The Impact of Taxation on Somaliland Economic Growth

Mohamed Hassan Mohamed

Accounting Morning A

DECLARATION

I hereby declare that this research paper and its findings are my original work and my

efforts and that it has not been submitted anywhere for any award, every effort is made

to indicate this clearly, with due reference to the literature, and acknowledgement of

collaborative research and discussions.

Name: ……………………...……………......

Signature: ……………………………………

Date: …………………………………………..

FACULTY OF MANAGEMENT SCIENCE AND INFORMATION TECHNOLOGY

Certificate

This is to certify that the project titled “The impact of taxation on Somaliland Economic

Growth” is a bona fide work done by Mohamed Hassan Mohamed Ahmed

in partial fulfillment of the requirement for the Faculty of MS-IT

faculty of Management Science and Information Technology

during the period 2013-2014

Advisor Head of Department

Kooshin Jamaal

______________________ _____________________

DEDICATION

I am passionately dedicating this work to my parents who have been the source of my

strength to continue with my further studies, encouraged me to work hard without

tiredness to complete my study in a successful manner and for the support they did for

me to achieve this level of academic endeavor and the support and guidance throughout

my life. You really played a great role to enable me reach this far. May Allah, the Almighty

grant you more happiness.

Acknowledgement

All praises and thanks are due to Allah (SWT), the creator, exalted, sustainer, and the

most merciful, who gave me the power and ability to complete this paper successfully,

I have taken efforts in this study. However, it would not have been possible without the

kind support and help of many individuals.

First of all I would like to express my appreciation, thanks and extend my advisor, Mr.,

Mohamed Koshin. Without his valuable and constructive advice this paper would not

have succeed. He encourages the development of this paper from the begging to end.

I would like to express my gratitude towards my parents for their kind cooperation and

encouragement which help me the completion of this research. .

I am particularly gratifying to special thanks to my classmates and my best friends;

Ahmed Hassan, Ismail Hussein, Abdurrahman Arale and Fatima Abdullah, Many thanks

goes to Ibrahim Hared Abdullah, for helping me to get valuable source to write this

research paper and his advice to continue my education.

Thank you All

Abstract

The purpose of this study is to clarify and analyze the impact of taxation on Somaliland

economic growth. The study will use a

descriptive research design. Descriptive research is used to obtain information concerning the

current status of the phenomena to describe what exists. The aim of the research project, and its

major purpose was to gain better understanding of the role in which tax plays the development

of economic growth.

This research study of the impact of taxation on Somaliland’s economy growth consists of five

chapters. The historical overview of taxation described in chapter 1, which also endow with a

concise overview of the research study. Chapter 2 presents the conceptual frame work and

external information of the study, chapter 3 summarize the overall research methodology like,

research design, target population, sample size, research techniques, time schedule and budget

plan or the total cost of the research study. Chapter 4 involves analyzing and interpretation of

the research question. In addition, the most frequently cited references, conclusion and

recommendation.

After analysis some businesses in our country; this paper presented in a form of tabulation,

chart and text as well, and we learned the capacity of their economic situations and their

characteristics, our findings pointed out the problems and constraints that they cannot grow up

or developed a new systems to improve their education and economic conditions in order to

improve the role of Somaliland economy growth.

Contents:

1: INTRODUCTION

1.1 Background of the study ……………………………………………………………………………………………………...

1.2 Problem statement……………………………………………………………………………………………………………...

1.3 Research Questions……………………………………………………………………………………………………………...

1.4 Aims and Objectives ……………………………………………………………………………………………………………

1.5 Organization of the paper …………………………………………………………………………………………………….

1.6 Scope Of The study ………………………………………………………………………………………………………………

1.7 Limitations of the study ……………………………………………………………………………………………………….

2 LITERATURE REVIEW

2.1 Overview ……………………………………………………………………………………………………………………….

2.2 Purposes and effects ……………………………………………………………………………………………..............

2.3 Kinds of taxes ………………………………………………………………………………………………………………...

2.3.1 Taxes on income ………………………………………………………………………………………………………

2.3.2 Social Contribution …………………………………………………………………………………………………..

2.3.3 Taxes on property ……………………………………………………………………………………………….......

2.3.4 Taxes on goods and services …………………………………………………………………………………….

2.3.5 Other Taxes ……………………………………………………………………………………………………………..

2.3.6 Descriptive labels given some taxes ………………………………………………………………………….

2.3.7 Proportional, progressive, regressive, and lump-sum ………………………………………………..

2.3.8 Direct and Indirect tax …………………………………………………………………………………………......

2.3.9 Fees and effective tax ……………………………………………………………………………………………….

2.4 History ……………………………………………………………………………………………………………………………….

2.4.1 Taxation Levels ………………………………………………………………………………………………………..

2.4.2 Forms of Taxation ……………………………………………………………………………………………………

2.5 Economic Effects ………………………………………………………………………………………………………………...

2.5.1 Tax Incidence …………………………………………………………………………………………………………..

2.5.2 Increased Economic Welfare ……………………………………………………………………………………

2.5.3 Reduced Economic Welfare ……………………………………………………………………………………...

3. METHODOLOGY

3.1 Research Design ……………………………………………………………………………………………………......

3.2 Target Population ……………………………………………………………………………………………………...

3.3 Sample size ………………………………………………………………………………………………………………..

3.4 Research Instruments ………………………………………………………………………………………………..

3.5 Data Analysis ……………………………………………………………………………………………………………

4. Data Analysis and Presentation

4.1 Analysis …………………………………………………………………………………………………………………….

5. CONCLUSION AND RECOMMENDATION

5.1 Conclusion ………………………………………………………………………………………………………………...

5.2 Recommendation ………………………………………………………………………………………………………

References ………………………………………………………………………………………………………………...

1.1 Background of the study

Somaliland tax system was original introduced by the British Protectorate management in

the early 20th century, the people of Somaliland protectorate considered taxation as an unjust

imposition by the colonizing or Protectorate power and thus it is unclean and profane.

In addition to that the business and trade activities were very limited; at that time the British

Protectorate administration faced a restriction in taxing, and its budget was required subsidies

from the British government, because the amount of revenue collected was not appropriate to

cover the expenditures of the administration.

Taxes are essential for the financing of government activities, but at the same time they

should be set and administered to be as growth enabling as possible. As would be expected, no

formal tax policy exists in the absence of a normal government apparatus such as treasury and

central bank.

However, Somaliland’s do adhere to an informal patchwork of duty and tax collection. The

duty and tax provide a large portion of the income enjoyed by Somaliland government.

The formulation and administration of tax structure is work of the ministry of finance in

collaboration with central bank which only acts as treasury for the government usually, the

ministry officials visit the businesses in quest for collecting the taxes. The taxes are self

assessment and declaratory.

No rigorous record/book keeping is required for the purpose of ascertaining the taxes,

rather entrepreneurs are required to keep only sales records.

The information sector and micro and small enterprises account for the majority of businesses

in Somaliland, making the tax base small and unreliable. Majority of these businesses are not

captured into the tax net and the tax compliance cost for those in the net is high. Many

operators keep little or no information and data on their operations making it difficult to

correctly assess tax liabilities, implying there is unfair competition among the enterprises.

Economic growth is the basis of increased prosperity. Growth comes from the accumulation of

capital (both human and physical) and from innovations which lead to technical progress.

Accumulation and innovation raise the productivity of inputs into production and increase the

potential level of output.

The rate of growth can be affected by policy through the effect that taxation has upon

economic decisions. An increase in taxation reduces the returns to investment (in both physical

and human capital) and Research and Development (R&D).

Lower returns mean less accumulation and innovation and hence a lower rate of growth. This is

the negative aspect of taxation. Taxation also has a positive aspect. Some public expenditure can

enhance productivity, such as the provision of infrastructure, public education, and health care.

Taxation provides the means to finance these expenditures and indirectly can contribute to an

increase in the growth rate.

1.2 STATEMENT OF PROBLEM

Economic growth is the basis of increased prosperity. Growth comes from the accumulation

of capital (both human and physical) and from innovations which lead to technical progress.

The main problem of this research is to find out broad information and clear picture about the

impact of taxation in the economic growth of Somaliland. This research papers indicates how

tax affects businesses and the key role which taxation plays the growth of Somaliland economic.

To examine and categorize the main issue the problems of taxation, thus; we have to see and

answer the following questions.

A. How taxation influences Somaliland economic growth?

B. How taxation plays vital task for the economic development in Somaliland?

C. Which way the government amasses the tax from businesses?

D. In which way the administration encourages anyone who is avoiding paying tax?

1.3 Research Questions

1. What kind of relationship between taxation and the economic growth of Somaliland?

2. Why government needs tax?

3. How tax cover the expenditure of the government?

1.4 Purpose of the Study The purpose of this paper is to discuss briefly economic growth of the country, causes by

taxation and how the government collects and encourages the citizens who are avoiding paying

it and the way in which government gain confidentially from businesses.

1.5 SCOPE OF THE STUDY This study is deeply impounded the role in which taxation manipulate the economic growth

of Somaliland.

The sample data of this research will be collected the capital of Somaliland- Hargeisa, and the

reason I choose to gather data from Hargeisa is that the main offices of the ministry of finance

are located at Hargeisa, and it will be focused just the way in tax affects the growth of economic

in Somaliland

1.6 AIMS AND OBJECTIVES The general goal of this research is to explore the impact of taxation in Somaliland economic

growth.

While specific goals of this research are:

� check up the range of government revenue which tax produces for the government

� to analyze and look deeply the problems that face the businesses according to tax

payment

� to clarify the relationship between the government and businesses

1.7 Organization Of The Paper

This paper has been organized in such this logic manner: First chapter examines the

background of the study, problem statement, purpose of the study, scope of the study objectives

of the study and the organization of the paper. Second chapter is the up-to-date information in

detail, which is the literature Review. The third chapter is analysis, which is the result of

questionnaire. The final chapter draws conclusion and suggests recommendations based on

findings it also answers to our problem statement, the aim of the study and its purpose.

1.8 Limitation of the Study

1. Limited time: this was a major study which even if it was a one and more – this study would

require more time. The amount of information available was substantial but the limited time

meant that we could either I) not be able to obtain all necessary information and/or II) not be

able to adequately verify information received.

2. Limited funds: funding for the study was also a limitation as the cost of an in-depth study in

one region is significantly more than was available for this study.

CHAPTER 2

2.1 Overview:

A tax (from the Latin taxo"rate") is a financial charge or other levy imposed upon a

taxpayer (an individual or legal entity) by a state or the functional equivalent of a state such

that failure to pay, or evasion of or resistance to collection, is punishable by law. Taxes are also

imposed by many administrative divisions. Taxes consist of direct or indirect taxes and may be

paid in money or as its labor equivalent.

The legal definition and the economic definition of taxes differ in that economists do not

consider many transfers to governments to be taxes. For example, some transfers to the public

sector are comparable to prices. Examples include tuition at public universities and fees for

utilities provided by local governments. Governments also obtain resources by creating money

(e.g., printing bills and minting coins), through voluntary gifts (e.g., contributions to public

universities and museums), by imposing penalties (e.g., traffic fines), by borrowing, and by

confiscating wealth. From the view of economists, a tax is a non-penal, yet compulsory transfer

of resources from the private to the public sector levied on a basis of predetermined criteria

and without reference to specific benefit received.

In modern taxation systems, taxes are levied in money; but, in-kind and corvée taxation is

characteristic of traditional or pre-capitalist states and their functional equivalents. The method

of taxation and the government expenditure of taxes raised is often highly debated in politics

and economics. Tax collection is performed by a government agency such as the Canada

Revenue Agency, the Internal Revenue Service (IRS) in the United States, or Her Majesty's

Revenue and Customs (HMRC) in the United Kingdom. When taxes are not fully paid, civil

penalties (such as fines or forfeiture) or criminal penalties (such as incarceration) may be

imposed on the non-paying entity or individual.

2.2 Purpose and Effects:

Money provided by taxation has been used by states and their functional equivalents

throughout history to carry out many functions. Some of these include expenditures on war, the

enforcement of law and public order, protection of property, economic infrastructure (roads,

legal tender, enforcement of contracts, etc.), public works, social engineering, subsidies, and the

operation of government itself. A portion of taxes also go to pay off the state's debt and the

interest this debt accumulates. Governments also use taxes to fund welfare and public services.

These services can include education systems, health care systems, and pensions for the elderly,

unemployment benefits, and public transportation. Energy, water and waste management

systems are also common public utilities. Colonial and modernizing states have also used cash

taxes to draw or force reluctant subsistence producers into cash economies.

Governments use different kinds of taxes and vary the tax rates. This is done to distribute

the tax burden among individuals or classes of the population involved in taxable activities,

such as business, or to redistribute resources between individuals or classes in the population.

Historically, the nobility were supported by taxes on the poor; modern social security systems

are intended to support the poor, the disabled, or the retired by taxes on those who are still

working. In addition, taxes are applied to fund foreign aid and military ventures, to influence

the macroeconomic performance of the economy (the government's strategy for doing this is

called its fiscal policy; see also tax exemption), or to modify patterns of consumption or

employment within an economy, by making some classes of transaction more or less attractive.

A nation's tax system is often a reflection of its communal values and/or the values of

those in power. To create a system of taxation, a nation must make choices regarding the

distribution of the tax burden—who will pay taxes and how much they will pay—and how the

taxes collected will be spent. In democratic nations where the public elects those in charge of

establishing the tax system, these choices reflect the type of community that the public wishes

to create. In countries where the public does not have a significant amount of influence over the

system of taxation, that system may be more of a reflection on the values of those in power.

All large businesses incur administrative costs in the process of delivering revenue

collected from customers to the suppliers of the goods or services being purchased. Taxation is

no different; the resource collected from the public through taxation is always greater than the

amount which can be used by the government. The difference is called the compliance cost and

includes for example the labor cost and other expenses incurred in complying with tax laws and

rules. The collection of a tax in order to spend it on a specified purpose, for example collecting a

tax on alcohol to pay directly for alcoholism rehabilitation centers, is called hypothecation. This

practice is often disliked by finance ministers, since it reduces their freedom of action. Some

economic theorists consider the concept to be intellectually dishonest since, in reality, money is

fungible. Furthermore, it often happens that taxes or excises initially levied to fund some

specific government programs are then later diverted to the government general fund. In some

cases, such taxes are collected in fundamentally inefficient ways, for example highway tolls.

Some economists, especially neo-classical economists, argue that all taxation creates

market distortion and results in economic inefficiency. They have therefore sought to identify the

kind of tax system that would minimize this distortion.

Since governments also resolve commercial disputes, especially in countries with common law,

similar arguments are sometimes used to justify a sales tax or value added tax. Others (e.g.,

libertarians) argue that most or all forms of taxes are immoral due to their involuntary (and

therefore eventually coercive/violent) nature. The most extreme anti-tax view is anarcho-

capitalism, in which the provision of all social services should be voluntarily bought by the

person(s) using them.

2.3 Kinds of Tax:

The Organization for Economic Co-operation and Development (OECD) publishes an analysis of

tax systems of member countries. As part of such analysis, OECD developed a definition and

system of classification of internal taxes, generally followed below. In addition, many countries

impose taxes (tariffs) on the import of goods.

2.3.1 Taxes on Income:

A. Income Tax:

An income tax is a government levy (tax) imposed on individuals or entities (taxpayers) that

vary with the income or profits (taxable income) of the taxpayer. Details vary widely by

jurisdiction. Many jurisdictions refer to income tax on business entities as companies’ tax or

corporation tax. Partnerships generally are not taxed; rather, the partners are taxed on their

share of partnership items. Tax may be imposed by both a country and subdivisions thereof.

Most jurisdictions exempt locally organized charitable organizations from tax. Income tax

generally is computed as the product of a tax rate multiplied by taxable income. The tax rate may

increase as taxable income increases (referred to as graduated rates). Tax rates may vary by type

or characteristics of the taxpayer. Capital gains may be taxed at different rates than other income.

Credits of various sorts may be allowed that reduce tax. Some jurisdictions impose the higher of

an income tax or a tax on an alternative base or measure of income.

Taxable income of taxpayers resident in the jurisdiction is generally total income less income

producing expenses and other deductions. Generally, only net gain from sale of property,

including goods held for sale, is included in income. Income of a corporation's shareholders

usually includes distributions of profits from the corporation. Deductions typically include all

income producing or business expenses including an allowance for recovery of costs of business

assets. Many jurisdictions allow notional deductions for individuals, and may allow deduction of

some personal expenses. Most jurisdictions either do not tax income earned outside the

jurisdiction or allow a credit for taxes paid to other jurisdictions on such income. Nonresidents

are taxed only on certain types of income from sources within the jurisdictions, with few

exceptions.

Personal income tax is often collected on a pay-as-you-earn basis, with small corrections

made soon after the end of the tax year. These corrections take one of two forms: payments to

the government, for taxpayers who have not paid enough during the tax year; and tax refunds

from the government for those who have overpaid. Income tax systems will often have

deductions available that lessen the total tax liability by reducing total taxable income. They

may allow losses from one type of income to be counted against another. For example, a loss

on the stock market may be deducted against taxes paid on wages. Other tax systems may

isolate the loss, such that business losses can only be deducted against business tax by

carrying forward the loss to later tax years.

Most jurisdictions require self-assessment of the tax and require payers of some types of

income to withhold tax from those payments. Advance payments of tax by taxpayers may be

required. Taxpayers not timely paying tax owed are generally subject to significant penalties,

which may include jail for individuals or revocation of an entity's legal existence

2.3.2 Social security contributions:

Many countries provide publicly funded retirement or health care systems. In connection

with these systems, the country typically requires employers and/or employees to make

compulsory payments. These payments are often computed by reference to wages or

earnings from self-employment. Tax rates are generally fixed, but a different rate may be

imposed on employers than on employees. Some systems provide an upper limit on earnings

subject to the tax. A few systems provide that the tax is payable only on wages above a

particular amount. Such upper or lower limits may apply for retirement but not health care

components of the tax

A. Negative Income Tax:

In economics, a negative income tax (abbreviated NIT) is a progressive income tax system

where people earning below a certain amount receive supplemental pay from the government

instead of paying taxes to the government. Such a system has been discussed by economists but

never fully implemented. It was developed by British politician Juliet Rhys-Williams in the 1940s

and later by United State economist Milton Friedman.

Negative income taxes can implement a basic income or supplement a guaranteed minimum

income system.

In a negative income tax system, people earning a certain income level would owe no

taxes; those earning more than that would pay a proportion of their income above that level; and

those below that level would receive a payment of a proportion of their shortfall, which is the

amount their income falls below that level.

B. Capital Gain Tax:

A capital gains tax (CGT) is a tax on capital gains, the profit realized on the sale of a non-

inventory asset that was purchased at a cost amount that was lower than the amount realized on

the sale. The most common capital gains are realized from the sale of stocks, bonds, precious

metals and property. Not all countries implement a capital gains tax and most have different

rates of taxation for individuals and corporations.

Capital gain is generally a gain on sale of capital assets that is those assets not held for sale in the

ordinary course of business. Capital assets include personal assets in many jurisdictions. Some

jurisdictions provide preferential rates of tax or only partial taxation for capital gains. Some

jurisdictions impose different rates or levels of capital gains taxation based on the length of time

the asset was held.

For equities, an example of a popular and liquid asset, national and state legislation often has a

large array of fiscal obligations that must be respected regarding capital gains. Taxes are

charged by the state over the transactions, dividends and capital gains on the stock market.

However, these fiscal obligations may vary from jurisdiction to jurisdiction.

2.3.3 Taxes on property:

Recurrent property taxes may be imposed on immovable property (real property) and some

classes of movable property. In addition, recurrent taxes may be imposed on net wealth of

individuals or corporations. Many jurisdictions impose estate tax, gift tax or other inheritance

taxes on property at death or gift transfer. Some jurisdictions impose taxes on financial or capital

transactions

A. Property Tax:

A property tax (or millage tax) is a levy on property that the owner is required to pay. The tax is

levied by the governing authority of the jurisdiction in which the property is located; it may be

paid to a national government, a federated state, a county or geographical region, or a

municipality. Multiple jurisdictions may tax the same property. This is in contrast to a rent and

mortgage tax, which is based on a percentage of the rent or mortgage value.

There are four broad types of property: land, improvements to land (immovable man-made

objects, such as buildings), personal property (movable man-made objects), and intangible

property. Real property (also called real estate or realty) means the combination of land and

improvements. Under a property tax system, the government requires and/or performs an

appraisal of the monetary value of each property, and tax is assessed in proportion to that

value. Forms of property tax used vary among countries and jurisdictions. Real property is

often taxed based on its classification. Classification is the grouping of properties based on

similar use. Properties in different classes are taxed at different rates. Examples of different

classes of property are residential, commercial, industrial and vacant real property. In Israel, for

example, property tax rates are double for vacant apartments versus occupied apartments.

A special assessment tax is sometimes confused with property tax. These are two distinct forms

of taxation: one (ad valorem tax) relies upon the fair market value of the property being taxed

for justification, and the other (special assessment) relies upon a special enhancement called a

"benefit" for its justification.

The property tax rate is often given as a percentage. It may also be expressed as per mile

(amount of tax per thousand currency units of property value), which is also known as a millage

rate or mill (which is also one-thousandth of a currency unit). To calculate the property tax, the

authority will multiply the assessed value of the property by the mill rate and then divide by

1,000. For example, a property with an assessed value of $50,000 located in a municipality with

a mill rate of 20 mills would have a property tax bill of $1,000 per year.

B. Land tax:

A land value tax (or site valuation tax) is a levy on the unimproved value of land only. It is an ad

valorem tax on land that disregards the value of buildings, personal property and other

improvements. A land value tax (LVT) is different from other property taxes, which are taxes on

the whole value of real estate: the combination of land, buildings, and improvements to the site.

Although the economic efficiency of a land value tax has been established knowledge since

Adam Smith, it was perhaps most famously promoted by Henry George. In his best selling work

Progress and Poverty (1879), George argued that when the site or location value of land was

improved by public works, its economic rent was the most logical source of public revenue. A

land value tax is also a progressive tax, in that it would be paid primarily by the wealthy, and

would reduce economic inequality. The philosophy that land rents extracted from nature

should be captured by society and used to replace taxes is often now known as Georgism.

Land value taxation is currently implemented throughout Denmark, Estonia, Russia, Hong Kong,

Singapore, and Taiwan. The tax has been applied in sub regions of Australia (New South Wales),

Mexico (Mexicali), and the United States (Pennsylvania).

C. Inheritance Tax:

An inheritance tax or estate tax is a levy paid by a person who inherits money or property or a

tax on the estate (money and property) of a person who has died. In international tax law, there

is a distinction between an estate tax and an inheritance tax: an estate tax is assessed on the

assets of the deceased, while an inheritance tax is assessed on the legacies received by the

beneficiaries of the estate. However, this distinction is not always respected in the language of

tax laws. For example, the "inheritance tax" in the United Kingdom is a tax on the assets of the

deceased, and is therefore, strictly speaking, an estate tax. For historical reasons, the term death

duty is still used colloquially (though not legally) in the United Kingdom and some

Commonwealth nations to refer to the estate tax.

Inheritance tax, estate tax, and death tax or duty is the names given to various taxes which arise

on the death of an individual. In United States tax law, there is a distinction between an estate

tax and an inheritance tax: the former taxes the personal representatives of the deceased, while

the latter taxes the beneficiaries of the estate. However, this distinction does not apply in other

jurisdictions; for example, if using this terminology UK inheritance tax would be an estate tax.

D. Expatriation Tax:

An expatriation tax or emigration tax is a tax on persons who cease to be tax resident in a

country. This often takes the form of a capital gains tax against unrealized gain attributable to

the period in which the taxpayer was a tax resident of the country in question. In most cases,

expatriation tax is assessed upon change of domicile or habitual residence; in the United States,

which is one of the few countries to tax its overseas citizens, the tax is applied upon

renunciation of citizenship instead.

An Expatriation Tax is a tax on individuals who renounce their citizenship or residence. The tax

is often imposed based on a deemed disposition of the entire individual's property. One

example is the United States under the American Jobs Creation Act, where any individual who

has a net worth of $2 million or an average income-tax liability of $127,000 who renounces his

or her citizenship and leaves the country is automatically assumed to have done so for tax

avoidance reasons and is subject to a higher tax rate.

E. Transfer tax:

A transfer tax is a tax on the passing of title to property from one person (or entity) to another.

In a narrow legal sense, a transfer tax is essentially a transaction fee imposed on the transfer of

title to property. This kind of tax is typically imposed where there is a legal requirement for

registration of the transfer, such as transfers of real estate, shares, or bond. Examples of such

taxes include some forms of stamp duty, real estate transfer tax, and levies for the formal

registration of a transfer. In some jurisdictions, transfers of certain forms of property require

confirmation by a notary. While notaries fees may add to the cost of the transaction, they are not

a transfer tax in the strict sense of the term.

In the United States, the term transfer tax also refers to Estate tax and Gift tax. Both these taxes

levy a charge on the transfer of property from a person (or that person's estate) to another

without consideration. In 1900, the United States Supreme Court in the case of Knowlton v.

Moore, 178 U.S. 41 (1900), confirmed that the estate tax was a tax on the transfer of property as

a result of a death and not a tax on the property itself. The taxpayer argued that the estate tax

was a direct tax and that, since it had not been apportioned among the states according to

population, it was unconstitutional. The Court ruled that the estate tax, as a transfer tax (and

not a tax on property by reason of its ownership) was an indirect tax. In the wake of Knowlton

the Internal Revenue Code of the United States continues to refer to the Estate tax and the

related Gift tax as "Transfer taxes."

In this broader sense, estate tax, gift tax, capital gains tax, sales tax on goods (not services), and

certain use taxes are all transfer taxes because they involve a tax on the transfer of title

F. Wealth (net worth) tax:

A wealth tax is generally conceived of as a levy based on the aggregate value of all household

assets, including owner-occupied housing; cash, bank deposits, money funds, and savings in

insurance and pension plans; investment in real estate and unincorporated businesses; and

corporate stock, financial securities, and personal trusts. A wealth tax is a tax on the

accumulated stock of purchasing power, in contrast to income tax, which is a tax on the flow of

assets (a change in stock)

2.3.4 Taxes on goods and services

A. Value – Added Tax (VAT)

A value added tax (VAT), also known as Goods and Services Tax (G.S.T), Single Business Tax, or

Turnover Tax in some countries, applies the equivalent of a sales tax to every operation that

creates value. To give an example, sheet steel is imported by a machine manufacturer. That

manufacturer will pay the VAT on the purchase price, remitting that amount to the government.

The manufacturer will then transform the steel into a machine, selling the machine for a higher

price to a wholesale distributor. The manufacturer will collect the VAT on the higher price, but

will remit to the government only the excess related to the "value added" (the price over the cost

of the sheet steel). The wholesale distributor will then continue the process, charging the retail

distributor the VAT on the entire price to the retailer, but remitting only the amount related to

the distribution mark-up to the government. The last VAT amount is paid by the eventual retail

customer who cannot recover any of the previously paid VAT. For a VAT and sales tax of identical

rates, the total tax paid is the same, but it is paid at differing points in the process.

VAT is usually administrated by requiring the company to complete a VAT return, giving details

of VAT it has been charged (referred to as input tax) and VAT it has charged to others (referred

to as output tax). The difference between output tax and input tax is payable to the Local Tax

authority. If input tax is greater than output tax the company can claim back money from the

Local Tax Authority.

A value-added tax (VAT) is a form of consumption tax. From the perspective of the buyer, it is a

tax on the purchase price. From that of the seller, it is a tax only on the value added to a product,

material, or service, from an accounting point of view, by this stage of its manufacture or

distribution. The manufacturer remits to the government the difference between these two

amounts, and retains the rest for themselves to offset the taxes they had previously paid on the

inputs.

The purpose of VAT is to generate tax revenues to the government similar to the corporate

income tax or the personal income tax.

The value added to a product by or with a business is the sale price charged to its customer,

minus the cost of materials and other taxable inputs. A VAT is like a sales tax in that ultimately

only the end consumer is taxed. It differs from the sales tax in that, with the latter, the tax is

collected and remitted to the government only once, at the point of purchase by the end

consumer. With the VAT, collections, remittances to the government, and credits for taxes

already paid occur each time a business in the supply chain purchases products

B. Sales Tax:

A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually

laws allow (or require) the seller to collect funds for the tax from the consumer at the point of

purchase.

Sales taxes are levied when a commodity is sold to its final consumer. Retail organizations

contend that such taxes discourage retail sales. The question of whether they are generally

progressive or regressive is a subject of much current debate. People with higher incomes spend

a lower proportion of them, so a flat-rate sales tax will tend to be regressive. It is therefore

common to exempt food, utilities and other necessities from sales taxes, since poor people spend

a higher proportion of their incomes on these commodities, so such exemptions make the tax

more progressive. This is the classic "You pay for what you spend" tax, as only those who spend

money on non-exempt (i.e. luxury) items pay the tax.

A small number of U.S. states rely entirely on sales taxes for state revenue, as those states do

not levy a state income tax. Such states tend to have a moderate to large amount of tourism or

inter-state travel that occurs within their borders, allowing the state to benefit from taxes from

people the state would otherwise not tax. In this way, the state is able to reduce the tax burden

on its citizens. The U.S. states that do not levy a state income tax are Alaska, Tennessee, Florida,

Nevada, South Dakota, Texas, Washington state, and Wyoming. Additionally, New Hampshire

and Tennessee levy state income taxes only on dividends and interest income. Of the above

states, only Alaska and New Hampshire do not levy a state sales tax. Additional information can

be obtained at the Federation of Tax Administrators website.

In the United States, there is a growing movement for the replacement of all federal payroll and

income taxes (both corporate and personal) with a national retail sales tax and monthly tax

rebate to households of citizens and legal resident aliens. The tax proposal is named Fair Tax. In

Canada, the federal sales tax is called the Goods and Services tax (GST) and now stands at 5%.

The provinces of British Columbia, Saskatchewan, Manitoba, and Prince Edward Island also

have a provincial sales tax [PST]. The provinces of Nova Scotia, New Brunswick, Newfoundland

& Labrador, and Ontario have harmonized their provincial sales taxes with the GST—

Harmonized Sales Tax [HST], and thus is a full VAT. The province of Quebec collects the Quebec

Sales Tax [QST] which is based on the GST with certain differences. Most businesses can claim

back the GST, HST and QST they pay, and so effectively it is the final consumer who pays the tax

C. Excise Tax:

An excise or excise tax (sometimes called a duty of excise special tax) is an inland tax on the sale,

or production for sale, of specific goods or a tax on a good produced for sale, or sold, within a

country or licenses for specific activities. Excises are distinguished from customs duties, which

are taxes on importation. Excises are inland taxes, whereas customs duties are border taxes.

An excise is considered an indirect tax, meaning that the producer or seller who pays the tax to

the government is expected to try to recover or shift the tax by raising the price paid by the

buyer. Excises are typically imposed in addition to another indirect tax such as a sales tax or

value added tax (VAT). In common terminology (but not necessarily in law)

Unlike an ad valorem, an excise is not a function of the value of the product being taxed. Excise

taxes are based on the quantity, not the value, of product purchased. For example, in the United

States, the Federal government imposes an excise tax of 18.4 cents per U.S. gallon (4.86¢/L) of

gasoline, while state governments levy an additional 8 to 28 cents per U.S. gallon. Excises on

particular commodities are frequently hypothecated. For example, a fuel excise (use tax) is

often used to pay for public transportation, especially roads and bridges and for the protection

of the environment. A special form of hypothecation arises where an excise is used to

compensate a party to a transaction for alleged uncontrollable abuse; for example, a blank

media tax is a tax on recordable media such as CD-Rs, whose proceeds are typically allocated to

copyright holders. Critics charge that such taxes blindly tax those who make legitimate and

illegitimate usages of the products; for instance, a person or corporation using CD-R's for data

archival should not have to subsidize the producers of popular music.

D. Tariff Tax:

A tariff is a tax on imports or exports (an international trade tariff). An import or export tariff

(also called customs duty or impost) is a charge for the movement of goods through a political

border. Tariffs discourage trade, and they may be used by governments to protect domestic

industries. A proportion of tariff revenues is often hypothecated to pay government to maintain a

navy or border police. The classic ways of cheating a tariff are smuggling or declaring a false

value of goods. Tax, tariff and trade rules in modern times are usually set together because of

their common impact on industrial policy, investment policy, and agricultural policy. A trade bloc

is a group of allied countries agreeing to minimize or eliminate tariffs against trade with each

other, and possibly to impose protective tariffs on imports from outside the bloc. A customs

union has a common external tariff, and the participating countries share the revenues from

tariffs on goods entering the customs union.

2.3.5 Other Taxes:

A. License Fees:

Occupational taxes or license fees may be imposed on businesses or individuals engaged in

certain businesses. Many jurisdictions impose a tax on vehicles

B. Poll Tax:

A poll tax, also called a per capita tax, or capitation tax, is a tax that levies a set amount per

individual. It is an example of the concept of fixed tax. Poll taxes are administratively cheap

because they are easy to compute and collect and difficult to cheat. Economists have considered

poll taxes economically efficient because people are presumed to be in fixed supply. However,

poll taxes are very unpopular because poorer people pay a higher proportion of their income

than richer people. In addition, the supply of people is in fact not fixed over time: on average,

couples will choose to have fewer children if a poll tax is imposed.

A poll tax (head tax or capitation tax, in U.S. English) is a tax of a portioned, fixed amount

applied to an individual in accordance with the census (as opposed to a percentage of income).

Head taxes were important sources of revenue for many governments from ancient times until

the 19th century. There have been several famous (and infamous) cases of head taxes in

history, notably in parts of the United States with the intent of disenfranchising poor people,

including African Americans, Native Americans, and white people of foreign descent. The tax

was marginal and never collected in practice, but payment of the tax would be a prerequisite for

minority voting. In the United Kingdom, poll taxes were levied by the governments of John of

Gaunt in the 14th century, Charles II in the 17th and Margaret Thatcher in the 20th century.

The word poll is an English word that once meant "head" - and still does, in some specialized

contexts - hence the name poll tax for a per-person tax. In the United States, however, the term

has come to be used almost exclusively for a fixed tax applied to voting. Since "going to the

polls" is today a common idiom for voting in many countries (deriving from the fact that early

voting involved head-counts), a new folk etymology has supplanted common knowledge of the

phrase's true origins.

2.3.6 Descriptive labels given some taxes

A. Ad Valorem Tax:

An ad valorem tax (Latin for "according to value") is a tax based on the value of real estate or

personal property. It is typically imposed at the time of a transaction, as in the case of a sales tax

or value-added tax (VAT). However, an ad valorem tax may also be imposed on an annual basis,

as in the case of a real or personal property tax, or in connection with another significant event.

An ad valorem tax is one where the tax base is the value of a good, service, or property. Sales

taxes, tariffs, property taxes, inheritance taxes, and value added taxes are different types of ad

valorem tax. An ad valorem tax is typically imposed at the time of a transaction (sales tax or

value added tax (VAT)) but it may be imposed on an annual basis (property tax) or in connection

with another significant event (inheritance tax or tariffs). An alternative to ad valorem taxation is

an excise tax, where the tax base is the quantity of something, regardless of its price.

B. Consumption Tax:

Consumption tax refers to any tax on non-investment spending, and can be implemented by

means of a sales tax, consumer value added tax, or by modifying an income tax to allow for

unlimited deductions for investment or savings.

A consumption tax is a tax on spending on goods and services. The tax base of such a tax is the

money spent on consumption. Consumption taxes are usually indirect, such as a sales tax or a

value added tax. However, a consumption tax can also be structured as a form of direct, personal

taxation, such as the Hall–Rabushka flat tax.

C. Environmental Tax:

This includes natural resources consumption tax, greenhouse gas tax (Carbon tax), "sulfuric tax",

and others. The stated purpose is to reduce the environmental impact by reprising.

2.3.7 Proportional, progressive, regressive, and lump-sum

An important feature of tax systems is the percentage of the tax burden as it relates to income or

consumption. The terms progressive, regressive, and proportional are used to describe the way

the rate progresses from low to high, from high to low, or proportionally. The terms describe a

distribution effect, which can be applied to any type of tax system (income or consumption) that

meets the definition.

A. A Progressive Tax:

progressive tax is a tax imposed so that the effective tax rate increases as the amount to

which the rate is applied increases

B. A Regressive Tax:

is the opposite of a progressive tax where the effective tax rate decreases as the amount to

which the rate is applied increases. This effect is commonly produced where means testing is

used to withdraw tax allowances or state benefits.

C. A Proportional Tax:

in between progressive and regressive tax is a proportional tax, where the effective tax rate is

fixed, while the amount to which the rate is applied increases.

D. A Lump-Sum:

A lump-sum tax is a tax that is a fixed amount, no matter the change in circumstance of the taxed

entity. This in actuality is a regressive tax as those with lower income must use higher

percentage of their income than those with higher income and therefore the effect of the tax

reduces as a function of income

The terms can also be used to apply meaning to the taxation of select consumption, such as a tax

on luxury goods and the exemption of basic necessities may be described as having progressive

effects as it increases a tax burden on high end consumption and decreases a tax burden on low

end consumption

2.3.8 Direct and Indirect Tax:

Taxes are sometimes referred to as "direct taxes" or "indirect taxes". The meaning of these

terms can vary in different contexts, which can sometimes lead to confusion. An economic

definition, by Atkinson, states that "...direct taxes may be adjusted to the individual

characteristics of the taxpayer, whereas indirect taxes are levied on transactions irrespective of

the circumstances of buyer or seller.

A. Direct Tax:

A direct tax is generally a tax paid directly to the government by the person on whom it is

imposed.

In a general sense, a direct tax is one imposed upon an individual person (juristic or natural) or

property (i.e. real and personal property, rental profits, livestock, crops, wages, etc.) as distinct

from a tax imposed upon a transaction. In this sense, indirect taxes such as a sales tax or a value

added tax (VAT) are imposed only if and when a taxable transaction occurs. People have the

freedom to engage in or refrain from such transactions; whereas a direct tax (in the general

sense) is imposed upon a person, typically in an unconditional manner, such as a poll-tax or

head-tax, which is imposed on the basis of the person's very life or existence, or a property tax

which is imposed upon the owner by virtue of ownership, rather than commercial use. Some

commentators have argued that "a direct tax is one that cannot be shifted by the taxpayer to

someone else, whereas an indirect tax can be.

The unconditional, inexorable aspect of the direct tax was a paramount concern of people in the

18th century seeking to escape tyrannical forms of government and to safeguard individual

liberty

B. Indirect Tax:

An indirect tax (such as sales tax, a specific tax, value added tax (VAT), or goods and services tax

(GST)) is a tax collected by an intermediary (such as a retail store) from the person who bears

the ultimate economic burden of the tax (such as the consumer). The intermediary later files a

tax return and forwards the tax proceeds to government with the return. In this sense, the term

indirect tax is contrasted with a direct tax which is collected directly by government from the

persons (legal or natural) on which it is imposed. Some commentators have argued that "a

direct tax is one that cannot be shifted by the taxpayer to someone else, whereas an indirect tax

can be.

An indirect tax may increase the price of a good so that consumers are actually paying the tax

by paying more for the products. Examples would be fuel, liquor, and cigarette taxes. An excise

duty on motor cars is paid in the first instance by the manufacturer of the cars; ultimately the

manufacturer transfers the burden of this duty to the buyer of the car in form of a higher price.

Thus, an indirect tax is such which can be shifted or passed on. The degree to which the burden

of a tax is shifted determines whether a tax is primarily direct or primarily indirect. This is a

function of the relative elasticity of the supply and demand of the goods or services being taxed.

Under this definition, even income taxes may be indirect

2.3.9 Fees and effective tax:

Governments may charge user fees, tolls, or other types of assessments in exchange of particular

goods, services, or use of property. These are generally not considered taxes, as long as they are

levied as payment for a direct benefit to the individual paying. Such fees include:

� Tolls: a fee charged to travel via a road, bridge, tunnel, canal, waterway or other transportation

facilities. Historically tolls have been used to pay for public bridge, road and tunnel projects. They have

also been used in privately constructed transport links. The toll is likely to be a fixed charge, possibly

graduated for vehicle type, or for distance on long routes.

� User fees, such as those charged for use of parks or other government owned facilities.

� Ruling fees charged by governmental agencies to make determinations in particular situations.

Some scholars refer to certain economic effects as taxes, though they are not levies imposed by

governments. These include:

� Inflation tax: the economic disadvantage suffered by holders of cash and cash equivalents in one

denomination of currency due to the effects of expansionary monetary policy

� Financial repression: Government policies such as interest rate caps on government debt,

financial regulations such as reserve requirements and capital controls, and barriers to entry in markets

where the government owns or controls businesses

2.4 History

The first known system of taxation was in Ancient Egypt around 3000–2800 BC in the first

dynasty of the Old Kingdom. The earliest and most widespread form of taxation was the corvée

and tithe. The corvée was forced labor provided to the state by peasants too poor to pay other

forms of taxation (labor in ancient Egyptian is a synonym for taxes). Records from the time

document that the pharaoh would conduct a biennial tour of the kingdom, collecting tithes from

the people. Other records are granary receipts on limestone flakes and papyrus.

In the Persian Empire, a regulated and sustainable tax system was introduced by Darius I the

Great in 500 BC; the Persian system of taxation was tailored to each Satrapy (the area ruled by a

Satrap or provincial governor). At differing times, there were between 20 and 30 Satrapies in

the Empire and each was assessed according to its supposed productivity. It was the

responsibility of the Satrap to collect the due amount and to send it to the emperor, after

deducting his expenses (the expenses and the power of deciding precisely how and from whom

to raise the money in the province, offer maximum opportunity for rich pickings). The

quantities demanded from the various provinces gave a vivid picture of their economic

potential. For instance, Babylon was assessed for the highest amount and for a startling mixture

of commodities; 1,000 silver talents and four months supply of food for the army. India, a

province fabled for its gold, was to supply gold dust equal in value to the very large amount of

4,680 silver talents. Egypt was known for the wealth of its crops; it was to be the granary of the

Persian Empire (and, later, of the Roman Empire) and was required to provide 120,000

measures of grain in addition to 700 talents of silver. This tax was exclusively levied on

Satrapies based on their lands, productive capacity and tribute levels.

The Rosetta Stone, a tax concession issued by Ptolemy V in 196 BC and written in three

languages "led to the most famous decipherment in history—the cracking of hieroglyphics"

In India, Islamic rulers imposed jizya (a poll tax on non-Muslims) starting in the 11th century

2.4.1 Taxation levels

Numerous records of government tax collection in Europe since at least the 17th century are still

available today. But taxation levels are hard to compare to the size and flow of the economy since

production numbers are not as readily available. Government expenditures and revenue in

France during the 17th century went from about 24.30 million livres in 1600–10 to about 126.86

million livres in 1650–59 to about 117.99 million livres in 1700–10 when government debt had

reached 1.6 billion livres. In 1780–89, it reached 421.50 million livres. Taxation as a percentage of

production of final goods may have reached 15%–20% during the 17th century in places such as

France, the Netherlands, and Scandinavia. During the war-filled years of the eighteenth and early

nineteenth century, tax rates in Europe increased dramatically as war became more expensive

and governments became more centralized and adept at gathering taxes. This increase was

greatest in England, Peter Mathias and Patrick O'Brien found that the tax burden increased by

85% over this period. Another study confirmed this number, finding that per capita tax revenues

had grown almost six fold over the eighteenth century, but that steady economic growth had

made the real burden on each individual only double over this period before the industrial

revolution. Average tax rates were higher in Britain than France the years before the French

Revolution, twice in per capita income comparison, but they were mostly placed on international

trade. In France, taxes were lower but the burden was mainly on landowners, individuals, and

internal trade and thus created far more resentment.

Taxation as a percentage of GDP in 2003 was 56.1% in Denmark, 54.5% in France, 49.0% in the

Euro area, 42.6% in the United Kingdom, 35.7% in the United States, 35.2% in Ireland, and

among all OECD members an average of 40.7%

2.4.2 Forms of Taxation

In monetary economies prior to fiat banking, a critical form of taxation were seigniorage, the tax

on the creation of money.

Other obsolete forms of taxation include:

• Scutage, which is paid in lieu of military service; strictly speaking, it is a commutation of a

non-tax obligation rather than a tax as such but functioning as a tax in practice.

• Tallage, a tax on feudal dependents.

• Tithe, a tax-like payment (one tenth of one's earnings or agricultural produce), paid to the

Church (and thus too specific to be a tax in strict technical terms). This should not be confused

with the modern practice of the same name which is normally voluntary.

• (Feudal) aids, a type of tax or due that was paid by a vassal to his lord during feudal times.

• Dane- geld, a medieval land tax originally raised to pay off raiding Danes and later used to

fund military expenditures.

• Carucage, a tax which replaced the dangled in England.

• Tax farming, the principle of assigning the responsibility for tax revenue collection to

private citizens or groups.

• So -cage, a feudal tax system based on land rent.

• Burg- age, a feudal tax system based on land rent.

Some principalities taxed windows, doors, or cabinets to reduce consumption of imported glass

and hardware. Armoires, hutches, and wardrobes were employed to evade taxes on doors and

cabinets. In some circumstances, taxes are also used to enforce public policy like congestion

charge (to cut road traffic and encourage public transport) in London. In Tsarist Russia, taxes

were clamped on beards. Today, one of the most-complicated taxation systems worldwide is in

Germany. Three quarters of the world's taxation literature refers to the German system.[citation

needed] Under the German system, there are 118 laws, 185 forms, and 96,000 regulations,

spending €3.7 billion to collect the income tax.[citation needed] In the United States, the IRS has

about 1,177 forms and instructions,28.4111 megabytes of Internal Revenue Code[35] which

contained 3.8 million words as of 1 February 2010, numerous tax regulations in the Code of

Federal Regulations, and supmentary material in the Internal Revenue Bulletin .Today,

governments in more advanced economies (i.e. Europe and North America) tend to rely more

on direct taxes, while developing economies (i.e. India and several African countries) rely more

on indirect taxes.

2.4.3 Economic Effects:

In economic terms, taxation transfers wealth from households or businesses to the government

of a nation. The side-effects of taxation and theories about how best to tax are an important

subject in microeconomics. Taxation is almost never a simple transfer of wealth. Economic

theories of taxation approach the question of how to maximize economic welfare through

taxation

2.4.4 Tax Incidence:

n economics, tax incidence is the analysis of the effect of a particular tax on the distribution of

economic welfare. Tax incidence is said to "fall" upon the group that ultimately bears the burden

of, or ultimately has to pay, the tax. The key concept is that the tax incidence or tax burden does

not depend on where the revenue is collected, but on the price elasticity of demand and price

elasticity of supply. The concept was brought to attention by the French Physiocrats and in

particular François Quesnay who argued that the incidence of all taxation falls ultimately on

landowners and is at the expense of land rent. For this reason they advocated the replacement of

the multiplicity of contemporary taxes by the Single Tax, or Impôt Unique. A leading advocate of

this tax was Turgot. In the first instance, however, the incidence of the tax falls elsewhere. For

example, a tax on apple farmers might actually be paid by owners of agricultural land but the

incidence may initially fall on consumers of apples.

Initially, the incidence of all labor related taxes such as income tax and mandatory pension

contributions falls on employers. This must be so at the margin since the employee must receive

more net of tax i.e. take-home than they can receive from the alternative, such as welfare benefit

payments. The tax surcharge may be as high as 80%.

The theory of tax incidence has a number of practical results. For example, United States Social

Security payroll taxes are paid half by the employee and half by the employer. However, some

economists think that the worker is bearing almost the entire burden of the tax because the

employer passes the tax on in the form of lower wages. The tax incidence is thus said to fall on

the employee

2.4.5 Increased Economic Welfare

Most taxes have side effects that reduce economic welfare, either by mandating unproductive

labor (compliance costs) or by creating distortions to economic incentives (deadweight loss

and perverse incentives).

Chapter 3: Methodology

3.1 Introduction

This chapter presents the research methodology of the study. It defines and justifies the

methods and process that was be used in order to collect data that are used in answering the

research questions.

This Chapter contains the following sections which are; research design, target population,

sample size and sampling technique, research instrument that is used in data collection,

research procedure, and data analysis.

3.2 Research design

This study will descriptive through survey research design. Survey research is An oriented

methodology used to investigate populations by selecting samples to analyze and discover

situations.

For conducting my research I will be using a questionnaire. This type of research

administered in interview style. I feel the respondent can respond more honesty and reliability

if they are assured of anonymous. I have tried to include some items in the questionnaire that

should provide some internal measures for the reliability. Since I will administer the

questionnaire only one timeMy survey questionnaire will consist of close-ended questions for

one thing fixed choice items make sense because I feel I can reasonably predict what people are

going to say. I also chose close ended questions because the data will be easier to enter into the

computer close ended questions will allow for greater uniformity of response.

The order of the items in this instrument will be the first part is company details. Second parts

will the variables that I am going to diagnose. I feel the instrument will measure this fairly

accurately because I asked about in several different ways this will allow for a test of the

reliability of the instrument.

3.3 Target population

My target population will be businesses existing in Hargiesa, Somaliland. And chosen by some

of them which will give me clear information how they influence the economic growth of the

country.

3.4 Sample size

In this area I will symbolize the number of respondents that will be selected from the

population to comprise or contain a sample, since stratified random sampling will be applied, the

sample size will be consists of 15 respondents who will be issued with the questionnaire.

3.5 Research Instruments

This study will focus on using questionnaires instead of other research instruments, and the

reason we choose this research instrument is that; questionnaire is very important tool when it

comes for collecting data and it allows the researcher to get close or almost found the fact. A

questionnaire is used since the study concerned with variables that cannot be direct observed.

The target population also almost well mentioned and is not likely to have very difficulties to

replying or answering the questionnaire items.

The questionnaire contains two types which are structured and unstructured questionnaires.

Structured questionnaires list close-end questions, which offer the respondents the ability to

answer whether “Yes” or “No”, while unstructured questionnaires are open questions, which

permits the respondents could answer in their own words.

As we already mentioned, this study will be used both the types of questionnaires; structured

and unstructured questionnaires.

3.6 Data Analysis

The data collected through the use of the questionnaires will be coded and analyzed with the

help of computer. The statistical packed for social science will be used specifically for the

purpose of analyzing the data obtained; this was helped to generate graphs and figures that will

be used to portray the results graphically.

Chapter 4: Data Analysis and Presentation

This chapter consists about the sample of business that indicates the population, through which

this sample is maintained or measured under

Table number 1: Responders by Gender

Description

Female

Male

Table number 1:- shows that 20% of the responders are female, in the other hand 80% of the

responders are male

Figure Number 1:

20%

Responders by Gender

Chapter 4: Data Analysis and Presentation

This chapter consists about the sample of business that indicates the population, through which

this sample is maintained or measured under several question in the system of questionnaire:

Table number 1: Responders by Gender:

Responders Percentage

4 20%

16 80%

shows that 20% of the responders are female, in the other hand 80% of the

80%

20%

Responders by Gender

This chapter consists about the sample of business that indicates the population, through which

several question in the system of questionnaire:-

Percentage

20%

80%

shows that 20% of the responders are female, in the other hand 80% of the

Male

Female

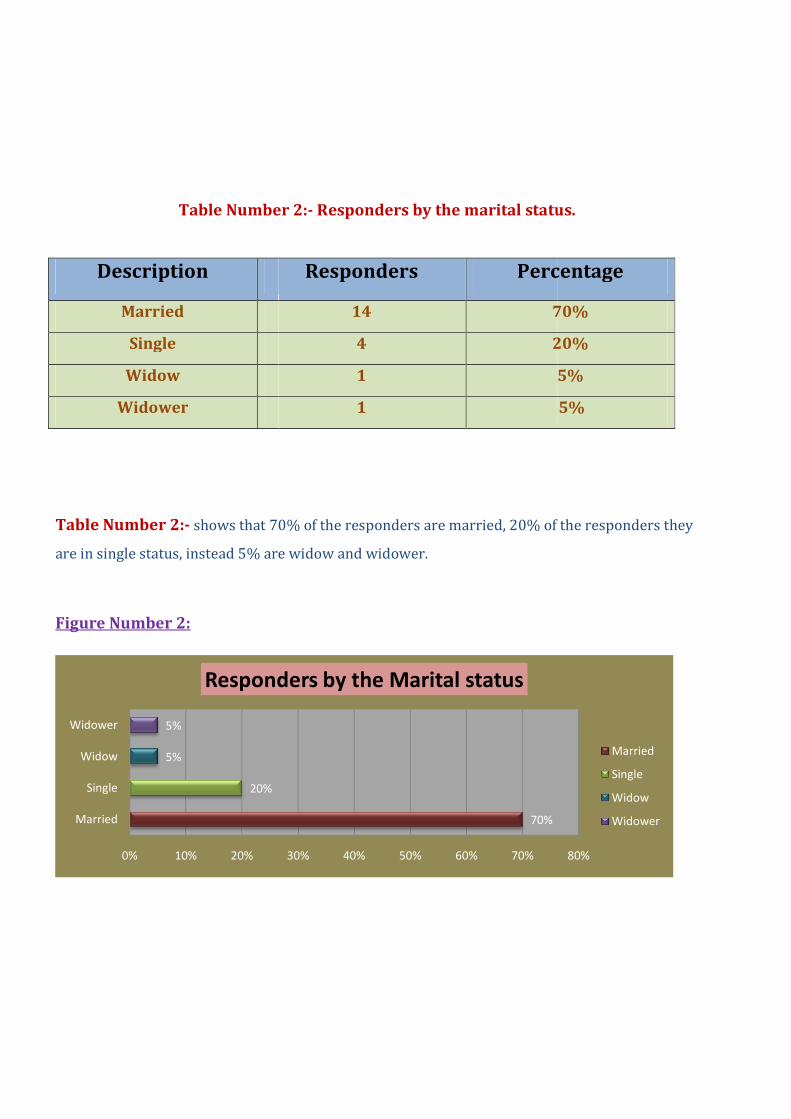

Table Number 2:

Description

Married

Single

Widow

Widower

Table Number 2:- shows that 70% of the responders are married, 20% of the

are in single status, instead 5% are widow and widower.

Figure Number 2:

20%

5%

5%

0% 10% 20%

Married

Single

Widow

Widower

Responders by the Marital status

Table Number 2:- Responders by the marital status.

Responders Percentage

14 70%

4 20%

1

1

shows that 70% of the responders are married, 20% of the

are in single status, instead 5% are widow and widower.

70%

30% 40% 50% 60% 70%

Responders by the Marital status

Responders by the marital status.

Percentage

70%

20%

5%

5%

shows that 70% of the responders are married, 20% of the responders they

80%

Married

Single

Widow

Widower

Table Number

Description

University level

Secondary level

Intermediate level

Primary level

Other

Table number 3:- shows that 35% of the responders are in university level, 30% of the

responders are in secondary level, 15% of the responders are in intermediate level, And 10% of

the responders are both in primary &

Figure Number 3:

0%

5%

10%

15%

20%

25%

30%

35%

40%

university level secaodary level

Responders by the Educational level

3:- Responders by the Educational level.

Responders Percentage

7 35%

6 30%

3 15%

2 10%

2 10%

shows that 35% of the responders are in university level, 30% of the

responders are in secondary level, 15% of the responders are in intermediate level, And 10% of

the responders are both in primary & Other level.

secaodary level internediate

level

primary level Other

Responders by the Educational level

Responders by the Educational level.

Percentage

35%

30%

15%

10%

10%

shows that 35% of the responders are in university level, 30% of the

responders are in secondary level, 15% of the responders are in intermediate level, And 10% of

university level

secaodary level

internediate level

primary level

Other

Table Number 4:

Description

Below 5

Between 5 – 10

Above 10

Table Number 4:- shows that 65% of the responders are below experience 5, although 20% of

the responders are between experiences 5

Figure Number 4

0% 10% 20%

Below 5

Between 5 - 10

Above 10

Responders by Experience

Table Number 4:- Responders by the Experience.

Responders Percentage

13

4

3

shows that 65% of the responders are below experience 5, although 20% of

the responders are between experiences 5 – 10. And 15% of the responders are above then a 10.

20% 30% 40% 50% 60% 70%

Responders by Experience

Responders by the Experience.

Percentage

65%

20%

15%

shows that 65% of the responders are below experience 5, although 20% of

10. And 15% of the responders are above then a 10.

Below 5

Between 5 - 10

Above 10

Table Number 5:

Description

Merchandising

Manufacturing

Service

Table Number 5:- shows that 45% of the responders are in sole Merchandising form, although

45% of the responders provide Service, And 10% for manufacturing level.

Figure Number 5:

45%

10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Merchandising Manufacturing

Responders by Business type

Table Number 5:- Responders by the services they provide.

Responders Percentage

9

2

9

shows that 45% of the responders are in sole Merchandising form, although

45% of the responders provide Service, And 10% for manufacturing level.

10%

45%

Manufacturing Service

Responders by Business type

Responders by the services they provide.

Percentage

45%

10%

45%

shows that 45% of the responders are in sole Merchandising form, although

Merchandising

Manufacturing

Service

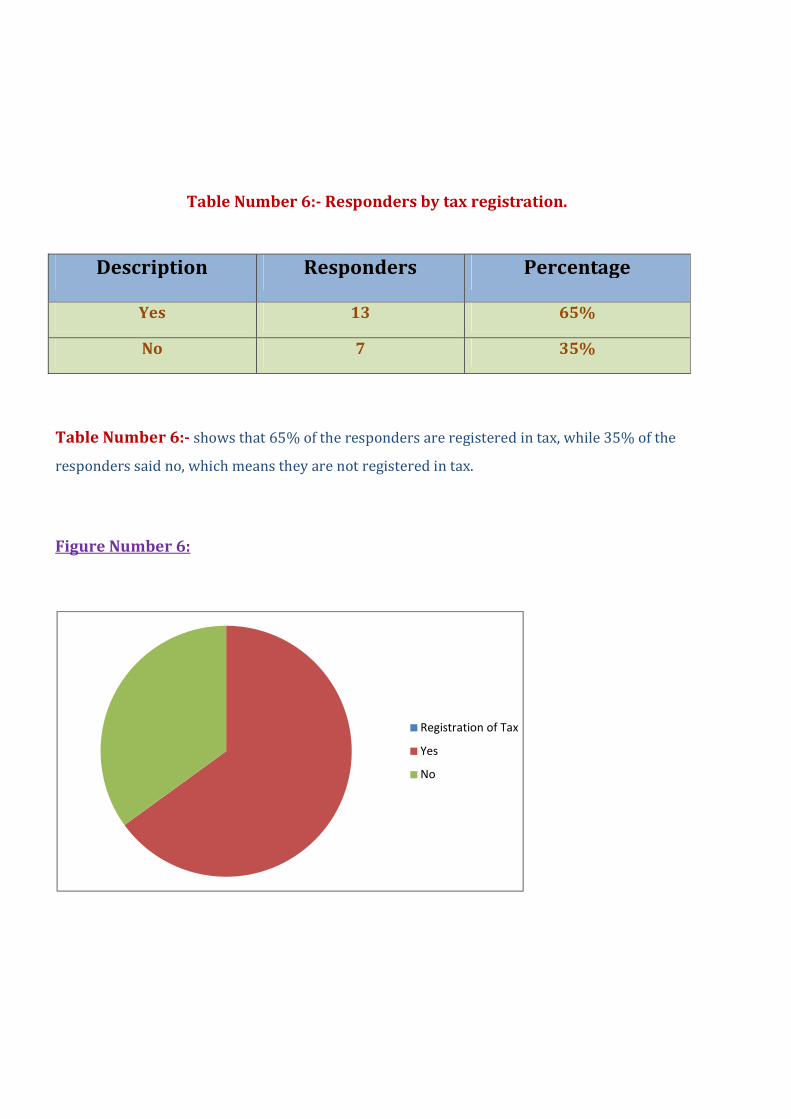

Table Number 6:- Responders by tax registration.

Description Responders Percentage

Yes 13 65%

No 7 35%

Table Number 6:- shows that 65% of the responders are registered in tax, while 35% of the

responders said no, which means they are not registered in tax.

Figure Number 6:

Registration of Tax

Yes

No

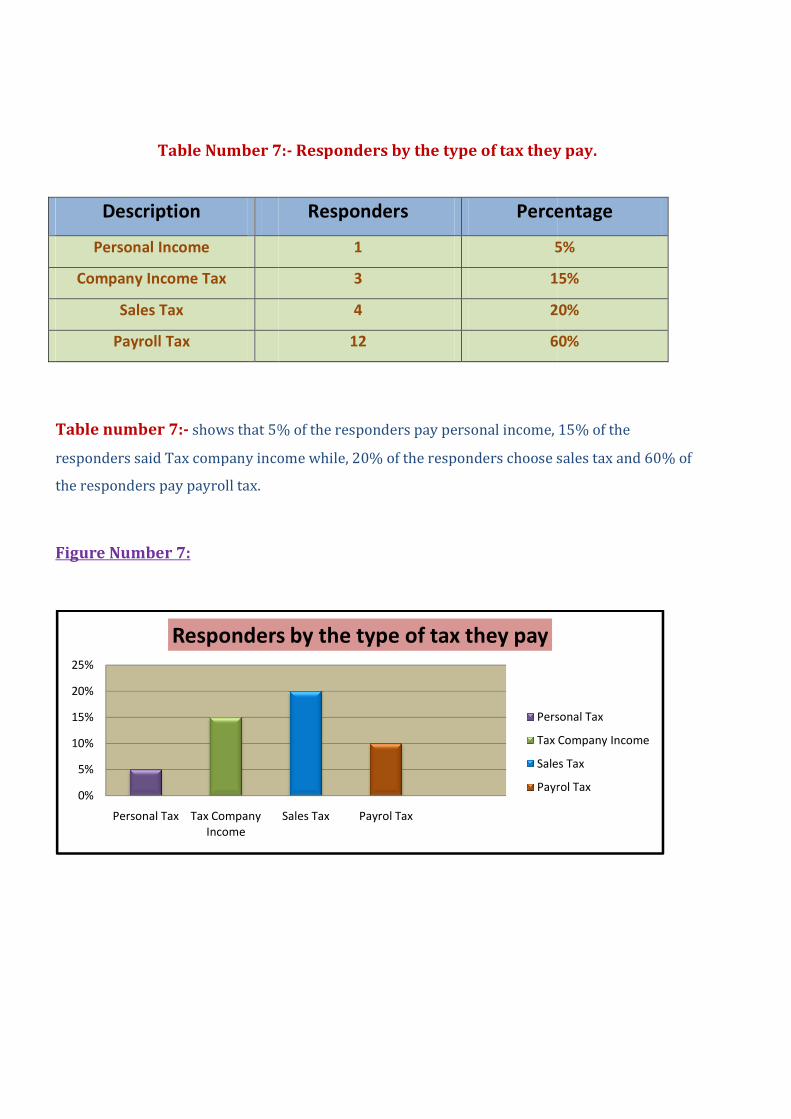

Table Number 7:

Description

Personal Income

Company Income Tax

Sales Tax

Payroll Tax

Table number 7:- shows that 5% of the r

responders said Tax company income while, 20

the responders pay payroll tax.

Figure Number 7:

0%

5%

10%

15%

20%

25%

Personal Tax Tax Company

Income

Responders by the type of tax they pay

Table Number 7:- Responders by the type of tax they pay.

Responders Percentage

1 5

3 15

4 20

12 60

% of the responders pay personal income, 1

aid Tax company income while, 20% of the responders choose sales tax and 6

Sales Tax Payrol Tax

Responders by the type of tax they pay

Personal Tax

Tax Company Income

Sales Tax

Payrol Tax

Responders by the type of tax they pay.

Percentage

5%

15%

20%

60%

esponders pay personal income, 15% of the

esponders choose sales tax and 60% of

Personal Tax

Tax Company Income

Sales Tax

Payrol Tax

Table Number 8:

Description

Yes

NO

Table Number 8:- shows that 90% of the responders are definitely aware of the importance of

tax, while 10% of my responders said no.

Figure Number 8:

10%

0% 20%

Yes

NO

Responders by the importance of tax

Table Number 8:- awareness the important of paying tax.

Responders Percentage

18 9

2 1

shows that 90% of the responders are definitely aware of the importance of

tax, while 10% of my responders said no.

90%

40% 60% 80%

Responders by the importance of tax

of paying tax.

Percentage

90%

10%

shows that 90% of the responders are definitely aware of the importance of

90%

100%

Yes

NO

Table Number 9:- Responders by the knowledgeable with tax matter

Description

Knowledgeable

Some Knowledgeable

Not Knowledgeable

Table Number 9:- shows that 70% of the responders are knowledgeable when it says tax

matter, 25% of the responders are Somehow Knowledgeable, while 5% are not knowledgeable

with tax matter.

Figure Number 9:

70%

20%

0%

20%

40%

60%

80%

Knowledgeable Some Knowledgeable

Responders by the knowledgeable with tax matter

Responders by the knowledgeable with tax matter

Responders Percentage

14 70%

5 25

1

shows that 70% of the responders are knowledgeable when it says tax

matter, 25% of the responders are Somehow Knowledgeable, while 5% are not knowledgeable

20%

5%

Some KnowledgeableNot Knowledgeable

Responders by the knowledgeable with tax matter

Knowledgeable

Some Knowledgeable

Not Knowledgeable

Responders by the knowledgeable with tax matter.

Percentage

70%

25%

5%

shows that 70% of the responders are knowledgeable when it says tax

matter, 25% of the responders are Somehow Knowledgeable, while 5% are not knowledgeable

Responders by the knowledgeable with tax matter

Knowledgeable

Some Knowledgeable

Not Knowledgeable

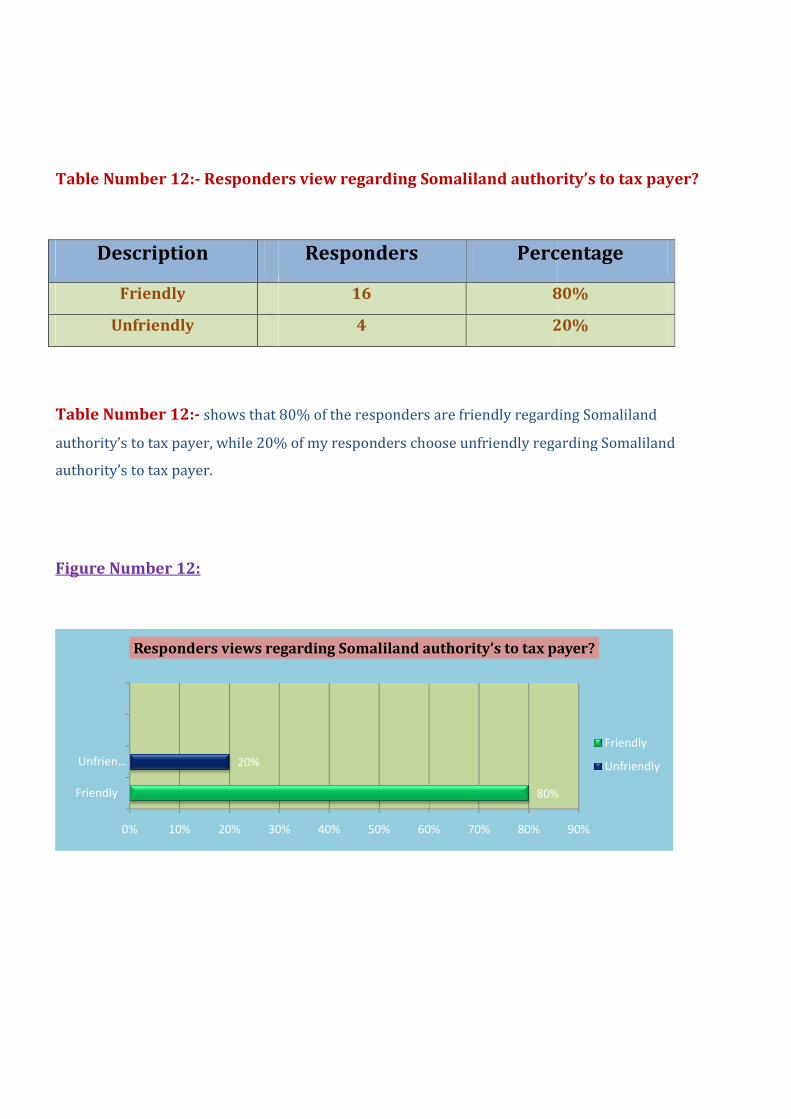

Table Number 10:- Responders by the View of current

Description

High

Fair

Low

Table number 10:- shows that 50% of the responders views are high, 15% of the responders

said that the current income tax rate is fair, while 35% choose that the

low.

Figure Number 10:

0%

10%

20%

30%

40%

50%

60%

High Fair

Responders view by the current Tax rate

Responders by the View of current income tax rates.

Responders Percentage

10 50

3 15

7 3

shows that 50% of the responders views are high, 15% of the responders

said that the current income tax rate is fair, while 35% choose that the rate of the current tax is

Low

Responders view by the current Tax rate

income tax rates.

Percentage