STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

1

Solutions for a Changing Landscape: Image Cash Letter with ACH

How Tarrant County used Check 21 Technology to Their Advantage

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

2

Agenda

Consumer to Business Payments

Changing Payments Landscape

Industry Update

Solutions for the Changing Landscape

Tarrant County Tax Office-Background

Tarrant County Tax Office-Back Office Project

Tarrant County Tax Office-What’s next?

Questions

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

3

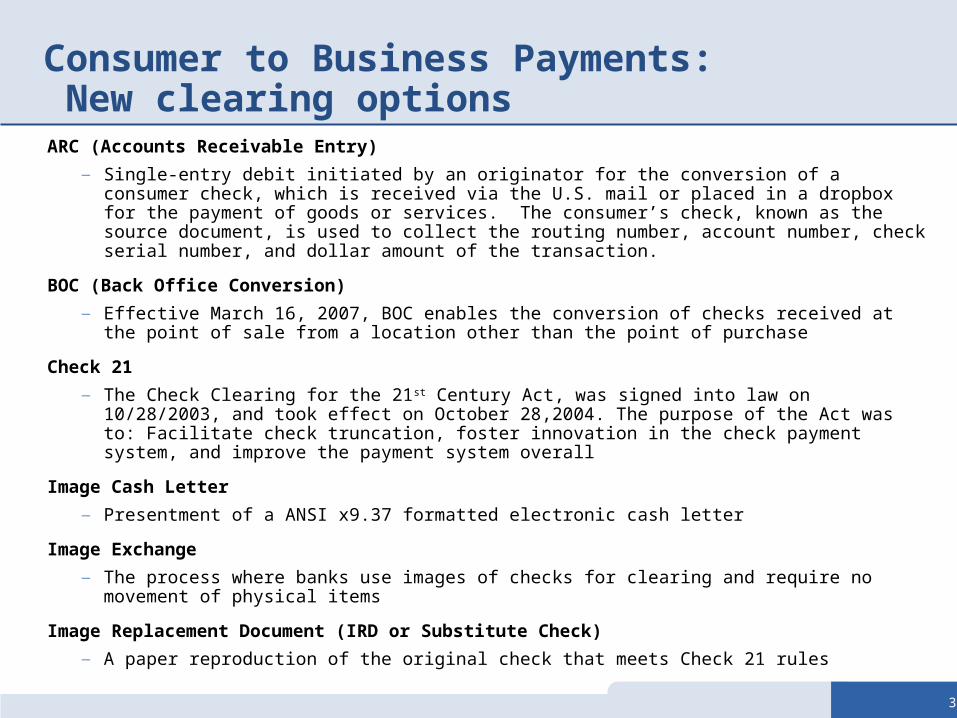

ARC (Accounts Receivable Entry)

― Single-entry debit initiated by an originator for the conversion of a consumer check, which is received via the U.S. mail or placed in a dropbox for the payment of goods or services. The consumer’s check, known as the source document, is used to collect the routing number, account number, check serial number, and dollar amount of the transaction.

BOC (Back Office Conversion)

― Effective March 16, 2007, BOC enables the conversion of checks received at the point of sale from a location other than the point of purchase

Check 21

― The Check Clearing for the 21st Century Act, was signed into law on 10/28/2003, and took effect on October 28,2004. The purpose of the Act was to: Facilitate check truncation, foster innovation in the check payment system, and improve the payment system overall

Image Cash Letter

― Presentment of a ANSI x9.37 formatted electronic cash letter

Image Exchange

― The process where banks use images of checks for clearing and require no movement of physical items

Image Replacement Document (IRD or Substitute Check)

― A paper reproduction of the original check that meets Check 21 rules

Consumer to Business Payments: New clearing options

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

4

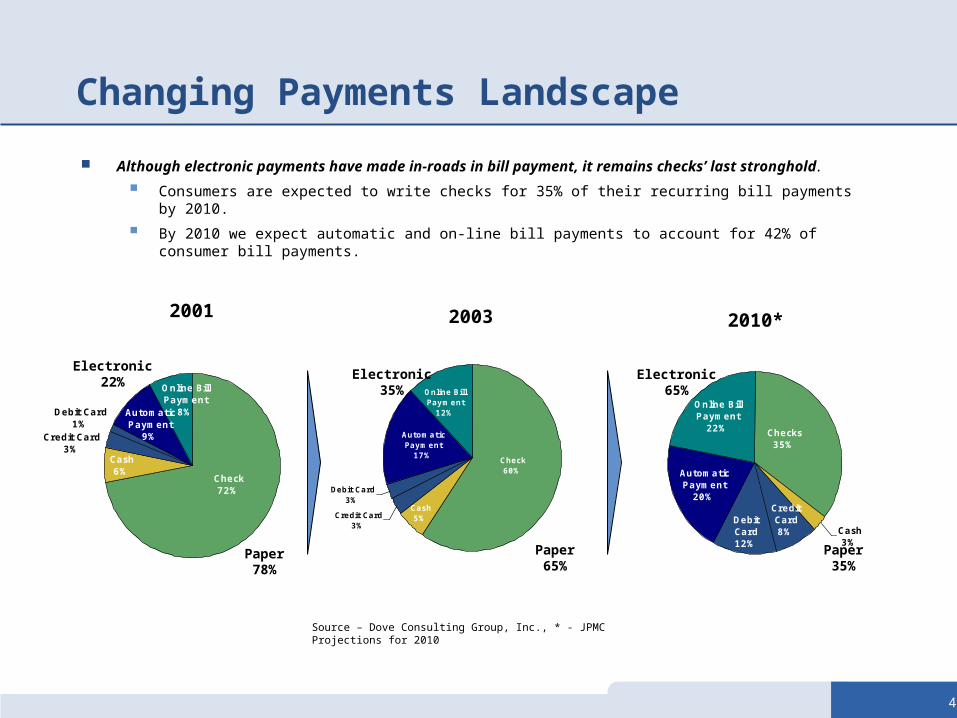

Changing Payments Landscape

Although electronic payments have made in-roads in bill payment, it remains checks’ last stronghold.

Consumers are expected to write checks for 35% of their recurring bill payments by 2010.

By 2010 we expect automatic and on-line bill payments to account for 42% of consumer bill payments.

Credit Card3%

Debit Card3%

Online Bill Payment

12%

Check60%

Automatic Payment

17%

Cash5%

Paper65%

Electronic35%

Debit Card1%

Credit Card3%

Cash6%

AutomaticPayment

9%

Online Bill Payment

8%

Check 72%

Electronic22%

Paper78%

2001 2003

Source – Dove Consulting Group, Inc., * - JPMC Projections for 2010

Checks35%

Online Bill Payment

22%

AutomaticPayment

20%

Cash3%

CreditCard8%

DebitCard12%

Electronic65%

Paper35%

2010*

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

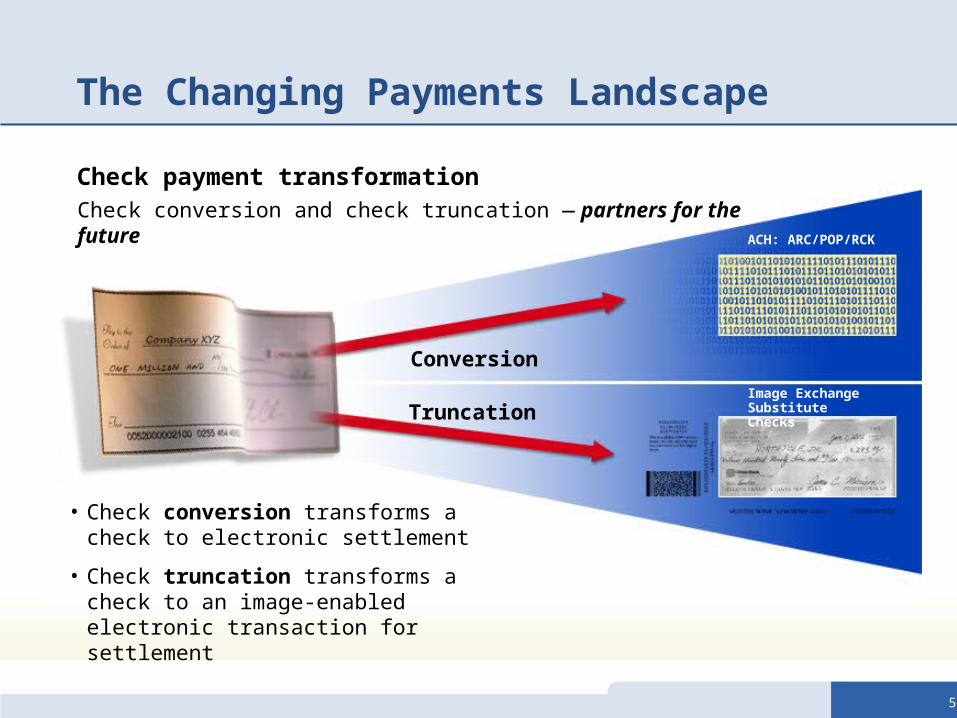

5

Conversion

Truncation

ACH: ARC/POP/RCK

Image ExchangeSubstitute Checks

Check conversion and check truncation — partners for the future

• Check conversion transforms a check to electronic settlement

• Check truncation transforms a check to an image-enabled electronic transaction for settlement

Check payment transformation

The Changing Payments Landscape

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

6

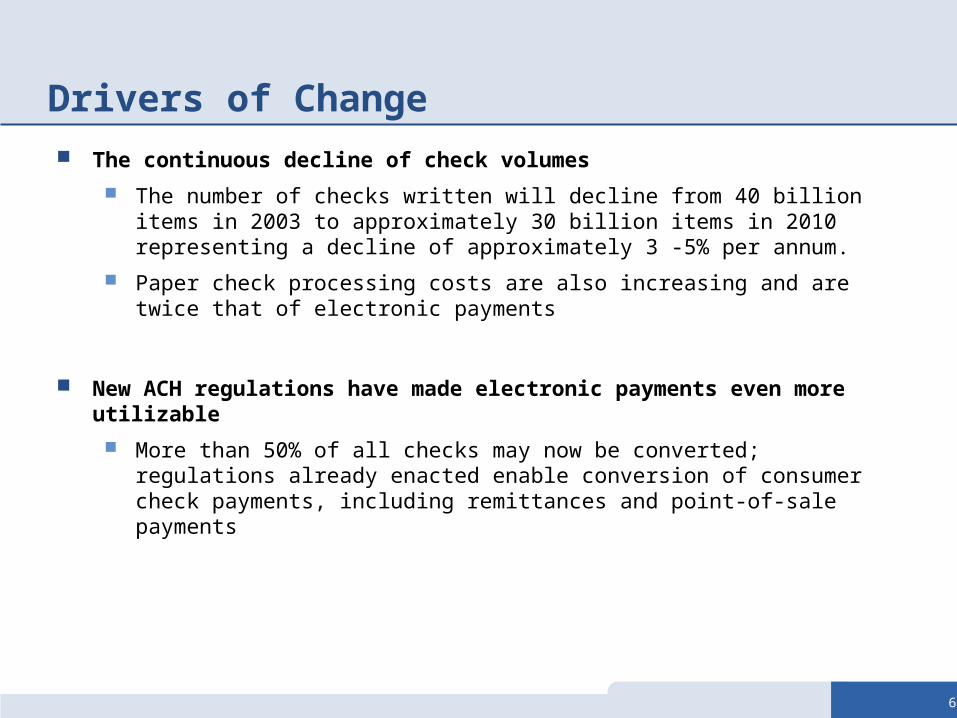

Drivers of Change The continuous decline of check volumes

The number of checks written will decline from 40 billion items in 2003 to approximately 30 billion items in 2010 representing a decline of approximately 3 -5% per annum.

Paper check processing costs are also increasing and are twice that of electronic payments

New ACH regulations have made electronic payments even more utilizable

More than 50% of all checks may now be converted; regulations already enacted enable conversion of consumer check payments, including remittances and point-of-sale payments

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

7

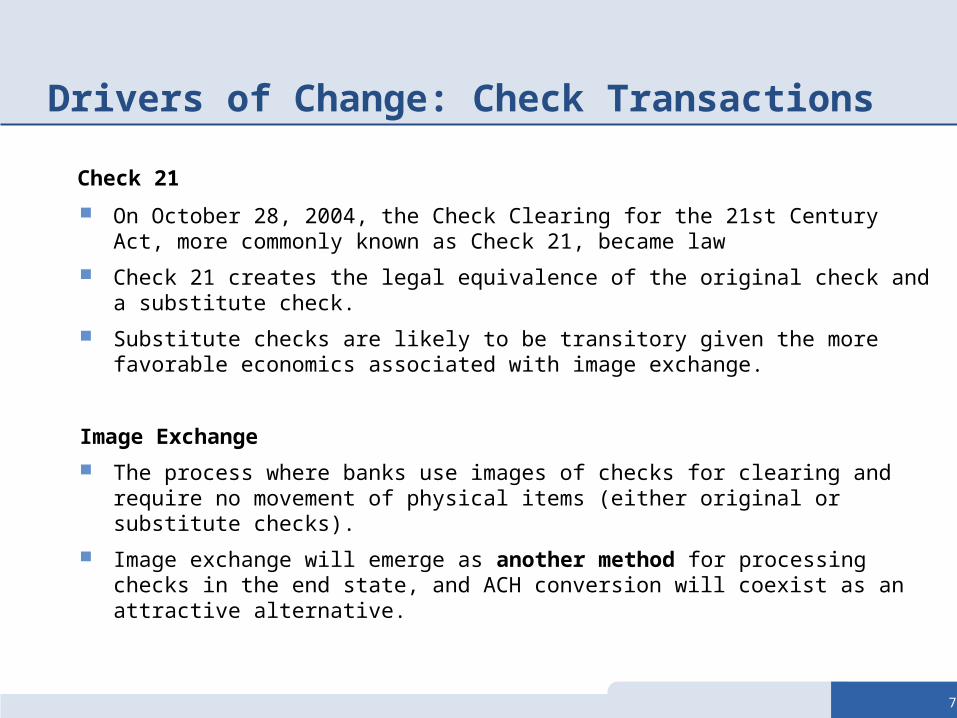

Check 21

On October 28, 2004, the Check Clearing for the 21st Century Act, more commonly known as Check 21, became law

Check 21 creates the legal equivalence of the original check and a substitute check.

Substitute checks are likely to be transitory given the more favorable economics associated with image exchange.

Image Exchange

The process where banks use images of checks for clearing and require no movement of physical items (either original or substitute checks).

Image exchange will emerge as another method for processing checks in the end state, and ACH conversion will coexist as an attractive alternative.

Drivers of Change: Check Transactions

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

8

Key messages

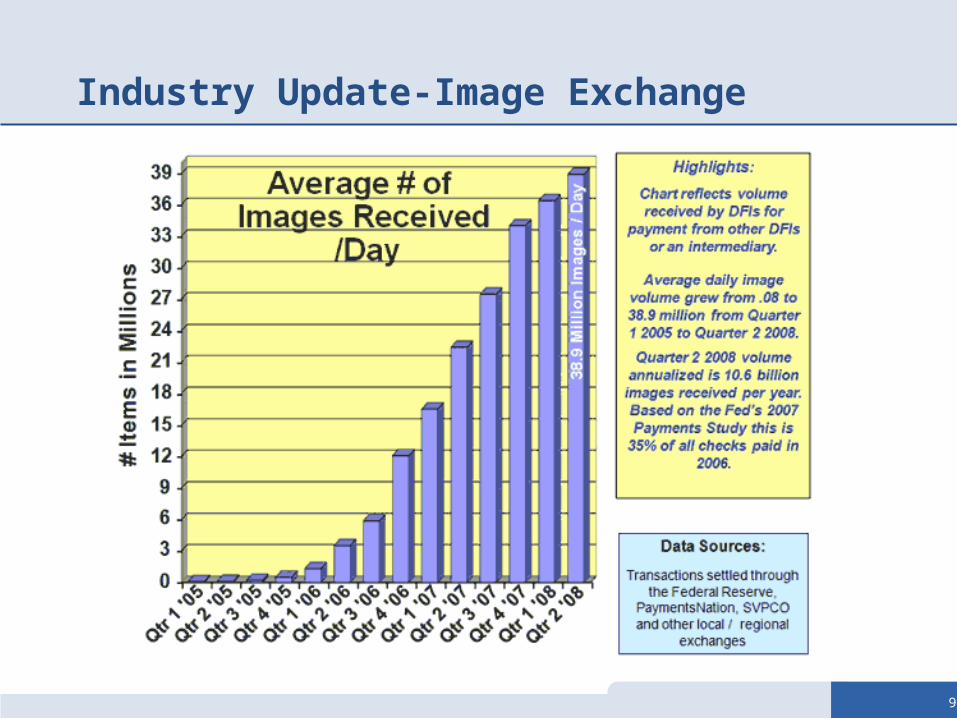

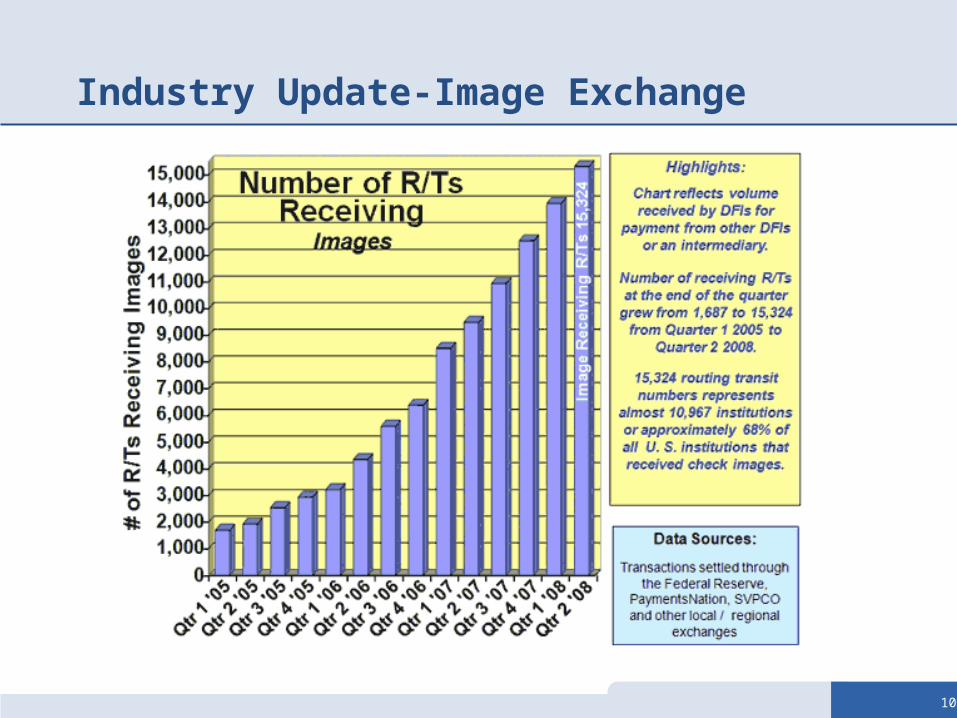

Paper checks are being transitioned to electronic images of checks at an unprecedented pace.

JPMorgan Chase’s Image exchange endpoints increased 118% in 2007.

We update our ICL availability quarterly.

IRD volume continues to erode.

Industry Update: Acceptance of Image Exchange

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

9

Industry Update-Image Exchange

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

10

Industry Update-Image Exchange

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

11

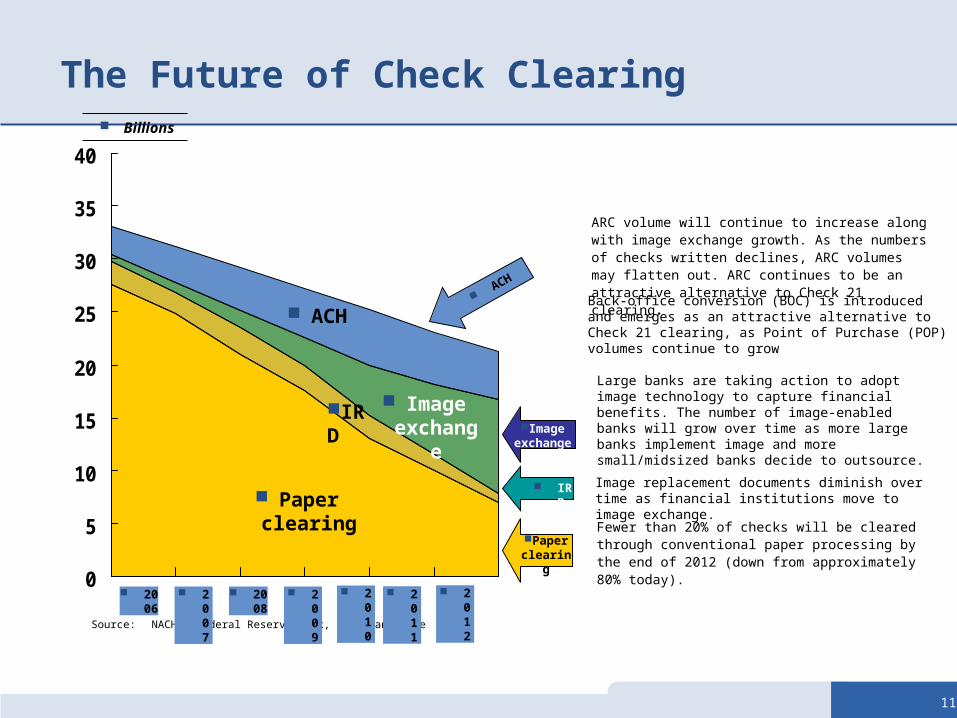

Source: NACHA, Federal Reserve Bank, JPMorgan Chase

0

5

10

15

20

25

30

35

40

Paper clearing

ACH

IRD

2006

2007

2008

2009

Billions

Large banks are taking action to adopt image technology to capture financial benefits. The number of image-enabled banks will grow over time as more large banks implement image and more small/midsized banks decide to outsource.

Image replacement documents diminish over time as financial institutions move to image exchange.

Fewer than 20% of checks will be cleared through conventional paper processing by the end of 2012 (down from approximately 80% today).

Image exchang

e

IRD

Paper clearing

Image exchan

ge

The Future of Check Clearing

2010

ACH

ARC volume will continue to increase along with image exchange growth. As the numbers of checks written declines, ARC volumes may flatten out. ARC continues to be an attractive alternative to Check 21 clearing.Back-office conversion (BOC) is introduced and emerges as an attractive alternative to Check 21 clearing, as Point of Purchase (POP) volumes continue to grow

2011

2012

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

12

Solutions for a Changing Landscape: Image Cash Letter with ACH

Solutions for a Changing Landscape: Image Cash Letter with ACH

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

13

Benefits of Image Cash Letter with ACH

Cost Savings and Efficiencies – Elimination of courier costs associated with transporting checks

to the bank. Elimination of risk associated with transporting original items

and consumer fraud Increasing emphasis is on Straight-through-processing (STP) Eliminate pass two in processing, no check encoding Eliminates the need for ARC decision engine, MICR verification

and ACH override/repair algorithms residing in house Substantially reduces file management Eliminates the need for your monitoring and managing

adjustments as the NACHA and Check 21 rules change Reduction of deposit preparation costs Supports a simplified disaster recovery process

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

14

Benefits of Image Cash Letter with ACH

Reduction in Bank Fees Exchange paper fees (that continue to increase as ICL erodes

the paper scale) for lower image fees Reduction in MICR reject and deposit adjustment fees Eliminate the need to maintain local deposit or check clearing

arrangements Aggregate your volumes for discount opportunities

Optimize Availability Image Cash Letter with ACH allows for later deposit deadlines,

providing an extended internal processing deadline Reduction/Elimination of holdover volumes Provides for weekend processing of ARC and check volumes

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

15

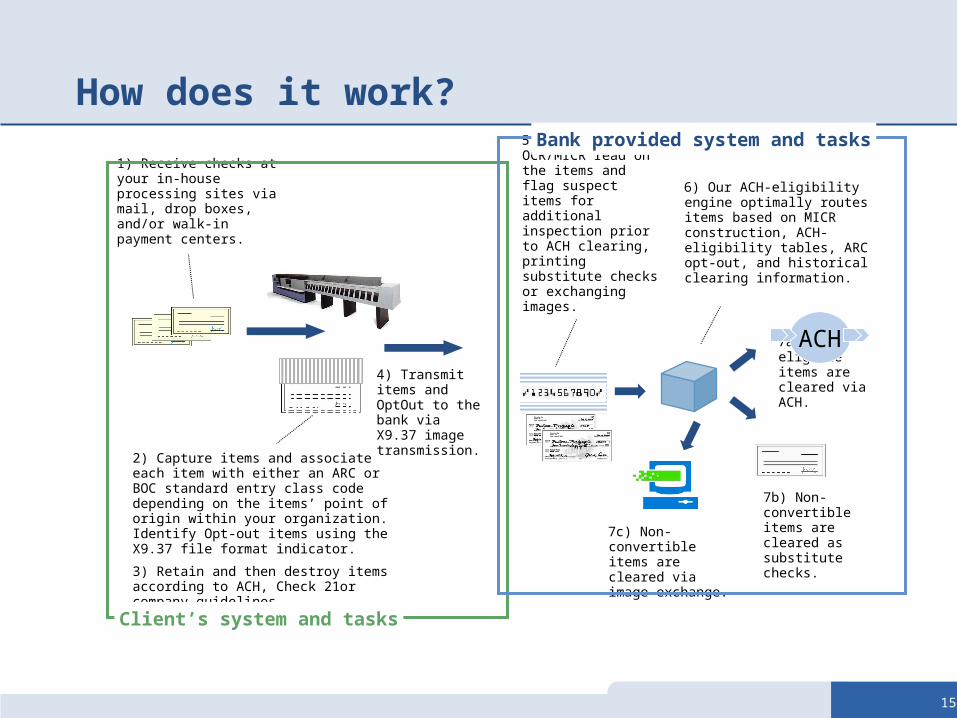

2) Capture items and associate each item with either an ARC or BOC standard entry class code depending on the items’ point of origin within your organization. Identify Opt-out items using the X9.37 file format indicator.

3) Retain and then destroy items according to ACH, Check 21or company guidelines.

7c) Non-convertible items are cleared via image exchange.

7b) Non-convertible items are cleared as substitute checks.

5) We perform OCR/MICR read on the items and flag suspect items for additional inspection prior to ACH clearing, printing substitute checks or exchanging images.

1) Receive checks at your in-house processing sites via mail, drop boxes, and/or walk-in payment centers.

6) Our ACH-eligibility engine optimally routes items based on MICR construction, ACH-eligibility tables, ARC opt-out, and historical clearing information.

4) Transmit items and OptOut to the bank via X9.37 image transmission.

7a) ARC eligible items are cleared via ACH.

How does it work?

Client’s system and tasks

Bank provided system and tasks

ACH

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

16

Image Cash Letter with ACH - Features

Reduce processing steps- eliminate need for pass two in processing

Reduce Programming- no in house decision process required Less Expensive – ACH clearing is more economical than traditional

check processes Lower return rates - Clients who have adopted ACH conversion

processes (Accounts Receivable Conversion) have experienced reductions in returned item rates by as much as 30 - 40% because electronic items are typically presented prior to paper items, and ACH rules allow an additional re-presentment of the item

Faster returns’ notification – ACH returns notifications are typically received within 2 business days’ from their submission, which can be faster than a similar check’s return timeframe

More electronic endpoints - ACH has over 14,000 electronic endpoints with the addition of over 13,000 Image Exchange points Check 21 the combined process reduces your cost for clearing items

Potentially reduced transportation costs – Conversion and clearing of your items electronically may allow you to reduce deposit-related transportation costs

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

17

Tarrant County Tax Office: Back Office Project

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

18

Tarrant County is an urban county located in the north central part of Texas.

Fort Worth serves as the county seat to a county population of approximately 1.7 million citizens.

The Tarrant County Tax Office assesses and collects 2.2 billion dollars, processes 1.4 million motor vehicle transactions, issues 4,000 liquor, beer and wine licenses and answers 2000 phone calls a day. The office has proven their commitment to providing the best in customer service through the use of best business practices and the latest technology.

Tarrant County Tax Office

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

19

o In July of 2001, Tarrant County initiated a Web Portal project called eGovernment. One of the advertised benefits of the new portal was the ability to pay taxes over the internet.

o eGovernment initiative was broadened to include other initiatives that improved the tax collection process by electronifying the payment process.

o Tarrant County Tax Assessor’s office was among the first to implement ARC.

o eGov has delivered tremendous results, allowing the municipality to electronically process over 35,000 property tax payments and 100,000 motor vehicle renewals during the past fiscal year. Credit card and eCheck payments for property tax made over the Web grew by 20 and 30 percent respectively last year.

o Implemented ACH Debit for auto dealershipso In 2007, the Tax Office launched the Back Office Project

and updated the Rapid Payment System (RPS) with new hardware and software to process payment for property and other taxes and fees.

Tarrant County eGovernment

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

20

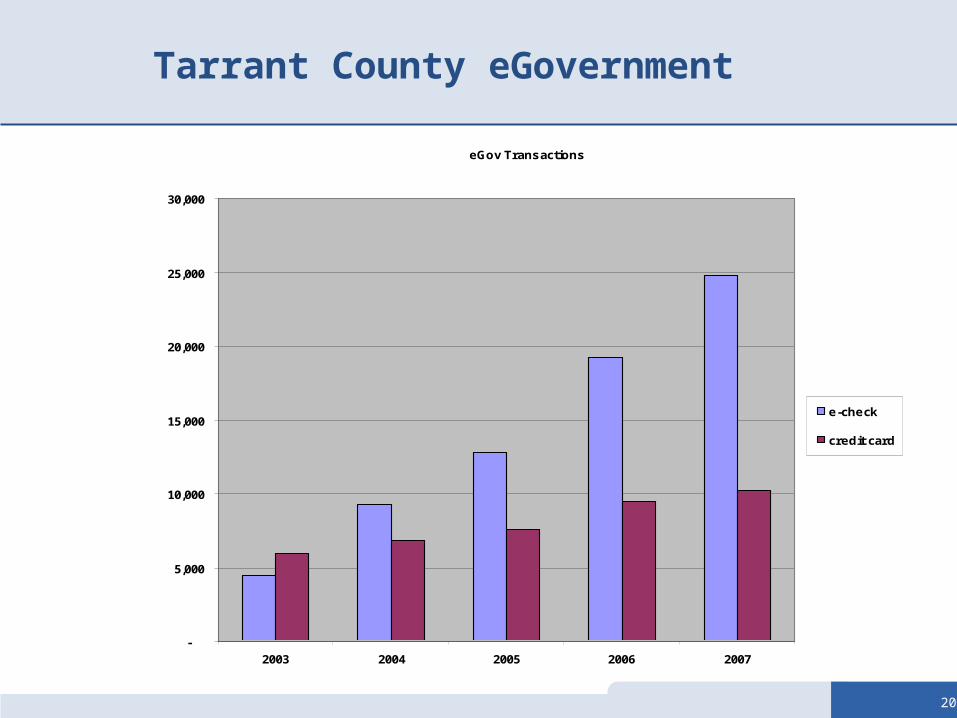

eGov Transactions

-

5,000

10,000

15,000

20,000

25,000

30,000

2003 2004 2005 2006 2007

e-check

credit card

Tarrant County eGovernment

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

21

The updated platform was designed to take advantage JPMorgan Chase’s ICL with ACH product’s ability to take one file for all check transactions.

Creating one file of all check transactions for transmission to the bank was new for everyone.

Successful implementation required close coordination with several parties including:

Multiple hardware and software vendors.

Internal IT and operational groups.

JPMorgan Chase.

Started with pilot to prove process and minimize surprises.

Full roll out was inclusive of property and motor vehicle taxes as well as beer and wine licensing fees

Implementing the changes

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

22

Financial Benefits

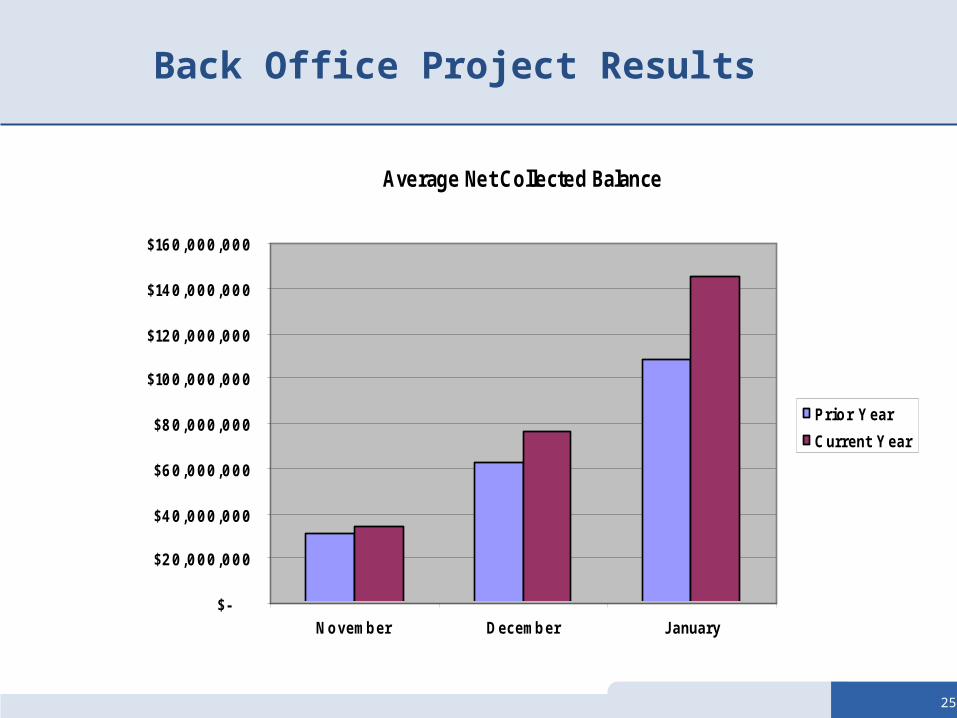

8% increase in collected and paid entities over historical averages.

Collected funds balance increase by an average of $37 million per day.

Reduced bank fees for clearing transactions.

Improved funds availability and earnings credit

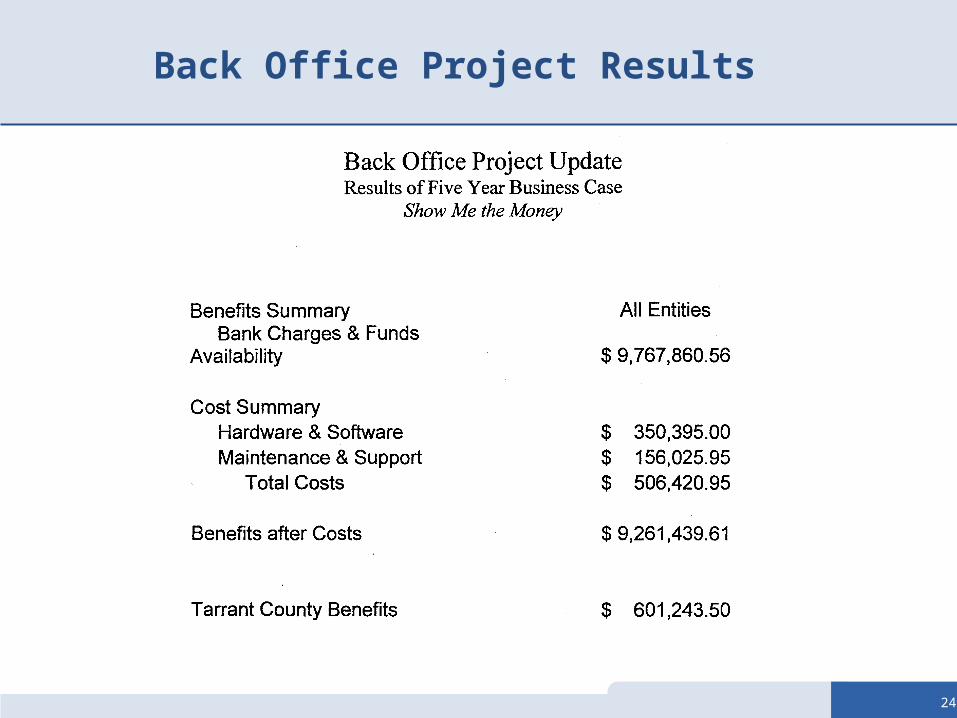

Five year net benefit to Tarrant County is $600,000

Five year net benefit to all entities is over $9mm

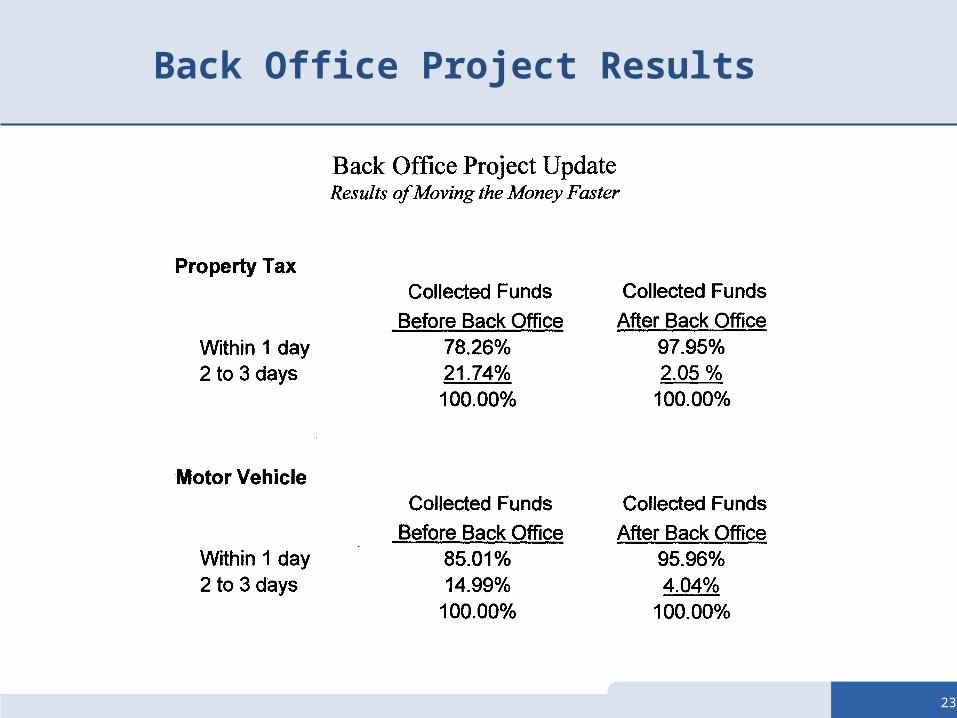

Back Office Project Results

Virtually 100% of 1 million checks are now sent to the bank electronically including property tax, motor vehicle tax, vehicle inventory tax, beer wine and liquor fees from 8 county locations

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

23

Back Office Project Results

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

24

Back Office Project Results

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

25

Average Net Collected Balance

$-

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

$160,000,000

November December J anuary

Prior Year

Current Year

Back Office Project Results

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

26

Project Results

Operational Benefits

Fewer payments processed manually.

Less overtime required during seasonal peak periods.

Databases are updated from electronic data obtained from checks & coupons.

Better control of checks returned from the bank.

No waiting on collected funds balances to pay entities.

Significant process change resulting in faster opening of mailed payments, as well as quicker posting and routing through banking systems.

Not dependent on armored car pick-up schedule

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

27

Future Projects

Back Office Project Phase 2. Image and archive correspondence that accompanies

mailed tax payments. Install new general ledger system that will allow for

real-time posting of tax payments.

Other Initiatives. Credit Card acceptance at point of sale for all Tax Office

Payments at all locations.

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

28

Questions?

© 2008 JPMorgan Chase & Co. All rights reserved.

JPMorgan Chase is licensed under U.S. Patent Numbers 5,910,988 and 6,032,137.

This document contains information that is the property of JPMorgan Chase & Co. It may not be copied, published, or used in whole or in part for any purpose other than as expressly authorized by JPMorgan Chase & Co.

This presentation contains projections and certain of the statements and data contained in this presentation are, by their nature, forward-looking. Past performance is not a guarantee of future results and the actual results for your organization may differ materially. Additionally, this presentation contains projections, statements and data provided by third parties, including the Federal Reserve. JPMorgan Chase does not warrant or guarantee the accuracy or completeness of such projections, statements or data. If you have any questions, please contact your customer representative.

STRICTLY PRIVATE AND CONFIDENTIAL © 2005 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC

29

Contacts

Jim Nave

Executive Director

J. P Morgan

Oil & Gas/Power

John MacCallum

Vice President

J.P. Morgan

Product Solution Specialist

Recommended