THE HOME OF THE

PROFESSIONAL ADVISER

Supporting Circumstantial WealthNavigating the challenges of advising 3rd party investors

For Adviser Use Only – Not approved for use with clients

Agenda

• Circumstantial wealth creation• What additional value can adviser add

– 3rd party– Professional introducers?– Vulnerable beneficiaries

• 3rd party investor types– Challenges of assessing investment risk for 3rd parties– Challenges of investment suitability for trusts

• Impact on your Practice– Reactive? Existing clients?– Proactive approach to professional introducers

• Help and support from Prudential

Circumstantial Wealth / 3rd Party Investors

• Critical illness• Court awards• Insurance payments• Trustees

– Generally– Vulnerable Beneficiaries

• Powers of Attorney• Court of Protection Deputy

Trusts for Vulnerable Beneficiaries

•Vulnerable Beneficiary defined:–person who is mentally or physically disabled, or

–relevant minor (under 18) and has lost a parent

•Qualifying Trust if assets capable of use only for disabled person

–even if no interest-in-possession, then no income can be applied for others

•Special tax treatment claimed by Vulnerable Person Election (VPE1)–Sent to HMRC by Trustees

•Trustees effectively taxed at vulnerable beneficiary’s rate–Income Tax

–Capital Gains Tax

•Inheritance Tax–transfer in to qualifying Trust is a PET, not a CLT

–transfer out to vulnerable beneficiary, no IHT

–no periodic charges

–assets part of beneficiary’s estate on death

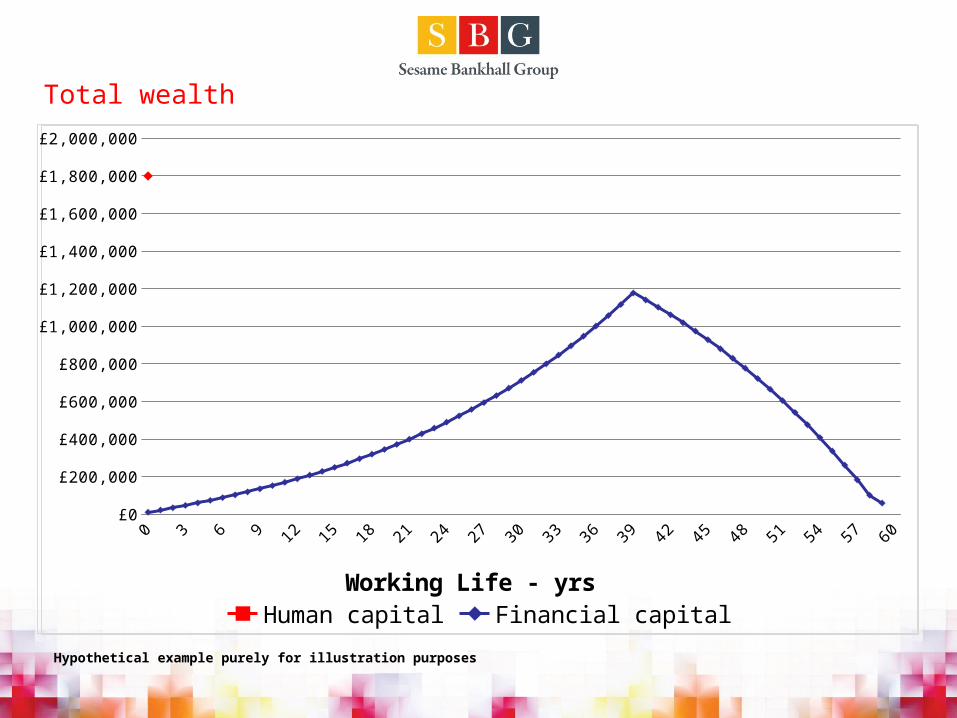

Total wealth

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

£1,800,000

£2,000,000

Human capital Financial capital

Working Life - yrs

Hypothetical example purely for illustration purposes

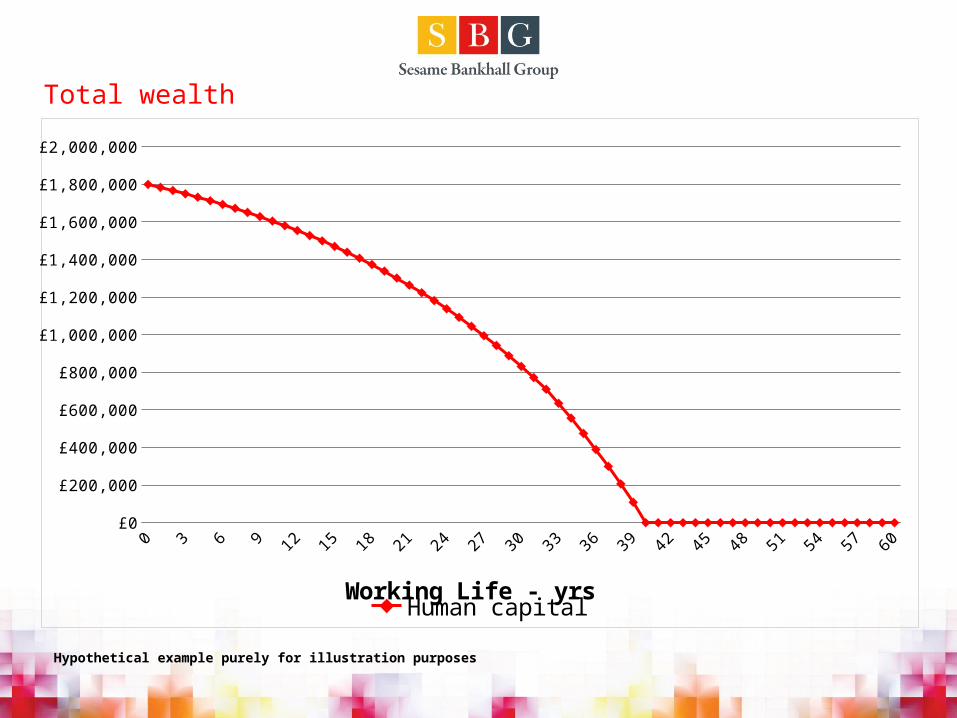

Total wealth

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

£1,800,000

£2,000,000

Human capitalWorking Life - yrs

Hypothetical example purely for illustration purposes

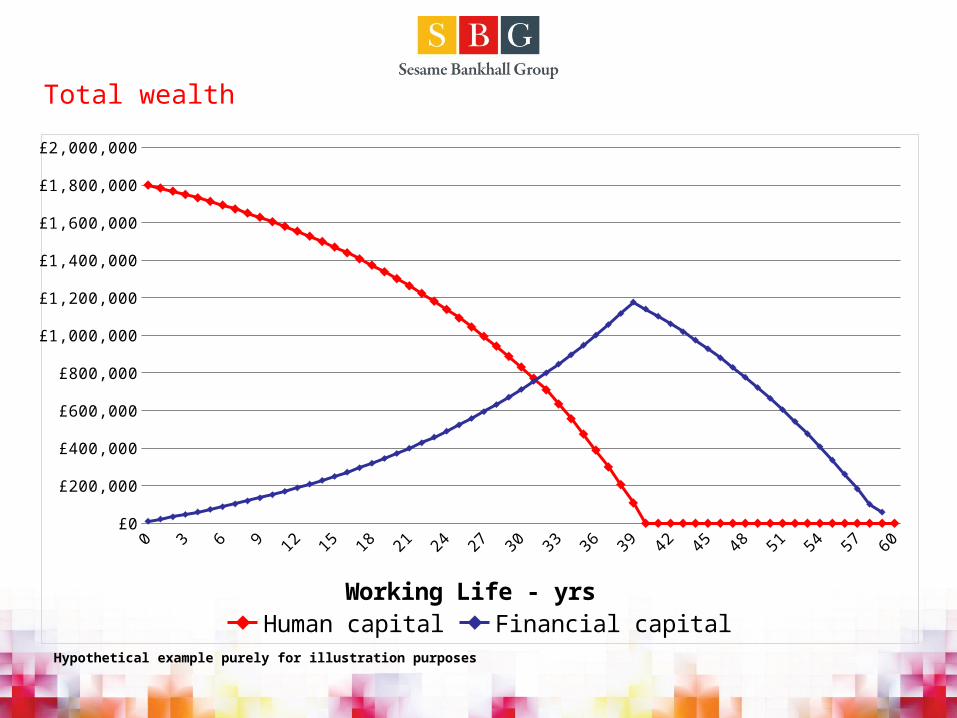

Total wealth

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

£1,800,000

£2,000,000

Human capital Financial capital

Working Life - yrs

Hypothetical example purely for illustration purposes

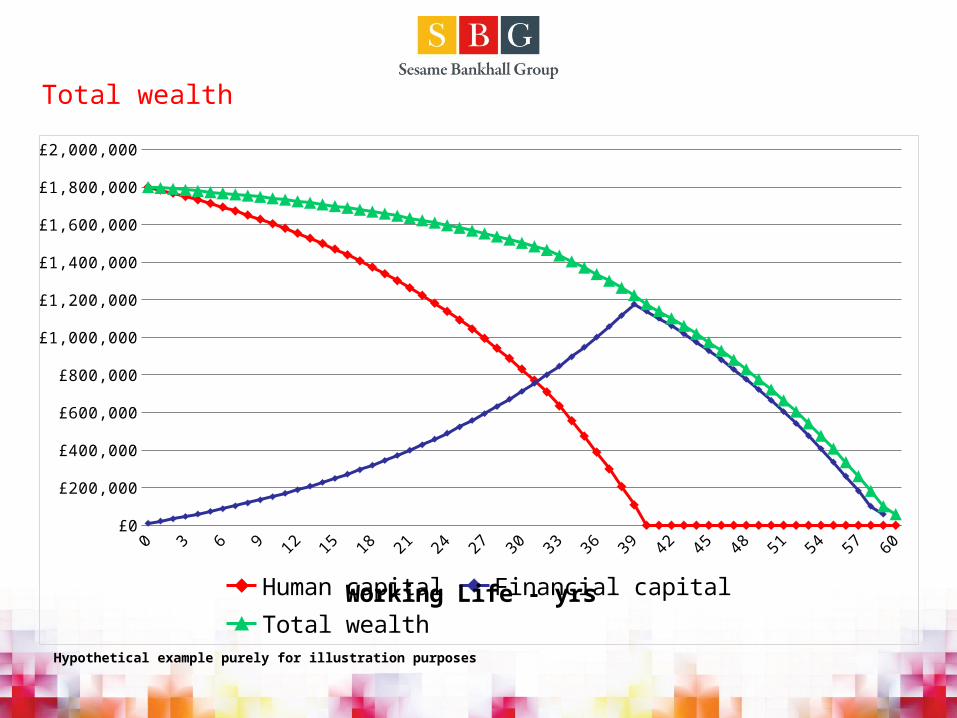

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

£1,800,000

£2,000,000

Human capital Financial capital Total wealth

Working Life - yrs

Hypothetical example purely for illustration purposes

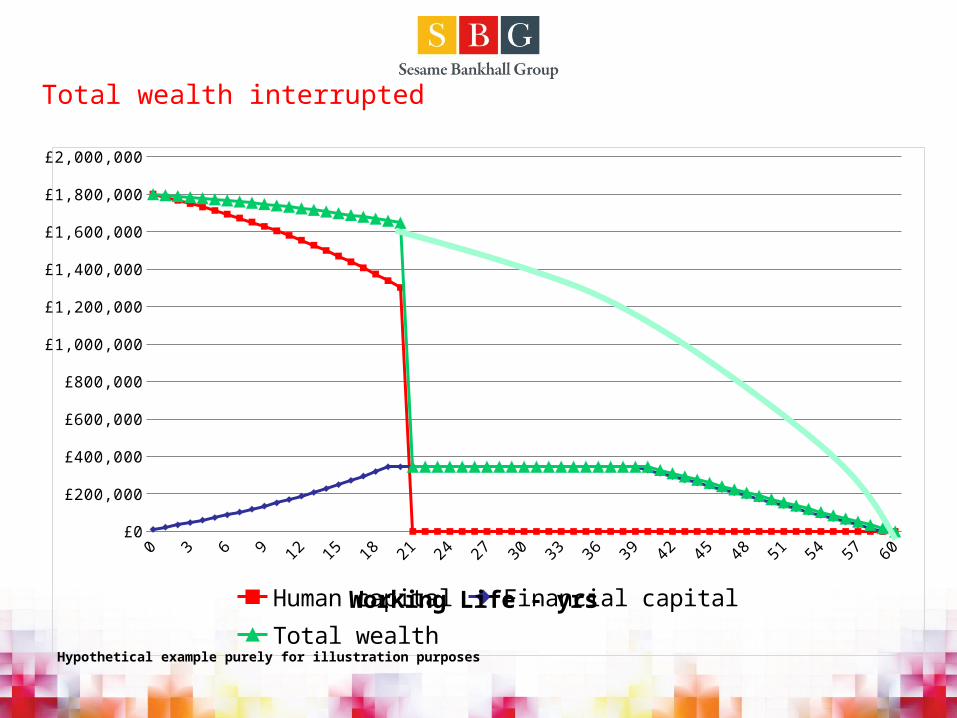

Total wealth

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

£1,800,000

£2,000,000

Human capital Financial capital Total wealth

Working Life - yrs

Hypothetical example purely for illustration purposes

Total wealth interrupted

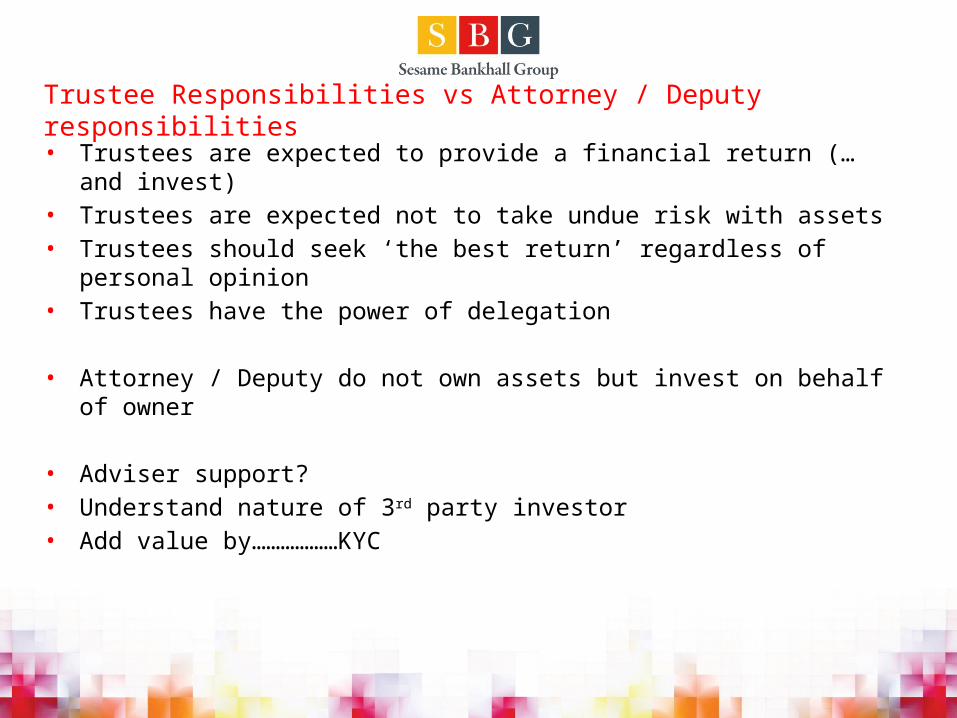

Trustee Responsibilities vs Attorney / Deputy responsibilities

• Trustees are expected to provide a financial return (…and invest)• Trustees are expected not to take undue risk with assets• Trustees should seek ‘the best return’ regardless of personal opinion• Trustees have the power of delegation

• Attorney / Deputy do not own assets but invest on behalf of owner

• Adviser support?• Understand nature of 3rd party investor• Add value by………………KYC

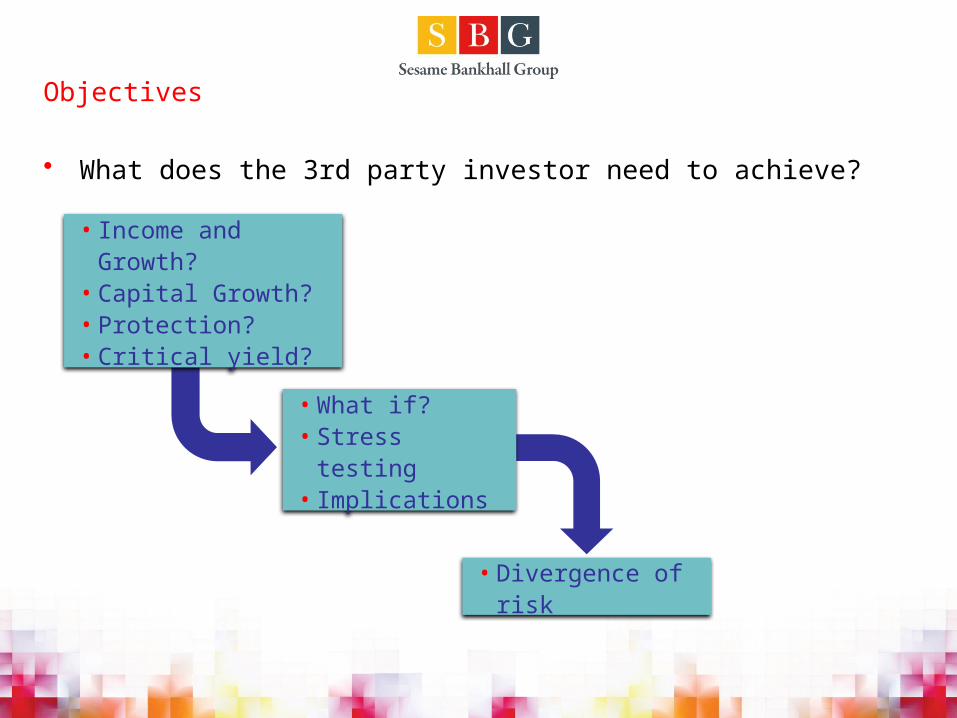

Objectives

• What does the 3rd party investor need to achieve?

• Income and Growth?• Capital Growth?• Protection?• Critical yield?

• What if?• Stress testing• Implications

• Divergence of risk

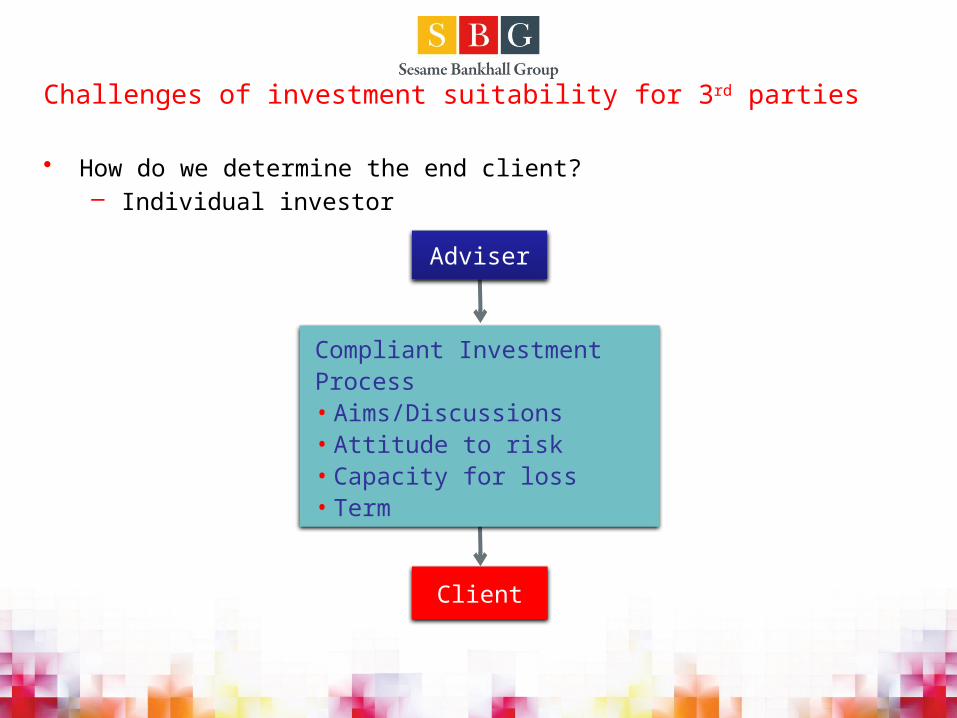

Challenges of investment suitability for 3rd parties

• How do we determine the end client?– Individual investor

Adviser

Client

Compliant Investment Process• Aims/Discussions• Attitude to risk• Capacity for loss• Term

Compliant Investment Process

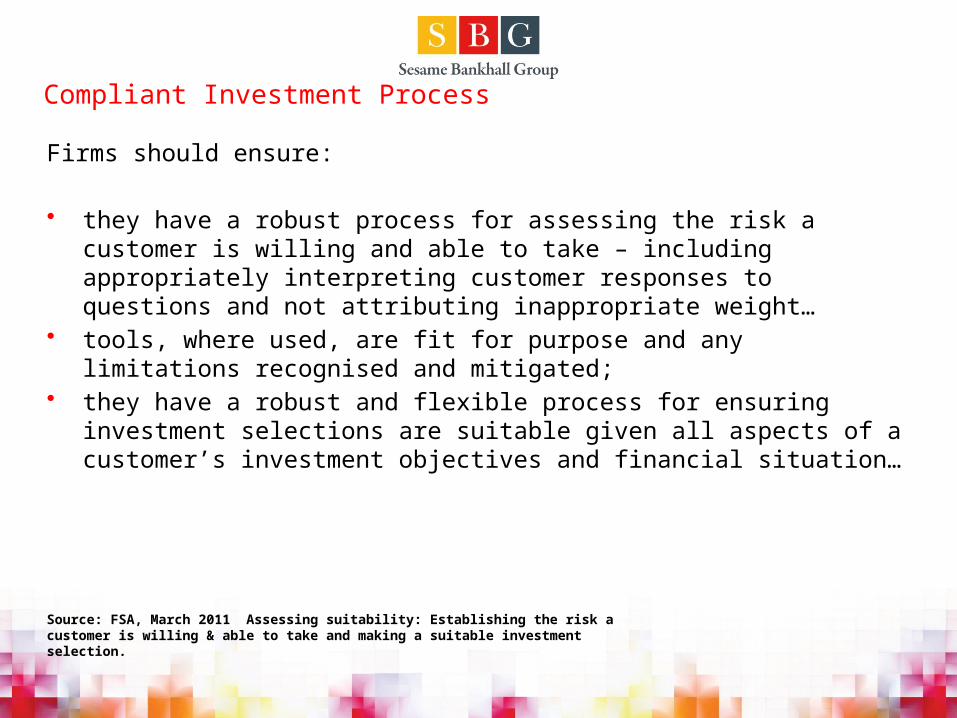

Firms should ensure:

• they have a robust process for assessing the risk a customer is willing and able to take – including appropriately interpreting customer responses to questions and not attributing inappropriate weight…

• tools, where used, are fit for purpose and any limitations recognised and mitigated;

• they have a robust and flexible process for ensuring investment selections are suitable given all aspects of a customer’s investment objectives and financial situation…

Source: FSA, March 2011 Assessing suitability: Establishing the risk a customer is willing & able to take and making a suitable investment selection.

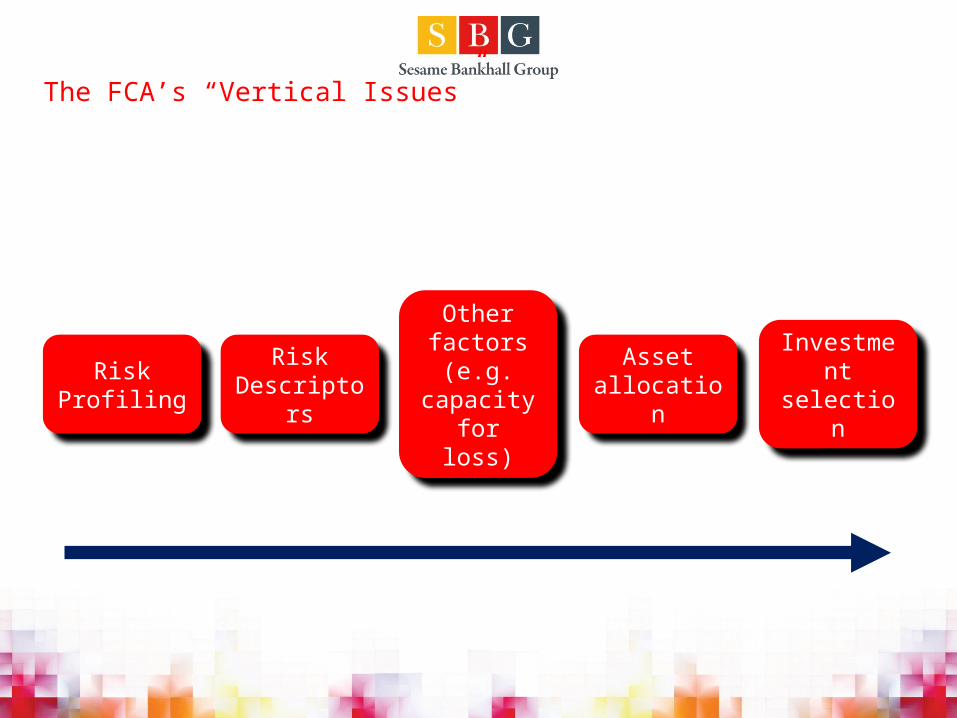

Risk Profiling

Risk Descriptors

Other factors (e.g.

capacity for loss)

Asset allocation

Investment selection

The FCA’s “Vertical Issues”

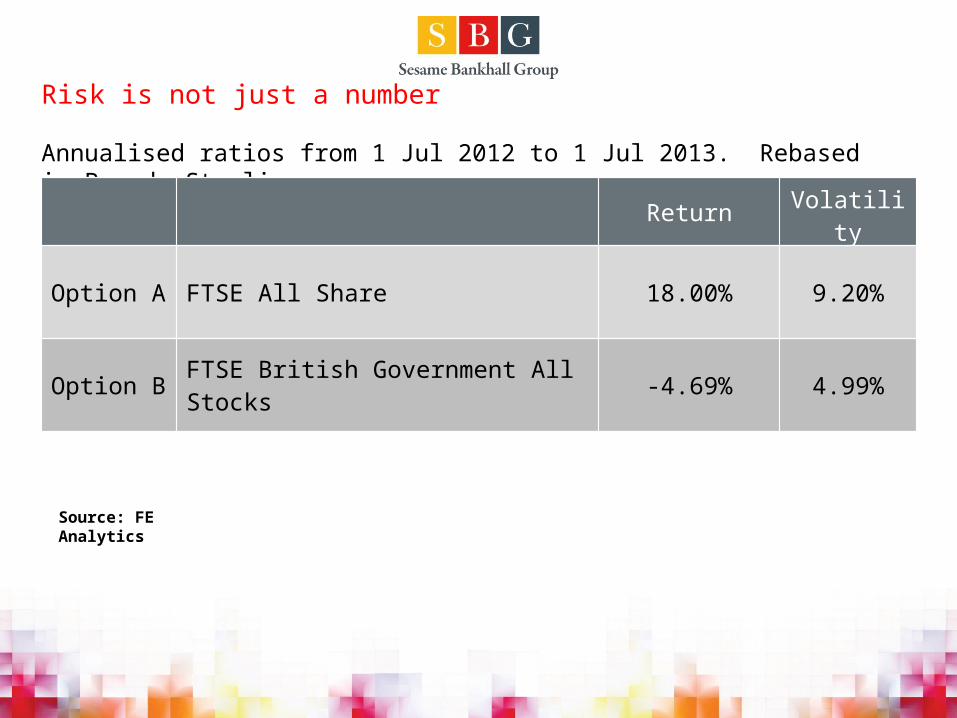

Risk is not just a number

Return Volatility

Option A -1.03% 16.68%

Option B 13.49% 6.16%

Annualised ratios from 1 Jul 2011 to 1 Jul 2012. Rebased in Pounds Sterling

Source: FE Analytics

Which would you pick?

Risk is not just a number

Annualised ratios from 1 Jul 2012 to 1 Jul 2013. Rebased in Pounds Sterling

Return Volatility

Option A FTSE All Share 18.00% 9.20%

Option B FTSE British Government All Stocks -4.69% 4.99%

Source: FE Analytics

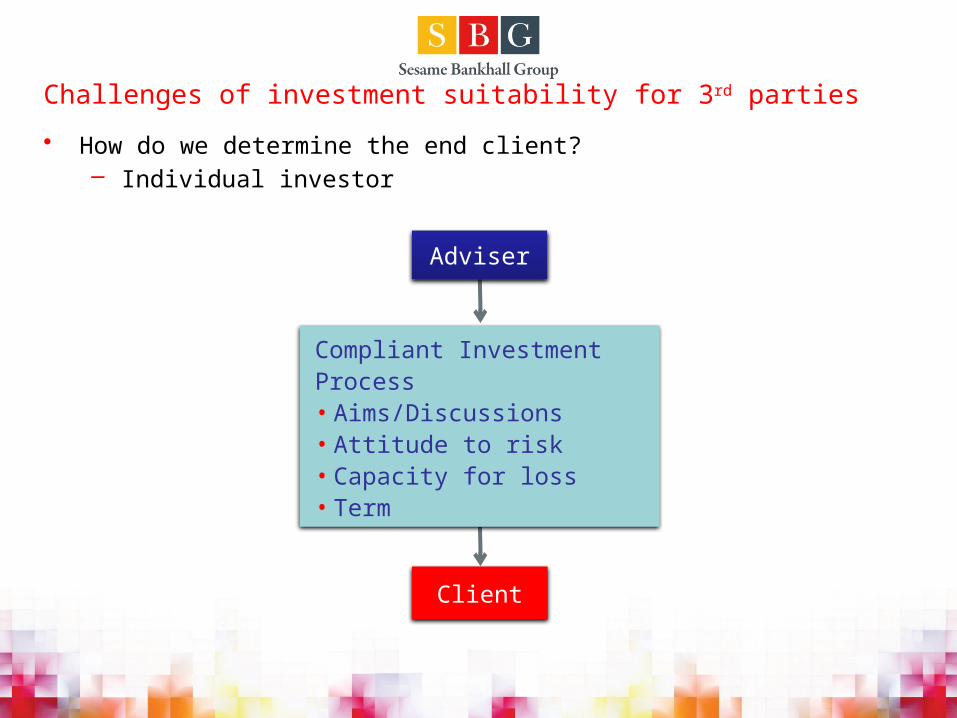

Challenges of investment suitability for 3rd parties

• How do we determine the end client?– Individual investor

Adviser

Client

Compliant Investment Process• Aims/Discussions• Attitude to risk• Capacity for loss• Term

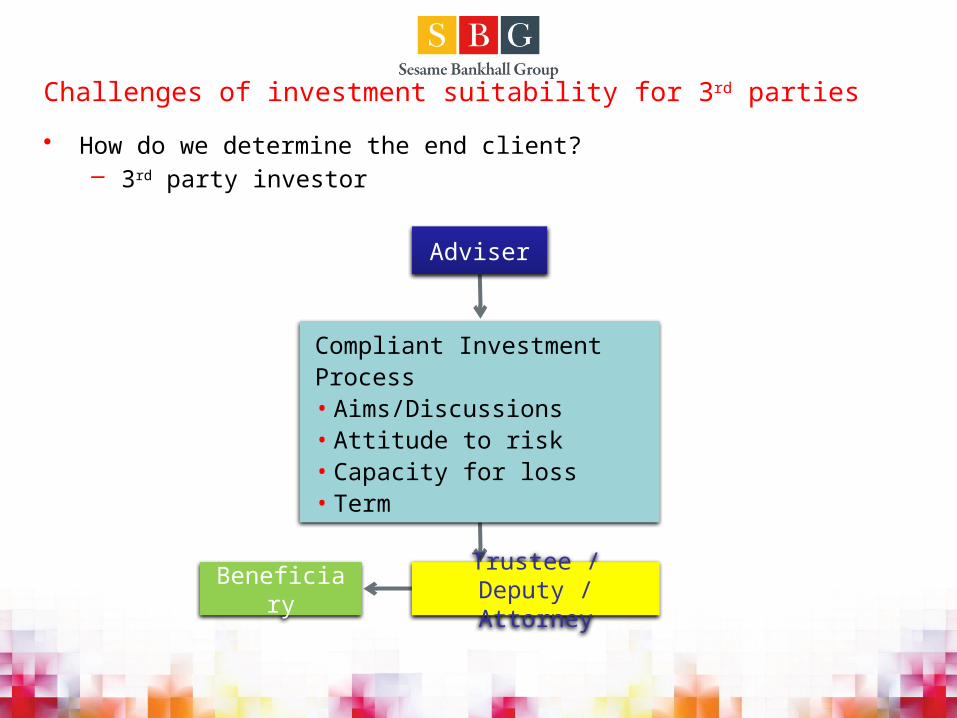

Challenges of investment suitability for 3rd parties

• How do we determine the end client?– 3rd party investor

Adviser

Compliant Investment Process• Aims/Discussions• Attitude to risk• Capacity for loss• Term

Trustee / Deputy / Attorney

Beneficiary

Thematic Review – FCA Key Findings

Potential problem

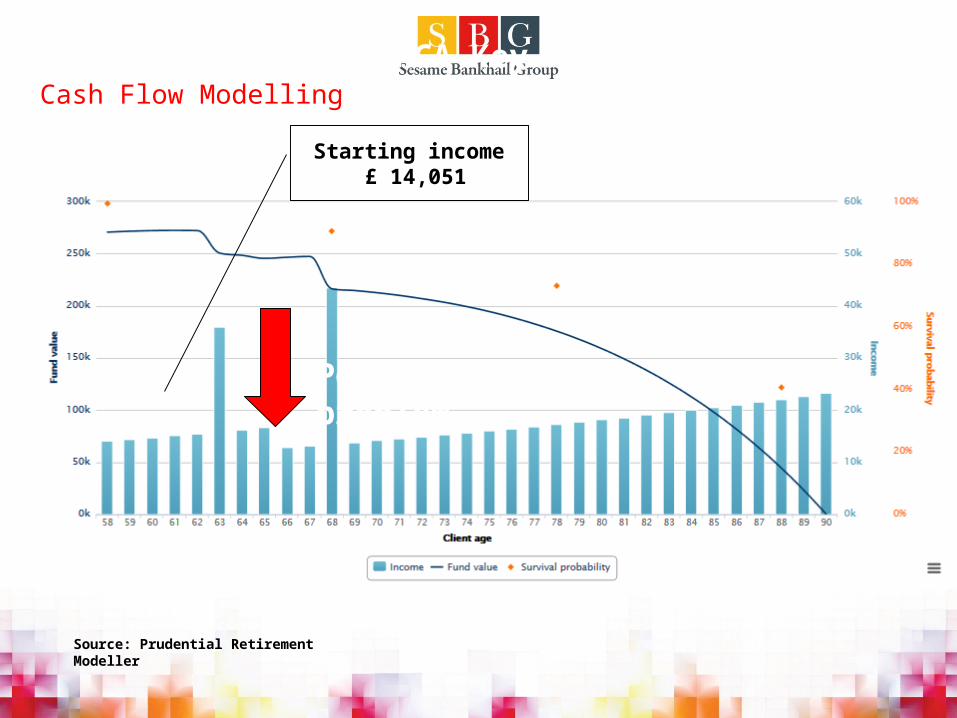

Cash Flow Modelling

Starting income £ 14,051

Source: Prudential Retirement Modeller

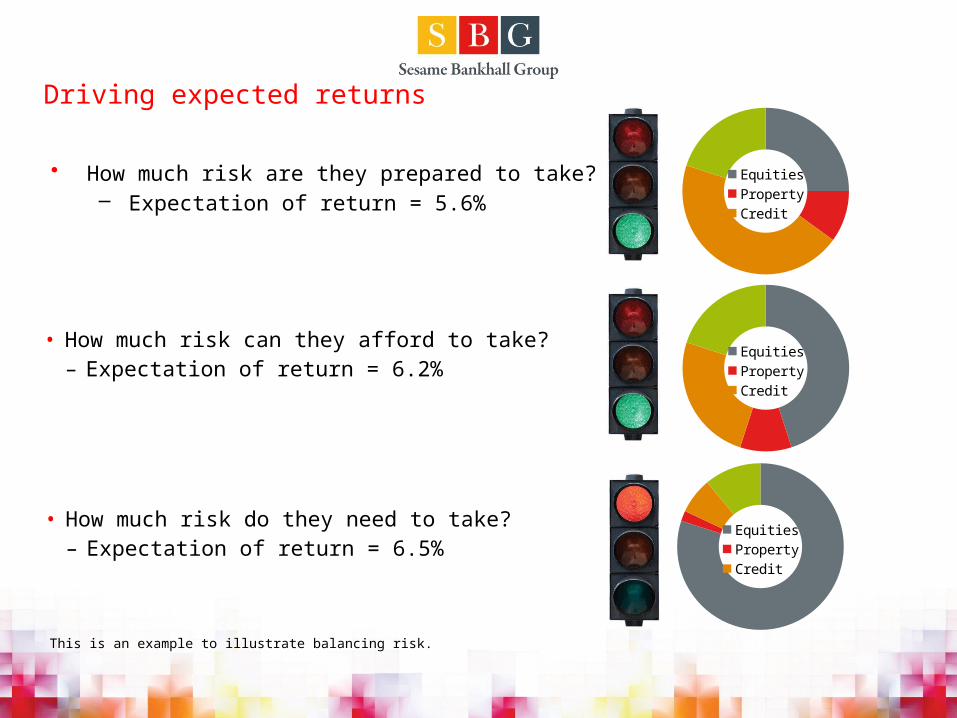

Driving expected returns

EquitiesPropertyCredit

EquitiesPropertyCredit

EquitiesPropertyCredit

• How much risk are they prepared to take?– Expectation of return = 5.6%

• How much risk can they afford to take?– Expectation of return = 6.2%

• How much risk do they need to take?– Expectation of return = 6.5%

This is an example to illustrate balancing risk.

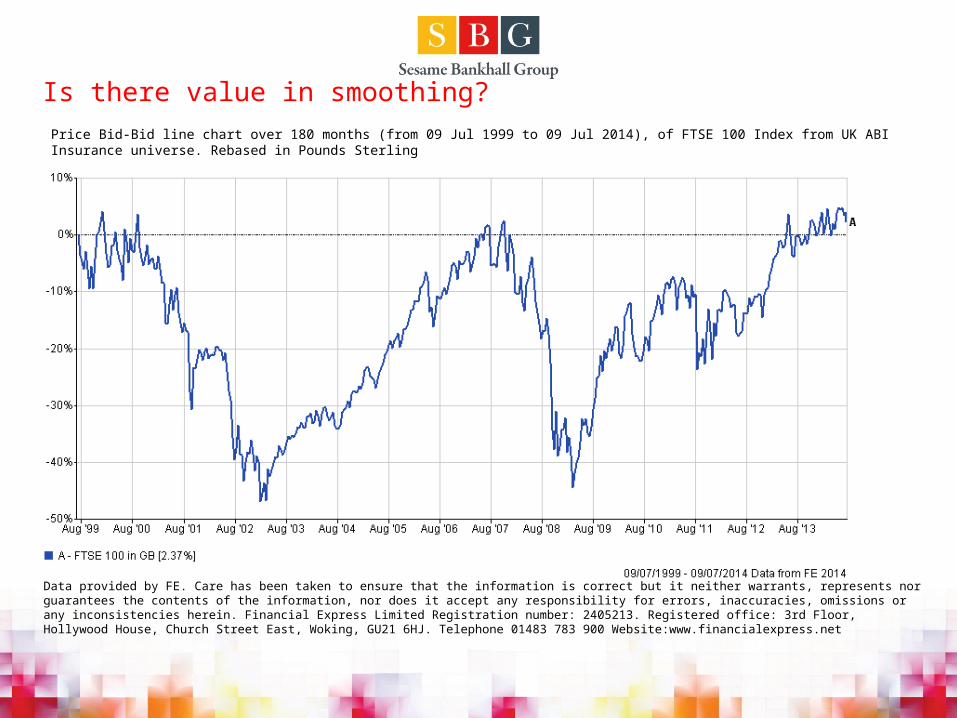

Is there value in smoothing?

Price Bid-Bid line chart over 180 months (from 09 Jul 1999 to 09 Jul 2014), of FTSE 100 Index from UK ABI Insurance universe. Rebased in Pounds Sterling

Data provided by FE. Care has been taken to ensure that the information is correct but it neither warrants, represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Financial Express Limited Registration number: 2405213. Registered office: 3rd Floor, Hollywood House, Church Street East, Woking, GU21 6HJ. Telephone 01483 783 900 Website:www.financialexpress.net

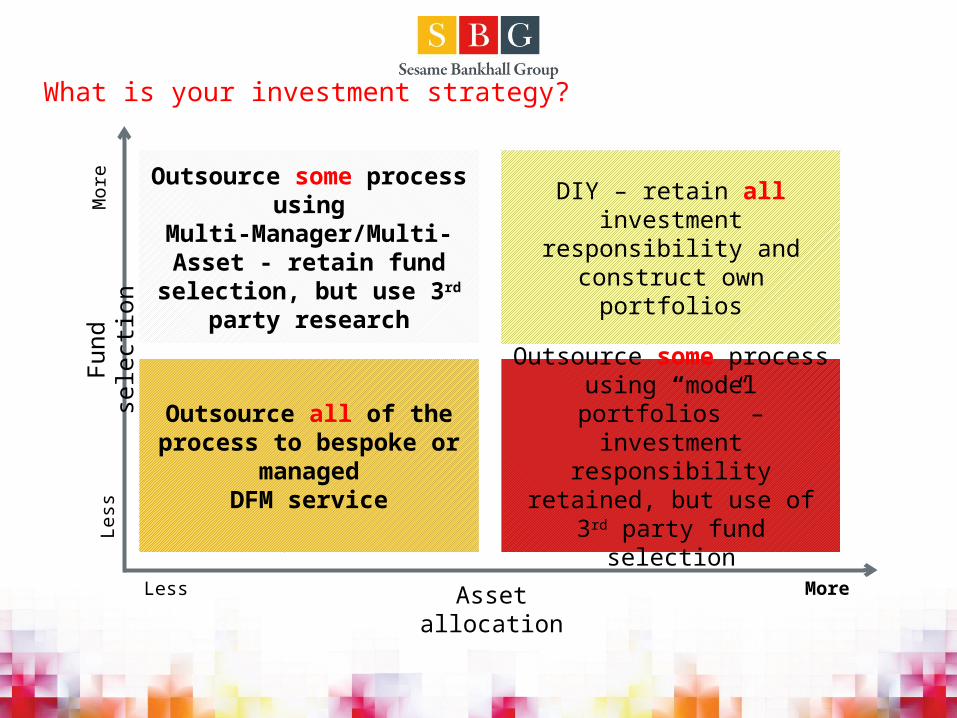

DIY – retain all investment responsibility and construct

own portfolios

Outsource some process using “model portfolios” – investment responsibility

retained, but use of 3rd party fund selection

Outsource all of the process to bespoke or

managedDFM service

Outsource some process using Multi-Manager/Multi-

Asset - retain fund selection, but use 3rd party

research

What is your investment strategy?

Asset allocation

Fun

d se

lect

ion

Less More

Less

Mor

e

Publications

Online support

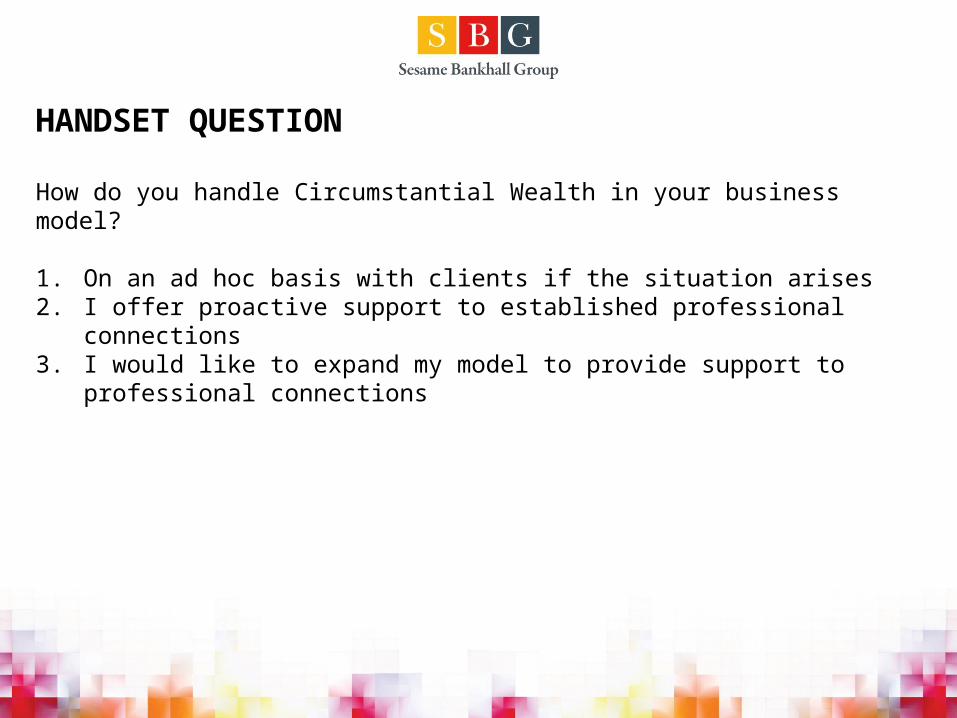

HANDSET QUESTION

How do you handle Circumstantial Wealth in your business model?

1. On an ad hoc basis with clients if the situation arises2. I offer proactive support to established professional connections3. I would like to expand my model to provide support to professional

connections

Summary

• Life changing events create the need for valued advice support

• Opportunity to review the support from your practice:- to existing clients- to existing professional connections- to potential professional connections

Important information

This presentation contains some forward thinking statements which should not be taken as fact. Information given is based on our current understanding, as at July 2014, of current taxation, legislation and HMRC practice, all of which are liable to change.

No reproduction, copy, transmission or amendment of this presentation maybe made without the written permission from Prudential.

“Prudential" is a trading name of The Prudential Assurance Company Limited, of Prudential Annuities Limited and of Prudential Retirement Income Limited. This name is also used by other companies within the Prudential Group, which between them provide a range of financial products including life assurance, pensions, savings and investment products. The Prudential Assurance Company Limited and Prudential Annuities Limited are registered in England and Wales. Registered Office at Laurence Pountney Hill, London, EC4R 0HH. Registered numbers 15454 and 2554213 respectively. Prudential Retirement Income Limited is registered in Scotland. Registered Office at Craigforth, Stirling FK9 4UE. Registered number SCO47842.

Authorised and regulated by the Financial Conduct Authority.

Recommended