Status Of Federal Student Loans

Presented by: Trisha Malloy, Outreach Representative, FAME

October 10, 2008

• Basic educational loan information• New loan limits• Changes to the PLUS loan • Current & expected changes to

federal loan availability

Agenda

Types of Federal Loans

• Federal Perkins Loan• Federal Stafford Loan

– Direct or FFELP– Subsidized & Unsubsidized

• Federal PLUS Loans– Direct or FFELP– Parent PLUS & Grad PLUS

Federal Perkins Loan

• Federally regulated• Student is the borrower & must be

enrolled at least half-time• Money comes from the federal

government and previously repaid Perkins loans at the school

• Only some schools have Perkins Loan Funds to offer to students

Federal Perkins Loan

• Must complete the FAFSA and meet eligibility guidelines

• Borrowers must complete a Master Promissory Note (MPN) - good for 10 years

• Disclosure form must be completed each year of borrowing

• Student will repay the loan to the school from which it was borrowed

Federal Perkins Loans

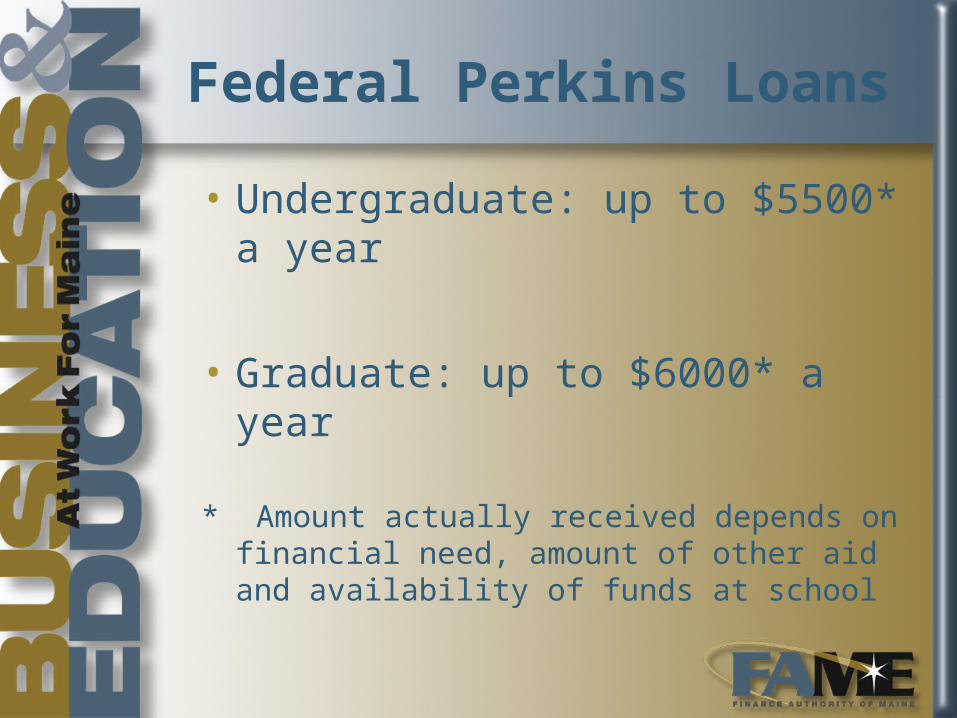

• Undergraduate: up to $5500* a year

• Graduate: up to $6000* a year

* Amount actually received depends on financial need, amount of other aid and availability of funds at school

Federal Perkins Loan

• Fees & Repayment– 5% Fixed Interest Rate– No fees– No interest accrues while in school– Up to 10 year repayment period depending

on amount owed– Exit Interview must be completed once

student is no longer enrolled at least half-time

– Numerous deferment & cancellation provisions exist

Federal Stafford Loan – Direct or FFELP

• Many schools choose to participate in either Direct Loan Program or FFEL Program.– Direct Loans funded by the federal

government – student repays the feds– FFEL Loans funded by banks and private

lending institutions – student repays the lending institution

• Some schools choose to offer both programs to students.– Become more common over the past year

with changes in lender programs.

Federal Stafford Loan

• Federally regulated• Student is the borrower• Student must be enrolled at least

half-time• Student must complete the FAFSA

form each year• Direct and FFEL Stafford Loans

have same regulations and different funding source

Federal Stafford Loan – Direct or FFELP

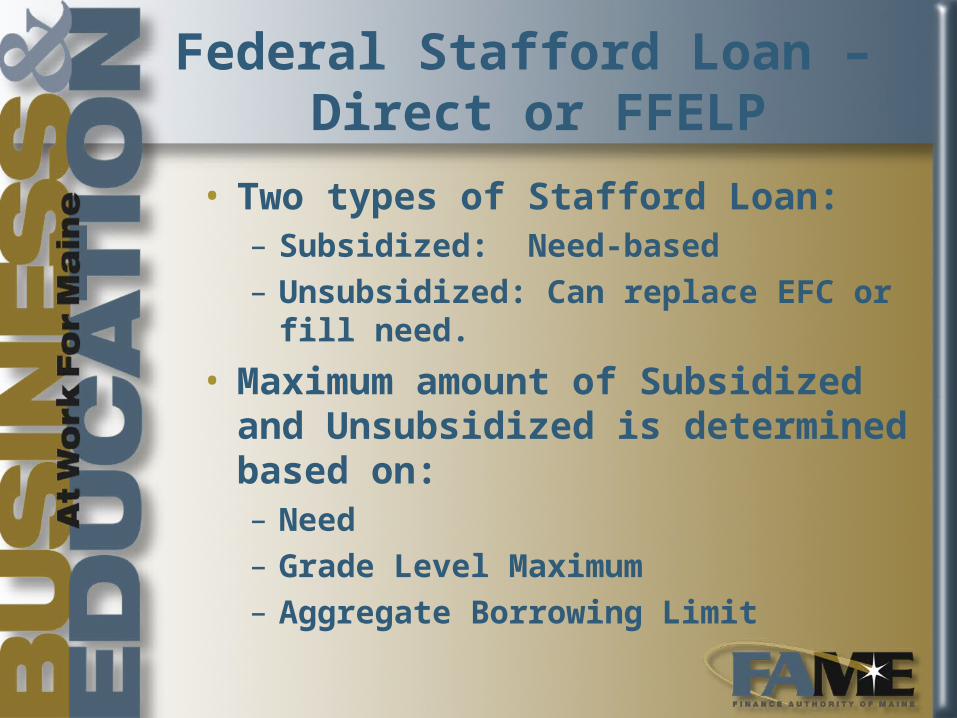

• Two types of Stafford Loan:– Subsidized: Need-based – Unsubsidized: Can replace EFC or fill

need.

• Maximum amount of Subsidized and Unsubsidized is determined based on:– Need– Grade Level Maximum– Aggregate Borrowing Limit

Federal Stafford Loan – Loan Limit Increases

Effective 7/1/08• 1st Year - $5500 (no more than $3500

subsidized)

• 2nd Year - $6500 (no more than $4500 subsidized)

• 3rd, 4th 5th Year – $7500 (no more than $5500 subsidized)

• Dependent students whose parents are denied a PLUS loan and independent students still qualify for the additional $4,000 or $5,000 unsubsidized Stafford loan based on grade level.

Federal Stafford Loan – Aggregate Loan Limits

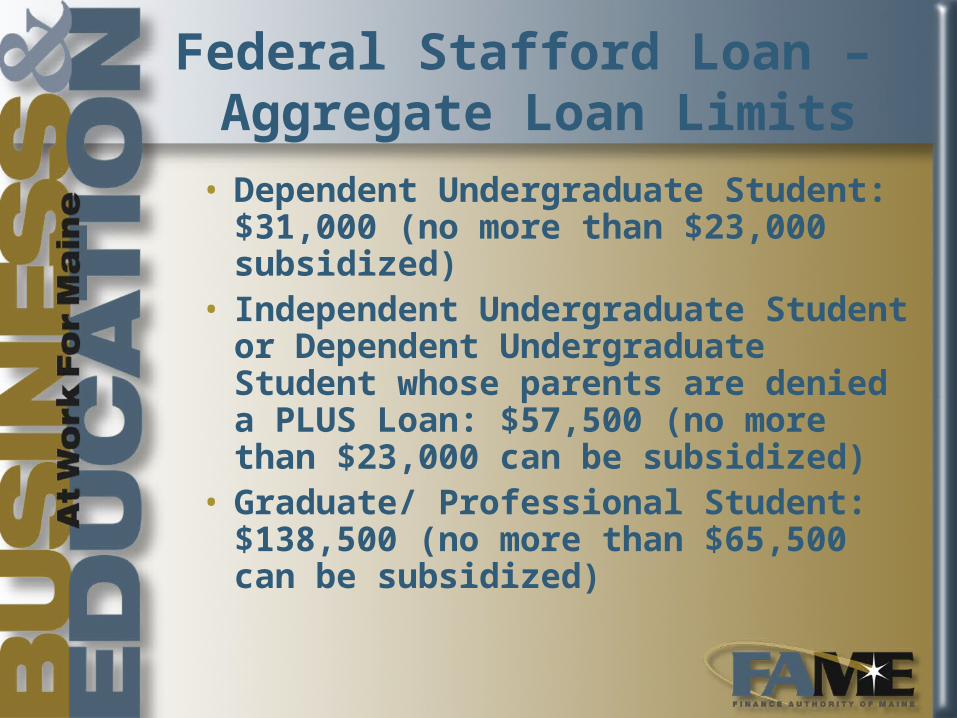

• Dependent Undergraduate Student: $31,000 (no more than $23,000 subsidized)

• Independent Undergraduate Student or Dependent Undergraduate Student whose parents are denied a PLUS Loan: $57,500 (no more than $23,000 can be subsidized)

• Graduate/ Professional Student: $138,500 (no more than $65,500 can be subsidized)

Stafford Loan Interest Rates

• Loans first disbursed between: – 7/1/08 - 6/30/09 = 6% – 7/1/09 - 6/30/10 = 5.6% – 7/1/10 - 6/30/11 = 4.5% – 7/1/11 - 6/30/12 = 3.4% – 7/1/12 and after = 6.8%

• Unsubsidized remains at 6.8% fixedRate Reductions apply to Undergraduate

Subsidized Stafford Loans only.

Stafford Loan Fees

• Up to 1% origination fee deducted proportionately from each disbursement

• 1% default fee • The origination fee will drop by .5%

each July until it is phased out completely

Stafford Loan Repayment

• Student has between 10 and 25 years (up to 30 yrs. for direct loans) to repay, depending on the amount owed and the type of repayment plan selected

• Numerous deferment provisions as well as some cancellation provisions exist

Stafford Loan Application

• Student must complete the FAFSA• Check with each individual school to

determine Stafford Loan application process• Student signs Master Promissory Note the first

time they borrow and it is good for 10 years• Entrance Interview is required the first time the

student borrows Stafford Loan prior to receiving funds

• Exit Interview must be completed when the student is no longer enrolled at least half-time

PLUS Loan ProgramDirect or FFELP

• Schools may choose to participate in either Direct Loan Program or FFEL Program.– Direct Loans funded by the federal

government – student repays the feds– FFEL Loans funded by banks and private

lending institutions – student repays the lending institution

• Some schools choose to offer both programs to students.– Many schools historically offered FFEL

PLUS loans even if they offered only Direct Loan Program Stafford Loans

Federal PLUS Loan Program

• There are 2 PLUS Loan Programs:– Parent PLUS Loans allow parents of

dependent undergraduate students to borrow to pay for educational expenses.

– Grad PLUS Loans allow graduate students to borrow to pay for educational expenses that are not covered by Stafford Loan or other financial aid.

PLUS Loan Program Changes

Effective 7/1/2008:• Lenders are allowed to consider parents

eligible for PLUS loans, even if parent has adverse credit during the period 1/1/07 to 12/31/09 if the adverse credit was a result of being delinquent on mortgage payments.

• PLUS Loan grace period now allows parents to defer payments on a parent PLUS loan until six months after the student ceases to be enrolled at least ½ time– Accrued interest can be paid or capitalize

quarterly

PLUS Loan Program

• Standard repayment – 10 years– Minimum $50 per month

• Interest accrues during periods of deferment

• Interest payments can be made during periods of deferment

• Interest may be capitalized no more frequently than quarterly

Current and Expected Changes to Federal Loan Availability

• 2008-09 Some students experienced delays in loan process and funding

• FAME continues to provide information and assistance to schools and students facing federal loan issues

• Extension of ECASLA (Ensuring Continued Access to Student Loans ACT) to include 2009/2010 Academic Year Loans will help the continuation of FFELP Loan Programs

Current and Expected Changes to Federal Loan Availability

• Some lenders have exited student loan market

• Some lenders have suspended student loan origination

• Many lenders have eliminated borrower benefit programs or significantly reduced these benefits

• Still many student lenders in the marketplace

• Many lenders are expecting to grow

Recommended