Security Analysts and Conflicts of Interest

Jay R. Ritter

Cordell Professor of Finance

University of Florida

Security analysts who work for brokerage firms that do investment banking, trade stocks (brokerage), and provide research on these stocks are known as “sell-side” analysts

I will focus exclusively on equity analysts

What do security analysts do?

Public pronouncements– Buy/sell recommendations– Target prices– Earnings forecasts– Written reports

What do security analysts do?

Private (telephone calls)– Summarizing information– Passing along private (inside) information

Sell-side security analysts are like professors

We don’t make money by selling our research papers to PBFJ and other journals

We get paid indirectly through a higher salary if we publish influential research papers

• Security analysts are paid indirectly if they attract

- investment banking deals

- trading commissions that include soft dollars

• Soft dollars are investor commissions paid for services in excess of pure trade execution.

Conflicts of interest

• Need to get information from management• Need to appease investors long in stock• Need to attract banking mandates

What do practitioners think?

“If an analyst is negative on you, you are not going to hand their bank a significant role in your stock issuance, that’s for sure. That person becomes the mouthpiece to the investment community for your firm.”

Amylin Pharmaceuticals CFO Mark Foletta, as quoted in Investment Dealer’s Digest.

These conflicts create an incentive to issue optimistic recommendations

During the TMT (Tech, Media, and Telecom) bubble of the late 1990s, these conflicts of interest became severe

Where were the regulators?

Recent years have seen major changes

The commissions per share paid by institutional investors in the US have collapsed in the last seven years from an average of about 4.5 cents per share to about 1.5 cents per share

This is a weighted average of ECNs, “crossing networks”, and full-service brokers

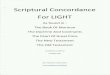

Proportion of buy, hold, and sell recommendations from U.S. sell-side analysts, 2000-2004. Source: Reuters Estimates

0

10

20

30

40

50

60

70

80

90

100

July 00

Jan 01

July 01

Jan 02

July 02

Jan 03

July 03

Jan 04

July 04

Per

Cen

t

BUY

HOLD

SELL

The Financial Services Authority (FSA) in the UK has encouraged unbundling

The salaries of sell-side analysts have been falling

Many sell-side analysts have moved to the buy-side

In Europe and North America, junior analyst jobs have been outsourced to India

More research is being offered on Asian stocks

What are the most important qualities of a good analyst?

a) Accurate earnings forecastsb) Timely buy and sell recommendationsc) Insightful written reportsd) Setting up meetings with managemente) Accessibility/responsiveness of phone callsf) Industry knowledge

Private value of informationInvestors are willing to pay for information only when it is valuable

Value can be measured as the ability to generate positive abnormal returns

The private value of public information is zero

The private value of private information can be considerable

This distinction is at the heart of the conflicts of interest problem

Academic research

Grossman and Stiglitz (1980 AER) “The Impossibility of Informationally Efficient Markets”

--There is an equilibrium degree of inefficiency

UnderwritersAffiliated: Managing syndicate members

– Lead underwriter(s)– Co-managers

Unaffiliated– Non-managing syndicate members– All others

Are conflicts of interest different for affiliated and unaffiliated analysts?

– Incumbent’s advantage– Currying favor

Bradley, Jordan, and Ritter (2008 RFS) “Analyst Behavior Following IPOs: The ‘Bubble Period’ Evidence”

Academic research focuses on public, measurable info like EPS forecasts

Institutional investors don’t care about this info

But are these measurable variables correlated with useful telephone calls?

A good book

Confessions of a Wall Street Analyst (2006)

by Dan Reingold with Jennifer Reingold

Dan Reingold was an II all-star analyst

who covered telecoms from 1984-2003

Summary Analyst conflicts are difficult to regulate

because of the economics of information

Information has different public and private value, so there is an externality

Academics are able to measure the public pronouncements, which institutional investors don’t care about

Recommended