Economic Impacts on New Jersey of Upgrading PSE&G’s

Susquehanna-Roseland Transmission System

Dr. Joseph J. Seneca

Dr. Michael L. Lahr

Dr. James W. Hughes

Will Irving

May 2009

Table of Contents

EXECUTIVE SUMMARY ........................................................................................................ i

INTRODUCTION................................................................................................................... 1

Project Background...................................................................................................... 1

Analytical Approach..................................................................................................... 1

Organization of the Report .......................................................................................... 2

ECONOMIC IMPACT ANALYSIS .......................................................................................... 3

Expenditures Considered in the Analysis................................................................... 3

R/ECON™ Input-Output Model................................................................................. 3

Transmission Line and Towers (Monopole Structures)............................................ 4

Expenditure Assumptions ............................................................................................ 4

Economic Impacts ....................................................................................................... 6

Transmission Line and Towers (Lattice Structures)............................................... 11

Expenditure Assumptions .......................................................................................... 11

Economic Impacts ..................................................................................................... 13

East Hanover/Roseland Switching Station............................................................... 17

Expenditure Assumptions .......................................................................................... 17

Economic Impacts ..................................................................................................... 18

Jefferson Switching Station........................................................................................ 22

Expenditure Assumptions .......................................................................................... 22

Economic Impacts ..................................................................................................... 23

Combined Economic Impacts (Monopole Towers).................................................. 27

Combined Economic Impacts (Lattice Towers)....................................................... 30

CONCLUSION .................................................................................................................... 33

APPENDIX A: ECONOMIC AND DEMOGRAPHIC PROFILES AND DYNAMICS.................... 34

APPENDIX B: INPUT-OUTPUT ANALYSIS ......................................................................... 53

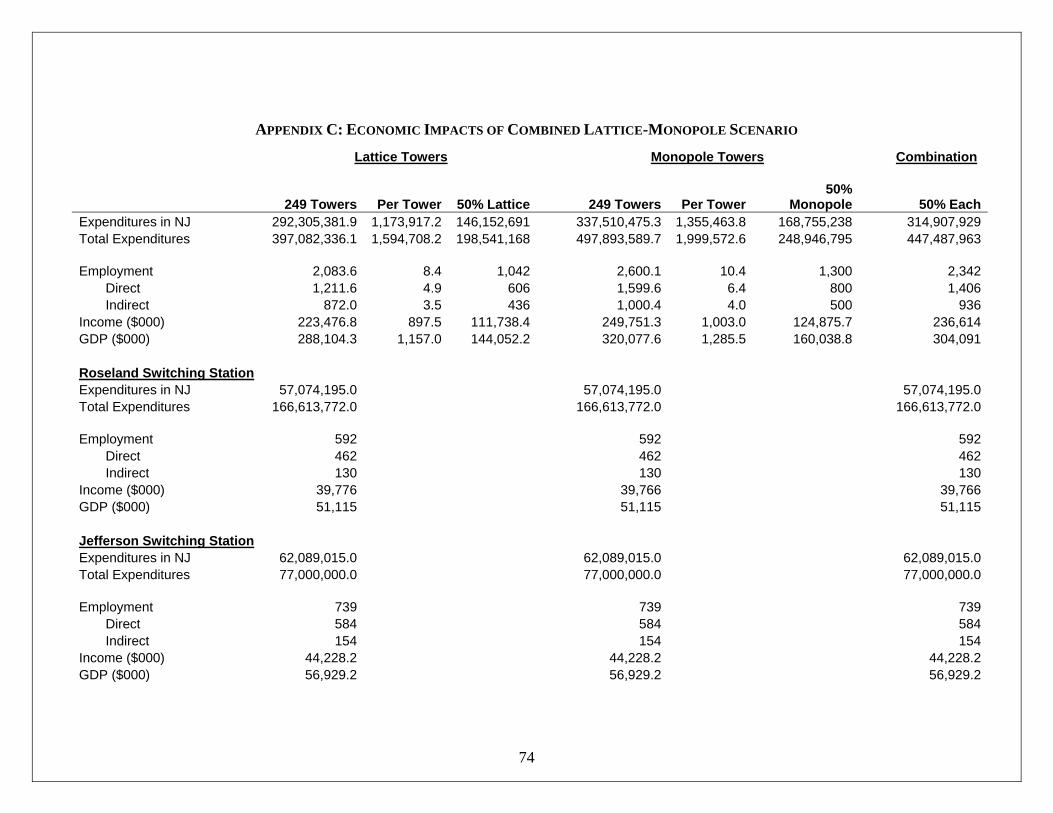

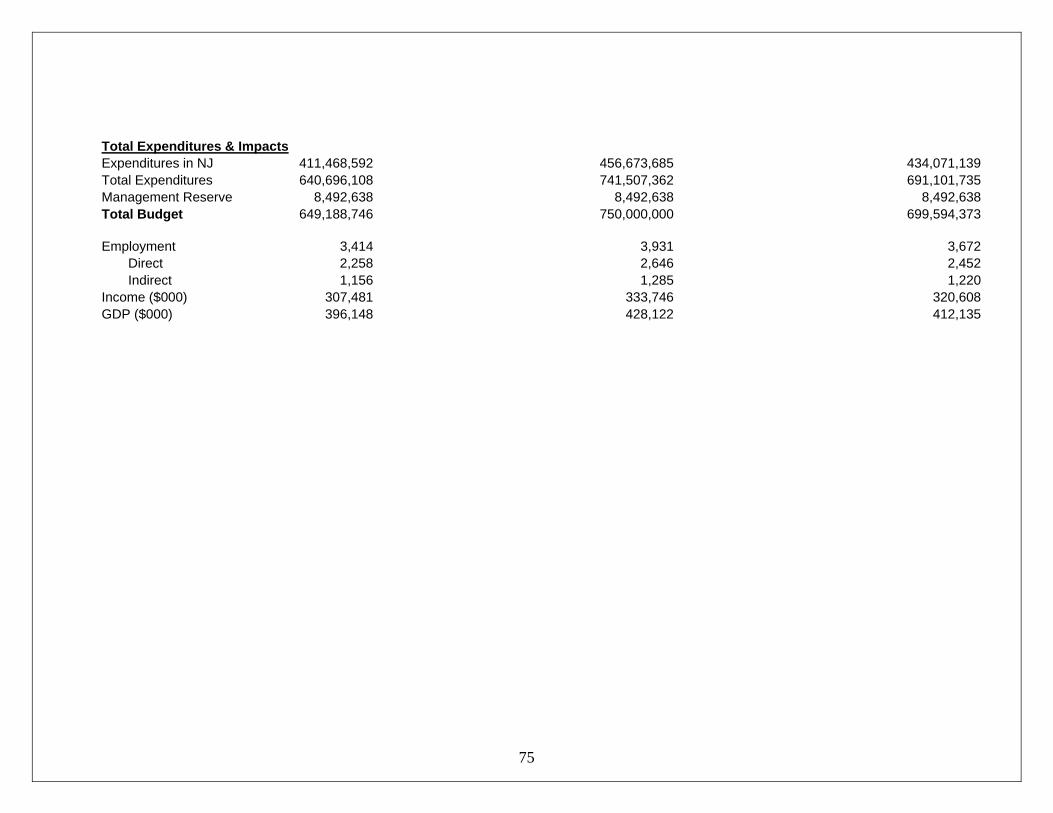

APPENDIX C: ECONOMIC IMPACTS OF COMBINED LATTICE-MONOPOLE SCENARIO... 74

i

EXECUTIVE SUMMARY

This report presents the estimated economic impacts in New Jersey of the

approximately $649 - $750 million in expenditures required for construction of the New

Jersey portion of the proposed upgrade to PSE&G’s Susquehanna-Roseland

Transmission Network. The economic impacts estimated are only those associated with

the expenditures to be made on construction of the network upgrade, and do not reflect

any of the potential ongoing economic impacts of the increased transmission capacity

once the upgrade is complete.

The proposed upgrade would add 500 kV of additional power transmission

capacity to the existing 230 kV network. This analysis examines the economic impacts

of the construction of two switching stations and of the transmission line and towers

required to accommodate the increased transmission capacity. Alternative scenarios are

presented to reflect the two different types of tower structures that may be used. If all

249 towers were lattice structures, the estimated total expenditures for the project would

be approximately $649 million, whereas if all the towers were monopole structures, the

estimated expenditures would total $750 million. (Appendix C at the end of the report

provides the aggregate expenditures and economic impacts for a 50%-50% split between

the two types of towers.)

The estimated economic impacts include both direct impacts and indirect impacts.

Direct impacts are those directly associated with the project expenditures, such as the

construction employment required for the project and purchases of material to be used in

construction of the switching station and towers. Indirect impacts are those generated by

the multiplier effects of the initial expenditures, as the salaries paid to workers and the

business revenue generated by the expenditures made on materials in New Jersey are then

re-spent throughout the economy, generating further economic activity and impacts in the

form of employment, gross domestic product, compensation (income) and tax revenues.

Based on the two expenditure scenarios associated with the different types of

towers and on the associated range of project expenditures to be made in New Jersey, the

following economic impacts were estimated:

ii

• Employment. It is estimated that construction of the switching stations and

transmission line and towers will generate from 3,415 to 3,931 total job-years

(one job-year is equal to one job lasting one year). This includes from 2,258 to

2,646 direct job-years, including construction employment, as well as design

work, consulting services and other

• Gross Domestic Product. It is estimated that the construction of the upgrade will

generate between $396.1 and $428.1 million in gross domestic product for New

Jersey.

• Compensation. It is estimated that the total compensation generated by both the

direct and the indirect employment generated by the construction of the upgraded

network will be between $307.5 million and $333.8 million.

• State Tax Revenues. It is estimated that the construction phase of the project will

generate between $8 and $9 million in state taxes.

• Local Tax Revenues. It is estimated that the construction phase of the project will

generate between $7.9 and $9.9 million in local taxes.

1

INTRODUCTION

This report presents the findings of an economic impact analysis of the

approximately $649-$750 million in expenditures required for construction of the New

Jersey portion of the proposed upgrade to PSE&G’s Susquehanna-Roseland

Transmission Network.

Project Background

PJM Interconnection, the regional authority overseeing electricity transmission in

all or part of 13 states, including New Jersey and Pennsylvania, has determined that the

existing 230 kV capacity of the transmission line running from Susquehanna,

Pennsylvania to Roseland, New Jersey is not sufficient to accommodate projected

demand growth in coming years. As a result, PJM has directed PSE&G of New Jersey

and PPL of Pennsylvania to upgrade the network by adding a new 500 kV capacity

transmission line to the existing network. The upgrade will require not only the addition

of the new power line itself, but also construction of new towers to accommodate both

the new 500 kV, as well as the existing 230 kV line, and the construction of two new

switching stations along the transmission route, one in Jefferson, New Jersey and one

near the line’s terminus in Roseland, New Jersey. This economic impact analysis covers

the estimated $649-$750 million of expenditures required for construction of the New

Jersey portion of the new line, including the two switching stations to be built in New

Jersey.

Analytical Approach

The economic impacts of the construction of the new transmission line in New

Jersey are estimated using the R/ECON™ Input-Output model developed and maintained

by the Center for Urban Policy Research at Rutgers University’s Edward J. Bloustein

School of Planning and Public Policy. The model provides estimates of a broad and

detailed range of economic impacts, including employment, gross domestic product,

income and tax revenues. A detailed description of the model and its methodology is

provided with the analysis.

2

The construction of each component of the new transmission infrastructure is

analyzed individually. That is, the transmission line and towers are analyzed separately,

as are each of the two switching stations. In addition, two separate analyses of the

transmission line and tower infrastructure are provided. Because the existing towers

currently carrying the 230 kV line do not meet the specifications required to handle two

lines of the given capacities discussed, an additional 249 new towers are required in New

Jersey. Some of these towers will be monopole structures (i.e., a single pole with

branches holding the transmission lines), while others will be wider lattice-type

structures. Because each of these tower types requires a different mix of material and

labor inputs, two separate analyses are provided, one assuming that all towers are

monopole, and the other assuming that all towers are lattice.

Organization of the Report

The report begins with a brief overview of the expenditures considered in the

analysis. This is followed by a description of the R/ECON™ Input-Output Model and its

application. Next, the analyses of the separate components of the transmission network

are presented. These analyses consist of the all-monopole transmission line and towers,

the all-lattice transmission line and towers, the Jefferson Switching Station, and the

Roseland/East Hanover Switching Station. Each analysis consists of a review of the

input expenditures used in the R/ECON™ Input-Output Model and a detailed

presentation of the estimated economic impacts of those expenditures. A final section

presents the combined impacts of the total investment in New Jersey for both the all-

monopole and all-lattice tower scenarios. This is followed by a brief summary and

conclusions. An appendix presents a brief economic profile of the areas in New Jersey

where the new transmission line would be built.

3

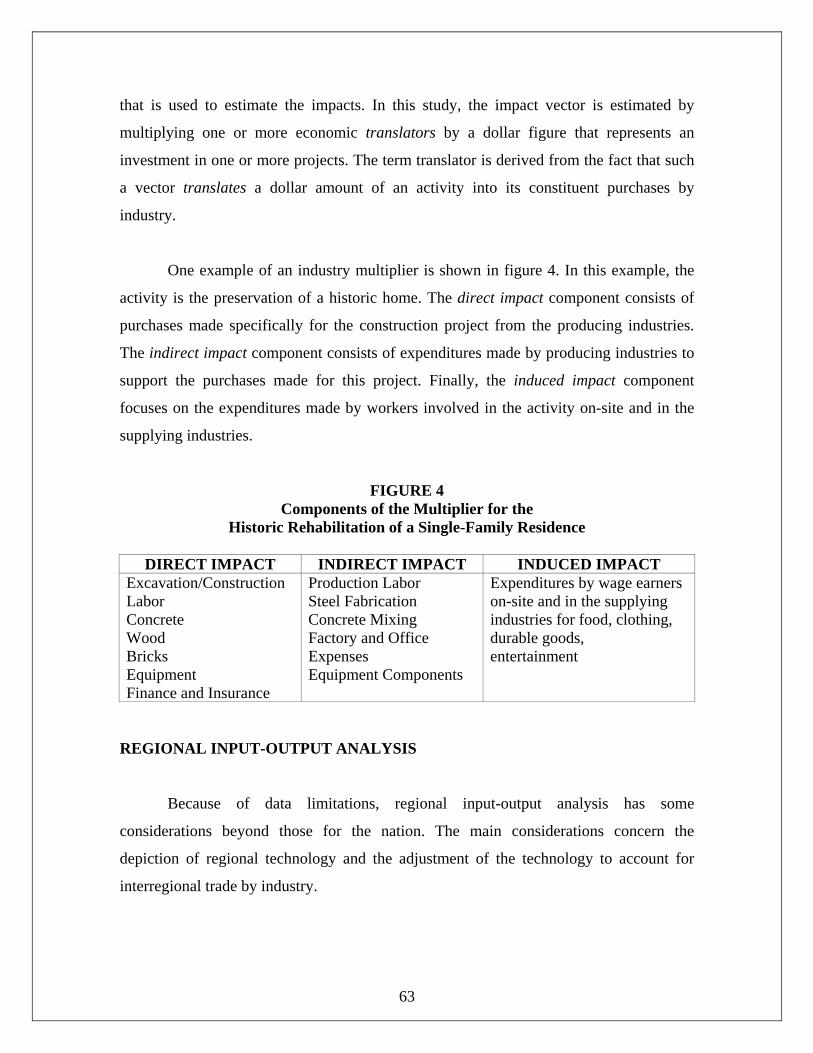

ECONOMIC IMPACT ANALYSIS

Expenditures Considered in the Analysis

Because of the highly specialized nature of the power transmission materials and

equipment needed for construction of the upgraded network, almost all the required

material will be purchased outside of New Jersey. As such, the majority of the impacts

measured in this analysis are generated via the employment of construction workers and

the purchase of specialized services associated with the project. The majority of these

workers and services are expected to come from New Jersey. Detailed explanations of

the specific expenditures made in New Jersey are provided for each component of the

analysis.

R/ECON™ Input-Output Model

The R/ECON™ Input-Output Model at the Center for Urban Policy Research at

the Bloustein School of Planning and Public Policy was used to measure the economic

impacts of the proposed expenditures for the Susquehanna-Roseland network upgrade.

The R/ECON™ model consists of 515 individual sectors of the New Jersey economy and

measures the effect of changes in expenditures in one industry on economic activity in all

other industries. Thus, the expenditures made on labor, materials, legal and design

services, and other inputs for the transmission line have both direct economic effects as

those expenditures become incomes and revenues for workers and businesses, and

subsequent indirect effects as those workers and businesses, in turn, spend those dollars

on other things – consumer goods, business investment expenditures, which, in turn,

become income for other workers and businesses. This income gets further spent, and so

on.

In summary, the R/ECON™ Input-Output model estimates both the direct

economic effects of the initial expenditures (in terms of jobs and income) and the indirect

(or multiplier) effects (in additional jobs and income) of the subsequent economic activity

that occurs following the initial expenditures. The model also estimates the gross

domestic product for New Jersey and the tax revenues generated by the combined direct

and indirect new economic activity caused by the initial spending.

4

Transmission Line and Towers (Monopole Structures)

Expenditure Assumptions

This estimate of the economic impacts for construction of the transmission line

and towers for the Susquehanna-Roseland network assumes that all towers are monopole

structures.1 In order to reflect the full scope of the expenditures included in PSE&G’s

cost estimates for construction of the transmission line and towers portion of the

upgraded network, it was necessary to make several assumptions and adjustments to the

various expenditure items included in PSE&G’s initial cost estimates. Following is an

explanation of this process.

PSE&G’s estimated total cost for construction of the transmission line and

monopole towers is $497.9 million.

The base cost of construction estimated by PSE&G for the all-monopole

transmission line and towers, including labor, materials, third party

professional services and PSE&G support, was $380.4 million, with an

additional 11% in estimated inflation costs (“escalation”) and an

additional 20% in contingency.

In order to incorporate all potential expenditures into the analysis, the

escalation (11%) and contingency (20%) estimates were distributed

proportionately between the costs of labor and material and the other

costs (professional services, PSE&G support, etc.) according to their

respective shares of the $380.4 million base cost.

In addition, the OH&P on labor (25% of base labor and material costs) and

material (10% of base labor and material costs), the Scope Modifications

on labor (15% of base labor and material costs) and material (15% of base

1 Scenarios assuming all monopole and all lattice tower structures are presented in the body of the report. A spreadsheet indicating the aggregate impacts of using 50% of each type of tower structure is presented in Appendix C.

5

labor and material costs), and the Inefficiencies on labor (18% of base

labor and material costs) were also distributed proportionately across the

labor and material components of the base construction cost structure.

The separate expenditures on labor and materials for the laying of tower

foundations were not broken out in PSE&G’s cost specifications. For

purposes of the analysis, 65% of the $59.4 million in expenditures on

foundations was allocated to labor, and the remaining 35% to material.

These various adjustments resulted in total allocations of $247.8 million

for transmission line construction labor and $171.9 million for material.

All direct construction labor was assumed to come from North Jersey.

All specialty materials (conductors, insulators, field wire, tower structures,

etc.) are assumed to be purchased from outside of New Jersey. As such, of

the material expenditures, only the concrete and other material used for

construction of the tower foundations was incorporated into the impact

estimate.

Of the “Other Costs” (i.e., professional services, PSE&G support, etc.)

associated with construction of the transmission line, the costs for

consulting services provided by Louis Berger, the cost of soil borings, the

costs of appraisals, title and mapping costs, and the costs of PSE&G legal

fees were incorporated into the economic impact estimate. These

expenditures totaled approximately $8 million.

In addition, PSE&G’s support costs were allocated according to the shares

reflected in the itemized cost breakdowns of PSE&G support in the cost

estimates for the two switching stations. All of these costs were

incorporated into the economic impact estimate, with the exception of

6

“Licensing/Permits/Bonds/Builder’s Risk.” Of this last category,

approximately $3.8 million in builder’s risk insurance was incorporated

into the expenditure estimates.

As a result of these assumptions and adjustments, $337.5 million of the

total $497.9 million estimate for construction of the transmission line and

towers (or 67.8%) was allocated to expenditures on labor, material and

services in New Jersey.

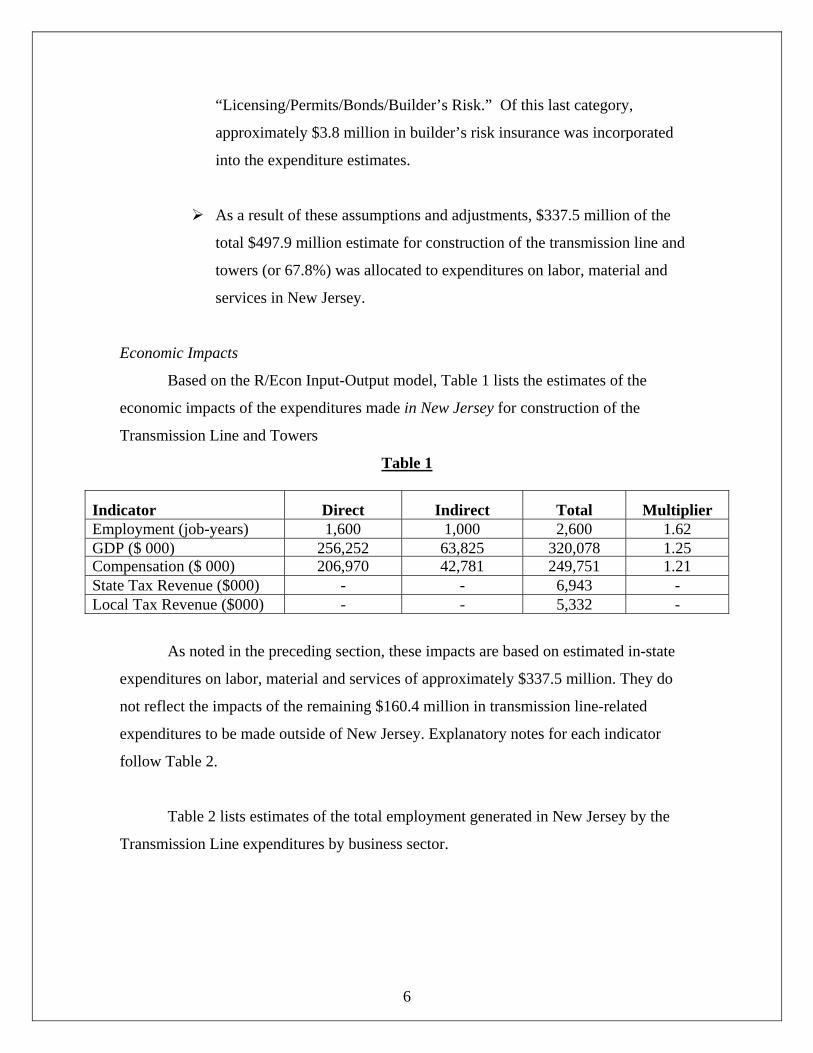

Economic Impacts

Based on the R/Econ Input-Output model, Table 1 lists the estimates of the

economic impacts of the expenditures made in New Jersey for construction of the

Transmission Line and Towers

Table 1

Indicator Direct Indirect Total Multiplier Employment (job-years) 1,600 1,000 2,600 1.62 GDP ($ 000) 256,252 63,825 320,078 1.25Compensation ($ 000) 206,970 42,781 249,751 1.21 State Tax Revenue ($000) - - 6,943 - Local Tax Revenue ($000) - - 5,332 -

As noted in the preceding section, these impacts are based on estimated in-state

expenditures on labor, material and services of approximately $337.5 million. They do

not reflect the impacts of the remaining $160.4 million in transmission line-related

expenditures to be made outside of New Jersey. Explanatory notes for each indicator

follow Table 2.

Table 2 lists estimates of the total employment generated in New Jersey by the

Transmission Line expenditures by business sector.

7

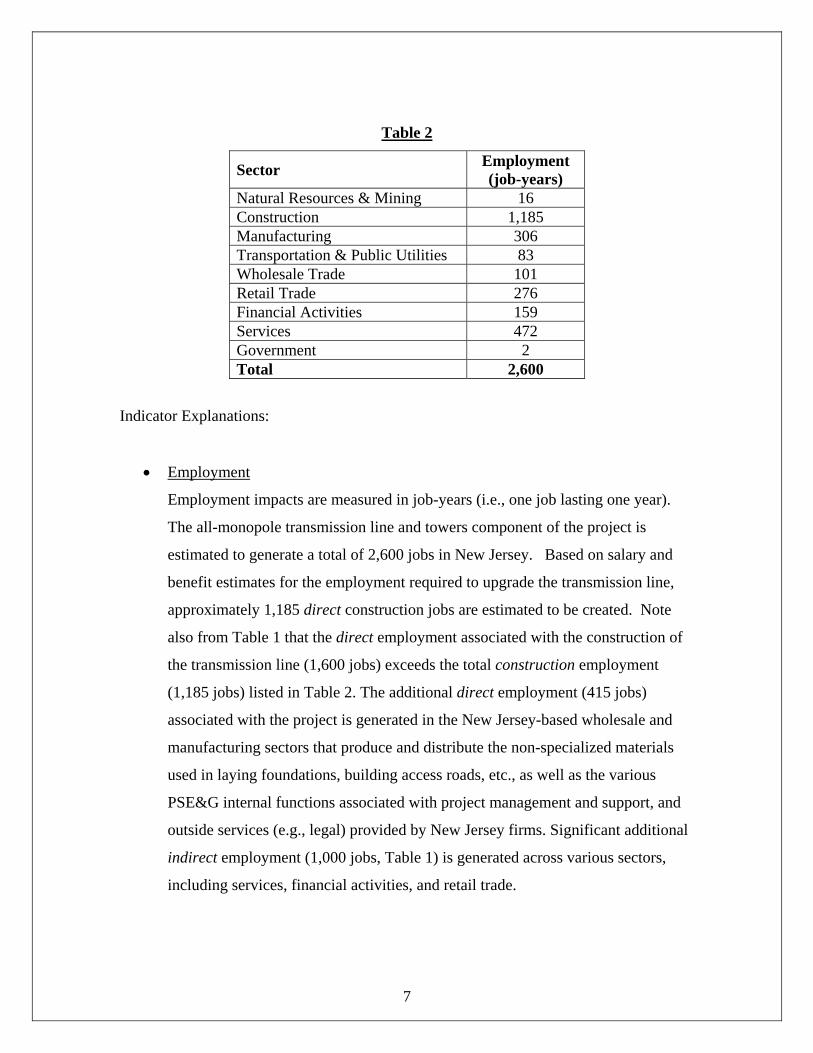

Table 2

Sector Employment (job-years)

Natural Resources & Mining 16 Construction 1,185 Manufacturing 306 Transportation & Public Utilities 83 Wholesale Trade 101 Retail Trade 276 Financial Activities 159 Services 472 Government 2 Total 2,600

Indicator Explanations:

• Employment

Employment impacts are measured in job-years (i.e., one job lasting one year).

The all-monopole transmission line and towers component of the project is

estimated to generate a total of 2,600 jobs in New Jersey. Based on salary and

benefit estimates for the employment required to upgrade the transmission line,

approximately 1,185 direct construction jobs are estimated to be created. Note

also from Table 1 that the direct employment associated with the construction of

the transmission line (1,600 jobs) exceeds the total construction employment

(1,185 jobs) listed in Table 2. The additional direct employment (415 jobs)

associated with the project is generated in the New Jersey-based wholesale and

manufacturing sectors that produce and distribute the non-specialized materials

used in laying foundations, building access roads, etc., as well as the various

PSE&G internal functions associated with project management and support, and

outside services (e.g., legal) provided by New Jersey firms. Significant additional

indirect employment (1,000 jobs, Table 1) is generated across various sectors,

including services, financial activities, and retail trade.

8

• GDP

Note that the total GDP generated in the state ($320.1 million, Table 1) is close to

the total expenditures estimated for New Jersey. By explicitly excluding those

material expenditures that are to be made outside of New Jersey, the model

minimizes the economic “leakage” that would normally be reflected were they to

have been included. That is, were the excluded $160.4 million in expenditures to

be included, the relative proportion of impacts leaked from the New Jersey

economy would be higher. This leakage is reflected in the per-million dollar

impacts reported below.

• Compensation

Compensation represents the total wages, salaries and supplements to wages and

salaries (i.e., employer contributions to government and private pension funds)

paid for all direct and indirect jobs generated as a result of the project

expenditures made in New Jersey. The transmission line and monopole towers

component is estimated to generate $249.8 million in compensation in New

Jersey.

• State Tax Revenues

State tax revenues are comprised of the income taxes associated with the salaries

paid to the workers in the direct and indirect jobs associated with the project, and

with the sales associated with the economic output generated by the project. The

transmission line and monopole towers component is estimated to generate $6.9

million in state tax revenues.

• Local Tax Revenues

The estimates of the increase in local tax revenues are for the entire state. The

increase represents a long-run estimate of property tax revenues generated by

payment of residential and commercial property taxes from the personal and

business incomes generated by the project and/or resulting from improvements

9

made to property caused by the increased economic activity generated by the

project.

Local tax revenues increase because the additional economic activity from the

transmission line project generates income for workers and revenues for

business2. The increases in personal incomes and in business revenues are, in

part, used to pay property taxes and to improve properties (both residential and

commercial). Thus, households benefitting from the additional jobs and resulting

incomes acquire and/or improve residential properties, and are able to pay rents

and mortgages and the associated property taxes. Similarly, business income and

profits also increase as a direct result of higher sales and output caused by the

project. Businesses subsequently acquire and/or improve their properties.

Historical New Jersey fiscal and economic data are used to measure the

relationship between business revenues and the amount of commercial property

tax revenues collected, and between household incomes and the amount of

residential property tax revenues collected.3 Given the increases in both

household income and the business revenues caused by the expenditures made on

the transmission line, the R/ECON™ Input-Output Model invokes the known

statistical relation of local property tax revenues to both household income and

business revenues in order to estimate the addition to local tax revenues

attributable to the transmission line project.

It is important to note that this additional tax revenue occurs over a period of time.

It is not an immediately generated impact. The economic sequence is as follows.

The additions/improvements to residential and commercial property financed by

the higher household incomes and higher business revenues are, in time, captured

by higher property assessments, which, in turn, generate higher local tax

2 For businesses, the revenue increase is measured in terms of value-added, and it is the change in value-added in the business sector that is the basis for the estimated change in property tax revenues. 3 For the entire state, approximately 76% of total local property tax revenues are attributable to residential property; with approximately 21% derived primarily from commercial and industrial property.

10

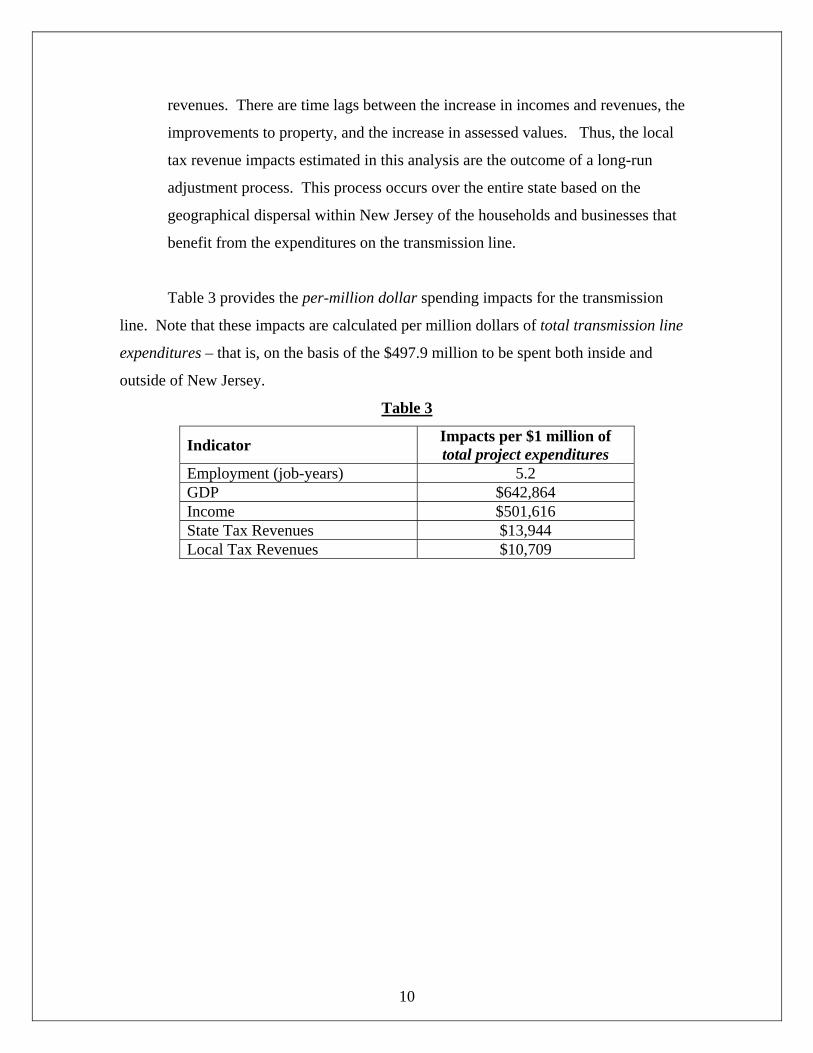

revenues. There are time lags between the increase in incomes and revenues, the

improvements to property, and the increase in assessed values. Thus, the local

tax revenue impacts estimated in this analysis are the outcome of a long-run

adjustment process. This process occurs over the entire state based on the

geographical dispersal within New Jersey of the households and businesses that

benefit from the expenditures on the transmission line.

Table 3 provides the per-million dollar spending impacts for the transmission

line. Note that these impacts are calculated per million dollars of total transmission line

expenditures – that is, on the basis of the $497.9 million to be spent both inside and

outside of New Jersey.

Table 3

Indicator Impacts per $1 million of total project expenditures

Employment (job-years) 5.2 GDP $642,864 Income $501,616 State Tax Revenues $13,944 Local Tax Revenues $10,709

11

Transmission Line and Towers (Lattice Structures)

Expenditure Assumptions

This estimate of the economic impacts for construction of the transmission line

and towers for the Susquehanna-Roseland network assumes that all towers are lattice

structures. In order to reflect the full scope of the expenditures included in PSE&G’s cost

estimates for construction of the transmission line and towers portion of the upgraded

network, it was necessary to make several assumptions and adjustments to the various

expenditure items included in PSE&G’s initial cost estimates. Following is an

explanation of this process.

PSE&G’s estimated total cost for construction of the transmission line and

lattice towers is $397.1 million.

The base cost of construction estimated by PSE&G for the all-lattice

transmission line and towers, including labor, materials, third party

professional services and PSE&G support, was $303.2 million, with an

additional 11% in estimated inflation costs (“escalation”) and an

additional 20% in contingency.

In order to incorporate all potential expenditures into the analysis, the

escalation (11%) and contingency (20%) estimates were distributed

proportionately between the costs of labor and material and the other

costs (professional services, PSE&G support, etc.) according to their

respective shares of the $303.2 million base cost.

In addition, the OH&P on labor (25% of base labor and material costs) and

material (10% of base labor and material costs), the Scope Modifications

on labor (15% of base labor and material costs) and material (15% of base

labor and material costs), and the Inefficiencies on labor (18% of base

labor and material costs) were also distributed proportionately across the

labor and material components of the base construction cost structure.

12

The separate expenditures on labor and materials for the laying of tower

foundations were not disaggregated in PSE&G’s cost specifications. For

purposes of the analysis, 65% of the $20.2 million in expenditures on

foundations was allocated to labor, and the remaining 35% to material.

These various adjustments resulted in total allocations of $239.2 million

for transmission line construction labor and $74.4 million for material.

All direct construction labor was assumed to come from North Jersey.

All specialty materials (conductors, insulators, field wire, tower structures,

etc.) are assumed to be purchased from outside of New Jersey. As such, of

the material expenditures, only the concrete and other material used for

construction of the tower foundations was incorporated into the impact

estimate.

Of the “Other Costs” (i.e., professional services, PSE&G support, etc.)

associated with construction of the transmission line, the costs for

consulting services provided by Louis Berger, the cost of soil borings, the

costs of appraisals, title and mapping costs, and the costs of PSE&G legal

fees were incorporated into the economic impact estimate. These

expenditures totaled approximately $8.1 million.

In addition, PSE&G’s support costs were allocated according to the shares

reflected in the itemized cost breakdowns of PSE&G support in the cost

estimates for the two switching stations. All of these costs were

incorporated into the economic impact estimate, with the exception of

“Licensing/Permits/Bonds/Builder’s Risk.” Of this last category,

approximately $3.1 million in builder’s risk insurance was incorporated

into the expenditure estimates.

13

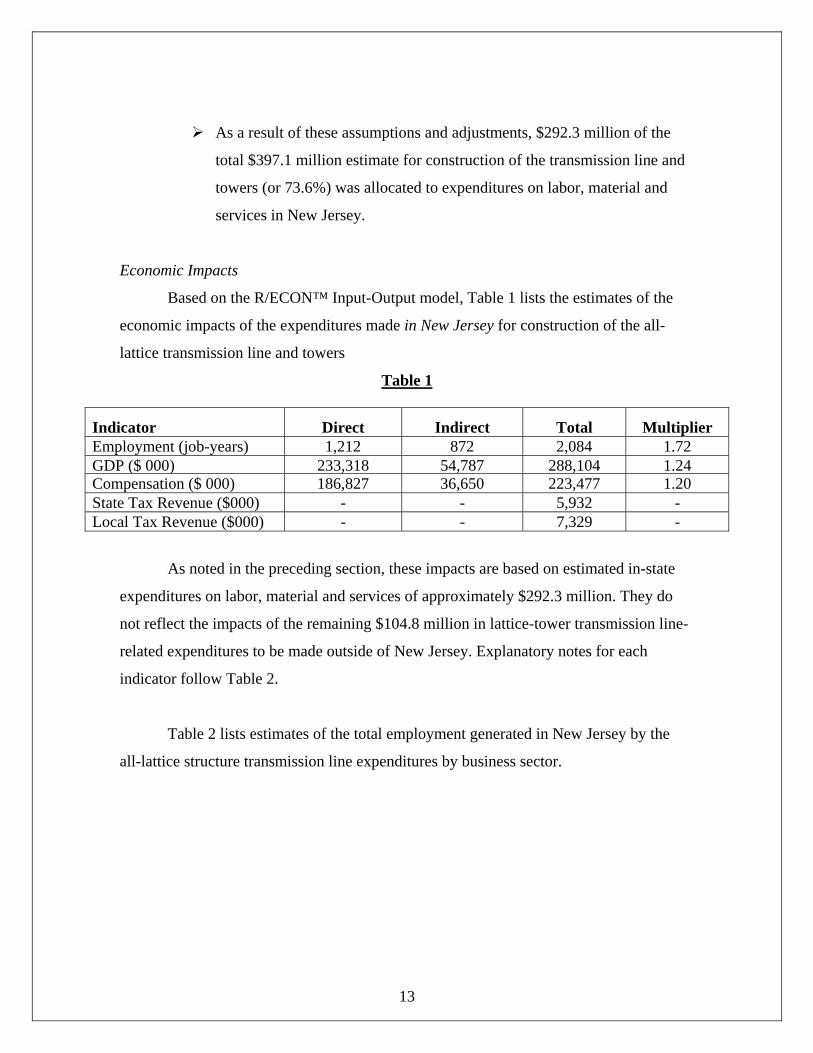

As a result of these assumptions and adjustments, $292.3 million of the

total $397.1 million estimate for construction of the transmission line and

towers (or 73.6%) was allocated to expenditures on labor, material and

services in New Jersey.

Economic Impacts

Based on the R/ECON™ Input-Output model, Table 1 lists the estimates of the

economic impacts of the expenditures made in New Jersey for construction of the all-

lattice transmission line and towers

Table 1

Indicator Direct Indirect Total Multiplier Employment (job-years) 1,212 872 2,084 1.72 GDP ($ 000) 233,318 54,787 288,104 1.24Compensation ($ 000) 186,827 36,650 223,477 1.20 State Tax Revenue ($000) - - 5,932 - Local Tax Revenue ($000) - - 7,329 -

As noted in the preceding section, these impacts are based on estimated in-state

expenditures on labor, material and services of approximately $292.3 million. They do

not reflect the impacts of the remaining $104.8 million in lattice-tower transmission line-

related expenditures to be made outside of New Jersey. Explanatory notes for each

indicator follow Table 2.

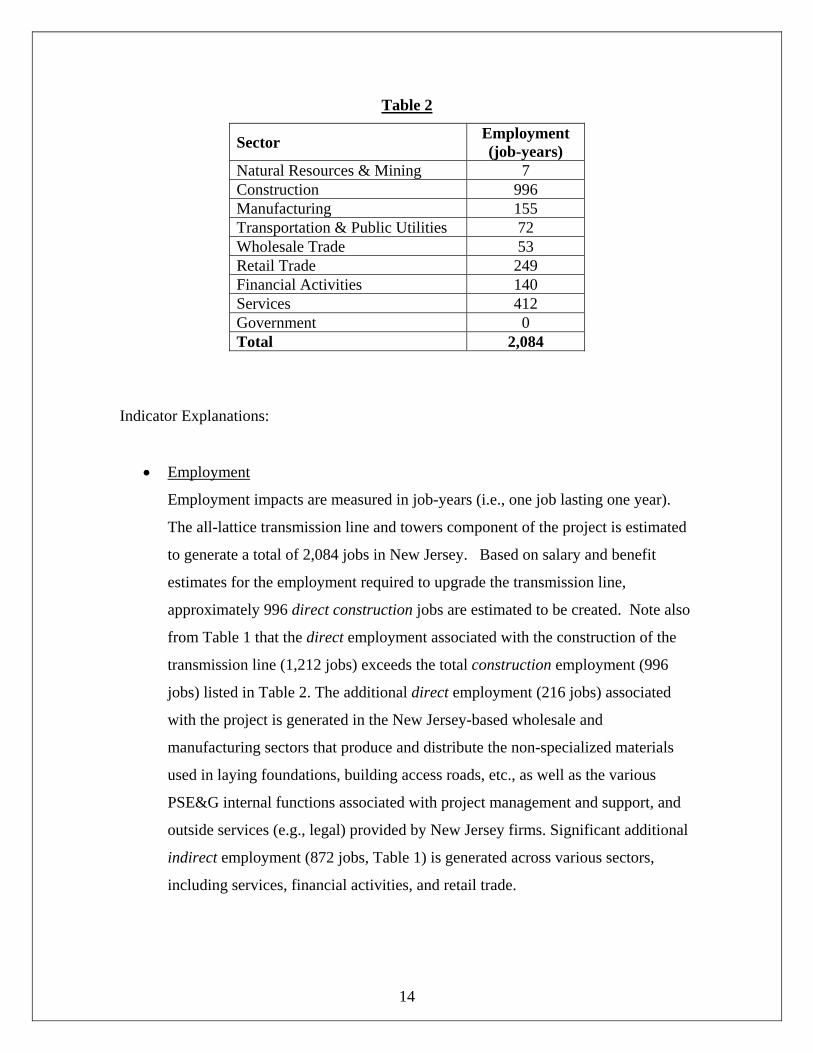

Table 2 lists estimates of the total employment generated in New Jersey by the

all-lattice structure transmission line expenditures by business sector.

14

Table 2

Sector Employment (job-years)

Natural Resources & Mining 7 Construction 996 Manufacturing 155 Transportation & Public Utilities 72 Wholesale Trade 53 Retail Trade 249 Financial Activities 140 Services 412 Government 0 Total 2,084

Indicator Explanations:

• Employment

Employment impacts are measured in job-years (i.e., one job lasting one year).

The all-lattice transmission line and towers component of the project is estimated

to generate a total of 2,084 jobs in New Jersey. Based on salary and benefit

estimates for the employment required to upgrade the transmission line,

approximately 996 direct construction jobs are estimated to be created. Note also

from Table 1 that the direct employment associated with the construction of the

transmission line (1,212 jobs) exceeds the total construction employment (996

jobs) listed in Table 2. The additional direct employment (216 jobs) associated

with the project is generated in the New Jersey-based wholesale and

manufacturing sectors that produce and distribute the non-specialized materials

used in laying foundations, building access roads, etc., as well as the various

PSE&G internal functions associated with project management and support, and

outside services (e.g., legal) provided by New Jersey firms. Significant additional

indirect employment (872 jobs, Table 1) is generated across various sectors,

including services, financial activities, and retail trade.

15

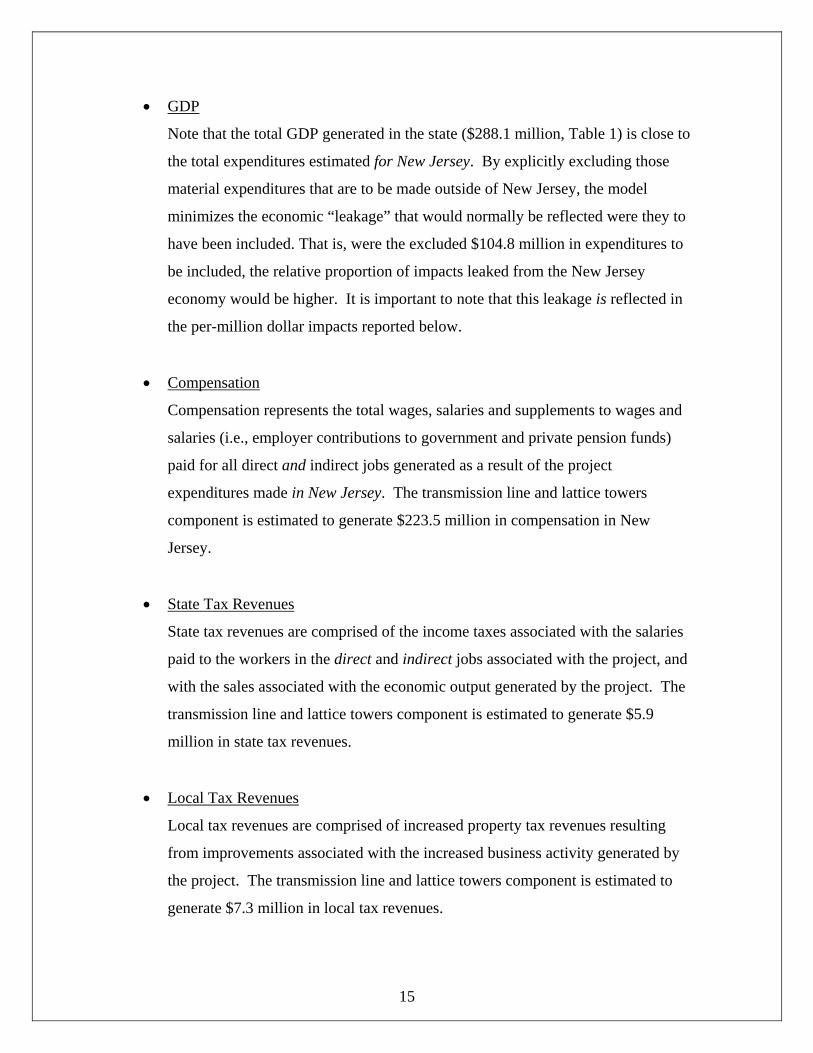

• GDP

Note that the total GDP generated in the state ($288.1 million, Table 1) is close to

the total expenditures estimated for New Jersey. By explicitly excluding those

material expenditures that are to be made outside of New Jersey, the model

minimizes the economic “leakage” that would normally be reflected were they to

have been included. That is, were the excluded $104.8 million in expenditures to

be included, the relative proportion of impacts leaked from the New Jersey

economy would be higher. It is important to note that this leakage is reflected in

the per-million dollar impacts reported below.

• Compensation

Compensation represents the total wages, salaries and supplements to wages and

salaries (i.e., employer contributions to government and private pension funds)

paid for all direct and indirect jobs generated as a result of the project

expenditures made in New Jersey. The transmission line and lattice towers

component is estimated to generate $223.5 million in compensation in New

Jersey.

• State Tax Revenues

State tax revenues are comprised of the income taxes associated with the salaries

paid to the workers in the direct and indirect jobs associated with the project, and

with the sales associated with the economic output generated by the project. The

transmission line and lattice towers component is estimated to generate $5.9

million in state tax revenues.

• Local Tax Revenues

Local tax revenues are comprised of increased property tax revenues resulting

from improvements associated with the increased business activity generated by

the project. The transmission line and lattice towers component is estimated to

generate $7.3 million in local tax revenues.

16

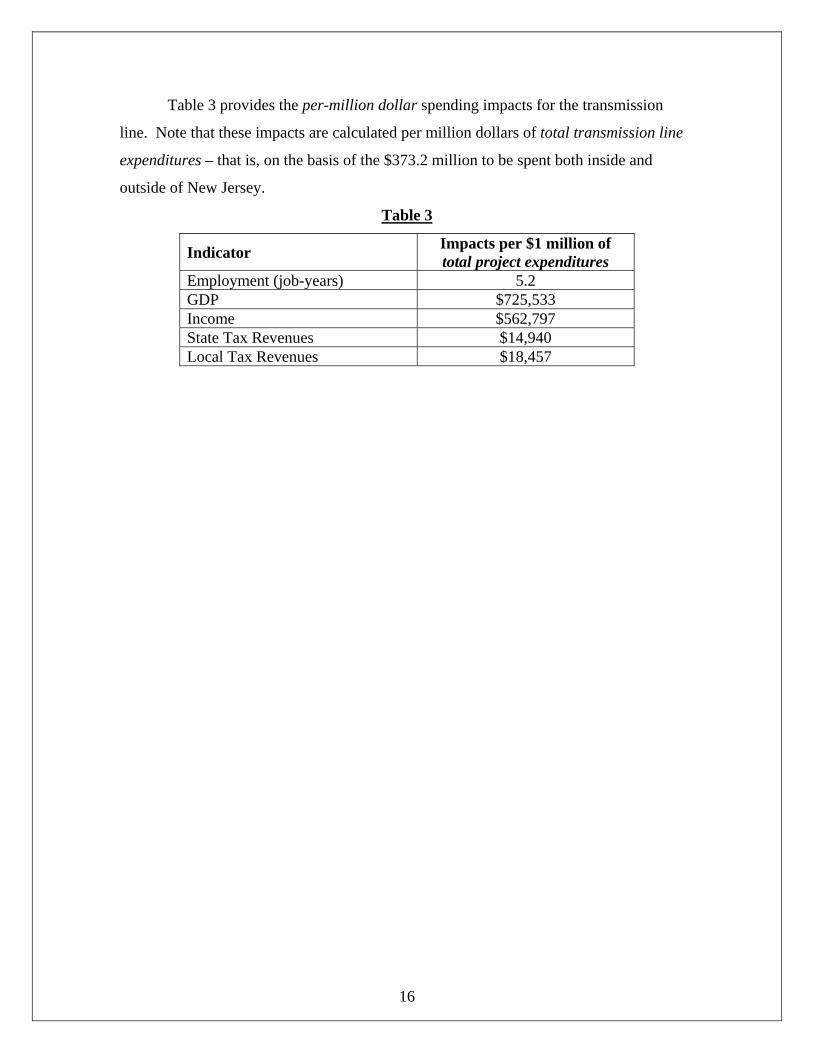

Table 3 provides the per-million dollar spending impacts for the transmission

line. Note that these impacts are calculated per million dollars of total transmission line

expenditures – that is, on the basis of the $373.2 million to be spent both inside and

outside of New Jersey.

Table 3

Indicator Impacts per $1 million of total project expenditures

Employment (job-years) 5.2 GDP $725,533 Income $562,797 State Tax Revenues $14,940 Local Tax Revenues $18,457

17

East Hanover/Roseland Switching Station

Expenditure Assumptions

In order to reflect the full range of expenditures incorporated into PSE&G’s cost

estimates for construction of the East Hanover/Roseland switching station portion of the

upgraded Susquehanna-Roseland network, the following assumptions and adjustments

were made to the various construction expenditures.

The total cost of construction for the East Hanover/Roseland switching

station was estimated at $166.6 million, including $125.6 million in base

costs and $41 million in contingency.

The contingency and escalation (32.6%) estimates were distributed

proportionately between the contractor’s labor and material costs, the

professional services costs, and the PSE&G support costs according to

their respective shares of the $125.6 million base cost.

Expenditures on transformers, circuit breakers, disconnect switches, and

other electronic equipment were assumed to be made outside of New

Jersey.

All direct construction labor was assumed to come from North Jersey.

As a result of these assumptions and adjustments, $57.1 million of the

total $166.6 million estimate for construction (or 34.3%) of the East

Hanover/Roseland Switching Station, was allocated to expenditures on

labor, material and services in New Jersey.

18

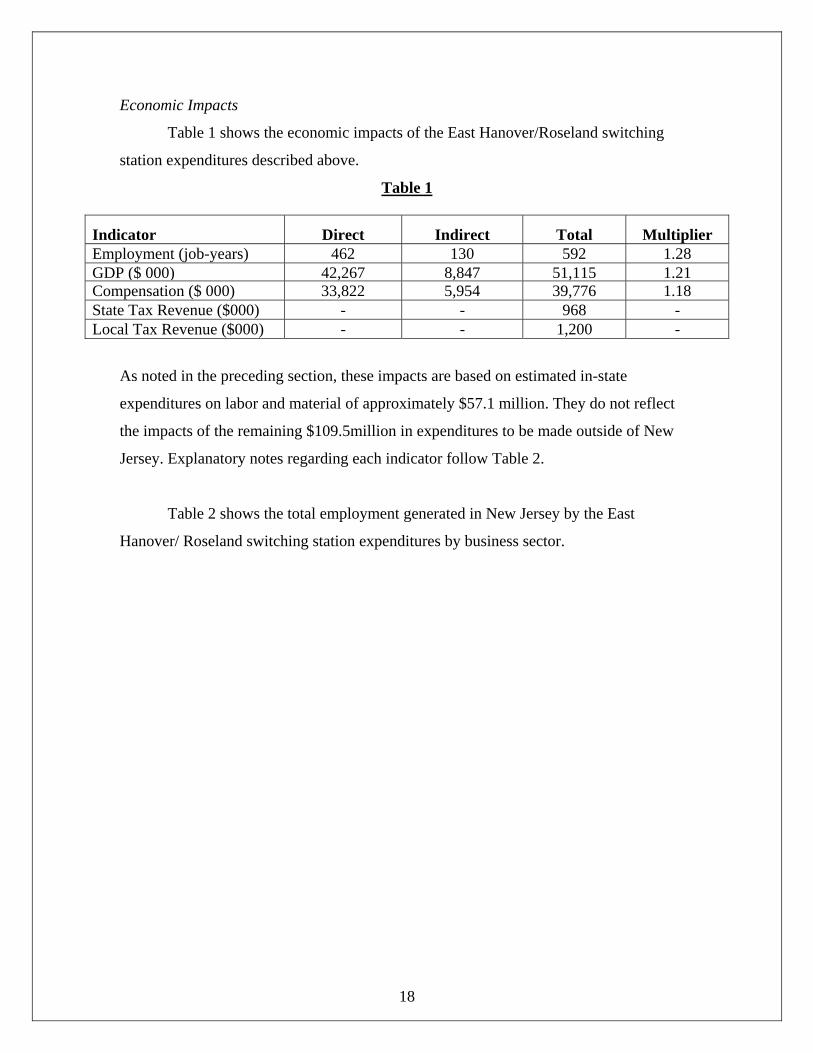

Economic Impacts

Table 1 shows the economic impacts of the East Hanover/Roseland switching

station expenditures described above.

Table 1

Indicator Direct Indirect Total Multiplier Employment (job-years) 462 130 592 1.28 GDP ($ 000) 42,267 8,847 51,115 1.21Compensation ($ 000) 33,822 5,954 39,776 1.18 State Tax Revenue ($000) - - 968 - Local Tax Revenue ($000) - - 1,200 -

As noted in the preceding section, these impacts are based on estimated in-state

expenditures on labor and material of approximately $57.1 million. They do not reflect

the impacts of the remaining $109.5million in expenditures to be made outside of New

Jersey. Explanatory notes regarding each indicator follow Table 2.

Table 2 shows the total employment generated in New Jersey by the East

Hanover/ Roseland switching station expenditures by business sector.

19

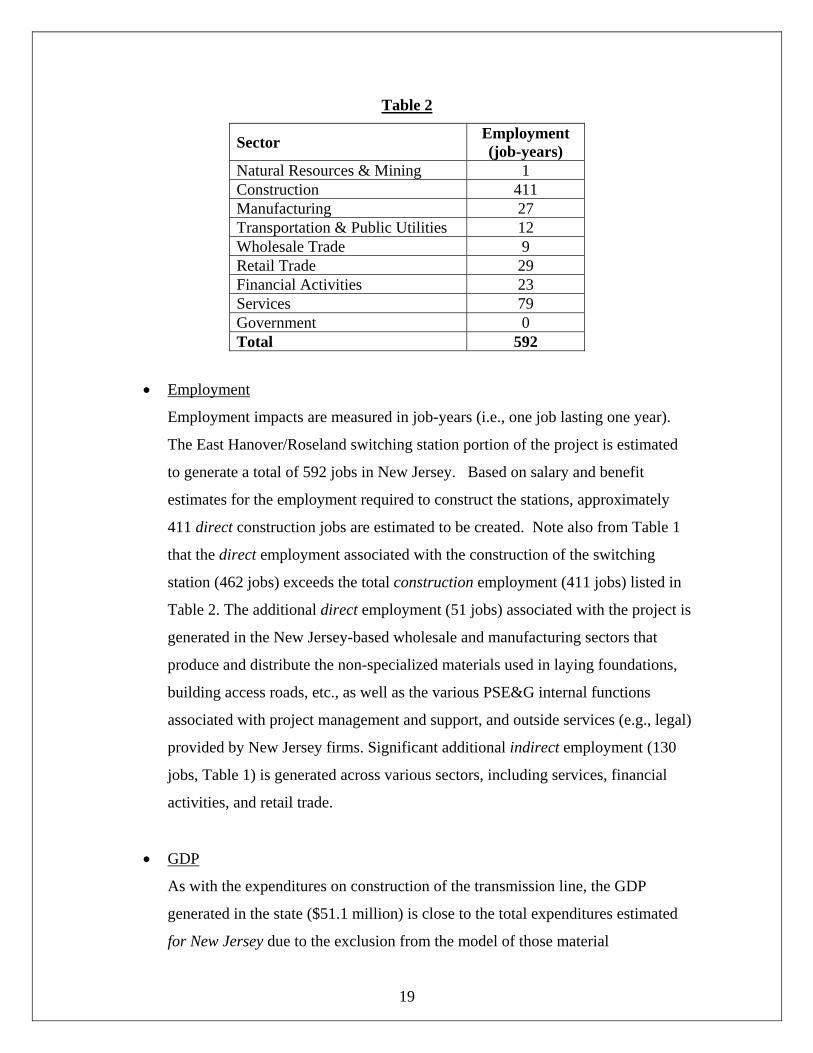

Table 2

Sector Employment (job-years)

Natural Resources & Mining 1 Construction 411 Manufacturing 27 Transportation & Public Utilities 12 Wholesale Trade 9 Retail Trade 29 Financial Activities 23 Services 79 Government 0 Total 592

• Employment

Employment impacts are measured in job-years (i.e., one job lasting one year).

The East Hanover/Roseland switching station portion of the project is estimated

to generate a total of 592 jobs in New Jersey. Based on salary and benefit

estimates for the employment required to construct the stations, approximately

411 direct construction jobs are estimated to be created. Note also from Table 1

that the direct employment associated with the construction of the switching

station (462 jobs) exceeds the total construction employment (411 jobs) listed in

Table 2. The additional direct employment (51 jobs) associated with the project is

generated in the New Jersey-based wholesale and manufacturing sectors that

produce and distribute the non-specialized materials used in laying foundations,

building access roads, etc., as well as the various PSE&G internal functions

associated with project management and support, and outside services (e.g., legal)

provided by New Jersey firms. Significant additional indirect employment (130

jobs, Table 1) is generated across various sectors, including services, financial

activities, and retail trade.

• GDP

As with the expenditures on construction of the transmission line, the GDP

generated in the state ($51.1 million) is close to the total expenditures estimated

for New Jersey due to the exclusion from the model of those material

20

expenditures that are to be made outside of New Jersey. The per-million-dollar

impacts reported below reflect the impact on New Jersey per million dollars of

total expenditures, including those expenditures made outside of the state.

• Compensation

Compensation represents the total wages, salaries and supplements to wages and

salaries (i.e., employer contributions to government and private pension funds)

paid for all direct and indirect jobs generated as a result of the project

expenditures made in New Jersey. The construction of the East

Hanover/Roseland switching station is estimated to generate $39.8 million in

compensation in New Jersey.

• State Tax Revenues

State tax revenues are comprised of the income taxes associated with the salaries

paid to the workers in the direct and indirect jobs associated with the project, and

with the sales associated with the economic output generated by the project. The

construction of the East Hanover/ Roseland switching station is estimated to

generate $.968 million in state tax revenues.

• Local Tax Revenues

Local tax revenues are comprised of increased property tax revenues resulting

from improvements associated with the increased business activity generated by

the project. The construction of the East Hanover/Roseland switching station is

estimated to generate $1.120 million in local tax revenues.

Table 3 provides the per-million-dollar spending impacts for the East

Hanover/Roseland switching station. Note that these impacts are calculated per million

dollars of total expenditures – that is, on the basis of the $166.6 million to be spent both

inside and outside of New Jersey.

21

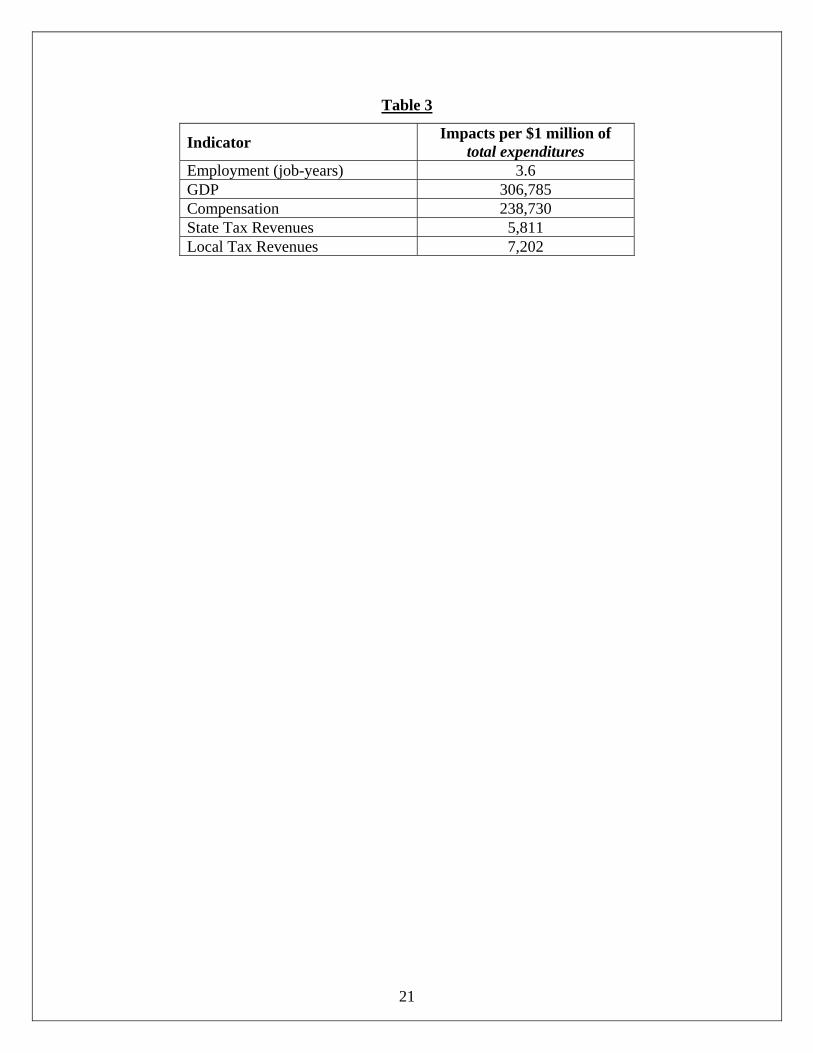

Table 3

Indicator Impacts per $1 million of total expenditures

Employment (job-years) 3.6 GDP 306,785 Compensation 238,730 State Tax Revenues 5,811 Local Tax Revenues 7,202

22

Jefferson Switching Station

Expenditure Assumptions

In order to reflect the full range of expenditures incorporated into PSE&G’s cost

estimates for construction of the Jefferson switching station portion of the upgraded

Susquehanna-Roseland network, it was necessary to make several assumptions and

adjustments to the various expenditure items listed for construction of the station.

Following is an explanation of this process.

The total cost of construction for the East Hanover/Roseland switching

station was estimated at $77 million, including $57.8 million in base costs,

$6.1 million in escalation costs and $13.1 million in contingency.

The escalation (10.5%) and contingency (22.7%) estimates were

distributed proportionately between the contractor’s labor and material

costs. The Professional Services costs and the PSE&G Support costs were

distributed according to their respective shares of the $57.8 million base

cost.

The Scope Assessment and Fees on the labor portion of the contractor’s

costs (34% of base costs) were combined with the labor costs.

Expenditures on circuit breakers, disconnect switches, and third party

professional services were assumed to be made outside of New Jersey.

Of the approximately $6.5 million in bulk material expenditures, 60% was

assumed to be electrical material, and 40% civil material, with 90% of the

electrical bulk being purchased outside New Jersey. The majority of civil

bulk material associated with site work, access roads, foundations, etc.,

was assumed to be purchased in New Jersey.

23

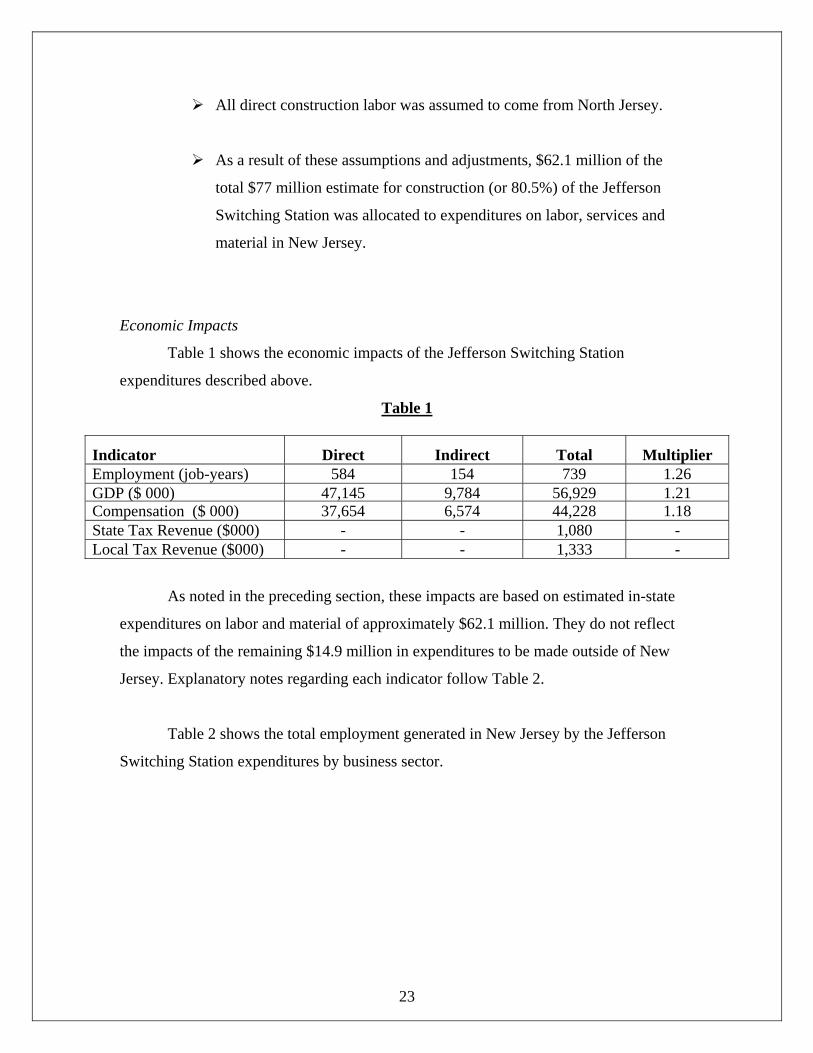

All direct construction labor was assumed to come from North Jersey.

As a result of these assumptions and adjustments, $62.1 million of the

total $77 million estimate for construction (or 80.5%) of the Jefferson

Switching Station was allocated to expenditures on labor, services and

material in New Jersey.

Economic Impacts

Table 1 shows the economic impacts of the Jefferson Switching Station

expenditures described above.

Table 1

Indicator Direct Indirect Total Multiplier Employment (job-years) 584 154 739 1.26 GDP ($ 000) 47,145 9,784 56,929 1.21Compensation ($ 000) 37,654 6,574 44,228 1.18 State Tax Revenue ($000) - - 1,080 - Local Tax Revenue ($000) - - 1,333 -

As noted in the preceding section, these impacts are based on estimated in-state

expenditures on labor and material of approximately $62.1 million. They do not reflect

the impacts of the remaining $14.9 million in expenditures to be made outside of New

Jersey. Explanatory notes regarding each indicator follow Table 2.

Table 2 shows the total employment generated in New Jersey by the Jefferson

Switching Station expenditures by business sector.

24

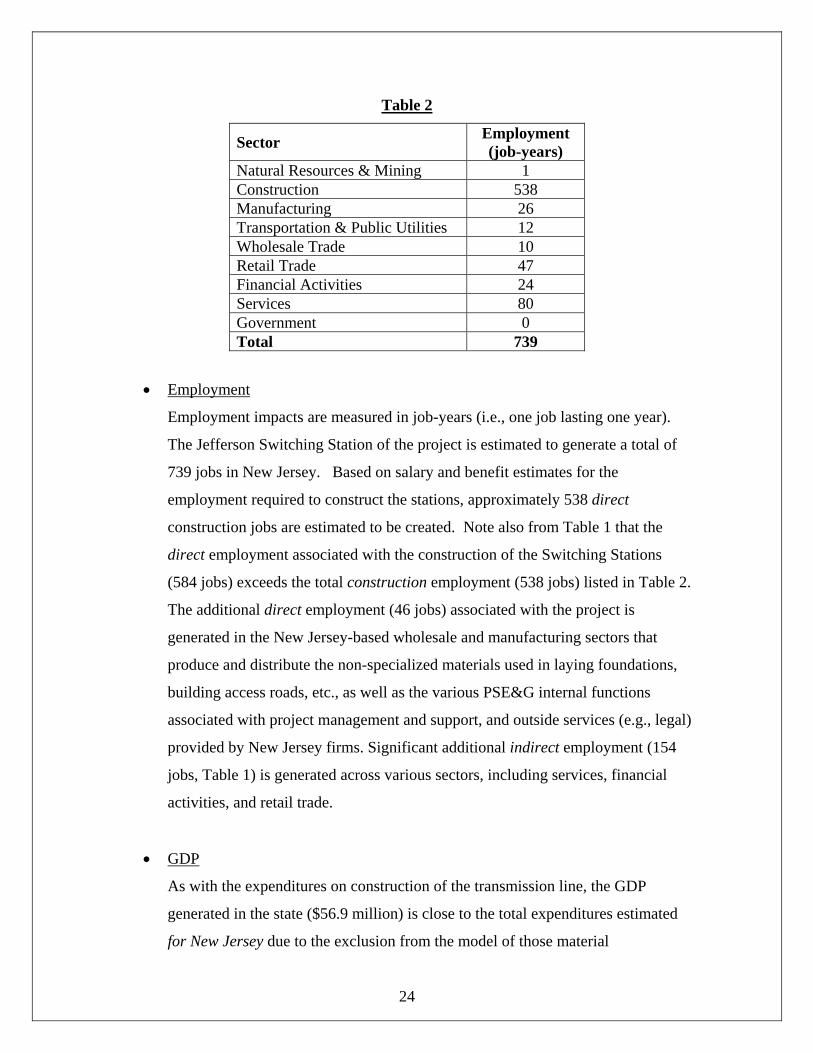

Table 2

Sector Employment (job-years)

Natural Resources & Mining 1 Construction 538 Manufacturing 26 Transportation & Public Utilities 12 Wholesale Trade 10 Retail Trade 47 Financial Activities 24 Services 80 Government 0 Total 739

• Employment

Employment impacts are measured in job-years (i.e., one job lasting one year).

The Jefferson Switching Station of the project is estimated to generate a total of

739 jobs in New Jersey. Based on salary and benefit estimates for the

employment required to construct the stations, approximately 538 direct

construction jobs are estimated to be created. Note also from Table 1 that the

direct employment associated with the construction of the Switching Stations

(584 jobs) exceeds the total construction employment (538 jobs) listed in Table 2.

The additional direct employment (46 jobs) associated with the project is

generated in the New Jersey-based wholesale and manufacturing sectors that

produce and distribute the non-specialized materials used in laying foundations,

building access roads, etc., as well as the various PSE&G internal functions

associated with project management and support, and outside services (e.g., legal)

provided by New Jersey firms. Significant additional indirect employment (154

jobs, Table 1) is generated across various sectors, including services, financial

activities, and retail trade.

• GDP

As with the expenditures on construction of the transmission line, the GDP

generated in the state ($56.9 million) is close to the total expenditures estimated

for New Jersey due to the exclusion from the model of those material

25

expenditures that are to be made outside of New Jersey. The per-million-dollar

impacts reported below reflect the impact on New Jersey per million dollars of

total expenditures, including those expenditures made outside of the state.

• Compensation

Compensation represents the total wages, salaries and supplements to wages and

salaries (i.e., employer contributions to government and private pension funds)

paid for all direct and indirect jobs generated as a result of the project

expenditures made in New Jersey. The construction of the Jefferson Switching

Station is estimated to generate $44.2 million in compensation in New Jersey.

• State Tax Revenues

State tax revenues are comprised of the income taxes associated with the salaries

paid to the workers in the direct and indirect jobs associated with the project, and

with the sales associated with the economic output generated by the project. The

construction of the Jefferson Switching Station is estimated to generate $1.1

million in state tax revenues.

• Local Tax Revenues

Local tax revenues are comprised of increased property tax revenues resulting

from improvements associated with the increased business activity generated by

the project. The construction of the Jefferson Switching Station is estimated to

generate $1.3 million in local tax revenues.

Table 3 provides the per-million-dollar spending impacts for the Jefferson

Switching Station. Note that these impacts are calculated per million dollars of total

transmission line expenditures – that is, on the basis of the $77 million to be spent both

inside and outside of New Jersey.

26

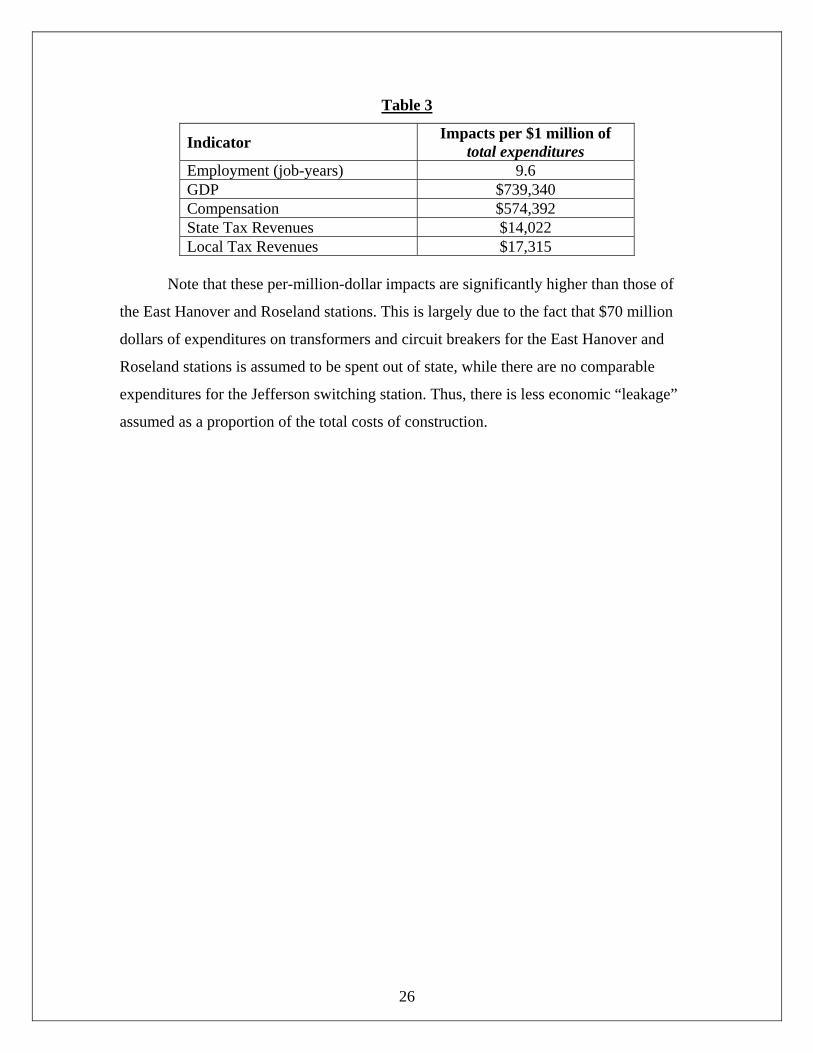

Table 3

Indicator Impacts per $1 million of total expenditures

Employment (job-years) 9.6 GDP $739,340 Compensation $574,392 State Tax Revenues $14,022 Local Tax Revenues $17,315

Note that these per-million-dollar impacts are significantly higher than those of

the East Hanover and Roseland stations. This is largely due to the fact that $70 million

dollars of expenditures on transformers and circuit breakers for the East Hanover and

Roseland stations is assumed to be spent out of state, while there are no comparable

expenditures for the Jefferson switching station. Thus, there is less economic “leakage”

assumed as a proportion of the total costs of construction.

27

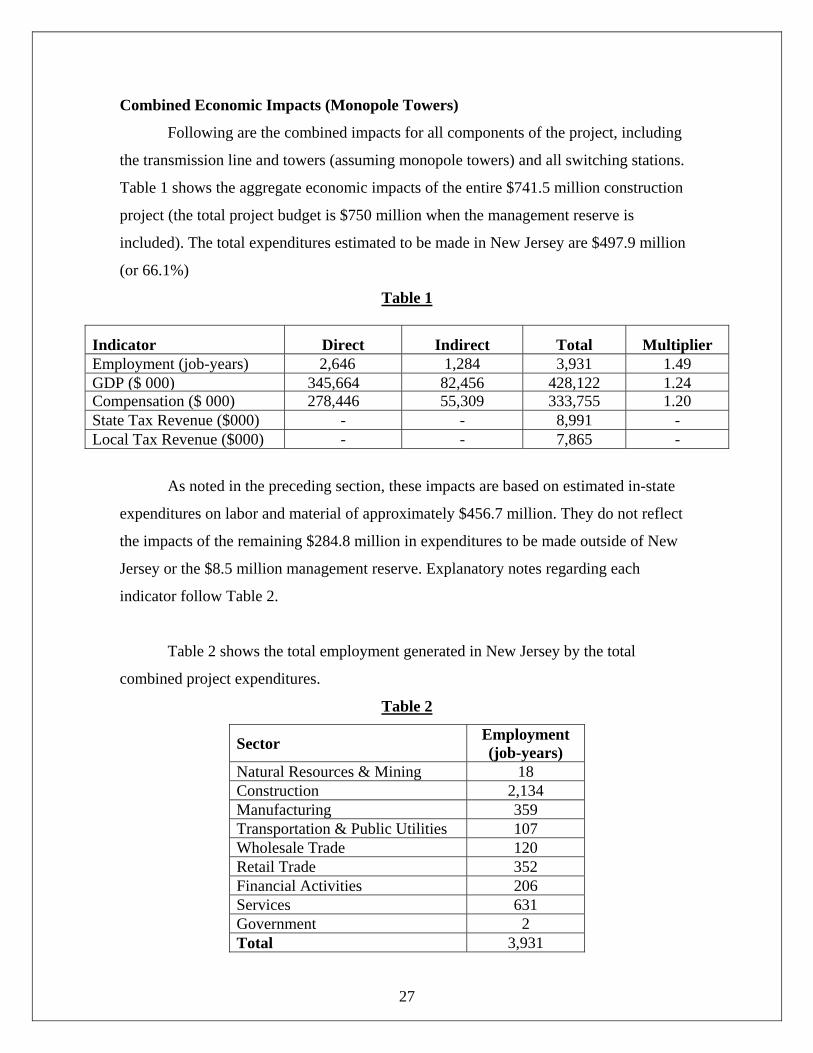

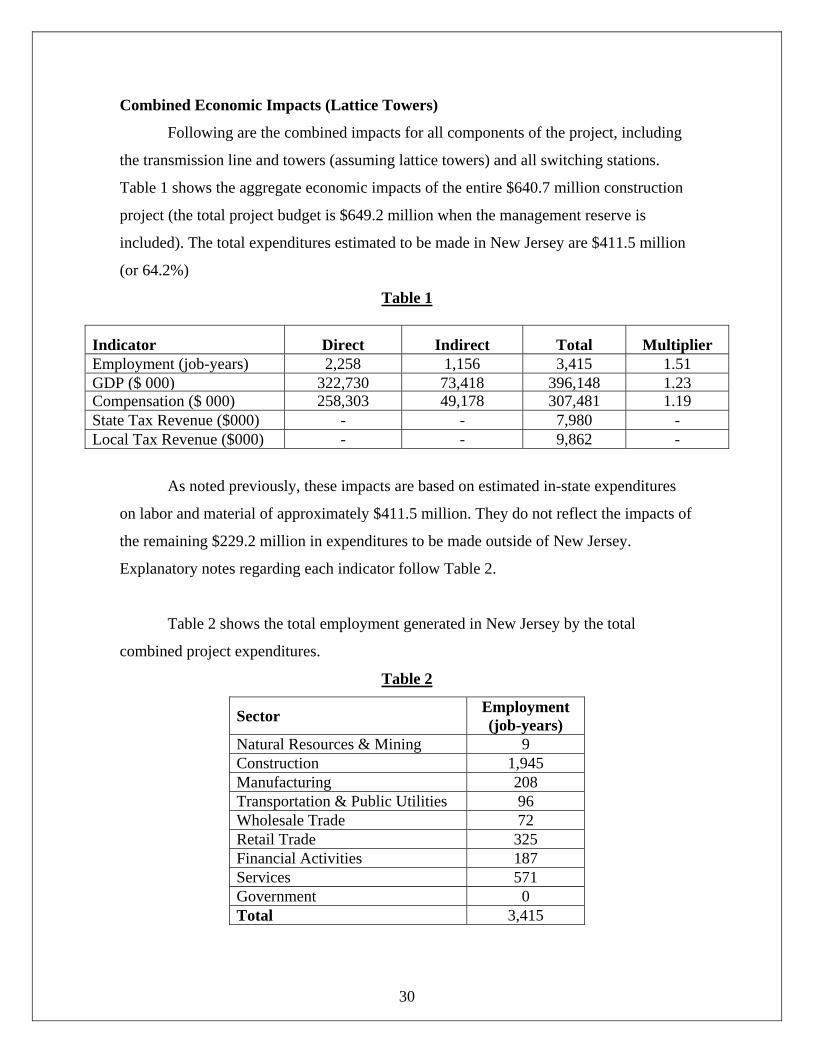

Combined Economic Impacts (Monopole Towers)

Following are the combined impacts for all components of the project, including

the transmission line and towers (assuming monopole towers) and all switching stations.

Table 1 shows the aggregate economic impacts of the entire $741.5 million construction

project (the total project budget is $750 million when the management reserve is

included). The total expenditures estimated to be made in New Jersey are $497.9 million

(or 66.1%)

Table 1

Indicator Direct Indirect Total Multiplier Employment (job-years) 2,646 1,284 3,931 1.49 GDP ($ 000) 345,664 82,456 428,122 1.24Compensation ($ 000) 278,446 55,309 333,755 1.20 State Tax Revenue ($000) - - 8,991 - Local Tax Revenue ($000) - - 7,865 -

As noted in the preceding section, these impacts are based on estimated in-state

expenditures on labor and material of approximately $456.7 million. They do not reflect

the impacts of the remaining $284.8 million in expenditures to be made outside of New

Jersey or the $8.5 million management reserve. Explanatory notes regarding each

indicator follow Table 2.

Table 2 shows the total employment generated in New Jersey by the total

combined project expenditures.

Table 2

Sector Employment (job-years)

Natural Resources & Mining 18 Construction 2,134 Manufacturing 359 Transportation & Public Utilities 107 Wholesale Trade 120 Retail Trade 352 Financial Activities 206 Services 631 Government 2 Total 3,931

28

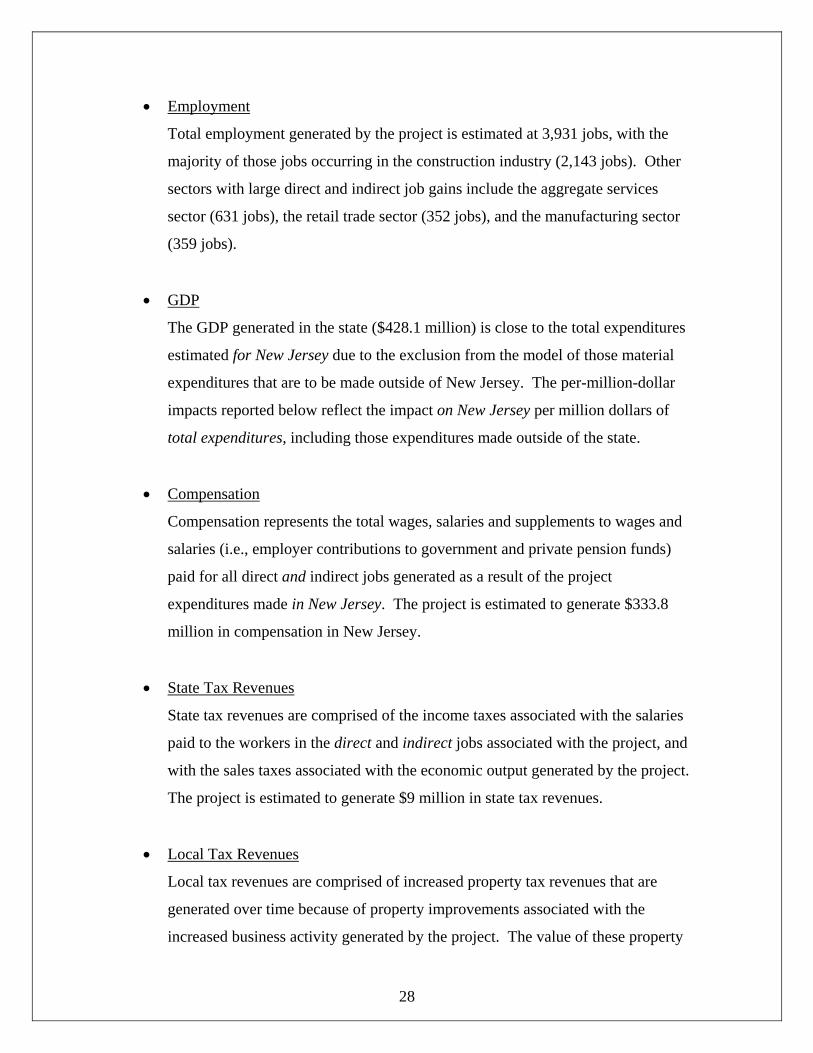

• Employment

Total employment generated by the project is estimated at 3,931 jobs, with the

majority of those jobs occurring in the construction industry (2,143 jobs). Other

sectors with large direct and indirect job gains include the aggregate services

sector (631 jobs), the retail trade sector (352 jobs), and the manufacturing sector

(359 jobs).

• GDP

The GDP generated in the state ($428.1 million) is close to the total expenditures

estimated for New Jersey due to the exclusion from the model of those material

expenditures that are to be made outside of New Jersey. The per-million-dollar

impacts reported below reflect the impact on New Jersey per million dollars of

total expenditures, including those expenditures made outside of the state.

• Compensation

Compensation represents the total wages, salaries and supplements to wages and

salaries (i.e., employer contributions to government and private pension funds)

paid for all direct and indirect jobs generated as a result of the project

expenditures made in New Jersey. The project is estimated to generate $333.8

million in compensation in New Jersey.

• State Tax Revenues

State tax revenues are comprised of the income taxes associated with the salaries

paid to the workers in the direct and indirect jobs associated with the project, and

with the sales taxes associated with the economic output generated by the project.

The project is estimated to generate $9 million in state tax revenues.

• Local Tax Revenues

Local tax revenues are comprised of increased property tax revenues that are

generated over time because of property improvements associated with the

increased business activity generated by the project. The value of these property

29

improvements is, in time, included in assessments and hence in property tax

revenues. The project is estimated to generate $7.9 million in local tax revenues.

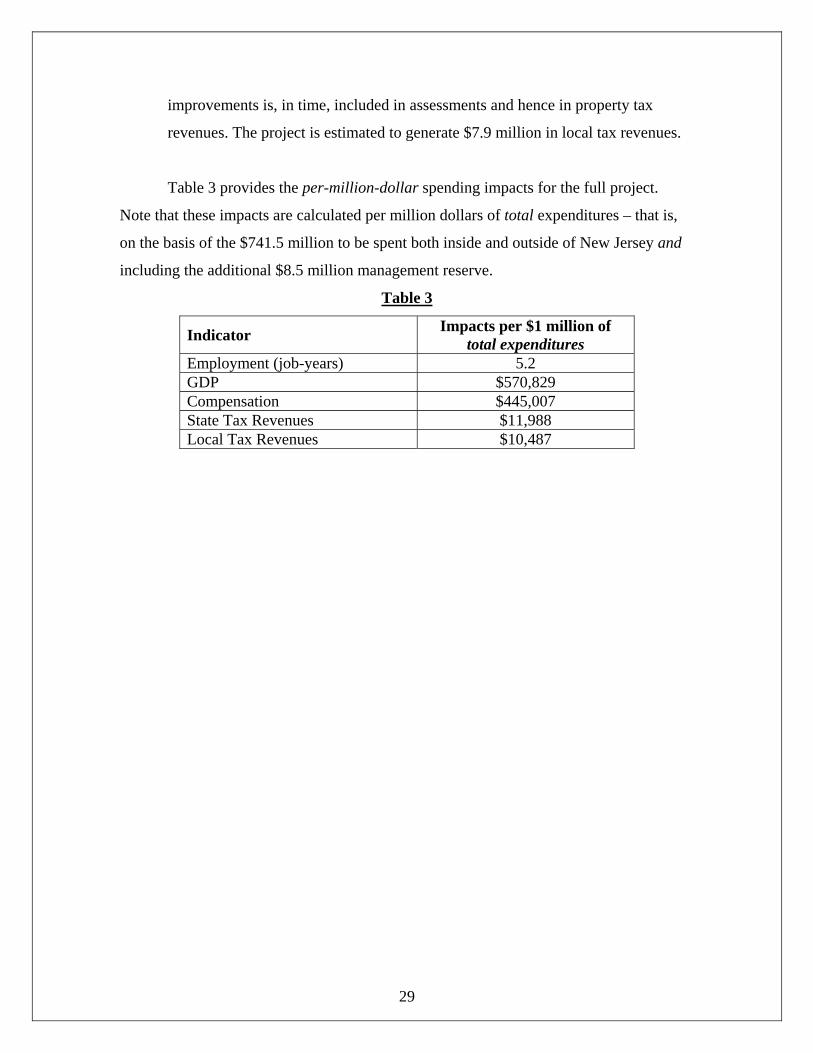

Table 3 provides the per-million-dollar spending impacts for the full project.

Note that these impacts are calculated per million dollars of total expenditures – that is,

on the basis of the $741.5 million to be spent both inside and outside of New Jersey and

including the additional $8.5 million management reserve.

Table 3

Indicator Impacts per $1 million of total expenditures

Employment (job-years) 5.2 GDP $570,829 Compensation $445,007 State Tax Revenues $11,988 Local Tax Revenues $10,487

30

Combined Economic Impacts (Lattice Towers)

Following are the combined impacts for all components of the project, including

the transmission line and towers (assuming lattice towers) and all switching stations.

Table 1 shows the aggregate economic impacts of the entire $640.7 million construction

project (the total project budget is $649.2 million when the management reserve is

included). The total expenditures estimated to be made in New Jersey are $411.5 million

(or 64.2%)

Table 1

Indicator Direct Indirect Total Multiplier Employment (job-years) 2,258 1,156 3,415 1.51 GDP ($ 000) 322,730 73,418 396,148 1.23Compensation ($ 000) 258,303 49,178 307,481 1.19 State Tax Revenue ($000) - - 7,980 - Local Tax Revenue ($000) - - 9,862 -

As noted previously, these impacts are based on estimated in-state expenditures

on labor and material of approximately $411.5 million. They do not reflect the impacts of

the remaining $229.2 million in expenditures to be made outside of New Jersey.

Explanatory notes regarding each indicator follow Table 2.

Table 2 shows the total employment generated in New Jersey by the total

combined project expenditures.

Table 2

Sector Employment (job-years)

Natural Resources & Mining 9 Construction 1,945 Manufacturing 208 Transportation & Public Utilities 96 Wholesale Trade 72 Retail Trade 325 Financial Activities 187 Services 571 Government 0 Total 3,415

31

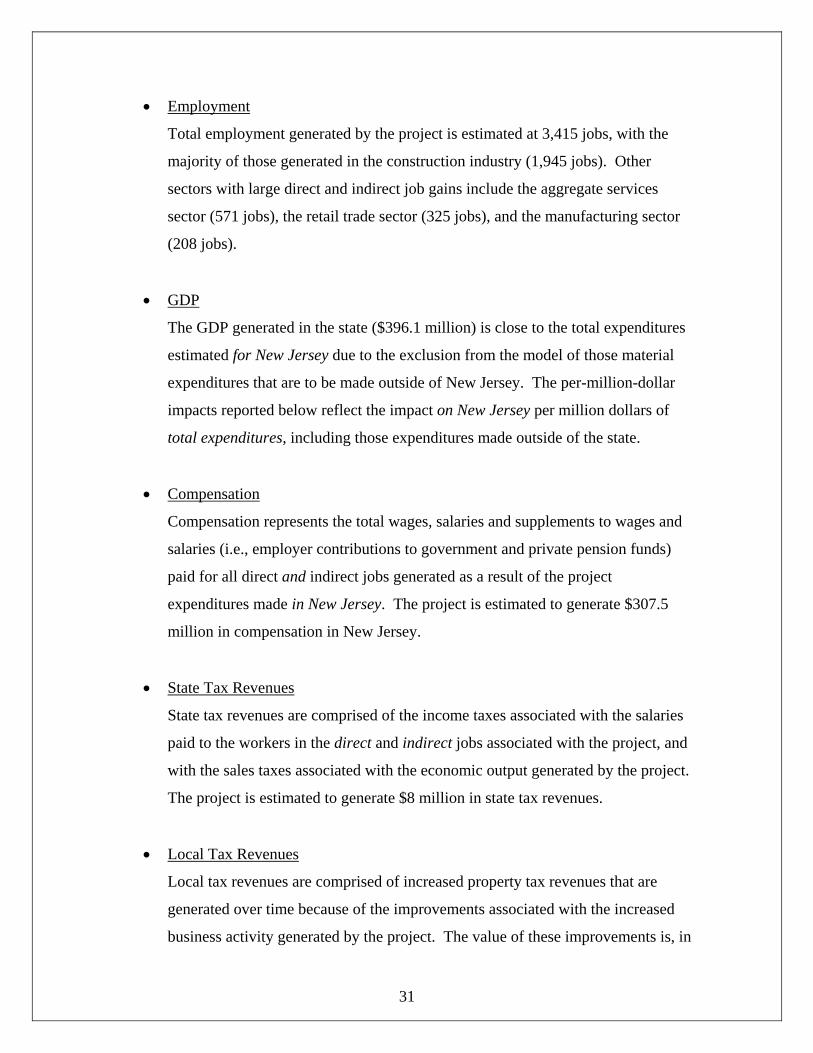

• Employment

Total employment generated by the project is estimated at 3,415 jobs, with the

majority of those generated in the construction industry (1,945 jobs). Other

sectors with large direct and indirect job gains include the aggregate services

sector (571 jobs), the retail trade sector (325 jobs), and the manufacturing sector

(208 jobs).

• GDP

The GDP generated in the state ($396.1 million) is close to the total expenditures

estimated for New Jersey due to the exclusion from the model of those material

expenditures that are to be made outside of New Jersey. The per-million-dollar

impacts reported below reflect the impact on New Jersey per million dollars of

total expenditures, including those expenditures made outside of the state.

• Compensation

Compensation represents the total wages, salaries and supplements to wages and

salaries (i.e., employer contributions to government and private pension funds)

paid for all direct and indirect jobs generated as a result of the project

expenditures made in New Jersey. The project is estimated to generate $307.5

million in compensation in New Jersey.

• State Tax Revenues

State tax revenues are comprised of the income taxes associated with the salaries

paid to the workers in the direct and indirect jobs associated with the project, and

with the sales taxes associated with the economic output generated by the project.

The project is estimated to generate $8 million in state tax revenues.

• Local Tax Revenues

Local tax revenues are comprised of increased property tax revenues that are

generated over time because of the improvements associated with the increased

business activity generated by the project. The value of these improvements is, in

32

time, included in assessments and hence in property taxes. The project is

estimated to generate $9.9 million in local tax revenues.

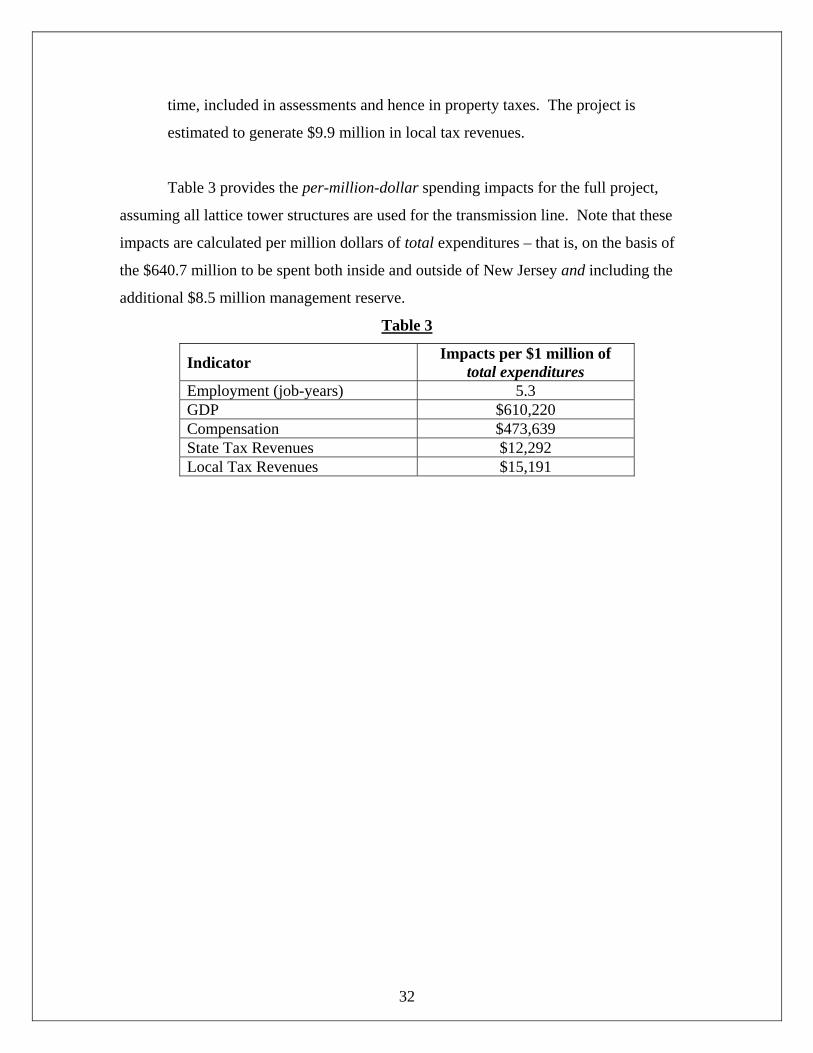

Table 3 provides the per-million-dollar spending impacts for the full project,

assuming all lattice tower structures are used for the transmission line. Note that these

impacts are calculated per million dollars of total expenditures – that is, on the basis of

the $640.7 million to be spent both inside and outside of New Jersey and including the

additional $8.5 million management reserve.

Table 3

Indicator Impacts per $1 million of total expenditures

Employment (job-years) 5.3 GDP $610,220 Compensation $473,639 State Tax Revenues $12,292 Local Tax Revenues $15,191

33

CONCLUSION

This report presents an economic impact analysis of the proposed upgrade of

PSE&G’s Susquehanna-Roseland transmission network. Using the Edward J. Bloustein

School’s R/ECON™ Input-Output model, impact estimates were generated for

construction of two switching stations and the transmission line and towers, including

separate analyses for two different types of tower. Based on the proposed employment

and other project expenditures to be made in New Jersey, we estimate that the $649.2

million (all lattice towers) to $750 million (all monopole towers) in project expenditures

($425.2 million to $467.7 million to be made in New Jersey), including management

reserves, will generate:

• between 3,415 (lattice) and 3,931 (monopole) job-years for workers in New

Jersey;

• between $396.1 million (lattice ) and $428.1 million (monopole) in gross

domestic product for the state;

• between $307.5 million (lattice) and $333.8 million in compensation for workers

in the jobs generated by the project in New Jersey;

• between $8 million (lattice) and $9 million (monopole) in state taxes; and

• between $7.9 million (monopole) and $9.9 million (lattice) in local taxes.

34

APPENDIX A: ECONOMIC AND DEMOGRAPHIC PROFILES AND DYNAMICS

The four counties where the transmission line work will occur – Essex, Morris,

Sussex, and Warren – together represent a microcosm of New Jersey, mirroring the

economic and demographic profile of the state, as well as the basic economic and

demographic dynamics of change. The four-county region has dense urban job and

residential concentrations, strong suburban job growth corridors and residential

communities, and dispersed rural-suburban territories characterized by very low density

development patterns.

The four-county economies are dominated by private service-providing

employment. The most significant service-providing sectors, in order of importance, are

trade, transportation, and utilities, professional and business services, and education and

health services. Employment growth rates in the four-county region have been relatively

modest, somewhat below those of the state, with education and health services the

leading growth sector.

Slow-growth demographics also characterize the four counties, with population

increases steadily declining through the decade. The principal reason for this slowdown

has been growing net migration losses – more people moving out than moving in – that

have now spread to even the low density counties of Sussex and Warren. The modest

population gains for the decade to date are due solely to net natural increase (births minus

deaths).

This Appendix examines the employment composition of the each of the counties

and the aggregated four-county region in the context of that of New Jersey as a whole, as

well as the patterns of change during the 2002-2008 period. This will be followed by a

demographic analysis of 2000-2008 period in terms of the basic components of

population change.

State, County, and Region Employment Analysis

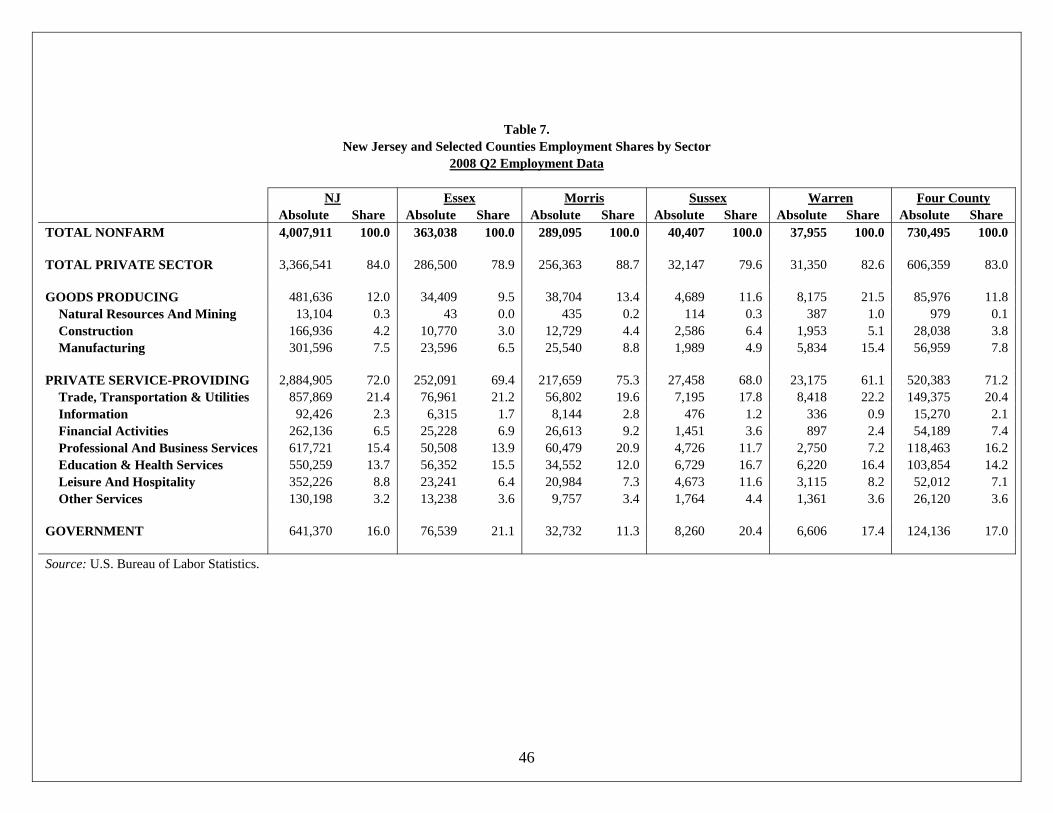

The economies of Essex, Morris, Sussex, and Warren counties in total accounted

for nearly one-fifth (18.2 percent) of New Jersey’s total payroll employment in 2008

(730,495 jobs out of a state total of 4,007,911 jobs). Essex was the largest (363,038 jobs)

35

of the four counties, followed by Morris (289,095 jobs). Much smaller in size are Sussex

(40,407 jobs) and Warren (37,955 jobs). In general, Essex tends to have a concentrated

urban employment base (as well as a secondary suburban one), while that of Morris is

largely suburban highway-corridor oriented. Thus, Essex is the densest economy,

followed by Morris. In contrast, employment in Sussex has a much less dense and more

dispersed suburban-rural pattern. Warren is a mixture of urban, suburban, and rural, with

much of the county similar to Sussex. However, there is an older manufacturing base

centered in the area around Phillipsburg. Thus, the employment geography of the four-

county region is quite heterogeneous in terms of geographic distribution and density,

mirroring quite closely that of New Jersey in its entirety.

This is much less the case in the composition and growth patterns of each county.

The broad general job dynamic in the 2002-2008 period has been employment growth in

private-service providing activities and government, and employment declines in goods-

producing industries. The sector that dominated private-sector growth was education and

health services. This stands as a microcosm of what has occurred in the New Jersey

economy.

Employment Data

To analyze the four counties, New Jersey as a whole will serve as the baseline.

The source of both county and statewide data is the Quarterly Census of Employment and

Wages (QCEW) produced by the U.S. Bureau of Labor Statistics. At the state level, the

QCEW differs slightly from the Current Employment Survey (CES) payroll employment

series, which is sample-based and is released monthly by the New Jersey Department of

Labor and Workforce Development. The advantage of the QCEW is that it is a full count

and not a sample, and is available at the county level; its disadvantage is that the data are

not as current as the CES. The state data in the QCEW are the sum of the 21 counties.

The analysis begins in the second quarter of 2002 and ends in the second quarter

of 2008, the last quarter of data availability. The period of measurement was designed to

have the beginning and end points at similar stages in the business cycle. New Jersey’s

employment had peaked in December 2000, the end of the great economic expansion of

36

the 1990s. It then contracted through early 2003, when growth resumed. Employment

then kept expanding until it once again peaked, in December 2007, when the current

recession began. So both the beginning and end points (second quarter of 2002 and

second quarter of 2008) were in recessionary periods, with a modest economic expansion

in between.

Employment is classified into categories defined by the North American Industry

Classification System (NAICS). The initial partition is between the private sector and the

public sector (government). The private sector is further disaggregated into good-

producing industries and service-providing industries. There are three major goods-

producing industries – natural resources and mining, construction, and manufacturing.

Of the three, manufacturing is the largest.

There are seven major industries in the service-providing group: trade,

transportation, and utilities; information; financial activities; professional and business

services; education and health services; leisure and hospitality; and other services. The

three largest are trade, transportation, and utilities, professional and business services,

and educational and health services. The smallest is information. We will refer to them

as sectors or classifications. The following is a more detailed, but not complete,

definition of these sectors.

Trade, Transportation, and Utilities include wholesale trade, retail trade, transportation,

warehousing, and utilities.

Information includes publishing, telecommunications, Internet service providers, and

data processing activities.

Financial Activities include finance, insurance, and real estate.

Professional and Business Services includes professional, scientific, and technical

services; legal and accounting services; architectural and engineering services,

advertising, management of companies and enterprises, and administrative support.

37

Education and Health Services includes private education, health care, and social

assistance.

Leisure and Hospitality includes arts, entertainment, recreation, gambling, amusements,

accommodations, and food services and drinking places.

Other Services include repair and maintenance, personal and laundry services, and

religious, grant making, civic, professional and similar organizations.

The Baseline New Jersey Employment Growth Pattern

Between 2002 Q2 and 2008 Q2, total employment in New Jersey increased by

111,377 jobs or 2.9 percent, from 3.9 million to 4.0 million (Table 1). This 2.9 percent

growth was considerably below the national 7.2 percent increase for the same time

period.

Employment growth in the state was concentrated in both the private service-

providing sector (+134,173 jobs or +4.9 percent) and government (+34,445 jobs or +5.7

percent). Public-sector employment growth, while smaller in absolute magnitude than

private service-providing employment growth, had a higher rate of increase (5.7 percent

versus 4.8 percent).

In contrast, employment in the private goods-producing sector declined by 57,241

jobs or -10.6 percent. This decline was largely due to the state’s long-term

manufacturing hemorrhage. New Jersey lost 64,377 manufacturing jobs between 2002

and 2008, or -17.6 percent. Thus, nearly one out five of the state’s manufacturing jobs

disappeared in a brief six-year period. In the goods-producing sector, this loss was only

partially counter-balanced by growth in construction employment (+6,315 jobs or +3.9

percent).

Education and health services had the largest employment increase of all of the

service-providing industries. Between 2002 Q2 and 2008 Q2, this sector gained 72,285

jobs, a rate of increase of 15.1 percent, and it accounted for 64.9 percent of the state’s

total employment growth (72,285 jobs out of 111,377 jobs). It was followed by leisure

and hospitality (+41,553 jobs), professional and business services (+40,139 jobs), other

38

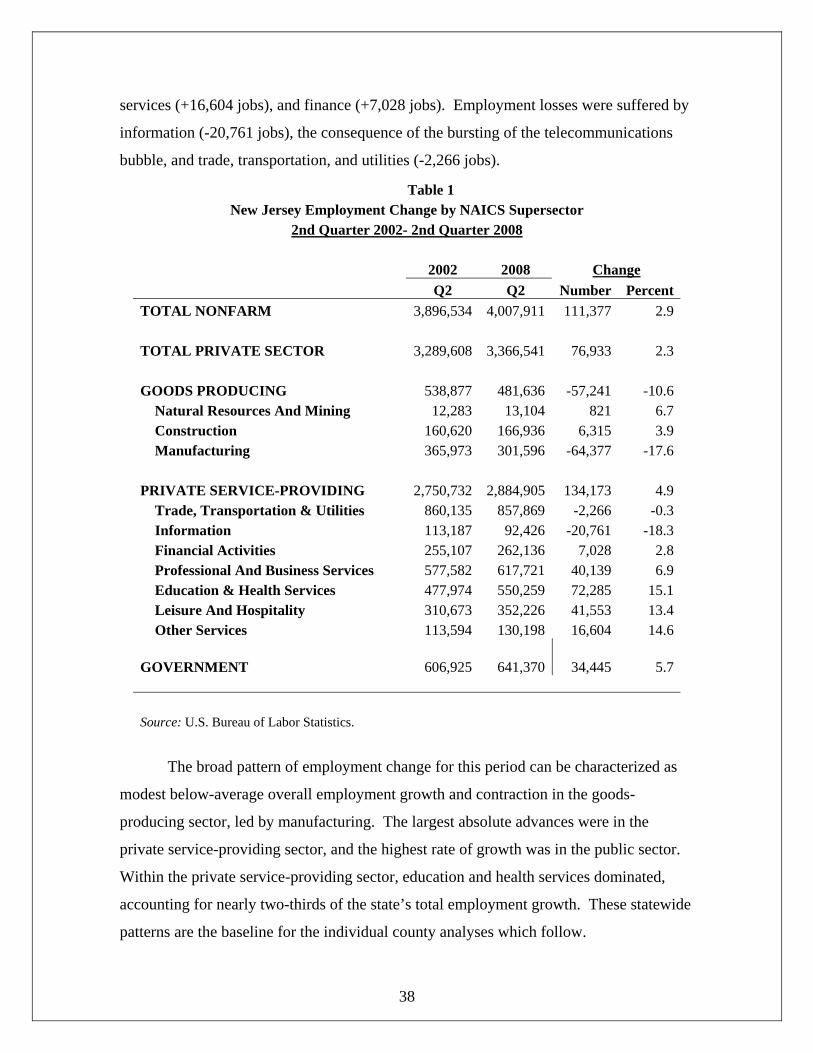

services (+16,604 jobs), and finance (+7,028 jobs). Employment losses were suffered by

information (-20,761 jobs), the consequence of the bursting of the telecommunications

bubble, and trade, transportation, and utilities (-2,266 jobs).

Table 1 New Jersey Employment Change by NAICS Supersector

2nd Quarter 2002- 2nd Quarter 2008 2002 2008 Change Q2 Q2 Number PercentTOTAL NONFARM 3,896,534 4,007,911 111,377 2.9 TOTAL PRIVATE SECTOR 3,289,608 3,366,541 76,933 2.3 GOODS PRODUCING 538,877 481,636 -57,241 -10.6

Natural Resources And Mining 12,283 13,104 821 6.7Construction 160,620 166,936 6,315 3.9Manufacturing 365,973 301,596 -64,377 -17.6

PRIVATE SERVICE-PROVIDING 2,750,732 2,884,905 134,173 4.9

Trade, Transportation & Utilities 860,135 857,869 -2,266 -0.3Information 113,187 92,426 -20,761 -18.3Financial Activities 255,107 262,136 7,028 2.8Professional And Business Services 577,582 617,721 40,139 6.9Education & Health Services 477,974 550,259 72,285 15.1Leisure And Hospitality 310,673 352,226 41,553 13.4Other Services 113,594 130,198 16,604 14.6

GOVERNMENT 606,925 641,370 34,445 5.7 Source: U.S. Bureau of Labor Statistics.

The broad pattern of employment change for this period can be characterized as

modest below-average overall employment growth and contraction in the goods-

producing sector, led by manufacturing. The largest absolute advances were in the

private service-providing sector, and the highest rate of growth was in the public sector.

Within the private service-providing sector, education and health services dominated,

accounting for nearly two-thirds of the state’s total employment growth. These statewide

patterns are the baseline for the individual county analyses which follow.

39

Essex County

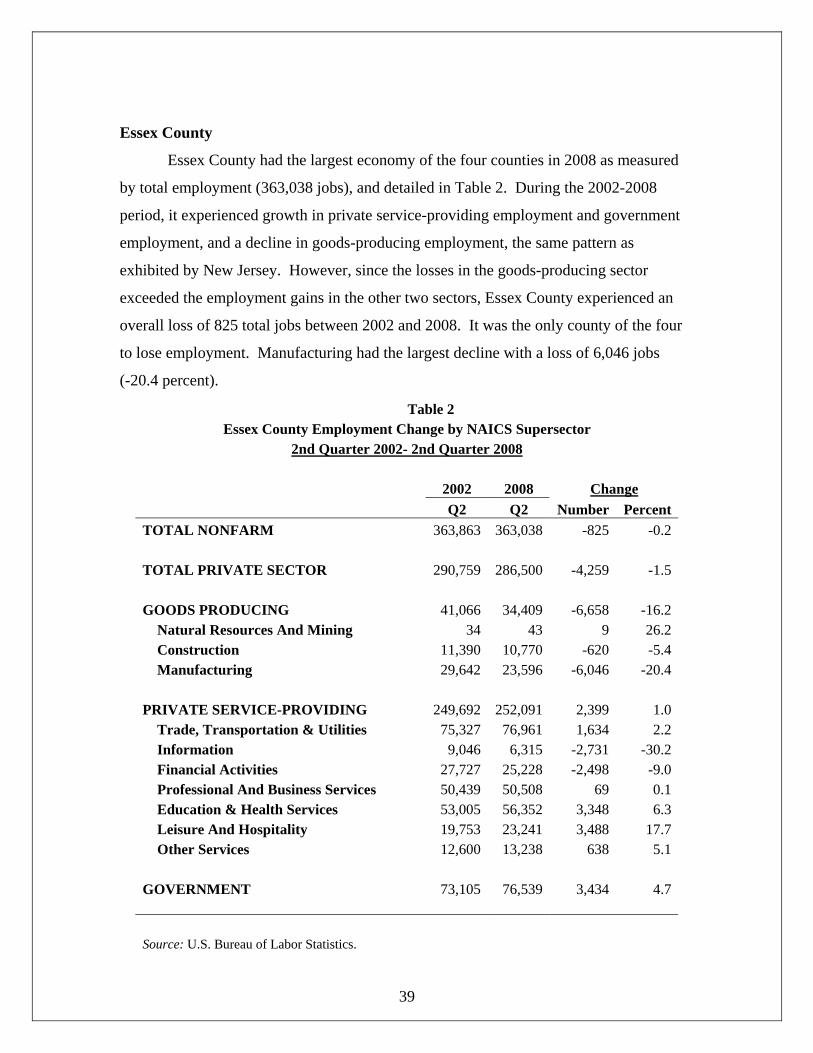

Essex County had the largest economy of the four counties in 2008 as measured

by total employment (363,038 jobs), and detailed in Table 2. During the 2002-2008

period, it experienced growth in private service-providing employment and government

employment, and a decline in goods-producing employment, the same pattern as

exhibited by New Jersey. However, since the losses in the goods-producing sector

exceeded the employment gains in the other two sectors, Essex County experienced an

overall loss of 825 total jobs between 2002 and 2008. It was the only county of the four

to lose employment. Manufacturing had the largest decline with a loss of 6,046 jobs

(-20.4 percent).

Table 2 Essex County Employment Change by NAICS Supersector

2nd Quarter 2002- 2nd Quarter 2008 2002 2008 Change Q2 Q2 Number PercentTOTAL NONFARM 363,863 363,038 -825 -0.2 TOTAL PRIVATE SECTOR 290,759 286,500 -4,259 -1.5 GOODS PRODUCING 41,066 34,409 -6,658 -16.2

Natural Resources And Mining 34 43 9 26.2Construction 11,390 10,770 -620 -5.4Manufacturing 29,642 23,596 -6,046 -20.4

PRIVATE SERVICE-PROVIDING 249,692 252,091 2,399 1.0

Trade, Transportation & Utilities 75,327 76,961 1,634 2.2Information 9,046 6,315 -2,731 -30.2Financial Activities 27,727 25,228 -2,498 -9.0Professional And Business Services 50,439 50,508 69 0.1Education & Health Services 53,005 56,352 3,348 6.3Leisure And Hospitality 19,753 23,241 3,488 17.7Other Services 12,600 13,238 638 5.1

GOVERNMENT 73,105 76,539 3,434 4.7 Source: U.S. Bureau of Labor Statistics.

40

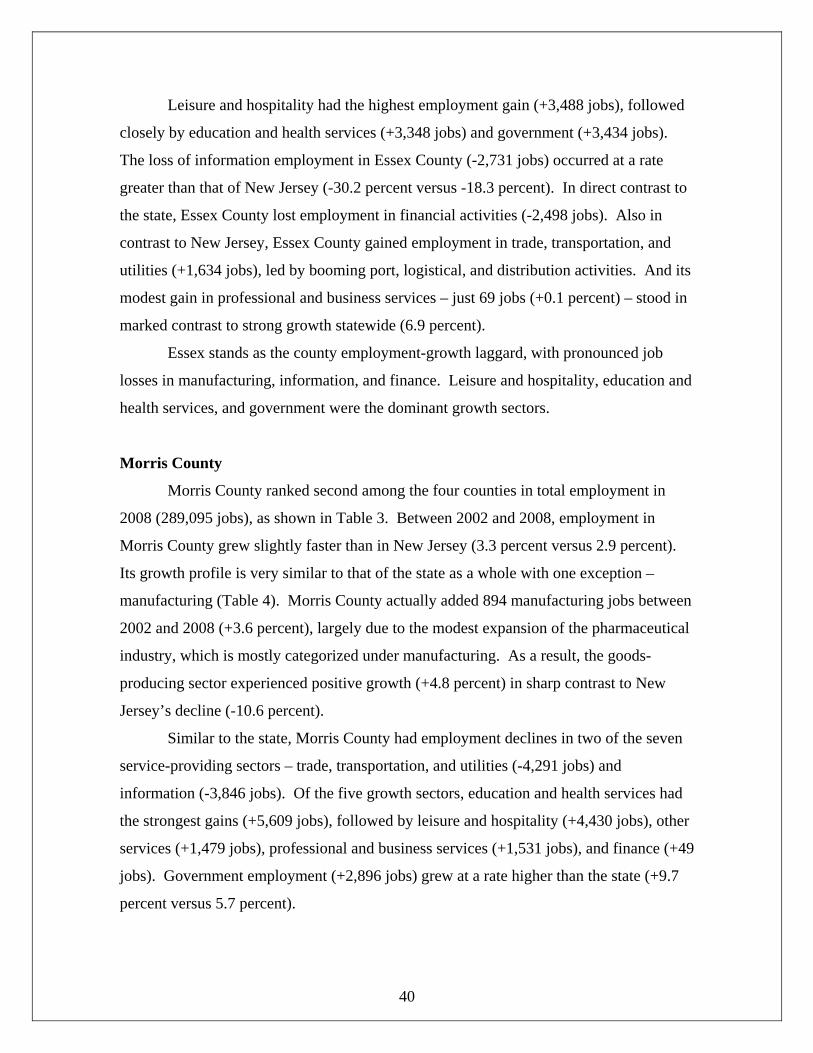

Leisure and hospitality had the highest employment gain (+3,488 jobs), followed

closely by education and health services (+3,348 jobs) and government (+3,434 jobs).

The loss of information employment in Essex County (-2,731 jobs) occurred at a rate

greater than that of New Jersey (-30.2 percent versus -18.3 percent). In direct contrast to

the state, Essex County lost employment in financial activities (-2,498 jobs). Also in

contrast to New Jersey, Essex County gained employment in trade, transportation, and

utilities (+1,634 jobs), led by booming port, logistical, and distribution activities. And its

modest gain in professional and business services – just 69 jobs (+0.1 percent) – stood in

marked contrast to strong growth statewide (6.9 percent).

Essex stands as the county employment-growth laggard, with pronounced job

losses in manufacturing, information, and finance. Leisure and hospitality, education and

health services, and government were the dominant growth sectors.

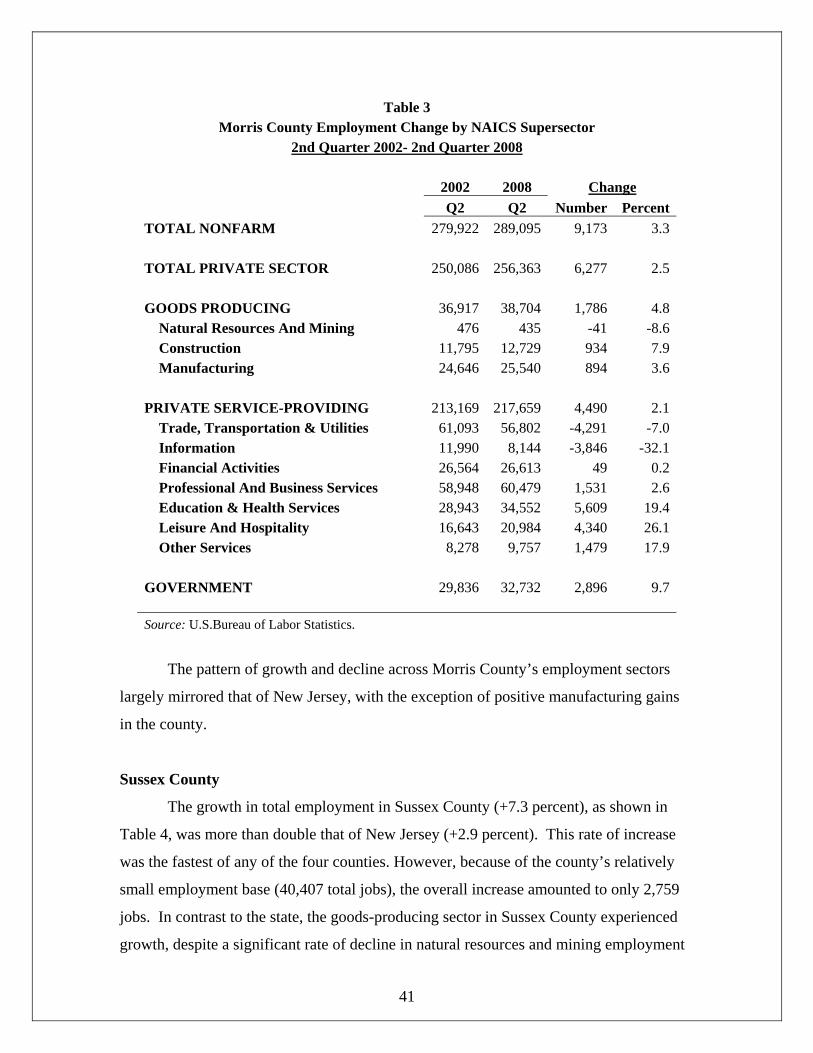

Morris County

Morris County ranked second among the four counties in total employment in

2008 (289,095 jobs), as shown in Table 3. Between 2002 and 2008, employment in

Morris County grew slightly faster than in New Jersey (3.3 percent versus 2.9 percent).

Its growth profile is very similar to that of the state as a whole with one exception –

manufacturing (Table 4). Morris County actually added 894 manufacturing jobs between

2002 and 2008 (+3.6 percent), largely due to the modest expansion of the pharmaceutical

industry, which is mostly categorized under manufacturing. As a result, the goods-

producing sector experienced positive growth (+4.8 percent) in sharp contrast to New

Jersey’s decline (-10.6 percent).

Similar to the state, Morris County had employment declines in two of the seven

service-providing sectors – trade, transportation, and utilities (-4,291 jobs) and

information (-3,846 jobs). Of the five growth sectors, education and health services had

the strongest gains (+5,609 jobs), followed by leisure and hospitality (+4,430 jobs), other

services (+1,479 jobs), professional and business services (+1,531 jobs), and finance (+49

jobs). Government employment (+2,896 jobs) grew at a rate higher than the state (+9.7

percent versus 5.7 percent).

41

Table 3 Morris County Employment Change by NAICS Supersector

2nd Quarter 2002- 2nd Quarter 2008 2002 2008 Change Q2 Q2 Number PercentTOTAL NONFARM 279,922 289,095 9,173 3.3 TOTAL PRIVATE SECTOR 250,086 256,363 6,277 2.5 GOODS PRODUCING 36,917 38,704 1,786 4.8

Natural Resources And Mining 476 435 -41 -8.6Construction 11,795 12,729 934 7.9Manufacturing 24,646 25,540 894 3.6

PRIVATE SERVICE-PROVIDING 213,169 217,659 4,490 2.1

Trade, Transportation & Utilities 61,093 56,802 -4,291 -7.0Information 11,990 8,144 -3,846 -32.1Financial Activities 26,564 26,613 49 0.2Professional And Business Services 58,948 60,479 1,531 2.6Education & Health Services 28,943 34,552 5,609 19.4Leisure And Hospitality 16,643 20,984 4,340 26.1Other Services 8,278 9,757 1,479 17.9

GOVERNMENT 29,836 32,732 2,896 9.7 Source: U.S.Bureau of Labor Statistics.

The pattern of growth and decline across Morris County’s employment sectors

largely mirrored that of New Jersey, with the exception of positive manufacturing gains

in the county.

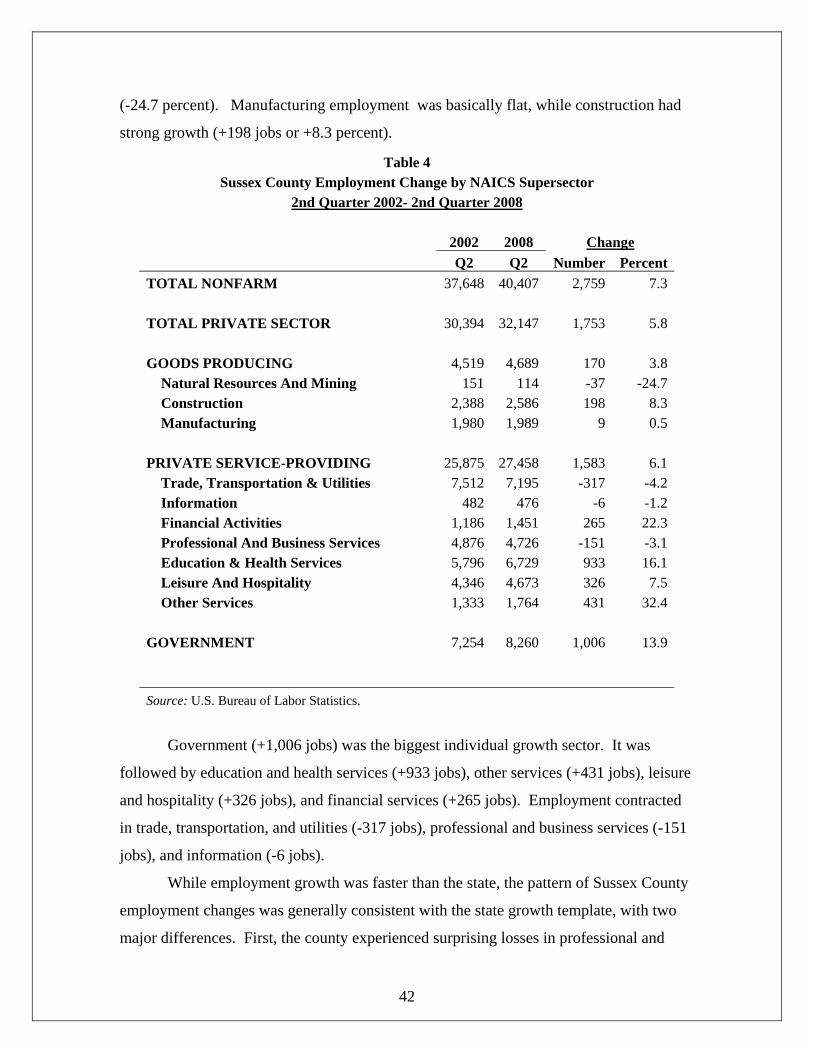

Sussex County

The growth in total employment in Sussex County (+7.3 percent), as shown in

Table 4, was more than double that of New Jersey (+2.9 percent). This rate of increase

was the fastest of any of the four counties. However, because of the county’s relatively

small employment base (40,407 total jobs), the overall increase amounted to only 2,759

jobs. In contrast to the state, the goods-producing sector in Sussex County experienced

growth, despite a significant rate of decline in natural resources and mining employment

42

(-24.7 percent). Manufacturing employment was basically flat, while construction had

strong growth (+198 jobs or +8.3 percent).

Table 4 Sussex County Employment Change by NAICS Supersector

2nd Quarter 2002- 2nd Quarter 2008 2002 2008 Change Q2 Q2 Number PercentTOTAL NONFARM 37,648 40,407 2,759 7.3 TOTAL PRIVATE SECTOR 30,394 32,147 1,753 5.8 GOODS PRODUCING 4,519 4,689 170 3.8

Natural Resources And Mining 151 114 -37 -24.7Construction 2,388 2,586 198 8.3Manufacturing 1,980 1,989 9 0.5

PRIVATE SERVICE-PROVIDING 25,875 27,458 1,583 6.1

Trade, Transportation & Utilities 7,512 7,195 -317 -4.2Information 482 476 -6 -1.2Financial Activities 1,186 1,451 265 22.3Professional And Business Services 4,876 4,726 -151 -3.1Education & Health Services 5,796 6,729 933 16.1Leisure And Hospitality 4,346 4,673 326 7.5Other Services 1,333 1,764 431 32.4

GOVERNMENT 7,254 8,260 1,006 13.9 Source: U.S. Bureau of Labor Statistics.

Government (+1,006 jobs) was the biggest individual growth sector. It was

followed by education and health services (+933 jobs), other services (+431 jobs), leisure

and hospitality (+326 jobs), and financial services (+265 jobs). Employment contracted

in trade, transportation, and utilities (-317 jobs), professional and business services (-151

jobs), and information (-6 jobs).

While employment growth was faster than the state, the pattern of Sussex County

employment changes was generally consistent with the state growth template, with two

major differences. First, the county experienced surprising losses in professional and

43

business services employment, and second, its manufacturing sector demonstrated job

stability in contrast to the significant losses experienced statewide.

Warren County

Warren County has the smallest economy, comprising just 37,955 jobs in 2008, as

detailed in Table 5. This total was slightly below that of Sussex County (40,407 jobs).

Its overall employment growth rate (+3.2 percent or +1,186 jobs) between 2002 and 2008

was slightly above that of the state (+2.9 percent). The general statewide pattern of

growth in service-providing and government employment, and decline in goods-

producing employment was also evident in Warren County.

Table 5 Warren County Employment Change by NAICS Supersector

2nd Quarter 2002- 2nd Quarter 2008 2002 2008 Change Q2 Q2 Number Percent TOTAL NONFARM 36,770 37,955 1,186 3.2 TOTAL PRIVATE SECTOR 30,881 31,350 469 1.5 GOODS PRODUCING 8,525 8,175 -350 -4.1

Natural Resources And Mining 286 387 101 35.2Construction 1,476 1,953 477 32.3Manufacturing 6,762 5,834 -928 -13.7

PRIVATE SERVICE-PROVIDING 22,356 23,175 819 3.7

Trade, Transportation & Utilities 8,968 8,418 -550 -6.1Information 305 336 31 10.1Financial Activities 954 897 -57 -5.9Professional And Business Services 2,590 2,750 160 6.2Education & Health Services 5,181 6,220 1,039 20.1Leisure And Hospitality 2,976 3,115 138 4.6Other Services 1,125 1,361 236 20.9

GOVERNMENT 5,889 6,606 717 12.2 Source: U.S. Bureau of Labor Statistics.

44

Within the goods-producing sector, which lost 350 jobs, the decline in

manufacturing employment (-928 jobs) overweighed the combined growth in

construction (+477 jobs) and in natural resources and mining (+101 jobs). In the service-

providing sector (+819 jobs), education and health services added 1,039 jobs (+20.1

percent), the highest of any private-sector employment category. Also growing at above-

state average rates were other services (+20.9 percent or +236 jobs), information (+10.1

percent or +31 jobs), professional and business services (+6.2 percent or 160 jobs), and

leisure and hospitality (+4.6 percent or 138 jobs). Employment losses were suffered in

trade, transportation, and utilities (-550 jobs) and financial activities (-57 jobs).

Government employment, grew by 717 jobs (+12.2 percent).

Warren County’s growth pattern during the 2002 and 2008 period was much more

dominated by government compared to New Jersey. Government accounted for 60.4

percent of Warren’s total employment growth (717 jobs out of a total 1,186 jobs). For

New Jersey as a whole, government accounted for 30.9 percent (34,445 jobs out of

111,377 jobs). While there were some minor differences in several sectors, the same

dynamic of goods-producing employment contraction and service-providing employment

expansion was evident in both Warren County and New Jersey.

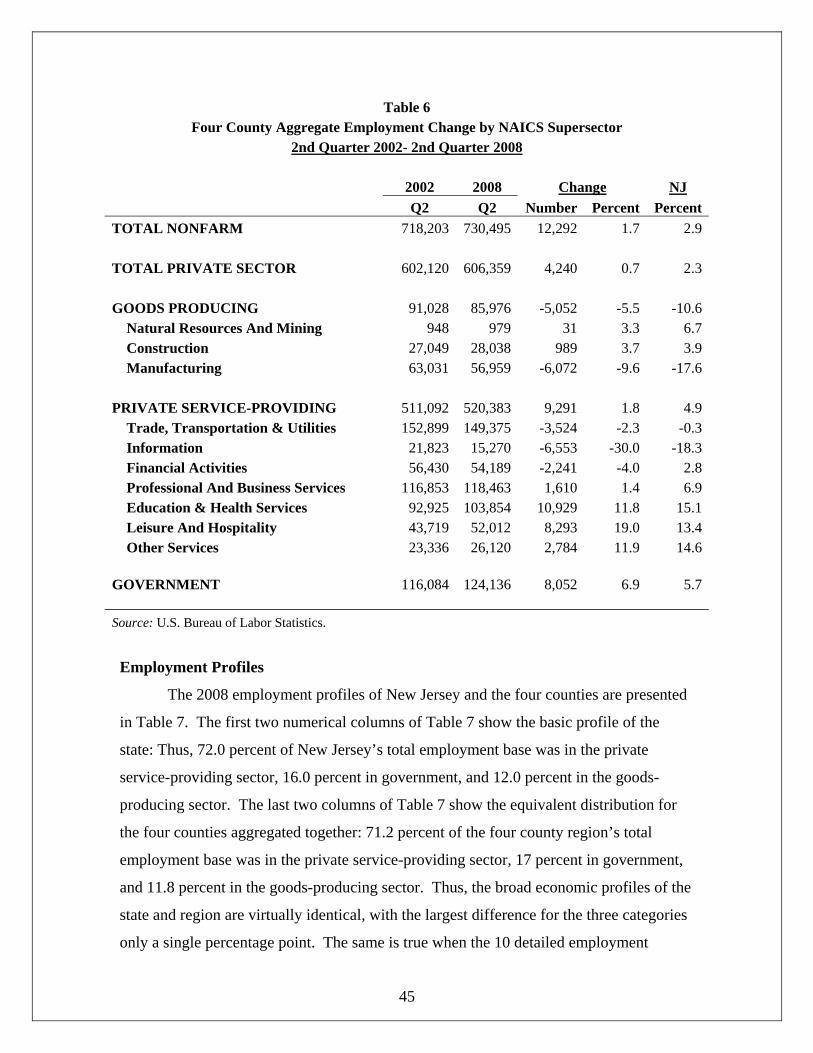

The Four County Region

Table 6 provides the four county aggregate employment levels and change for the

2002-2008 period, along with the percentage change for the state as a whole.

Employment in he four counties combined is growing somewhat slower than the New

Jersey, mainly due to mature Essex County, which is virtually built out. But outside of

this distinction, aggregating the four counties together tends to mute the individual

county differences. This aggregation results in a region where the broad patterns of

change – or the order of magnitude of the changes – are relatively close to those of the

state as a whole. Thus, the region strongly mirrors New Jersey.

45

Table 6 Four County Aggregate Employment Change by NAICS Supersector

2nd Quarter 2002- 2nd Quarter 2008 2002 2008 Change NJ Q2 Q2 Number Percent PercentTOTAL NONFARM 718,203 730,495 12,292 1.7 2.9 TOTAL PRIVATE SECTOR 602,120 606,359 4,240 0.7 2.3 GOODS PRODUCING 91,028 85,976 -5,052 -5.5 -10.6

Natural Resources And Mining 948 979 31 3.3 6.7Construction 27,049 28,038 989 3.7 3.9Manufacturing 63,031 56,959 -6,072 -9.6 -17.6

PRIVATE SERVICE-PROVIDING 511,092 520,383 9,291 1.8 4.9