The Role of Renewables in Your The Role of Renewables in Your Future Resource PortfolioFuture Resource Portfolio

APPA National ConferenceAPPA National ConferenceJune 12, 2006June 12, 2006

Colorado Springs Utilities’ ApproachColorado Springs Utilities’ ApproachDiane Johnson

General Manager, Strategic PlanningColorado Springs Utilities

Presentation OverviewPresentation Overview

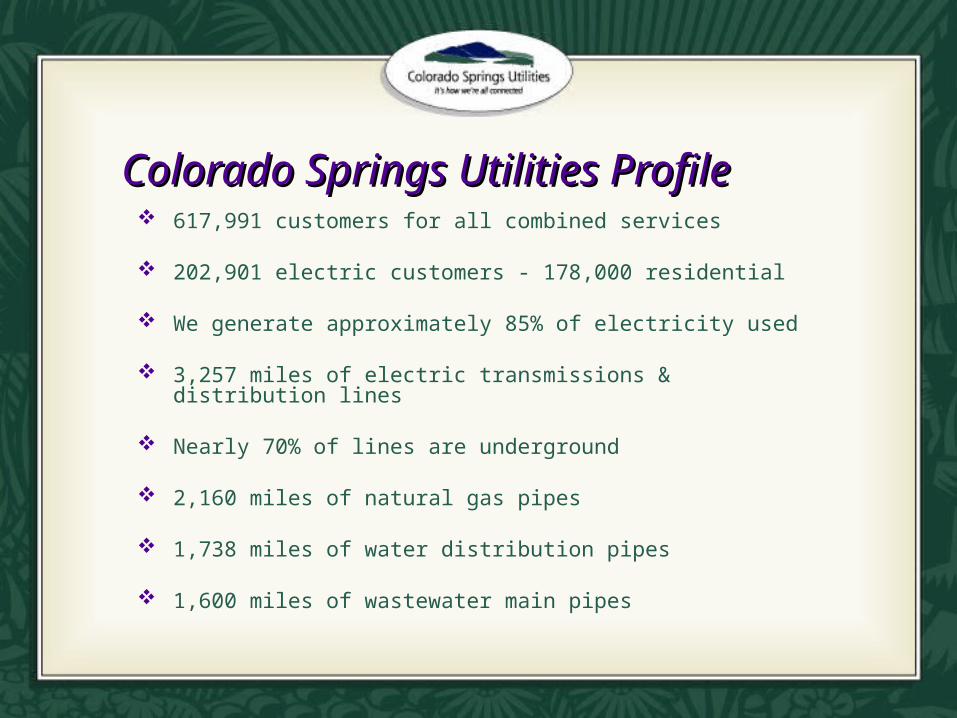

Colorado Springs Utilities Profile

Framework for a Renewable Energy Strategy Community Drivers – Customer surveys Industry Drivers – EIRP & WAPA requirements Regulatory Drivers – RPS - Amendment 37 Challenges & Potential Opportunities

Customer-side renewables programs Customer-side renewable energy plan Net metering PV rebate program Green product program

Colorado Springs Utilities ProfileColorado Springs Utilities Profile 617,991 customers for all combined services

202,901 electric customers - 178,000 residential

We generate approximately 85% of electricity used

3,257 miles of electric transmissions & distribution lines

Nearly 70% of lines are underground

2,160 miles of natural gas pipes

1,738 miles of water distribution pipes

1,600 miles of wastewater main pipes

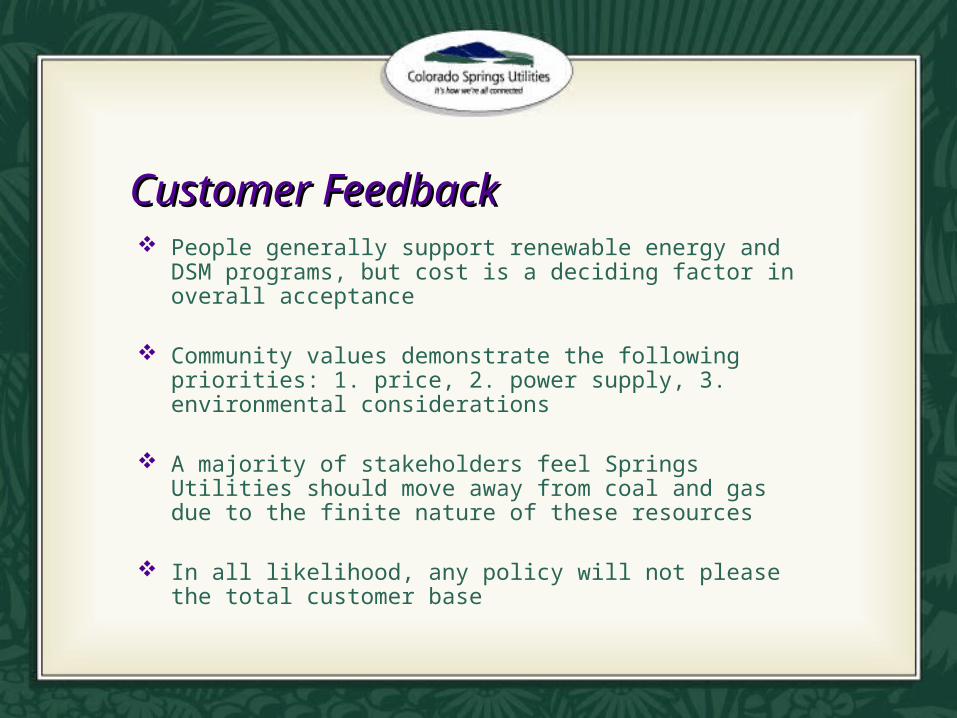

Customer FeedbackCustomer Feedback People generally support renewable energy and DSM

programs, but cost is a deciding factor in overall acceptance

Community values demonstrate the following priorities: 1. price, 2. power supply, 3. environmental considerations

A majority of stakeholders feel Springs Utilities should move away from coal and gas due to the finite nature of these resources

In all likelihood, any policy will not please the total customer base

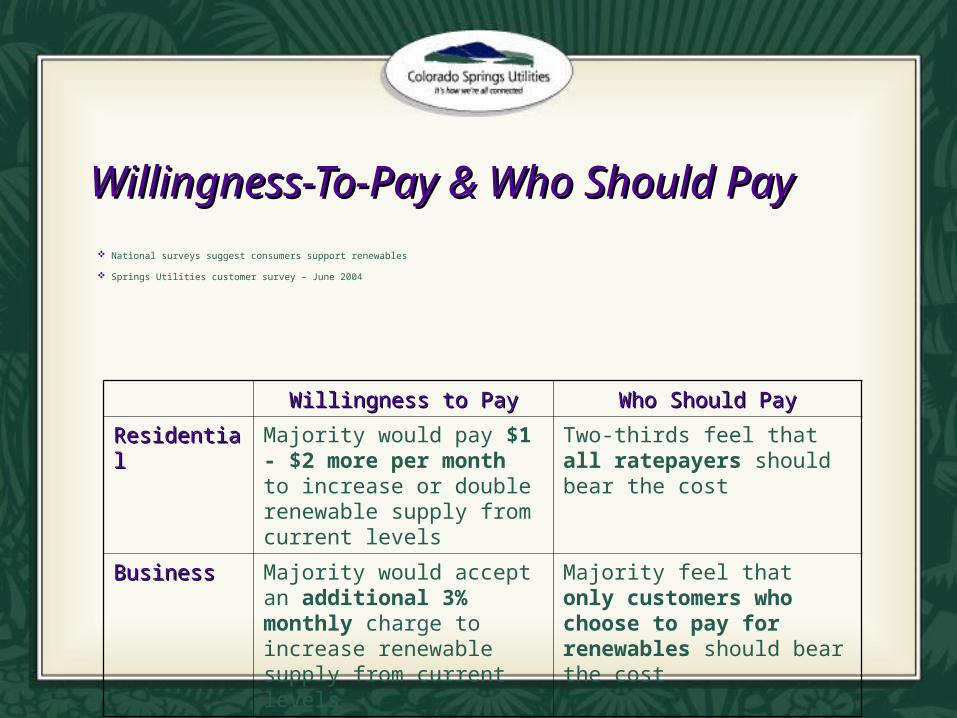

Willingness-To-Pay & Who Should PayWillingness-To-Pay & Who Should Pay

National surveys suggest consumers support renewables

Springs Utilities customer survey – June 2004

Willingness to PayWillingness to Pay Who Should PayWho Should Pay

ResidentialResidential Majority would pay $1 - $2 more per month to increase or double renewable supply from current levels

Two-thirds feel that all ratepayers should bear the cost

BusinessBusiness Majority would accept an additional 3% monthly charge to increase renewable supply from current levels

Majority feel that only customers who choose to pay for renewables should bear the cost

EIRP DriversEIRP Drivers Sound strategic & operational planning

Required by WAPA – PPA for 70MW large hydro

Minimize cost of electricity (rates)

Meet reliability requirements

Maintain financial soundness

Promote environmental stewardship

Balance risk and cost

Provide flexible plans

Public Process & Advisory Groups

EIRPAnalysis

Environmental & Reliability Requirements

Forecasts

Influencing Customers’Consumption thru DSM

Direction & Recommendations

ConventionalCoal, Gas, etc.

Renewable StrategyHydro, Wind, Solar, etc.

Supply Side Options

Transmission

Existing & New• Supply side resources• Demand side & RE programs• Legislative agenda• Short & long term budgets• Rate structure

Utilities BoardPolicies and Limitations

• Education• Efficiency• Regulation

• Load shaping• Rate Structure• Economic Development

EIRP Analysis ProcessEIRP Analysis ProcessGeneral Public Preference

Gen

eral

Pub

lic P

refe

renc

e

General Public Preference is to Rates Low

New REN by

2011

Current DSM Modest ModerateModerate to Aggressive

Aggressive

Refe

ren

ce

Case Coal-2014

Coal-2019Coal-2023

Coal-2015Coal-2020Coal-2024

Coal-2016Coal-2020

Coal-2018Coal-2023

Coal-2020

Lo

w

8 MW

3 MW Small Hydro-20065MW Wind-2006

Coal-2014Coal-2019Coal-2023

3 MW Small Hydro-20065MW Wind-2006

Coal-2015Coal-2020Coal-2024

3 MW Small Hydro-20065MW Wind-2006

Coal-2016Coal-2021

3 MW Small Hydro-20065MW Wind-2006

Coal-2018Coal-2023

3 MW Small Hydro-20065MW Wind-2006

Coal-2020

Me

diu

m

26 MW

3MW Small Hydro-200610MW Wind-2006

13MW Med Hydro-2011Coal-2015Coal-2019Coal-2024

3MW Small Hydro-200610MW Wind-2006

13MW Med Hydro-2011Coal-2016Coal-2020

3MW Small Hydro-200610MW Wind-2006

13MW Med Hydro-2011Coal-2016Coal-2021

3MW Small Hydro-200610MW Wind-2006

13MW Med Hydro-2011Coal-2019Coal-2023

3MW Small Hydro-200610MW Wind-2006

13MW Med Hydro-2011Coal-2021

Hig

h

50 MW

3MW Small Hydro-200625MW Wind-2006

1MW PV-20077MW Biomass-2011

13MW Med Hydro-20111MW PV-2011

Coal-2015Coal-2020Gas-2024

3MW Small Hydro-200625MW Wind-2006

1MW PV-20077MW Biomass-2011

13MW Med Hydro-20111MW PV-2011

Coal-2016Coal-2021

3MW Small Hydro-200625MW Wind-2006

1MW PV-20077MW Biomass-2011

13MW Med Hydro-20111MW PV-2011

Coal-2017Coal-2021

3MW Small Hydro-200625MW Wind-2006

1MW PV-20077MW Biomass-2011

13MW Med Hydro-20111MW PV-2011

Coal-2019Coal-2023

3MW Small Hydro-200625MW Wind-2006

1MW PV-20077MW Biomass-2011

13MW Med Hydro-20111MW PV-2011

Coal-2021

24 MW 38 MW 86 MW 128 MW

DEMAND SIDE MANAGEMENT OPTIONS

RE

NE

WA

BL

ES

DSM Cumulative Thru 2014

Operational Issues with WindOperational Issues with Wind•Wind integration is challenging for smaller utilitiesWind integration is challenging for smaller utilities•Wind RFP – supply profile is anti-coincident to demandWind RFP – supply profile is anti-coincident to demand

Wind Annual Capacity Factors

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Hour

Wind Avg CF Typical summer peak day

WIND AVG HOURLY PROFILE

SUMMER PEAK DAY HOURLY PROFILE

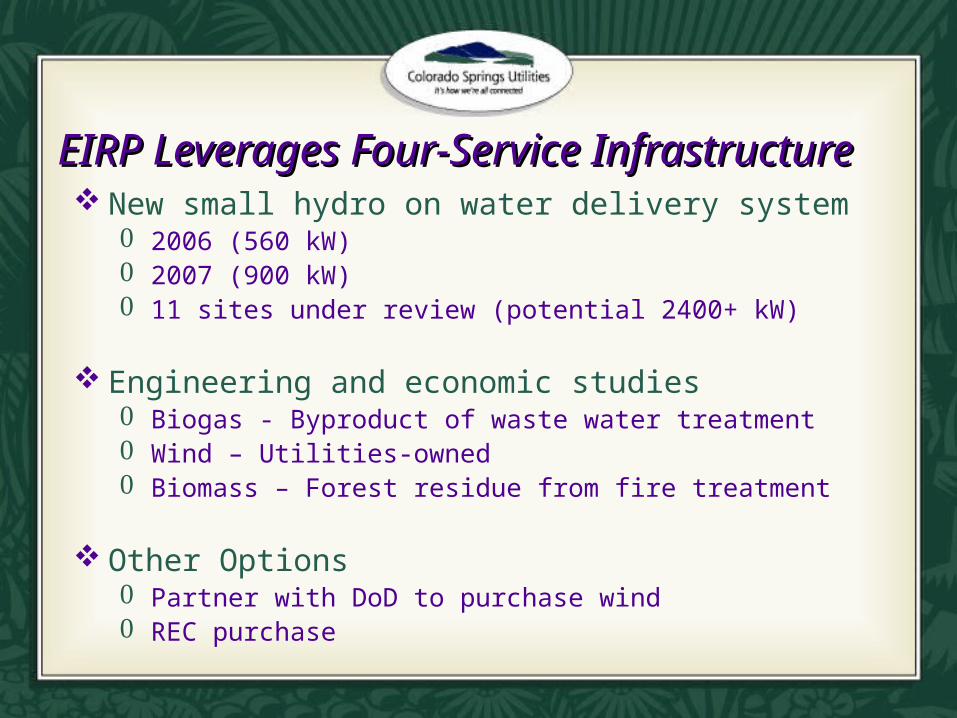

EIRP Leverages Four-Service InfrastructureEIRP Leverages Four-Service Infrastructure New small hydro on water delivery system

2006 (560 kW) 2007 (900 kW) 11 sites under review (potential 2400+ kW)

Engineering and economic studies Biogas - Byproduct of waste water treatment Wind – Utilities-owned Biomass – Forest residue from fire treatment

Other Options Partner with DoD to purchase wind REC purchase

EIRP SummaryEIRP Summary 2004 EIRP Recommendations

Medium Renewables• 3 MW Hydro• 10 MW Wind• 13 MW Medium Hydro• Conduct additional analysis of biomass options, 2005-6

Moderate (National average) DSM • 0.25% of energy per year, 0.4% of demand

Traditional supply side resources • Coal – 2016• Coal – 2021

Key Drivers for 2006 EIRP Update/Changes Economics Operational issues RPS - Amendment 37 – Decision to self-certify

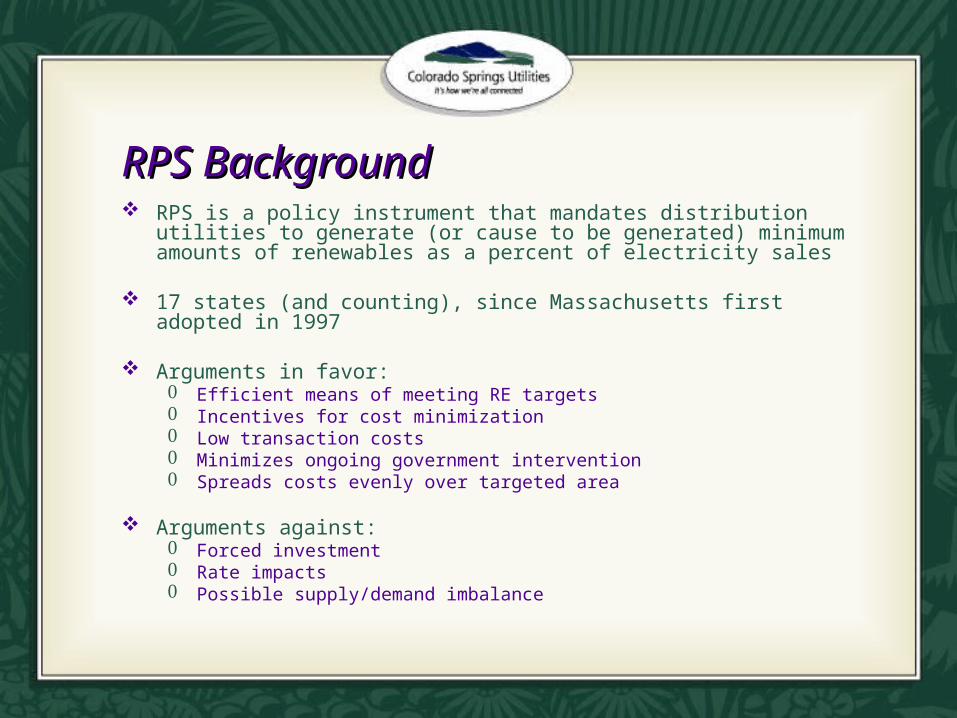

RPS BackgroundRPS Background RPS is a policy instrument that mandates distribution utilities to generate

(or cause to be generated) minimum amounts of renewables as a percent of electricity sales

17 states (and counting), since Massachusetts first adopted in 1997

Arguments in favor: Efficient means of meeting RE targets Incentives for cost minimization Low transaction costs Minimizes ongoing government intervention Spreads costs evenly over targeted area

Arguments against: Forced investment Rate impacts Possible supply/demand imbalance

Colorado Amendment 37Colorado Amendment 37 RPS passed by Colorado voters in Nov. 2004 – the first ever voter-initiated

RPS

Renewable Energy Standard 3% of retail sales by 2007; 6% by 2011; 10% by 2015 1.25 in-state multiplier Average standard compared to RPS policies in other states

Eligible renewables – wind, solar, biomass, small hydro (<10 MW), geothermal, RECs

Solar Mandates for IOUs 0.4% or retail sales by 2015 (1/2 on customer-side) Minimum rebates for solar PV – $2 per watt

Rate Cap – Maximum 1% retail rate impact on each customer’s annual electricity bill

Municipal Utilities Option to self-certify - no solar mandates Option to exempt through local election

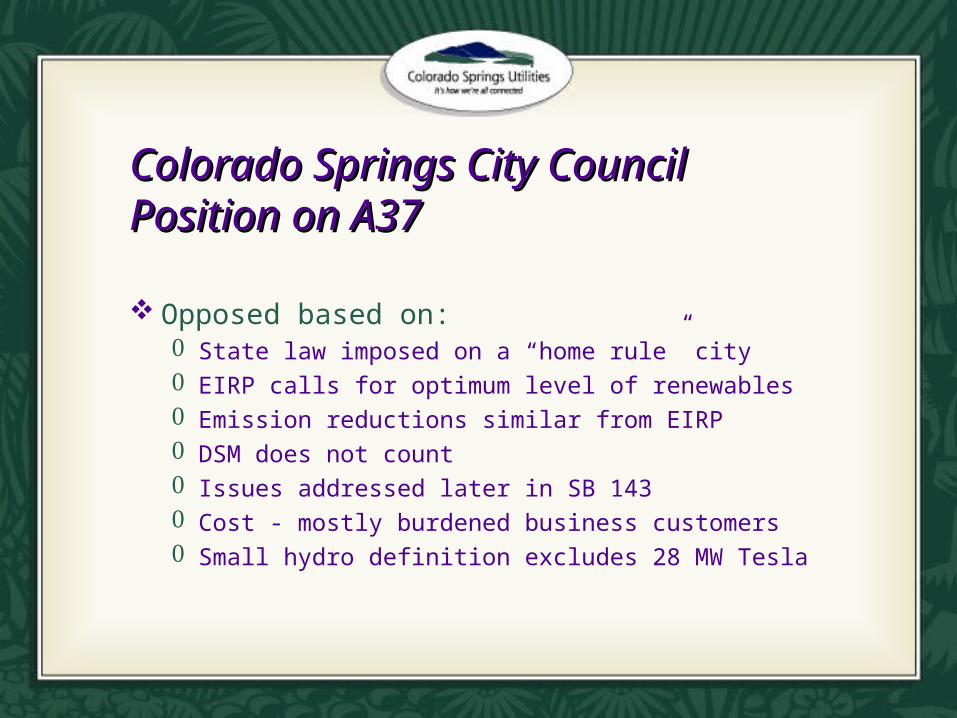

Colorado Springs City Council Colorado Springs City Council Position on A37Position on A37

Opposed based on: State law imposed on a “home rule” city EIRP calls for optimum level of renewables Emission reductions similar from EIRP DSM does not count Issues addressed later in SB 143 Cost - mostly burdened business customers Small hydro definition excludes 28 MW Tesla

Amendment 37 Election ResultsAmendment 37 Election Results

Yes No

Colorado1,029,445 53% 898,360 47%

El Paso County98,518 45% 122,866 55%

City of Colorado Springs 46% 54%

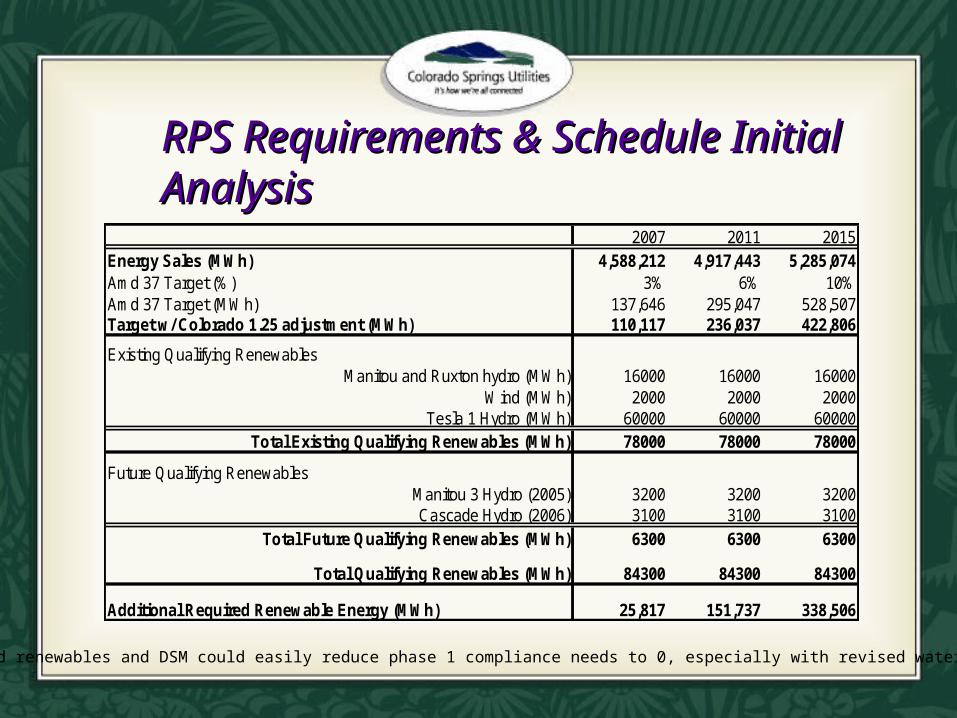

RPS Requirements & Schedule RPS Requirements & Schedule Initial AnalysisInitial Analysis

Planned renewables and DSM could easily reduce phase 1 compliance needs to 0, especially with revised water limits

2007 2011 2015Energy Sales (MWh) 4,588,212 4,917,443 5,285,074Amd 37 Target (%) 3% 6% 10%Amd 37 Target (MWh) 137,646 295,047 528,507Target w/ Colorado 1.25 adjustment (MWh) 110,117 236,037 422,806

Existing Qualifying RenewablesManitou and Ruxton hydro (MWh) 16000 16000 16000

Wind (MWh) 2000 2000 2000Tesla 1 Hydro (MWh) 60000 60000 60000

Total Existing Qualifying Renewables (MWh) 78000 78000 78000

Future Qualifying RenewablesManitou 3 Hydro (2005) 3200 3200 3200Cascade Hydro (2006) 3100 3100 3100

Total Future Qualifying Renewables (MWh) 6300 6300 6300

Total Qualifying Renewables (MWh) 84300 84300 84300

Additional Required Renewable Energy (MWh) 25,817 151,737 338,506

Customer-side Renewables and Customer-side Renewables and Amendment 37 StrategyAmendment 37 Strategy Amendment 37 (SB 143) compliance

Our direction is to comply with Amendment 37 by self-certifying a “substantially similar” renewable energy standard

We support & encourage voluntary additions of RE to our system

Springs Utilities’ objectives with customer-side RE programs Support the intent of Amendment 37 Provide customers greater choice Be good stewards of the environment Ensure safety and reliability of distributed energy resources Gain experience with small-scale, distributed generation Be an active partner in RE market development (e.g. PV)

Operational strategy – combine customer-side RE with DSM

Customer-side Renewable Energy PlanCustomer-side Renewable Energy Plan Background

2004 Renewable Energy Options Assessment study identified leading customer-side renewable energy options

Purpose Support the intent of EIRP Consistent with organizational strategy and environmental goals Acknowledge strategic role of customer-side renewables – i.e., A37

Objectives of the Customer-side Plan Benchmarking Gap analysis Develop scenarios Establish strategic direction Outline a 5-year tactical plan

Customer-side Scenario Contributions to Amendment 37 Compliance (2005-2011)

70,000

90,000

110,000

130,000

150,000

170,000

190,000

210,000

230,000

250,000

2005 2006 2007 2008 2009 2010 2011

MW

hs

of

Ren

ewab

les

A37 Targets

BAU Customer-sideScenario

Modest Customer-side Scenario

Moderate Customer-side Scenario

Aggressive Customer-side Scenario

Supply-sideResources

Note: Hatch marks overlap for customer-side scenarios with aggressive on bottom

109,295

232,016

Net Metering Pilot ProgramNet Metering Pilot Program Launched in 2004 to formalize what was an informal policy

City Council approved “enhancements” in the 2006 Rate Case

Supports RE plans and parallels amendment 37 requirements

Current participation 1 commercial customer 4 residential customers

More systems expected due to rebate program

$4 per watt (AC) rebate – residential, C&I

Modest budget ($220,000) 2006 Participation goal – 60 kW Process

Reservation request Pre-inspection Rebate claim Post-inspection Interconnection authorization

More info at www.csu.org/residential/rebates/renew_rebate/index.html

Renewable Energy Rebate Program Renewable Energy Rebate Program (Photovoltaics) (Photovoltaics)

Green Power ProductGreen Power Product

Available since 1998

Objective are: (1) to give customers choice (2) to capture un-tapped demand exhibited in “willingness-to-pay” surveys

Sold in blocks: $3.32/100kWh, monthly payment

Hedging benefit – Electric cost adjustment credit for each block purchased

Customers: 1000 residential, 15 business

1 MW wind contract Source: Ponnequin Wind Farm on CO/WY border Actual wind production depends on intermittent resource True-up discrepancy with RECs or purchased wind

SummarySummary Balancing cost, reliability and environmental stewardship

Leveraging four-service infrastructure

Addressing the challenges of wind integration

Meeting RPS - Amendment 37 obligations via Springs Utilities’ own renewable energy standard

Supporting emerging renewable energy technologies through PV rebates & green product programs

Responding to diverse customer views on cost of renewables through voluntary programs

Questions??Questions??

Contact: Diane Johnson

General Manager, Strategic Planning

Colorado Springs Utilities

719.668.7513

Recommended