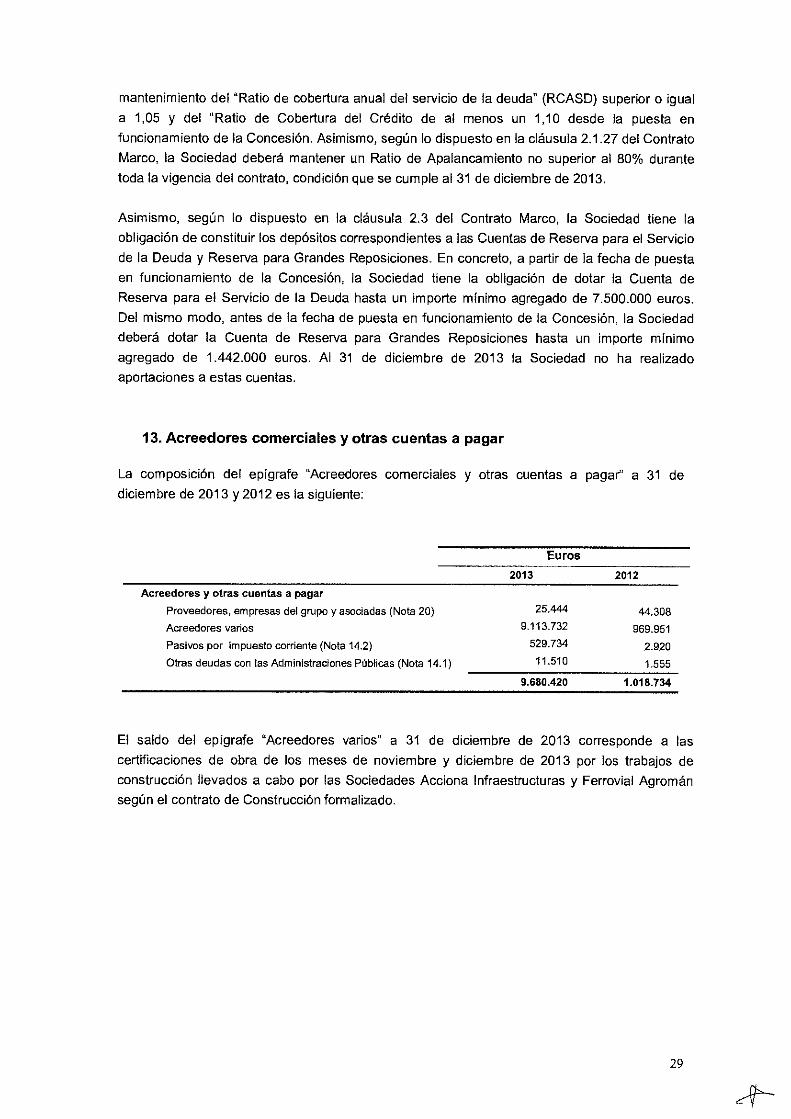

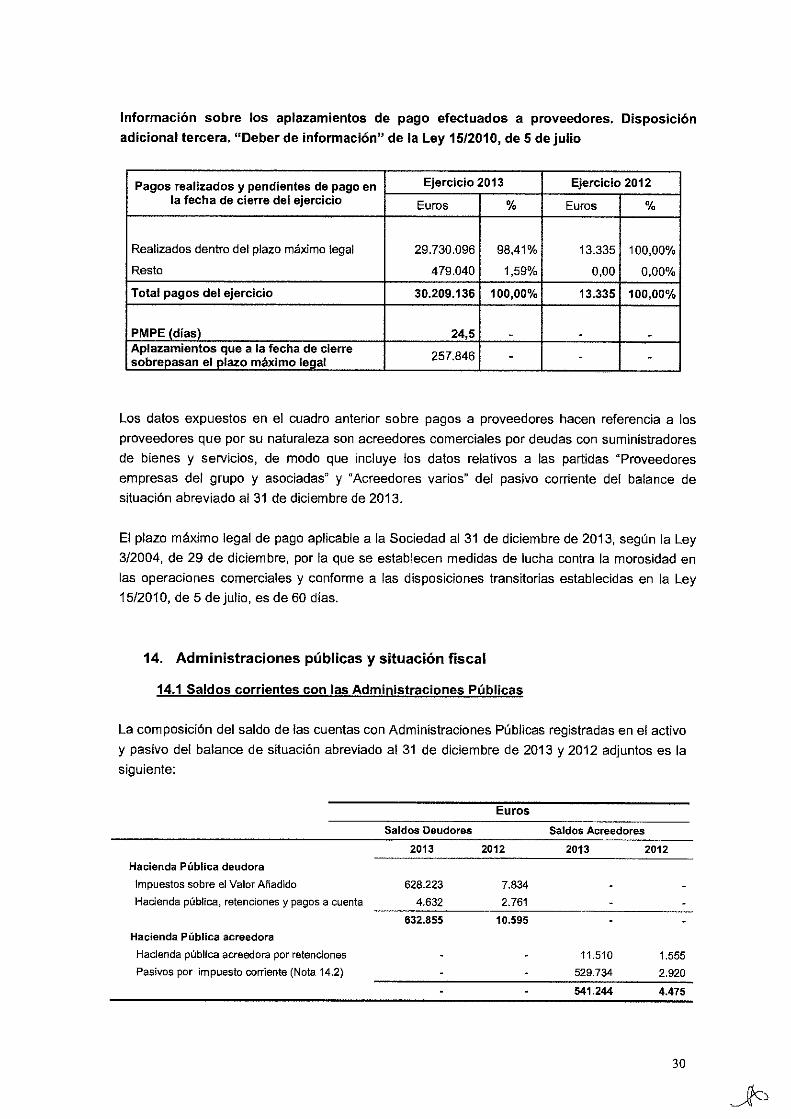

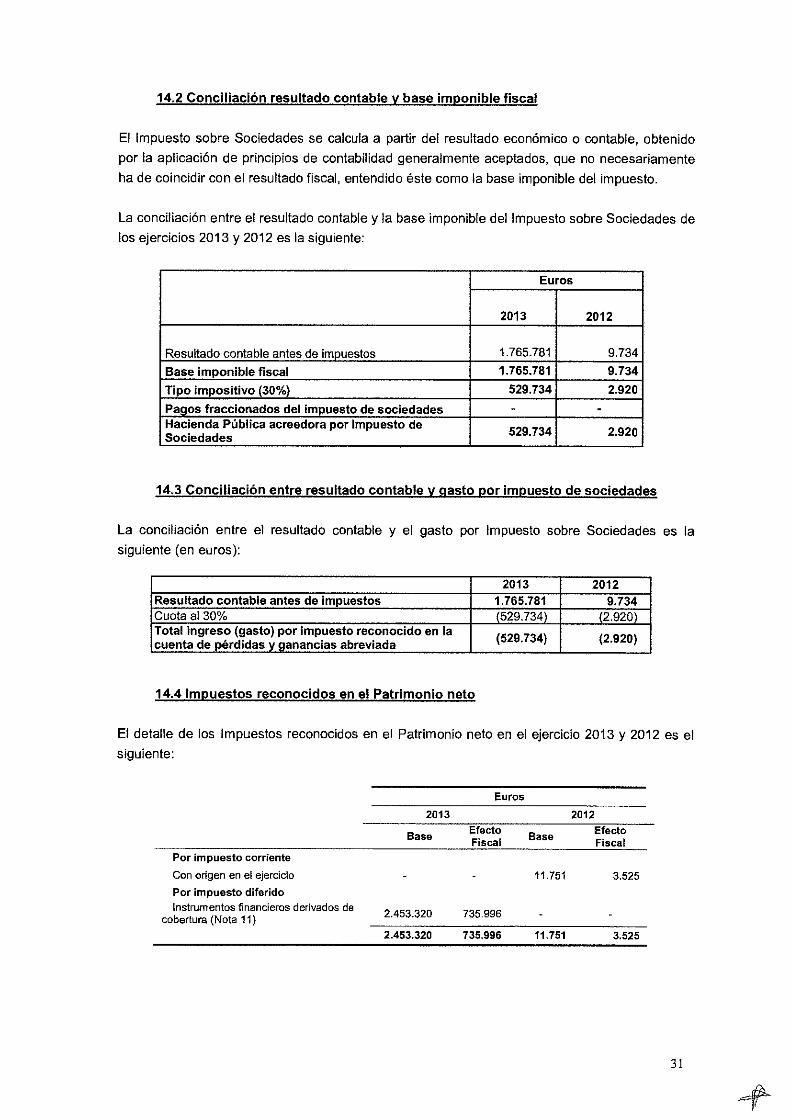

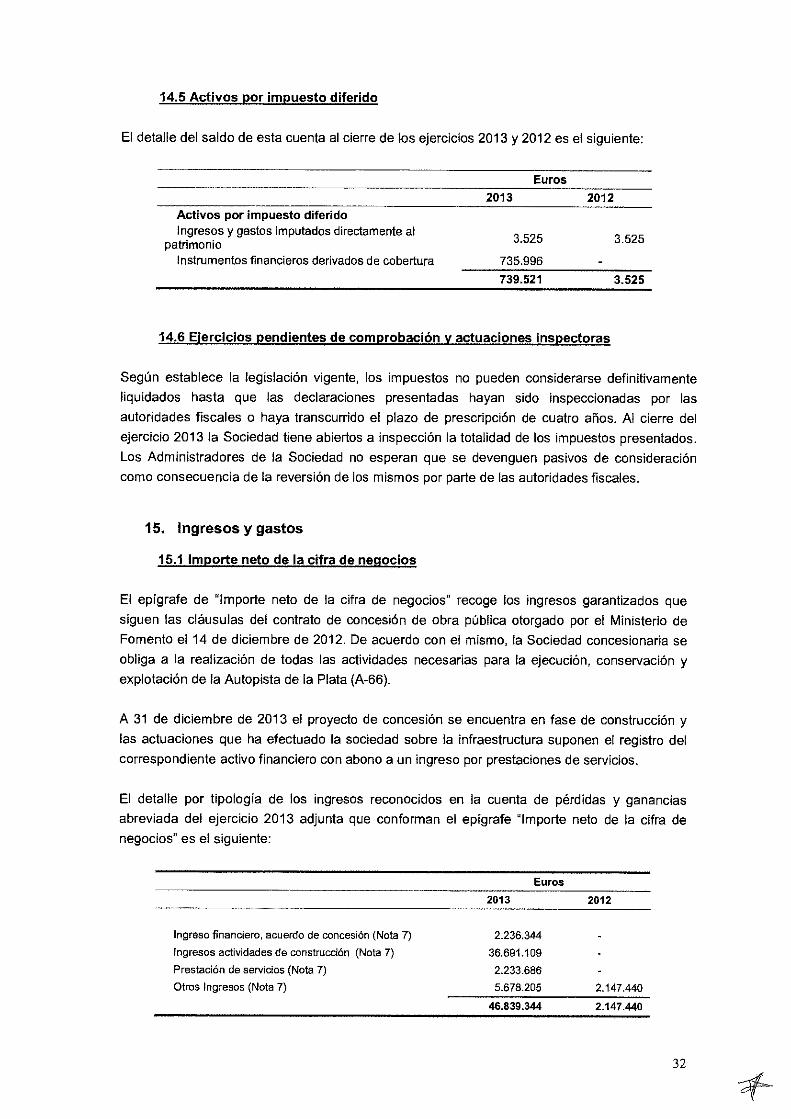

OFFERING CIRCULAR

Sociedad Concesionaria Autovía de la Plata, S.A.

(incorporated in Spain with limited liability)

€184,500,000

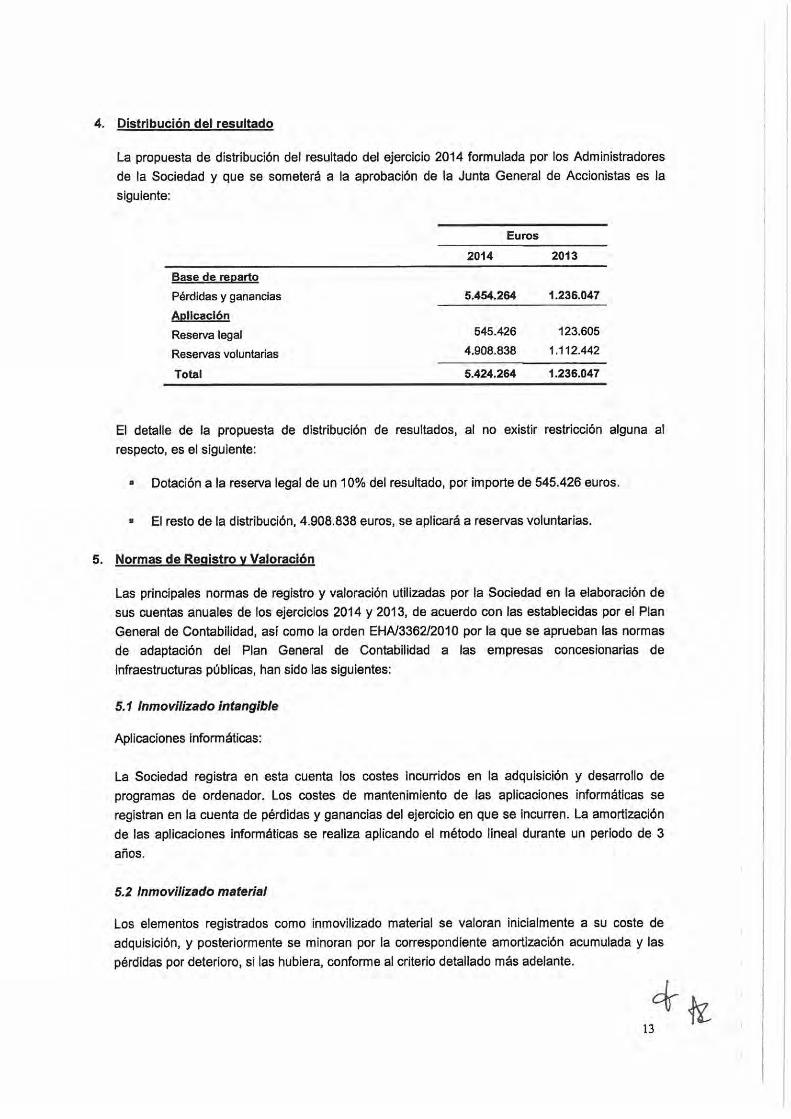

3.169 per cent. Bonds due 31 December 2041

Issue Price 100 per cent.

OFFERING CIRCULAR (DOCUMENTO INFORMATIVO DE INCORPORACIÓN) ON THE EVENTUAL

ADMISSION (INCORPORACIÓN) OF SECURITIES ON THE SPANISH ALTERNATIVE FIXED-INCOME

MARKET (MARF)

The €184,500,000. 3.169 per cent. Bonds due 31 December 2041 (the Bonds) have been issued by Sociedad Concesionaria

Autovía de la Plata, S.A. (the SPV, the Issuer or the Company), a corporation (Sociedad Anónima) organised under the

laws of Spain, registered in the Madrid Companies Register in volume 30,409, sheet 177, section 8ª, page M-547341, with

tax identification number A-86591278.

The Bonds are constituted by a trust deed (the Trust Deed) dated the Closing Date (as defined below) between the Issuer

and BNP Paribas Trust Corporation UK Limited as bond trustee (in this capacity, the Bond Trustee).

This offering circular (the Offering Circular) constitutes a Documento Informativo de Incorporación for the purposes of

admission (incorporación) of the Bonds to the Multilateral Trading System known as Alternative Fixed Income

Market (Mercado Alternativo de Renta Fija or MARF). MARF adopts the legal structure of a multilateral trading

facility (MTF), under the terms provided for in Articles 118 et seq. of the Law 24/1988 on Securities Market (LMV),

constituting an alternative, unofficial and not regulated market for the trading of fixed-income securities in accordance with

the provisions of Directive 2004/39/EC.

The Issuer will request the admission (incorporación) of the Bonds to trading on MARF within 30 days following the

Closing Date (as defined below). The denomination of the Bonds shall be €100,000.

Interest on the Bonds accrues from (and including) 27 May 2015 (the Closing Date). Interest on the Bonds is payable semi-

annually in arrear on 30 June and 31 December in each year, commencing on 30 June 2015. Payments on the Bonds will be

made without deduction for or on account of taxes in Spain to the extent described under and subject to the customary

exceptions described in "Terms and Conditions of the Bonds — Taxation".

The Bonds mature on 31 December 2041 but may be redeemed before then at the option of the Issuer in whole at any time at

their principal amount together with accrued interest and a make whole premium. The Bonds are also subject to redemption

in whole or in part, at their principal amount, together with accrued interest, at the option of the Issuer at any time in the

event of certain changes affecting taxation in Spain. In addition, if the Concession Agreement (as defined below) is

terminated, then the Issuer shall, upon receipt of the relevant Compensation (as defined below), immediately pay such

Compensation into the General Account (as defined below) and in the manner described herein redeem the Bonds in whole

at their principal amount, together with accrued but unpaid interest to such date, and, in certain circumstances, a make whole

premium. See "Terms and Conditions of the Bonds – Redemption and Purchase" for details of these and other circumstances

in which the Bonds may be redeemed early. The Bonds contain certain obligations for the Issuer, as detailed in Condition 5

(General Covenants) of the Bonds.

1

The Bonds constitute senior obligations of the Issuer, to be secured as provided for in Condition 3 (Security). The Security

will be held in accordance with the terms of a security trust and subordination deed (the Security Trust and Subordination

Deed) dated the Closing Date between, inter alios, the Issuer and BNP Paribas Trust Corporation UK Limited as security

agent (in this capacity, the Security Agent). See also "Terms and Conditions of the Bonds – Security".

The Bonds are represented by book entries in Iberclear. See "Summary of Clearance and Settlement Procedures applicable

to Book-Entry Notes".

The Bonds are expected to be rated BBB by Standard & Poor's Rating Services (S&P) on or about the Closing Date. A

rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, reduction or withdrawal at

any time by the assigning rating agency. S&P is established in the EU and registered under Regulation (EC) No 1060/2009

(the CRA Regulation).

Prospective investors should have regard to the factors described under the section of this Offering Circular headed "Risk

Factors" on page 16 of this Offering Circular.

This Offering Circular (Documento Informativo de Incorporación) is not a prospectus (folleto informativo) within the

meaning of Directive 2004/39/EC and has not been registered with the National Securities Market Commission (CNMV).

The offering of the Bonds does not constitute a public offering in accordance with the provisions of Article 30bis of the

LMV and therefore there is no obligation to approve, register and publish a prospectus (folleto informativo) with the CNMV.

As established by rule 2 of Circular 3/2014 of MARF, dated 29 October, this issuance of Bonds is intended exclusively for

professional and qualified investors in accordance with the provisions of Article 78bis 2 of the LMV and Article 39 of Royal

Decree 1310/2005 of 4 November, with regard to the admission of securities to trading on official secondary markets, public

offerings or subscription and the prospectus required for this purpose (Royal Decree 1310/2005).

No action has been taken in any jurisdiction to permit a public offering of the Bonds or the possession or distribution of the

Offering Circular or any other offering material in any country or jurisdiction where such action is required for said purpose.

SOLE ARRANGER AND GLOBAL COORDINATOR

HSBC BANK plc

JOINT BOOKRUNNERS

HSBC BANK plc

BANCO BILBAO VIZCAYA ARGENTARIA, S.A. BANCO SANTANDER, S.A.

The date of this Offering Circular is 27 May 2015

2

IMPORTANT NOTICES

This Offering Circular in relation to the Bonds includes the required information as established in Annex 1-B of

Circular 3/2014 of MARF, dated 29 October, on admission and exclusion of securities on MARF and the

procedures with respect to the same.

None of the Issuer nor HSBC Bank plc, Banco Bilbao Vizcaya Argentaria, S.A. and Banco Santander, S.A. (the

Joint Bookrunners), the Bond Trustee nor the Security Agent has authorised anyone to provide information to

potential investors different from the information contained in this Offering Circular and other publicly

available information. Potential investors should not base their investment decision on information other than

that contained in this Offering Circular and alternative sources of public information. Any information or

representation not contained in this Offering Circular must not be relied upon as having been authorised by or

on behalf of the Issuer, the Joint Bookrunners, the Bond Trustee or the Security Agent.

Neither the delivery of this Offering Circular nor any sale made in connection herewith shall, under any

circumstances, create any implication that there has been no change in the affairs of the Issuer since the date

hereof or the date upon which this Offering Circular has been most recently amended or supplemented or that

there has been no adverse change in the financial position of the Issuer since the date hereof or the date upon

which this Offering Circular has been most recently amended or supplemented, or that the information

contained in it or any other information supplied in connection with the Bonds is correct as of any time

subsequent to the date on which it is supplied or, if different, the date indicated in the document containing the

same.

To the fullest extent permitted by law, none of the Joint Bookrunners, the Bond Trustee nor the Security Agent

assumes any liability for the contents of the Offering Circular or for any other statement made or purported to be

made by the Joint Bookrunners, the Bond Trustee or the Security Agent or on their behalf in connection with the

Issuer or the issue and offering of the Bonds. The Joint Bookrunners, the Bond Trustee and the Security Agent

accordingly disclaim all and any liability whether arising in tort or contract or otherwise (save as referred to

above) which it might otherwise have in respect of this Offering Circular or any such statement.

None of the governing body of MARF, the CNMV, the Joint Bookrunners, the Bond Trustee nor the Security

Agent has approved or verified the contents of the Offering Circular, the financial statements of the Issuer, the

rating report or the risk of the issuance required under Circular 3/2014. The governing body of MARF does not

acknowledge or confirm the completeness, understanding or consistency of the information included in the

documentation provided to them by the Issuer in relation to the issuance of the Bonds.

The Bonds are represented by book entries in Iberclear (as defined below). The Issuer expressly declares that it

has met the requirements for registration and settlement of the transaction in Iberclear. See "Summary of

Clearance and Settlement Procedures applicable to Book-Entry Notes".

The Issuer accepts responsibility for the information contained in this Offering Circular. To the best of the

knowledge and belief of the Issuer (which has taken all reasonable care to ensure that such is the case), the

information contained in this Offering Circular is in accordance with the facts and does not omit anything likely

to affect the import of such information.

The Issuer expressly declares that it is aware and knows the requirements and conditions necessary for

admission of the Bonds on MARF under current legislation and the requirements of its governing bodies and

expressly agrees to comply therewith.

This Offering Circular does not constitute an offer of, or an invitation by or on behalf of the Issuer or the Joint

Bookrunners to subscribe or purchase, any of the Bonds. The distribution of this Offering Circular and the

offering of the Bonds in certain jurisdictions may be restricted by law. Persons into whose possession this

Offering Circular comes are required by the Issuer and the Joint Bookrunners to inform themselves about and to

observe any such restrictions.

3

It is recommended that potential investors fully and carefully read the Offering Circular prior to any investment

decision. Potential investors should, in addition, have regard to each original document described, or referred to,

in this Offering Circular. All descriptions of documents referred to in this Offering Circular are qualified in their

entirety by reference to the terms of the original documents.

For a description of further restrictions on offers and sales of Bonds and distribution of this Offering Circular,

see the section of this Offering Circular headed "Sale of the Bonds".

The Bonds have not been and will not be registered under the U.S. Securities Act of 1933 (the Securities Act).

Subject to certain exceptions, Bonds may not be offered or sold within the United States or to U.S. persons.

Unless otherwise specified or the context requires, all references herein to euro or € are to the single currency

introduced at the start of the third stage of European Economic and Monetary Union pursuant to the Treaty on

the functioning of the European Union, as amended from time to time.

REGULATION OF INVESTMENTS IN SECURITISATIONS

The Issuer is of the opinion that the requirements of Articles 404-410 of the Capital Requirements Regulation

(Regulation (EU) No. 575/2013) and corresponding requirements adopted pursuant to Article 17 of the EU

Alternative Investment Fund Managers Directive (Directive 2011/61/EU) and Article 135(2) of the EU

Solvency II Directive (Directive 2009/138/EC, as amended by Directive 2014/51/EU) do not apply to the

Bonds. Investors in the Bonds are responsible for analysing their own regulatory position and none of the Issuer,

the Joint Bookrunners or any of the parties to the transaction of which the Bonds form part makes any

representation to any prospective investor or purchaser of the Bonds regarding the regulatory capital treatment

of their investment in the Bonds on the Closing Date or at any time in the future.

Articles 404-410 of the Capital Requirements Regulation, corresponding requirements under other regulations

and directives and any other changes to the regulation or regulatory treatment of the Bonds for some or all

investors may negatively impact the regulatory position of individual investors and, in addition, have a negative

impact on the price and liquidity of the Bonds in the secondary market.

FORWARD-LOOKING STATEMENTS

This Offering Circular contains various forward-looking statements regarding events and trends that are subject

to risks and uncertainties that could cause the actual results, performance or achievements of the Issuer to differ

materially from the information presented herein. Such forward-looking statements are based on numerous

assumptions regarding the Issuer's present and future business strategies and the environment in which the

Issuer will operate in the future.

When used in this Offering Circular, the words "estimate", "project", "intend", "anticipate", "believe", "expect",

"should", "plan", "targets", "aims", "will", "would", "may", "could", "continue" and similar expressions, as they

relate to the Issuer, its management and the Project, are intended to identify such forward-looking statements.

All statements other than statements of historical fact included in this Offering Circular, including, without

limitation, those statements regarding the Issuer's financial position, business strategy, management plans and

objectives for future operations, are forward-looking statements. These forward-looking statements involve

known and unknown risks, uncertainties and other factors, which may cause the Issuer's actual results,

performance or achievements, or industry results, to be materially different from any future results, performance

or achievements expressed or implied by these forward-looking statements. Readers are cautioned not to place

undue reliance on these forward-looking statements, which speak only as at the date hereof. Save as otherwise

required by any rules or regulations, the Issuer does not undertake any obligations publicly to release the result

of any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to

reflect the occurrence of unanticipated events.

Additional factors that could cause actual results, performance or achievements to differ materially include, but

are not limited to, those discussed under the section of this Offering Circular headed "Risk Factors". Any

4

forward-looking statements contained in this Offering Circular speak only as at the date of this Offering

Circular.

Without prejudice to any requirements under applicable laws and regulations, the Issuer expressly disclaims any

obligation or undertaking to disseminate after the date of this Offering Circular any updates or revisions to any

forward-looking statements contained herein to reflect any change in expectations thereof or any change in

events, conditions or circumstances on which any such forward-looking statement is based.

Save as required by any applicable rules or regulations, the Issuer is not under any obligation to update any

forward-looking information set forth in this Offering Circular and does not intend to do so.

5

Table of Contents

Page

TRANSACTION OVERVIEW ............................................................................................................................. 6

RISK FACTORS...................................................................................................................................................15

DESCRIPTION OF THE ISSUER .......................................................................................................................31

DESCRIPTION OF THE REGULATORY REGIME ..........................................................................................36

DESCRIPTION OF THE PROJECT ....................................................................................................................43

DESCRIPTION OF THE CONCESSION AGREEMENT AND THE CONSTRUCTION CONTRACT ..........48

SELECTED HISTORICAL FINANCIAL INFORMATION ...............................................................................57

SUMMARY OF THE FINANCE DOCUMENTS................................................................................................59

TERMS AND CONDITIONS OF THE BONDS .................................................................................................61

SALE OF THE BONDS......................................................................................................................................120

USE OF PROCEEDS..........................................................................................................................................122

FUNCTIONS OF THE REGISTERED ADVISER (ASESOR REGISTRADO) OF MARF ...............................123

SUMMARY OF CLEARANCE AND SETTLEMENT PROCEDURES APPLICABLE TO BOOK-ENTRY NOTES................................................................................................................................................................125

TAXATION ........................................................................................................................................................128

GENERAL INFORMATION .............................................................................................................................136

SIGNATURES....................................................................................................................................................138

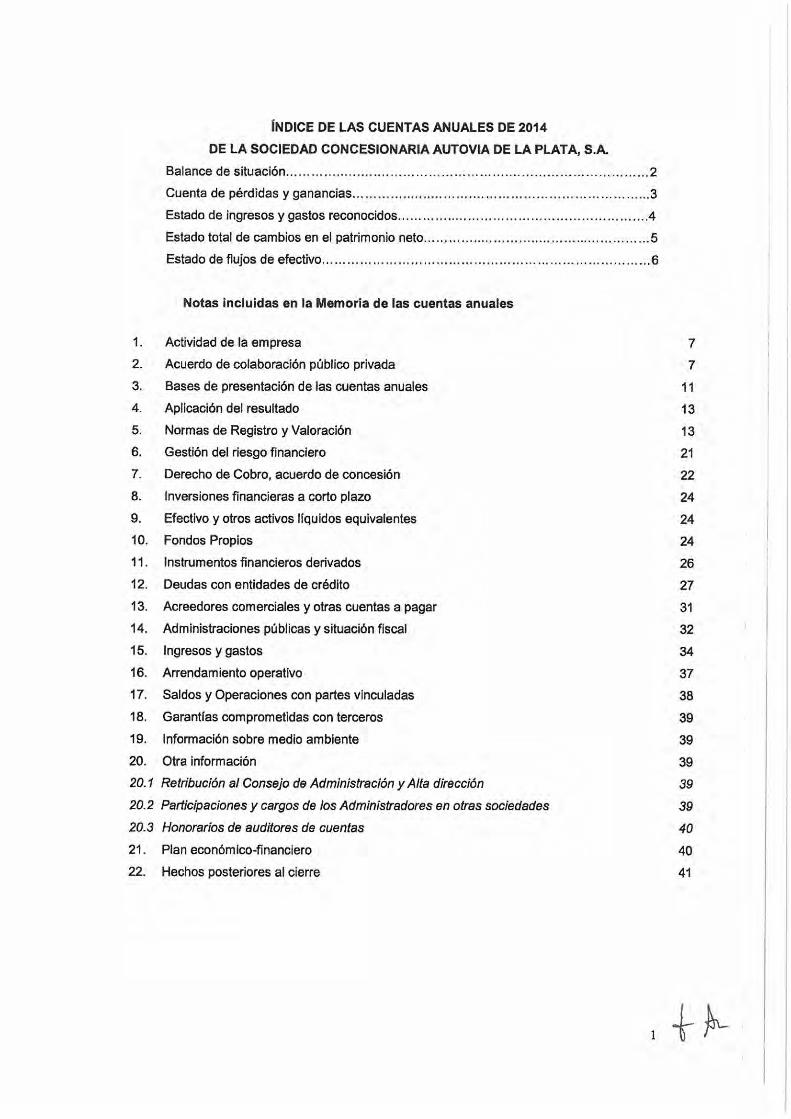

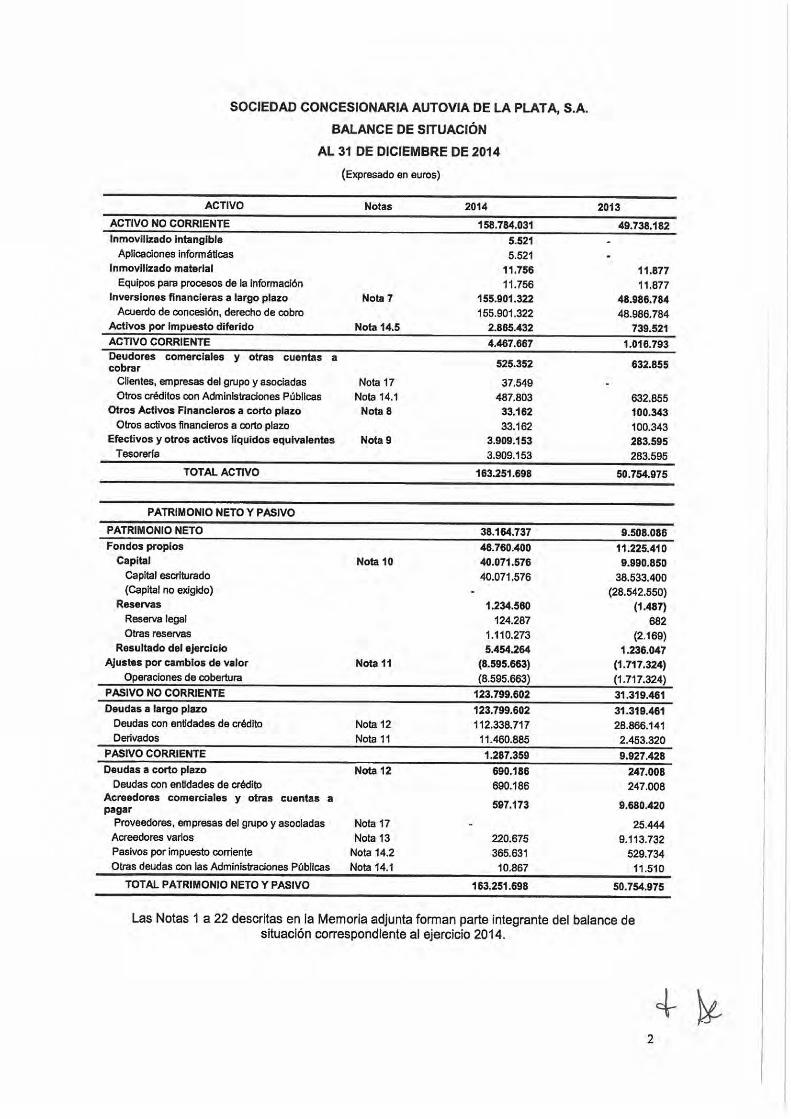

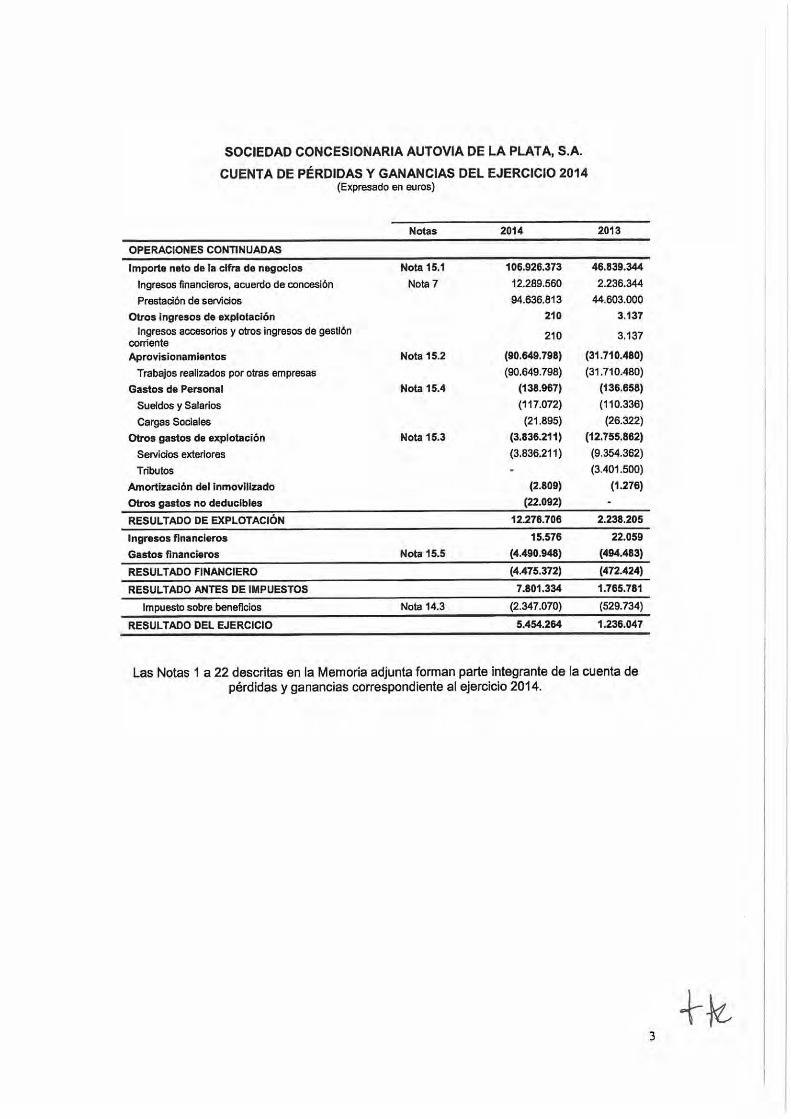

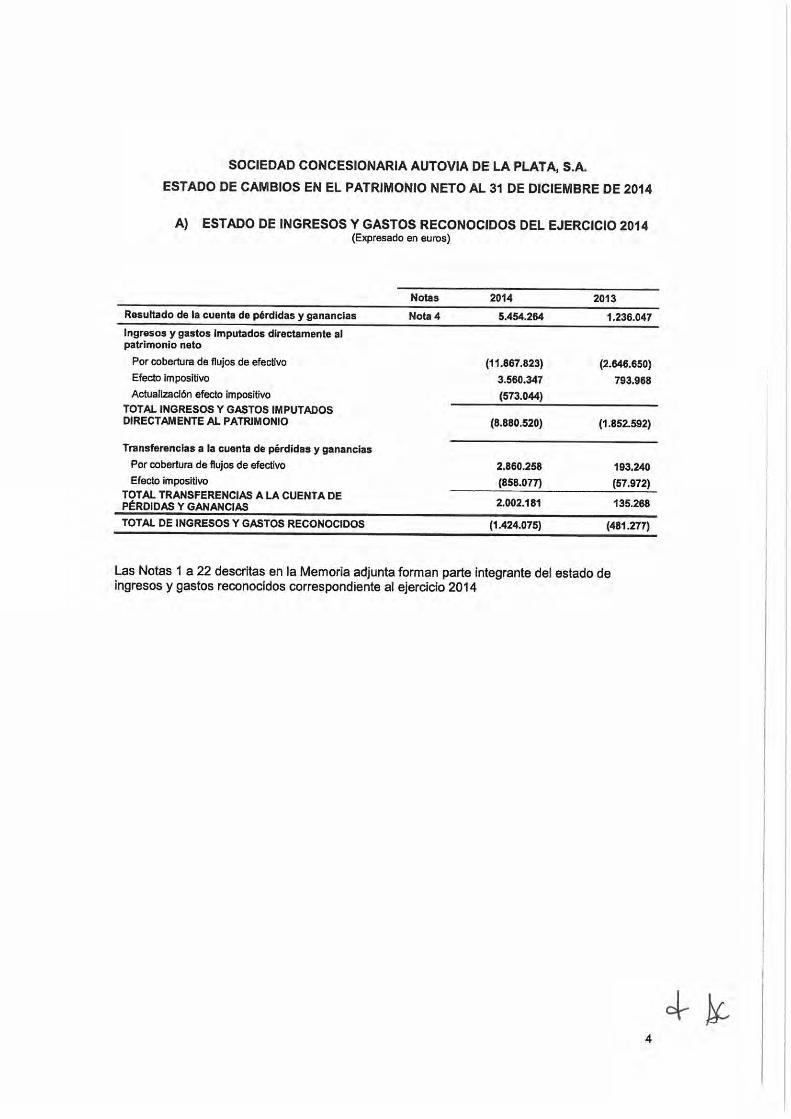

Annex 1 Financial Statements of the Issuer for the year ending 31 December 2014 ..........................................141

Annex 2 Financial Statements of the Issuer for the year ending 31 December 2013 ..........................................142

6

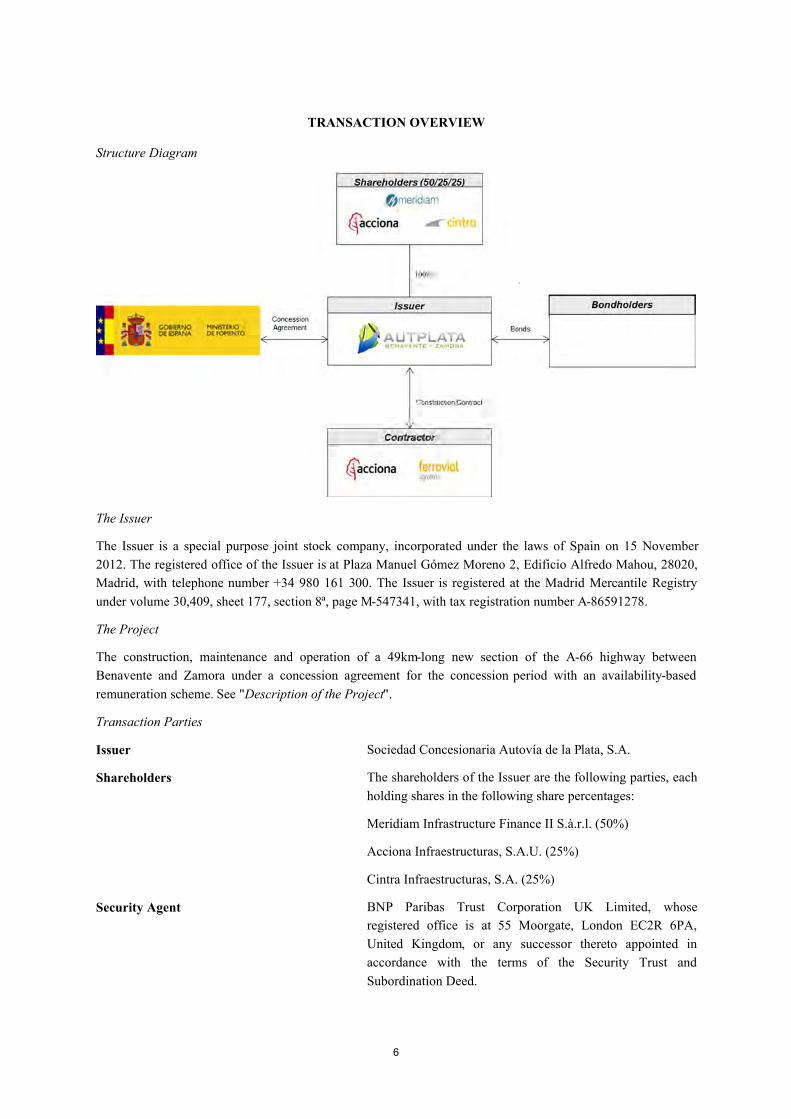

TRANSACTION OVERVIEW

Structure Diagram

The Issuer

The Issuer is a special purpose joint stock company, incorporated under the laws of Spain on 15 November

2012. The registered office of the Issuer is at Plaza Manuel Gómez Moreno 2, Edificio Alfredo Mahou, 28020,

Madrid, with telephone number +34 980 161 300. The Issuer is registered at the Madrid Mercantile Registry

under volume 30,409, sheet 177, section 8ª, page M-547341, with tax registration number A-86591278.

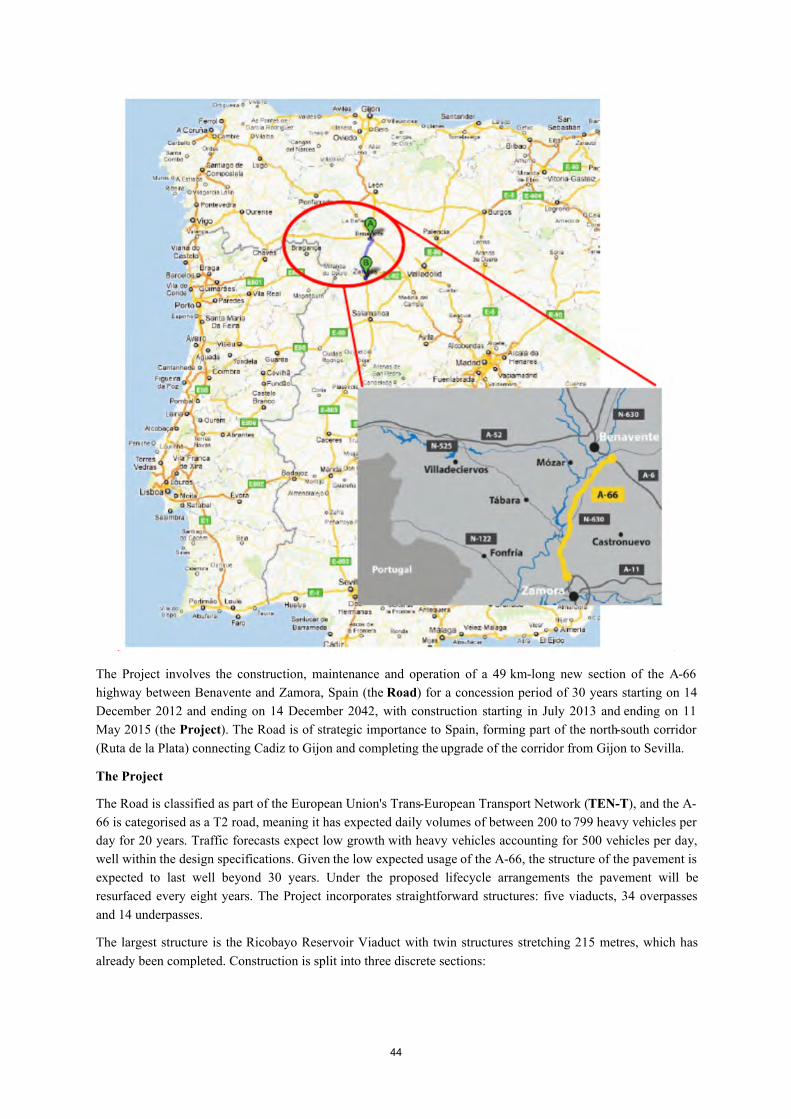

The Project

The construction, maintenance and operation of a 49km-long new section of the A-66 highway between

Benavente and Zamora under a concession agreement for the concession period with an availability-based

remuneration scheme. See "Description of the Project".

Transaction Parties

Issuer Sociedad Concesionaria Autovía de la Plata, S.A.

Shareholders The shareholders of the Issuer are the following parties, each

holding shares in the following share percentages:

Meridiam Infrastructure Finance II S.à.r.l. (50%)

Acciona Infraestructuras, S.A.U. (25%)

Cintra Infraestructuras, S.A. (25%)

Security Agent BNP Paribas Trust Corporation UK Limited, whose

registered office is at 55 Moorgate, London EC2R 6PA,

United Kingdom, or any successor thereto appointed in

accordance with the terms of the Security Trust and

Subordination Deed.

7

Account Bank Banco Bilbao Vizcaya Argentaria, S.A.

Bond Trustee BNP Paribas Trust Corporation UK Limited, whose

registered office is at 55 Moorgate, London EC2R 6PA,

United Kingdom, has been appointed as trustee for the

holders from time to time of the Bonds pursuant to the Trust

Deed.

Sole Arranger and Global Coordinator HSBC Bank plc.

Joint Bookrunners HSBC Bank plc, Banco Bilbao Vizcaya Argentaria, S.A. and

Banco Santander, S.A.

Agent Banco Bilbao Vizcaya Argentaria, S.A.

The Bonds

Name of the Issuance Issuance of Bonds by Sociedad Concesionaria Autovía de la

Plata S.A. 2015.

Amount €184,500,000

Currency Euro

Pricing Date 12 May 2015

Closing Date 27 May 2015

Form The Bonds have been issued in uncertificated, dematerialised

book-entry form (anotaciones en cuenta) in euro in an

aggregate nominal amount of €184,500,000 and

denominations of €100,000 (pursuant to which 1,845 Bonds

have been created).

Registration, clearing and settlement The Bonds are registered with the Spanish Sociedad de

Gestión de los Sistemas de Registro, Compensación y

Liquidación de Valores, S.A. Unipersonal (Iberclear) as

managing entity of the central registry of the Spanish

clearance and settlement system (the Spanish Central

Registry).

Investors in the Bonds who do not have, directly or indirectly

through their custodians, a participating account with

Iberclear may participate in the Bonds through bridge

accounts maintained by each of Euroclear Bank S.A./N.V.

(Euroclear) and Clearstream Banking, société anonyme,

Luxembourg (Clearstream Luxembourg) with Iberclear.

ISIN Code The Spanish National Numbering Agency (Agencia Nacional

de Codificación de Valores) has assigned the following ISIN

to the Bonds: ES0205068002.

Title and transfer In accordance with Article 15 of Royal Decree Law 116/1992

of 14 February on representation of securities through book

entries and clearing and settlement of securities transactions

(Real Decreto 116/1992, de 14 de febrero, sobre

representación de valores por medio de anotaciones en

8

cuenta y compensación y liquidación de operaciones

bursátiles) (RD 116/1992), each person shown in the

registries maintained by the respective Iberclear Members (or

the Spanish Central Registry itself if the Bondholder is an

Iberclear Member) as being a holder of Bonds shall be

considered the holder of the principal amount of the Bonds

recorded therein and Bondholder shall be construed

accordingly.

One or more certificates (each a Certificate) attesting to the

relevant Bondholder's holding of the Bonds in the relevant

registry will be delivered by the relevant Iberclear Member

or, where the Bondholder is itself an Iberclear Member, by

Iberclear (in each case, in accordance with the requirements

of Spanish law and the relevant Iberclear Member's or, as the

case may be, Iberclear's procedures) to such Bondholder

upon such Bondholder's request.

Each Bondholder will be treated (except as otherwise

required by Spanish law) as the legitimate owner of the

relevant Bonds for all purposes (whether or not it is overdue

and regardless of any notice of ownership, trust or any

interest or annotation of, or the theft or loss of, the Certificate

issued in respect of it).

The Bonds are issued without any restrictions on their

transferability. In accordance with Article 12 of RD

116/1992, title to securities represented through book entries

(as is the case with regard to the Bonds) may pass through

book transfer. Consequently, the Bonds may be transferred

and title to the Bonds may pass (subject to Spanish law and

to compliance with all applicable rules, restrictions and

requirements of Iberclear or, as the case may be, the relevant

Iberclear Member) upon registration in the relevant registry

of each Iberclear Member and/or the Spanish Central

Registry itself, as applicable.

Clearing Systems Iberclear, Clearstream Luxembourg and Euroclear.

Denomination of Bonds €100,000

Status and Ranking The Bonds constitute direct, senior and unconditional

obligations of the Issuer, to be secured on a first priority basis

as contemplated in Condition 3 (Security), and upon

insolvency of the Issuer will rank pari passu among

themselves (unless, with respect to a Bondholder, the Bonds

qualify as subordinated claims pursuant to article 92 and

subsequent of the Law 22/2003 (Ley Concursal) of 9 July

2003 (the Spanish Insolvency Law), as amended and save

for such obligations that may be preferred by provisions of

law that are mandatory and of general application). The

Security will be held in accordance with the terms of a

security trust and subordination deed dated the Closing Date

9

between, inter alia, the Issuer and the Security Agent.

Interest Interest on the Bonds accrues from (and including) the

Closing Date. The Bonds are interest-bearing and interest

will be calculated on the Principal Amount Outstanding of

each Bond on an Actual/360 (non-adjusted) basis. Interest

will accrue at the fixed rate of 3.169 per cent. per annum and

will be payable semi-annually in arrear, on 30 June and 31

December in each year, commencing on 30 June 2015.

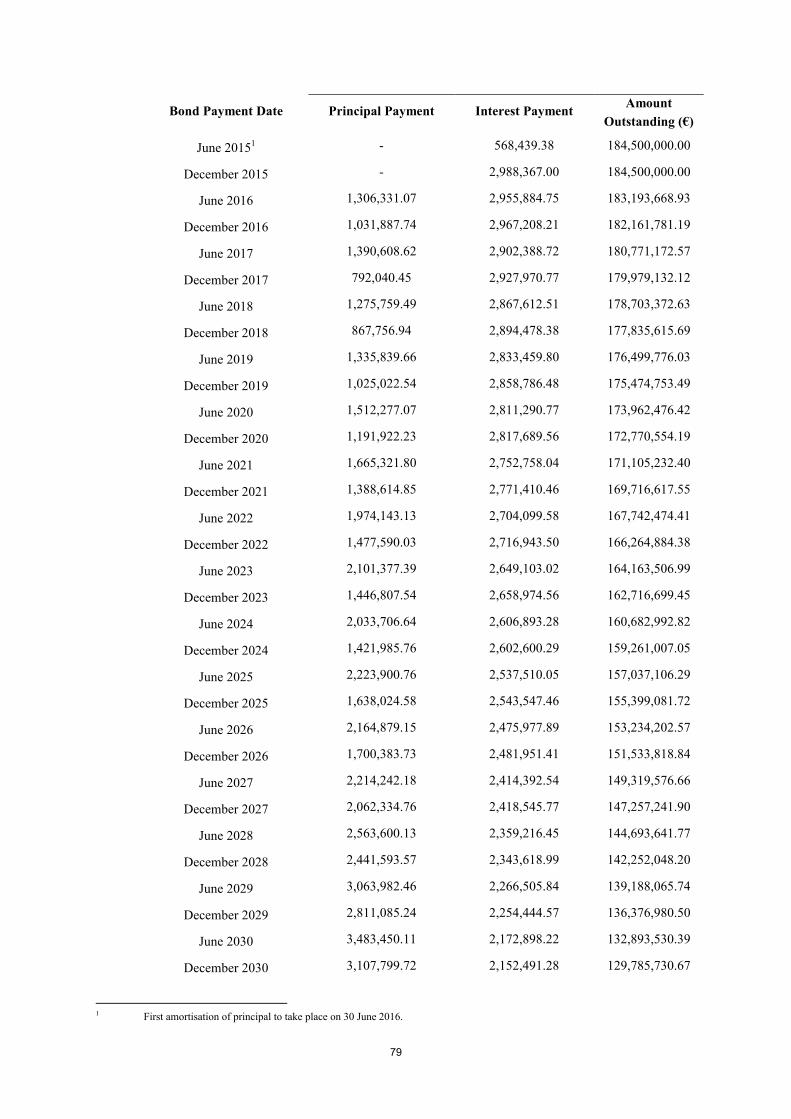

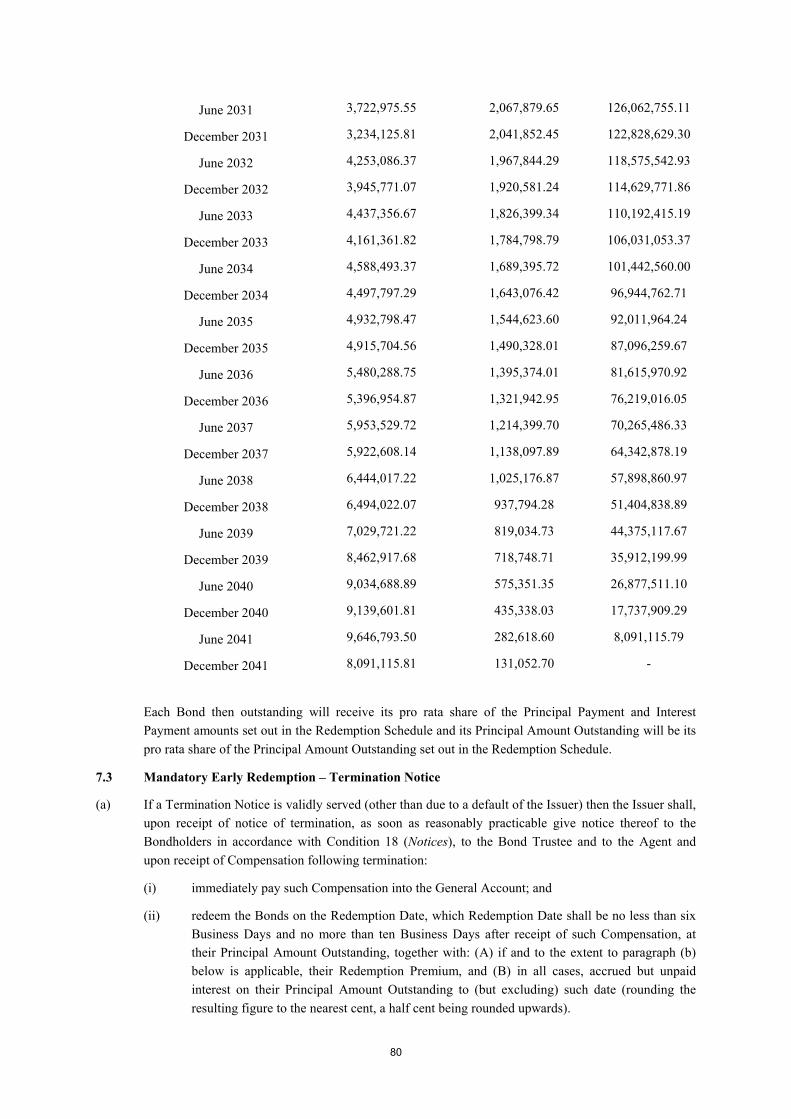

Scheduled Redemption The Bonds will be redeemed in part on 30 June and 31

December in each year according to the schedule set out at

Condition 7.2 (Scheduled Redemption). See "Terms and

Conditions of the Bonds" below.

Optional Redemption for Taxation The Issuer may, at its option, redeem: (i) all (but not some

only) of the Bonds; or (ii) only such Bonds in respect of

which Additional Amounts are required to be paid, in each

case at their Principal Amount Outstanding plus accrued but

unpaid interest, pursuant to Condition 7.5. (Redemption for

taxation). See "Terms and Conditions of the Bonds" below.

Optional Redemption The Issuer may, at any time and at its option, redeem the

Bonds in whole but not in part at their Principal Amount

Outstanding plus accrued interest and a make whole

premium, pursuant to Condition 7.6. (Optional Redemption).

See "Terms and Conditions of the Bonds" below.

Mandatory Early Redemption There will be a Mandatory Early Redemption of the Bonds

upon receipt by the Issuer of compensation proceeds under

the Concession Agreement on termination pursuant to

Condition 7.3 (Mandatory Early Redemption-Termination

Notice). See "Terms and Conditions of the Bonds" below.

Such early redemption will occur at par, and, in certain

circumstances, with payment of an additional make whole

premium, as described in more detail under Condition 7.3.

(Mandatory Early Redemption-Termination Notice). See

"Terms and Conditions of the Bonds" below.

Events of Default See Condition 11 (Events of Default) under "Terms and

Conditions of the Bonds" below.

Withholding Tax Payments of principal, interest and any other amounts

(including, where applicable, make whole premium) payable

in respect of the Bonds will be made free and clear of and

without withholding or deduction for or on account of, any

tax imposed or levied by or within Spain or by or within any

department, political subdivision or governmental authority

of or in Spain having power to tax, unless required by law. If

so required by law, the Issuer shall pay any additional

amounts to Bondholders in respect of any amounts required

to be withheld or deducted, subject to certain exceptions as

described in Condition 10 (Taxation) under "Terms and

10

Conditions of the Bonds" below.

Issue Price 100 per cent. of Principal Amount Outstanding.

Final Maturity Date 31 December 2041

Purchases The Issuer may at any time purchase Bonds in the open

market or otherwise at any price. Any Bonds purchased by

the Issuer may be cancelled and, if so cancelled, may not be

reissued or resold.

Ratings The rating to be assigned to the Bonds on or around the

Closing Date is expected to be BBB from Standard & Poor's

Rating Services.

A credit rating is not a recommendation to buy, sell or hold

securities and may be subject to revision, suspension or

withdrawal at any time by the assigning rating organisation.

Each credit rating should be evaluated independently of any

other rating and, among other things, will depend on the

performance of the business of the Issuer from time to time.

Admission to trading and listing Application will be made to MARF, within 30 days

following the Closing Date, for the Bonds to be admitted to

trading (incorporados) on this multilateral trading system in

accordance with the rules of such system.

Governing law The Bonds, and any non-contractual obligations arising out

of or in connection with the Bonds, are governed by, and

shall be construed in accordance with, English law, except

that the form and the status of the Bonds as described in

Condition 1 (Form, Denomination and Status) and the title to

the Bonds and transfer of the Bonds as described in

Condition 2 (Register, Title and Transfers) as set out in the

section of this Offering Circular headed "Terms and

Conditions of the Bonds" will be governed by Spanish law.

The Initial Security Documents and any non-contractual

obligations arising out of or in connection with the Initial

Security Documents will be governed by Spanish law.

Selling Restrictions There are restrictions on the offer, sale and transfer of the

Bonds in the United Kingdom, the United States and Spain

and other relevant jurisdictions, and such other restrictions as

may be required in connection with the offering and sale of

the Bonds (see the section headed "Sale of the Bonds"

below).

Information The Issuer will be obliged to make available to the Bond

Trustee, the Security Agent and the Bondholders certain

important information relating to the Project, including

(among other information):

(a) within 30 days of each Calculation Date, a

Compliance Certificate containing information

specified in Condition 4.6 (Compliance Certificate)

11

of the Trust Deed;

(b) as soon as reasonably practicable following the

preparation thereof, any Updated Base Case (as

defined in, and prepared in accordance with

Condition 4.5 (Updated Base Case);

(c) within 30 days of each Calculation Date, a duly

completed Investor Report, containing the

information required pursuant to Condition 4.7

(Investor Report); and

(d) within 15 days, before the start of each of its

financial years, a budget as required by Condition

4.8 (Budget).

Security, Cash Flows and Priorities of Payment

Security The initial Security will consist of the following first ranking

Security Interests, each governed by Spanish law:

(a) a pledge over the Issuer's assignable rights, present

and future, and receivables under: (i) the Project

Documents; (ii) certain Insurances taken out by the

Issuer with regard to the Project; and (ii) any letter

of credit (avales) granted in favour of the Issuer

with regards to the Project, including the

Expropriation Letters of Credit and the Construction

Performance Bonds;

(b) a pledge over the Project Accounts; and

(c) a pledge over the Issuer's share capital.

Investors should see the section of this Offering Circular

headed "Summary of the Finance Documents-Initial Security

Documents" for more details.

Pre-Enforcement Priorities of Payment Prior to the enforcement of the transaction security, subject to

certain exceptions, including for Compensation paid into the

General Account which is required by Condition 7.3

(Mandatory Early Redemption – Termination Notice) to be

applied to redeem the Bonds, and subject to any Equity Cure

Amount paid into the General Account having been applied

to redeem the Bonds (in whole or in part), as may be required

in accordance with Condition 7.4 (Mandatory Prepayment –

Equity Cure), the Issuer may only withdraw amounts from

the General Account if they are applied for the following

purposes in the following order:

(a) first, in payment of all fees, costs and expenses

incurred by the Bond Trustee and the Security

Agent under or in connection with the Finance

Documents;

12

(b) second, in payment of all fees, costs and expenses

incurred by any Administrative Party (other than the

Bond Trustee and Security Agent) under or in

connection with the Finance Documents;

(c) third, payment of any Project Costs then due but

unpaid;

(d) fourth, payments of all interest on the Bonds;

(e) fifth, scheduled principal instalments under the

Bonds;

(f) sixth, on the Closing Date and on each Calculation

Date, a transfer to the Debt Service Reserve

Account to the extent required by the Account Bank

Agreement;

(g) seventh, on the Closing Date and on each

Calculation Date, a transfer to the Maintenance

Reserve Account to the extent required by the

Account Bank Agreement;

(h) eighth, in or towards satisfaction of any mandatory

early redemption under Condition 7.3 (Mandatory

Early Redemption – Termination Notice);

(i) ninth, in or towards satisfaction of any optional

redemption under Condition 7.5 (Redemption for

Taxation);

(j) tenth, in or towards satisfaction of any optional

redemption under Condition 7.6 (Optional

Redemption);

(k) eleventh, in and towards payment of any and all

other amounts due under the Bonds; and

(l) twelfth, to the extent permitted by and in accordance

with Condition 5.20 (Restricted Payments), a

transfer to the Distribution Account.

Investors should see the section of this Offering Circular

headed "Summary of the Finance Documents" for more

details on the Project Accounts and the Account Bank

Agreement.

Post-Enforcement Priorities of Payment To the extent permitted by applicable law, all amounts

received or recovered by the Security Agent in connection

with the Finance Documents or the realisation or

enforcement of all or any part of the transaction security must

be held by the Security Agent and applied (at any time as the

Security Agent, in its discretion, sees fit) in the following

order of priority:

(a) first, on a pro rata and pari passu basis, in or

13

towards payment of any unpaid fees, costs and

expenses and all other liabilities (including by way

of indemnity) of the Bond Trustee, Security Agent

and any receiver or delegate appointed under the

Initial Security Documents;

(b) second, on a pro rata and pari passu basis, in or

towards payment of any fees, costs and expenses of

any other Secured Creditor under or in connection

with any Finance Document;

(c) third, in or towards payment of all interest due under

the Bonds;

(d) fourth, in or towards payment of all principal then

due under the Bonds;

(e) fifth, in or towards payment of any and all other

amounts due under the Bonds; and

(f) sixth, the surplus (if any), subject to any mandatory

provision of any applicable law, to the Issuer or

other person entitled to it.

Investors should see the section of this Offering Circular

headed "Summary of the Finance Documents" for more

details.

Project Accounts The Issuer will be required to maintain the following bank

accounts with the Account Bank in accordance with the

Account Bank Agreement:

(a) the General Account;

(b) the Debt Service Reserve Account;

(c) the Maintenance Reserve Account;

(d) the Insurance Proceeds Account and Disposal

Proceeds Account; and

(e) if opened, the Expropriation Reserve Account.

Investors should see the section of this Offering Circular

headed "Summary of the Finance Documents" for more

details on the Project Accounts and the Account Bank

Agreement.

Restricted Payments Subject to certain exceptions for Permitted Payments or

Permitted Transactions, the Issuer may only make Restricted

Payments from funds standing to the credit of the

Distribution Account. The Issuer will be allowed to pay

amounts into the Distribution Account on satisfaction of the

following conditions:

(a) no Default is subsisting or would result from making any

such Restricted Payment;

14

(b) the balance of the Debt Service Reserve Account is at

least the Debt Service Reserve Minimum Balance;

(c) the balance of the Maintenance Reserve Account is at

least the Maintenance Reserve Minimum Balance;

(d) the Forecasted DSCR on the most recent Calculation

Date is at least 1.15:1;

(e) the Historic DSCR on the most recent Calculation Date

is at least 1.15:1;

(f) the BLCR taking into account the proposed Restricted

Payment on the most recent Calculation Date is at least

1.15:1; and

(g) the Issuer is in compliance with its obligations under

paragraph (d) of Condition 5.25 (Project Accounts).

Investors should see Condition 5.20 (Restricted Payment) of

the section of this Offering Circular headed "Terms and

Conditions of the Bonds" for more details.

Amounts standing to the credit of the Distribution Account

will be available for distribution by the Issuer to the

Shareholders at any time, without restriction.

15

RISK FACTORS

The Issuer believes that the following factors may affect its ability to fulfil its obligations under the Bonds. All of

these factors are contingencies which may or may not occur and the Issuer is not in a position to express a view

on the likelihood of any such contingency occurring.

Factors which the Issuer believes may be material for the purpose of assessing the market risks associated with

the Bonds are also described below.

The Issuer believes that the factors described below represent the principal risks inherent in investing in the

Bonds, but the Issuer may be unable to pay interest, principal or other amounts on or in connection with the

Bonds for other reasons, and the Issuer does not represent that the statements below regarding the risks of

holding the Bonds are exhaustive. Prospective investors should also read the detailed information set out

elsewhere in this Offering Circular (including any documents incorporated by reference herein) and reach their

own views prior to making any investment decision. Prospective investors should note that the risks relating to

the Issuer, its industry and the Bonds summarised in the section of this document headed "Transaction

Overview" are the risks that the Issuer believes to be the most essential to an assessment by a prospective

investor of whether to consider an investment in the Bonds.

RISK FACTORS RELATING TO THE ISSUER AND PROJECT

The Issuer has limited business operations and sources of funds

The Issuer is a special purpose vehicle with no business operations other than those in relation to the

construction, operation and maintenance of the Project. Following the Closing Date, the Issuer's principal

sources of funds to meet its obligations under the Bonds will be revenues generated by the Project. Other than

such amounts, the Issuer will not have any other funds available to it to meet its obligations under the Bonds.

Insufficiency of the level of cover provided by the Construction Performance Bonds

Under the Construction Contract, the Contractor assumes, subject to agreed liability caps in certain cases, all

risks, responsibilities, terms, conditions, rights and obligations related to the Works established for the Issuer

under the Concession Agreement. See the sections of this Offering Circular headed "Description of the Project"

and "Description of the Concession Agreement and Construction Contract".

The Contractor has posted Construction Performance Bonds (as defined in the section of this Offering Circular

headed "Description of the Concession Agreement and the Construction Contract") to secure its obligations

under the Construction Contract. However, amounts payable under the Construction Performance Bonds may be

insufficient to satisfy the potential liability to the Issuer in the event the Contractor does not fulfil its obligations

under the Construction Contract. In such event, the Issuer would be responsible for any amount in excess due to

the Authority, which could adversely affect the Issue’s ability to make payments under the Bonds.

Early termination of the Concession Agreement

According to the LCSP (as defined below), there are a number of early termination events which entitle the

parties to terminate the Concession Agreement: extinguishment of the legal personality of the Issuer; the

declaration of insolvency; mutual agreement by the parties; Issuer's delay in meeting its deadlines; failure to

comply with any essential obligation under the Concession Agreement; the Authority's delay for more than eight

months in complying with its payment obligations; and certain force majeure events. See the section of this

Offering Circular headed "Description of the Regulatory Regime".

The Concession Agreement provides that, on early termination of the Concession Agreement (for any reason),

the Issuer has a right to be compensated by the Authority for the amount (importe) of its investment (in relation

to the expropriation of the Land, execution of the construction Works and acquisition of the goods that are

necessary for the operation of the Concession Agreement), taking into account depreciation in relation to the

16

time pending for the termination of the Concession Agreement and the economic and financial plan. The

resulting amount has to be determined within a six-month period.

The concept of compensation for the amount of the investment is not defined in the regulatory framework

applicable to the Project, nor does the regulatory framework establish a methodology for determining it. In an

early termination scenario, the Issuer expects that the Authority would determine the early termination payment

by reference to the economic and financial plan which makes reference to the financial statements of the Issuer.

However, absent any guidelines, there can be no assurances as to how the calculations for determining the early

termination payment shall be carried out by the Authority. One approach would be for the early termination

payment to be determined by reference to the book value of the assets as they appear in the Issuer's financial

statements, but a more conservative calculation would also be possible (whereby the book value of the assets is

estimated with a different account and depreciation method to that used by the Issuer).

In case of termination for reasons attributable to the Authority, the Authority shall also compensate the Issuer

for any damages caused to it. In order to determine the amount of compensation due, in accordance with law,

the future profits that the Issuer will fail to receive should be taken into account, based on operating results of

the last five years where possible, and the loss of value of the works and installations that shall not be delivered

to the Authority, considering the level of depreciation. However, there are no specific guidelines determined by

the law or Spanish Supreme Court decisions.

If the Concession Agreement is terminated for reasons attributable to the Issuer, the Concession Performance

Bond (as defined in the section of this Offering Circular headed "Description of the Concession Agreement and

the Construction Contract") shall be enforced and the Issuer shall indemnify the Authority for any damages

incurred in excess of the amount obtained from the enforcement of the Concession Performance Bond.

In case of events of force majeure that result in the termination of the Concession Agreement, the Authority

shall compensate the Issuer for the works already carried out and the higher cost in which the Issuer has incurred

into as a result of the indebtedness with third parties.

The Authority's estimate of amounts payable to the Issuer upon early termination may be less than the Issuer's

estimate, which could result in the Issuer receiving insufficient funds to satisfy its payment obligations under a

mandatory early redemption scenario. Under applicable law, the Authority is empowered to make the final

determination of the amount payable to the Issuer and, as a result, the amounts payable by the Authority upon

early termination may not be sufficient or sufficiently timely to enable the Issuer to meet its payment obligations

under the Bonds on a timely basis.

Force majeure

Various events are characterised in the Concession Agreement as force majeure events, principally war,

earthquakes and flooding, which directly cause the Issuer to be unable to comply with all or a material part of its

obligations under the agreement. Upon the occurrence of a force majeure event, the Issuer will be relieved from

liability to the extent that it is unable to perform its obligations. In case of force majeure events that completely

impede the execution of the Issuer's obligations under the Concession Agreement, the Concession Agreement

will be terminated and the Authority shall compensate the Issuer as set forth above.

In the event that the term of the Concession Agreement is suspended due to a force majeure event, the

Availability Payments expected to be received for such term may be adjusted as the Issuer will only be paid for

the operations carried out. Although, in such a situation, the Issuer may be able to recover Availability Payments

through an extension of the term of the Concession Agreement, its ability to make timely payments on the

Bonds may be adversely affected.

Events not covered by insurance policies

Although the Issuer is required to subscribe and maintain at its expense insurance policies throughout the term

of the Concession Agreement with respect to the Works (including contractors’ "all risks" insurance, accident

17

cover insurance, civil liability insurance and property damage insurance), events may occur that may not be

covered by those policies.

Environmental risk

Under the Concession Agreement, any environmental risk that arises during the operation phase of the

Concession or related to major overhauls, which may be required for keeping the infrastructure suitable for its

use during the term of the Concession or the conservation of the infrastructure since the moment in which it is

put into service after the first works are finished, shall be the responsibility of the Issuer. Therefore, once the

maintenance depot and service area have been received by the Issuer, the Contractor will no longer be

responsible for site condition and security.

In addition, pollution cover is provided under the Project's insurance policies. To the extent that the Contractor

is not liable to indemnify the Issuer and there is no insurance cover, the Issuer may have a residual risk in

respect of environmental liabilities.

Handback

The Concession Agreement provides that the Works are to be handed back to the Authority following the

termination or expiration of the Concession Agreement in a working condition sufficiently perfect to provide the

services and complying with the quality of service indicators without any deduction or infringement. In relation

to this, the Authority may carry out inspections in the area of the Concession as to determine the compliance by

the Issuer of its obligations under the Concession Agreement. Inspections may be carried out only during the

term of the Concession.

Failure to satisfy this condition could result in the liability of the Issuer to the Authority under the Concession

Agreement. Any such expenses in excess of budgeted amounts could adversely affect the Issuer's ability to

make payments under the Bonds.

Expropriations costs

Pursuant to the Construction Contract, the Issuer must make available to the Contractor all land required for the

development of the Works (the Lands). On the date of execution of the Construction Contract, and following

the relevant expropriation procedure legally established, the Issuer had obtained legal availability to provide

access for the Contractor of all Lands affected by the Works.

To run the expropriation processes, the Issuer has appointed a third party, Inserinco, s.l.,an experienced

company in relation to expropriation on road projects in Spain to undertake the expropriation. The Issuer has

been able to secure prices with 94% of landowners through mutual agreement with 100% access secured. For

the remaining 74 landowners who did not accept the mutual agreement, expropriations will be processed via an

administrative procedure which could ultimately go before an administrative jury. The Issuer has established a

worst case budget where: (i) prices proposed by landowners are accepted; and (ii) where no proposal is put

forward, the budgeted amount equals three times historical prices. Each of the Shareholders of the Issuer has put

in place an Expropriation Letter of Credit with a top tier European bank to cover what the Issuer estimates to be

the worst case amount that the Issuer might have to pay under these proceedings.

However, amounts payable under the expropriation process may exceed the amounts covered under the

Expropriation Letters of Credit. In such event, the Issuer would be responsible for any amount in excess due to

the landlords which could adversely affect the Issuer’s ability to make payments under the Bonds.

Availability Payments

Availability Payments will be made on a monthly basis by the Public Works Ministry (Ministerio de Fomento)

and therefore are a direct obligation of the Spanish Government. The Issuer is exposed to the credit quality of

the Kingdom of Spain and the willingness of the Government to continue to make its contractual availability

payments which could impact the Issuer's ability to make timely payments of the Bonds.

18

Availability Payment Deductions

The Issuer has prepared a Financial Model analysing the amounts and timing of receipt of payments under the

Concession Agreement and payments due to the Contractor and in respect of debt service, which has resulted in

an expectation that the Issuer will always have sufficient excess revenues to meet the cover ratios set out in the

Concession Agreement and to meet its payment obligations to Bondholders. Availability Payments may be

reduced if the Issuer fails to meet certain quality of service indicators and availability of road sections indicators

specified in the Concession Agreement, subject to certain grace periods and other reliefs/exceptions. In

circumstances where there is a service shortfall, and deductions and/or penalties are incurred under the

Concession Agreement, then the risk of deductions and/or penalties will fall on the Issuer.

In relation to the above, during the exploitation phase, the penalties to be imposed by the Authority (which will

be deducted from the Availability Payments) cannot exceed 20% of the income obtained for the operation of the

Road during the prior year. If such limits are exceeded, the Authority may terminate the Concession Agreement.

The 20% limit applies to all penalties and is separate from the readjustments to the Monthly Fee.

Where the deductions and/or penalties arise from any activities of the Contractor, responsibility for such

deductions and/or penalties will be passed to the Contractor subject to the agreed limitations on liability (which

are subject to certain specified exclusions). In other circumstances, this risk may reduce the Issuer's revenues

which may adversely affect the Issuer's ability to make payments on the Bonds.

Indexation

Under the Concession Agreement, 85% of the value of the monthly Availability Payments is indexed based on

the Spanish National Consumer Price Index (Índice de Precios al Consumidor) (CPI). This index is calculated

by the Spanish National Statistics Institute (Instituto Nacional de Estadística) and measures variations in prices

of a selected group of goods and services typically consumed by Spanish families. As a result, the index may not

precisely reflect variations in prices of the goods and services required by the Issuer to satisfy its operations and

maintenance obligations. There is a risk that the indexation factor as calculated under the Concession

Agreement will not fully reflect the underlying price inflation of the Project's operating costs. The Issuer's cost

of financing is fixed and therefore in a deflationary scenario revenues will reduce in line with the indexed

payments which will reduce the debt service coverage ratios. This risk is borne by the Issuer and could result in

the Issuer's available cash flow being insufficient to meet its payment obligations in respect of the Bonds on a

timely basis.

No recourse against contractors

None of the Contractor, its sub-contractors or the sub-contractors of the Issuer has any obligation to make

payments under the Bonds or otherwise compensate the Bondholders for any unpaid amount under the Bonds

and as such the Bondholders will have no recourse against any of them.

Quality of Service Indicators

Individual Quality of Service (QoS) indicators have prescribed correction factors covering quality of Roads,

safety, accidents and lane availability. Any correction factor will be applied monthly until such time as the

performance is recovered and the QoS indicator is met. The operation and maintenance strategy of the Issuer is

designed to mitigate the risk of failing QoS requirements. Penalties may be applicable if rectification of the QoS

indicator factor is not completed within the prescribed timescales. Both penalties and the correction factor could

be applied concurrently, in case of underperformance. Lane closures beyond the control of the Issuer should not

incur penalties if reacted to within prescribed timescales. The operation and maintenance strategy of the Issuer is

to conduct regular inspections of the asset quality and adherence to the QoS standards which should minimise

the level of penalties applicable. Penalties could be applicable on a case by case basis for scenarios not subject

to performance indicators under the QoS requirements.

19

The Issuer's advisers have calculated that the penalties could range between 5% and 26% of the Monthly Fee,

depending on the severity of the breach. If penalties are applied, this could adversely affect the Issuer's ability to

make payments under the Bonds.

Dependence on third parties

The Issuer is a party to contracts with a number of other third parties that have agreed to perform certain

services in relation to the Bonds (e.g. financial institutions and insurance companies). Disruptions in such

services or failures by such third parties to carry out these services could require the Issuer to obtain

replacement services, which may be more costly or unavailable. The inability of the Issuer to obtain the

provision of such services could have an adverse effect on its ability to make payments under the Bonds and/or

early redemption of the Bonds.

Change in Law

Poor economic conditions have affected, and continue to affect, government budgets and threaten the

continuation of government subsidies such as feed-in tariffs, tax benefits and other similar subsidies that benefit

the Issuer’s business. Such conditions may also lead to adverse changes in law, such as the amendments to the

Spanish tax law affecting the Issuer's ability to deduct finance costs. The reduction or elimination of such

subsidies or adverse changes in law could have a material adverse impact on the profitability of the Project and

therefore on the Issuer's ability to make payments under the Bonds.

Increase of operating and maintenance costs

As costs are not fixed via a contract, the Issuer is exposed to fluctuations in the price and supply of items

required for the operation and maintenance of the Project. The ability to outsource in the future and the

experience of the Contractor mitigates this risk; however, they do not fully eliminate the Issuer's exposure to

commodity prices and supply risk, which could materially and adversely affect the profitability of the Project

and therefore could adversely affect the Issuer's ability to make payments under the Bonds.

There is a risk that the expected timing of maintenance expenditure will change due to defects found in the

future or higher than expected traffic volumes. Under the Construction Contract, there is a one year warranty for

defective materials from the Contractor and unlimited liability of the Contractor in relation to the repairs and

remedies of the defects set forth in the Acta de Comprobación de Obras or that are noticed after the signing of

the Acta de Comprobación de Obras and that, pursuant to the Concession Agreement, the Terms of Tender and

the applicable legislation, shall be borne by the Issuer. Traffic forecasts have been provided by the Authority,

and forecasted traffic is well below the design level of the Project assets.

Health and safety regulations

The Issuer is responsible for complying with all health and safety regulations regarding the development of the

Project. However, under the Construction Contract, this risk will be passed down to the Contractor (subject to its

overall caps on liability). See “Description of the Concession Agreement and the Construction Contract-

Penalties and Limitation of liability”).To the extent that, due to the caps on liability of the Contractor, there is a

remaining amount to pay in relation to penalties imposed by the Authority or the Authority decides to terminate

the Concession Agreement, the Issuer may have a residual risk which could adversely affect the Issuer's ability

to make payments under the Bonds.

RISK FACTORS RELATING TO THE SECURITY

The Bonds will not be secured initially

The Bonds will not be secured initially by the Security under the Initial Security Documents. Although the

Issuer and the Shareholders executed the Initial Security Documents on the Closing Date, the validity and

effectiveness of such documents are subject to (i) the fulfilment of a condition subsequent (condición

suspensiva) (which shall be attested by the Notary through the relevant annotation (diligencia) on the Initial

20

Security Documents) and completion of certain other perfection requirements. That condition subsequent

requires (i) that Banco Bilbao Vizcaya Argentaria, S.A. (BBVA) (as settlement agent) issues a certificate

confirming that BBVA has made the relevant payments to Banco Bilbao Vizcaya Argentaria, S.A. (as operative

agent) under the commercial facility agreement and to Banco Bilbao Vizcaya Argentaria, S.A. and to Banco

Santander, S.A. (as swap providers) under the Hedging Agreements and (ii) that EIB has confirmed to the

Notary (by email) the receipt of the relevant payment made by BBVA.

Under the Conditions, the Issuer has undertaken to ensure that the Security is as described in paragraph (b) of

Condition 3 (Security) by no later than 1 June 2015 at 23:59 Madrid time. However, the Issuer cannot assure

that the condition subsequent will be fulfilled on the Closing Date or by this deadline, in which case the Security

under the Initial Security Documents would not be granted.

Insolvency of the Issuer before the granting of Security

As mentioned above, the Security will not be valid and effective until the fulfilment of the condition subsequent

and completion of certain other perfection requirements.

Furthermore, under section 90.2 of the Spanish Insolvency Law, the Security in order to be recognised in the

lists of creditors and assets should be valid and enforceable against third parties when the insolvency

proceedings are opened. However, according to article 1120 of Spanish Civil Code, if the condition is fulfilled,

the relevant Court would analyse since when the obligation under condition precedent is considered to be

binding which includes the possibility of considering to be retroactively binding since the very first moment in

which the obligation was granted if all the requirements were met at that moment (although under condition

precedent). We are not aware of any precedent in Spanish Insolvency Proceedings of the recognition of the

securities under condition precedent which are fulfilled after insolvency declaration. Hence, in case of

insolvency of the Issuer after the Closing Date and before the condition subsequent is fulfilled, the Bondholders

would face a risk of not benefitting from the Security within the insolvency proceedings (concurso), depending

on the construction of the relevant Court to be made between article 90.2 of the Spanish Insolvency Law and

article 1120 of the Spanish Civil Code.

Enforcement of Security may be affected by restrictions under Spanish insolvency law

Spanish insolvency law foresees a suspension of the enforcement powers held by creditors holding securities in

the event of insolvency of the debtor.

Article 5bis of the Spanish Insolvency Law 22/2003 of 9 July (the Spanish Insolvency Law) (Ley Concursal)

states that if a debtor notifies the commercial court (Juzgado de lo Mercantil) that it has started negotiating with

its creditors in order to obtain their approval regarding: (i) a refinancing agreement as referred to under article

71.bis.1 of the Spanish Insolvency Law; (ii) a refinancing agreement as referred to under the Fourth Additional

Provision (Disposición Adicional Cuarta) of the Spanish Insolvency Law; or (iii) an advance proposal of

arrangement between creditors (propuesta anticipada de convenio), its obligation to file an application for

volunteer insolvency shall be suspended for three months. Following those three months, the debtor will have an

additional period of one month to submit such application.

As from the date of such notice and during such pre-insolvency period, no court or out-of-court enforcement

proceedings of securities over any assets or rights of the debtor that are necessary for the continuity of its

business may be initiated, and those legal proceedings initiated prior to such notice shall be suspended.

Nevertheless, public law claims shall not be subject to this enforcement limitation.

In addition, no individual financial creditor may initiate enforcement actions against the debtor (and those

already initiated shall be suspended) if creditors holding at least 51% of the financial liabilities against the

debtor have expressly agreed to start negotiating with the debtor in order to arrange a refinancing agreement and

have also agreed not to file or continue enforcement actions against the debtor while the debtor and its creditors

are still negotiating.

21

Despite the foregoing, secured creditors will still be entitled to bring court or out-of-court enforcement

proceedings against the corresponding secured assets. However, once proceedings have been initiated, they shall

be immediately suspended.

Once the debtor is declared insolvent, enforcement of security over any assets of the debtor which are necessary

for the continuity of its business shall be suspended until the earliest of the following occurs: (i) the approval of

an arrangement between creditors, unless such agreement is binding on those secured creditors, in which case

the provisions under such agreement will apply; and (ii) in case the liquidation period has not been initiated, the

first anniversary of the declaration of insolvency. Enforcement shall be suspended even if, at the time of the

declaration of insolvency, the relevant notices of public auction have been published. The suspension may be

lifted or the commencement of enforcement proceedings may be possible if a court resolution which considers

that the charged asset is not necessary for the continuity of the debtor's business is obtained from the judge in

charge of the debtor's insolvency proceedings. Although, for the purposes of such declaration, the Spanish

Insolvency Law points out that those shares or participations in companies whose only activity is the holding of

one asset and the liabilities deemed necessary for its financing shall not be deemed necessary for the continuity

of the debtor's business, provided that the enforcement of securities over those shares or participations does not

lead to a termination event or an amending event that allows the insolvent debtor to maintain development of the

relevant asset, the interpretation of the corresponding Article of the Spanish Insolvency Law is controversial and

there are multiple interpretations between scholars and the existing case law. Finally, the enforcement of

Securities shall be subject to Spanish law and, in particular, to the Spanish Insolvency Law, when applicable,

which may lead to delays in enforcement.

Enforcement of Security may be affected by the appointment of a Security Agent

The Bondholders shall not have any individual powers in order to enforce any Security granted in respect of the

Bonds, except through the Security Agent, who shall enforce these rights following the instructions of the Bond

Trustee given in accordance with the Security Trust and Subordination Deed. Given that Spanish law does not

recognise the concept of a "security agent", there is uncertainty as to whether a Spanish court would recognise

the concept and authority of the Security Agent and whether this could eventually cause delays in the

enforcement of Security or prevent its enforcement in the terms stated under the Initial Security Documents.

Some lawyers maintain that a security agent would only be entitled to enforce Security to the extent that it

secures its part of the secured obligations, but not as per the part of the remaining creditors' secured obligations.

The Security Agent may be required to provide evidence of its representation of all the Secured Creditors in

order to enforce the Security. Therefore, validity and enforceability of the Security granted in favour of the

Bondholders through the Security Agent may be subject to certain limitations.

Release and registration of the non-possessory pledges over credit rights

Pursuant to Article 3 of Law 16 December 1954 on Chattel Mortgage and Non-possessory pledges (the Non-

Possessory Pledge Law), both the release of the Spanish law non-possessory pledges granted in relation to the

Existing Financing and the granting of the new Spanish law non-possessory pledge in relation to the Bonds have

to be executed before a Spanish notary and be formalised by virtue of a public deed (escritura pública) or a deed

(póliza). Both the release of the Spanish non-possessory pledges granted in relation to the Existing Financing

and the granting of the new Spanish non-possessory pledge have been executed subject to the condition

subsequent, as described above.

Once the condition subsequent is fulfilled, in order to be effective, Article 3 of the Non-Possessory Pledge Law

provides that the release of the Spanish non-possessory pledges granted in relation to the Existing Financing and

the granting of the new Spanish non-possessory pledge have to be registered with the corresponding Registry of

Moveable Assets (Registro de Bienes Muebles). Furthermore, pursuant to Article 418 of the Mortgage

Regulation (Reglamento Hipotecario) and Article 71 of the Non-Possessory Pledge Law, the Spanish notary

before whom the release of the Spanish non-possessory pledges granted in relation to the Existing Financing and

the new Spanish non-possessory pledge in relation to the Bonds have been granted, once executed, must send a

22

notice (comunicación) of the execution of such documents to the relevant Registry of Moveable Assets by

telefax on the Closing Date and in the corresponding order (i.e. the release of the Spanish non-possessory

pledges granted in relation to the Existing Financing will be sent first and immediately after the granting of the

new Spanish non-possessory pledge).

The recipient registrar shall make an annotation of document submission (asiento de presentación) (the

Annotation) on the Registry of Moveable Assets records. This will be done before any analysis by the

corresponding registrar is carried out on the submitted documents in order to reserve priority. The Annotation of

the documents will be made by order of reception (firstly the release of the Spanish non-possessory pledges

granted in relation to the Existing Financing, secondly the granting of the new Spanish non-possessory pledge)

on the date the corresponding telefax is received or, in case the telefax is received after the Moveable Assets

Registry business hours, on the business day immediately after. Pursuant to Article 24 of the Mortgage Law

(Ley Hipotecaria), which applies to non-possessory pledges in those aspects non expressly regulated in the Non-

Possessory Pledge Law, the date on which the Annotation is made will become the date of (retroactive) effective

registration of both the release of the Spanish non-possessory pledges granted in relation to the Existing Facility

and of the new Spanish non-possessory pledge once the registrar, after having reviewed the relevant documents,

effects their registration.

Under Article 17 of the Mortgage Law, the Annotation will protect against registration of any other document

that is contradictory to the terms of the document(s) being considered by the Moveable Asset Registry (for

example, a new non-possessory pledge) for a period of 60 business days.

As explained above, the perfection of the new Spanish non-possessory pledge is subject to its registration in the

relevant Movable Assets Registry. Spanish registrars are highly qualified law officers who will only accept

registration of the relevant documents upon examination of their conformity with mandatory Spanish law and

the relevant registrar may refuse to register such documents, or any amendment, assignment or transfer thereof

if he or she considers the documents have any rectifiable defects (defectos subsanables).

If, when analysing the new Spanish non-possessory pledge, the relevant registrar ascertains that it contains

rectifiable defects, pursuant to Article 38 of the Regulations on the Registration of the Chattle Mortgage and

Non-Possessory Pledge (Reglamento del Registro de Hipoteca Mobiliaria y Prenda sin Desplazamiento) and the

Third Additional Provision of the Non-Possessory Pledge Law, the Annotation will be automatically extended

for an additional period of 60 business days since the date on which the registrar’s assessment containing the

rectifiable defects is issued. The 60 business day’s period may be extended to 180 business days upon written

request to the Registrar.

Accordingly, the Security may be affected as follows:

(a) The release of the Spanish non-possessory pledges in relation to the Existing Financing and the

granting of the new Spanish non-possessory pledge must be registered with the corresponding

Moveable assets Registry in order to become effective.

(b) If the Spanish non-possessory pledges in relation to the Existing Financing are not released, the new

Spanish non-possessory pledge will rank second to the existing one.

(c) If the Registrar does not register the non-possessory pledges in relation to the Existing Financing right

away but requires further explanations/documentation, the analysis of the new non-possessory pledge

will be suspended until registration of the release is effective.

RISK FACTORS RELATING TO TAXATION

Certain payments in respect of the Bonds may be impacted by the EU Savings Directive

Under Council Directive 2003/48/EC on the taxation of savings income (the EU Savings Directive), Member

States of the European Union (the EU Member States and each an EU Member State) are required to provide

to the tax authorities of other EU Member States details of certain payments of interest or similar income paid or

23

secured by a person established in an EU Member State to or for the benefit of an individual resident in another

EU Member State or certain limited types of entities established in another EU Member State.

For a transitional period, Austria is required (unless during that period it elects otherwise) to operate a

withholding system in relation to such payments (subject to a procedure whereby, on meeting certain conditions,

the beneficial owner of the interest or other income may request that no tax be withheld). The end of the

transitional period is dependent upon the conclusion of certain other agreements relating to information

exchange with certain other countries. A number of non-EU countries and territories, including Switzerland,

have adopted similar measures (a withholding system in the case of Switzerland).

On 24 March 2014, the Council of the European Union adopted a Council Directive (the Amending Directive)

amending and broadening the scope of the requirements described above. The Amending Directive requires EU

Member States to apply these new requirements from 1 January 2017, and if they were to take effect the

changes would expand the range of payments covered by the EU Savings Directive, in particular to include

additional types of income payable on securities. The Amending Directive would also expand the circumstances

in which payments that indirectly benefit an individual resident in an EU Member State must be reported or

subject to withholding. This approach would apply to payments made to, or secured for, persons, entities or

legal arrangements (including trusts) where certain conditions are satisfied, and may in some cases apply where

the person, entity or arrangement is established or effectively managed outside of the European Union.

However, on March 2015, the European Commission proposed the repeal of the Savings Directive from 1

January 2017 in the case of Austria and from 1 January 2016 in the case of all other Member States (subject to

ongoing requirements to fulfil administrative obligations such as the reporting and exchange of information

relating to, and accounting for withholding taxes on, payments made before those dates and certain other

transitional provisions in the case of Austria). This is to prevent overlap between the Savings Directive and a

new automatic exchange of information regime to be implemented under Council Directive 2011/16/EU on

Administrative Cooperation in the field of Taxation (as amended by Council Directive 2014/107/EU). The

proposal also provides that, if it proceeds, Member States will not be required to apply the new requirements of

the Amending Directive.

If a payment were to be made or collected through an EU Member State (or any non-EU country or territory

which has adopted similar measures in order to conform to the EU Savings Directive) which applies a

withholding tax system as referred to above and an amount of, or in respect of, tax were to be withheld from that

payment, neither the Issuer nor any Agent (as defined in the Terms and Conditions of the Bonds) nor any other

person would be obliged to pay additional amounts with respect to any Bond as a result of the imposition of

such withholding tax. The Issuer will be required to maintain a Agent in an EU Member State (if any) that

would not be obliged to withhold or deduct tax pursuant to the relevant national legislation implementing, or

introduced in order to conform to, the EU Savings Directive (so long as there was such a member state).

Potential investors who are in any doubt as to their tax position should consult their own independent tax

advisers.

The proposed financial transactions tax (FTT)

On 14 February 2013, the European Commission published a proposal (the Commission's Proposal) for a

Directive for a common FTT in Belgium, Germany, Estonia, Greece, Spain, France, Italy, Austria, Portugal,

Slovenia and Slovakia (the participating Member States).