Recent Court Cases on Brazilian CFC Legislation

Jérôme van StandenNovember 2012

AgendaBrazilian CFC Rules

1. General Overview

2. ADI 2,588

Recent Court Cases

1.Eagle I and II

2.Camargo Correa

3.Normus

4.Vale

5.Marcopolo

6.Brazil Foods

Brazilian CFC RulesGeneral Overview

Brazilian CFC Rules | General Overview

History

Market globalization prompted the Brazilian government to adopt the

worldwide income taxation regime for corporate entities as of January 1st,

1996

Law 9,249/1995, regulated by Normative Instruction (“IN”) 38/1996,

introduced the levy of corporate income tax on foreign profits, earnings

and capital gains for corporate entities headquartered in Brazil

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation4

Law 9,532/1997 brought to the Brazilian legal system criteria to

determine the availability of foreign profits (i.e. in case of branches, at the

moment of their inclusion on the company‟s book and in case of

subsidiaries or affiliates, when they were paid, credited, used, delivered or

remitted to the Brazilian legal entity)

Foreign profits, earnings and capital gains recorded as of October 1st,

1999 have become subject to Social Contribution Tax (CSLL), through

Provisory Measure (“MP”) 1,858-7/1999

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation5

Brazilian CFC Rules | General Overview

Article 74 of MP 2,158-35/2001 introduced an automatic taxation

system whereby foreign profits would be considered available to the

Brazilian company by the end of each calendar year, regardless of actually

distributed or not

Enacted to regulate article 74 of MP 2,158-35/2001 (and to replace IN

38/1996), IN 213/2002 created special cases where foreign profits shall

be considered as available to the Brazilian parent company for tax

purposes

Corporate entities recording foreign source earnings and capital gains

must calculate Income Tax according to taxable profit based on accounting

records

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation6

Brazilian CFC Rules | General Overview

Brazilian CFC Rules | General Overview

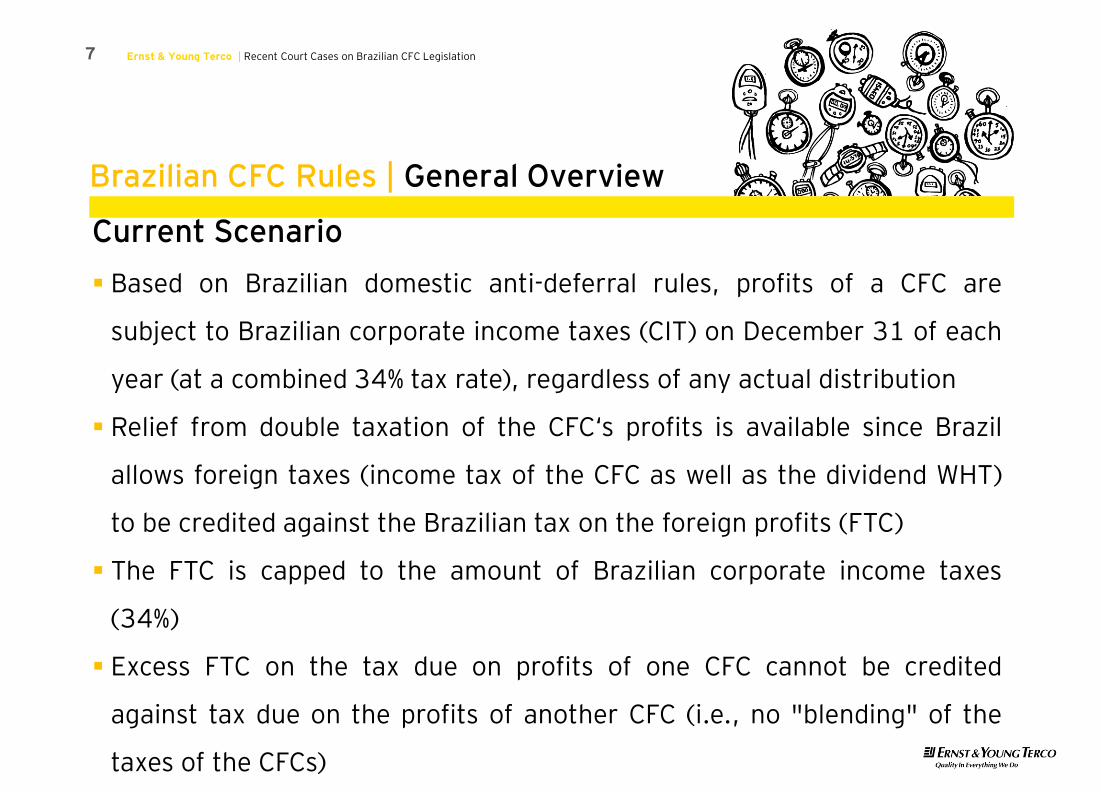

Current Scenario

Based on Brazilian domestic anti-deferral rules, profits of a CFC are

subject to Brazilian corporate income taxes (CIT) on December 31 of each

year (at a combined 34% tax rate), regardless of any actual distribution

Relief from double taxation of the CFC„s profits is available since Brazil

allows foreign taxes (income tax of the CFC as well as the dividend WHT)

to be credited against the Brazilian tax on the foreign profits (FTC)

The FTC is capped to the amount of Brazilian corporate income taxes

(34%)

Excess FTC on the tax due on profits of one CFC cannot be credited

against tax due on the profits of another CFC (i.e., no "blending" of the

taxes of the CFCs)

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation7

Brazilian CFC Rules | General Overview

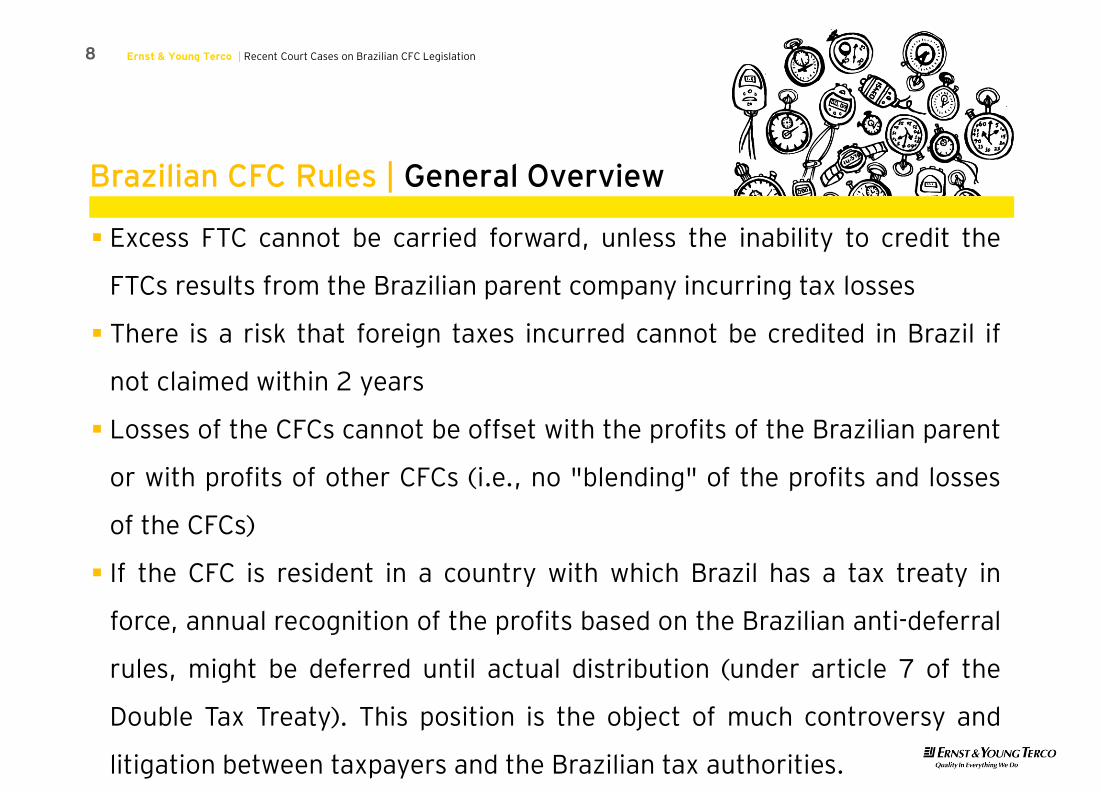

Excess FTC cannot be carried forward, unless the inability to credit the

FTCs results from the Brazilian parent company incurring tax losses

There is a risk that foreign taxes incurred cannot be credited in Brazil if

not claimed within 2 years

Losses of the CFCs cannot be offset with the profits of the Brazilian parent

or with profits of other CFCs (i.e., no "blending" of the profits and losses

of the CFCs)

If the CFC is resident in a country with which Brazil has a tax treaty in

force, annual recognition of the profits based on the Brazilian anti-deferral

rules, might be deferred until actual distribution (under article 7 of the

Double Tax Treaty). This position is the object of much controversy and

litigation between taxpayers and the Brazilian tax authorities.

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation8

Brazilian CFC Rules | General Overview

Criticism

Brazilian CFC rules are highly criticized due to:

A company that holds an investment in a controlled or affiliated

foreign company, which is in a profit position, should offer to taxation

in Brazil such profits on December 31 of each year regardless of

whether they were actually distributed or not

Brazilian CFC legislation does not distinguish between: (i) passive or

active income; (ii) tax regime to which the CFC is subject to (high or

low taxed), (iii) type of company (no basket rules)

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation9

Brazilian CFC Rules | General Overview

In case the Brazilian company holds less than 20% of the participation

in a CFC, automatic taxation does not apply – cash basis

CFC capital/operational losses cannot be picked up in the Brazilian

parent

There is no distinction if the CFC is a branch or a separate subsidiary

It notably differs from international standards

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation10

Brazilian CFC Rules | ADI 2,588

Article 74 of MP n° 2.158-35/01 and its sole paragraph also brings an

intense debate regarding their constitutionality since they introduced a

triggering event for corporate income taxes, which seems to be not

consistent with the tax legal system currently in force in Brazil

The Brazilian Supreme Court is currently ruling on the constitutionality of

the provision introduced in the Brazilian legal system by article 74 of MP n°

2158-35/01 and the paragraph 2 of article 43 of the Brazilian Tax Code

(CFC Rules) - ADIn 2,588

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation11

Brazilian CFC Rules | ADI 2,588

The judgment has started in 2001 and so far it is still very difficult to

determine which will probably be the prevailing decision. So far, nine

Ministers from the Supreme Court, from a total of 11 Ministers of which

only ten are able to vote on the constitutionality issue, declared their

opinion on the constitutionality issue:

One Minister (Ellen Gracie) voted for the partial unconstitutionality in

respect to foreign affiliates

Four Ministers (Nelson Jobim, Eros Grau, Carlos Ayres Britto and Cezar

Peluso) voted for the constitutionality and

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation12

Brazilian CFC Rules | ADI 2,588

Four Ministers (Marco Aurélio, Sepúlveda Pertence, Ricardo

Lewandowski and Celso de Mello) voted for the unconstitutionality of

the CFC Rules

Minister Joaquim Barbosa should be next one to vote on the

constitutionality or not of the provisions

Supreme Court Decision on Extraordinary Appeal (RE) 611.586 (Leading

Case):

General repercussion confirmed

Effects of a potential positive ruling

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation13

Recent Court Cases

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation15

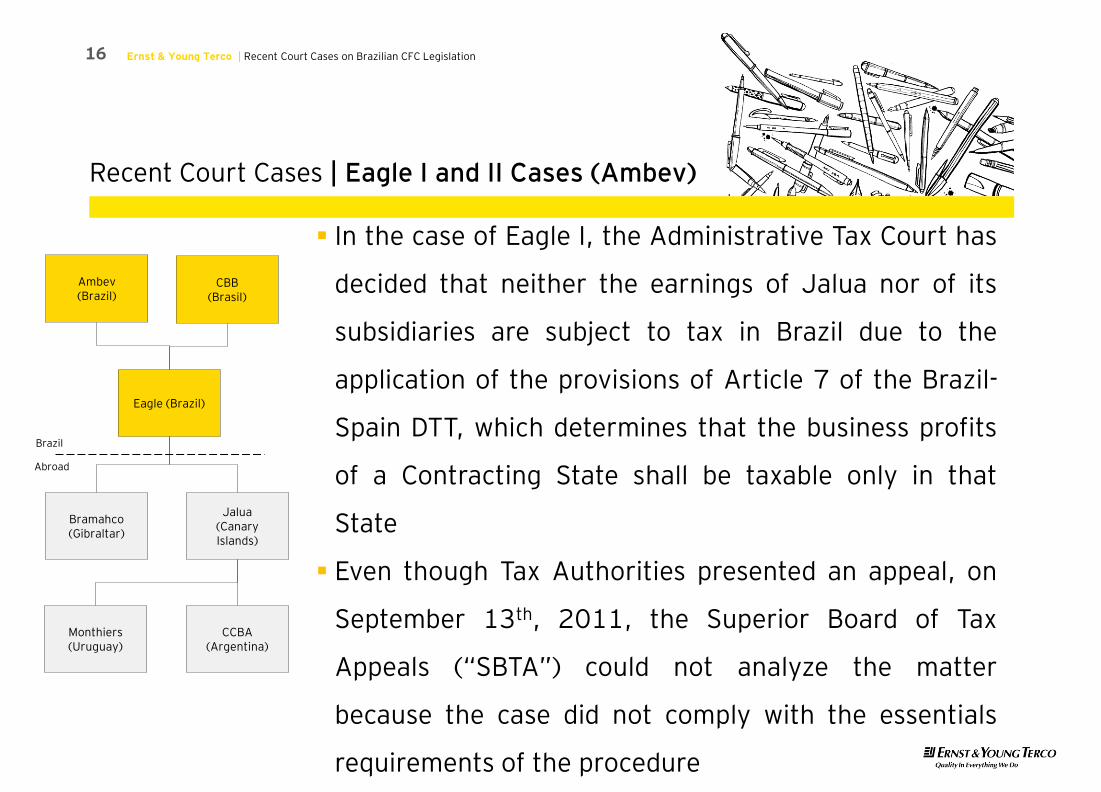

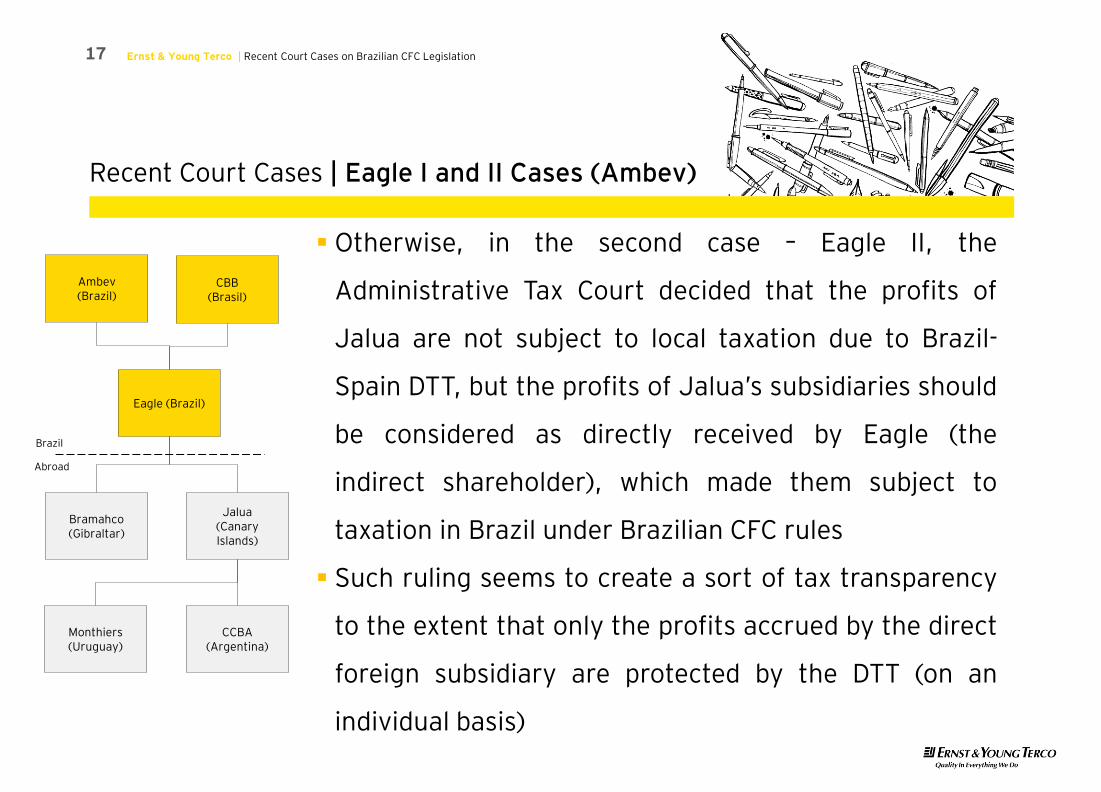

Recent Court Cases | Eagle I and II Cases (Ambev)

In January 2005, Brazilian Tax Authorities assessed

Eagle Distribuidora de Bebidas S.A. (“Eagle”) for not

taxing the earnings of Jalua Spain S.L. (“Jalua”) and

Brahmaco, its foreign subsidiaries in Canary Islands

and Gibraltar, in accordance with Article 74 of MP n°

2158-35/2001. Jalua also owns two subsidiaries:

Monthiers (Uruguay) and CCBA (Argentina)

Eagle I refers to calendar years 2000 and 2001

(previous to the CFC rules currently in force), while

Eagle II refers to calendar year 2002

Eagle (Brazil)

Jalua(Canary Islands)

Monthiers (Uruguay)

CCBA (Argentina)

Bramahco (Gibraltar)

Ambev(Brazil)

CBB(Brasil)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation16

Recent Court Cases | Eagle I and II Cases (Ambev)

In the case of Eagle I, the Administrative Tax Court has

decided that neither the earnings of Jalua nor of its

subsidiaries are subject to tax in Brazil due to the

application of the provisions of Article 7 of the Brazil-

Spain DTT, which determines that the business profits

of a Contracting State shall be taxable only in that

State

Even though Tax Authorities presented an appeal, on

September 13th, 2011, the Superior Board of Tax

Appeals (“SBTA”) could not analyze the matter

because the case did not comply with the essentials

requirements of the procedure

Eagle (Brazil)

Jalua(Canary Islands)

Monthiers (Uruguay)

CCBA (Argentina)

Bramahco (Gibraltar)

Ambev(Brazil)

CBB(Brasil)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation17

Recent Court Cases | Eagle I and II Cases (Ambev)

Otherwise, in the second case – Eagle II, the

Administrative Tax Court decided that the profits of

Jalua are not subject to local taxation due to Brazil-

Spain DTT, but the profits of Jalua‟s subsidiaries should

be considered as directly received by Eagle (the

indirect shareholder), which made them subject to

taxation in Brazil under Brazilian CFC rules

Such ruling seems to create a sort of tax transparency

to the extent that only the profits accrued by the direct

foreign subsidiary are protected by the DTT (on an

individual basis)

Eagle (Brazil)

Jalua(Canary Islands)

Monthiers (Uruguay)

CCBA (Argentina)

Bramahco (Gibraltar)

Ambev(Brazil)

CBB(Brasil)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation18

Recent Court Cases | Camargo Correa Case

In this case, the Administrative Tax Court has ruled on

the taxation of the profits earned by subsidiaries of a

Brazilian parent, located in Portugal and Luxembourg

Both countries have concluded DTTs with Brazil

The Administrative Tax Court ruled that article 74 of MP

2.158-35/01 actually provides for a deemed profit

distribution, which should qualify as dividend income,

subject to article 10 provision of the Brazil-Portugal DTT

Camargo Correa(Brazil)

Subsidiary(Luxembourg)

Subsidiary (Portugal)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation19

Recent Court Cases | Camargo Correa Case

Although the Brazil-Portugal DTT prohibits the taxation

of the non-distributed profits (under article 10,

paragraph 5), the Court understood that the DTT does

not prevent Brazil from taxing the profits earned by the

Brazilian shareholders of the Portuguese company

As to the Luxembourg subsidiary, the Administrative Tax

Court has ruled that it could not benefit from the Brazil-

Luxembourg DTT since it was a Holding 1929 company

(i.e. not subject to treaty benefits)

Camargo Correa(Brazil)

Subsidiary(Luxembourg)

Subsidiary (Portugal)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation20

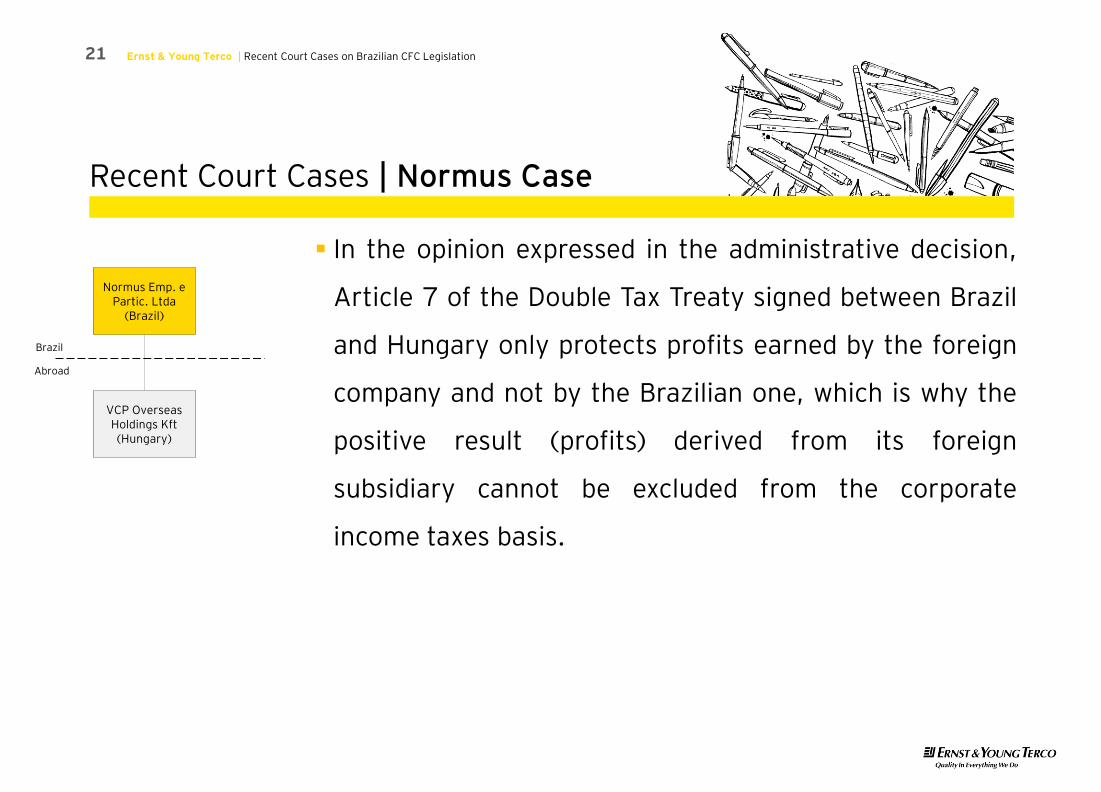

Recent Court Cases | Normus Case

On January 27th, 2011, Administrative Tax Court

decided for the taxation, for Brazilian corporate income

taxes purposes, of profits earned by a subsidiary located

in Hungary.

The decision considered that, since the Brazilian

company has recognized foreign profits for accounting

purposes based on the net equity method of accounting,

its profits, income and capital gain earned abroad should

be taxed in Brazil in the end of each fiscal year, under

Article 25 of Law 9,249/95 and Article 74 of the

Provisional Measure 2,158/01.

Normus Emp. e Partic. Ltda

(Brazil)

VCP Overseas Holdings Kft(Hungary)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation21

Recent Court Cases | Normus Case

In the opinion expressed in the administrative decision,

Article 7 of the Double Tax Treaty signed between Brazil

and Hungary only protects profits earned by the foreign

company and not by the Brazilian one, which is why the

positive result (profits) derived from its foreign

subsidiary cannot be excluded from the corporate

income taxes basis.

Normus Emp. e Partic. Ltda

(Brazil)

VCP Overseas Holdings Kft(Hungary)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation22

Recent Court Cases | Normus Case

Despite the unfavorable decision, it is worth noting that

one of the counselors, who decided this case,

understood for the non-taxation of the result of the net

equity method of accounting. In addition, this decision

was unanimous with respect to the non-taxation of the

currency exchange results registered over the foreign

investment.

Normus Emp. e Partic. Ltda

(Brazil)

VCP Overseas Holdings Kft(Hungary)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation23

Recent Court Cases | Vale Case

On March 29th, 2011, the Federal Judicial Court has

ruled on the taxation, for Brazilian corporate income

taxes purposes, of profits earned by the Vale‟s

subsidiaries located in Belgium, Denmark and

Luxembourg

The Court considered that Article 74 of the MP no

2.518/01 does not offend the concept of “income”

established by Federal Constitution/88, given that the

law may legitimately establish criteria as to determine

when the profit is considered as available for tax

purposes

Vale(Brazil)

Subsidiary(Denmark)

Subsidiary(Luxembourg)

Subsidiary(Belgium)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation24

Recent Court Cases | Vale Case

In its appeal, Vale claimed that Article 74 of the MP no

2.518/01 is incompatible with the treaties to avoid

double taxation entered into by Brazil with the States of

domicile of the subsidiary companies, as well as it has

extrapolated the permission granted by Article 43,

heading and paragraph 2, of the Brazilian Tax Code,

which states that “In the hypothesis of income or

earnings arising abroad, the law shall establish the

conditions and the moment at which they will be

considered available, for purposes of the levy of tax

referred to in this article”

Vale(Brazil)

Subsidiary(Denmark)

Subsidiary(Luxembourg)

Subsidiary(Belgium)

Brazil

Abroad

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation25

Recent Court Cases | Vale Case

However, the Court ruled that there is no infringement

of Tax Treaties. In their opinion, in accordance with said

treaty, the State where the parent company is

headquartered can tax not only the income earned

inside its territory, but also the foreign income earned

by subsidiaries located abroad

Vale(Brazil)

Subsidiary(Denmark)

Subsidiary(Luxembourg)

Subsidiary(Belgium)

Brazil

Abroad

Recent Court Cases | Marcopolo Cases

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation26

The Brazilian Tax Authorities ("BTA") assessed

Marcopolo S/A for operations from 2001 to 2007, which

consisted of exporting vehicle chassis and bodies to two

subsidiaries: Marcopolo International Corporation

("MIC"), based in the British Virgin Islands, and Ilmot

International Corporation ("ILMOT"), Uruguay

They were also questioned about some sales to third

parties based in tax havens. These export transaction

were made to MIC and ILMOT - intermediating related

companies, named reinvoincing centers - that marketed

directly to end consumers

Marcopolo (Brazil)

ILMOT (Uruguay)

MIC (British Islands)

Recent Court Cases | Marcopolo Cases

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation27

As a result of this tax assessment, Marcopolo was

charged regarding corporate income taxes, ex-officio fine

for fraud and qualified fine for not providing sufficient

information when requested, as the BTA understood that

the export transactions made by Marcopolo to its

subsidiaries located abroad were a sham and lacked any

real substance. The BTA also affirmed that the

constitution of these trading companies was totally

unnecessary and had the sole purpose of avoiding the

taxation of the income in Brazil since the trading

companies are located in tax havens. Both understanding

were confirmed by the Taxpayers‟ Council at the time

Marcopolo (Brazil)

ILMOT (Uruguay)

MIC (British Islands)

Recent Court Cases | Marcopolo Cases

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation28

This case has a relevant role in the analysis regarding the

economic substance necessary in a foreign corporate

structure for Brazilian tax purposes

In recent decisions as regards as different fiscal years,

the Administrative Tax Court decided that (i) the named

“underpricing” policy cannot be understood as income

omission to the extent that the sales had accounting

records, and (ii) there was no fraud as BTA were not able

to prove the taxpayer‟s intention of sham, reason why the

ex-officio fine was disqualified

Marcopolo (Brazil)

ILMOT (Uruguay)

MIC (British Islands)

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation29

Recent Court Cases | Brazil Foods Case

Although such decision has not been published yet, it seems to be relevant

for CFC purposes from what the press has made available to us

In this Case, the Brazilian parent owned one direct foreign subsidiary (first

tier) and three indirect foreign subsidiaries (second tier) through such first

tier one

Brazilian Tax Authorities (“BTA”) have assessed individual results of all

foreign subsidiaries although Normative Instruction 213/2002 provides

for the vertical consolidation

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation30

Recent Court Cases | Brazil Foods Case

Under article 1, paragraph 6 of Normative Instruction 213/2002, the

profits generated at the level of the foreign subsidiaries should be

consolidated at the level of the first tier foreign subsidiary for the

purposes of determining the profit subject to taxation in Brazil under

Brazilian CFC rules

In this context, the Administrative Tax Court ruled on the need for the

vertical consolidation since only the consolidated result should be subject

to taxation in Brazil under the applicable rules

Ernst & Young Terco | Recent Court Cases on Brazilian CFC Legislation31

Recent Court Cases | Supreme Court Cases

Constitutionality of Article 74 of MP 2158-35/2001

COAMO – RE 611.586

EMPRESA BRASILEIRA DE COMPRESSORES S/A – EMBRACO – RE

541.090

Thank you!

Recommended