The Global Economic Outlook

May 2005

Jay H. Bryson, Global EconomistWachovia Corporation

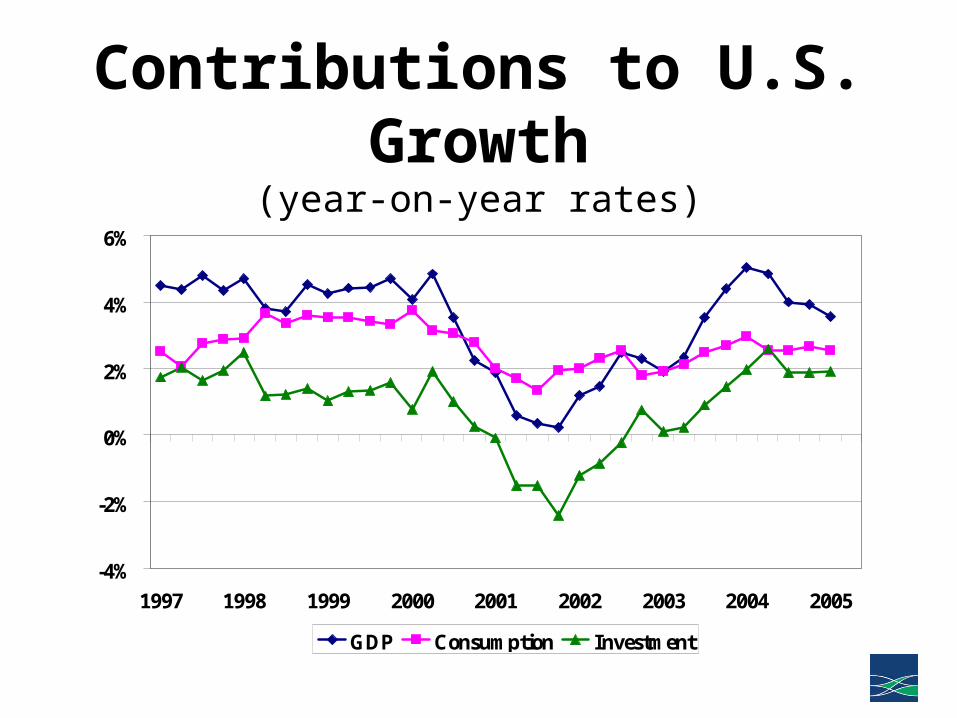

Contributions to U.S. Growth(year-on-year rates)

-4%

-2%

0%

2%

4%

6%

1997 1998 1999 2000 2001 2002 2003 2004 2005

GDP Consumption Investment

U.S. Real GDP Components(year-on-year growth)

-2%

0%

2%

4%

6%

1998 1999 2000 2001 2002 2003 2004 2005

GDP Productivity Employment

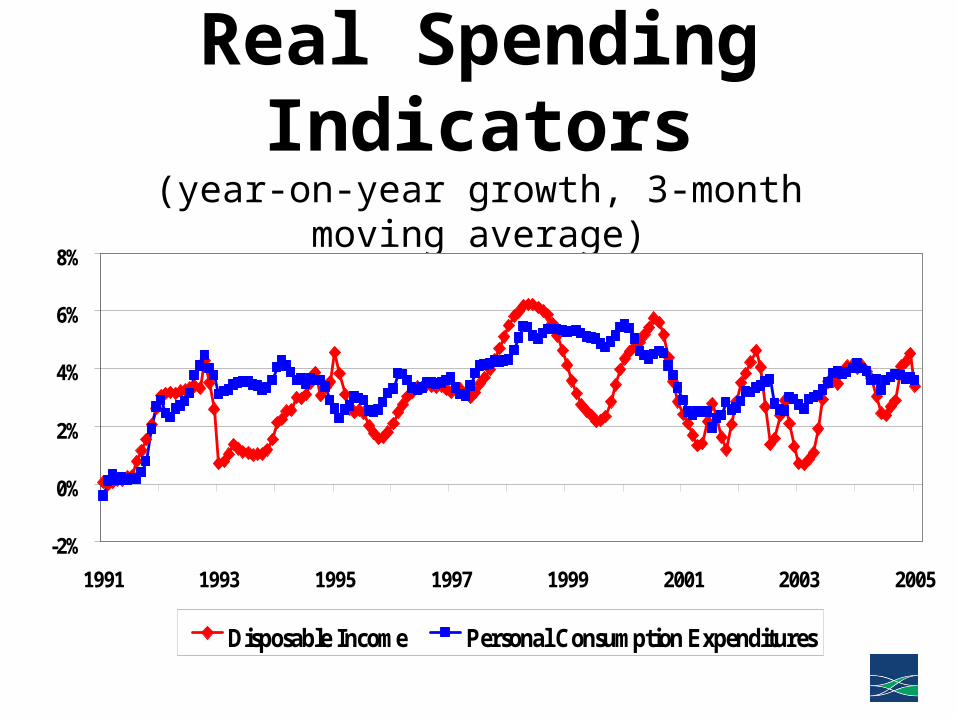

Real Spending Indicators(year-on-year growth, 3-month moving average)

-2%

0%

2%

4%

6%

8%

1991 1993 1995 1997 1999 2001 2003 2005

Disposable Income Personal Consumption Expenditures

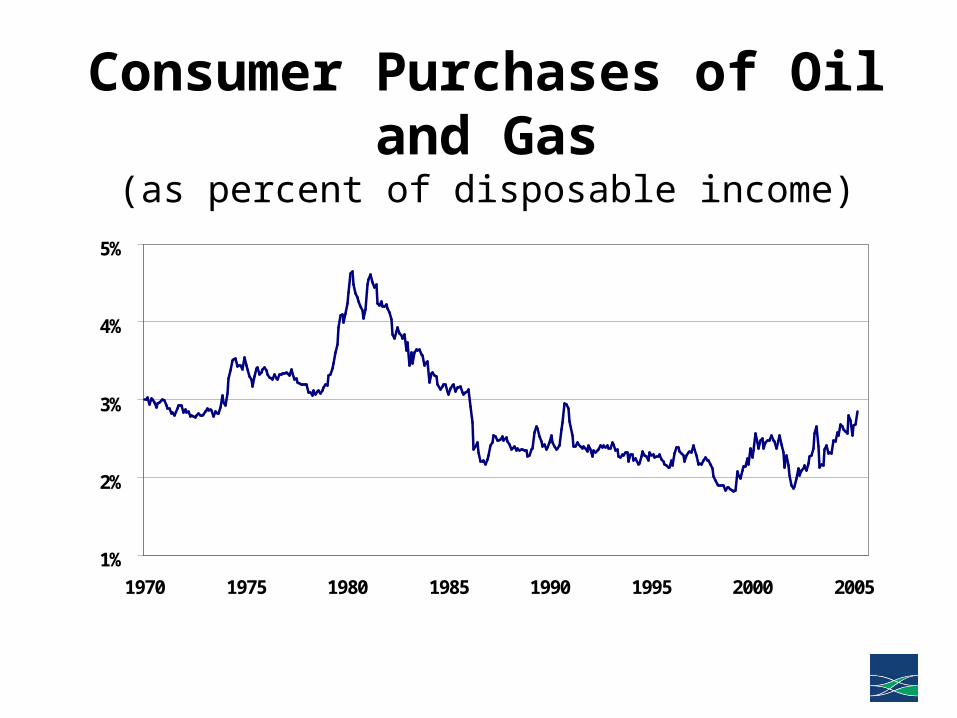

Consumer Purchases of Oil and Gas(as percent of disposable income)

1%

2%

3%

4%

5%

1970 1975 1980 1985 1990 1995 2000 2005

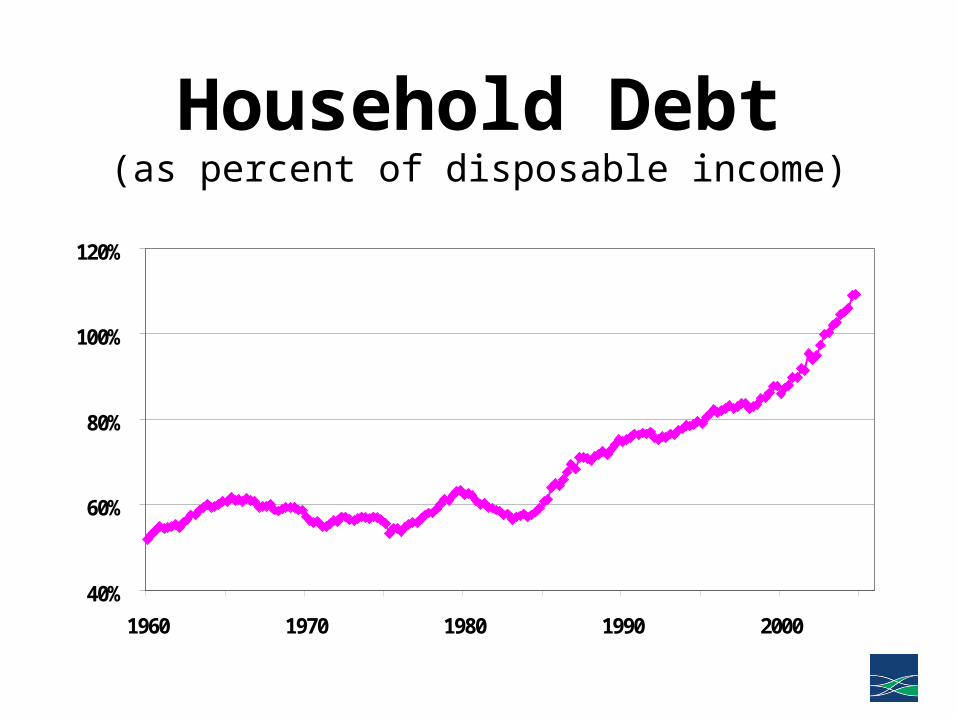

Household Debt(as percent of disposable income)

40%

60%

80%

100%

120%

1960 1970 1980 1990 2000

Household Financial Indicators

20%

25%

30%

35%

40%

45%

1960 1970 1980 1990 2000

6%

8%

10%

12%

14%

16%

Liabilities as % of financial assets (LHS) debt service as % of disposable income

Inventory-to-Sales Ratio(months of inventories at current sales pace)

1.2

1.3

1.4

1.5

1.6

1990 1992 1994 1996 1998 2000 2002 2004

“Core” Capital Goods Orders(year-on-year growth, 3-month moving average)

-30%

-20%

-10%

0%

10%

20%

1997 1998 1999 2000 2001 2002 2003 2004 2005

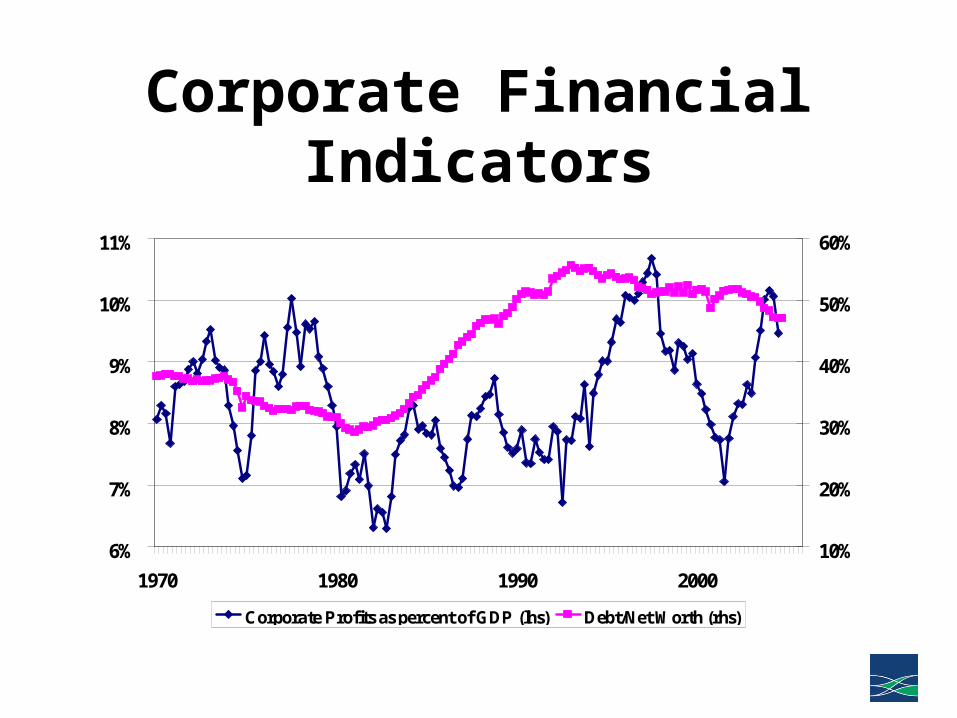

Corporate Financial Indicators

6%

7%

8%

9%

10%

11%

1970 1980 1990 2000

10%

20%

30%

40%

50%

60%

Corporate Profits as percent of GDP (lhs) Debt/Net Worth (rhs)

“Core” PCE Deflator(year-on-year change)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1995 1997 1999 2001 2003 2005

U.S. Outlook05-Q2 05-Q3 05-Q4 06-Q1 06-Q2 06-Q3 06-Q4

GDP Growth 3.1 3.1 3.2 3.3 3.3 3.3 3.3

PCE 2.3 2.7 2.8 2.7 2.7 2.6 2.6

BFI 8.2 7.8 7.8 7.9 8.2 8.3 8.3

"Core" CPI Inflation 2.5 2.6 2.7 2.8 2.8 2.9 3.0

Fed Funds Rate 3.25 3.75 4.00 4.25 4.50 4.75 4.75

10-Year Treasury 4.70 5.00 5.20 5.40 5.50 5.80 5.90

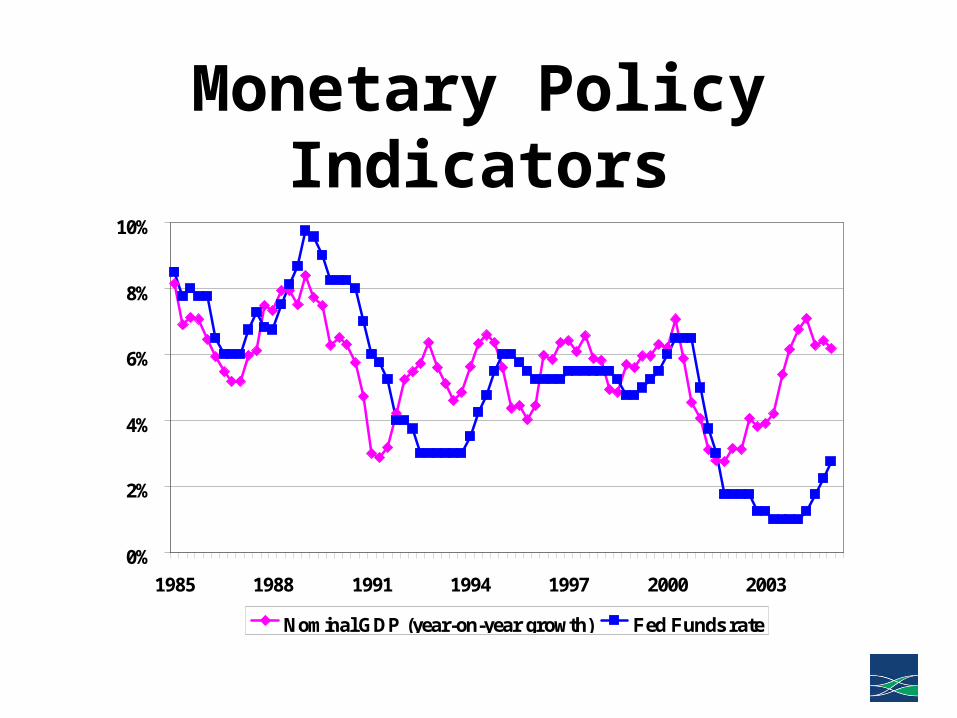

Monetary Policy Indicators

0%

2%

4%

6%

8%

10%

1985 1988 1991 1994 1997 2000 2003

Nominal GDP (year-on-year growth) Fed Funds rate

U.S. External Indicators(4-quarter moving sums)

0

200

400

600

800

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

billi

ons

of d

olla

rs

Current Account Deficit Private Capital Inflows

Trade in Goods & Services(year-on-year growth, 3-month moving average)

-20%

-10%

0%

10%

20%

30%

1998 1999 2000 2001 2002 2003 2004 2005

Exports Imports

Dollar Exchange RatesCurrency 05-Q2 05-Q3 05-Q4 06-Q1 06-Q2 06-Q3 06-Q4

Euro ($/€) 1.32 1.36 1.40 1.42 1.43 1.44 1.45

U.K. ($/£) 1.90 1.92 1.94 1.95 1.96 1.97 1.97

Switzerland (CHF/$) 1.18 1.15 1.12 1.11 1.11 1.10 1.10

Japan (¥/$) 105 102 100 97 94 92 90

Canada (C$/US$) 1.20 1.18 1.16 1.15 1.14 1.13 1.12

Global Exports(as percent of Global GDP)

0%

5%

10%

15%

20%

25%

30%

1970 1975 1980 1985 1990 1995 2000

Imports-to-Shipments Ratios

2%

3%

4%

5%

1994 1996 1998 2000 2002 2004

10%

20%

30%

40%

Printed Materials (left) All Manufacturing Industries (right)

Real GDP Growth Rates(year-on-year rates)

0%

2%

4%

6%

8%

10%

12%

1997 1998 1999 2000 2001 2002 2003 2004 2005

China India

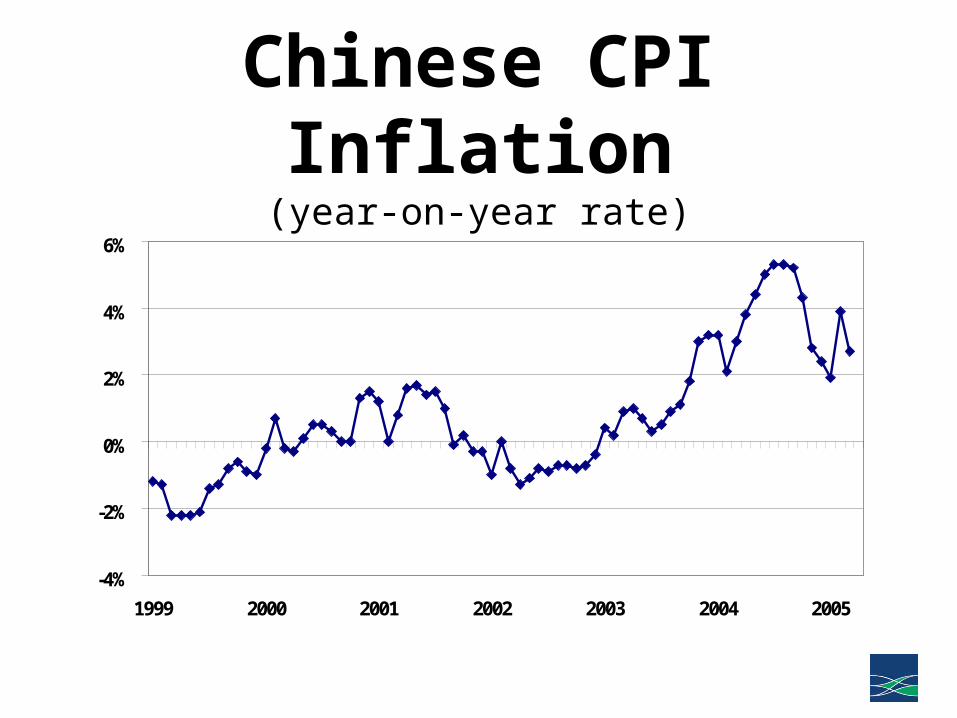

Chinese CPI Inflation(year-on-year rate)

-4%

-2%

0%

2%

4%

6%

1999 2000 2001 2002 2003 2004 2005

Chinese Industrial Production(year-on-year growth, 3-month moving average)

0%

5%

10%

15%

20%

25%

1999 2000 2001 2002 2003 2004 2005

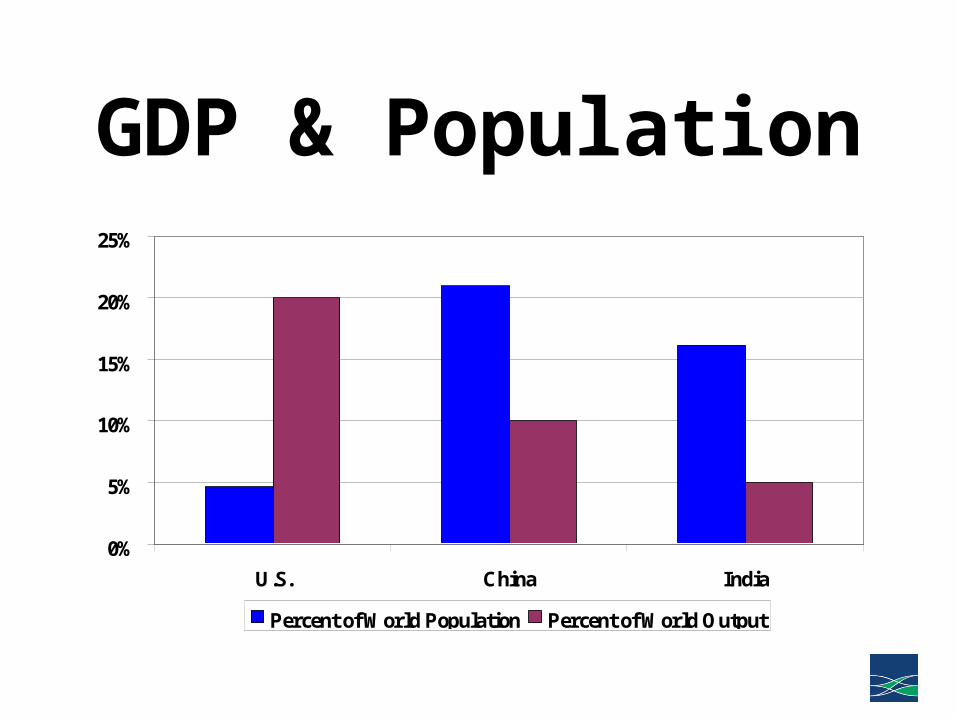

GDP & Population

0%

5%

10%

15%

20%

25%

U.S. China India

Percent of World Population Percent of World Output

Real GDP

0

200

400

600

800

1000

1200

1400

1600

0 10 20 30 40 50 60

years

inde

x

US: 1869-1929 China: 1978-2004 Japan: 1955-2004

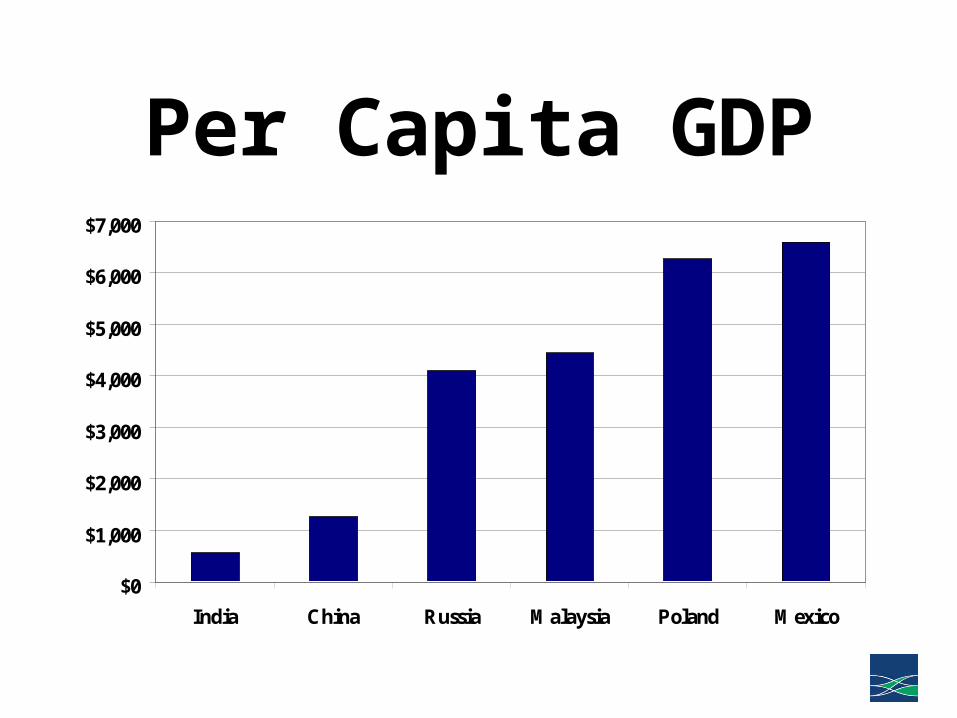

Per Capita GDP

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

India China Russia Malaysia Poland Mexico

Chinese Renminbi• Although not necessarily imminent, the

currency will become more flexible.• China is slowly liberalizing its financial

system. Flexibility needs to be seen in that context.

• Managed float?• Not apparent that currency would

necessarily appreciate in long run.

Notable Near-Term RisksUpside

• Synchronous global upswing in capital spending.

• Decline in foreign savings rates.

• More fiscal stimulus, especially in the Eurozone.

Downside

• Dollar crash.• Geopolitical tension

(terrorism, Iran/North Korea).

• Spike in oil prices.• Inflation scare in U.S.

Summary of Near-Term Outlook

• Global growth should be solid in 2005, albeit somewhat slower than last year.

• Inflation is starting to turn up, although a return to the 1970’s is very unlikely.

• Short-term interest rates should rise further over the next year or so.

• Dollar should trend even lower.

Recommended