1 | P a g e

SUGGESTED SOLUTION

(Date : 30 April, 2014)

Head Office : Shraddha, 3rd Floor, Near Chinai College, Andheri (E), Mumbai – 69.

Tel : (022) 26836666

2 | P a g e

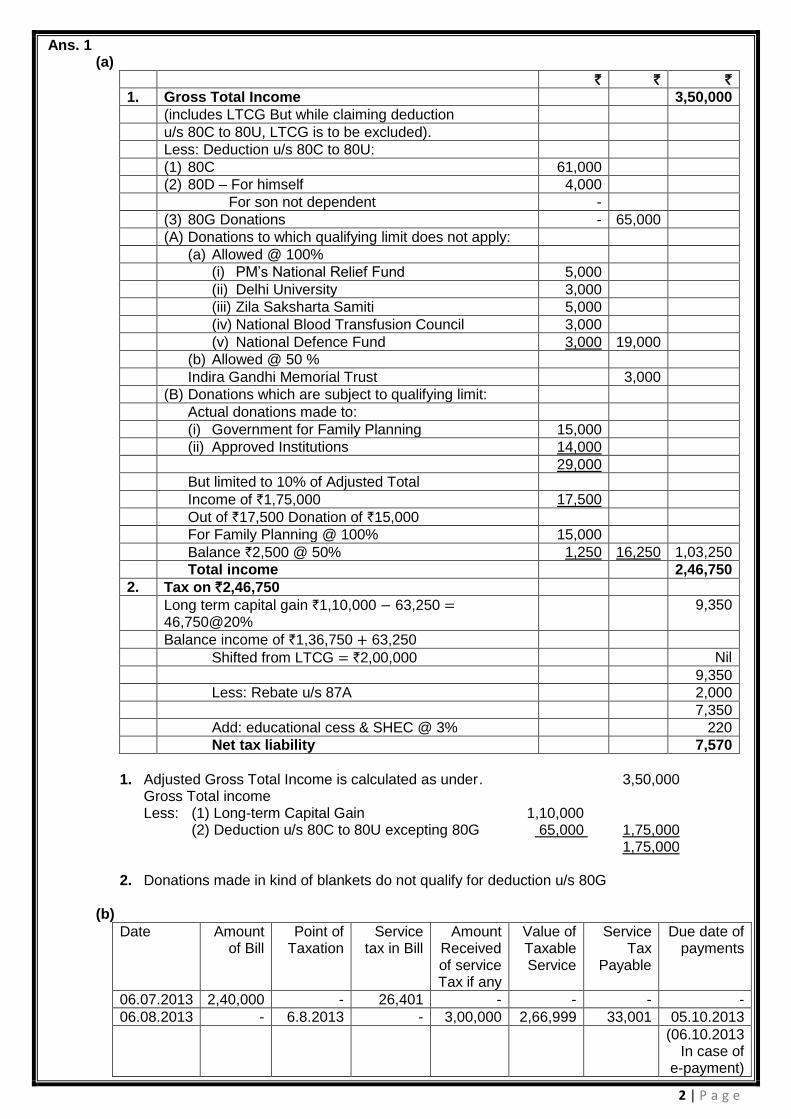

Ans. 1 (a)

` ` `

1. Gross Total Income 3,50,000

(includes LTCG But while claiming deduction

u/s 80C to 80U, LTCG is to be excluded).

Less: Deduction u/s 80C to 80U:

(1) 80C 61,000

(2) 80D – For himself 4,000

For son not dependent -

(3) 80G Donations - 65,000

(A) Donations to which qualifying limit does not apply:

(a) Allowed @ 100%

(i) PM’s National Relief Fund 5,000

(ii) Delhi University 3,000

(iii) Zila Saksharta Samiti 5,000

(iv) National Blood Transfusion Council 3,000

(v) National Defence Fund 3,000 19,000

(b) Allowed @ 50 %

Indira Gandhi Memorial Trust 3,000

(B) Donations which are subject to qualifying limit:

Actual donations made to:

(i) Government for Family Planning 15,000

(ii) Approved Institutions 14,000

29,000

But limited to 10% of Adjusted Total

Income of `1,75,000 17,500

Out of `17,500 Donation of `15,000

For Family Planning @ 100% 15,000

Balance `2,500 @ 50% 1,250 16,250 1,03,250

Total income 2,46,750

2. Tax on `2,46,750

Long term capital gain `1,10,000 63,250 46,750@20%

9,350

Balance income of `1,36,750 63,250

Shifted from LTCG `2,00,000 Nil

9,350

Less: Rebate u/s 87A 2,000

7,350

Add: educational cess & SHEC @ 3% 220

Net tax liability 7,570

1. Adjusted Gross Total Income is calculated as under . 3,50,000

Gross Total income Less: (1) Long-term Capital Gain 1,10,000 (2) Deduction u/s 80C to 80U excepting 80G 65,000 1,75,000 1,75,000

2. Donations made in kind of blankets do not qualify for deduction u/s 80G

(b)

Date Amount of Bill

Point of Taxation

Service tax in Bill

Amount Received of service Tax if any

Value of Taxable Service

Service Tax

Payable

Due date of payments

06.07.2013 2,40,000 - 26,401 - - - -

06.08.2013 - 6.8.2013 - 3,00,000 2,66,999 33,001 05.10.2013

(06.10.2013 In case of

e-payment)

3 | P a g e

08.08.2013 2,31,399 8.8.2013 28,601 - 2,31,399 28,601 -do-

05.09.2013 - 5.9.2013 - 1,60,000 1,42,399 17,601 -do-

28.09.2013 - 28.9.2013 - 2,50,000 2,22,499 27,501 -do-

8,63,296 1,06,704

(c)

Tax liability of Raj

Selling price – `2,40,000 VAT Net payable

`2,40,000 12.5% 30,000

Less: Input VAT credit Nil 30,000

Tax liability of Shyam

Selling price – `3,00,000 VAT Net payable

`3,00,000 12.5% 37,500 Less: Input VAT credit 30,000 7,500

Tax liability of Tarang

Selling price – `4,00,000 VAT Net payable

`4,00,000 12.5% 50,000

Less: Input VAT credit 37,500 12,500

Tax liability of Retailer

Selling price – `5,00,000 VAT Net payable

`5,00,000 12.5% 62,500 Less: Input VAT credit 50,000 12,500

Ans. 2

(a) Income from Salaries for the assessment year 2014-15 Basic Salary (`30,000 9) 2,70,000

Dearness Allowance (`6,000 9) 54,000

House Rent Allowance (`3,750 9) 33,750

Conveyance Allowance (`1,300 9) (800 9) 4,500 Gratuity received 6,00,000 Less: exempt minimum of the following limits (a) `6,00,000 – Actual amount (b) `5,40,000 – ½ month average salary for 30 years

(36, 000/2 30)

(c) `10,00,000 5,40,000 60,000 Leave salary received 3,60,000 Less: Exempt minimum of the following limits (a) `3,60,000 (10 month average salary) (b) `3,60,000 (amount actually received) (c) `3,00,000 (amount specified by Government) (d) `3,60,000 (cash equivalent to unavailed leave) 3,00,000 60,000 Pension 3/4 of commuted 4,50,000 Hence 1/3 of pension

2,00,000

Taxable 2,50,000 Un-commuted pension (3 3,750) 11,250

7,43,500 Less: Employment Tax 1,000

Income from Salary 7,42,500

4 | P a g e

Note:- In the absence of information, it is assumed that there was no change in the basic salary of last 10 months (b)

1. Value of service provided in the previous financial year exceeded `50,00,000 In this question the service provider is a partnership firm, hence service tax is payable after the end of each quarter and not monthly

Point of Taxation of Service Value of Taxable Service

July 2013 15,00,000 3,00,000 (Exempt service) 12,00,000

August 2013 20,00,000 2,00,000 (Exempt service) 18,00,000 September 2013 (advance received for service yet to be rendered) 5,00,000

Total Value of services on which service tax is payable 35,00,000

Amount of service tax payable @ 12.36% of `35,00,000 4,32,600

Service tax should be deposited by 5.10.2013 (6.10.2013 in case of e-payment) Service tax is payable even if the payment of `4,00,000 has not been received for the service rendered in August 2013. 2. Since the services provided in the preceding financial year did not exceed `50,00,000, the

liability to make payment of service tax shall arise on the basis of receipt of payment. August 2013 `15,00,000 `3,00,000 (Exempt service) 12,00,000 September 2013 `16,00,000 `2,00,000 14,00,000

September 2013 Advance received 5,00,000

31,00,000

Amount of service tax payable @ 12.36% of ` 31,00,000 = `3,83,160 Service tax shall be deposited by 5.10.2013 to 6.10.2013 in case of payment.

(c) Total Sale Price Input VAT credit 1. Cost of imported RM of China 12,00,000 - 2. Cost of imported from other states 20,40,000 3. Cost of goods purchased form sale

(`22,50,000 100 /112.5) 20,00,000 2,50,000

4. Other expenditure 2,00,000

Total 54,40,000 5. Net profit 25% on cost (see working note) 13,60,000

Total S.P 68,00,000 Vat Payable Sale to Sarkar 60 % of `68,00,000, 40,80,000 12.5% VAT 5,10,000 VAT Sale to Karan 30 % of `68,00,000 20,40,00 2% CST 40,800 CST Sale to Yash 10 % of `68,00,000 Nil VAT Payable ` 5,10,000 2,50,000 2,60,000 CST payable 40,800 Nil 40,800

Working note : 1. calculation of Profit on Cost Assume S.P. 100 Profit 20% of S.P. 20

Profit on cost 20 100/80 25% 2. Goods which have been imported from other states are not eligible for VAT credit.

Ans. 3

(a) Total income of the firm

` ` Book Profit 59,000 Net Profit as per P/L A/C Add: In admissible expenses Donations 4,000 Depreciation 3,000 Typewriter Purchase 3,200 Income-tax 2,720

5 | P a g e

Interest on capital in excess of 12% p.a. 7,000 Provision for bad debt 2,300 22,220 81,220 Less: Income to treated separately Interest on Government Securities 3,000 Dividends 7,000 Long-term capital gain 2,000 Lottery income 20,000 32,000 Less: Admissible expense Depreciation as per Income-tax Act Furniture @ 10% on `30,000 3,000 Typewriter @ 15 % on `3,200 480 3,480 Income from business 45,740 Income from capital gain Long-term capital gain 2,000 Income from other sources Interest on Government Securities 3,000 Dividends Exempt Lottery income 20,000 23,000 Total income 70,740 Less: Deduction u/s 80G 50% of `4,000 2,000

Total income 68,740 Tax payable by firm Income other than LTCG and lottery – `46,740 @ 30% 14,022 Lottery income - @ 30 % on `20,000 6,000 Long-term capita; gain- `2,000 @ 20% 400 Tax payable 20,422 Add : Education cess & SHEC @ 3% 613 21,035 Total rounded off 21,040

(b)

Computation of Value of Taxable Service for the F.Y. 2013-14

Particulars Amount (`)

Services rendered in tax planning 50,000

Representation of client before CESTAT 40,000

Preparation of financial statements 4,00,000

Certification of documents under export and Import policy 1,50,000

Receipt for the legal service given in the month of December, 2012 50,000

Gross receipts (including service tax) 6,90,000

Value of Taxable services (6,90,000 100 /112.36) 6,14,098

(c)

Computation of VAT eligible for carry forward

Particulars Notes Amount (`) Amount (`)

A. Purchased during the month 4,80,000

B. Input tax paid @ 12.5% (input tax) a 12.5% 60,000

C. Intra state sales during the month 12,00,000

D. Tax @4% on sales of goods c 4% 48,000

E. Net VAT liability during the month d b, if positive

Nil

F. Input credit after set-off b d 12,000

G. Inter State sales 6,00,000

H. CST liability to be paid on inter-state sales g 2% 12,000

I. Credit to be carried forward f h Nil

In case, if the CST liability is `10,000/-, then the credit to be carried forward will be `2,000.

6 | P a g e

Ans. 4 (a)

Assessment year 2014-15 Rohan Mohan Soham Johar ` ` ` `

WDV as on 1.4.2013 1,70,000 90,000 1,50,000 1,70,000 Addition during the year

(i) For 180 days or more 2,00,000 2,00,000 2,00,000 80,000 (ii) Less than 180 days 2,00,000 2,00,000 2,00,000 2,00,000

Total 5,70,000 4,90,000 5,50,000 4,50,000 Less Sale Proceeds of Plant sold During the year 1,00,000 4,00,000 3,90,000 4,50,000

In case ‘M’ limited to total value W.D.V. for the purpose of charging Depreciation as on 31.3.2014 4,70,000 90,000 1,60,000 Nil Depreciation allowed during the year In case of R

15% on `2,70,000 55,500 7.5% on `2,00,000

In case of G 6,750 7.5% on `90,000

In case of S 12,000 7.5% on `1,60,000 -

W.D.V. as on 1.4.2014 4,14,500 83,250 1,48,000 Nil

Short-term capital gain in case of M - - - 4,57,000 Less: Cost of acquisition plus the value of the asset purchased during the year

`1,70,000 2,80,000 4,50,000

Short-term capital gain 7,000

(b)

` ` (i) Income from house property (-) 45,000

Set off from long-term capital gain 45,000 Nil

(ii) Profit and Gains from Business

- Business income 2,20,000 - Speculation business 15,000 2,35,000

(iii) Capital Gains

- long-term capital gains 1,30,000 - Short-term capital loss (-) 27,000

1,03,000 Less: Loss from house property 45,000 Interest from other source 12,000 57,000 46,000

(iv) Loss under the head other sources 12,000

Less: Set off – Long-term capital gain 12,000 Nil

Gross total income 2,81,000

(c)

Computation of taxable income or Mrs. R `

Income from Salary 2,20,000 Income from other sources: Lottery income 7,000

Gross total income 2,27,000 Tax on `7,000 of lottery income @ 30% 2,100 Tax on `2,20,000 2,000 4,100 Less: Tax rebate 2,000 2,100

7 | P a g e

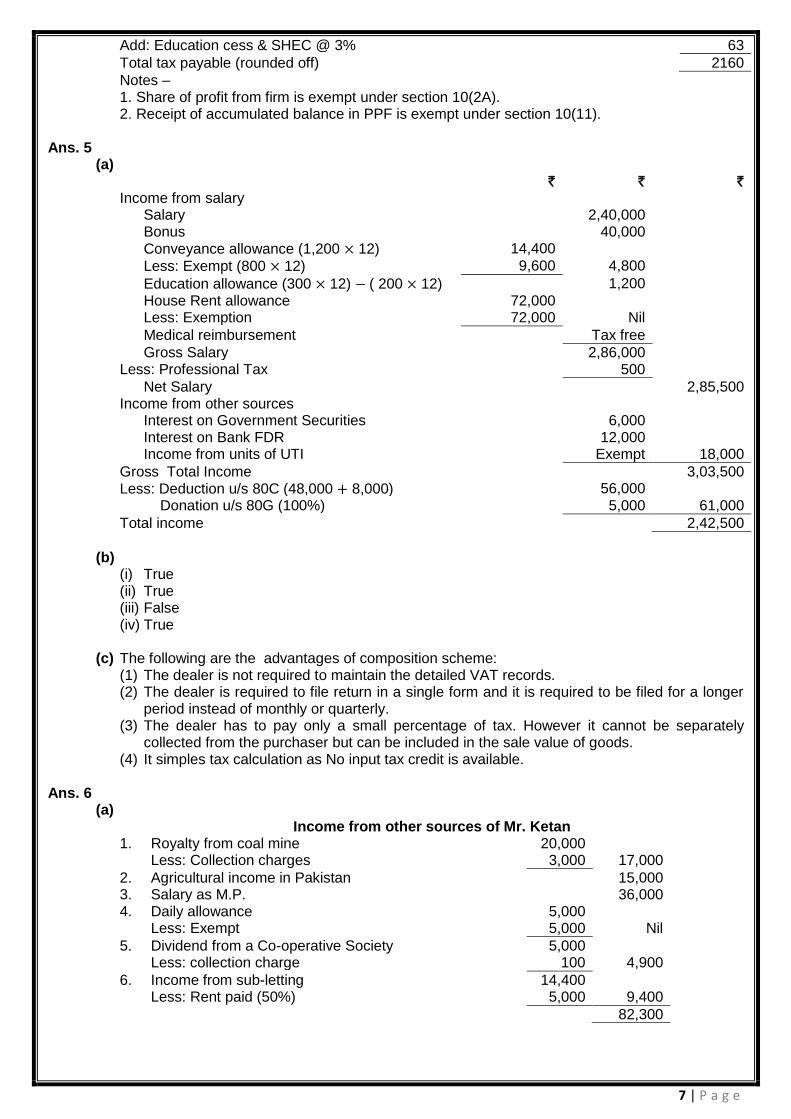

Add: Education cess & SHEC @ 3% 63

Total tax payable (rounded off) 2160

Notes – 1. Share of profit from firm is exempt under section 10(2A). 2. Receipt of accumulated balance in PPF is exempt under section 10(11).

Ans. 5 (a)

` ` ` Income from salary

Salary 2,40,000 Bonus 40,000 Conveyance allowance (1,200 12) 14,400

Less: Exempt (800 12) 9,600 4,800

Education allowance (300 12) ( 200 12) 1,200

House Rent allowance 72,000 Less: Exemption 72,000 Nil

Medical reimbursement Tax free

Gross Salary 2,86,000 Less: Professional Tax 500

Net Salary 2,85,500 Income from other sources

Interest on Government Securities 6,000 Interest on Bank FDR 12,000 Income from units of UTI Exempt 18,000

Gross Total Income 3,03,500 Less: Deduction u/s 80C (48,000 8,000) 56,000

Donation u/s 80G (100%) 5,000 61,000

Total income 2,42,500

(b)

(i) True (ii) True (iii) False (iv) True

(c) The following are the advantages of composition scheme:

(1) The dealer is not required to maintain the detailed VAT records. (2) The dealer is required to file return in a single form and it is required to be filed for a longer

period instead of monthly or quarterly. (3) The dealer has to pay only a small percentage of tax. However it cannot be separately

collected from the purchaser but can be included in the sale value of goods. (4) It simples tax calculation as No input tax credit is available.

Ans. 6

(a) Income from other sources of Mr. Ketan

1. Royalty from coal mine 20,000 Less: Collection charges 3,000 17,000

2. Agricultural income in Pakistan 15,000 3. Salary as M.P. 36,000 4. Daily allowance 5,000

Less: Exempt 5,000 Nil

5. Dividend from a Co-operative Society 5,000 Less: collection charge 100 4,900

6. Income from sub-letting 14,400 Less: Rent paid (50%) 5,000 9,400

82,300

8 | P a g e

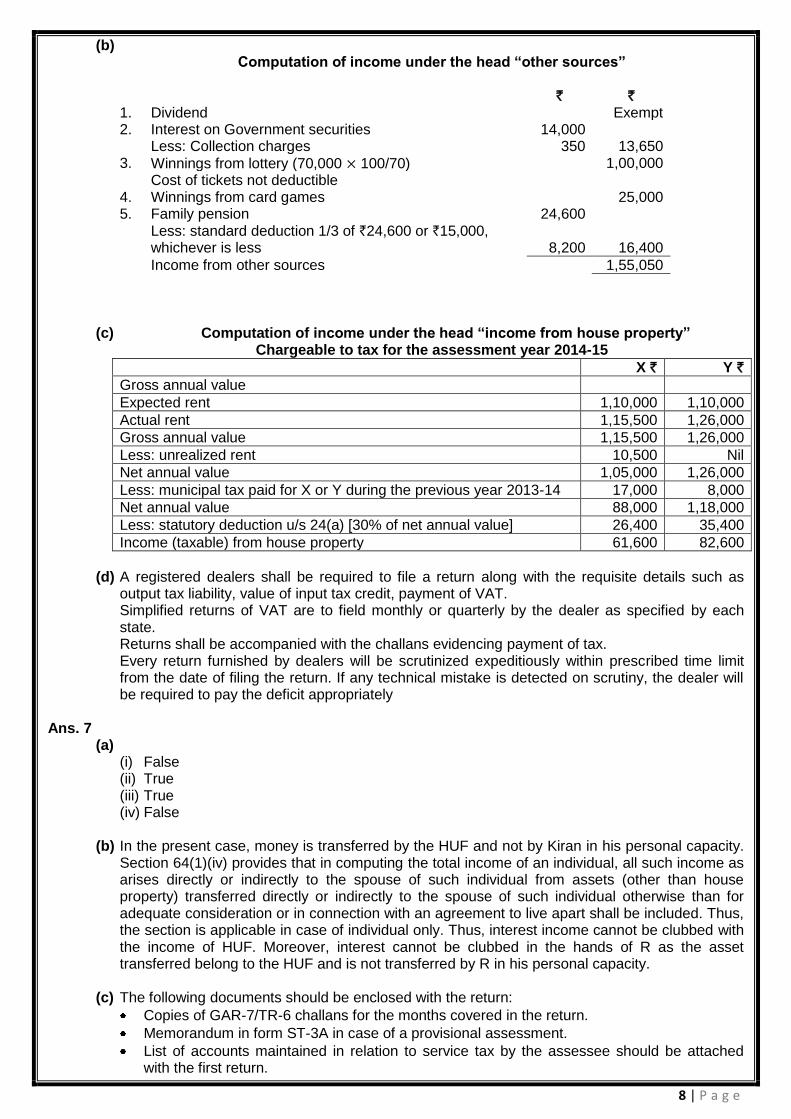

(b) Computation of income under the head “other sources”

` `

1. Dividend Exempt 2. Interest on Government securities 14,000

Less: Collection charges 350 13,650 3. Winnings from lottery (70,000 100/70) 1,00,000

Cost of tickets not deductible 4. Winnings from card games 25,000 5. Family pension 24,600

Less: standard deduction 1/3 of `24,600 or `15,000, whichever is less 8,200 16,400

Income from other sources 1,55,050

(c) Computation of income under the head “income from house property” Chargeable to tax for the assessment year 2014-15

X ` Y `

Gross annual value

Expected rent 1,10,000 1,10,000

Actual rent 1,15,500 1,26,000

Gross annual value 1,15,500 1,26,000

Less: unrealized rent 10,500 Nil

Net annual value 1,05,000 1,26,000

Less: municipal tax paid for X or Y during the previous year 2013-14 17,000 8,000

Net annual value 88,000 1,18,000

Less: statutory deduction u/s 24(a) [30% of net annual value] 26,400 35,400

Income (taxable) from house property 61,600 82,600

(d) A registered dealers shall be required to file a return along with the requisite details such as

output tax liability, value of input tax credit, payment of VAT. Simplified returns of VAT are to field monthly or quarterly by the dealer as specified by each state. Returns shall be accompanied with the challans evidencing payment of tax. Every return furnished by dealers will be scrutinized expeditiously within prescribed time limit from the date of filing the return. If any technical mistake is detected on scrutiny, the dealer will be required to pay the deficit appropriately

Ans. 7 (a)

(i) False (ii) True (iii) True (iv) False

(b) In the present case, money is transferred by the HUF and not by Kiran in his personal capacity.

Section 64(1)(iv) provides that in computing the total income of an individual, all such income as arises directly or indirectly to the spouse of such individual from assets (other than house property) transferred directly or indirectly to the spouse of such individual otherwise than for adequate consideration or in connection with an agreement to live apart shall be included. Thus, the section is applicable in case of individual only. Thus, interest income cannot be clubbed with the income of HUF. Moreover, interest cannot be clubbed in the hands of R as the asset transferred belong to the HUF and is not transferred by R in his personal capacity.

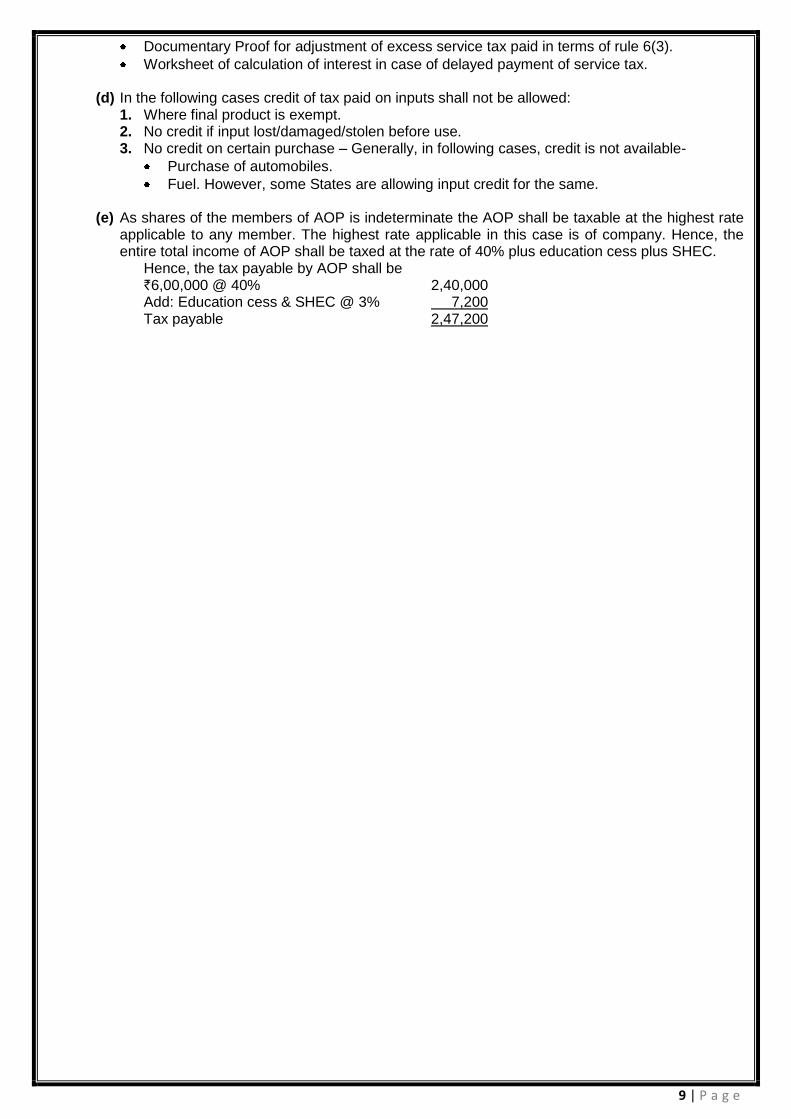

(c) The following documents should be enclosed with the return:

Copies of GAR-7/TR-6 challans for the months covered in the return.

Memorandum in form ST-3A in case of a provisional assessment.

List of accounts maintained in relation to service tax by the assessee should be attached with the first return.

9 | P a g e

Documentary Proof for adjustment of excess service tax paid in terms of rule 6(3).

Worksheet of calculation of interest in case of delayed payment of service tax.

(d) In the following cases credit of tax paid on inputs shall not be allowed: 1. Where final product is exempt. 2. No credit if input lost/damaged/stolen before use. 3. No credit on certain purchase – Generally, in following cases, credit is not available-

Purchase of automobiles.

Fuel. However, some States are allowing input credit for the same.

(e) As shares of the members of AOP is indeterminate the AOP shall be taxable at the highest rate applicable to any member. The highest rate applicable in this case is of company. Hence, the entire total income of AOP shall be taxed at the rate of 40% plus education cess plus SHEC.

Hence, the tax payable by AOP shall be `6,00,000 @ 40% 2,40,000 Add: Education cess & SHEC @ 3% 7,200 Tax payable 2,47,200

10 | P a g e

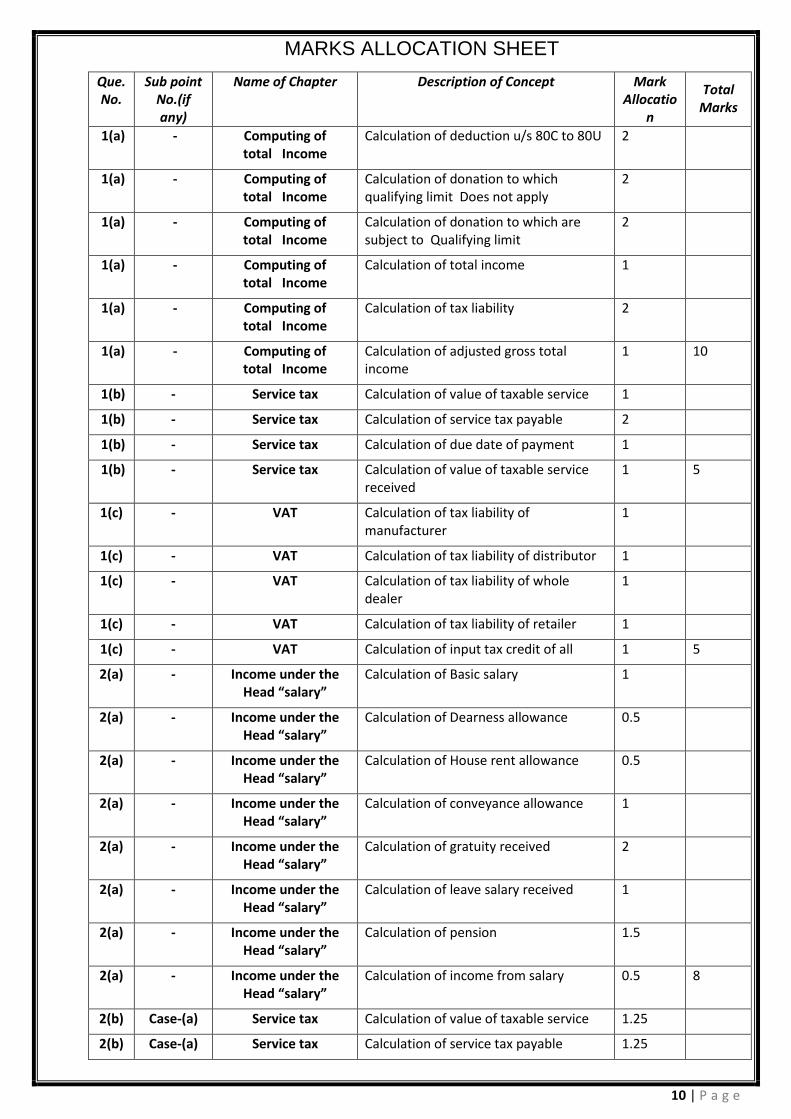

MARKS ALLOCATION SHEET

Que. No.

Sub point No.(if any)

Name of Chapter Description of Concept Mark Allocatio

n

Total Marks

1(a) - Computing of total Income

Calculation of deduction u/s 80C to 80U 2

1(a) - Computing of total Income

Calculation of donation to which qualifying limit Does not apply

2

1(a) - Computing of total Income

Calculation of donation to which are subject to Qualifying limit

2

1(a) - Computing of total Income

Calculation of total income 1

1(a) - Computing of total Income

Calculation of tax liability 2

1(a) - Computing of total Income

Calculation of adjusted gross total income

1 10

1(b) - Service tax Calculation of value of taxable service 1

1(b) - Service tax Calculation of service tax payable 2

1(b) - Service tax Calculation of due date of payment 1

1(b) - Service tax Calculation of value of taxable service received

1 5

1(c) - VAT Calculation of tax liability of manufacturer

1

1(c) - VAT Calculation of tax liability of distributor 1

1(c) - VAT Calculation of tax liability of whole dealer

1

1(c) - VAT Calculation of tax liability of retailer 1

1(c) - VAT Calculation of input tax credit of all 1 5

2(a) - Income under the Head “salary”

Calculation of Basic salary 1

2(a) - Income under the Head “salary”

Calculation of Dearness allowance 0.5

2(a) - Income under the Head “salary”

Calculation of House rent allowance 0.5

2(a) - Income under the Head “salary”

Calculation of conveyance allowance 1

2(a) - Income under the Head “salary”

Calculation of gratuity received 2

2(a) - Income under the Head “salary”

Calculation of leave salary received 1

2(a) - Income under the Head “salary”

Calculation of pension 1.5

2(a) - Income under the Head “salary”

Calculation of income from salary 0.5 8

2(b) Case-(a) Service tax Calculation of value of taxable service 1.25

2(b) Case-(a) Service tax Calculation of service tax payable 1.25

11 | P a g e

2(b) Case-(b) Service tax Calculation of value of taxable service 1.25

2(b) Case-(b) Service tax Calculation of service tax payable 1.25 5

2(c) - VAT Calculation of total sale price 1

2(c) - VAT Calculation of other expenditure 1

2(c) - VAT Calculation of VAT payable 1

2(c) - VAT Calculation of CST payable 1

2(c) - VAT Calculation of profit on cost 1 5

3(a) - Assessment of firms Calculation of admissible expenses 1.5

3(a) - Assessment of firms Calculation of income to treated separately

1.5

3(a) - Assessment of firms Calculation of income from business 0.5

3(a) - Assessment of firms Calculation of income from capital gain 0.5

3(a) - Assessment of firms Calculation of income from other sources

2

3(a) - Assessment of firms Calculation of deduction u/s 80G 1

3(a) - Assessment of firms Calculation of tax payable 1 8

3(b) - Service tax Calculation of Gross receipts 3

3(b) - Service tax Calculation of value of taxable services 1 4

3(C) - VAT Calculation of net VAT liability 2

3(C) - VAT Calculation of CST liability 1

3(C) - VAT Calculation of credit to be carried forward

1 4

4(a) - Income under the Head “capital gain”

Calculation of depreciation for the previous year

3

4(a) - Income under the Head “capital gain”

Calculation of written down value of asset

3

4(a) - Income under the Head “capital gain”

Calculation of short term capital gain 2 8

4(b) - Set off/ carry forward Of losses

Calculation of income from house property

0.5

4(b) - Set off/ carry forward Of losses

Calculation of profit & gain from business

1

4(b) - Set off/ carry forward Of losses

Calculation of capital gain 1

4(b) - Set off/ carry forward Of losses

Calculation of other sources 1

4(b) - Set off/ carry forward Of losses

Calculation of gross total income 0.5 4

4(c) - Non-taxable income Calculation of Gross total income 2

4(c) - Non-taxable income Calculation of total tax payable 2 4

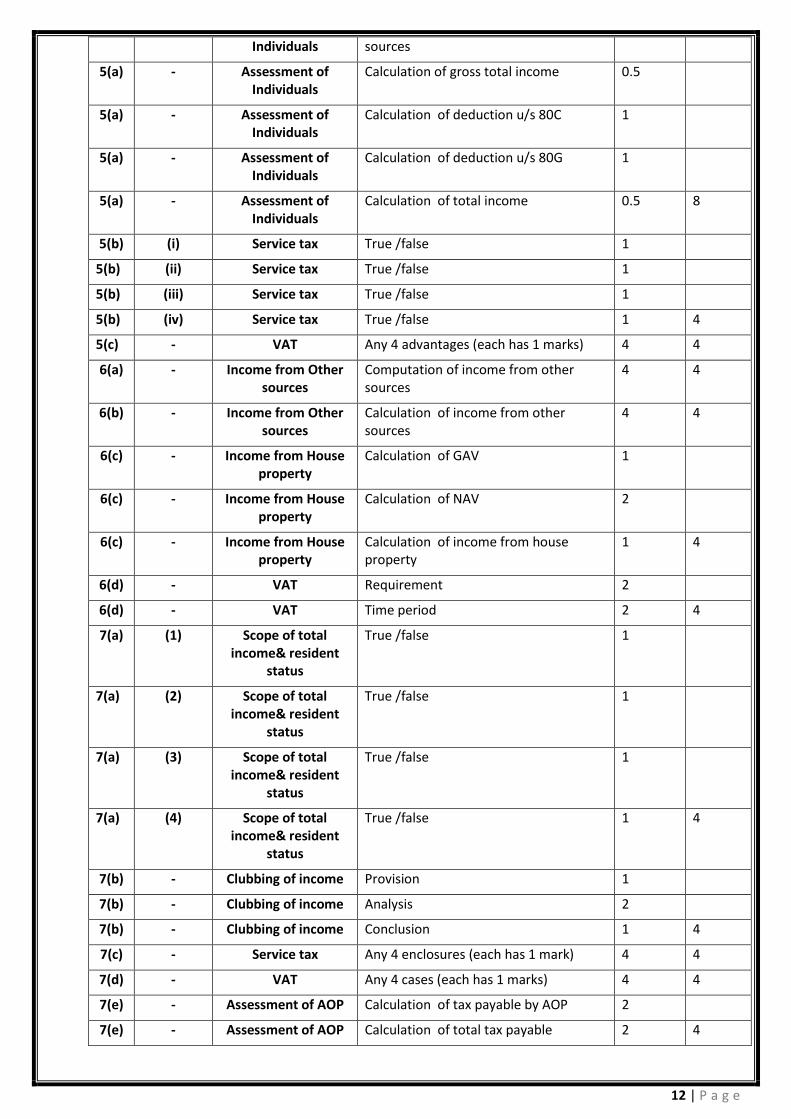

5(a) - Assessment of Individuals

Calculation of income from salary 2

5(a) - Assessment of Individuals

Calculation of net salary 1

5(a) - Assessment of Calculation of income from other 2

12 | P a g e

Individuals sources

5(a) - Assessment of Individuals

Calculation of gross total income 0.5

5(a) - Assessment of Individuals

Calculation of deduction u/s 80C 1

5(a) - Assessment of Individuals

Calculation of deduction u/s 80G 1

5(a) - Assessment of Individuals

Calculation of total income 0.5 8

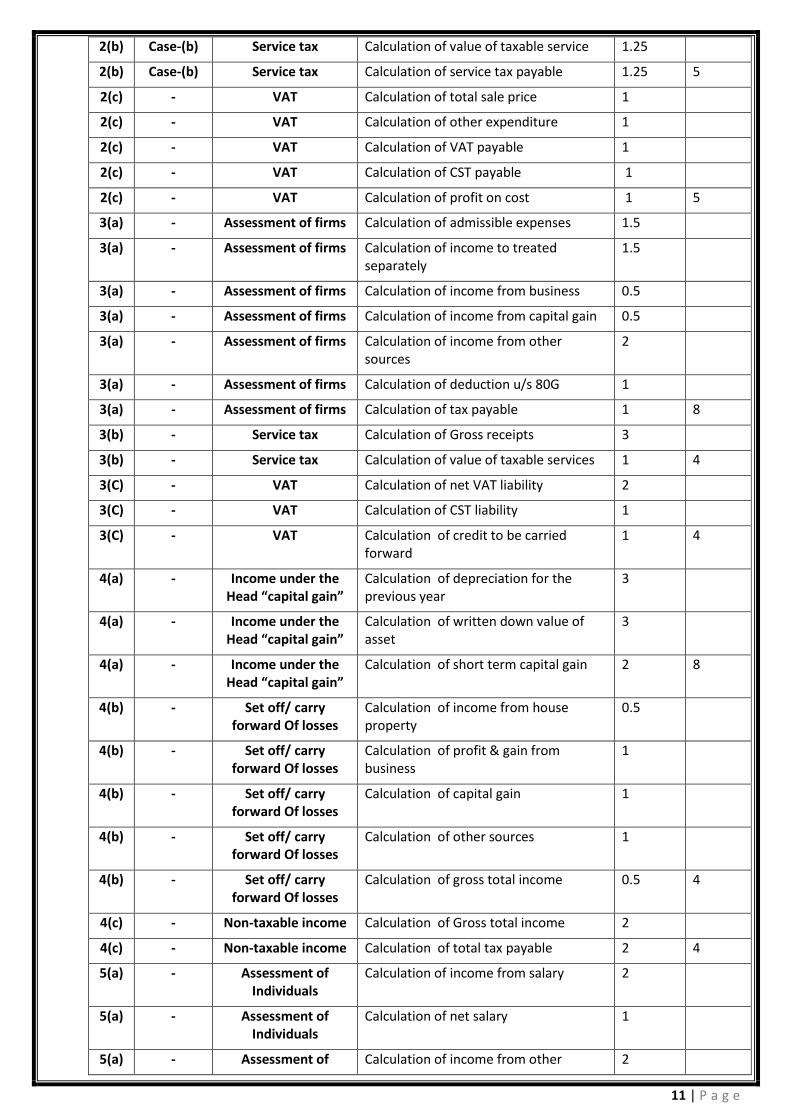

5(b) (i) Service tax True /false 1

5(b) (ii) Service tax True /false 1

5(b) (iii) Service tax True /false 1

5(b) (iv) Service tax True /false 1 4

5(c) - VAT Any 4 advantages (each has 1 marks) 4 4

6(a) - Income from Other sources

Computation of income from other sources

4 4

6(b) - Income from Other sources

Calculation of income from other sources

4 4

6(c) - Income from House property

Calculation of GAV 1

6(c) - Income from House property

Calculation of NAV 2

6(c) - Income from House property

Calculation of income from house property

1 4

6(d) - VAT Requirement 2

6(d) - VAT Time period 2 4

7(a) (1) Scope of total income& resident

status

True /false 1

7(a) (2) Scope of total income& resident

status

True /false 1

7(a) (3) Scope of total income& resident

status

True /false 1

7(a) (4) Scope of total income& resident

status

True /false 1 4

7(b) - Clubbing of income Provision 1

7(b) - Clubbing of income Analysis 2

7(b) - Clubbing of income Conclusion 1 4

7(c) - Service tax Any 4 enclosures (each has 1 mark) 4 4

7(d) - VAT Any 4 cases (each has 1 marks) 4 4

7(e) - Assessment of AOP Calculation of tax payable by AOP 2

7(e) - Assessment of AOP Calculation of total tax payable 2 4

Recommended