The Venture Capital Opportunity in South East Asia

Affin Hwang Capital Conference Series 2015 Navigating Through Turbulent Times

Hi! I’m Alexander Jarvis

• Partner at Jungle responsible for SEA investments

• Helped build some $1bn+ companies

• Financial Institutions M&A (London)

Some of my Previous Experience

There’s a lot of money to be made in Venture Capital

But the US has Given it a Bad Rap Around the Bubble of 1999

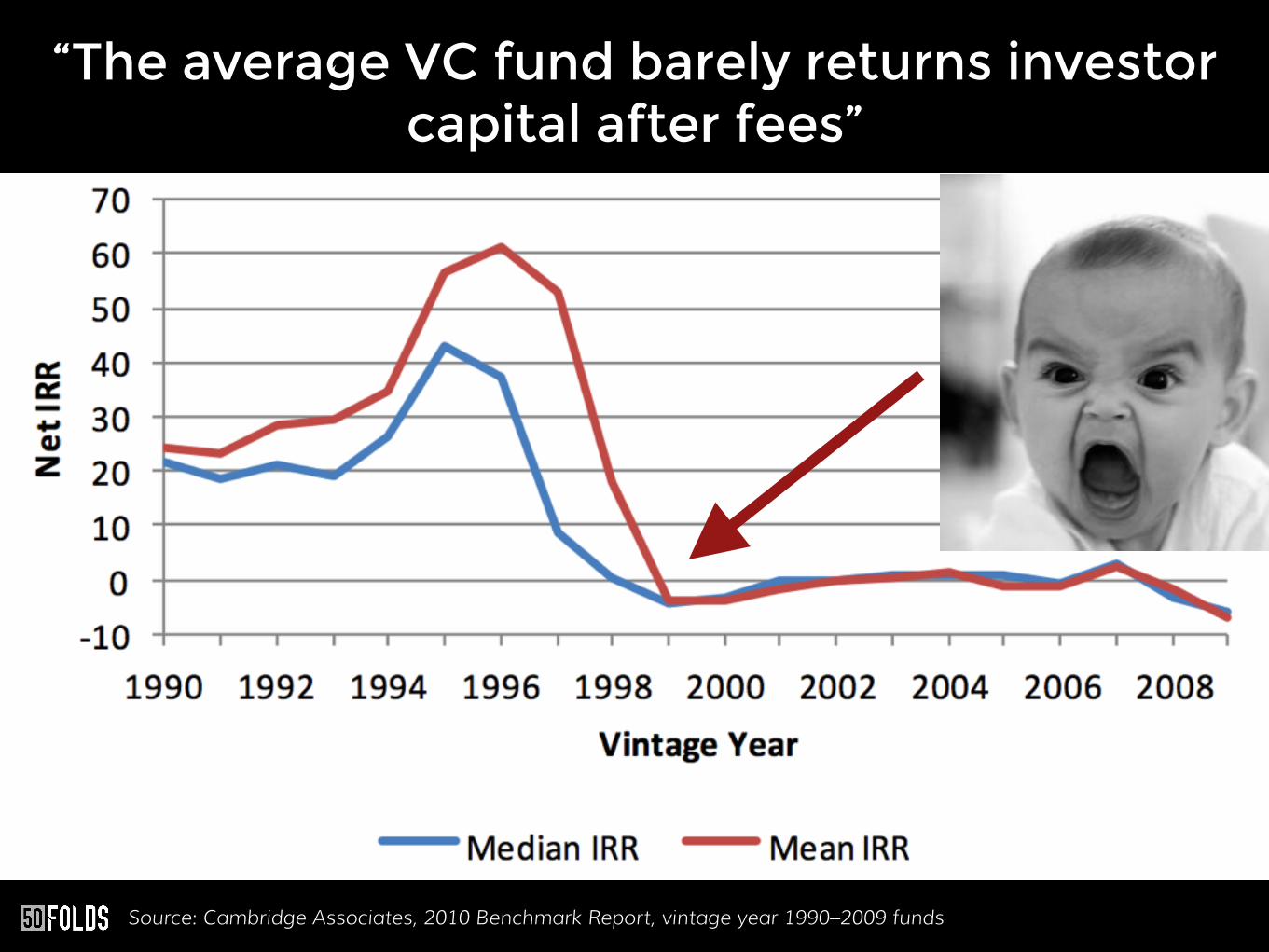

“The average VC fund barely returns investor capital after fees”

Source: Cambridge Associates, 2010 Benchmark Report, vintage year 1990–2009 funds

All attributed to US investor Mark Suster from Upfront Ventures presentation “It’s morning in VC.” Read it!

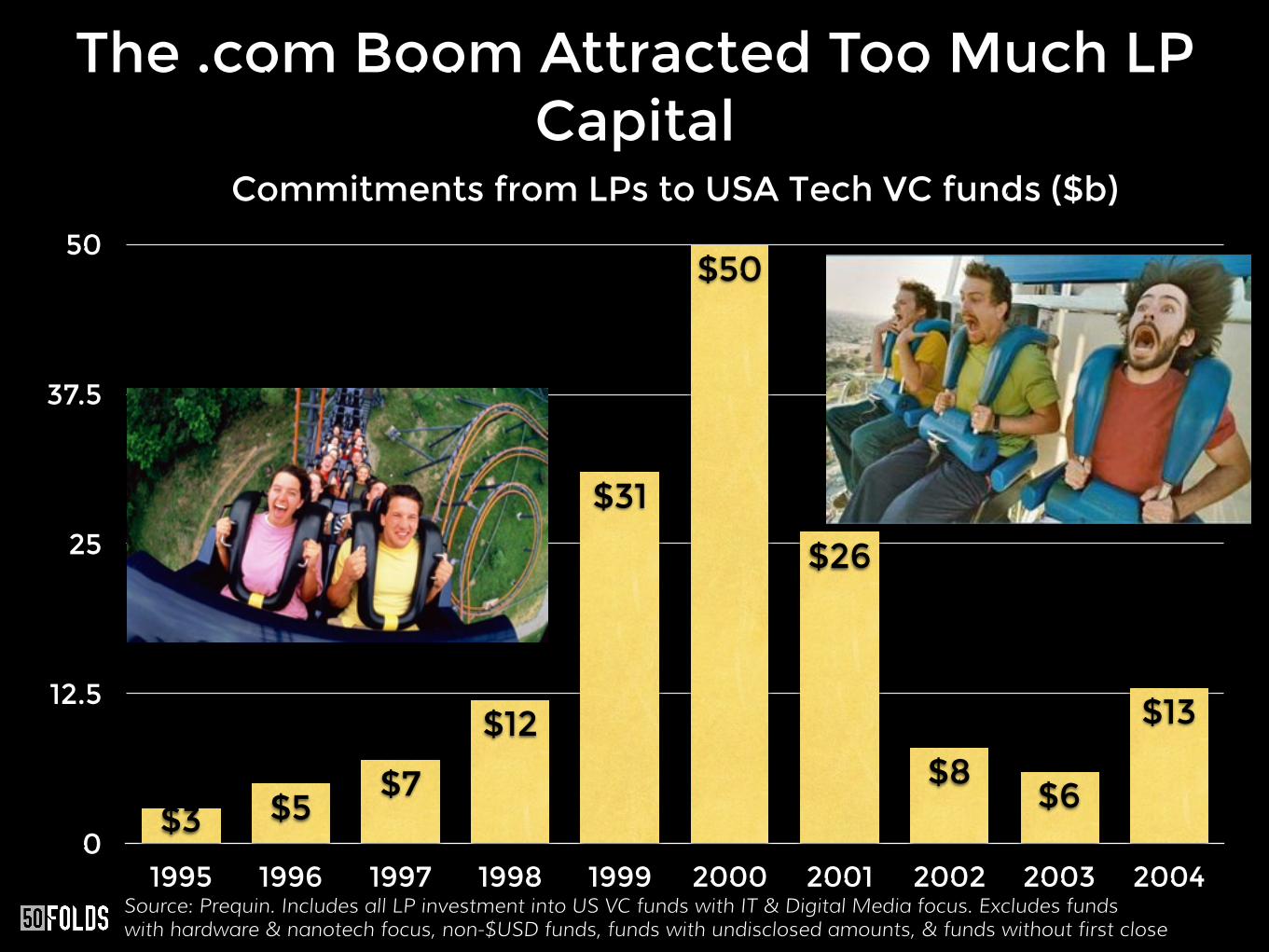

The .com Boom Attracted Too Much LP Capital

Commitments from LPs to USA Tech VC funds ($b)

0

12.5

25

37.5

50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

$13

$6$8

$26

$50

$31

$12

$7$5$3

Source: Prequin. Includes all LP investment into US VC funds with IT & Digital Media focus. Excludes funds with hardware & nanotech focus, non-$USD funds, funds with undisclosed amounts, & funds without first close

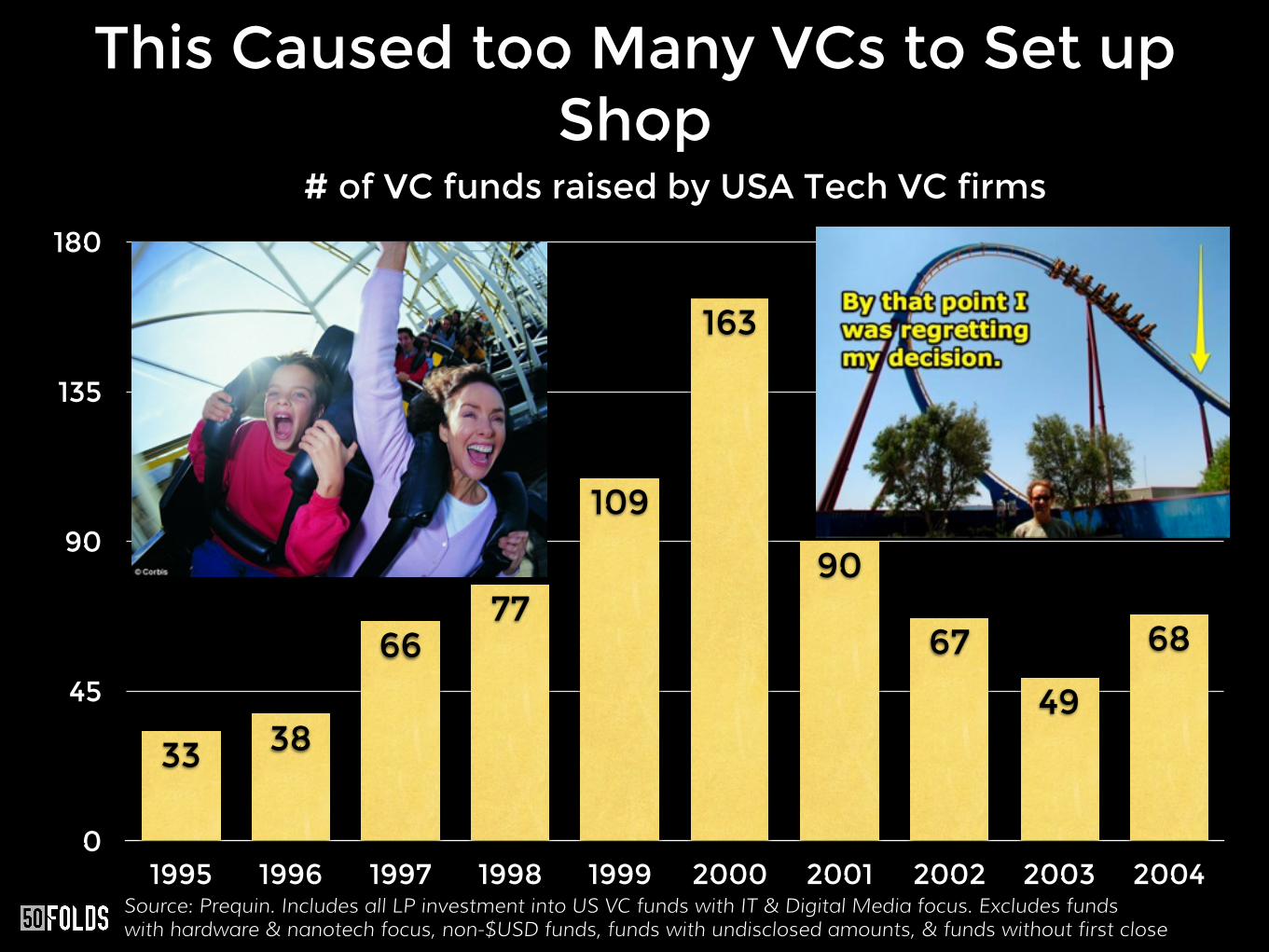

This Caused too Many VCs to Set up Shop

# of VC funds raised by USA Tech VC firms

0

45

90

135

180

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

68

49

67

90

163

109

7766

3833

Source: Prequin. Includes all LP investment into US VC funds with IT & Digital Media focus. Excludes funds with hardware & nanotech focus, non-$USD funds, funds with undisclosed amounts, & funds without first close

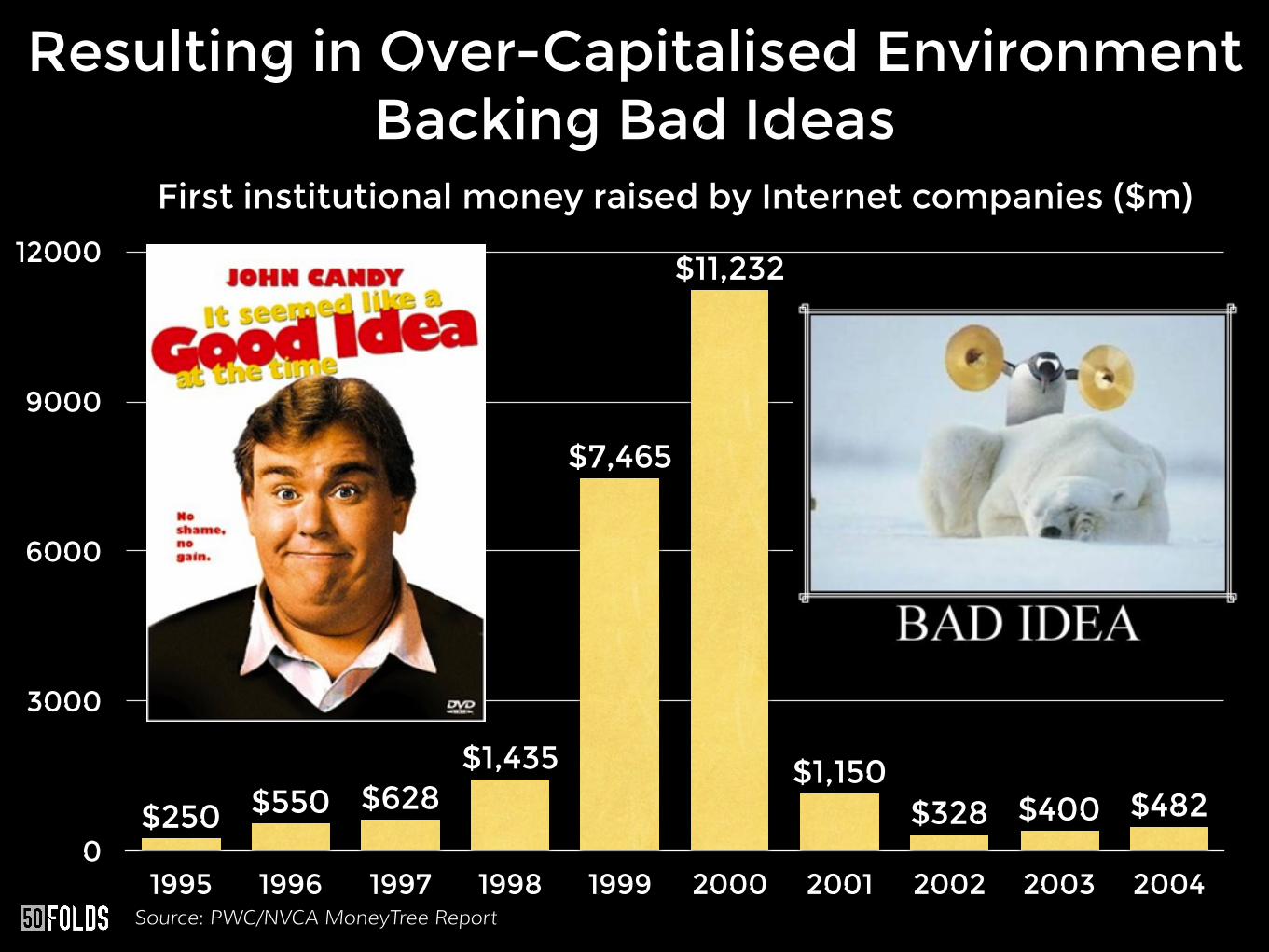

Resulting in Over-Capitalised Environment Backing Bad Ideas

First institutional money raised by Internet companies ($m)

0

3000

6000

9000

12000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

$482$400$328$1,150

$11,232

$7,465

$1,435$628$550$250

Source: PWC/NVCA MoneyTree Report

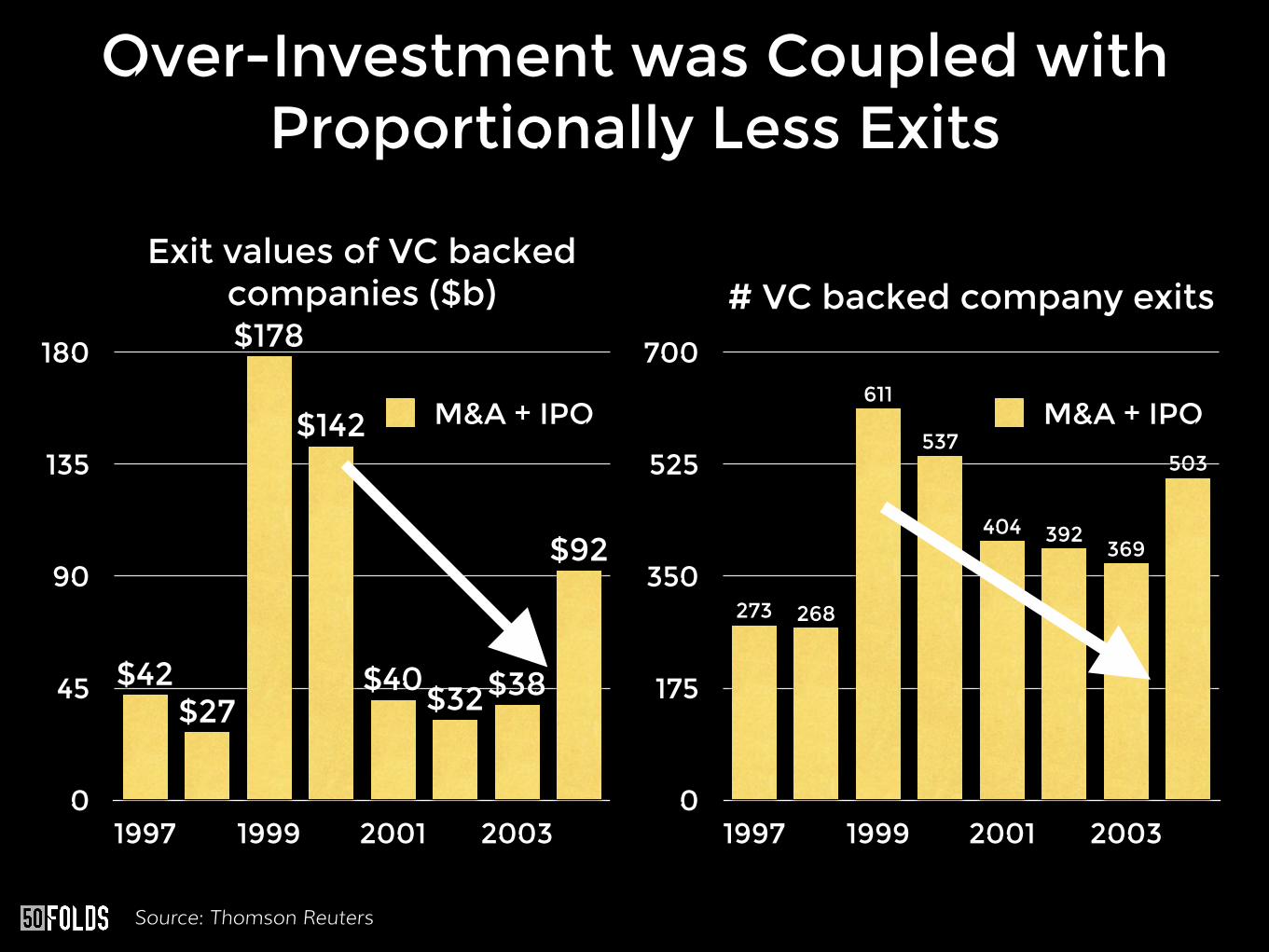

Over-Investment was Coupled with Proportionally Less Exits

Exit values of VC backed companies ($b)

0

45

90

135

180

1997 1999 2001 2003

$92

$38$32$40

$142

$178

$27$42

M&A + IPO

# VC backed company exits

0

175

350

525

700

1997 1999 2001 2003

503

369392404

537

611

268273

M&A + IPO

Source: Thomson Reuters

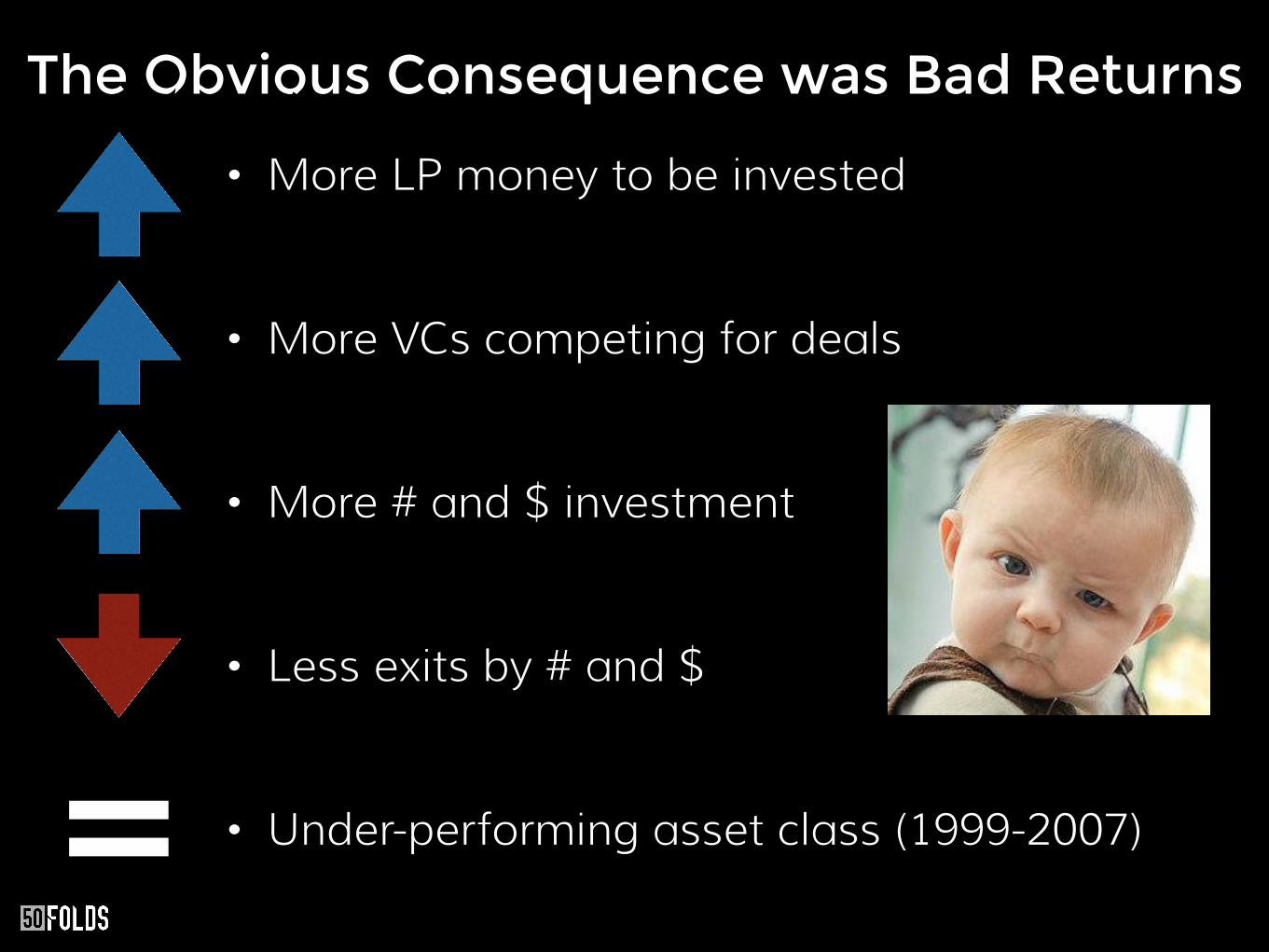

• More LP money to be invested

• More VCs competing for deals

• More # and $ investment

• Less exits by # and $

• Under-performing asset class (1999-2007)

The Obvious Consequence was Bad Returns

=

LPs

?

Not Exactly… So What Changed?

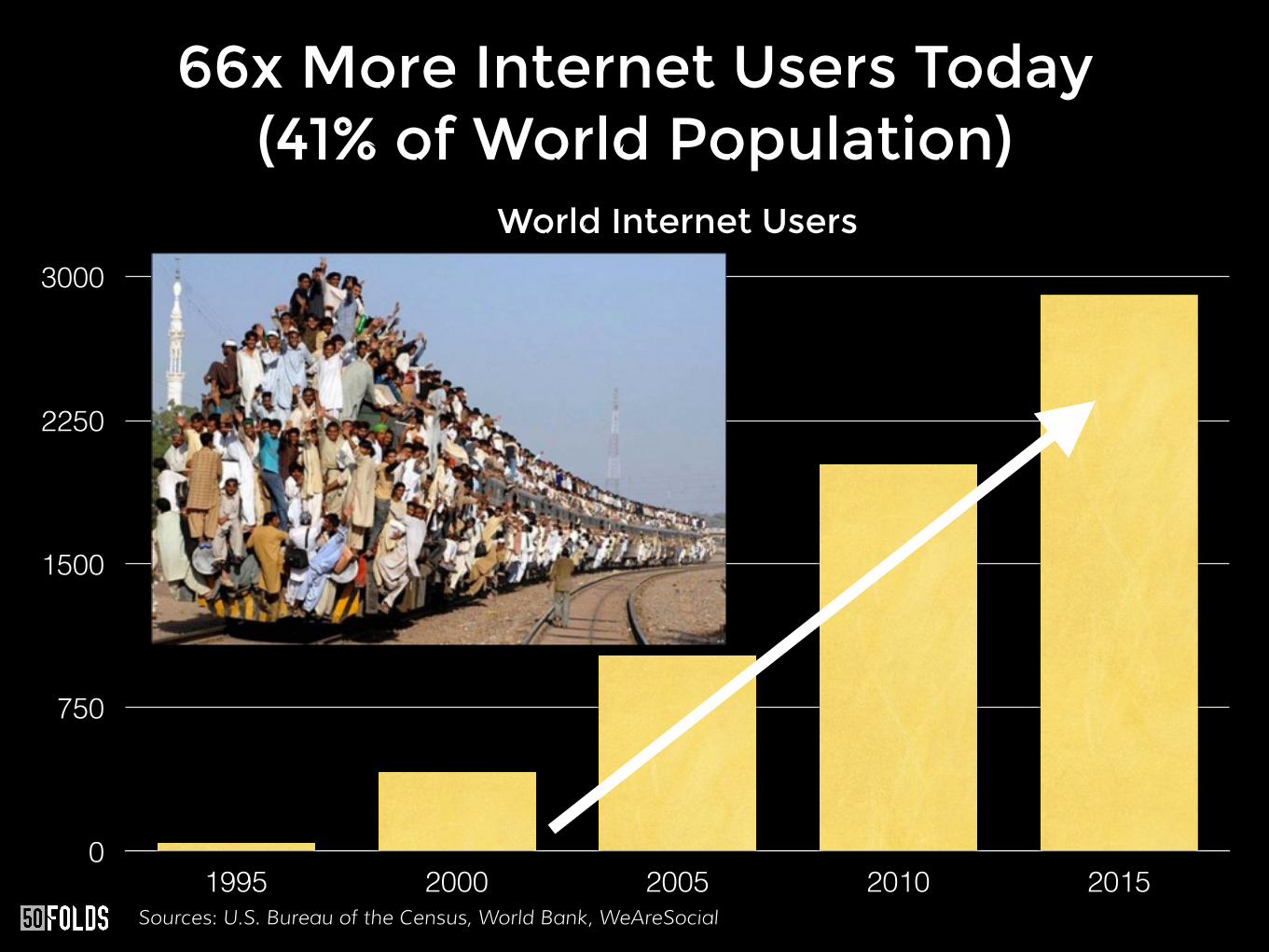

66x More Internet Users Today (41% of World Population)

2,908

2015

41%

66x

World Internet Users

0

750

1500

2250

3000

1995 2000 2005 2010 2015Sources: U.S. Bureau of the Census, World Bank, WeAreSocial

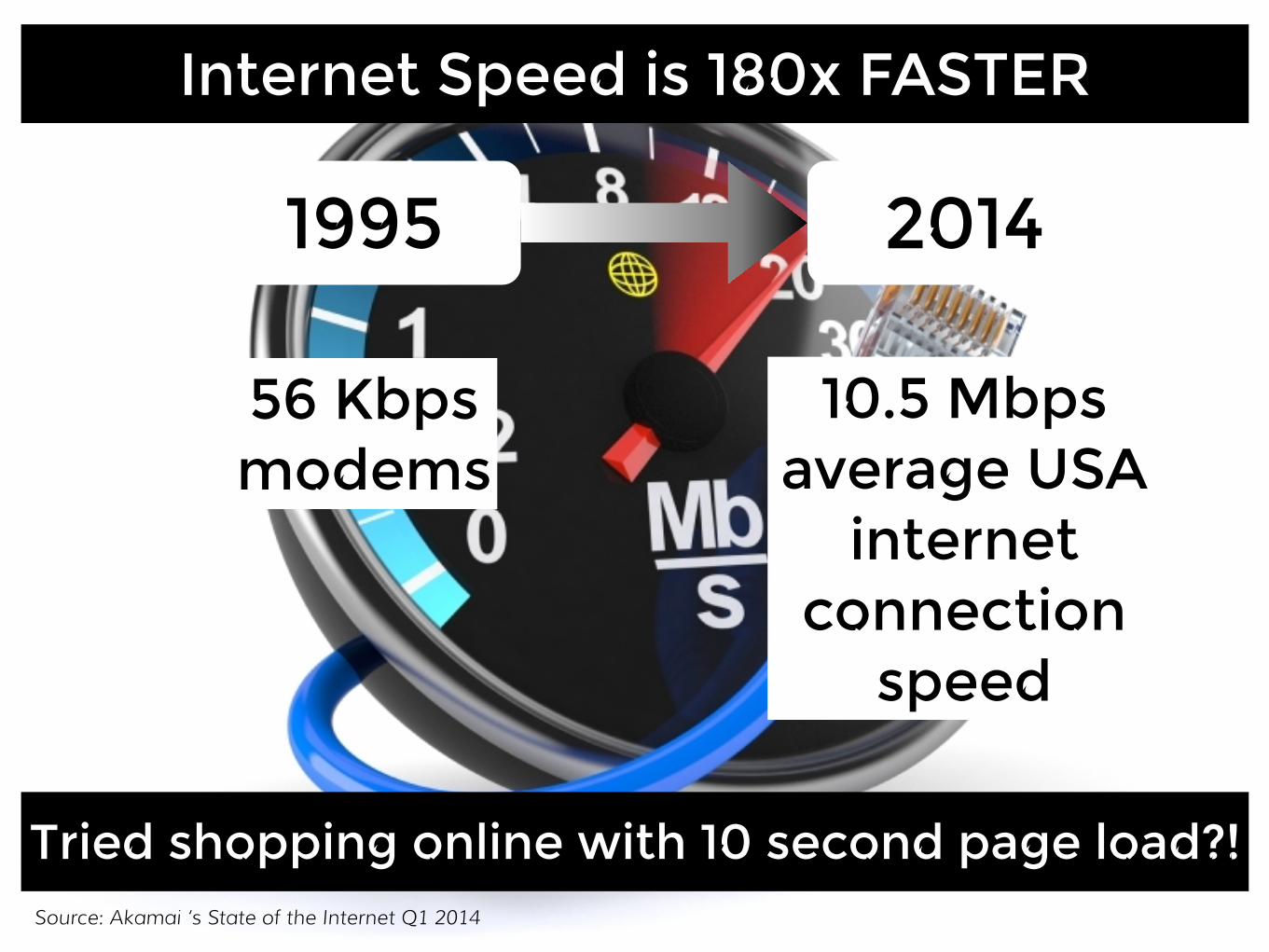

Internet Speed is 180x FASTER

1995 2014

56 Kbps modems

10.5 Mbps average USA

internet connection

speed

Source: Akamai ‘s State of the Internet Q1 2014

Tried shopping online with 10 second page load?!

Everyone is Mobile on Smartphones

• Personal

• Location aware

• At point of purchase

164m • USA smartphone

users

119m • USA tablet users

Source: 2014 Statista forecasts

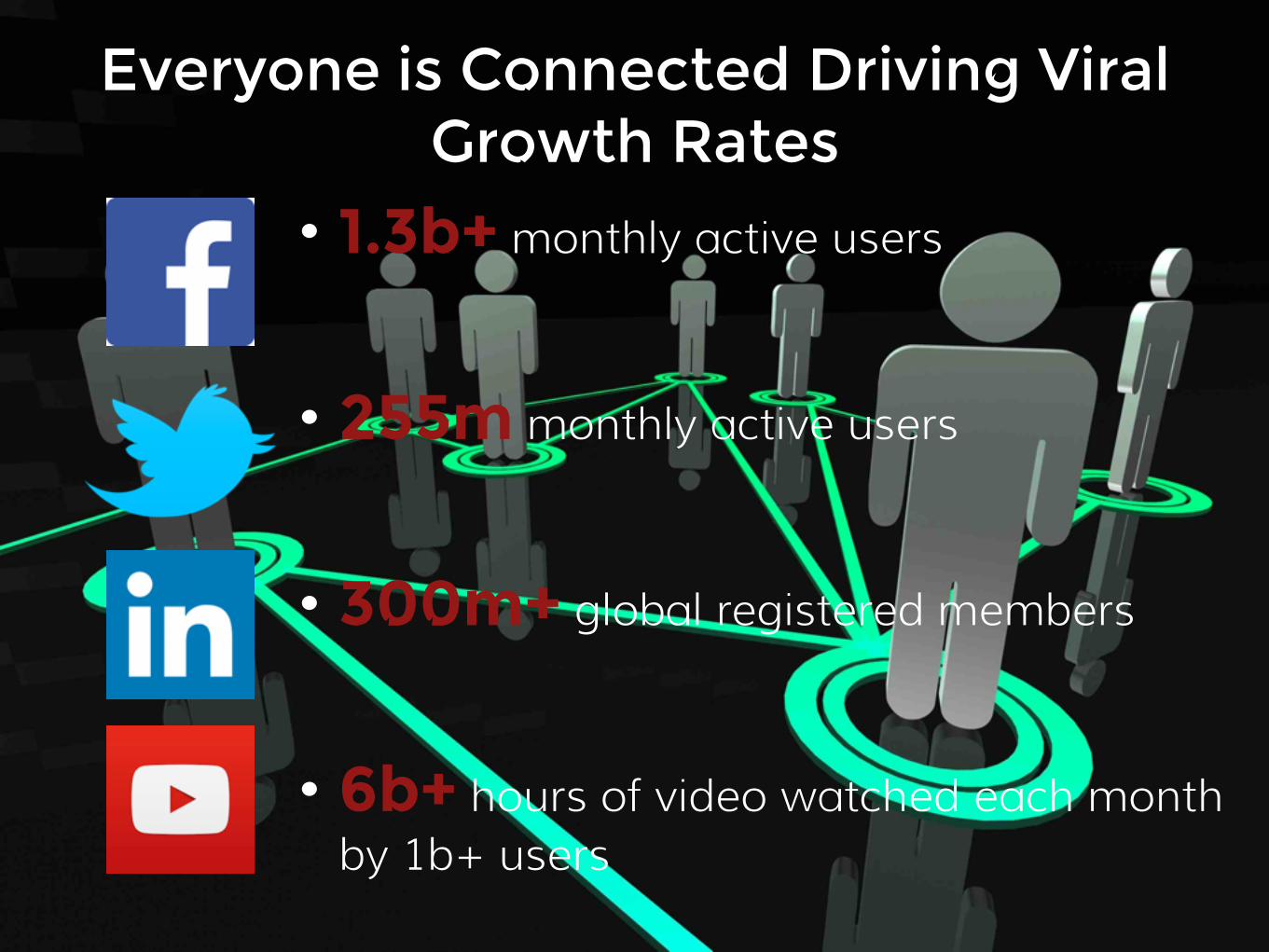

Everyone is Connected Driving Viral Growth Rates

• 1.3b+ monthly active users

• 255m monthly active users

• 300m+ global registered members

• 6b+ hours of video watched each month by 1b+ users

Credit Cards are Now on File with One Click Shopping

1 billion Digital shoppers worldwide

$1.5 trillion Global ecom spend

The Apple app ecosystem alone estimated to be $25b in 2014 (from $0 in 2008)

Sources: eMarketer, WSJ

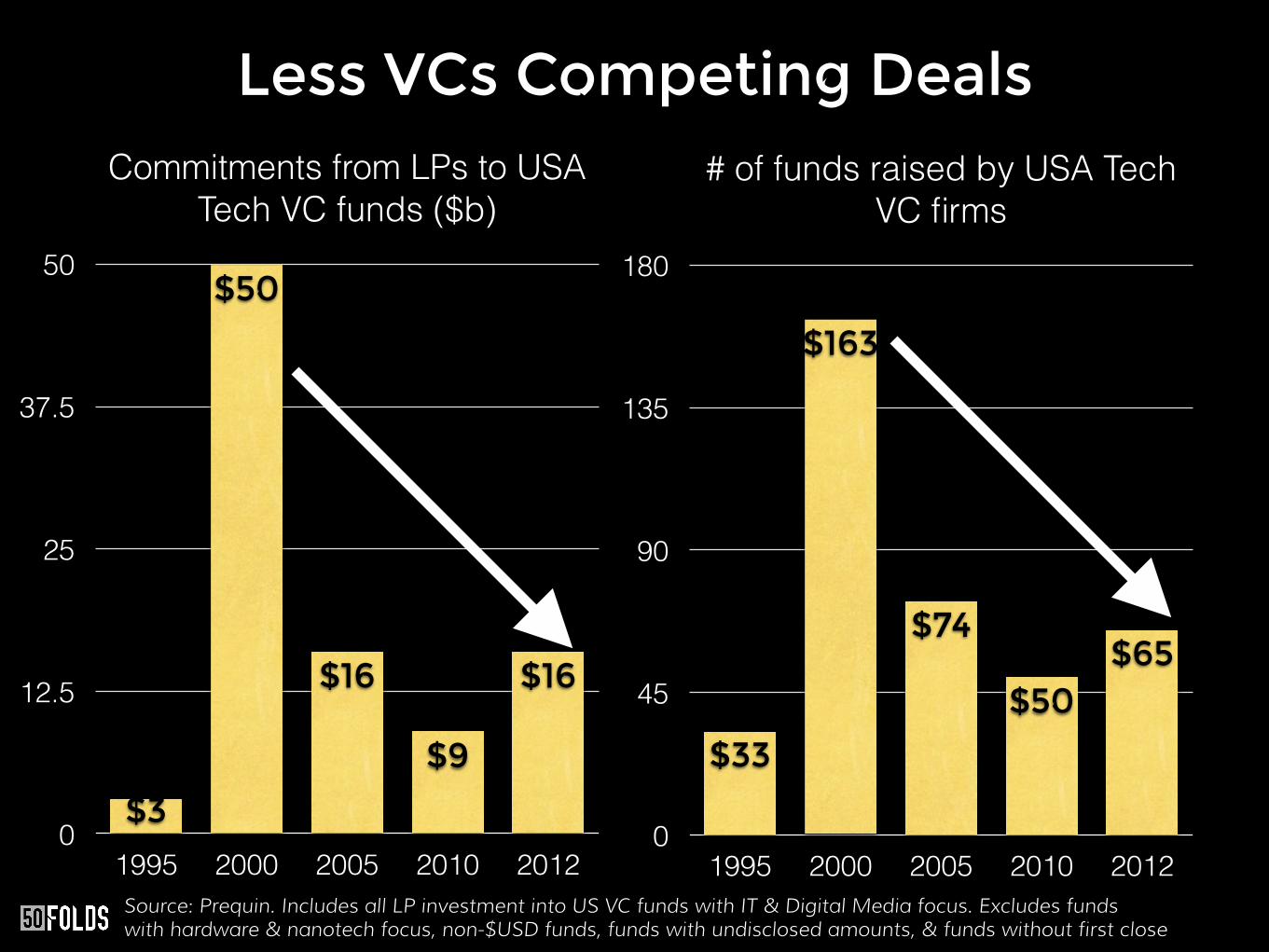

Less VCs Competing DealsCommitments from LPs to USA

Tech VC funds ($b)

0

12.5

25

37.5

50

1995 2000 2005 2010 2012

$16

$9

$16

$50

$3

# of funds raised by USA Tech VC firms

0

45

90

135

180

1995 2000 2005 2010 2012

$65$50

$74

$163

$33

Source: Prequin. Includes all LP investment into US VC funds with IT & Digital Media focus. Excludes funds with hardware & nanotech focus, non-$USD funds, funds with undisclosed amounts, & funds without first close

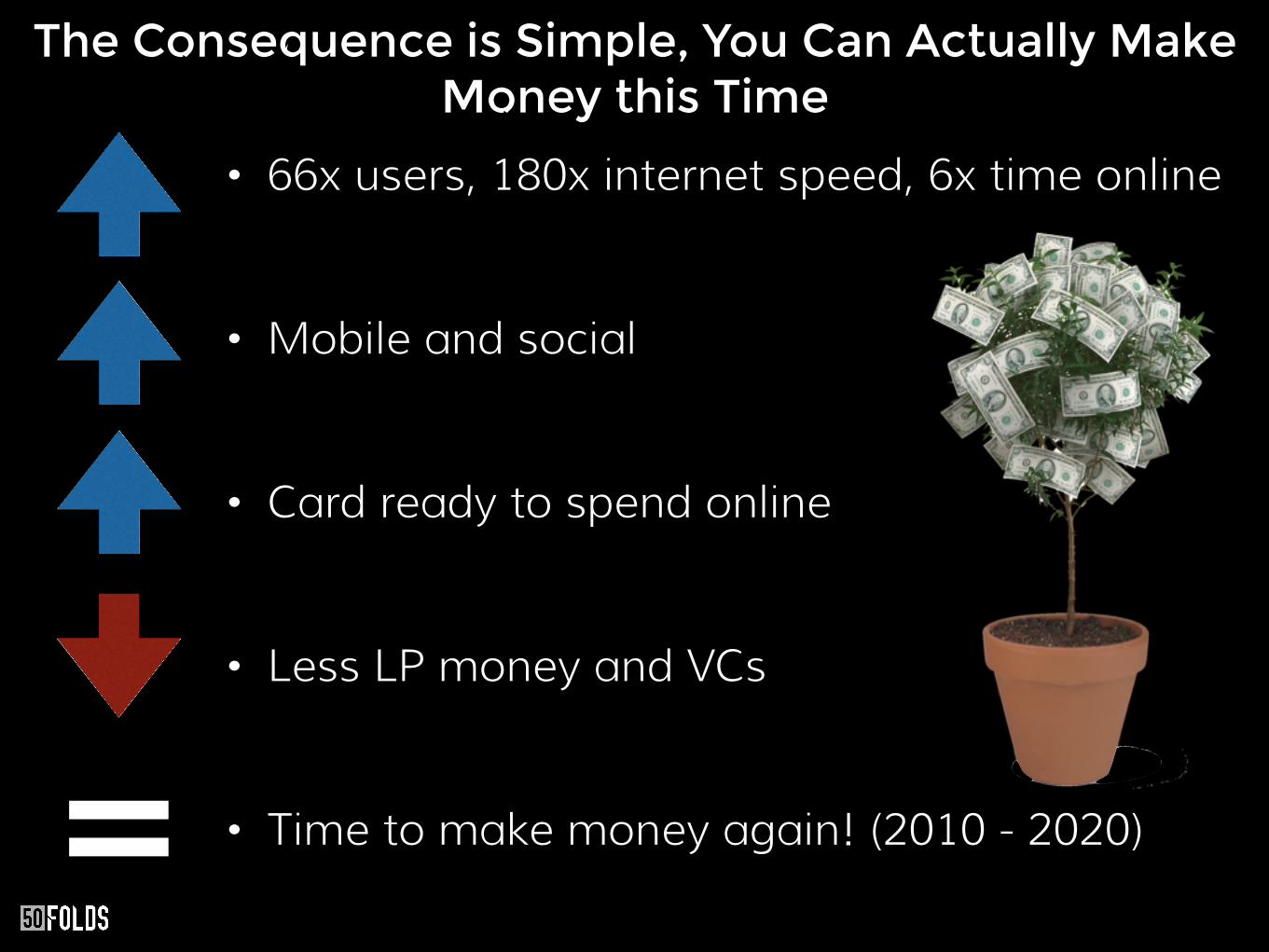

• 66x users, 180x internet speed, 6x time online

• Mobile and social

• Card ready to spend online

• Less LP money and VCs

• Time to make money again! (2010 - 2020)

The Consequence is Simple, You Can Actually Make Money this Time

=

That’s America, but what About Here?

The Same Dynamics are Already Evident in Asia, but we will Grow Faster

SEA is Bigger Than the USA in Many Respects

Source: Social, Digital & Mobile in APAC, WeAreSocial, 2014

SEA USA2x

70%

90%

2x

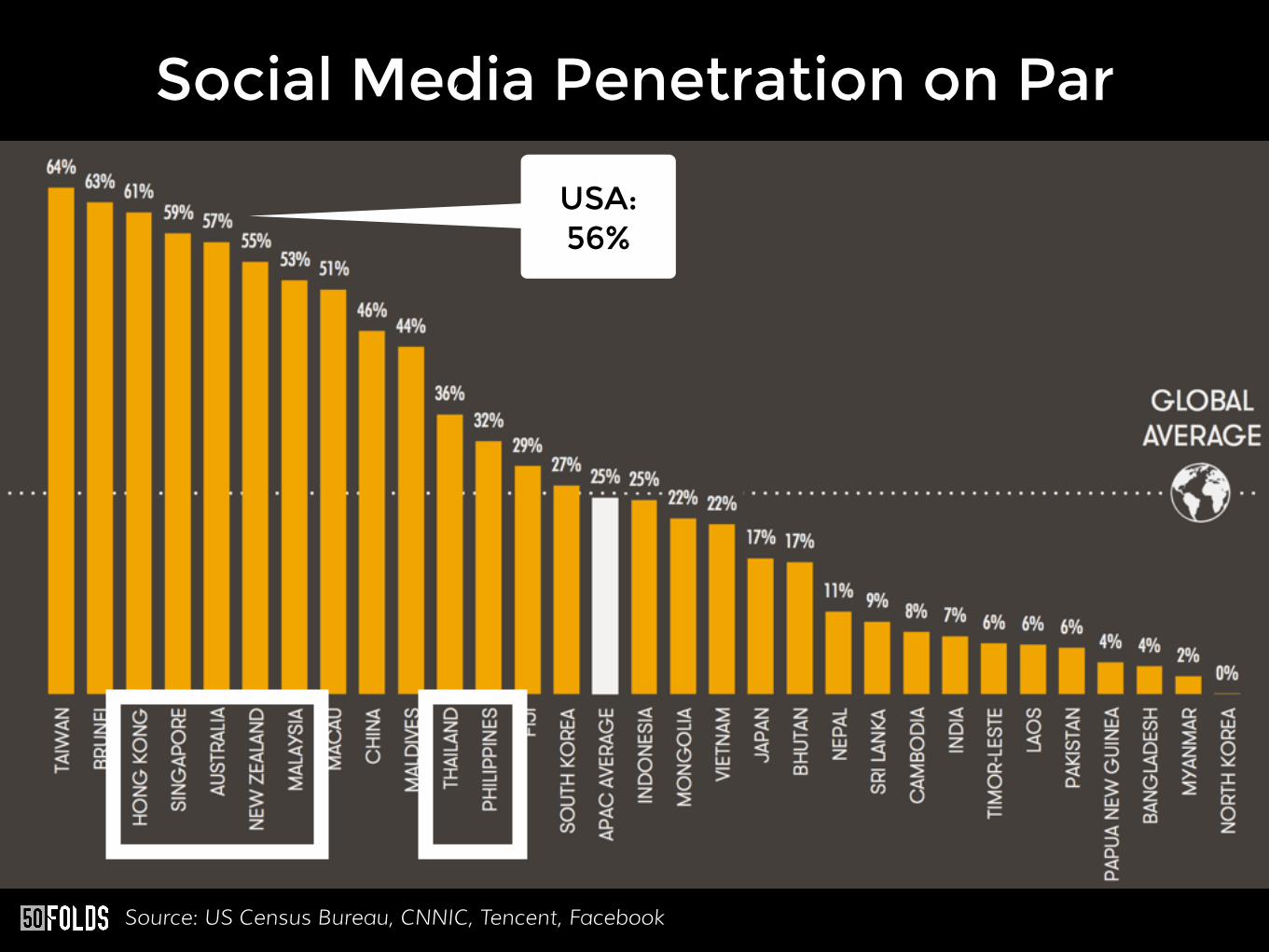

Social Media Penetration on Par

Source: US Census Bureau, CNNIC, Tencent, Facebook

USA: 56%

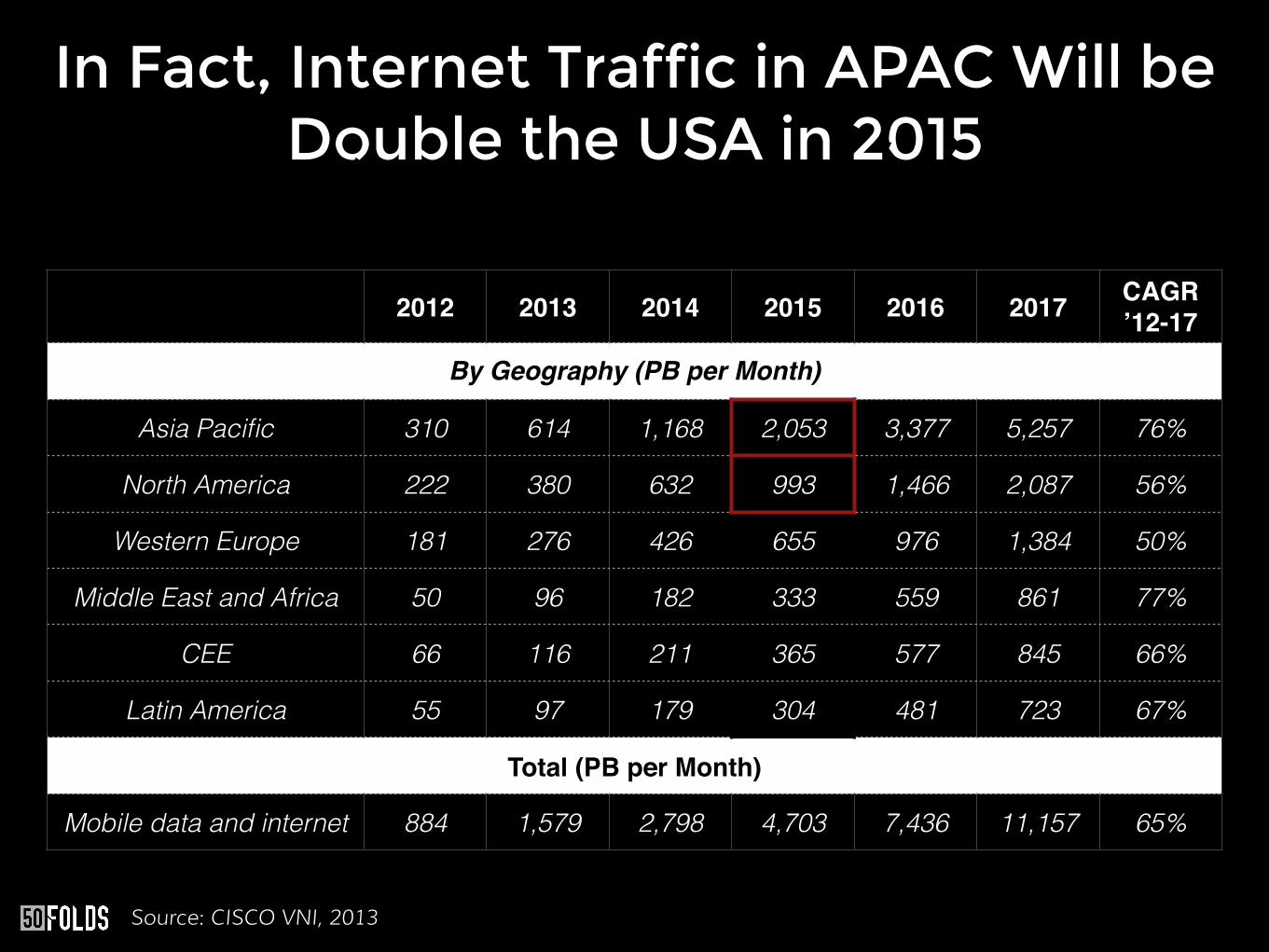

In Fact, Internet Traffic in APAC Will be Double the USA in 2015

2012 2013 2014 2015 2016 2017 CAGR ’12-17

By Geography (PB per Month)

Asia Pacific 310 614 1,168 2,053 3,377 5,257 76%

North America 222 380 632 993 1,466 2,087 56%

Western Europe 181 276 426 655 976 1,384 50%

Middle East and Africa 50 96 182 333 559 861 77%

CEE 66 116 211 365 577 845 66%

Latin America 55 97 179 304 481 723 67%

Total (PB per Month)

Mobile data and internet 884 1,579 2,798 4,703 7,436 11,157 65%

Source: CISCO VNI, 2013

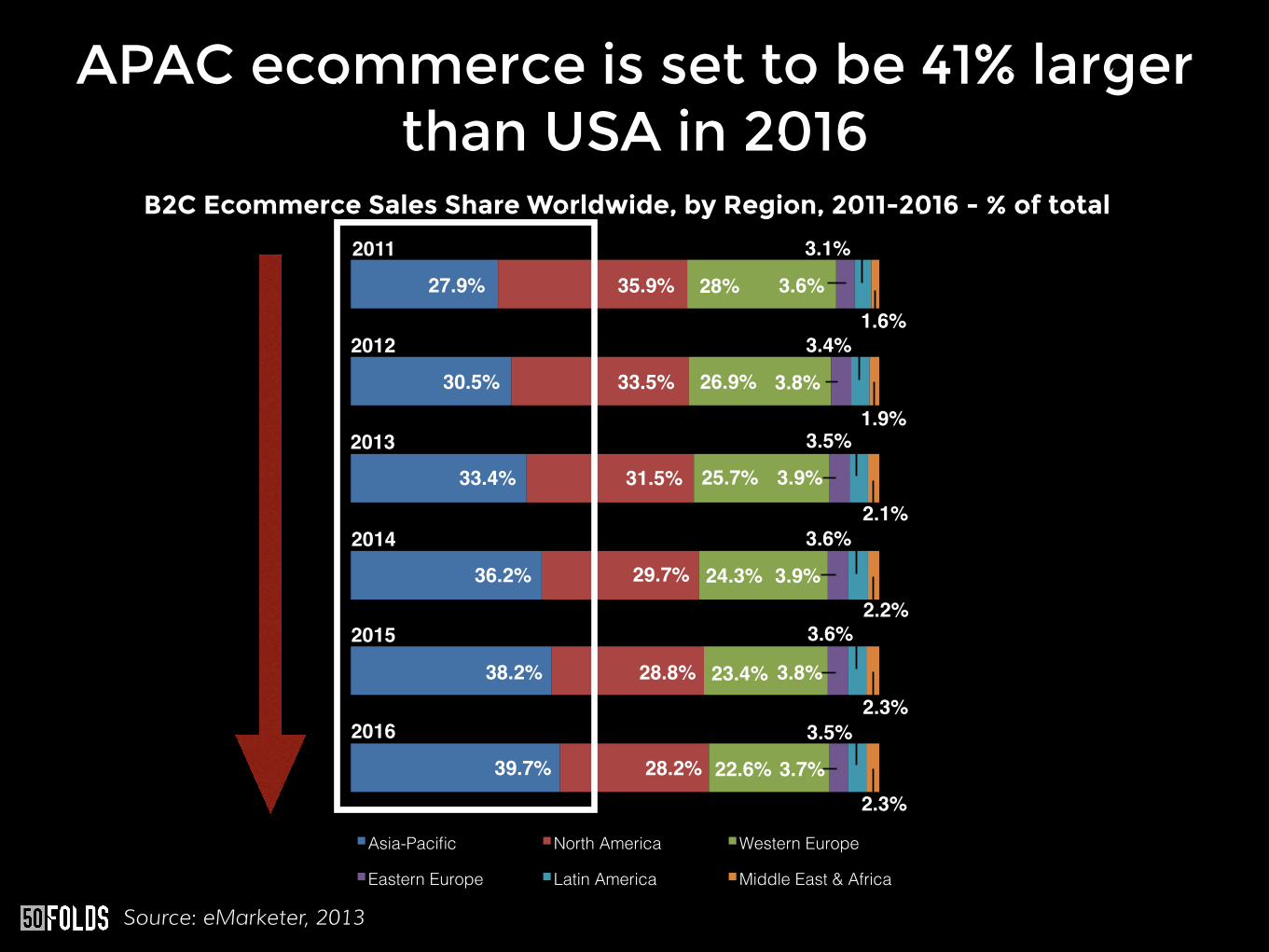

APAC ecommerce is set to be 41% larger than USA in 2016

2.2%!

Asia-Pacific! North America! Western Europe !

Eastern Europe! Latin America! Middle East & Africa!

2.1%!

27.9%! 35.9%! 28%! 3.6%!

3.1%!

1.6%!

2011!

30.5%! 33.5%! 26.9%! 3.8%!

3.4%!

1.9%!

2012!

33.4%! 31.5%! 25.7%! 3.9%!

3.5%!2013!

36.2%! 29.7%! 24.3%! 3.9%!

3.6%!2014!

2015!

2016!2.3%!

38.2%! 28.8%! 23.4%!3.8%!

3.6%!

2.3%!

39.7%! 28.2%! 22.6%!3.7%!

3.5%!

Source: eMarketer, 2013

B2C Ecommerce Sales Share Worldwide, by Region, 2011-2016 - % of total

China Has Proven You Can Build Bigger Than in America

India is Making Progress too and has 4+ Consumer Unicorns

So What Does SEA Have Going for it?

The Early Signs are Encouraging

There has Been a lot of Seed Stage Activity

In 2012 NRF TIS Scheme in SG Created a Lot of VCs Which Drove Seed Funding

• Hired, trained and fired a lot of people

• Many former employees set up companies

• Invested incredible amounts of marketing money • Educated customers (Very costly) • Increase in ecommerce penetration % • New and existing businesses are more viable

Rocket Internet Entered Market

Started to be More Corporate and Independent Accelerators

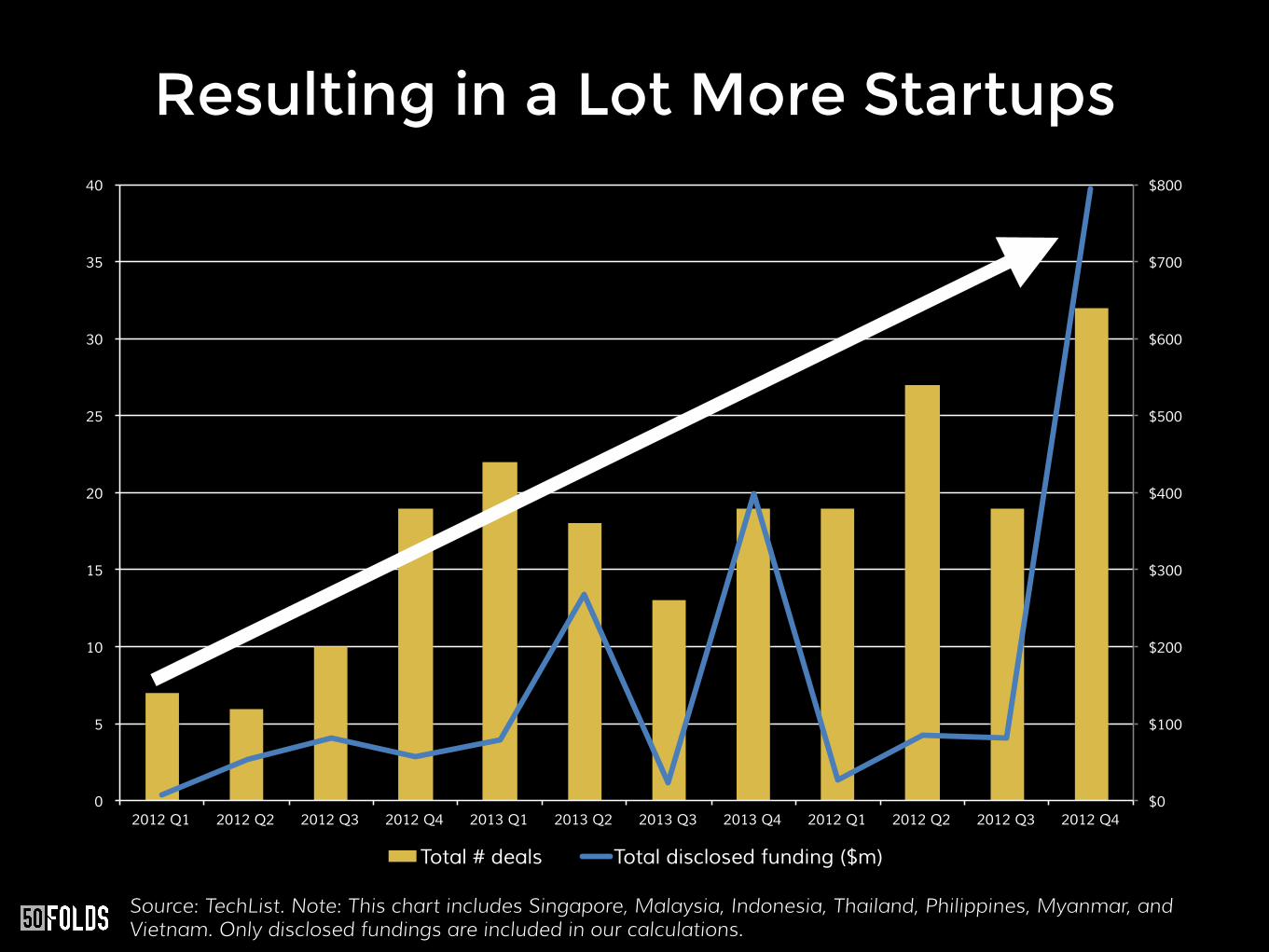

Resulting in a Lot More Startups

Source: TechList. Note: This chart includes Singapore, Malaysia, Indonesia, Thailand, Philippines, Myanmar, and Vietnam. Only disclosed fundings are included in our calculations.

$0

$100

$200

$300

$400

$500

$600

$700

$800

0

5

10

15

20

25

30

35

40

2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4

Total # deals Total disclosed funding ($m)

Hard Slog to Date has Rewarded the Diligent (But it took a long time

to get big)

$11.8 billion spent acquiring Asian startups

in the last 6 years

$2.6 billion was on SEA startups

• JobStreet / Seek - A$545 • Viki / Rakuten - $200m • ZipDial / Twitter - N/A • Travelmob / HomeAway - $22m • Zopim / ZenDesk - ~$30m • SGCarMart / SPH - $48m • JobCentral / CareerBuilder - N/A • Detik / Para Group - $60m • Tarad / Rakuten - N/A

There Have Been Some Decent Acquisitions

Lots of brand name

foreign acquirers

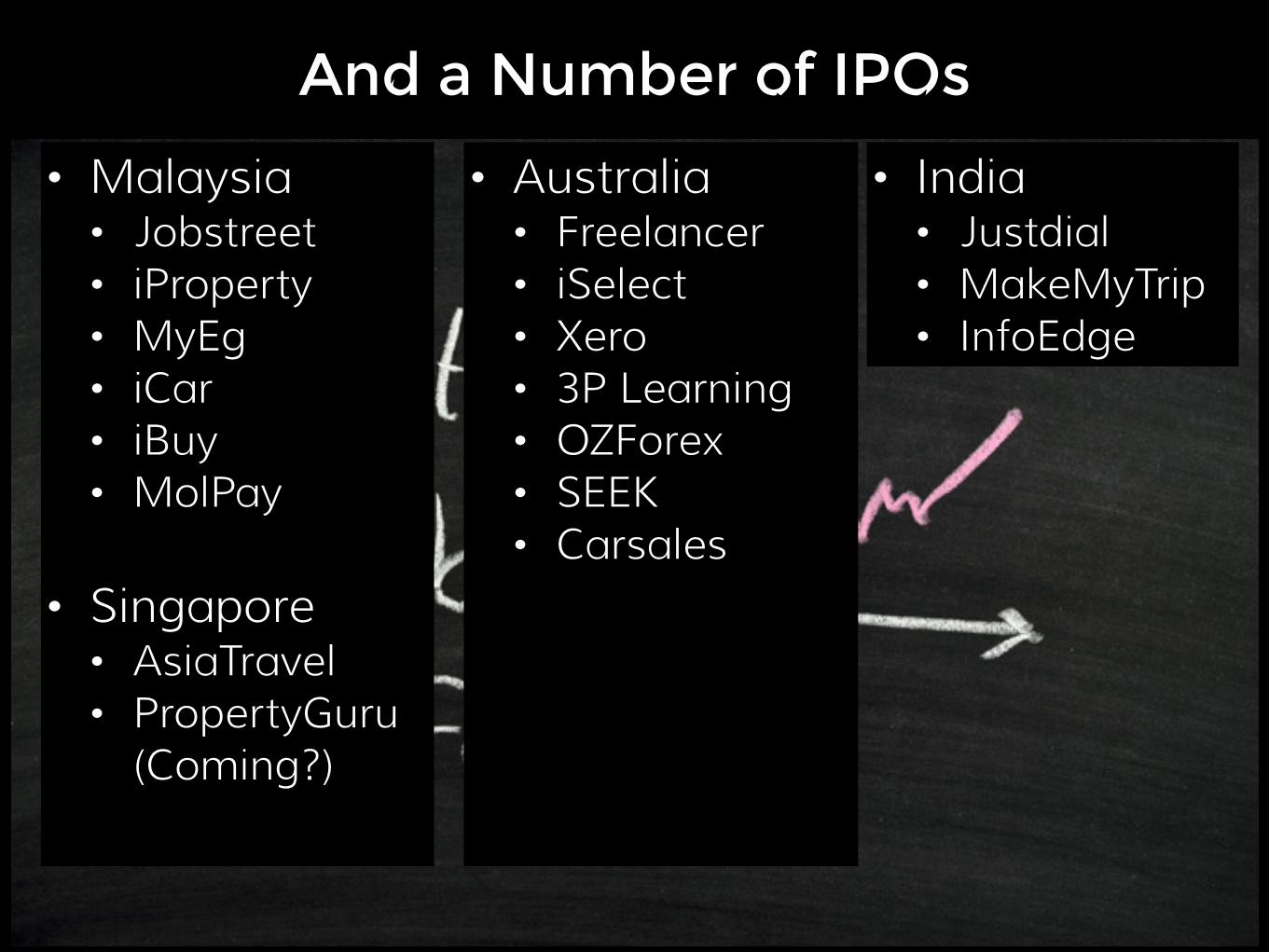

• Australia • Freelancer • iSelect • Xero • 3P Learning • OZForex • SEEK • Carsales

And a Number of IPOs

• Malaysia • Jobstreet • iProperty • MyEg • iCar • iBuy • MolPay

• Singapore • AsiaTravel • PropertyGuru

(Coming?)

• India • Justdial • MakeMyTrip • InfoEdge

That was before, things have changed in past 2

years

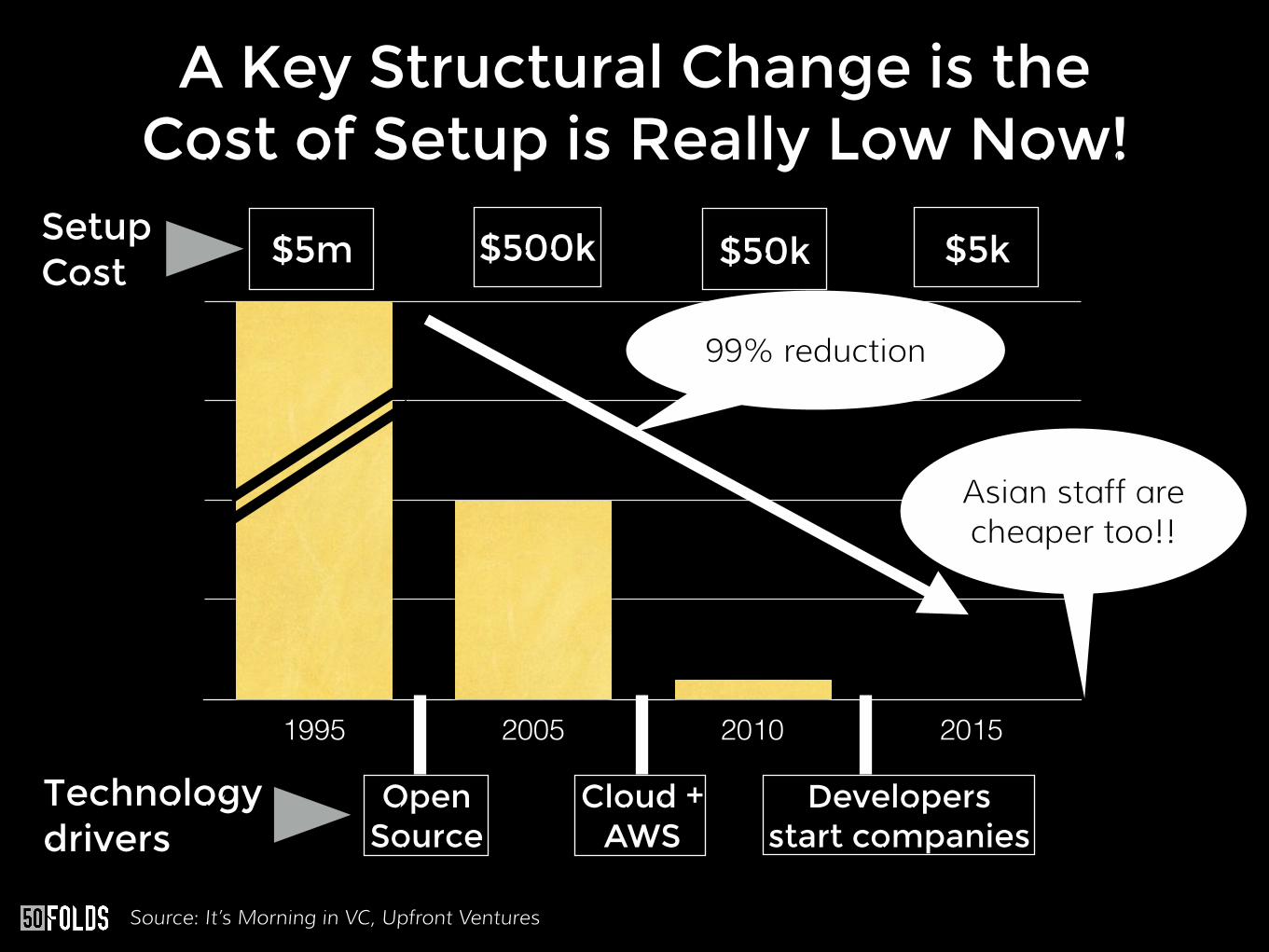

A Key Structural Change is the Cost of Setup is Really Low Now!

1995 2005 2010 2015

$5m $500k $50k $5k

Technology drivers

Open Source

Cloud + AWS

Developers start companies

99% reduction

Source: It’s Morning in VC, Upfront Ventures

Asian staff are cheaper too!!

Setup Cost

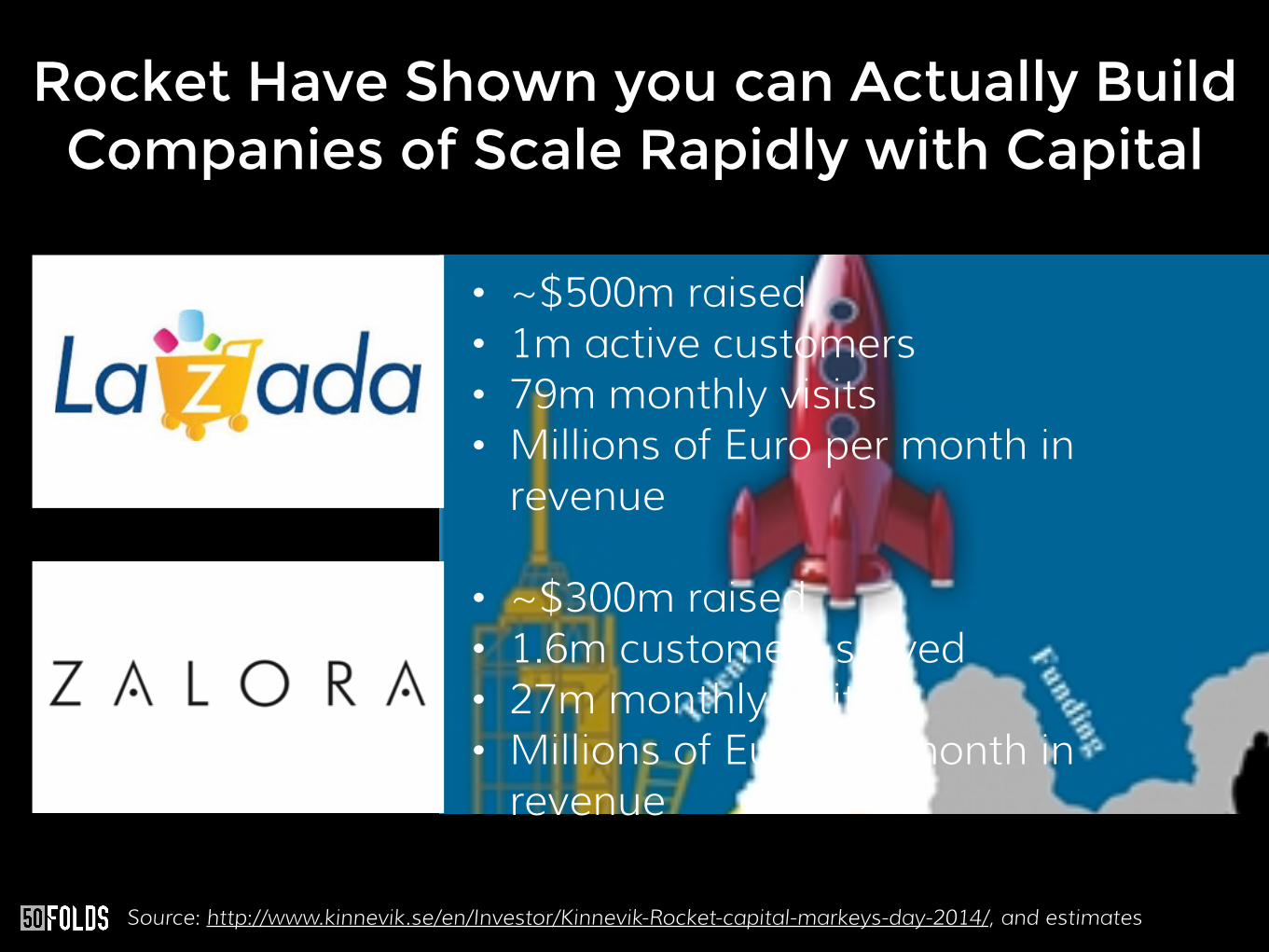

Startups are raising more money and getting

bigger faster

• ~$500m raised • 1m active customers • 79m monthly visits • Millions of Euro per month in

revenue

• ~$300m raised • 1.6m customers served • 27m monthly visits • Millions of Euro per month in

revenue

Rocket Have Shown you can Actually Build Companies of Scale Rapidly with Capital

Source: http://www.kinnevik.se/en/Investor/Kinnevik-Rocket-capital-markeys-day-2014/, and estimates

Local Companies are Following Suit

• Huge, growing online regional market

• Growing exit market

• Increasingly higher quality companies

• But limited capital available!

• Opportunity? (2015 - 2025)

Logically, There is a Big Opportunity in SEA

=

So What Does the Future Hold?

Investments

• Increased volume of structures to pump out a volume of startups

• Reverse shifts in investment stage focus for early and late stage investors • More Series-A funds in SEA • Late stage VCs move to Seed stage in India to

make ‘call options’

• Increased availability of early stage financing, but still limitations on investable companies

Increased Early Stage Focus for Different Reasons

• More foreign investors enter the market • Continued foreign investment from Japan, • Chinese mobilising • Nascent interest from US and EU

• Local large family conglomerates start committing more capital

• More later stage funding announcements

More Foreign Money and Late Stage Investments

Valuations and Exits

• Seed valuations for great companies will increase as will the investment sizes

• Continue to be small exits

• Messaging companies may make purchases to ‘fill in’ their ecosystems, global brands make niche acquisitions

Valuations Increase Across the Board and More Small Exits

Operating Environment

• Introduction of ASEAN but no obvious benefit

• Potential for more questionable regulation, particularly in ecommerce • Thailand and Indonesia?

• Continued HR challenges resulting in wage inflation and importation of specialty talent

Governments Get in the Way and Costs of Staff Rise

Startups

• Increased regionalization of local companies and category leader dominance

• Start to see more overseas expansion of well funded EU/US companies

Bigger Regional Companies and Foreign Invasion

• More startups in ‘hot’ verticals

• Foreign entrepreneurs and Rocket grads will drive a lot of new startups

• Struggling startups will complain there is a Series-A crunch

More of Everything- More Startups and More Failures

Honestly…

You Missed China

You Sort of Missed India.

Now is a Great Time to Access South East Asia

Want to know

Leverage the Venture Capital Opportunity?

Let’s Have a Chat

• www.AlexanderJarvis.com

• @ADJBlog

• sg.linkedin.com/in/alexanderdjarvis/

Recommended