Salzer ElectronicsSwitching on Growth

Analyst: Tarang Bhanushali

Stock Data

Sensex: 23,779

52 Week h/l (Rs): 364 / 160

Market cap (Rscr) : 251

6m Avg t/o (Rscr): 3

Bloomberg code: SZE IB

BSE code: 517059

NSE code: SALZERELEC

FV (Rs): 10

Div yield (%): 0.8

Prices as on Mar 1, 2016

Company Rating Grid

Low High

1 2 3 4 5

Earnings Growth

Cash Flow

B/S Strength

Valuation appeal

Risk

Shareholding Pattern

Jun‐15 Sep‐15 Dec‐15

Promoters 31.3 25.8 25.8

FII+DII 1.8 18.1 14.7

Others 66.9 56.1 59.5

Share Price Trend

40

60

80

100

120

140

160

Mar‐15 Jun‐15 Oct‐15 Feb‐16

Salzer Electronics Sensex

Salzer Electronics Ltd Switching on Growth

BUY Sector: Industrials Sector View: Positive

CMP: Rs181 1‐yr Target: Rs253 Upside: 40%

This report is published by IIFL ‘India Private Clients’ research desk. IIFL has other business units with independent research teams separated by 'Chinese walls' catering to different sets of customers having varying objectives, risk profiles, investment horizon, etc. The views and opinions expressed in this document may at times be contrary in terms of rating, target prices,

estimates and views on sectors and markets… (Read the complete disclaimer at the back of this report)

Company Report

March 02, 2016

Salzer Electronics Ltd has transformed itself from a rotary switch manufacturer to a leading player that offers total and customized electrical solutions. The company has added a range of products over the past three decades and is a preferred supplier to OEMs such as GE and Schneider. It is the largest supplier of rotary and load break switches to Indian Railways. The company provides superior customized products backed by tie‐ups with global electrical majors, in‐house manufacturing capabilities, and strong R&D. We expect the company to witness 21.9% revenue CAGR over FY15‐18, driven by a strong product portfolio, introduction of new products, and revival in demand for electrical products. The company is focused on expanding its high‐margin industrial switch gear segment. This coupled with lower interest expenses will enable the company to clock 29.5% earnings CAGR over the same period. Buoyed by a healthy balance sheet following capital infusion and strong earnings growth, we initiate coverage on the company with a BUY rating for a target price of Rs. 253.

Strong product portfolio to lead revenue growth Salzer has constantly managed to add new products to its basket via agreements with foreign partners or through in‐house engineering and R&D. The company is the largest manufacturer and is a market leader in CAM operated rotary switches. The company has established strong relationships across the world, backed by robust engineering capabilities. It also has a marketing tie‐up with Larsen & Toubro to sell its building products to retail customers. The company’s industrial switch gear business (52% revenue share in FY15) registered strong growth (20% CAGR) over the last two years, backed by introduction of new products, and repeat orders. Salzer expects to launch four new products in this segment over FY15‐17: three phase dry type transformer, latching relay, and motor protection circuit breaker (MPCB) and capacitor. These products will likely boost topline. We estimate 21.9% revenue CAGR over FY15‐18, led by 20% CAGR in the existing industrial switchgear business and contribution of Rs. 80cr from new products.

Financial Highlights Y/e 31 Mar (Rs cr) FY15 FY16E FY17E FY18E

Revenues 283.3 364.2 409.1 514.1

yoy growth (%) 15.9 28.5 12.3 25.7

Operating profit 35.5 47.1 53.0 69.4

OPM (%) 12.5 12.9 12.9 13.5

Reported PAT 12.0 20.0 23.7 35.2

yoy growth (%) 41.9 67.0 18.5 48.5

EPS (Rs) 11.7 14.4 17.0 25.3

P/E (x) 15.4 12.5 10.6 7.1

EV/EBITDA (x) 7.6 6.6 5.8 4.4

Debt/Equity (x) 0.9 0.4 0.3 0.3

RoE (%) 11.7 12.5 10.6 14.1

RoCE (%) 15.4 16.3 14.9 18.7 Source: Company, India Infoline Research

Page 2 of 20

Salzer Electronics Ltd

Revenue share of the industrial switchgear segment is expected to increase from 51.9% in FY15 to 65.5% over the next three years Led by strong revenue growth and expansion in margins, operating profit would clock 25.1% CAGR over FY15‐18E

Margins to expand due to higher share of switchgear business We expect the company to report 40bps expansion in margins in FY16, led by strong revenue growth, focus on high‐margin products, and lower commodity prices. Margins would also benefit from the execution of energy management orders in FY16. Revenue share of the industrial switchgear segment is expected to increase from 51.9% in FY15 to 65.5% over the next three years, owing to the addition of new products and company’s increased focus on this segment. Margins in the industrial switchgear segment (16‐18%) are higher compared with the other two segments (8‐10%). We envisage further expansions in margins to 13.5% in FY18 from 12.5% in FY15 as a result of higher contribution from the switchgear segment, higher execution, and lower commodity prices.

Earnings to surge 2.2x over FY15-18E

Led by strong revenue growth and expansion in margins, operating profit would clock 25.1% CAGR over FY15‐18E. Following the recent equity infusion via QIP and preferential allotment to promoters, we expect interest costs to decline. The company will likely register PAT CAGR of 43.2% over FY15‐18E driven by a combination of jump in operating profit and lower interest costs. Recent QIP and full conversion of warrants would lead to 35% dilution on FY15 equity base. Consequently, earnings CAGR would be lower at 29.5% over the sale period. The scrip is trading at 7.2x FY18E P/E, which we believe is relatively attractive, as earnings growth is expected to be robust over the next three years. We value the company at 10x FY18 EPS of Rs. 25.3 for a target price of Rs. 253, an upside of 40% from current levels.

Rerating to continue on the back of strong earnings growth

Source: Company, India Infoline Research

0

5

10

15

20

25

Apr‐10 Jan‐11 Nov‐11 Sep‐12 Jul‐13 May‐14 Mar‐15 Jan‐16

(X) P/E Average

0

50

100

150

200

250

300

350

400

450

Apr‐10 Dec‐10 Sep‐11May‐12 Feb‐13 Nov‐13 Jul‐14 Apr‐15 Jan‐16

(Rs) 20.4

16.5

12.5x

8.5x

4.6x

Page 3 of 20

Salzer Electronics Ltd

Switchgear is the largest segment with more than 10 products and a revenue contribution of 52% in FY15

The company manufactures more than 15 products catering to different industries through its five in‐house manufacturing facilities It is the largest supplier of rotary and load break switches to the Indian Railways

Strong product portfolio Salzer Electronics Limited was established in 1985 to design and manufacture CAM operated rotary switches in technical collaboration with M/s. Saelzer Schaltgerate Fabrik, GmbH., Germany. Post this, the company has transformed into a leading player that offers total and customized electrical solutions in switchgear, wires and cables, and energy management systems. Salzer operates in four segments: switchgear, building segment, wires and cables, and energy management. Switchgear is the largest segment with more than 10 products and a revenue contribution of 52% in FY15. The company has continuously achieved leadership position in the following segments: (1) Market Leader in the rotary switches business with 40% market share and the largest producer in Asia; (2) Largest producer of cable ducts (wiring channels) in Asia; and (3) Largest exporter of load break switches from India. The company is the largest manufacturer of CAM operated rotary switches with 25%market share. The company has introduced new projects, owing to its strong engineering capabilities backed by robust in‐house manufacturing and R&D over the years. Product portfolio

Industrial Switch Gear Business Building segment Business

Transformers Modular Switches

Terminal Blocks Wires & Cables

Rotary Switches MCBs (Under Development)

Isolators Changeovers

General Purpose relays

Wiring Ducts Copper Business

MPCBs Wires & Cables

Contactors & OLRs Flexible Bus Bars

Control Panels Enameled Wires

Bunched Conductors

Energy Management Business Tinned Copper Wires

Energy Savers

Street Light Controllers Source: Company, India Infoline Research

The company manufactures more than 15 products catering to different industries through its five in‐house manufacturing facilities. It is working in collaboration with Plitron Manufacturing, Canada for toroidal transformers and has entered into a JV with C3 Controls, an American Company to manufacture and market contactors and overload relays. It is also setting up a manufacturing facility for three more products that will likely be introduced over the next two years. Also, in‐house manufacturing and R&D enable superior customization of products for customers. Salzer has been identified as a preferred supplier by large MNCs such as General Electric and Schneider. It is the largest supplier of rotary and load break switches to the Indian Railways and has a strong OE customer base comprising companies such as BHEL, Honeywell, ABB, and Siemens and large PSUs such as Nuclear Power Corporation of India.

Page 4 of 20

Salzer Electronics Ltd

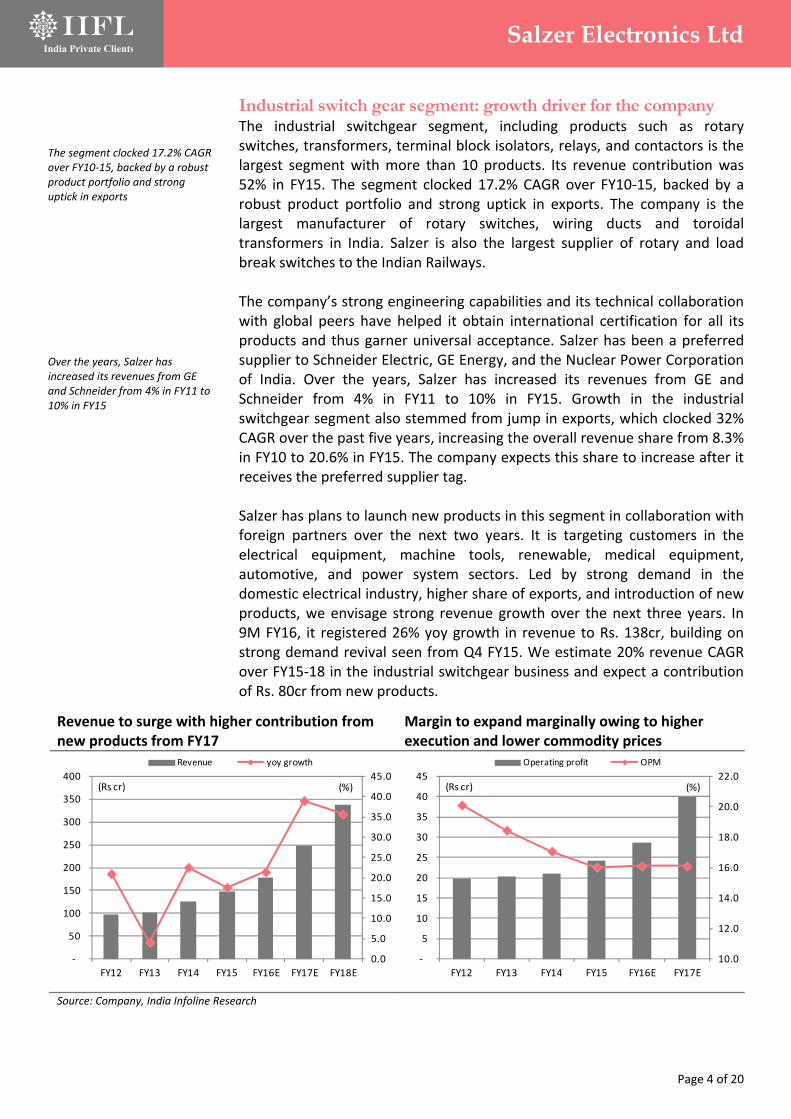

The segment clocked 17.2% CAGR over FY10‐15, backed by a robust product portfolio and strong uptick in exports

Over the years, Salzer has increased its revenues from GE and Schneider from 4% in FY11 to 10% in FY15

Industrial switch gear segment: growth driver for the company The industrial switchgear segment, including products such as rotary switches, transformers, terminal block isolators, relays, and contactors is the largest segment with more than 10 products. Its revenue contribution was 52% in FY15. The segment clocked 17.2% CAGR over FY10‐15, backed by a robust product portfolio and strong uptick in exports. The company is the largest manufacturer of rotary switches, wiring ducts and toroidal transformers in India. Salzer is also the largest supplier of rotary and load break switches to the Indian Railways. The company’s strong engineering capabilities and its technical collaboration with global peers have helped it obtain international certification for all its products and thus garner universal acceptance. Salzer has been a preferred supplier to Schneider Electric, GE Energy, and the Nuclear Power Corporation of India. Over the years, Salzer has increased its revenues from GE and Schneider from 4% in FY11 to 10% in FY15. Growth in the industrial switchgear segment also stemmed from jump in exports, which clocked 32% CAGR over the past five years, increasing the overall revenue share from 8.3% in FY10 to 20.6% in FY15. The company expects this share to increase after it receives the preferred supplier tag. Salzer has plans to launch new products in this segment in collaboration with foreign partners over the next two years. It is targeting customers in the electrical equipment, machine tools, renewable, medical equipment, automotive, and power system sectors. Led by strong demand in the domestic electrical industry, higher share of exports, and introduction of new products, we envisage strong revenue growth over the next three years. In 9M FY16, it registered 26% yoy growth in revenue to Rs. 138cr, building on strong demand revival seen from Q4 FY15. We estimate 20% revenue CAGR over FY15‐18 in the industrial switchgear business and expect a contribution of Rs. 80cr from new products.

Revenue to surge with higher contribution from new products from FY17

Margin to expand marginally owing to higher execution and lower commodity prices

Source: Company, India Infoline Research

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

‐

50

100

150

200

250

300

350

400

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Revenue yoy growth

10.0

12.0

14.0

16.0

18.0

20.0

22.0

‐

5

10

15

20

25

30

35

40

45

FY12 FY13 FY14 FY15 FY16E FY17E

(%)(Rs cr)

Operating profit OPM

Page 5 of 20

Salzer Electronics Ltd

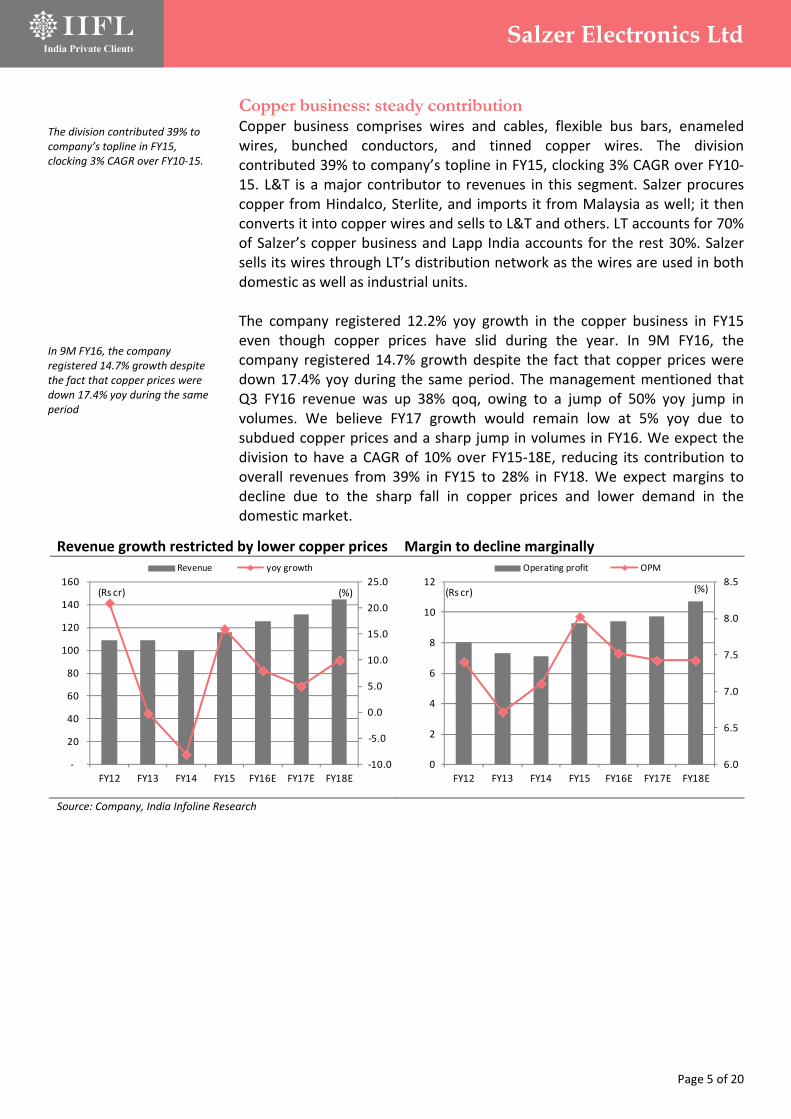

The division contributed 39% to company’s topline in FY15, clocking 3% CAGR over FY10‐15.

In 9M FY16, the company registered 14.7% growth despite the fact that copper prices were down 17.4% yoy during the same period

Copper business: steady contribution Copper business comprises wires and cables, flexible bus bars, enameled wires, bunched conductors, and tinned copper wires. The division contributed 39% to company’s topline in FY15, clocking 3% CAGR over FY10‐15. L&T is a major contributor to revenues in this segment. Salzer procures copper from Hindalco, Sterlite, and imports it from Malaysia as well; it then converts it into copper wires and sells to L&T and others. LT accounts for 70% of Salzer’s copper business and Lapp India accounts for the rest 30%. Salzer sells its wires through LT’s distribution network as the wires are used in both domestic as well as industrial units. The company registered 12.2% yoy growth in the copper business in FY15 even though copper prices have slid during the year. In 9M FY16, the company registered 14.7% growth despite the fact that copper prices were down 17.4% yoy during the same period. The management mentioned that Q3 FY16 revenue was up 38% qoq, owing to a jump of 50% yoy jump in volumes. We believe FY17 growth would remain low at 5% yoy due to subdued copper prices and a sharp jump in volumes in FY16. We expect the division to have a CAGR of 10% over FY15‐18E, reducing its contribution to overall revenues from 39% in FY15 to 28% in FY18. We expect margins to decline due to the sharp fall in copper prices and lower demand in the domestic market.

Revenue growth restricted by lower copper prices Margin to decline marginally

Source: Company, India Infoline Research

‐10.0

‐5.0

0.0

5.0

10.0

15.0

20.0

25.0

‐

20

40

60

80

100

120

140

160

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Revenue yoy growth

6.0

6.5

7.0

7.5

8.0

8.5

0

2

4

6

8

10

12

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Operating profit OPM

Page 6 of 20

Salzer Electronics Ltd

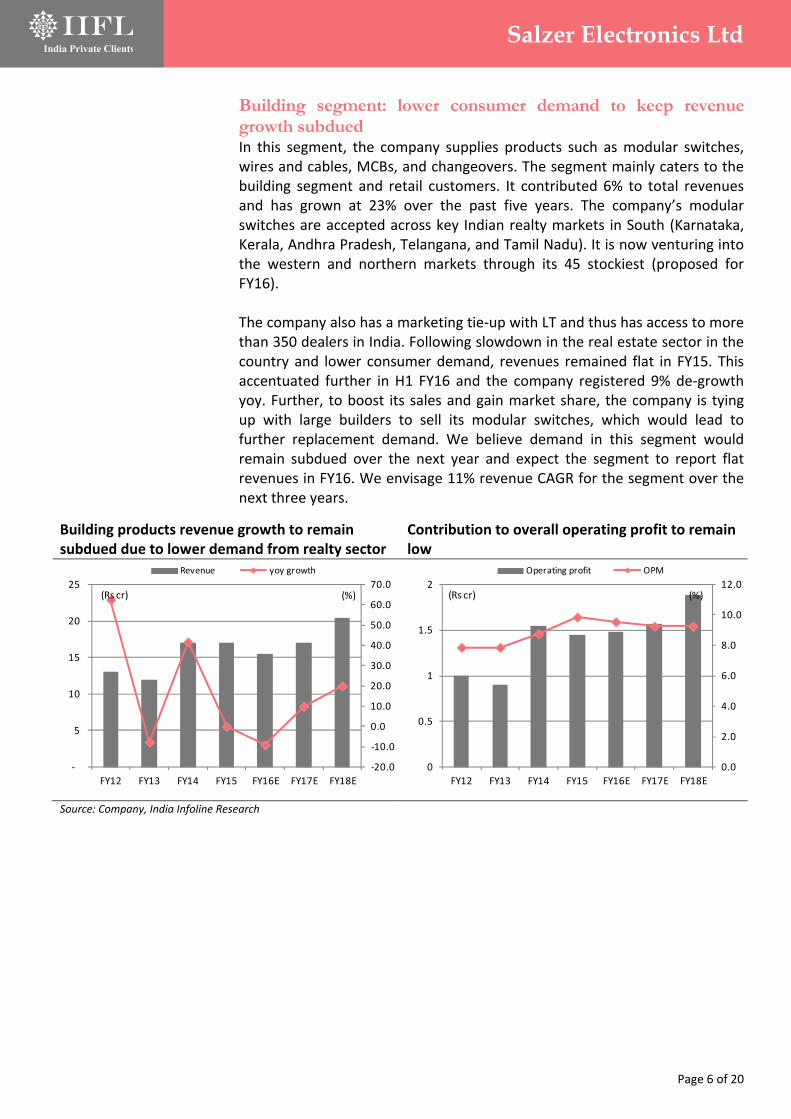

Building segment: lower consumer demand to keep revenue growth subdued In this segment, the company supplies products such as modular switches, wires and cables, MCBs, and changeovers. The segment mainly caters to the building segment and retail customers. It contributed 6% to total revenues and has grown at 23% over the past five years. The company’s modular switches are accepted across key Indian realty markets in South (Karnataka, Kerala, Andhra Pradesh, Telangana, and Tamil Nadu). It is now venturing into the western and northern markets through its 45 stockiest (proposed for FY16). The company also has a marketing tie‐up with LT and thus has access to more than 350 dealers in India. Following slowdown in the real estate sector in the country and lower consumer demand, revenues remained flat in FY15. This accentuated further in H1 FY16 and the company registered 9% de‐growth yoy. Further, to boost its sales and gain market share, the company is tying up with large builders to sell its modular switches, which would lead to further replacement demand. We believe demand in this segment would remain subdued over the next year and expect the segment to report flat revenues in FY16. We envisage 11% revenue CAGR for the segment over the next three years.

Building products revenue growth to remain subdued due to lower demand from realty sector

Contribution to overall operating profit to remain low

Source: Company, India Infoline Research

‐20.0

‐10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

‐

5

10

15

20

25

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Revenue yoy growth

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0

0.5

1

1.5

2

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Operating profit OPM

Page 7 of 20

Salzer Electronics Ltd

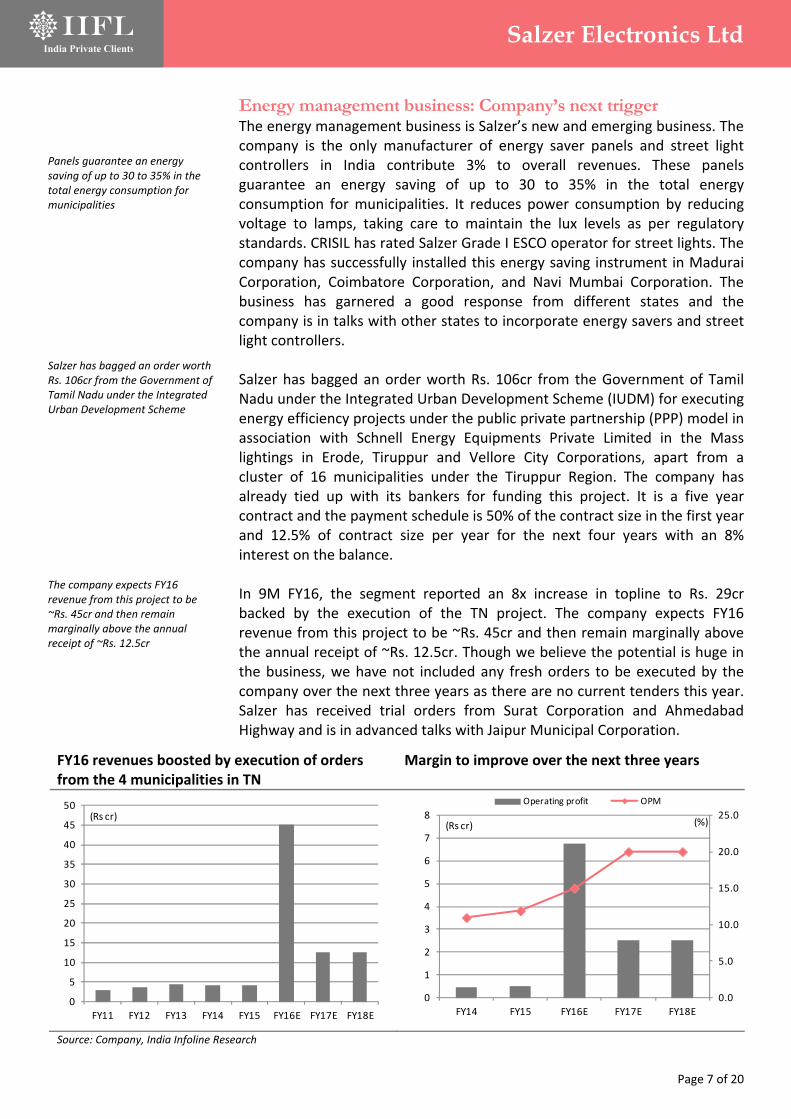

Panels guarantee an energy saving of up to 30 to 35% in the total energy consumption for municipalities

Salzer has bagged an order worth Rs. 106cr from the Government of Tamil Nadu under the Integrated Urban Development Scheme

The company expects FY16 revenue from this project to be ~Rs. 45cr and then remain marginally above the annual receipt of ~Rs. 12.5cr

Energy management business: Company’s next trigger The energy management business is Salzer’s new and emerging business. The company is the only manufacturer of energy saver panels and street light controllers in India contribute 3% to overall revenues. These panels guarantee an energy saving of up to 30 to 35% in the total energy consumption for municipalities. It reduces power consumption by reducing voltage to lamps, taking care to maintain the lux levels as per regulatory standards. CRISIL has rated Salzer Grade I ESCO operator for street lights. The company has successfully installed this energy saving instrument in Madurai Corporation, Coimbatore Corporation, and Navi Mumbai Corporation. The business has garnered a good response from different states and the company is in talks with other states to incorporate energy savers and street light controllers. Salzer has bagged an order worth Rs. 106cr from the Government of Tamil Nadu under the Integrated Urban Development Scheme (IUDM) for executing energy efficiency projects under the public private partnership (PPP) model in association with Schnell Energy Equipments Private Limited in the Mass lightings in Erode, Tiruppur and Vellore City Corporations, apart from a cluster of 16 municipalities under the Tiruppur Region. The company has already tied up with its bankers for funding this project. It is a five year contract and the payment schedule is 50% of the contract size in the first year and 12.5% of contract size per year for the next four years with an 8% interest on the balance. In 9M FY16, the segment reported an 8x increase in topline to Rs. 29cr backed by the execution of the TN project. The company expects FY16 revenue from this project to be ~Rs. 45cr and then remain marginally above the annual receipt of ~Rs. 12.5cr. Though we believe the potential is huge in the business, we have not included any fresh orders to be executed by the company over the next three years as there are no current tenders this year. Salzer has received trial orders from Surat Corporation and Ahmedabad Highway and is in advanced talks with Jaipur Municipal Corporation.

FY16 revenues boosted by execution of orders from the 4 municipalities in TN

Margin to improve over the next three years

Source: Company, India Infoline Research

0

5

10

15

20

25

30

35

40

45

50

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(Rs cr)

0.0

5.0

10.0

15.0

20.0

25.0

0

1

2

3

4

5

6

7

8

FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Operating profit OPM

Page 8 of 20

Salzer Electronics Ltd

The total market size for three phase dry type transformers is estimated at ~Rs. 2,000cr; it is being supplied by only two Indian manufacturers as of now and another company will likely start supplying soon

The management sees high potential in developing economies as every smart meter has one latch relay

Salzer has developed a motor protection circuit breaker (MPCB) through its in‐house designing team and R&D

New product to drive revenue growth from FY18 The company plans to add four new products to its product portfolio over the next two years. First, the company plans to add three phase dry type transformers to its product suite. It has already tied up with Trafomodern, an Austrian company for technology transfer, wherein Salzer will use Trafomodern’s model technology, design, and assistance to manufacture dry type air‐cooled transformers, which are hi‐tech products with applications in medium‐sized UPS, renewable energy businesses such as solar inverter signals, railways including metro coaches, regular air‐conditioned railway coaches, and in the marine and power generation industries. The total market size for this product is estimated at ~Rs. 2,000cr; it is being supplied by only two Indian manufacturers as of now and another company will likely start supplying soon. For this product, the company will invest Rs. 22cr to set up manufacturing facilities and it expects revenue of Rs. 20cr in FY17; revenue CAGR will likely be at 35% over the next five years. The second product to be introduced is latching relay, particularly used in smart meters, wherein the company is in advanced talks with a foreign partner. The management sees high potential in developing economies as every smart meter has one latch relay. The project has been delayed as the partners want to time the business a little bit later in FY16 so that the project comes up at the same time when there is a requirement in the Indian market. As per management, revenue CAGR from this product stood at 40%. We have not taken any revenues from this product as the management has not mentioned any major timelines. Any contribution from this product would pose upside risks to our estimates. The third product to be introduced is capacitors. Capacitors are widely used in electronic units for power conditioning, power factor correction, motor starter application, smoothing, filtering, and bypassing. IEEMA estimates its market to have 30% CAGR over the next five years from the current market size of Rs. 750Cr, owing to the rising demand across industries to save energy. The company would incur a capex of Rs. 10cr for this product and expects to start commercial production in H1 FY17. The management would use its existing relationship with OEMs and expects the product to contribute Rs. 7cr in FY17 and Rs. 20cr in FY18. Salzer has developed a motor protection circuit breaker (MPCB) through its in‐house designing team and R&D. An MPCB is a specialized electromechanical device that can be used with motor circuits and it provides a safe electrical supply for motors. As per the management, a large share of local demand for this product will be met through imports, as few Indian companies manufacture it. The company is also in talks with GE for a marketing tie‐up for this product. The company has already incurred a capex of Rs. 6cr for this product and expects to start commercial production in H1 FY17. Since the product is under certification, revenue contribution would be minimal in FY17; the management expects the product to contribute Rs. 20cr in FY18.

Page 9 of 20

Salzer Electronics Ltd

Exports as a % of sales increased from 8% in FY10 to 24% in FY15

Salzer has recently signed a distribution agreement with IPD Group Ltd of Australia, a leading electrical distributor/wholesaler and manufacturer in Australia for marketing and selling Salzer branded electrical products for Solar Photovoltaic applications in Australia and New Zealand

The company is targeting exports as a % of sales to increase from 24% in FY15 to 30% in FY16 and 40% by FY20

Surge in exports to boost topline Salzer has over the years focused on increasing the share of exports in its overall revenue mix to become a global product supplier. The company has a direct network across 50 countries and has 40 international distributors. Salzer is India’s largest and only exporter of rotary switches, cable ducts, and isolators. Exports as a % of sales increased from 8% in FY10 to 24% in FY15. No country accounted for more than 10% of the company’s revenues. Over the past five years, export revenue CAGR stood at 32% as against the company revenue CAGR of 10%. Despite a weak economic global sentiment and slowing down of capex, the company had a revenue growth of 24.6% in FY15. It is growing its presence in Latin America and Africa, which it believes are vast and growing markets. The company is also targeting to increase its sales to North America as its products have been successfully accepted in the region. Salzer has recently signed a distribution agreement with IPD Group Ltd of Australia, a leading electrical distributor/wholesaler and manufacturer in Australia for marketing and selling Salzer branded electrical products for Solar Photovoltaic applications in Australia and New Zealand. Australia is one of the largest markets for Solar Photovotaic applications and Salzer’s DC isolators can be used for 1000 VDC application in various indoor and outdoor mountings. During FY16, the company targets to double its share of sales to North America from 7% in FY15. We believe that this is possible, considering that the company was selected as the preferred supplier by GE and Schneider in FY15. The company has already seen an increase in business from the above two companies in H1 FY16 and expects more momentum in the future. In Q1 FY16, the company saw an increase of 27% yoy from Schneider and 17% from GE. The management indicated that incremental revenue from its preferred supplier is yet to be realized because the projects are at various stages of testing and finalization. It believes H2 FY16 growth from these two suppliers would remain at higher levels. The company is targeting exports as a % of sales to increase from 24% in FY15 to 30% in FY16 and 40% by FY20.

Share of exports has increased to 23.4% in FY15 from 8% in FY10

India accounted for 3/4th of the total sales in FY15

Source: Company, India Infoline Research

0.0

5.0

10.0

15.0

20.0

25.0

‐

10

20

30

40

50

60

70

FY10 FY11 FY12 FY13 FY14 FY15

(%)(Rs cr)

Exports % of revenue

77

2

3

13

5

India

Others

North America

Europe

Rest of Asia

Page 10 of 20

Salzer Electronics Ltd

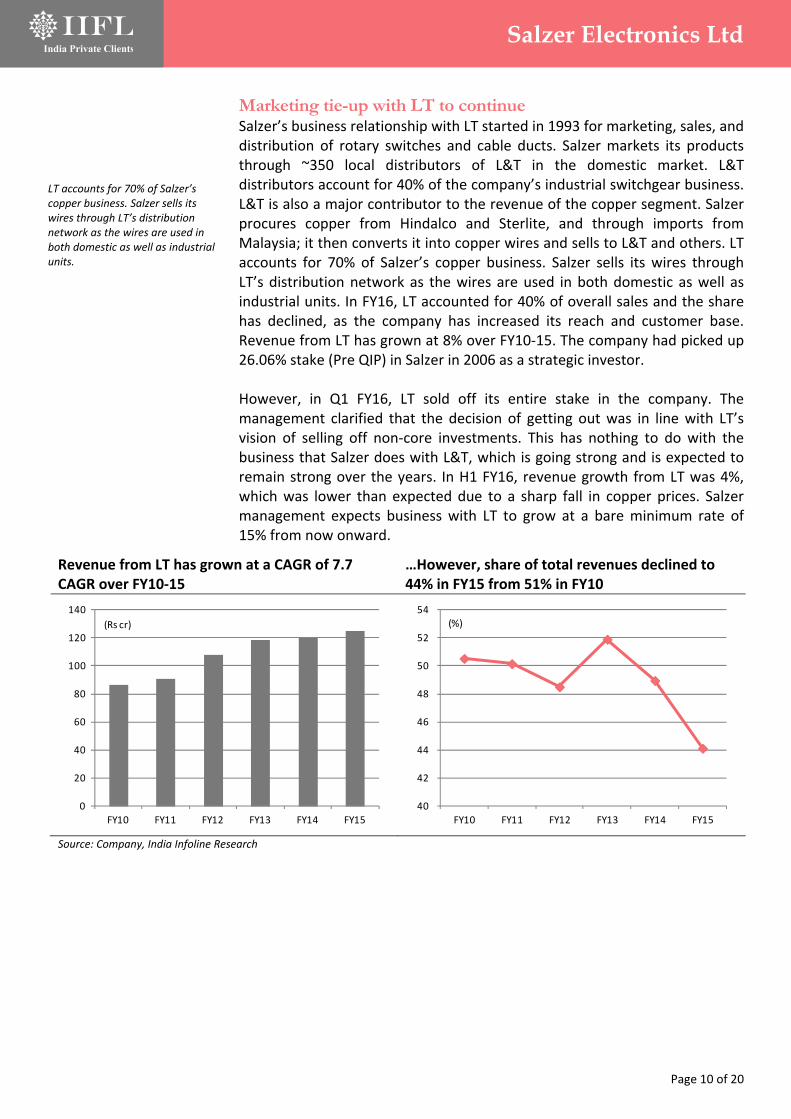

LT accounts for 70% of Salzer’s copper business. Salzer sells its wires through LT’s distribution network as the wires are used in both domestic as well as industrial units.

Marketing tie-up with LT to continue Salzer’s business relationship with LT started in 1993 for marketing, sales, and distribution of rotary switches and cable ducts. Salzer markets its products through ~350 local distributors of L&T in the domestic market. L&T distributors account for 40% of the company’s industrial switchgear business. L&T is also a major contributor to the revenue of the copper segment. Salzer procures copper from Hindalco and Sterlite, and through imports from Malaysia; it then converts it into copper wires and sells to L&T and others. LT accounts for 70% of Salzer’s copper business. Salzer sells its wires through LT’s distribution network as the wires are used in both domestic as well as industrial units. In FY16, LT accounted for 40% of overall sales and the share has declined, as the company has increased its reach and customer base. Revenue from LT has grown at 8% over FY10‐15. The company had picked up 26.06% stake (Pre QIP) in Salzer in 2006 as a strategic investor. However, in Q1 FY16, LT sold off its entire stake in the company. The management clarified that the decision of getting out was in line with LT’s vision of selling off non‐core investments. This has nothing to do with the business that Salzer does with L&T, which is going strong and is expected to remain strong over the years. In H1 FY16, revenue growth from LT was 4%, which was lower than expected due to a sharp fall in copper prices. Salzer management expects business with LT to grow at a bare minimum rate of 15% from now onward.

Revenue from LT has grown at a CAGR of 7.7 CAGR over FY10‐15

…However, share of total revenues declined to 44% in FY15 from 51% in FY10

Source: Company, India Infoline Research

0

20

40

60

80

100

120

140

FY10 FY11 FY12 FY13 FY14 FY15

(Rs cr)

40

42

44

46

48

50

52

54

FY10 FY11 FY12 FY13 FY14 FY15

(%)

Page 11 of 20

Salzer Electronics Ltd

We expect debt to reduce by 30% over the next three years, after accounting for a capex of Rs. 83cr over FY15‐18

Recent equity infusion to reduce debt and fund future capex The company has raised Rs. 62cr via QIP to fund new product development and new projects. In addition, the company has also issued 0.1cr share warrants to its promoters at a price of Rs. 251. Promoters have already converted ~37% of the warrants allotted and are expected to convert the entire warrants by the end of FY16. Thus, the company has raised Rs. 87cr for setting up manufacturing plants for its new products, funding working capital requirements, and repaying some debt. Of the amount collected, the company will invest Rs 22cr to set up a dry type transformer capacity, Rs 8cr for MCCB product development, and fund the capex required for setting up a capacitor plant and use the balance money to cut short‐term debt. We expect debt to reduce by 30% over the next three years, after accounting for a capex of Rs. 83cr over FY15‐18. We expect the company to reduce its debt from Rs. 93cr at the end of FY15 to Rs. 88cr by FY18, backed by recent equity infusion and steady cash flows starting FY17. D/E to decline sharply over equity infusion

Source: Company, India Infoline Research

0.0

0.2

0.4

0.6

0.8

1.0

‐

20

40

60

80

100

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Gross debt D/E

Page 12 of 20

Salzer Electronics Ltd

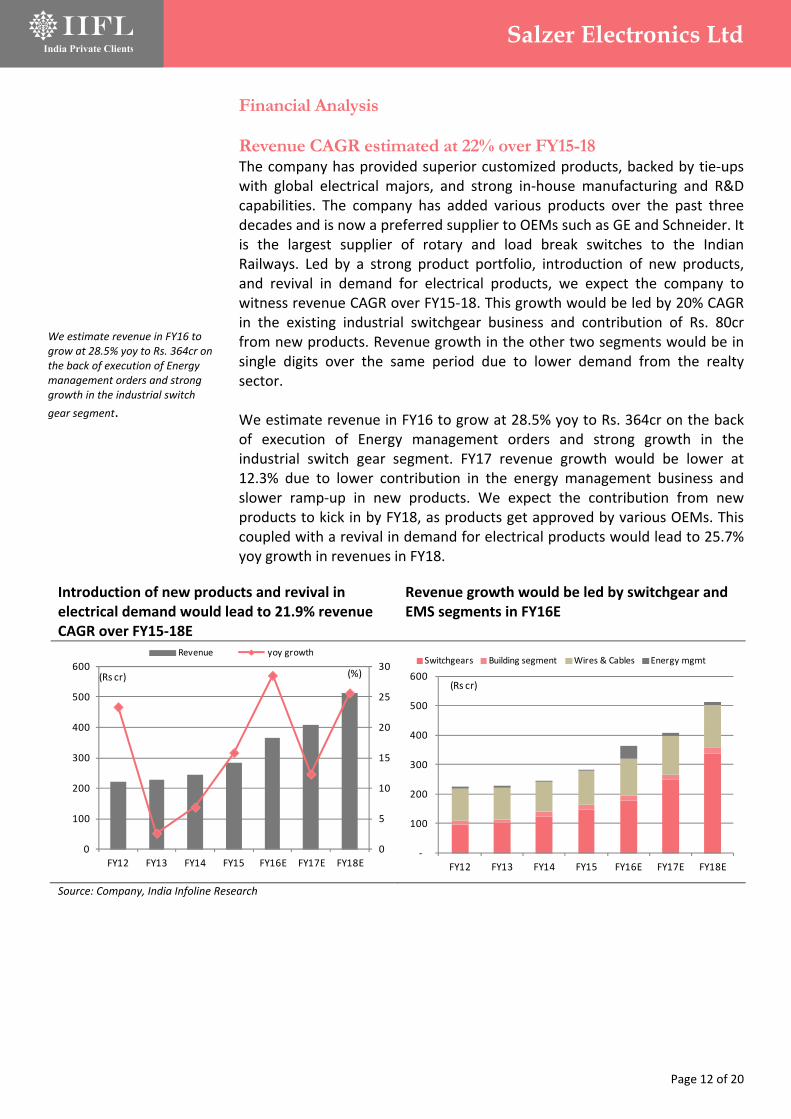

We estimate revenue in FY16 to grow at 28.5% yoy to Rs. 364cr on the back of execution of Energy management orders and strong growth in the industrial switch

gear segment.

Financial Analysis

Revenue CAGR estimated at 22% over FY15-18 The company has provided superior customized products, backed by tie‐ups with global electrical majors, and strong in‐house manufacturing and R&D capabilities. The company has added various products over the past three decades and is now a preferred supplier to OEMs such as GE and Schneider. It is the largest supplier of rotary and load break switches to the Indian Railways. Led by a strong product portfolio, introduction of new products, and revival in demand for electrical products, we expect the company to witness revenue CAGR over FY15‐18. This growth would be led by 20% CAGR in the existing industrial switchgear business and contribution of Rs. 80cr from new products. Revenue growth in the other two segments would be in single digits over the same period due to lower demand from the realty sector. We estimate revenue in FY16 to grow at 28.5% yoy to Rs. 364cr on the back of execution of Energy management orders and strong growth in the industrial switch gear segment. FY17 revenue growth would be lower at 12.3% due to lower contribution in the energy management business and slower ramp‐up in new products. We expect the contribution from new products to kick in by FY18, as products get approved by various OEMs. This coupled with a revival in demand for electrical products would lead to 25.7% yoy growth in revenues in FY18.

Introduction of new products and revival in electrical demand would lead to 21.9% revenue CAGR over FY15‐18E

Revenue growth would be led by switchgear and EMS segments in FY16E

Source: Company, India Infoline Research

0

5

10

15

20

25

30

0

100

200

300

400

500

600

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Revenue yoy growth

‐

100

200

300

400

500

600

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(Rs cr)

Switchgears Building segment Wires & Cables Energy mgmt

Page 13 of 20

Salzer Electronics Ltd

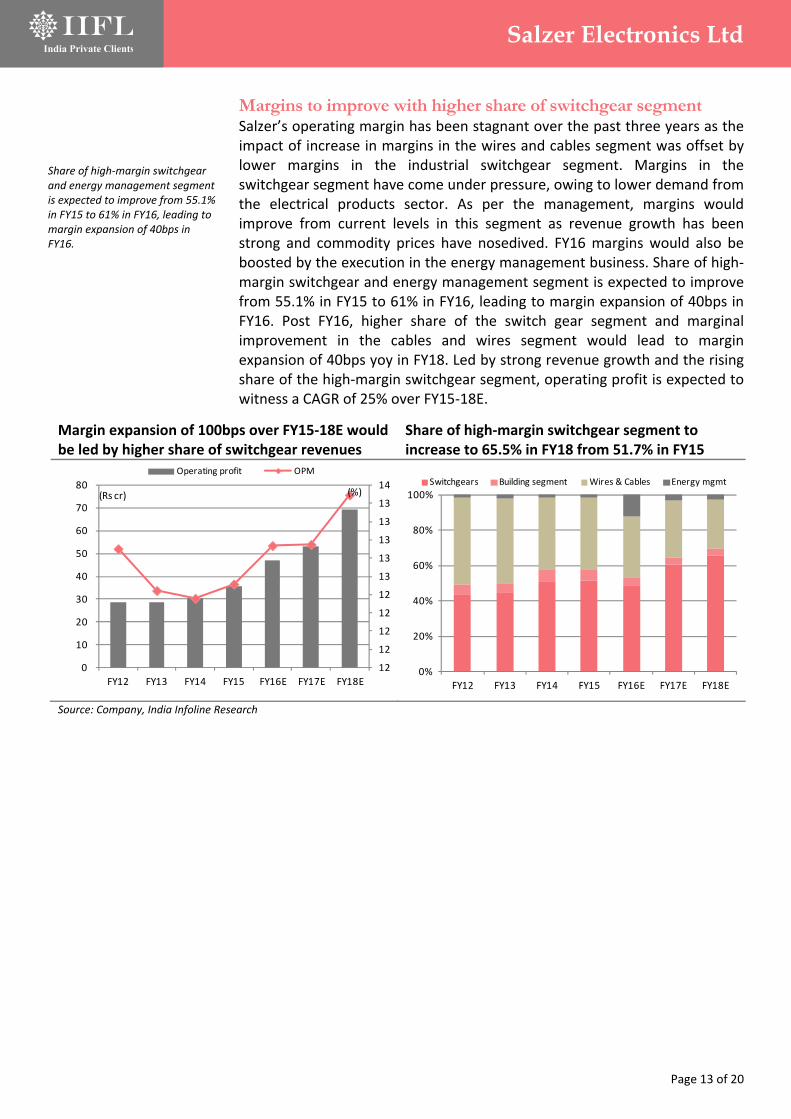

Share of high‐margin switchgear and energy management segment is expected to improve from 55.1% in FY15 to 61% in FY16, leading to margin expansion of 40bps in FY16.

Margins to improve with higher share of switchgear segment Salzer’s operating margin has been stagnant over the past three years as the impact of increase in margins in the wires and cables segment was offset by lower margins in the industrial switchgear segment. Margins in the switchgear segment have come under pressure, owing to lower demand from the electrical products sector. As per the management, margins would improve from current levels in this segment as revenue growth has been strong and commodity prices have nosedived. FY16 margins would also be boosted by the execution in the energy management business. Share of high‐margin switchgear and energy management segment is expected to improve from 55.1% in FY15 to 61% in FY16, leading to margin expansion of 40bps in FY16. Post FY16, higher share of the switch gear segment and marginal improvement in the cables and wires segment would lead to margin expansion of 40bps yoy in FY18. Led by strong revenue growth and the rising share of the high‐margin switchgear segment, operating profit is expected to witness a CAGR of 25% over FY15‐18E.

Margin expansion of 100bps over FY15‐18E would be led by higher share of switchgear revenues

Share of high‐margin switchgear segment to increase to 65.5% in FY18 from 51.7% in FY15

Source: Company, India Infoline Research

12

12

12

12

12

13

13

13

13

13

14

0

10

20

30

40

50

60

70

80

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

Operating profit OPM

0%

20%

40%

60%

80%

100%

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Switchgears Building segment Wires & Cables Energy mgmt

Page 14 of 20

Salzer Electronics Ltd

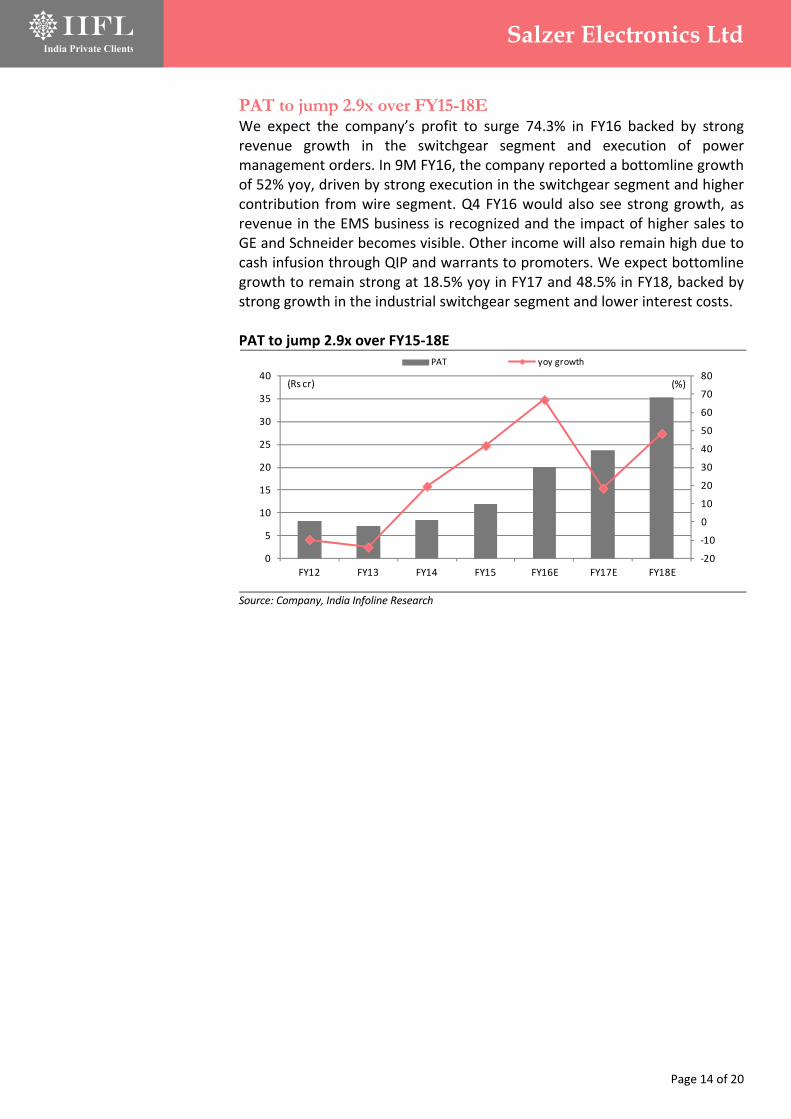

PAT to jump 2.9x over FY15-18E We expect the company’s profit to surge 74.3% in FY16 backed by strong revenue growth in the switchgear segment and execution of power management orders. In 9M FY16, the company reported a bottomline growth of 52% yoy, driven by strong execution in the switchgear segment and higher contribution from wire segment. Q4 FY16 would also see strong growth, as revenue in the EMS business is recognized and the impact of higher sales to GE and Schneider becomes visible. Other income will also remain high due to cash infusion through QIP and warrants to promoters. We expect bottomline growth to remain strong at 18.5% yoy in FY17 and 48.5% in FY18, backed by strong growth in the industrial switchgear segment and lower interest costs. PAT to jump 2.9x over FY15‐18E

Source: Company, India Infoline Research

‐20

‐10

0

10

20

30

40

50

60

70

80

0

5

10

15

20

25

30

35

40

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

(%)(Rs cr)

PAT yoy growth

Page 15 of 20

Salzer Electronics Ltd

The company has added more than 15 products to its basket over the past three decades

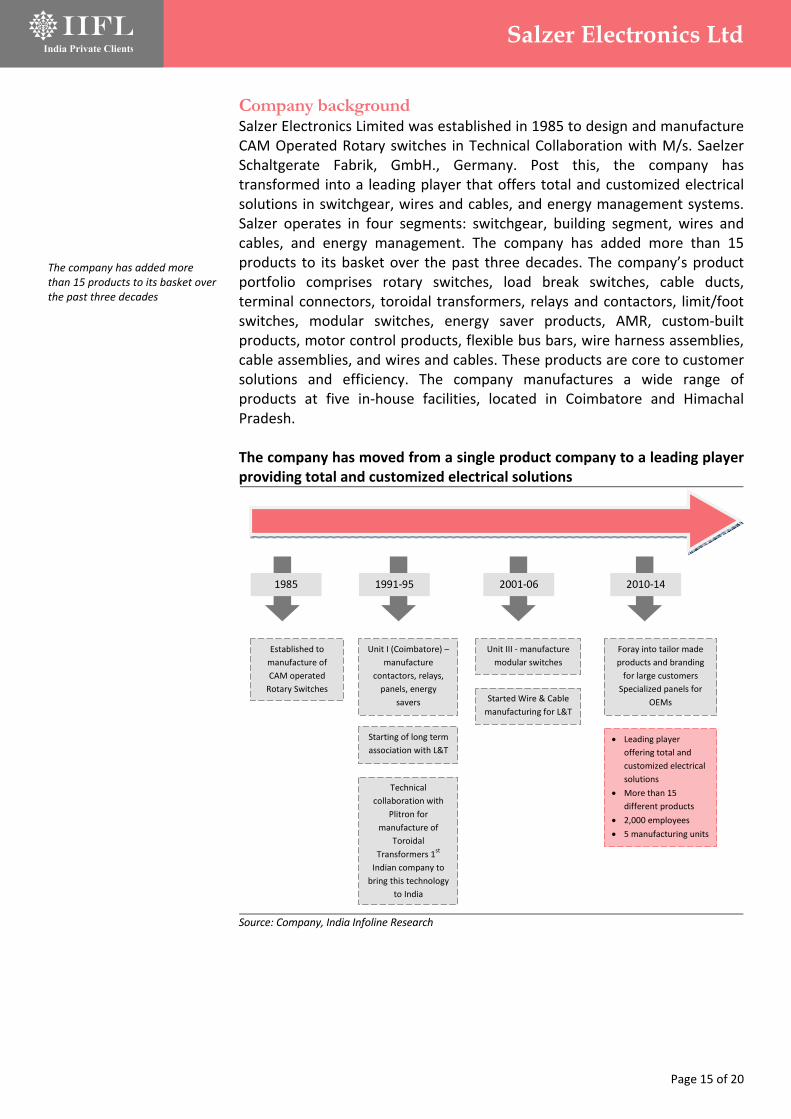

Company background Salzer Electronics Limited was established in 1985 to design and manufacture CAM Operated Rotary switches in Technical Collaboration with M/s. Saelzer Schaltgerate Fabrik, GmbH., Germany. Post this, the company has transformed into a leading player that offers total and customized electrical solutions in switchgear, wires and cables, and energy management systems. Salzer operates in four segments: switchgear, building segment, wires and cables, and energy management. The company has added more than 15 products to its basket over the past three decades. The company’s product portfolio comprises rotary switches, load break switches, cable ducts, terminal connectors, toroidal transformers, relays and contactors, limit/foot switches, modular switches, energy saver products, AMR, custom‐built products, motor control products, flexible bus bars, wire harness assemblies, cable assemblies, and wires and cables. These products are core to customer solutions and efficiency. The company manufactures a wide range of products at five in‐house facilities, located in Coimbatore and Himachal Pradesh. The company has moved from a single product company to a leading player providing total and customized electrical solutions

Source: Company, India Infoline Research

Established to

manufacture of

CAM operated

Rotary Switches

Unit I (Coimbatore) –

manufacture

contactors, relays,

panels, energy

savers

Unit III ‐ manufacture

modular switches

Foray into tailor made

products and branding

for large customers

Specialized panels for

OEMs

Starting of long term

association with L&T

Technical

collaboration with

Plitron for

manufacture of

Toroidal

Transformers 1st

Indian company to

bring this technology

to India

Started Wire & Cable

manufacturing for L&T

Leading player

offering total and

customized electrical

solutions

More than 15

different products

2,000 employees

5 manufacturing units

1985 1991‐95 2001‐06 2010‐14

Page 16 of 20

Salzer Electronics Ltd

Salzer has wonderful support from its customers, enabling it to build an organization into a group of five companies with international affiliations and export avenues to more than 50 countries in a span of 30 years. The company is working in collaboration with Plitron Manufacturing, Canada for toroidal transformers and has a JV with C3 Controls, an American company to manufacture and market contactors and overload relays. It is also setting up a manufacturing facility for three more products to be introduced over the next two years. Also, in‐house manufacturing and R&D enable superior customization of products for customers.

Most products are internationally certified

Source: Company, India Infoline Research

Salzer’s business relationship with LT started in 1993 for marketing, sales, and distribution of rotary switches and cable ducts. Salzer markets its products through ~350 local distributors of L&T in domestic market. L&T distributors account for 40% of the company’s industrial switchgear business and 70% of Salzer’s copper business. Salzer has been identified as a preferred supplier by large MNCs such as General Electric and Schneider. It is the largest supplier of rotary and load break switches to the Indian Railways. It also has a strong OE customer base comprising companies such as BHEL, Honeywell, ABB, and Siemens and PSUs such as Nuclear Power Corporation of India.

Major customers include large OEMs

Source: Company, India Infoline Research

Page 17 of 20

Salzer Electronics Ltd

Salzer was founded and promoted by Mr. R. Doraiswamy, a first generation entrepreneur and a sector veteran with over 20 years of industrial experience. The second generation has stepped into the business with Mr. Rajesh Doraiswamy, Jt. Managing Director and CFO, spearheading the day‐to‐day operations. Key Management

Name & Designation Qualification & Experience R.Doraiswamy, Managing Director

Core promoter with over 2 decades of experience

Qualified electrical engineer and technocrat entrepreneur Vast Experience in foreign collaboration and wide global contacts

D.Rajeshkumar, Joint Managing Director

Electrical Engineer, India; Post Graduate in Business Management, US

JMD and CEO of Company ‐ responsible for driving the vision of company’s global contacts

S.Baskarasubramanian, Director‐Corporate Affairs &CS

Qualified Company Secretary & member of FCS India

Wide experience in company law/corporate affairs

P.Sivakumar, GM – Marketing Corporate

• Bachelor in Engineering with 22 years of experience

• Responsible for Sales and Marketing division M Laksminarayana, GM ‐ Operations

B.E (Electrical) with 17 years of experience

Responsible for Production, Planning, Inventory Management, Maintenance, and General Administration

Source: Company, India Infoline Research

Page 18 of 20

Salzer Electronics Ltd

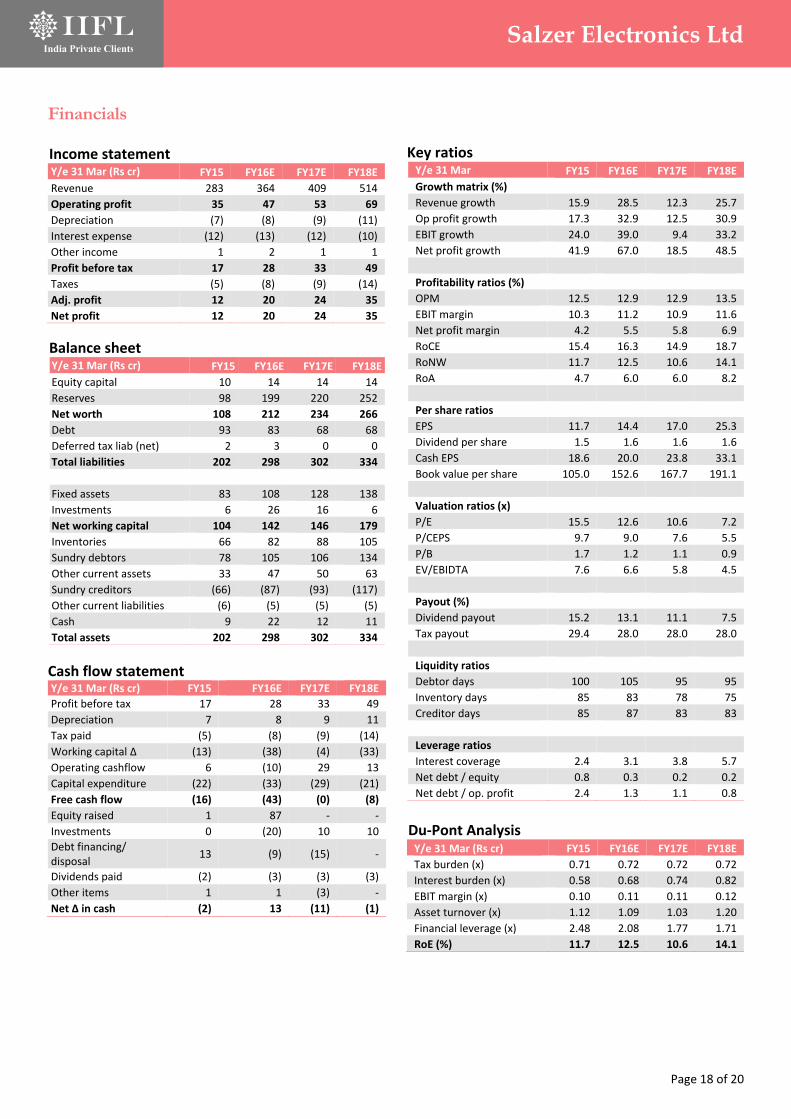

Financials Income statement Y/e 31 Mar (Rs cr) FY15 FY16E FY17E FY18E

Revenue 283 364 409 514

Operating profit 35 47 53 69

Depreciation (7) (8) (9) (11)

Interest expense (12) (13) (12) (10)

Other income 1 2 1 1

Profit before tax 17 28 33 49

Taxes (5) (8) (9) (14)

Adj. profit 12 20 24 35

Net profit 12 20 24 35

Balance sheet Y/e 31 Mar (Rs cr) FY15 FY16E FY17E FY18E

Equity capital 10 14 14 14

Reserves 98 199 220 252

Net worth 108 212 234 266

Debt 93 83 68 68

Deferred tax liab (net) 2 3 0 0

Total liabilities 202 298 302 334

Fixed assets 83 108 128 138

Investments 6 26 16 6

Net working capital 104 142 146 179

Inventories 66 82 88 105

Sundry debtors 78 105 106 134

Other current assets 33 47 50 63

Sundry creditors (66) (87) (93) (117)

Other current liabilities (6) (5) (5) (5)

Cash 9 22 12 11

Total assets 202 298 302 334

Cash flow statement Y/e 31 Mar (Rs cr) FY15 FY16E FY17E FY18E

Profit before tax 17 28 33 49

Depreciation 7 8 9 11

Tax paid (5) (8) (9) (14)

Working capital ∆ (13) (38) (4) (33)

Operating cashflow 6 (10) 29 13

Capital expenditure (22) (33) (29) (21)

Free cash flow (16) (43) (0) (8)

Equity raised 1 87 ‐ ‐

Investments 0 (20) 10 10

Debt financing/ disposal

13 (9) (15) ‐

Dividends paid (2) (3) (3) (3)

Other items 1 1 (3) ‐

Net ∆ in cash (2) 13 (11) (1)

Key ratios Y/e 31 Mar FY15 FY16E FY17E FY18E

Growth matrix (%)

Revenue growth 15.9 28.5 12.3 25.7

Op profit growth 17.3 32.9 12.5 30.9

EBIT growth 24.0 39.0 9.4 33.2

Net profit growth 41.9 67.0 18.5 48.5

Profitability ratios (%)

OPM 12.5 12.9 12.9 13.5

EBIT margin 10.3 11.2 10.9 11.6

Net profit margin 4.2 5.5 5.8 6.9

RoCE 15.4 16.3 14.9 18.7

RoNW 11.7 12.5 10.6 14.1

RoA 4.7 6.0 6.0 8.2

Per share ratios

EPS 11.7 14.4 17.0 25.3

Dividend per share 1.5 1.6 1.6 1.6

Cash EPS 18.6 20.0 23.8 33.1

Book value per share 105.0 152.6 167.7 191.1

Valuation ratios (x)

P/E 15.5 12.6 10.6 7.2

P/CEPS 9.7 9.0 7.6 5.5

P/B 1.7 1.2 1.1 0.9

EV/EBIDTA 7.6 6.6 5.8 4.5

Payout (%)

Dividend payout 15.2 13.1 11.1 7.5

Tax payout 29.4 28.0 28.0 28.0

Liquidity ratios

Debtor days 100 105 95 95

Inventory days 85 83 78 75

Creditor days 85 87 83 83

Leverage ratios

Interest coverage 2.4 3.1 3.8 5.7

Net debt / equity 0.8 0.3 0.2 0.2

Net debt / op. profit 2.4 1.3 1.1 0.8

Du‐Pont Analysis Y/e 31 Mar (Rs cr) FY15 FY16E FY17E FY18E

Tax burden (x) 0.71 0.72 0.72 0.72

Interest burden (x) 0.58 0.68 0.74 0.82

EBIT margin (x) 0.10 0.11 0.11 0.12

Asset turnover (x) 1.12 1.09 1.03 1.20

Financial leverage (x) 2.48 2.08 1.77 1.71

RoE (%) 11.7 12.5 10.6 14.1

Page 19 of 20

‘Best Broker of the Year’ – by Zee Business for contribution to broking Nirmal Jain, Chairman, IIFL, received the award for The Best Broker of the Year (for contribution to broking in India) at India's Best Market Analyst Awards 2014 organised by the Zee Business in Mumbai. The award was presented by the guest of Honour Amit Shah, president of the Bharatiya Janata Party and Piyush Goel, Minister of state with independent charge for power, coal new and renewable energy.

Recommendation parameters for fundamental reports:

Buy – Absolute return of over +15%

Accumulate – Absolute return between 0% to +15%

Reduce – Absolute return between 0% to ‐10%

Sell – Absolute return below ‐10%

Call Failure ‐ In case of a Buy report, if the stock falls 20% below the recommended price on a closing basis, unless otherwise specified by the analyst; or, in case of a Sell report, if the stock rises 20% above the recommended price on a closing basis, unless otherwise specified by the analyst

India Infoline Group (hereinafter referred as IIFL) is engaged in diversified financial services business including equity broking, DP services, merchant banking, portfolio management services, distribution of Mutual Fund, insurance products and other investment products and also loans and finance business. India Infoline Ltd (“hereinafter referred as IIL”) is a part of the IIFL and is a member of the National Stock Exchange of India Limited (“NSE”) and the BSE Limited (“BSE”). IIL is also a Depository Participant registered with NSDL & CDSL, a SEBI registered merchant banker and a SEBI registered portfolio manager. IIL is a large broking house catering to retail, HNI and institutional clients. It operates through its branches and authorised persons and sub‐brokers spread across the country and the clients are provided online trading through internet and offline trading through branches and Customer Care. Terms & Conditions and Other Disclosures:‐ a) This research report (“Report”) is for the personal information of the authorised recipient(s) and is not for public distribution and should not be

reproduced or redistributed to any other person or in any form without IIL’s prior permission. The information provided in the Report is from publicly available data, which we believe, are reliable. While reasonable endeavors have been made to present reliable data in the Report so far as it relates to current and historical information, butIIL does not guarantee the accuracy or completeness of the data in the Report. Accordingly, IIL or any of its connected persons including its directors or subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained, views and opinions expressed in this publication.

b) Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment of its original date of publication by IIFL and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments.

c) The Report also includes analysis and views of our research team. The Report is purely for information purposes and does not construe to be investment recommendation/advice or an offer or solicitation of an offer to buy/sell any securities. The opinions expressed in the Report are our current opinions as of the date of the Report and may be subject to change from time to time without notice. IIL or any persons connected with it do not accept any liability arising from the use of this document.

d) Investors should not solely rely on the information contained in this Report and must make investment decisions based on their own investment objectives, judgment, risk profile and financial position. The recipients of this Report may take professional advice before acting on this information.

e) IIL has other business segments / divisions with independent research teams separated by 'Chinese walls' catering to different sets of customers having varying objectives, risk profiles, investment horizon, etc and therefore, may at times have, different and contrary views on stocks, sectors and markets.

f) This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to local law, regulation or which would subject IIL and its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this Report may come are required to inform themselves of and to observe such restrictions.

g) As IIL along with its associates, are engaged in various financial services business and so might have financial, business or other interests in other entities including the subject company/ies mentioned in this Report. However, IIL encourages independence in preparation of research report and strives to minimize conflict in preparation of research report. IIL and its associates did not receive any compensation or other benefits from the subject company/ies mentioned in the Report or from a third party in connection with preparation of the Report. Accordingly, IIL and its associates do not have any material conflict of interest at the time of publication of this Report.

Page 20 of 20

h) As IIL and its associates are engaged in various financial services business, it might have:‐

(a) received any compensation (except in connection with the preparation of this Report) from the subject company in the past twelve months; (b) managed or co‐managed public offering of securities for the subject company in the past twelve months; (c) received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (d) received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (e) engaged in market making activity for the subject company.

i) IIL and its associates collectively do not own(in their proprietary position) 1% or more of the equity securities of the subject company/ies mentioned in the report as of the last day of the month preceding the publication of the research report.

j) The Research Analyst/s engaged in preparation of this Report or his/her relative

(a) does not have any financial interests in the subject company/ies mentioned in this report; (b) does not own 1% or more of the equity securities of the subject company mentioned in the report as of the last day of the month preceding the publication of the research report; (c) does not have any other material conflict of interest at the time of publication of the research report.

k) The Research Analyst/s engaged in preparation of this Report:‐

(a) has not received any compensation from the subject company in the past twelve months; (b) has not managed or co‐managed public offering of securities for the subject company in the past twelve months; (c) has not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (d) has not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (e) has not received any compensation or other benefits from the subject company or third party in connection with the research report; (f) has not served as an officer, director or employee of the subject company; (g) is not engaged in market making activity for the subject company.

We submit that no material disciplinary action has been taken on IIL by any regulatory authority impacting Equity Research Analysis. A graph of daily closing prices of securities is available at http://www.nseindia.com/ChartApp/install/charts/mainpage.jsp, www.bseindia.com and http://economictimes.indiatimes.com/markets/stocks/stock‐quotes. (Choose a company from the list on the browser and select the “three years” period in the price chart).

Published in 2016. © India Infoline Ltd 2016 India Infoline Limited (Formerly “India Infoline Distribution Company Limited”), CIN No.: U99999MH1996PLC132983, Corporate Office – IIFL Centre, Kamala City, Senapati Bapat Marg, Lower Parel, Mumbai – 400013 Tel: (91‐22) 4249 9000 .Fax: (91‐22) 40609049, Regd. Office – IIFL House, Sun Infotech Park, Road No. 16V, Plot No. B‐23, MIDC, Thane Industrial Area, Wagle Estate, Thane – 400604 Tel: (91‐22) 25806650. Fax: (91‐22) 25806654 E‐mail: [email protected] Website: www.indiainfoline.com, Refer www.indiainfoline.com for detail of Associates. National Stock Exchange of India Ltd. SEBI Regn. No. : INB231097537/ INF231097537/ INE231097537, Bombay Stock Exchange Ltd. SEBI Regn. No.:INB011097533/ INF011097533/ BSE‐Currency, MCX Stock Exchange Ltd. SEBI Regn. No.: INB261097530/ INF261097530/ INE261097537, United Stock Exchange Ltd. SEBI Regn. No.: INE271097532, PMS SEBI Regn. No. INP000002213, IA SEBI Regn. No. INA000000623, SEBI RA Regn.:‐ INH000000248.

For Research related queries, write to: Amar Ambani, Head of Research at [email protected] For Sales and Account related information, write to customer care: [email protected] or call on 91‐22 4007 1000

Recommended