Tanker supply until 2015Platts

Navigating Through Market Challengesby

[email protected] Research and Projects

Athens 26 October 2009

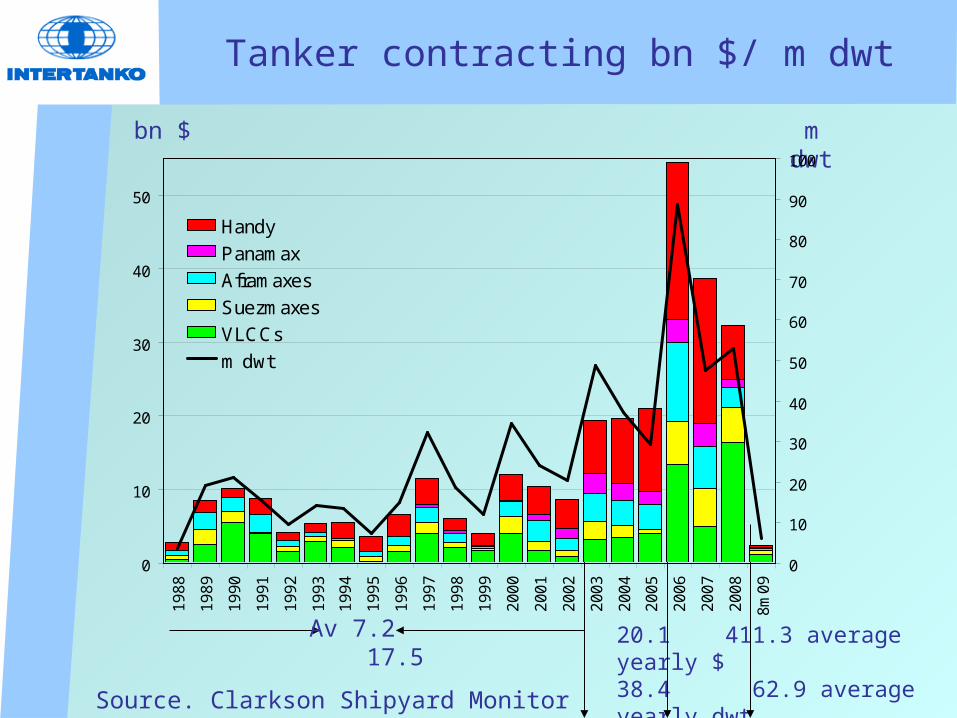

Tanker contracting bn $/ m dwt

bn $

Source. Clarkson Shipyard Monitor

m dwt

Av 7.2 17.5

20.1 411.3 average yearly $ 38.4 62.9 average yearly dwt

0

10

20

30

40

501

98

8

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

8m

09

0

10

20

30

40

50

60

70

80

90

100

Handy

Panamax

Aframaxes

Suezmaxes

VLCCs

m dwt

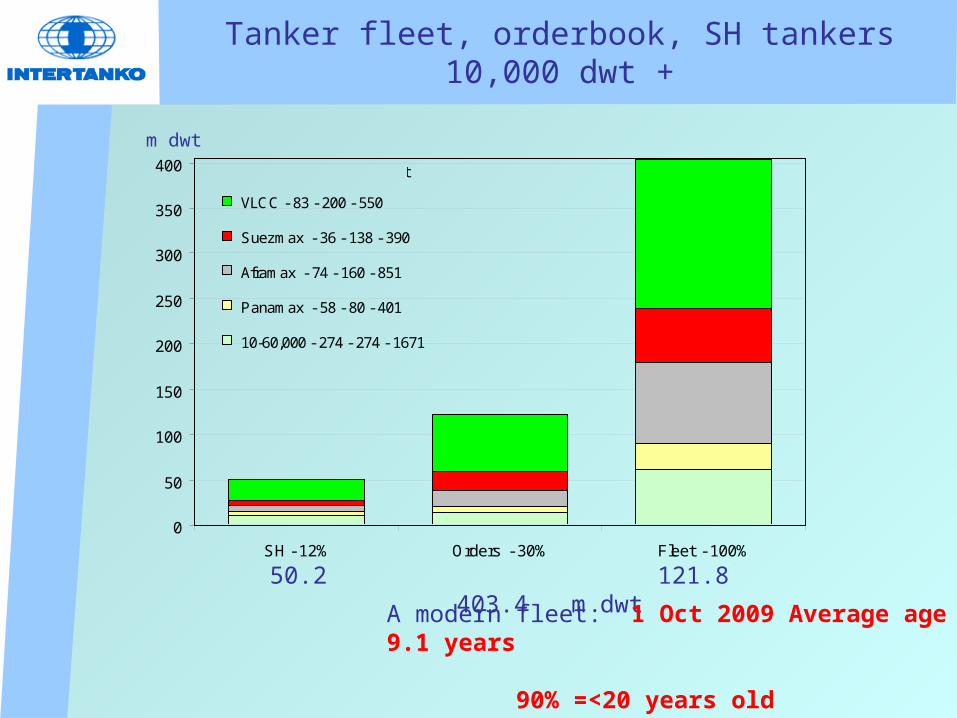

Tanker fleet, orderbook, SH tankers10,000 dwt +

50.2 121.8 403.4 m dwt

m dwt

A modern fleet: 1 Oct 2009 Average age 9.1 years 90% =<20 years old 79% =<15 years old 67% =<10 years old

0

50

100

150

200

250

300

350

400

SH - 12% Orders - 30% Fleet - 100%

VLCC - 83 - 200 - 550

Suezmax - 36 - 138 - 390

Aframax - 74 - 160 - 851

Panamax - 58 - 80 - 401

10-60,000 - 274 - 274 - 1671

14%

38%

36%

Segment - SH - Orders - fleet

20%24%

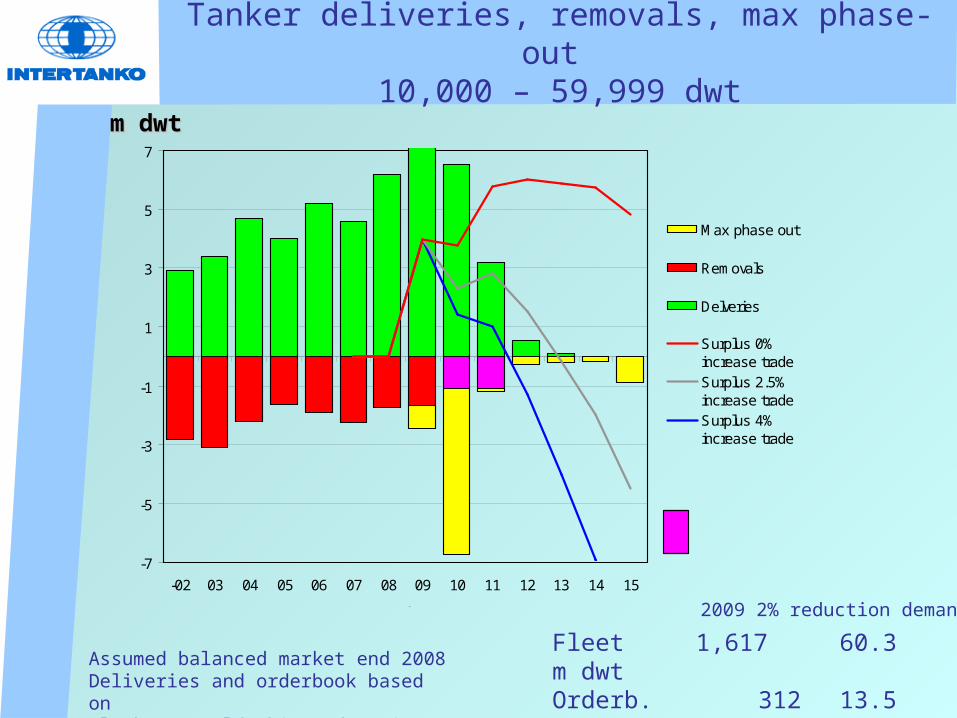

Tanker deliveries, removals, max phase-out 10,000 – 59,999 dwt

m dwtm dwt

Assumed balanced market end 2008Deliveries and orderbook based on Clarkson World Shipyard Monitor

Fleet 1,617 60.3 m dwtOrderb. 312 13.5 “ 22%Not DH 356 11.2 ” 20%

2009 2% reduction demand

-7

-5

-3

-1

1

3

5

7

-02 03 04 05 06 07 08 09 10 11 12 13 14 15

Max phase out

Removals

Delveries

Surplus 0%increase tradeSurplus 2.5%increase tradeSurplus 4%increase trade

year

Tonnage overhang

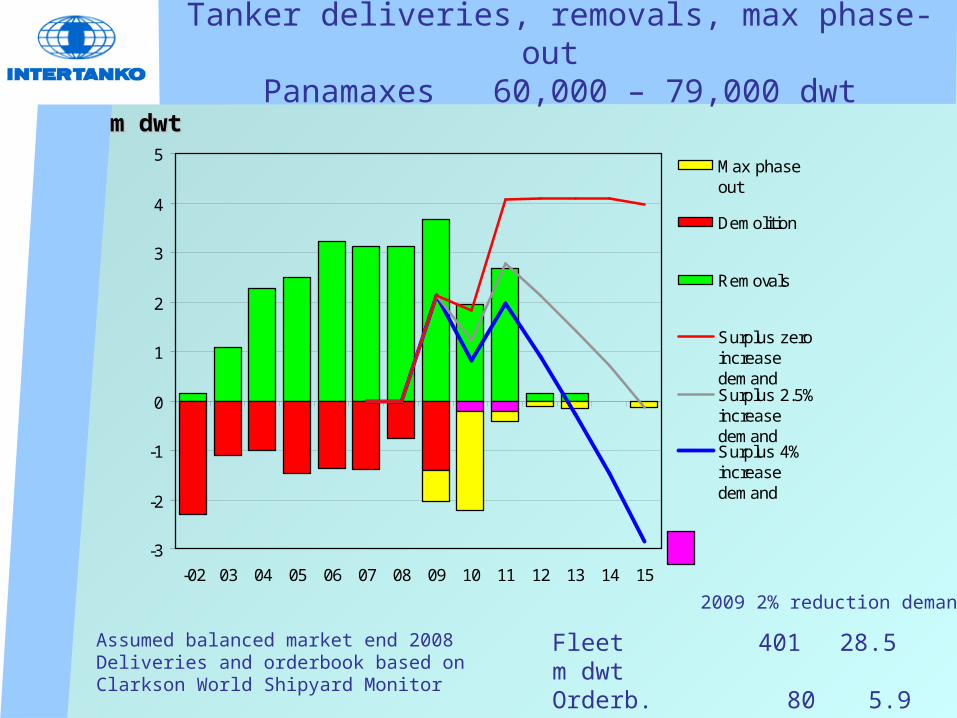

Tanker deliveries, removals, max phase-out Panamaxes 60,000 – 79,000 dwt

m dwtm dwt

Assumed balanced market end 2008Deliveries and orderbook based on Clarkson World Shipyard Monitor

Fleet 401 28.5 m dwtOrderb. 80 5.9 “ 21%Not DH 58 3.9 ” 14%

2009 2% reduction demand

-3

-2

-1

0

1

2

3

4

5

-02 03 04 05 06 07 08 09 10 11 12 13 14 15

Max phaseout

Demolition

Removals

Surplus zeroincreasedemandSurplus 2.5%increasedemandSurplus 4%increasedemand

Tonnage overhang

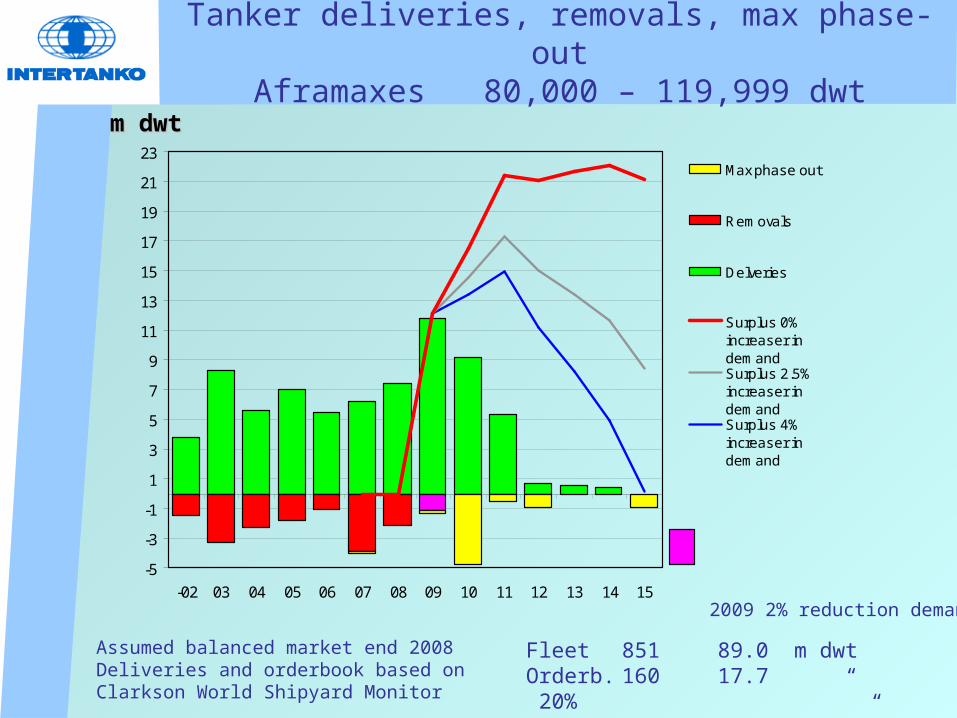

Tanker deliveries, removals, max phase-outAframaxes 80,000 – 119,999 dwt

m dwtm dwt

Assumed balanced market end 2008Deliveries and orderbook based on Clarkson World Shipyard Monitor

Fleet 851 89.0 m dwtOrderb. 160 17.7 “ 20%Not DH 74 7.1 ” 8%

2009 2% reduction demand

-5

-3

-1

1

3

5

7

9

11

13

15

17

19

21

23

-02 03 04 05 06 07 08 09 10 11 12 13 14 15

Max phase out

Removals

Delveries

Surplus 0%increaser indemandSurplus 2.5%increaser indemandSurplus 4%increaser indemand

year

Tonnage overhang

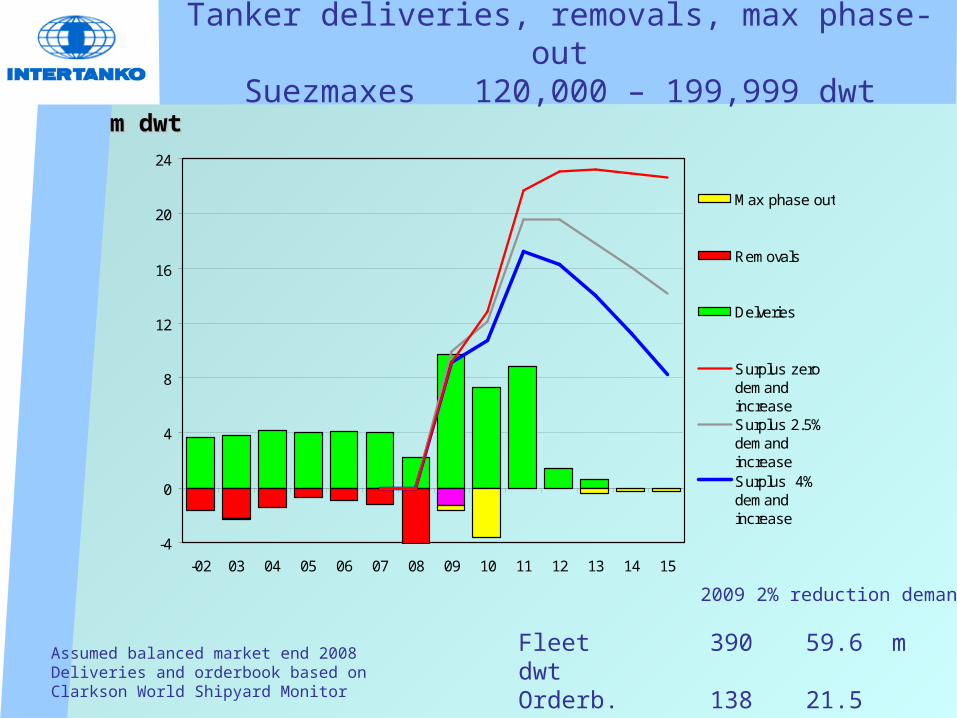

Tanker deliveries, removals, max phase-outSuezmaxes 120,000 – 199,999 dwt

m dwtm dwt

Assumed balanced market end 2008Deliveries and orderbook based on Clarkson World Shipyard Monitor

Fleet 390 59.6 m dwtOrderb. 138 21.5 “ 36%Not DH 36 5.1 ” 9%

2009 2% reduction demand

-4

0

4

8

12

16

20

24

-02 03 04 05 06 07 08 09 10 11 12 13 14 15

Max phase out

Removals

Delveries

Surplus zerodemandincreaseSurplus 2.5%demandincreaseSurplus 4%demandincrease

year

Tanker deliveries, removals, max phase-outVLCCs 200,000 dwt +

m dwtm dwt

Assumed balanced market end 2008Deliveries and orderbook based on Clarkson World Shipyard Monitor

Fleet 550 165.4 m dwtOrderb. 200 62.2 “ 38%Not DH 83 22.8 ” 14%

2009 2% reduction demand

-20

-12

-4

4

12

20

28

36

44

52

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Max phase out

Removals

Delveries

Surplus zeroincrease

Surplus 2.5%increase

Surplus 4%increase

year

Assumed removal of DH tankers

Assumed deliveries of new orders

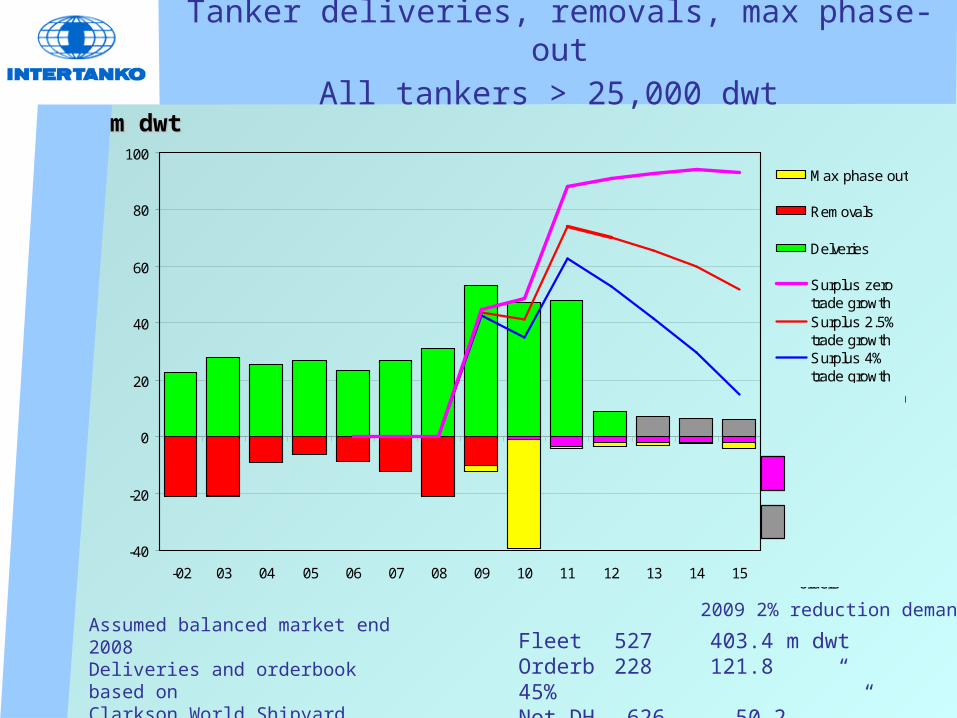

Tanker deliveries, removals, max phase-outAll tankers > 25,000 dwt

m dwtm dwt

Assumed balanced market end 2008Deliveries and orderbook based on Clarkson World Shipyard Monitor

Fleet 527 403.4 m dwtOrderb 228 121.8 “ 45%Not DH 626 50.2 ” 12%

2009 2% reduction demand

-40

-20

0

20

40

60

80

100

-02 03 04 05 06 07 08 09 10 11 12 13 14 15

Max phase out

Removals

Delveries

Surplus zerotrade growthSurplus 2.5%trade growthSurplus 4%trade growth

year

Assumed removals of DH tankers

Assumed deliveries of new orders

Minus 2% growth in 2009 and the above scenarios later

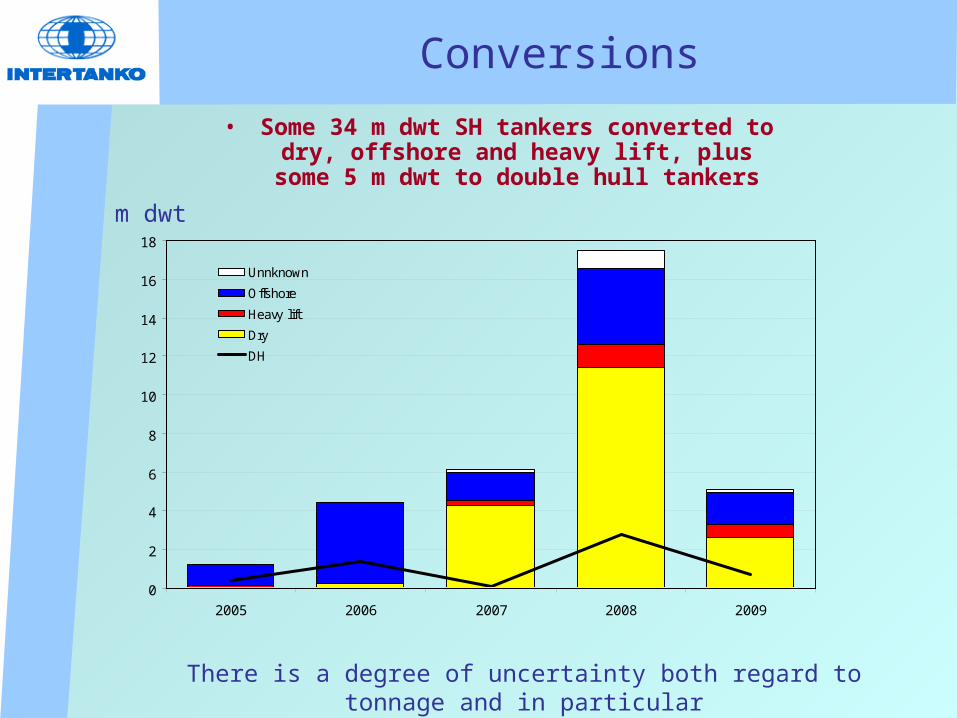

Conversions

• Some 34 m dwt SH tankers converted to dry, offshore and heavy lift, plus some 5

m dwt to double hull tankersm dwt

There is a degree of uncertainty both regard to tonnage and in particularthe timing of conversion

0

2

4

6

8

10

12

14

16

18

2005 2006 2007 2008 2009

Unnknown

Offshore

Heavy lift

Dry

DH

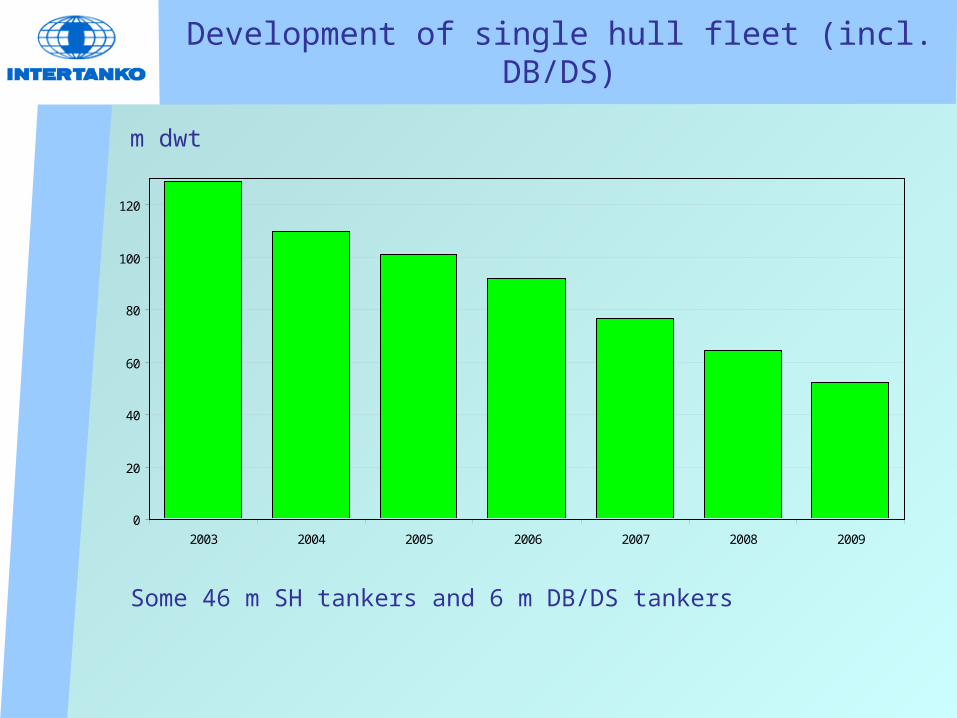

Development of single hull fleet (incl. DB/DS)

m dwt

0

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008 2009

Some 46 m SH tankers and 6 m DB/DS tankers

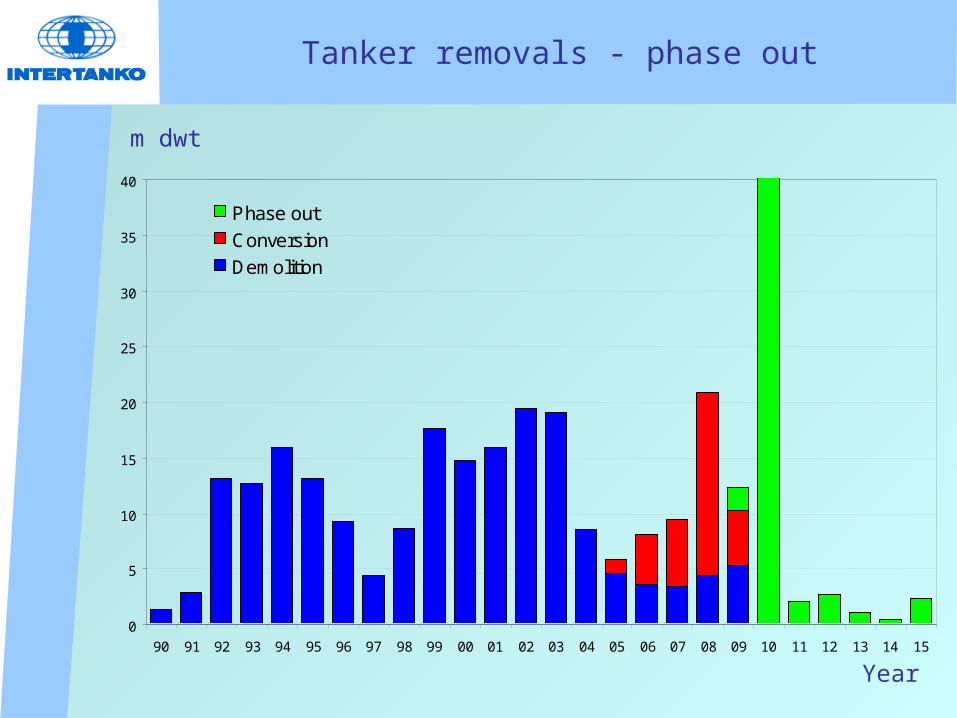

Tanker removals - phase out

m dwt

0

5

10

15

20

25

30

35

40

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Phase out

Conversion

Demolition

Year

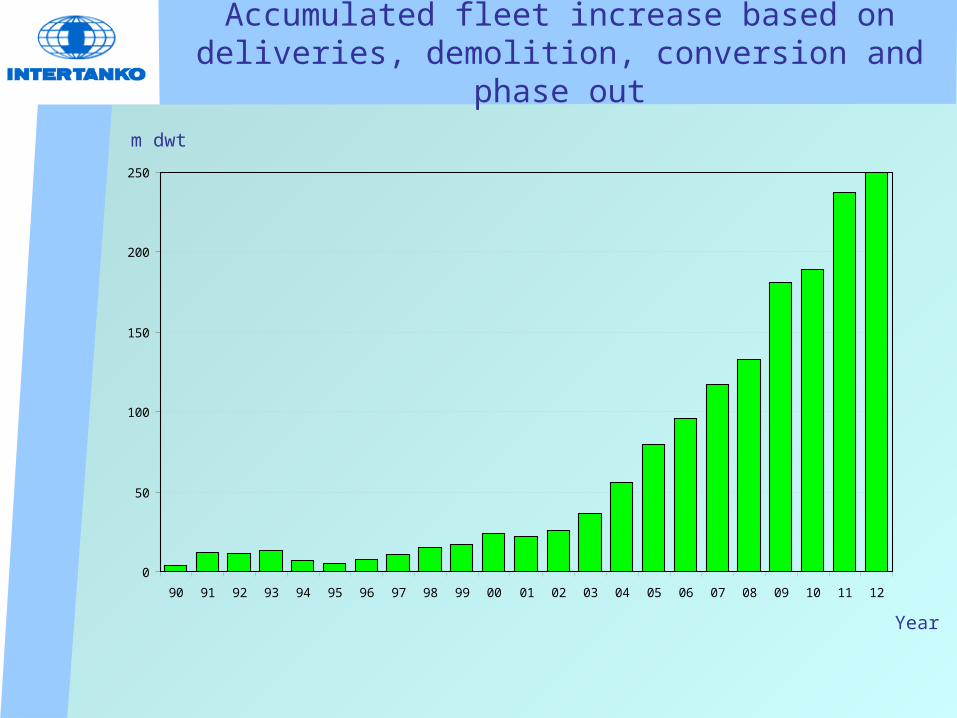

Accumulated fleet increase based on deliveries, demolition, conversion and phase out

m dwt

Year

0

50

100

150

200

250

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

With current orderbook:Accumulated fleet increase 1990 - 2002 (13 years) : 26 m dwtAccumulated fleet increase 2003 - 2012 (10 years) : 224 m dwt

Based on LR Fairplay database

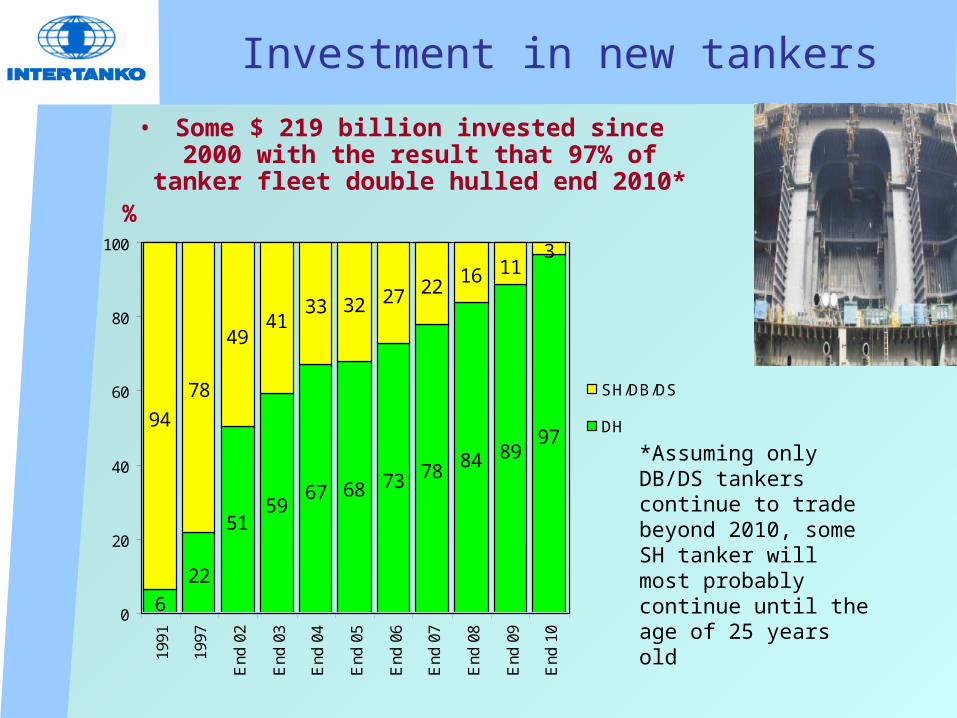

Investment in new tankers

• Some $ 219 billion invested since 2000 with the result that 97% of tanker fleet

double hulled end 2010*

*Assuming only DB/DS tankers continue to trade beyond 2010, some SH tanker will most probably continue until the age of 25 years old

%

6

22

5159

67 68 73 7884 89

9794

78

4941

33 32 27 2216 11

3

0

20

40

60

80

100

1991

1997

End

02

End

03

End

04

End

05

End

06

End

07

End

08

End

09

End

10

SH/DB/DS

DH

% dwt share:

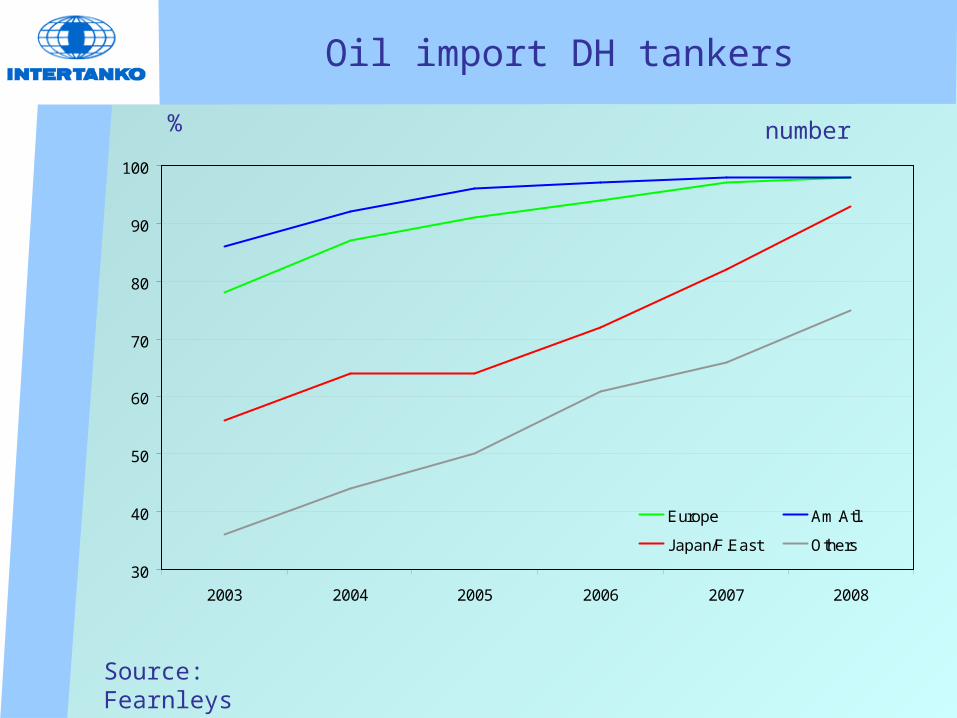

Oil import DH tankers

Source: Fearnleys

% number

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008

Europe Am.Atl.

Japan/F.East Others

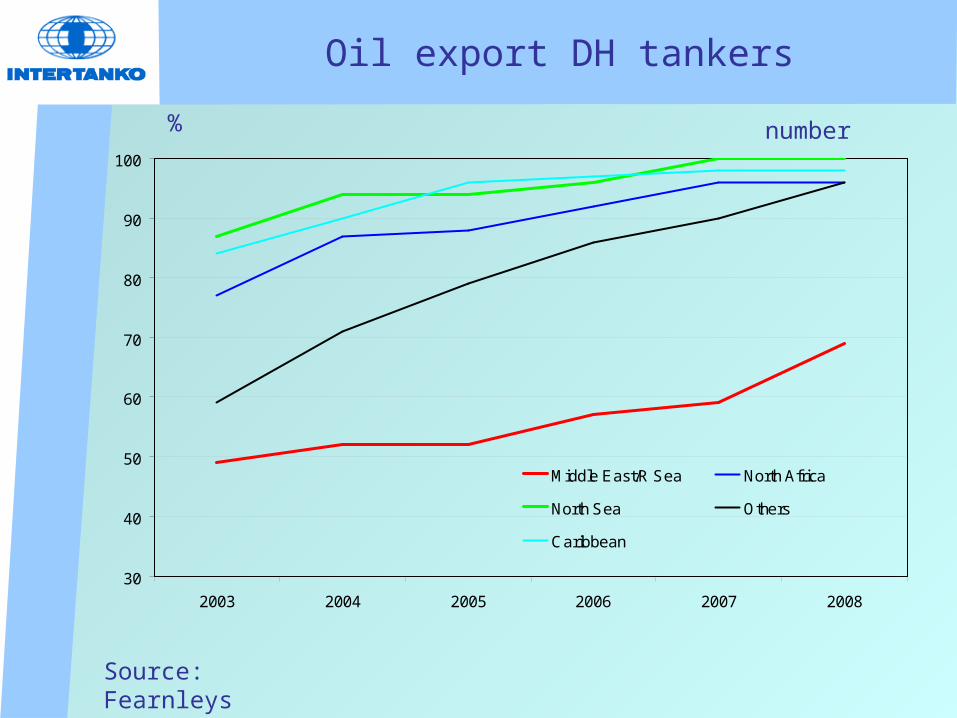

Oil export DH tankers

Source: Fearnleys

% number

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008

Middle East/R Sea North Africa

North Sea Others

Caribbean

SH trading beyond 2010?

– Australia No– China No– EU No– Mexico No– Romania No– S Korea No– Philippines No– UAE No

no official note to IMO on

– Bahamas Yes– Barbados Yes– Liberia Yes– Marshall Isl. Yes– Panama Flag Yes– Japan Yes– Singapore Yes– India Yes– Hong Kong * Yes

*20 years

Flag/Port States positions MARPOL 20 Trading until the age of 25 years

– United States N/A OPA90

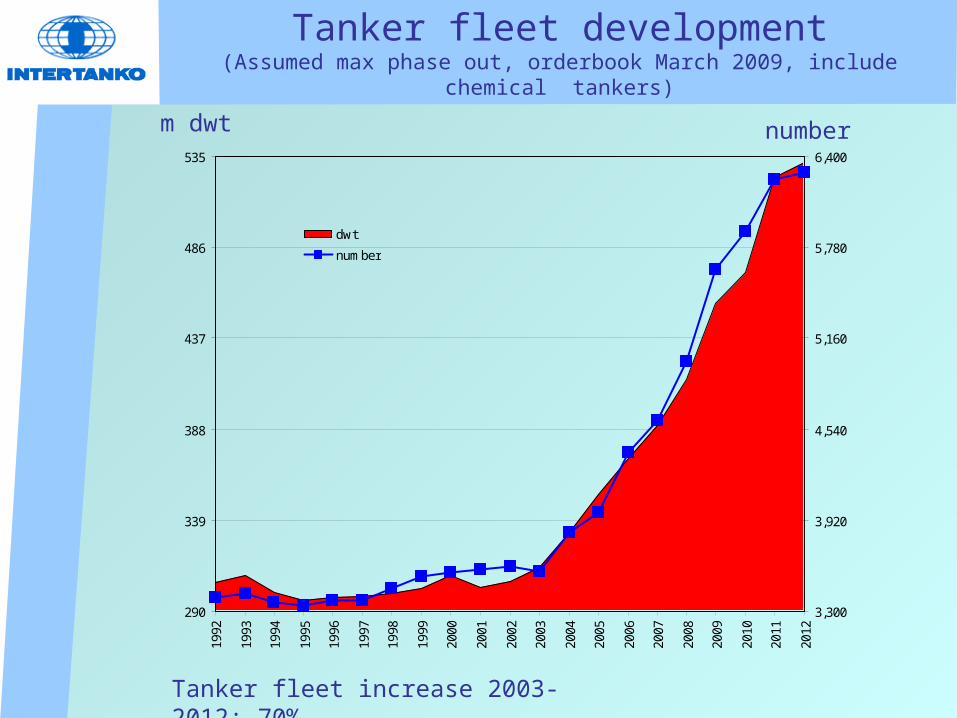

Tanker fleet development(Assumed max phase out, orderbook March 2009, include chemical tankers)

Tanker fleet increase 2003-2012: 70%

m dwt number

290

339

388

437

486

535

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

3,300

3,920

4,540

5,160

5,780

6,400

dwt

number

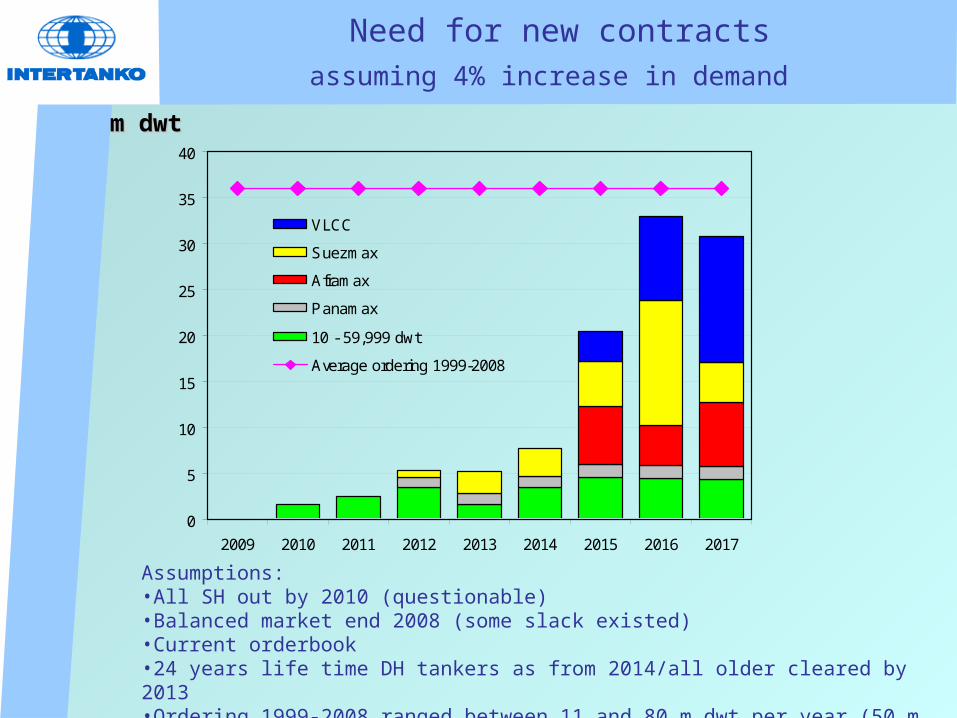

Need for new contractsassuming 4% increase in demand

m dwtm dwt

Assumptions:•All SH out by 2010 (questionable)•Balanced market end 2008 (some slack existed)•Current orderbook •24 years life time DH tankers as from 2014/all older cleared by 2013•Ordering 1999-2008 ranged between 11 and 80 m dwt per year (50 m dwt in 2008)

0

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013 2014 2015 2016 2017

VLCC

Suezmax

Aframax

Panamax

10 - 59,999 dwt

Average ordering 1999-2008

Need for new contractsassuming 4% increase in demand

Conclusion

Conclusion

• A tanker surplus is building up unless demand is strong

• No need for additional tanker orders over the next of years

Recommended