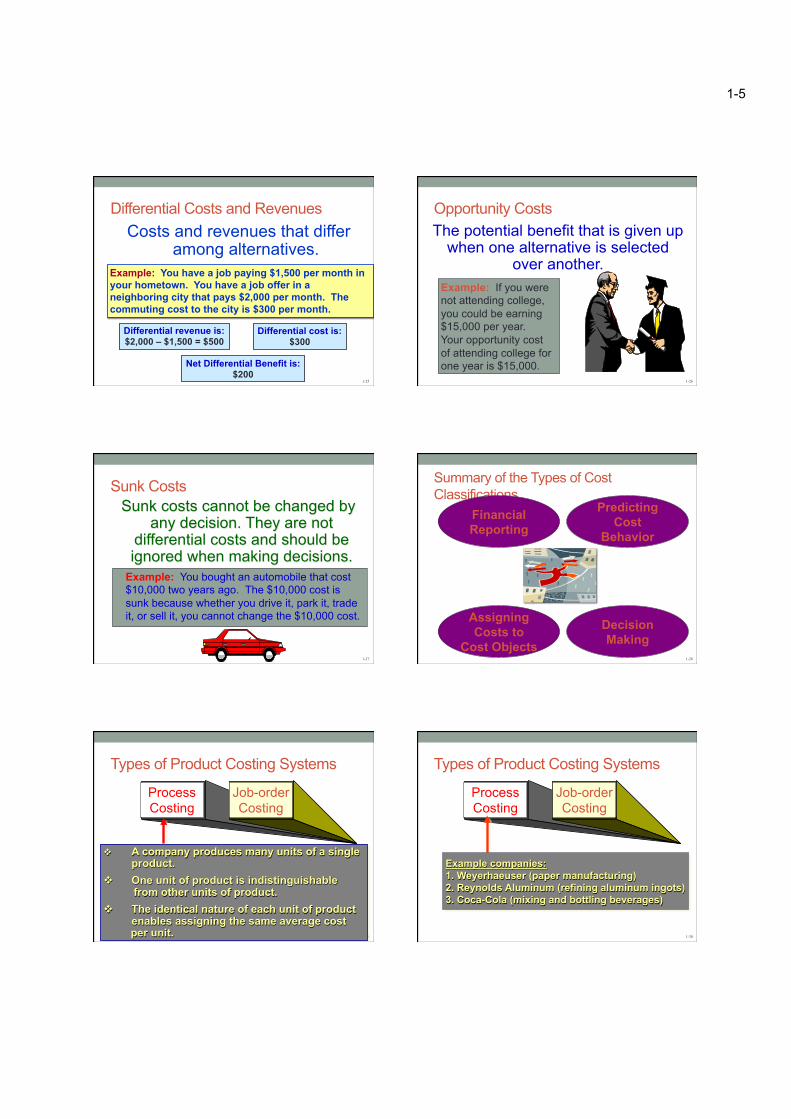

1-25

Differential Costs and Revenues Costs and revenues that differ

among alternatives. Example: You have a job paying $1,500 per month in your hometown. You have a job offer in a neighboring city that pays $2,000 per month. The commuting cost to the city is $300 per month.

Differential revenue is: $2,000 – $1,500 = $500

Differential cost is: $300

Net Differential Benefit is: $200

1-26

Opportunity Costs The potential benefit that is given up

when one alternative is selected over another.

Example: If you were not attending college, you could be earning $15,000 per year. Your opportunity cost of attending college for one year is $15,000.

1-27

Sunk Costs Sunk costs cannot be changed by

any decision. They are not differential costs and should be ignored when making decisions.

Example: You bought an automobile that cost $10,000 two years ago. The $10,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $10,000 cost.

1-28

Summary of the Types of Cost Classifications

Financial Reporting

Predicting Cost

Behavior

Assigning Costs to

Cost Objects

Decision Making

1-29

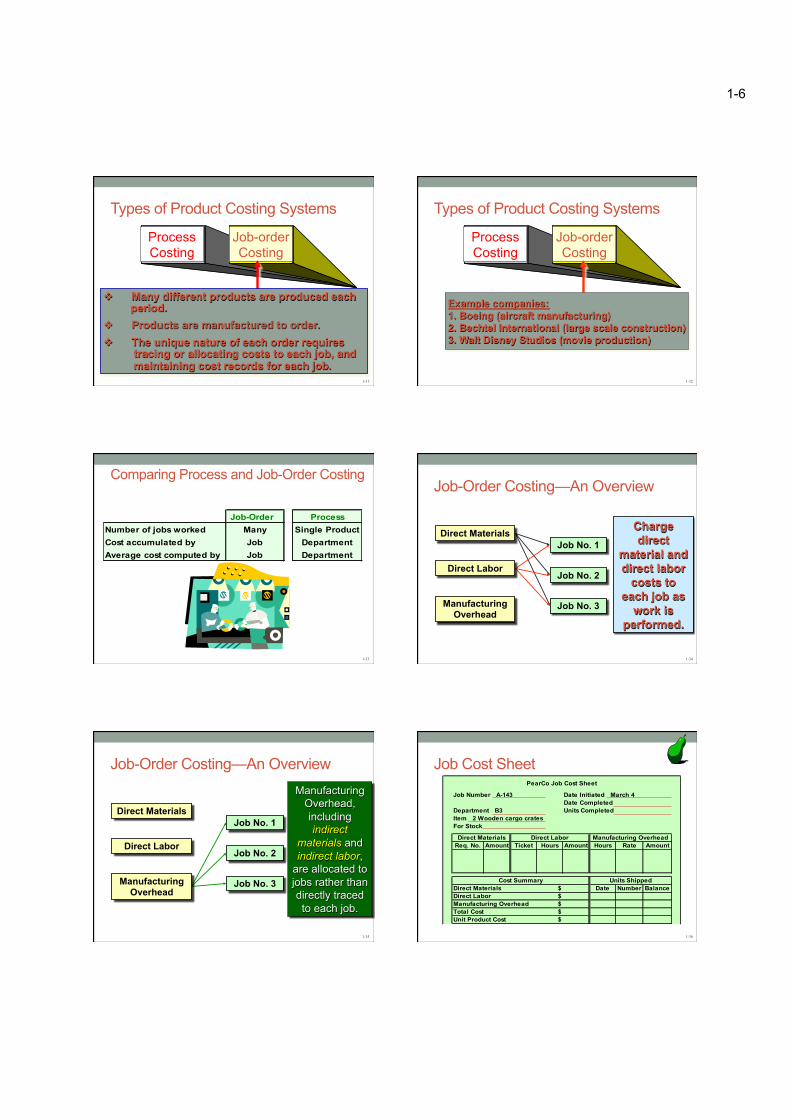

Types of Product Costing Systems

Process Costing

Job-order Costing

v A company produces many units of a single product.

v One unit of product is indistinguishable from other units of product. v The identical nature of each unit of product

enables assigning the same average cost per unit. 1-30

Types of Product Costing Systems

Process Costing

Job-order Costing

Example companies: 1. Weyerhaeuser (paper manufacturing) 2. Reynolds Aluminum (refining aluminum ingots) 3. Coca-Cola (mixing and bottling beverages)

1-6

1-31

Types of Product Costing Systems

Process Costing

Job-order Costing

v Many different products are produced each period. v Products are manufactured to order. v The unique nature of each order requires tracing or allocating costs to each job, and maintaining cost records for each job.

1-32

Types of Product Costing Systems

Process Costing

Job-order Costing

Example companies: 1. Boeing (aircraft manufacturing) 2. Bechtel International (large scale construction) 3. Walt Disney Studios (movie production)

1-33

Comparing Process and Job-Order Costing

Job-Order ProcessNumber of jobs worked Many Single ProductCost accumulated by

Individual Job Department

Average cost computed by Job Department

1-34

Manufacturing Overhead

Job No. 1

Job No. 2

Job No. 3

Charge direct

material and direct labor

costs to each job as

work is performed.

Job-Order Costing—An Overview

Direct Materials

Direct Labor

1-35

Manufacturing Overhead, including indirect

materials and indirect labor,

are allocated to jobs rather than directly traced to each job.

Job-Order Costing—An Overview

Direct Materials

Direct Labor

Job No. 1

Job No. 2

Job No. 3 Manufacturing Overhead

1-36

Job Cost Sheet PearCo Job Cost Sheet

Job Number A-143 Date Initiated March 4Date Completed

Department B3 Units CompletedItem 2 Wooden cargo cratesFor Stock

Direct Materials Direct Labor Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate Amount

Cost Summary Units ShippedDirect Materials $ Date Number BalanceDirect Labor $Manufacturing Overhead $Total Cost $Unit Product Cost $

1-7

1-37

Materials Requisition Form PearCo Materials Requisition Form

Materials Requisition Number X7 - 6890 Date March 4Job Number to Be Charged A - 143Department B3

Description Quantity Unit Cost Total Cost2 x 4, 12 feet 12 3.00$ 36.00$ 1 x 6, 12 feet 20 4.00 80.00

116.00$

AuthorizedSignature Will$E .$D elite

1-38

Job Cost Sheet PearCo Job Cost Sheet

Job Number A-143 Date Initiated March 4Date Completed

Department B3 Units CompletedItem 2 Wooden cargo cratesFor Stock

Direct Materials Direct Labor Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7 - 6890 116$

Cost Summary Units ShippedDirect Materials $ Date Number BalanceDirect Labor $Manufacturing Overhead $Total Cost $Unit Product Cost $

1-39

Employee Time Ticket PearCo Employee Time Ticket

Time Ticket No. 36 Date March 5

Employee I. M. Skilled Station 42

TimeStarted Ended Completed Rate Amount Job No.

8:00 12:00 4.0 11.00$ 44.00$ A-1431:00 5:00 4.0 11.00 44.00 A-143

Totals 8.00 88.00$

Supervisor C . M. W o rk m a n

1-40

Job Cost Sheet PearCo Job Cost Sheet

Job Number A-143 Date Initiated March 4Date Completed

Department B3 Units CompletedItem 2 Wooden cargo cratesFor Stock

Direct Materials Direct Labor Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7 - 6890 116$ 36 8 88$

Cost Summary Units ShippedDirect Materials $ Date Number BalanceDirect Labor $Manufacturing Overhead $Total Cost $Unit Product Cost $

1-41

Application of Manufacturing Overhead Manufacturing overhead is applied to jobs that

are in process. An allocation base, such as direct labor hours, direct labor dollars, or

machine hours, is used to assign manufacturing overhead to individual jobs.

We use an allocation base because:

1. It is impossible or difficult to trace overhead costs to particular jobs.

2. Manufacturing overhead consists of many different items ranging from the grease used in machines to a production manager’s salary.

3. Many types of manufacturing overhead costs are fixed even though output fluctuates during the period.

1-42

Tutorial n Review of today’s and last week’s lecture

n Complete Review Problems n 1-6 n 1-13

Recommended