Practical applications of the Government’s Infrastructure Carbon Review

Dr Jean-Yves CherruaultSustain Ltd

Tel: [email protected]

South-West Low Carbon Business Breakfast

February 2015

John SmithSainsbury’s PLC

“Infrastructure is the backbone of any modern, successful and

competitive economy”

• Build on the previous NIP publications from 2010-12, holistic

approach in assessing to challenges facing infrastructure in the UK,

and developing plans for future action

• Plan of action for the next decade for public investment and

infrastructure

HM Treasury, National Infrastructure Plan (NIP) 2013

NIP

1. Strengthening the delivery of government infrastructure projects

2. Streamlining the planning system

3. Optimising efficiency and value for money via:

• Promoting cross-sectoral working, addressing skills requirements

• Infrastructure Costs Review: Cost Review Programme, Final

Report, Spring 2014;

Key workstream:

• Infrastructure Carbon Review: Demonstrate how saving

carbon saves money

NIP: Creating the right environment for delivery

NIP

John SmithSainsbury’s PLC

Why does reducing capital and operational carbon

make good business sense?

• Reduces costs

• Unlocks innovation and drives better solutions

• Drives resource efficiency

• Provides competitive advantages

• Contribution to climate change mitigation

“Pursuing a low carbon agenda stimulates innovation, making

businesses more competitive not only in their home markets but

on the international stage too”

Report is targeted at Infrastructure leaders – who can effect change

Purpose of ICR 2013 report: “To make carbon

reduction part of the DNA of infrastructure

in the UK”

ICR

John SmithSainsbury’s PLC

ICR

We can successfully drive down

carbon when asked, but this is rarely

a contractual requirement. Clients

need to demand reductions and

provide incentives!We want to demonstrate best practice

in reducing carbon, but the regulatory

environment does not support action

in this area

Carbon reduction makes a lot of

sense, BUT we can’t direct clients to

drive low carbon solutions because it

is not part of the mandate from the

Government!If carbon reduction makes so much

sense, why don’t they just get on and

do it??

Contractors

Clients

RegulatorsGovernment

Structural blockages in the value chain: Who will move

first?

John SmithSainsbury’s PLC

A summary of the key terminology used in the Infrastructure

Carbon Review:

• Capital carbon, or ‘CapCarb’ = Emissions associated with

creation of the asset. It is the same as the ‘cradle to construction

embodied carbon’. Therefore once the asset is constructed and

ready to use it is beyond the boundaries of capital carbon.

• Operational Carbon, or ‘OpCarb’ = emissions associated with

the operation and maintenance of an asset. This includes

energy to operate the asset and the embodied carbon of

material maintenance and repair.

• Whole life carbon = CapCab + OpCarb

Terminology

ICR

Our businessConclusions

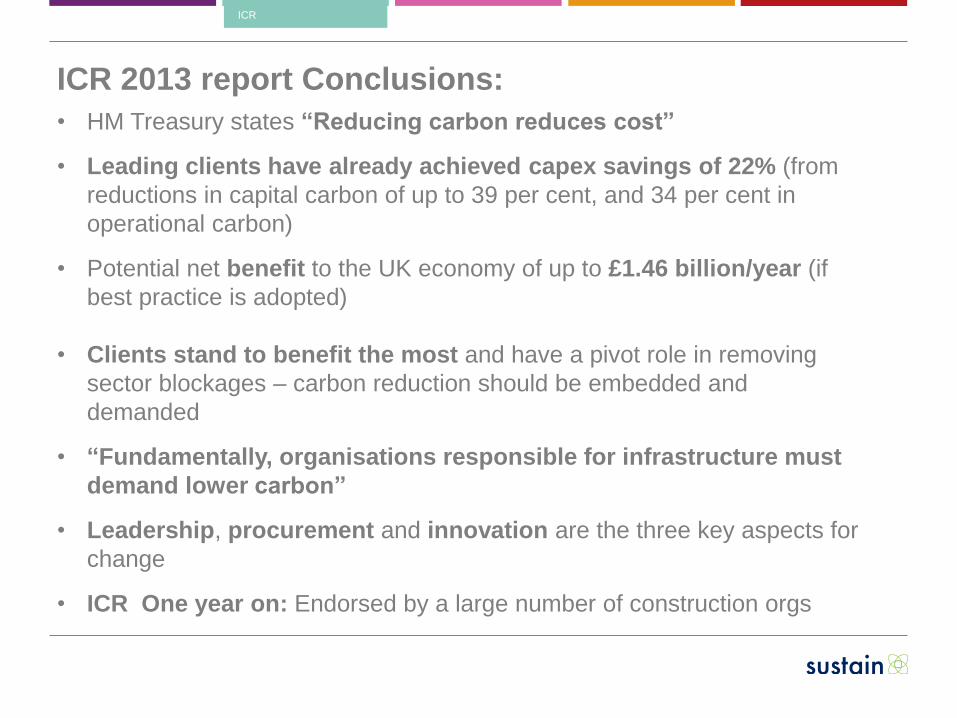

• HM Treasury states “Reducing carbon reduces cost”

• Leading clients have already achieved capex savings of 22% (from

reductions in capital carbon of up to 39 per cent, and 34 per cent in

operational carbon)

• Potential net benefit to the UK economy of up to £1.46 billion/year (if

best practice is adopted)

• Clients stand to benefit the most and have a pivot role in removing

sector blockages – carbon reduction should be embedded and

demanded

• “Fundamentally, organisations responsible for infrastructure must

demand lower carbon”

• Leadership, procurement and innovation are the three key aspects for

change

• ICR One year on: Endorsed by a large number of construction orgs

ICR 2013 report Conclusions:

High level driversICR

NIP and Transport: London Underground

• NIP 2013 highlights the importance of the London Underground

by stating that it “provides the connectivity required to unlock

investment in underdeveloped parts of the city”. Aside from

Crossrail, the LU commands a large proportion of capital value

(£8.9bn) within London’s Projects and Programmes pipeline

London Underground

London Underground and London

• London forecast to grow by twice the population of Bristol by

2022 (8.4m to 9.4m)

• LU passenger demand to grow by 60% by 2050

• Station infrastructure will continue to be created and upgraded

for years to come….opportunities to address carbon early as

advocated by the ICR

London Underground

Improvement Plan

(Stations)

Future Stations

Phase 3

Dialogue input &

Lessons learned

Phase 2

Proof of Concept

Study

Phase 1

Study

ITT Dialogue Detail design

Vision: Wider Business

Existing

Policies

2014 2015 2016+

Req

uir

em

en

ts

Camden Town

Holborn

Elephant & Castle

Kennington & NLE

Old Street

Paddington

Victoria

Tottenham Court Road

Bond Street

Bank

Paddington BLL

VauxhallInnovative Contractor Engagement (ICE)

Next Tranche

of

Future Stations

London Underground ICR Response A methodological approach

Carbon Reduction Maturity Matrix

London Underground

Level Level One – Foundation

Level Two – Embed

Level Three – Practice

Level Four – Excel

1) Strategy, Policy and Leadership

2) Management and Governance

3) Procurement and Supply Chain

4) Station Technologies, Data and Information

• ICR: Infrastructure clients stand to benefit the most. They have a

pivot role in removing sector blockages to make carbon reduction

happen

• The organisation has a unique opportunity to respond to the

energy and carbon challenge through the Station Capacity

Programme: LU can use energy and carbon in these programmes

as a proxy for higher value so that the organisation gets the most

from station assets and technologies

• Take early action in the station upgrade programme: Station

upgrade represents an opportunity to mitigate significant carbon

related cost increase at (almost) no cost increase

• Policy context is right, Infrastructure Cost Review: Alongside the

Green Construction Board, the government is working with industry

to develop a new standard (Publicly Available Specification) to

support the recommendations of the Infrastructure Carbon Review

Key opportunities

Opportunities

• Leadership, procurement and innovation are the three key aspects

for change (ICR), however: • Leadership: Leaders require less risks and more certainty for value for

money

• Innovation: The positive impact of innovation needs to be quantified and

valued in the procurement process. Innovative solutions can lack track

record of performance

• Procurement: Suppliers require clarity and consistency in the process to

provide a platform for engagement (ICE)

• Current focus is on the delivery of “hard” aspects: Carbon and

sustainability are often viewed as “Soft” matters and projects

constraints rather than opportunities

• Whole Life Carbon needs to be embedded in key industry

developments to become business as usual: Asset Management

Standard (ISO 55000) and Whole Life Cost methodologies and tools,

Systems Approach and BIM

Key challenges

Challenges

Recommended