8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 1/122

Some important Service industries

in India

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 2/122

Hospitality Industry

Health Industry

Education & Entertainment services

Insurance Industry

Telecom IndustryBPO /ITES services

Financial services

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 3/122

Tourism & Hospitality Industryin India

A service sector growth industry

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 4/122

The Service Culture

The service culture focuses on servingand satisfying the customer

Empowers employees to solve customerproblems

Majority of many countries GDP isservice based

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 5/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 6/122

India: An emerging superpower

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 7/122

Indias GDP will exceed

Italys in 2020,

Frances in 2020

Germanys in 2025 and

Japans in 2035

Goldman Sachs Projections (US 2003 $ Billion)

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 8/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 9/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 10/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 11/122

Why these brands areLeaders?

Marriott

Disney

British Airways

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 12/122

Ritz-Carlton Leadership Center offers innovativeways to:

Increase employee retention and loyalty

Increase customer retention and loyalty

Achieve service excellence in yourindustry

Effectively drive your organizations

culture, philosophy, vision, and mission

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 13/122

The Invisible Organizationand System

A service organization management must

decide what they want the guest to seeand what they want to keep out of the

guests vision

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 14/122

Contact Personnel

Contact personnel have a direct impact on the satisfaction of customers

Characteristic of inseparability of customer and employee during service

delivery system

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 15/122

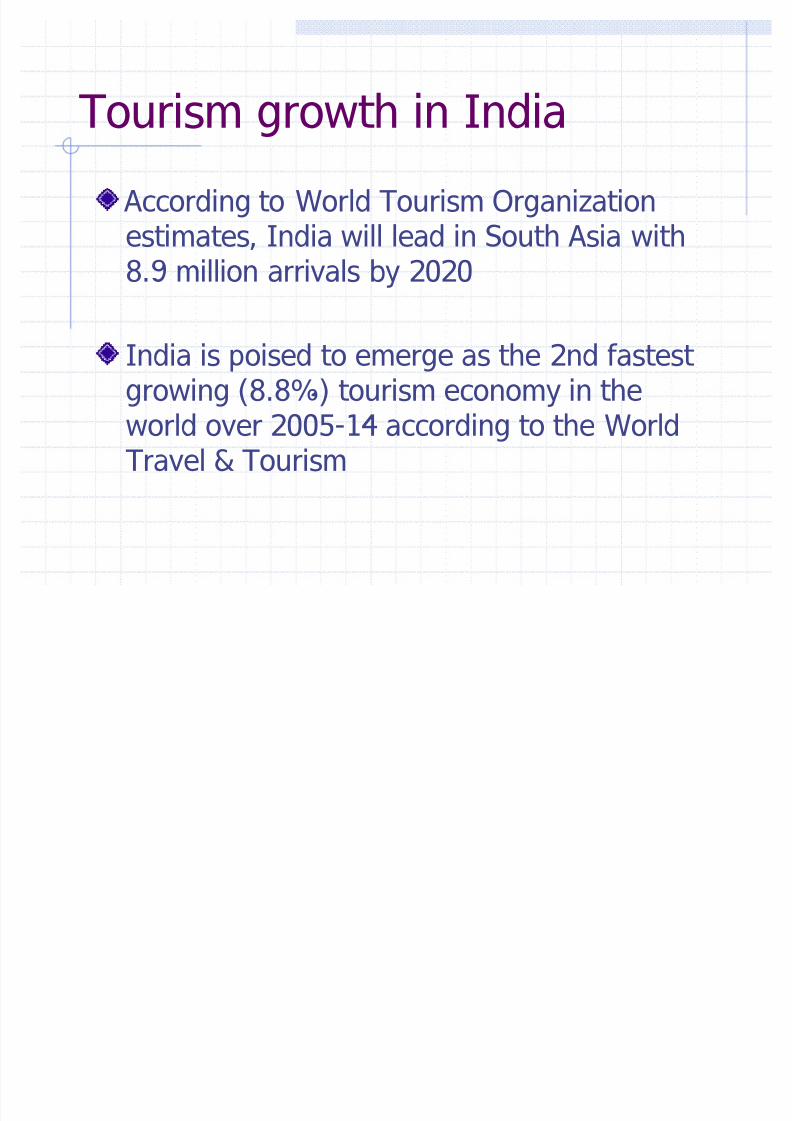

Tourism growth in India

According to World Tourism Organizationestimates, India will lead in South Asia with

8.9 million arrivals by 2020

India is poised to emerge as the 2nd fastest growing (8.8%) tourism economy in the

world over 2005-14 according to the WorldTravel & Tourism

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 16/122

Foreign earnings

There has been a growth of more than 13%in foreign tourist arrivals at 3.9 million during

2005, up from 3.4 million foreign tourists whovisited India during previous year.

Foreign exchange earnings from foreign

tourists were up by more than 20% at $5,730.86 million in 2005, up from $4,769million earned the previous year.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 17/122

Indian air travel to grow 20% each year for the next 5years

Government and private operators will invest $20 billionin aircraft and infrastructure over the next five years

Air India will be adding 68 aircraft to its present fleet,Indian Airlines 43 and private airlines around 275

By 2010, Indian airports will be handling between 90and 100 million passengers (59 million domestic & 35million international passengers)

Air travel and India

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 18/122

Tourist destinations

North East States such as Sikkim, Assam andNagaland have emerged as major players. The majorfocus in 2005 was to develop tourism infrastructure inthe region.

New States Uttaranchal attracted 14 million touristsand in 2004 witnessed a growth of 40% in 2005. Majorfocus on marketing to attract high spending tourists,initiatives to create world-class infrastructure.

Beautiful South Aggressive marketing has helpedachieve over 25% growth in tourism in southernstates. Andhra Pradesh and Karnataka are witnessingan upswing in foreign tourists.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 19/122

Forms of tourism

Cultural tourism & Round Trips covering thepopular circuits comprising of the Golden Triangle,Rajasthan, N. India & in South the well knowntemples, backwaters & beaches.

Mass tourism Goa is a tourism based economyand a leader in this sector, is all set to promotemass tourism. Goa also won the 2nd most popularwinter destination in UK.

Commonwealth Games 2010 the government is investing in infrastructure, to further developtourism in and around Delhi.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 20/122

An all-year round destination.

Throughout the world,India is perceived as aOctober to April winterdestination.

Marketing initiativesby both theGovernment and theprivate sector is nowsuccessfullyaddressing & changingthis perception.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 21/122

New Tourism Products

Monsoon magic - focus on months from April toOctober

Rural & village tourism - the tourism ministry is

laying special emphasis on infrastructure development in various rural destinations in India.

Medical tourism - the Indian Healthcare Deliverymarket is estimated at US$ 18.7 billion. The industry is

growing at about 13 per cent annually.

Luxury tourism e.g. Palace on Wheels, Palaces

Adventure tourism with emphasis on eco-tourism

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 22/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 23/122

Ecotourism in Kerala

There has been a majorgrowth in ecotourismthat is sustainable and

environmentally non-invasive.

Resorts are designedusing local labour forcesand local materials.

Energy sources aresustainable: cow dungand wood

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 24/122

The market for Ecotourism

Ecotourism tendsto be geared to a

young andwealthy market.

Activities aremarketed and lifestyle emphasised.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 25/122

Medical tourism in India

Medical care in the USA and private health care in UK is veryexpensive. India has well-trained doctors who will work for alower fee than they could expect abroad.

Medical tourism offers people the option of kneereplacements, hip replacements, heart care, cosmetic &dental surgery in India.

Hundreds of people have treatment abroad, saving them agreat deal of money in treatment costs.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 26/122

Managing Employees as Part of the Product

Employees are critical

Training and motivating employees toprovide good customer service isinternal marketing

A point-of-encounter is any point at which the employee encounters the

customer

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 27/122

Common Virtues RegardingService Quality

1. Customer obsessed

2. History of top management commitment toquality

3.H

igh service quality standards set

4. Monitor performance closely

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 28/122

Stress Advantages ofNonownership

The customer does not have ownershipof service product

Stress as a benefit

Rather than own and staff corporate

lodging, negotiate a rate with a hotel andpay for only what you use

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 29/122

Managing Employees asPart of the Product

Employees are critical

Training and motivating employees to providegood customer service is internal marketing

A point-of-encounter is any point at whichthe employee encounters the customer

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 30/122

Internal and Interactive

MarketingInternal marketing means the servicefirm must effectively train and

motivate customer contact employees

Interactive marketing means theperceived service quality dependsheavily upon the buyer-sellerinteraction during the serviceencounter

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 31/122

Bottom line

Managers do not control thequality of the product when the

product is a service . . . .The quality of the service is in aprecarious state

it is in the hands of the serviceworkers who produce and deliverit.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 32/122

Marketing Education: What is it?

What Does It Do?

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 33/122

Mission of MarketingEducation

The Mission of Marketing Education is toenable students to understand and apply

marketing, management, andentrepreneurial principles; to make rationaleconomic decisions; and to exhibit socialresponsibility in a global economy.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 34/122

The Marketing EducationCurriculum should:

Encourage students to think critically.

Stress the integration of and articulation

with academics. Be sequenced so that broad-based

understandings and skills provide afoundation to support advanced study of marketing.

Stress the importance of interpersonalskills in diverse societies.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 35/122

Enable students to acquire broad

understandings of and skills in marketing sothey can transfer their skills and knowledgebetween and among industries.

Enable students to understand and use

technology to perform marketing activities. Foster a realistic understanding of work.

Foster an understanding and appreciation of business ethics.

Utilize a variety of types of interactions withthe business community.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 36/122

Marketing EducationStandards

Marketing Education integrates academicconcepts and technology applicationsthroughout the curriculum Academic Concepts: The study of marketing

incorporates many academic understandingsincluding math, reading, writing, speaking,sociology, psychology, geography.

Technology Applications: The successfulimplementation of marketing requires the useof technology.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 37/122

Professional Development

Analyze employer expectations in thebusiness environment.

Identify employment opportunities inmarketing and business.

Utilize resources that can contribute toprofessional development.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 38/122

Marketing Education CurriculumPlanning Guide

The complete list of performanceindicators for the Foundations and the

Functions can be found in the national Marketing Education CurriculumPlanning Guide.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 39/122

INDIA IN THE NEW KNOWLEDGE ECONOMY

The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 40/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 41/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 42/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 43/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 44/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 45/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 46/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 47/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 48/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 49/122

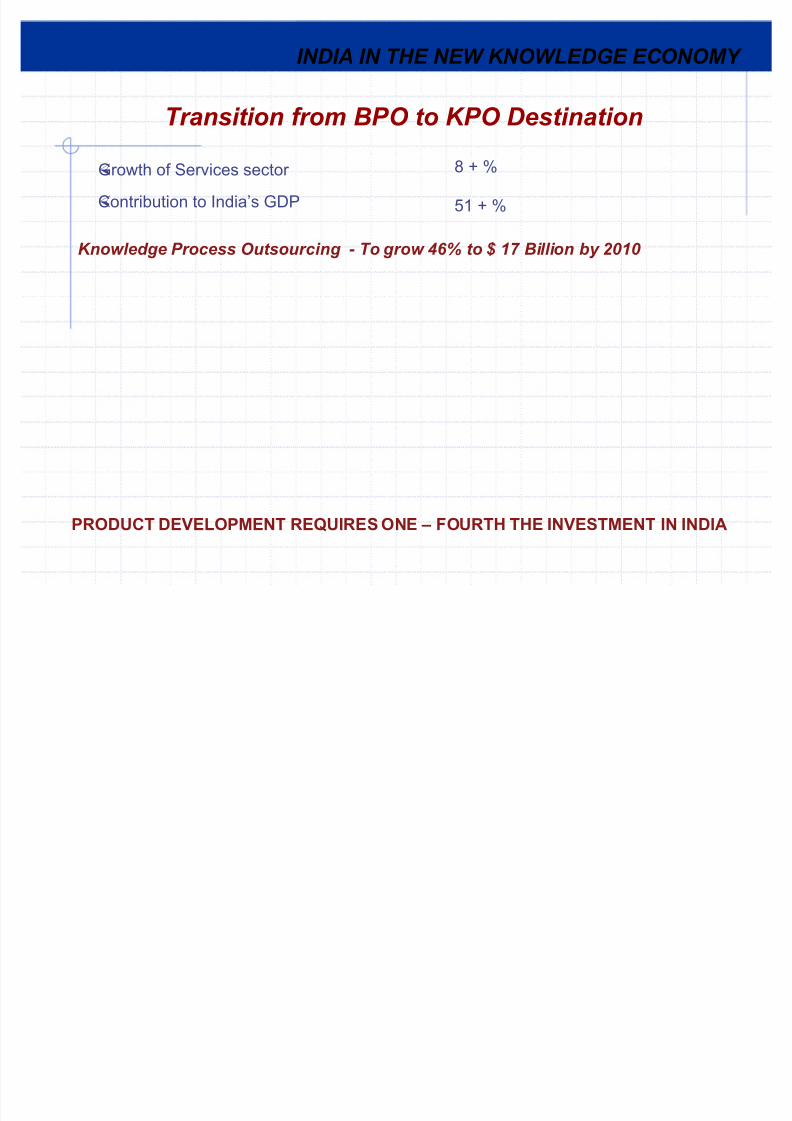

INDIA IN THE N EW K NO WLE DG E EC ONOMY

Transition from BP O to KP O Destination

Growth of Services sector

Contribution to India¶s GDP

8 + %

51 + %

Knowledge Process Ou tsou rcing - To grow 46% to $ 17 Billion by 2010

PRODUCT DEVELOPMENT REQUIRES ONE ± FOURTH THE INVESTMENT IN INDIA

INDIA IN THE NEW KNOWLEDGE ECONOMY

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 50/122

INDIA IN THE NEW KNOWLEDGE ECONOMY

Healthcare

Pharma & Biotechnology

Information & CommunicationTechnology (ICT)

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 51/122

Indian Healthcare : The Changing Scenario

Current Healthcare Landscape

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 52/122

Indian Healthcare : The Changing Scenario

INDIA SPENDS US $ 22.7 BILLION ON HEALTHCARE

3.7 19

22.7

5.2% ofGDP

TotalHealthc

are

Market

Pharmamarket

*

Healthcare

delivery

market

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 53/122

Indian Healthcare : The Changing Scenario

THE HEALTHCARE DELIVER Y SECTOR PLAYS ANIMPORTANT ROLE IN THE ECONOMY TODAY

Sector Direct employment Revenues/GDP

Million, 2000-2001 Per cent, 2000-2001

4.0

5.3

1.0

1.2

1.6

0.8

1.7

0.4

5.2

4.8

3.5

3.0

1.8

1.4

0.9

1.7

Healthcare

Education

Retail banking

Power

Railways

Telecom

Hotels, restaurants

IT

Healthcare is the

largest serviceindustry in termsof revenues and

the secondlargest after education in

terms of employment

By 2012, the sector could account for 7 to 8 per cent of GDP and provide

direct and indirect employment of 9 million

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 54/122

Indian Healthcare : The Changing Scenario

IN TERMS OF DELIVER Y, PRIVATE PROVIDERS CAPTURE 63%0F THE US $ 19 BILLION SPEND

6337

Government and publicemployers*

Healthcare provision, 2002

Per cent of total spending

Private providers(individual, charitableand for-profit)

100% = US $ 19 billion

* Including government spend (20%), public employers¶ spend (11%) and out-of-pocket spend at government providers (6%)

Source: McKinsey analysis

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 55/122

Indian Healthcare : The Changing Scenario

INDIA: AN EMERGING HEALTHCARE HUB

INDIAN HEALTHCARE CAPABILITY

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 56/122

Over 60,000 cardiac surgeriesdone per year with out comes atpar with international standards

Multi organ transplants like Renal,Liver, Heart, Bone MarrowTransplants, are successfullyperformed at one tenth the cost.

Patients from over

55countriestreated at Indian Hospitals.

INDIAN HEALTHCARE CAPABILITYFACT#1: Proven Indian healthcare system

INDIA HAS THE OPPOURTUNITY TO PROVIDE THE BEST OF

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 57/122

Ayurveda recognized as anofficial healthcare system inHungary.

Doctors in the west areincreasingly prescribing Indian

Systems of Medicine

More than 70% of theAmerican population prefer anatural approach to health

Americans are said to

spend around $25bn onnon-traditional medicaltherapies and products *

Ayurveda

Yoga

Siddha

India¶s Gift to the World

INDIA HAS THE OPPOURTUNITY TO PROVIDE THE BEST OFTHE WEST & EASTERN HEALTCARE SYSTEMS

Indian Systems Of Medicine ³ Staging a Comeback´

HEALTHCARE THE SUNRISE INDUSTRY

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 58/122

Physicians, Nurses, Medical Technicians and Other ScientificOccupations will Become Growth Industries to Rival the IT Sector

within the Next Decade

- India Vision 2020 Report

HEALTHCARE.THE SUNRISE INDUSTRY

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 59/122

HUGE GROWTH POTENTIAL ± TO GROW BETWEENUS $ 43 ± US $ 60 BILLION IN 2012

* With 6% GDP real growth per year

US $ IN BILLION at 2000-2001 prices

2001

Private

spending

Government

spending

ESTIMATE

2012

Scenario 1:Baselineincrease in

private spend

2012

Scenario 2:Baselinewith

insurance inmiddle class

2012

Scenario 3:Baseline withinsurance and

highgovernment

spending

19

43

51.0

60.0

3.76

15.24

8.0

8.0

17.0

35.0

43.043.0

KeyAssumption 1% GDP

GovernmentSpending 1% GDP 2% GDP

Indian Healthcare : The Changing Scenario

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 60/122

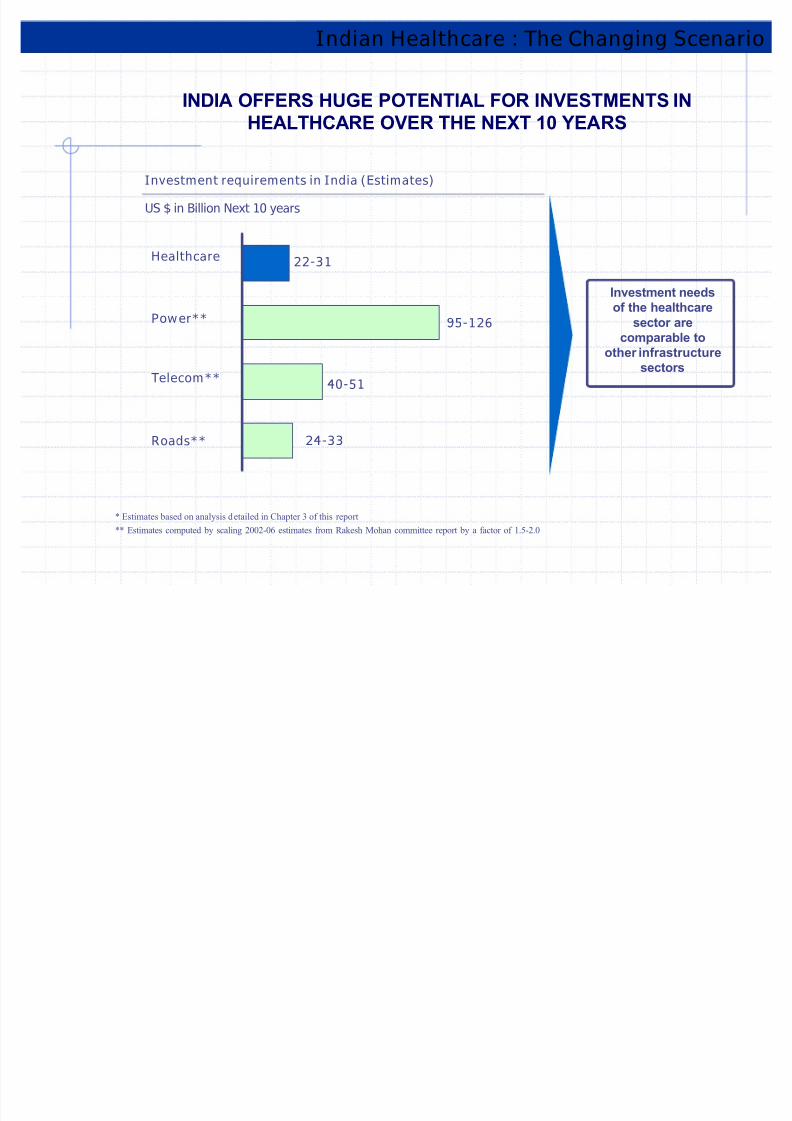

INDIA OFFERS HUGE POTENTIAL FOR INVESTMENTS INHEALTHCARE OVER THE NEXT 10 YEARS

Investment requirements in India (Estimates)

US $ in Billion Next 10 years

Healthcare

Power**

Telecom**

Roads**

22-31

24-33

40-51

95-126

* Estimates based on analysis detailed in Chapter 3 of this report

** Estimates computed by scaling 2002-06 estimates from Rakesh Mohan committee report by a factor of 1.5-2.0

Investment needsof the healthcare

sector arecomparable to

other infrastructuresectors

Indian Healthcare : The Changing Scenario

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 61/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 62/122

India¶s Growth Sectors -

Pharmaceuticals & Biotech

INDIA IN THE NEW KNOWLEDGE ECONOMY

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 63/122

The Indian Pharmaceutical Industry has practically achieved

Self sufficiency

&

Global recognition

as a

Low cost producer

of High-quality bulk drugs & formulations

KEY ACHIEVEMENTS

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 64/122

KEY ACHIEVEMENTS

India has the 2nd highestnumber of qualified doctors

in the world. Of every sixmedical doctors in the US,

one is Indian

700,000 science and

engineering graduates &1500 PhDs qualify annually.Over 15,000 scientists

Investigational New Drugstage costs about $100 to

150 million in US, butcosts only around $10 to

15 million in India

Indian companies are offeringcustom synthesis services at

30-50% cost savings comparedto global costs

While clinical trials cost

approximately $300 to350 million in US, theycost only about $25

million in India

India¶s huge populationand the prevalence of a

wide spectrum of diseaseconditions offer a wide

patient-resource for clinicaltrials

CHANGING FACE OF INDIAN PHARMA

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 65/122

CHANGING FACE OF INDIAN PHARMA

Players thinkinglocal

Players thinkingglobal

Top 5 Companies Sales & ExportR

evenues

Source: Company reports

Rank Company Sales ($ mn) Exports ($ mn) Exports %

1 Ranbaxy 969 736 76%

2 Cipla 400 163 41%3 Dr .Reddy's Lab 336 212 63%

4 Aurobindo Pharma 264 128 48%5 Lupin 210 92 44%

Pharmaceutical exportsincreased at a CAGR of 23%

during FY1995-FY2002

Indian pharma companies filed thelargest number of Drug Master Files(DMFs) for APIs and 23% of ANDAswith the USFDA during 2003

Ranbaxy acquired RPG Aventis,France; Wockhardt acquired CP Pharmaceuticals, UK; Zydus Cadilaacquired Alpharma, France

Export revenues now contributeover half the total revenues for

the Indian pharma majors

CHANGING FACE OF INDIAN PHARMA

CHANGING FACE OF INDIAN PHARMA

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 66/122

CHANGING FACE OF INDIAN PHARMA

MNC-DomesticCompetition

MNC-DomesticCollaboration

New Drug Research

Glaxo SmithKline'srecent R&D alliance withRanbaxy Laboratories

Clinical Trials

Novartis, Astra Zeneca andEli Lilly making India a

global hub for clinical trials

Co-marketing

Glaxo-Cipla,Wockhardt-Bayer,

Ranbaxy-Knoll tie-ups

In-licensing

Ranbaxy licensingagreement with KSB, UKfor marketing TransMID

Pharma - IT

Novartis processes drugsafety data and is designing

clinical development software

Local research

Astra Zeneca¶s $40 millionR&D facility in Bangalore

for TB drug discovery

COLLABORATION

CHANGING FACE OF INDIAN PHARMA

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 67/122

BIOTECHNOLOGY

INDIA IN THE NEW KNOWLEDGE ECONOMY

Market A Consistent Uptrend

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 68/122

Market - A Consistent Uptrend

2002-03

2010

25% growth in investment

70% growth in employment

74% growth in R&Dmanpower

10% of global industry

1 million skilled jobs

USD 5 billion annual

revenues

SOURCE FROM INDIA

GOING GLOBAL IN BIOTECH

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 69/122

S

Indias first geneticallyengineered vaccine costsless than half the price of

competing vaccines

Bio Agri -

India (2nd

largest producer of food) offerssignificant opportunities

to source products

Biogenerics -$25 billionbiological

products goingoff patent in2004. Indiancompaniesstrong in

biogenerics

Biocon was the first enzyme company globallyto receive ISO certification

in 1993

India: largest producer of Measles &

DTP vaccines. Vaccine exports toover 130 countries

Clinton Foundationsourcing HIV treatment from four firms - threeof which are from India

Shantha Biotech-

SHANVAC-B meets40% of the global

demand of HepatitisB vaccine.

The India Advantage

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 70/122

The India Advantage

Trained manpowerand knowledge base

Rich biodiversity Extensive clinical trialsopportunities

Excellent networkof research laboratories

Well-developedbase industries

INDIA IN THE NEW KNOWLEDGE ECONOMY

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 71/122

Information & Communication

Technology (ICT)

INDIA IN THE NEW KNOWLEDGE ECONOMY

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 72/122

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 73/122

INSUR ANCE SECTOR

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 74/122

Insurance, in law and economics, is a form of risk management

primarily used to hedge against the risk of a contingent loss.

Insurance is defined as the equitable transfer of the risk of a potentialloss, from one entity to another, in exchange for a premium.

Insurance rate is a factor used to determine the amount, called the

premium, to be charged for a certain amount of insurance coverage

Risk management, the practice of appraising and controlling risk, has

evolved as a discrete field of study and practice

What is INSURANCE?

Evolution India

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 75/122

Evolution India

1818 - Oriental Life Insurance Company ± 1st Insurance Company.

1870 - Bombay Mutual Life Assurance Society ± 1st Life Insurance

Company.

1912 - The Indian Life Assurance Companies Act enacted the 1st Law to

Regulate the Life Insurance Business.

1928 - The Indian Insurance Companies Act enacted to enable the

government to collect statistical information about both life & non-lifeinsurance businesses.

Contd«..

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 76/122

1938: Earlier legislation consolidated & amended the Insurance Act with theobjective of protecting the interests of the insuring public.

1956: 245 Indian & foreign insurers & provident societies are taken over by the central government & nationalized.

LIC formed by an Act of Parliament, viz. LIC Act, 1956, with a capitalcontribution of Rs. 5 crore from the Government of India.

The first General Insurance Company established in the year 1850 inCalcutta by the British.

T f I

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 77/122

Types of Insurance

Life insurance

Non - Life Insurance

(general insurance)

Property (eg.Builders risk insurance)

Aviation(eg.Private aircraft insurance)

Marine (eg. Marine hull insurance)

Miscellaneous (eg.Purchase insurance)

Insurance Sector Reforms

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 78/122

In 1993, Malhotra Committee - headed by former Finance Secretary & RBI

Governor R.N. Malhotra.

Objective - to create more efficient & competitive financial system.

Key recommendations of the reform;

1.Structure: ± a. government stake 50% in insurance companies.

2.Competition:

Private Companies with a minimum paid up capital of Rs.1bn should be

allowed to enter the sector. No Company should deal in both life and general insurance through a

single entity.

Foreign companies may be allowed to enter the industry in collaborationwith the domestic companies.

Regulatory Body:

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 79/122

g y y

The insurance act should be changed.

An insurance regulatory body should be set up.

Controller of insurance-a part of the Finance Ministry ± should be made

independent.

Investments :

Mandatory Investments of LIC Life Fund in government securities to be

reduced from 75% to 50%.

GIC and its subsidiaries are not to hold more than 5% in any company.

Customer Service:

LIC should pay interest on delay on payment beyond 30 days.

Insurance companies must be encouraged to set up unit link pension plans.

THE GLOBAL PLAYERS

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 80/122

TH E GLOBAL PLAYERS

in Life insurance

AVIVA

American International Group, Inc. American International Group, Inc.

(AIG) (AIG)

Prudential PLC Prudential PLC

A i Lif I

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 81/122

Aviva is the fifth-largest insurance group of the world & the biggest in theUK.

They are among the leading providers of life & pensions products in

Europe.

Aviva has a 35 million-customer base worldwide and more than £332 billion

of assets under management.

The mission of Aviva is: ³to provide prosperity and peace of mind for our

customers´.

Aviva Life Insurance

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 82/122

Aviva was the first foreign insurance company in India to set up itsrepresentative office in 1995.

In India Aviva has a joint venture with Dabur.

Aviva has 112 Branches in India.

Aviva products are available in 392 towns & cities across India.

Annual sales turnover is over Rs.12 billion.

AVIVA INDIA

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 83/122

Provides value for money

Flexibility

Transparency.

It has been among the 1st to

introduce the more modern Unit

Linked Products in the market.

[eg.whole life insurance(life long)]

Good products to offer.

Reasons for Growth

American International Group Inc

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 84/122

AIG is the world's leading international insurance & financial

services org, with operations in more than 130 countries & jurisdictions.

In the United States, AIG companies are the largest underwritersof commercial & industrial insurance.

AIG companies are the largest underwriters. AIG also has one of the

largest U.S. retirement savings.

AIG American General is a top-ranked life insurer.

A major focus of AIG's insurance business model is the concept of an

American International Group, Inc.(AIG)

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 85/122

Tata AIG General Insurance company is a joint venture between the

Tata Group & American International Group, Inc

The Tata AIG General Insurance companys offers a complete range of insurance solutions

The Tata AIG s product innovation

The rural difference

The enhancement of distribution channels

TATA AIG

R f G h

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 86/122

Innovative Offers,

Customer-Centric Products,

Increasing Awareness Levels of

Consumers Enhanced Service Standards,

Reaching out to the customerthrough a number of distribution

and communications channels

Providing advice to thecustomer

Reasons for Growth

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 87/122

Prudential PLC is an international financial services company.

It has a product range of personal banking, insurance, pensions andretail investments, to institutional fund management and propertyinvestments .

In the UK Prudential is a leading life & pensions provider witharound 7 million customers.

It is Asias leading European life insurer with life and fundmanagement operations in 12 countries serving some seven millioncustomers.

PRUDENTIAL PLC Est.1848

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 88/122

ICICI Prudential Life Insurance Company is a joint venture between ICICI

Bank & Prudential PLC.

I

CI

CI

Prudential was amongst the first private sector insurance companies to begin operations in December 2000.

The company has a network of about 56,000 advisors; as well as 7 banc

assurance and 150 corporate agent tie-ups.

For the past four years, ICICI Prudential has retained its position as the No. 1

private life insurer in the country.

ICICI PRUDENTIAL

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 89/122

Lucrative offers

High standard service

Customer-centric products

Good communication

techniques

Use of customer feedback

in improvement of offers.

Reasons for Growth

LIFE INSURANCE CORPORATION

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 90/122

LIFE INSUR ANCE CORPOR ATION

FORMATION:

Insurance corporation LIC was formed in September 1956 by an act of parliament

LIC was formed with the capital contribution of 5 crores from the govt. of India and has the sole mandate of conducting life insurance business inIndia.

Before the formation of LIC there where 245 Indian and foreign insurers inIndia.

OBJECTIVES:

To maximize mobilization of peoples savings by making insurance linked

saving adequately attractive.

To spread life insurance much more widely and in particularly in rural area,

providing them with insurance at reasonable price and adequate finance

cover.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 91/122

LIC has come a long way since its nationalization in 1956 over 40 yearslater in 1997

LIC had grown from Rs. 3.78 billion of new business in 1957 to Rs 555.5

billion

The rural India accounting for around 40% of the business.

In 1997, LIC had spread to the farthest corners of the country with anextensive network of over 8 lakh agents, 2048 branches(1370cities), 100Divisional office, 7 Zonal offices and 1 Central office.

LIC has branch offices in U.K., Mauritius, & Fiji. In U.K .

G ROWTH:

Reasons for Growth

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 92/122

³LIC IS TO BE IDENTIFIED AS AN EPITOME OF CUSTOMER

CARE AND CONCERN I N THE ENTIRE SERVICE I NDUSTRY´

-Chairman G N BAJPAI

The IT initiative

The company, has invested over Rs. 400 crore in technology up gradation.

LIC now plans to increase the MAN to 33 more Cities by the end of the year

so that they have 4 I cities on the WAN. That will make it the biggest

network in the whole country, including that of the railways

LIC¶s Game Plan:

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 93/122

THE CUSTOMER FOCUS INITIATIVE

Premium payment facility through internet, smart card, credit card

Tie up with banks for payment of premium through ATM¶S

Market focus initiative

Launching schemes for the rural areas designed to meet their

requirement. Derive 60% of its new business from rural areas

The corporation will soon go in for restructuring and is talking withleading management institutes such as the IIM of Lucknow for brushingup its marketing skills, IIM Ahmedabad for fine-tuning its investmentskills & IIM Bangalore for polishing its IT skills.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 94/122

The Sub-Prime Crisis Effect

The property/casualty and life insurance industry will not be materiallyaffected by credit market developments.

Because both by law and by the nature of their business, insurers generallylimit themselves to the low-risk end of the investing universe.

A small number of P/C insurers provide insurance on the credit-worthinesson mortgage-backed securities.

The loss ratios for the credit insurance products of these companies arelikely to rise due to increased delinquencies and defaults.

Contd..

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 95/122

At least half of these companies are parts of larger financial servicesgroups, so that the experience of this line of business is, for them, a small

part of their overall operations.

As such, it is much too early to estimate the dimensions of the claimsexperience that may emerge from the recent credit market developments.

Of course some companies will be affected more than others, and the depth

and length of the credit market ³challenges´ might be more adverse than

many experts currently foresee .

But for now, these developments do not appear poised to adversely affect

the insurance industry¶s ability to pay its claims and continue to have

financially successful operations.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 96/122

INDIAN SCENARIO OFINSUR ANCE

The 15 private players together saw their business grow 32 % to Rs 848 crore

with a market share of 28 44 %

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 97/122

with a market share of 28.44 %.

I nsurers Premium[Rs.Cr.]

ICICI Prudential 271.00

Bajaj Allianz 124.00

SBI Life 90.00

HDFC Standard 70.00

Max New York Life 69.00

Tata AIG 48.00

Aviva 39.00

Reliance Life 33.00

y Birla Sunlife 28.00

y Kotak Mahindra Old

Mutual 26.00

y ING Vysya 22.00

y Met Life 19.00

y Shriram Life 4.50

y Sahara Life 1.70

y Bharti Axa Life 0.72

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 98/122

ICICI Prudential - premium income rising 84.5 % to Rs 271 crore - 9.08% marketshare.

Bajaj Allianz - 15 % in business - collected Rs 124 crore - 4.16 % market share.

general insurance industry grew 16 % in April,

New India - With 8 % growth in premium collection at Rs 651 crore, retained itsnumber one slot by cornering 20.72 % of market share.

ICICI Lombard - new premium 36 % to Rs 448 crore - a market share of 14.28 %

ICICI Lombard - the second-largest non-life insurance player.

Oriental Insurance premium collection at Rs 413 crore & a market of 13.16 %.

United India - 3 % growth in business at Rs 407 crore & 12.97 % of the market.

³Indian Insurance Industry: New Avenues for Growth 2012´,

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 99/122

The potential of the Indian insurance industry is huge. HOW???

«.. It has an annual growth rate of 15-20% &

«..the largest number of life insurance policies in force.

Total value of the Indian insurance market (2004-05) is at Rs. 450 billion

(US$10 billion).

Insurance & Banking Services¶ contribution to the country's gross domestic

product (GDP) is 7%

The funds available with the state-owned Life Insurance Corporation (LIC) for

investments are 8% of GDP.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 100/122

The year 1999 saw a revolution in the Indian insurance sector------the ending of

government monopoly -----the passage of the I nsurance Regulatory and

Development Authority ( I RDA) Bill

³A foreign partner can hold 26% equity in an insurance company, but there was a proposal to increase this limit to 49%.

Foreign investments of Rs. 8.7 billion have poured into the Indian market & 21private companies have been granted licenses.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 101/122

LIC PRIVATE PLAYERS

Growth ² 21.87% Growth ² 129%Earned ² Rs.197.86 billion[04-05]

Sold ² 2.4 billion policies

Earned ² Rs.55.57 billion[04-05]

Against Rs.24.29 billion [03-04]

Market share ²

87.04% 78.07% 75%

Market share ²

13% 22% 24%

India's insurance sector to see 500 per cent growth by 2010: Study

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 102/122

India's insurance sector - 500 % growth over the next three years -60 billion-dollar industry by 2010

India's more than one billion people are uninsured, the study by the Associated Chambers of Commerce and Industry (Assocham) said.

'A large part of rural India is still untapped due to poor distribution, largedistances & high costs relative to returns, said Assocham president

Anil K Agarwal

He said the study had revealed that rural & semi-urban India wouldcontribute 35 billion dollars to the Indian insurance industry by2010.

The study added that the urban sector insurance was estimated to reach 25 billion dollars by 2010, life insurance 15 billion and non- lifeinsurance 10 billion dollars.

Source: Business News

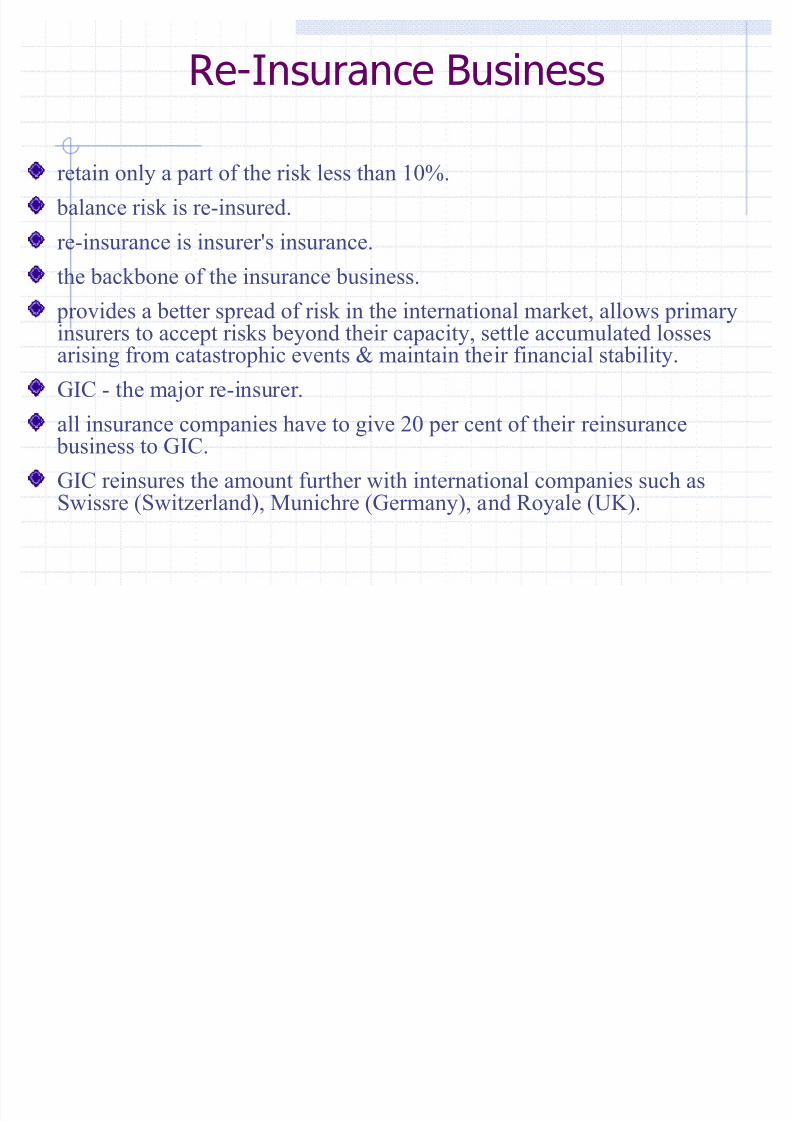

Re-Insurance Business

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 103/122

Re Insurance Business

retain only a part of the risk less than 10%.

balance risk is re-insured.

re-insurance is insurer's insurance.

the backbone of the insurance business.

provides a better spread of risk in the international market, allows primaryinsurers to accept risks beyond their capacity, settle accumulated lossesarising from catastrophic events & maintain their financial stability.

GIC - the major re-insurer.

all insurance companies have to give 20 per cent of their reinsurance business to GIC.

GIC reinsures the amount further with international companies such asSwissre (Switzerland), Munichre (Germany), and Royale (UK).

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 104/122

Careers

Jobs in insurance involve helping individuals and business

manage risk to protect themselves from catastrophic losses

and to anticipate potential risk problems.

Insurance brokers and agents

Claims handlers [are responsible for investigating incidents and paying claims. They decide the extent and validity of the claim]

Underwriters [assess risks and decide whether to accept applicationsfor insurance cover - and on what terms]

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 105/122

Insurance can be summed up as

´Praying for the best ««being PREPARED for the

WORESTµ.

Conclusion

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 106/122

.Where Do I Keep My Money?.Evaluating Financial Services

.Banks, Yesterday and Today

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 107/122

Where Do I Keep My Money?

Overview

The functions of banks

The cost of alternative financial services

The stability of banks

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 108/122

PLACES TO SAVE MONEY

Would you save your money in any of theseplaces? Why? Why not? Can you think of otherplaces to save money?

Bed & Mattress Cookie Jar

Pillow Wallet Money Belt Small House Safe

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 109/122

ALTERNATIVE FINANCIAL SERVICES

Check-Cashing Services

Check-Deferrals, Cash Advances, Payday Loans

Pawn Shops

Rapid Tax Refunds

Rent-to-Own

Other Financial Services

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 110/122

Overview

Formal and informal financial services

Costs of alternative financial services and

average bank accounts Advantages of establishing a banking relationship

Evaluating Financial Services

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 111/122

INFORMALFINANCIALSERVICES

Payday lenders Check cashing services Rent-to-own stores Pawn shops Title lenders Loans from family/friends

Cultural savings clubs Remittances offered through

nonfinancial institutions

FORMALFINANCIALSERVICES

Accounts Credit cards Loans Investment vehicles Direct deposit Wire transfers/ remittances

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 112/122

ADVANTAGES OF ESTABLISHING ABANKING RELATIONSHIP

Nearly everyone needs a bank account to help manage his

or her day-to-day money.

Bank accounts can help you to: Pay bills Manage your money Receive money

Send money to a friend or family member Keep your money secure Start building wealth Earn interest

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 113/122

Banks, Yesterday

and TodayOverview

The many traditional financial services provided

by a bank

Other expanded financial services provided by a

bank

The impact of banks throughout the community

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 114/122

EXPANDEDSERVICESOF BANKS

Insurance Sales Small Business Advising

and Loans Investments Credit Cards

Remittances

TRADITIONALSERVICESOF BANKS

Checking Accounts Savings Accounts CDs (Certificates of

Deposit) Savings Bonds

Loans Car Home Personal

Safe Deposit Boxes

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 115/122

FINANCIAL SERVICESMODERNIZATION ACT (1999)

Transformed the banking industry. Eliminated many

restrictions among companies in the securities,banking, and insurance industries.

Results? Banks may offer some insurance and investment

services.

Investment and insurance companies may offersome traditional banking services. Investments arenot insured by FDIC.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 116/122

SOME COMMUNITY-RELATEDSERVICES OF BANKS

Bank employees mentor students in areas of basic financial skills.

Bank employees serve on communityorganizations boards of directors.

Banks provide scholarships to students goinginto the banking profession.

Banks fund affordable housing construction.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 117/122

Do you know?

New survey results from Demandwareindicate that retailers are not prepared

to meet the demands of smart consumers who use multiple, web-enabled touch points to interact withbrands. The data highlights a gap

between the touch points that retailerscurrently offer and the ways consumersexpect to interact with brands now and

in the future.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 118/122

More women are launching online

shopping ventures and taking on high-profile roles at such companies,especially sites devoted to fashion, food

and other segments where shoppersare overwhelmingly female, this storysays. Sites including Gilt Groupe, Rent the Runway, and One Kings Lane were

all founded by women, and suchventures make up a rare niche forwomen in the male-dominated

technology industry.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 119/122

McCormick and Schmicks RestaurantsGains New Insight into Dining Trends

and Financial Performance with IBMCognos Express ( BI & planningsolutions )

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 120/122

Online sales of groceries and consumerpackaged goods are on track to hit $25

billion by 2014, more than double theexisting level, according to Nielsen. Thecompany partnered with MyWebGrocerto launch a service that tracks online

grocery sales.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 121/122

France's Carrefour is developing aninformation technology platform to

facilitate online shopping in India.Subhodip Bandyopadhyay, a director at Carrefour, said the platform is beingcreated while "keeping in mind the

Indian IT growth story and tech-savvybusiness establishments all over India,particularly in National Capital Region.

8/3/2019 Service Industries

http://slidepdf.com/reader/full/service-industries 122/122

Recommended