Indian Organized Retail SectorIssues & Predictions

1

India is the fifth largest retail market globally, with a size of INR 16

trillion, and has been growing at 15% per annum.

Organized retail accounts for just 5% of total retail sales and has been

growing at 35% CAGR.

India’s robust macro- and microeconomic fundamentals, such as

robust GDP growth, higher incomes, increasing personal consumption,

favourable demographics and supportive government policies, surely

increased the growth in the retail sector but it all couldn’t helped in

stopping the operational costs thus reducing in the overall margins.

2

We have structured the report broadly into three

categories:

(1)Learning from the past

(2) Consolidation

(3) Critical issues

(4) View on future

3

During 2005-2007, the sector was in a hyper growth phase. In pursuit to capture market,

companies made strategic as well as operational errors which has been broadly

classified as follows:

Race for increasing retail space resulting in haphazard growth.

Unviable formats.

High lease rentals.

Manpower costs and productivity issues.

Poor backend infrastructure.

Entry of too many new players.

4

1) Race for increasing retail space resulting in haphazard growth: Organized

retailers entered the race of adding retail space without proper due diligence

on the catchment area, mall density and acceptability of organized retail.

2) Unviable formats: Large players entered numerous formats, some of which

proved to be unviable.

3) High lease rentals: Retail is a tough business to operate, PAT margins are

as low as 2-3%. Indian organized retail follows the lease rental model due to

high real estate costs and paucity of quality malls. Lease rentals should ideally

be 3-6% of sales depending upon the format.

However, rentals in a few specialty stores touched Rs 300/sq feet/month

during the heydays - in a period of two years, lease rentals in general

increased 50-70%. The increase was more evident in FY08 and FY09 due to

decline in same store sales growth. Currently, the price/sq feet can reach in

thousands.

5

4) Manpower costs and productivity issues: As trained manpower was scarce,

salaries of experienced retailing professionals went through the roof.

5) Poor Backend infrastructure: Retailers focused all their energies on store

openings and neglected the backend.

6) Entry of too many new players: Viewing it as a sunrise sector, too many

players entered organized retail and some have perished.

6

In the global slowdown phase starting from 2007, the Indian retail players paused, to realize their past mistakes and took time and efforts to re-organize themselves:

Focus on profitable growth

Exit from unprofitable stores/formats

Rental renegotiation/revenue sharing arrangements

Reduction in salaries/ higher manpower productivity

Significant investments in backend

Exit of unsuccessful new entrants

7

1) Focus on profitable growth: Retailers paused and realized their errors and startedusing analytics for insights into the business, but analytics used was onlyconcentrated towards the finding of most feasible location to open a new store.

2)Exit from unprofitable stores/formats: whole new set of formats and store sizes, with aview to capture consumption and increase share in consumer wallet. The industry hastried to control costs and address the issue by way of store closure, exit from formats,restructuring of format, Change of location.

3)Rental renegotiation/revenue sharing arrangements: After touching the unprecedentedhighs, lease rentals softened, revenue sharing arrangements came into picture.

4) Reduction in salaries/ higher manpower productivity: stopped paying fancy salaries to attract the top talent.

5) Significant investments in backend: Post the slowdown, retailers have been making huge investments to strengthen their backend systems.

6) Exit of unsuccessful new entrants

8

Soaring real estate prices.

Intense competition : customers, now have the option to select any of the

stores they want.

Reduction in customer loyalty: customers, are now smart enough in saving

their time and money, only increase in per capita income or GDP doesn’t

always help.

No cheap labor.

Exponential increase in operating costs like electricity bills, salary for the

staff, vendor management costs, relationship building costs and other

miscellaneous but mandatory costs.

9

Standard Cost reduction scenario:

Air India used silver spoon from 1948 to 1962, gradually they came down to stainless steel and finally a

plastic spoon.

Transformational Change:

Apple changed the way people used to think about music, with proper planning they are the leaders in the

market now.

Retail industry should now have to act smart and move towards the transformational changes.

10

Since, the fixed operating costs can’t be reduced for any retail, hence this research

revolves around the following questions:

How to achieve the maximum positive footfalls?

What is the buying behavioral pattern of a customer?

What is the customers’ psychology while going to any retail store?

What if, the cost can be reduced through following a eco-green building

model?

This research will aim at attracting new customers as well as retaining old ones, and

suggest possible future models to increase profit and provide better value to a

customer

So we started this project to help reduce operating cost of existing retail business

and suggest possible future model to increase profit and provide better value to

customer

11

Questionnaire: Prepared to meet our objective.

Pilot testing: Data collection to validate and verify the research objective.

Survey: Data collected using offline and online methods.

Data Validation: Cleaning and extracting useful data.

Data Exploration: To analyze which store has maximum footfalls based on

gender, age group and marital status.

Clustering and Segmentation: To understand the shopping behavior of

customers, like the preferable time and which day of the week they shop.

Regression Analysis: For the SWOT analysis of the retail stores, based on

the parameters in the questionnaire.

Correlation Analysis: Finding the relationship between the variables.

Summarizing the results.

12

Tools used:

Microsoft Office Excel 2007

Bas SAS 9.1

SAS Enterprise Miner 6.1

SAS Enterprise Guide 4.2

13

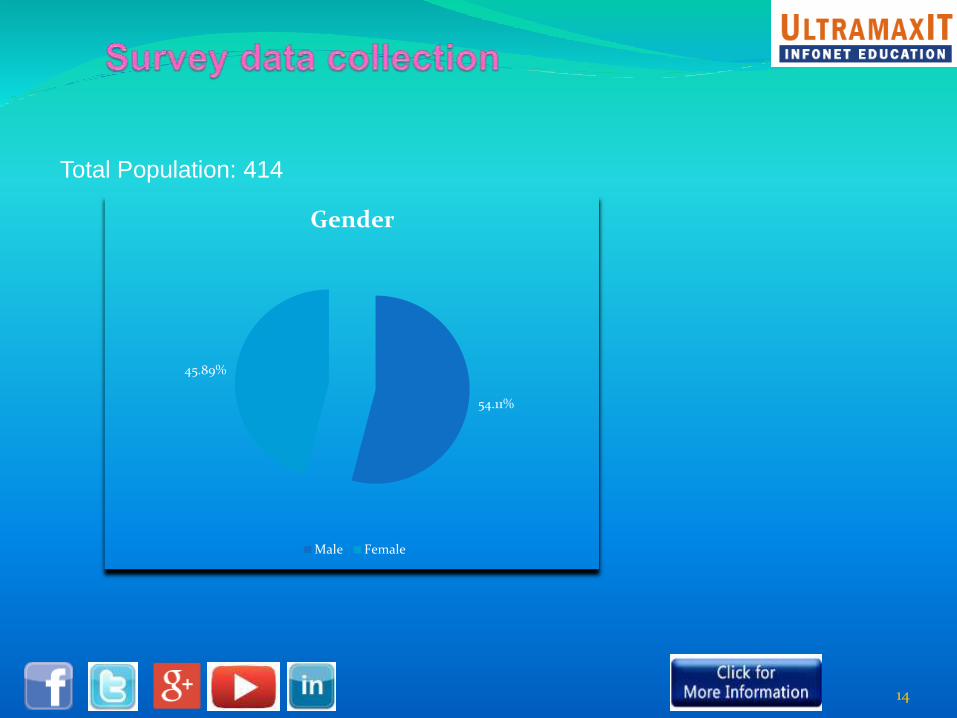

Total Population: 414

54.11%

45.89%

Gender

Male Female

14

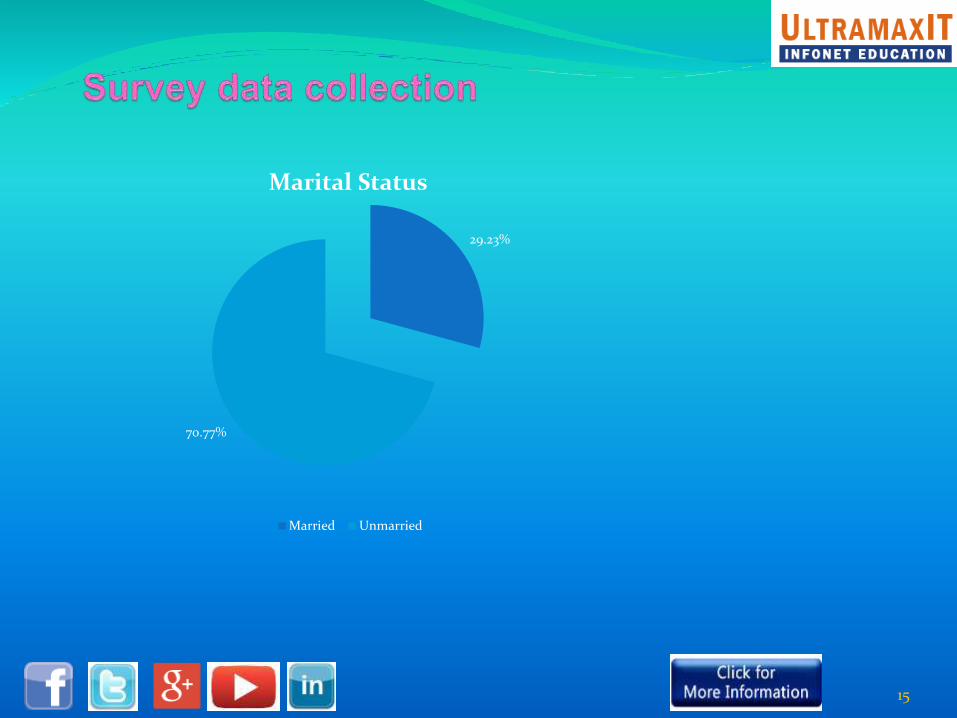

29.23%

70.77%

Marital Status

Married Unmarried

15

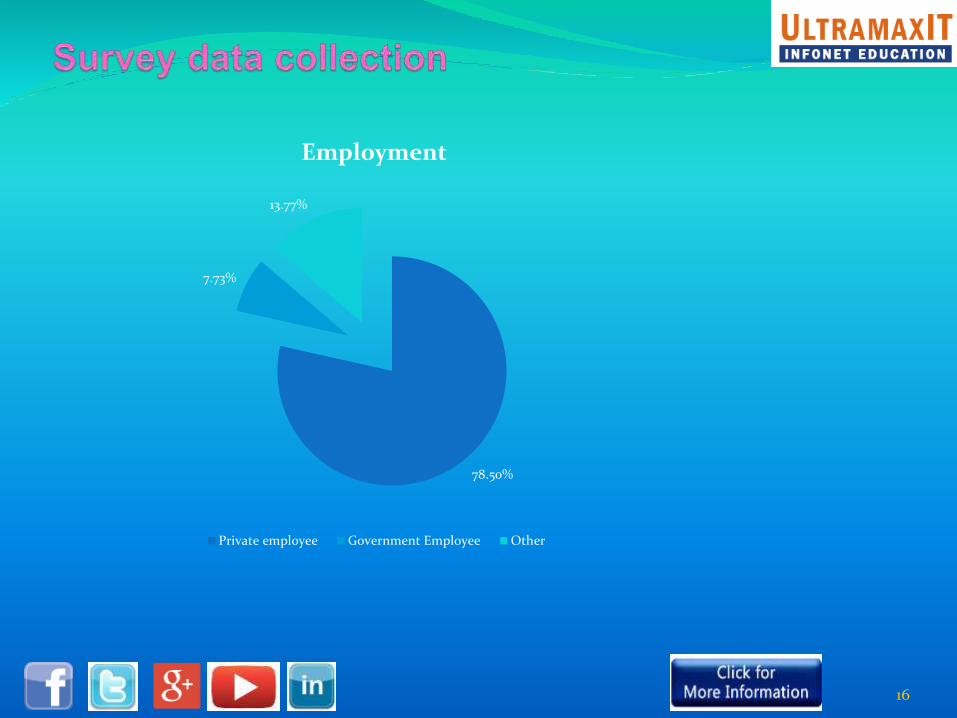

78.50%

7.73%

13.77%

Employment

Private employee Government Employee Other

16

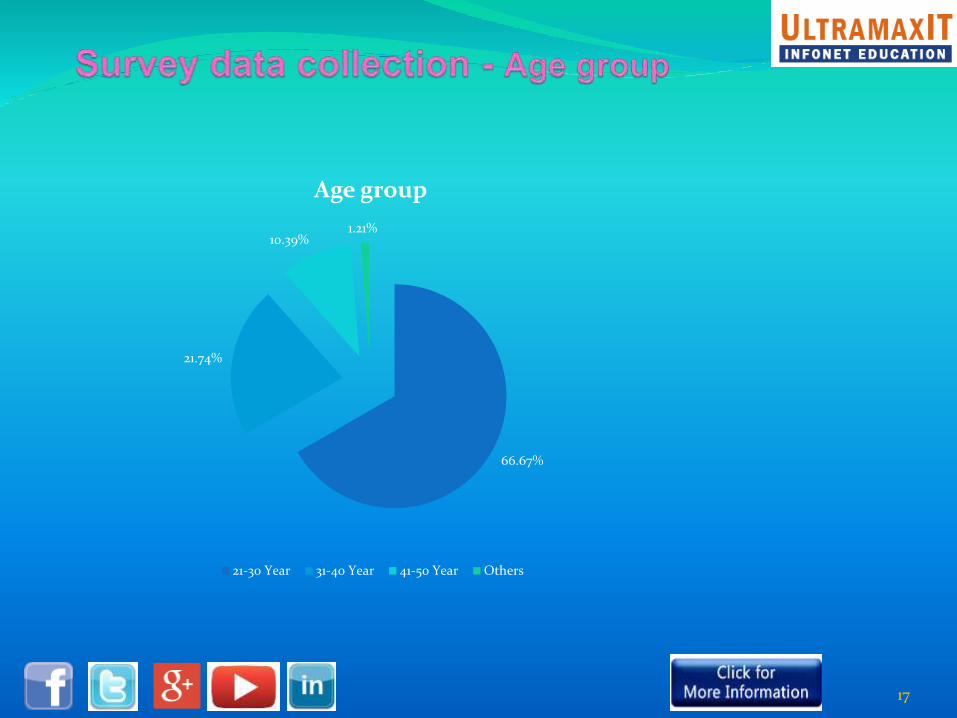

66.67%

21.74%

10.39%1.21%

Age group

21-30 Year 31-40 Year 41-50 Year Others

17

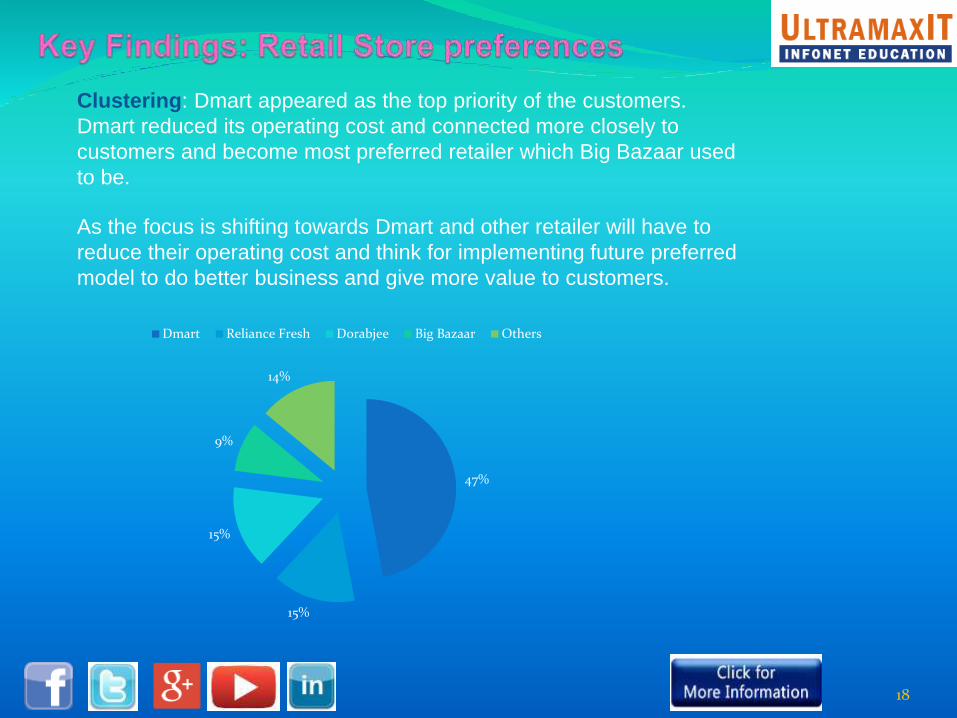

Clustering: Dmart appeared as the top priority of the customers.

Dmart reduced its operating cost and connected more closely to

customers and become most preferred retailer which Big Bazaar used

to be.

As the focus is shifting towards Dmart and other retailer will have to

reduce their operating cost and think for implementing future preferred

model to do better business and give more value to customers.

47%

15%

15%

9%

14%

Dmart Reliance Fresh Dorabjee Big Bazaar Others

18

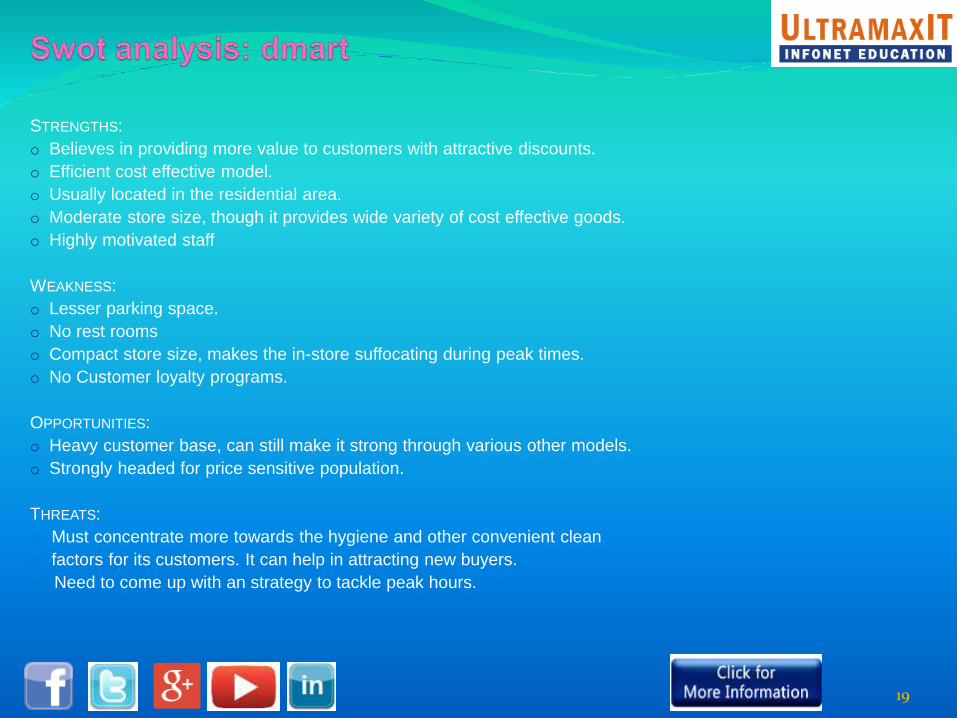

STRENGTHS:

o Believes in providing more value to customers with attractive discounts.

o Efficient cost effective model.

o Usually located in the residential area.

o Moderate store size, though it provides wide variety of cost effective goods.

o Highly motivated staff

WEAKNESS:

o Lesser parking space.

o No rest rooms

o Compact store size, makes the in-store suffocating during peak times.

o No Customer loyalty programs.

OPPORTUNITIES:

o Heavy customer base, can still make it strong through various other models.

o Strongly headed for price sensitive population.

THREATS:

o Must concentrate more towards the hygiene and other convenient clean

o factors for its customers. It can help in attracting new buyers.

o Need to come up with an strategy to tackle peak hours.

19

STRENGTHS:

Strong supplier tie-ups.

Huge advertising budgets, having potential to have new customers.

WEAKNESS:

Lesser savings comparatively to D-Mart.

Lesser variety of goods.

Discounts and offers are released for about to expire goods.

OPPORTUNITIES:

Should use the supplies efficiently.

Must concentrate on the quality of goods offered.

Should use the customer card in analyzing their buying trends.

THREATS:

Price sensitive population are continuously ignoring the store.

Major threat is for its survival.

20

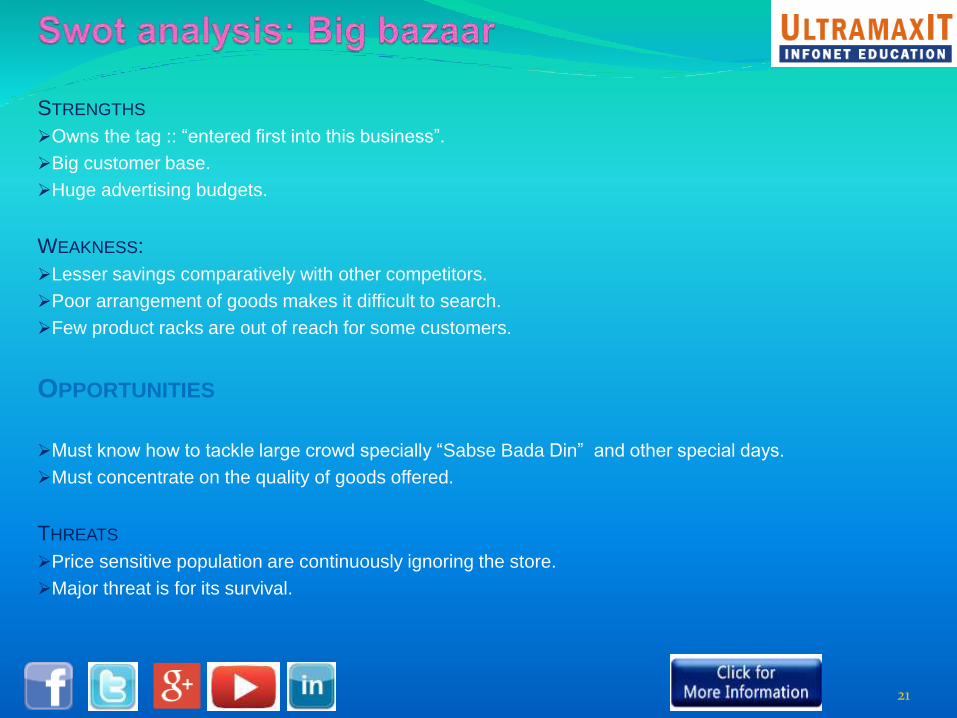

STRENGTHS

Owns the tag :: “entered first into this business”.

Big customer base.

Huge advertising budgets.

WEAKNESS:

Lesser savings comparatively with other competitors.

Poor arrangement of goods makes it difficult to search.

Few product racks are out of reach for some customers.

OPPORTUNITIES

Must know how to tackle large crowd specially “Sabse Bada Din” and other special days.

Must concentrate on the quality of goods offered.

THREATS

Price sensitive population are continuously ignoring the store.

Major threat is for its survival.

21

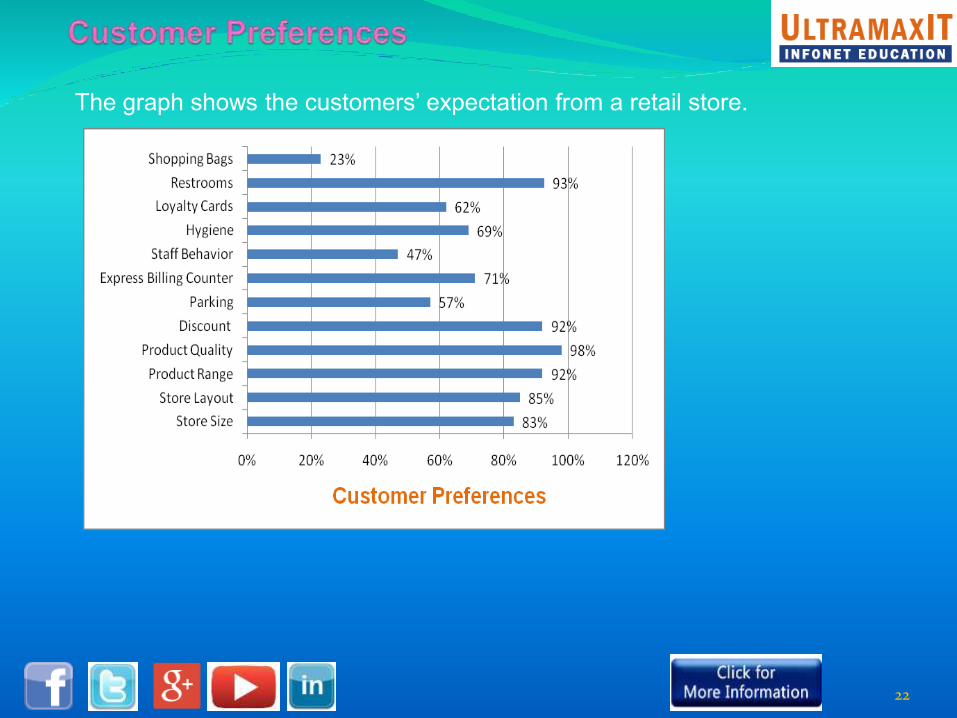

The graph shows the customers’ expectation from a retail store.

22

Majority customers coming on Saturday and Sunday.

Based on the feedback during the research, there were many people visiting the

stores weekdays unwillingly so as to avoid the weekend rush.

23

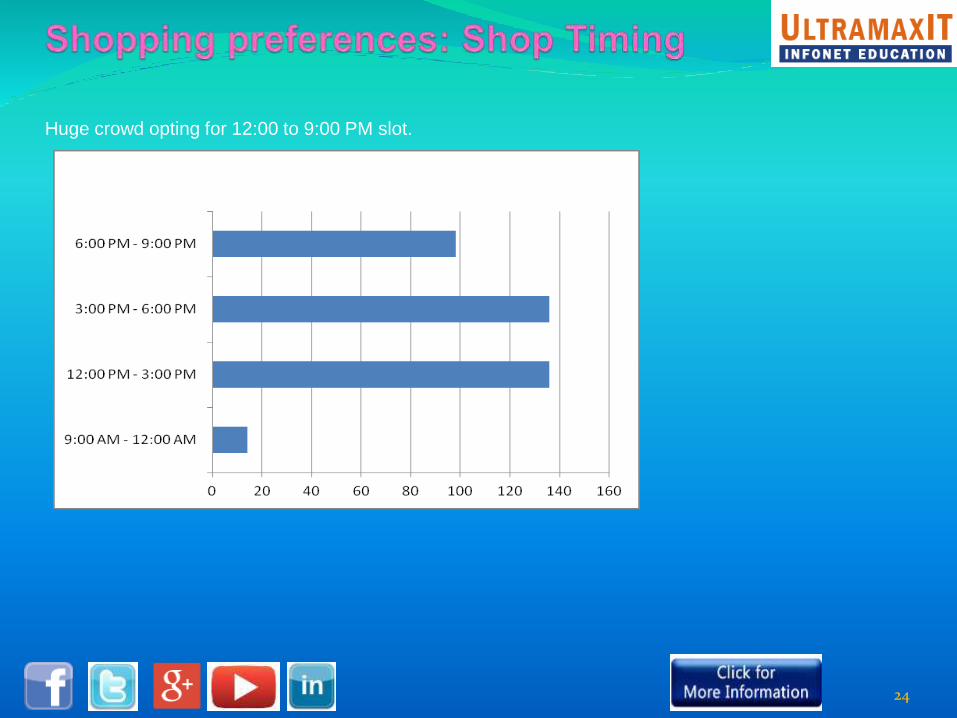

Huge crowd opting for 12:00 to 9:00 PM slot.

24

Based on day and time preference by most of customers we have suggested below solutions to retain

customers more happily coming on weekend and can reduce their operating cost.

HAPPY HOURS: Since the majority customers visit during weekends, after 3:00 PM, so the concept of happy

hours might help, which retailers can introduce from morning to 12:00 Noon and can start store little early in

morning on weekend or holidays.

EXPRESS COUNTERS: Increase the minimum items in express counters. In this way more customer will be

handled in express counter.

REDUCE MANPOWER AND ENERGY ON LEAST SHOPPED DAY: Retailer can return to old working style.

Keep store close on least shopping day and give more value to existing customers and can build long

relationship. So saving in operating cost and retaining customers.

CUSTOMER LOYALTY PROGRAM: Introducing customer loyalty programs to study the buying behavior of the

customers. Retail companies should work more towards customer satisfaction, e.g. wishing them on their

special days, offer special discounts to them on those days.

TOKEN SYSTEM: Retailers can introduce token system, to the customers standing in queue. Customers can

hang the token in their trolley and collect their goods later when they are called. In this way customer would

be happily retained.

25

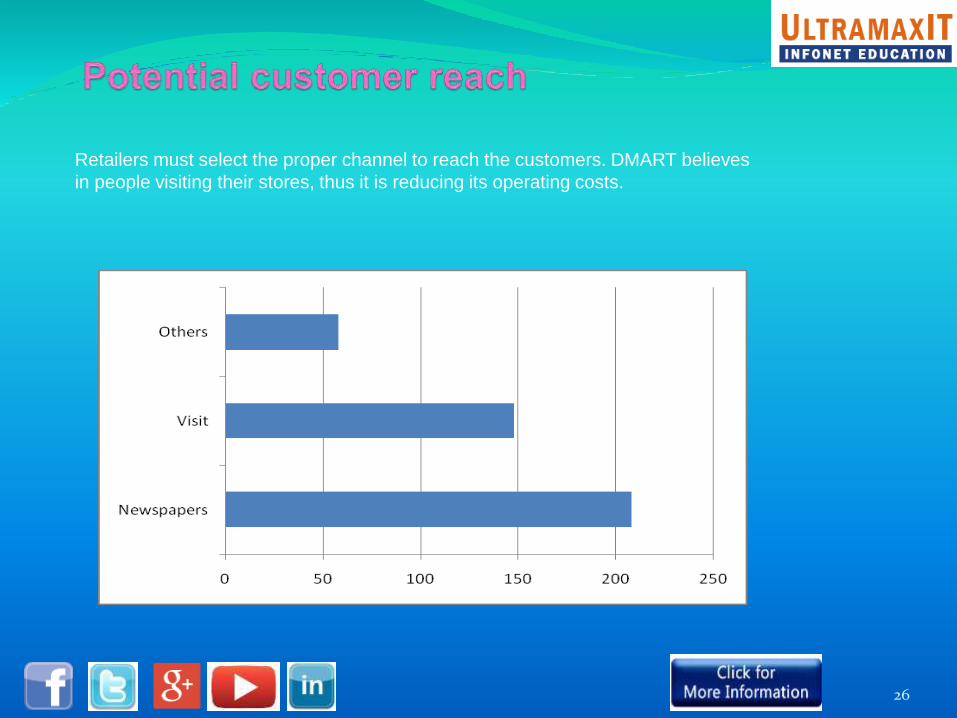

Retailers must select the proper channel to reach the customers. DMART believes

in people visiting their stores, thus it is reducing its operating costs.

26

Below future models will help retailers utilize their existing space and resources to attract more customers and better satisfy existing customers.

Based on our research, we conclude that people are interested for:

Mobile Application Home Delivery: 88.04%Mobile Application Order and Pick-up: 92.39%Shop and Drop: 97.82%Online Home Delivery: 55.6%Home Delivery Extra pay: 78.3%

Hence, we can assume that people are more interested towards the online model, moreover they are also willing to pay some extra for the same. Above model can help increasing customers and also retaining customers happily for longer time.

27

Order-Pick-up and Online model is the top preference for married couples. Married have prime

responsibility for grocery so retailer should think to act for such segment.

Lesser working days preferred by many married males if better offers are made available. While

unmarried has no such priority whether a store is functioning for all 7 days or 6 days.

Females influence more instead of males for shopping the grocery items, So retailers should think

whom to focus more.

Online model found to be more preferred among the population. Still, females were in favour of

rejecting the online model for the grocery item as they can’t look and feel the items online, but at the

same time they wish branded products can be home delivered.

Based on our research, people are also even ready to pay extra for the home delivery.

28

ORDER AND PICK UP: A process in which people can call and block their

order, the goods can be collected while returning on their way home. This

process can be implemented through online, mobile application or a small

call centre.

SHOP AND DROP: A process in which people visits the store, shops and in

turn has the option of delivering the goods at their doorstep.

ONLINE MODEL: This model can include both website and the mobile

application. Based on the analysis major population is even interested in

paying extra for home delivery.

29

Green building can help reducing operating cost primarily in air conditioning and light. Retailer can also opt for carbon credit too. Below building consume very little electricity in lighting but it is without air conditioning but feel like centrally air conditioned.id retailers can opt for carbon credit too.

30

We have covered only operating cost and future option but many analytic

area is there in retailing which should also be taken care for better

business:

ASSORTMENT OPTIMIZATION AND SHELF SPACE ALLOCATION - Using analytics

to determine what products to offer in what quantities.

CUSTOMER DRIVEN MARKETING - Use of customer data to segment, target,

and personalize offerings.

INTEGRATED FORECASTING - The use of statistical forecasting to support

multiple functions.

LOCALIZATION AND CLUSTERING - Tailoring multiple aspects of retailing to

local stores or similar clusters

31

MARKETING MIX MODELLING - Determining which marketing investments

work, and which are less effective.

PRICING OPTIMIZATION - Using analytics to determine the optimal pricing

of products and services through their lifecycles.

PRODUCT RECOMMENDATION - Using analytical approaches to recommend

product offerings for particular customers.

WORKFORCE ANALYTICS - Optimization of staffing with regard to cost,

customer shopping patterns, and locations

32

STORE LEVEL EMPOWERMENT - Giving store managers and employees

the ability to analyze their businesses.

ANALYTICAL PERFORMANCE MANAGEMENT - Predicting financial

performance from nonfinancial and intangible performance factors

MULTI CHANNEL ANALYTICS AND DATA INTEGRATION -

Integration of data and analytics across multiple customer channels or

touch points.

33

Clientling analytics

Demand shaping analytics

Sentiment analysis

34

Given the current retail environment, it may take a bit longer for retailers to

transform themselves into precision analytical machines.

However, the overall trends are clear: retail is a data-intensive industry, and

taking advantage of all that data to operate and manage the business better

requires analytics.

The good news—and the bad—for retail analytics is that most retailers have

only scratched the surface of what is possible.

The food on the analytical table for retailers is both bounteous and delicious; all

that remains is for retail executives to revive their appetites, and eat heartily!

35

Ultramaxit

Make Your Learning More Powerful with Ultramax

A Wing 601 & 602 Vertex Vikas

Building,

S. Radha Krishna Road,

Andheri East Mumbai – 400069

Phone: +91-22-

61398700/01/02/03/04/99

2Floor,Shan Hira Building , Above

Titan Showroom,

M.G. Road ,Camp,Pune – 411001

Phone: +91-20-41463502/05/06/07

36

Recommended