oneonone2017.efghermes.Com

We are proud to welcome you to the region’s premier investor event, the One on One conference. As we organize the most successful MENA investor conference for the 13th year – while simultaneously expanding into new markets and launching new products – we turn our focus towards unlocking new opportunities amidst a rapidly-changing economic environment on both a regional and global scale, with an

Welcome to the 13th Annual One on One Conference emphasis on the vast potential we see in frontier markets. Over the years, the One on One conference has established itself as the region’s most valuable investor platform matching equity investors with high-level executives and industry professionals in an engaging format, aiming to identify and facilitate new investment opportunities throughout shifting economic patterns in an emergent region.

The 13th Annual One On One Conference

the pulseof mena & frontier markets

atlantis, The Palm, Dubai, Uae | 6-8 march 2017

The 13th annual one on one Conference • 1

oneonone2017.efghermes.Com

Regional Outlook C O N T I N U E D > >

2017 will be a challenging year for emerging and frontier markets. Brexit and the election of Donald Trump mean that protectionism is a rising risk to EM growth. Rising growth expectations in the US have driven bond yields and the dollar higher, and capital is likely to flow out of emerging markets after strong inflows in 2016. However, we believe several factors will support selected emerging markets. The first is

internal; reforming economies, particularly smaller ones, will be able to win a bigger piece of EM-dedicated investment and, potentially, trade. The second is external; investment-heavy fiscal expansion in the US can potentially drive greater demand for industrial commodities, supporting export growth in certain emerging markets.

EgyptThe float of the Egyptian Pound was a step in the right direction for Egypt. Despite short-term inflationary pressures and higher interest rates, the free float will unleash the full potential of the Egyptian market and economy. We believe the float will lead to strong Foreign Portfolio Flows (FPIs) and Foreign Direct Investments (FDIs) which will improve FX currency in circulation and help the Egyptian economy and Egyptian companies grow at a much faster rate than seen since 2011.

UAEA stronger economic outlook than GCC peers is likely to continue as the country enjoys a diversified economy and capital inflows. Low pressure on fiscal balances will allow Abu Dhabi to reverse its fiscal retrenchment in 2017, leading to accelerated economic growth. In parallel, Dubai is continuing with an expansionary fiscal budget as it continues to boost investments ahead of the Dubai Expo in 2020.

The 13th annual one on one Conference • 2

oneonone2017.efghermes.Com

QatarGovernment is expected to continue spending on infrastructure projects, especially those linked to World Cup 2022 and Qatar vision 2030. Qatar benefits from a low budget breakeven oil price, but further pressure on gas prices is a risk, especially as global LNG supply picks up.

OmanThe Sultanate is expected to see slow GDP growth continuing in 2017, on the back of ongoing austerity measures. Low oil prices indicate that the budget deficit will continue at high levels in the near future, given the high budget breakeven for Oman (2nd highest in the GCC after Bahrain).

Regional Outlook C O N T I N U E D > >

KSA2017 may see some recovery in growth after a difficult 2016 for the Kingdom, but fiscal retrenchment remains an important theme given the limited recovery in oil prices in 2016. MSCI EM status will be an important driver of investor interest in KSA.

BahrainBahrain’s economic growth is expected to slow to 2% in 2016 and 1.7% in 2017 on the back of continued austerity measures that will further hit consumption. Domestic political unrest and escalating regional risks are a drag on growth and investor confidence, though the former has eased since 2011. Bahrain’s ease of doing business ratings are the highest of the GCC countries.

The 13th annual one on one Conference • 3

oneonone2017.efghermes.Com

Regional Outlook C O N T I N U E D > >

KuwaitHaving the lowest break-even oil price amongst the GCC countries, Kuwait’s macro stability is supported by low deficits and very high levels of foreign assets. Economic activity is picking up as the government’s investment program is finally gaining pace from a low base. Parliamentary elections planned for late 2016 are a key development for the continuation of political stability.

MoroccoThe Moroccan economy remains vulnerable to shifts in agriculture, though activity could pick up slightly in 2017. Non-agricultural activity is expected to remain at 3%. Morocco is expected to move towards a flexible FX regime in 2017.

IraqIraq is subject to critical challenges: oil production has increased while oil prices remain relatively low. The government is recovering territory from ISIS, but the campaign is increasing tensions between major political groups. Macroeconomic stability remains in question, in light of the recent shrinking of non-oil revenues.

JordanEconomic growth is likely to remain at around the 3%-mark as regional political instability continues to weigh on economic activity. The government recently renewed its Stand-By Agreement with the IMF, providing a cushion against external shock. In addition, foreign reserves remain at a comfortable level. Fiscal deficits have been reduced to low single digits as share of GDP, but the country remains dependent on foreign grants to fund its deficit.

The 13th annual one on one Conference • 4

oneonone2017.efghermes.Com

Regional Outlook C O N T I N U E D > >

LebanonThe macro-economic outlook has improved in the light of the recent resolution of the political deadlock. This has started to boost investor confidence, though things are still at an early stage. A lasting recovery in sentiment and boost to GDP growth in Lebanon is still dependent on Syria’s conflict resolution.

PakistanPakistan’s economy should continue to grow at a rate above 5% in 2017 as the country benefits from improvements in security, rising FDI (notably the China-Pakistan Economic Corridor) and relatively low oil prices. Low inflation and the lead-up to elections in 1H2018 will also be favorable for growth, while the pending MSCI EM upgrade (set for May 2017) should have a positive impact on stock market performance.

ZimbabweThe outlook for Zimbabwe’s economy is poor. The agricultural economy shrank last year and a financial crisis, caused by ongoing arrear payments to state-owned enterprises, continues. The economy requires a strong reduction in the public wage bill (which accounts for 70% of total expenditures) in order to avoid further accumulation of public debt.

UgandaThe IMF trimmed growth expectations for Uganda to 5% in FY16/17 and the central bank has gradually cut interest rates by 400 basis points in 2016 to support economic growth momentum.

The 13th annual one on one Conference • 5

oneonone2017.efghermes.Com

Regional Outlook C O N T I N U E D > >

KenyaGDP growth in 1H2016 came in at 6.2% from 5.6% last year, according to the IMF. The Kenyan economy has benefited from low oil prices, a general improvement in all sectors, namely agriculture, and an uptick in tourism on the back of improved security. The recent government decision to cap interest rates at 4% above the Central Bank of Kenya increased risk on overall growth through its effect on private sector credit.

BangladeshGrowth should continue at roughly 6% in 2017. Large external funding for infrastructure projects in Bangladesh has been received from China, along with commitment from the Asian Development Bank and the World Bank to increase funding. Bangladesh’s exports remain strong in the textile sector; however, the economy will continue to face increased pressures from falling remittances from the Gulf states (which account for half of total remittances) and a high public wage bill.

Sri LankaSri Lanka has received approval for an IMF facility worth USD 1.5 billion over 36 months, which should allow the economy to grow at a rate above 5%. However, Sri Lanka needs to improve export competitiveness, widen the tax base, and work towards effective public management restructuring to ensure healthy medium-term growth.

GhanaGrowth in Ghana should recover in 2017 and 2018 as problems in the oil sector are resolved. Relatively stable currency and tight monetary policy have helped contain inflation, which – along with favorable external balance and FDI inflows - should support growth going forward and help contain a prevailing high domestic financing cost. Problems in the oil sector, weak commodity prices, and fiscal challenges are all concerns ahead of December elections.

The 13th annual one on one Conference • 6

oneonone2017.efghermes.Com

ZambiaZambia’s GDP growth is expected remain at around 3% in 2016 and below 4% in 2017, down from 4.9% in 2014, with China’s economic slowdown and falling FDI dragging on growth. Further subsidy cuts, high inflation, persistent power shortages, and poor harvests are downside risks to growth.

Regional Outlook C O N T I N U E D > >

MauritiusThe economy in Mauritius is estimated to grow at above 3.5% in 2016, driven by a modest recovery in investment especially in the industrial sector. Inflation is to remain contained given limited imported price shocks. Growth is expected to slow down in 2017 and 2018 as more interventionist policies adopted by the government are set to be implemented, expected to weigh negatively on economic activity and place further pressure inequality.

RwandaGDP growth in Rwanda is expected to remain robust, driven by foreign and public investment, services, exports, and political stability. Private investment, which is largely informal, will continue to face major constraints, including poor infrastructure and lack of access to electricity. The government’s ability to implement its investment plans as part of Vision 2020 will be limited by weak domestic revenue collection and uncertain foreign aid inflows (30-40% of the budget).

BotswanaDiamond-rich Botswana’s economy is expected to rebound to 3.5% in 2016 and 4.1% in 2017, mostly driven by growth in the mining sector (assuming stable demand from advanced economies). State revenue will remain low as it relies on two volatile sources - minerals (40%) and Southern African Customs Union (SACU) inflows (25%, likely to remain soft on weaker South African growth), but spending will continue to grow as part of as part of the Economic Stimulus Program.

The 13th annual one on one Conference • 7

oneonone2017.efghermes.Com

TanzaniaExpansionary fiscal policy is likely to support strong economic activity in the medium-term as the government focuses on infrastructure development. Growth is therefore likely to remain above 5%. Risks to the outlook include lower donor support and widening twin deficits on the back of the strong fiscal expansion.

Regional Outlook

NigeriaForeign exchange shortages are likely to weigh further on economic activity following this year’s contraction - the first in over ten years. The widening gap between the parallel and official rates hints to no near-term resolution to FX shortages. Inflation, running at double-digits and reaching multi-year highs, is eroding real incomes, further depressing economic activity. On a positive note, restored security is allowing the government to increase oil production, which might help ease shortages.

The 13th annual one on one Conference • 8

oneonone2017.efghermes.Com

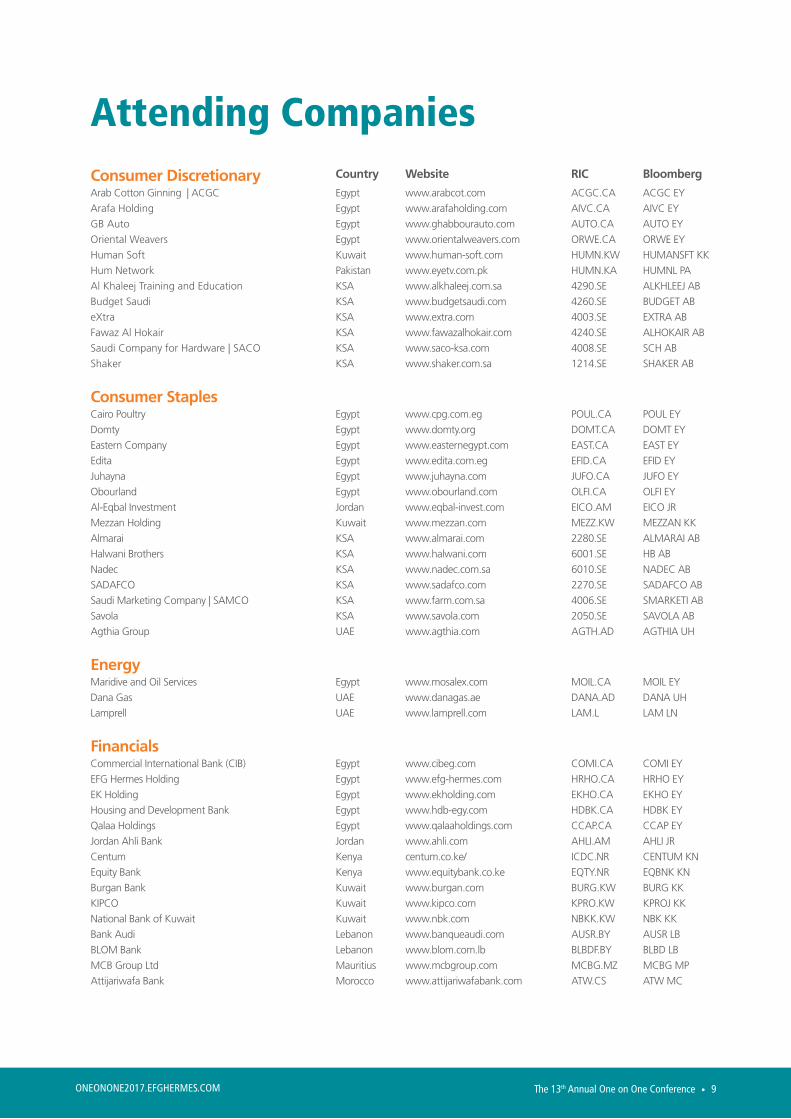

Attending CompaniesConsumer Discretionary Country Website RIC Bloomberg

Arab Cotton Ginning | ACGC Egypt www.arabcot.com ACGC.CA ACGC EY

Arafa Holding Egypt www.arafaholding.com AIVC.CA AIVC EY

GB Auto Egypt www.ghabbourauto.com AUTO.CA AUTO EY

Oriental Weavers Egypt www.orientalweavers.com ORWE.CA ORWE EY

Human Soft Kuwait www.human-soft.com HUMN.KW HUMANSFT KK

Hum Network Pakistan www.eyetv.com.pk HUMN.KA HUMNL PA

Al Khaleej Training and Education KSA www.alkhaleej.com.sa 4290.SE ALKHLEEJ AB

Budget Saudi KSA www.budgetsaudi.com 4260.SE BUDGET AB

eXtra KSA www.extra.com 4003.SE EXTRA AB

Fawaz Al Hokair KSA www.fawazalhokair.com 4240.SE ALHOKAIR AB

Saudi Company for Hardware | SACO KSA www.saco-ksa.com 4008.SE SCH AB

Shaker KSA www.shaker.com.sa 1214.SE SHAKER AB

Consumer StaplesCairo Poultry Egypt www.cpg.com.eg POUL.CA POUL EY

Domty Egypt www.domty.org DOMT.CA DOMT EY

Eastern Company Egypt www.easternegypt.com EAST.CA EAST EY

Edita Egypt www.edita.com.eg EFID.CA EFID EY

Juhayna Egypt www.juhayna.com JUFO.CA JUFO EY

Obourland Egypt www.obourland.com OLFI.CA OLFI EY

Al-Eqbal Investment Jordan www.eqbal-invest.com EICO.AM EICO JR

Mezzan Holding Kuwait www.mezzan.com MEZZ.KW MEZZAN KK

Almarai KSA www.almarai.com 2280.SE ALMARAI AB

Halwani Brothers KSA www.halwani.com 6001.SE HB AB

Nadec KSA www.nadec.com.sa 6010.SE NADEC AB

SADAFCO KSA www.sadafco.com 2270.SE SADAFCO AB

Saudi Marketing Company | SAMCO KSA www.farm.com.sa 4006.SE SMARKETI AB

Savola KSA www.savola.com 2050.SE SAVOLA AB

Agthia Group UAE www.agthia.com AGTH.AD AGTHIA UH

EnergyMaridive and Oil Services Egypt www.mosalex.com MOIL.CA MOIL EY

Dana Gas UAE www.danagas.ae DANA.AD DANA UH

Lamprell UAE www.lamprell.com LAM.L LAM LN

FinancialsCommercial International Bank (CIB) Egypt www.cibeg.com COMI.CA COMI EY

EFG Hermes Holding Egypt www.efg-hermes.com HRHO.CA HRHO EY

EK Holding Egypt www.ekholding.com EKHO.CA EKHO EY

Housing and Development Bank Egypt www.hdb-egy.com HDBK.CA HDBK EY

Qalaa Holdings Egypt www.qalaaholdings.com CCAP.CA CCAP EY

Jordan Ahli Bank Jordan www.ahli.com AHLI.AM AHLI JR

Centum Kenya centum.co.ke/ ICDC.NR CENTUM KN

Equity Bank Kenya www.equitybank.co.ke EQTY.NR EQBNK KN

Burgan Bank Kuwait www.burgan.com BURG.KW BURG KK

KIPCO Kuwait www.kipco.com KPRO.KW KPROJ KK

National Bank of Kuwait Kuwait www.nbk.com NBKK.KW NBK KK

Bank Audi Lebanon www.banqueaudi.com AUSR.BY AUSR LB

BLOM Bank Lebanon www.blom.com.lb BLBDF.BY BLBD LB

MCB Group Ltd Mauritius www.mcbgroup.com MCBG.MZ MCBG MP

Attijariwafa Bank Morocco www.attijariwafabank.com ATW.CS ATW MC

The 13th annual one on one Conference • 9

oneonone2017.efghermes.Com

Financials (cont’d)Bank Muscat Oman www.bankmuscat.com BMAO.OM BKMB OM

National Bank of Oman Oman www.nbo.co.om NBO.OM NBOB OM

Bank Alfalah Limited Pakistan www.bankalfalah.com BAFL.KA BAFL PA

MCB Bank Limited Pakistan www.mcb.com.pk MCBBI.PK MCB PA

Pakistan Stock Exchange Pakistan www.psx.com.pk N/A EPRX PA

Qatar National Bank Qatar www.qnb.com.qa QNBK.QA QNBK QD

Alawwal Bank KSA www.shb.com.sa 1040.SE ALAWWAL AB

Bupa KSA www.bupa.com.sa 8210.SE BUPA AB

Stanbic Bank Uganda Uganda WWW.STANBICBANK.CO.UG SBU.UG SBU UG

Abu Dhabi Islamic Bank UAE www.adib.ae ADIB.AD ADIB UH

Afkar Capital UAE ETF UAE afkarcapital.com UAETF.DU UAETF UH

Amanat Holdings UAE www.amanat.ae AMANT.DU AMANAT UH

Dubai Financial Market |DFM UAE www.dfm.ae DFM.DU DFM UH

Dubai Islamic Bank UAE www.dib.ae DISB.DU DIB UH

Emirates NBD UAE www.emiratesnbd.com ENBD.DU EMIRATES UH

FGB - NBAD Group Meeting UAE N/A N/A N/A

First Gulf Bank UAE www.fgb.ae FGB.AD FGB UH

Mashreq Bank UAE www.mashreqbank.com/uae/en/ MASB.DU MASQ UH

National Bank of Abu Dhabi UAE www.nbad.com NBAD.AD NBAD UH

RAK Bank UAE www.rakbank.ae RAKB.AD RAKBANK UH

Union National Bank UAE www.unb.co.ae UNB.AD UNB UH

Waha Capital UAE www.wahacapital.ae WAHA.AD WAHA UH

Health CareCleopatra Hospitals Egypt www.cleopatrahospital.com CLHO.CA CLHO EY

EIPICO Egypt www.eipico.com.eg PHAR.CA PHAR EY

Integrated Diagnostics Holdings (IDH) Egypt www.idhcorp.com IDHC.L IDHC LN

Dar Al Dawa Jordan www.dadgroup.com DADI.AM DADI JR

Al Hammadi Company for Development & Investment KSA www.alhammadi.com 4007.SE ALHAMMAD AB

Dallah Healthcare KSA www.dallahhealth.com 4004.SE DALLAH AB

Index Providers

FTSE Russell MENA & Frontier

www.ftserussell.com N/A N/A

MSCI MENA & Frontier

www.msci.com N/A N/A

IndustrialsElsewedy Electric Egypt www.elsewedyelectric.com SWDY.CA SWDY EY

Lecico Egypt Egypt www.lecicoegypt.com LCSW.CA LCSW EY

Orascom Construction Limited Egypt www.orascom.com ORAS.CA ORAS EY

Mannai Corporation Qatar www.mannai.com MCCS.QA MCCS QD

Bawan Company KSA www.bawan.com.sa 1302.SE BAWAN AB

Saudi Ceramics KSA www.saudiceramics.com 2040.SE SCERCO AB

Saudi Industrial Services Company | SISCO KSA www.sisco.com.sa 2190.SE SISCO AB

Air Arabia (TBC) UAE www.airarabia.com AIRA.DU AIRARABI UH

Aramex UAE www.aramex.com ARMX.DU ARMX UH

DP World UAE www.dpworld.com DPW.DI DPW DU

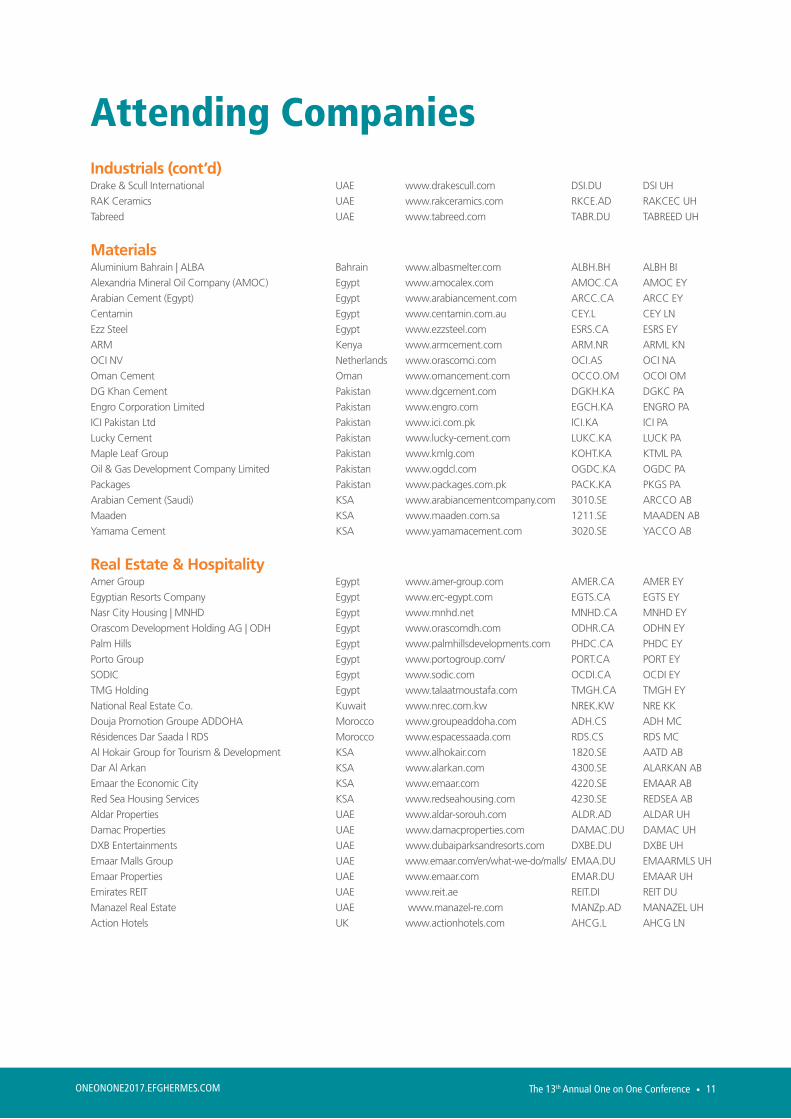

Attending Companies

The 13th annual one on one Conference • 10

oneonone2017.efghermes.Com

Industrials (cont’d)Drake & Scull International UAE www.drakescull.com DSI.DU DSI UH

RAK Ceramics UAE www.rakceramics.com RKCE.AD RAKCEC UH

Tabreed UAE www.tabreed.com TABR.DU TABREED UH

MaterialsAluminium Bahrain | ALBA Bahrain www.albasmelter.com ALBH.BH ALBH BI

Alexandria Mineral Oil Company (AMOC) Egypt www.amocalex.com AMOC.CA AMOC EY

Arabian Cement (Egypt) Egypt www.arabiancement.com ARCC.CA ARCC EY

Centamin Egypt www.centamin.com.au CEY.L CEY LN

Ezz Steel Egypt www.ezzsteel.com ESRS.CA ESRS EY

ARM Kenya www.armcement.com ARM.NR ARML KN

OCI NV Netherlands www.orascomci.com OCI.AS OCI NA

Oman Cement Oman www.omancement.com OCCO.OM OCOI OM

DG Khan Cement Pakistan www.dgcement.com DGKH.KA DGKC PA

Engro Corporation Limited Pakistan www.engro.com EGCH.KA ENGRO PA

ICI Pakistan Ltd Pakistan www.ici.com.pk ICI.KA ICI PA

Lucky Cement Pakistan www.lucky-cement.com LUKC.KA LUCK PA

Maple Leaf Group Pakistan www.kmlg.com KOHT.KA KTML PA

Oil & Gas Development Company Limited Pakistan www.ogdcl.com OGDC.KA OGDC PA

Packages Pakistan www.packages.com.pk PACK.KA PKGS PA

Arabian Cement (Saudi) KSA www.arabiancementcompany.com 3010.SE ARCCO AB

Maaden KSA www.maaden.com.sa 1211.SE MAADEN AB

Yamama Cement KSA www.yamamacement.com 3020.SE YACCO AB

Real Estate & HospitalityAmer Group Egypt www.amer-group.com AMER.CA AMER EY

Egyptian Resorts Company Egypt www.erc-egypt.com EGTS.CA EGTS EY

Nasr City Housing | MNHD Egypt www.mnhd.net MNHD.CA MNHD EY

Orascom Development Holding AG | ODH Egypt www.orascomdh.com ODHR.CA ODHN EY

Palm Hills Egypt www.palmhillsdevelopments.com PHDC.CA PHDC EY

Porto Group Egypt www.portogroup.com/ PORT.CA PORT EY

SODIC Egypt www.sodic.com OCDI.CA OCDI EY

TMG Holding Egypt www.talaatmoustafa.com TMGH.CA TMGH EY

National Real Estate Co. Kuwait www.nrec.com.kw NREK.KW NRE KK

Douja Promotion Groupe ADDOHA Morocco www.groupeaddoha.com ADH.CS ADH MC

Résidences Dar Saada l RDS Morocco www.espacessaada.com RDS.CS RDS MC

Al Hokair Group for Tourism & Development KSA www.alhokair.com 1820.SE AATD AB

Dar Al Arkan KSA www.alarkan.com 4300.SE ALARKAN AB

Emaar the Economic City KSA www.emaar.com 4220.SE EMAAR AB

Red Sea Housing Services KSA www.redseahousing.com 4230.SE REDSEA AB

Aldar Properties UAE www.aldar-sorouh.com ALDR.AD ALDAR UH

Damac Properties UAE www.damacproperties.com DAMAC.DU DAMAC UH

DXB Entertainments UAE www.dubaiparksandresorts.com DXBE.DU DXBE UH

Emaar Malls Group UAE www.emaar.com/en/what-we-do/malls/ EMAA.DU EMAARMLS UH

Emaar Properties UAE www.emaar.com EMAR.DU EMAAR UH

Emirates REIT UAE www.reit.ae REIT.DI REIT DU

Manazel Real Estate UAE www.manazel-re.com MANZp.AD MANAZEL UH

Action Hotels UK www.actionhotels.com AHCG.L AHCG LN

Attending Companies

The 13th annual one on one Conference • 11

oneonone2017.efghermes.Com

ResearchEFG Hermes Research - Banking MENA Region N/A N/A N/A

EFG Hermes Research - Consumer & Retail MENA Region N/A N/A N/A

EFG Hermes Research - Macro & Strategy MENA Region N/A N/A N/A

EFG Hermes Research-Chemicals MENA Region N/A N/A N/A

EFG Hermes Research-General Industries and Healthcare MENA Region N/A N/A N/A

EFG Hermes Research-Real Estate & Construction MENA Region N/A N/A N/A

EFG Hermes Research-Telecoms MENA Region N/A N/A N/A

Telecommunication ServicesGlobal Telecom Egypt www.otelecom.com GLTDq.L GLTD LI

Safaricom Kenya www.safaricom.co.ke SCOM.NR SAFCOM KN

Viva Kuwait Telecommunications Kuwait www.viva.com.kw VIVA.KW VIVA KK

Maroc Télécom Morocco www.iam.ma IAM.CS IAM MC

Omantel Oman www.omantel.om OTL.OM OTEL OM

Ooredoo Oman Oman www.ooredoo.om ORDS.OM ORDS OM

Ooredoo Group Qatar www.ooredoo.qa ORDS.QA ORDS QD

Saudi Telecom KSA www.stc.com.sa 7010.SE STC AB

Zain KSA KSA www.sa.zain.com 7030.SE ZAINKSA AB

Attending Companies

The 13th annual one on one Conference • 12

oneonone2017.efghermes.Com

Venue: DubaiThe 13th Annual One on One Conference is being held at Atlantis, The Palm, a stunning resort at the heart of the Palm Jumeirah in Dubai.

The 13th annual one on one Conference

atlantis, The Palm, Dubai, Uae

Dubai is not only an international city and the business hub of the Middle East, but also a tourist paradise, complete with world class shopping, fine dining, and iconic skyscrapers and high-rise buildings. With a strategic location between Europe and Asia, Dubai is at the center of our increasingly

global world and acts a major transport hub for passengers and cargo. The bustling Emirate has ramped up spending in preparation for hosting the World Expo 2020, with an emphasis on investments in various sectors such as real estate and renewable energy.

The 13th annual one on one Conference • 13

oneonone2017.efghermes.Com

* After the morning registration period, registration and scheduling will continue from 11:00 - 18:30 at the West Wing, Atlantis on the 8th floor, room no. 8320.

Agenda

Day

1

Day

2

Day

3

Monday, March 6th, 2017

Tuesday, March 7th, 2017

Wednesday, March 8th, 2017

07:00-09:00 Standing Breakfast and Registration* [Atlantis Ballroom Foyer, West Wing, Atlantis]

09:00-11:00 Main Session [Atlantis Ballroom, Atlantis]

11:00-12:50 One on One Meetings [7th, 8th & 9th Floor, West Wing, Atlantis]

13:00-14:30 Lunch [Saffron Restaurant, Atlantis]

14:30-18:20 One on One Meetings [7th, 8th & 9th Floor, West Wing, Atlantis]

20:30-23:30 Gala Dinner [Venue TBC]

08:00-19:00 Registration & Scheduling [8th Floor, Room No. 8320, West Wing, Atlantis]

08:30-12:20 One on One Meetings [7th, 8th & 9th Floor, West Wing, Atlantis]

12:30-14:00 Lunch [Saffron Restaurant, Atlantis]

14:05-19:00 One on One Meetings [7th, 8th & 9th Floor, West Wing, Atlantis]

08:00-19:00 Registration & Scheduling [8th Floor, Room No. 8320, West Wing, Atlantis]

08:30-12:20 One on One Meetings [7th, 8th & 9th Floor, West Wing, Atlantis]

12:30-14:00 Lunch [Saffron Restaurant, Atlantis]

14:05-19:00 One on One Meetings [7th, 8th & 9th Floor, West Wing, Atlantis]

** Above agenda is subject to change

The 13th annual one on one Conference • 14

oneonone2017.efghermes.Com

Accommodation Guests are kindly requested to book their own rooms at a special EFG Hermes conference rate at the Atlantis, The Palm Hotel. A reservation link will appear in your browser after you submit your registration for the conference. Alternatively, you may choose to book at your convenience by clicking a reservation link that will be included in your registration confirmation email.

More information about room types can be found at:http://oneonone2017.efghermes.com/

Additional ServicesAtlantis, The Palm will be responsible for the below additional services throughout the conference. Kindly consult their website or contact them for questions regarding the following: • Help obtaining visas• Airport meet and greet service• Arrangement of ground transportation• Coordination of private aircraft logistics• Arrangement of excursions

useful Information C O N T I N U E D > > VisaVisas to the UAE may be obtained through Emirate Airlines or Atlantis, The Palm hotel. For terms and conditions for obtaining the visa through the hotel, please consult this form, as well as the hotel visa application form and credit card authorization form.

Citizens of the GCC nations of Bahrain, Kuwait, Oman, Qatar and Saudi Arabia do not require a visa to travel to the UAE.

Below is a list of countries for citizens who may obtain a 30-day visit visa free of charge directly at the UAE airport:

Andorra, Australia, Austria, Belgium, Brunei, Bulgaria, Canada, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hong Kong, Hungary, Iceland, Ireland, Italy, Japan, Latvia, Liechtenstein, Lithuania, Luxembourg, Malaysia, Monaco, Netherlands, New Zealand, Norway, Poland, Portugal, Romania, San Marino, Singapore, Slovakia, Slovenia, South Korea, Spain, Sweden, Switzerland, United Kingdom, United States of America, Vatican City.

The 13th annual one on one Conference • 15

oneonone2017.efghermes.Com

ClimateThe average temperature in Dubai in March is 26 Celsius (79 Fahrenheit), with highs of 29 Celsius (84 Fahrenheit) and lows of 23 (73 Fahrenheit) in the evenings. Precipitation is rare.

Time ZoneDubai is four hours ahead of Greenwich Mean Time.

Dress CodeFormal business attire is appropriate throughout the conference. A light sweater or jacket may be appropriate in the evening when the weather is cooler.

LanguageThe official language of the meetings is English.

Contact InformationEmail: [email protected] Website: https://oneonone2017.efghermes.com

Important DeadlinesRegistration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 02 February 2017Flight information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 02 February 2017High resolution logo (presenting companies) . . . . . . . . . . . . . . . . . . . . . . . . . 02 February 2017A/V Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 02 February 2017Presentation (presenting companies) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 February 2017Shipping Form (presenting companies) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 February 2017

useful Information

The 13th annual one on one Conference • 16

Recommended

![khaleej times - ACMA Times... · 2019. 4. 25. · khaleej times Tuesday, May 1, 2018 [1422635] Created Date: 5/1/2018 10:49:34 AM](https://img.pdfslide.us/doc/110x75/60dcd0572eae9f77be4736d8/khaleej-times-acma-times-2019-4-25-khaleej-times-tuesday-may-1-2018.jpg)