www.hifreqecon.com/TELUSPC

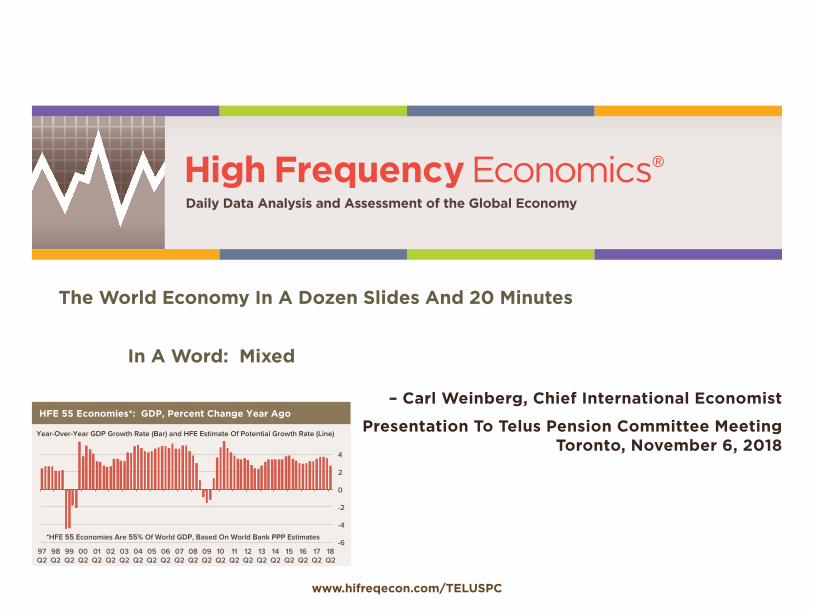

The World Economy In A Dozen Slides And 20 Minutes

In A Word: Mixed

– Carl Weinberg, Chief International Economist

Presentation To Telus Pension Committee MeetingToronto, November 6, 2018

-6

-4

-2

0

2

4

97 Q2

98 Q2

99 Q2

00 Q2

01 Q2

02 Q2

03 Q2

04 Q2

05 Q2

06 Q2

07 Q2

08 Q2

09 Q2

10 Q2

11 Q2

12 Q2

13 Q2

14 Q2

15 Q2

16 Q2

17 Q2

18 Q2

*HFE 55 Economies Are 55% Of World GDP, Based On World Bank PPP Estimates

HFE 55 Economies*: GDP, Percent Change Year Ago

Year-Over-Year GDP Growth Rate (Bar) and HFE Estimate Of Potential Growth Rate (Line)

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 2

WORLD

China United States

Canada

United Kingdom

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 3

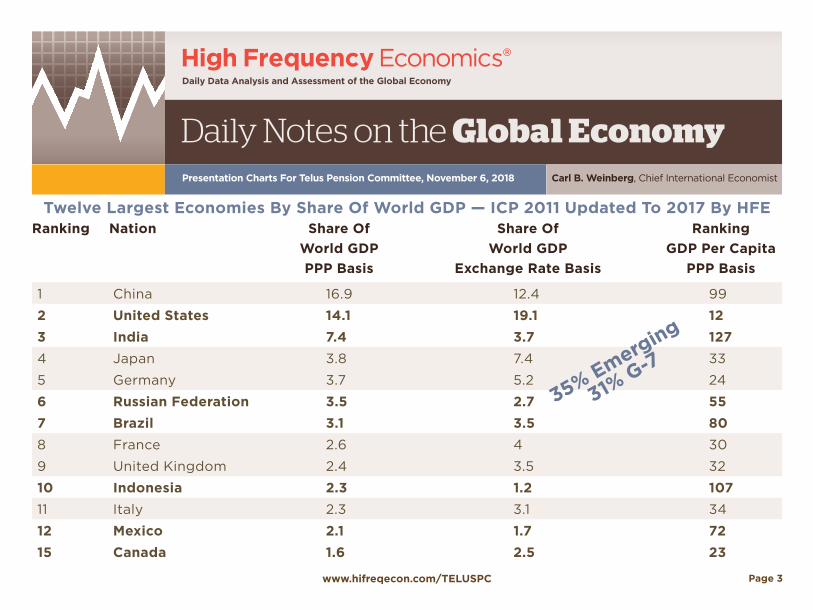

Twelve Largest Economies By Share Of World GDP — ICP 2011 Updated To 2017 By HFERanking Nation Share Of Share Of Ranking World GDP World GDP GDP Per Capita PPP Basis Exchange Rate Basis PPP Basis

1 China 16.9 12.4 99

2 United States 14.1 19.1 123 India 7.4 3.7 1274 Japan 3.8 7.4 33

5 Germany 3.7 5.2 24

6 Russian Federation 3.5 2.7 557 Brazil 3.1 3.5 808 France 2.6 4 30

9 United Kingdom 2.4 3.5 32

10 Indonesia 2.3 1.2 10711 Italy 2.3 3.1 34

12 Mexico 2.1 1.7 7215 Canada 1.6 2.5 23

35% Emerging

31% G-7

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 4 0

1

2

3

4

5

6

7

8

9

Oct 04

Oct 05

Oct 06

Oct 07

Oct 08

Oct 09

Oct 10

Oct 11

Oct 12

Oct 13

Oct 14

Oct 15

Oct 16

Oct 17

Oct 18

Canada: Unemployment Rate, Percent

-30 -25 -20 -15 -10 -5 0 5

10 15 20

-5 -4 -3 -2 -1 0 1 2 3 4 5

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Canada: Monthly Domestic Product & Manufacturing Output

Green Line Is Mfg Production, %chya, Left Axis Columns Are Monthly GDP, %chya, Right Axis

-1

0

1

2

3

4

Sep 05

Sep 06

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

Sep 12

Sep 13

Sep 14

Sep 15

Sep 16

Sep 17

Sep 18

Sep 19f

HFE Projection

Canada: CPI, Percent Change Year Ago

Yellow Line Shows CPI Ex-Energy, Oct 18 Onward Is HFE Forecast Black Line Is CPI-TRIM, No Forecast

-5

-4

-3

-2

-1

0

1

2

3

Aug 99

Aug 00

Aug 01

Aug 02

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Canada: Real Weekly Earnings, Percent Change Year Ago

Black Line Shows 12-Month Moving Average

-10 -8 -6 -4 -2 0 2 4 6 8

97 Q2

98 Q2

99 Q2

00 Q2

01 Q2

02 Q2

03 Q2

04 Q2

05 Q2

06 Q2

07 Q2

08 Q2

09 Q2

10 Q2

11 Q2

12 Q2

13 Q2

14 Q2

15 Q2

16 Q2

17 Q2

18 Q2

Canada: GDP

Seasonally Adjusted Annual Rate (Bar) and Percent Change Year Ago (Line) Calculated From Seasonally Adjusted Data Through 2018 Q2

1500

1550

1600

1650

1700

1750

1800

1850

1900

1950

Q4 08

Q2 09

Q4 09

Q2 10

Q4 10

Q2 11

Q4 11

Q2 12

Q4 12

Q2 13

Q4 13

Q2 14

Q4 14

Q2 15

Q4 15

Q2 16

Q4 16

Q2 17

Q4 17

Q2 18

Canada: Actual GDP Vs HFE Full Capacity GDP Billions Of Constant C$, Quarterly Data

Black Line Is HFE Peak-To-Peak Capacity GDP Blue Line Is Actual GDP

-3.0 -2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0

Oct 04

Oct 05

Oct 06

Oct 07

Oct 08

Oct 09

Oct 10

Oct 11

Oct 12

Oct 13

Oct 14

Oct 15

Oct 16

Oct 17

Oct 18

Canada: Employment, Percent Change Year Ago

Line Shows Private Sector Employment

Canada’s Economy Is Chugging AlongGrowth is, however, slowing. Just the same, it is still growing at the top of the BoC’s estimates of its potential rate. With a 44-year low unemployment rate and full capacity use the BoC cannot simply sit tight and hope that the economy continues to slow. A move back to neutral, at least, has been promised. That means a 2.5% policy rate at a min-ium, or three hikes in the next nine months (One 25bps every other rate setting.) That is about the same pace we expect the Fed will raise rates.

-25

-20

-15

-10

-5

0

5

Q2 09

Q4 09

Q2 10

Q4 10

Q2 11

Q4 11

Q2 12

Q4 12

Q2 13

Q4 13

Q2 14

Q4 14

Q2 15

Q4 15

Q2 16

Q4 16

Q2 17

Q4 17

Q2 18

Canada: Current Account Balance, C$ Billions

Quarterly Rate, Line Shows Four Quarter Moving Average

Record

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

1.65

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

12-Month Trend Line shown

Canada: Manufacturing Inventories-To-Sales Ratio

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 5

High Frequency Economics® — Fiscal Easing + Fed Tightening + “Art of the Deal” Trade Policy = ? September 26, 2018 Page 12

© 2018 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com

Inverted Yield Curves Signal Recessions, But Not Always

The yield curve is probaby the most consistent and reliable component of the index of leading indicators for signaling recessions, but there have been false signals, most notably in 1966 and 1998. Not surprisingly, inversions have coincided with Fed tightening cycles; similarly, most, but not all, Fed tightening cycles in recent decades have culminated in recessions: A notable exception was the 1994 tightening cycle, when the curve flattened significantly but not did not invert.

-12

-9

-6

-3

0

3

6

9

-8

-6

-4

-2

0

2

4

6

60 65 70 75 80 85 90 95 00 05 10 15

Yield Curve: 10-Year Minus 2-Year Treasury Yield, Percentage Points (Left) Yield Curve: 10-Year Minus Federal Funds Rate, Percentage Points (Left) Real GDP, %chya (Right)

Shaded Bars Denote Recession Periods

1966 1998

Recesions Have Been Preceded By Inverted Curves, But Some False Signals

-4

0

4

8

12

16

20

24

77 83 89 95 01 07 13

Real Fed Funds Rate, Deflated With %Y/Y In Core PCE Prices, % Nominal Fed Funds Rate, %

Shaded Bars Denote Recession Periods

...Similarly, Fed Tightening Cycles Have Tended To Be Followed By Recessions

-1 0 1 2 3 4 5 6 7 8 9

90 95 00 05 10 15

10-Year Term Premium*, % Nominal 10-Year Treasury Yield, % 10-Year Risk-Neutral Yield*, %

*NY Fed data; methodology developed by Tobias Adrian, Richard Crump & Emanuel Moench.

“Bond Market Conundrum”

Shaded Bars Mark Fed Tightening Periods

Is This Time Different? Bond Market Term Premiums Are Historically Low

Is this time different? Term premiums in the bond market are historically low, likely due in large part to central bank bond purchases—QE.

0.0

0.2

0.4

0.6

0.8

1.0

72 77 82 87 92 97 02 07 12 17

Long-Term Spread Model Near-Term Spread Model Shaded Bars Denote Recession Periods

Note: Chart replicated from "(Don't Fear) The Yield Curve," a paper written by Fed economists Eric Engstrom and Steve Sharpe; most recent readings estimated by HFE.

Estimated Probability Of Recession Within One Year

Yield Curve Models Still Signaling Low Recession Probability

High Frequency Economics® — Fiscal Easing + Fed Tightening + “Art of the Deal” Trade Policy = ? September 26, 2018 Page 3

© 2018 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com

Weak Recovery Has Been Strong Enough To Reduce Unemployment Rate

Real GDP growth has been exceptionally weak by past expansion standards—2.3% at an annual rate on average during the nine years of expansion—but potential growth has also been lower than in past cycles and the unemployment rate has trended down. We estimate an unemployment-rate-neu-tral, or “potential” growth rate of just 1.4%, on average, for the past decade, down from 3.0% in the previous two decades.

The Fed’s mandate relates to the labor market and inflation, not GDP and inflation. Inflation remains low, but the unemployment rate is already be-low the median Fed official estimate of the full-employment level, and it is still trending down.

100

110

120

130

140

150

160

0 4 8 12 16 20 24 28 32 36

1961-69 1970-73 1975-80 1980-81 1982-90 1991-2001 2001-07 2009- Real GDP During Recoveries, Trough=100

Quarters After Trough

Current Cycle

GDP Growth Has Been Weak By Past Standards

-7

-6

-5

-4

-3

-2

-1

0

0 4 8 12 16 20 24 28 32 36

1961-69 1970-73 1975-80 1980-81 1982-90 1991-2001 2001-07 2009- Change In Unemployment Rate From Peak During Recoveries, Percentage Points

Quarters After Peak

Current Cycle

...Yet Unemployment Rate Has Been Falling Rapidly

-6

-3

0

3

6

9 -3.0

-1.5

0.0

1.5

3.0

4.5 60 65 70 75 80 85 90 95 00 05 10 15

Unemployment Rate, Change From Year Ago, Pct Pts (Left, Scale Inverted) Real GDP, %chya (Right, Scale)

Shaded Bars Denote Recession Periods

Potential Growth Rate Has Been Below 2% In Recent Years

-1

0

1

2

3

4

5

60 65 70 75 80 85 90 95 00 05 10 15 20 25

CBO Estimate Of Potential Labor Force Growth, Annual % Change CBO Estimate Of Potential Productivity Growth, Annual % Change CBO Estimate Of Potential Real GDP Growth, Annual % Change

Historical Projected

Both Productivity And Labor Force Growth Have Slowed

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 6

High Frequency Economics® — Fiscal Easing + Fed Tightening + “Art of the Deal” Trade Policy = ? September 26, 2018 Page 4

© 2018 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com

Tight Labor Market Just Starting To Put Upward Pressure On Wages; Core PCE Inflation Up To 2% The unemployment rate has continued to decline and wage gains have started to edge up. The average hourly earnings series was up 2.9% y/y in August, up from 2.5% y/y last year. The private wage series in the ECI was up 2.9% y/y in Q2, versus 2.6% y/y in all of 2017 and 2.3% y/y in 2016. Moreover, wage gains and inflation are not supposed to accelerate significantly until the unemployment rate drops below the estimated NAIRU level, and that just happened during 2017. Upward pressure on wages is likely to intensify as the unemployment rate falls some more.

Core inflation has moved up recently as well, although the extent to which the rise is slack-related, or due to other factors, is still unclear. The 12-month change in the core PCE index is 2.0%, in line with the Fed’s goal for the overall PCE index over time.

-1.5

0.0

1.5

3.0

4.5

07 09 11 13 15 17

Core PCE Price Index, %chya Total PCE Price Index, %chya

Fed's 2% Goal For PCE Prices

Mission Accomplished For Fed? Core PCE Inflation At 2.0%

0.5

1.0

1.5

2.0

2.5

3.0

3.5

-30

-20

-10

0

10

20

30

40

03 05 07 09 11 13 15 17

NFIB: Net Percentage Raising Average Selling Prices (Left) Core CPI, %chya (Right) Core PCE Price Index, %chya (Right)

...NFIB Selling Price Series Is Showing Net Strengthening

1.2

2.0

2.8

3.6

07 09 11 13 15 17

ECI: Private Sector Wages & Salaries, %chya Employment Report: Average Hourly Earnings, %chya

Wage Gains Have Been Accelerating, Most Clearly In The ECI

-2.4

-1.2

0.0

1.2

-5.0

-2.5

0.0

2.5

83 87 91 95 99 03 07 11 15

CBO Estimate Of Unemployment Gap* (Left) Acceleration/Deceleration In Private Wage Component Of ECI† (Right)

*Reported unemployment rate minus CBO estimate of NAIRU. †%chya minus %chya one year earlier, four-quarter average.

...Consistent With The NAIRU Framework

The unemployment rate has continued to decline and wage gains have started to edge up. The average hourly earnings series was up 3.1% y/y in October, up from 2.5% y/y last year. The private wage series in the ECI was up 3.1% y/y in Q3, versus 2.9% y/y in all of 2017 and 2.3% y/y in 2016. Moreover, wage gains and inflation are not supposed to accelerate significantly until the unemployment rate drops below the estimated NAIRU level, and that just happened during 2017. Upward pressure on wages is likely to intensify as the unemployment rate falls some more.

Core inflation has moved up recently as well, although the extent to which the rise is slack-related, or due to other factors, is still unclear. The 12-month change in the core PCE index is 2.0%, in line with the Fed’s goal for the overall PCE index over time.

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 7

High Frequency Economics® — Fiscal Easing + Fed Tightening + “Art of the Deal” Trade Policy = ? September 26, 2018 Page 11

© 2018 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com

Fed Likely To Keep Tightening As Unemployment Keeps FallingThe Fed has raised the funds rate by 175 basis points thus far. Markets are pricing in about another 90 basis points by the end of 2019, below the 125 basis points implied by the dot plot. We think Fed officials will have to tighten by more than they expect as the unemployment rate keeps falling.

The funds rate is roughly zero in real terms. The neutral real level may well be lower now than in the past, but the current level is almost 300 basis points below the level at the end of the last tightening cycle. Moreover, the expanded balance sheet is also still providing stimulus.

2.1

2.3

2.5

2.7

2.9

3.1

3.3

3.5

0

2

4

6

8

10

12

14

83 87 91 95 99 03 07 11 15

10-Year Treasury Yield, % (Left) S&P 500, Log Scale (Right) Bars Denote Fed Tightening Periods

Markets Have Varied During Fed Tightening Cycles

Fed Officials’ Estimates For Appropriate Fed Funds Rate

% At Year-End, as of June 2018 FOMC Meeting

2018 2019 2020Longer

RunMedian Estimate 2.375 3.125 3.375 2.875Mean Estimate 2.242 2.958 3.308 2.825

Fed Officials’ Economic Projections

Median, %ch Q4/Q4, Unless Noted, as of June 2018 FOMC Meeting

2018 2019 2020Longer

RunReal GDP 2.8 2.4 2.0 1.8Unemployment Rate* 3.6 3.5 3.5 4.5PCE Prices 2.1 2.1 2.1 2.0Core PCE Prices 2.0 2.1 2.1*Q4 level

Nominal Funds Rate Target (%)

Real Funds Rate (%)*

Start End Start End Start EndMar 83 Aug 84 8.50 11.50 2.6 7.5Apr 87 Feb 89 6.00 9.75 3.2 5.1Feb 94 Feb 95 3.00 6.00 0.8 3.7Jun 99 May 00 4.75 6.50 3.5 4.8Jun 04 Jun 06 1.00 5.25 -0.9 2.9Dec 15 0.13 -1.3*Deflated with %chya in core PCE prices.

Fed Tightening Cycles

3.5

4.5

5.5

6.5

7.5

8.5

9.5

11 12 13 14 15 16 17 18 19 20

Actual Reported Rate Mid-Point Of Fed Projections, As Of Nov 2011 Mid-Point Of Fed Projections, As Of Jun 2014 Mid-Point Of Fed Projections, As Of Jun 2015 Median Of Fed Projections, As Of Jun 2016 Median Of Fed Projections, As Of Jun 2017 Median Of Fed Projections, As Of Jun 2018

Unemployment Rate, %

Median Fed Estimate For Longer-Run Normal Unemployment Rate: 4.5%

Unemployment Keeps Falling Faster Than Expected By The Fed

The Fed has raised the funds rate by 200 basis points thus far. Markets are pricing in about another 90 basis points by the end of 2019, below the 100 basis points implied by the dot plot. We think Fed officials will have to tighten by more than they expect as the unemployment rate keeps falling.

The funds rate is roughly zero in real terms. The neutral real level may well be lower now than in the past, but the current level is 300 basis points below the level at the end of the last tighten-ing cycle. Moreover, the expanded balance sheet is also still providing stimulus. We don’t expect any new signal on policy from Fed officials this week, consistent with no backing away from the gradual tightening path signaled by the dot plot at the last meeting. We suspect the weakening in equities is being viewed as no more than minor volatility at this point

Fed Officials’ Economic Projections

Median, %ch Q4/Q4, Unless Noted

2018 2019 2020 2021Longer

RunReal GDP

June 2018 2.8 2.4 2.0 1.8September 2018 3.1 2.5 2.0 1.8 1.8

Unemployment Rate*June 2018 3.6 3.5 3.5 4.5September 2018 3.7 3.5 3.5 3.7 4.5

PCE InflationJune 2018 2.1 2.1 2.1 2.0September 2018 2.1 2.0 2.1 2.1 2.0

Core PCE PricesJune 2018 2.0 2.1 2.1September 2018 2.0 2.1 2.1 2.1

*Q4 Level, %

Fed Officials’ Estimates For Appropriate Fed Funds Rate

% At Year-End

2018 2019 2020 2021Longer

RunMedian Estimate

June 2018 2.375 3.125 3.375 2.875September 2018 2.375 3.125 3.375 3.375 3.0

Mean Estimate

June 2018 2.242 2.958 3.308 2.825September 2018 2.313 3.016 3.281 3.234 2.883

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 8

-12

-10

-8

-6

-4

-2

0

2

4

00 Q3

01 Q3

02 Q3

03 Q3

04 Q3

05 Q3

06 Q3

07 Q3

08 Q3

09 Q3

10 Q3

11 Q3

12 Q3

13 Q3

14 Q3

15 Q3

16 Q3

17 Q3

18 Q3p

Euro Zone: GDP Growth

Line Shows Percent Change Year Ago, Bars Show Quarterly Annualized Rate

-8

-6

-4

-2

0

2

4

6

Sep 03

Sep 04

Sep 05

Sep 06

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

Sep 12

Sep 13

Sep 14

Sep 15

Sep 16

Sep 17

Sep 18f

Euro Zone: Retail Sales Volume, Percent Change Year Ago

Green Line Shows Annualized Change Of 3-Month Moving Average

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Oct 09

Apr 10

Oct 10

Apr 11

Oct 11

Apr 12

Oct 12

Apr 13

Oct 13

Apr 14

Oct 14

Apr 15

Oct 15

Apr 16

Oct 16

Apr 17

Oct 17

Apr 18

Oct 18f

Apr 19f

Oct 19f

Euro Zone: CPI, Percent Change Year Ago

Blue Bars Are CPI, Green Line Is Core CPI, Black Line Is ECB Inflation Target Oct 18 Onward Is HFE Forecast

-35 -30 -25 -20 -15 -10 -5 0 5 10

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Euro Zone: Industrial Production, Percent Change Year Ago Black Line Shows Annualized Percentage Change In Three-Month Moving Average Blue Line Shows Percent Change Since April 2008 Peak

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 9

0

0.5

1

1.5

2

2.5

3

3.5

Q2 09

Q4 09

Q2 10

Q4 10

Q2 11

Q4 11

Q2 12

Q4 12

Q2 13

Q4 13

Q2 14

Q4 14

Q2 15

Q4 15

Q2 16

Q4 16

Q2 17

Q4 17

Q2 18

Euro Zone: Total Labor Costs Vs Wage Costs

Percent Change Year Ago, Bars Show Total Labor Costs, Line Shows Wage Costs Only

0

2

4

6

8

10

12

14

Sep 04

Sep 05

Sep 06

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

Sep 12

Sep 13

Sep 14

Sep 15

Sep 16

Sep 17

Sep 18

Euro Zone Ex-Germany: Unemployment Rate, Percent

Monthly Data, Calculations By HFE, Yellow Bars Show Eurozone Ex-Germany Red Bars Are Total Euro Zone

-6

-3

0

3

6

9

12

15

Sep 00

Sep 01

Sep 02

Sep 03

Sep 04

Sep 05

Sep 06

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

Sep 12

Sep 13

Sep 14

Sep 15

Sep 16

Sep 17

Sep 18

Total MFI Lending Lending To SMEs Ex-Mortgages Mortgages

Euro Zone: Bank Lending, Percent Change Year Ago

-3.5 -3.0 -2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0

Jul 08

Mar 09

Nov 09

Jul 10

Mar 11

Nov 11

Jul 12

Mar 13

Nov 13

Jul 14

Mar 15

Nov 15

Jul 16

Mar 17

Nov 17

Jul 18

Euro Zone: Employment, Percent Change Year Ago

Line Is Three-Month Moving Average

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 10

-15

-10

-5

0

5

10

15

20

25

0

2

4

6

8

10

12

10 Q3

11 Q1

11 Q3

12 Q1

12 Q3

13 Q1

13 Q3

14 Q1

14 Q3

15 Q1

15 Q3

16 Q1

16 Q3

17 Q1

17 Q3

18 Q1

18 Q3

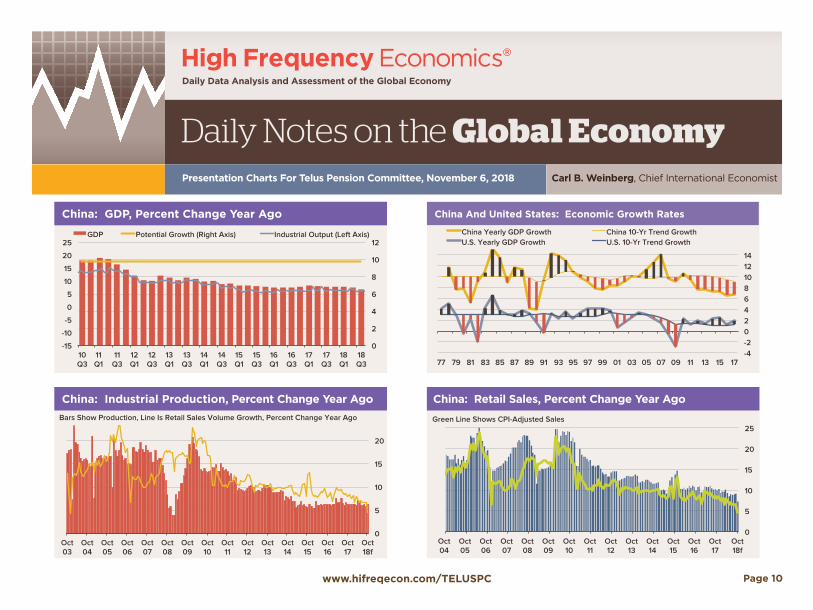

GDP Potential Growth (Right Axis) Industrial Output (Left Axis)

China: GDP Vs Industrial Output, Percent Change Year Ago China: GDP, Percent Change Year Ago

0

5

10

15

20

25

Oct 04

Oct 05

Oct 06

Oct 07

Oct 08

Oct 09

Oct 10

Oct 11

Oct 12

Oct 13

Oct 14

Oct 15

Oct 16

Oct 17

Oct 18f

China: Retail Sales, Percent Change Year Ago

Green Line Shows CPI-Adjusted Sales

China: Retail Sales, Percent Change Year Ago

-4 -2 0 2 4 6 8 10 12 14

77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

China Yearly GDP Growth China 10-Yr Trend Growth U.S. Yearly GDP Growth U.S. 10-Yr Trend Growth

China And United States: Economic Growth Rates

0

5

10

15

20

Oct 03

Oct 04

Oct 05

Oct 06

Oct 07

Oct 08

Oct 09

Oct 10

Oct 11

Oct 12

Oct 13

Oct 14

Oct 15

Oct 16

Oct 17

Oct 18f

China: Industrial Production Vs Retail Sales Volumes

Bars Show Production, Line Is Retail Sales Volume Growth, Percent Change Year Ago

China: Industrial Production, Percent Change Year Ago

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 11

The Silk Road Is The Future: Embrace It

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 12

The Silk Roads And OBORTrade

Links 60% Of The World’s Population Europe Is 340 million China Is 1.4 billion Others Are 2.7 billion

Who Jointly Produce 40% Of The World’s GDP. Europe Is 12%, China Is 17%, Others Are 11%

Containers Do Not Have To Go Back Toward China EmptyFor EU Exporters, A Ten-Fold Increase In The Number Of Consumers They Can Reach!

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 13

The Prize: Made In China 2025• Research and development: Establish 15 national “innovation centers” by

2020 and 40 by 2025, to develop technologies.

• Manufacture smarter: Lower operating costs, shorten production times and slash defect rates, each by 30% by 2020 and 50% by 2025.

• Industrial self sufficiency: Produce 40% of core components in all manu-facturing by 2020, 70% by 2025.

• Environmental responsibility: In all sectors, reduce emissions per unit pro-duced by 20%, lower energy use per unit of output below world average by 2025 and build 1,000 green factories by 2025.

• Build significant shares of global manufacturing of ten sectors : Aerospace, rail, high-tech autos, hi-tech marine, power grids, machine tools, nuclear plants and equipment, medical equipment.

Carl B. Weinberg, Chief International EconomistPresentation Charts For Telus Pension Committee, November 6, 2018

www.hifreqecon.com/TELUSPC Page 14

Recommended