EXECUTIVE SUMMARY

1.0 INTRODUCTION 1.1 Overview of the titanium metal industry 1.2 Structure of report 1.3 Confidentialityanddisclaimer

2.0 TITANIUM METAL INDUSTRY OVERVIEW 2.1 The titanium metal supply chain 2.2 History of the titanium metal sector 2.3 Titanium metal products – overview 2.4 End-market applications 2.5 Associated markets

3.0 PROPERTIES AND NATURE OF TITANIUM 3.1 Titanium bearing resources 3.2 Mining and processing of titanium feedstocks 3.3 Beneficiatedtitaniumproducts3.4 Titanium feedstock production in 2013 3.5 Properties of titanium 3.6 Comparison with other metals 3.7 Processing, alloys and compounds

4.0 MANUFACTURE OF TITANIUM PRODUCTS 4.1 Titanium tetrachloride production 4.2 Titanium sponge production 4.3 Melting techniques 4.4 Mill processing 4.5 Titanium powder manufacture 4.6 Titanium recycling

5.0 ECONOMICS OF TITANIUM METAL MANUFACTURE

5.1 Methodology 5.2 Overall industry cost structure 5.3 Costs of TiCl4 production 5.4 Costs of titanium sponge production 5.5 Major cost drivers and trends.

6.0 DEMAND FOR TITANIUM 6.1 Demand in end-use sectors 6.2 Commercial aerospace6.3 Industrial sector 6.4 Defence 6.5 Emerging applications

7.0 SUPPLY OF TITANIUM 7.1 Supply developments in 2013 7.2 Regional distribution

8.0 INTERNATIONAL TRADE AND PRICING 8.1 Internationaltradeflows8.2 Duties and tariffs8.3-8.16 US Japan, China, Russia, Kazakhstan, Ukraine,

Germany, France, UK, Italy, The Netherlands, Austria, Spain, South Korea, Taiwan

8.18 Other countries

9.0 EMERGING TITANIUM METAL TECHNOLOGIES9.1 Overview of new extraction technologies 9.2 Cost advantages of new extraction technologies 9.3 Titanium quality in new processes 9.4 Powder consolidation, ally and product development 9.5 Solid freeform fabrication 9.6 Trends in emerging technologies

10.0 INDUSTRY TRENDS AND OUTLOOK 10.1 Current themes 10.2 The global titanium industry 10.3 Commercial aerospace market 10.4 Industrial markets 10.5 Defence markets 10.6 New technologies

APPENDIX 1 - PRODUCER PROFILES

For more information contact TZMI | +61 8 9359 6000 | [email protected] | tzmi.com

TITANIUM METAL ANNUAL REVIEW SAMPLE

NEW EDITION OUT NOW!

TABLE OF CONTENTS

SAMPLE OF 2013 EDITION

OVERVIEW OF TITANIUM AND THE TITANIUM INDUSTRY

The multi billion dollar titanium metal market is examined from the perspective of the entire value chain.

US$110 million titanium

feedstock market

US$2.94 billion titanium sponge market

US$5.41 billion milled

products market

T Z M I6

TiTanium meTal annual Review 2013

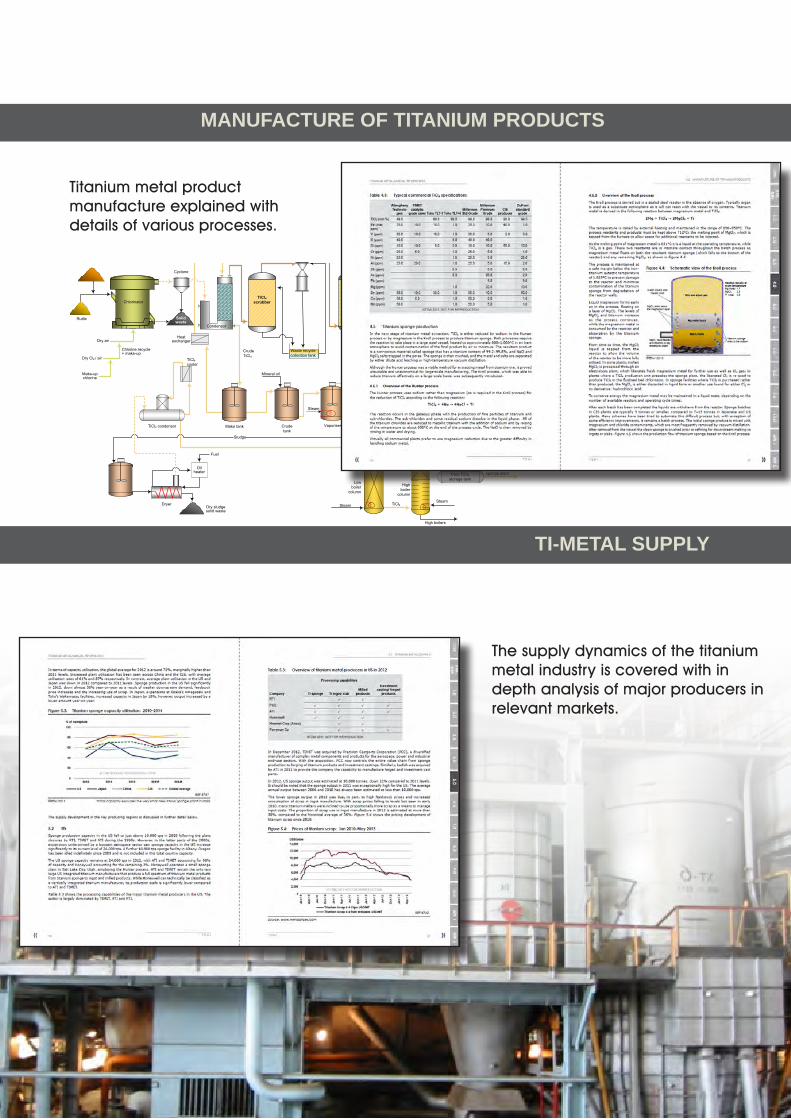

andcarbon,andheatedtomorethan900°C.ThisresultsinthecreationofTiCl4andamixtureofcarbondioxideandcarbonmonoxide.

Purification: The TiCl4isdistilledtoremoveanyremainingimpuritiessuchasvanadium,zirconium,silicon,magnesiumandanyresidualiron.

Sponge production:Oncetheimpuritieshavebeenremoved,theTiCl4isreactedwithmagnesiumat1,100°C.Argonispumpedintothecontainertopreventcontaminationwithoxygenornitrogen.Thereactionproducessolidtitaniumandmagnesiumchloride,whichisremovedfromthereactorbyboringandthentreatedtoremoveexcessmagnesiumandmagnesiumchloride.

Theresultantsolidisaporousmetalcalledasponge.

Alloy creation:Thetitaniumspongeiscombinedwiththealloyadditionsinanelectrodearcfurnacetocreatevariousalloys.Typically,aningotisre-meltedmultipletimestoproduceacommercially-acceptablegrade.

MoredetailregardingtheseprocessingstepsisprovidedinChapter 4.

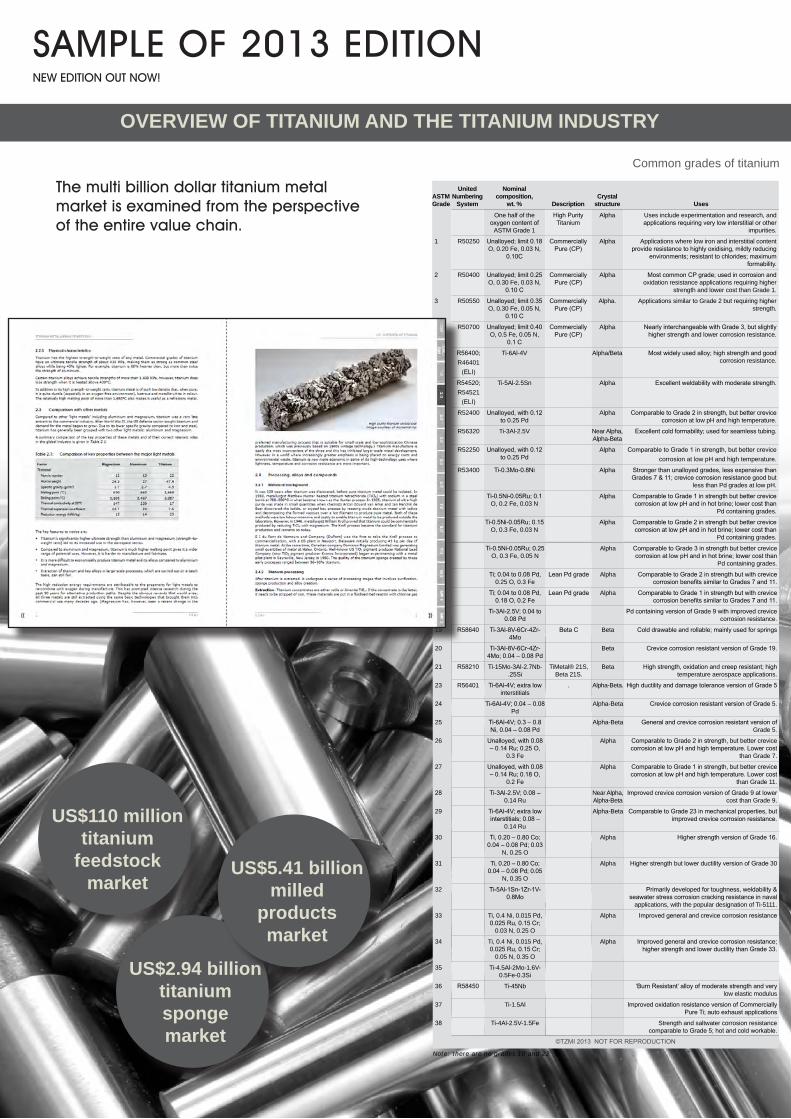

Table 2.2: Common grades of titanium

Astm Grade

united numbering

system

nominal composition,

wt. % descriptioncrystal

structure uses

One half of the oxygen content of

ASTM Grade 1

High Purity Titanium

Alpha Uses include experimentation and research, and applications requiring very low interstitial or other

impurities.

1 R50250 Unalloyed; limit 0.18 O, 0.20 Fe, 0.03 N,

0.10C

Commercially Pure (CP)

Alpha Applications where low iron and interstitial content provide resistance to highly oxidising, mildly reducing

environments; resistant to chlorides; maximum formability.

2 R50400 Unalloyed; limit 0.25 O, 0.30 Fe, 0.03 N,

0.10 C

Commercially Pure (CP)

Alpha Most common CP grade; used in corrosion and oxidation resistance applications requiring higher

strength and lower cost than Grade 1.

3 R50550 Unalloyed; limit 0.35 O, 0.30 Fe, 0.05 N,

0.10 C

Commercially Pure (CP)

Alpha. Applications similar to Grade 2 but requiring higher strength.

4 R50700 Unalloyed; limit 0.40 O, 0.5 Fe, 0.05 N,

0.1 C

Commercially Pure (CP)

Alpha Nearly interchangeable with Grade 3, but slightly higher strength and lower corrosion resistance.

5 R56400; R46401

(ELI)

Ti-6Al-4V Alpha/Beta Most widely used alloy; high strength and good corrosion resistance.

6 R54520; R54521

(ELI)

Ti-5Al-2.5Sn Alpha Excellent weldability with moderate strength.

7 R52400 Unalloyed, with 0.12 to 0.25 Pd

Alpha Comparable to Grade 2 in strength, but better crevice corrosion at low pH and high temperature.

9 R56320 Ti-3Al-2.5V Near Alpha, Alpha-Beta

Excellent cold formability; used for seamless tubing.

11 R52250 Unalloyed, with 0.12 to 0.25 Pd

Alpha Comparable to Grade 1 in strength, but better crevice corrosion at low pH and high temperature.

12 R53400 Ti-0.3Mo-0.8Ni Alpha Stronger than unalloyed grades, less expensive than Grades 7 & 11; crevice corrosion resistance good but

less than Pd grades at low pH.

13 Ti-0.5Ni-0.05Ru; 0.1 O, 0.2 Fe, 0.03 N

Alpha Comparable to Grade 1 in strength but better crevice corrosion at low pH and in hot brine; lower cost than

Pd containing grades.

14 Ti-0.5Ni-0.05Ru; 0.15 O, 0.3 Fe, 0.03 N

Alpha Comparable to Grade 2 in strength but better crevice corrosion at low pH and in hot brine; lower cost than

Pd containing grades.

«

7T Z M I

2.0 OvervIew Of TITanIuM

Astm Grade

united numbering

system

nominal composition,

wt. % descriptioncrystal

structure uses

15 Ti-0.5Ni-0.05Ru; 0.25 O, 0.3 Fe, 0.05 N

Alpha Comparable to Grade 3 in strength but better crevice corrosion at low pH and in hot brine; lower cost than

Pd containing grades.

16 Ti; 0.04 to 0.08 Pd, 0.25 O, 0.3 Fe

Lean Pd grade Alpha Comparable to Grade 2 in strength but with crevice corrosion benefits similar to Grades 7 and 11.

17 Ti; 0.04 to 0.08 Pd, 0.18 O, 0.2 Fe

Lean Pd grade Alpha Comparable to Grade 1 in strength but with crevice corrosion benefits similar to Grades 7 and 11.

18 Ti-3Al-2.5V; 0.04 to 0.08 Pd

Pd containing version of Grade 9 with improved crevice corrosion resistance.

19 R58640 Ti-3Al-8V-6Cr-4Zr-4Mo

Beta C Beta Cold drawable and rollable; mainly used for springs

20 Ti-3Al-8V-6Cr-4Zr-4Mo; 0.04 – 0.08 Pd

Beta Crevice corrosion resistant version of Grade 19.

21 R58210 Ti-15Mo-3Al-2.7Nb-.25Si

TiMetal® 21S, Beta 21S.

Beta High strength, oxidation and creep resistant; high temperature aerospace applications.

23 R56401 Ti-6Al-4V; extra low interstitials

. Alpha-Beta. High ductility and damage tolerance version of Grade 5

24 Ti-6Al-4V; 0.04 – 0.08 Pd

Alpha-Beta Crevice corrosion resistant version of Grade 5.

25 Ti-6Al-4V; 0.3 – 0.8 Ni, 0.04 – 0.08 Pd

Alpha-Beta General and crevice corrosion resistant version of Grade 5.

26 Unalloyed, with 0.08 – 0.14 Ru; 0.25 O,

0.3 Fe

Alpha Comparable to Grade 2 in strength, but better crevice corrosion at low pH and high temperature. Lower cost

than Grade 7.

27 Unalloyed, with 0.08 – 0.14 Ru; 0.18 O,

0.2 Fe

Alpha Comparable to Grade 1 in strength, but better crevice corrosion at low pH and high temperature. Lower cost

than Grade 11.

28 Ti-3Al-2.5V; 0.08 – 0.14 Ru

Near Alpha, Alpha-Beta

Improved crevice corrosion version of Grade 9 at lower cost than Grade 9.

29 Ti-6Al-4V; extra low interstitials; 0.08 –

0.14 Ru

Alpha-Beta Comparable to Grade 23 in mechanical properties, but improved crevice corrosion resistance.

30 Ti, 0.20 – 0.80 Co; 0.04 – 0.08 Pd; 0.03

N, 0.25 O

Alpha Higher strength version of Grade 16.

31 Ti, 0.20 – 0.80 Co; 0.04 – 0.08 Pd; 0.05

N, 0.35 O

Alpha Higher strength but lower ductility version of Grade 30

32 Ti-5Al-1Sn-1Zr-1V-0.8Mo

Primarily developed for toughness, weldability & seawater stress corrosion cracking resistance in naval

applications, with the popular designation of Ti-5111.

33 Ti, 0.4 Ni, 0.015 Pd, 0.025 Ru, 0.15 Cr;

0.03 N, 0.25 O

Alpha Improved general and crevice corrosion resistance

34 Ti, 0.4 Ni, 0.015 Pd, 0.025 Ru, 0.15 Cr;

0.05 N, 0.35 O

Alpha Improved general and crevice corrosion resistance; higher strength and lower ductility than Grade 33.

35 Ti-4.5Al-2Mo-1.6V-0.5Fe-0.3Si

36 R58450 Ti-45Nb ‘Burn Resistant’ alloy of moderate strength and very low elastic modulus

37 Ti-1.5Al Improved oxidation resistance version of Commercially Pure Ti; auto exhaust applications

38 Ti-4Al-2.5V-1.5Fe Strength and saltwater corrosion resistance comparable to Grade 5; hot and cold workable.

©TZMI 2013 NOT FOR REPROdUCTION

Note: there are no grades 10 and 22

»

APP. 1

APP. 2

ExEc

SumC

ON

T1.0

3.04.0

5.06.0

7.08.0

9.010.0

2.0

Common grades of titanium

NEW EDITION OUT NOW!

MANUFACTURE OF TITANIUM PRODUCTS

The supply dynamics of the titanium metal industry is covered with in depth analysis of major producers in relevant markets.

TI-METAL SUPPLY

Heat exchanger

High boiler

column

Heat exchanger

TiCl4 condensor

Dryer

Treated distillate tank

Coke

Rutile

Cyclone

Condensor

Solid waste

Venturi scrubber

Waste recycle collection tank

SOx scrubber

Steam

Scrub liquor recirculation

tank

Caustic recirculation

tank

Sludge

Make-up chlorine

Chlorine recycle + make-up

Dry Cl2 / air

Dry air

Oil heater

Chlorinator

Fuel

Low boiler

column

Heat exchanger

Pure TiCl4 to sponge plant

Steam

Dry sludge solid waste

CO incinerator and waste heat boiler

TiCl4

Clean gas

Stack

Mineral oil

TiCl4

TiCl4cooler

CrudeTiCl4

High boilers

Low boilers

Water

VaporiserCrude tank

Make tank

TiCl4scrubber

Chlorine scrubber

SteamSteam

Pure TiCl4storage tank

Titanium metal product manufacture explained with details of various processes.

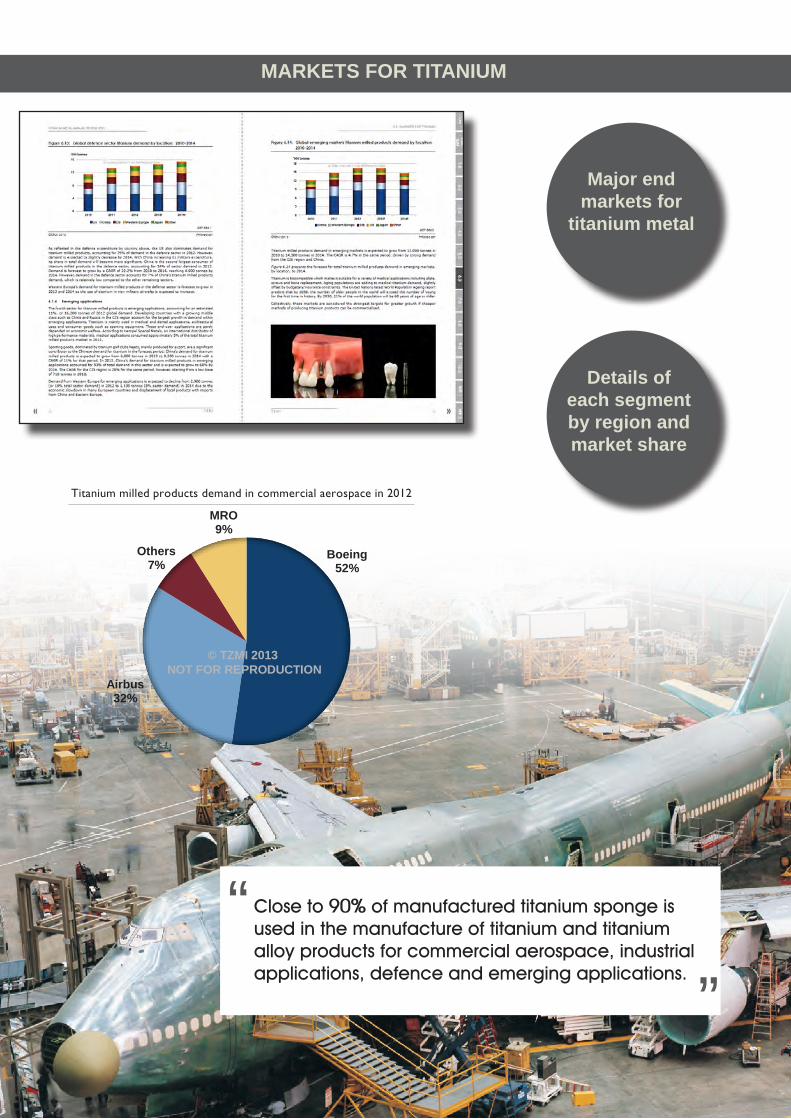

MARKETS FOR TITANIUM

Boeing52%

Airbus32%

Others7%

MRO9%

© TZMI 2013 NOT FOR REPRODUCTION

Titanium milled products demand in commercial aerospace in 2012

Close to 90% of manufactured titanium sponge is used in the manufacture of titanium and titanium alloy products for commercial aerospace, industrial applications, defence and emerging applications.

“”

Major end markets for

titanium metal

Details of each segment by region and market share

ECONOMICS OF PRODUCTION

Supply dynamics

Regional analysis by

segment

Cost inputs by

region and segment

Demand drivers

Manufacturing costs

removed for sam

ple editionSUPPLY AND DEMAND

INDUSTRY TRENDS AND OUTLOOK

EMERGING TECHNOLOGIES

Updates on developments

Strategic issues for the

industry

New processes

Key challenges

in the future

New technology

Outlook for titanium metal

markets

APPENDIX

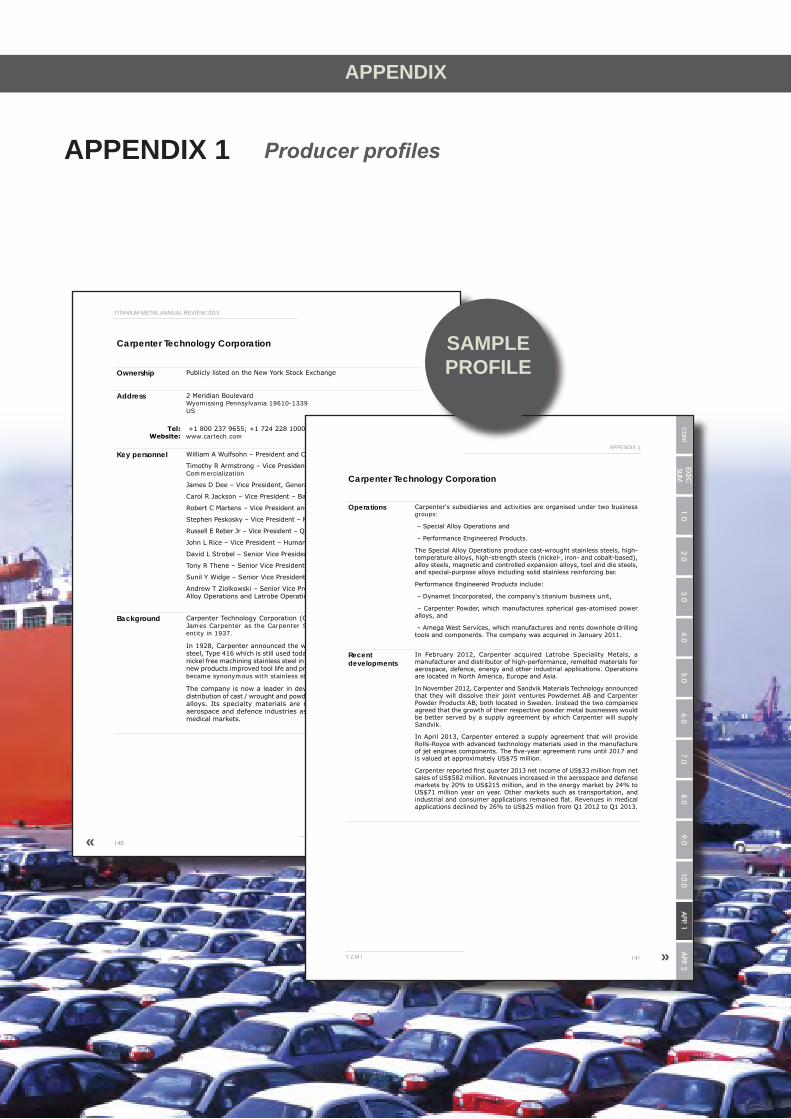

APPENDIX 1 Producer profiles

T Z M I140

TiTanium meTal annual Review 2013

Carpenter Technology Corporation

Ownership PubliclylistedontheNewYorkStockExchange

Address 2MeridianBoulevardWyomissing Pennsylvania 19610-1339US

Tel:Website:

+18002379655;+17242281000 www.cartech.com

Key personnel WilliamAWulfsohn–PresidentandChiefExecutiveOfficer

TimothyRArmstrong–VicePresident–ResearchandProductCommercialization

JamesDDee–VicePresident,GeneralCounselandSecretary

CarolRJackson–VicePresident–Bar,Wire,StripandPlateProducts

RobertCMartens–VicePresidentandChiefInformationOfficer

StephenPeskosky–VicePresident–ForgedBarandBilletBusinessGroup

RussellEReberJr–VicePresident–Quality,Technical&CustomerService

JohnLRice–VicePresident–HumanResources

DavidLStrobel–SeniorVicePresident–GlobalOperations

TonyRThene–SeniorVicePresidentandChiefFinancialOfficer

SunilYWidge–SeniorVicePresident–StrategicBusiness

AndrewTZiolkowski–SeniorVicePresident–Commercial,SpecialityAlloyOperationsandLatrobeOperations

Background CarpenterTechnologyCorporation(Carpenter)wasfoundedin1889byJames Carpenter as the Carpenter Steel Company. It became a public entity in 1937.

In1928,Carpenterannouncedtheworld'sfirstfreemachiningstainlesssteel,Type416whichisstillusedtodayandfollowedwiththefirstchromenickelfreemachiningstainlesssteelin1934,knowntodayasType303.Thenewproductsimprovedtoollifeandproductivityandasaresult,Carpenterbecame synonymous with stainless steels.

Thecompanyisnowaleaderindeveloping,manufacturingandinthedistributionofcast/wroughtandpowdermetalstainlesssteelandspecialityalloys. Its specialtymaterials aremanufactured for the automotive,aerospaceanddefenceindustriesaswellasforenergy,industrialandmedicalmarkets.

«

141T Z M I

APPendIx 1

Carpenter Technology Corporation

Operations Carpenter'ssubsidiariesandactivitiesareorganisedundertwobusinessgroups:

–SpecialAlloyOperationsand

–PerformanceEngineeredProducts.

TheSpecialAlloyOperationsproducecast-wroughtstainlesssteels,high-temperaturealloys,high-strengthsteels(nickel-,iron-andcobalt-based),alloysteels,magneticandcontrolledexpansionalloys,toolanddiesteels,andspecial-purposealloysincludingsolidstainlessreinforcingbar.

PerformanceEngineeredProductsinclude:

–DynametIncorporated,thecompany'stitaniumbusinessunit,

–CarpenterPowder,whichmanufacturessphericalgas-atomisedpoweralloys,and

–AmegaWestServices,whichmanufacturesandrentsdownholedrillingtoolsandcomponents.ThecompanywasacquiredinJanuary2011.

Recent developments

In February 2012, Carpenter acquired Latrobe Speciality Metals, amanufactureranddistributorofhigh-performance,remeltedmaterialsforaerospace,defence,energyandotherindustrialapplications.OperationsarelocatedinNorthAmerica,EuropeandAsia.

InNovember2012,CarpenterandSandvikMaterialsTechnologyannouncedthattheywilldissolvetheirjointventuresPowdernetABandCarpenterPowderProductsAB,bothlocatedinSweden.InsteadthetwocompaniesagreedthatthegrowthoftheirrespectivepowdermetalbusinesseswouldbebetterservedbyasupplyagreementbywhichCarpenterwillsupplySandvik.

InApril2013,CarpenterenteredasupplyagreementthatwillprovideRolls-Roycewithadvancedtechnologymaterialsusedinthemanufactureofjetenginescomponents.Thefive-yearagreementrunsuntil2017andisvaluedatapproximatelyUS$75million.

Carpenterreportedfirstquarter2013netincomeofUS$33millionfromnetsalesofUS$582million.Revenuesincreasedintheaerospaceanddefensemarketsby20%toUS$215million,andintheenergymarketby24%toUS$71millionyearonyear.Othermarketssuchastransportation,andindustrialandconsumerapplicationsremainedflat.Revenuesinmedicalapplicationsdeclinedby26%toUS$25millionfromQ12012toQ12013.

» APP. 2

ExEc

SumC

ON

T1.0

2.03.0

4.05.0

6.07.0

8.09.0

10.0A

PP. 1

SAMPLE PROFILE

SAMPLE PAGES

T Z M Ivi

TiTanium meTal annual Review 2013

Ref 8853

0

10

20

30

40

50

60

70

2010 2011 2012 2013f 2014f

'000 tonnes

MRO Others Airbus Boeing

© TZMI 2013 NOT FOR REPRODUCTION

©TZMI 2013

Titanium milled products demand in aerospace: 2010–2014

Industrial applications

Approximatelyhalfofthetotaldemandfortitaniummilledproductsisconsumedbytheindustrialsector.Titaniumisusedextensivelyinawiderangeofindustries,primarilyduetoitscorrosionandchemicalresistanceacrossawiderangeofaggressiveapplications.

Themainindustriesthatusetitaniuminclude:

• chemicalprocessingplants,

• powergenerationforcoolingwaterapplications,

• oilandgasforavarietyofseawaterandstorageapplications,

• marineuses,particularlyforcoolingwatersystemusingseawater,

• desalinationforindustrialanddrinkingwater,and

• thenon-ferrousmetallurgicalsector.

Thelargestindustrialapplicationfortitaniummilledproductsisinthechemicalsub-sector,whichaccountedfor52%,or36,300tonnesofthe69,500tonnestotalindustrialdemandin2012.Powerapplicationswerethesecondlargestsegment,accountingfor11,800tonnes,followedbydesalination(6,400tonnes),ships(4,400tonnes)andmetallurgicalapplications(4,100tonnes).

Thenextmostcommonuseofmilledtitaniumintheindustrialsectorisinheatexchangers,pipes,vesselsandvalvesforthechemical,powerandwatertreatmentsectors.

TZMIforecastglobaldemandfortitaniummilledproductsintheindustrialsectortogrowfrom58,600tonnesin2010to86,600tonnesby2014,a10.3%CAGR.

« viiT Z M I

ExEcuTIvE SuMMary

Ref 8857

Power17%

Oil & Gas3%

Desal9%

Ships6%

Chemical52%

Auto4%

Metallurgy6%

Chlor-Alkali3%

© TZMI 2013 NOT FOR REPRODUCTION

©TZMI 2013

Global demand for industrial applications by end-use sector in 2012

Chinaisthelargestconsumeroftitaniumfortheindustrialsector.In2012,Chinaconsumedalmosthalfofthedemandfortitaniummilledproductsintheindustrialsector.Withinthissector,75%ofChina’sdemandcamefromthechemicalsub-sector.

China’sdemandfortitaniummilledproductsintheindustrialsectorisforecasttogrowby12%CAGRfrom2010to2014,estimatedtoconsume41,100tonnesofproductby2014.

Thefollowingfigurepresentstheforecastforglobaltitaniumdemandintheindustrialsector,bylocation, from 2010 to 2014.

Ref 8859

0

20

40

60

80

100

2010 2011 2012 2013f 2014f

'000 tonnes

China Western Europe CIS Japan US Other

© TZMI 2013 NOT FOR REPRODUCTION

©TZMI 2013 f=forecast

Global industrial sector titanium demand by location: 2010–2014

»

APP. 1

APP. 2

CO

NT

1.02.0

3.04.0

5.06.0

7.08.0

9.010.0

ExEc

Sum

Includes

134 pages, plus

66 company profiles

88 easy-to-

read charts, images and

detailed tables

SAMPLE EDITIONSAMPLE EDITION

electronic version (PDF)

with easy-to-navigate

buttons

Recommended