Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

Current State of the Retirement Income Industry

Panelists: Rebekah Barsch, Northwestern Mutual

Tom Hegna, TomHegna.com Curtis Cloke, Thrive Income Distribution System

Moderator: Chris Raham, Ernst & Young LLP

Presenting Sponsor: Produced By:

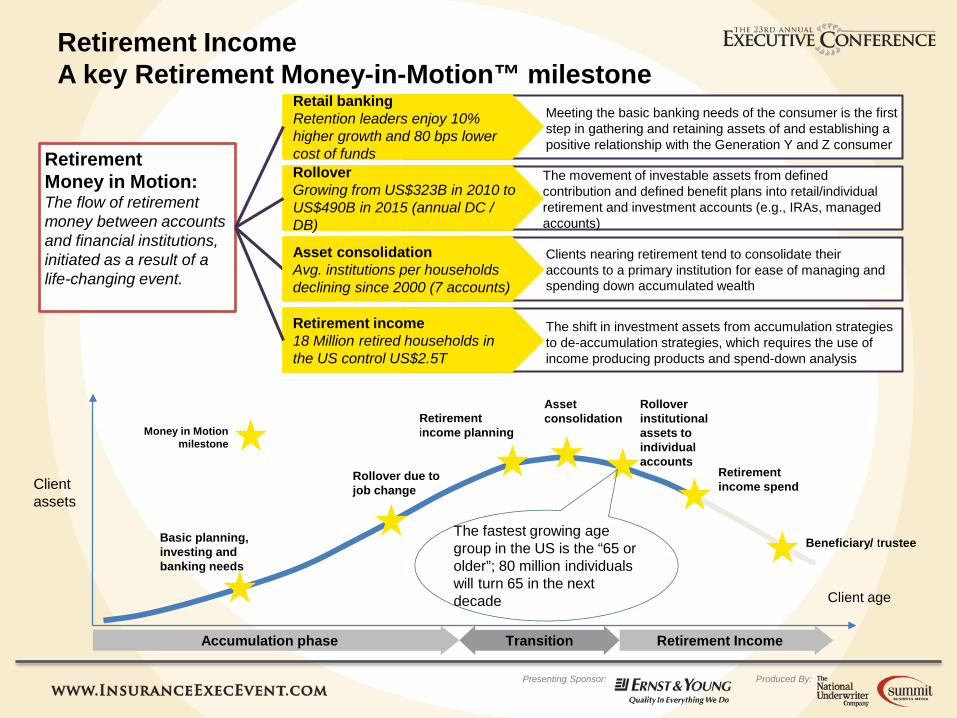

Retirement Income A key Retirement Money-in-Motion™ milestone

Rollover Growing from US$323B in 2010 to US$490B in 2015 (annual DC / DB)

The movement of investable assets from defined contribution and defined benefit plans into retail/individual retirement and investment accounts (e.g., IRAs, managed accounts)

Asset consolidation Avg. institutions per households declining since 2000 (7 accounts)

Clients nearing retirement tend to consolidate their accounts to a primary institution for ease of managing and spending down accumulated wealth

Retirement income 18 Million retired households in the US control US$2.5T

The shift in investment assets from accumulation strategies to de-accumulation strategies, which requires the use of income producing products and spend-down analysis

Retirement Money in Motion: The flow of retirement money between accounts and financial institutions, initiated as a result of a life-changing event.

Retail banking Retention leaders enjoy 10% higher growth and 80 bps lower cost of funds

Meeting the basic banking needs of the consumer is the first step in gathering and retaining assets of and establishing a positive relationship with the Generation Y and Z consumer

Client age

Client assets

Accumulation phase Retirement Income Transition

Retirement income spend

Asset consolidation

Rollover due to job change

Rollover institutional assets to individual accounts

The fastest growing age group in the US is the “65 or older”; 80 million individuals will turn 65 in the next decade

Money in Motion milestone

Beneficiary/ trustee

Retirement income planning

Basic planning, investing and banking needs

Presenting Sponsor: Produced By:

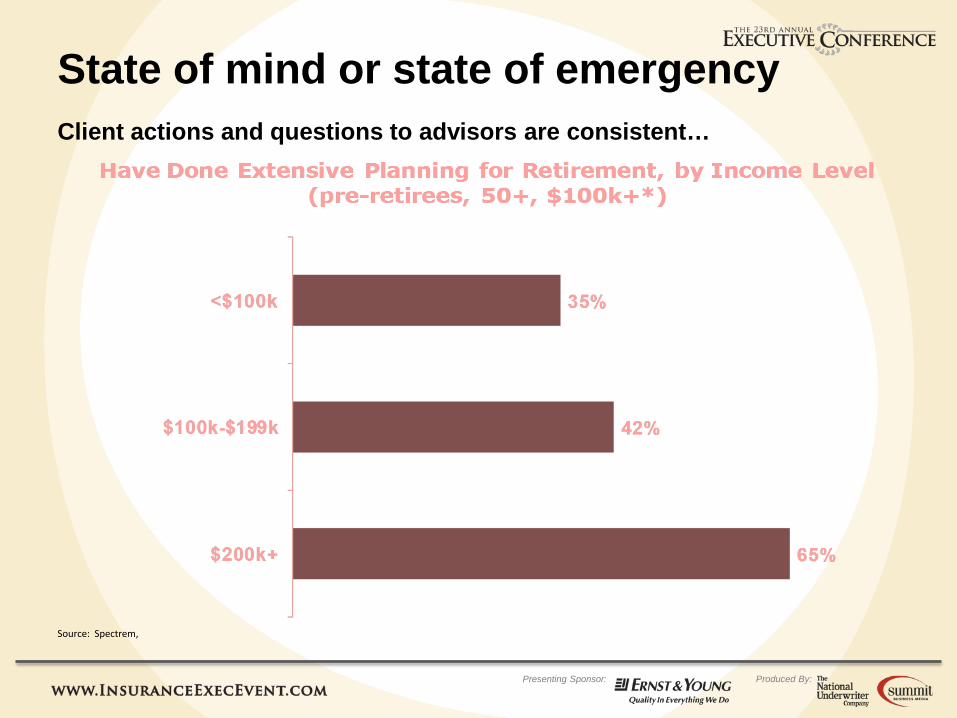

State of mind or state of emergency Client actions and questions to advisors are consistent…

Source: Spectrem,

Presenting Sponsor: Produced By:

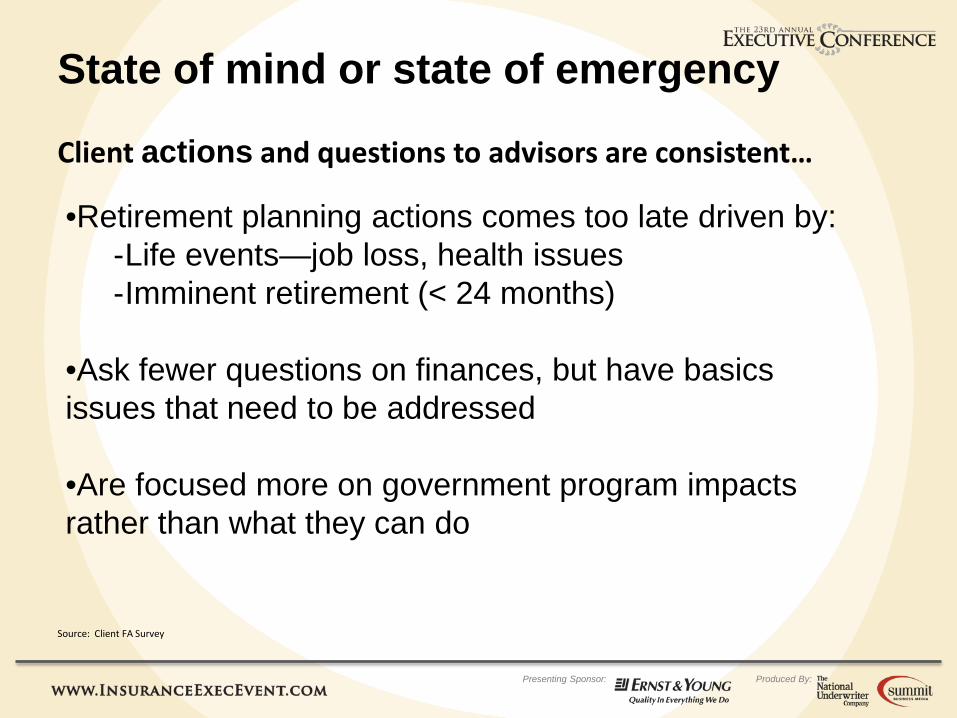

State of mind or state of emergency

Client actions and questions to advisors are consistent…

•Retirement planning actions comes too late driven by: -Life events—job loss, health issues -Imminent retirement (< 24 months)

•Ask fewer questions on finances, but have basics issues that need to be addressed

•Are focused more on government program impacts rather than what they can do

Source: Client FA Survey

Presenting Sponsor: Produced By:

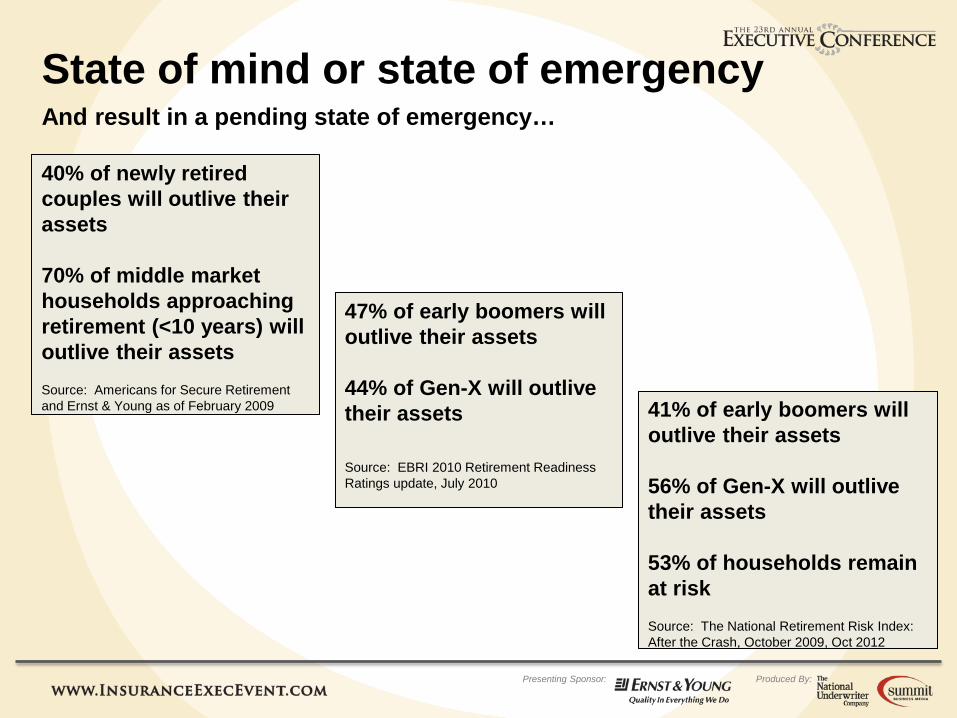

State of mind or state of emergency

40% of newly retired couples will outlive their assets 70% of middle market households approaching retirement (<10 years) will outlive their assets Source: Americans for Secure Retirement and Ernst & Young as of February 2009

47% of early boomers will outlive their assets 44% of Gen-X will outlive their assets Source: EBRI 2010 Retirement Readiness Ratings update, July 2010

And result in a pending state of emergency…

41% of early boomers will outlive their assets 56% of Gen-X will outlive their assets 53% of households remain at risk Source: The National Retirement Risk Index: After the Crash, October 2009, Oct 2012

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

Northwestern Mutual’s Perspective

Rebekah Barsch VP – Market Strategy and Training

Northwestern Mutual

Presenting Sponsor: Produced By:

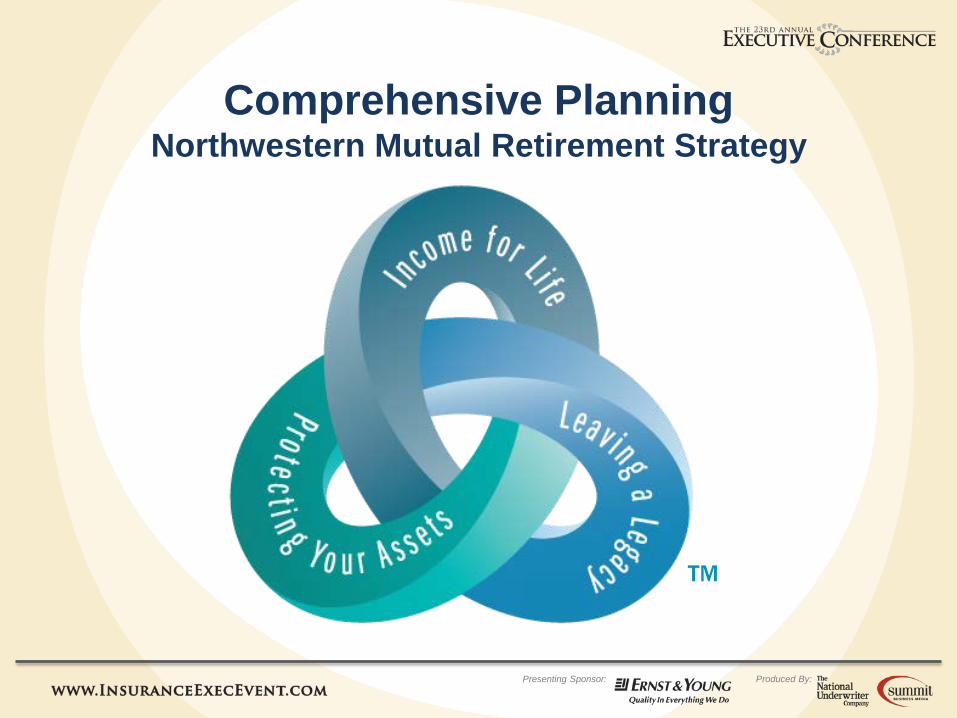

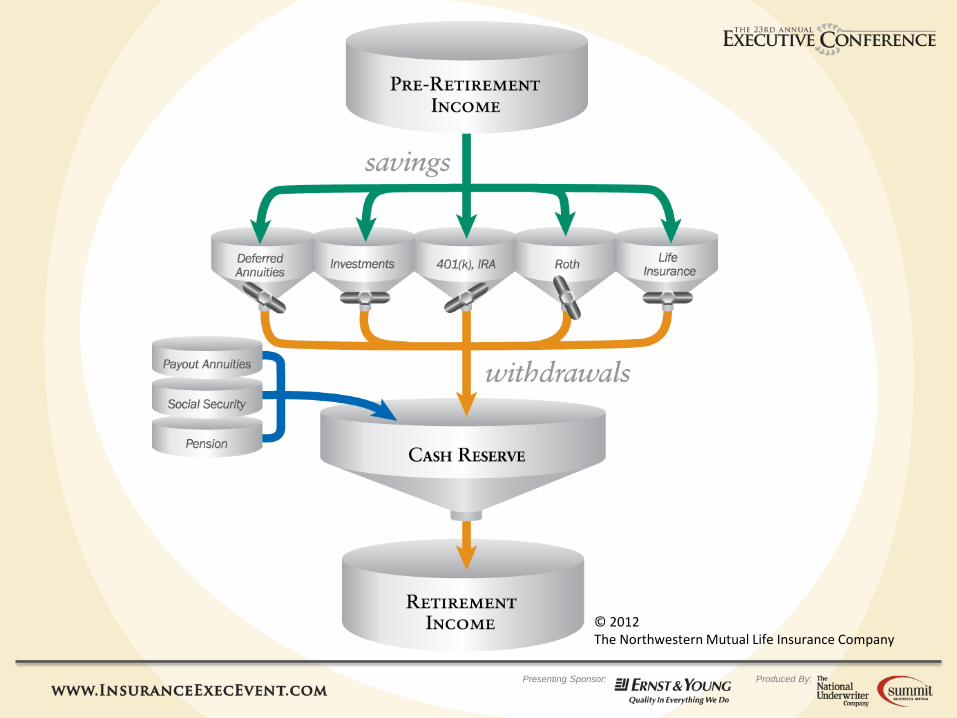

Comprehensive Planning Northwestern Mutual Retirement Strategy

TM

Presenting Sponsor: Produced By:

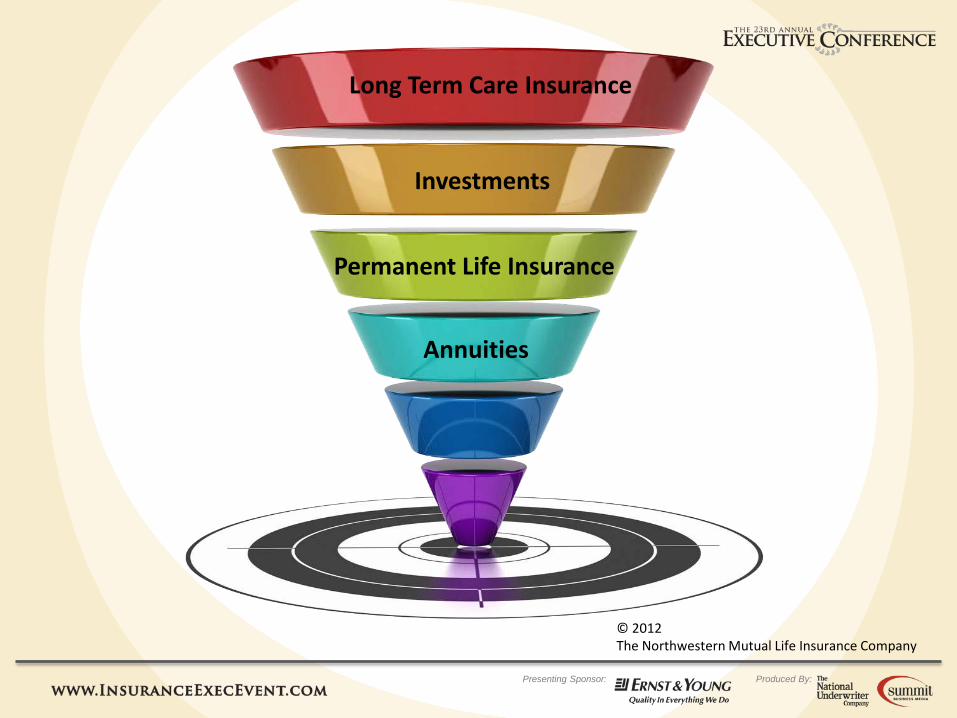

Investments

Long Term Care Insurance

Permanent Life Insurance

Annuities

© 2012 The Northwestern Mutual Life Insurance Company

Presenting Sponsor: Produced By:

© 2012 The Northwestern Mutual Life Insurance Company

Presenting Sponsor: Produced By:

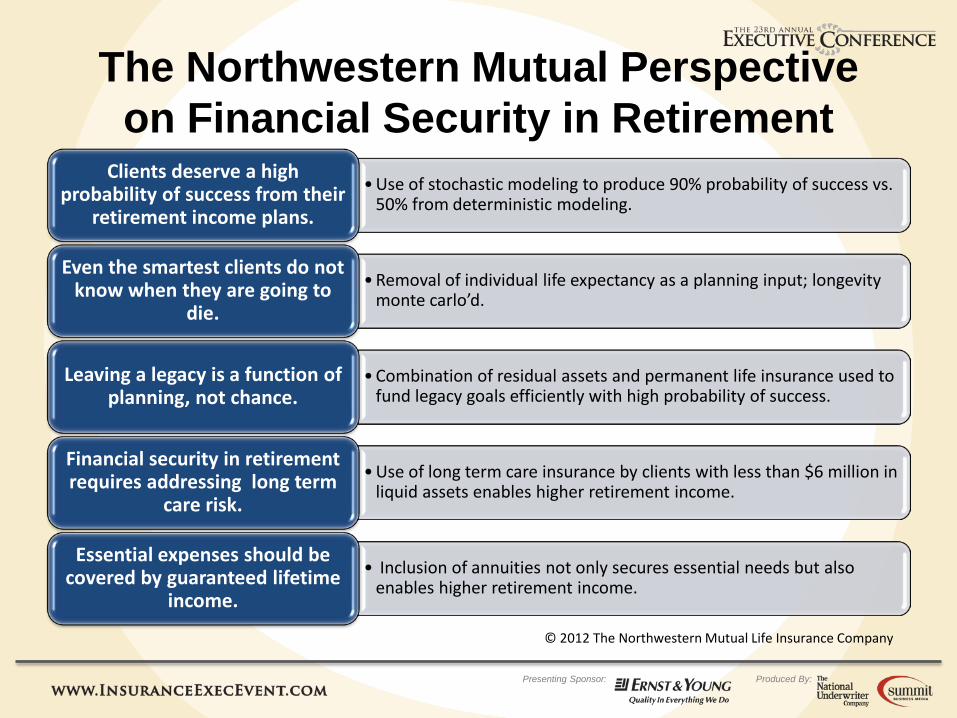

The Northwestern Mutual Perspective on Financial Security in Retirement

© 2012 The Northwestern Mutual Life Insurance Company

•Use of stochastic modeling to produce 90% probability of success vs. 50% from deterministic modeling.

Clients deserve a high probability of success from their

retirement income plans.

•Removal of individual life expectancy as a planning input; longevity monte carlo’d.

Even the smartest clients do not know when they are going to

die.

•Combination of residual assets and permanent life insurance used to fund legacy goals efficiently with high probability of success.

Leaving a legacy is a function of planning, not chance.

•Use of long term care insurance by clients with less than $6 million in liquid assets enables higher retirement income.

Financial security in retirement requires addressing long term

care risk.

• Inclusion of annuities not only secures essential needs but also enables higher retirement income.

Essential expenses should be covered by guaranteed lifetime

income.

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

It’s all about Alpha RETIREMENT ALPHA that is…

Tom Hegna CLU, ChFC, CASL President, TomHegna.com

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

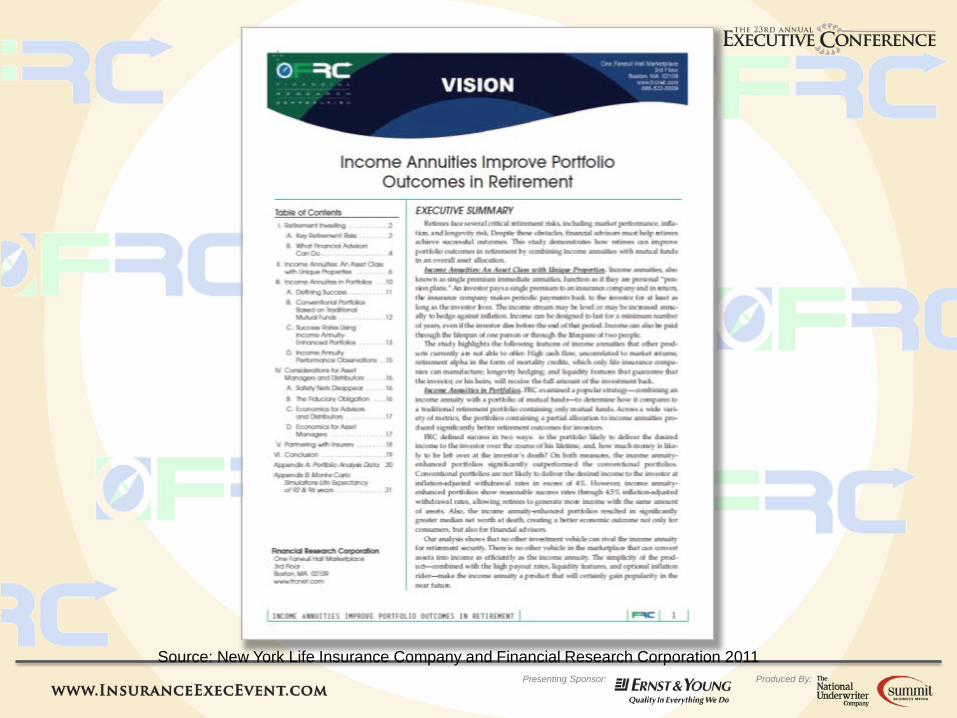

Source: New York Life Insurance Company and Financial Research Corporation 2011

Presenting Sponsor: Produced By:

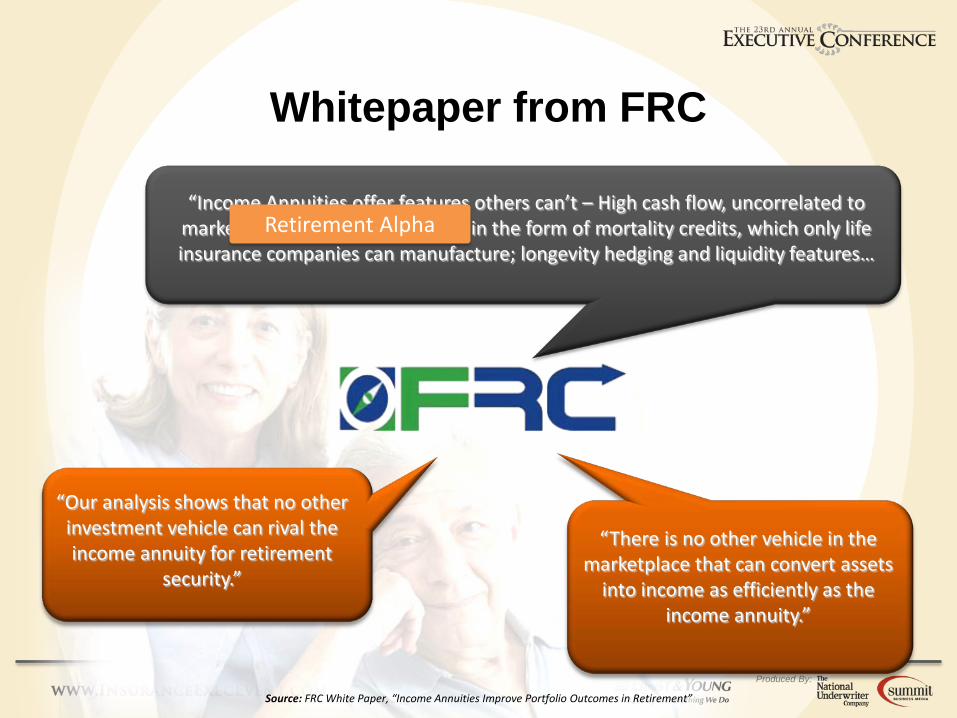

“There is no other vehicle in the marketplace that can convert assets

into income as efficiently as the income annuity.”

“Our analysis shows that no other investment vehicle can rival the income annuity for retirement

security.”

“Income Annuities offer features others can’t – High cash flow, uncorrelated to market returns; retirement alpha in the form of mortality credits, which only life insurance companies can manufacture; longevity hedging and liquidity features…

Source: FRC White Paper, “Income Annuities Improve Portfolio Outcomes in Retirement”

Whitepaper from FRC

Retirement Alpha

Presenting Sponsor: Produced By:

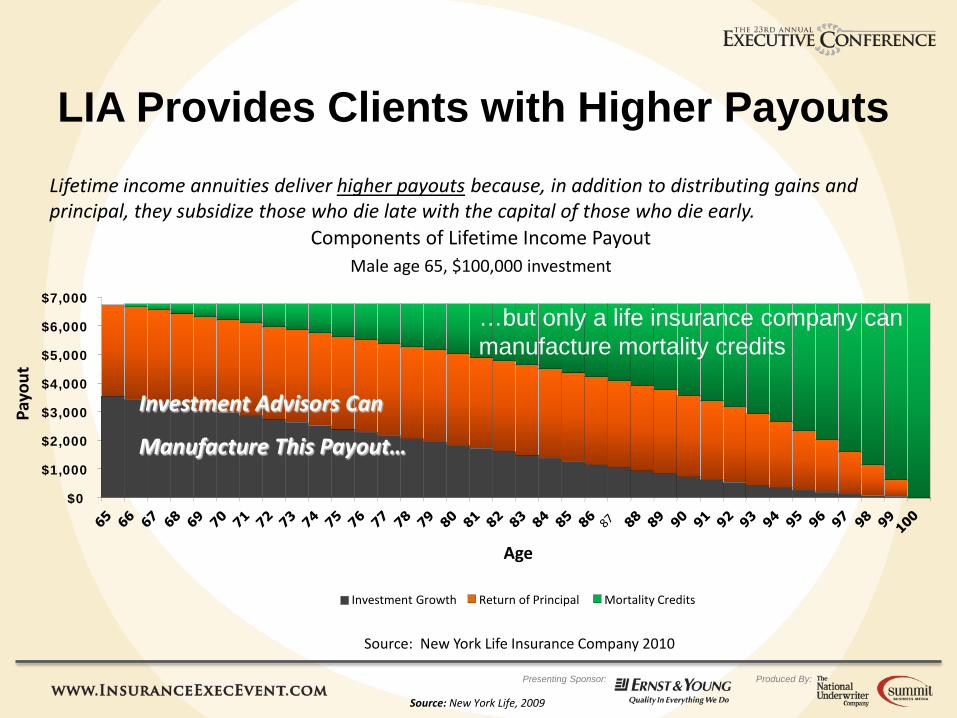

…but only an insurance company can

manufacture a mortality pool.

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Age

Payo

ut

Investment Growth Return of Principal Mortality Credits

LIA Provides Clients with Higher Payouts

Components of Lifetime Income Payout Male age 65, $100,000 investment

Lifetime income annuities deliver higher payouts because, in addition to distributing gains and principal, they subsidize those who die late with the capital of those who die early.

Source: New York Life, 2009

Investment Advisors Can

Manufacture This Payout…

…but only a life insurance company can manufacture mortality credits

Source: New York Life Insurance Company 2010

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

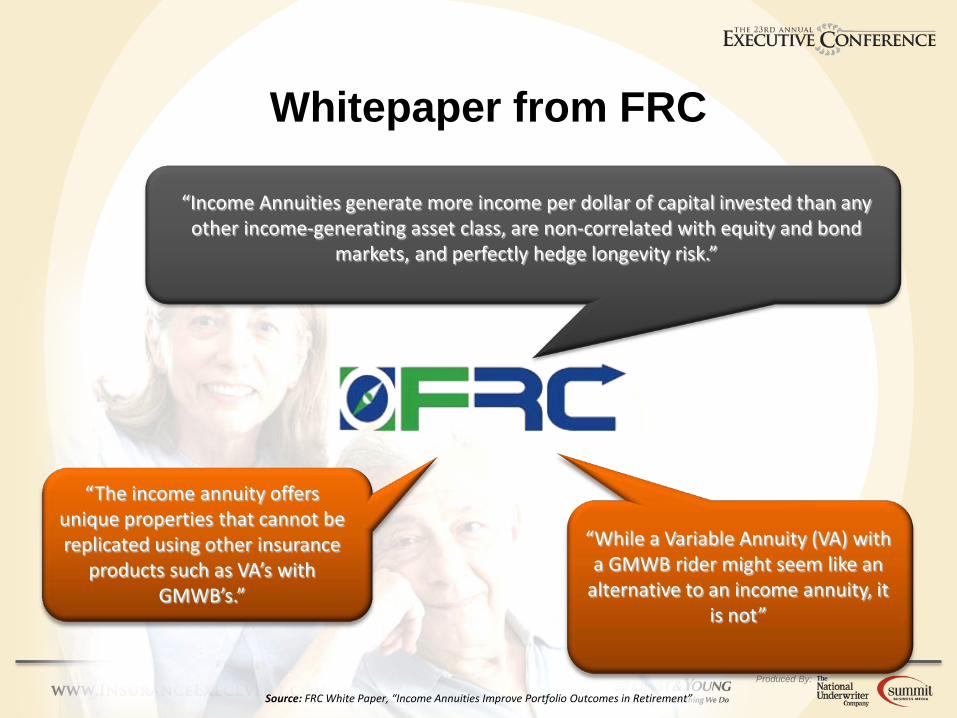

“While a Variable Annuity (VA) with a GMWB rider might seem like an

alternative to an income annuity, it is not”

“The income annuity offers unique properties that cannot be replicated using other insurance

products such as VA’s with GMWB’s.”

“Income Annuities generate more income per dollar of capital invested than any other income-generating asset class, are non-correlated with equity and bond

markets, and perfectly hedge longevity risk.”

Source: FRC White Paper, “Income Annuities Improve Portfolio Outcomes in Retirement”

Whitepaper from FRC

Presenting Sponsor: Produced By:

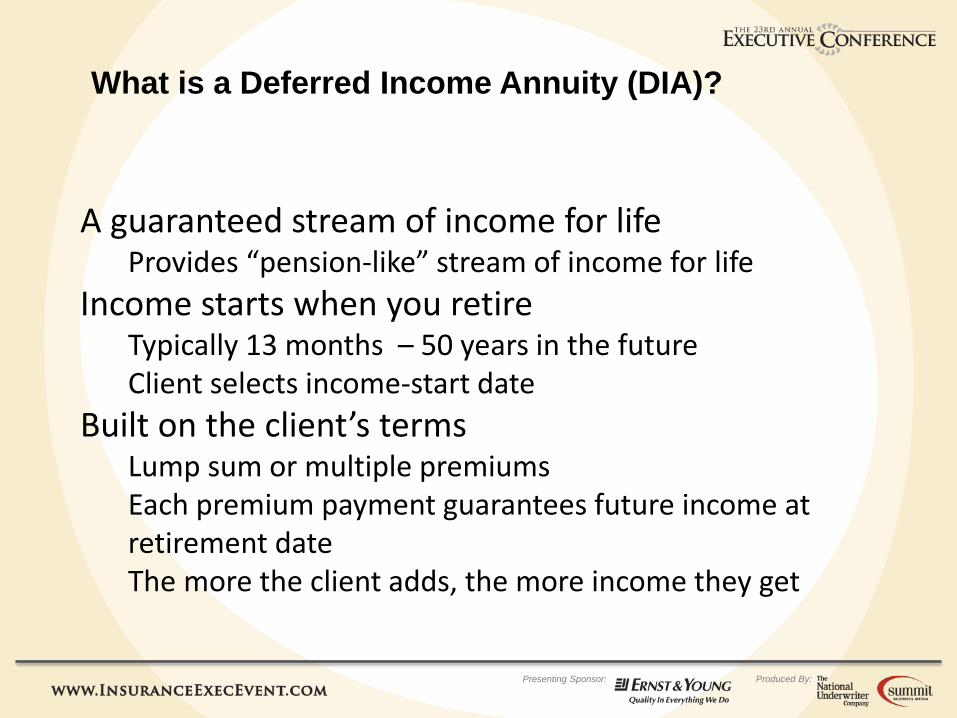

What is a Deferred Income Annuity (DIA)?

A guaranteed stream of income for life Provides “pension-like” stream of income for life

Income starts when you retire Typically 13 months – 50 years in the future Client selects income-start date

Built on the client’s terms Lump sum or multiple premiums Each premium payment guarantees future income at retirement date The more the client adds, the more income they get

Presenting Sponsor: Produced By:

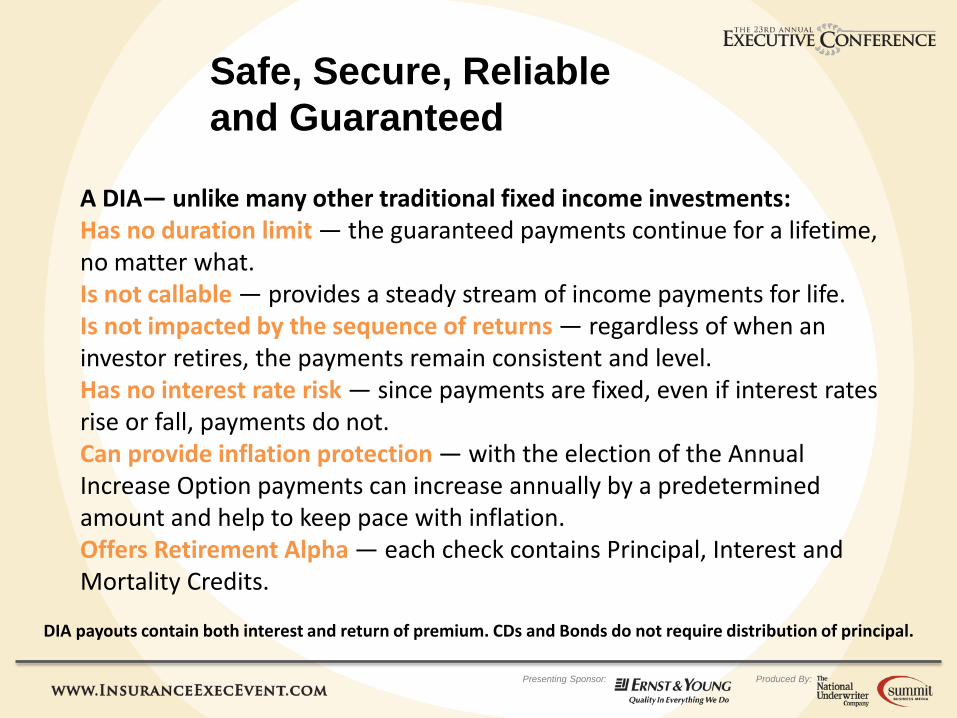

Safe, Secure, Reliable and Guaranteed

A DIA— unlike many other traditional fixed income investments: Has no duration limit — the guaranteed payments continue for a lifetime, no matter what. Is not callable — provides a steady stream of income payments for life. Is not impacted by the sequence of returns — regardless of when an investor retires, the payments remain consistent and level. Has no interest rate risk — since payments are fixed, even if interest rates rise or fall, payments do not. Can provide inflation protection — with the election of the Annual Increase Option payments can increase annually by a predetermined amount and help to keep pace with inflation. Offers Retirement Alpha — each check contains Principal, Interest and Mortality Credits.

DIA payouts contain both interest and return of premium. CDs and Bonds do not require distribution of principal.

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

Retirement RIOT™

Curtis V. Cloke, CLTC, LUTCF CEO / Founder

Thrive Income Distribution System

Presenting Sponsor: Produced By:

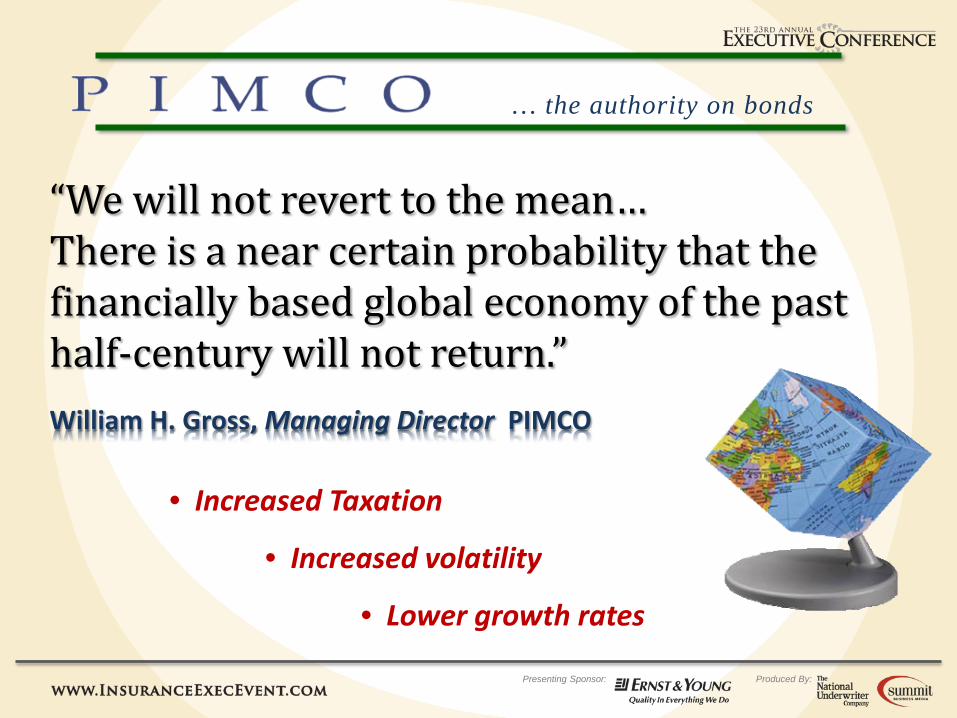

… the authority on bonds

“We will not revert to the mean… There is a near certain probability that the financially based global economy of the past half-century will not return.” William H. Gross, Managing Director PIMCO

• Increased Taxation

• Increased volatility

• Lower growth rates

Presenting Sponsor: Produced By:

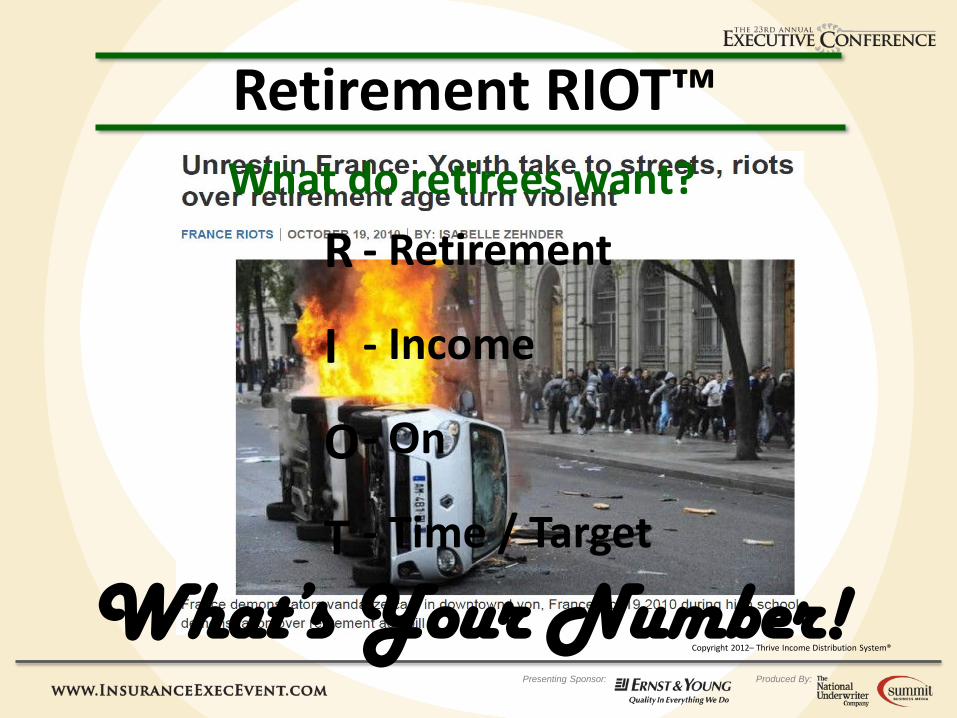

What do retirees want?

Retirement RIOT™

R

I

O

T

- Retirement

- Income

- On

- Time / Target

What’s Your Number! Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

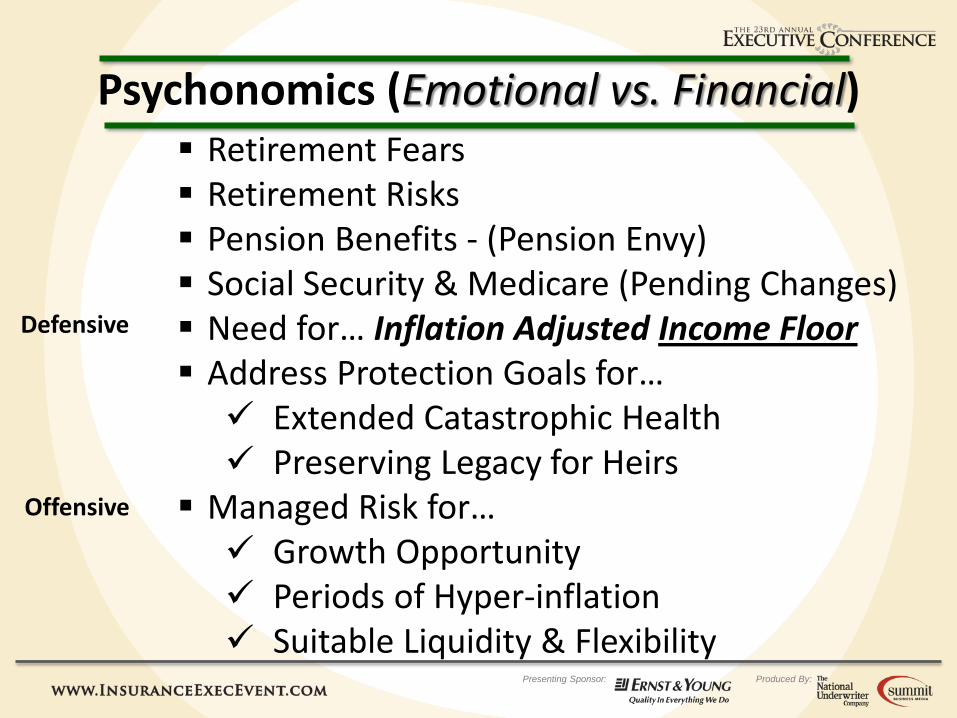

Psychonomics (Emotional vs. Financial) Retirement Fears Retirement Risks Pension Benefits - (Pension Envy) Social Security & Medicare (Pending Changes) Need for… Inflation Adjusted Income Floor Address Protection Goals for… Extended Catastrophic Health Preserving Legacy for Heirs

Managed Risk for… Growth Opportunity Periods of Hyper-inflation Suitable Liquidity & Flexibility

Defensive

Offensive

Presenting Sponsor: Produced By:

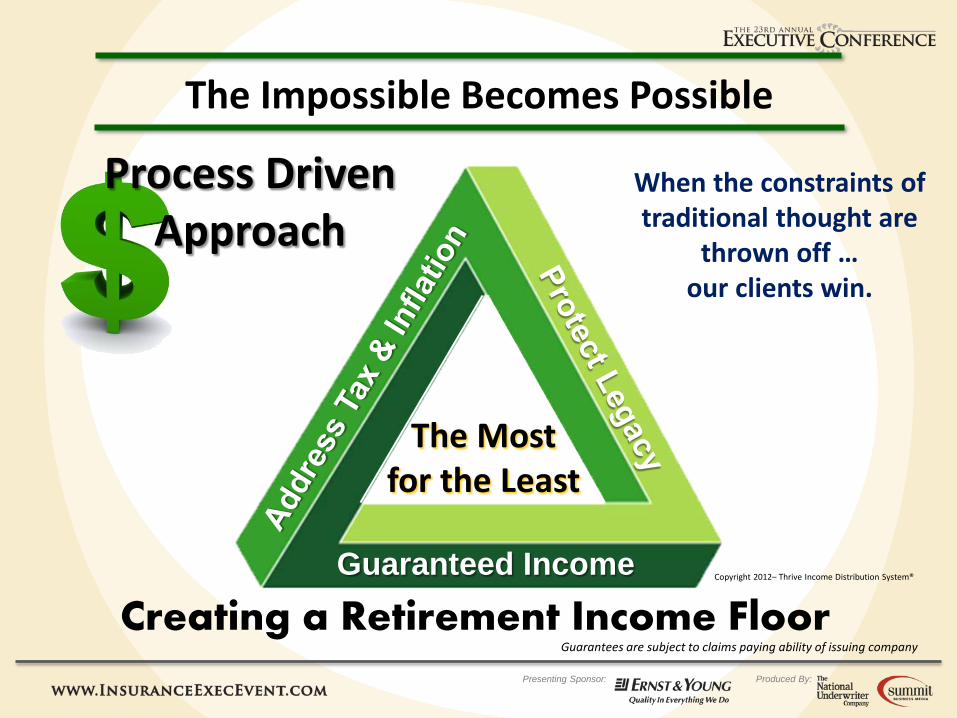

Guaranteed Income

The Most for the Least

The Impossible Becomes Possible

Guarantees are subject to claims paying ability of issuing company

When the constraints of traditional thought are

thrown off … our clients win.

Creating a Retirement Income Floor

Process Driven Approach

Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

Single Premium Immediate Annuity

help us optimize what our clients want? What combination of Guaranteed* Solutions

Guaranteed Solutions Require Insurance

Guaranteed Lifetime Withdrawal Benefit

Rider to Deferred Annuity

Single Premium Deferred Income Annuity

Income Rider Withdrawals

Annuitized Payments

Annuitized Payments

Income NOW Income LATER

Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

Guarantee Income

Maximize Returns

Minimize Risk

Beat Inflation

Leave Legacy

Minimize Taxes

Many goals to achieve

… Meets emotional and financial needs for a lifetime

Creating a Retirement Plan is Complex

26

Process

Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

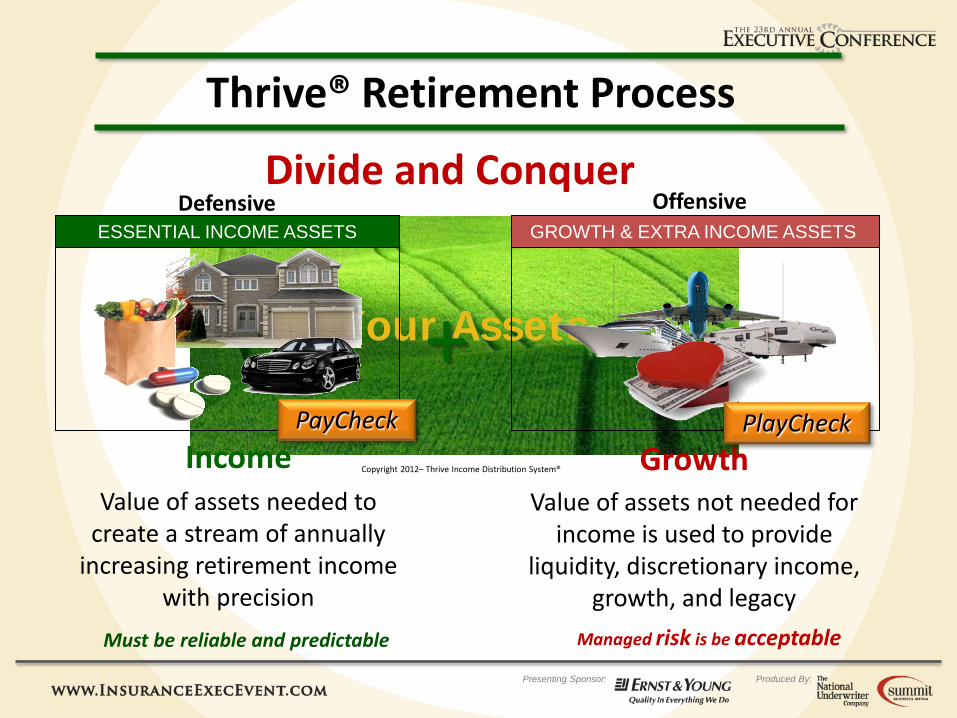

Thrive® Retirement Process

Your Assets

Income Value of assets needed to

create a stream of annually increasing retirement income

with precision

Growth Value of assets not needed for

income is used to provide liquidity, discretionary income,

growth, and legacy

+ ESSENTIAL INCOME ASSETS GROWTH & EXTRA INCOME ASSETS

PayCheck PlayCheck

Must be reliable and predictable

Managed risk is be acceptable

Divide and Conquer Defensive Offensive

Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

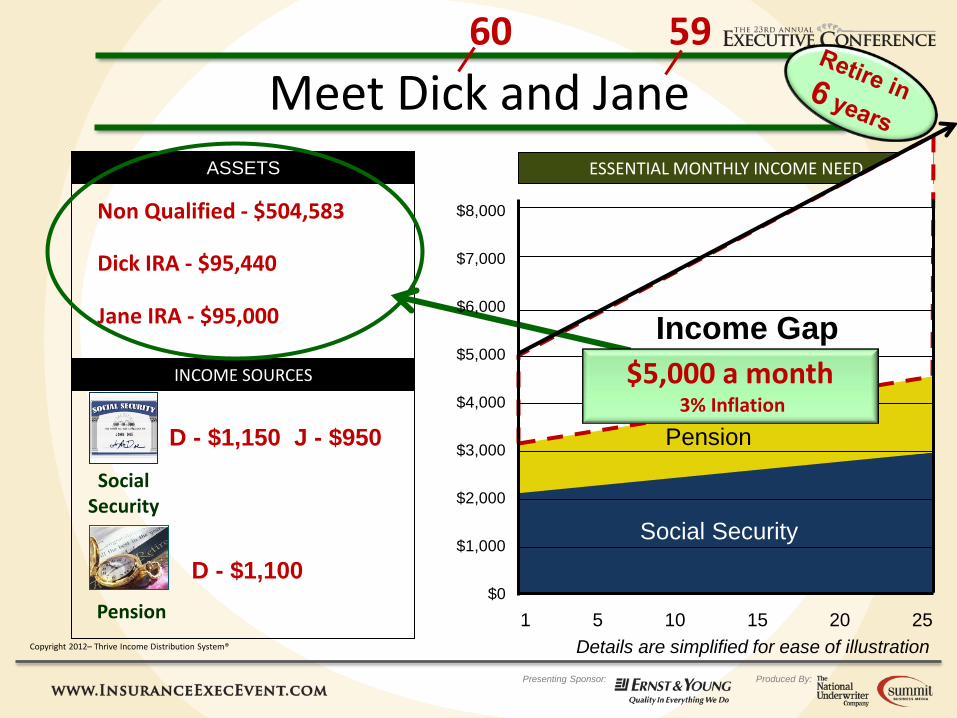

Meet Dick and Jane ASSETS

60 59

Details are simplified for ease of illustration

Pension

Social Security

D - $1,150 J - $950

D - $1,100

Non Qualified - $504,583

Dick IRA - $95,440

Jane IRA - $95,000

ESSENTIAL MONTHLY INCOME NEED

Income Gap INCOME SOURCES

Social Security

Pension

$8,000

$7,000

$6,000

$5,000

$4,000

$3,000

$2,000

$1,000

$0

1 5 10 15 20 25

$5,000 a month 3% Inflation

Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

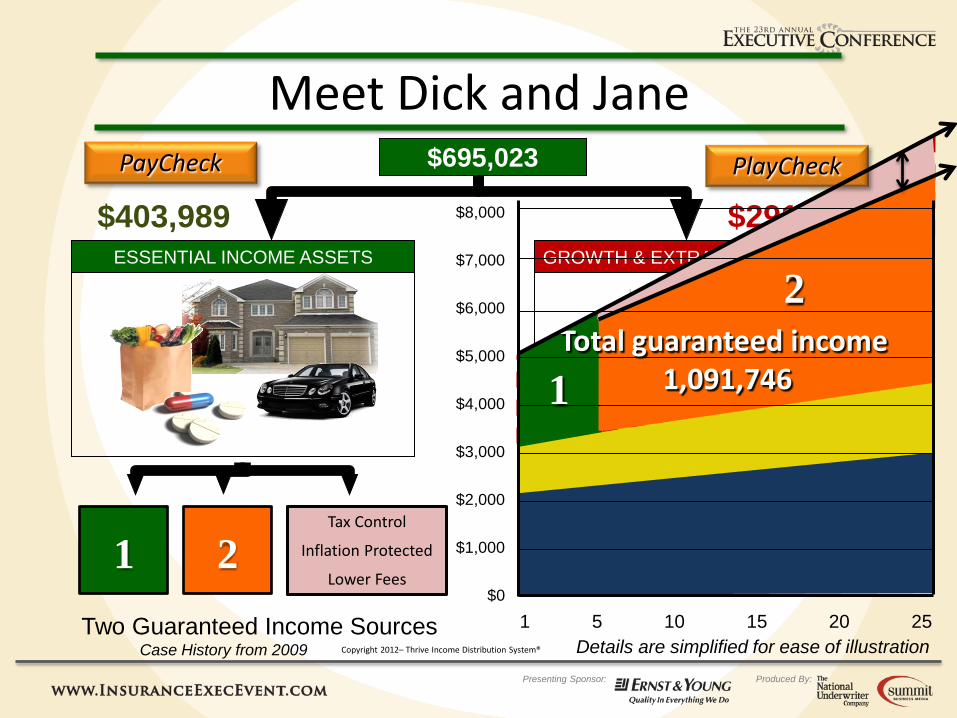

ESSENTIAL INCOME ASSETS GROWTH & EXTRA INCOME ASSETS

Details are simplified for ease of illustration

$695,023 $403,989 $291,034

Tax Control

Inflation Protected

Lower Fees

Two Guaranteed Income Sources Case History from 2009

1 2

$8,000

$7,000

$6,000

$5,000

$4,000

$3,000

$2,000

$1,000

$0

1 5 10 15 20 25

Total guaranteed income 1,091,746 1

2

Meet Dick and Jane PayCheck PlayCheck

Copyright 2012– Thrive Income Distribution System®

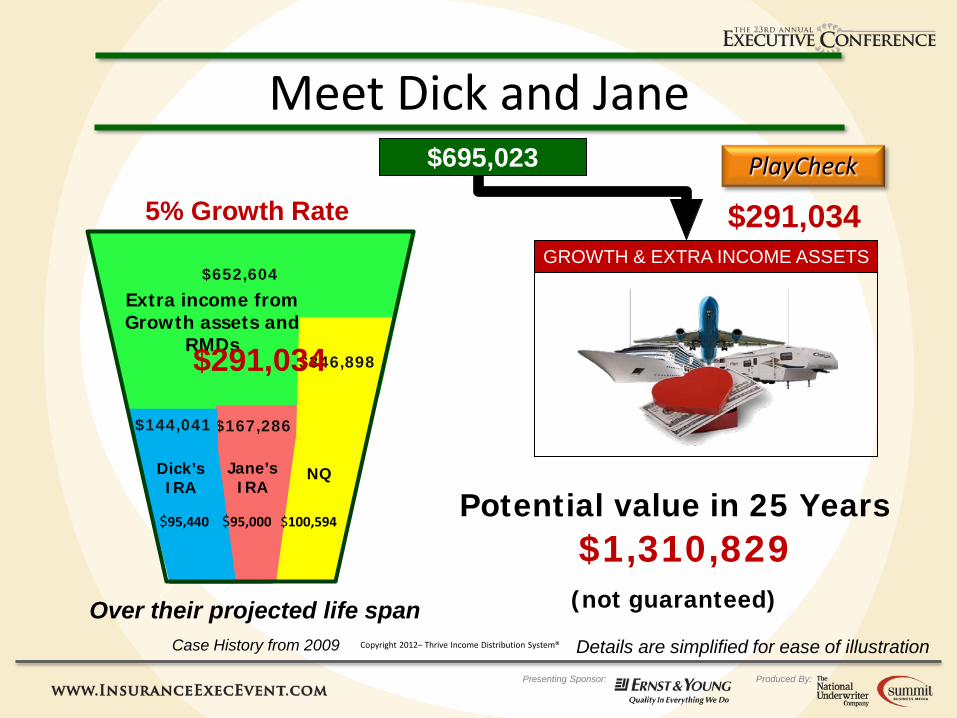

Presenting Sponsor: Produced By:

Extra income from Growth assets and

RMDs $346,898

$167,286 $144,041

$652,604

Dick’s IRA

Jane’s IRA

NQ

$95,440 $95,000 $100,594 Potential value in 25 Years

$1,310,829

(not guaranteed)

GROWTH & EXTRA INCOME ASSETS

$695,023 $291,034 5% Growth Rate

Over their projected life span Details are simplified for ease of illustration Case History from 2009

$291,034

Meet Dick and Jane PlayCheck

Copyright 2012– Thrive Income Distribution System®

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

Questions?

Presenting Sponsor: Produced By:

Presenting Sponsor: Produced By:

Thank you!

Recommended