23rd Annual Schedulers & Dispatchers ConferenceSan Diego, CA – January 15-18, 2012

SIFL and Non-Business Use Tax Rules:Turning the Gray to Black and White

San Diego, California| 01/17/2012

SIFL and Non-Business Use Tax Rules

Gerald GradyCSX CorporationJacksonville, FL

Mike NicholsNBAA

Washington, DC

George Rice, CPARice & AssociatesCosta Mesa, CA

Presenters

2

What Is Personal Use?

• Personal Use

– Flight is not for the business of the company

– Can include flights that are business for the pax, but not for thecompany’s business

– Vacation, Entertainment, Recreation

• On any aircraft the employer provides

– Chartered aircraft, fractional aircraft share, wholly-owned aircraft

• Employee includes:

– Employees, partners, directors, independent contractors, certainformer employees

– Guest of employee (even if employee is not on board/recipient offlight)

3

FAA Considerations

For a Part 91 operator

4

FAA Considerations

• Part 91 operator options for personal use payment

– Time sharing agreement

• Aircraft + crew leased to employee

• Allows limited cost reimbursement

see FAR 91.501(c)(1) and 91.501(d)(1) through (d)(10)

5

FAA Considerations

• Part 91 operator options for personal use payment

– Recent FAA legal interpretation

• Full cost reimbursement as permitted by91.501(b)(5) may be allowed for certain flights

– Must have in place:

• Action by Board naming execs whose plans areroutinely changed

• Company must maintain this list

• Company keeps records that flight was “routinepersonal travel”

see NBAA Member Resource: FAA Legal InterpretationPermits Reimbursements for Certain Personal Flights 6

IRS Considerations

Impact on the employee

7

IRS Considerations

• The IRS views personal flights on the companyaircraft as a taxable fringe benefit

• Employee pays payroll tax and income tax on thevalue of the flight

– W-2 or 1099

• One of two methods may be used to determine thevalue:

– Fair Market Value (the charter rate)

– Standard Industry Fare Level (SIFL)

Impact on the Employee

8

IRS Considerations

• Fair Market Value:

– Charter rate used for the flight – one rate no matter howmany people are on board the aircraft

– Don’t fudge the numbers

– Keep a record of the charter quote

– Obtain a charter quote from a local 3rd party charter operatorlocal to where the flight originates

– Usually (not always) more expensive for the employee

Impact on the Employee

9

www.nbaa.org/admin/taxes/personal-use/

10

IRS Considerations

• SIFL:

– Designed to equate first class airfare

– Calculated per person

– Based on statute miles flown

• 1 nautical mile = 1.15 statute miles

– Employee status is a factor

• Control employee vs. non-control employee

– Aircraft weight is a factor

Impact on the Employee

11

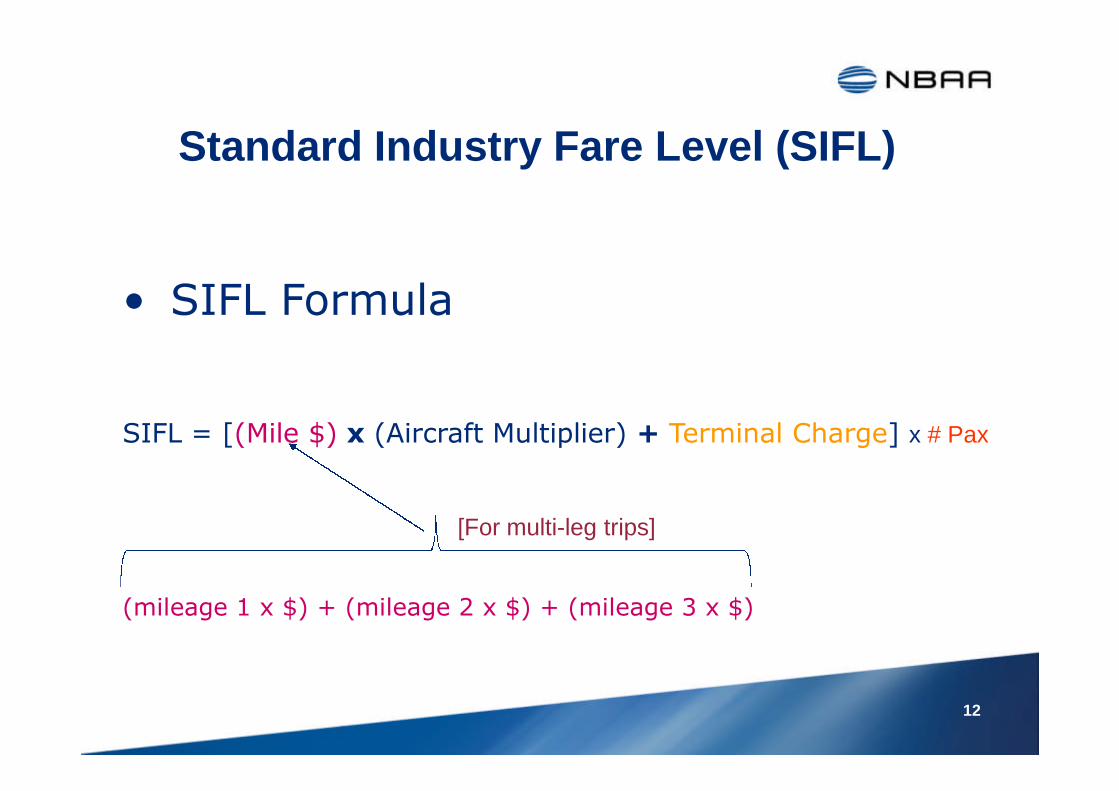

Standard Industry Fare Level (SIFL)

• SIFL Formula

SIFL = [(Mile $) x (Aircraft Multiplier) + Terminal Charge] x # Pax

(mileage 1 x $) + (mileage 2 x $) + (mileage 3 x $)

12

[For multi-leg trips]

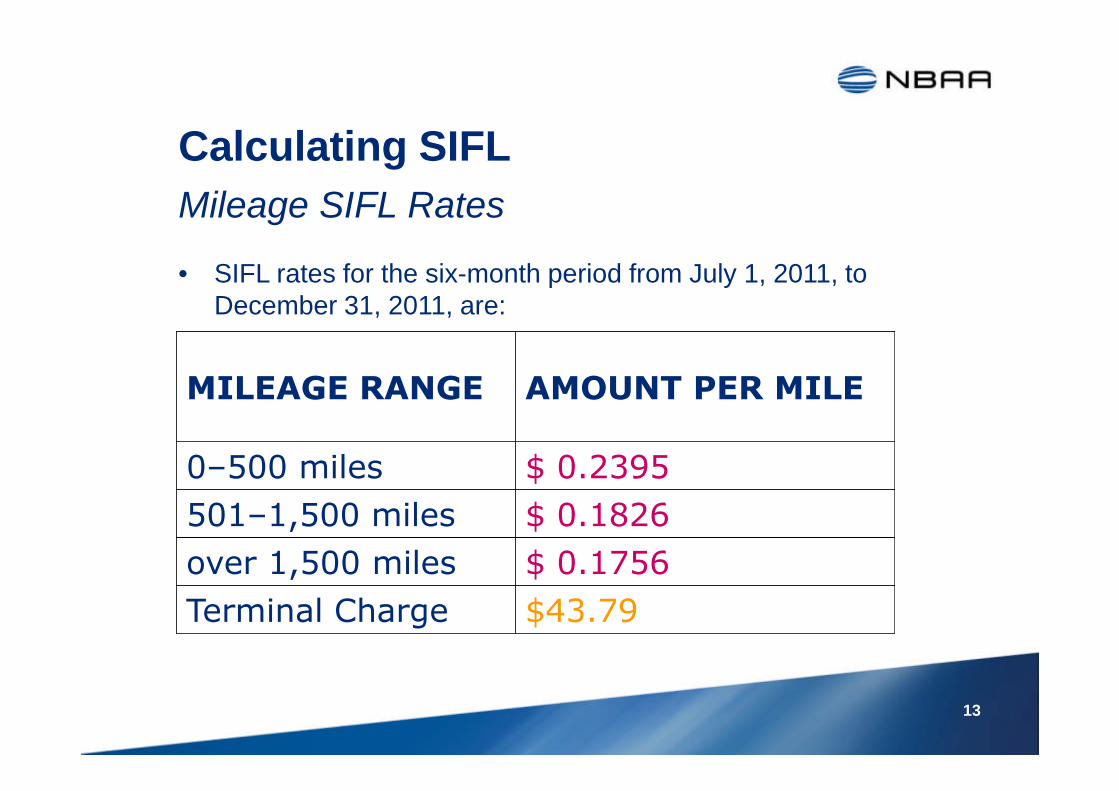

Calculating SIFL

• SIFL rates for the six-month period from July 1, 2011, toDecember 31, 2011, are:

Mileage SIFL Rates

MILEAGE RANGE AMOUNT PER MILE

0–500 miles $ 0.2395

501–1,500 miles $ 0.1826

over 1,500 miles $ 0.1756

Terminal Charge $43.79

13

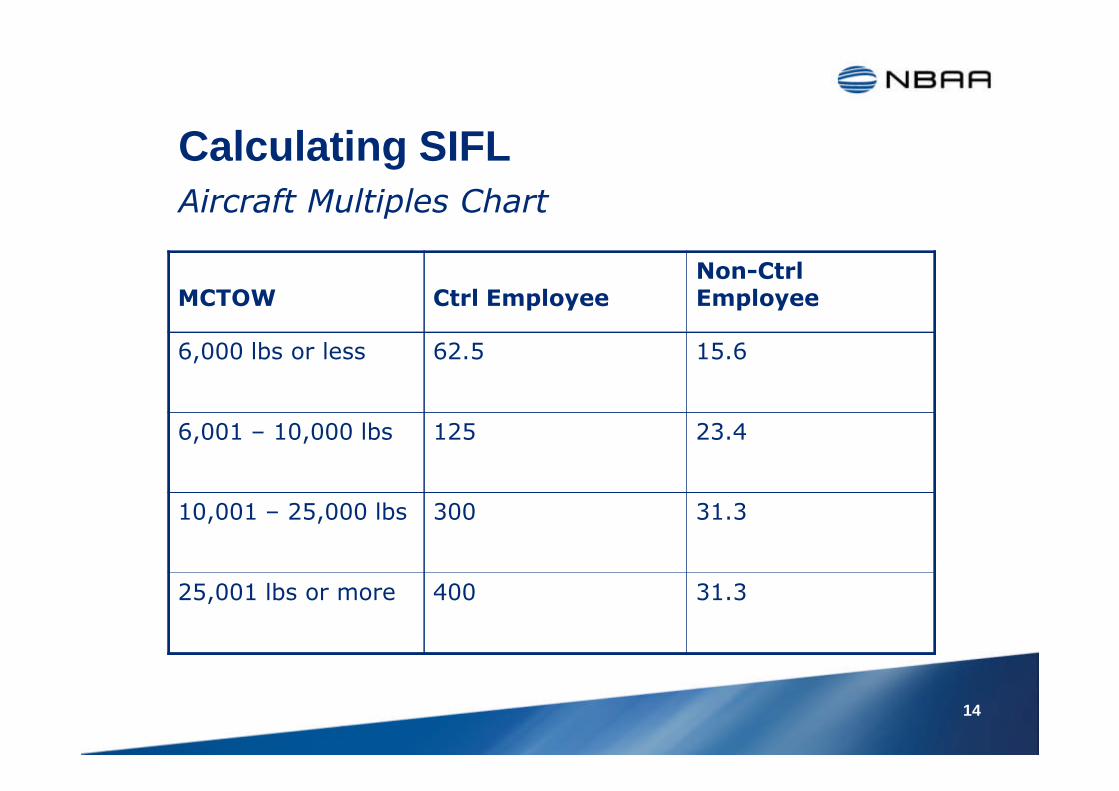

Calculating SIFL

MCTOW Ctrl EmployeeNon-CtrlEmployee

6,000 lbs or less 62.5 15.6

6,001 – 10,000 lbs 125 23.4

10,001 – 25,000 lbs 300 31.3

25,001 lbs or more 400 31.3

Aircraft Multiples Chart

14

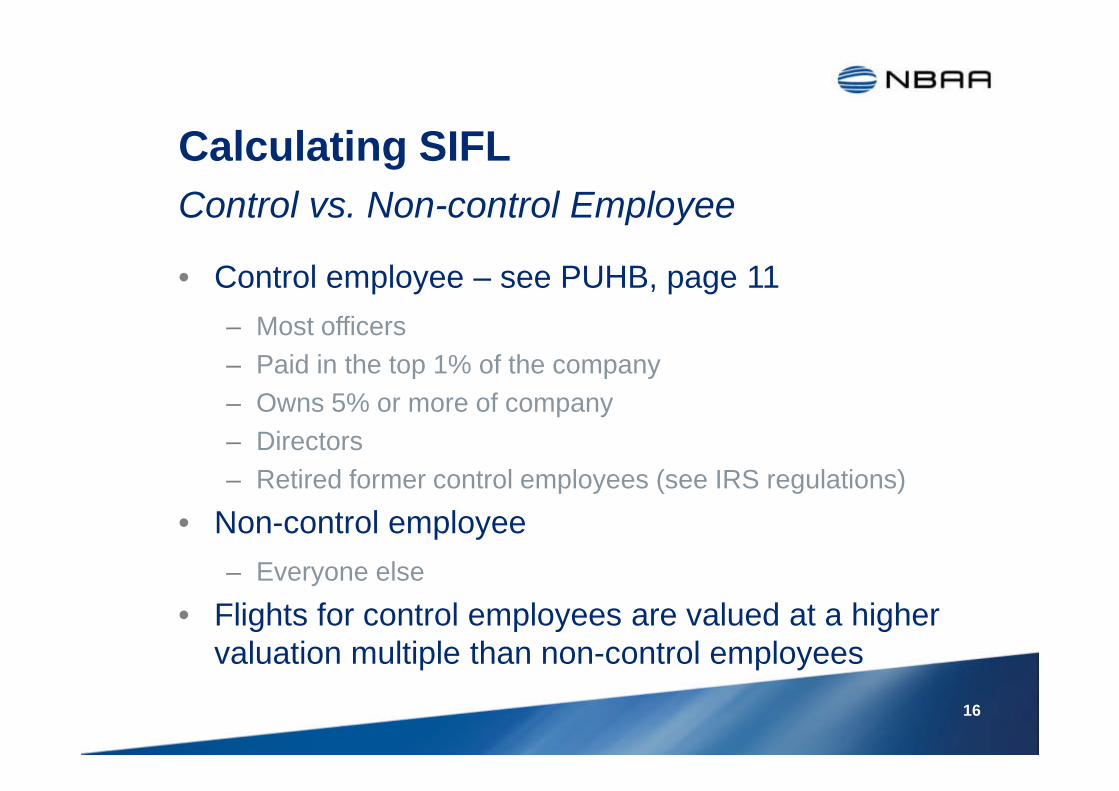

Calculating SIFL

• Control employee – see PUHB, page 11

– Most officers

– Paid in the top 1% of the company

– Owns 5% or more of company

– Directors

– Retired former control employees (see IRS regulations)

• Non-control employee

– Everyone else

• Flights for control employees are valued at a highervaluation multiple than non-control employees

Control vs. Non-control Employee

16

Calculating SIFL

• “Flight” means each time the Employee Boards andDeplanes

– A round trip includes at least two flights.

– If no employee is on board, no benefit received. (No chargefor repositioning flights)

• Landings for fuel, weather, or emergencies are“intermediate stops”

– “Ignore” these intermediate stops when calculating theemployee’s flight distances

17

Other SIFL Considerations

• Mixing business with pleasure

– One destination; two purposes for the employee

• What was the primary purpose of the passenger?

– How much time was spent on business? On personal?

– Who was on the trip (employee alone or with spouse, kids)?

– Not up to S&D to decide purpose of the trip

• Can help inform employees how these flights could beviewed

• Provide trip form where employee characterizes purposeof the trip and is on the hook via their signature

18

Other SIFL Considerations

• Mixed use flights – primarily business

– Multiple destinations; some for business, some for pleasure

– If trip primarily for employer’s business – include in incomevalue of total trip less business flights

• Mixed use flights – primarily personal

– Multiple destinations; some for business, some for pleasure

– If trip primarily personal – include in income value of personalflights that would have been taken if no business

19

SIFL: Special Rules & Exceptions

• General Rule: In most cases, spousal travel ispersonal

• Requirements for spouse to be treated as a businessflight:

– Must be an employee of the employer

– Must travel on bona fide business purpose

– The travel expense must be otherwise deductible

• The mere expectation of the employer company that aspouse will attend a function requiring travel does notconstitute employment

Spousal Travel

20

SIFL: Special Rules & Exceptions

• Age – it helps to be young!

– Children under 2 years of age are not included in valuation

– Be certain to document the age of the child in your paperwork

21

SIFL: Special Rules & Exceptions

• 50% Seating Capacity Rule:

– If 50% of the seating capacity is filled withemployees traveling on business when theemployee or family member boards and deplanes,then no fringe benefit is imputed.

– Seating Capacity: Max number of seats installedon the aircraft at any time on or prior to the date ofthe flight within 24 months

– Seats Not Legal & Not Used for Takeoff NotCounted

22

SIFL: Special Rules & Exceptions

• “Bona Fide Business-Oriented Security Concerns:”

– Must Have a Study Done

– Must be Part of a Complete Program• But May Be Limited to Certain Areas

– Specific Study for Family Members if they TravelWithout Employee

– Use a 200% Multiplier regardless of Aircraft Weightand Control Status of Employee

– For Control Employees in Aircraft over 10,000pounds, this is a significant savings

23

SIFL: Special Rules & Exceptions

Foreign Travel

• Disallowance Rule applies only to individuals– see PUHB, page 12,13.

• Does not apply to employer company

• SIFL Calc for Business Trip > 7 days uses thismethodology

• Conventions & Seminars

24

IRS Considerations

Impact on the Company – Personal Entertainment Use

25

Personal Entertainment Use Disallowed

General Rule: The allocable costs of operating personalentertainment flights on behalf of “specifiedindividuals” is not deductible.

• “Specified Individual” is defined by SEC regs

Tax Regulations require:

• Individual passenger tracking & classification

• Allocation methods are mandated

• Costs & Expenses are broadly defined

26

Personal Entertainment Use Disallowance

• Specified Individuals

– Officer

– Director, or

– 10% or more owner

– See NBAA Personal Use Handbook, page 21

• Different than Control Employee

– Control Employee – 5% ownership

This rule applies only to

27

Personal Entertainment Use Disallowance

• Definition of entertainment

– Activity generally considered to constitute entertainment,amusement or recreation

• Examples of entertainment activities

– Nightclubs, cocktail lounges, theatres, country clubs, golf andathletic clubs, sporting events, hunting, fishing, vacation

– Sailing, sightseeing, Kentucky Derby, Superbowl, parties

28

Personal Entertainment Use Disallowance

• Commuting to/from work or between homes

• Other personal business travel

– Attend director meetings (unrelated company)

– Investment Activity

– Meetings with tax accountant, attorney or broker

• Other routine personal travel

– Medical doctor, visit sick relatives

– Taking children to school

• Funeral

• Charitable activity

Examples of non-entertainment activities

29

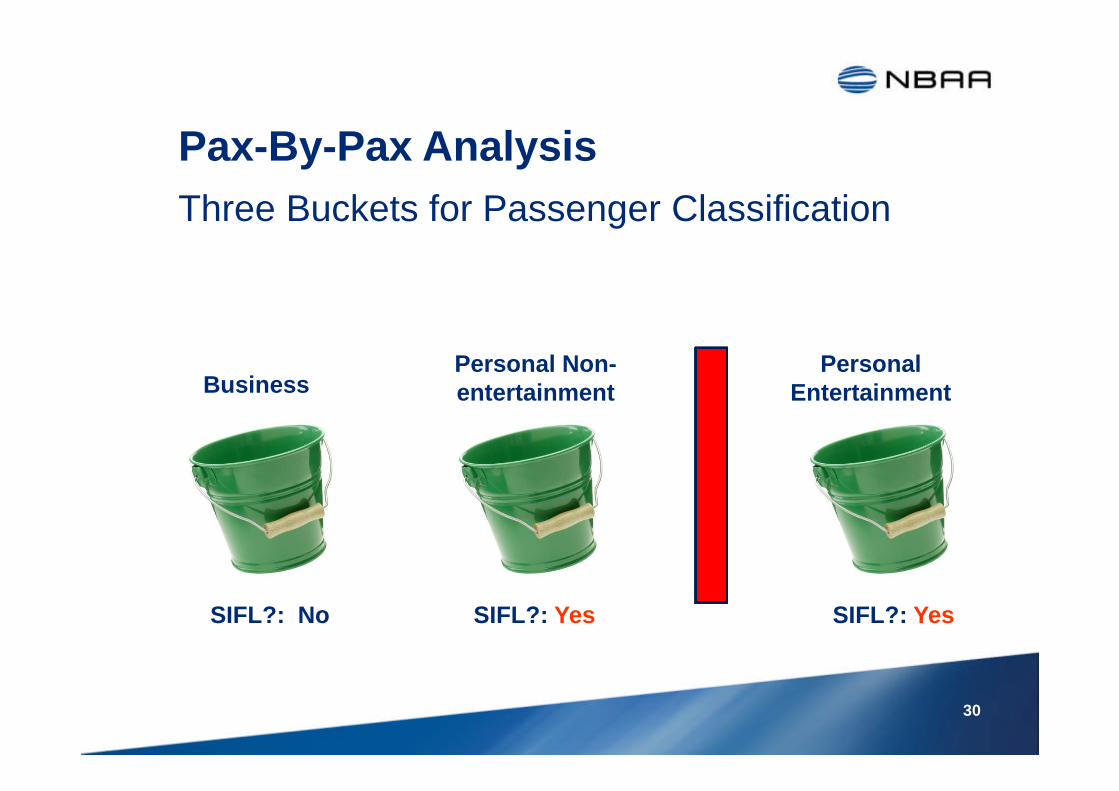

Pax-By-Pax Analysis

Three Buckets for Passenger Classification

30

Personal Non-entertainment

PersonalEntertainmentBusiness

SIFL?: No SIFL?: Yes SIFL?: Yes

Classification of Flights

• Business

– Includes “Business Entertainment”

– No SIFL income; Fully deductible

• Personal Non-entertainment

– Report SIFL income; Fully deductible

• Personal Entertainment

– Report SIFL income

– NOT deductible (except for SIFL amount)

Three Primary Buckets for Flights

31

Personal Entertainment Use Disallowance

• Expenses Included

– IRS views broadly

– Proposed regulations list many expenses to include –see NBAA Personal Use Handbook, page 24

– Tax Depreciation is included, straight line election?

– More than one aircraft? Aggregation of costs

– Clarification expected in final regulations

• e.g., is interest on aircraft loan payment disallowed?

Expenses Subject To Disallowance

32

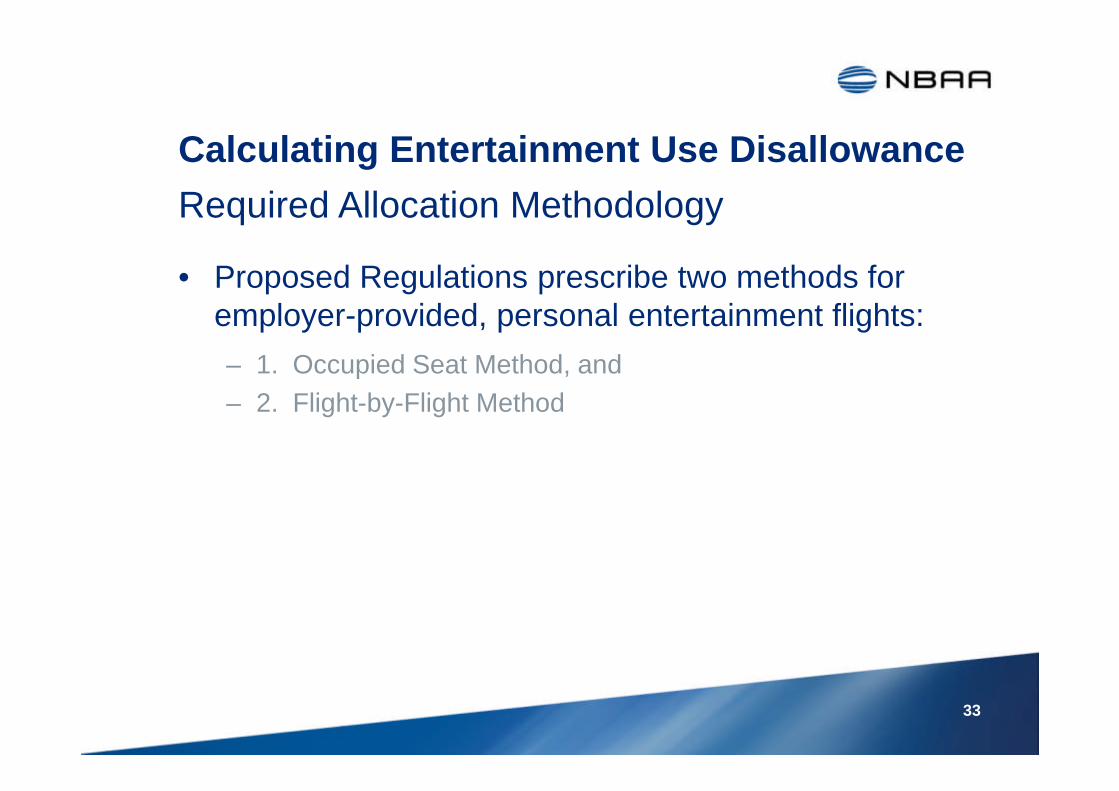

Calculating Entertainment Use Disallowance

• Proposed Regulations prescribe two methods foremployer-provided, personal entertainment flights:

– 1. Occupied Seat Method, and

– 2. Flight-by-Flight Method

Required Allocation Methodology

33

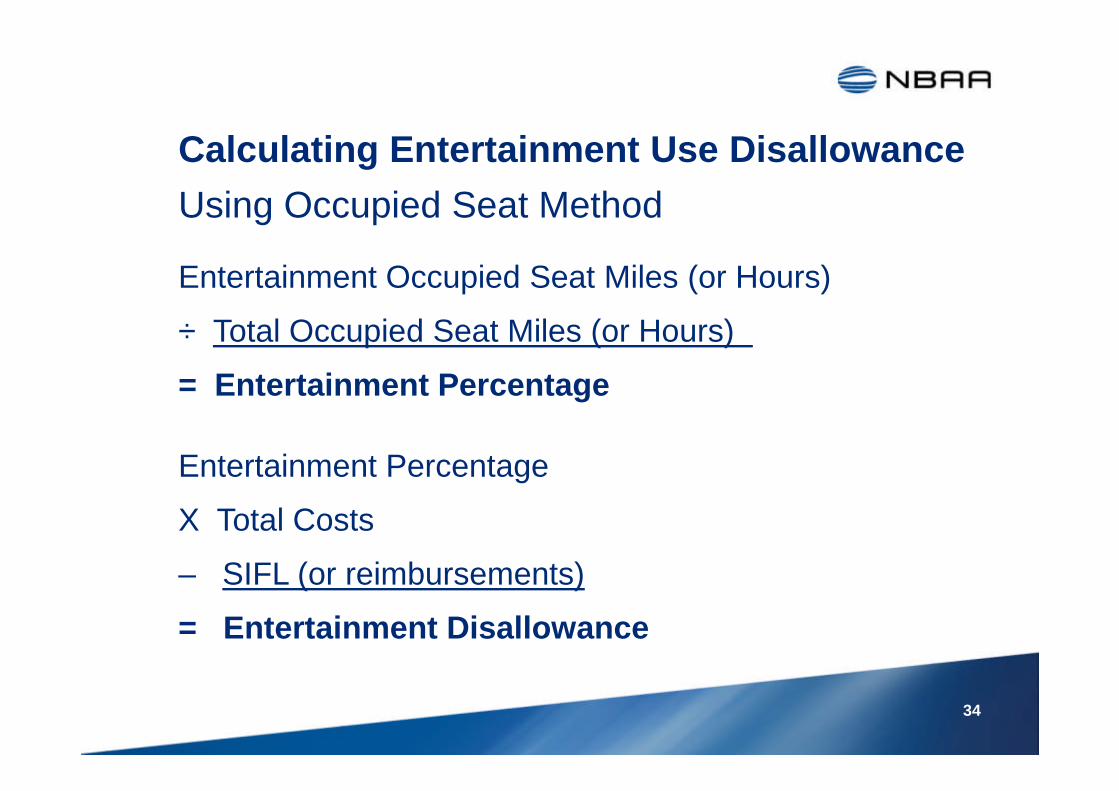

Calculating Entertainment Use Disallowance

Entertainment Occupied Seat Miles (or Hours)

÷ Total Occupied Seat Miles (or Hours)

= Entertainment Percentage

Entertainment Percentage

X Total Costs

– SIFL (or reimbursements)

= Entertainment Disallowance

Using Occupied Seat Method

34

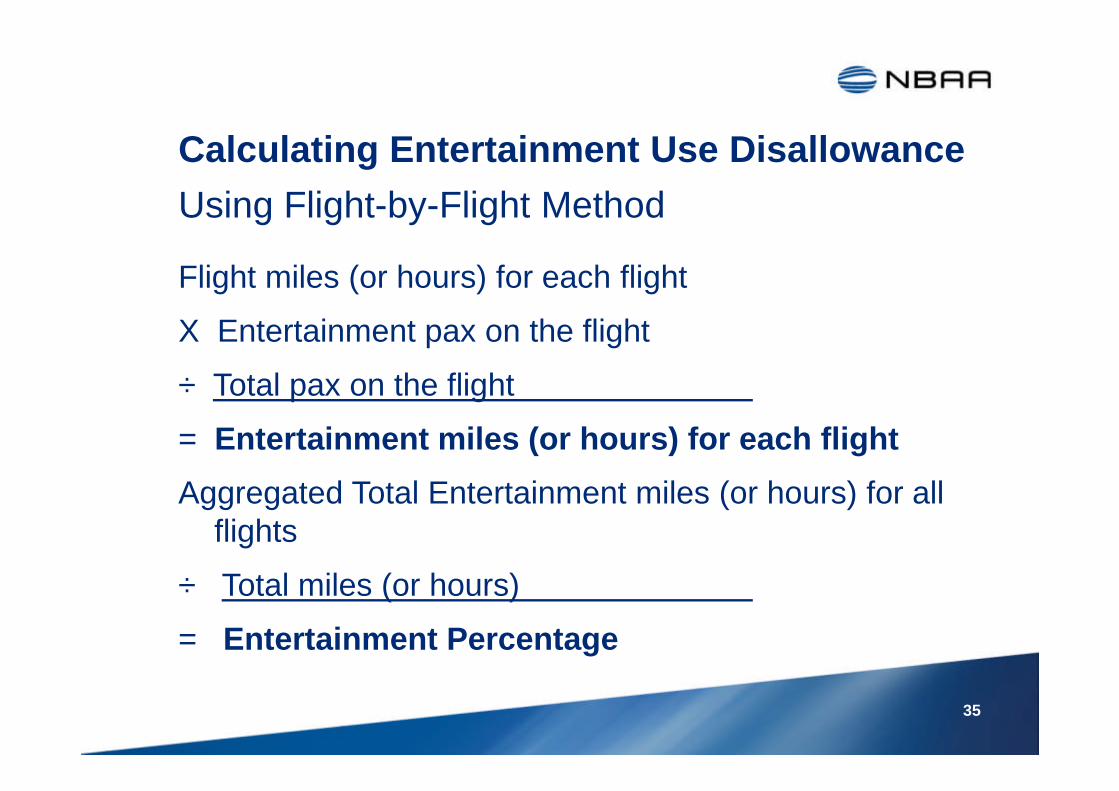

Calculating Entertainment Use Disallowance

Flight miles (or hours) for each flight

X Entertainment pax on the flight

÷ Total pax on the flight

= Entertainment miles (or hours) for each flight

Aggregated Total Entertainment miles (or hours) for allflights

÷ Total miles (or hours)

= Entertainment Percentage

Using Flight-by-Flight Method

35

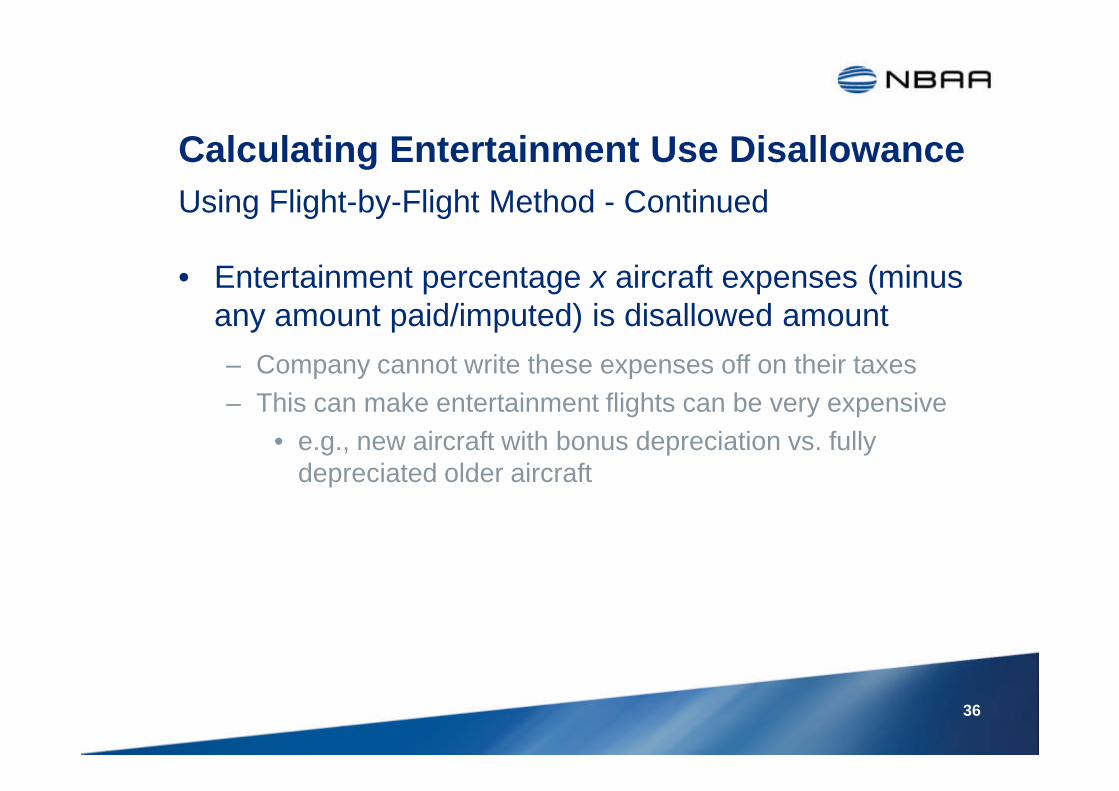

Calculating Entertainment Use Disallowance

• Entertainment percentage x aircraft expenses (minusany amount paid/imputed) is disallowed amount

– Company cannot write these expenses off on their taxes

– This can make entertainment flights can be very expensive

• e.g., new aircraft with bonus depreciation vs. fullydepreciated older aircraft

Using Flight-by-Flight Method - Continued

36

For More Information

• NBAA’s Aviation Taxes Web Site:

– http://www.NBAA.org/taxes• NBAA Personal Use Handbook

• Nichols Interpretation resource

• Historical SIFL Rates

• Personal Use Calculator

• NBAA’s Ops Service Group

– [email protected] or 202.783.9250

• NBAA Tax Forums / Tax Conference

– http://www.NBAA.org/seminars37

Personal Use Scenarios

Definitions

• CHQ = Company headquarters, aircraft home base

• CSL = Company Secondary Location

• EPR = Executive Primary Residence

• ESR = Executive Secondary Residence

• CUS = Customer Business Location

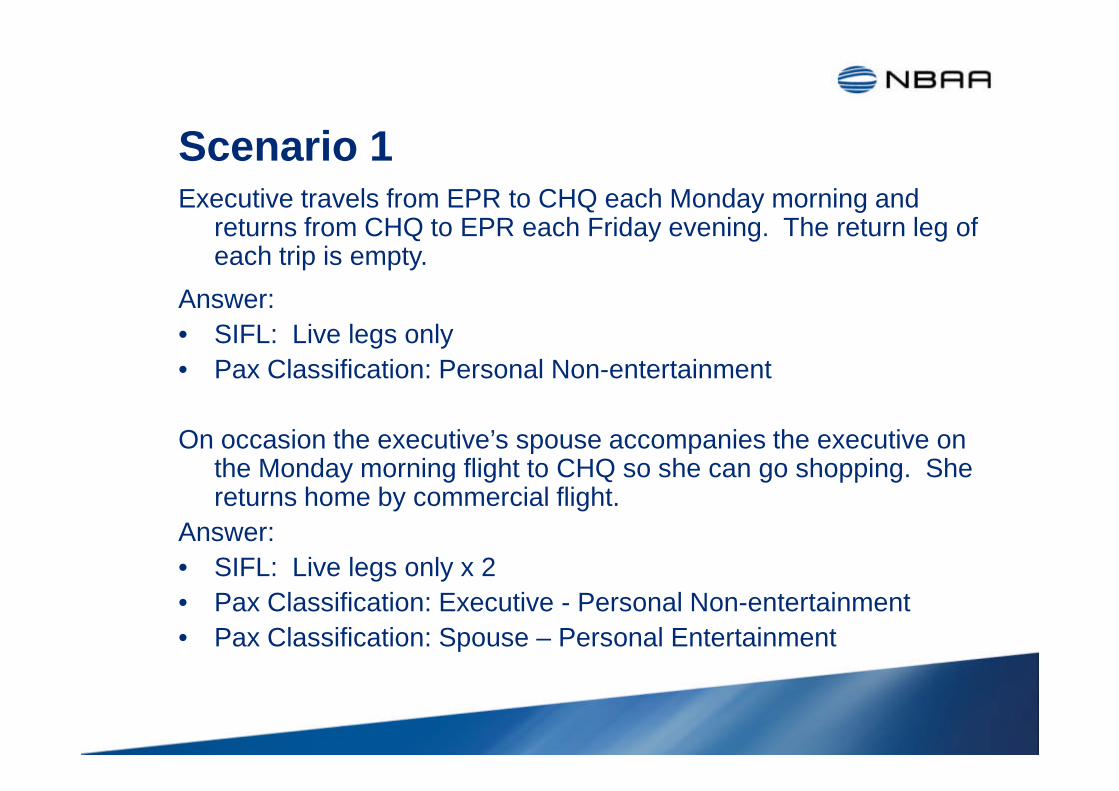

Scenario 1Executive travels from EPR to CHQ each Monday morning and

returns from CHQ to EPR each Friday evening. The return leg ofeach trip is empty.

Answer:

• SIFL: Live legs only

• Pax Classification: Personal Non-entertainment

On occasion the executive’s spouse accompanies the executive onthe Monday morning flight to CHQ so she can go shopping. Shereturns home by commercial flight.

Answer:

• SIFL: Live legs only x 2

• Pax Classification: Executive - Personal Non-entertainment

• Pax Classification: Spouse – Personal Entertainment

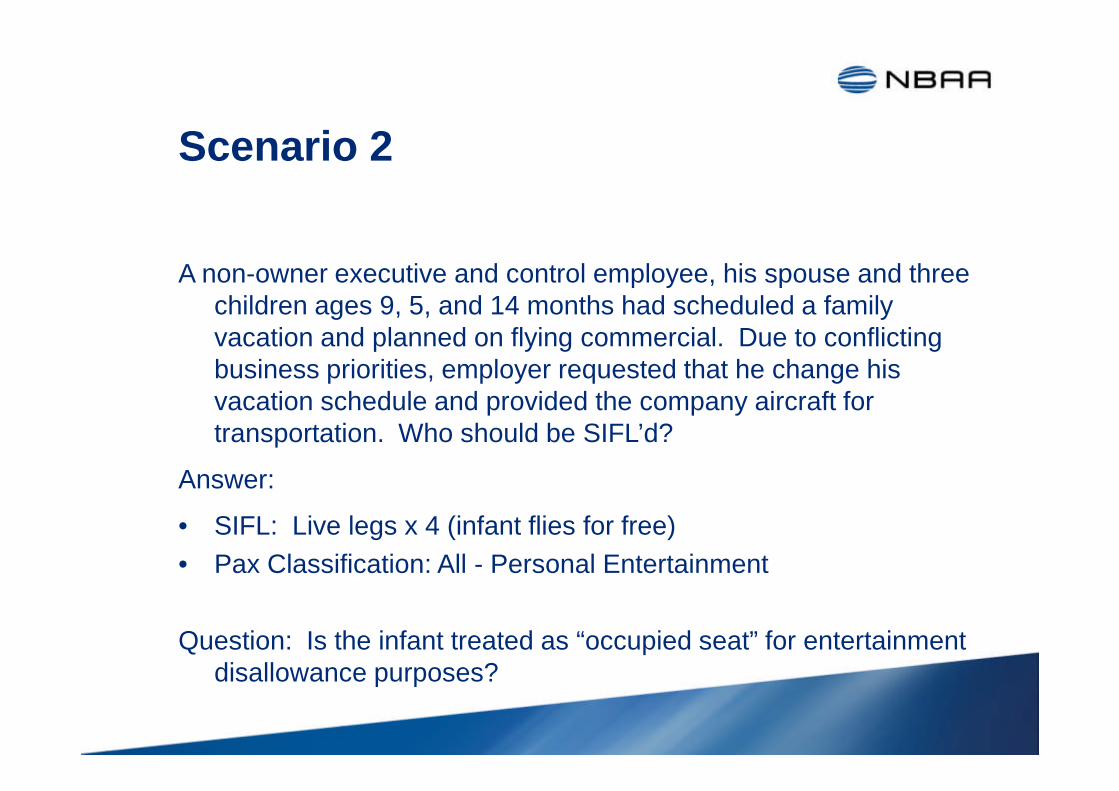

Scenario 2

A non-owner executive and control employee, his spouse and threechildren ages 9, 5, and 14 months had scheduled a familyvacation and planned on flying commercial. Due to conflictingbusiness priorities, employer requested that he change hisvacation schedule and provided the company aircraft fortransportation. Who should be SIFL’d?

Answer:

• SIFL: Live legs x 4 (infant flies for free)

• Pax Classification: All - Personal Entertainment

Question: Is the infant treated as “occupied seat” for entertainmentdisallowance purposes?

Scenario 3

Company dispatches its aircraft to bring outside directors to CHQfor a company board meeting. That evening a dinner isscheduled in a nearby restaurant and directors spouses, whilenot invited to the board meeting, are expected to attend thedinner. What is the SIFL treatment? What is the paxclassification for entertainment disallowance?

Answer:

• SIFL: Outside Director, No – clearly business travel

• SIFL: Spouse Yes, clearly personal travel

• Pax Classification:

– Director: Business

– Spouse: Depends on facts & circumstances

Scenario 4

The owner of Company A (the employer) and a senior executive ofCompany B via their long standing working relationship havebecome personal friends. Company A dispatches it aircraft onFriday afternoon to fetch the senior executive of B and hisspouse to CHQ for diner that evening and a round of golf onSaturday morning.

Scenario 5

The senior executive is a legal resident of a state other than CHQwhere he votes and maintains his primary residence. Theexecutive also maintains a ESR near CHQ. The Company’slargest customer location is very near the ESR such that theaircraft lands at the same airport for both destinations. Theexecutive (and sometimes his spouse) frequently travels to thisairport on Fridays where he conducts customer business andthen decides to spend the weekend at his EPR returning to CHQon Monday morning.

Scenario 6

Company B (a customer of Company A, the Employer) conducts anannual golf outing as a vendor appreciation event. Othercompeting vendors to Company A will also be invited. The entiresenior management team (5 individuals) of Company A and twoindividuals from the sales department (middle management) areinvited and decide to go. All seats on the aircraft will be filled.

Question: Are the employees of Company A on a business orpersonal trip? If personal, is it also entertainment?

45

Recommended