“THE ROAD TO HAMBANTHOTA”

W K H Wegapitiya

Chairman,

LAUGFS Holdings Limited

An Investor’s Perspective

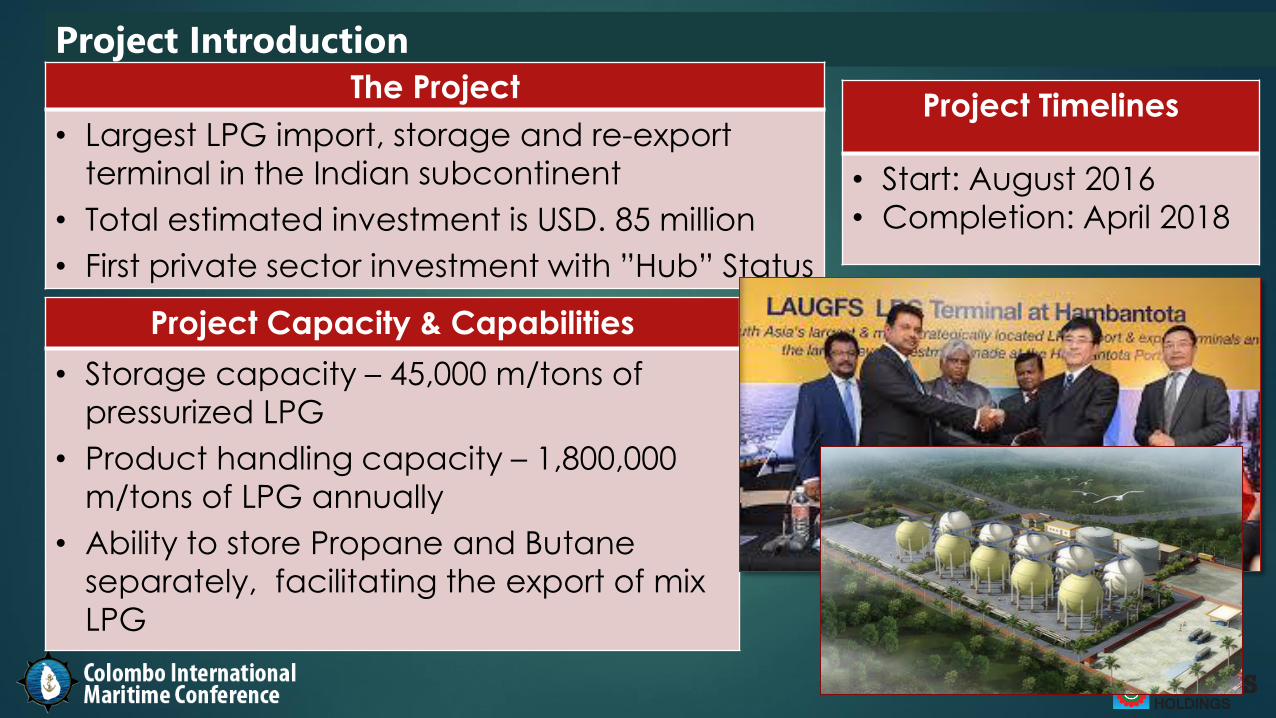

Project Timelines

• Start: August 2016

• Completion: April 2018

Project Capacity & Capabilities

• Storage capacity – 45,000 m/tons of

pressurized LPG

• Product handling capacity – 1,800,000

m/tons of LPG annually

• Ability to store Propane and Butane

separately, facilitating the export of mix

LPG

Project Introduction

The Project

• Largest LPG import, storage and re-export

terminal in the Indian subcontinent

• Total estimated investment is USD. 85 million

• First private sector investment with ”Hub” Status

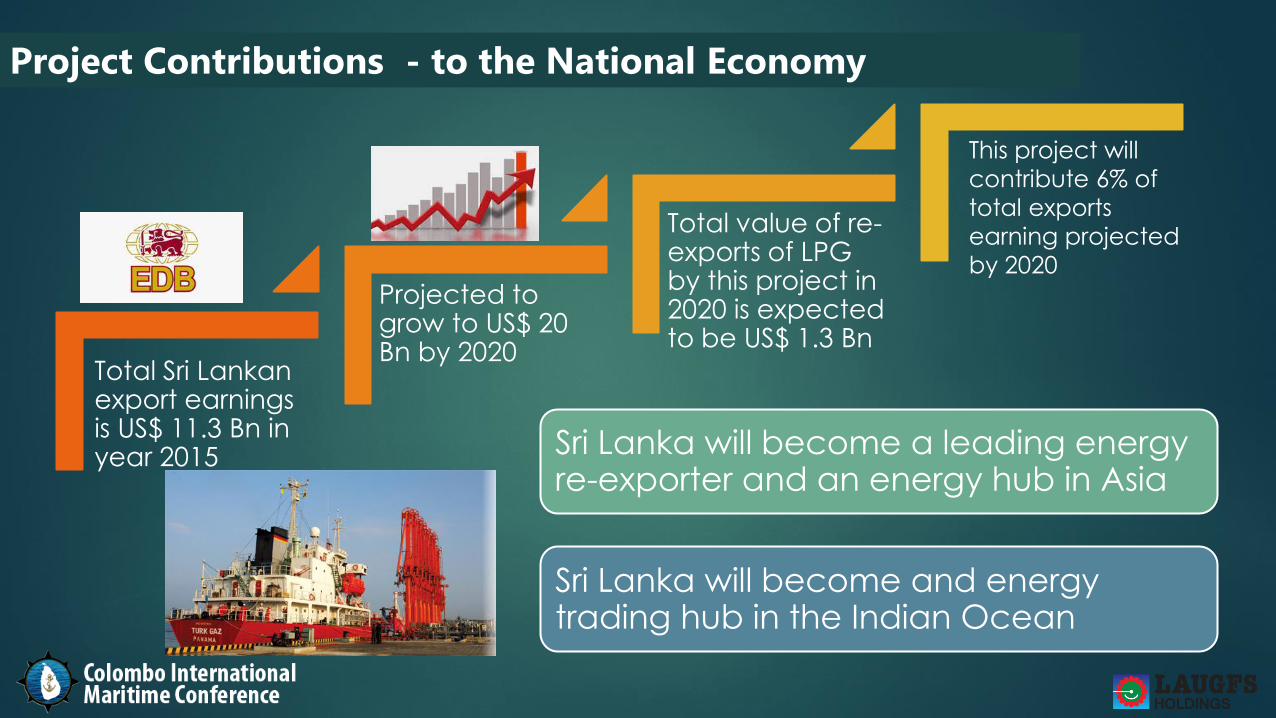

Project Contributions - to the National Economy

Total value of re-exports of LPG by this project in 2020 is expected to be US$ 1.3 Bn

This project will

contribute 6% of

total exports

earning projected

by 2020

Sri Lanka will become a leading energy re-exporter and an energy hub in Asia

Sri Lanka will become and energy trading hub in the Indian Ocean

Total Sri Lankan export earnings is US$ 11.3 Bn in year 2015

Projected to grow to US$ 20 Bn by 2020

This project will require 15 to 20 LPG ships to provide logistics support – VLGC, Fully refrigerated and midsize pressurized LPG carriers

This will create about 500 new employments in the maritime sector, other than the direct project related employments

USD.5.5 million additional annual income to the Sri Lanka Ports Authority

Growth in the Sri Lankan maritime industry – Ship chandelling, ship repairs, maritime training

Project Contributions - to the Maritime Industry

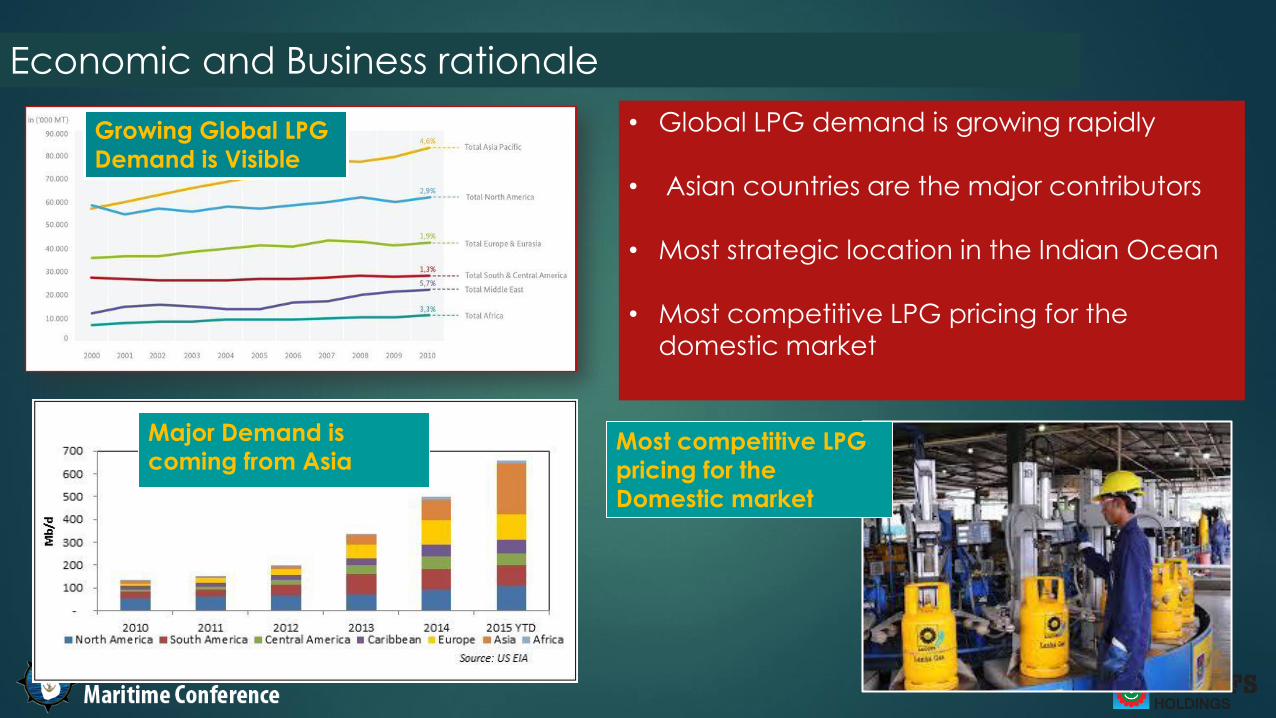

Growing Global LPG

Demand is Visible

• Global LPG demand is growing rapidly

• Asian countries are the major contributors

• Most strategic location in the Indian Ocean

• Most competitive LPG pricing for the

domestic market

Economic and Business rationale

Most competitive LPG

pricing for the

Domestic market

Major Demand is

coming from Asia

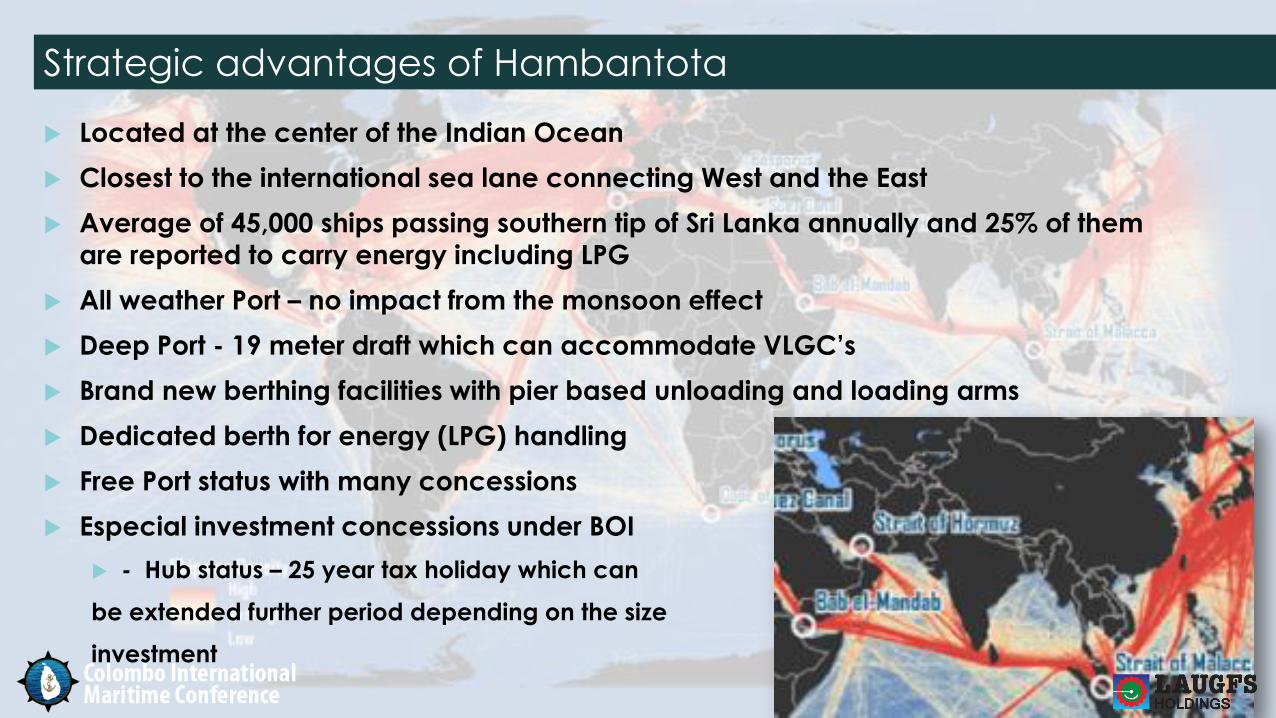

Strategic advantages of Hambantota

Located at the center of the Indian Ocean

Closest to the international sea lane connecting West and the East

Average of 45,000 ships passing southern tip of Sri Lanka annually and 25% of them

are reported to carry energy including LPG

All weather Port – no impact from the monsoon effect

Deep Port - 19 meter draft which can accommodate VLGC’s

Brand new berthing facilities with pier based unloading and loading arms

Dedicated berth for energy (LPG) handling

Free Port status with many concessions

Especial investment concessions under BOI

- Hub status – 25 year tax holiday which can

be extended further period depending on the size

investment

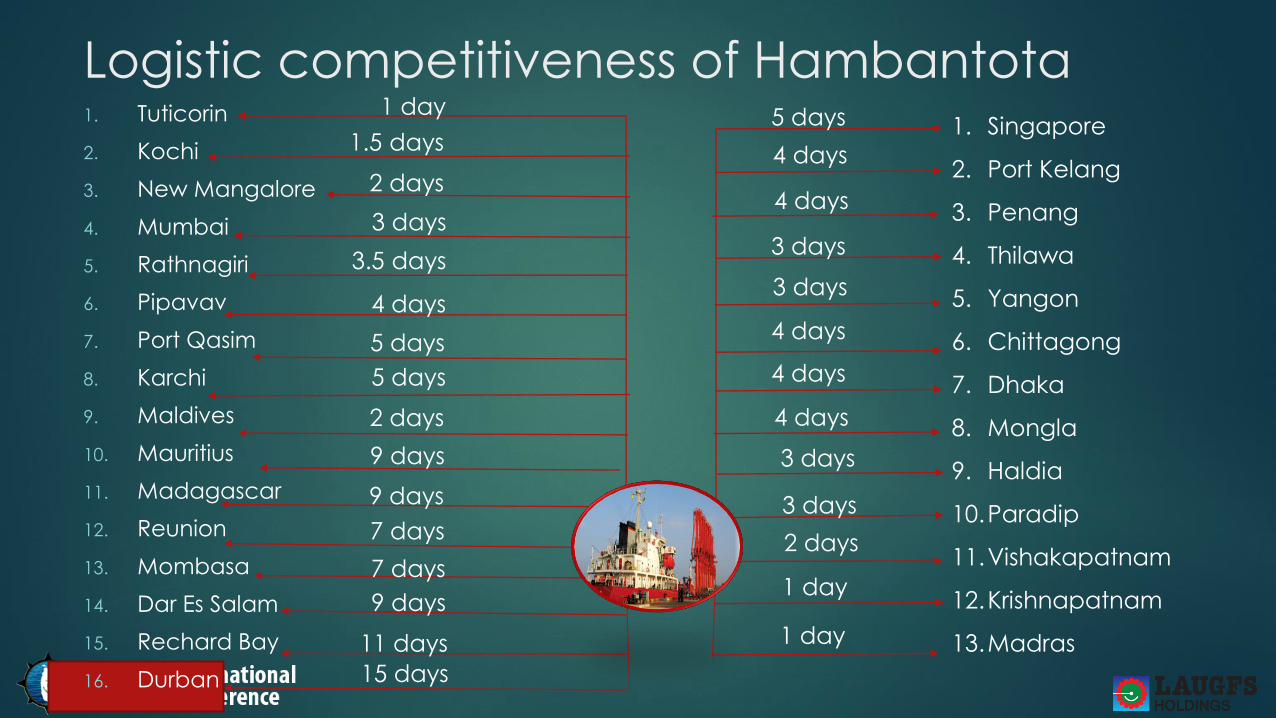

13 Ports to the East import LPG

17 Ports to the west import LPG

Maximum 5 days of sailing to the East

Maximum of 7-10 days to the West

Most logistic and cost competitive location for LPG business

Logistic Competitiveness for LPG

Logistic competitiveness of Hambantota 1. Singapore

2. Port Kelang

3. Penang

4. Thilawa

5. Yangon

6. Chittagong

7. Dhaka

8. Mongla

9. Haldia

10.Paradip

11.Vishakapatnam

12.Krishnapatnam

13.Madras

5 days

4 days

4 days

3 days

3 days

4 days

4 days

4 days

3 days

3 days

2 days

1 day

1 day

1 day

11 days

9 days

2 days

1.5 days

2 days

3 days

3.5 days

4 days

5 days

5 days

9 days

7 days

15 days

9 days

7 days

1. Tuticorin

2. Kochi

3. New Mangalore

4. Mumbai

5. Rathnagiri

6. Pipavav

7. Port Qasim

8. Karchi

9. Maldives

10. Mauritius

11. Madagascar

12. Reunion

13. Mombasa

14. Dar Es Salam

15. Rechard Bay

16. Durban

LAUGFS LPG TERMINAL HAMBANTOTA

- A Contributor Towards Economic and Social Prosperity

for Sri Lanka and the Region

PROJECT ASPIRATIONS

THANK YOU !

Recommended