SAP® Financial Consolidation, starter kit for financial and regulatory reporting for banking, SP5 Configuration Overview (Appendix)

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

2

Copyright © 2014 SAP® BusinessObjects™. All rights reserved. SAP BusinessObjects and its logos, BusinessObjects, Crystal Reports®, SAP BusinessObjects Rapid Mart™, SAP BusinessObjects Data Insight™, SAP BusinessObjects Desktop Intelligence™, SAP BusinessObjects Rapid Marts®, SAP BusinessObjects Watchlist Security™, SAP BusinessObjects Web Intelligence®, and Xcelsius® are trademarks or registered trademarks of Business Objects, an SAP company and/or affiliated companies in the United States and/or other countries. SAP® is a registered trademark of SAP AG in Germany and/or other countries. All other names mentioned herein may be trademarks of their respective owners.

2014-10-01 Legal Disclaimer No part of this starter kit may be reproduced or transmitted in any form or for any purpose without the express permission of SAP AG. The information contained herein may be changed without prior notice.

Some software products marketed by SAP AG and its distributors contain proprietary software components of other software vendors.

The information in this starter kit is proprietary to SAP. No part of this starter kit’s content may be reproduced, copied, or transmitted in any form or for any purpose without the express prior permission of SAP AG. This starter kit is not subject to your license agreement or any other agreement with SAP. This starter kit contains only intended content, and pre-customized elements of the SAP® product and is not intended to be binding upon SAP to any particular course of business, product strategy, and/or development. Please note that this starter kit is subject to change and may be changed by SAP at any time without notice. SAP assumes no responsibility for errors or omissions in this starter kit. SAP does not warrant the accuracy or completeness of the information, text, pre-configured elements, or other items contained within this starter kit.

SAP DOES NOT PROVIDE LEGAL, FINANCIAL OR ACCOUNTING ADVICE OR SERVICES.

SAP WILL NOT BE RESPONSIBLE FOR ANY NONCOMPLIANCE OR ADVERSE RESULTS AS A RESULT OF YOUR USE OR RELIANCE ON THE STARTER KIT.

THIS STARTER KIT IS PROVIDED WITHOUT A WARRANTY OF ANY KIND, EITHER EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO THE IMPLIED WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, OR NON-INFRINGEMENT.

SAP SHALL HAVE NO LIABILITY FOR DAMAGES OF ANY KIND INCLUDING WITHOUT LIMITATION DIRECT, SPECIAL, INDIRECT, OR CONSEQUENTIAL DAMAGES THAT MAY RESULT FROM THE USE OF THIS STARTER KIT. THIS LIMITATION SHALL NOT APPLY IN CASES OF INTENT OR GROSS NEGLIGENCE.

The statutory liability for personal injury and defective products (under German law) is not affected. SAP has no control over the use of pre-customized elements contained in this starter kit and does not endorse your use of the starter kit nor provide any warranty whatsoever relating to third-party use of the starter kit.

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

3

TABLE OF CONTENTS

A. LIST OF FINANCIAL ACCOUNTS ........................................................................................................ 4

1. Assets .................................................................................................................................................... 4

2. Equity ..................................................................................................................................................... 6

3. Liabilities ............................................................................................................................................... 8

4. Income statement ................................................................................................................................. 9

B. LIST OF PACKAGE SCHEDULES ...................................................................................................... 13

C. LIST OF FLOWS .................................................................................................................................. 22

1. List of accounting flows ..................................................................................................................... 22

2. List of flows for IFRS notes ............................................................................................................... 22

3. List of FINREP flows ........................................................................................................................... 23

D. PACKAGE CONTROLS ....................................................................................................................... 25

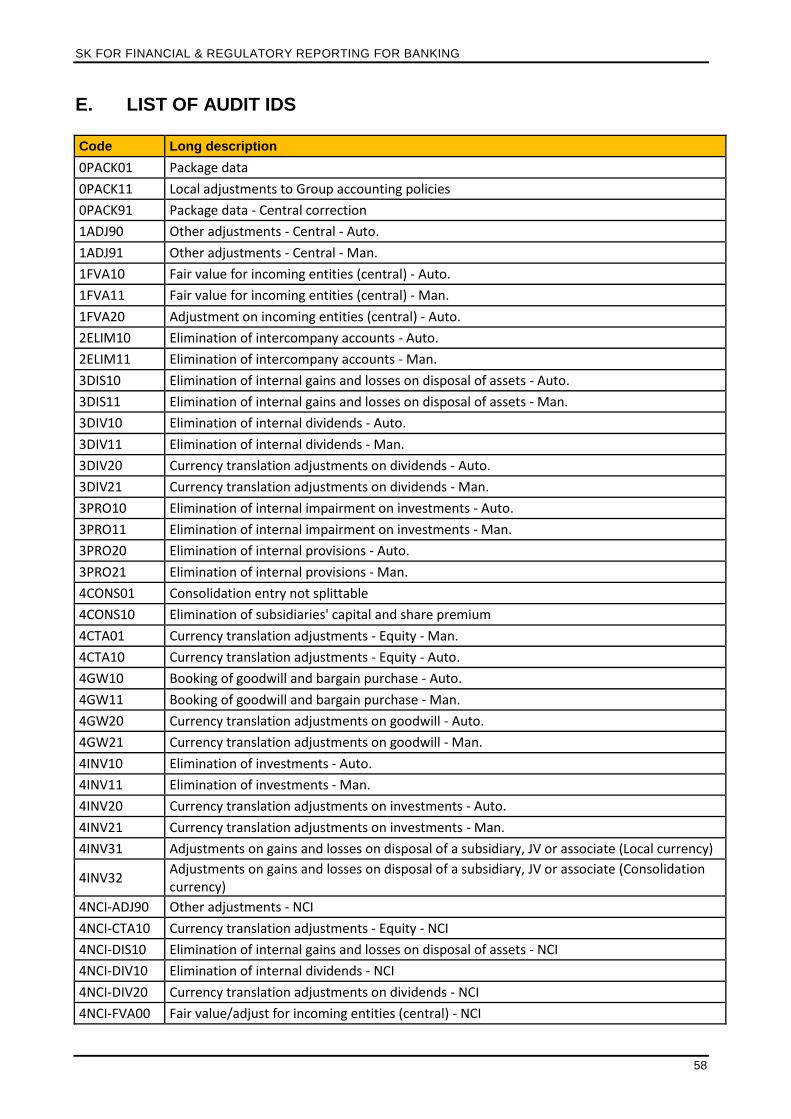

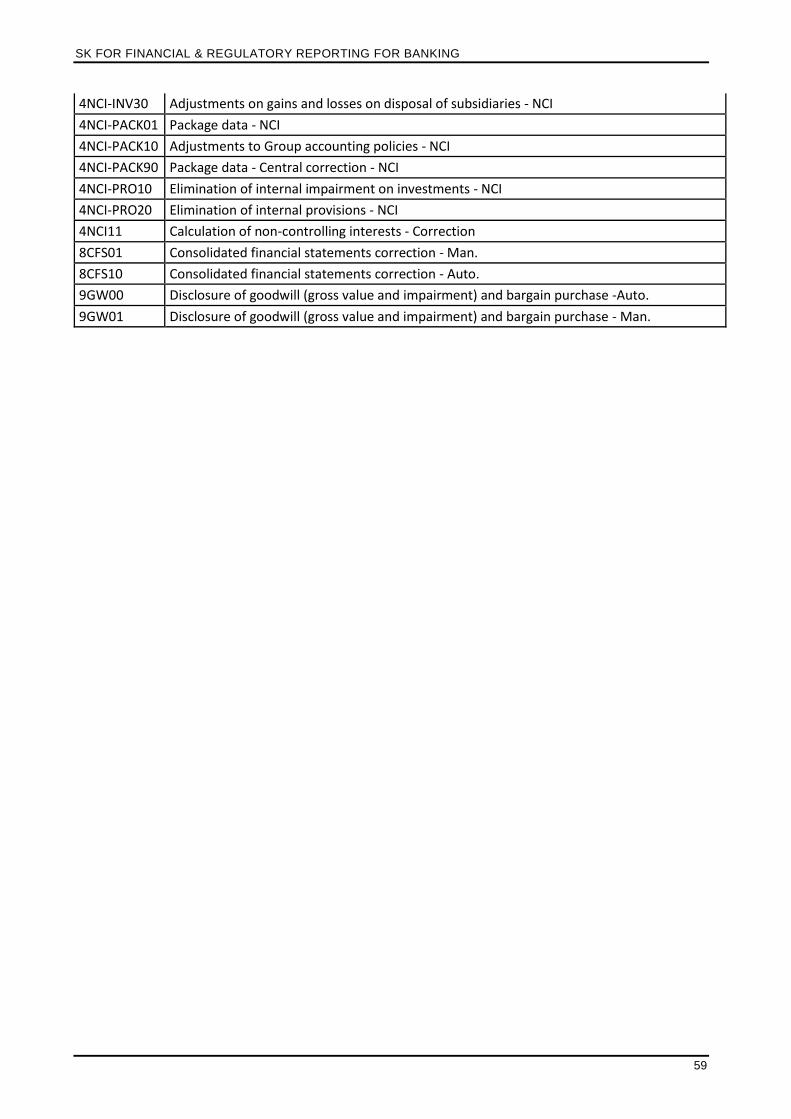

E. LIST OF AUDIT IDS ............................................................................................................................. 58

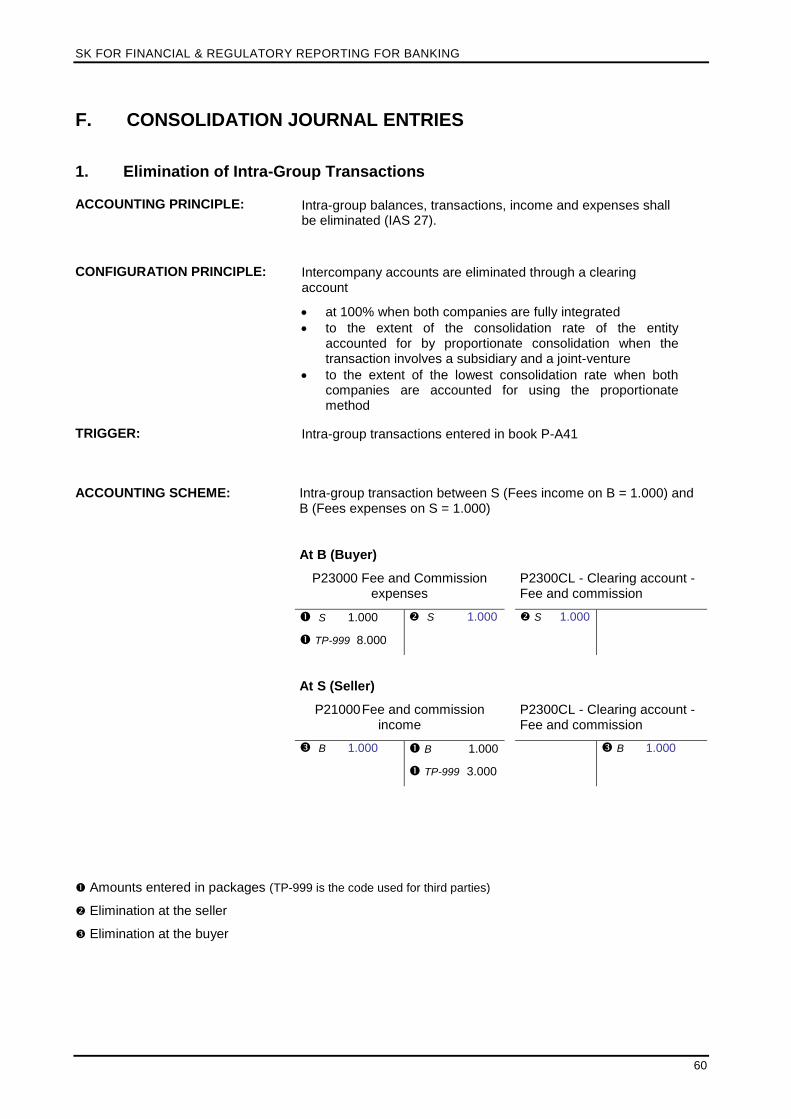

F. CONSOLIDATION JOURNAL ENTRIES............................................................................................. 60

1. Elimination of Intra-Group Transactions .......................................................................................... 60

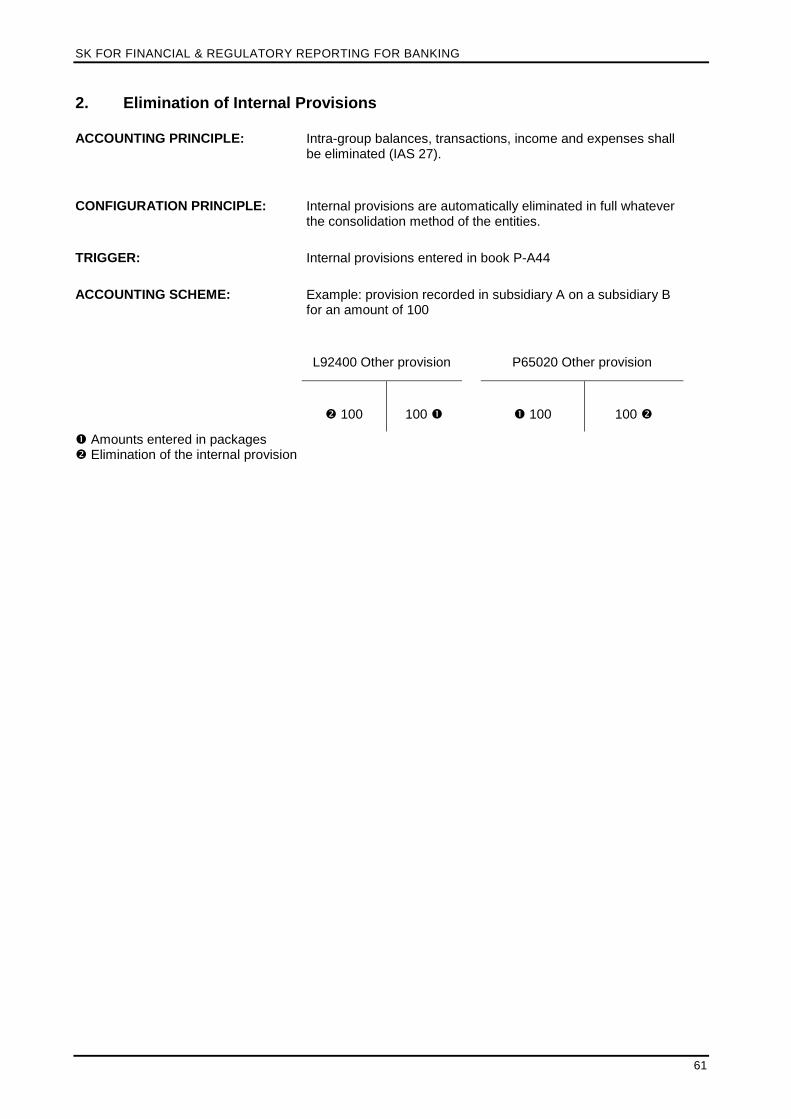

2. Elimination of Internal Provisions ..................................................................................................... 61

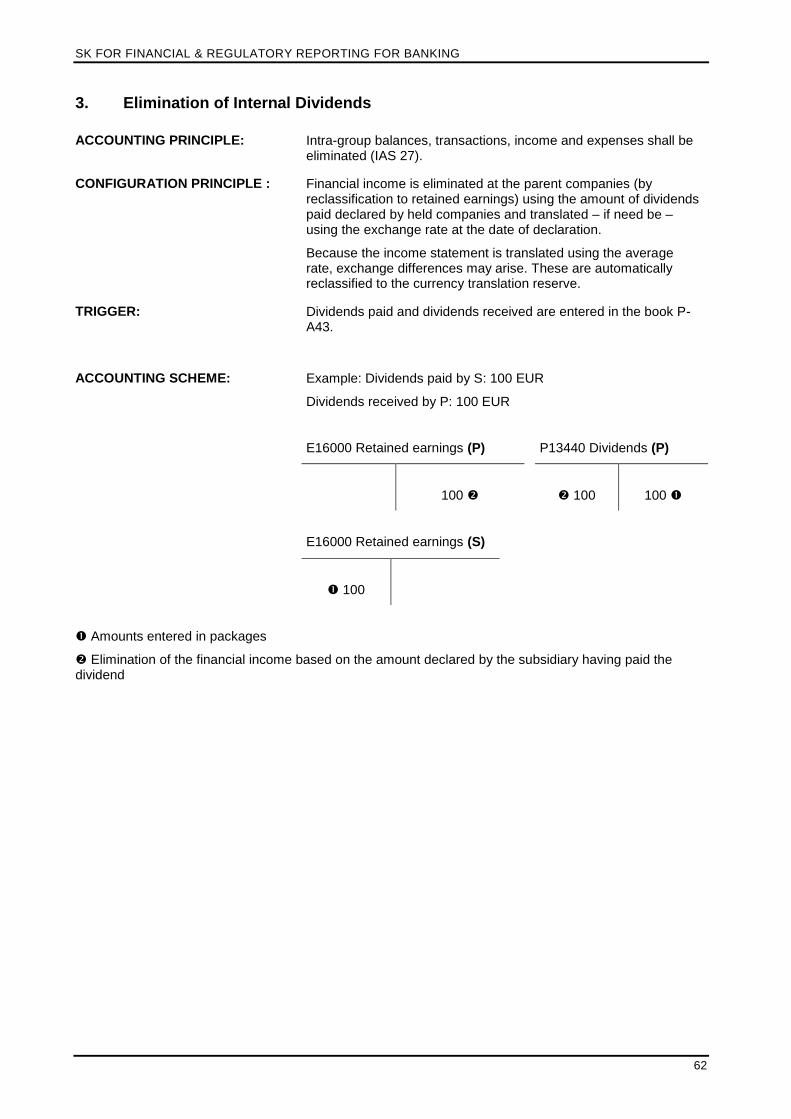

3. Elimination of Internal Dividends ...................................................................................................... 62

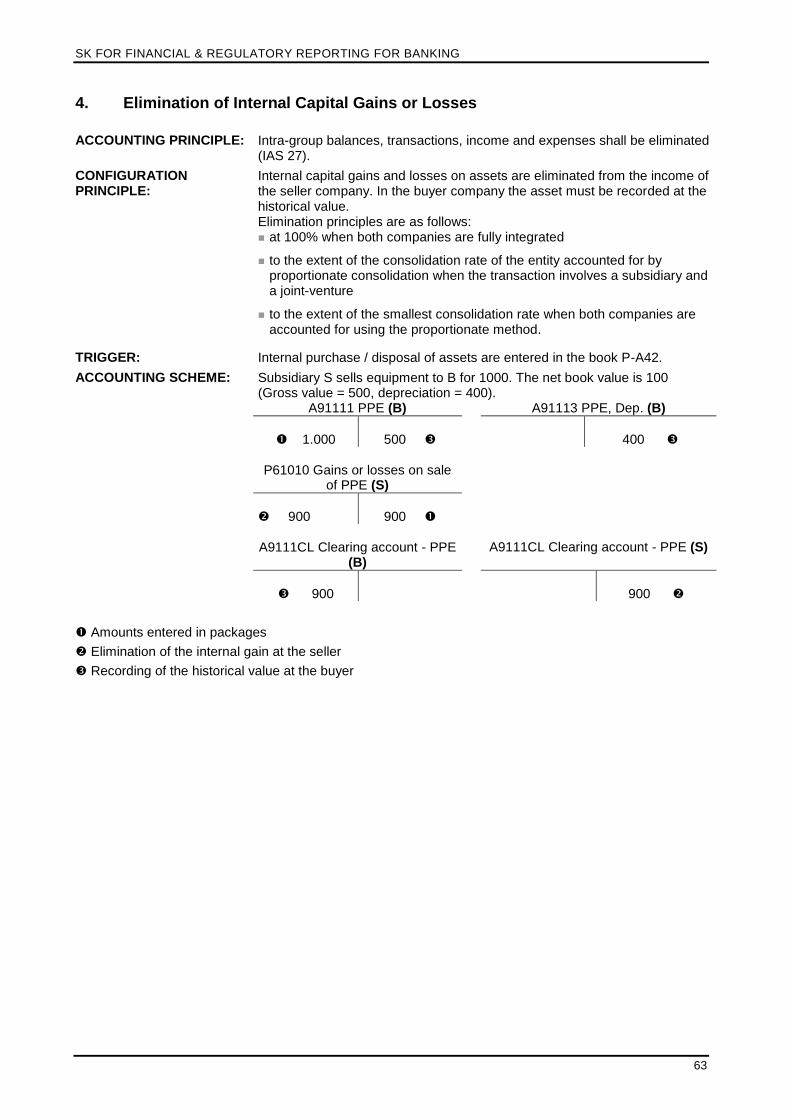

4. Elimination of Internal Capital Gains or Losses .............................................................................. 63

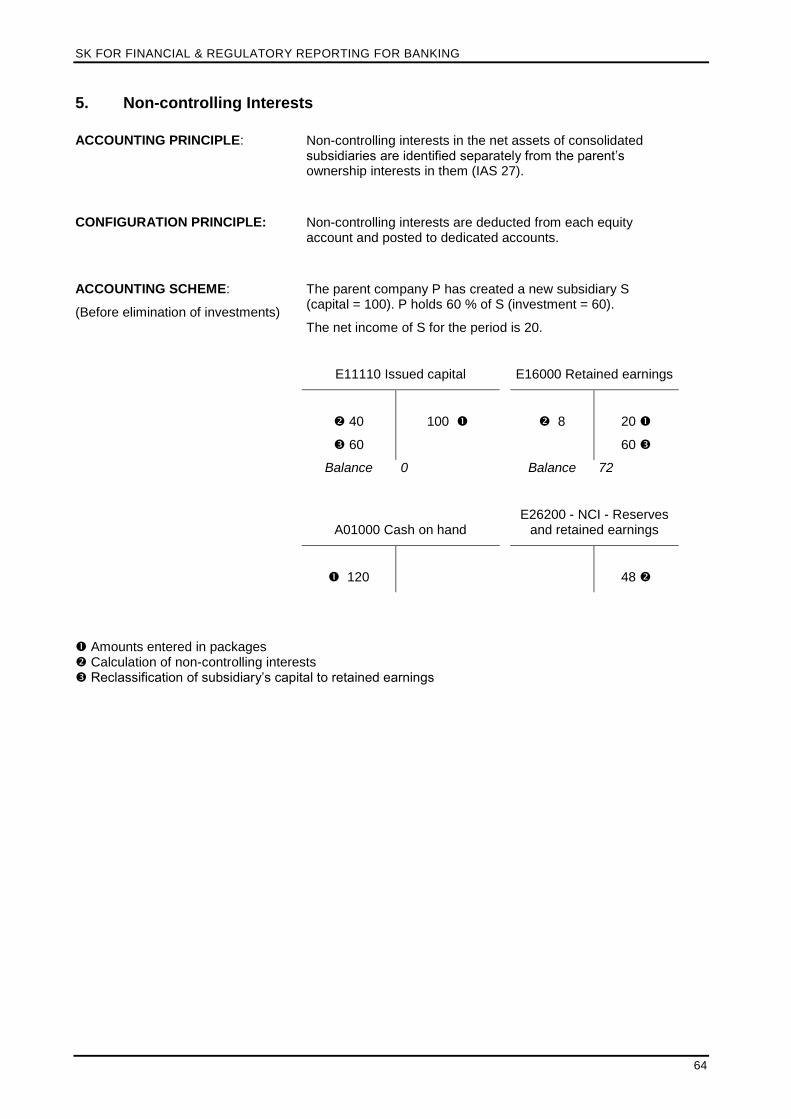

5. Non-controlling Interests ................................................................................................................... 64

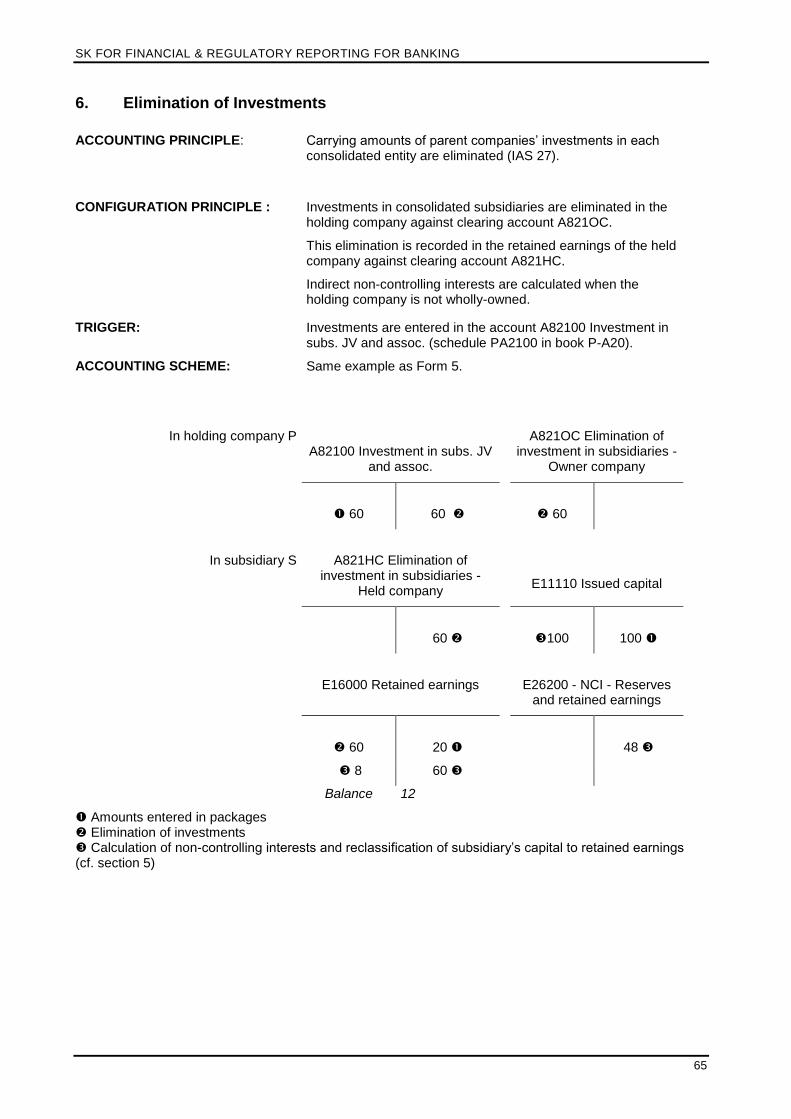

6. Elimination of Investments ................................................................................................................ 65

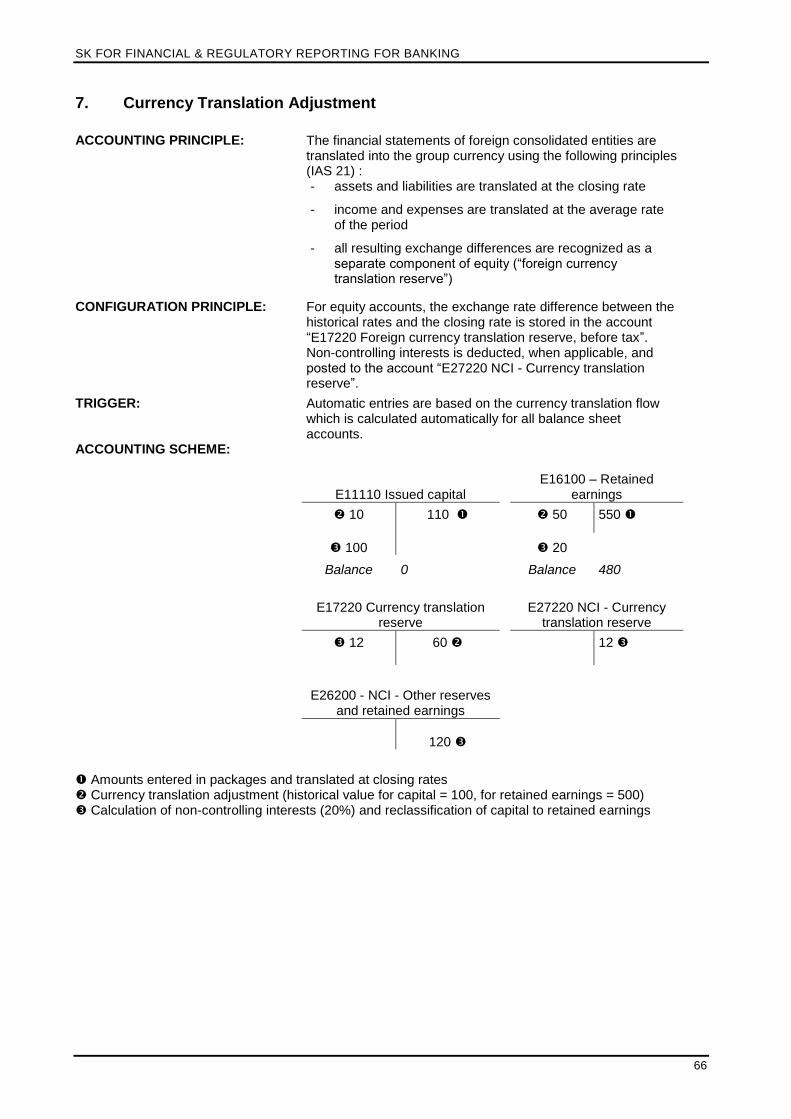

7. Currency Translation Adjustment ..................................................................................................... 66

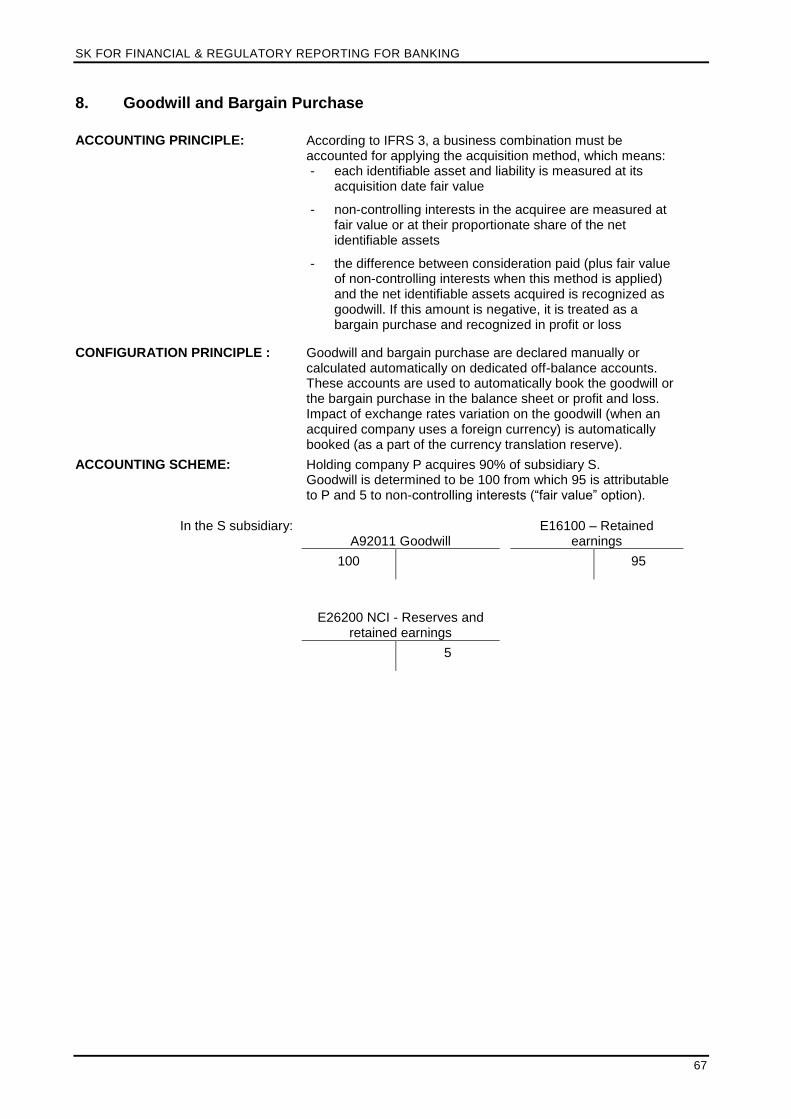

8. Goodwill and Bargain Purchase ........................................................................................................ 67

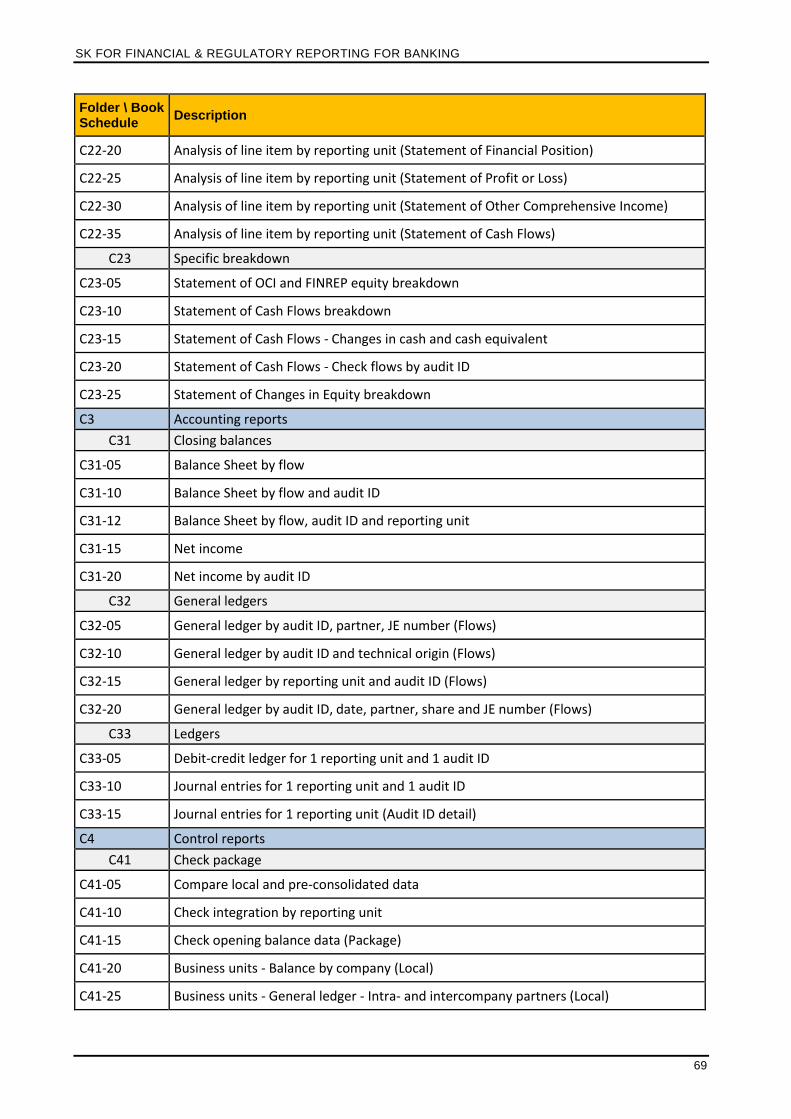

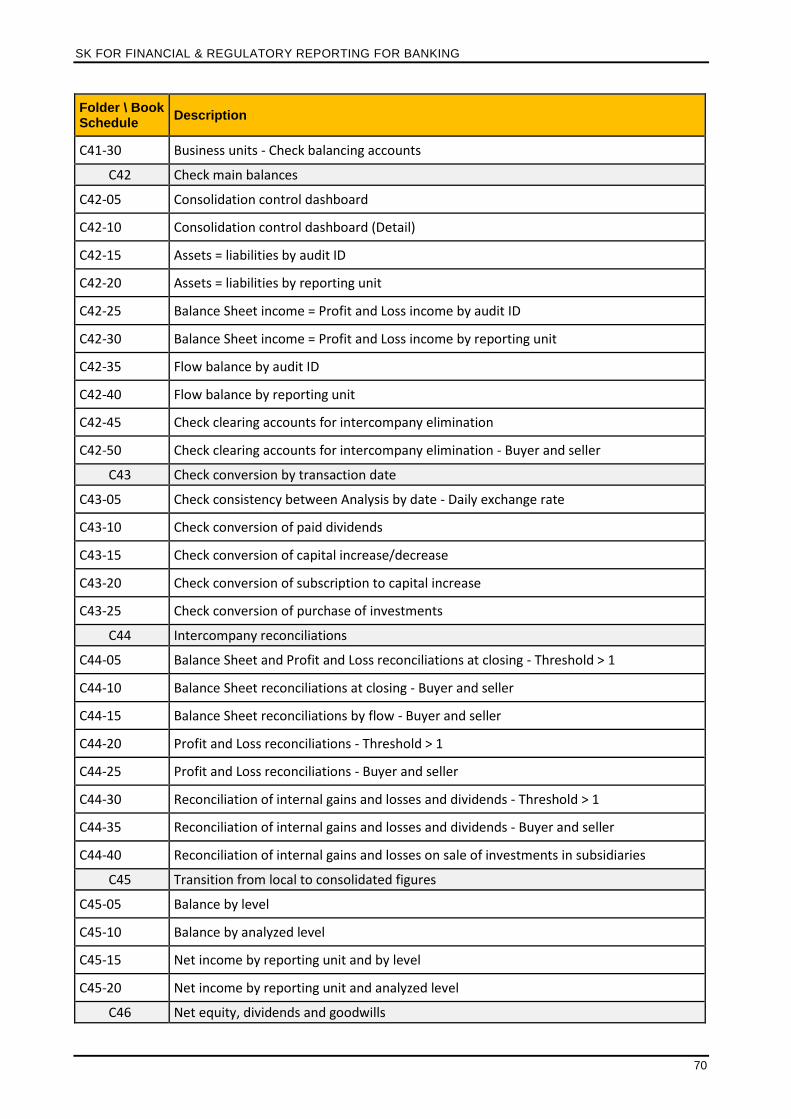

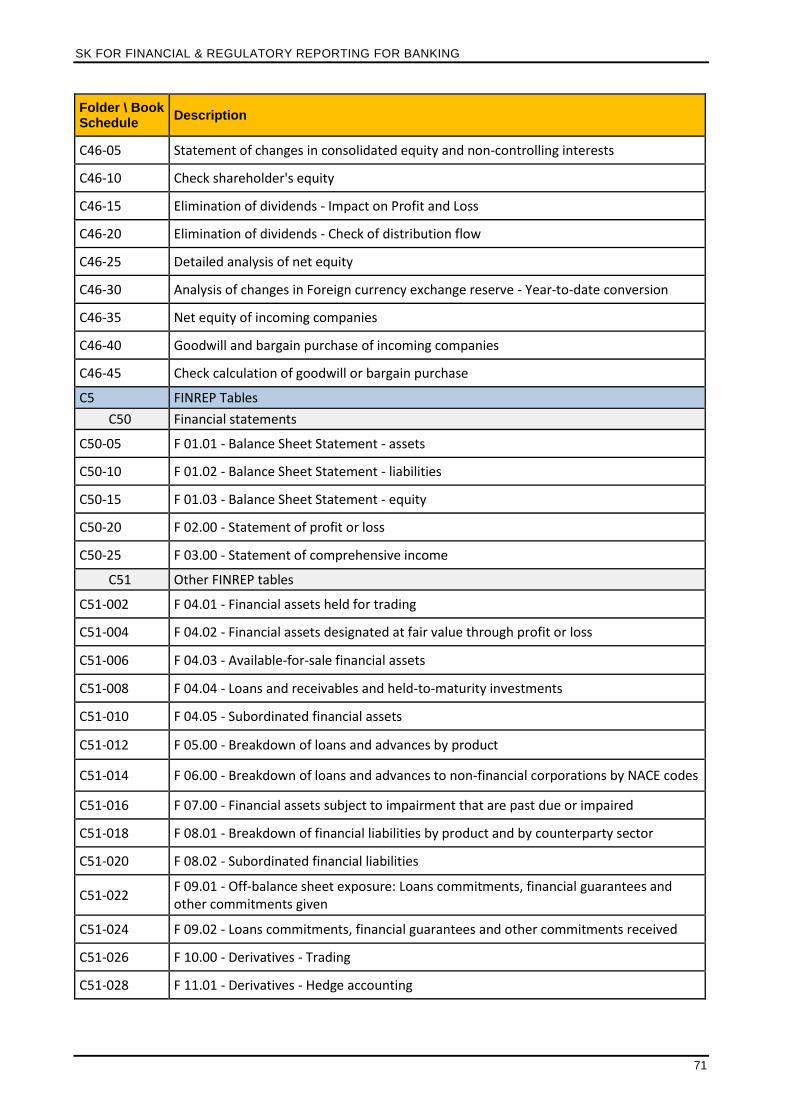

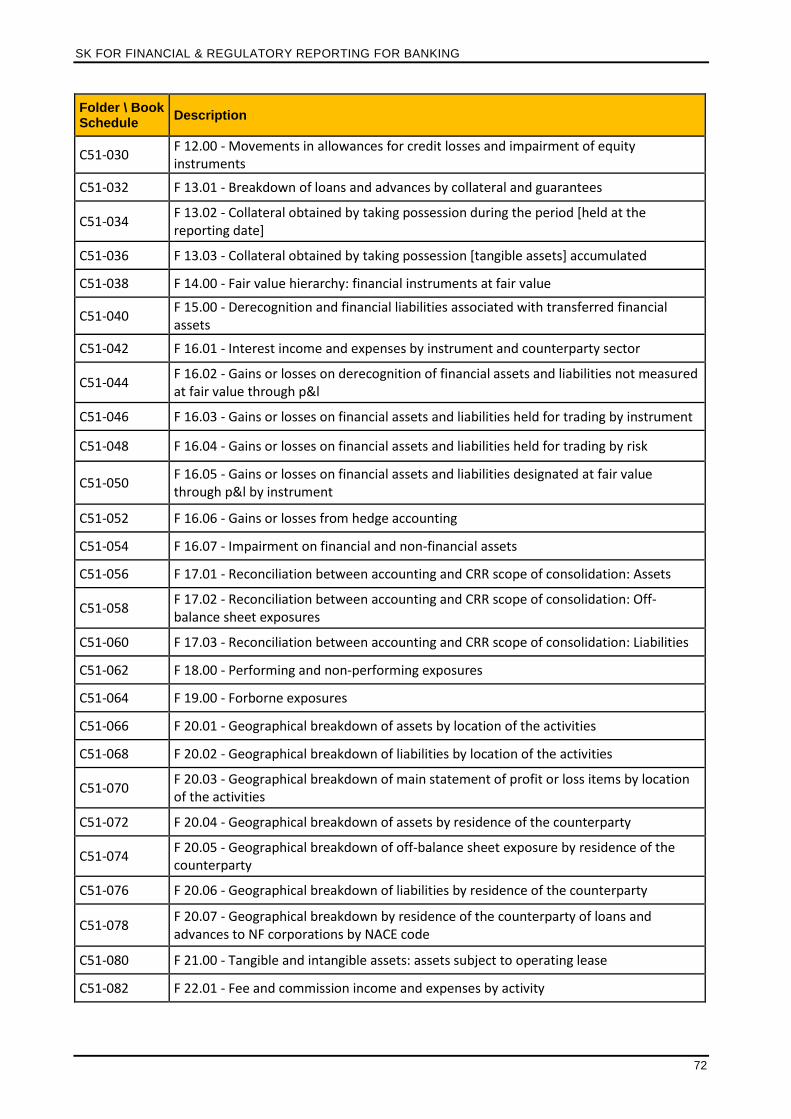

G. LIST OF RETRIEVAL SCHEDULES ................................................................................................... 68

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

4

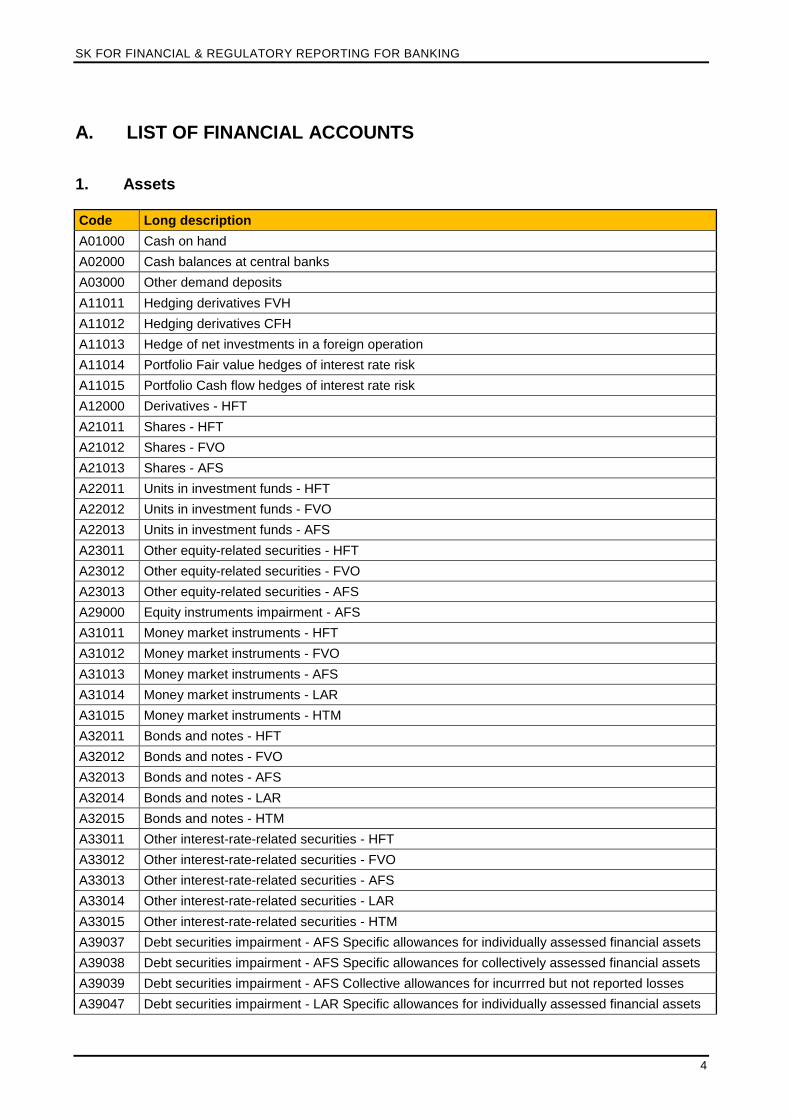

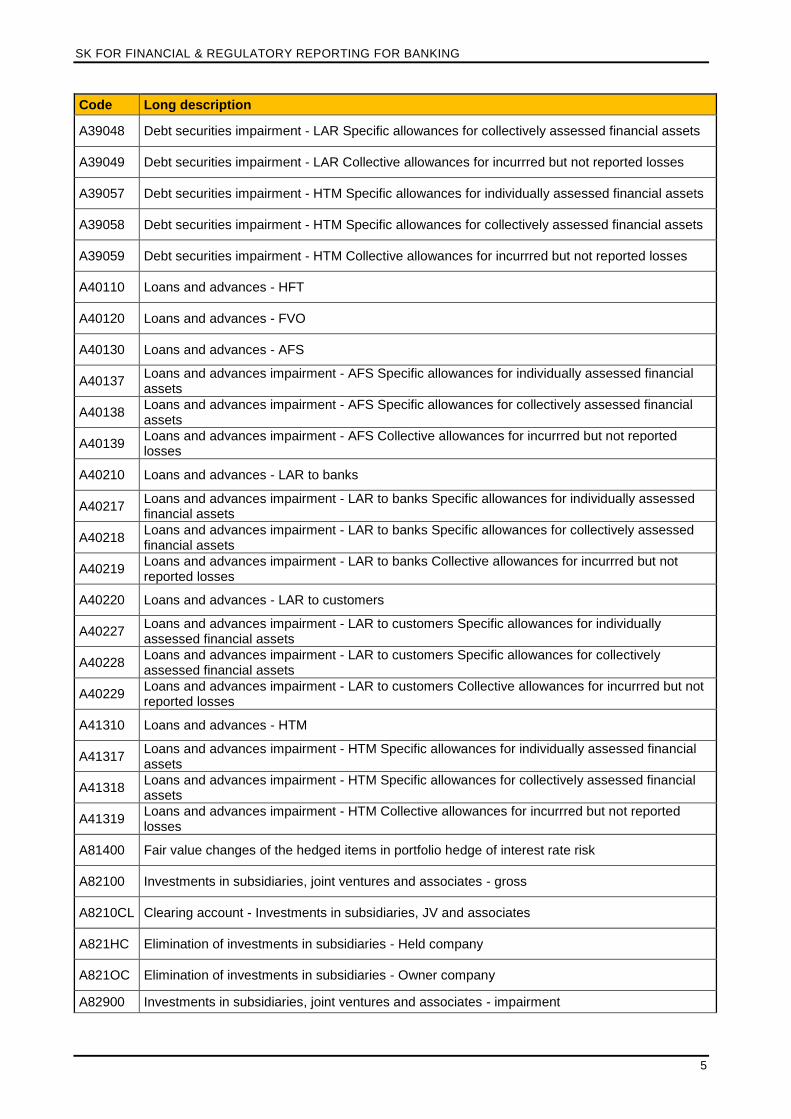

A. LIST OF FINANCIAL ACCOUNTS

1. Assets

Code Long description

A01000 Cash on hand

A02000 Cash balances at central banks

A03000 Other demand deposits

A11011 Hedging derivatives FVH

A11012 Hedging derivatives CFH

A11013 Hedge of net investments in a foreign operation

A11014 Portfolio Fair value hedges of interest rate risk

A11015 Portfolio Cash flow hedges of interest rate risk

A12000 Derivatives - HFT

A21011 Shares - HFT

A21012 Shares - FVO

A21013 Shares - AFS

A22011 Units in investment funds - HFT

A22012 Units in investment funds - FVO

A22013 Units in investment funds - AFS

A23011 Other equity-related securities - HFT

A23012 Other equity-related securities - FVO

A23013 Other equity-related securities - AFS

A29000 Equity instruments impairment - AFS

A31011 Money market instruments - HFT

A31012 Money market instruments - FVO

A31013 Money market instruments - AFS

A31014 Money market instruments - LAR

A31015 Money market instruments - HTM

A32011 Bonds and notes - HFT

A32012 Bonds and notes - FVO

A32013 Bonds and notes - AFS

A32014 Bonds and notes - LAR

A32015 Bonds and notes - HTM

A33011 Other interest-rate-related securities - HFT

A33012 Other interest-rate-related securities - FVO

A33013 Other interest-rate-related securities - AFS

A33014 Other interest-rate-related securities - LAR

A33015 Other interest-rate-related securities - HTM

A39037 Debt securities impairment - AFS Specific allowances for individually assessed financial assets

A39038 Debt securities impairment - AFS Specific allowances for collectively assessed financial assets

A39039 Debt securities impairment - AFS Collective allowances for incurrred but not reported losses

A39047 Debt securities impairment - LAR Specific allowances for individually assessed financial assets

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

5

Code Long description

A39048 Debt securities impairment - LAR Specific allowances for collectively assessed financial assets

A39049 Debt securities impairment - LAR Collective allowances for incurrred but not reported losses

A39057 Debt securities impairment - HTM Specific allowances for individually assessed financial assets

A39058 Debt securities impairment - HTM Specific allowances for collectively assessed financial assets

A39059 Debt securities impairment - HTM Collective allowances for incurrred but not reported losses

A40110 Loans and advances - HFT

A40120 Loans and advances - FVO

A40130 Loans and advances - AFS

A40137 Loans and advances impairment - AFS Specific allowances for individually assessed financial assets

A40138 Loans and advances impairment - AFS Specific allowances for collectively assessed financial assets

A40139 Loans and advances impairment - AFS Collective allowances for incurrred but not reported losses

A40210 Loans and advances - LAR to banks

A40217 Loans and advances impairment - LAR to banks Specific allowances for individually assessed financial assets

A40218 Loans and advances impairment - LAR to banks Specific allowances for collectively assessed financial assets

A40219 Loans and advances impairment - LAR to banks Collective allowances for incurrred but not reported losses

A40220 Loans and advances - LAR to customers

A40227 Loans and advances impairment - LAR to customers Specific allowances for individually assessed financial assets

A40228 Loans and advances impairment - LAR to customers Specific allowances for collectively assessed financial assets

A40229 Loans and advances impairment - LAR to customers Collective allowances for incurrred but not reported losses

A41310 Loans and advances - HTM

A41317 Loans and advances impairment - HTM Specific allowances for individually assessed financial assets

A41318 Loans and advances impairment - HTM Specific allowances for collectively assessed financial assets

A41319 Loans and advances impairment - HTM Collective allowances for incurrred but not reported losses

A81400 Fair value changes of the hedged items in portfolio hedge of interest rate risk

A82100 Investments in subsidiaries, joint ventures and associates - gross

A8210CL Clearing account - Investments in subsidiaries, JV and associates

A821HC Elimination of investments in subsidiaries - Held company

A821OC Elimination of investments in subsidiaries - Owner company

A82900 Investments in subsidiaries, joint ventures and associates - impairment

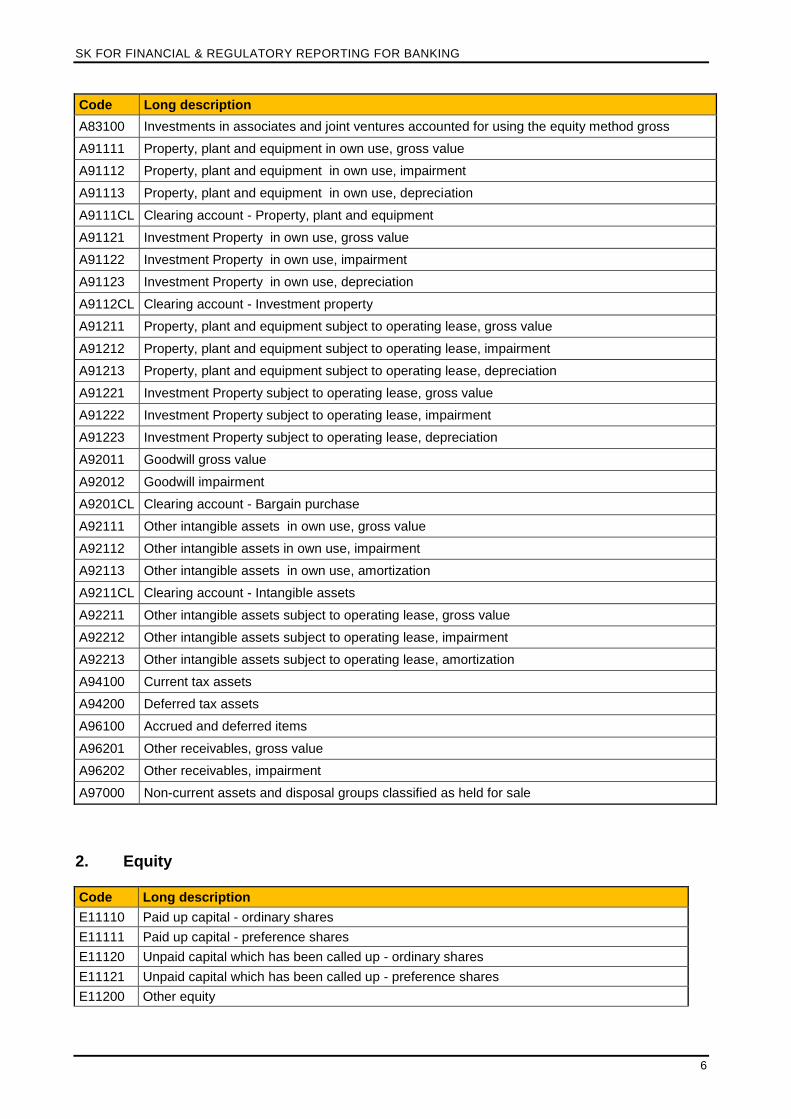

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

6

Code Long description

A83100 Investments in associates and joint ventures accounted for using the equity method gross

A91111 Property, plant and equipment in own use, gross value

A91112 Property, plant and equipment in own use, impairment

A91113 Property, plant and equipment in own use, depreciation

A9111CL Clearing account - Property, plant and equipment

A91121 Investment Property in own use, gross value

A91122 Investment Property in own use, impairment

A91123 Investment Property in own use, depreciation

A9112CL Clearing account - Investment property

A91211 Property, plant and equipment subject to operating lease, gross value

A91212 Property, plant and equipment subject to operating lease, impairment

A91213 Property, plant and equipment subject to operating lease, depreciation

A91221 Investment Property subject to operating lease, gross value

A91222 Investment Property subject to operating lease, impairment

A91223 Investment Property subject to operating lease, depreciation

A92011 Goodwill gross value

A92012 Goodwill impairment

A9201CL Clearing account - Bargain purchase

A92111 Other intangible assets in own use, gross value

A92112 Other intangible assets in own use, impairment

A92113 Other intangible assets in own use, amortization

A9211CL Clearing account - Intangible assets

A92211 Other intangible assets subject to operating lease, gross value

A92212 Other intangible assets subject to operating lease, impairment

A92213 Other intangible assets subject to operating lease, amortization

A94100 Current tax assets

A94200 Deferred tax assets

A96100 Accrued and deferred items

A96201 Other receivables, gross value

A96202 Other receivables, impairment

A97000 Non-current assets and disposal groups classified as held for sale

2. Equity

Code Long description

E11110 Paid up capital - ordinary shares

E11111 Paid up capital - preference shares

E11120 Unpaid capital which has been called up - ordinary shares

E11121 Unpaid capital which has been called up - preference shares

E11200 Other equity

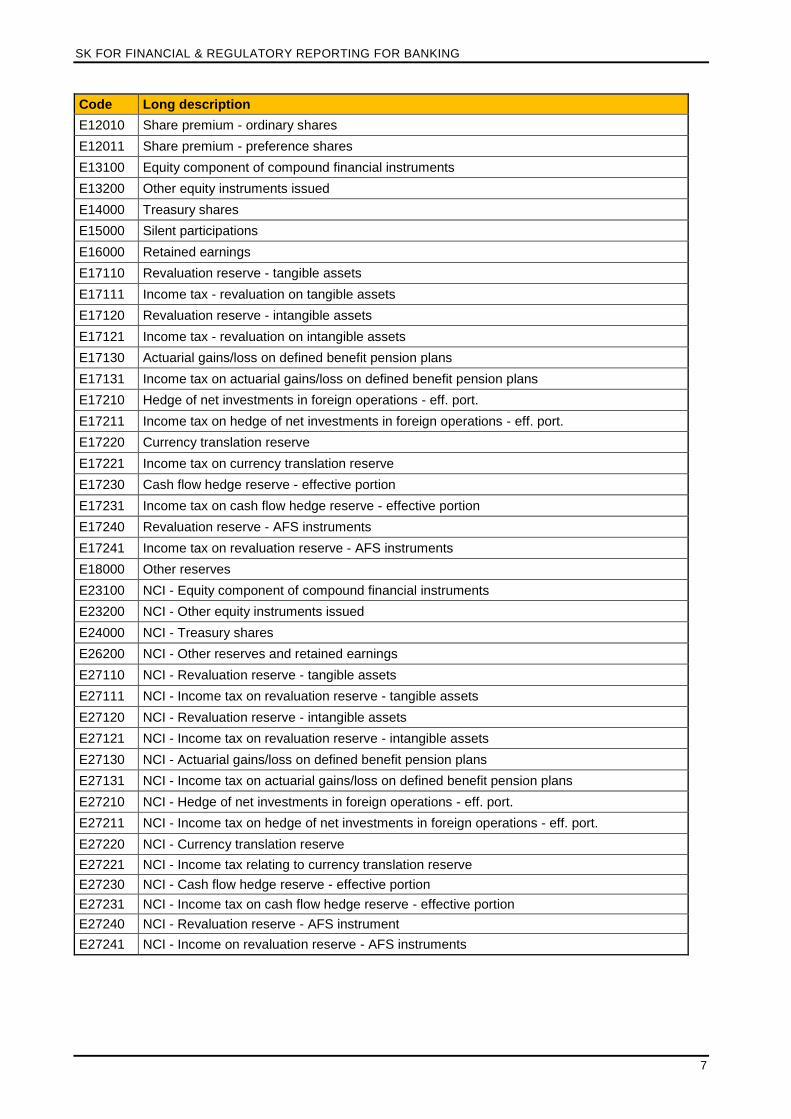

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

7

Code Long description

E12010 Share premium - ordinary shares

E12011 Share premium - preference shares

E13100 Equity component of compound financial instruments

E13200 Other equity instruments issued

E14000 Treasury shares

E15000 Silent participations

E16000 Retained earnings

E17110 Revaluation reserve - tangible assets

E17111 Income tax - revaluation on tangible assets

E17120 Revaluation reserve - intangible assets

E17121 Income tax - revaluation on intangible assets

E17130 Actuarial gains/loss on defined benefit pension plans

E17131 Income tax on actuarial gains/loss on defined benefit pension plans

E17210 Hedge of net investments in foreign operations - eff. port.

E17211 Income tax on hedge of net investments in foreign operations - eff. port.

E17220 Currency translation reserve

E17221 Income tax on currency translation reserve

E17230 Cash flow hedge reserve - effective portion

E17231 Income tax on cash flow hedge reserve - effective portion

E17240 Revaluation reserve - AFS instruments

E17241 Income tax on revaluation reserve - AFS instruments

E18000 Other reserves

E23100 NCI - Equity component of compound financial instruments

E23200 NCI - Other equity instruments issued

E24000 NCI - Treasury shares

E26200 NCI - Other reserves and retained earnings

E27110 NCI - Revaluation reserve - tangible assets

E27111 NCI - Income tax on revaluation reserve - tangible assets

E27120 NCI - Revaluation reserve - intangible assets

E27121 NCI - Income tax on revaluation reserve - intangible assets

E27130 NCI - Actuarial gains/loss on defined benefit pension plans

E27131 NCI - Income tax on actuarial gains/loss on defined benefit pension plans

E27210 NCI - Hedge of net investments in foreign operations - eff. port.

E27211 NCI - Income tax on hedge of net investments in foreign operations - eff. port.

E27220 NCI - Currency translation reserve

E27221 NCI - Income tax relating to currency translation reserve

E27230 NCI - Cash flow hedge reserve - effective portion

E27231 NCI - Income tax on cash flow hedge reserve - effective portion

E27240 NCI - Revaluation reserve - AFS instrument

E27241 NCI - Income on revaluation reserve - AFS instruments

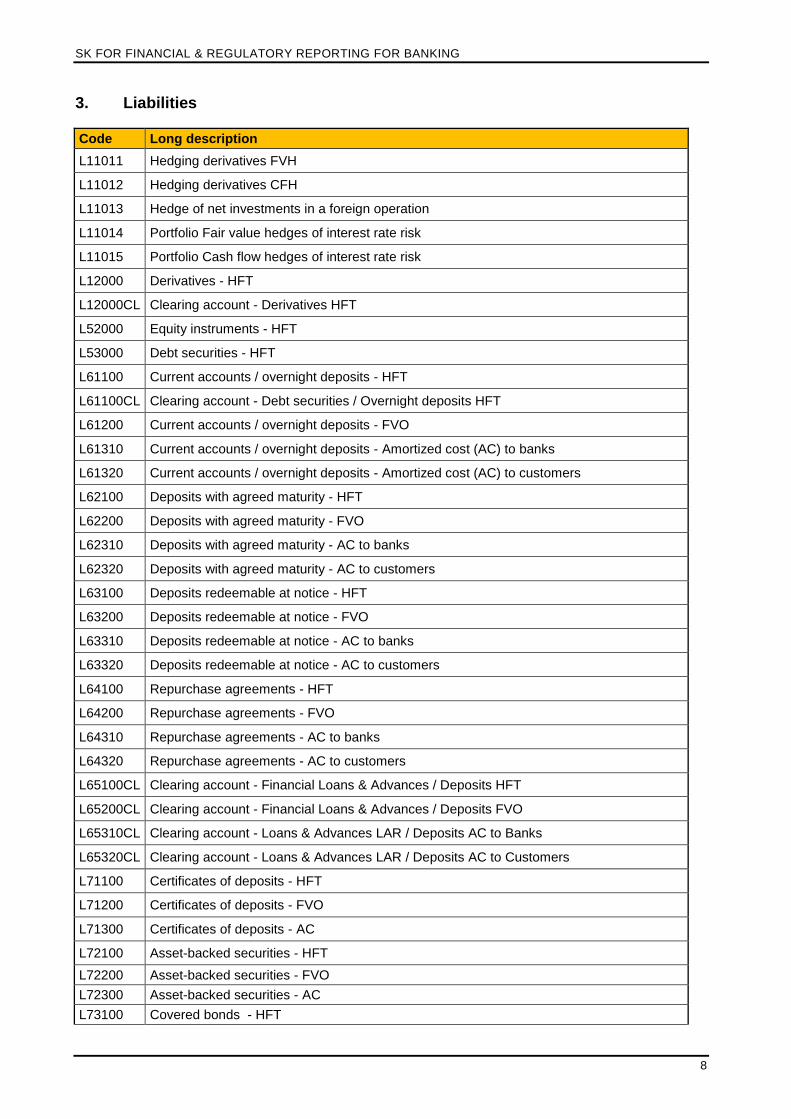

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

8

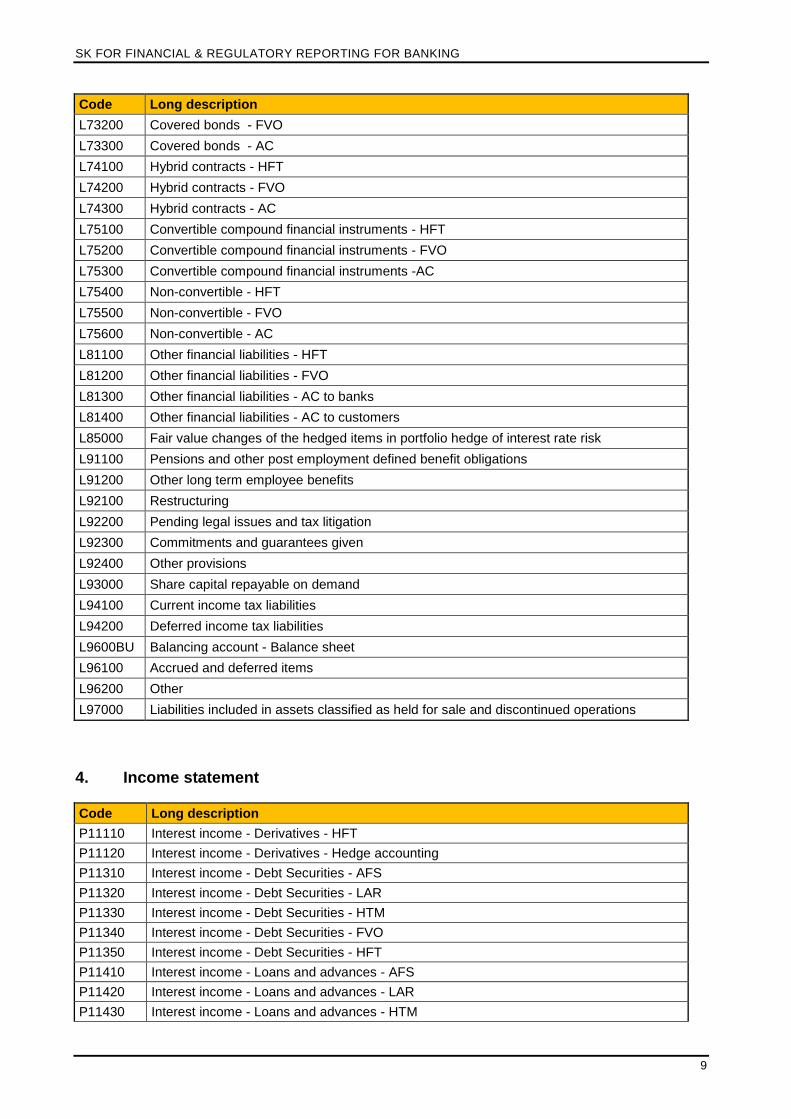

3. Liabilities

Code Long description

L11011 Hedging derivatives FVH

L11012 Hedging derivatives CFH

L11013 Hedge of net investments in a foreign operation

L11014 Portfolio Fair value hedges of interest rate risk

L11015 Portfolio Cash flow hedges of interest rate risk

L12000 Derivatives - HFT

L12000CL Clearing account - Derivatives HFT

L52000 Equity instruments - HFT

L53000 Debt securities - HFT

L61100 Current accounts / overnight deposits - HFT

L61100CL Clearing account - Debt securities / Overnight deposits HFT

L61200 Current accounts / overnight deposits - FVO

L61310 Current accounts / overnight deposits - Amortized cost (AC) to banks

L61320 Current accounts / overnight deposits - Amortized cost (AC) to customers

L62100 Deposits with agreed maturity - HFT

L62200 Deposits with agreed maturity - FVO

L62310 Deposits with agreed maturity - AC to banks

L62320 Deposits with agreed maturity - AC to customers

L63100 Deposits redeemable at notice - HFT

L63200 Deposits redeemable at notice - FVO

L63310 Deposits redeemable at notice - AC to banks

L63320 Deposits redeemable at notice - AC to customers

L64100 Repurchase agreements - HFT

L64200 Repurchase agreements - FVO

L64310 Repurchase agreements - AC to banks

L64320 Repurchase agreements - AC to customers

L65100CL Clearing account - Financial Loans & Advances / Deposits HFT

L65200CL Clearing account - Financial Loans & Advances / Deposits FVO

L65310CL Clearing account - Loans & Advances LAR / Deposits AC to Banks

L65320CL Clearing account - Loans & Advances LAR / Deposits AC to Customers

L71100 Certificates of deposits - HFT

L71200 Certificates of deposits - FVO

L71300 Certificates of deposits - AC

L72100 Asset-backed securities - HFT

L72200 Asset-backed securities - FVO

L72300 Asset-backed securities - AC

L73100 Covered bonds - HFT

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

9

Code Long description

L73200 Covered bonds - FVO

L73300 Covered bonds - AC

L74100 Hybrid contracts - HFT

L74200 Hybrid contracts - FVO

L74300 Hybrid contracts - AC

L75100 Convertible compound financial instruments - HFT

L75200 Convertible compound financial instruments - FVO

L75300 Convertible compound financial instruments -AC

L75400 Non-convertible - HFT

L75500 Non-convertible - FVO

L75600 Non-convertible - AC

L81100 Other financial liabilities - HFT

L81200 Other financial liabilities - FVO

L81300 Other financial liabilities - AC to banks

L81400 Other financial liabilities - AC to customers

L85000 Fair value changes of the hedged items in portfolio hedge of interest rate risk

L91100 Pensions and other post employment defined benefit obligations

L91200 Other long term employee benefits

L92100 Restructuring

L92200 Pending legal issues and tax litigation

L92300 Commitments and guarantees given

L92400 Other provisions

L93000 Share capital repayable on demand

L94100 Current income tax liabilities

L94200 Deferred income tax liabilities

L9600BU Balancing account - Balance sheet

L96100 Accrued and deferred items

L96200 Other

L97000 Liabilities included in assets classified as held for sale and discontinued operations

4. Income statement

Code Long description

P11110 Interest income - Derivatives - HFT

P11120 Interest income - Derivatives - Hedge accounting

P11310 Interest income - Debt Securities - AFS

P11320 Interest income - Debt Securities - LAR

P11330 Interest income - Debt Securities - HTM

P11340 Interest income - Debt Securities - FVO

P11350 Interest income - Debt Securities - HFT

P11410 Interest income - Loans and advances - AFS

P11420 Interest income - Loans and advances - LAR

P11430 Interest income - Loans and advances - HTM

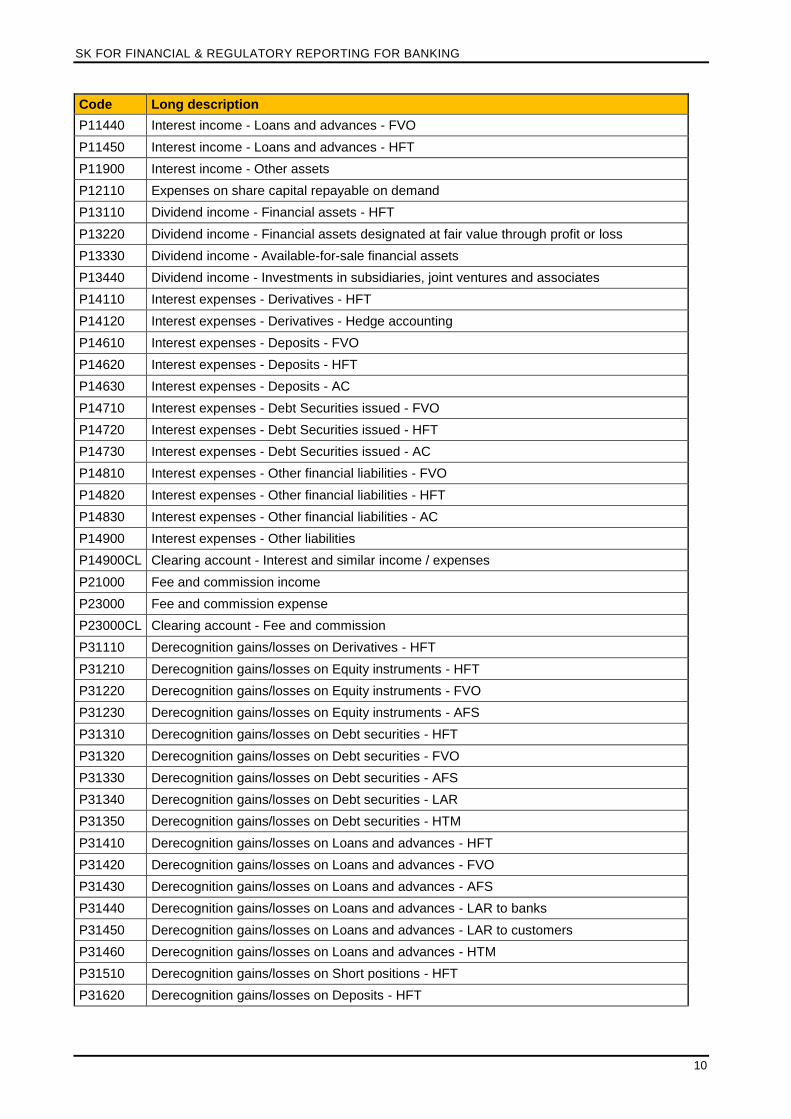

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

10

Code Long description

P11440 Interest income - Loans and advances - FVO

P11450 Interest income - Loans and advances - HFT

P11900 Interest income - Other assets

P12110 Expenses on share capital repayable on demand

P13110 Dividend income - Financial assets - HFT

P13220 Dividend income - Financial assets designated at fair value through profit or loss

P13330 Dividend income - Available-for-sale financial assets

P13440 Dividend income - Investments in subsidiaries, joint ventures and associates

P14110 Interest expenses - Derivatives - HFT

P14120 Interest expenses - Derivatives - Hedge accounting

P14610 Interest expenses - Deposits - FVO

P14620 Interest expenses - Deposits - HFT

P14630 Interest expenses - Deposits - AC

P14710 Interest expenses - Debt Securities issued - FVO

P14720 Interest expenses - Debt Securities issued - HFT

P14730 Interest expenses - Debt Securities issued - AC

P14810 Interest expenses - Other financial liabilities - FVO

P14820 Interest expenses - Other financial liabilities - HFT

P14830 Interest expenses - Other financial liabilities - AC

P14900 Interest expenses - Other liabilities

P14900CL Clearing account - Interest and similar income / expenses

P21000 Fee and commission income

P23000 Fee and commission expense

P23000CL Clearing account - Fee and commission

P31110 Derecognition gains/losses on Derivatives - HFT

P31210 Derecognition gains/losses on Equity instruments - HFT

P31220 Derecognition gains/losses on Equity instruments - FVO

P31230 Derecognition gains/losses on Equity instruments - AFS

P31310 Derecognition gains/losses on Debt securities - HFT

P31320 Derecognition gains/losses on Debt securities - FVO

P31330 Derecognition gains/losses on Debt securities - AFS

P31340 Derecognition gains/losses on Debt securities - LAR

P31350 Derecognition gains/losses on Debt securities - HTM

P31410 Derecognition gains/losses on Loans and advances - HFT

P31420 Derecognition gains/losses on Loans and advances - FVO

P31430 Derecognition gains/losses on Loans and advances - AFS

P31440 Derecognition gains/losses on Loans and advances - LAR to banks

P31450 Derecognition gains/losses on Loans and advances - LAR to customers

P31460 Derecognition gains/losses on Loans and advances - HTM

P31510 Derecognition gains/losses on Short positions - HFT

P31620 Derecognition gains/losses on Deposits - HFT

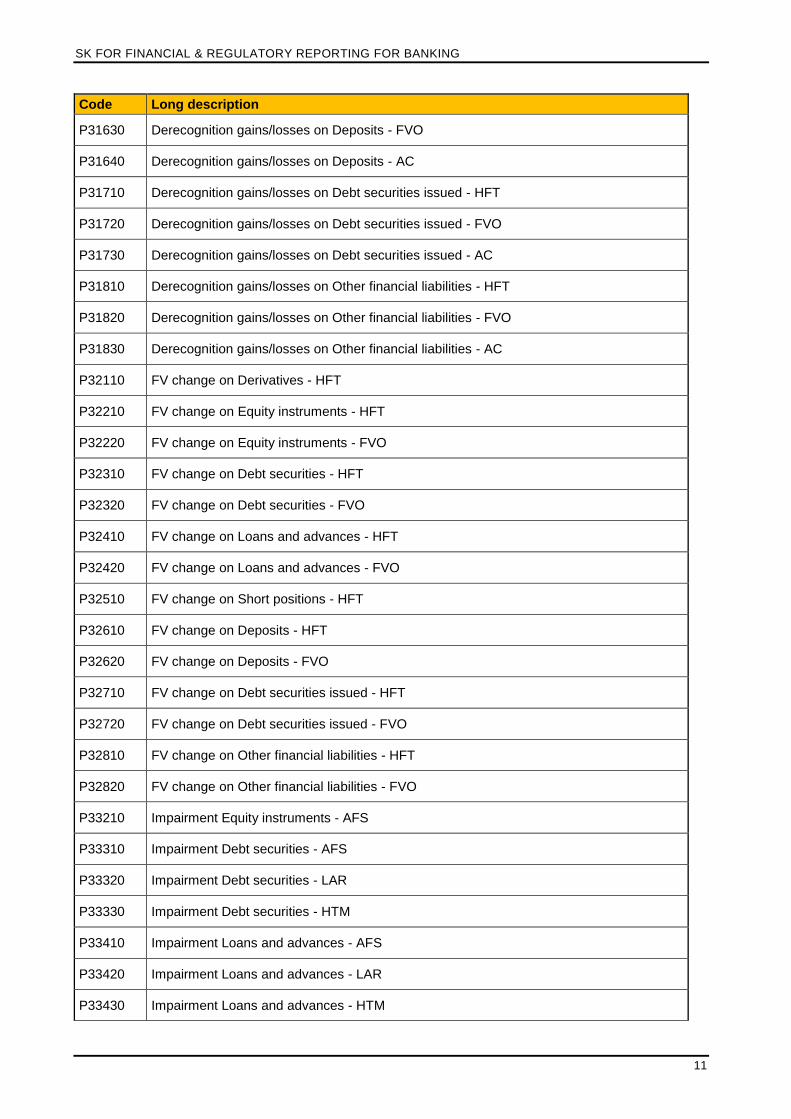

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

11

Code Long description

P31630 Derecognition gains/losses on Deposits - FVO

P31640 Derecognition gains/losses on Deposits - AC

P31710 Derecognition gains/losses on Debt securities issued - HFT

P31720 Derecognition gains/losses on Debt securities issued - FVO

P31730 Derecognition gains/losses on Debt securities issued - AC

P31810 Derecognition gains/losses on Other financial liabilities - HFT

P31820 Derecognition gains/losses on Other financial liabilities - FVO

P31830 Derecognition gains/losses on Other financial liabilities - AC

P32110 FV change on Derivatives - HFT

P32210 FV change on Equity instruments - HFT

P32220 FV change on Equity instruments - FVO

P32310 FV change on Debt securities - HFT

P32320 FV change on Debt securities - FVO

P32410 FV change on Loans and advances - HFT

P32420 FV change on Loans and advances - FVO

P32510 FV change on Short positions - HFT

P32610 FV change on Deposits - HFT

P32620 FV change on Deposits - FVO

P32710 FV change on Debt securities issued - HFT

P32720 FV change on Debt securities issued - FVO

P32810 FV change on Other financial liabilities - HFT

P32820 FV change on Other financial liabilities - FVO

P33210 Impairment Equity instruments - AFS

P33310 Impairment Debt securities - AFS

P33320 Impairment Debt securities - LAR

P33330 Impairment Debt securities - HTM

P33410 Impairment Loans and advances - AFS

P33420 Impairment Loans and advances - LAR

P33430 Impairment Loans and advances - HTM

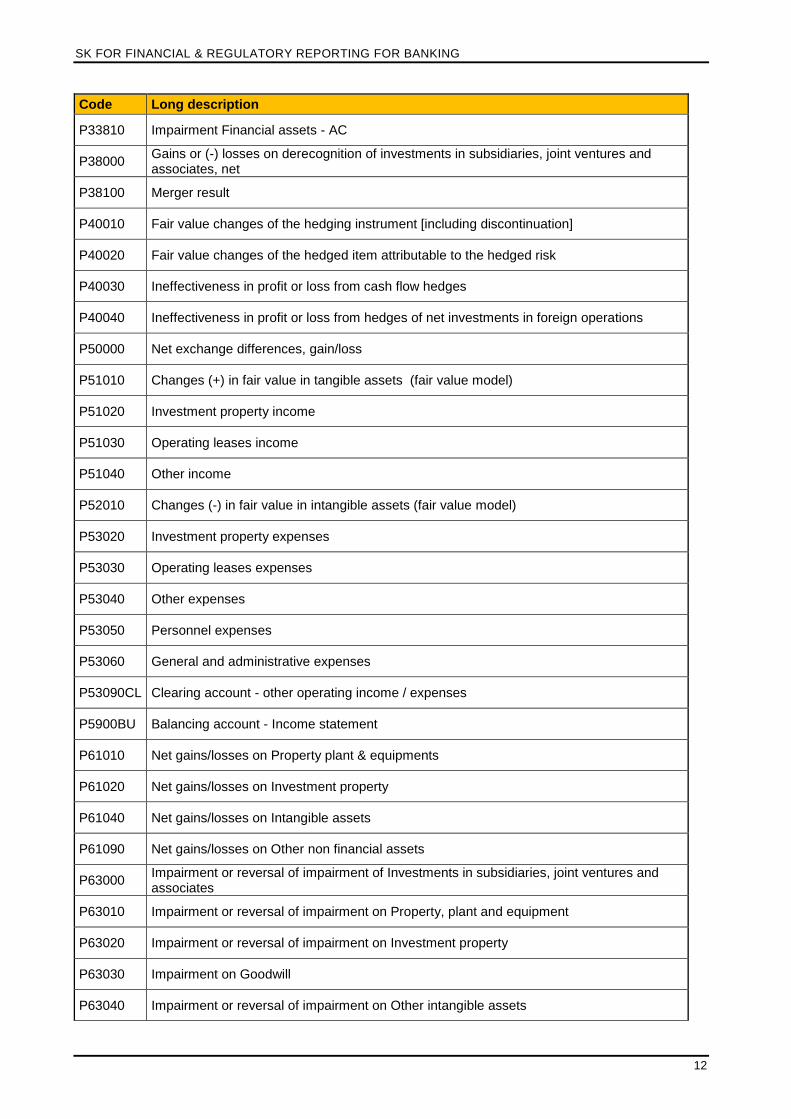

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

12

Code Long description

P33810 Impairment Financial assets - AC

P38000 Gains or (-) losses on derecognition of investments in subsidiaries, joint ventures and associates, net

P38100 Merger result

P40010 Fair value changes of the hedging instrument [including discontinuation]

P40020 Fair value changes of the hedged item attributable to the hedged risk

P40030 Ineffectiveness in profit or loss from cash flow hedges

P40040 Ineffectiveness in profit or loss from hedges of net investments in foreign operations

P50000 Net exchange differences, gain/loss

P51010 Changes (+) in fair value in tangible assets (fair value model)

P51020 Investment property income

P51030 Operating leases income

P51040 Other income

P52010 Changes (-) in fair value in intangible assets (fair value model)

P53020 Investment property expenses

P53030 Operating leases expenses

P53040 Other expenses

P53050 Personnel expenses

P53060 General and administrative expenses

P53090CL Clearing account - other operating income / expenses

P5900BU Balancing account - Income statement

P61010 Net gains/losses on Property plant & equipments

P61020 Net gains/losses on Investment property

P61040 Net gains/losses on Intangible assets

P61090 Net gains/losses on Other non financial assets

P63000 Impairment or reversal of impairment of Investments in subsidiaries, joint ventures and associates

P63010 Impairment or reversal of impairment on Property, plant and equipment

P63020 Impairment or reversal of impairment on Investment property

P63030 Impairment on Goodwill

P63040 Impairment or reversal of impairment on Other intangible assets

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

13

Code Long description

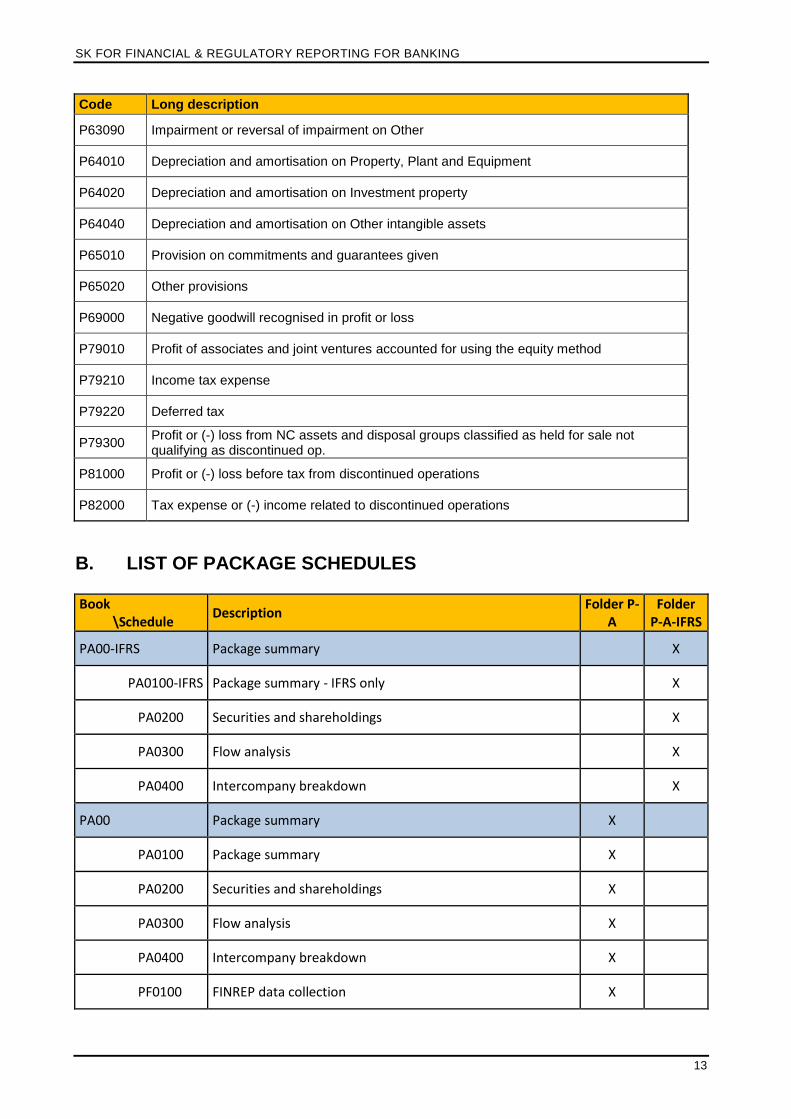

P63090 Impairment or reversal of impairment on Other

P64010 Depreciation and amortisation on Property, Plant and Equipment

P64020 Depreciation and amortisation on Investment property

P64040 Depreciation and amortisation on Other intangible assets

P65010 Provision on commitments and guarantees given

P65020 Other provisions

P69000 Negative goodwill recognised in profit or loss

P79010 Profit of associates and joint ventures accounted for using the equity method

P79210 Income tax expense

P79220 Deferred tax

P79300 Profit or (-) loss from NC assets and disposal groups classified as held for sale not qualifying as discontinued op.

P81000 Profit or (-) loss before tax from discontinued operations

P82000 Tax expense or (-) income related to discontinued operations

B. LIST OF PACKAGE SCHEDULES

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

PA00-IFRS Package summary X

PA0100-IFRS Package summary - IFRS only X

PA0200 Securities and shareholdings X

PA0300 Flow analysis X

PA0400 Intercompany breakdown X

PA00 Package summary X

PA0100 Package summary X

PA0200 Securities and shareholdings X

PA0300 Flow analysis X

PA0400 Intercompany breakdown X

PF0100 FINREP data collection X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

14

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

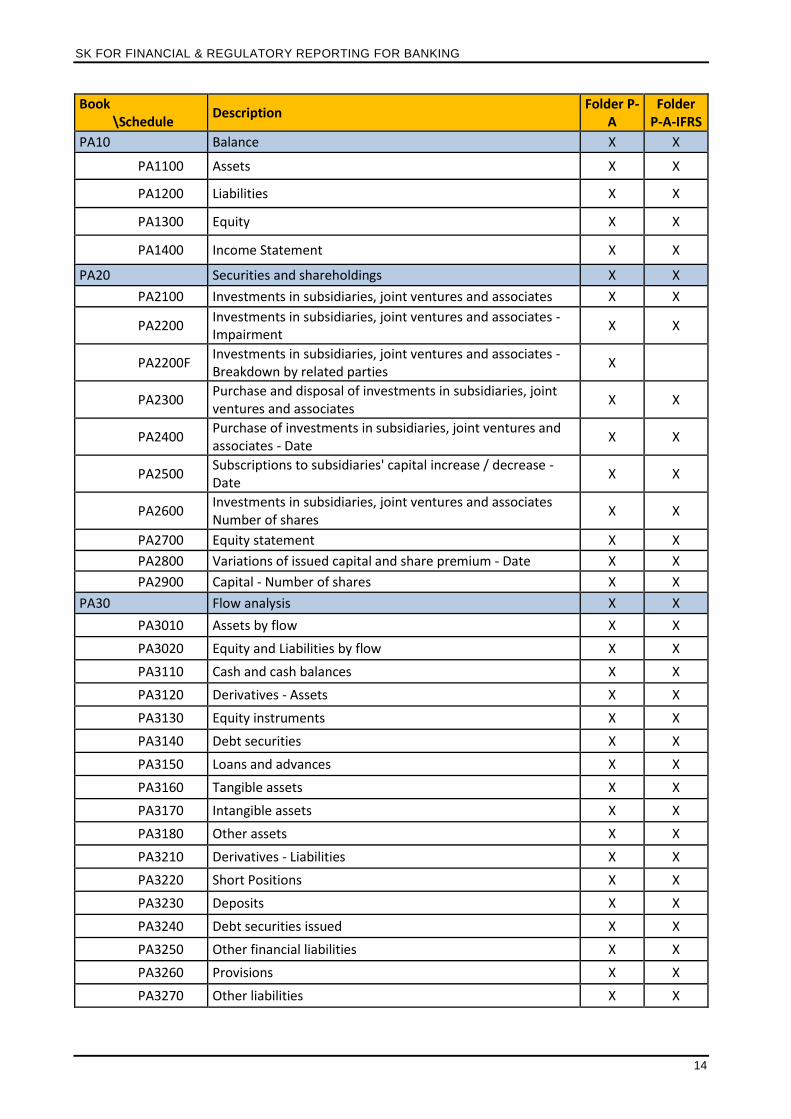

PA10 Balance X X

PA1100 Assets X X

PA1200 Liabilities X X

PA1300 Equity X X

PA1400 Income Statement X X

PA20 Securities and shareholdings X X

PA2100 Investments in subsidiaries, joint ventures and associates X X

PA2200 Investments in subsidiaries, joint ventures and associates - Impairment

X X

PA2200F Investments in subsidiaries, joint ventures and associates - Breakdown by related parties

X

PA2300 Purchase and disposal of investments in subsidiaries, joint ventures and associates

X X

PA2400 Purchase of investments in subsidiaries, joint ventures and associates - Date

X X

PA2500 Subscriptions to subsidiaries' capital increase / decrease - Date

X X

PA2600 Investments in subsidiaries, joint ventures and associates Number of shares

X X

PA2700 Equity statement X X

PA2800 Variations of issued capital and share premium - Date X X

PA2900 Capital - Number of shares X X

PA30 Flow analysis X X

PA3010 Assets by flow X X

PA3020 Equity and Liabilities by flow X X

PA3110 Cash and cash balances X X

PA3120 Derivatives - Assets X X

PA3130 Equity instruments X X

PA3140 Debt securities X X

PA3150 Loans and advances X X

PA3160 Tangible assets X X

PA3170 Intangible assets X X

PA3180 Other assets X X

PA3210 Derivatives - Liabilities X X

PA3220 Short Positions X X

PA3230 Deposits X X

PA3240 Debt securities issued X X

PA3250 Other financial liabilities X X

PA3260 Provisions X X

PA3270 Other liabilities X X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

15

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

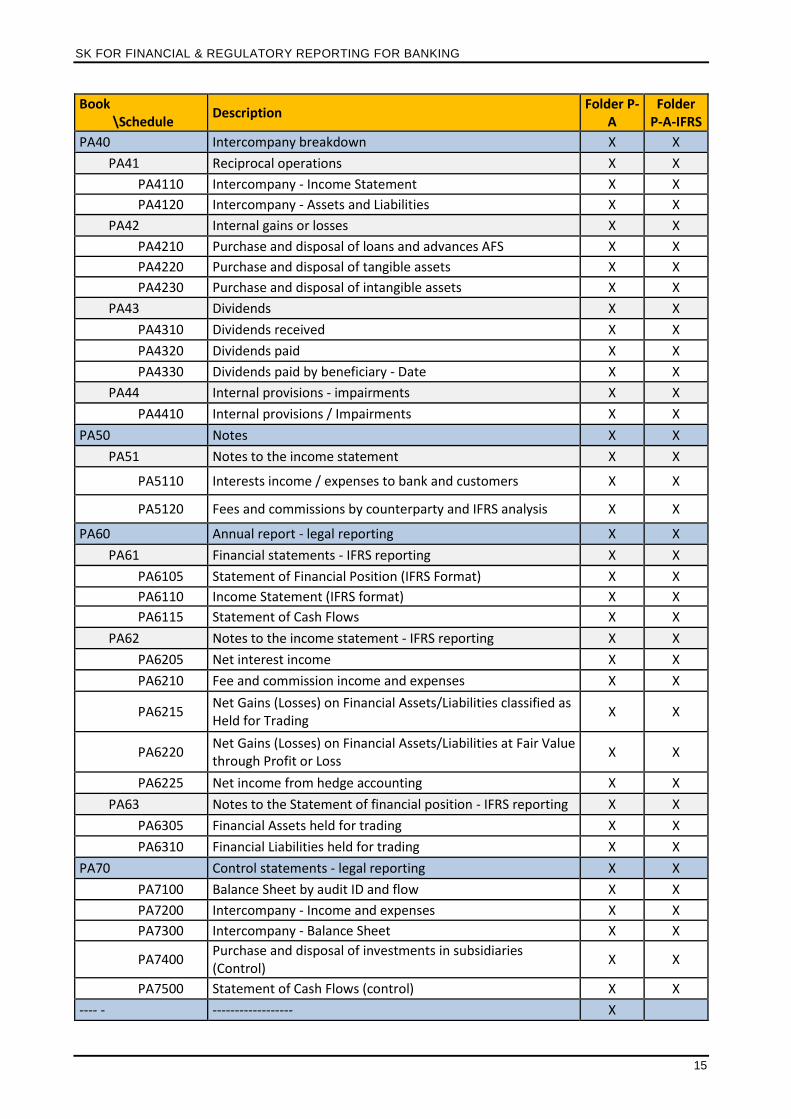

PA40 Intercompany breakdown X X

PA41 Reciprocal operations X X

PA4110 Intercompany - Income Statement X X

PA4120 Intercompany - Assets and Liabilities X X

PA42 Internal gains or losses X X

PA4210 Purchase and disposal of loans and advances AFS X X

PA4220 Purchase and disposal of tangible assets X X

PA4230 Purchase and disposal of intangible assets X X

PA43 Dividends X X

PA4310 Dividends received X X

PA4320 Dividends paid X X

PA4330 Dividends paid by beneficiary - Date X X

PA44 Internal provisions - impairments X X

PA4410 Internal provisions / Impairments X X

PA50 Notes X X

PA51 Notes to the income statement X X

PA5110 Interests income / expenses to bank and customers X X

PA5120 Fees and commissions by counterparty and IFRS analysis X X

PA60 Annual report - legal reporting X X

PA61 Financial statements - IFRS reporting X X

PA6105 Statement of Financial Position (IFRS Format) X X

PA6110 Income Statement (IFRS format) X X

PA6115 Statement of Cash Flows X X

PA62 Notes to the income statement - IFRS reporting X X

PA6205 Net interest income X X

PA6210 Fee and commission income and expenses X X

PA6215 Net Gains (Losses) on Financial Assets/Liabilities classified as Held for Trading

X X

PA6220 Net Gains (Losses) on Financial Assets/Liabilities at Fair Value through Profit or Loss

X X

PA6225 Net income from hedge accounting X X

PA63 Notes to the Statement of financial position - IFRS reporting X X

PA6305 Financial Assets held for trading X X

PA6310 Financial Liabilities held for trading X X

PA70 Control statements - legal reporting X X

PA7100 Balance Sheet by audit ID and flow X X

PA7200 Intercompany - Income and expenses X X

PA7300 Intercompany - Balance Sheet X X

PA7400 Purchase and disposal of investments in subsidiaries (Control)

X X

PA7500 Statement of Cash Flows (control) X X

---- - ------------------ X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

16

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

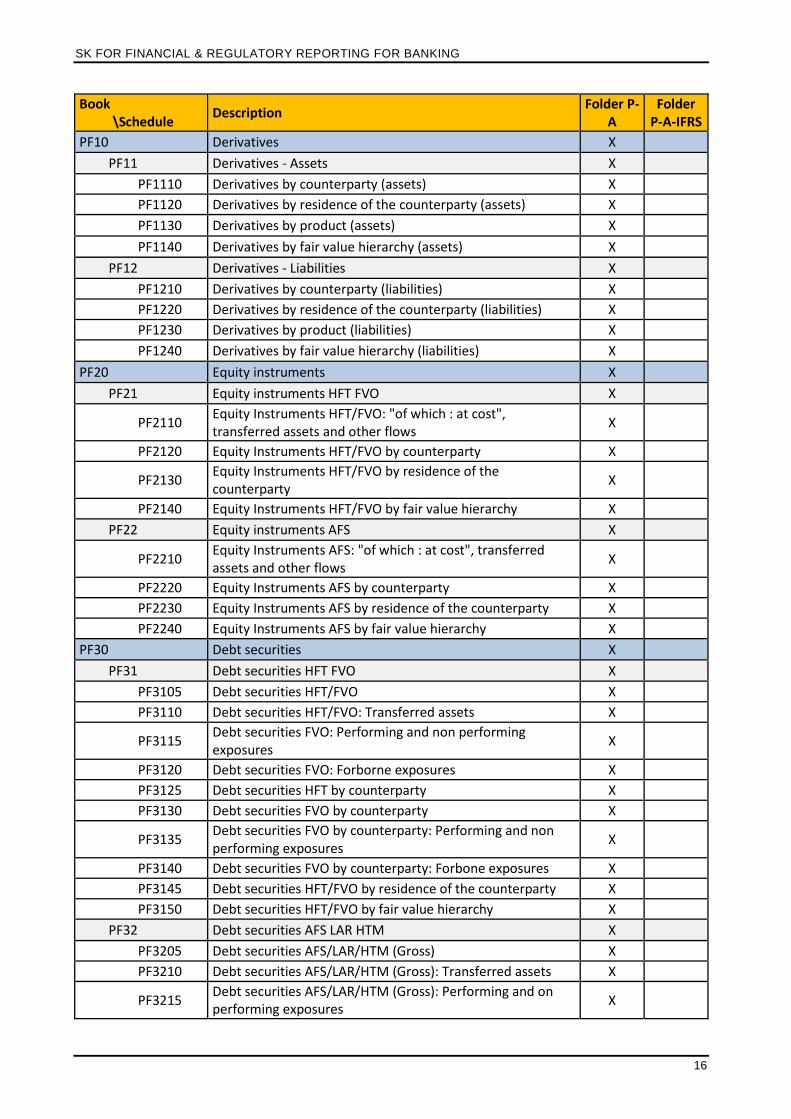

PF10 Derivatives X

PF11 Derivatives - Assets X

PF1110 Derivatives by counterparty (assets) X

PF1120 Derivatives by residence of the counterparty (assets) X

PF1130 Derivatives by product (assets) X

PF1140 Derivatives by fair value hierarchy (assets) X

PF12 Derivatives - Liabilities X

PF1210 Derivatives by counterparty (liabilities) X

PF1220 Derivatives by residence of the counterparty (liabilities) X

PF1230 Derivatives by product (liabilities) X

PF1240 Derivatives by fair value hierarchy (liabilities) X

PF20 Equity instruments X

PF21 Equity instruments HFT FVO X

PF2110 Equity Instruments HFT/FVO: "of which : at cost", transferred assets and other flows

X

PF2120 Equity Instruments HFT/FVO by counterparty X

PF2130 Equity Instruments HFT/FVO by residence of the counterparty

X

PF2140 Equity Instruments HFT/FVO by fair value hierarchy X

PF22 Equity instruments AFS X

PF2210 Equity Instruments AFS: "of which : at cost", transferred assets and other flows

X

PF2220 Equity Instruments AFS by counterparty X

PF2230 Equity Instruments AFS by residence of the counterparty X

PF2240 Equity Instruments AFS by fair value hierarchy X

PF30 Debt securities X

PF31 Debt securities HFT FVO X

PF3105 Debt securities HFT/FVO X

PF3110 Debt securities HFT/FVO: Transferred assets X

PF3115 Debt securities FVO: Performing and non performing exposures

X

PF3120 Debt securities FVO: Forborne exposures X

PF3125 Debt securities HFT by counterparty X

PF3130 Debt securities FVO by counterparty X

PF3135 Debt securities FVO by counterparty: Performing and non performing exposures

X

PF3140 Debt securities FVO by counterparty: Forbone exposures X

PF3145 Debt securities HFT/FVO by residence of the counterparty X

PF3150 Debt securities HFT/FVO by fair value hierarchy X

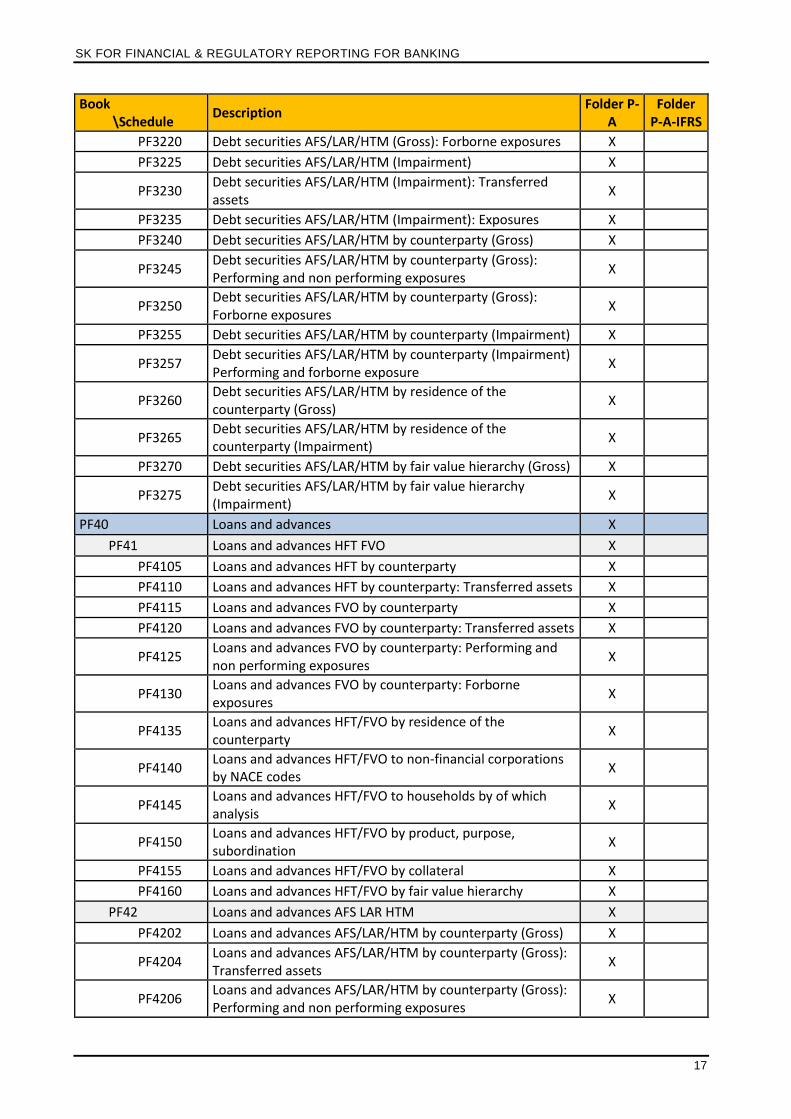

PF32 Debt securities AFS LAR HTM X

PF3205 Debt securities AFS/LAR/HTM (Gross) X

PF3210 Debt securities AFS/LAR/HTM (Gross): Transferred assets X

PF3215 Debt securities AFS/LAR/HTM (Gross): Performing and on performing exposures

X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

17

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

PF3220 Debt securities AFS/LAR/HTM (Gross): Forborne exposures X

PF3225 Debt securities AFS/LAR/HTM (Impairment) X

PF3230 Debt securities AFS/LAR/HTM (Impairment): Transferred assets

X

PF3235 Debt securities AFS/LAR/HTM (Impairment): Exposures X

PF3240 Debt securities AFS/LAR/HTM by counterparty (Gross) X

PF3245 Debt securities AFS/LAR/HTM by counterparty (Gross): Performing and non performing exposures

X

PF3250 Debt securities AFS/LAR/HTM by counterparty (Gross): Forborne exposures

X

PF3255 Debt securities AFS/LAR/HTM by counterparty (Impairment) X

PF3257 Debt securities AFS/LAR/HTM by counterparty (Impairment) Performing and forborne exposure

X

PF3260 Debt securities AFS/LAR/HTM by residence of the counterparty (Gross)

X

PF3265 Debt securities AFS/LAR/HTM by residence of the counterparty (Impairment)

X

PF3270 Debt securities AFS/LAR/HTM by fair value hierarchy (Gross) X

PF3275 Debt securities AFS/LAR/HTM by fair value hierarchy (Impairment)

X

PF40 Loans and advances X

PF41 Loans and advances HFT FVO X

PF4105 Loans and advances HFT by counterparty X

PF4110 Loans and advances HFT by counterparty: Transferred assets X

PF4115 Loans and advances FVO by counterparty X

PF4120 Loans and advances FVO by counterparty: Transferred assets X

PF4125 Loans and advances FVO by counterparty: Performing and non performing exposures

X

PF4130 Loans and advances FVO by counterparty: Forborne exposures

X

PF4135 Loans and advances HFT/FVO by residence of the counterparty

X

PF4140 Loans and advances HFT/FVO to non-financial corporations by NACE codes

X

PF4145 Loans and advances HFT/FVO to households by of which analysis

X

PF4150 Loans and advances HFT/FVO by product, purpose, subordination

X

PF4155 Loans and advances HFT/FVO by collateral X

PF4160 Loans and advances HFT/FVO by fair value hierarchy X

PF42 Loans and advances AFS LAR HTM X

PF4202 Loans and advances AFS/LAR/HTM by counterparty (Gross) X

PF4204 Loans and advances AFS/LAR/HTM by counterparty (Gross): Transferred assets

X

PF4206 Loans and advances AFS/LAR/HTM by counterparty (Gross): Performing and non performing exposures

X

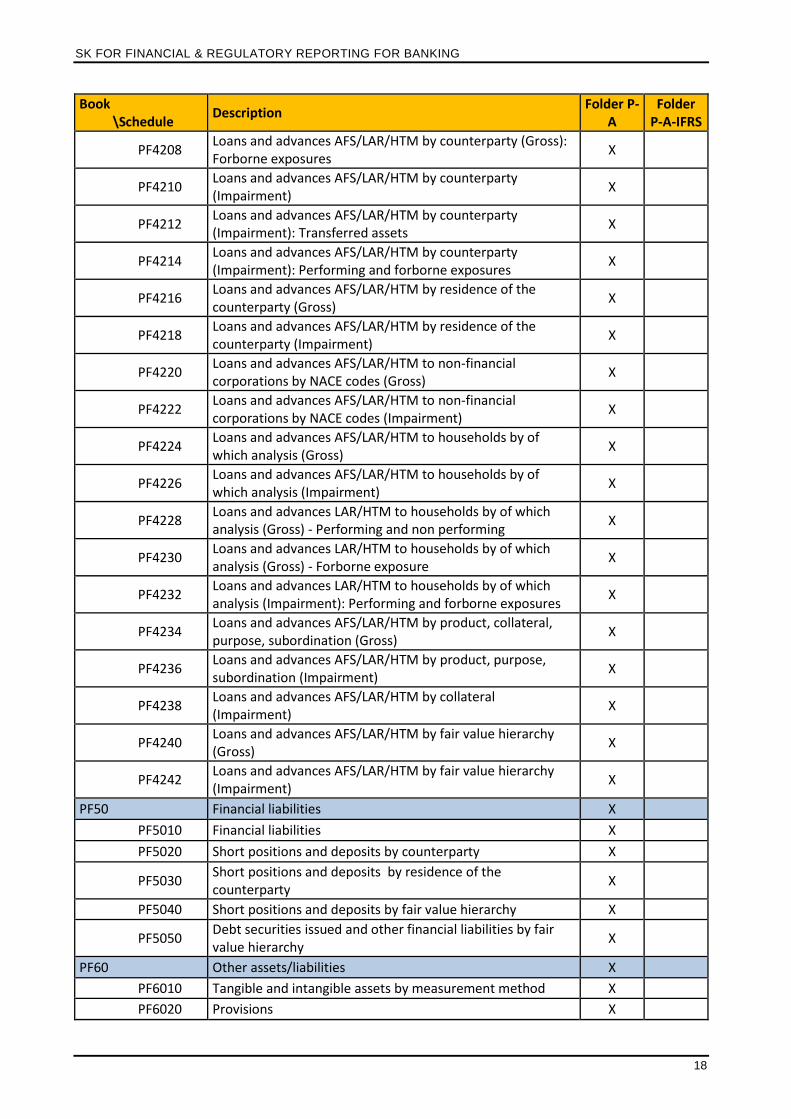

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

18

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

PF4208 Loans and advances AFS/LAR/HTM by counterparty (Gross): Forborne exposures

X

PF4210 Loans and advances AFS/LAR/HTM by counterparty (Impairment)

X

PF4212 Loans and advances AFS/LAR/HTM by counterparty (Impairment): Transferred assets

X

PF4214 Loans and advances AFS/LAR/HTM by counterparty (Impairment): Performing and forborne exposures

X

PF4216 Loans and advances AFS/LAR/HTM by residence of the counterparty (Gross)

X

PF4218 Loans and advances AFS/LAR/HTM by residence of the counterparty (Impairment)

X

PF4220 Loans and advances AFS/LAR/HTM to non-financial corporations by NACE codes (Gross)

X

PF4222 Loans and advances AFS/LAR/HTM to non-financial corporations by NACE codes (Impairment)

X

PF4224 Loans and advances AFS/LAR/HTM to households by of which analysis (Gross)

X

PF4226 Loans and advances AFS/LAR/HTM to households by of which analysis (Impairment)

X

PF4228 Loans and advances LAR/HTM to households by of which analysis (Gross) - Performing and non performing

X

PF4230 Loans and advances LAR/HTM to households by of which analysis (Gross) - Forborne exposure

X

PF4232 Loans and advances LAR/HTM to households by of which analysis (Impairment): Performing and forborne exposures

X

PF4234 Loans and advances AFS/LAR/HTM by product, collateral, purpose, subordination (Gross)

X

PF4236 Loans and advances AFS/LAR/HTM by product, purpose, subordination (Impairment)

X

PF4238 Loans and advances AFS/LAR/HTM by collateral (Impairment)

X

PF4240 Loans and advances AFS/LAR/HTM by fair value hierarchy (Gross)

X

PF4242 Loans and advances AFS/LAR/HTM by fair value hierarchy (Impairment)

X

PF50 Financial liabilities X

PF5010 Financial liabilities X

PF5020 Short positions and deposits by counterparty X

PF5030 Short positions and deposits by residence of the counterparty

X

PF5040 Short positions and deposits by fair value hierarchy X

PF5050 Debt securities issued and other financial liabilities by fair value hierarchy

X

PF60 Other assets/liabilities X

PF6010 Tangible and intangible assets by measurement method X

PF6020 Provisions X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

19

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

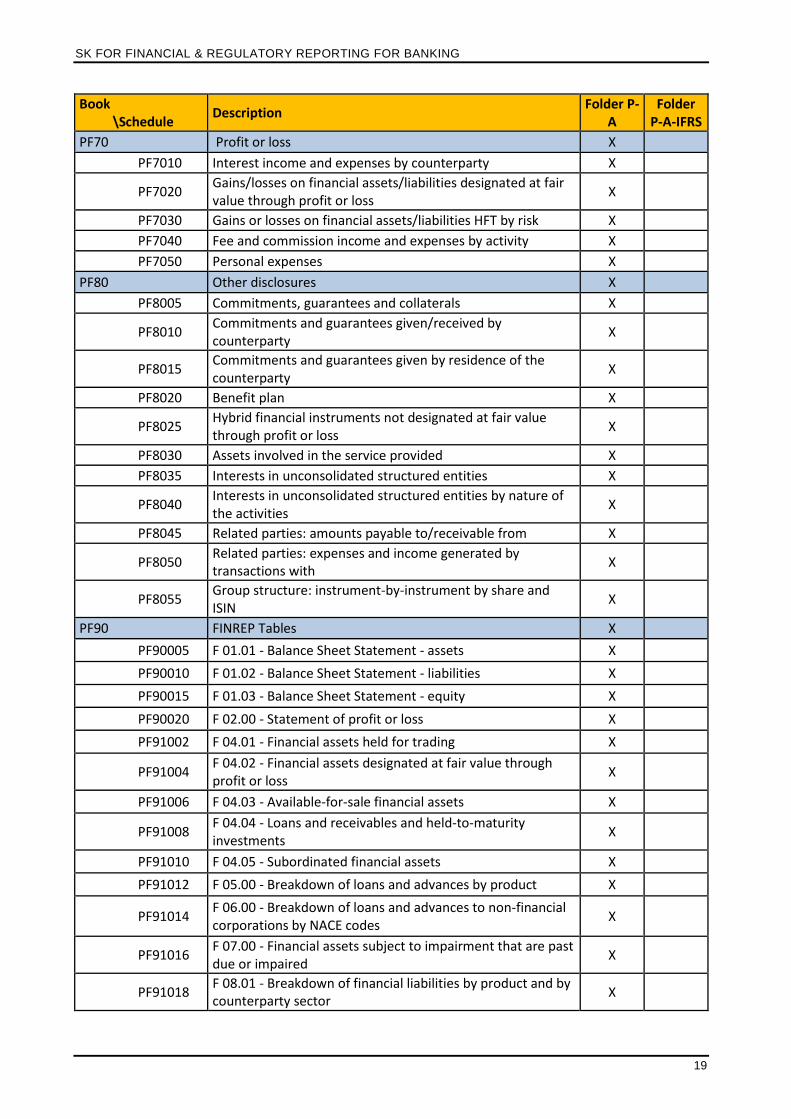

PF70 Profit or loss X

PF7010 Interest income and expenses by counterparty X

PF7020 Gains/losses on financial assets/liabilities designated at fair value through profit or loss

X

PF7030 Gains or losses on financial assets/liabilities HFT by risk X

PF7040 Fee and commission income and expenses by activity X

PF7050 Personal expenses X

PF80 Other disclosures X

PF8005 Commitments, guarantees and collaterals X

PF8010 Commitments and guarantees given/received by counterparty

X

PF8015 Commitments and guarantees given by residence of the counterparty

X

PF8020 Benefit plan X

PF8025 Hybrid financial instruments not designated at fair value through profit or loss

X

PF8030 Assets involved in the service provided X

PF8035 Interests in unconsolidated structured entities X

PF8040 Interests in unconsolidated structured entities by nature of the activities

X

PF8045 Related parties: amounts payable to/receivable from X

PF8050 Related parties: expenses and income generated by transactions with

X

PF8055 Group structure: instrument-by-instrument by share and ISIN

X

PF90 FINREP Tables X

PF90005 F 01.01 - Balance Sheet Statement - assets X

PF90010 F 01.02 - Balance Sheet Statement - liabilities X

PF90015 F 01.03 - Balance Sheet Statement - equity X

PF90020 F 02.00 - Statement of profit or loss X

PF91002 F 04.01 - Financial assets held for trading X

PF91004 F 04.02 - Financial assets designated at fair value through profit or loss

X

PF91006 F 04.03 - Available-for-sale financial assets X

PF91008 F 04.04 - Loans and receivables and held-to-maturity investments

X

PF91010 F 04.05 - Subordinated financial assets X

PF91012 F 05.00 - Breakdown of loans and advances by product X

PF91014 F 06.00 - Breakdown of loans and advances to non-financial corporations by NACE codes

X

PF91016 F 07.00 - Financial assets subject to impairment that are past due or impaired

X

PF91018 F 08.01 - Breakdown of financial liabilities by product and by counterparty sector

X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

20

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

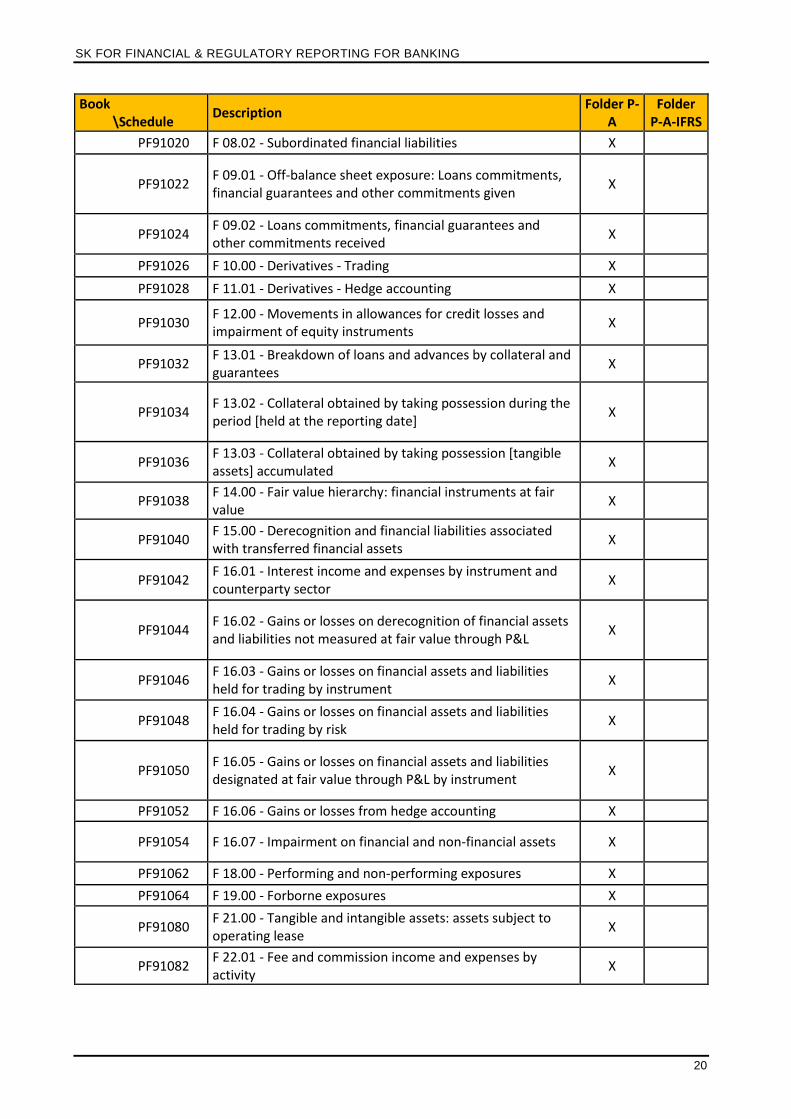

PF91020 F 08.02 - Subordinated financial liabilities X

PF91022 F 09.01 - Off-balance sheet exposure: Loans commitments, financial guarantees and other commitments given

X

PF91024 F 09.02 - Loans commitments, financial guarantees and other commitments received

X

PF91026 F 10.00 - Derivatives - Trading X

PF91028 F 11.01 - Derivatives - Hedge accounting X

PF91030 F 12.00 - Movements in allowances for credit losses and impairment of equity instruments

X

PF91032 F 13.01 - Breakdown of loans and advances by collateral and guarantees

X

PF91034 F 13.02 - Collateral obtained by taking possession during the period [held at the reporting date]

X

PF91036 F 13.03 - Collateral obtained by taking possession [tangible assets] accumulated

X

PF91038 F 14.00 - Fair value hierarchy: financial instruments at fair value

X

PF91040 F 15.00 - Derecognition and financial liabilities associated with transferred financial assets

X

PF91042 F 16.01 - Interest income and expenses by instrument and counterparty sector

X

PF91044 F 16.02 - Gains or losses on derecognition of financial assets and liabilities not measured at fair value through P&L

X

PF91046 F 16.03 - Gains or losses on financial assets and liabilities held for trading by instrument

X

PF91048 F 16.04 - Gains or losses on financial assets and liabilities held for trading by risk

X

PF91050 F 16.05 - Gains or losses on financial assets and liabilities designated at fair value through P&L by instrument

X

PF91052 F 16.06 - Gains or losses from hedge accounting X

PF91054 F 16.07 - Impairment on financial and non-financial assets X

PF91062 F 18.00 - Performing and non-performing exposures X

PF91064 F 19.00 - Forborne exposures X

PF91080 F 21.00 - Tangible and intangible assets: assets subject to operating lease

X

PF91082 F 22.01 - Fee and commission income and expenses by activity

X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

21

Book \Schedule

Description Folder P-

A Folder

P-A-IFRS

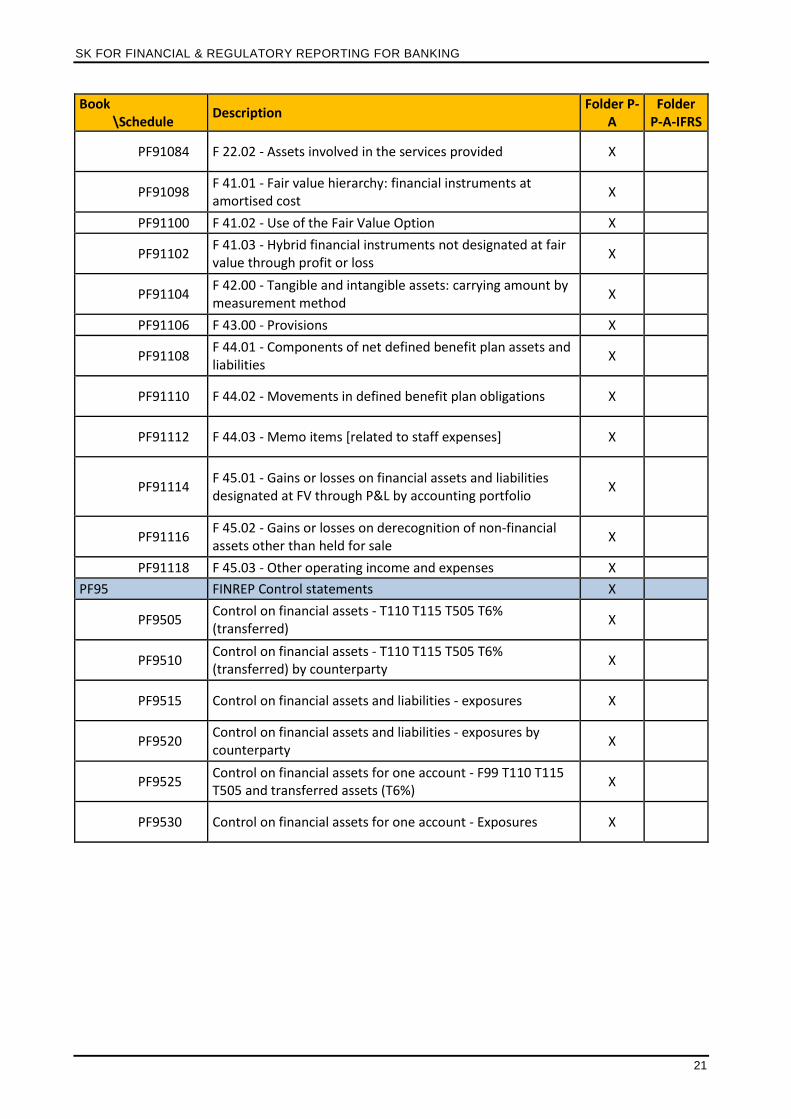

PF91084 F 22.02 - Assets involved in the services provided X

PF91098 F 41.01 - Fair value hierarchy: financial instruments at amortised cost

X

PF91100 F 41.02 - Use of the Fair Value Option X

PF91102 F 41.03 - Hybrid financial instruments not designated at fair value through profit or loss

X

PF91104 F 42.00 - Tangible and intangible assets: carrying amount by measurement method

X

PF91106 F 43.00 - Provisions X

PF91108 F 44.01 - Components of net defined benefit plan assets and liabilities

X

PF91110 F 44.02 - Movements in defined benefit plan obligations X

PF91112 F 44.03 - Memo items [related to staff expenses] X

PF91114 F 45.01 - Gains or losses on financial assets and liabilities designated at FV through P&L by accounting portfolio

X

PF91116 F 45.02 - Gains or losses on derecognition of non-financial assets other than held for sale

X

PF91118 F 45.03 - Other operating income and expenses X

PF95 FINREP Control statements X

PF9505 Control on financial assets - T110 T115 T505 T6% (transferred)

X

PF9510 Control on financial assets - T110 T115 T505 T6% (transferred) by counterparty

X

PF9515 Control on financial assets and liabilities - exposures X

PF9520 Control on financial assets and liabilities - exposures by counterparty

X

PF9525 Control on financial assets for one account - F99 T110 T115 T505 and transferred assets (T6%)

X

PF9530 Control on financial assets for one account - Exposures X

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

22

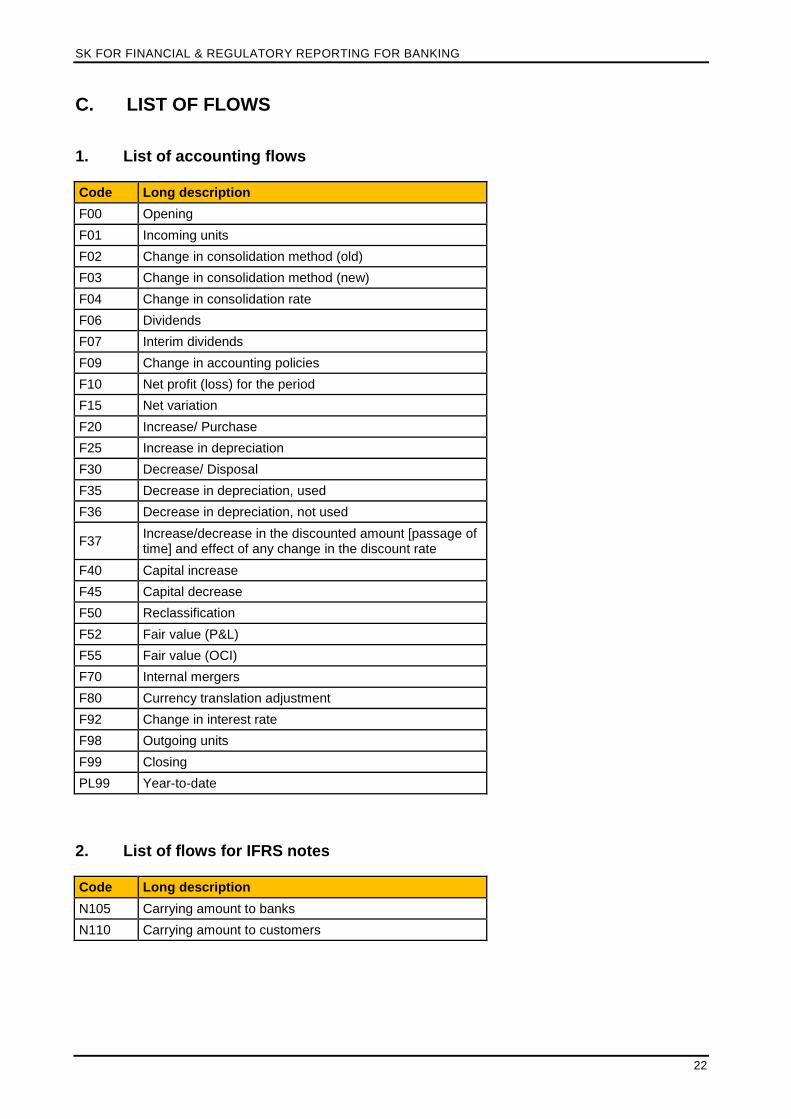

C. LIST OF FLOWS

1. List of accounting flows

Code Long description

F00 Opening

F01 Incoming units

F02 Change in consolidation method (old)

F03 Change in consolidation method (new)

F04 Change in consolidation rate

F06 Dividends

F07 Interim dividends

F09 Change in accounting policies

F10 Net profit (loss) for the period

F15 Net variation

F20 Increase/ Purchase

F25 Increase in depreciation

F30 Decrease/ Disposal

F35 Decrease in depreciation, used

F36 Decrease in depreciation, not used

F37 Increase/decrease in the discounted amount [passage of time] and effect of any change in the discount rate

F40 Capital increase

F45 Capital decrease

F50 Reclassification

F52 Fair value (P&L)

F55 Fair value (OCI)

F70 Internal mergers

F80 Currency translation adjustment

F92 Change in interest rate

F98 Outgoing units

F99 Closing

PL99 Year-to-date

2. List of flows for IFRS notes

Code Long description

N105 Carrying amount to banks

N110 Carrying amount to customers

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

23

3. List of FINREP flows

Code Long description

T105 Accumulated changes in fair value due to credit risk

T110 Of which: debt forbearance

T115 Of which: non-performing

T125 Carrying amount of unimpaired assets

T130 Carrying amount of impaired assets

T135 Accumulated write-offs

T205 Past due but not impaired ≤ 30 days

T210 Past due but not impaired > 30 days ≤ 60 days

T215 Past due but not impaired > 60 days ≤ 90 days

T220 Past due but not impaired > 90 days ≤ 180 days

T225 Past due but not impaired > 180 days ≤ 1 year

T230 Past due but not impaired > 1 year

T300 Performing

T305 Not past due or Past due <= 30 days

T310 Past due > 30 days <= 60 days

T315 Past due > 60 days <= 90 days

T320 Non-performing

T325 Unlikely to pay that are not past-due or past-due < 90 days

T330 Past due > 90 days <= 180 days

T335 Past due > 180 days <= 1 year

T340 Past due > 1 year

T350 Of which: defaulted

T355 Of which: impaired

T360 on performing exposures

T365 on non-performing exposures

T370 Unlikely to pay that are not past-due or past-due < 90 days

T375 Past due > 90 days <= 180 days

T380 Past due > 180 days <= 1 year

T385 Past due > 1 year

T390 Collateral received on non-performing exposures

T395 Financial guarantees received on non-performing exposures

T400 Performing exposures with forbearance measures

T405 Instruments with modifications in their terms and conditions

T410 Refinancing

T415 of which: Performing forborne exposures under probation

T420 Non-performing exposures with forbearance measures

T425 Instruments with modifications in their terms and conditions

T430 Refinancing

T435 of which: Defaulted

T440 of which: Impaired

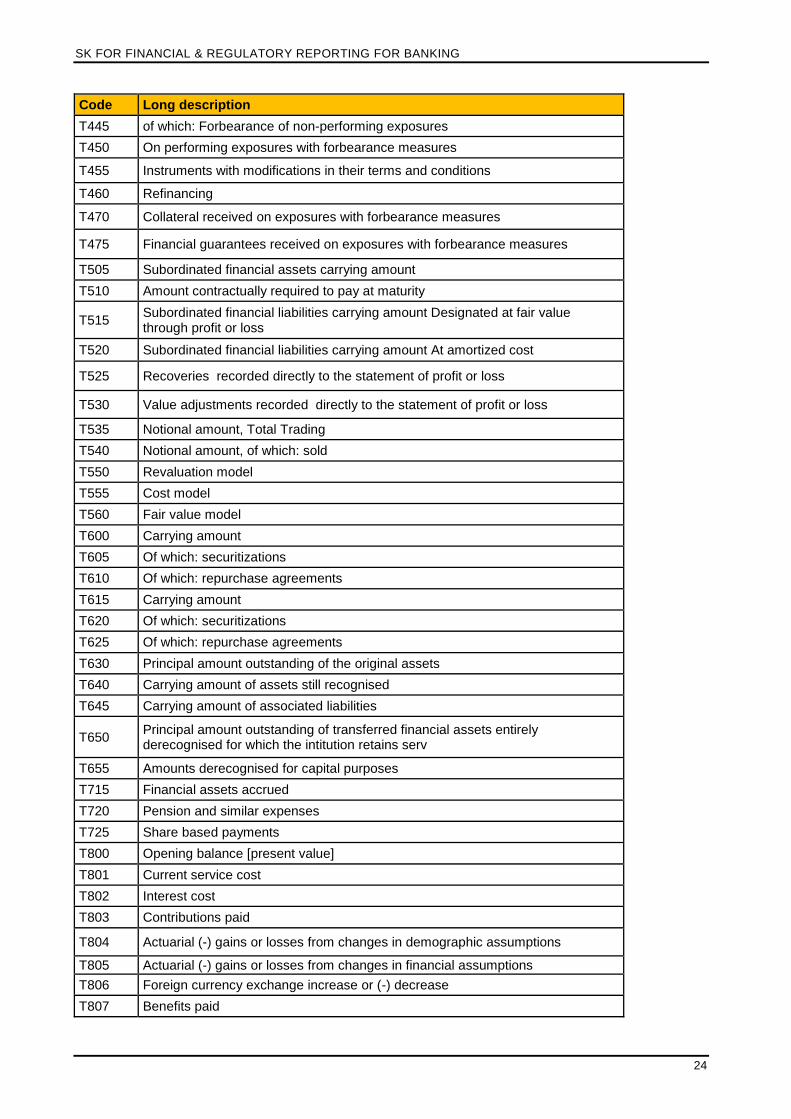

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

24

Code Long description

T445 of which: Forbearance of non-performing exposures

T450 On performing exposures with forbearance measures

T455 Instruments with modifications in their terms and conditions

T460 Refinancing

T470 Collateral received on exposures with forbearance measures

T475 Financial guarantees received on exposures with forbearance measures

T505 Subordinated financial assets carrying amount

T510 Amount contractually required to pay at maturity

T515 Subordinated financial liabilities carrying amount Designated at fair value through profit or loss

T520 Subordinated financial liabilities carrying amount At amortized cost

T525 Recoveries recorded directly to the statement of profit or loss

T530 Value adjustments recorded directly to the statement of profit or loss

T535 Notional amount, Total Trading

T540 Notional amount, of which: sold

T550 Revaluation model

T555 Cost model

T560 Fair value model

T600 Carrying amount

T605 Of which: securitizations

T610 Of which: repurchase agreements

T615 Carrying amount

T620 Of which: securitizations

T625 Of which: repurchase agreements

T630 Principal amount outstanding of the original assets

T640 Carrying amount of assets still recognised

T645 Carrying amount of associated liabilities

T650 Principal amount outstanding of transferred financial assets entirely derecognised for which the intitution retains serv

T655 Amounts derecognised for capital purposes

T715 Financial assets accrued

T720 Pension and similar expenses

T725 Share based payments

T800 Opening balance [present value]

T801 Current service cost

T802 Interest cost

T803 Contributions paid

T804 Actuarial (-) gains or losses from changes in demographic assumptions

T805 Actuarial (-) gains or losses from changes in financial assumptions

T806 Foreign currency exchange increase or (-) decrease

T807 Benefits paid

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

25

Code Long description

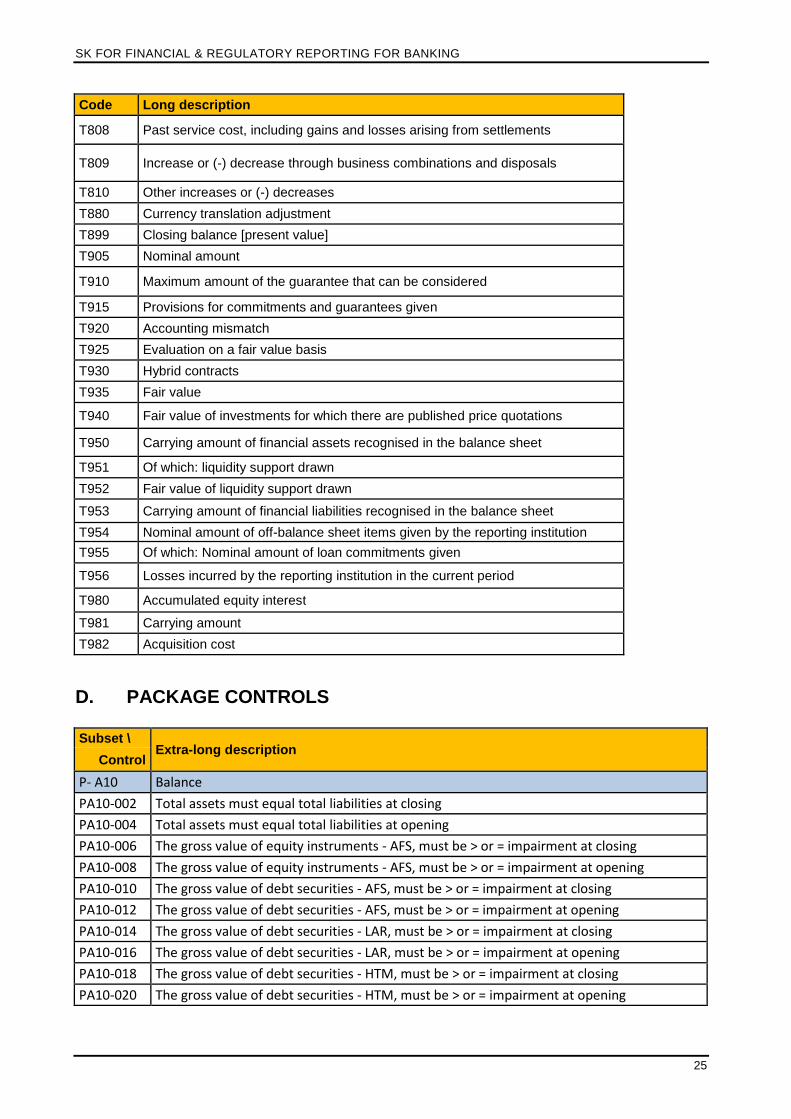

T808 Past service cost, including gains and losses arising from settlements

T809 Increase or (-) decrease through business combinations and disposals

T810 Other increases or (-) decreases

T880 Currency translation adjustment

T899 Closing balance [present value]

T905 Nominal amount

T910 Maximum amount of the guarantee that can be considered

T915 Provisions for commitments and guarantees given

T920 Accounting mismatch

T925 Evaluation on a fair value basis

T930 Hybrid contracts

T935 Fair value

T940 Fair value of investments for which there are published price quotations

T950 Carrying amount of financial assets recognised in the balance sheet

T951 Of which: liquidity support drawn

T952 Fair value of liquidity support drawn

T953 Carrying amount of financial liabilities recognised in the balance sheet

T954 Nominal amount of off-balance sheet items given by the reporting institution

T955 Of which: Nominal amount of loan commitments given

T956 Losses incurred by the reporting institution in the current period

T980 Accumulated equity interest

T981 Carrying amount

T982 Acquisition cost

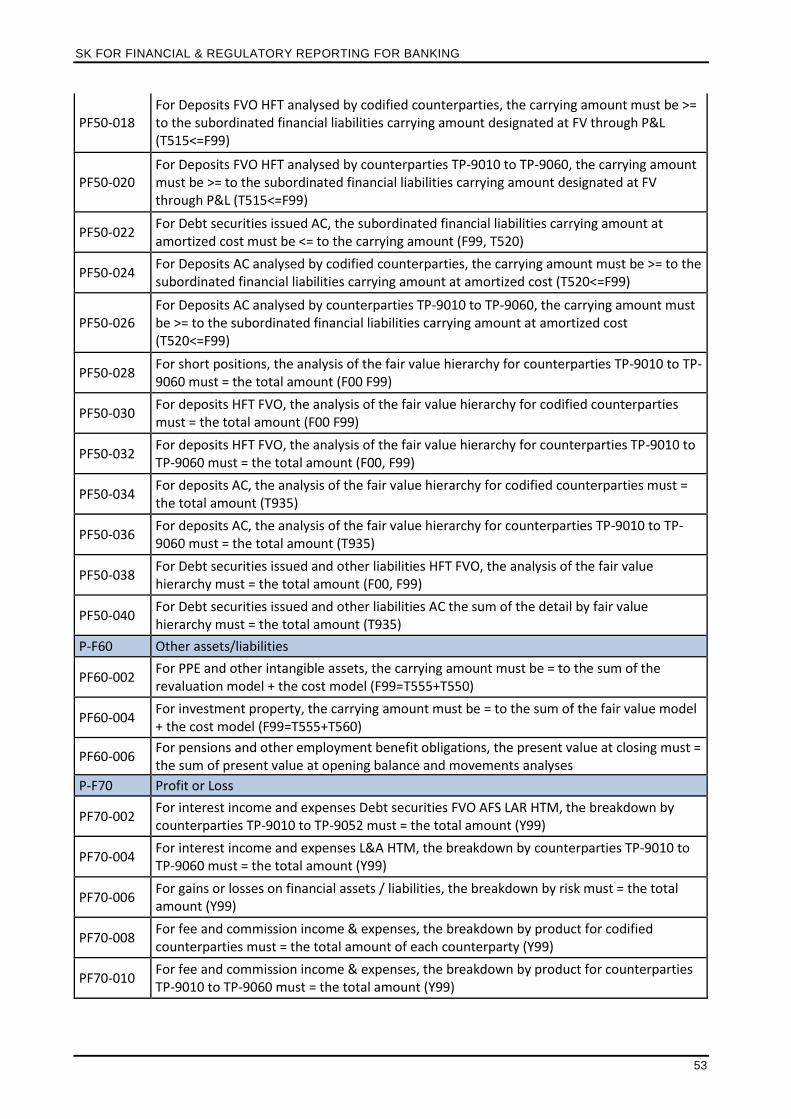

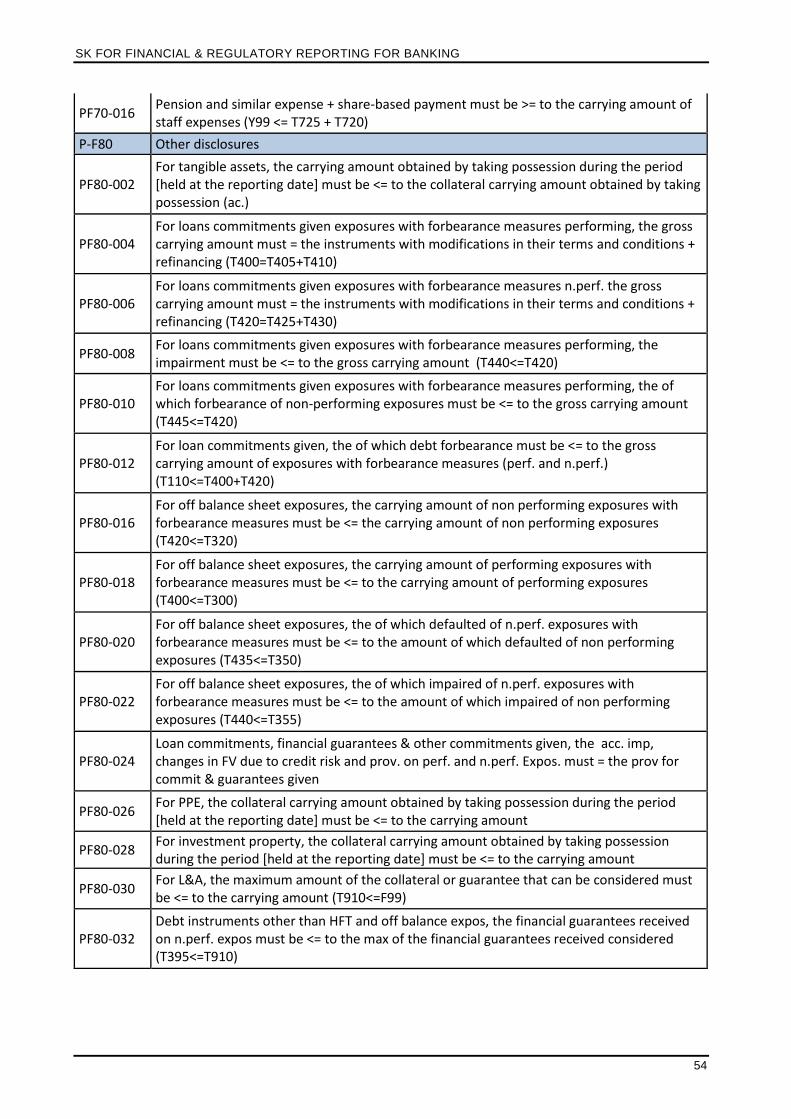

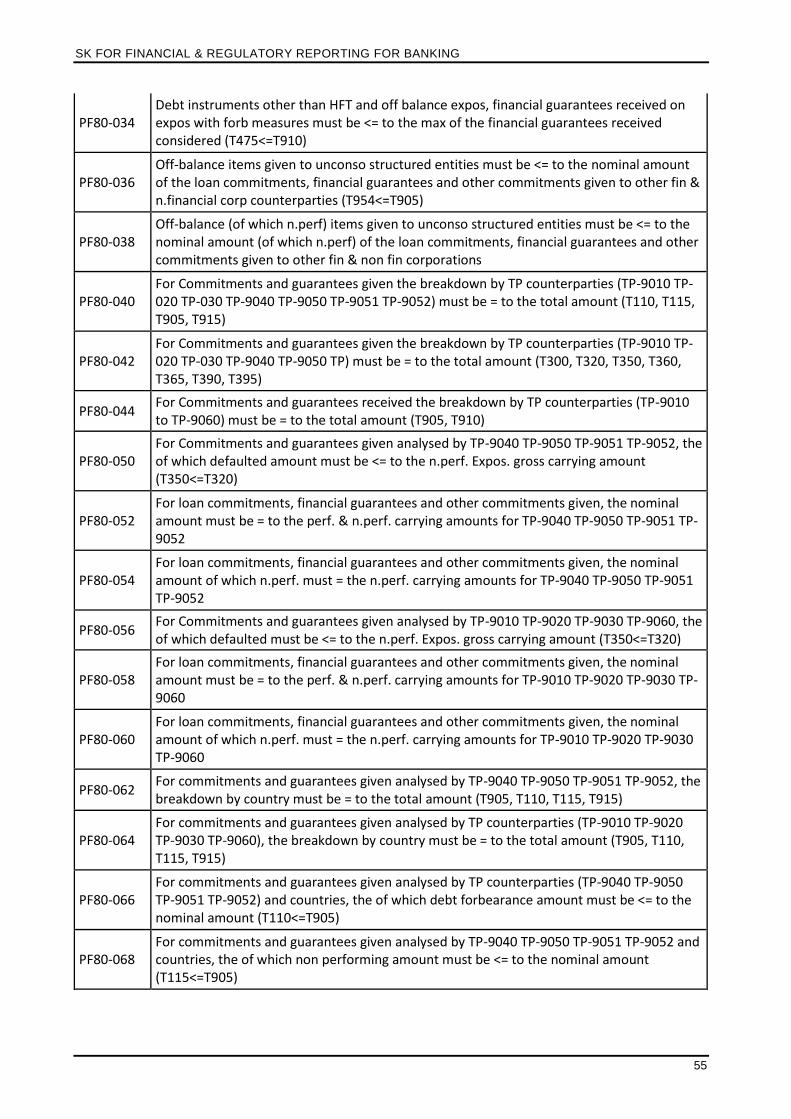

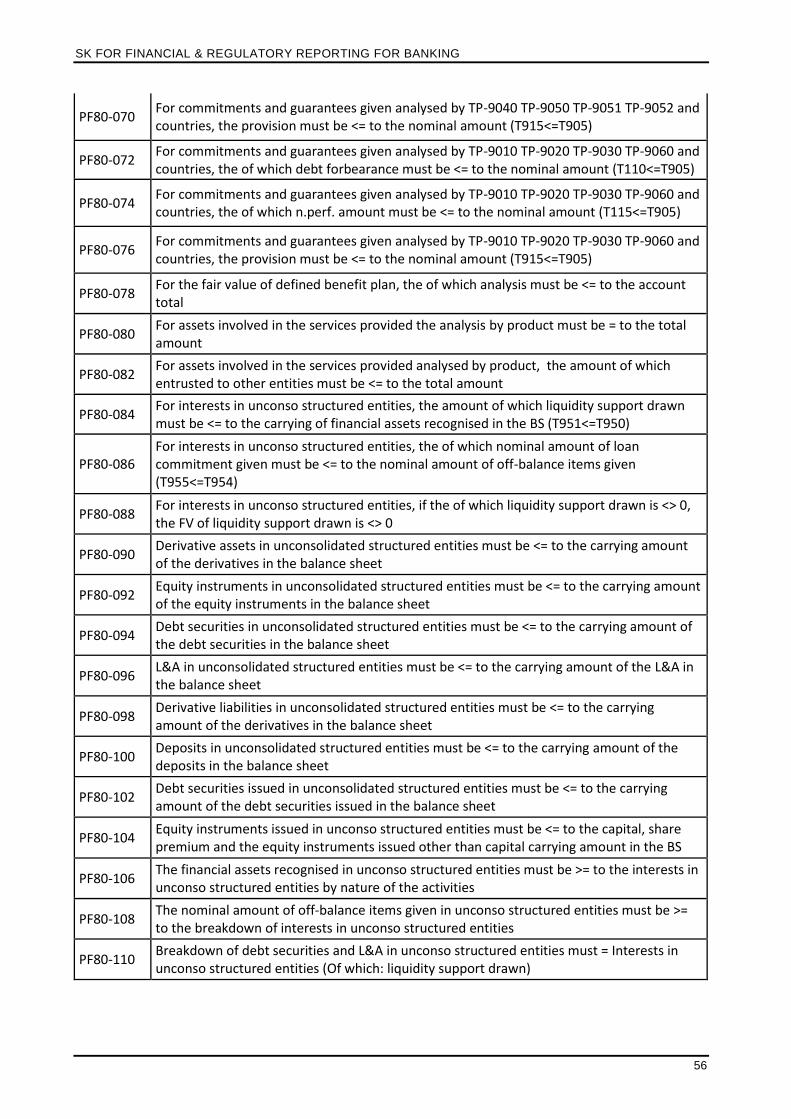

D. PACKAGE CONTROLS

Subset \ Extra-long description

Control

P- A10 Balance

PA10-002 Total assets must equal total liabilities at closing

PA10-004 Total assets must equal total liabilities at opening

PA10-006 The gross value of equity instruments - AFS, must be > or = impairment at closing

PA10-008 The gross value of equity instruments - AFS, must be > or = impairment at opening

PA10-010 The gross value of debt securities - AFS, must be > or = impairment at closing

PA10-012 The gross value of debt securities - AFS, must be > or = impairment at opening

PA10-014 The gross value of debt securities - LAR, must be > or = impairment at closing

PA10-016 The gross value of debt securities - LAR, must be > or = impairment at opening

PA10-018 The gross value of debt securities - HTM, must be > or = impairment at closing

PA10-020 The gross value of debt securities - HTM, must be > or = impairment at opening

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

26

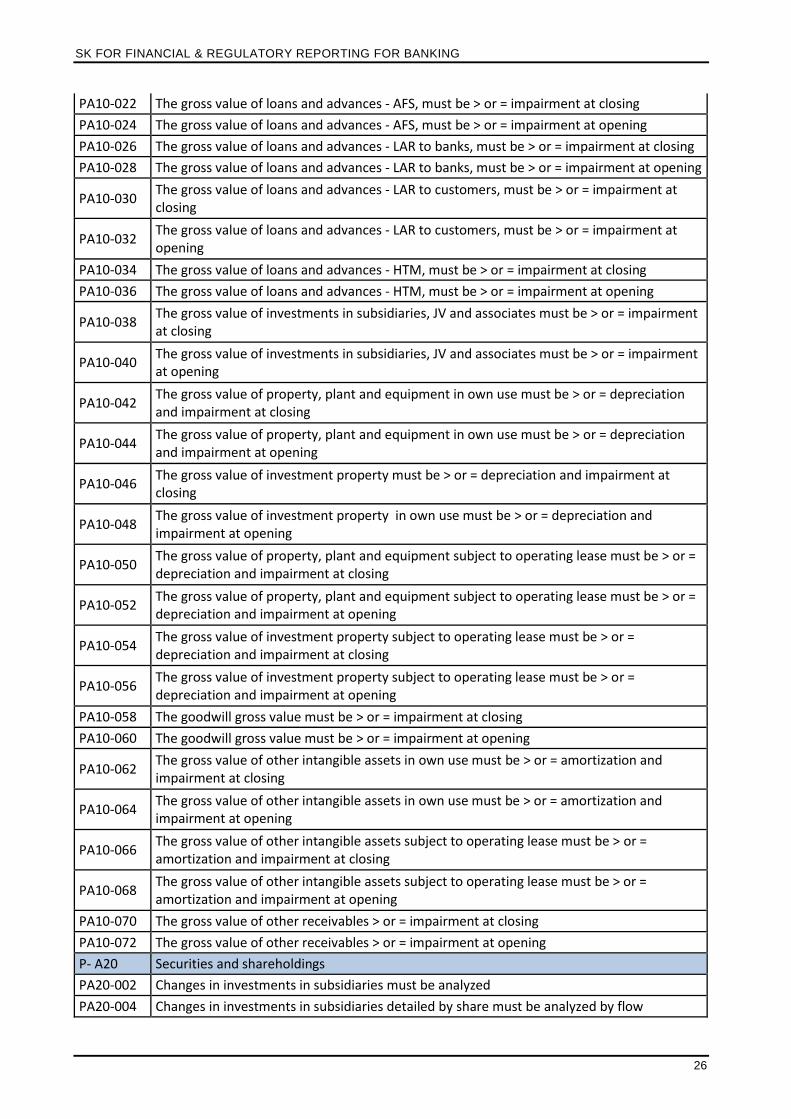

PA10-022 The gross value of loans and advances - AFS, must be > or = impairment at closing

PA10-024 The gross value of loans and advances - AFS, must be > or = impairment at opening

PA10-026 The gross value of loans and advances - LAR to banks, must be > or = impairment at closing

PA10-028 The gross value of loans and advances - LAR to banks, must be > or = impairment at opening

PA10-030 The gross value of loans and advances - LAR to customers, must be > or = impairment at closing

PA10-032 The gross value of loans and advances - LAR to customers, must be > or = impairment at opening

PA10-034 The gross value of loans and advances - HTM, must be > or = impairment at closing

PA10-036 The gross value of loans and advances - HTM, must be > or = impairment at opening

PA10-038 The gross value of investments in subsidiaries, JV and associates must be > or = impairment at closing

PA10-040 The gross value of investments in subsidiaries, JV and associates must be > or = impairment at opening

PA10-042 The gross value of property, plant and equipment in own use must be > or = depreciation and impairment at closing

PA10-044 The gross value of property, plant and equipment in own use must be > or = depreciation and impairment at opening

PA10-046 The gross value of investment property must be > or = depreciation and impairment at closing

PA10-048 The gross value of investment property in own use must be > or = depreciation and impairment at opening

PA10-050 The gross value of property, plant and equipment subject to operating lease must be > or = depreciation and impairment at closing

PA10-052 The gross value of property, plant and equipment subject to operating lease must be > or = depreciation and impairment at opening

PA10-054 The gross value of investment property subject to operating lease must be > or = depreciation and impairment at closing

PA10-056 The gross value of investment property subject to operating lease must be > or = depreciation and impairment at opening

PA10-058 The goodwill gross value must be > or = impairment at closing

PA10-060 The goodwill gross value must be > or = impairment at opening

PA10-062 The gross value of other intangible assets in own use must be > or = amortization and impairment at closing

PA10-064 The gross value of other intangible assets in own use must be > or = amortization and impairment at opening

PA10-066 The gross value of other intangible assets subject to operating lease must be > or = amortization and impairment at closing

PA10-068 The gross value of other intangible assets subject to operating lease must be > or = amortization and impairment at opening

PA10-070 The gross value of other receivables > or = impairment at closing

PA10-072 The gross value of other receivables > or = impairment at opening

P- A20 Securities and shareholdings

PA20-002 Changes in investments in subsidiaries must be analyzed

PA20-004 Changes in investments in subsidiaries detailed by share must be analyzed by flow

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

27

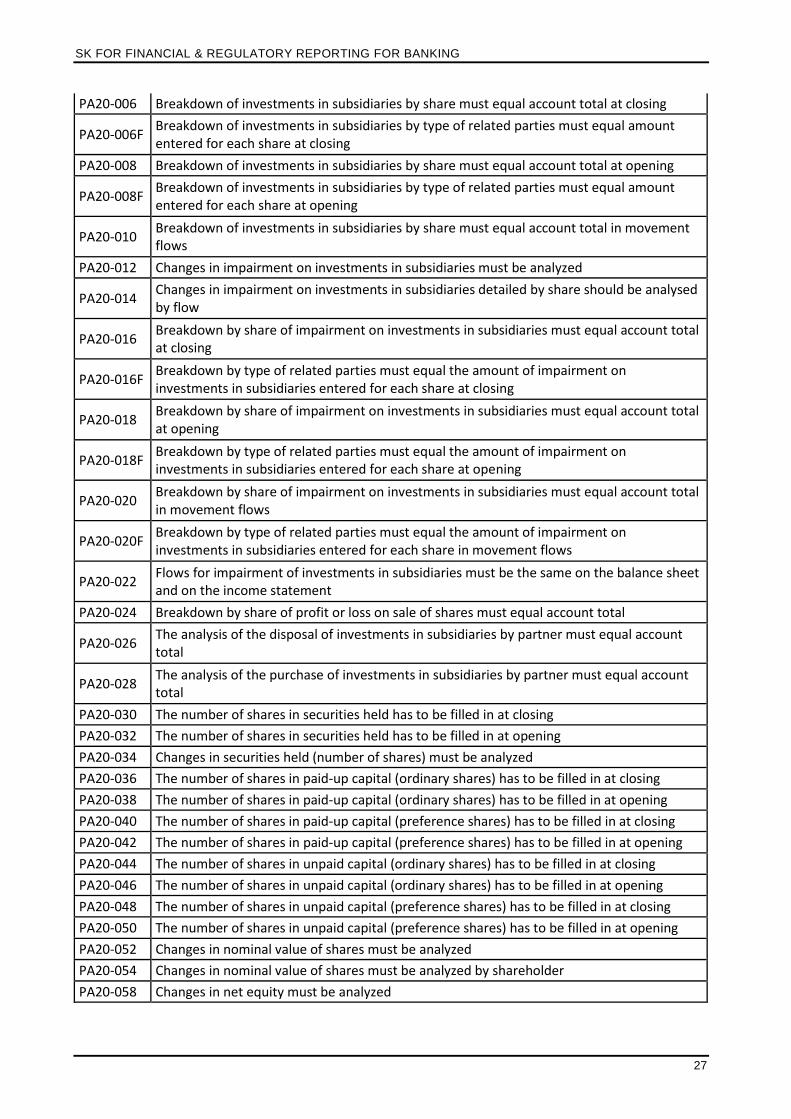

PA20-006 Breakdown of investments in subsidiaries by share must equal account total at closing

PA20-006F Breakdown of investments in subsidiaries by type of related parties must equal amount entered for each share at closing

PA20-008 Breakdown of investments in subsidiaries by share must equal account total at opening

PA20-008F Breakdown of investments in subsidiaries by type of related parties must equal amount entered for each share at opening

PA20-010 Breakdown of investments in subsidiaries by share must equal account total in movement flows

PA20-012 Changes in impairment on investments in subsidiaries must be analyzed

PA20-014 Changes in impairment on investments in subsidiaries detailed by share should be analysed by flow

PA20-016 Breakdown by share of impairment on investments in subsidiaries must equal account total at closing

PA20-016F Breakdown by type of related parties must equal the amount of impairment on investments in subsidiaries entered for each share at closing

PA20-018 Breakdown by share of impairment on investments in subsidiaries must equal account total at opening

PA20-018F Breakdown by type of related parties must equal the amount of impairment on investments in subsidiaries entered for each share at opening

PA20-020 Breakdown by share of impairment on investments in subsidiaries must equal account total in movement flows

PA20-020F Breakdown by type of related parties must equal the amount of impairment on investments in subsidiaries entered for each share in movement flows

PA20-022 Flows for impairment of investments in subsidiaries must be the same on the balance sheet and on the income statement

PA20-024 Breakdown by share of profit or loss on sale of shares must equal account total

PA20-026 The analysis of the disposal of investments in subsidiaries by partner must equal account total

PA20-028 The analysis of the purchase of investments in subsidiaries by partner must equal account total

PA20-030 The number of shares in securities held has to be filled in at closing

PA20-032 The number of shares in securities held has to be filled in at opening

PA20-034 Changes in securities held (number of shares) must be analyzed

PA20-036 The number of shares in paid-up capital (ordinary shares) has to be filled in at closing

PA20-038 The number of shares in paid-up capital (ordinary shares) has to be filled in at opening

PA20-040 The number of shares in paid-up capital (preference shares) has to be filled in at closing

PA20-042 The number of shares in paid-up capital (preference shares) has to be filled in at opening

PA20-044 The number of shares in unpaid capital (ordinary shares) has to be filled in at closing

PA20-046 The number of shares in unpaid capital (ordinary shares) has to be filled in at opening

PA20-048 The number of shares in unpaid capital (preference shares) has to be filled in at closing

PA20-050 The number of shares in unpaid capital (preference shares) has to be filled in at opening

PA20-052 Changes in nominal value of shares must be analyzed

PA20-054 Changes in nominal value of shares must be analyzed by shareholder

PA20-058 Changes in net equity must be analyzed

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

28

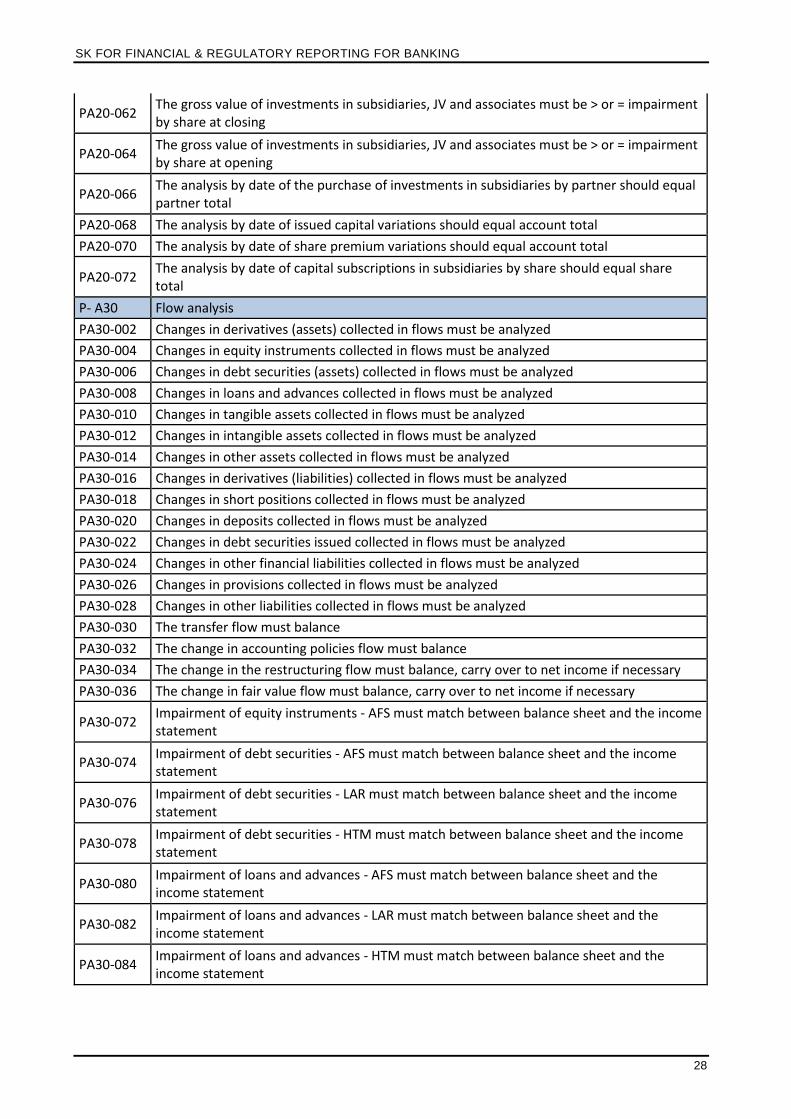

PA20-062 The gross value of investments in subsidiaries, JV and associates must be > or = impairment by share at closing

PA20-064 The gross value of investments in subsidiaries, JV and associates must be > or = impairment by share at opening

PA20-066 The analysis by date of the purchase of investments in subsidiaries by partner should equal partner total

PA20-068 The analysis by date of issued capital variations should equal account total

PA20-070 The analysis by date of share premium variations should equal account total

PA20-072 The analysis by date of capital subscriptions in subsidiaries by share should equal share total

P- A30 Flow analysis

PA30-002 Changes in derivatives (assets) collected in flows must be analyzed

PA30-004 Changes in equity instruments collected in flows must be analyzed

PA30-006 Changes in debt securities (assets) collected in flows must be analyzed

PA30-008 Changes in loans and advances collected in flows must be analyzed

PA30-010 Changes in tangible assets collected in flows must be analyzed

PA30-012 Changes in intangible assets collected in flows must be analyzed

PA30-014 Changes in other assets collected in flows must be analyzed

PA30-016 Changes in derivatives (liabilities) collected in flows must be analyzed

PA30-018 Changes in short positions collected in flows must be analyzed

PA30-020 Changes in deposits collected in flows must be analyzed

PA30-022 Changes in debt securities issued collected in flows must be analyzed

PA30-024 Changes in other financial liabilities collected in flows must be analyzed

PA30-026 Changes in provisions collected in flows must be analyzed

PA30-028 Changes in other liabilities collected in flows must be analyzed

PA30-030 The transfer flow must balance

PA30-032 The change in accounting policies flow must balance

PA30-034 The change in the restructuring flow must balance, carry over to net income if necessary

PA30-036 The change in fair value flow must balance, carry over to net income if necessary

PA30-072 Impairment of equity instruments - AFS must match between balance sheet and the income statement

PA30-074 Impairment of debt securities - AFS must match between balance sheet and the income statement

PA30-076 Impairment of debt securities - LAR must match between balance sheet and the income statement

PA30-078 Impairment of debt securities - HTM must match between balance sheet and the income statement

PA30-080 Impairment of loans and advances - AFS must match between balance sheet and the income statement

PA30-082 Impairment of loans and advances - LAR must match between balance sheet and the income statement

PA30-084 Impairment of loans and advances - HTM must match between balance sheet and the income statement

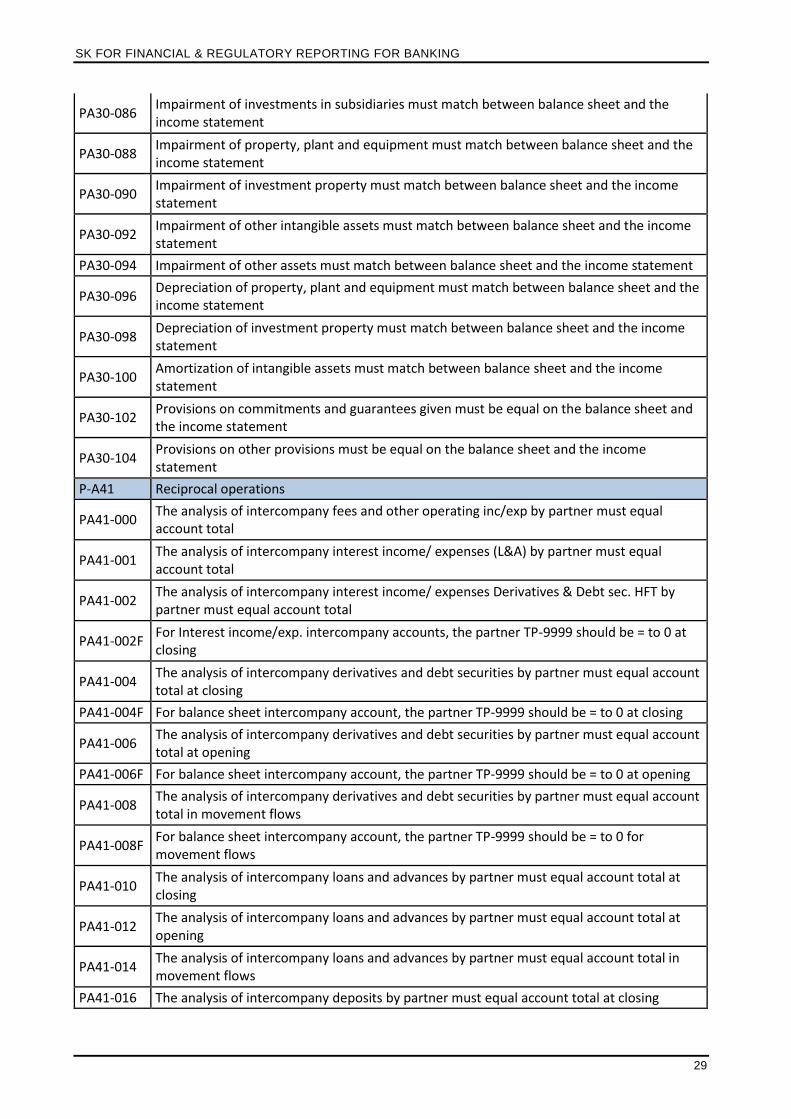

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

29

PA30-086 Impairment of investments in subsidiaries must match between balance sheet and the income statement

PA30-088 Impairment of property, plant and equipment must match between balance sheet and the income statement

PA30-090 Impairment of investment property must match between balance sheet and the income statement

PA30-092 Impairment of other intangible assets must match between balance sheet and the income statement

PA30-094 Impairment of other assets must match between balance sheet and the income statement

PA30-096 Depreciation of property, plant and equipment must match between balance sheet and the income statement

PA30-098 Depreciation of investment property must match between balance sheet and the income statement

PA30-100 Amortization of intangible assets must match between balance sheet and the income statement

PA30-102 Provisions on commitments and guarantees given must be equal on the balance sheet and the income statement

PA30-104 Provisions on other provisions must be equal on the balance sheet and the income statement

P-A41 Reciprocal operations

PA41-000 The analysis of intercompany fees and other operating inc/exp by partner must equal account total

PA41-001 The analysis of intercompany interest income/ expenses (L&A) by partner must equal account total

PA41-002 The analysis of intercompany interest income/ expenses Derivatives & Debt sec. HFT by partner must equal account total

PA41-002F For Interest income/exp. intercompany accounts, the partner TP-9999 should be = to 0 at closing

PA41-004 The analysis of intercompany derivatives and debt securities by partner must equal account total at closing

PA41-004F For balance sheet intercompany account, the partner TP-9999 should be = to 0 at closing

PA41-006 The analysis of intercompany derivatives and debt securities by partner must equal account total at opening

PA41-006F For balance sheet intercompany account, the partner TP-9999 should be = to 0 at opening

PA41-008 The analysis of intercompany derivatives and debt securities by partner must equal account total in movement flows

PA41-008F For balance sheet intercompany account, the partner TP-9999 should be = to 0 for movement flows

PA41-010 The analysis of intercompany loans and advances by partner must equal account total at closing

PA41-012 The analysis of intercompany loans and advances by partner must equal account total at opening

PA41-014 The analysis of intercompany loans and advances by partner must equal account total in movement flows

PA41-016 The analysis of intercompany deposits by partner must equal account total at closing

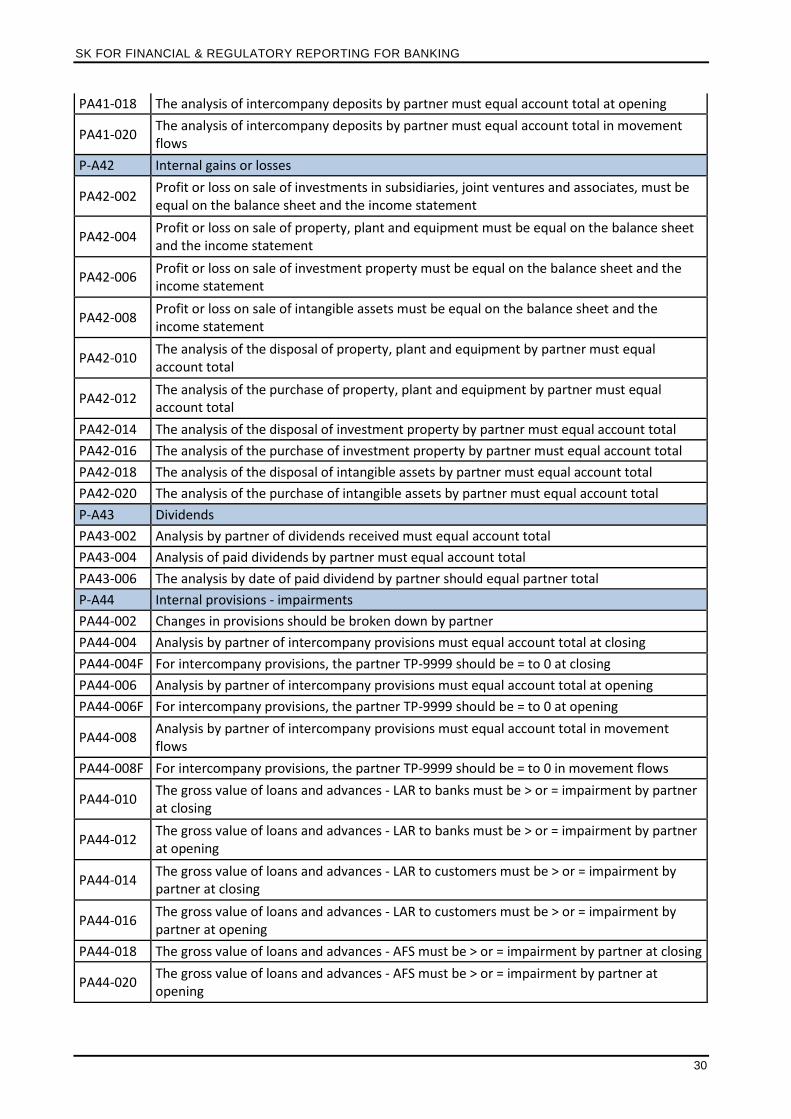

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

30

PA41-018 The analysis of intercompany deposits by partner must equal account total at opening

PA41-020 The analysis of intercompany deposits by partner must equal account total in movement flows

P-A42 Internal gains or losses

PA42-002 Profit or loss on sale of investments in subsidiaries, joint ventures and associates, must be equal on the balance sheet and the income statement

PA42-004 Profit or loss on sale of property, plant and equipment must be equal on the balance sheet and the income statement

PA42-006 Profit or loss on sale of investment property must be equal on the balance sheet and the income statement

PA42-008 Profit or loss on sale of intangible assets must be equal on the balance sheet and the income statement

PA42-010 The analysis of the disposal of property, plant and equipment by partner must equal account total

PA42-012 The analysis of the purchase of property, plant and equipment by partner must equal account total

PA42-014 The analysis of the disposal of investment property by partner must equal account total

PA42-016 The analysis of the purchase of investment property by partner must equal account total

PA42-018 The analysis of the disposal of intangible assets by partner must equal account total

PA42-020 The analysis of the purchase of intangible assets by partner must equal account total

P-A43 Dividends

PA43-002 Analysis by partner of dividends received must equal account total

PA43-004 Analysis of paid dividends by partner must equal account total

PA43-006 The analysis by date of paid dividend by partner should equal partner total

P-A44 Internal provisions - impairments

PA44-002 Changes in provisions should be broken down by partner

PA44-004 Analysis by partner of intercompany provisions must equal account total at closing

PA44-004F For intercompany provisions, the partner TP-9999 should be = to 0 at closing

PA44-006 Analysis by partner of intercompany provisions must equal account total at opening

PA44-006F For intercompany provisions, the partner TP-9999 should be = to 0 at opening

PA44-008 Analysis by partner of intercompany provisions must equal account total in movement flows

PA44-008F For intercompany provisions, the partner TP-9999 should be = to 0 in movement flows

PA44-010 The gross value of loans and advances - LAR to banks must be > or = impairment by partner at closing

PA44-012 The gross value of loans and advances - LAR to banks must be > or = impairment by partner at opening

PA44-014 The gross value of loans and advances - LAR to customers must be > or = impairment by partner at closing

PA44-016 The gross value of loans and advances - LAR to customers must be > or = impairment by partner at opening

PA44-018 The gross value of loans and advances - AFS must be > or = impairment by partner at closing

PA44-020 The gross value of loans and advances - AFS must be > or = impairment by partner at opening

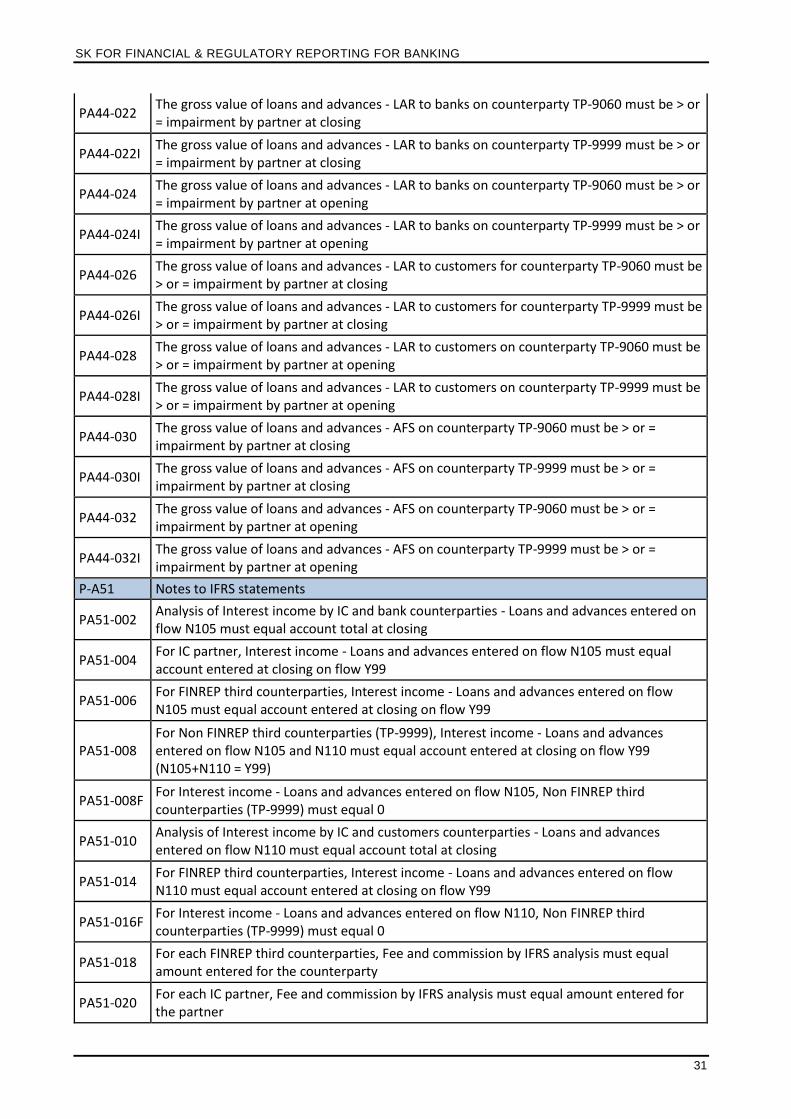

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

31

PA44-022 The gross value of loans and advances - LAR to banks on counterparty TP-9060 must be > or = impairment by partner at closing

PA44-022I The gross value of loans and advances - LAR to banks on counterparty TP-9999 must be > or = impairment by partner at closing

PA44-024 The gross value of loans and advances - LAR to banks on counterparty TP-9060 must be > or = impairment by partner at opening

PA44-024I The gross value of loans and advances - LAR to banks on counterparty TP-9999 must be > or = impairment by partner at opening

PA44-026 The gross value of loans and advances - LAR to customers for counterparty TP-9060 must be > or = impairment by partner at closing

PA44-026I The gross value of loans and advances - LAR to customers for counterparty TP-9999 must be > or = impairment by partner at closing

PA44-028 The gross value of loans and advances - LAR to customers on counterparty TP-9060 must be > or = impairment by partner at opening

PA44-028I The gross value of loans and advances - LAR to customers on counterparty TP-9999 must be > or = impairment by partner at opening

PA44-030 The gross value of loans and advances - AFS on counterparty TP-9060 must be > or = impairment by partner at closing

PA44-030I The gross value of loans and advances - AFS on counterparty TP-9999 must be > or = impairment by partner at closing

PA44-032 The gross value of loans and advances - AFS on counterparty TP-9060 must be > or = impairment by partner at opening

PA44-032I The gross value of loans and advances - AFS on counterparty TP-9999 must be > or = impairment by partner at opening

P-A51 Notes to IFRS statements

PA51-002 Analysis of Interest income by IC and bank counterparties - Loans and advances entered on flow N105 must equal account total at closing

PA51-004 For IC partner, Interest income - Loans and advances entered on flow N105 must equal account entered at closing on flow Y99

PA51-006 For FINREP third counterparties, Interest income - Loans and advances entered on flow N105 must equal account entered at closing on flow Y99

PA51-008 For Non FINREP third counterparties (TP-9999), Interest income - Loans and advances entered on flow N105 and N110 must equal account entered at closing on flow Y99 (N105+N110 = Y99)

PA51-008F For Interest income - Loans and advances entered on flow N105, Non FINREP third counterparties (TP-9999) must equal 0

PA51-010 Analysis of Interest income by IC and customers counterparties - Loans and advances entered on flow N110 must equal account total at closing

PA51-014 For FINREP third counterparties, Interest income - Loans and advances entered on flow N110 must equal account entered at closing on flow Y99

PA51-016F For Interest income - Loans and advances entered on flow N110, Non FINREP third counterparties (TP-9999) must equal 0

PA51-018 For each FINREP third counterparties, Fee and commission by IFRS analysis must equal amount entered for the counterparty

PA51-020 For each IC partner, Fee and commission by IFRS analysis must equal amount entered for the partner

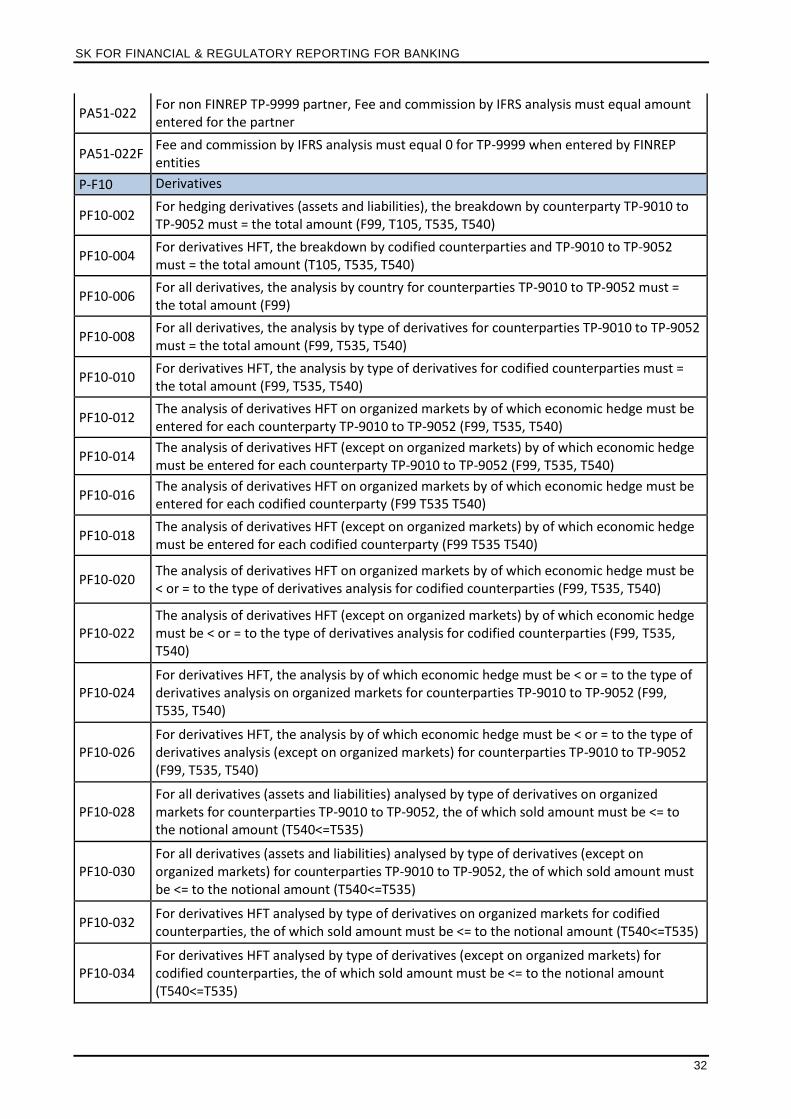

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

32

PA51-022 For non FINREP TP-9999 partner, Fee and commission by IFRS analysis must equal amount entered for the partner

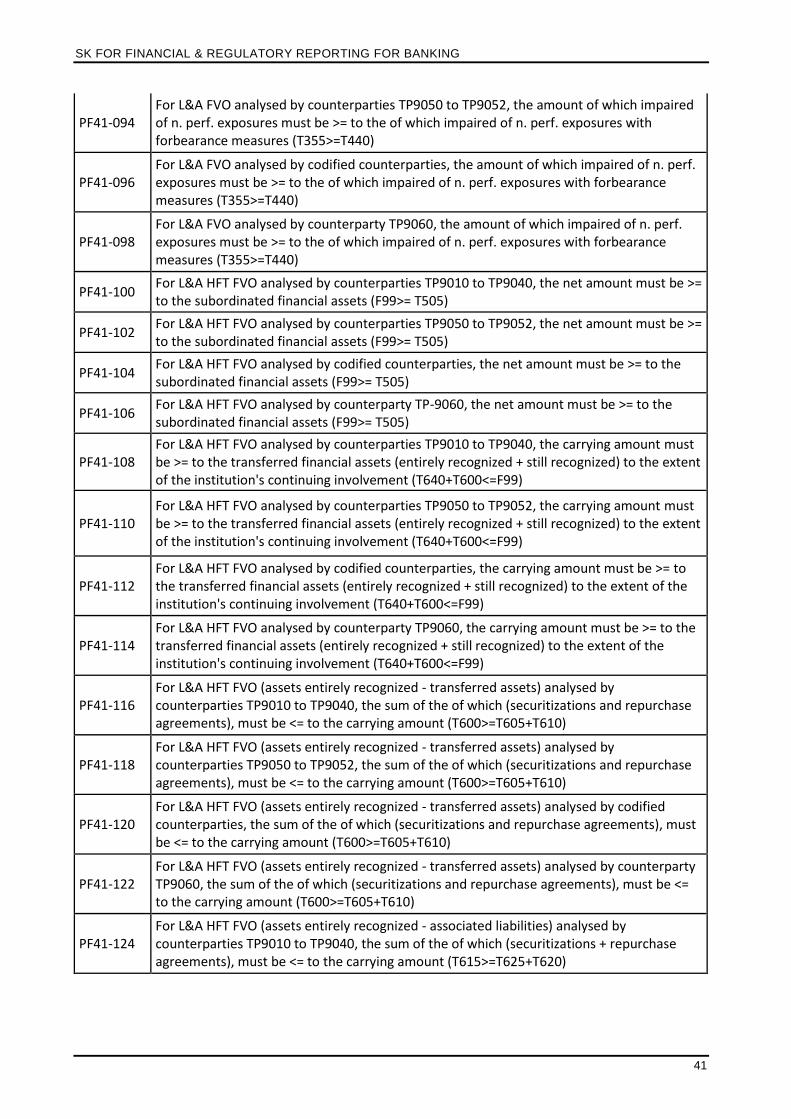

PA51-022F Fee and commission by IFRS analysis must equal 0 for TP-9999 when entered by FINREP entities

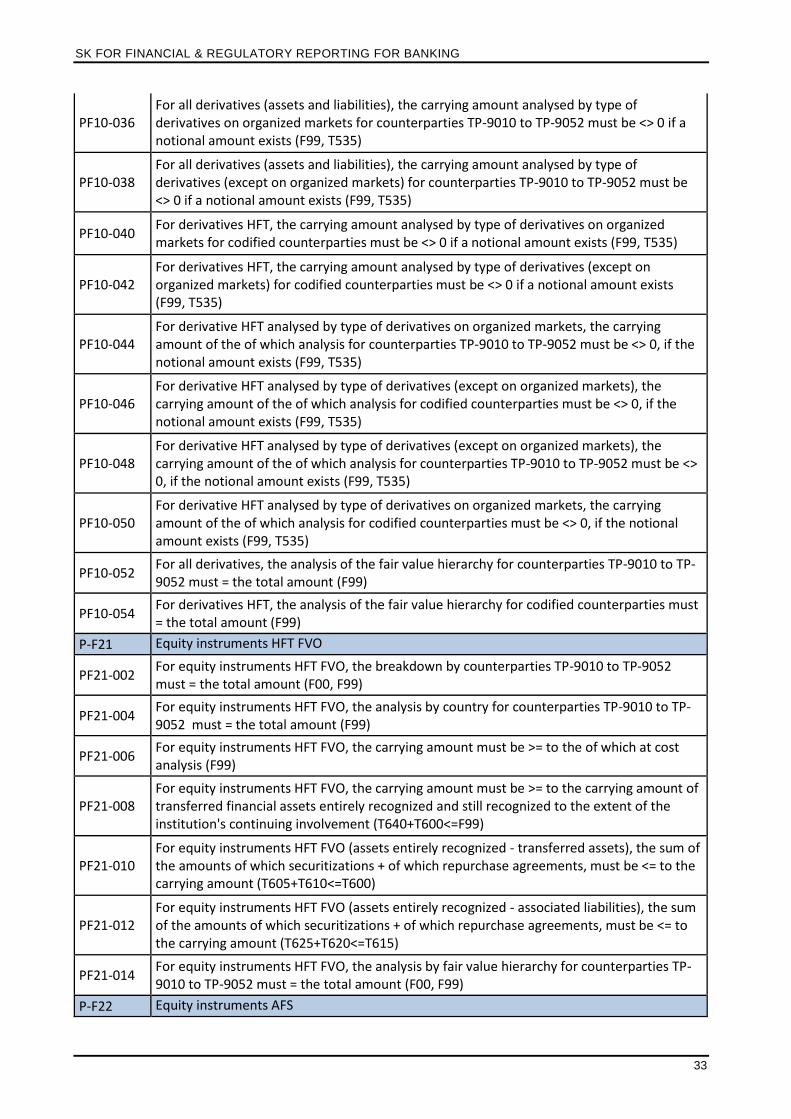

P-F10 Derivatives

PF10-002 For hedging derivatives (assets and liabilities), the breakdown by counterparty TP-9010 to TP-9052 must = the total amount (F99, T105, T535, T540)

PF10-004 For derivatives HFT, the breakdown by codified counterparties and TP-9010 to TP-9052 must = the total amount (T105, T535, T540)

PF10-006 For all derivatives, the analysis by country for counterparties TP-9010 to TP-9052 must = the total amount (F99)

PF10-008 For all derivatives, the analysis by type of derivatives for counterparties TP-9010 to TP-9052 must = the total amount (F99, T535, T540)

PF10-010 For derivatives HFT, the analysis by type of derivatives for codified counterparties must = the total amount (F99, T535, T540)

PF10-012 The analysis of derivatives HFT on organized markets by of which economic hedge must be entered for each counterparty TP-9010 to TP-9052 (F99, T535, T540)

PF10-014 The analysis of derivatives HFT (except on organized markets) by of which economic hedge must be entered for each counterparty TP-9010 to TP-9052 (F99, T535, T540)

PF10-016 The analysis of derivatives HFT on organized markets by of which economic hedge must be entered for each codified counterparty (F99 T535 T540)

PF10-018 The analysis of derivatives HFT (except on organized markets) by of which economic hedge must be entered for each codified counterparty (F99 T535 T540)

PF10-020 The analysis of derivatives HFT on organized markets by of which economic hedge must be < or = to the type of derivatives analysis for codified counterparties (F99, T535, T540)

PF10-022 The analysis of derivatives HFT (except on organized markets) by of which economic hedge must be < or = to the type of derivatives analysis for codified counterparties (F99, T535, T540)

PF10-024 For derivatives HFT, the analysis by of which economic hedge must be < or = to the type of derivatives analysis on organized markets for counterparties TP-9010 to TP-9052 (F99, T535, T540)

PF10-026 For derivatives HFT, the analysis by of which economic hedge must be < or = to the type of derivatives analysis (except on organized markets) for counterparties TP-9010 to TP-9052 (F99, T535, T540)

PF10-028 For all derivatives (assets and liabilities) analysed by type of derivatives on organized markets for counterparties TP-9010 to TP-9052, the of which sold amount must be <= to the notional amount (T540<=T535)

PF10-030 For all derivatives (assets and liabilities) analysed by type of derivatives (except on organized markets) for counterparties TP-9010 to TP-9052, the of which sold amount must be <= to the notional amount (T540<=T535)

PF10-032 For derivatives HFT analysed by type of derivatives on organized markets for codified counterparties, the of which sold amount must be <= to the notional amount (T540<=T535)

PF10-034 For derivatives HFT analysed by type of derivatives (except on organized markets) for codified counterparties, the of which sold amount must be <= to the notional amount (T540<=T535)

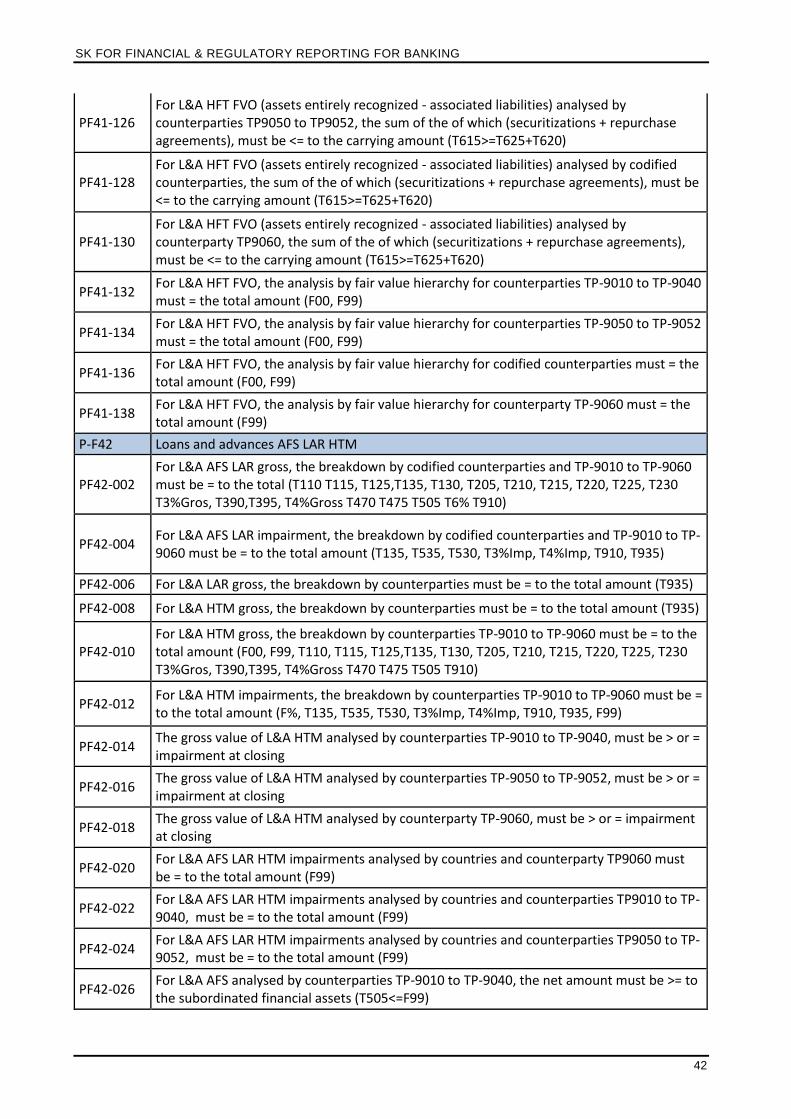

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

33

PF10-036 For all derivatives (assets and liabilities), the carrying amount analysed by type of derivatives on organized markets for counterparties TP-9010 to TP-9052 must be <> 0 if a notional amount exists (F99, T535)

PF10-038 For all derivatives (assets and liabilities), the carrying amount analysed by type of derivatives (except on organized markets) for counterparties TP-9010 to TP-9052 must be <> 0 if a notional amount exists (F99, T535)

PF10-040 For derivatives HFT, the carrying amount analysed by type of derivatives on organized markets for codified counterparties must be <> 0 if a notional amount exists (F99, T535)

PF10-042 For derivatives HFT, the carrying amount analysed by type of derivatives (except on organized markets) for codified counterparties must be <> 0 if a notional amount exists (F99, T535)

PF10-044 For derivative HFT analysed by type of derivatives on organized markets, the carrying amount of the of which analysis for counterparties TP-9010 to TP-9052 must be <> 0, if the notional amount exists (F99, T535)

PF10-046 For derivative HFT analysed by type of derivatives (except on organized markets), the carrying amount of the of which analysis for codified counterparties must be <> 0, if the notional amount exists (F99, T535)

PF10-048 For derivative HFT analysed by type of derivatives (except on organized markets), the carrying amount of the of which analysis for counterparties TP-9010 to TP-9052 must be <> 0, if the notional amount exists (F99, T535)

PF10-050 For derivative HFT analysed by type of derivatives on organized markets, the carrying amount of the of which analysis for codified counterparties must be <> 0, if the notional amount exists (F99, T535)

PF10-052 For all derivatives, the analysis of the fair value hierarchy for counterparties TP-9010 to TP-9052 must = the total amount (F99)

PF10-054 For derivatives HFT, the analysis of the fair value hierarchy for codified counterparties must = the total amount (F99)

P-F21 Equity instruments HFT FVO

PF21-002 For equity instruments HFT FVO, the breakdown by counterparties TP-9010 to TP-9052 must = the total amount (F00, F99)

PF21-004 For equity instruments HFT FVO, the analysis by country for counterparties TP-9010 to TP-9052 must = the total amount (F99)

PF21-006 For equity instruments HFT FVO, the carrying amount must be >= to the of which at cost analysis (F99)

PF21-008 For equity instruments HFT FVO, the carrying amount must be >= to the carrying amount of transferred financial assets entirely recognized and still recognized to the extent of the institution's continuing involvement (T640+T600<=F99)

PF21-010 For equity instruments HFT FVO (assets entirely recognized - transferred assets), the sum of the amounts of which securitizations + of which repurchase agreements, must be <= to the carrying amount (T605+T610<=T600)

PF21-012 For equity instruments HFT FVO (assets entirely recognized - associated liabilities), the sum of the amounts of which securitizations + of which repurchase agreements, must be <= to the carrying amount (T625+T620<=T615)

PF21-014 For equity instruments HFT FVO, the analysis by fair value hierarchy for counterparties TP-9010 to TP-9052 must = the total amount (F00, F99)

P-F22 Equity instruments AFS

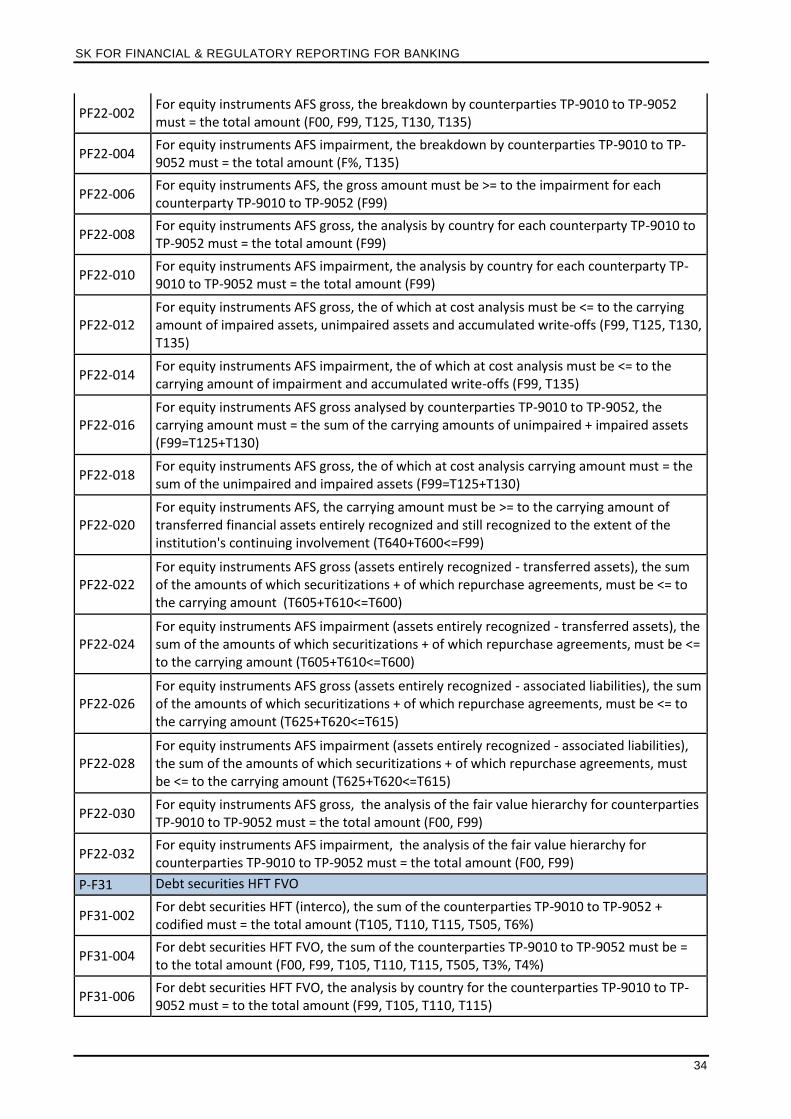

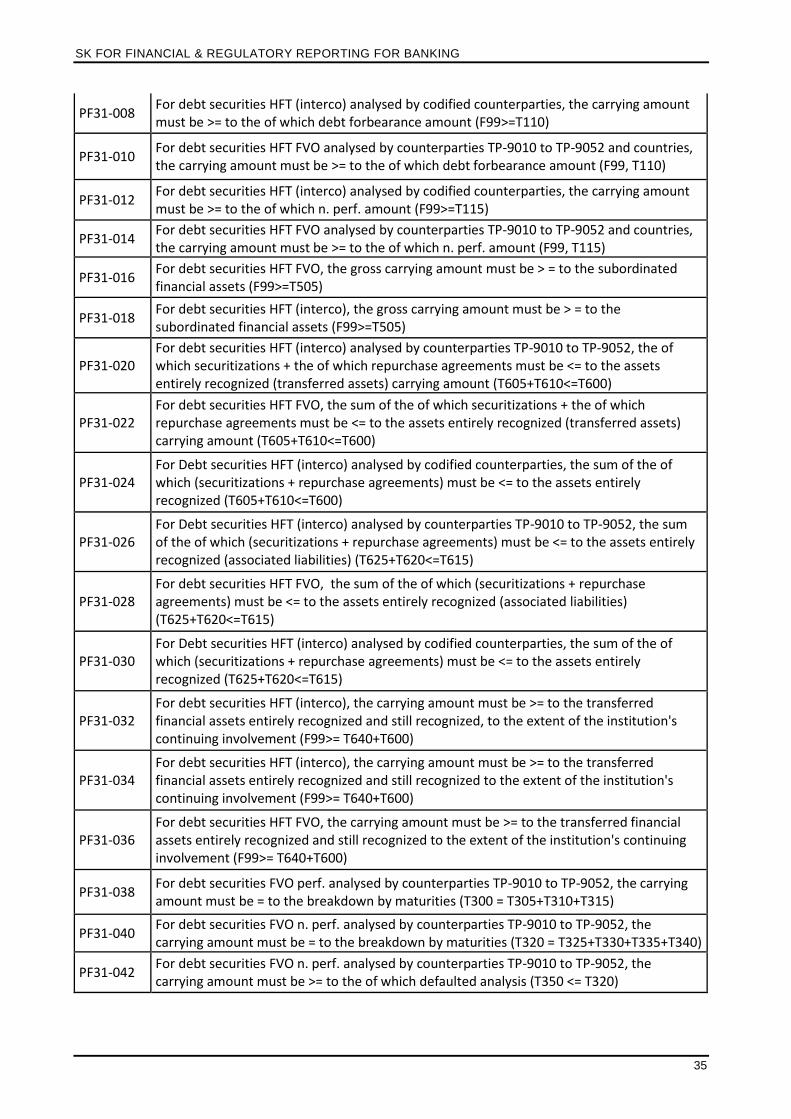

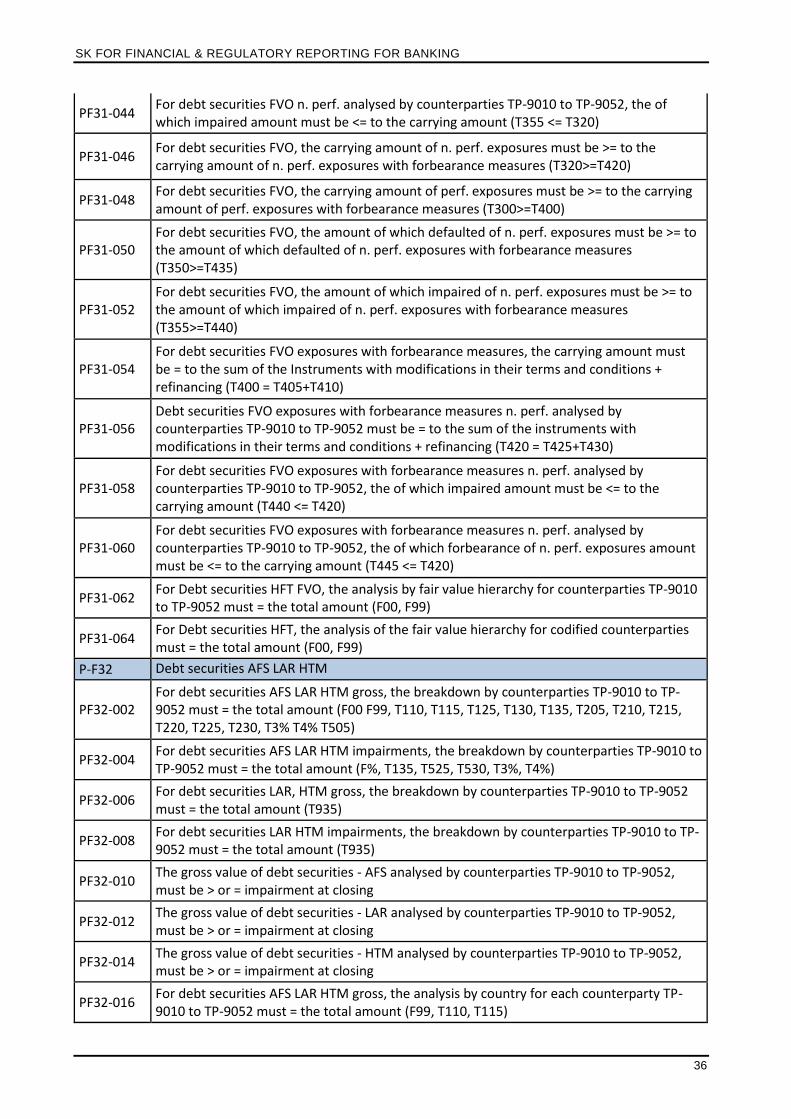

SK FOR FINANCIAL & REGULATORY REPORTING FOR BANKING

34

PF22-002 For equity instruments AFS gross, the breakdown by counterparties TP-9010 to TP-9052 must = the total amount (F00, F99, T125, T130, T135)

PF22-004 For equity instruments AFS impairment, the breakdown by counterparties TP-9010 to TP-9052 must = the total amount (F%, T135)

PF22-006 For equity instruments AFS, the gross amount must be >= to the impairment for each counterparty TP-9010 to TP-9052 (F99)

PF22-008 For equity instruments AFS gross, the analysis by country for each counterparty TP-9010 to TP-9052 must = the total amount (F99)

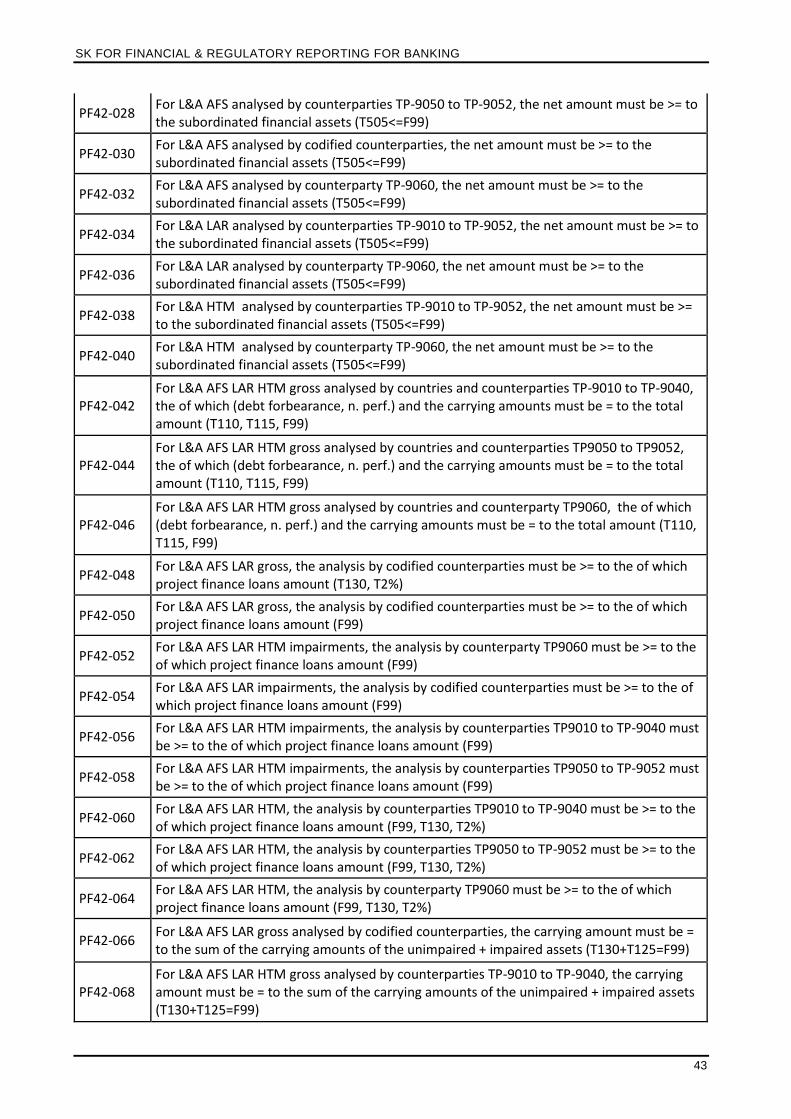

PF22-010 For equity instruments AFS impairment, the analysis by country for each counterparty TP-9010 to TP-9052 must = the total amount (F99)