The development of IFRS and its application, controversy and prospects in the EU and

the UK

Beijing22 January 2008

2

Isobel Sharp

President, The Institute of Chartered Accountants of Scotland

Member, IASB Working Group

Member, UK Accounting Standards Board 2000 – 2005

Author, Various IFRS Financial Statements textbooks

3

The development of IFRS

• International Acounting Standards Committee established in 1973

• New International Accounting Standards Board established in 2001

• IFRS accepted or required in 111 countries

• Expected to rise to 150 countries by 2011

4

IFRS application

5

IFRS application

• Asia – China leading the way

• Japan, India, South Korea

• Americas- Canada 2011- Brazil 2010- USA?

• Global single set of high quality accounting standards

6

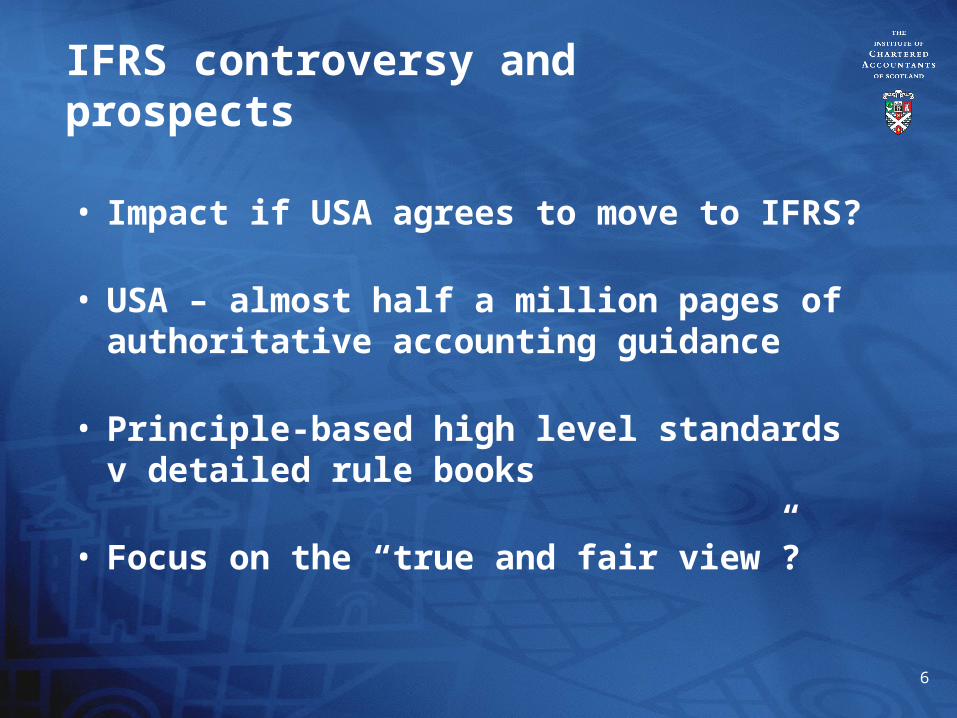

IFRS controversy and prospects

• Impact if USA agrees to move to IFRS?

• USA – almost half a million pages of authoritative accounting guidance

• Principle-based high level standards v detailed rule books

• Focus on the “true and fair view”?

7

IFRS controversy in Europe

• Complicated approval process in Europe

• Political pressure

• Delaying approval of new IFRSs

8

IFRS controversy in Europe

Two routes

EC RegulationNo 1606/2001

National GAAP

Required for consolidated financial statements for

listed securities companies

Based on EU 4th and 7th Company Law Directives –

subject to change via Directives

National jurisdictions could require/allow others (single companies or consolidated)

to move to IFRS

National jurisdictions may wish to move to IFRS over

time

9

IFRS volunteers – single companies

10

IFRS banned for single companies

11

IFRS don’t knows

12

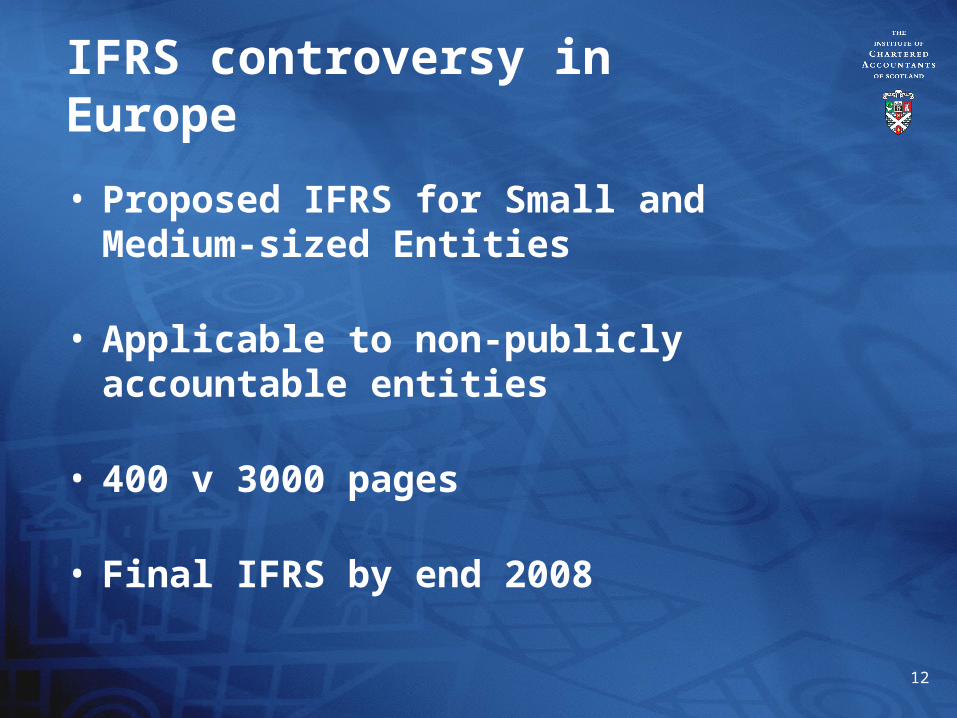

IFRS controversy in Europe

• Proposed IFRS for Small and Medium-sized Entities

• Applicable to non-publicly accountable entities

• 400 v 3000 pages

• Final IFRS by end 2008

13

IFRS prospects

• Great success so far

• Asia extremely important, with Europe divided and USA coming in

• ICAS very excited about co-operation with CICPA

The development of IFRS and its application, controversy and prospects in the EU and

the UK

Beijing22 January 2008

Recommended