Replacement of mining trucks

Víctor Barrientos Boccardo

Jefe Mantenimiento Mina

Cerro Negro Norte I CAP Minería

INDEX

1. Introduction

2. Developed methodology

3. Results3. Results

4. Conclusions & limitations

1/30

1. Introduction

2. Developed methodology

3. Results

INDEX

3. Results

4. Conclusions & limitations

2/30

1. Introduction

In this study, we address the issues of

replacement of mining truck with

60.000 operating hours

3/30

1. Introduction

In this study, we want to determine for

mining trucks 60,000 hours of operation (8

years) which would have been the time of

replacement and if now is the time to do itreplacement and if now is the time to do it

4/30

1. Introduction

a) We have reliable information

maintenance costs and useful lives

major and minor components

b) These trucks are used in an open pit

mine

5/30

1. Introduction

c) Downtime costs or costs not produce are

included for this study

d) The maintenance outsourcing (dealer)

6/30

1. Introduction

2. Developed methodology

3. Results

INDEX

3. Results

4. Conclusions & limitations

7/30

It uses the methodology of calculation of

equivalent annual costs (EAC) to

determine which year should have

replaced mining trucksreplaced mining trucks

8/30

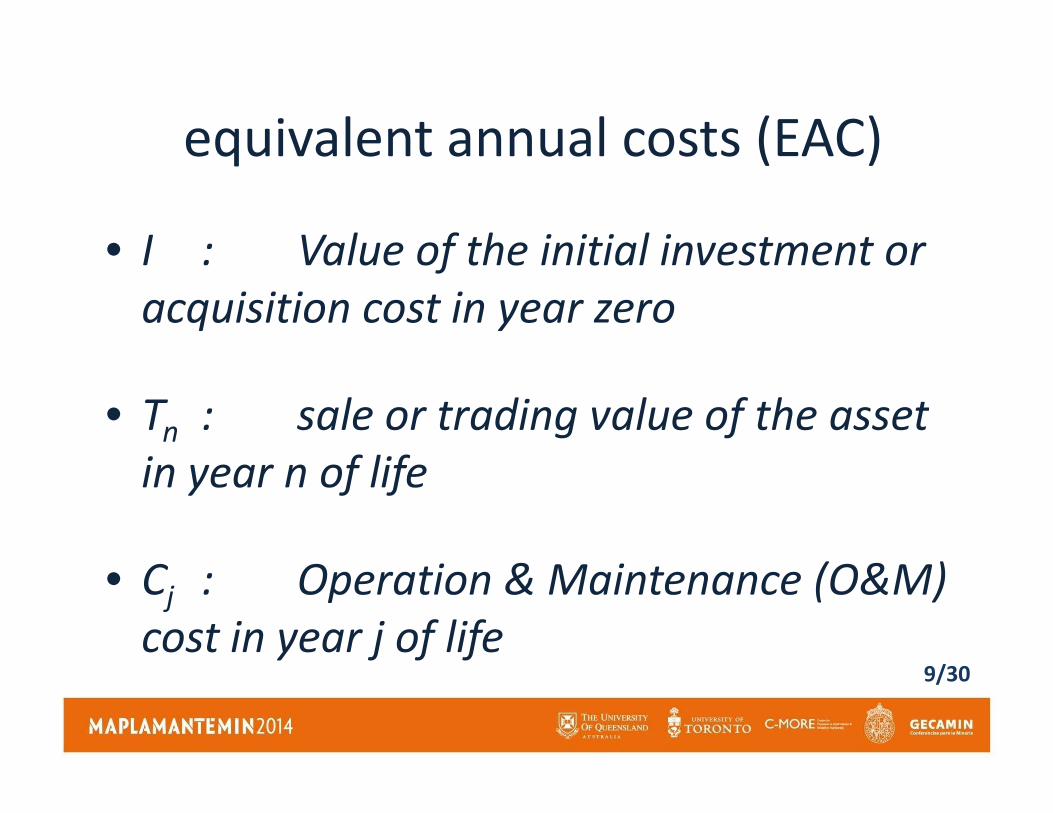

2. Equivale

equivalent annual costs (EAC) nt

Annual Costs• I : Value of the initial investment or

acquisition cost in year zero

• T : sale or trading value of the asset• Tn : sale or trading value of the asset

in year n of life

• Cj : Operation & Maintenance (O&M)

cost in year j of life9/30

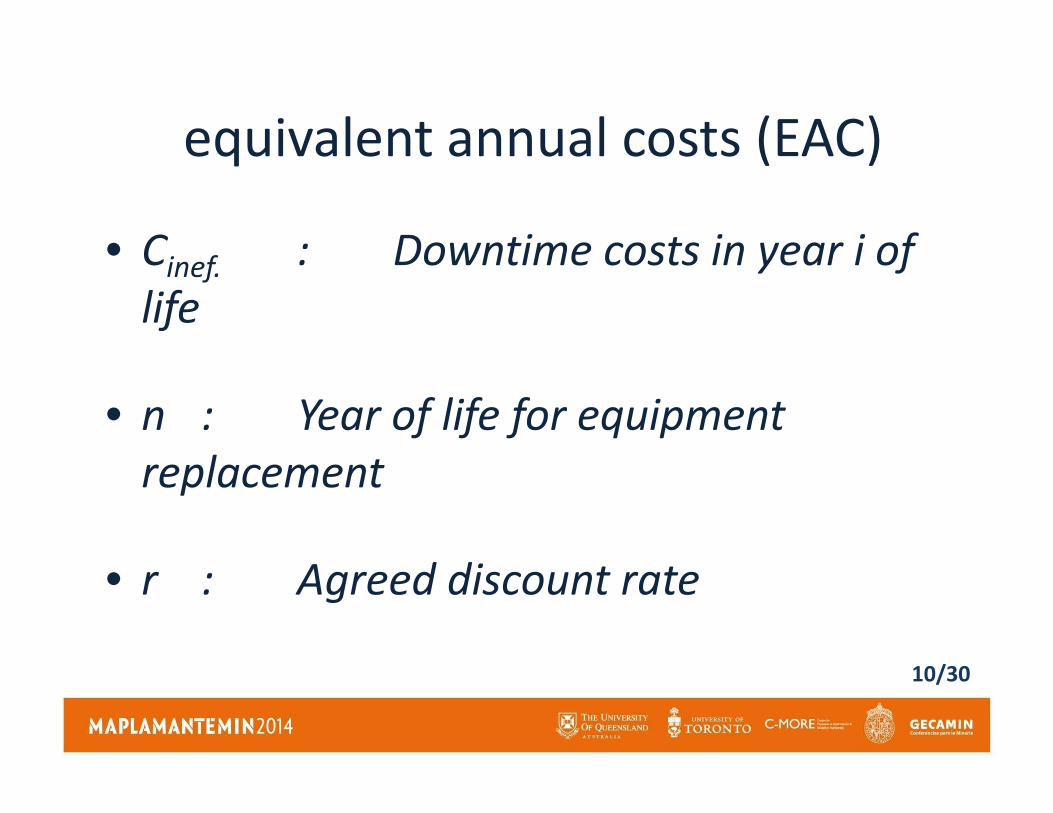

• Cinef. : Downtime costs in year i of

life

• n : Year of life for equipment

2. Equivale

equivalent annual costs (EAC) nt

Annual Costs

• n : Year of life for equipment

replacement

• r : Agreed discount rate

10/30

How the methodology of

Equivalente Annual Cost (EAC)

is mathematically expresed?

11/30

is mathematically expresed?

2. Methodology

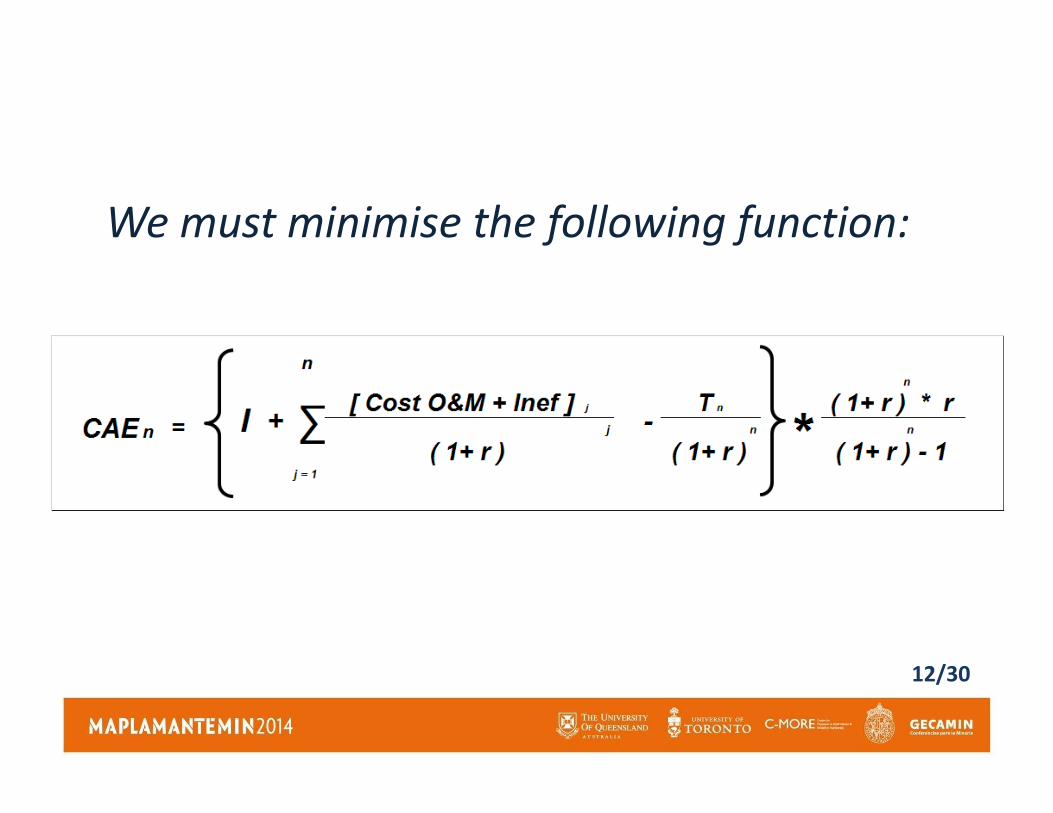

We must minimise the following function:

12/30

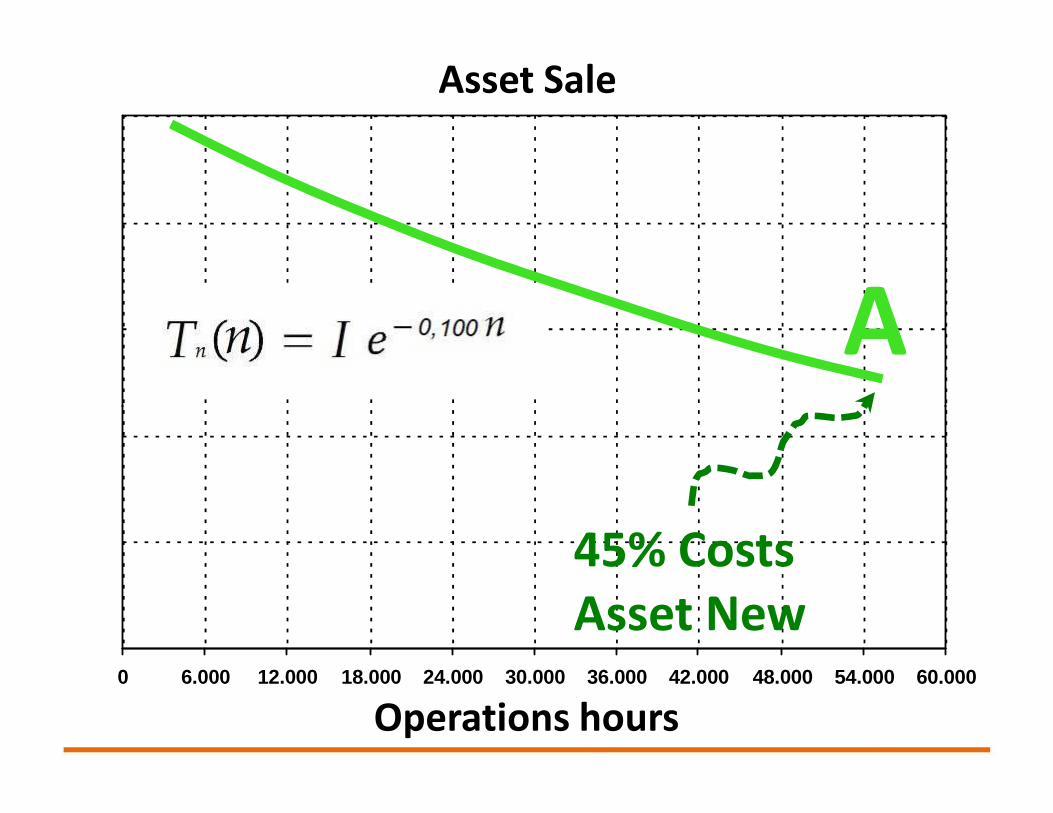

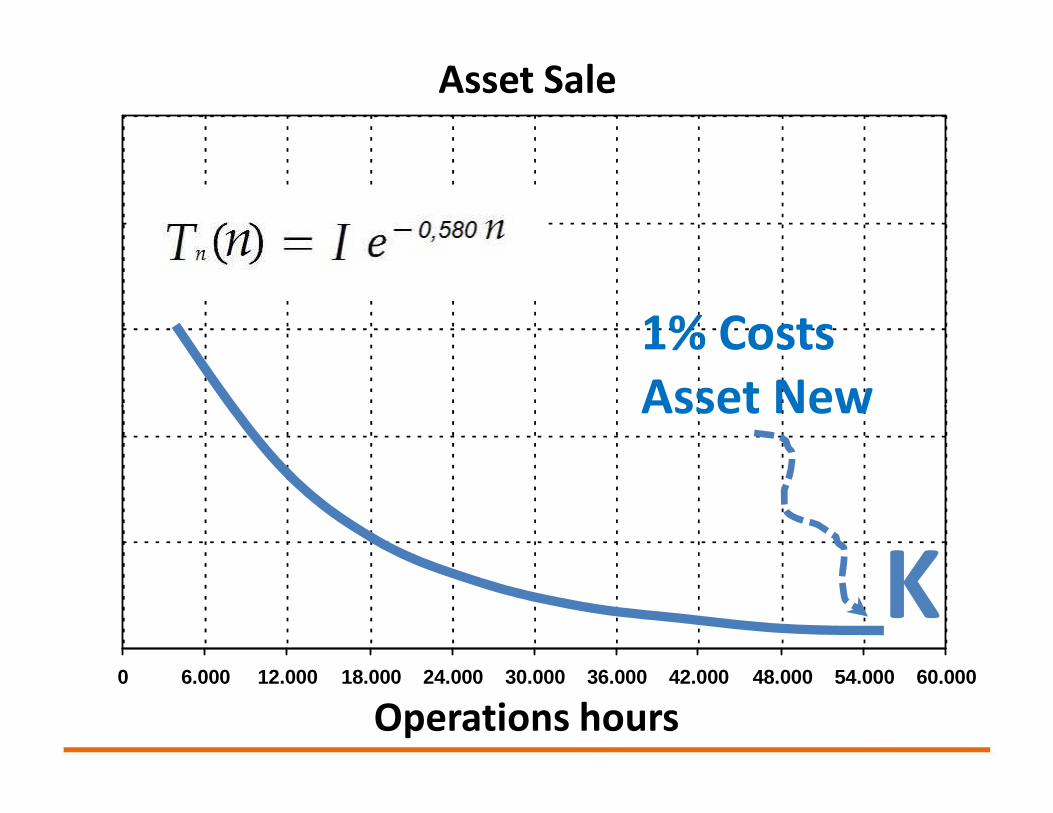

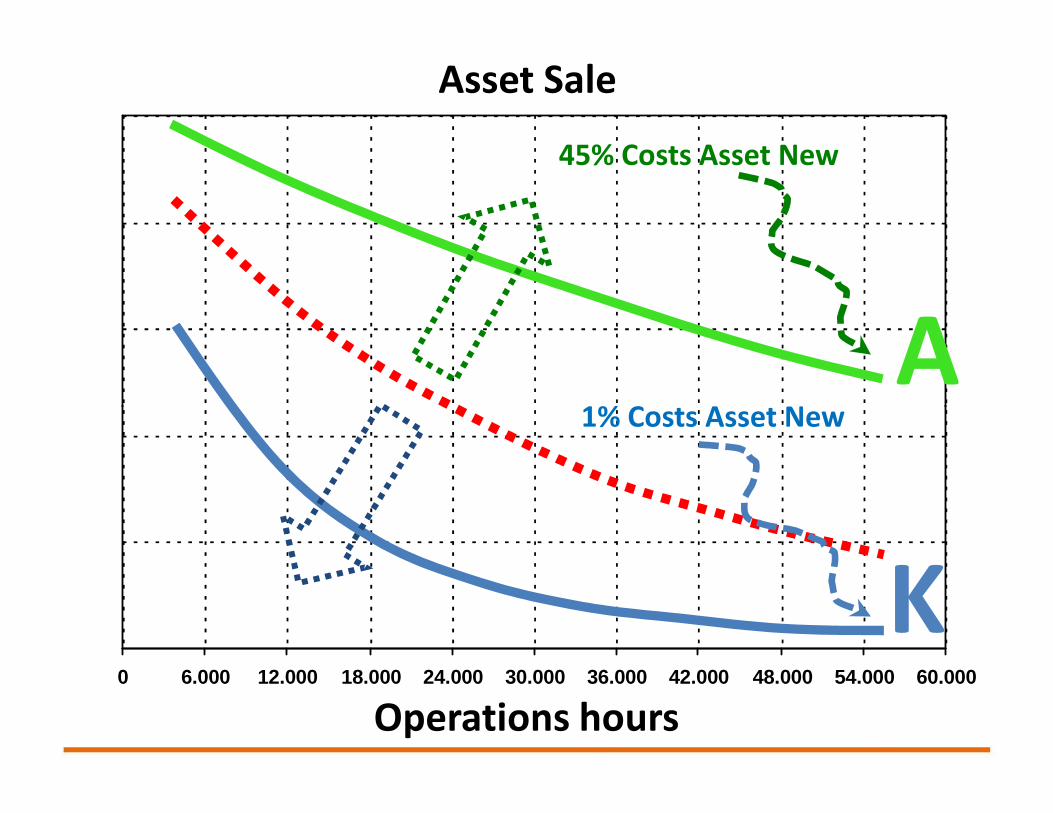

We make a sensitivity analysis for the sale

of the Asset Sale of ten form of

depreciation

13/30

Asset Sale

A

0 6.000 12.000 18.000 24.000 30.000 36.000 42.000 48.000 54.000 60.000

Operations hours

45% Costs

Asset New

Asset Sale

1% Costs

Asset New

0 6.000 12.000 18.000 24.000 30.000 36.000 42.000 48.000 54.000 60.000

Operations hours

Asset New

K

Asset Sale

45% Costs Asset New

1% Costs Asset New

A

0 6.000 12.000 18.000 24.000 30.000 36.000 42.000 48.000 54.000 60.000

Operations hours

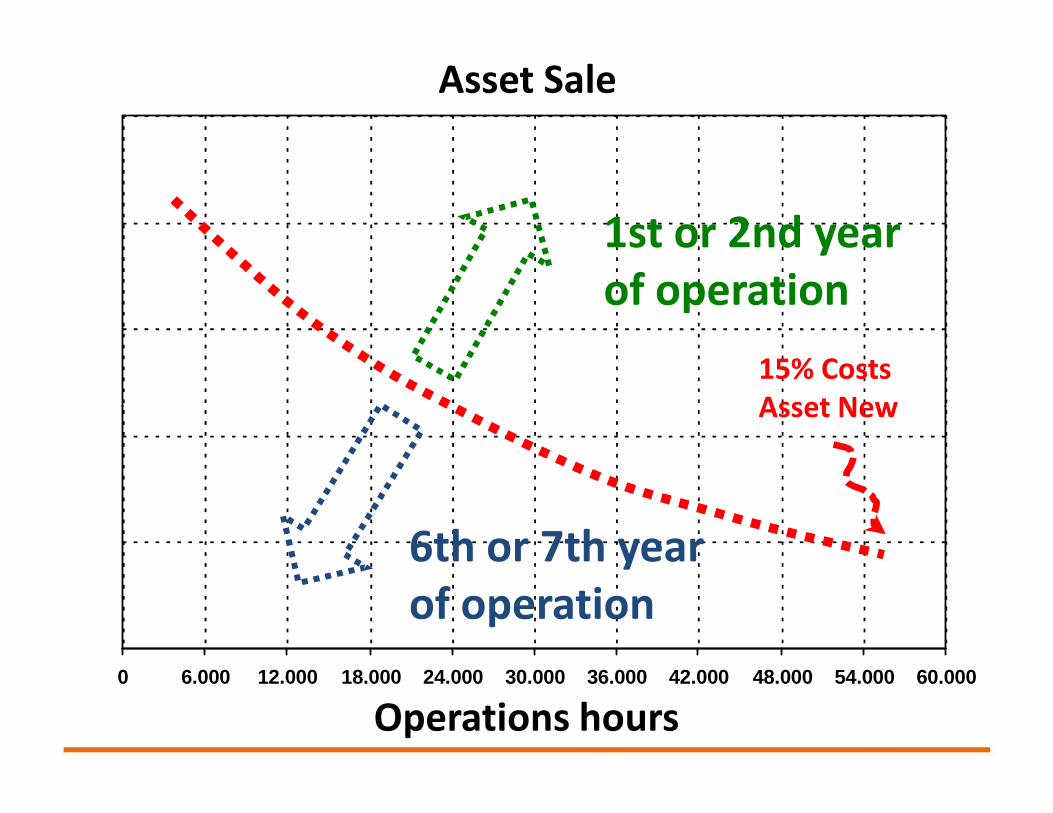

1% Costs Asset New

K

A

Asset Sale

1st or 2nd year

of operation

15% Costs

Asset New

0 6.000 12.000 18.000 24.000 30.000 36.000 42.000 48.000 54.000 60.000

Operations hours

6th or 7th year

of operation

Asset New

1. Introduction

2. Developed methodology

3. Results

INDEX

3. Results

4. Conclusions & limitations

18/30

3. Results

In a 2-dimensional graph

considering

X-axis: Hour meter of the equipmentX-axis: Hour meter of the equipment

(hours)

Y-axis: Dollars (US$)

19/30

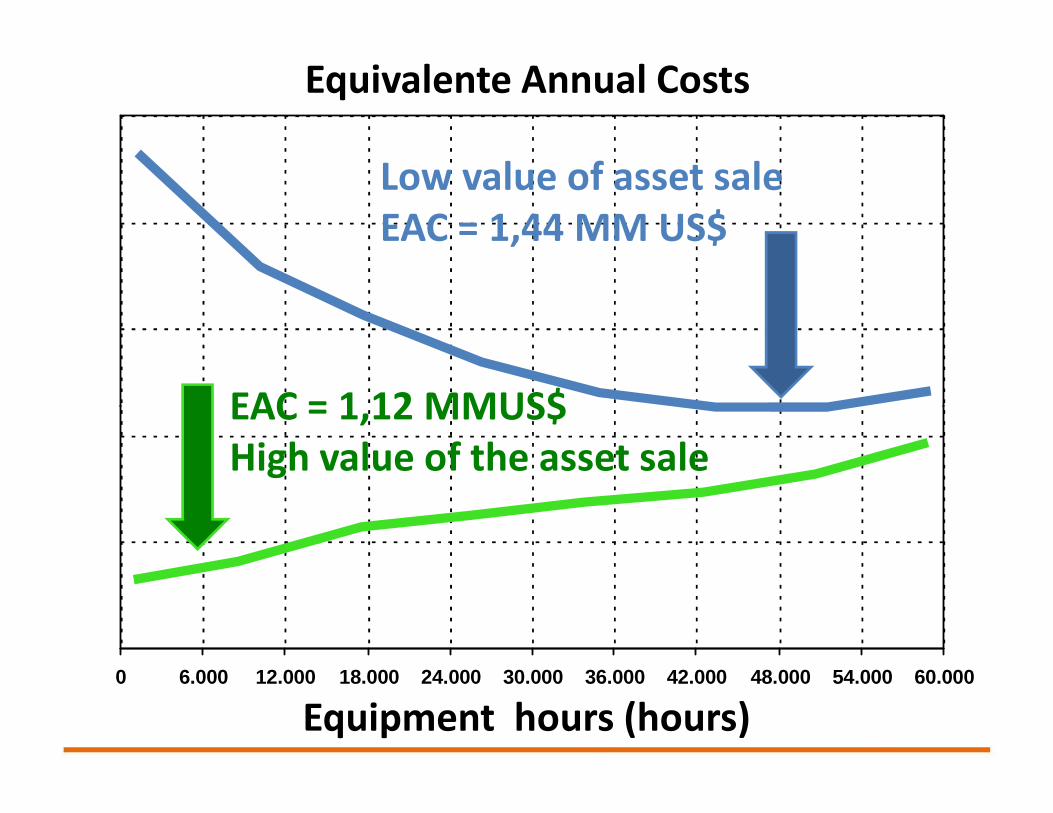

Equivalente Annual Costs

EAC = 1,12 MMUS$

Low value of asset sale

EAC = 1,44 MM US$

0 6.000 12.000 18.000 24.000 30.000 36.000 42.000 48.000 54.000 60.000

Equipment hours (hours)

EAC = 1,12 MMUS$

High value of the asset sale

Equivalente Annual Costs

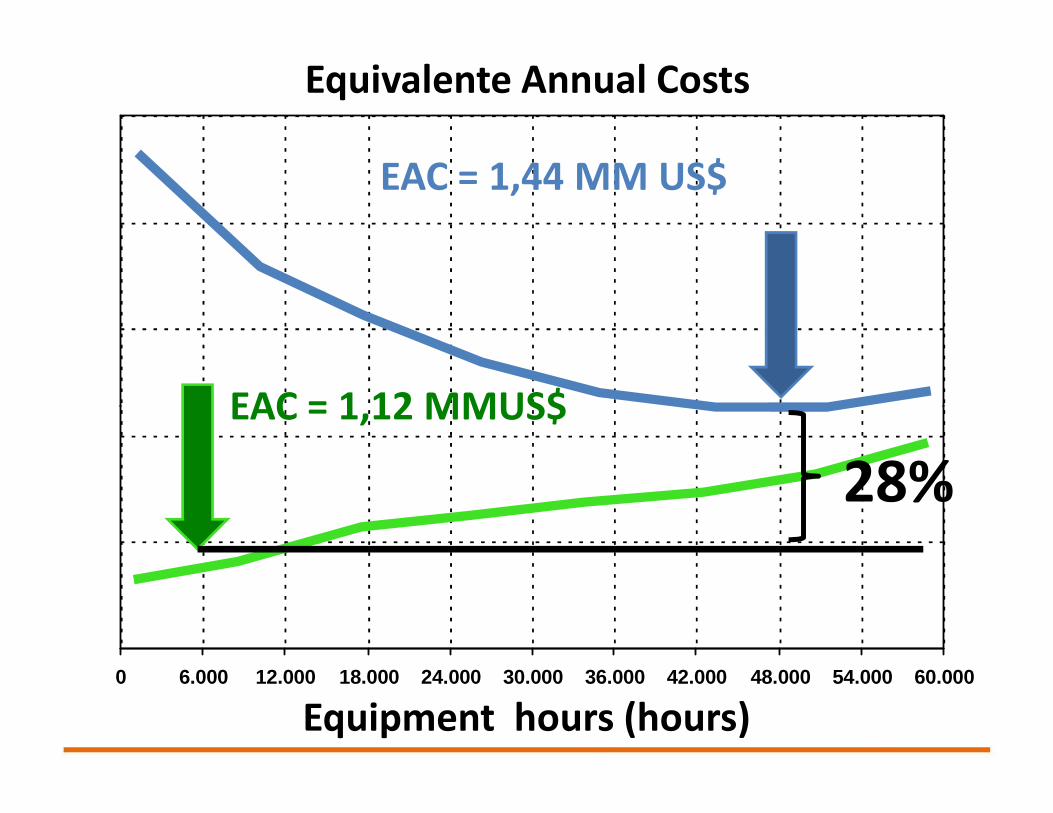

EAC = 1,12 MMUS$

EAC = 1,44 MM US$

0 6.000 12.000 18.000 24.000 30.000 36.000 42.000 48.000 54.000 60.000

Equipment hours (hours)

EAC = 1,12 MMUS$

28%

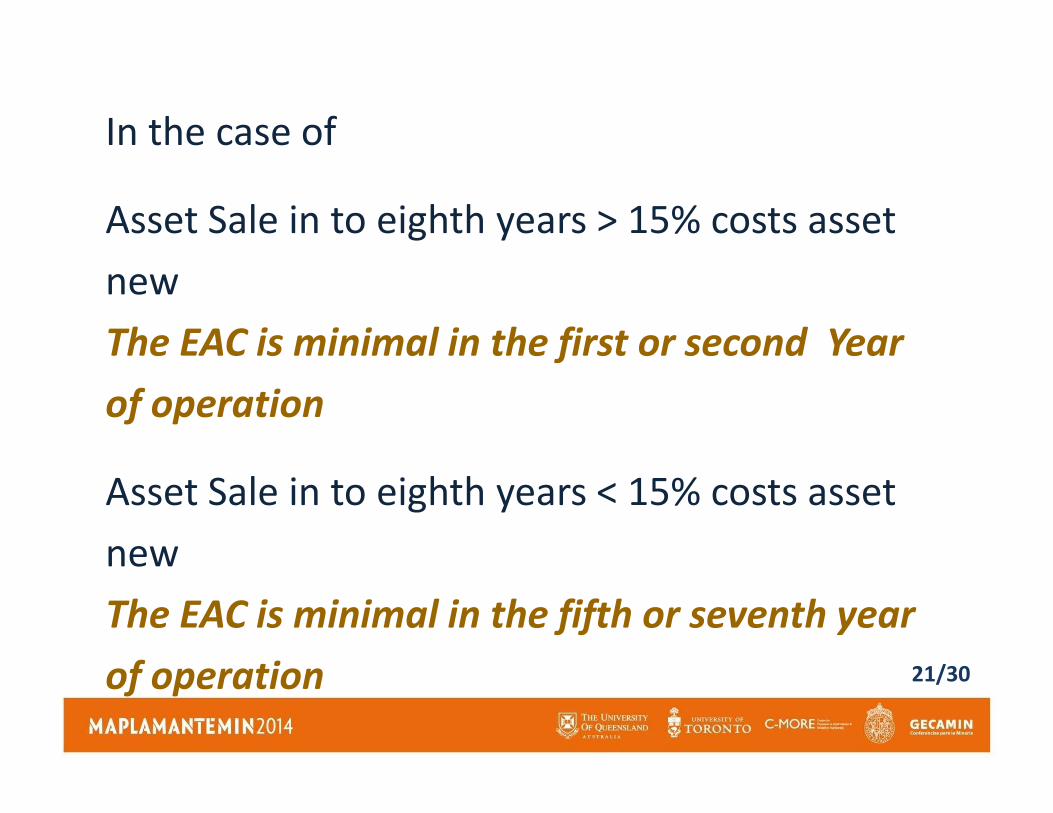

In the case of

Asset Sale in to eighth years > 15% costs asset

new

The EAC is minimal in the first or second Year

of operationof operation

Asset Sale in to eighth years < 15% costs asset

new

The EAC is minimal in the fifth or seventh year

of operation 21/30

1. Introductions

2. Developed methodology

3. Results

INDEX

3. Results

4. Conclusions & limitations

22/30

With the information obtained for this case

study, we can say that:

• The operations and maintenence costs

are increasing over the yearsare increasing over the years

• The availability of the first year of

operation is higher than in the

following years23/30

• The operations and maintenence costs

were strongly influenced by the

strategy change of major and minor

components used

24/30

• This strategy use condition monitoring

to extend the useful life of components,

delaying their return, obtaining

increases in availability and cost

decreases in the early years, movingdecreases in the early years, moving

these non-availability and costs to

future years

25/30

• For the case study, this non-availability

strongly affected in the eighth year of

operation, with availability 13% lower

than in the first year of operation,

resulting in a loss of production due toresulting in a loss of production due to

lack of truck

• For all simulations the time of

replacement is now 26/30

• If the sale of the asset, we can get a

HIGH value sale in the first years of

operation, I should sell it at that time

• Conversely, if the asset sale we can get• Conversely, if the asset sale we can get

a LOW sales value in the first years of

operation, I should sell it after

27/30

Thanks you very much

Víctor Barrientos Boccardo

CAP Minería I Cerro Negro Norte

28/30

Recommended