Resource Seeking, the Role of Government and Value Creation of Chinese Cross-border Mergers and Acquisitions

By

Agyenim Boateng¹, Wei Huang, Min Du Chengqi Wang & Xiuping Hua

¹Agyenim Boateng,

University of Huddersfield Queensgate, Huddersfield,

UK, HD1 3DH E-mail: [email protected]

2

Resource Seeking, the Role of Government and Value Creation of Chinese Cross-Border

Mergers and Acquisitions

Abstract

Two decades of market-oriented reforms and open-door policies have spurred the unprecedented

growth of Chinese multinational corporations abroad. This paper considers the role of

government and institutional influences on value creation through cross-border mergers and

acquisitions by Chinese firms during the period from 1998 to 2008. The findings indicate that

Chinese bidders experience wealth gains ranging from 0.73% - 0.89% over a 3-day event

window. Our cross-sectional analysis indicates that the reforms in the foreign currency approval

system, the deal size and the regional location of the target firms exert significant impact on

shareholder wealth. Another intriguing finding is that Chinese acquirers that conform to the

government resource-seeking policy achieve positive gains; this finding provides support for the

conformity-performance debate under institutional theory.

Keywords: Institutions, Government, Cross-border M&A, Value Creation, China

3

Resource Seeking, the Role of Government and Value Creation of Chinese Cross-Border Mergers and Acquisitions

Introduction

After two decades of market and economic reforms, Chinese companies have began to extend

their global reach and consolidate within their industries. As a result, the number of Chinese

firms engaged in cross-border merger and acquisition (CBM&A) activities in recent years is on

the rise. The value of outward mergers and acquisitions, which stood at only 17 million US

dollars in 1988, reached a value of $42 billion in 2008 (see UNCTAD, 2009). The rise in

outward mergers and acquisitions (M&A) activities in China has been attributed to a number of

factors, including resource seeking behaviour of Chinese firms (UNCTAD, 2006; Boateng,

Wang and Yang, 2008), the role of Chinese government and its reform policies, a high volume of

cross-border trade leading to foreign reserves of over 2 trillion U.S. dollars and China’s

continuous growth in GDP at a rate of 10% over the past two decades. In particular, the “go

abroad” strategy initiated by the Chinese government, which actively provides financial and

other support mechanisms to Chinese firms, has been a powerful force behind the surge in

CBM&A activities. Recent studies by Luo, Xue and Han (2010); Peng, Wang and Jiang (2008)

have documented that Chinese government are behind the rise in outward mergers and

acquisitions, but none of these studies gives attention to the effects of the government

involvement on CBM&A outcome. This is a significant omission, given the extent of the

Chinese government’s role in the economy. Hitt et al. (2004) indicate that the Chinese

government’s authority over businesses is pervasive and pronounced. The M&A decisions of

Chinese firms are driven by institutional constraints and incentives. As part of the economic

reforms, the Chinese government has maintained its ability to reward or discipline firms

4

depending on their adherence to government directives (Luo, 2000). Deng (2008) echoes similar

views and points out that, due to the prevalence of various institutional constraints in China,

government endorsements are essential for CBM&As to occur. For example, Chinese

government through its “go abroad” policy has created priority sectors in line with national

policy goals of seeking resources which China lacks and all investments complying with these

guidelines in the “go abroad” strategy enjoy favourable financial support, tax holidays, and other

favourable treatment. Basic finance theory suggests that managers are organisationally rational

and implement strategies (which include political and institutional pressures) that they think will

lead to higher performance (Simon, 1976). Some firms therefore see investment in the Chinese

government designated priority sectors as a means of circumventing problems such as the

lending bias of China’s state-dominated banking system at low rate against their firms (Huang,

2003), heavy government regulations and other transaction costs (Guriev, 2004). The above is in

addition to the fact that, government endorsement in China is important and firms are under

pressure to conform to government policy agenda and raise the national flag. It would therefore

be somewhat of a surprise if corporate managers in China did not respond to these pressures. The

government ‘‘helping hand’’ theory of government-business relationship (Che and Qian, 1998)

in shaping international expansion behaviour and the pressures on firms to conform to state-

directed policies have implications for the cost of doing business, impact firms’ confidence and

firm value (Kofele-Kale, 1992, Boddewyn and Brewer, 1994).

Despite this, no study has explicitly examined the link between the role of governments and

value creation by Chinese firms. The few studies in this area examining whether conformity to

government-directed policies has positive effects on firms’ substantive performance and firm

5

value include Donaldson (1995); Deephouse (1999); Westphal, Gulati and Shortell (1997) but

have produced mix results. Empirical research suggests that conformity leads to higher

performance because of legitimacy. Positive correlation between conformity and firm value were

reported by Abrahamson and Hegeman (1994) and Miller and Chen (1995). They observed that

conformity reduces risks, enhances opportunities for competitive advantage and hence the firm

value. However, Meyer and Scott (1983); Deephouse (1999); Luo (2001) suggest that conformity

to government-directed policies allows organisations to reap more positive social evaluations,

(i.e. social acceptability). This is because state, as ultimate authority, plays a role by endorsing a

firm’s strategy that falls within its national economic and strategic framework to bolster the

economy and enhance national competitiveness. However, Kennedy and Fiss (2008); and

Donaldson (1995) argued that the choice between conformity and performance-enhancing

templates for organising is a false dichotomy, and managers are unlikely to select templates

merely on account of their social acceptability.

In this paper, we contribute to this sparse literature by examining the effect of cross-border

acquisitions on the market valuation of the acquiring firm and explore the role played by Chinese

government in creating value for Chinese bidders. We argue that the economic rationale behind

acquisitions is based on the belief that gains can accrue via reduction in transaction costs and

acquisition of strategic assets. By conforming to government-directed policies, firms demonstrate

their legitimacy. The basic argument here is that a firm which conforms and avoids legitimacy

challenges tend to obtain higher quality of resources at more favourable terms ((DiMaggio and

Powell, 1983). Both reforms and conformity to government-directed policies reduce costs and

legitimacy improves firm’s value (Deephouse, 1999). Consequently, if stock markets are

efficient in pricing assets then shareholders wealth would be enhanced if Chinese firms’

6

investments conform to the government directed priority sectors as such investments would be

perceived as good news. Using the data from the Chinese Stock Market and Accounting

Research Database (CSMAR), this study employs standard event study methodology to capture

the impact of acquisition announcement on firm value around the announcement date and

analyses the impact of government and institutional influences on Chinese CBM&As from 1998

to 2008 under the assumption that Chinese stock markets are semi-strong efficient1.

In terms of contribution, this paper overcomes an overwhelming bias in previous M&A studies,

which have concentrated on advanced market economies and have used traditional economic

factors to explain CBM&A wealth creation. We provide new insights into the implications of the

role of government policies on M&As and highlight the role of government in China’s emerging

economy as a source of value creation. In comparison with previous studies, this research

represents the first relatively large-sample study on CBM&As and value creation carried out in

the Chinese context.

The main findings of this study indicate that Chinese acquirers in the international market for

corporate control experience significant wealth gains around the announcement date of

acquisition. Cross-sectional regression results show that conformity to the government-directed

policy to invest in priority sectors and reforms in the foreign currency approval process influence

the wealth gains of Chinese acquirers.

1 Semi-strong efficiency is the ability of stock prices to adjust to the release of new information to market under efficient market hypothesis (EMH). EMH posits that stock prices will react or adjust instantaneously to reflect the release information such as announcement of major investment,

7

The rest of the paper is structured as follows: Section 2 reviews the previous theoretical and

empirical studies. Section 3 presents the sample selection and method used in this study.

Following that is the analysis of the wealth effects and the factors that influence the wealth gains

from the M&As of Chinese acquirers. The final section concludes the paper and discusses the

implications of the study.

Relevant Literature: Government, Institutions, Wealth Effects and M&As

A number of theoretical perspectives have been used to explain how firms enter foreign markets,

including transaction cost theory (Hennart, 1989; Buckley and Casson, 1976), ownership,

location and internalisation (OLI) paradigm (Dunning, 1993) and institutional theory (Brouthers,

2002, Delios and Beamish, 1999). Overall, the predominant theoretical view of FDI is premised

on the asset-exploitation perspective. With this perspective, firms make the most of their rent-

yielding proprietary resources and knowledge-based capabilities by internalising resources

within the firm when expanding into overseas markets (Buckley and Casson, 1976; Hymer,

1976). The above perspectives were developed largely in the context of the advanced market

economies of North America and Western Europe, researchers such as Lall (1983) and Wells

(1983) describe their limited applicability in the context of firms from one developing country

entering into other developing countries. It is argued that firms from developing countries

expand mostly into similar or less developed countries using proprietary advantages such as low

input costs, inexpensive labour, managerial skills and advantages associated with conglomerate

ownership (Gubbi et al., 2010). While prior studies have used the above theoretical perspectives

to examine a firm’s choice of international entry mode in developed and developing market

economies, recent studies suggest that institutional theory appears to be the most applicable

8

theory when explaining enterprise behaviour in emerging markets (Child and Rodrigues, 2005,

Buckley et al., 2007, Hoskinsson et. al., 2000). Institutional theory’s explanatory power is

attributed to the fact that government and societal influences are stronger in emerging economies

than in developed countries (Hoskisson et al., 2000). Moreover, institutions defined as “the rules

of the game” help shape the strategies, structures, and competitiveness of firms (North, 1990).

Researchers argue that a firm’s strategic choices are driven by the institutional framework in

which the firm is embedded (Porter, 1990, Scott, 2002). The role an institution within an

economy is to reduce both transaction and information costs through reducing uncertainty, thus

establishing a stable structure that facilitates interaction and allows enterprises to move beyond

institutional barriers (see Oliver, 1991). Despite the above reasons, Luo, Xue and Han (2010;

p.68) suggest that “the specific policies enacted by home country governments has yet to be

systematically examined in the literature, hence the role of home governments in promoting

outward foreign direct investment (OFDI) and nurturing the growth of emerging market

enterprises” is not well understood. In this section, we review the existing literature on the role of

government and home country institutions.

The Role of Government

Political economists have long observed the pivotal role played by governments and home

country institutions in shaping international expansion behaviour and the trajectory of

multinational enterprises (see Boddewyn, 1988; Kofele-Kale, 1992, Moran, 1985; Boddewyn

and Brewer, 1994). Leone (1986: 6) aptly points out that “the acts of government create

individual winners and losers in the marketplace”. It is readily acknowledged that it is the

9

government that creates legislation to regulate the economy and that establishes both the

regulatory and competitive environments in which businesses operate; however, the

government’s relationship with businesses in enhancing their growth and success is

complementary and complex (Boddewyn, 1988; Boddewyn and Brewer, 1994).

Most governments of emerging economies that support local firms decisions to ‘go abroad’ do so

with the assumption that these firms will bring in advanced technology, natural resources and

managerial know-how that home countries lack and that they will help bolster the national

economy and enhance national competitiveness (Luo, 2001). Luo, Xue and Han (2010) echo

these views and suggest that the Chinese “go abroad” policy has political dimensions and is

based on national interest (to acquire scarce resources such as natural resources, technology,

finance, managerial capabilities and other intangible assets) and the need to improve the

efficiency of Chinese firms and the Chinese economy. It is important to point out that the tacit

nature of some types of proprietary and intangible know-how, resources and capabilities makes

them difficult to purchase through market transactions (Coff, 1999, Gupta and Govindarajan,

2000). However, Capron, Dussauge, and Mitchell (1998) have noted that the market for firms

may be more efficient than the market for some resources, thus making acquisitions the popular

choice for gaining and reconfiguring new resources and capabilities. In short, CBM&As give

firms in emerging economies access to key strategic resources that may not be available at home,

thereby enhancing their capacity to be competitive. Therefore, it is not surprising that China has

taken a number of steps to encourage local firms to expand internationally, including i) creating

policy banks for credit support at lower lending rates and other incentives for firms venturing

abroad; ii) streamlining administrative procedures and decentralising them to local levels of

government; iii) easing capital control; iv) providing information and guidance on investment

10

opportunities abroad; and v) reducing political and investment risks through bilateral and

multilateral agreements with countries and international institutions.

Government, Institutions and Value of Firms

Stretching the above point further, Boddewyn (1975pp. 194) argues that “government relations

are … largely unavoidable, and they are particularly important for multinational firms whose

legitimacy and loyalty are frequently questioned by government at home and abroad”. The

underlying concern is that company managers will ignore, to their immense detriment, the

importance of governments in their business strategy. This line of thinking is consistent with the

views of Wooten and Hoffman (2008), Scott (2001) and Zucker (1987) who strenuously argue

that organisations should adapt their decisions to external forces such as governments to gain

legitimacy and ensure their survival. Explaining this point clearly, DiMaggio and Powell (1983;

1991) Oliver (1997), Tsui et al., (2004), and Peng (2003); and Scott (1987) point out that,

organisations may make decisions voluntarily in response to pressures to conform to the strategic

direction and policies of the government or involuntarily in response to coercion by powerful

institutional forces that control critical resources or have legislative powers, i.e., coercive

isomorphism. Yet prior studies have been confined to traditional economic factors and wealth

creation (See Morck and Yeung, 1992; Kang, 1993; Markides and Ittner, 1994) and ignored the

role of institutions. Among the few studies investigating the wealth gains of CBM&As in the

context of emerging economies is a study by Boateng et al. (2008) that found significant positive

wealth gains for Chinese acquirers without analysing the factors on which the wealth was created.

Gubbi et al. (2010), examined 425 acquisitions by Indian firms and reported positive and

11

significant cumulative abnormal returns of 2.58% around the announcement date. On the other

hand, Aybar and Ficci (2009) studied 433 CBM&As announcements associated with 58 bidding

emerging markets multinationals and reported negative and significant cumulative abnormal

returns of 0.09% and 0.12% over two- and three-day event windows. In summary, the literature

offers conflicting evidence about the wealth effects of CBM&As by acquirers from emerging

markets, and none of these studies attempt to shed light on the link between the institutions and

the value of the emerging market firms. This study aims to fill the void in the literature by

providing evidence on wealth gains to Chinese bidders and the factors influencing such gains

from CBM&A activities. More specifically, this study focuses on the role of the Chinese

government’s reforms policy in respect of currency approval process and conformity to state-

directed policies to explain the wealth gains that can accrue to Chinese bidders.

Hypotheses Development

North (1990) suggests that any attempt to examine a firm’s strategic choice requires an

understanding of the institutional framework in which the firm is embedded. Scott (2001), and

Buckley et al., (2007), concur and argue that the institutional and regulatory framework of an

emerging economy can shape the domestic firms’ strategy and determine their ability to invest

abroad. Since the 1980s, the Chinese government has created and used several institutions such

as the Ministry of Commerce (MOC), the People’s Bank of China (PBC), the State

Administration of Foreign Exchange (SAFE), the State Owned Asset Supervision and

Administration Commission (SASAC) and the State Development and Reform Commission to

guide and manage overseas FDI. These institutions have been at the forefront of reforming,

12

providing support and developing the regulatory environment in which Chinese businesses

operate. As a result, we have seen a phenomenal rise of Chinese OFDI to a total of over 118

billion dollars, with M&As accounting for over 90 percent of this amount in the first half of 2008

alone. Below, we develop a set of hypotheses involving the two main factors of interest that this

study attempts to explore:

Conformity to Government Policy Direction and Value Creation (CGOPD)

The Chinese government, through its “go abroad” policy, has classified some sectors as

strategic2; these sectors receive more active support, and firms that conform to the direction of

government policies can more readily access inputs, such as cheaper sources of funds, and other

incentives. Zhang, Zhou and Ebbers (2010) point out that because of the China’s booming

economy, securing natural resources abroad has become the state imperative. Acquiring

advanced technology, management expertise and energy resources abroad is perceived as an

important means to strengthen firm’s international competitiveness. In line with the “go abroad

strategy”, government supports the firms’ overseas acquisitions through value-added taxes and

favourable financing (UNCTAD, 2005; Xiao & Sun, 2005). For example, the Chinese National

Development and Reform Commission (NDRC) and China EXIM Bank jointly issued ‘‘Notice

concerning the policy on providing credit and loan support for overseas projects encouraged by

the State’’ indicating that a low-rate loan will be provided if the FDI projects fulfil at least one of

the following requirements: exploring the a natural resource that China lacks (including energy; 2 In recent years, an expressed goal of state-directed Chinese overseas direct investment has been to access advanced proprietary technology; natural resources and other immobile strategic assets and other capabilities (Deng, 2003; Cai, 1999; Wu and Sia, 2002). The Chinese government provides support in the form of information on obstacles and problems encountered by OFDI firms, lower lending rate credit funds for companies engaged in acquisitions for the following: i) energy; natural resources in mining, gas and oil, promotion of textiles exports. The priority sector in this study include: minerals, petroleum, textiles; research and development (R &D).

13

natural resources in mining, gas and oil); promoting textiles export; and R&D activity using

advanced international technology. Deng (2008) documents that Chinese firms increasingly use

cross-border acquisitions to acquire natural resources and advanced technology because they are

under pressure to conform to the state investment policy direction and bring in the resources that

China lacks. Although a number of researchers such as Donaldson (1995); Deephouse (1999);

Meyers and Rowan (1977); DiMaggio and Powell (1983) have investigated the link between

conformity and firm value, but the results appear inconclusive. Given the unique environment in

China and the fact that government endorsement does not only confers legitimacy but viewed as

firms devoted to national course and therefore are supported with favourable financial incentives,

conformity to national policy agenda may lead to value creation. We argue that conformity leads

to legitimacy and acquisition of financial resources at more favourable terms in China. Moreover,

analysts in financial markets recognise that technological resources acquired by the Chinese

firms from abroad can be taken back to home country, internalised and generate spillovers in

China (see Ranamurti, 2012). Therefore, conformity may provide a positive signal to the stock

markets about the prospects for firm whose strategic goal is to maximise shareholder wealth - the

only direct measure of shareholder value (Lubatkin and Shrieves, 1986; (McGee, Thomas and

Wilson, 2005). Accordingly, the following hypothesis addresses the impact of the role of the

Chinese government on the acquiring firms’ value.

H1: Chinese acquiring firms that conform to the government investment policy direction by

investing in the designated priority sectors will lead to a positive impact on shareholder value.

14

Government Reforms Policy (GOVREF)

Buckley et al. (2007, p.503) argue that “the institutional environment is likely to have a far-

reaching and profound effect on the internationalisation decisions of Chinese firms”. We argue

that liberalisation, institutional reform and outward investment procedures reduce bureaucracy

and generate positive wealth effect when acquisitions are announced due to potential reduction in

the costs of doing business. It is expected that the ensuing efficiencies associated with the

reforms may lead to value for Chinese acquirers on assumption that the stock markets in China

are efficient. We delineate below the key phases of the liberalisation of the foreign currency

approval system for overseas investment – the single reform policy that has undergone a

complete decentralisation from the State Council to the Provincial level.

1998-2006: Centralised Approval System for foreign currency

A standardised approach with greater scrutiny and monitoring procedures put in place

to approve outward investments. State Council involved in the approval process.

Currency approval required from the State Administration of Foreign Exchange

(SAFE). Entry into the World Trade Organisation (WTO). Policies to encourage

outward investment activities in textiles, energy, natural resources and R&D activities.

The “go-abroad” strategy or zou chu qu directive adopted by 17th Congress in 2002. In

2002, limited decentralisation from the central agency to selected local authorities for

projects of US 1 million or less, with overall investment capital of US$ 200 million.

Further decentralisation in 2005, with a local limit of US 10 million and the quota later

expanded to US 5 billion (Cai, 1999; Wu and Sia, 2002)

15

2006- present: Fully Decentralised Currency Approval System

Both SOEs and private enterprises are actively encouraged to invest overseas,

particularly in sectors considered strategic to China, with active state support.

Guidelines, establishment of specialised funds to help firms go abroad. In June 2006,

the overall investment quota for foreign currency is abolished. The quota for

purchasing foreign exchange for overseas investments was revoked and the necessary

foreign exchange for domestic investors to invest abroad was extended to self-owned

foreign exchange, the foreign exchange purchased by RMB, or the domestic and

overseas foreign exchange loans. We argue that easing the control of foreign exchange

required to undertake acquisitions abroad reduces cost and increase firm flexibility and

value. We therefore test the following hypothesis:

H2: Chinese acquirers engaged in CBM&A will create more wealth after the foreign exchange

approval reforms compared to the pre-reforms period.

Data and Methodology

Sample Selection and Characteristics

Panel A of Table 1 provides data on the sample selection of Chinese bidders. The sample

analysed in this study consists of mainland Chinese listed companies engaged in CBM&As

during the period 1998 - 2008. The announcement and completion dates as well as the parties

involved were identified from the GTA database from Hong Kong. The initial requirements for

inclusion in the study were as follows: i) the acquirer had to be publicly listed in the Shanghai

and Shenzhen Stock Exchanges under A Share, which provides data on cross-border M&As in

16

China; ii) neither the targets nor the acquirers could be a trust or financial firm. The resulting

sample included 445 bidders. The next requirement for inclusion was the availability of share

price data from the Chinese Stock Market and Accounting Database (CSMAR). To properly

separate the effects of each acquisition, the bidder could not be involved in multiple

acquisitions within three months. The acquiring firm must have its shares traded in Shanghai

and Shenzhen. In addition, we required that there must be at least 280 days of continuous data

around the announcement date. The event window was defined as a period of 260 days prior to

and 20 days following the announcement. Finally, there could not be a contaminating

announcement within ten business days before or after the announcement. It is important to

point out that the data from CSMAR database was compared with Thomson SDC Platinum

M&A database and Datastream. CSMAR database appears to provide relatively more up-to-

date information in terms of number of acquisitions and stock returns with fewer missing values.

The final, usable sample consisted of 148 cross-border acquisitions by Chinese bidders. It is

pertinent to point out that, lack of stock price data was the most important reason for the

exclusion from the final sample. In most of these cases, the listing occurred after the event. The

final sample compared favourably with a recent and similar study in Chinese context with a

sample of 68 drawn from SDC Platinum M&As Database for 1991-2008 period by Bhagat,

Malhotra and Zhu (2011). Panels B, C, D, E and F of Table 2 highlight locations of the targets,

priority/non-priority dichotomy by industry type, number of deals from 1998 through

September 2008 and sectoral distribution. It is apparent from Table 1 that most of the

acquisitions occurred in Asia (54.1%), with the rest taking place in advanced Western countries

(the U.S. and Western Europe). In terms of priority and non-priority industry classification,

over 40 percent of the acquisitions were in sectors designated by the government as priority

17

sectors, while the rest were in non-priority sectors. In terms of frequency by year, the highest

number of deals occurred in 2004 and 2005, followed by 2006 and 2008; the lowest number

were in 1998. The sectoral distribution is categorised into seven sectors, with manufacturing

having the highest number of acquisitions (30.4%), followed by general trade (20.3%), then R

& D (16.2%). The remaining sectors are transport and communication (10.8%), natural

resources & energy (10.1%), building & construction (6.8%) and textiles & apparel (5.4%).

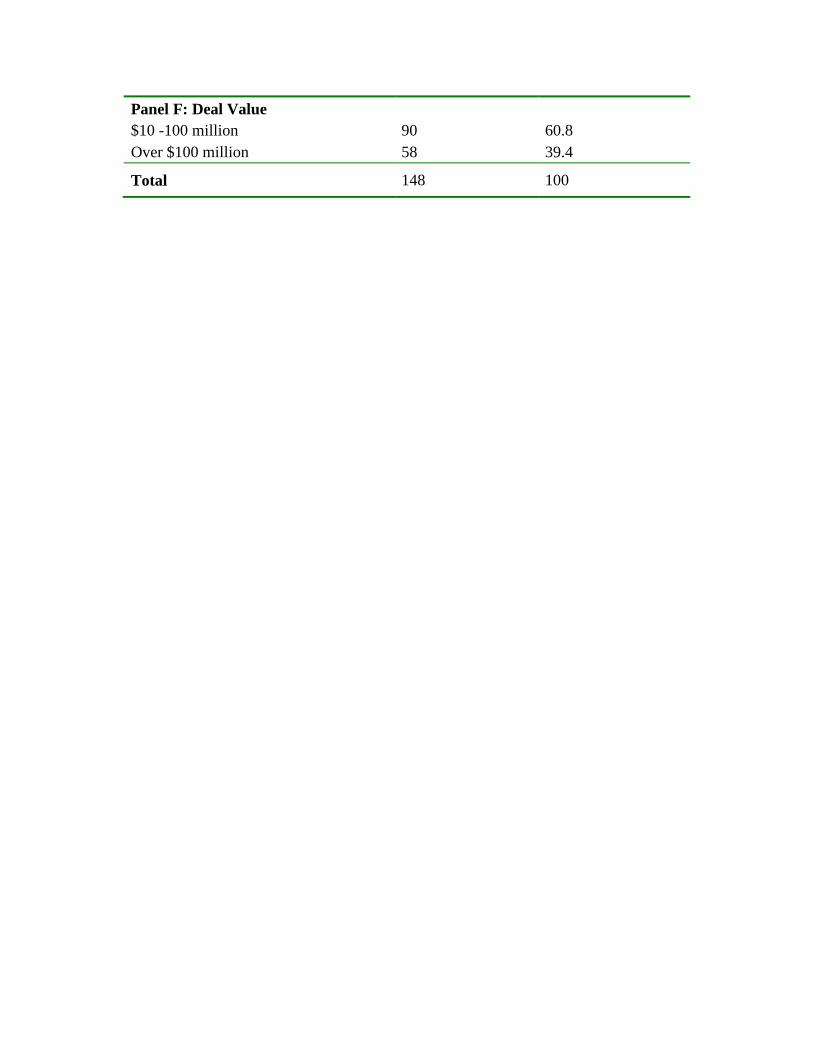

Regarding the investment values of the acquisition, firms with investment value from 10-100

million dollar account for 60.8 percent while 39.4 percent have over 100 million dollars.

(Insert Table 1 here)

Methodology

To measure shareholder wealth changes, standard event study methodology (Brown and Warner,

1985) is employed to measure the wealth effects of M&A announcements on participating firms.

The event study approach allows researchers to conclude whether an event had a positive or a

negative effect on shareholder wealth. To derive the cumulative abnormal returns (CARs),

expected returns are based on a 260-day return prior to the announcement of the foreign

acquisition. We considered the following event widows: (-1, 0), (-1,+1), (-5,+5). The following

standard market model equation was used to calculate the normal return of the sample firms’

common stock:

Rjt = αj + βjRmt + εjt (1)

where,

t = day measured relative to event,

18

Rjt = return on security j on day t,

Rmt = Shanghai and Shenzhen Composite Index (a proxy for the market

portfolio of risky assets),

αj = estimated period intercept of firm j,

βj = OLS estimates of firm j’s market model parameters,

εjt = the error term of security j on the sample event day t.

The abnormal returns (AR) for each sample event j on day t are obtained as follows:

ARjt = Rjt – (αj + βj Rmt) (2)

where,

t = day measured relative to event,

ARjt = excess return to security j for day t,

Rjt = return on security j during day t,

Rmt = Shanghai and Shenzhen Composite Index (a proxy for the market

portfolio of risky assets),

αj = estimated period intercept of firm j,

βj = OLS estimates of firm j’s market model parameters.

Daily abnormal excess returns are calculated for each sample event in the study over the event

window. For a sample of N sample events, the daily average abnormal return for each day t is

estimated as:

ARt = 1

/N

jAR jt N

=∑ . (3)

19

The cumulative abnormal return (CAR) for each security j, CARj, is calculated by summing

average abnormal returns over the event period as follows:

∑=

=L

KtjtLKJ ARCAR ,, (4)

where the LKJCAR ,, is for the period from t = day K until t = day L.

The cumulative average abnormal returns (CAARs) over the event time period from day K to

day L are calculated as:

∑=

=N

JLKJLK CAR

NCAAR

1,,,

1 (5)

To correct for serial correlation of daily event period abnormal returns for the same firm, Coutts,

Mills and Roberts (1995) recommend using standardising cumulative abnormal returns for

longer event windows. Accordingly, each firm’s cumulative abnormal return is standardised by

dividing the CARs by respective standard errors. To calculate the statistical significance of the

tests, standardised abnormal returns and standardised cumulative abnormal returns are used to

calculate a Z statistic.

Using the Z-statistic, p-values were calculated for standardised abnormal returns and cumulative

abnormal returns over the event window. Under the null hypothesis of no stock price effect, this

statistic will have, approximately, a standard normal distribution. We report the standardised

CARs for the following event windows: (-5,+5; -1,+1; 0,+1). The CARs are utilised as dependent

variables in the cross-sectional analysis, and the tests of differences are all standardised.

20

Cross-Sectional Analysis of Cumulative Abnormal Returns (CARs)

Control Variables

Based on extant studies, a number of control variables are taken into account, including: home

country gross domestic product (LGDP) (Kiymaz, 2004); deal size (Uddin and Boateng, 2009);

exchange Rate (EXRATE) (Kish and Vasconcellos, 1993); Kiymaz, 2004). Regional location of

the Target (REGION); Kiymaz (2004); Control (CONTR) (Kiymaz, 2004). We take into account

the profitable of the acquiring firms in that highly profitable firms may drive performance. We

measure profitability using the ratio of operating profit to sales (PROFIT). The sample includes

firms from seven industry classifications. We control the sectors in line with previous studies, for

example, Doukas and Travlos (1988), who reported wealth gains across different sectors. Earlier

studies suggest that having full control of the target would give the acquiring firm the flexibility

of imposing the management style and expertise of the bidder thereby leading to more value

creation for the bidder. Chari, Ouimet and Tesar (2004) find evidence that acquiring firm’s value

is associated with controlling stake.

Variables Measurement

Cumulative Abnormal Returns (CARs)

We employ stock market reaction to the announcement, as reflected in the firm’s share price

movement around the announcement of the M&A event. We chose shareholder wealth creation

for the following reasons: i) it is widely accepted in finance literature that the goal of a firm is to

maximise the wealth of its shareholders, which is measured by stock prices, and prior studies in

finance and strategic management have extensively used market reaction in M&A studies (see

Delong, 2001; Sudarsanam and Mahate, 2003; McGee, Thomas and Wilson, 2005); ii) Haleblian,

21

Kim and Rajagopalan (2006) and Kale, Dyer and Singh (2002), point out that share price

movement has a better predictive validity than other objective measures such as profitability, in

that it is an ex-ante performance measure that has been found to correlate with ex-post

performance; and iii) share price movement is relatively unbiased compared to other measures

and invariant to differences in accounting policies across nations (Cording, Christmann and King,

2008). Following Kiymaz (2004), we measure the M&A short-term performance of Chinese

acquirers using the cumulative abnormal returns (CARs) for the event window 0, 1 period.

Independent and Control Variables

The manner in which the independent variables are measured is shown in Table 2.

(Insert Table 2 here)

Empirical Results

Short-run wealth effects

Wealth gains to Chinese bidder firms during the 21 day period surrounding the merger

announcement are shown in Table 3. The average abnormal returns (ARRs) for Chinese bidders

are 0.73% and 0.89% on days 0 and +1 and are statistically significant. The significant daily

return that occurs on day -1 (0.36%) may be due to information leak prior to the announcement.

However, the positive AAR on day +10 appears to be due to factors other than the announcement.

Panel B of Table 4 reports four different cumulative abnormal returns (CARs) for the Chinese

acquiring firms. For the (-1, 0) and (-1, +1) windows, our results indicate that, on average,

announcements of international acquisitions by Chinese bidders are associated with positive

22

abnormal returns. Positive market returns for the two- and three-day event windows range from

0.01% to 0.02% respectively. However, the CAR for window (-5, +5) is not statistically

significant3. Overall, the dominance of positive reactions suggest that investors perceive Chinese

CBM&As as value-creating strategic initiatives. These results are consistent with the findings of

Morck and Yeung (1992), and a similar study by Boateng, Wang and Wang (2008), who find

that CBM&As by Chinese firms increase the wealth of the acquirers. However, the results are at

variance with the conclusions drawn by Click and Harrison (2000); Hitt et al. (2001) and Aybar

and Ficici (2009). Our results confirm that Chinese stock markets are efficient and that all

publicly announced information is reflected in stock prices. In the next section, we discuss the

factors that may account for the positive reactions of investors.

Insert Table 3 here

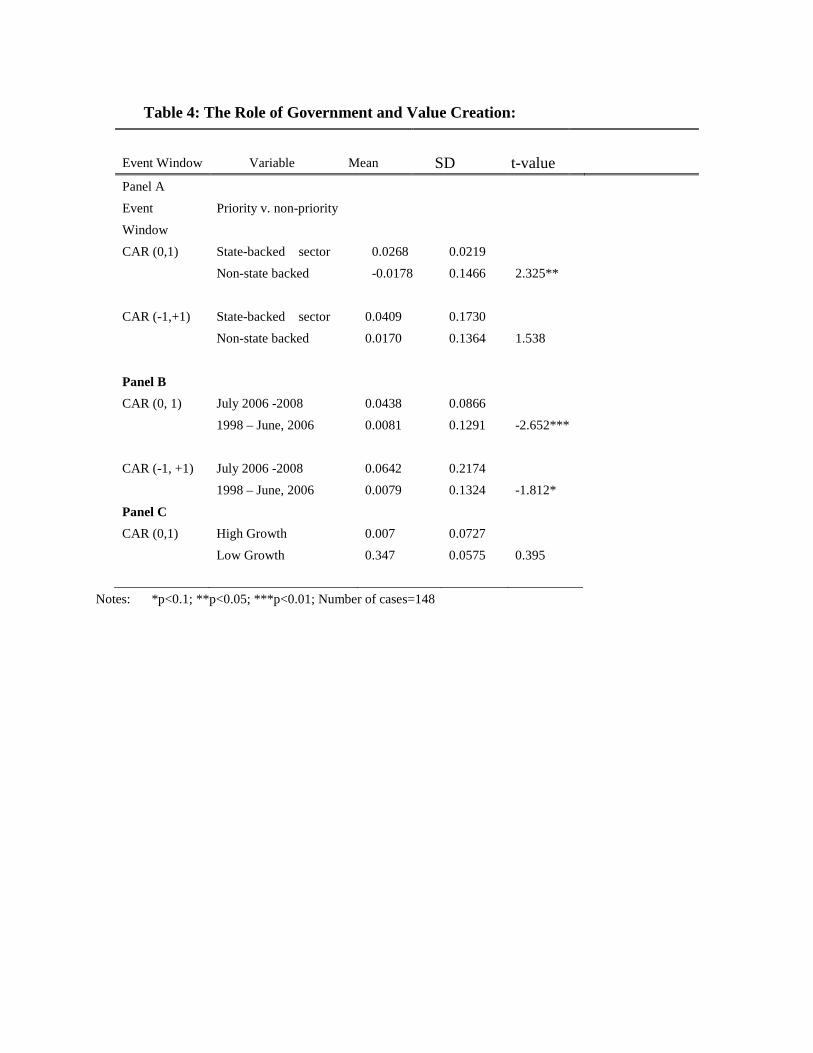

Panels A and B of Table 4 report the t-test results of CARs for Chinese bidders in two different

windows in respect to state-backed priority/non-state-backed dichotomy type by industry and the

role of government-based foreign currency reforms. Chinese bidders making acquisitions both in

the state-backed sectors and after currency approval reforms enjoyed positive abnormal returns

for the two event windows. The results suggest that a state-backed sector has higher mean scores

compared to non-state backed sectors, with one of the event windows (0,+1) being significant at

1%. This finding suggests that the state-backed sectors tend to create more value compared to

non-state-backed sectors. Regarding the foreign currency reforms for undertaking outward

investments, the results indicate that the mean scores for the post-reforms period are statistically

3 No consensus has emerged among researchers with regard to the proper length of event window for calculating CARs (see Mc Williams, Siegel and Teoch, 1999 for review)

23

significantly higher than the period prior to the reforms for the two event windows, suggesting

that reforms lead to positive investor reactions. Panel C shows a test of differences between high

growth firms and low growth firms based on the profitability of the acquiring firms. T-test results

indicate that the differences between the high growth firms and low growth firms are statistically

insignificant.

(Insert Table 4 here)

Table 5 shows summary statistics for the dependent and independent variables. The table reports

the mean, standard deviation and minimum and maximum values for the variables used in the

regression analysis. The mean value for Asia appears to be higher than for the U.S. and Europe.

(Insert Table 5 here)

Cross-sectional Regression Results

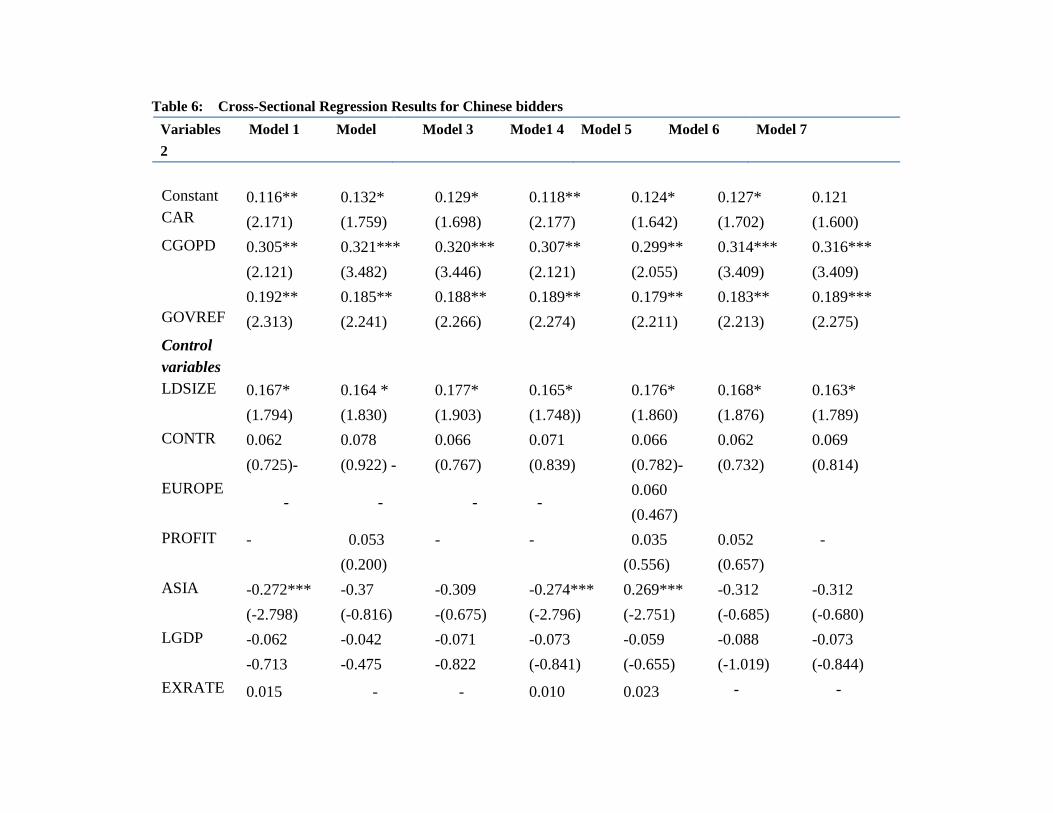

The regression results for Chinese bidders are reported in Table 6. This table shows that the F-

values for all the seven regression models are statistically highly significant. The adjusted 2R

range from 16.9% to 18.6%, suggesting that, the regression procedure explains the variation in

the change in wealth gains of Chinese bidders. The total amount of variation explained by the

models appear reasonable and compare favourably to other CBM&A studies, such as Kiymaz

(2004), who obtained an overall Adjusted R square of 4% and 12% for his studies of a target

firm’s performance for CBM&As. The impact of the role of the Chinese government on the

wealth gains of Chinese bidders is evident in Table 6. The coefficient of the two variables,

CGOPD and GOVREF in models 1 to 7 are significantly positive, indicating that the Chinese

24

government plays a significant role in the wealth creation of Chinese acquirers. The results

provide support for hypotheses 1 and 2. Models 1 - 6 incorporate the main variables conformity,

foreign exchange reform and control variables including the acquirer characteristics,

macroeconomic variables with sectors entered in successive. The positive coefficient of the state-

backed sectors variable indicates a positive and significant relationship between the state-backed

sectors and wealth gains. This finding is interesting suggesting that, Chinese government through

its investment policy framework relentlessly pursue certain long-term objectives to help Chinese

firms acquire the resources they lack and thereby create wealth for these acquirers. The result is

consistent with the point made by Rui and Yip (2008) who argue that, Chinese firms strategically

use CBM&As to achieve specific goals, such as acquiring strategic resources and capabilities to

offset their competitive weaknesses through the use of government support and other incentives

and minimisation of institutional constraints. It is important to point out that, Chinese firms

engage in CBM&As in the government designated priority sectors enjoy privileged access to

low-cost capital and other incentives provided by the Chinese government. Conforming to the

state-directed policy to acquire strategic assets therefore helps these firms to gain legitimacy,

social support and prestige in the market place, which, in turn, leads to maximisation of

shareholder wealth creation as reflected in share prices. The results of this study indicate that

conforming to the government-directed policy tend to help emerging Chinese firms to offset

ownership and location disadvantages consistent to the conclusion made by Aggarwal and

Agmon (1990) in their study on the role government of developing countries. The results

therefore render some support for the conformity-performance debate under the institutional

theory. The results also indicate that specific policies enacted by emerging country governments

create value for acquiring firms and this appears to support the conclusion drawn by Boddewyn

25

and Brewer (1994) and Leone (1986) that the acts of government can create winners in the

marketplace by improving firm’s competitive advantage.

Another important finding is related to the impact of the liberalisation of the foreign currency

approval system on the wealth effects of Chinese acquirers. The results suggest that

decentralising the currency approval system on outward investment is beneficial to Chinese firms

engaged in international acquisitions. The results support the notion that liberalising the foreign

currency approval procedures reduces bureaucracy and the costs of doing business, thereby

generating positive wealth effects when acquisitions are announced.

Robust Check

To check the robustness of this finding, we carried out the Chow test for differences that may be

due to the structural changes which may cause differences in the intercept or the slope coefficient

or both. We divided 1998-2008 into two as follow: 1998- June 2006 and July 2006-2008 where

complete foreign exchange reforms occurred. We compute the F-value as follows:

)2/(][

/)]([

2121

21

knnRSSRSS

kRSSRSSRSSF

nn

nnN

−++

+−= (6)

where

=NRSS Restricted residual sum of squares with knndf −+= 21 ,

K= number of parameters estimated,

=+ 21 nn RSSRSS Unrestricted residual sum of squares.

26

Under the null hypothesis 0H that the parameters are stable, we accept the null hypothesis and

conclude that there is no significant change in the parameters between the two periods4.

The results for the control variables suggest that the variables LDSIZE and ASIA impact the

wealth gains accruing to Chinese bidders. However, the EXRATE dummy, LGDP, PROFIT,

EUROPE and the sector-level dummies appear not to have significant effects on the wealth gains

of Chinese acquirers. The lack of effect of the EXRATE rate may be due to virtually fixed nature

of Chinese currency (Renminbi), which is allowed to float within limited margins. The

coefficient for the GDP has a negative sign and the results are not statistically significant. The

LDSIZE has a positive coefficient, indicating that deal size impacts the wealth gain accruing to

Chinese bidders, which is surprising. The expectation that large deals will have the potential to

reduce free cash flows that can be spent in the future, or lead to merger integration problems

thereby conveying a negative signal to the stock market that limited funds are available for future

investment opportunities. However, this appears not to be the case, and the findings support the

conclusions drawn by Asquith et al., (1983), Jarrell and Poulsen, (1989), and Houston and

Ryngaert (1994) whose studies find that average wealth gains to the bidders are associated with

large target size.

Following the work of Kiymaz (2004), we use regional location as control variables. To avoid a

dummy trap 5, the U.S. variable is chosen as a benchmark and other regional dummies are

defined relative to the U.S. The findings in respect to other regional groups are interpreted

4 Our calculated value is 3.34 and at 0.05 critical value of ( =)125,1F 3.92; the test statistics for calculated F<3.92 5 We include two dummy variables for three regions to avoid a “dummy variable trap” and perfect multicollinearity, as recommended by Gujarati (2003), before running the regression.

27

relative to the U.S. The coefficient for the EUROPE variable is positive but statistically

insignificant suggesting that Chinese bidders do experience wealth gains with European

acquisitions, but the gains are statistically insignificant relative to U.S. acquisitions. With regard

to Asia, our results suggest that acquisitions in Asia tend to be value-decreasing compared to

their counterparts in the U.S. and Europe. The coefficient for Asia is negative and statistically

significant. This finding may be explained by the fact that Asia contains diverse countries with

idiosyncratic institutions and legal environments compared to the U.S. For example, the single

market in Europe has created the opportunity for less costly operation across national borders

due to the presence of a common legal environment; this is also true for the U.S. The reduced

operating cost may generate a positive reaction from investors leading to wealth gains for bidders.

Another plausible explanation may be the strategic asset-seeking nature of Chinese acquisitions

in Western Europe and the U.S.; most investments are in motor and communication equipment

manufacturing and technology-related firms that are normally available these countries. Given

that Chinese firms lack these resources, the markets may see acquisition announcements in U.S.

and EUROPE as an opportunity to acquire strategic assets and are therefore more likely to react

positively to such announcements and, consequently, create wealth for the bidders.

We also found home LGDP to be negative and statistically insignificant and with a sign opposite

to that predicted by the model. PROFIT has positive coefficient but the results are not

statistically significant indicating that level of profits of acquiring firms do not create value for

Chinese acquirers. All the sector dummy variables appear to have statistically insignificant

impact on wealth creation for the acquirers. Regarding the impact of level of economic

development of target firm, our results indicate a negative and insignificant effect on wealth

28

gains of Chinese acquirers contrary to our expectation. The CONTR variable has positive but

statistically insignificant impact on wealth gains of acquirers.

Sectoral Analysis

Table 7 reports the effects of various sectors on value creation by the Chinese acquirers. The

results indicate that two sectors, namely, energy and natural resources and transport and

communication have significant impact on wealth creation. The results are in line with the

Chinese government resource seeking policy. It is worth pointing out that, studies such as

Boateng et al., (2008); Rui and Yip (2008); Deng (2007; 2009) have provided an unequivocal

support for resource-seeking behaviour of Chinese firms within the government investment

policy framework. For example, the need to acquire resources in energy, natural resources and

technology in motor and communication equipment industry have led to some high profile

acquisitions in the oil sector, communication equipment and motor car industry such as the

takeover of TCL acquisition of Thomson’s TV (France); Lenovo’s acquisition of IBM’S pc unit

in 2005; Volvo of Netherlands; Rover in the UK; and the acquisition of Canada-based PetroKaz

by China National Petroleum Corporation with massive government support. The significant

impact of reforms in the currency approval system on wealth gains in the energy and resources;

textile and apparel; transport and communication sectors suggest that these priority sectors have

benefited from the reforms in currency approval system. The results confirm the important role

played by Chinese government and indicate that the M&A decisions of Chinese firms are driven

by institutional constraints and incentives put in place by the government rendering support for

institutional theory.

29

The results for the control variables suggest that the variables LDSIZE, level of control,

EXRATE and ASIA appear to negative and significant impact the wealth creation of Chinese

bidders on a number of sectors including energy, manufacturing, general trade, service, and

transport and communication. However, the EXRATE and LGDP appear to have significant

effects on the wealth gains in energy & natural resources and transport and communication

sectors.

(Insert Table 7 here)

Summary and Conclusion

This study has investigated the wealth creation and factors that impact on the wealth effects of

CBM&As by Chinese bidders. Using a sample of 148 acquisitions announcements by Chinese

firms in the U.S., Europe and Asia, this paper makes some significant contributions on two fronts.

First, much of the academic research on M&As over the past three decades have centred on one

crucial question: do M&As create value? This question is of crucial importance to researchers

and practicing managers and the quest to answer it is important, yet existing studies, which have

been based in advanced market economies, have produced mixed and inconclusive results (see

Morck and Yeung, 1991; Markides and Ittner, 1994; Moeller and Schlingemann, 2005; Eun,

Kolodny, & Scheraga, 1996). This study is one of the rare attempts to examine whether

international acquisitions by firms from China, the biggest emerging economy and one that has

seen unprecedented reforms over the past two decades, creates value for the acquiring firms.

Second, we make contribution to the institutional theory by test whether conforming to the

30

Chinese government-directed policies and reforms in the currency approval system lead to

wealth creation for Chinese bidders in the global market for corporate control.

We find evidence of positive abnormal returns for Chinese acquirers and identify the contextual

factors under which CBM&As create value. Our findings indicate that the average abnormal

returns for Chinese bidders range from 0.73%-0.89% over the 3-day event window, suggesting

that acquisition announcements of Chinese firms, on average, are perceived by investors to

create wealth for shareholders. The results appear to support the findings of Morck and Yeung

(1992), and a similar study by Boateng, Wang and Wang (2008), who find that CBM&As by

Chinese firms increase the wealth of the acquirers.

The cross-sectional results obtained indicate that government-backed priority sectors and the

reforms in the foreign currency approval system have positively influenced the wealth gains of

Chinese acquirers. We conclude that Chinese firms backed by the state and seeking strategic

assets tend to increase firm value and therefore provide support for the institutional theory. The

underlying cause of the wealth improvement is that Chinese firms conform to government-

directed policy and acquire strategic assets not available at home to bolster national

competitiveness. In return, the state provides support such as low interest loans and other

incentives to these firms, thereby eliciting a positive reaction from investors regarding the future

prospects of the firms and their values. We therefore conclude that conformity to government

strategic policy direction has a positive effect on shareholder wealth creation and render support

to studies such as Deephouse (1999); Westphal, Gulati and Shortell, 1997); DiMaggio and

Powell (1983). Another important conclusion is that specific reforms, such as easing restrictions

31

on currency for outward investments, improve firm value. We therefore suggest that the

government should take additional steps to further reduce other restrictions on outward

investments.

Regarding control variables, we find that the size of the deal is associated with value creation.

However, our results indicate that Asian targets have a negative and significant impact on

shareholder wealth. This suggests that international expansion to Asia by Chinese bidders is

associated with value destruction, as opposed to the U.S. and Europe acquisitions.

The policy implication of the above results is that home country policies and institutions do not

only shape international expansion strategies of firms but also provide opportunities for

significant value-creating activities, which correlate positively with market expectations. The

findings appear to support the conclusion drawn by Gubbi et al., (2010), who point out that

international acquisitions provide an opportunity to acquire resources and reconfigure

capabilities, which facilitates strategic and organisational transformation of firms from emerging

markets.

Although this study has elucidated the wealth effects of Chinese acquirers and the factors

influencing value creation, these findings should be considered preliminary; first, given that the

study concentrated on only home country variables. Second, despite a number of steps taken to

ensure the robustness of our results, the study used two measures for conformity to government-

directed policy and reforms in foreign currency approval system variables. We suggest that

future studies should examine both home and host country variables and consider additional

measures for conformity and reforms to currency approval systems.

32

References

Abrahamson, E. and R. Hegeman (1994). Strategic conformity: An institutional theory explanation? Paper presented at the annual meeting of the Academy of Management, Dallas, TX. Aggarwal, R. and Agmon, T. (1990). The international success of developing country firms: the role of government – directed comparative advantage, Management International Review, 30 (2), pp.163-180. Ali-Yrkko, J. (2002). Mergers and acquisitions: Reasons and Results, Discussion paper series, No. 792, The Research Institute of the Finnish Economy (ETLA). Asquith, P., Bruner, R.F. and Mullins, D.W. (1983), The gains to bidding firms from mergers, Journal of Financial Economics, Vol. 11, pp. 121-139. Aybar, B. and Ficici, A. (2009). Cross-border acquisitions and firm value: An analysis of emerging market multinationals, Journal of International Business Studies, 40, pp.1217 -1338. Barney, J. (1991). Firm Capabilities and sustained competitive advantage, Journal of Management, 17 (1), pp.99 -120. Boateng, A., Wang, Qian, and Yang, Tianle (2008). Cross-Border M&As by Chinese Firms: An Analysis of Strategic Motives and Performance, Thunderbird International Business Review, Vol. 50, No. 4, July/August, pp. 259-270. Boddewyn, J.J. (1975). Multinational Business-Government Relations: Six Principles for Effectiveness. In Multinational Corporations and Governments, ed. P.Boarman and H. Schollhammer, pp. 193-202, New York: Wiley. Boddewyn, J.J. (1988). Political aspects of MNE Theory, Journal of International Business Studies, Fall, pp. 341-363. Boddewyn, J.J. and Brewer, T.L. (1994). International Business Political Behaviour: New Theoretical Direction, Academy of Management Review, 19, 1, pp. 119-143. Brouthers, K.D. (2002). Institutional, culture and transaction cost influences on entry mode choice and performance, Journal of International Business Studies, 33, pp.203-221. Brouthers, K. D., & Brouthers, L. E. (2000). Acquisition or greenfield start-up? Institutional, cultural and transaction cost influences. Strategic Management Journal, 21(1): 89–97. Brown, S. J., & Warner, J. B. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1): 3–31. Buckley, P. J., & Casson, M. (1976). The future of the multinational enterprise. London: Macmillan.

33

Buckley, P.J., Clegg, L.J., Cross, A.R, Liu, X., Voss, H and Zheng, P. (2007). The Determinants of Chinese Outward Foreign Direct Investment, Journal of International Business Studies, 38, 499-518. Cai, K.G. (1999). Outward FDI, a novel dimension of China’s integration into regional and global economy, China Quarterly, 160 (December) 856-880. Capron, L., Dussauge, P., & Mitchell, W. (1998). Resource redeployment following horizontal acquisitions in Europe and North America, 1988–1992. Strategic Management Journal, 19(7): 631–661. Chan, K.C and Fung, H-G., and Thapa S. (2007). China Financial Research: A. Review and Synthesis, International Review of Economics and Finance, 16, pp. 416-428. Chari, A., Ouimet, P. P., & Tesar, L. L. (2005). Cross border mergers and acquisitions in emerging markets: The stock market valuation of corporate control, Working Paper, University of Michigan. Chen, Y.Y. & Young, M.N. (2010). Cross-border mergers and acquisitions by Chinese listed companies: A principle-principle perspective, Asia Pacific Journal of Management, 27, 523-539. Child, J.,&Rodrigues,S.B. (2005).The internationalization of Chinese firms: A case for theoretical extension? Management and OrganizationReview, 1 (3), 381–410 Click, R. W., & Harrison, P. (2000). Does multinationality matter?Evidence of value destruction in US multinational corporations, FEDS Working Paper 2000-21, Federal Reserve System. Coff, R. W. (1999). How buyers cope with uncertainty when acquiring firms in knowledge-intensive industries: Caveat emptor. Organization Science, 10(2): 144–161. Cording, M., Christmann, P., & King, D. R. (2008). Reducing causal ambiguity in acquisition integration: Intermediate goals as mediators between integration decisions and acquisition performance. Academy of Management Journal, 51(4): 744–767. Coutts, J. A., Mills, T. C., & Roberts, J. (1995). Testing cumulative prediction errors in event study methodology. Journal of Forecasting, 14(2): 107–115. Cybo-Ottone, A., Murgia, M., (2000). Mergers and shareholder wealth in European banking. Journal of Banking and Finance 24, 831–859. Deephouse, D.L. (1999). To be different, or to be the same? It’s is a question (and theory) of strategic balance, Strategic Management Journal, 20: 147-166.

34

Delios, Andrew and Paul W. Beamish. (1999). Ownership strategy of Japanese firms: Transactional, institutional and experience influences. Strategic Management Journal, 20(10): 915-933.

Delong, G. (2001). ‘Stockholder gains from focusing versus diversifying bank mergers’, Journal of Financial Economics, 59, pp. 221–252. Deng, P. (2008). Why do Chinese Firms tend to acquire strategic assets in international expansion? Journal of World Business, 44, 74-84. DiMaggio, P.J. and Powel, W. (1991). Constructing an organisational field as professional project: U.S. art museums, 1920-1940. In W.W. Powell & P.J. DiMaggio (eds.), The new institutionalism in organisational analysis: 267-292. Chicago: University of Chicago Press. DiMaggio P.J. and Powell W. (1983). The iron cage revisited: Institutional Isomorphism and collective rationality in organisational fields, American Sociological Review, 48: 147-160 Donaldson, L. (1995). American anti-management theories of organisation, Cambridge, UK, Cambridge University Press. Doukas, J. and Travlos, N.G. (1988). The Effect of Corporate Multinationalism on Shareholders’ Wealth: Evidence from International Acquisitions, Journal of Finance, Vol. 43(5), pp. 1161-1175. Dunning, J.H. (1993). Multinational enterprise and the global economy, UK: Addison-Wesley Publishers. Eun, C. S., Kolodny, R., & Scheraga, C. (1996). Cross-border acquisitions and shareholder wealth: Tests of the synergy and internalization hypotheses. Journal of Banking and Finance, 20(9), 1559–1582 Fligstein, N. (1991). The structural transformation of American industry: An institutional account of the causes of diversification in the largest firms, 1919- 1979, In W. W. Powell and P. J. DiMaggio (eds.),The New Institutionalism in Organizational Analysis. University of Chicago Press, Chicago, IL, pp. 311-336 Gubbi, S.R., Aulakh, P.S., Ray, S., Sarkar, M.B., Chittoor, R. (2010). Do International Acquisitions by emerging-economy firms create shareholder value? The case of Indian firms, Journal of International Business Studies, 41, 397-418 Gujarati, Damordar, N. (2003). Basic Econometrics, 4th edition, McGraw Hill, New York. Gupta, A. K., & Govindarajan, V. 2000. Knowledge flows within multinational corporations. Strategic Management Journal, 21(4): 473–496.

35

Haleblian, J., Kim, J., & Rajagopalan, N. (2006). The influence of acquisition experience and performance on acquisition behavior: Evidence from the US commercial banking industry. Academy of Management Journal, 49(2): 357–370. Hartford, J. (1999). Corporate Cash Reserves and Acquisitions, Journal of Finance, 54, PP. 1969 -1997. Healy, P.M.and Palepu, K.G. (1993). International Corporate equity acquisitions, who, where and why?. In Froot, K.A (ed.), Foreign Direct Investment, University of Chicago Press, Chicago, pp.231-250. Heeley, Michael, B., King, David, R and Covin, Jeffrey, G. (2006). Effects of Firm R&D Investment and Environment on Acquisition Likelihood, Journal of Management Studies, 43, 7, November, pp. 1513-1535. Hennart, J.F. (1989). Can the “new forms of investment” substitute for the “old forms”? A transaction cost perspective, Journal of International Business Studies, 20, pp. 211-234 Hitt, Michael, A., Ahstrom, D., Dacin, M.T. and Levitas, E. (2004). The Institutional effects on Strategic alliances partner selection in transitional economies: China versus Russia, Organization Science, 15, 2, pp 173-185. Hitt, M. A., Hoskisson, R. E., & Ireland, D. R. (2001). A mid-range theory of the interactive effects of international and product diversification on innovation and performance. Journal of Management, 20(2): 297–326. Hoskisson, Robert, E., Eden, L., Lau, Chung, M., Wright, M. (2000). Strategy in Emerging Economies, Academy of Management Journal, Vol. 43, No. 3 pp.249-267 Houston, J.F., Ryngaert, M.D. (1994). The overall gains from the large bank mergers. Journal of Banking and Finance 18, pp. 1155–1176. Hymer, S.H. (1976). The International Operation of National Firms: A Study of Direct Foreign Investments, Cambridge MA: MIT Press. Ingham, H., Kran, I. and Lovestam, A. (1992), Mergers and profitability: A managerial success story?, Journal of Management Studies, Vol. 29(2), pp. 195-208. Jarrell, G.A., and Poulsen, A.B., (1989). The returns to acquiring firms in tender offers: Evidence from three decades. Financial Management 18, pp. 12–19. Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance and takeovers. American Economic Review, 76(2): 323–329. Jensen, M.C. and Ruback, R.S. (1983). The market for corporate control: The scientific evidence, Journal of Financial Economics, Vol. 11, pp. 5-50.

36

Kale, P., Dyer, J. H., & Singh, H. 2002. Alliance capability, stock market response, and long-term alliance success: The role of the alliance function. Strategic Management Journal, 23(8): 747–767 Kang, J-K. 1993. The international market for corporate control: Mergers and acquisitions of US firms by Japanese firms, Journal of Financial Economics, Vol. 34, pp. 345-371. Kennedy, M.T.and Fiss, P.C. (2009). Institutionalisation, framing, and diffusion: The logic of TQM adoption and Implementation decisions among U.S. hospitals, Academy of Management Journal, In press Kish, R.J. and Vasconcellos, G.M. (1993) An empirical analysis of factors affecting cross-border acquisitions: US-Japan, Management International Review, Vol. 33 (3), pp. 227-245.

Kiymaz, H.(2004). Cross –border acquisitions of US Financial institutions: impact of macroeconomic factors, Journal of Banking & Finance, 28, pp.1413-1439. Kiymaz, H. and Mukherjee, T.K. (2000). The impact of country diversification on wealth effects in cross-border mergers, The Financial Review, Vol. 35(2), pp. 37-58. Kofele-Kale, N. (1992). The political economy of foreign direct investment: A framework for analysing investment laws and regulations in developing countries, Law and Policy in International Business, 23, 3, pp. 619-772. Lall, S. (1983). The new multinationals: The spread of third world enterprises. New York: Wiley Leone, R.A. (1986). Who profits: Winners, losers and government regulation, New York: Basic Books. Lubatkin, M. and R. E. Shrieves (1986). Towards reconciliation of market performance measures to strategic management research, Academy of Management Review, 11, pp. 497–512. Luo, Y. (2000). Partnering with Chinese Firms: Lessons for International Managers, Ashgate, Singapore. Luo, Y. (2001). Toward a cooperative view of MNC-host government relations: Building blocks and performance implications, Journal of International Business Studies, 32 (2), pp.401-420. Luo, Y., Xue, Q., Han, B. (2010). How emerging governments promote outward FDI: Experience from China, Journal of World Business, 45, pp. 68-79. Luo, Y. and Tung, R. (2007). International expansion of emerging market enterprises: A Springboard Perspective, Journal of International Business Studies, 38, 4, pp. 481-498.

37

Markides, C. and Ittner, C.D. (1994). Shareholders benefit from corporate international diversification: Evidence from US international acquisitions, Journal of International Business Studies, Vol. 25(2), pp. 343-366. Mathews, J. A. (2006). Dragon multinationals: New players in 21st century globalization. Asia Pacific Journal of Management, 23(1): 5–27. McGee, J., H. Thomas and D. C. Wilson (2005). Strategy: Analysis & Practice. London: McGraw-Hill. McWilliams, A., & Siegel, D. (1997). Event studies in management research: Theoretical and empirical issues. Academy of Management Journal, 40(3): 626–657. Moran, T. (1985). Multinational corporations: The political economy of foreign direct investment, Lexington, MA, Lexington Books. Morck, R. and Yeung, B. (1992). Internalization: An Event Study Test, Journal of International Economics, Vol. 33, pp. 41-56. Moeller, Sara, B and Schlingemann, Frederik, P. (2005). Global Diversification and bidder gains: A comparison between cross-border and domestic acquisitions, Journal of Banking and Finance, 29, 533-564. Myers, J.W. and Rowan, B. (1977). Institutionalised organisations: Formal structure as myth and ceremony, American Journal of Sociology, 83:340-363. North, D.C. (1990). Institutions, Institutional Change and Economic Performance, Cambridge, Cambridge University Press. Oliver, C. (1991). Strategic responses to institutional processes, Academy of Management Review, 16: 145-179. Oliver, C. (1997). Sustainable competitive advantage: Combining institutional and resource based views, Strategic Management Journal, 18 (9), pp.697-713. Peng, W.M. 2003. Institutional Transition and Strategic choices, Academy of Management Review, 28, pp275-296. Porter, M. (1990). The Competitive advantage of nations, New York, Free Press Ramamurti, R. 2012. What is really different about emerging market multinationals? Global Strategy Journal, 2(1): 41–47 Roberts, P. W. and R. Greenwood (1997). Integrating transaction cost and institutional theories: Toward a constrained-efficiency framework for understanding organizational design adoption? Academy of Management Review, 22, pp. 346-373.

38

Rui, H and Yip, George, S. (2008). Foreign Acquisitions by Chinese firms: A strategic intent perspective, Journal of World Business, 43, pp.213-226. Scott, W.R. (1987). Organizations: Rational, Natural and Open Systems. Englewood Cliffs, NJ: Prentice Hall. Scott, W.R. (2001). Institutions and organisations (2nd ed.). Thousand Oaks, CA: Sage Scott,W.R.(2002).The changing world of Chinese enterprises: An institutional perspective’.In A.S.Tsui C.-M.Lau(Eds.), Management of enterprises in the People’s Republic of China (pp. 59–78).Boston: Kluwer Academic Press Sudarsanam, S. and A. A. Mahate (2003). Glamour acquirers, method of payment and post-acquisition performance: the UK evidence, Journal of Business Finance and Accounting, 30, pp. 299–342. Tsui, A.S., Schoonhoven, C.B., Myers, M.W., Lau, C.M. and Milkovich, G.T. (2004). Organisation and Management in the midst of societal transformation, The People’s Republic of China, Organisation Science, 15, 2, 133-144. Uddin, M. and Boateng, A. (2009). An Analysis of Short-run Performance of the UK Cross-border Mergers and Acquisitions: Evidence from the Acquiring Firms, Review of Accounting & Finance, Vol. 8, No 4. UNCTAD. (2005). World investment report 2005: Transnational corporations and the internationalization of R&D. NewYork and Geneva: UNCTAD UNCTAD (2006). World Investment Report: FDI from developing and transitional economies: implications for development, New York and Geneva: United Nations. UNCTAD (2009). World Investment Report: Transnational Corporations, Agricultural production and Development, New York and Geneva: United Nations. Vasconcellos, G.M., Madura, J. and Kish, R.K. (1990). An empirical investigation of factors affecting cross-border acquisitions: The US/UK experience, Global Finance Journal, Vol. 1(3), pp. 173-189. Waheed, A and Mathur, I. (1995). Wealth effects of foreign expansion by US banks, Journal of Banking and Finance, 19, pp. 823-842 Wells, L. T. 1983. Third world multinationals: The rise of foreign investment from developing countries. Cambridge, MA: MIT Press.

39

Westphal. J.D, Gulati, R. and Shortell, S.M. (1997). Customization or Conformity? An Institutional and network perspective on the content and consequences of TQM adoption, Administrative Science Quarterly, 42: 366-394 Wooten, M. and Hoffman, A. J. (2008). Organisational fields: Past, present, and future. In R.Greenwood, C.Oliver, K. Sahlin & R. Suddably (eds.), The Handbook of organisational institutionalism: 130-147, Thousand Oaks, CA: Sage. Wu, F and Sia Y.H (2002). China’s rising investment in Southeast Asia and outlook, Journal of Asian Business, 18, 2, 41-61. Xiao, J., & Sun, F. (2005).The challenges facing outbound Chinese M&A. International Financial Law Review, 24 (12), 44–46. Zhang, J.,Zhou, C., Ebbers, H. (2012). Completion of Chinese Overseas Acquisitions: Institutional Perspectives and Evidence, International Business Review, Zucker, L.G. (1987). Normal change or risky business: Institutional effects on the “hazard” of change in hospital organisations, 1959-1979, Journal of Management Studies, 24: 671-700

Table 1: Sample Selection and Sample Characteristics of Chinese Bidders Panel A: Sample Selection Number Percentage CBM&A after Initial Restrictions 445 100 Less: No data/News/missing values 287 8.1 Less Multiple Acquisitions 10 5.8 Net Sample 148 86.1 Panel B: Frequency by Region Asia/Pacific North America European Union Total

80 28 40 148

54.1 18.9 27.0 100

Panel C: Industry Classification Strategic Asset seeking (Priority) 63 42.6 Non-priority (No government support) 85 57.4 Total 148 100 Panel D: Frequency by Year 1998 5 3.3 1999 6 4.1 2000 8 5.4 2001 9 6.2 2002 11 7.4 2003 13 8.8 2004 20 13.5 2005 20 13.5 2006 19 12.8 2007 18 12.2 2008 19 12.8 Panel E: Sectoral Distribution Energy & Natural resources 15 10.1 Manufacturing 45 30.4 General Trade 30 20.3 Textile and Apparel 8 5.4 R & D 24 16.2 Building & Construction 10 6.8 Transport & Communication 16 10.8

Panel F: Deal Value $10 -100 million 90 60.8 Over $100 million 58 39.4

Total 148 100

Table 2: Measurement of Independent Variables Variables Measurement Government Priority Sector (CGOPD)

The sample was classified into two sectors: the top-priority sector, backed by the state, and the non-priority sector. A dummy variable representing state-backed sectors (strategic assets seeking) was constructed. Strategic assets seeking companies backed by the Chinese government are equal to 1, otherwise the value is zero.

Government Reforms Policy (GOVREF)

We measure the role of government reforms with a dummy variable: 0= 1998-June, 2006; 1 = July, 2006 – 2008, when the foreign currency approval system for outward investment was abolished.

Home country Gross Domestic Product (LGDP)

The GDP variable is measured as log of GDP during the study period.

Regional Location of the Target (REGION)

Following the work of Kiymaz (2004), a set of regional dummy variables were created based on the target firms geographical location. The Asia dummy variable is equal to one if the acquisition takes place in Asia, and zero otherwise. The U.S. and EUROPE variables are constructed similarly to the Asian dummies.

Exchange Rate (EXRATE)

A dummy for the period when the Chinese currency was fixed (0 = fixed rate; 1 = variable within limited margins).

Deal size (SIZE)

We measured the deal size by the natural log of the amount paid for the target firm

Sector A dummy variable for each sector: 1=Energy & natural resources; 0 =otherwise; 1= Manufacturing; 0 =otherwise; 1= General trade; 0 = otherwise; 1= Textiles & Apparel; 0= otherwise; 1=Service; 0=otherwise 1= Building & Construction; 0=otherwise; 1= Transport & Communication; 0 =otherwise

Control (CONTR) A dummy variable: 1=acquisition gives the acquirer control of the firm; 0=otherwise

Level of economic development (DEVLOP)

Based on IMF’s classification, target countries are classified into two groups: developed and developing economy. A dummy variable: 1= acquisition takes place in a developing country; 0 =otherwise

Notes: For the purpose of this study, priority sectors include: minerals, petroleum, fishery, agriculture products, textiles; motor, communication equipment manufacturing (Cai, 1999; Wu and Sia, 2002).

Table 3: Abnormal returns to Chinese acquirers surrounding the announcement of CBM&As Event Days AAR (%) t-statistics Panel A: Average Daily Abnormal Returns -10 0.0016 0.9636 -9 0.0013 0.4881 -8 - 0.0021 0.3009 -7 0.0013 1.2279 -6 0.0012 0.8967 -5 0.0011 0.2069 -4 0.0032 1.5847 -3 0.0002 -0.2746 -2 -0.0001 0.1707 -1 0.0036 1.7136* 0 0.0073 3.8227*** +1 0.0089 3.7935*** +2 0.0035 1.2583 +3 0.0017 0.8219 +4 0.0007 -0.0530 +5 -0.0011 -0.5609 +6 0.0030 1.3299 +7 0.0019 -0.7557 +8 -0.0018 -0.5587 +9 0.0015 0.7790 +10 0.0024 2.3613** Panel B: Cumulative Abnormal Returns (CAR)

Windows CARs (%) t-statistics CARs (-1,0) 0.0109 2.8655*** CARs (-1,1) 0.0197 3.2916*** CARs(-5,5) 0.0286 1.0879

Note: The null hypothesis is that the average abnormal returns are not statistically different from zero. ***, **, and * indicate statistical significance at the 1%, 5% and 10% levels, respectively.

Table 4: The Role of Government and Value Creation:

Event Window Variable Mean

SD t-value

Panel A Event Window

Priority v. non-priority

CAR (0,1) State-backed sector 0.0268 0.0219 Non-state backed -0.0178 0.1466 2.325** CAR (-1,+1) State-backed sector 0.0409 0.1730 Non-state backed 0.0170 0.1364 1.538

Panel B

CAR (0, 1) July 2006 -2008 0.0438 0.0866 1998 – June, 2006 0.0081 0.1291 -2.652*** CAR (-1, +1) July 2006 -2008 0.0642 0.2174 1998 – June, 2006 0.0079 0.1324 -1.812*

Panel C CAR (0,1) High Growth 0.007 0.0727 Low Growth 0.347 0.0575 0.395

Notes: *p<0.1; **p<0.05; ***p<0.01; Number of cases=148

Table 5: Summary Statistics

Variables Mean Standard Dev Minimum Maximum

CGOPD 0.21 0.408 0.00 1.00 GOVREF 0.28 0.452 0.00 1.00 CAR (0, +1) 0.015 0.687 -0.1747 0.3342 LGDP 11.258 1.305 8.858 12.264 CONTR 3.135 1.623 10.00 100.00

Energy 0.1014 0.30282 0.00 1.00 Manufacturing 0.3041 0.46157 0.00 1.00 General Trade 0.2027 0.30282 0.00 1.00

Textile 0.0541 0.22689 0.00 1.00 R&D 0.1622 0.36985 0.00 1.00