The External Environment for Developing Countries

October 2009The World Bank

Development EconomicsProspects Group

The DOW regains 10,000

9/1/20089/2/20089/3/20089/4/20089/5/20089/8/20089/9/20089/10/20089/11/20089/12/20089/15/20089/16/20089/17/20089/18/20089/19/20089/22/20089/23/20089/24/20089/25/20089/26/20089/29/20089/30/200810/1/200810/2/200810/3/200810/6/200810/7/200810/8/200810/9/200810/10/200810/13/200810/14/200810/15/200810/16/200810/17/200810/20/200810/21/200810/22/200810/23/200810/24/200810/27/200810/28/200810/29/200810/30/200810/31/200811/3/200811/4/200811/5/200811/6/200811/7/200811/10/200811/11/200811/12/200811/13/200811/14/200811/17/200811/18/200811/19/200811/20/200811/21/200811/24/200811/25/200811/26/200811/27/200811/28/200812/1/200812/2/200812/3/200812/4/200812/5/200812/8/200812/9/200812/10/200812/11/200812/12/200812/15/200812/16/200812/17/200812/18/200812/19/200812/22/200812/23/200812/24/200812/25/200812/26/200812/29/200812/30/200812/31/20081/1/20091/2/20091/5/20091/6/20091/7/20091/8/20091/9/20091/12/20091/13/20091/14/20091/15/20091/16/20091/19/20091/20/20091/21/20091/22/20091/23/20091/26/20091/27/20091/28/20091/29/20091/30/20092/2/20092/3/20092/4/20092/5/20092/6/20092/9/20092/10/20092/11/20092/12/20092/13/20092/16/20092/17/20092/18/20092/19/20092/20/20092/23/20092/24/20092/25/20092/26/20092/27/20093/2/20093/3/20093/4/20093/5/20093/6/20093/9/20093/10/20093/11/20093/12/20093/13/20093/16/20093/17/20093/18/20093/19/20093/20/20093/23/20093/24/20093/25/20093/26/20093/27/20093/30/20093/31/20094/1/20094/2/20094/3/20094/6/20094/7/20094/8/20094/9/20094/10/20094/13/20094/14/20094/15/20094/16/20094/17/20094/20/20094/21/20094/22/20094/23/20094/24/20094/27/20094/28/20094/29/20094/30/20095/1/20095/4/20095/5/20095/6/20095/7/20095/8/20095/11/20095/12/20095/13/20095/14/20095/15/20095/18/20095/19/20095/20/20095/21/20095/22/20095/25/20095/26/20095/27/20095/28/20095/29/20096/1/20096/2/20096/3/20096/4/20096/5/20096/8/20096/9/20096/10/20096/11/20096/12/20096/15/20096/16/20096/17/20096/18/20096/19/20096/22/20096/23/20096/24/20096/25/20096/26/20096/29/20096/30/20097/1/20097/2/20097/3/20097/6/20097/7/20097/8/20097/9/20097/10/20097/13/20097/14/20097/15/20097/16/20097/17/20097/20/20097/21/20097/22/20097/23/20097/24/20097/27/20097/28/20097/29/20097/30/20097/31/20098/3/20098/4/20098/5/20098/6/20098/7/20098/10/20098/11/20098/12/20098/13/20098/14/20098/17/20098/18/20098/19/20098/20/20098/21/20098/24/20098/25/20098/26/20098/27/20098/28/20098/31/20099/1/20099/2/20099/3/20099/4/20099/7/20099/8/20099/9/20099/10/20099/11/20099/14/20099/15/20099/16/20099/17/20099/18/20099/21/20099/22/20099/23/20099/24/20099/25/20099/28/20099/29/20099/30/200910/1/200910/2/200910/5/200910/6/200910/7/200910/8/200910/9/200910/12/200910/13/200910/14/200910/15/200910/16/200910/19/200910/20/20096,000

7,000

8,000

9,000

10,000

11,000

12,000

DJIA

Source: Thomson/Datastream.

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-0975

80

85

90

95

100

Source: JPMorgan-Chase.

Nominal effective rate [NEER]

Dollar declines imply a return to pre-crisis levels of the effective exchange rate

Indices, 2000=100.

Real effective rate [REER]

Neer 87.1Neer 85.5

Industrial countries

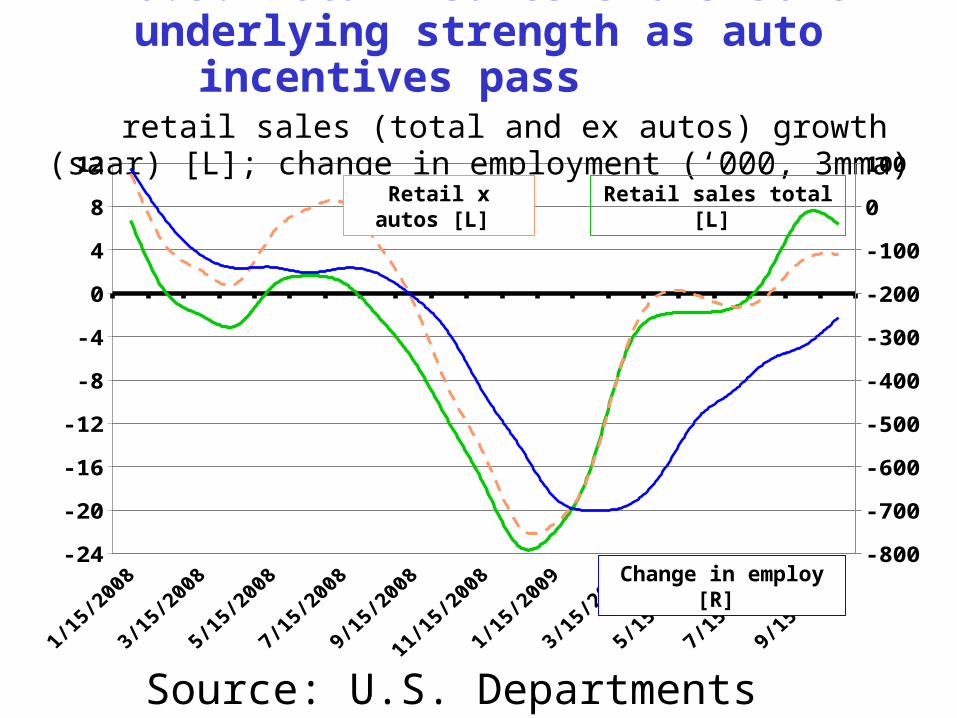

U.S. retail sales shows some underlying strength as auto incentives pass

retail sales (total and ex autos) growth (saar) [L]; change in employment (‘000, 3mma) [R]

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09-24

-20

-16

-12

-8

-4

0

4

8

12

-800

-700

-600

-500

-400

-300

-200

-100

0

100

Source: U.S. Departments of Commerce and Labor.

Retail x autos [L]

Change in employ [R]

Retail sales total [L]

A revival in both domestic and foreign demand is coming to support output growth

export volumes, capital goods orders ch%

(saar) [L]; IP mfgr ch% (saar) [R]

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09-50

-38

-25

-13

0

13

25

-25

-20

-15

-10

-5

0

5

10

Source: Department of Commerce and Federal Reserve System.

Capital goods orders [L]

IP manufacuring [R]

Export volumes [L]

Actual FY-2008 Preliminary FY-2009-4

-3

-2

-1

0

1

2

3ReceiptsOutlays

Source: Treasury, OMB and CBO.

U.S. spending up 17.8%, receipts down 16.6% yields fiscal deficit of about 10% of GDP

acutal FY 2008 and preliminary FY 2009 federal budget accounts ($trillion)

Deficit: $459 billion, 3.2% GDP

Deficit: $1,409 billion, 9.9% GDP

A change in sentiment toward stronger growth in Japan?

household spending and wages, ch% (y/y) [L]; Tokyo consumer sentiment [R]

Jan-08 Jun-08 Nov-08 Apr-09 Sep-09-10

-8

-6

-4

-2

0

2

4

27.5

32.5

37.5

42.5

Source: Japan Cabinet Office.

Consumer confidence [R]

Wages, growth y/y [L]

Household expenditure [L]

Japan’s orders-, exports and production take another leg up during August

core machinery orders, export volumes and mfgr output, ch% saar

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09-80

-60

-40

-20

0

20

40

60

Source: Bank of Japan and Japan Cabinet Office.

Production

Core machinery orders

Goods export volumes

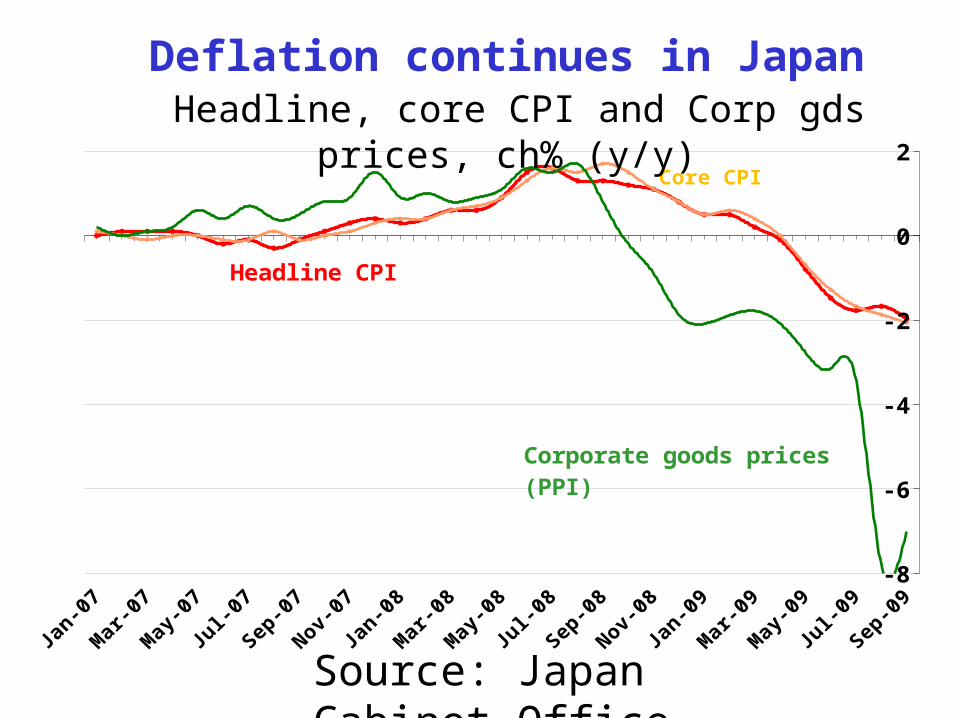

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09-8

-6

-4

-2

0

2

Headline CPI

Corporate goods prices (PPI)

Core CPI

Deflation continues in Japan Headline, core CPI and Corp gds prices,

ch% (y/y)

Source: Japan Cabinet Office.

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09-50.0

-37.5

-25.0

-12.5

0.0

12.5

25.0

Euro Area production moves sharply higher in August– due in part to auto incentives

manufacturing output, ch% (saar)

Germany

Source: Eurostat.

Euro Area

Italy

France

Household spending remains weakas unemployment continues to mount

Euro Area unemployment rate (%) [L] and retail volume growth (y/y) [R]

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-097.0

7.5

8.0

8.5

9.0

9.5

10.0

-5

-4

-3

-2

-1

0

1

2

Source: EUROSTAT.

Italy [R]

France [R]

Germany sales [R]

EA unemployment rate [L]

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-0980

100

120

140

160

180

zloty sterling rouble dollar yen

Euro appreciation may come to affect export prospects

euro cross exchange rates for select trade partners (LCU per euro)

Source: Thomson/Datastream and DECPG.

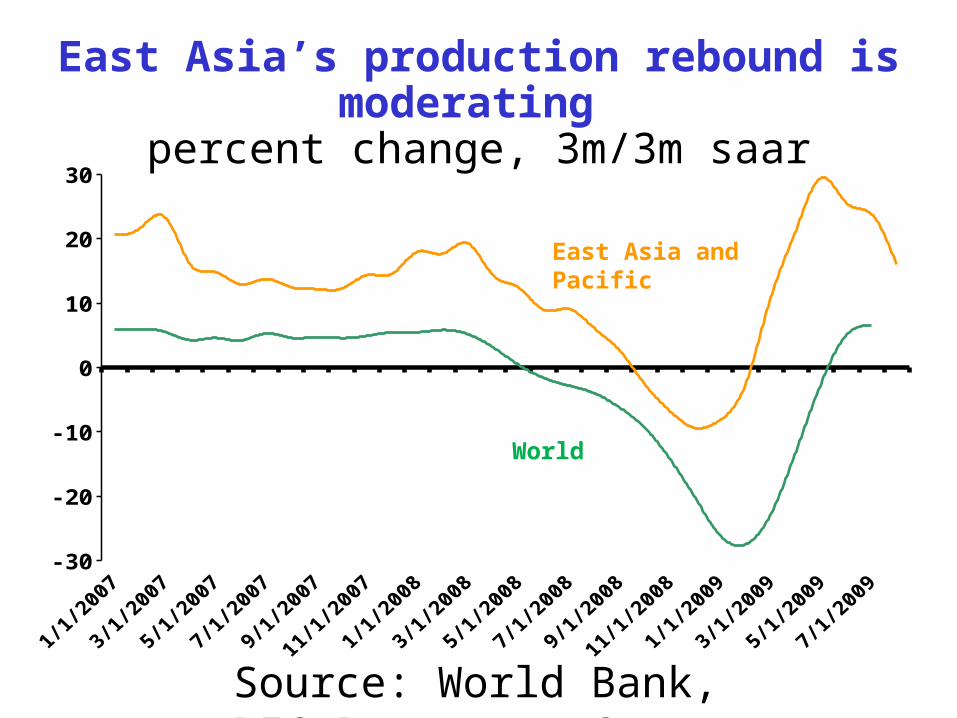

Industrial production

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09-30

-20

-10

0

10

20

30

East Asia’s production rebound is moderating

percent change, 3m/3m saar

World

East Asia and Pacific

Source: World Bank, DEC Prospects Group

High income country developments driving the global IP

cycle

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08 Q4-08 Q1-09 Q2-09 Q3-09-8

-6

-4

-2

0

2

4

6High Income Countries

Developing countries excl China

China

Source: World Bank, DEC Prospects Group.

contributions to global IP growth (% q-o-q)

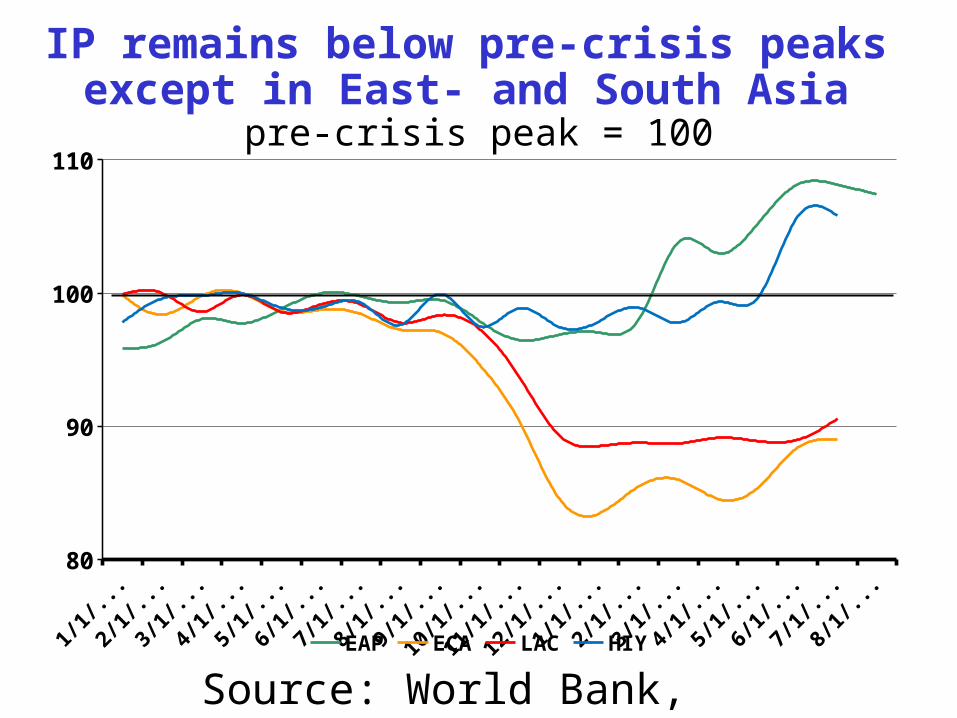

Jan-08 Jul-08 Jan-09 Jul-0980

90

100

110

EAP ECA LAC SAS

IP remains below pre-crisis peaks except in East- and South Asia

pre-crisis peak = 100

Source: World Bank, DEC Prospects Group

International trade

U.S. trade deficit shrinks as personal savings rate rises from record lows

Trade balance $ bn [R]; Personal savings as a percent of disposable income [L]

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-080

2

4

6

8

-80

-70

-60

-50

-40

-30

-20

-10

0

Source: U.S. Department of Commerce.

Trade balance [R]

Personal Savings rate [L]

Source: Haver Analytics.

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09-80

-60

-40

-20

0

20

40

60

80

15

20

25

30

35

40

Fixed asset investments [R]

Total imports excl. oil [L]

Investment-driven imports by China poised to slow

gross fixed capital formation [R]; Imports excl oil [L] %chg saar

Emerging Asia leads import recovery Total import volumes, 3mma seasonally

adjusted annualized % change

-80

-60

-40

-20

0

20

40

60

80

100

High Income countries

Source: World Bank, DEC Prospects Group.

East Asia including China

East Asia excl. China

Oil prices

Oil prices and OECD oil stocks

Jan-00Feb-00Mar-00Apr-00May-00Jun-00Jul-00Aug-00Sep-00Oct-00Nov-00Dec-00Jan-01Feb-01Mar-01Apr-01May-01Jun-01Jul-01Aug-01Sep-01Oct-01Nov-01Dec-01Jan-02Feb-02Mar-02Apr-02May-02Jun-02Jul-02Aug-02Sep-02Oct-02Nov-02Dec-02Jan-03Feb-03Mar-03Apr-03May-03Jun-03Jul-03Aug-03Sep-03Oct-03Nov-03Dec-03Jan-04Feb-04Mar-04Apr-04May-04Jun-04Jul-04Aug-04Sep-04Oct-04Nov-04Dec-04Jan-05Feb-05Mar-05Apr-05May-05Jun-05Jul-05Aug-05Sep-05Oct-05Nov-05Dec-05Jan-06Feb-06Mar-06Apr-06May-06Jun-06Jul-06Aug-06Sep-06Oct-06Nov-06Dec-06Jan-07Feb-07Mar-07Apr-07May-07Jun-07Jul-07Aug-07Sep-07Oct-07Nov-07Dec-07Jan-08Feb-08Mar-08Apr-08May-08Jun-08Jul-08Aug-08Sep-08Oct-08Nov-08Dec-08Jan-09Feb-09Mar-09Apr-09May-09Jun-09Jul-09Aug-09Sep-09Oct-09Nov-09Dec-09Jan-090

20

40

60

80

100

120

140

2,300

2,400

2,500

2,600

2,700

2,800

$/bbl million bbl

Oil price [L scale]

OECD stocks [R]

Source: IEA and DECPG Commodities Group.

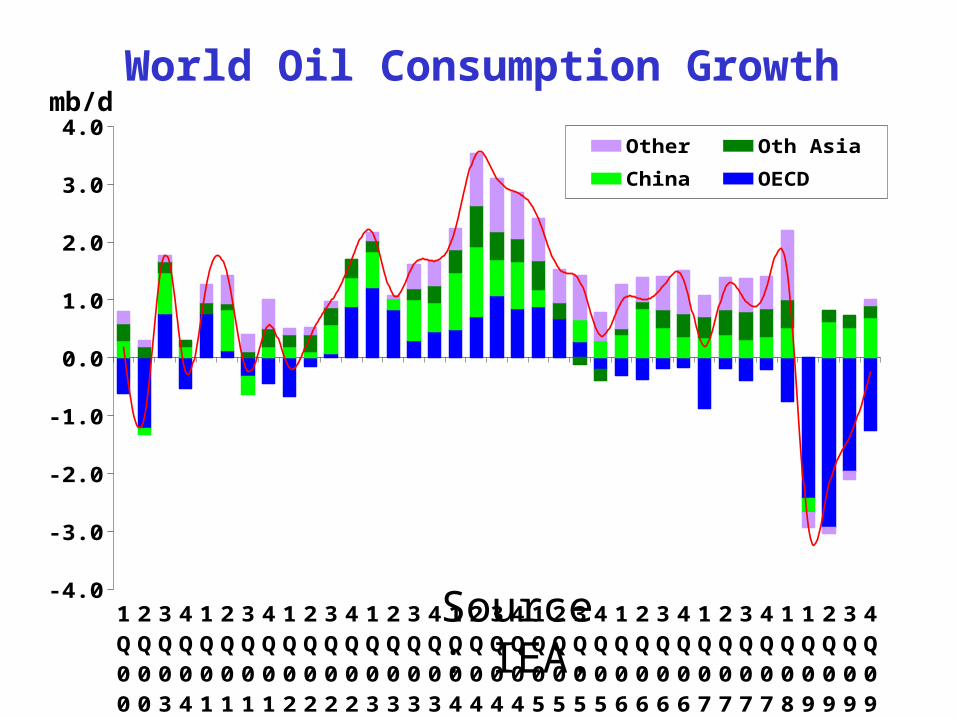

World Oil Consumption Growth

1Q00

2Q00

3Q03

4Q04

1Q01

2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

1Q09

2Q09

3Q09

4Q09

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0Other Oth Asia China

OECD TOTAL

mb/d

Source: IEA.

OPEC Spare Capacity (mb/d)

Jan-01Feb-01Mar-01Apr-01May-01Jun-01Jul-01Aug-01Sep-01Oct-01Nov-01Dec-01Jan-02Feb-02Mar-02Apr-02May-02Jun-02Jul-02Aug-02Sep-02Oct-02Nov-02Dec-02Jan-03Feb-03Mar-03Apr-03May-03Jun-03Jul-03Aug-03Sep-03Oct-03Nov-03Dec-03Jan-04Feb-04Mar-04Apr-04May-04Jun-04Jul-04Aug-04Sep-04Oct-04Nov-04Dec-04Jan-05Feb-05Mar-05Apr-05May-05Jun-05Jul-05Aug-05Sep-05Oct-05Nov-05Dec-05Jan-06Feb-06Mar-06Apr-06May-06Jun-06Jul-06Aug-06Sep-06Oct-06Nov-06Dec-06Jan-07Feb-07Mar-07Apr-07May-07Jun-07Jul-07Aug-07Sep-07Oct-07Nov-07Dec-07Jan-08Feb-08Mar-08Apr-08May-08Jun-08Jul-08Aug-08Sep-08Oct-08Nov-08Dec-08Jan-09Feb-09Mar-09Apr-09May-09Jun-09Jul-09Aug-09Sep-090

1

2

3

4

5

6

7

Source: IEA and DECPG Commodities Group.

Non-oil commodity prices

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09100

150

200

250

300

350

Grains

Fats & Oils

Other Food

Beverages

Fats & Oils, and grains off in October(2000=100)

Source: DECPG Commodities Group.

Copper stocks and prices

Jan-05Apr-0

5

Aug-05Dec-05

Apr-06

Aug-06Dec-06

Apr-07

Aug-07

Nov-07Mar-0

8Jul-0

8

Nov-08Mar-0

9Jul-0

91000

2000

3000

4000

5000

6000

7000

8000

9000

0

100

200

300

400

500

600

$/ton ‘000 tons

Copper price

LME stocks

Source: LME and DECPG Commodities Group.

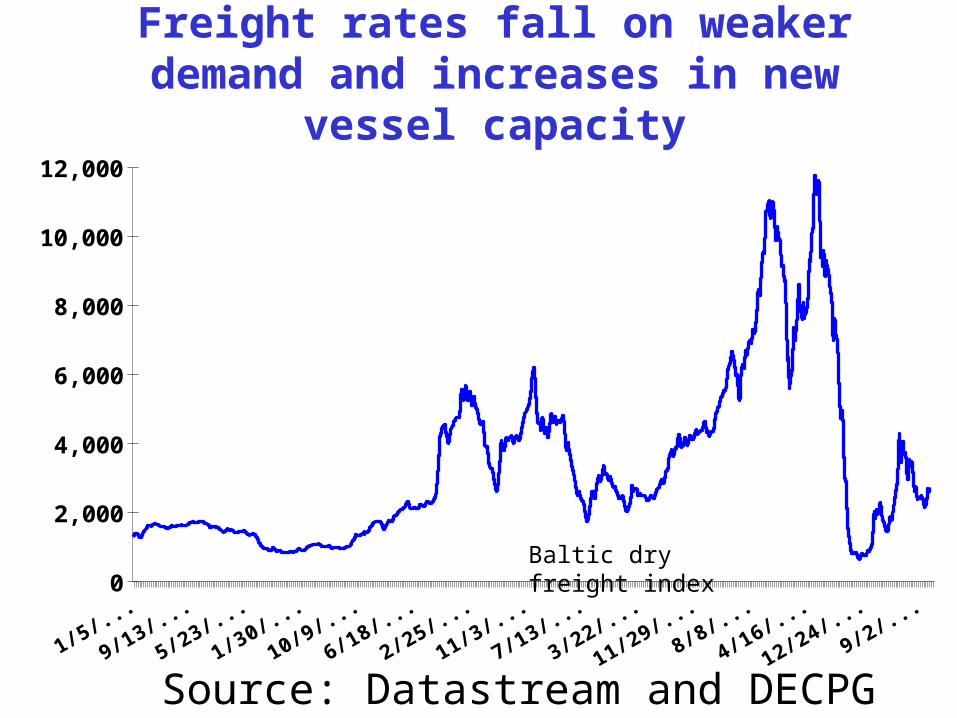

Freight rates fall on weaker demand and increases in new vessel capacity

Jan-00

Aug-00Feb-01

Sep-01Apr-0

2

Nov-02Jun-03

Jan-04

Aug-04Mar-0

5Oct-0

5

May-06

Nov-06Jun-07

Jan-08

Aug-08Mar-0

9Oct-0

90

2,000

4,000

6,000

8,000

10,000

12,000

Baltic dry freight index

Source: Datastream and DECPG Commodities Group.

International Finance

A substantial pickup in flows in September

Source: DECPG Finance Team.

Gross capital flows to developing countries

$ billion 2007

Total H1 Q3 Jan-Sep Total H1 Q3 Aug Sep Jan-Sep

Total 652 258 82 340 390 110 97 14 42 207

Bonds 146 53 9 62 65 36 37 4 13 73

Banks 312 151 63 214 257 40 22 6 9 63

Equity 194 54 10 64 68 33 38 4 21 71

Lat. America 156 61 18 80 90 37 32 1 15 69

Bonds 45 17 1 18 20 15 21 1 11 36

E. Europe 247 99 35 134 157 22 25 3 8 47

Bonds 64 27 7 35 35 13 11 1 1 24

Asia 188 69 18 88 98 44 32 6 15 76

Bonds 23 7 0 7 7 6 3 1 1 9

Others 61 28 11 38 45 7 8 2 4 15

2008 2009

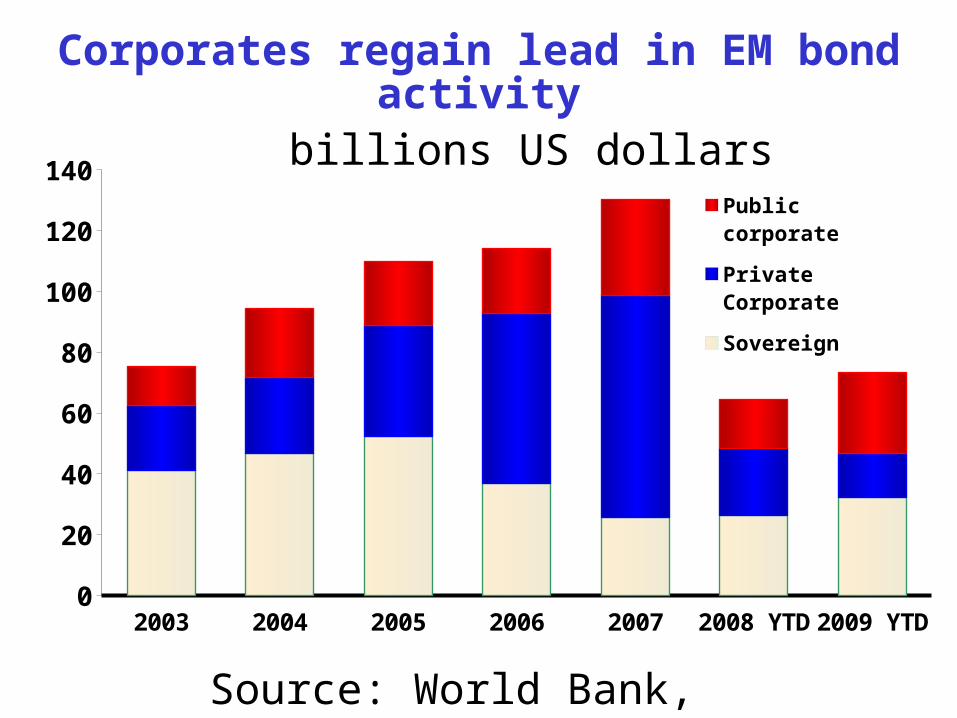

2003 2004 2005 2006 2007 2008 YTD 2009 YTD0

20

40

60

80

100

120

140Public cor-porate

Private Cor-porate

Sovereign

Corporates regain lead in EM bond activity billions US dollars

Source: World Bank, DEC Prospects Group

EM IPO activity regains momentum

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-090

1000

2000

3000

4000

5000

6000

7000

8000

0

5

10

15

20

25

30

Source: DECPG, Finance Team.

Capital raised [Bars, left]

Number of deals [Line, right]

Currencies

Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-091.230

1.270

1.310

1.350

1.390

1.430

1.470

1.510

1.550

1.590

1.630 86

90

94

98

102

106

110

Source: Thomson/Datastream.

yen/USD

USD/Euro (inverse)

Dollar’s fall picks up in September and October

USD per Euro (inverse) [Left] and Yen per USD [right]

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-0975

80

85

90

95

100

Source: JPMorgan-Chase.

Nominal effective rate [NEER]

Dollar declines imply a return to pre-crisis levels of the effective exchange rate

Indices, 2000=100.

Real effective rate [REER]

Neer 87.1Neer 85.5

The External Environment for Developing Countries

October 2009The World Bank

Development EconomicsProspects Group

Recommended