Thailand Country Profile

Business Process Outsourcing (BPO)

Information Technology Outsourcing (ITO)

for

Submission on

CBI KPO program 2014-2020

The Centre for the Promotion of Imports from developing countries (CBI)

The Netherlands

Conducted by

Software Park Thailand

under

National Science and Technology Development Agency (NSTDA)

Table of Content

Topics Page

1

Introduction

Description of Characteristic of BPO 3

Description of Characteristic of ITO 3

Key Strength and Weakness 7

Government support regarding to BPO and ITO 9

IT and BPO industry development strategies and initiatives 11

Quality of certification and support for IT and BPO industry 13

Key Stakeholders of BPO and ITO industry 13

Key bottlenecks for export development of the BPO and ITO industry 16

The most important Export markets for ITO and BPO products and services 16

Number of exporting companies in the ITO and BPO industry 16

Country Profile Thailand for CBI KPO services

1.IntroductionToday the economics crisis forces many business to seek the effective method to reduce cost and enhance the

internal operations. The concept of global Business Process Outsourcing (BPO) and Information Technology

Outsourcing (ITO) has been growing since decade. Many Business concerns the budget of IT investment in order

to reach cost optimization while delivering paradigm for the best services.

Over few years, Thailand has proven as the international reputation on BPO and ITO as the center of excellence

to conduct the world class software outsourcing. The software industry gains the strong complementary

elements: a centric manufacturing of international software leading companies that align the global market

leaders and numerously indigenous companies who achieve the significant global market success. Thai software

has been recognized internationally as being dynamic, highly innovative, technically expert and international

standard adept.

Since 2008 to 2010 Thailand has been ranked as the Top 30 global destination for IT outsourcing by Gartner. Thai

Software Industry today comprises over 1,900 companies, employing over 100,000 people, with combines sales

growth 17.2% The vast majority of software activities are exported, so that the number of software exporting

last year achieved USD 14 billion (2010). (annual report Ministry of ICT ,2011) 1

The upcoming Asean Economic Community 2015 (AEC 2015) give the opportunity to trigger point of a

paradigm shift and integrated the economics in all Asean Regions. Thailand as the strategic location was proven

as the Hub of Asean Detroit export and manufacturing in automotive industry. Thailand is also location of hugh

foreign investment from Japan, USA, UK Germany and so on. Thailand has been recognized as one of 30 top

destination of global IT outsourcing ranked by Gartner. Some international leading software companies such as

Thomas Reuters and DSTi located the development center since 2001 to employ Thai IT professional more than

1,500 people and to deliberate quality software to global market place.

AEC 2015 will synergy platform to regional single market and production based which require removal of trade

barrier among countries (Asean + 3 countries; China, Japan and Korea) will deliver collaboration across business

sectors especially software concerned as the services will be key driver to shift the business model that

revolutionize the industrial sectors in the near future.

Why Thailand: Destination for BPO and ITO

Situated in the strategic location in Asia-Pacific region Thailand offers ranges of advantages to foreign business

firms. According to World Competitiveness Scorecared 2009 2 shows Thailand ICT statistics as 26th rank top in the

world on the domestic consumption in ICT sector represents 24 millions internet users, increasing number of 69

millions mobile users and augmented social network as a number of Facebook reached more than 13 million

users.

__________________________________________

1 The annual report Ministry of ICT Thailand ,2011

2 The World Competitiveness Scorecared ,2009 1

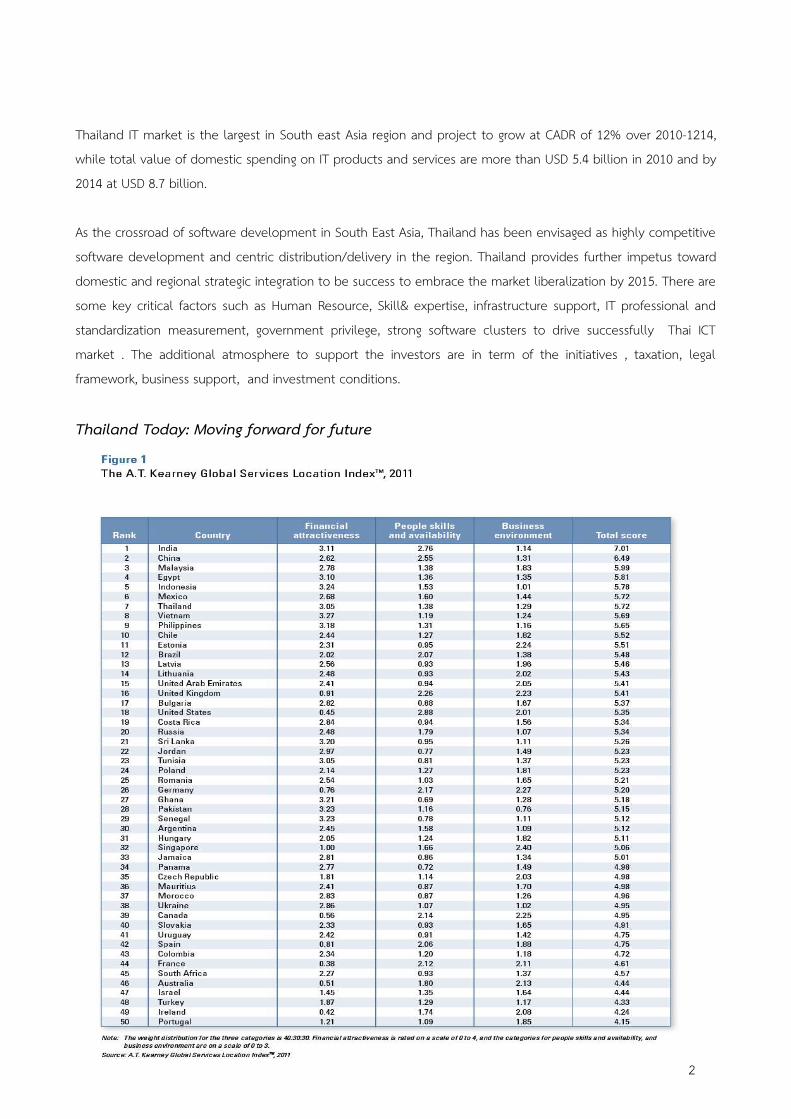

Thailand IT market is the largest in South east Asia region and project to grow at CADR of 12% over 2010-1214,

while total value of domestic spending on IT products and services are more than USD 5.4 billion in 2010 and by

2014 at USD 8.7 billion.

As the crossroad of software development in South East Asia, Thailand has been envisaged as highly competitive

software development and centric distribution/delivery in the region. Thailand provides further impetus toward

domestic and regional strategic integration to be success to embrace the market liberalization by 2015. There are

some key critical factors such as Human Resource, Skill& expertise, infrastructure support, IT professional and

standardization measurement, government privilege, strong software clusters to drive successfully Thai ICT

market . The additional atmosphere to support the investors are in term of the initiatives , taxation, legal

framework, business support, and investment conditions.

Thailand Today: Moving forward for future

2

From Kearney Global Service 3 Nowadays Thailand move to main contender of global software outsourcing

destination ranked on 7th Global service location on 2011. The attractive indicators are on the financial attraction,

people skill and business environment respectively.

2. Characteristics of BPO and ITO Thailand services

2.1 Business Process Outsourcing (BPO)

The late 20th century and the beginning of the 2nd millennium saw a huge development in the BPO sector.

Owing to the dependence of the BPO industry on information technology, IT Jobs in BPO are generally divided

into two categories, back office outsourcing and front office outsourcing. There is a stark difference between

these two categories of BPO jobs.

BPO in Thailand is not outstanding compared to ITO , mostly BPO in Thailand is in term of internal BPO such as

Human Resource, Lawyer, Accounting, Call Center, Selling, Marketing. In Thailand there are oversea companies

who looking for outsourcing services. However there are very few BPO buyers to subcontract local outsourcing in

Thailand. This cause language capabilities in specific business area.

2.2 Information Technology Outsourcing (ITO)

Gartner accredited Thailand as “10 leading locations for offshore services in Asia Pacific 2007-2011”.These are

assets to Western and Japanese investors. Like most other manufacturing industries, Thailand is gaining its

acceptance in IT services outsourcing.

Over the past decade Thailand has gradually turned to be the destination for offshore outsourcing location. For

instance, Thomas Reuter has established the Software Center since 2001 after 18-months deliberation of global

development site.

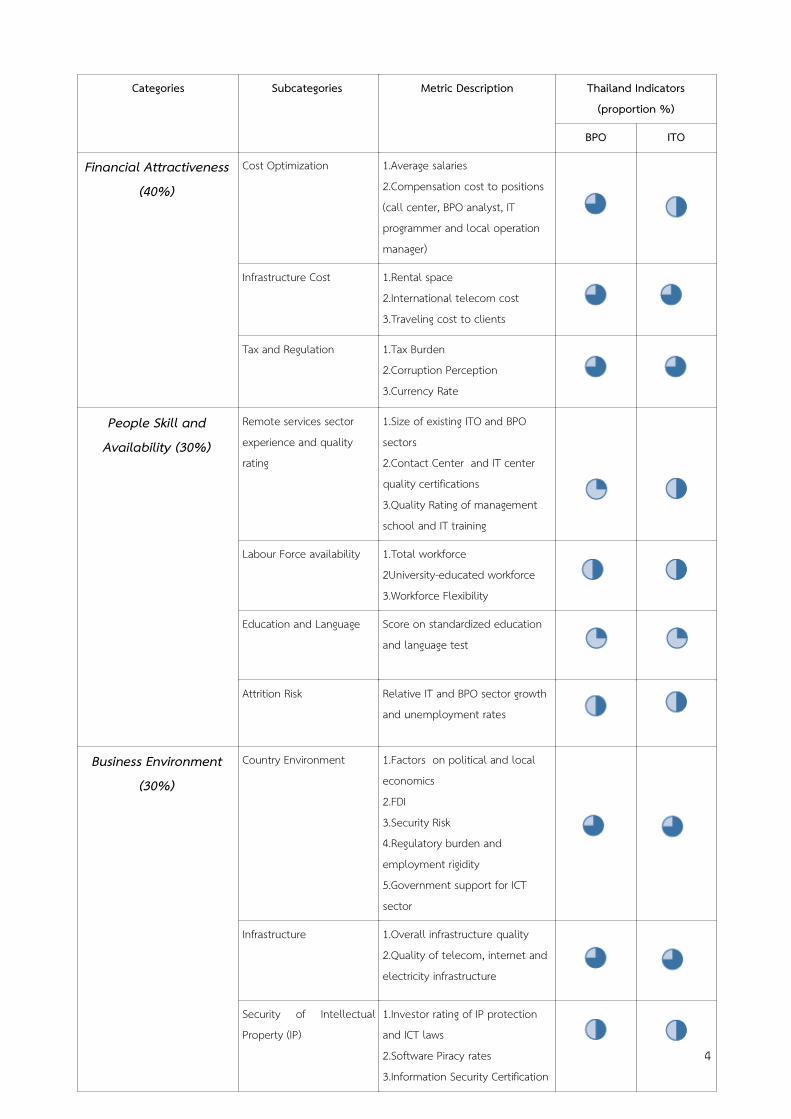

From ITO and BPO table , we divided into three categories as following

1. Financial Attractiveness

2. People Skill and Availability

3. Business Environment

___________________________________________

3 A.T Kearney Global Service Location Index 2011

3

Categories Subcategories Metric Description Thailand Indicators

(proportion %)

BPO ITO

Financial Attractiveness

(40%)

Cost Optimization 1.Average salaries

2.Compensation cost to positions

(call center, BPO analyst, IT

programmer and local operation

manager)

Infrastructure Cost 1.Rental space

2.International telecom cost

3.Traveling cost to clients

Tax and Regulation 1.Tax Burden

2.Corruption Perception

3.Currency Rate

People Skill and

Availability (30%)

Remote services sector

experience and quality

rating

1.Size of existing ITO and BPO

sectors

2.Contact Center and IT center

quality certifications

3.Quality Rating of management

school and IT training

Labour Force availability 1.Total workforce

2University-educated workforce

3.Workforce Flexibility

Education and Language Score on standardized education

and language test

Attrition Risk Relative IT and BPO sector growth

and unemployment rates

Business Environment

(30%)

Country Environment 1.Factors on political and local

economics

2.FDI

3.Security Risk

4.Regulatory burden and

employment rigidity

5.Government support for ICT

sector

Infrastructure 1.Overall infrastructure quality

2.Quality of telecom, internet and

electricity infrastructure

Security of Intellectual

Property (IP)

1.Investor rating of IP protection

and ICT laws

2.Software Piracy rates

3.Information Security Certification

4

Remarks:

High activities: Lower activity

Even top three location remains in India, China, and Malaysia are outstanding to provide the off shoring software

services activity, Thailand is rank as the significant player. One article from the Global Service location 4 (top 10

locations based on their capabilities as figure following

Thailand focus on niche quality of software services which produce output on the qualified graduates and

English capabilities moving up to value chain of BPO and ITO industries due to large workforce and cost

competitiveness.

Thailand skillful workforce:

The software sector in Thailand has been driven by the highly skilled and well educated workforce. Thailand

education system transforms the variety of IT professional courses set by the standard nationwide.

___________________________________________

4 A.T Kearney Global Service Location Index 2011

5

Thailand development policy delegates the opportunity to the geographic clusters such as the IT valley in the

northern of Thailand and outsourcing cluster in Phuket.

The development of language skill in Thailand has been proven as the various interpretation skill. Thailand is

also the largest IS/ISV communities to do outsourcing in Southeast Asia region. Also now we have certified 47

companies CMMI appraisal and more than 70 certified PSP developers training and ranked at 3rd in the world.

The number of certified software professional in PM, Software Quality Assurance and software tester were

approved by Quality Assurance Institute (QAI) achieved 80 persons.

The industry development is underwritten by the continued state investment in education and research. The

information and communication technologies are the priority area supported by the government; therefore the

investment in R &D has also significantly risen. The Ministry of ICT has invested to initiative projects to

collaboration among academic, research and industries to ensure the optimum usage of resource and apply

successful commercialization. From INSEAD global IT report show the Quality of Education in country which

represented perception index 1-7. Thailand was ranked at 3.6 scale. There are more than 100 universities

produce more than 4,000 skill professional workers annually. Some institutions, for example Software Park

Thailand provided professional high skill enterprises training such as IT professional, project management, and

software process.

From figure about the population with English as the first and the second language (Cambridge Encyclopedia of

English language, KPMG analysis) 5 show 3% of 65 million people in country know english as second language

( 2.5 million). The multiple language skill rise the localization business opportunities because localization enabler

for international businesses. Adequate recruitment of the best skill and talent workforce are in various industrial

sectors. A case in point,ProZ.com, the largest online community of translators and the Localization Industry

Standards Association (LISA), the leading organization for companies involved in localization and globalization is

located in Bangkok to promote the localization and translation industry in domestic and global arena.

Case studies

The largest software development site globally. Asia Online, the machine translation company has also set up its

operational headquarters in Bangkok, from where it conducts R&D and daily business operations. Likewise Asia

Online currently employs more than 400 staffs and is in the process of being incorporated in other 10 Asian

countries.

One more interesting niche market in Thailand are animation, design and graphic development. With creativity,

Thai developers step forward from neighbor countries in term of character, design and emotion. The animation

industries USD 736,700 which categorized to animation industry USD 381,200 and Game industry reached USD

355,500 6

___________________________________________

5 KPMG Analysis, Cambridge Encyclopedia 2010

6 Thailand-Canadian Collaboration Forum 11-14 October 2011, Bangkok 6

3.SWOT Analysis

BPO

Strengths

-Skill workforces

-Quality Assurance

-Business Environment

Weakness

-Language-lacking in quality in english instruction

-Lack of adequate infrastructure

-Lack of adequate promotional support.

Opportunities

-Hugh hub of FDI

-ASEAN AEC 2015

Threats

-Unstable political situations

Positioning

Market of BPO in Thailand

Besides being a famous tourist destination and the auto making hub for Southeast Asia, Thailand is best known

as a tourist destination, the government of Thailand is attempting a lot to encourage business and make higher

investments in Business Process Outsourcing (BPO). The opportunities for global BPO in Thailand are obstructed

by lack of government support and vision, limited access to investment capital, and lack of regulations regarding

privacy or security, as per to research analysts. They also cited the adequate of infrastructure, ICT research

facilities, labor policies, etc. in the BPO market of Thailand.

For these reasons , Office of the Board of Investment (BOI) decided to encourage higher and better investments

in Business Process Outsourcing. It has expanded Activity 7.22 for including not only call centers, but also an

array of services under the new category of BPO. This activity will include finance and accounting services,

administrative services, sales and marketing services, human resources support, international call centers and

data processing, and customer services, just to name a few. Recently, the India-based company, Infosys, has

decided to put up its BPO in Thailand.( www.sitagita.com) 7

Case Studies

Infosys targets Thailand for banking solutions suite. Software major Infosys said on Wednesday that it had

identified Thailand as a key target market for its global banking solutions suite, Finacle, and entered into a

partnership with Datamat Public Company Ltd. and Yip in Tsoi & Co Ltd in that country to market the product in

the region. 7

PRTRBPO.COM directly addresses the increasing need of our customers for value added business process

outsourcing services in Bangkok and Thailand. These requirements, to date, have been in the provision of PC /

Sales Team Management, Sales Outsourcing, Warranty Management, a number of retail related services and a

series of unusual management projects. PRTRBPO.COM is a relatively new business and was established to

ensure that PRTR is able to provide, as a separate resource, the business and project management skills that

address the increasing trend within Thailand’s business community for the outsourcing of many varied and

interesting areas of business. PRTR has looked to Europe and America in understanding the future trends that are

developing in Thailand and is ready and actively participating in providing interesting and original solutions to any

business process outsourcing requirement. (http://www.prtrbpo.com) 8

Best Practice

One of the successful BPO in Thailand according to human resource and payroll outsourcing to the oversea

clients who established own business in Thailand.

Humanica Thailand.

Humanica provides a full range of human resource management services from payroll outsourcing to HR

intelligence and talent management . We are also the number one SAP B1 reseller in Thailand. Our team has

extensive experiences in implementing ERP solutions for many years. With our practical approach drawn from

ERP experts, we help you to implement the ERP project to serve your business requirements on time and cost

effective.

Furthermore, they have a Performance Management team can help to implement the business intelligence

capability

Their PMS experts can help to design, develop and deliver the business intelligence system to enhance ability

to manage performance effectively. (www.humanica.com) 9

___________________________________________

7 http://sitagita.com/bpo/different-countries/thailand.html

8 http://www.prtrbpo.com

9 http://www.humanica.com/index.html

8

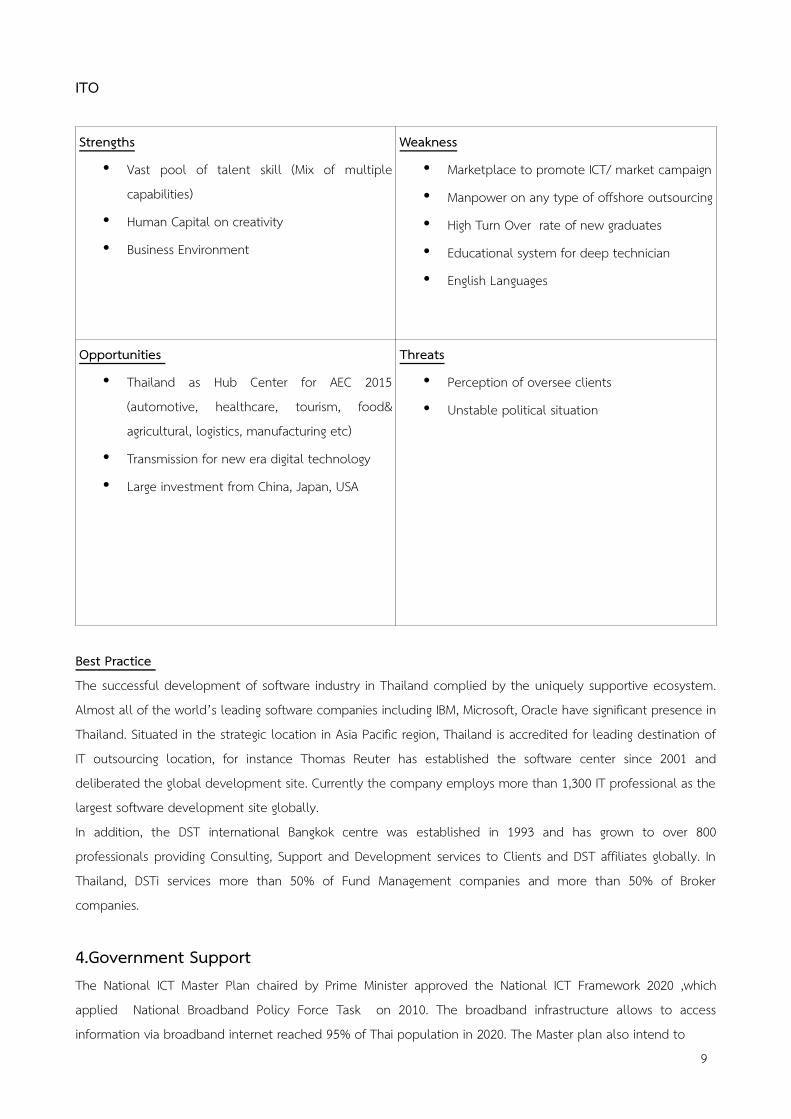

ITO

Strengths

• Vast pool of talent skill (Mix of multiple

capabilities)

• Human Capital on creativity

• Business Environment

Weakness

• Marketplace to promote ICT/ market campaign

• Manpower on any type of offshore outsourcing

• High Turn Over rate of new graduates

• Educational system for deep technician

• English Languages

Opportunities

• Thailand as Hub Center for AEC 2015

(automotive, healthcare, tourism, food&

agricultural, logistics, manufacturing etc)

• Transmission for new era digital technology

• Large investment from China, Japan, USA

Threats

• Perception of oversee clients

• Unstable political situation

Best Practice

The successful development of software industry in Thailand complied by the uniquely supportive ecosystem.

Almost all of the world’s leading software companies including IBM, Microsoft, Oracle have significant presence in

Thailand. Situated in the strategic location in Asia Pacific region, Thailand is accredited for leading destination of

IT outsourcing location, for instance Thomas Reuter has established the software center since 2001 and

deliberated the global development site. Currently the company employs more than 1,300 IT professional as the

largest software development site globally.

In addition, the DST international Bangkok centre was established in 1993 and has grown to over 800

professionals providing Consulting, Support and Development services to Clients and DST affiliates globally. In

Thailand, DSTi services more than 50% of Fund Management companies and more than 50% of Broker

companies.

4.Government Support The National ICT Master Plan chaired by Prime Minister approved the National ICT Framework 2020 ,which

applied National Broadband Policy Force Task on 2010. The broadband infrastructure allows to access

information via broadband internet reached 95% of Thai population in 2020. The Master plan also intend to

9

invest human capital and IT literacy, to apply ICT enabling value creation to others industries and to develop

ICT for green economy and ICT for good governance. The government invests IT enabler services in the e-

government projects as well as offering the tax exemption privilege for 8 years for foreign start up companies,

also provides incentives for the working permission, equipment and machinery. The government offers the ICT

infrastructure to promote the development of 4G, Enterprise 2.0 and also security system in domestic and

international.

Linkage to AEC 2015: Single marketplace

With the paradigm of AEC 2015, the integration of ASEAN countries + 6 reach more than 50% of the world

population (3,284 millions) and consumed 22% world GDP which value USD 12,250 billion. The conceptional

framework of the ASEAN ICT Master plan will be enhance the human capital and apply the horizontal industries

the thematic track on digital economy, new media and social network. The community transform the mechanism

to pursue partnerships and collaboration with the regional counterpart and alliances. The vertical industries

which will comply the ICT enabler as the strategic STI keys such as Creative & Digital contents, Logistics ,

Toursim+ medical tourism , automotive parts, processed food and electronics etc. will be key drive to applied

ICT as engine to to raise competitiveness in AEC 2015. Complied to ASEAN ICT master plan, which use ICT as a

tool to rise the ASEAN Economic growth and also provide the linkage to integrate the infrastructure, Thailand

government has positioned Thai ICT industry as flagship on ASEAN strategic location.

Mapping Thailand as the strategic location of AEC 2015

Within 2012 telecommunication and ICT, one of four service industries that were stimulated to open free zone

market such as aero transportation, healthcare, tourism, will open 70% own foreign stakeholders. This is the

direction that Thailand has to open more Foreign Direct Investment (FDI) located in whole country. In the

meantime, Thai investor can run oversee business in ASEAN including the cross border Data Processing Services in

ASEAN members. More thai skilled workforce will work border less across the region. Some vertical industries

which effect by AEC 2015 and need software as an enabling platform to reinforce the value chain and operation

such as logistic and electronics assembly will invest more in order to get more competitiveness.

Case Studies: Logistic

In order to get cost optimization; Thailand positioned the strategic location on logistics. The government

agencies launched the Master Plan for Thailand Logistic by creating the awareness of using IT as enabling on

logistics or called “ E-logistics” implemented marketplace with AEC 2012. The main strategic plan in on “ the

national single window” which will be applied in the import-export on logistics methodology to linkage the

paperless that implement digital technologies to integrate E-transportation, e-custom, e-declaration, e-container,

e manifest, trading community, banking and insurance to single platform. This platform will penetrate to Asean

Single Window in 2012. This will drive Thailand as the center hub in logistics both ASEAN export and import

location.

Case Studies: Automotive

Thailand called ''Detroit of Asia,'' produces car plants over the past decade and initial vehicles manufacturers are

10

made for export to more than 200 countries. The strengths of Thailand core value in the supply chain for car

Assembly, skill & experience workforce and also has been invested infrastructure by the government. Under the

paradigm of AEC 2015, Thailand is positioned to be Diesel automotive part assembly integrated to the whole

supply chain of Automotive in ASEAN. The automotive industries promote to apply ICT as enabler for

manufacturing, cost optimization, especially transform to the clients' orientation The ICT will help the

production line and manage the core value chain of industries to get better services and get competitiveness in

the global marketplace.

Case Studies: Tablet and device investment from the government to primary school

Thailand's Cabinet has approved the purchase of 860,000 tablet computers from a little-known Chinese

company for students in the first year of primary school. The software developer will take this opportunities to

create any contents and application on the mobility devices. The education institutes in Thailand have more

than 60,000 around the countries and proportion of users would be more than 600,000 students. The projects

will take hugh auction and procurement in the long term.

5.Strategies and Initiatives

Strategies Description

5.1 Positioning Thailand as

strategic software development in

ASEAN and Global

-Increase more professional skills by improving the education system and provide

more multiple national training

-Determine the strategic industries direction that used value added ICT enabler such

as tourism, medical healthcare, software application in mobile devices etc.

-Set up the ICT integrated committee to push Thai ICT master plan.

-Launch the Telecommunication policy to comply with the ASEAN digital broadcasting

which will align with the 4G mobile service.

-Promote the Market -Entry methodology through ASEAN by sharing information,

looking for strategic partnership, exchange human resource, knowledge transfer etc.

-Focus on the niche software development by using the N2N model to integrate

potential small and medium software developers to bundle the selling services in

specific industries such as tourism, healthcare, financial management, and logistics.

Strategies Description

5.2 Partnership and Alliance with

domestic and regional

-Increase more software park in distance area that boost the domestic demand, also

create the job for local people and get competitiveness.

-Create the promoting program to transfer knowledge , skill and expertise among

region such as Exchange technician programmer with japan companies

-Make future collaboration program through the networking channels for example,

exchange inbound-outbound delegation, infrastructure; business matching program,

internship, rental office space, and so on.

11

Strategies Description

5.3.Benchmarking; identify; focus

on a niche market (specific niche

in global competition)

In order to sustain the ASEAN ICT competitiveness, Thai ICT industries must focus on

the software as a service application (Saas) in specific area such as our core value

vertical industries such as tourism , food , digital media and animation, medical

healthcare, automotive and logistics. These vertical industries align with the know-how

and workforce skill.

Strategies Description

5.4. Awareness Creation of IT

enabler on the vertical industries

in domestic market.

Thailand is also focusing on the growth of the IT domestic demand especially high

software skill and expertise on the vertical software industry applications such as

tourism, financial services, logistics, hospital, food, agriculture, manufacturing industries.

In addition, hyper growth software services such as animation, mobile application,

multimedia and graphic are being promoted. This is also a result from the

government’s efforts on the development of 3G and Wimax, web 2.0 and security

services.

Strategies Description

5.5 Build Cluster and Platform for

emerging technologies.

-Trends of technologies are

change dramatically, Thai ICT

industries positioned on the new

emerging technologies according

to many research indicators to

map with the potential local

demand as following

Cloud Computing: The concept of IT usage with cost optimization make cloud

computing as the one potential driver for any business sectors. Today many private

applied cloud computing passed the software as a service (Saas) model by billing the

monthly service instead of software licensing. These provide great opportunities for

software developers to create various applications served on the cloud services. In

case of cloud infrastructure, AEC 2015 will allocate the concept of data centre free

zone and and provide the backup side outside among borders.

Mobile Application: The Office of the National Broadcasting and Telecommunication

Commission will comply with the ASEAN digital broadcasting. The government have

to provide the infrastructure and also extend the mobile broad width that will serve

the 4G for mobile industries. This will reinforce new mobile application and build the

mobile platform to serve the mobile communities and developers. Yet the mobile

industries will grow but the mobility device such as tablet help and transform

business methodology of many industries such as insurance, event organizer, printing

etc. The demand of vertical industries will build new application and new experience

for the end users.

Digital technology: The Digital Technology covered Record binary code combination

of digit (0,1) bits represent words / images and also Telecommunication (transmit

messages) such as TV broadband,sound, media,music, images, phone, cable system,

internet and social network (American encyclopedia) will be new trend for ASEAN ICT.

The digital technology transform the traditional industries to be more effectiveness,

reduce cost and increase customer satisfaction. For example Thailand logistic master

plan will use the national single window that apply digital tool in order to integrate

data, paperless and also certify the e signature or the printing industries which applied

digital technology for e-book, e-magazine that transform business model and also

revolutionize the whole industries.

12

Strategies Description

5.6 Build Manpower to meet ITO/

BPO global standards.

-Thailand education system transforms a various of IT professional nationwide that

produce more than 100,000 workforces. More than 100 universities produce more

than 10,000 skill developers annually. The universities provide standard courses

and workshop across the country. The IT workforce have dispersed and worked

through Software Park Alliance in other regions such as E-Saan Software Park in

KhonKhaen and Korat Software Park in the eastern and outsourcing pillar at Phuket,

south of Thailand. Thailand was selected to be strategic location for global software

development .

-Thailand education system transforms variety of IT professional courses set by

new education standards nationwide to uplift IT professional skill and experience.

-University training courses are readily available in software development, localization,

translation, internationalization and other specific fields. In AEC 2015 Thailand

government 's policy insist to enhance the quality of manpower by means of

increased skill workforce, multiple language skill and analytic skill.

Initiatives

Tax exemption and working permit for private to increase more professional skill workforce.

6.Quality Certifications and Support

- The Ministry Of ICT in cooperation with Ministry of Labor determine standard ICT professional will comply to

ASEAN cross border labor. This measurement will define the professional qualification, certificate and also

compensation to the single standardization such as System Analyst, Networking and system executives, ICT

Project management, organizational architecture and design software; network and ICT security, and software

developers. In addition, software testing and software certificate will be a must to Thai workforce to meet the

global standard.

-Government privilege will provide system for professional skill testing and certification and allocate the portion

of budget to make more ICT experts.

-Thailand will develop IT professional Repository dominated in the region and also establish institute of IT

professional measurement to produce more qualified IT professional since high school whole countries.

7. Key Stakeholders

Associations

1.The Association of Thai ICT Industry (ATCI),

Further information: www.atci.or.th

1. Promoting Thai ICT industry through business collaboration and sustained growth.

2. Focusing ICT human resource development.

13

3. Working with the government to formulate policy to stimulate ICT uses and technological advancement.

4. Acting as a representative of Thailand in the international arena to enhance the country’s reputation and to

build relationships across the region.

2.The Association of Software Industry (ATSI)

Further information: www.atsi.or.th

1. Solve problem of Thai IT entrepreneurs to reinforce Thai software globally.

2. Promote software enabling to other industries efficiency.

3.Thai Software Export Promotion Association (TSEP)

www.tsep.or.th

1.To compete globally, TSEP companies must strive to be “Best in Class” in each areas of expertise

2.Focus & become niche ICT players in industries where Thai companies are well established

3.Organize & attend Buyers Meets Sellers Events & Trade Missions with emphasis on meeting corporate decision

makers, exploring their ICT needs and showcase our solutions and capabilities to domestic, regional & global

customers

4.Find new business partners to exchange market expertise, know-how on domestic & overseas business, co-

marketing activities.

Organizations

1.National Electronics and Computer Technology Center (NECTEC)

Further information: www.nectec.or.th

NECTEC was established on 16 September 1986, initially as a project under the Ministry of Science, Technology

and Energy (the former name of the Ministry of Science and Technology). In 1991, NECTEC was transformed into

a specialized national center under the National Science and Technology Development Agency (NSTDA), a new

agency following the enactment of the Science and Technology Development Act of 1991.

NECTEC contributes to the development of Thailand's capability in electronics and computer technologies

through:

I. Research, development, design and engineering

II. Technology transfer to industries and communities

III. Human resource development

IV. Policy research and industrial intelligence and knowledge infrastructure

2.The Software Industry Promotion Agency (SIPA)

Www.sipa.or.th

A public organization, established on September 24, 2003 under the administrative supervision of the Ministry of

Information and Communication Technology. SIPA acts as a lead agency that develops plans and policies to

advocate Thai software industry with a focus on promoting and developing software and digital content

entrepreneurs, improving human resource, supporting investments and market opportunities, boosting research

activities and technology instructions as well as supporting and developing measures to protect the Intellectual

Property Rights to software. The goal is to make Thai software industry domestically and internationally

14

recognized. Thus, this is consistent with the Government Policy that defines a development of software industry

as a main strategy to build competitiveness of the country.

3.Software Park Thailand

Www.swpark.or.th

An organization under the National Science and Technology Development Agency (NSTDA). Our task is to support

and strengthen those in the Software industry by any means necessary, be it in procurement of human

resources, marketing, securing investment and even with the latest technology. Our aim is to help each and

every stakeholder in Thailand’s software industry from manufacturing industry to agriculture as well as the

service sector-Software can help all increase their efficiency and their potential. We aim to grow the domestic

software industry and instill confidence in this industry for overseas operators wishing to establish themselves in

Thailand.

Regional Software Park Around countries Alliance:Thailand Software Park Alliance (TSPA)1.Software Park Thailand

2.Software Park Phuket

3.E-Saan Software Park

4.Korat Software Park

Software Park Thailand lead the regional alliances as the business model and share the infrastructure; facilities

and activities to promote the networking, marketing channels through software houses ' members. They signed

MOU among organizations on March 2012.

International development Program

1.The Asia Oceania Regional Software Park Alliance is an international collaboration among 22 software related

organizations from 13 economies such as Malaysia, Brunei, China, Hong Kong, Vietnam and Thailand etc. in the

Asia Oceania Region.

It was initiated during the Regional Software Park Forum 2007 in Bangkok, Thailand with the idea to create a

mutual collaborative linkage among Software Park operators and/or IT related organizations in this region which

can subsequently be extended to their tenants and members. A year later, the initiative has brought results with

the establishment of the Asia Oceania Regional Software Park Alliance where all alliance members signed the

official Memorandum of Understanding in Xiamen China on September 8, 2008 agreed to establish a network by

pooling resources among the members to assist local software/IT business in the region to go global and place

software/IT industry development in the Asia Oceania on the world scenario

2.The Asian-Oceanian Computing Industry Organization (ASOCIO) is a group of IT industry associations coming

from economies in the Asia and Oceania region. ASOCIO is established in 1984 with the objective is to promote,

encourage and foster relationships and trade between its members, and to develop the computing industry in

the region.

Presently, ASOCIO represents the interests of 29 economies, comprising 22 members from Australia, Bangladesh,

Brunei, Chinese Taipei, Hong Kong, India, Indonesia, Japan, Laos, Macao, Malaysia, Mongolia, Myanmar, Nepal,

15

New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Thailand, Vietnam and seven guest

members from USA, UK, Canada, Spain, Russia, France, and Kenya. Today, ASOCIOs members account for more

than 10,000 ICT companies and represent approximately US$350 billion of ICT revenue in the region.

ATCI is now leading the ASOCIO in Thailand and the next meeting will be held in Nepal.

3. CBI ITO Program 2009-2013

Software Park Thailand facilitated as counterpart to the Centre for the Promotion of Imports from developing

countries (CBI) is cordially inviting you to join with the CBI IT outsourcing Export Coaching Program (CBI ITO ECP)

2008-2010 from Netherlands. This program is selected developing countries with sake of delivering services to

provide assessment to EU market, offer business transfer and technology information, provide matchmaking and

promotion opportunities by the EU consultants.

Overview of program is to select 10-20 companies from developing countries through CBI counterpart and assist

them to enter the European market. During the program selected companies will be provided training, coaching,

and consulting and market entry assistant.

8.Best Practice

Emergence Technologies : Flagship for Thai ICT Ecosystem

Thai software Industry has adopted the software road map in order to reinforce the ICT industry ecosystem for

new market development and initiate the start up environment. Technologies have been changed dynamically

and made short computing cycle of products and turned on software as services. Thai ICT industry has to shift

spontaneously by following the technology trend and apply to global market orientation. There are some

emergence technologies that Thai ICT industry will focus on such as Mobile application, Cloud computing, Social

Analytics, and Social Networking.

The significant Enterprise 2.0 will lead the technology trend for mobile application technology especially on

mobile devices and smart phone. This will augment number of mobile content developers,mcommerce and

mpayment in the near future. Many Thai private and government organizations get recognition to apply

mobilizing application to execute value creation to their business performance and also embrace the platform to

support mobility. The emergence of cloud computing will support and manage remote cloud implementation to

the organizations both infrastructure and Saas delivery of cloud services. This technology will then become the

social media and turn on the cloud security concern in business sectors. Finally social networking will

collaborate the connection, networking, tools & services for the marketing and CSR activities for any

organizations. The enterprise 2.0 will create the new platform,communities and security serviced providers to

enhance and shift the business model of private sectors in order to adjust to any changes and survive in global

economic circumstance. These emergence technologies will support the industrial SMEs strategies and

performances to apply new business models in order to gain the competitiveness and work efficiency in the

global market. One successful story was applied Business Continuity for cloud computing and mobile

application in flood crisis in Thailand in 2011, the virtual technology can help SMEs and privates to access any

time, anywhere and any devices. This is helpful engine that can carry on the business efficiency even on the

crisis situations.

16

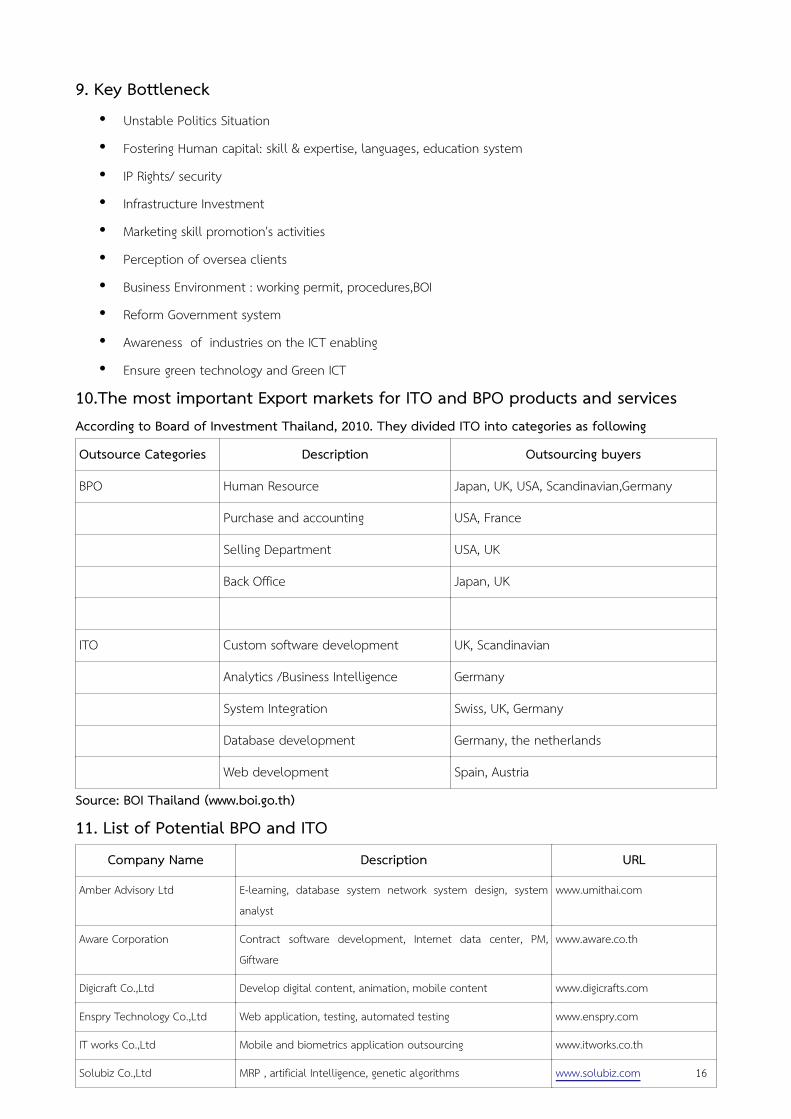

9. Key Bottleneck

• Unstable Politics Situation

• Fostering Human capital: skill & expertise, languages, education system

• IP Rights/ security

• Infrastructure Investment

• Marketing skill promotion's activities

• Perception of oversea clients

• Business Environment : working permit, procedures,BOI

• Reform Government system

• Awareness of industries on the ICT enabling

• Ensure green technology and Green ICT

10.The most important Export markets for ITO and BPO products and servicesAccording to Board of Investment Thailand, 2010. They divided ITO into categories as following

Outsource Categories Description Outsourcing buyers

BPO Human Resource Japan, UK, USA, Scandinavian,Germany

Purchase and accounting USA, France

Selling Department USA, UK

Back Office Japan, UK

ITO Custom software development UK, Scandinavian

Analytics /Business Intelligence Germany

System Integration Swiss, UK, Germany

Database development Germany, the netherlands

Web development Spain, Austria

Source: BOI Thailand (www.boi.go.th)

11. List of Potential BPO and ITO

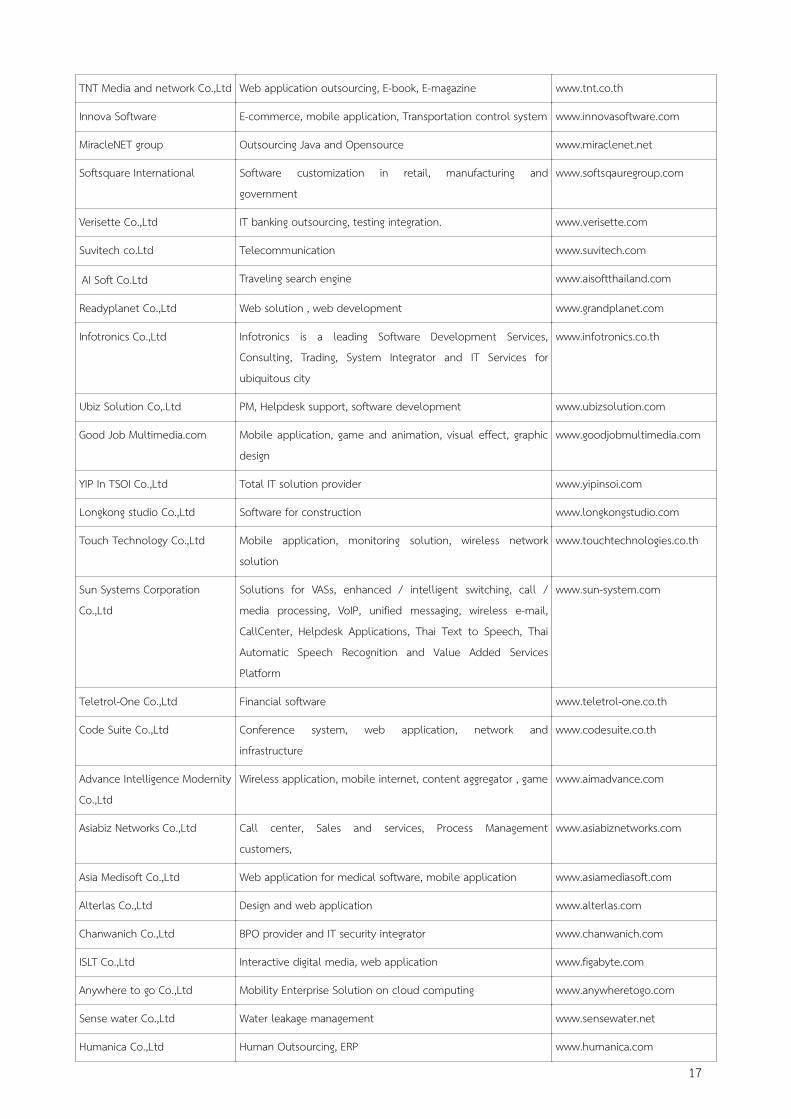

Company Name Description URL

Amber Advisory Ltd E-learning, database system network system design, system

analyst

www.umithai.com

Aware Corporation Contract software development, Internet data center, PM,

Giftware

www.aware.co.th

Digicraft Co.,Ltd Develop digital content, animation, mobile content www.digicrafts.com

Enspry Technology Co.,Ltd Web application, testing, automated testing www.enspry.com

IT works Co.,Ltd Mobile and biometrics application outsourcing www.itworks.co.th

Solubiz Co.,Ltd MRP , artificial Intelligence, genetic algorithms www.solubiz.com 16

TNT Media and network Co.,Ltd Web application outsourcing, E-book, E-magazine www.tnt.co.th

Innova Software E-commerce, mobile application, Transportation control system www.innovasoftware.com

MiracleNET group Outsourcing Java and Opensource www.miraclenet.net

Softsquare International Software customization in retail, manufacturing and

government

www.softsqauregroup.com

Verisette Co.,Ltd IT banking outsourcing, testing integration. www.verisette.com

Suvitech co.Ltd Telecommunication www.suvitech.com

AI Soft Co.Ltd Traveling search engine www.aisoftthailand.com

Readyplanet Co.,Ltd Web solution , web development www.grandplanet.com

Infotronics Co.,Ltd Infotronics is a leading Software Development Services,

Consulting, Trading, System Integrator and IT Services for

ubiquitous city

www.infotronics.co.th

Ubiz Solution Co,.Ltd PM, Helpdesk support, software development www.ubizsolution.com

Good Job Multimedia.com Mobile application, game and animation, visual effect, graphic

design

www.goodjobmultimedia.com

YIP In TSOI Co.,Ltd Total IT solution provider www.yipinsoi.com

Longkong studio Co.,Ltd Software for construction www.longkongstudio.com

Touch Technology Co.,Ltd Mobile application, monitoring solution, wireless network

solution

www.touchtechnologies.co.th

Sun Systems Corporation

Co.,Ltd

Solutions for VASs, enhanced / intelligent switching, call /

media processing, VoIP, unified messaging, wireless e-mail,

CallCenter, Helpdesk Applications, Thai Text to Speech, Thai

Automatic Speech Recognition and Value Added Services

Platform

www.sun-system.com

Teletrol-One Co.,Ltd Financial software www.teletrol-one.co.th

Code Suite Co.,Ltd Conference system, web application, network and

infrastructure

www.codesuite.co.th

Advance Intelligence Modernity

Co.,Ltd

Wireless application, mobile internet, content aggregator , game www.aimadvance.com

Asiabiz Networks Co.,Ltd Call center, Sales and services, Process Management

customers,

www.asiabiznetworks.com

Asia Medisoft Co.,Ltd Web application for medical software, mobile application www.asiamediasoft.com

Alterlas Co.,Ltd Design and web application www.alterlas.com

Chanwanich Co.,Ltd BPO provider and IT security integrator www.chanwanich.com

ISLT Co.,Ltd Interactive digital media, web application www.figabyte.com

Anywhere to go Co.,Ltd Mobility Enterprise Solution on cloud computing www.anywheretogo.com

Sense water Co.,Ltd Water leakage management www.sensewater.net

Humanica Co.,Ltd Human Outsourcing, ERP www.humanica.com

17

Bibliography

The annual report Ministry of ICT Thailand 2011, “ Thailand ICT Market 2011 and outlook 2012” , Software

Industry Promotion Agency (SIPA), page 54.

The IMD World Competitiveness Yearbook (WCY); The World Competitiveness Scorecared, page 19.

A.T Kearney ; A.T Kearney Global Service Location Index 2011; page 23

Cambridge Encyclopedia 2010 , “KPMG Landscape Report Analysis” , page 18

Thailand-Canadian Collaboration Forum 11-14 October 2011, Bangkok; page 32

http://sitagita.com, “ BPO Thailand”

http://www.prtrbpo.com, “company profile”

http://www.humanica.com; “company profile”

http://www.boi.or.th ; “Board of Investment Thailand ” (BOI), 2011

Recommended