R&D Investor Day

LainateJanuary 30, 2015

1

2

Safe HarbourThis presentation may include forward-looking statements that are based on our

management’s beliefs and assumptions and on information currently available to our

management.

The inclusion of forward-looking statements should not be regarded as a

representation by Cosmo that any of its plans will be achieved. Actual results may

differ materially from those set forth in this presentation due to the risks and

uncertainties inherent in Cosmo’s ability to develop and expand its business,

successfully complete development of its current product candidates and current and

future collaborations for the development and commercialisation of its product

candidates and reduce costs (including staff costs), the market for drugs to treat IBD

diseases, Cosmo’s anticipated future revenues, capital expenditures and financial

resources and other similar statements, may be "forward-looking" and as such involve

risks and uncertainties and risks related to the collaboration between Partners and

Cosmo, including the potential for delays in the development programs for Methylene

Blue MMX®, Rifamycin SV MMX®, and CB-03-01. No assurance can be given that the

results anticipated in such forward looking statements will occur. Actual events or

results may differ materially from Cosmo’s expectations due to factors which include,

but are not limited to, increased competition, Cosmo’s ability to finance expansion

plans, the results of Cosmo’s research and development activities, the success of

Cosmo’s products, regulatory, legislative and judicial developments or changes in

market and/or overall economic conditions. Cosmo assumes no responsibility to

update forward-looking statements or to adapt them to future events or

developments.

You are cautioned not to place undue reliance on these forward-looking statements,

which speak only as of the date hereof, and Cosmo undertakes no obligation to revise

or update this presentation.

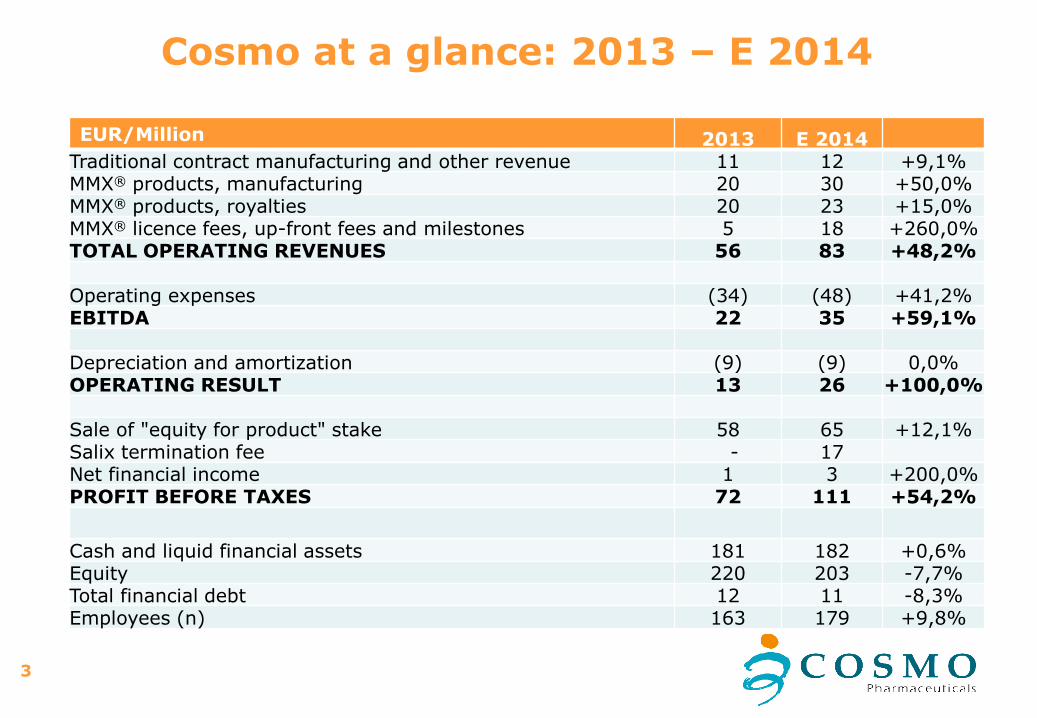

3

EUR/Million 2013 E 2014Traditional contract manufacturing and other revenue 11 12 +9,1%MMX® products, manufacturing 20 30 +50,0%MMX® products, royalties 20 23 +15,0%MMX® licence fees, up-front fees and milestones 5 18 +260,0%TOTAL OPERATING REVENUES 56 83 +48,2%

Operating expenses (34) (48) +41,2%EBITDA 22 35 +59,1%

Depreciation and amortization (9) (9) 0,0%OPERATING RESULT 13 26 +100,0%

Sale of "equity for product" stake 58 65 +12,1%Salix termination fee - 17Net financial income 1 3 +200,0%PROFIT BEFORE TAXES 72 111 +54,2%

Cash and liquid financial assets 181 182 +0,6%Equity 220 203 -7,7%Total financial debt 12 11 -8,3%Employees (n) 163 179 +9,8%

Cosmo at a glance: 2013 – E 2014

4

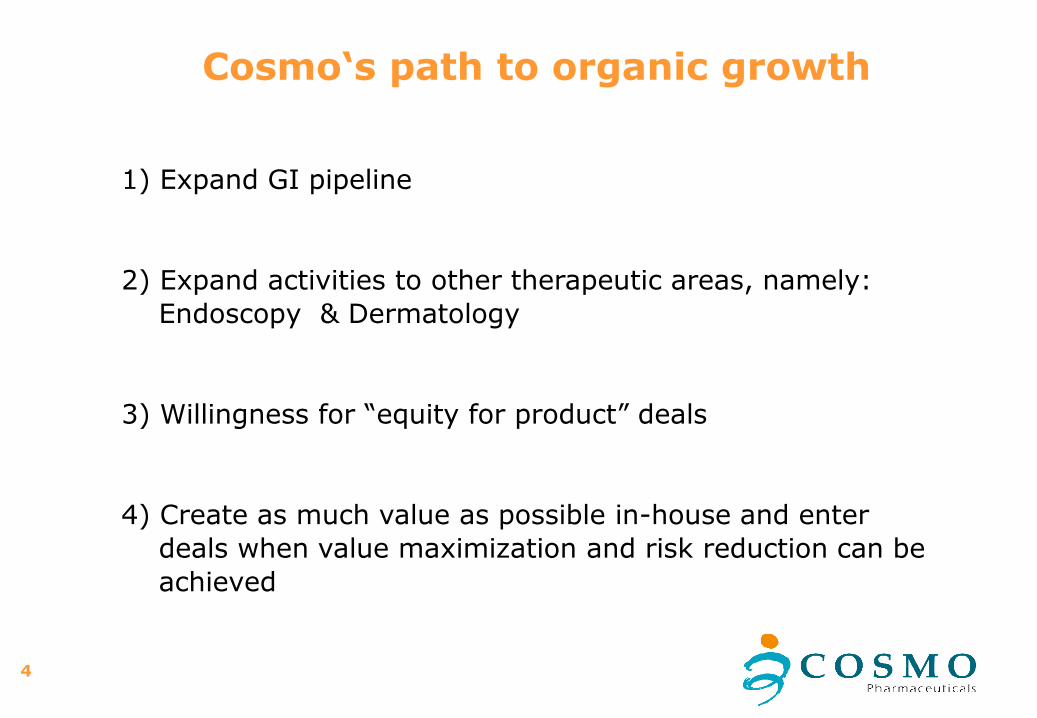

Cosmo‘s path to organic growth

1) Expand GI pipeline

2) Expand activities to other therapeutic areas, namely:

Endoscopy & Dermatology

3) Willingness for “equity for product” deals

4) Create as much value as possible in-house and enter

deals when value maximization and risk reduction can be

achieved

5

•Lialda

•Uceris

Two very successful products in the market

Launch in 2007First year Sales $ 50 m

second year sales $ 140 m 2013 year sales $ 529 m

Launch 2013First year sales $ 66 m

second year sales > $ 150 mPatent protection extended from 2020 to 2031

6

Products on the market

GI

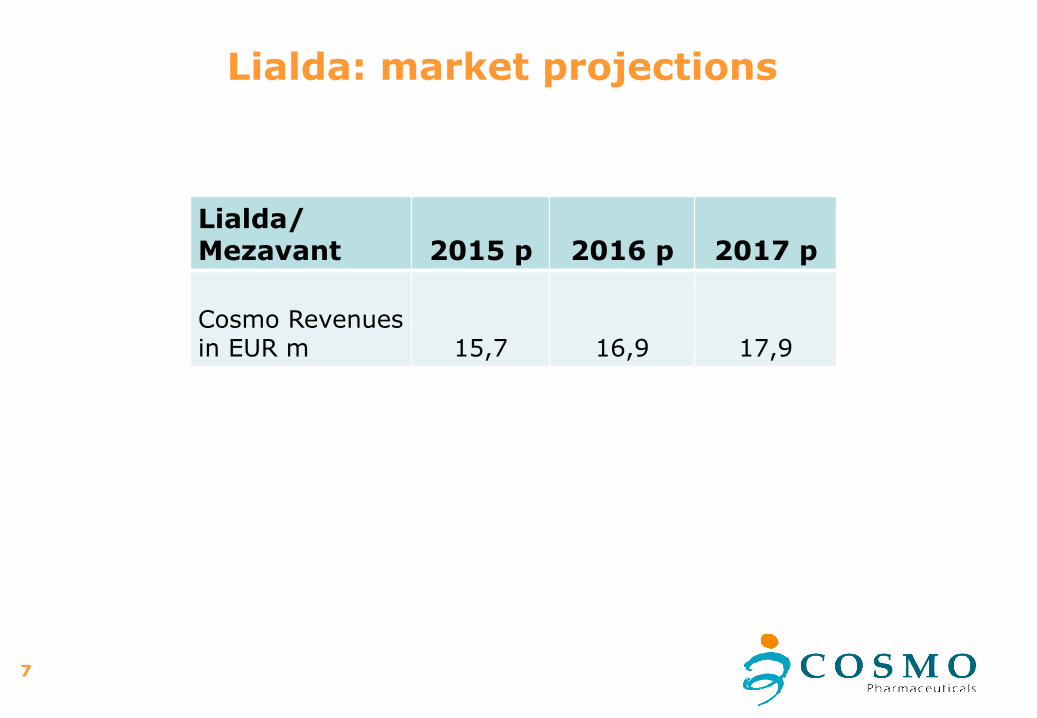

Lialda/Mezavant 2015 p 2016 p 2017 p

Cosmo Revenues in EUR m 15,7 16,9 17,9

7

Lialda: market projections

8

Lialda: litigation update

Genericising Lialda is quite challenging

• 4 par. IV litigations currently pending (first filed 2010) for counterfeiting/infringement against Zydus/Cadila, Osmotica, Mylanand Watson (now Actavis)

• Cosmo/Shire have won in first instance against Watson (now Actavis) as the Court ruled US6,773,720 patent covering Lialda as valid and the ANDA formulation in infringement. Watson appealed, the federal court amended the claim construction order, Cosmo/Shire challenged such order to the Supreme Court, the Supreme Court ordered the lower court to re-examine the order in light of the ruling in the Tevavs. Sandoz case; this will significantly extend the duration of the trial

• In the meanwhile, the 30-months stay period has expired but no ANDA filer has yet launched “at risk”, possibly because if subsequently found guilty it would be exposed to triple damages

• Furthermore Watson (now Actavis) has seen its ANDA being rejectedfor lack of bio-equivalence

9

Uceris: market projections

Uceris 2015 p 2016 p 2017 proyalties & manufacturing income in EUR m 29.9 37.4 43.9

10

Source CCFA 2014

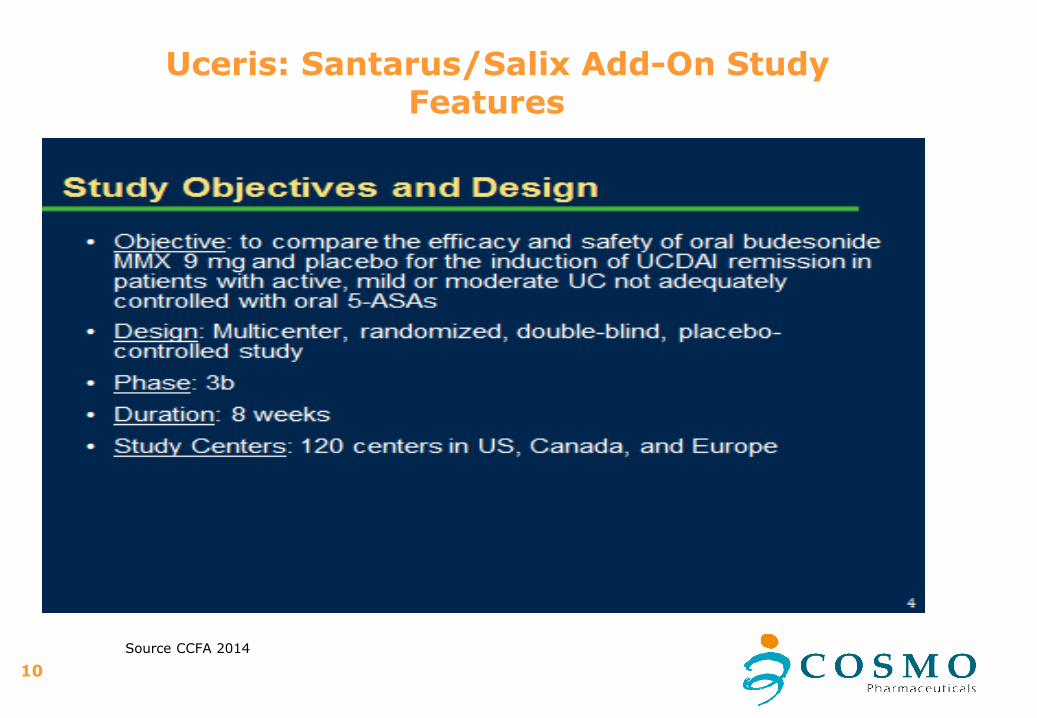

Uceris: Santarus/Salix Add-On StudyFeatures

11Source CCFA 2014

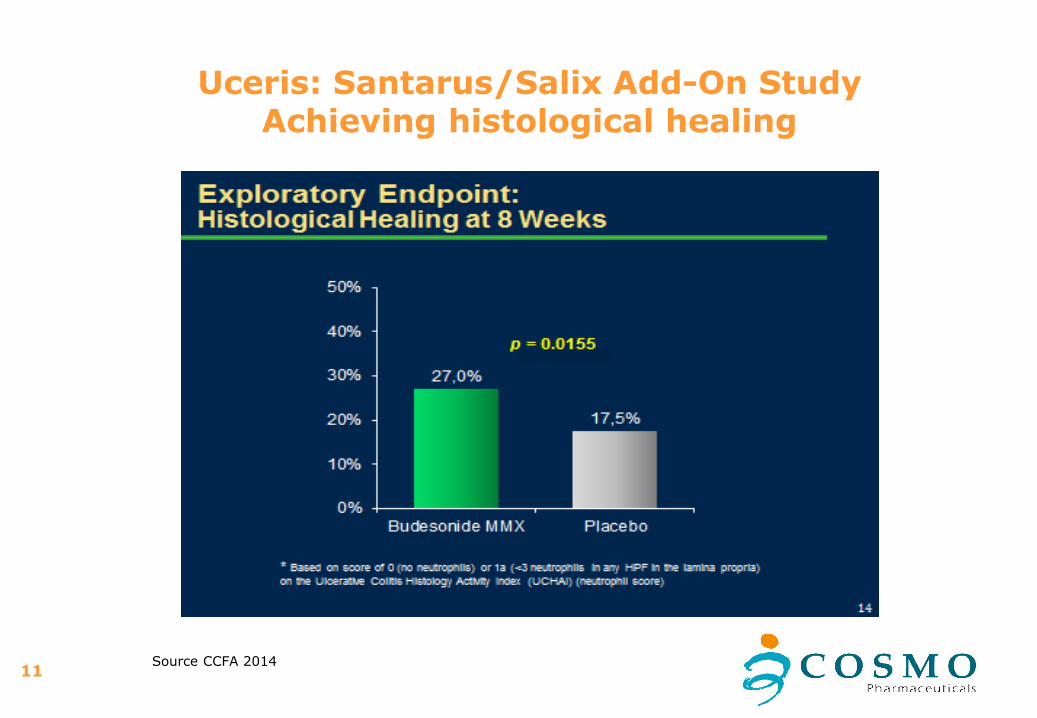

Uceris: Santarus/Salix Add-On Study Achieving histological healing

12

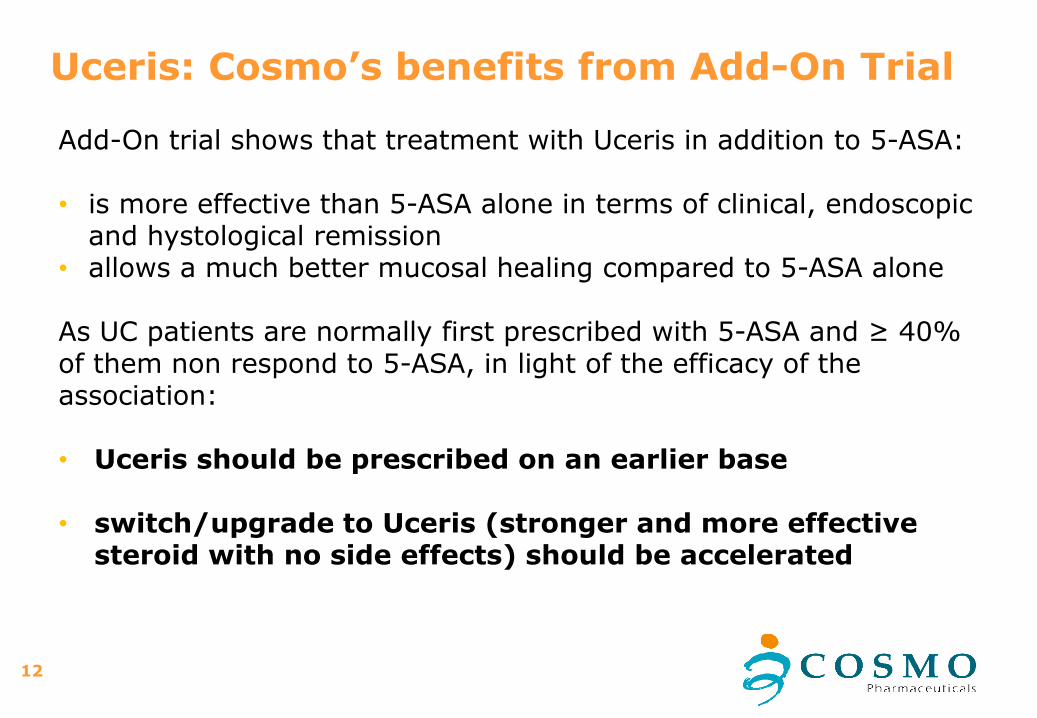

Uceris: Cosmo’s benefits from Add-On Trial

Add-On trial shows that treatment with Uceris in addition to 5-ASA:

• is more effective than 5-ASA alone in terms of clinical, endoscopicand hystological remission

• allows a much better mucosal healing compared to 5-ASA alone

As UC patients are normally first prescribed with 5-ASA and ≥ 40% of them non respond to 5-ASA, in light of the efficacy of the association:

• Uceris should be prescribed on an earlier base

• switch/upgrade to Uceris (stronger and more effectivesteroid with no side effects) should be accelerated

13

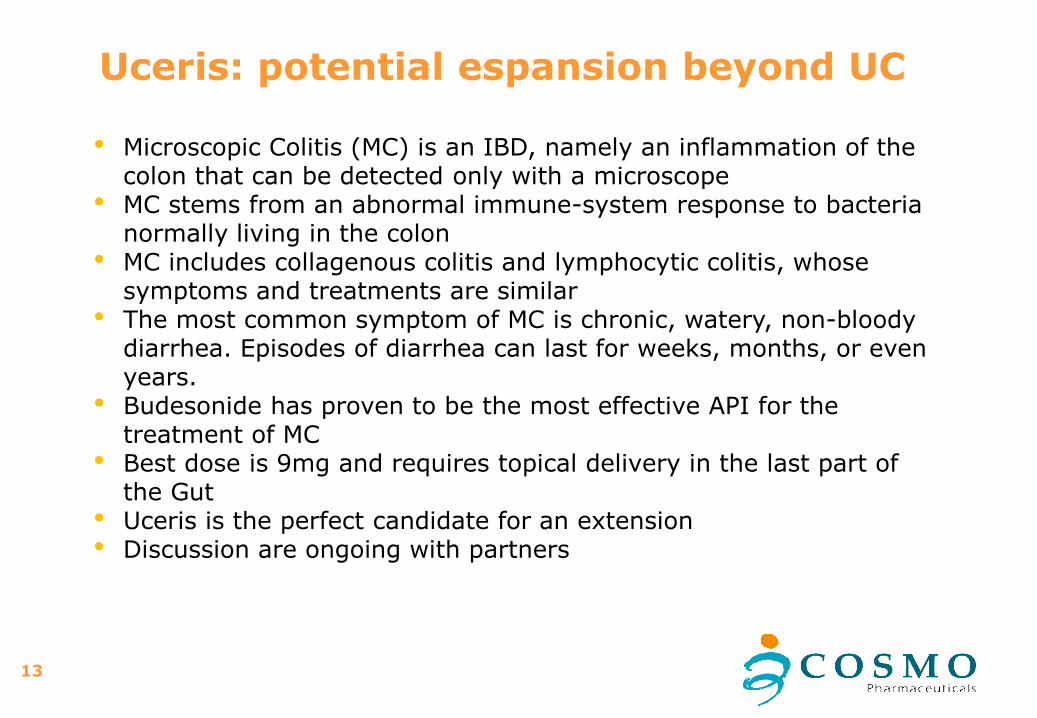

Uceris: potential espansion beyond UC

• Microscopic Colitis (MC) is an IBD, namely an inflammation of the colon that can be detected only with a microscope

• MC stems from an abnormal immune-system response to bacteria normally living in the colon

• MC includes collagenous colitis and lymphocytic colitis, whose symptoms and treatments are similar

• The most common symptom of MC is chronic, watery, non-bloody diarrhea. Episodes of diarrhea can last for weeks, months, or even years.

• Budesonide has proven to be the most effective API for the treatment of MC

• Best dose is 9mg and requires topical delivery in the last part of the Gut

• Uceris is the perfect candidate for an extension• Discussion are ongoing with partners

14

Uceris Patent Protection (2020-2031)FDA Orange Book listing

Appl No Prod No Patent NoPatentExpiration

DrugSubstanceClaim

DrugProductClaim

Patent UseCode

DelistRequested

N203634 001 7410651 Jun9,2020

Y U - 1325

N203634 001 7431943 Jun9,2020

Y

N203634 001 8293273 Jun9,2020

Y

N203634 001 8784888 Jun9,2020

Y

N203634 001 8895064 Sep7,2031

Y

N203634 001 RE43799 Jun9,2020

Y U - 1325

15

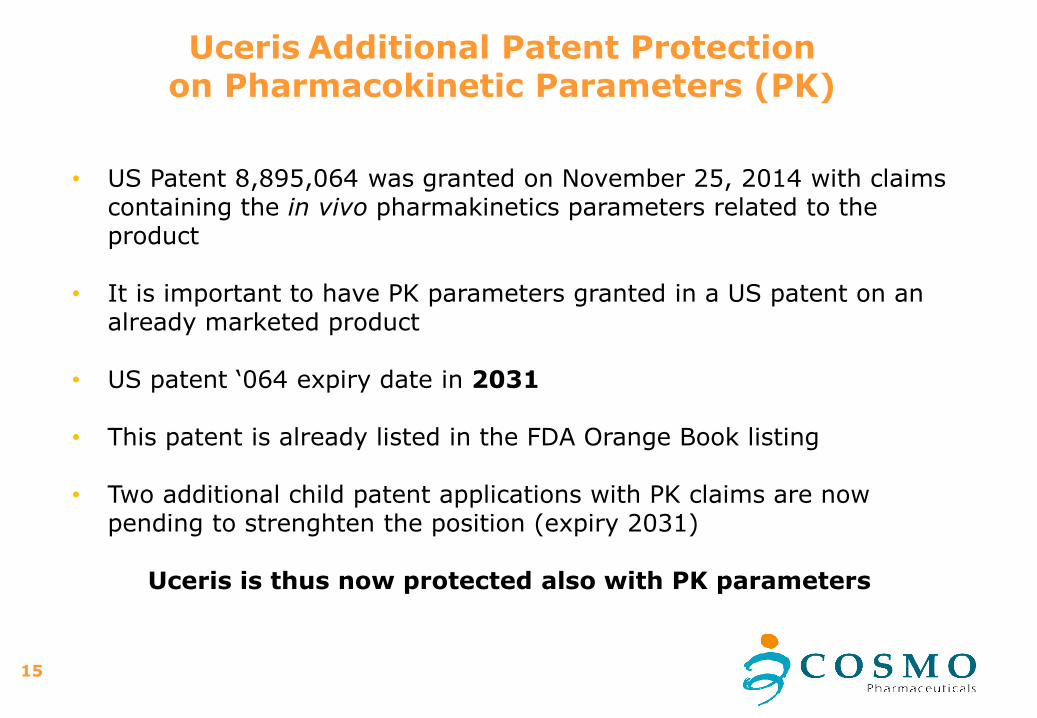

Uceris Additional Patent Protectionon Pharmacokinetic Parameters (PK)

• US Patent 8,895,064 was granted on November 25, 2014 with claimscontaining the in vivo pharmakinetics parameters related to the product

• It is important to have PK parameters granted in a US patent on an already marketed product

• US patent ‘064 expiry date in 2031

• This patent is already listed in the FDA Orange Book listing

• Two additional child patent applications with PK claims are nowpending to strenghten the position (expiry 2031)

Uceris is thus now protected also with PK parameters

16

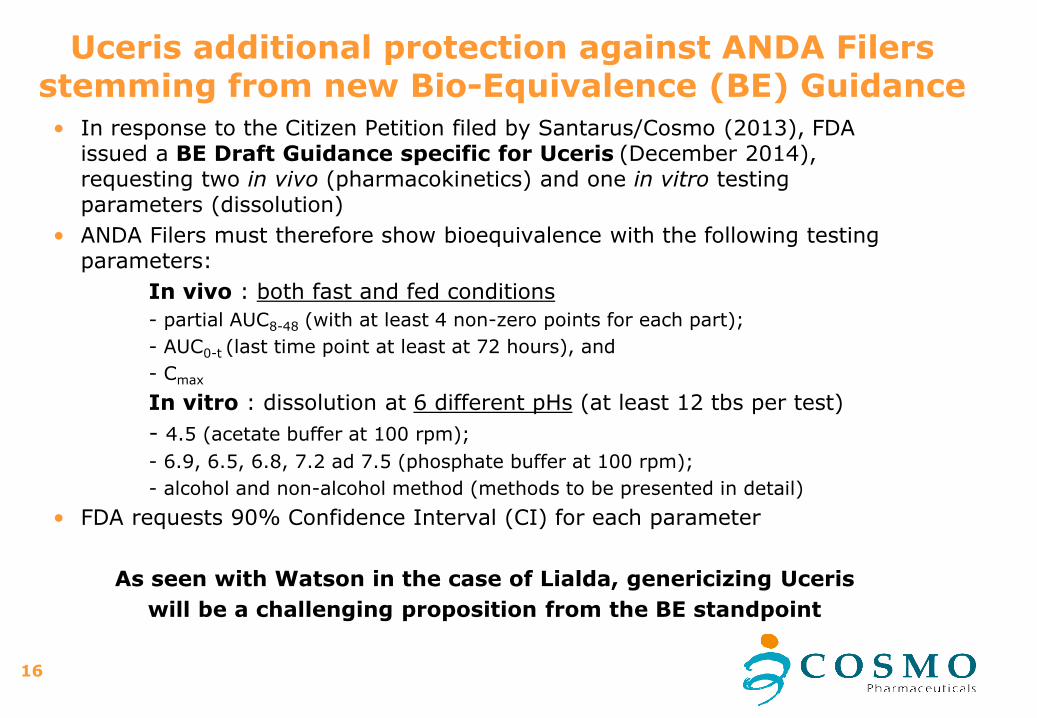

• In response to the Citizen Petition filed by Santarus/Cosmo (2013), FDA issued a BE Draft Guidance specific for Uceris (December 2014), requesting two in vivo (pharmacokinetics) and one in vitro testing parameters (dissolution)

• ANDA Filers must therefore show bioequivalence with the following testing parameters:

In vivo : both fast and fed conditions

- partial AUC8-48 (with at least 4 non-zero points for each part);

- AUC0-t (last time point at least at 72 hours), and

- Cmax

In vitro : dissolution at 6 different pHs (at least 12 tbs per test)

- 4.5 (acetate buffer at 100 rpm);

- 6.9, 6.5, 6.8, 7.2 ad 7.5 (phosphate buffer at 100 rpm);

- alcohol and non-alcohol method (methods to be presented in detail)

• FDA requests 90% Confidence Interval (CI) for each parameter

As seen with Watson in the case of Lialda, genericizing Uceris

will be a challenging proposition from the BE standpoint

Uceris additional protection against ANDA Filersstemming from new Bio-Equivalence (BE) Guidance

17

Cortiment

• Cortiment was successfully launched in The Netherlands in2013. Market dynamics (units/inhabitants) equal to US

• Approval extended in 27 EU countries with MRP concluded inOctober 2014

• Launch sequence on the basis of National approvals and ofprice optimization, starting from Q1 2015

• Product presentation at 2015 ECCO in a dedicated satellitesymposium

18

Cortiment: RoW approval path

Cortiment marketing authorization application (MAA) already submitted in :

• Australia

• Israel/Jordan/Kuwait/Lebanon

• Brazil

• South Africa

• Russia

• Mexico

Submissions in CH, Turkey, UAE, Chile, Canada to follow

Expected approvals in 2015:

• Australia

• Israel/Lebanon

• Jordan/Kuwait

• Russia

• Mexico

19

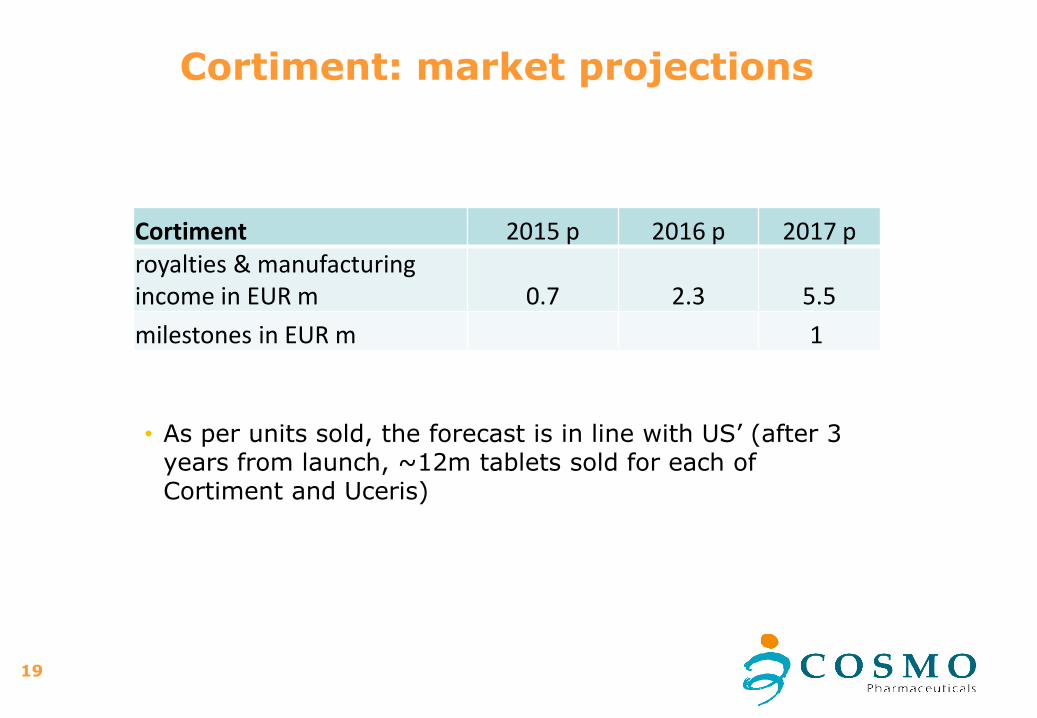

Cortiment: market projections

Cortiment 2015 p 2016 p 2017 proyalties & manufacturing income in EUR m 0.7 2.3 5.5

milestones in EUR m 1

• As per units sold, the forecast is in line with US’ (after 3 years from launch, ~12m tablets sold for each of Cortiment and Uceris)

20

• Jan-Apr: 3 weeks TV and 3 months radio advertising, highly successful

• 90’000 packs sold in the market in the ads period

• test confirmed the market need of products to regulate intestinal functions in healthy subjects

Next steps:

• classification of Zacol as a medical device (ZacolMed)

• export model in EU/US with selected commercial partners

ZACOL NMX

21

Products under development

GI Pipeline

22

GI Pipeline - Rifamycin

NCE (in US) antibiotic with negligible absorption after oral administration

and lower possibility of resistance. Candidate for 10 years exclusivity

in USA under GAIN Act

Indication currently sought: Travellers’ Diarrhoea

Clinical status:

Two pivotal clinical trials were required to support registration:

1 – US trial (superiority vs. placebo) completed successfully in LatAm

2 – EU trial (non inferiority vs. Cypro) ongoingTrial begun in India by Falk. After 800 patients, due to unexpected localregulatory issues affecting all clinical trials the trial was put on hold. Falk has now moved the trial in LatAm (Mexico, Perù, Guatemala and Ecuador)

Development Timeline: NDA filing set for 1Q 2016

23

GI Pipeline - Rifamycinsubsequent indications

Uncomplicated Diverticulitis

• Phase II managed by Falk in Germany, Italy, Hungary and Romania. • approximately 100 patients enrolled.• expansion to other two countries ongoing.

Development timeline: interim analysis by end of 2015

IBS

• New formulation containing 600mg/tablet already developed aiming atbetter patients compliance• Seeking an earlier API delivery in the small intestine and colon

Development Timeline:Phase I/II to start in 1Q 15

24

GI Pipeline - MoAb MMX

Target: to deliver MoAb topically in the intestine, in order to avoid toxicity associated with their systemic absorption and reduce immunoreactions

Potential indication: Ulcerative Colitis (maintenance of remission),as an ideal follow-up to Uceris-Cortiment/Lialda

Evidence:

• Proven preservation of chemical structure of MoAb in MMX tabletsand functional activity maintained in colonic environment

• Successful efficacy model in mice

• Infliximab Bio-better under scale up process

• Phase I/II trial planned to start in 2015

25

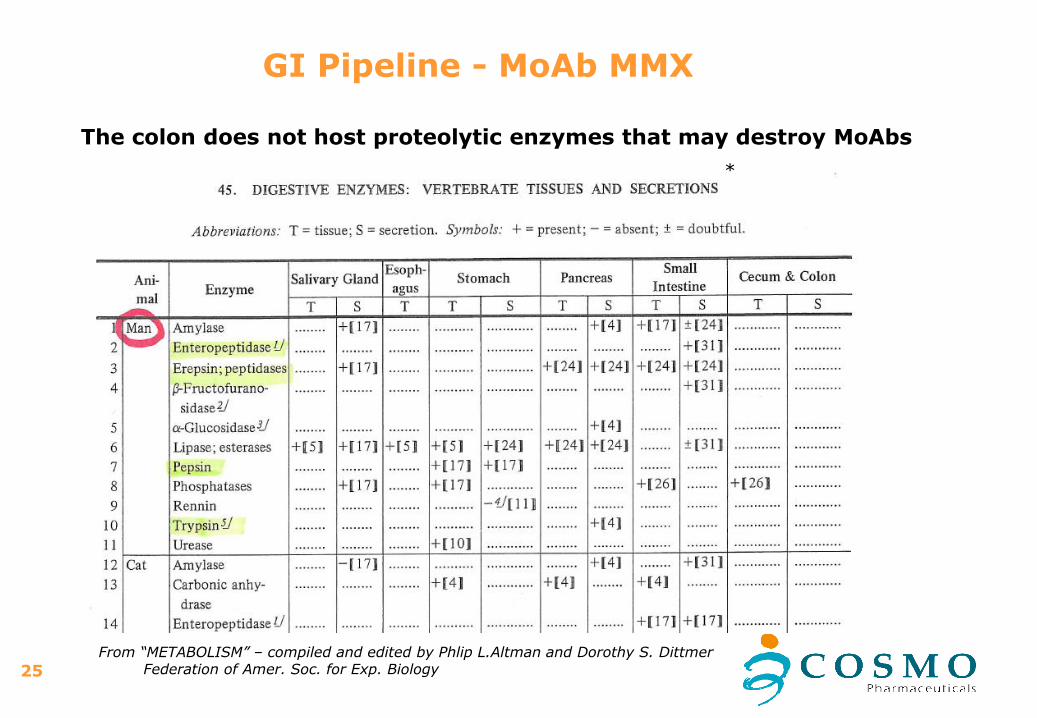

GI Pipeline - MoAb MMX

*

From “METABOLISM” – compiled and edited by Phlip L.Altman and Dorothy S. DittmerFederation of Amer. Soc. for Exp. Biology

The colon does not host proteolytic enzymes that may destroy MoAbs

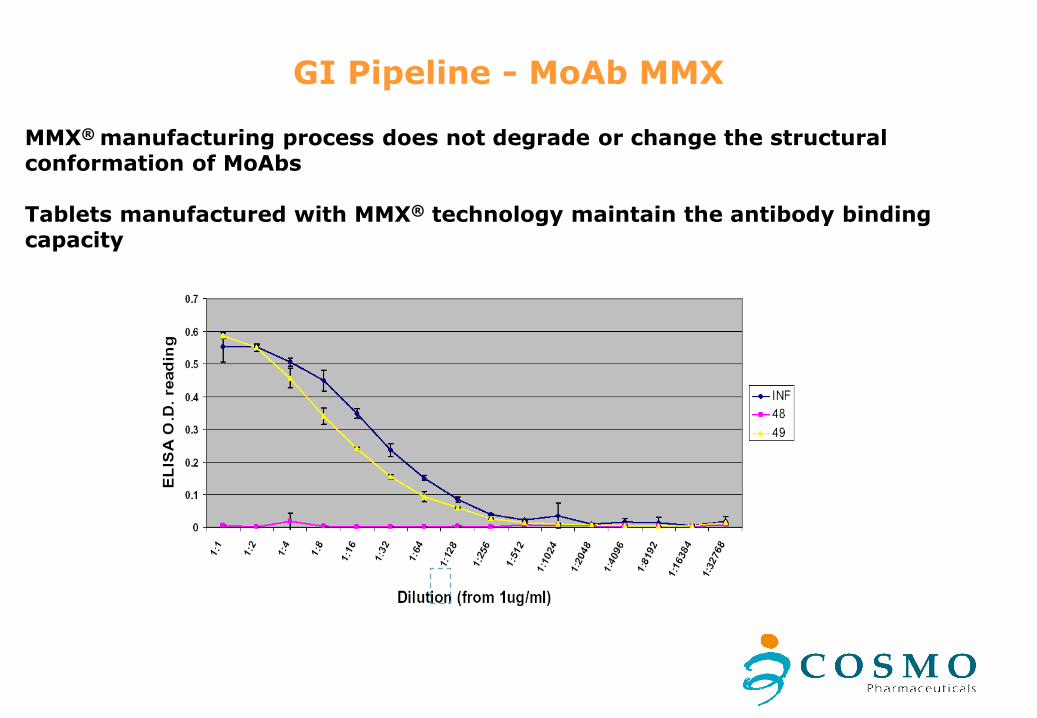

GI Pipeline - MoAb MMX

MMX® manufacturing process does not degrade or change the structural conformation of MoAbs

Tablets manufactured with MMX® technology maintain the antibody binding capacity

LNCaP TNFa-induced cell death inhibited by anti-TNFa

0,E+00

2,E+04

4,E+04

6,E+04

8,E+04

1,E+05

1,E+05

1,E+05

2,E+05

2,E+05

2,E+05

0,01 0,10 1,00 10,00 100,00

Molar Excess Antibody over TNFa

Re

lati

ve

Ce

ll N

um

be

r

MMX-48MMX-49

Inflixno TNF

z

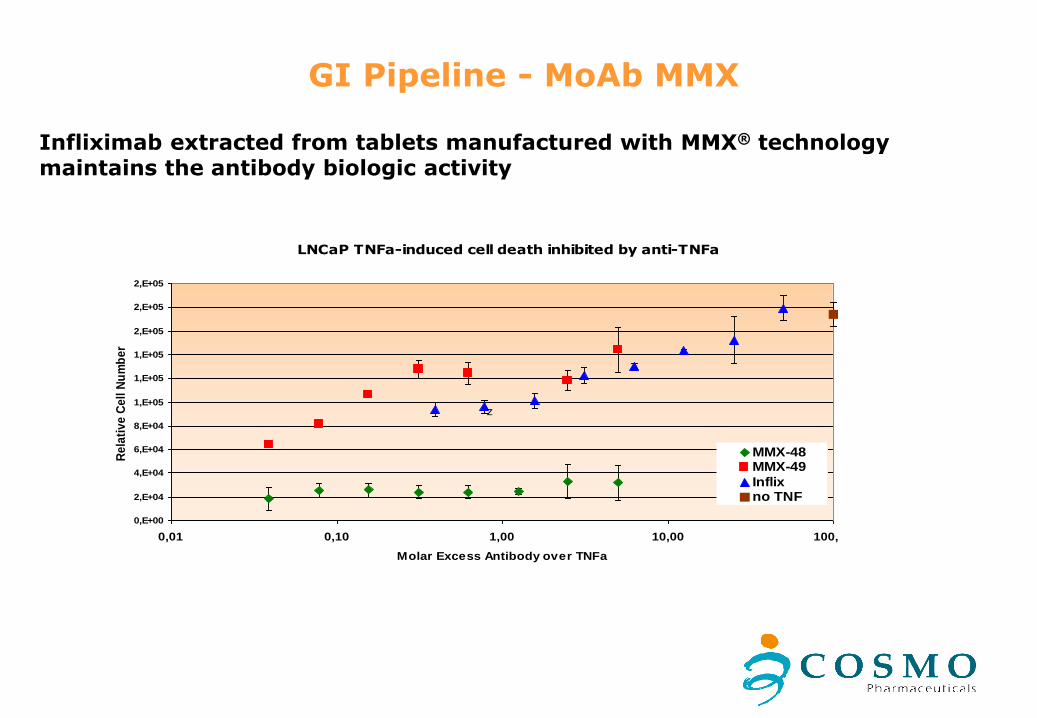

GI Pipeline - MoAb MMX

Infliximab extracted from tablets manufactured with MMX® technology maintains the antibody biologic activity

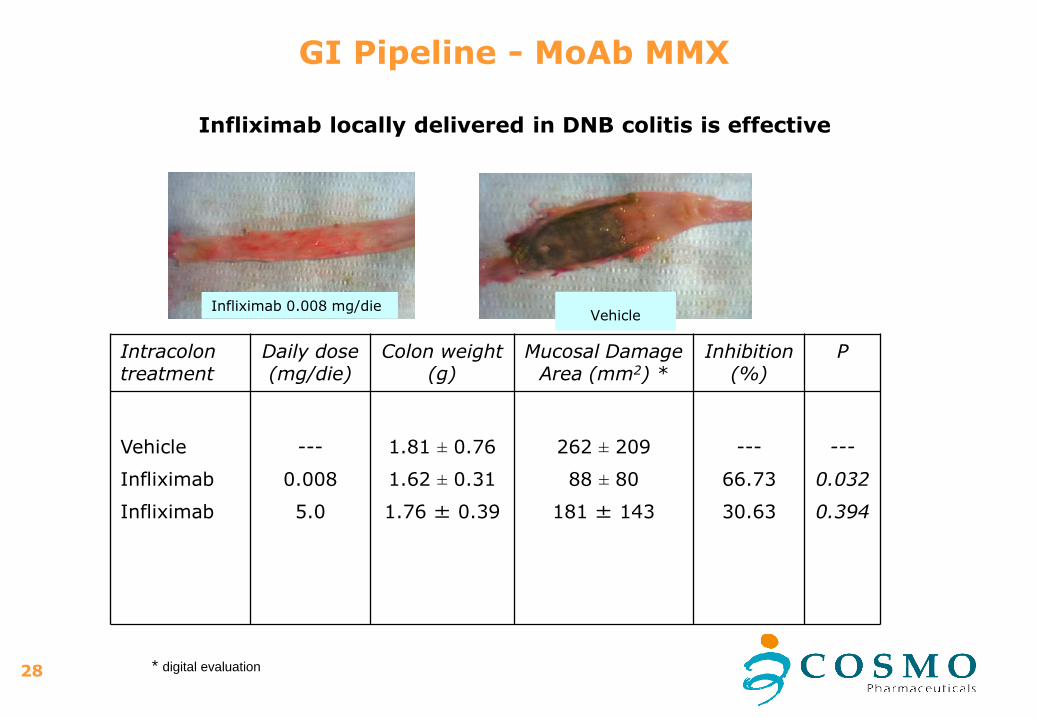

28

Intracolontreatment

Daily dose(mg/die)

Colon weight(g)

Mucosal DamageArea (mm2) *

Inhibition(%)

P

Vehicle

Infliximab

Infliximab

---

0.008

5.0

1.81 ± 0.76

1.62 ± 0.31

1.76 ± 0.39

262 ± 209

88 ± 80

181 ± 143

---

66.73

30.63

---

0.032

0.394

* digital evaluation

GI Pipeline - MoAb MMX

Infliximab 0.008 mg/dieVehicle

Infliximab locally delivered in DNB colitis is effective

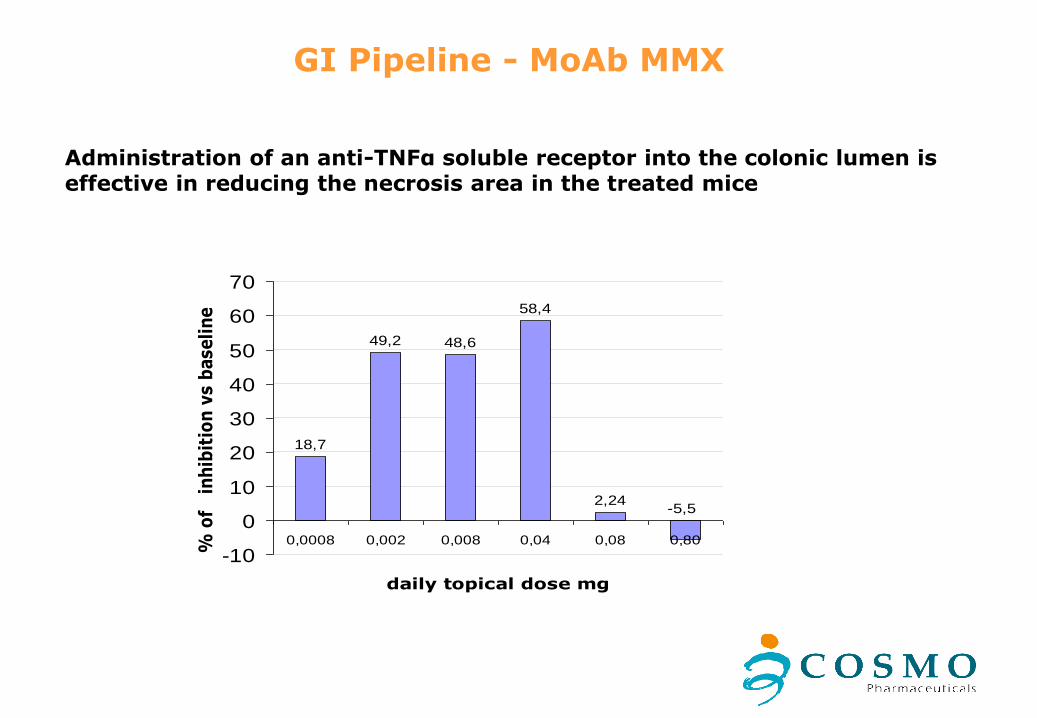

Administration of an anti-TNFα soluble receptor into the colonic lumen is effective in reducing the necrosis area in the treated mice

18,7

49,2 48,6

58,4

2,24-5,5

-10

0

10

20

30

40

50

60

70

0,0008 0,002 0,008 0,04 0,08 0,80

daily topical dose mg

% o

f

inh

ibit

ion

vs b

aseli

ne

GI Pipeline - MoAb MMX

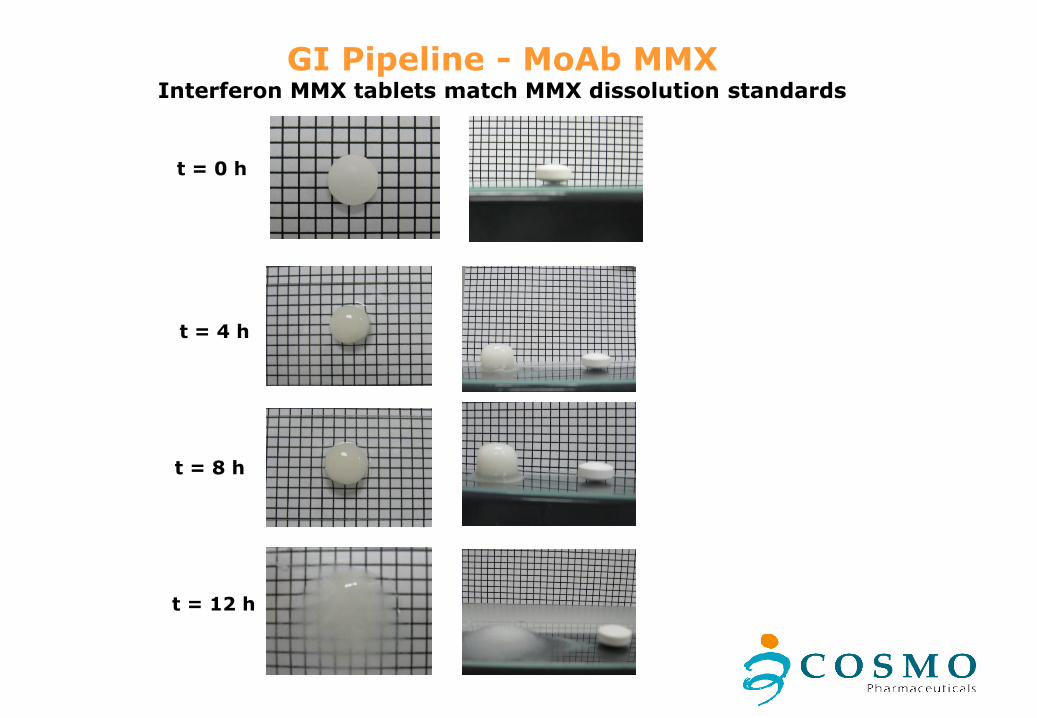

GI Pipeline - MoAb MMXInterferon MMX tablets match MMX dissolution standards

t = 0 h

t = 4 h

t = 8 h

t = 12 h

GI Pipeline - MoAb MMX

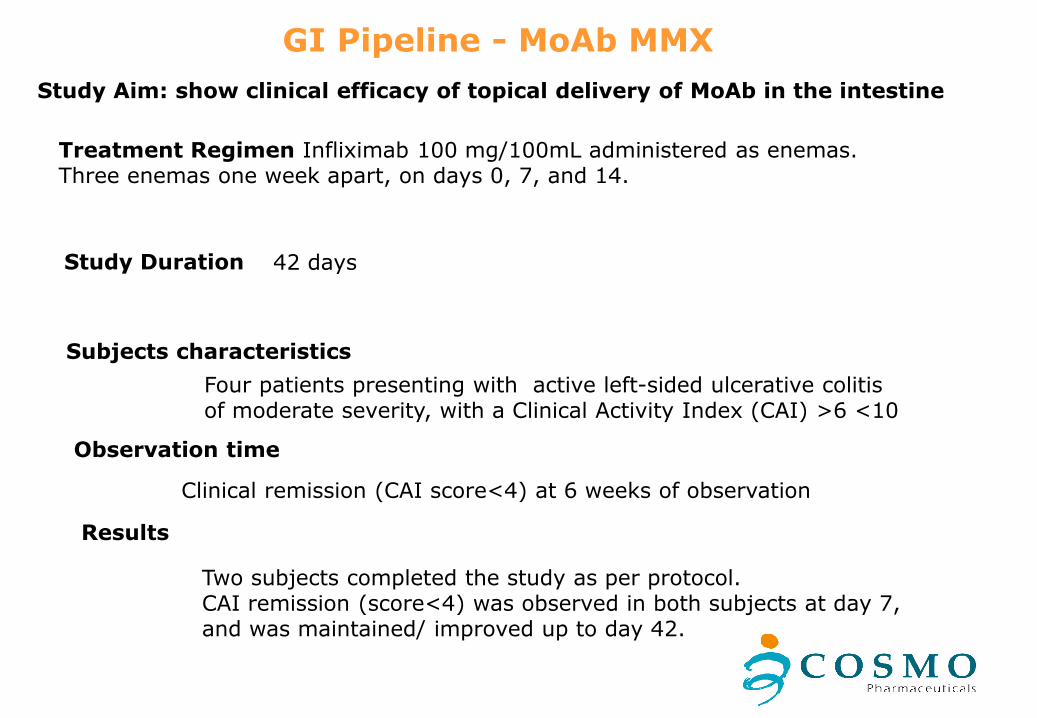

Treatment Regimen Infliximab 100 mg/100mL administered as enemas.Three enemas one week apart, on days 0, 7, and 14.

Study Duration 42 days

Subjects characteristics

Four patients presenting with active left-sided ulcerative colitisof moderate severity, with a Clinical Activity Index (CAI) >6 <10

Observation time

Results

Two subjects completed the study as per protocol.CAI remission (score<4) was observed in both subjects at day 7,and was maintained/ improved up to day 42.

Clinical remission (CAI score<4) at 6 weeks of observation

Study Aim: show clinical efficacy of topical delivery of MoAb in the intestine

GI Pipeline - MoAb MMX

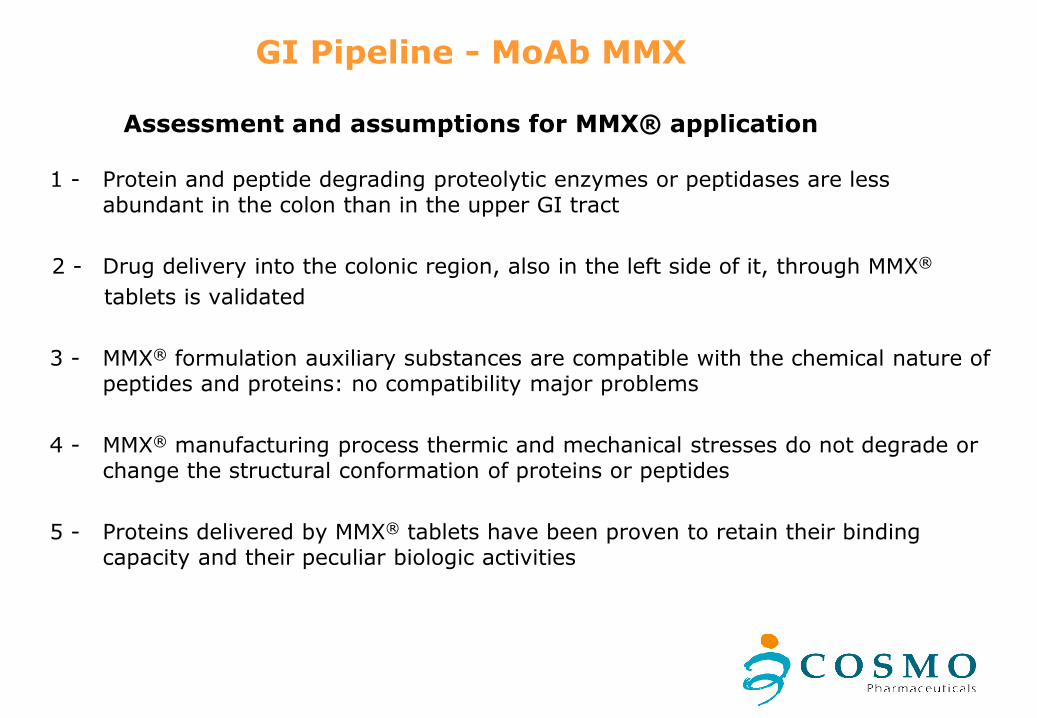

Assessment and assumptions for MMX® application

1 - Protein and peptide degrading proteolytic enzymes or peptidases are less abundant in the colon than in the upper GI tract

2 - Drug delivery into the colonic region, also in the left side of it, through MMX®

tablets is validated

3 - MMX® formulation auxiliary substances are compatible with the chemical nature of peptides and proteins: no compatibility major problems

4 - MMX® manufacturing process thermic and mechanical stresses do not degrade or change the structural conformation of proteins or peptides

5 - Proteins delivered by MMX® tablets have been proven to retain their binding capacity and their peculiar biologic activities

33

GI Pipeline - MoAb MMX

Development timeline:

• Formulation and analytical development ongoing with model APIs

• Generation by AIMM of a series of stable Remicade bio-better clones

• AIMM bio-better with physico-chemical and biological properties similar to Remicade (before and after lyophilization)

• Selected clone has been transferred to a protein mfrg company for large scale production

• Batches available for MMX manufacturing by end of Q2 2015

34

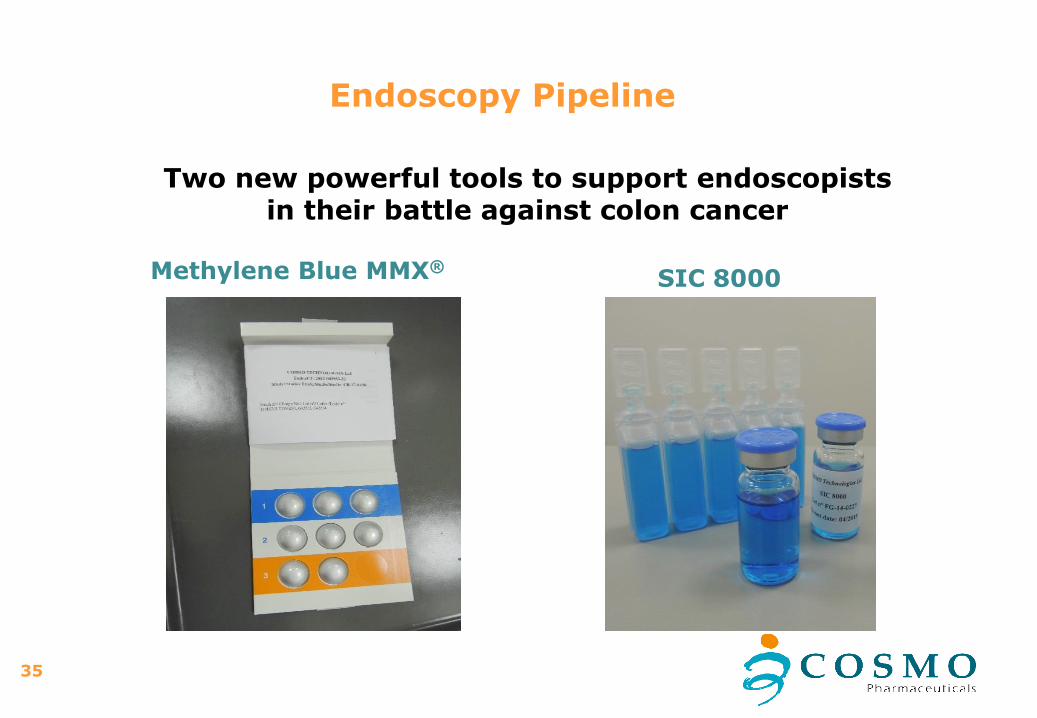

Products under development

Endoscopy Pipeline

35

Endoscopy Pipeline

Two new powerful tools to support endoscopistsin their battle against colon cancer

Methylene Blue MMX®SIC 8000

36

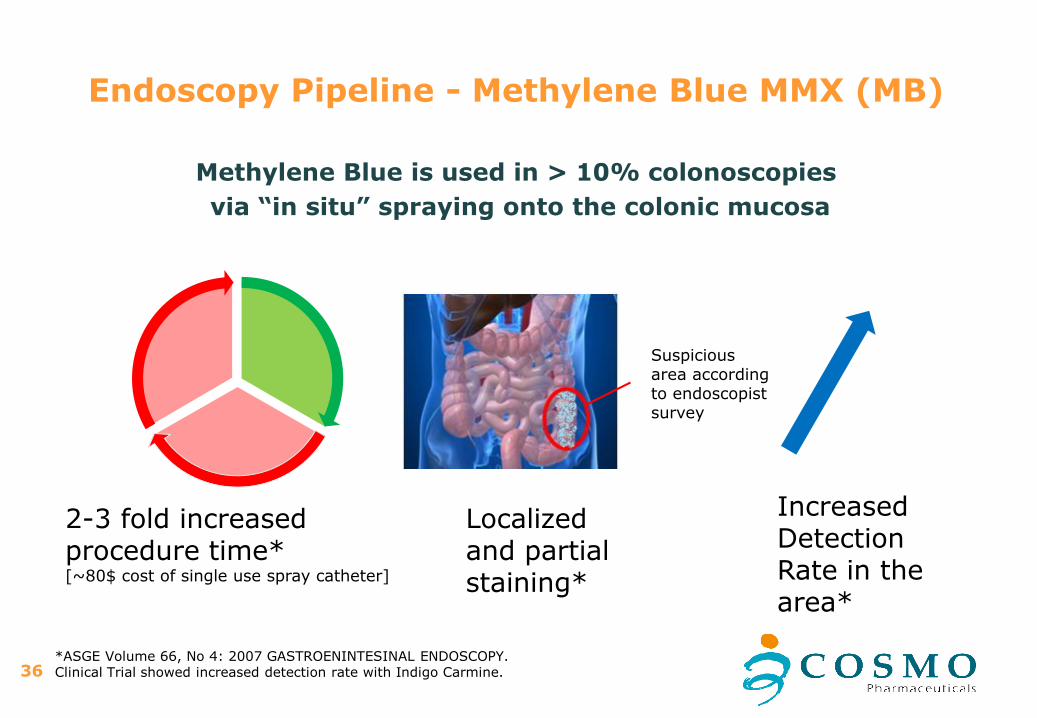

Endoscopy Pipeline - Methylene Blue MMX (MB)

Methylene Blue is used in > 10% colonoscopies

via “in situ” spraying onto the colonic mucosa

*ASGE Volume 66, No 4: 2007 GASTROENINTESINAL ENDOSCOPY. Clinical Trial showed increased detection rate with Indigo Carmine.

2-3 fold increased procedure time*[~80$ cost of single use spray catheter]

Localized and partial staining*

Suspicious area according to endoscopistsurvey

Increased Detection Rate in the area*

37

38

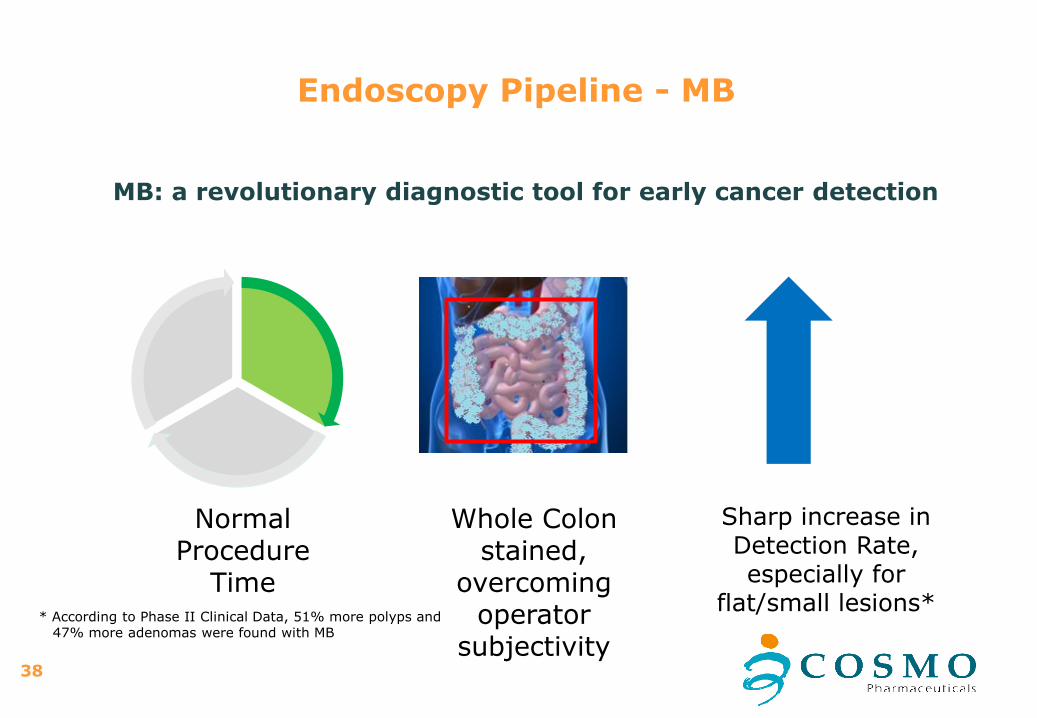

Endoscopy Pipeline - MB

MB: a revolutionary diagnostic tool for early cancer detection

* According to Phase II Clinical Data, 51% more polyps and47% more adenomas were found with MB

Normal Procedure

Time

Whole Colon stained,

overcoming operator

subjectivity

Sharp increase in Detection Rate, especially for

flat/small lesions*

39

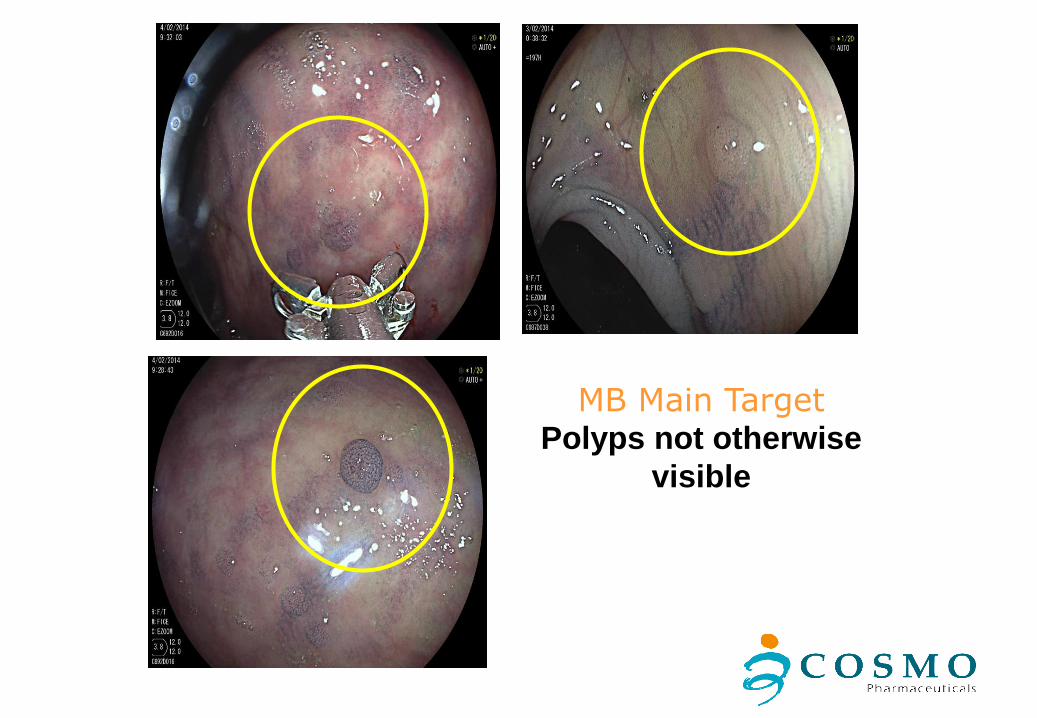

MB Main TargetPolyps not otherwise

visible

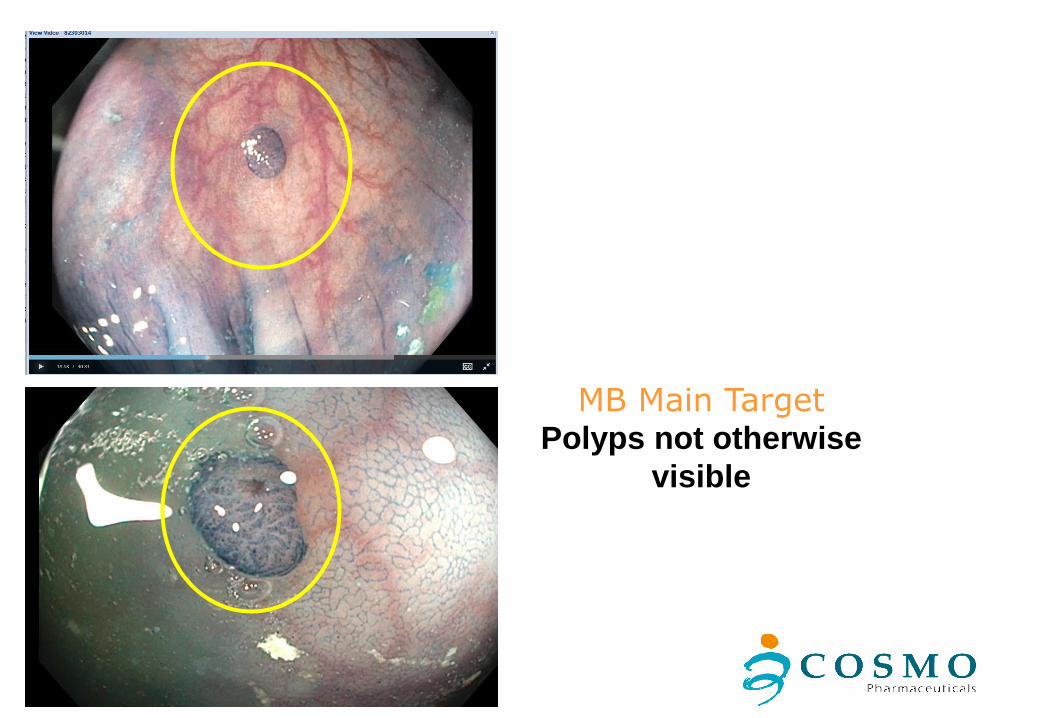

MB Main TargetPolyps not otherwise

visible

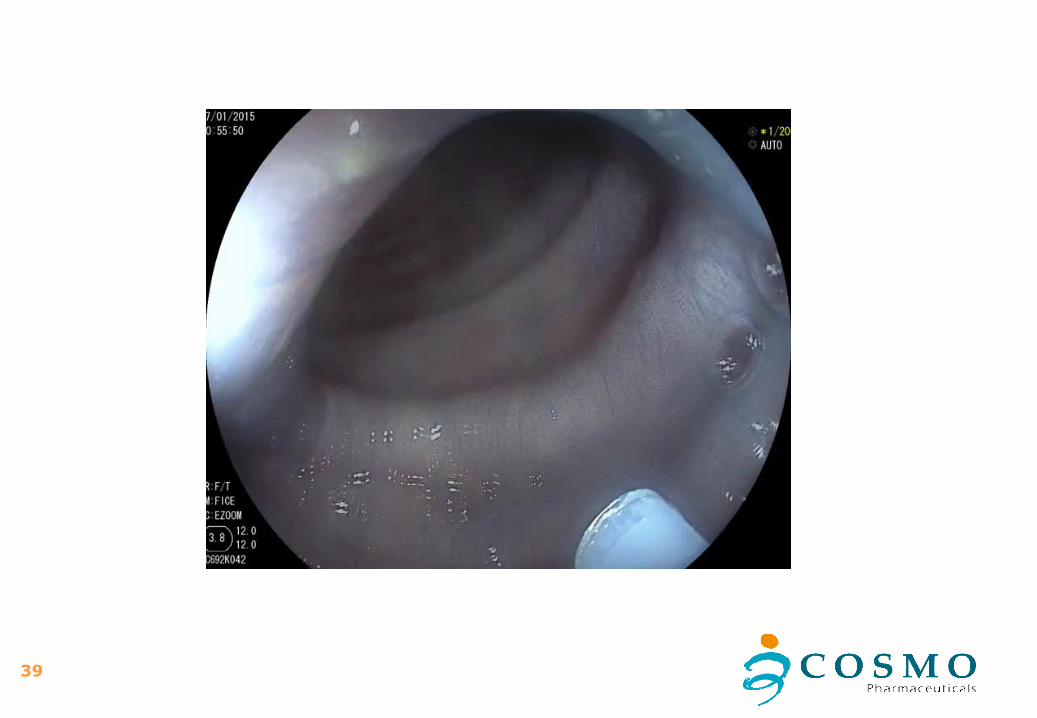

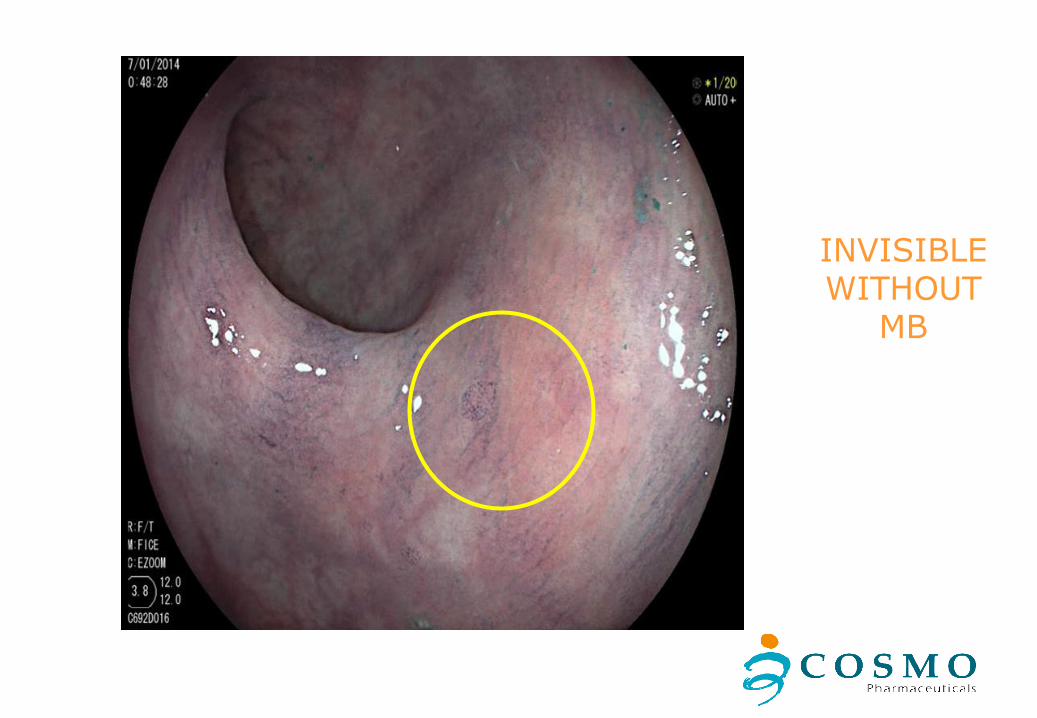

INVISIBLE WITHOUT

MB

43

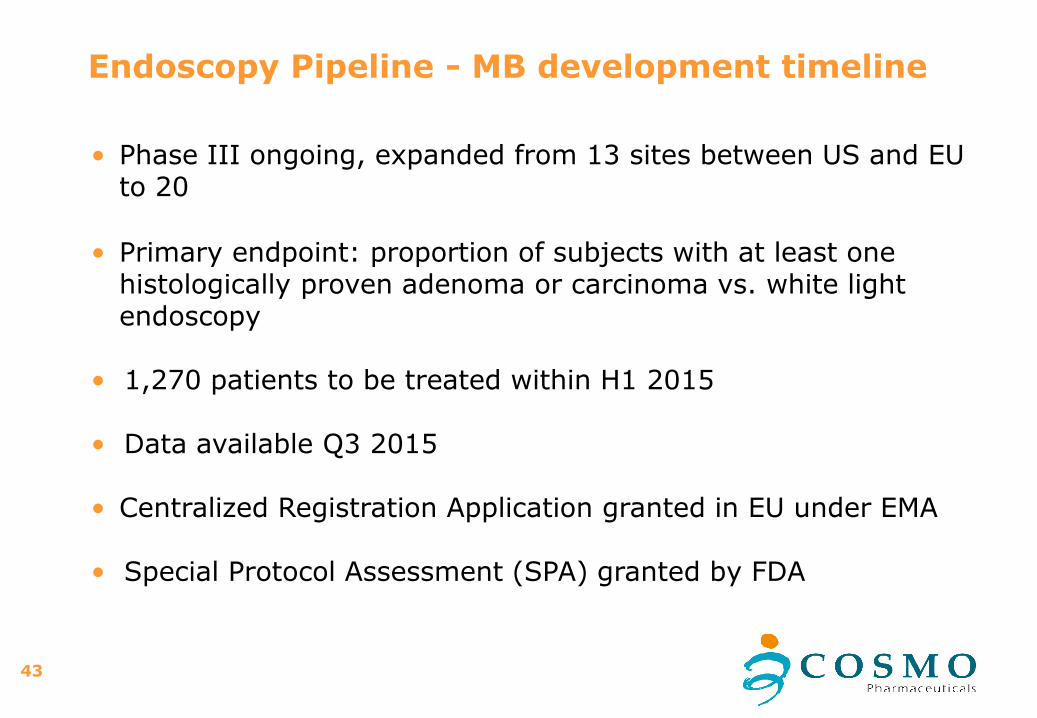

Endoscopy Pipeline - MB development timeline

• Phase III ongoing, expanded from 13 sites between US and EU to 20

• Primary endpoint: proportion of subjects with at least one histologically proven adenoma or carcinoma vs. white light endoscopy

• 1,270 patients to be treated within H1 2015

• Data available Q3 2015

• Centralized Registration Application granted in EU under EMA

• Special Protocol Assessment (SPA) granted by FDA

44

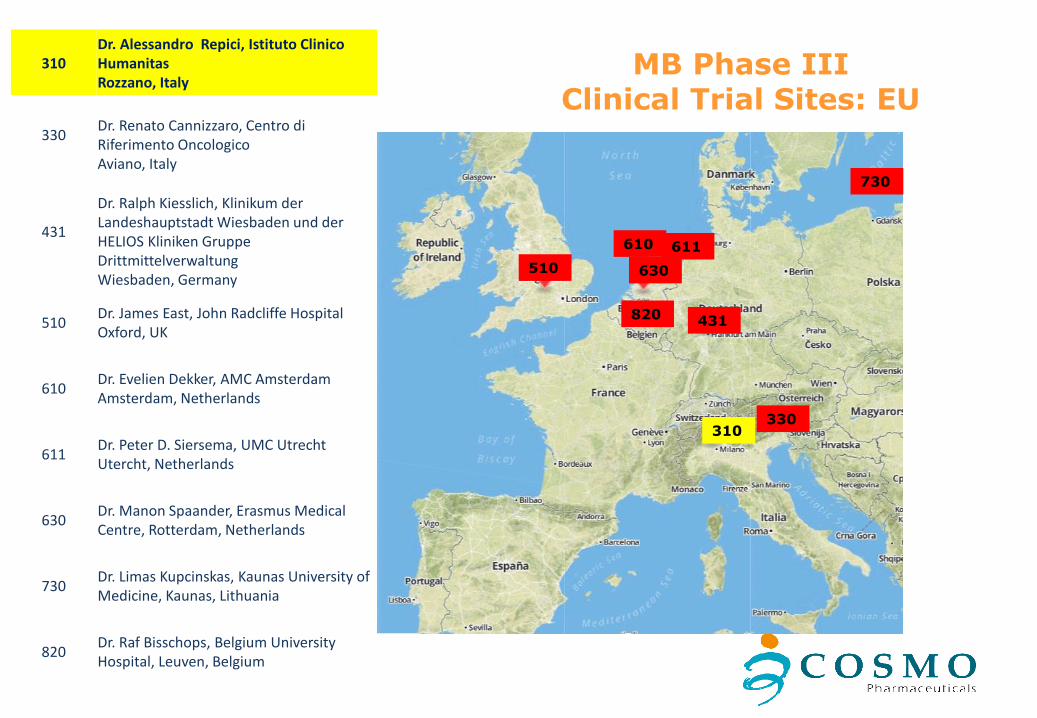

MB Phase IIIClinical Trial Sites: EU

510 630

610

431

310

310Dr. Alessandro Repici, Istituto ClinicoHumanitasRozzano, Italy

330Dr. Renato Cannizzaro, Centro di Riferimento Oncologico Aviano, Italy

431

Dr. Ralph Kiesslich, Klinikum der Landeshauptstadt Wiesbaden und der HELIOS Kliniken GruppeDrittmittelverwaltungWiesbaden, Germany

510Dr. James East, John Radcliffe HospitalOxford, UK

610Dr. Evelien Dekker, AMC Amsterdam Amsterdam, Netherlands

611Dr. Peter D. Siersema, UMC Utrecht Utercht, Netherlands

630Dr. Manon Spaander, Erasmus Medical Centre, Rotterdam, Netherlands

730Dr. Limas Kupcinskas, Kaunas University of Medicine, Kaunas, Lithuania

820Dr. Raf Bisschops, Belgium University Hospital, Leuven, Belgium

611

820

730

330

45

MB Phase IIIClinical Trial Sites:

North America

110

131

130

111

132

230

130Dr. Michael WallaceMayo Clinic Jacksonville, FL

131Dr. Prateek SharmaUniversity of Kansas School of Medicine, Kansas City, MO

110Dr. Francisco RamirezMayo Clinic, Scottsdale, AZ

111Prof David BruiningMayo Clinic, Rochester, MN

114Dr David Gatof, Clinical Research of the RockiesLafayette, CO

132Dr. Marcia (Mimi) CantoJ Hopkins, Baltimore, MD

230Dr. Norman Marcon, St. Michael's HospitalToronto, Canada

112

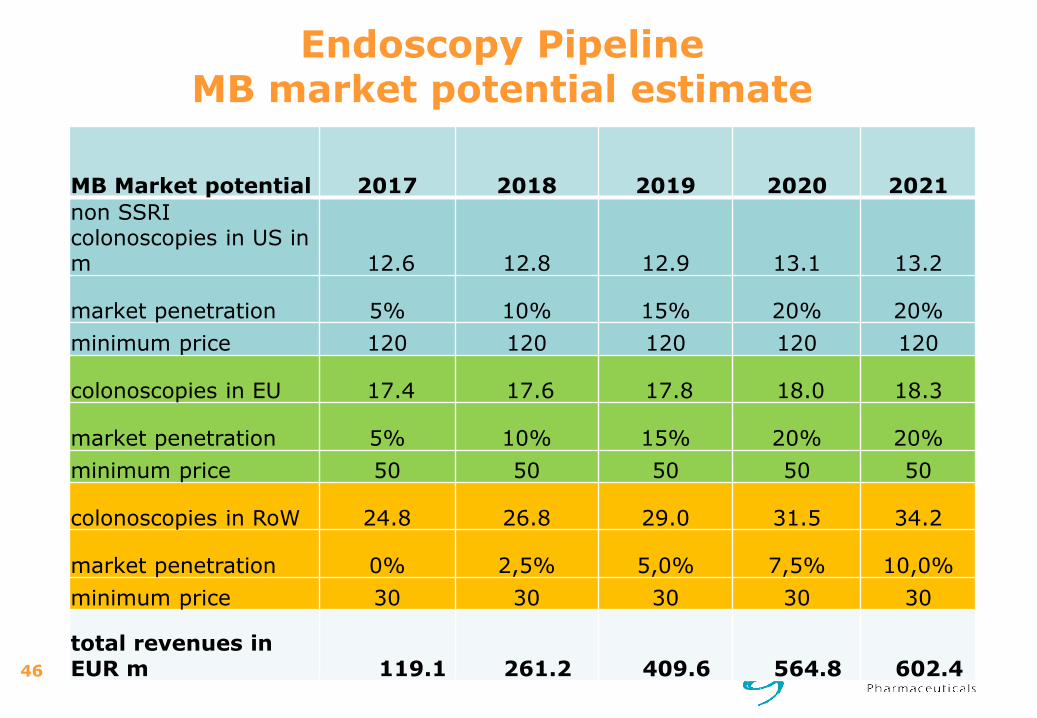

MB Market potential 2017 2018 2019 2020 2021

non SSRI colonoscopies in US in m 12.6 12.8 12.9 13.1 13.2

market penetration 5% 10% 15% 20% 20%

minimum price 120 120 120 120 120

colonoscopies in EU 17.4 17.6 17.8 18.0 18.3

market penetration 5% 10% 15% 20% 20%

minimum price 50 50 50 50 50

colonoscopies in RoW 24.8 26.8 29.0 31.5 34.2

market penetration 0% 2,5% 5,0% 7,5% 10,0%

minimum price 30 30 30 30 30

total revenues in EUR m 119.1 261.2 409.6 564.8 602.4 46

Endoscopy PipelineMB market potential estimate

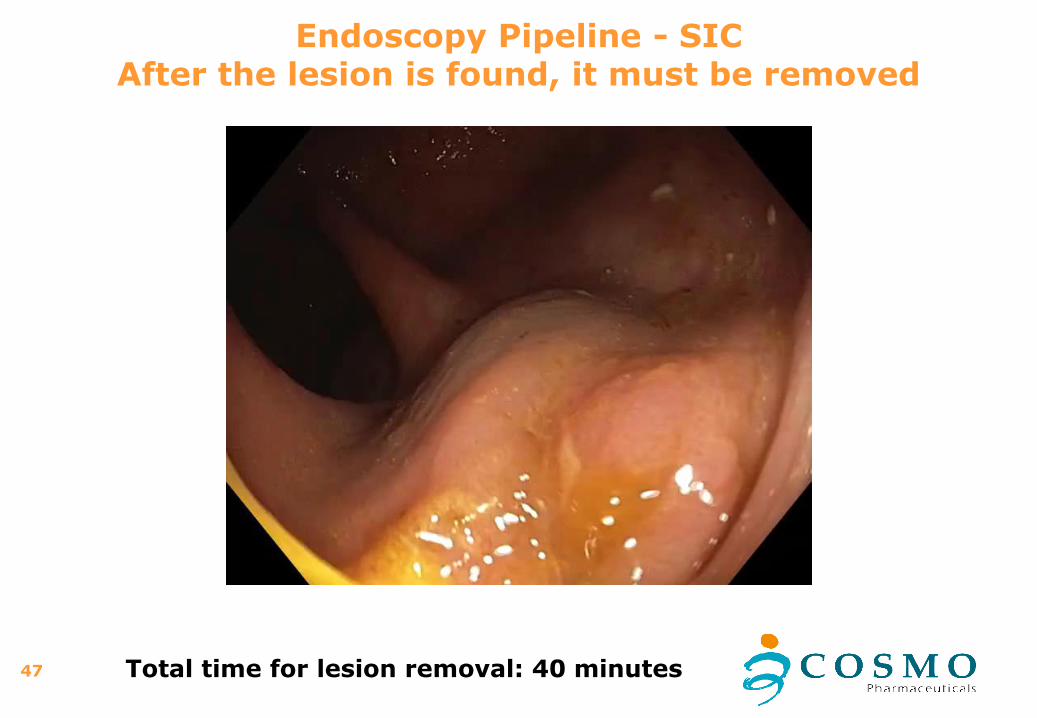

Endoscopy Pipeline - SICAfter the lesion is found, it must be removed

47 Total time for lesion removal: 40 minutes

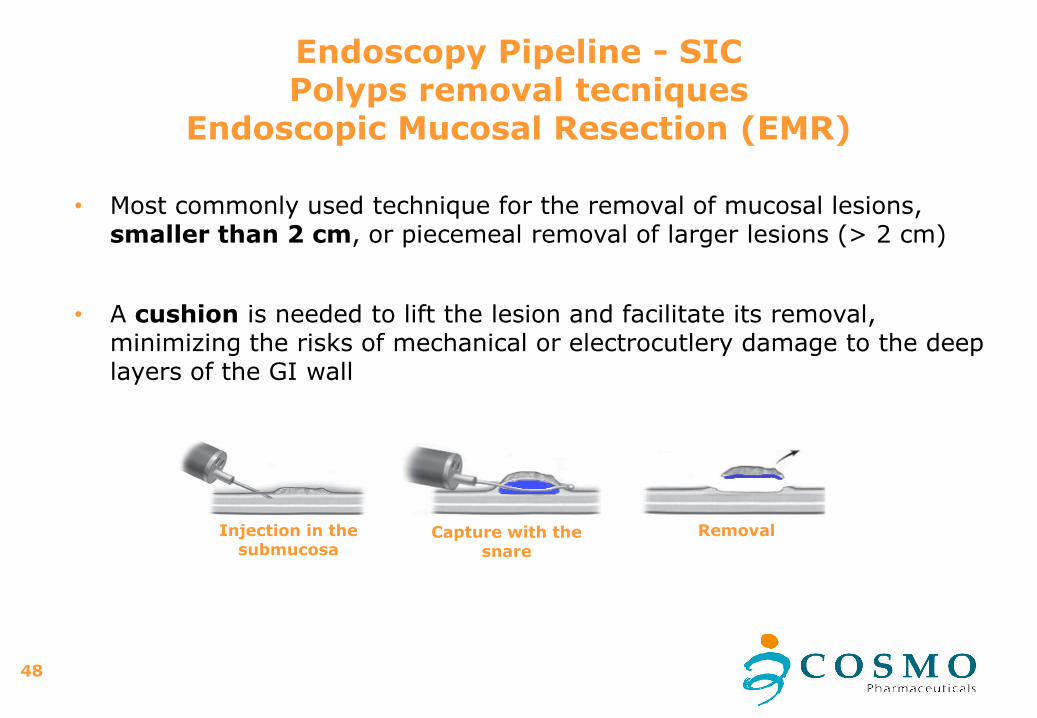

Endoscopy Pipeline - SICPolyps removal tecniques

Endoscopic Mucosal Resection (EMR)

48

• Most commonly used technique for the removal of mucosal lesions, smaller than 2 cm, or piecemeal removal of larger lesions (> 2 cm)

• A cushion is needed to lift the lesion and facilitate its removal, minimizing the risks of mechanical or electrocutlery damage to the deep layers of the GI wall

Injection in the submucosa

Capture with the snare

Removal

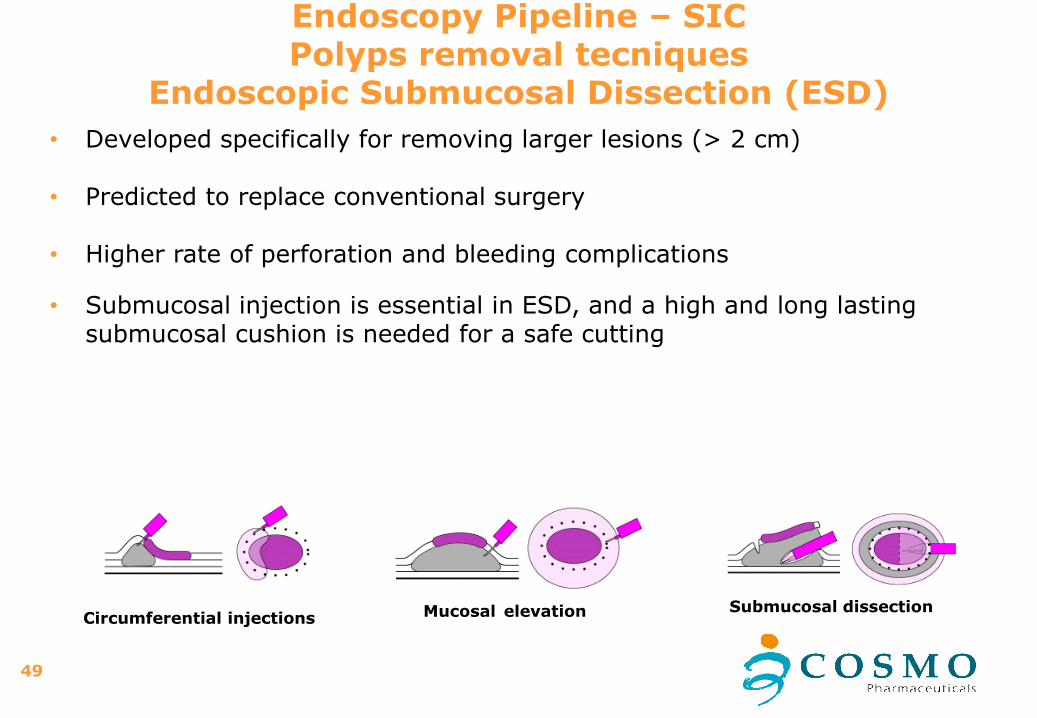

Endoscopy Pipeline – SICPolyps removal tecniques

Endoscopic Submucosal Dissection (ESD)

49

Circumferential injections Mucosal elevation Submucosal dissection

• Developed specifically for removing larger lesions (> 2 cm)

• Predicted to replace conventional surgery

• Higher rate of perforation and bleeding complications

• Submucosal injection is essential in ESD, and a high and long lasting submucosal cushion is needed for a safe cutting

Endoscopy Pipeline - SIC

50

• To avoid risk of perforation, particularly for flat polyps, endoscopists needto create a ’’safety cushion‘‘ between the lesion and the deep layers of the GI wall

• Current procedures foresee the injection of normal saline solution, which is easy to inject but dissipates quickly

• Longer lasting cushions are obtained with expensive Hyaluronic Acid solutions or self made cocktails

• Strong need to obtain similar long lasting effect with alternative solutions: ideal product should:

• have low viscosity to facilitate injection• Provide a long lasting cushion (> 30 min)• Include a dye to enhance borders definition• be safe and bio-compatible• Affordable in terms of pricing

51

• SIC 8000 (SIC) is a Submucosal Injectable Composition, easy to be injected, developed to be used in endoscopic resection procedures in the GI tract

• SIC creates a long lasting cushion which is essential for a successful Endoscopic Mucosal Resection (EMR) or Endoscopic SubmucosalDissection (ESD)

• SIC is dyed with methylene blue, so it helps in visualizing the lesion and performing the resection procedure, minimizing risk of perforation

• SIC is covered by two international and one US patent applications filed in 2014 (priority 2013)

Endoscopy Pipeline - SIC

Endoscopy Pipeline - SICSIC satisfies an unmet need

52

• No products for this indication currently available in the US market

• Most commonly used submucosal injectable solution is normal saline, but several injections needed to maintain the cushion

• Hyaluronic acid solutions are known to be long lasting, but expensive Sigmavisc® in EU costs 50€ for 5 ml, Muco-up® in Japan costs 55€ for 5 ml

• Other patented compositions not on US market for impracticality

• Easy to use: no additional or customized devices (such as syringe pumps or other pumps) needed to administer SIC 8000

No currently used solutions meet medical needsin endoscopic practice

53

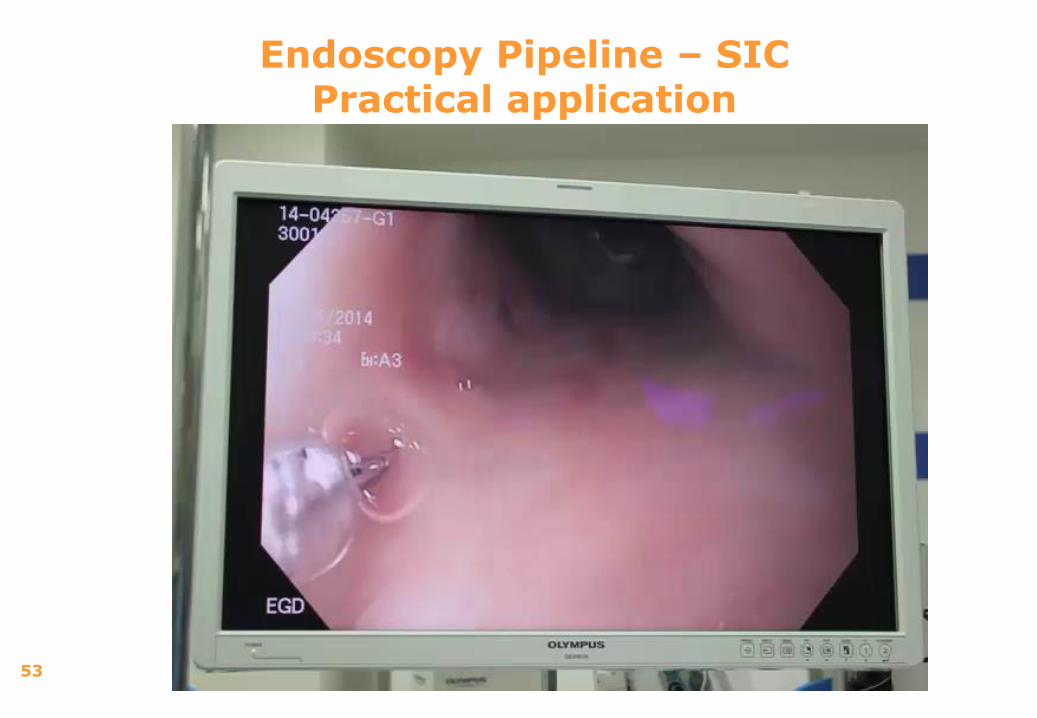

Endoscopy Pipeline – SICPractical application

54

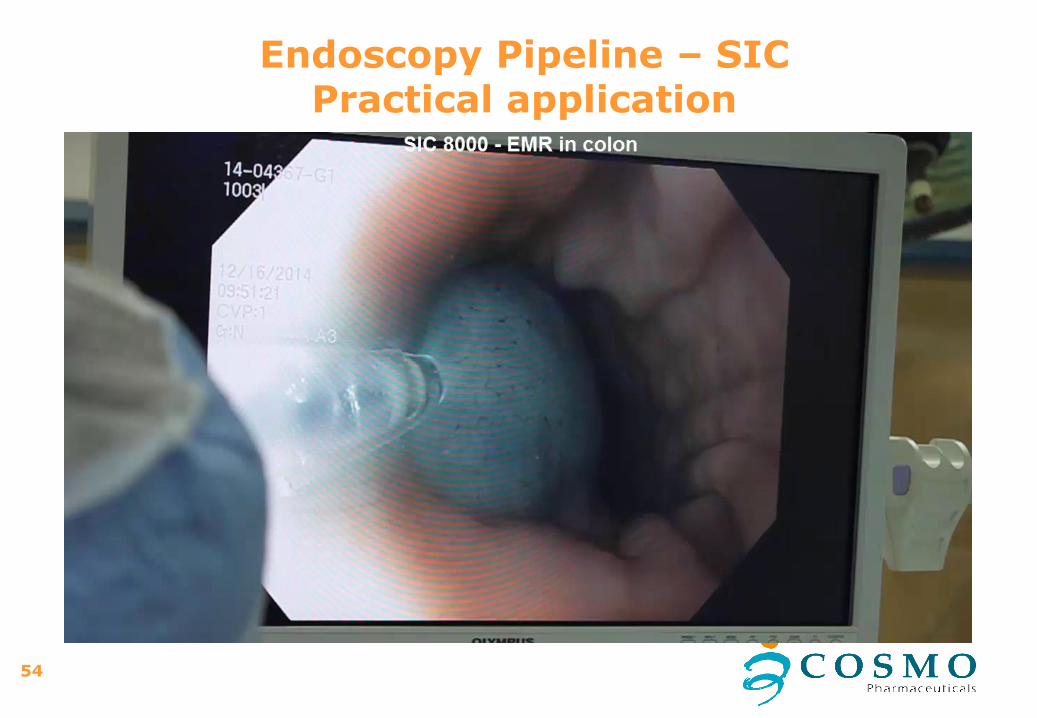

Endoscopy Pipeline – SICPractical application

55

Endoscopy Pipeline – SICPractical application

56

Endoscopy Pipeline – SICDevelopment as agreed with FDA is completed

• 3 biocompatibility studies (as per ISO 10993 standard)

In vitro cytotoxicity

Acute intracutaneous reactivity study in rabbits

Delayed dermal sensitization in guinea pigs

Biocompatibility studies demonstrated that SIC 8000 is biocompatible: not

cytotoxic, not irritating, not sensitizing

• 5 preclinical GLP studies on animals:

Tolerability study in minipigs

Tolerability study in dogs

Tolerability study in pigs

EMR/ESD procedures using SIC 8000 in pigs (stomach + colon)

Feasibility study of EMR/ESD procedures in pigs (stomach + colon + esophagus)

• Aim of the preclinical studies: full characterization of the product (efficacy/safety

profile) in conditions simulating and mimicking the actual use of the product on

human patients

• Animal species selection based on the animal models currently used for endoscopic

training procedures

57

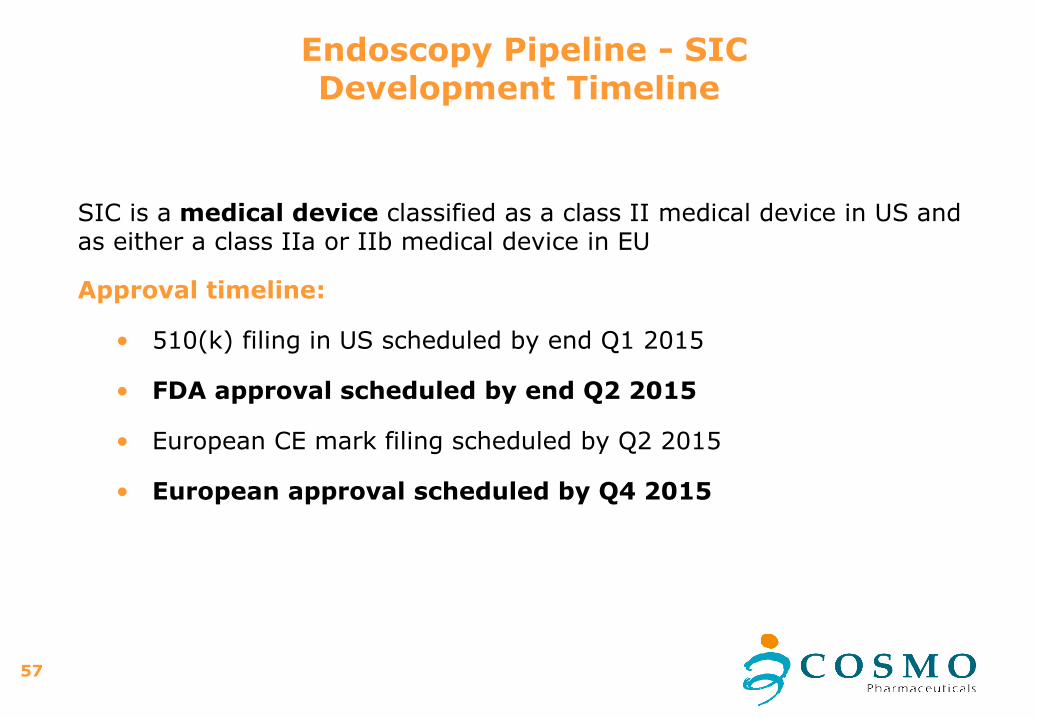

Endoscopy Pipeline - SICDevelopment Timeline

SIC is a medical device classified as a class II medical device in US and as either a class IIa or IIb medical device in EU

Approval timeline:

• 510(k) filing in US scheduled by end Q1 2015

• FDA approval scheduled by end Q2 2015

• European CE mark filing scheduled by Q2 2015

• European approval scheduled by Q4 2015

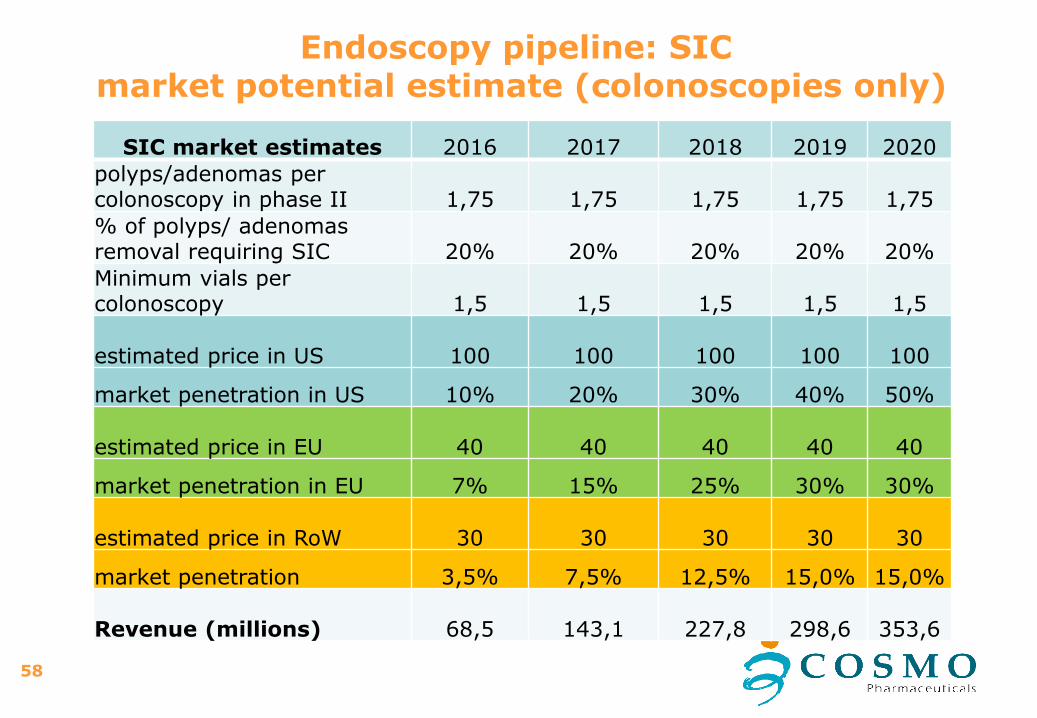

SIC market estimates 2016 2017 2018 2019 2020

polyps/adenomas per colonoscopy in phase II 1,75 1,75 1,75 1,75 1,75

% of polyps/ adenomas removal requiring SIC 20% 20% 20% 20% 20%

Minimum vials per colonoscopy 1,5 1,5 1,5 1,5 1,5

estimated price in US 100 100 100 100 100

market penetration in US 10% 20% 30% 40% 50%

estimated price in EU 40 40 40 40 40

market penetration in EU 7% 15% 25% 30% 30%

estimated price in RoW 30 30 30 30 30

market penetration 3,5% 7,5% 12,5% 15,0% 15,0%

Revenue (millions) 68,5 143,1 227,8 298,6 353,6

58

Endoscopy pipeline: SICmarket potential estimate (colonoscopies only)

59

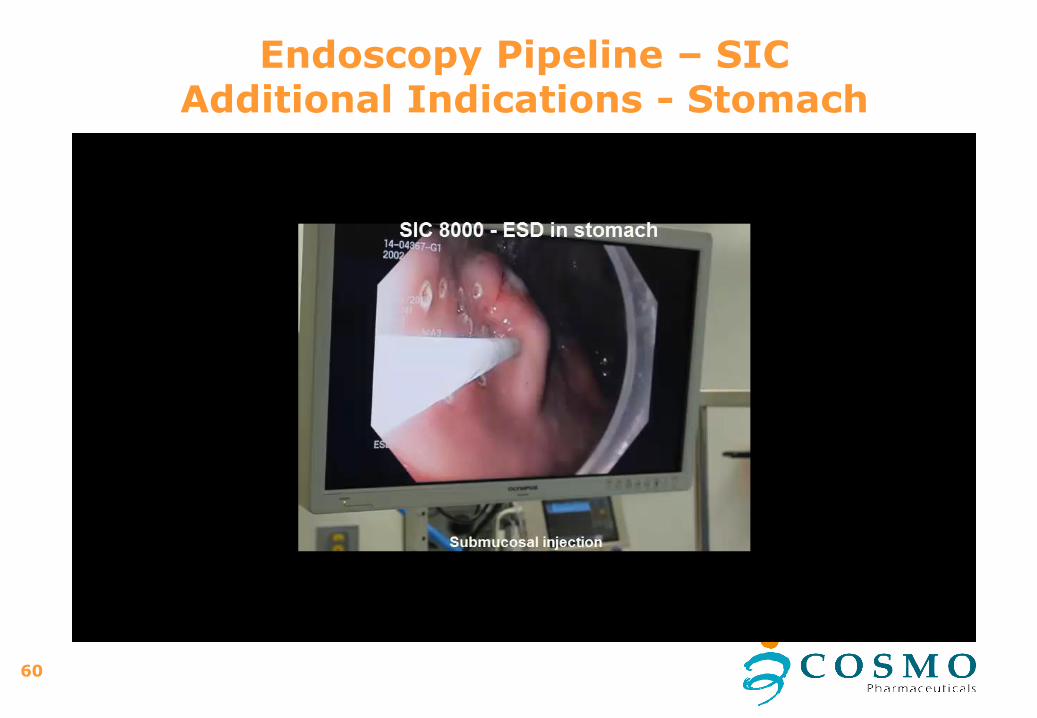

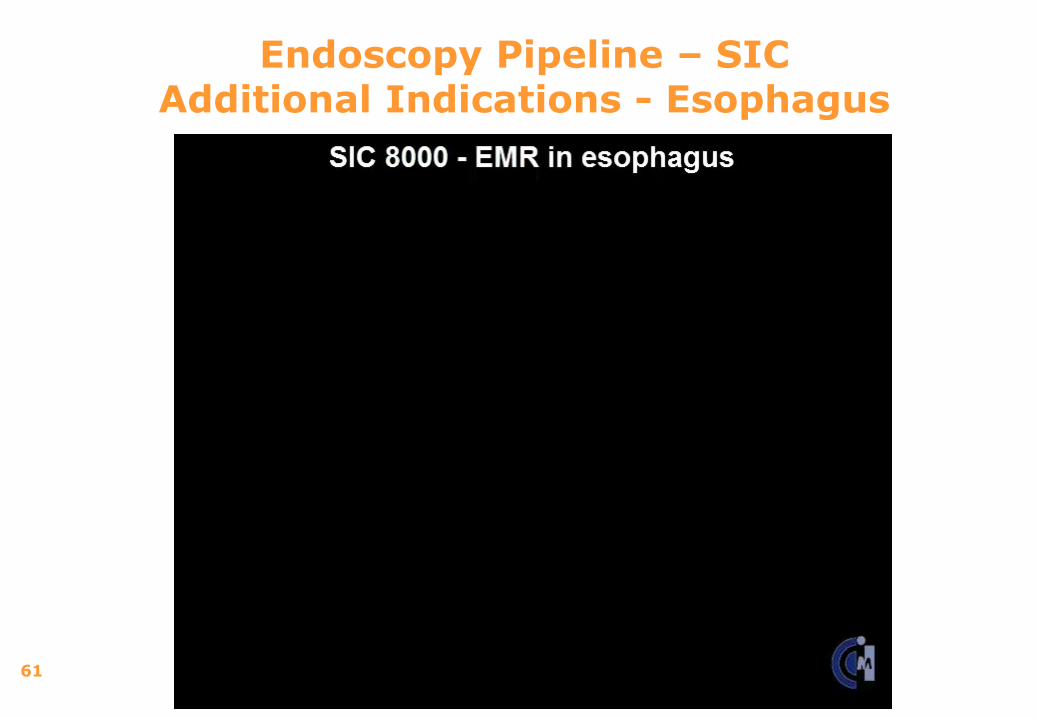

Endoscopy pipeline: SICmarket potential (additional indications)

The tissues of the esophagus, stomach and duodenum are quite similar to those of the colon. Inspection of these three tracts is conducted by Esophagogastroduodenoscopy (ECG). SIC can be used in all these tracts.

As many ECGs are performed as colonoscopies, both in the US and Europe.

During ECG, removal of tissues/polyps is frequently necessary and will require SIC as per below examples:

Barrett Esophagus

• Caused by GERD, ~ 1,6% of population affected

• Requires an ECG every 3 years

• Tissue removal required in ~ 10% all cases

Stomach & duodenal polyps

• polyps requiring extraction are found in around 0,7% of all procedures

60

Endoscopy Pipeline – SICAdditional Indications - Stomach

61

Endoscopy Pipeline – SICAdditional Indications - Esophagus

62

Products under development

Dermatology Pipeline

Product Pre-clinical Phase I Phase II Phase III MA Launch

CB-03-01ACNE

CB-03-01ALOPECIA

CB-06-02AS 101

CB-06-04 ACNE ANTIBIOTIC

Dermatology pipeline

64

Dermatology: a market with little innovation and many opportunities

• No NCE in Acne in the US market in the last 15 years

• Dermatologists generally prescribe 2-3 products at the same time as they look for new therapeutic options

• Historically dermatology has had the lowest product failure rate in clinical trials

• Probability of success in phase III clinical trials is high

• Market has important cosmetic and life-style implications

65

Dermatology Pipeline Acne market dynamics & opportunity

85% of all persons age 12-24 get acne, characterized as a chronic disease

In US 17 m person have acne, 35 m prescriptions are written p.a. primarily generics as there are no new drugs

WW market ~ $ 3 b; US Market at $ 2.3 b, growing by ~ 1% p.a. • Topical antibiotics market share ~ 29%• Topical retinoid market ~ 25%• Oral antibiotic market ~ 41%

Excellent opportunity for new topical drugs withnovel treatment forms and very low side effects

66

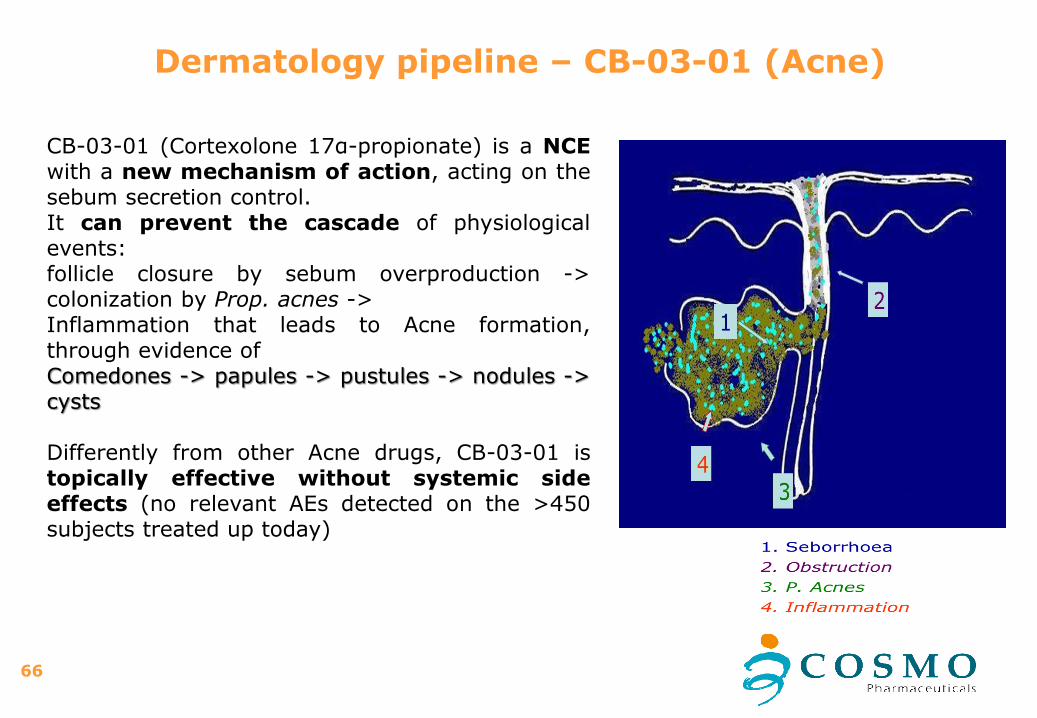

Dermatology pipeline – CB-03-01 (Acne)

CB-03-01 (Cortexolone 17α-propionate) is a NCEwith a new mechanism of action, acting on thesebum secretion control.It can prevent the cascade of physiologicalevents:follicle closure by sebum overproduction ->colonization by Prop. acnes ->Inflammation that leads to Acne formation,through evidence ofComedones -> papules -> pustules -> nodules ->cysts

Differently from other Acne drugs, CB-03-01 istopically effective without systemic sideeffects (no relevant AEs detected on the >450subjects treated up today)

67

Dermatology pipeline – CB-03-01 (Acne)Phase II overview

Phase II dose ranging trial completed in US

360 patients – 4 doses + vehicle

Best dose identified (1% BID)

No adverse events

Dermatology pipeline – CB-03-01 (Acne)Phase II overview

68

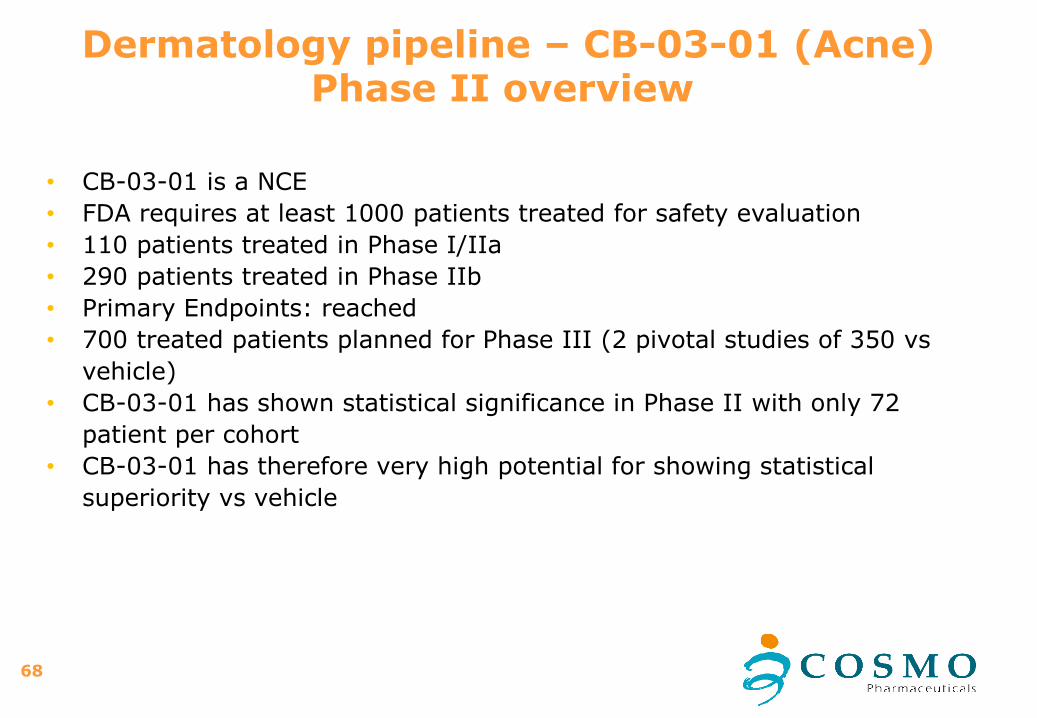

• CB-03-01 is a NCE

• FDA requires at least 1000 patients treated for safety evaluation

• 110 patients treated in Phase I/IIa

• 290 patients treated in Phase IIb

• Primary Endpoints: reached

• 700 treated patients planned for Phase III (2 pivotal studies of 350 vs

vehicle)

• CB-03-01 has shown statistical significance in Phase II with only 72

patient per cohort

• CB-03-01 has therefore very high potential for showing statistical

superiority vs vehicle

69

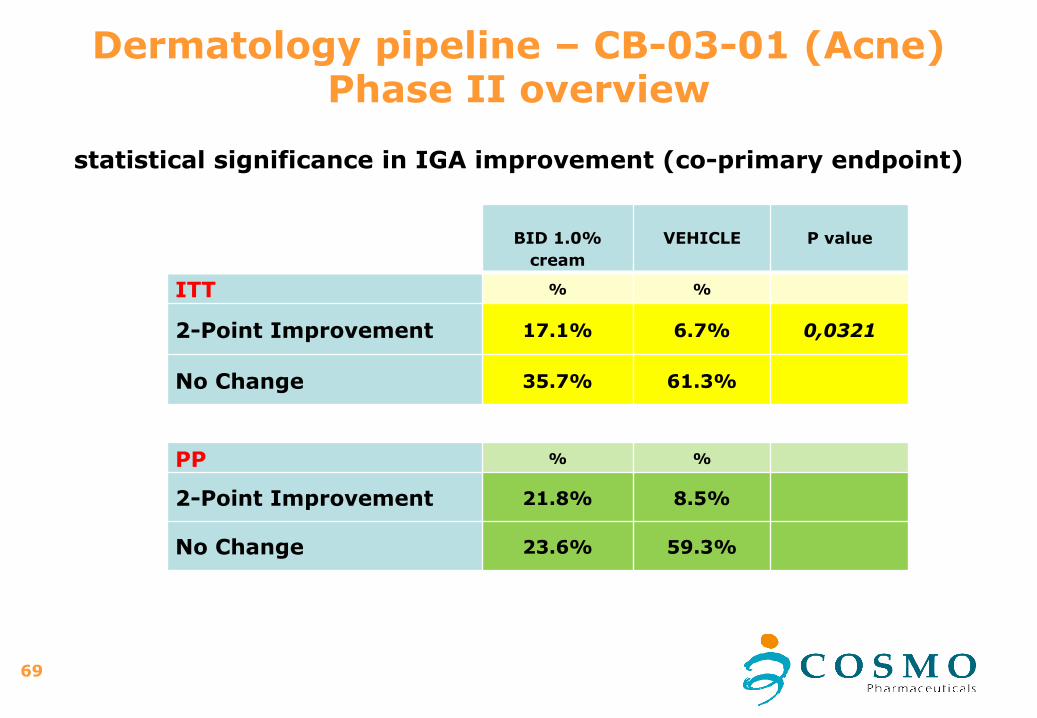

statistical significance in IGA improvement (co-primary endpoint)

BID 1.0%

cream

VEHICLE P value

ITT % %

2-Point Improvement 17.1% 6.7% 0,0321

No Change 35.7% 61.3%

PP % %

2-Point Improvement 21.8% 8.5%

No Change 23.6% 59.3%

Dermatology pipeline – CB-03-01 (Acne)Phase II overview

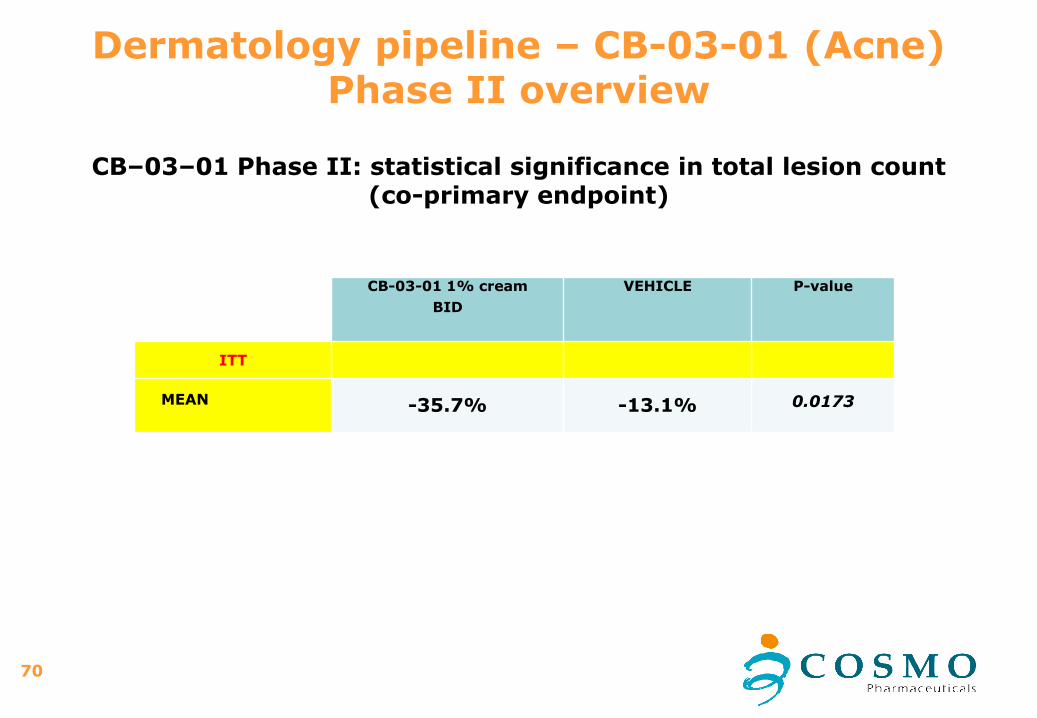

CB–03–01 Phase II: statistical significance in total lesion count(co-primary endpoint)

70

CB-03-01 1% cream

BID

VEHICLE P-value

ITT

MEAN -35.7% -13.1% 0.0173

Dermatology pipeline – CB-03-01 (Acne)Phase II overview

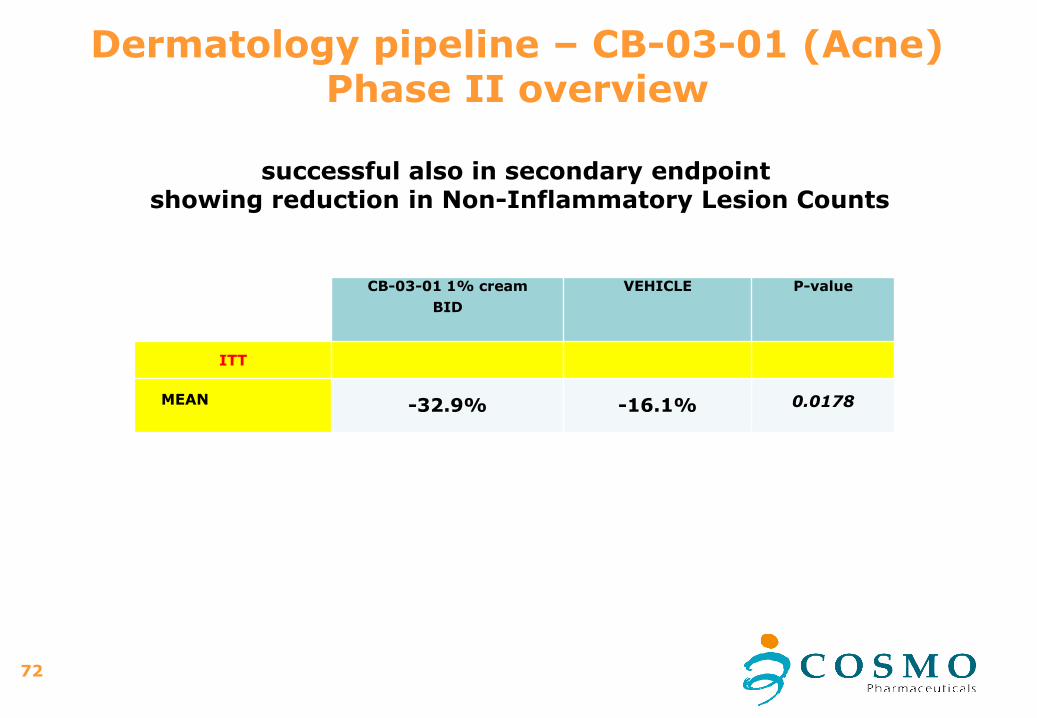

successful also in secondary endpointshowing reduction in Inflammatory Lesion Counts

71

CB-03-01 1% cream BID VEHICLE P-value*

ITT % %

MEAN -37.2% -27.0% 0.0384

* Kruskal Wallis test

Dermatology pipeline – CB-03-01 (Acne)Phase II overview

72

CB-03-01 1% cream

BID

VEHICLE P-value

ITT

MEAN -32.9% -16.1% 0.0178

successful also in secondary endpointshowing reduction in Non-Inflammatory Lesion Counts

Dermatology pipeline – CB-03-01 (Acne)Phase II overview

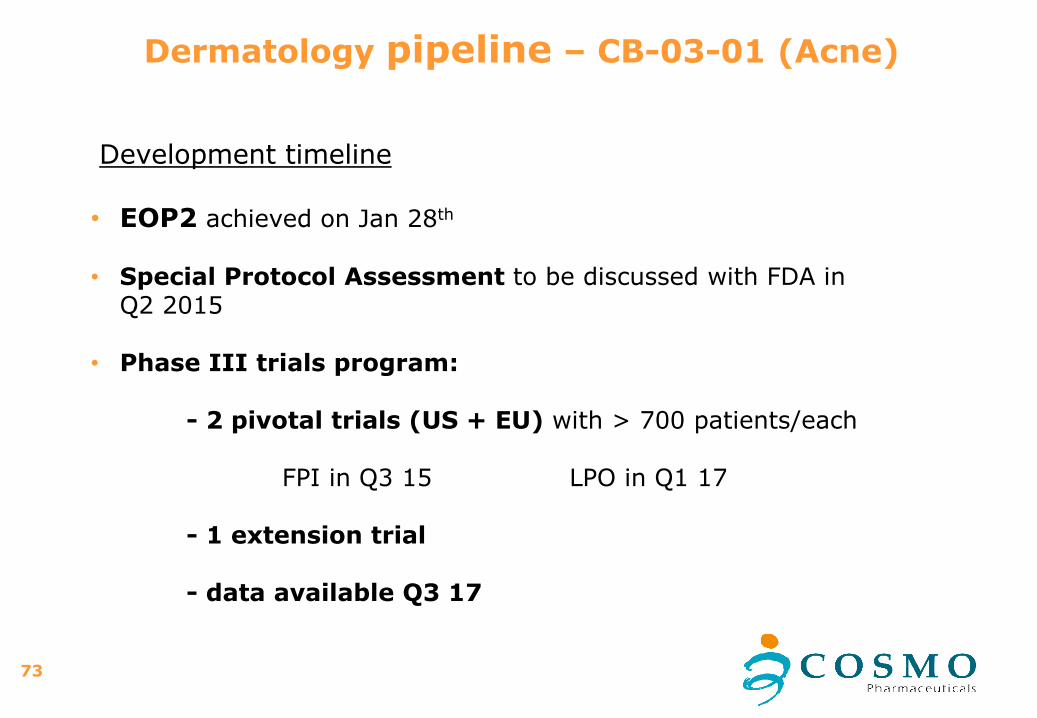

73

Development timeline

• EOP2 achieved on Jan 28th

• Special Protocol Assessment to be discussed with FDA in Q2 2015

• Phase III trials program:

- 2 pivotal trials (US + EU) with > 700 patients/each

FPI in Q3 15 LPO in Q1 17

- 1 extension trial

- data available Q3 17

Dermatology pipeline – CB-03-01 (Acne)

74

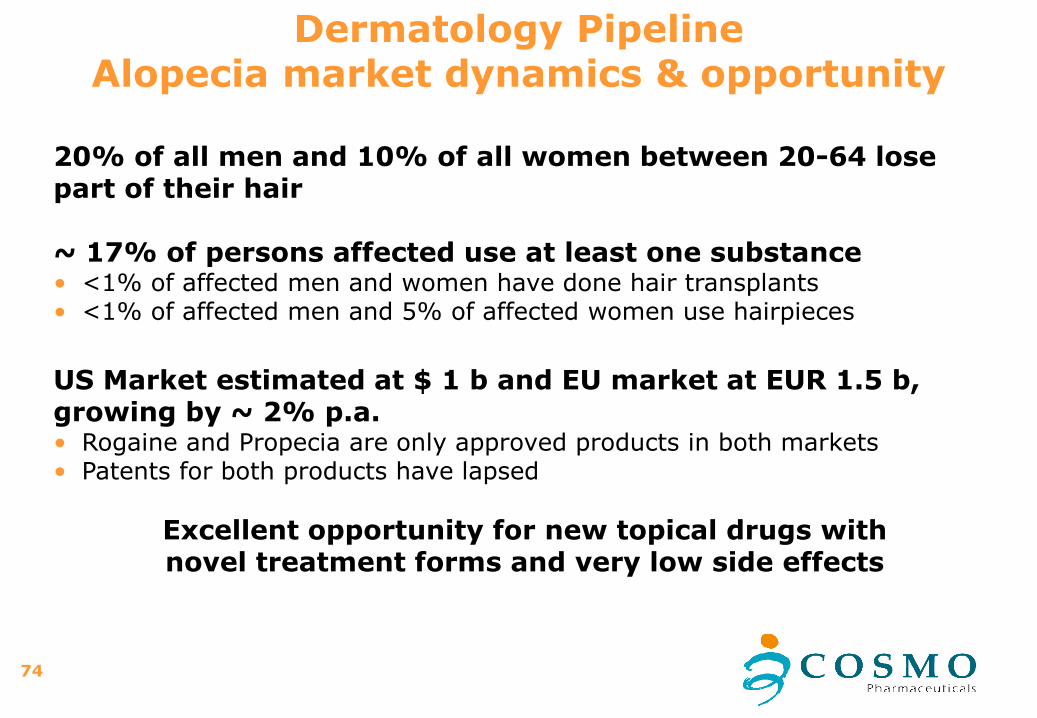

Dermatology Pipeline Alopecia market dynamics & opportunity

20% of all men and 10% of all women between 20-64 lose part of their hair

~ 17% of persons affected use at least one substance• <1% of affected men and women have done hair transplants• <1% of affected men and 5% of affected women use hairpieces

US Market estimated at $ 1 b and EU market at EUR 1.5 b, growing by ~ 2% p.a. • Rogaine and Propecia are only approved products in both markets• Patents for both products have lapsed

Excellent opportunity for new topical drugs with novel treatment forms and very low side effects

Dermatology Pipeline – CB-03-01 (Alopecia)

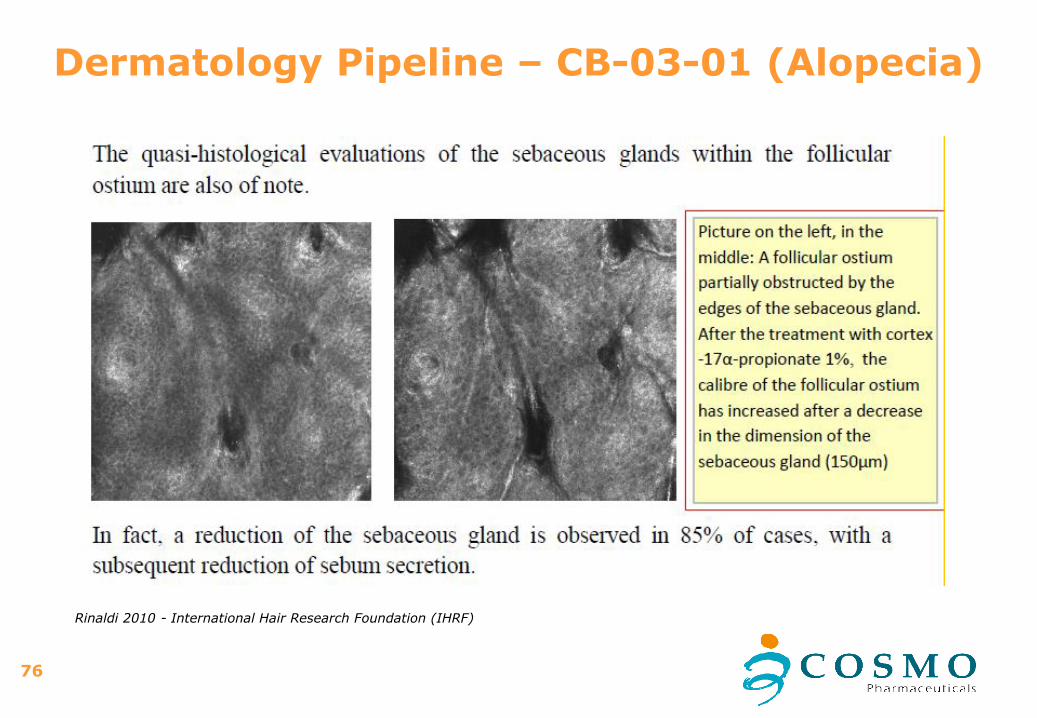

76

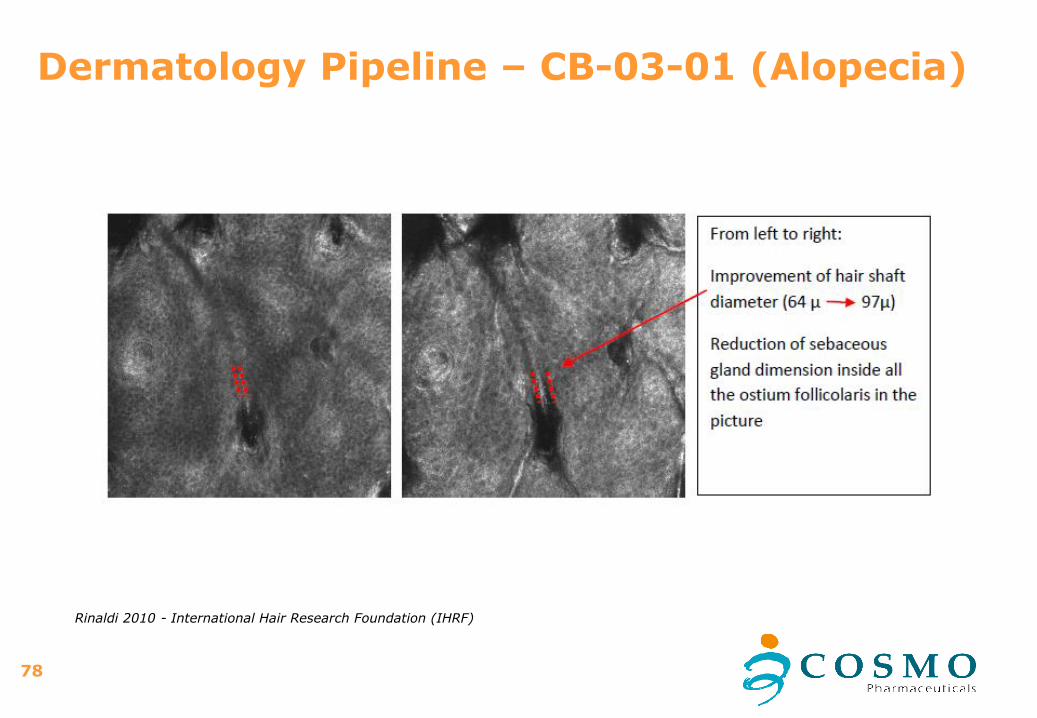

Dermatology Pipeline – CB-03-01 (Alopecia)

Rinaldi 2010 - International Hair Research Foundation (IHRF)

77

Dermatology Pipeline – CB-03-01 (Alopecia)

Rinaldi 2010 - International Hair Research Foundation (IHRF)

78

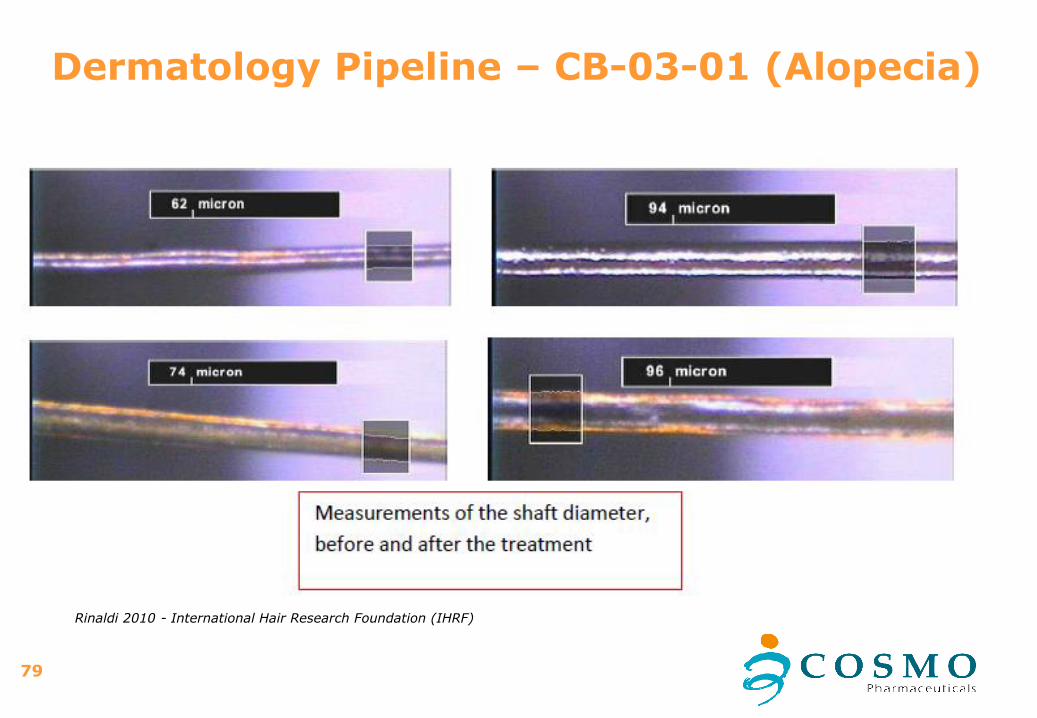

Dermatology Pipeline – CB-03-01 (Alopecia)

Rinaldi 2010 - International Hair Research Foundation (IHRF)

79

Dermatology Pipeline – CB-03-01 (Alopecia)

Rinaldi 2010 - International Hair Research Foundation (IHRF)

80

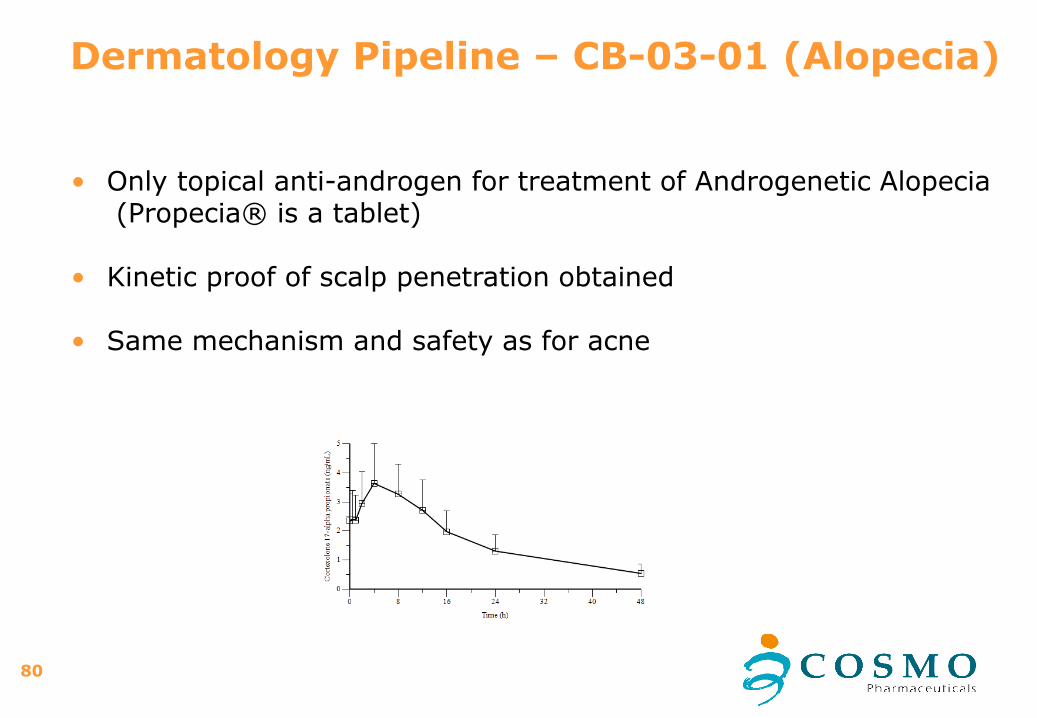

Dermatology Pipeline – CB-03-01 (Alopecia)

• Only topical anti-androgen for treatment of Androgenetic Alopecia(Propecia® is a tablet)

• Kinetic proof of scalp penetration obtained

• Same mechanism and safety as for acne

81

Development timeline

• POC Phase II ongoing in USA: 90 patients, double blind, 3 parallel arms, placebo and Minoxidil controlled, 26 weeks of treatment, endpoints on scalp darkness and patientsatisfaction.

• The Modified Norwood-Hamilton Scale is used to assess the eligibility of subjects at the Screening Visit. Subject has to have mild to moderate AGA in temple and vertex region rating Modified Hamilton-Norwood Scale III vertex to V (IIIv, IV, V) with ongoing hair loss to be eligible for this study

• Recruitment is in progress and treatment will be completed by end of 2015

Dermatology Pipeline – CB-03-01 (Alopecia)

82

Dermatology Pipeline – CB-06-02 (HPV)market dynamics & opportunity

>20 m persons are infected with HPV in the US, around 1% ofsexually active persons in US have visible external genital warts(AGW)

HPV can lead to cancer and should be eradicated

In western countries many young children are vaccinated against the Papillomavirus • the vaccine is ineffective on persons that already have the virus

Current market

• around 360’000 persons develop AGW each year in US

• there are ~ 600’000 TRX each year • main products prescribed are Imiquimod based

83

Dermatology Pipeline – CB-06-02 (HPV)

• Anogenital warts (AGWs) is a common, highly infectious disease caused by the human papillomavirus (HPV)

• Tellurium based compound for treatment of HPV and genital warts

• HPV vaccination is currently in regression because of fertility concerns

84

Dermatology Pipeline – CB-06-02 (HPV)

American family Physician December 15, 2004, 70 (12)

85

Development timeline

• POC Phase II ongoing in Israel on 30 + 30 patients, double blind, parallel arms, 12 weeks of treatment + 3 months of follow up, endpoints on remission and recurrence rates

• Trial Completion foreseen by Q1 2016

Dermatology Pipeline – CB-06-02 (HPV)

86

Dermatology Pipeline – CB-06-01 (Acne)

• Topical antibiotic for the treatment of Acne

• Ideal complement to CB-03-01

• NCE with very potent and selective properties

• Effective with bacterial strains resistant to other antibiotics

87

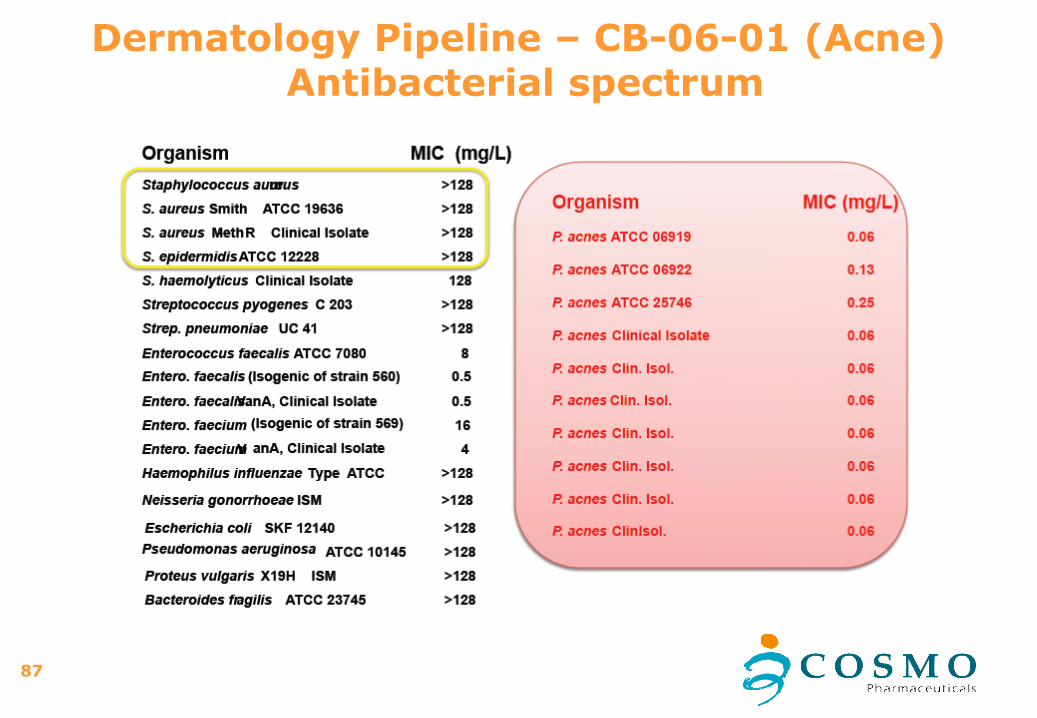

Dermatology Pipeline – CB-06-01 (Acne)Antibacterial spectrum

88

Dermatology Pipeline – CB-06-01 (Acne)Activity against antibiotic-resistant P. acnes

89

Dermatology Pipeline – CB-06-01 (Acne)

Development timeline

• POC Phase II ongoing with a gel formulation, completion by Q1 2016

90

Cosmo Corporate Matters

91

Cosmo Corporate MattersNo impact of FX turmoil on Cosmo

No costs in CHF

Only 9% of costs in $, rest in EUR

49% of revenues in $; 51% in EUR

All liabilities are in EUR

92

Cosmo Corporate Matters

Cash & Liquid Investmentsas of 1/12/2015

EUR 123.6 mUSD 63.7 m

93

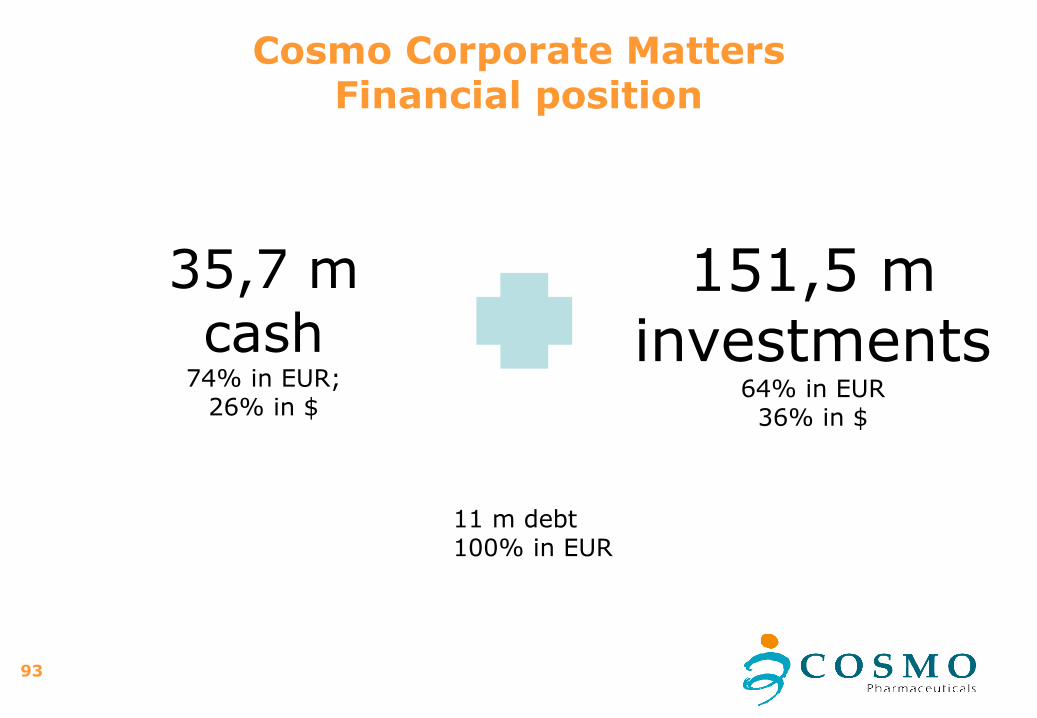

Cosmo Corporate MattersFinancial position

35,7 m cash

74% in EUR; 26% in $

151,5 m investments

64% in EUR36% in $

11 m debt100% in EUR

94

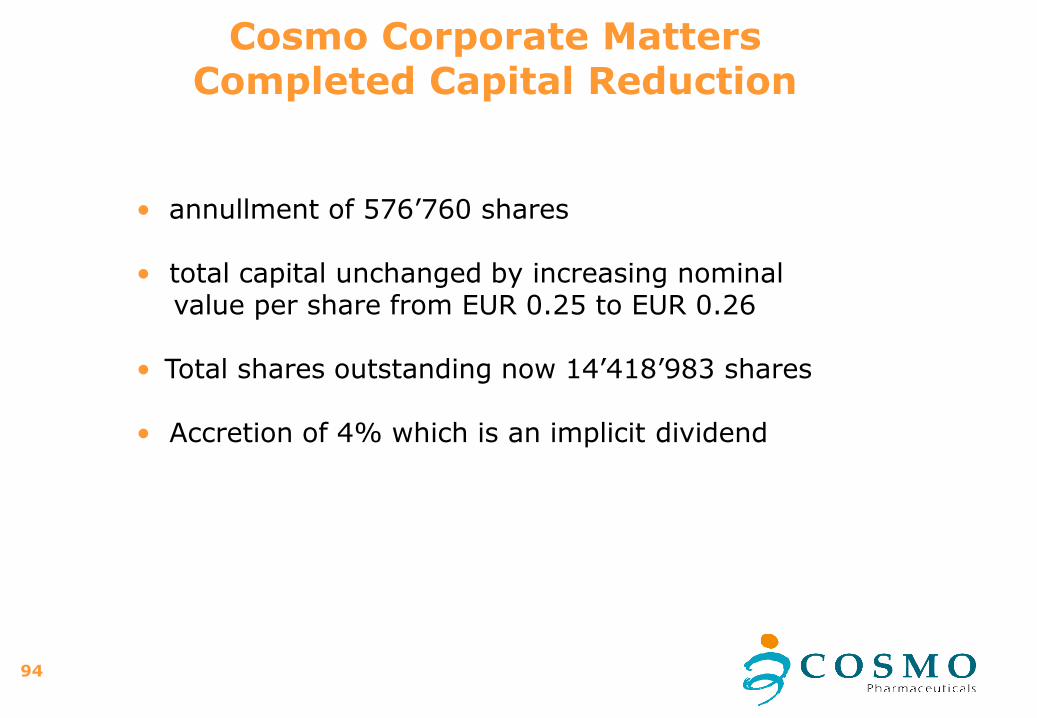

Cosmo Corporate MattersCompleted Capital Reduction

• annullment of 576’760 shares

• total capital unchanged by increasing nominal value per share from EUR 0.25 to EUR 0.26

• Total shares outstanding now 14’418’983 shares

• Accretion of 4% which is an implicit dividend

95

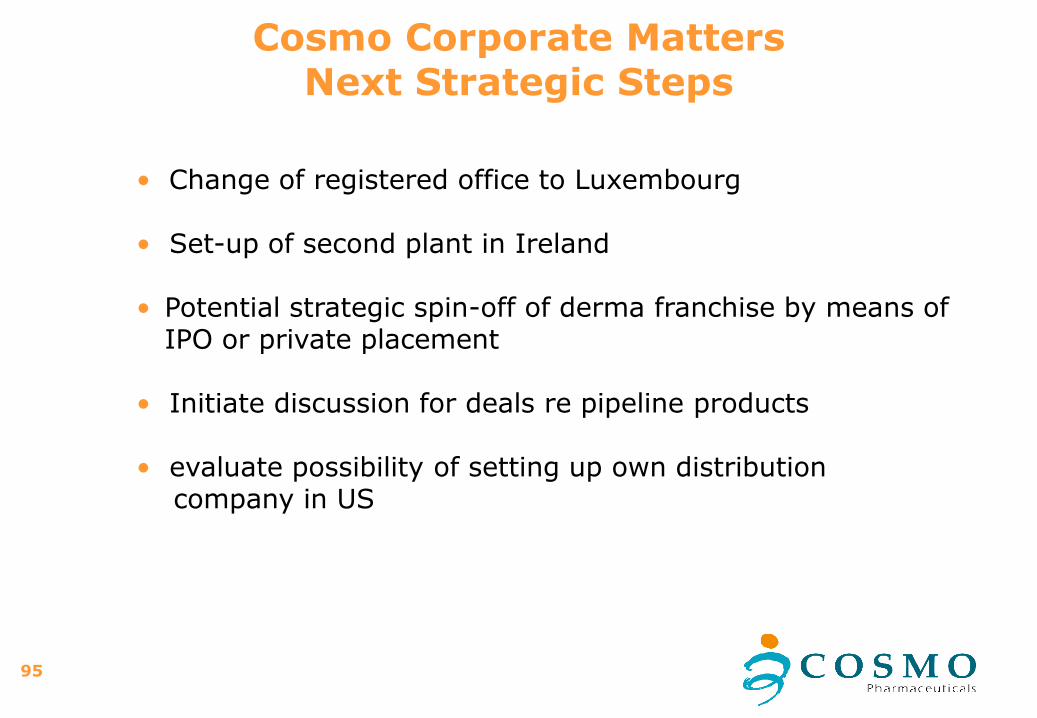

Cosmo Corporate MattersNext Strategic Steps

• Change of registered office to Luxembourg

• Set-up of second plant in Ireland

• Potential strategic spin-off of derma franchise by means of IPO or private placement

• Initiate discussion for deals re pipeline products

• evaluate possibility of setting up own distribution company in US

96

Cosmo Corporate MattersTransfer of Seat to Luxembourg

• Filing for registration in Luxembourg early February

• Registration takes place in 10-20 days

• After registration in Luxembourg, filing for cancellation in Italy

97

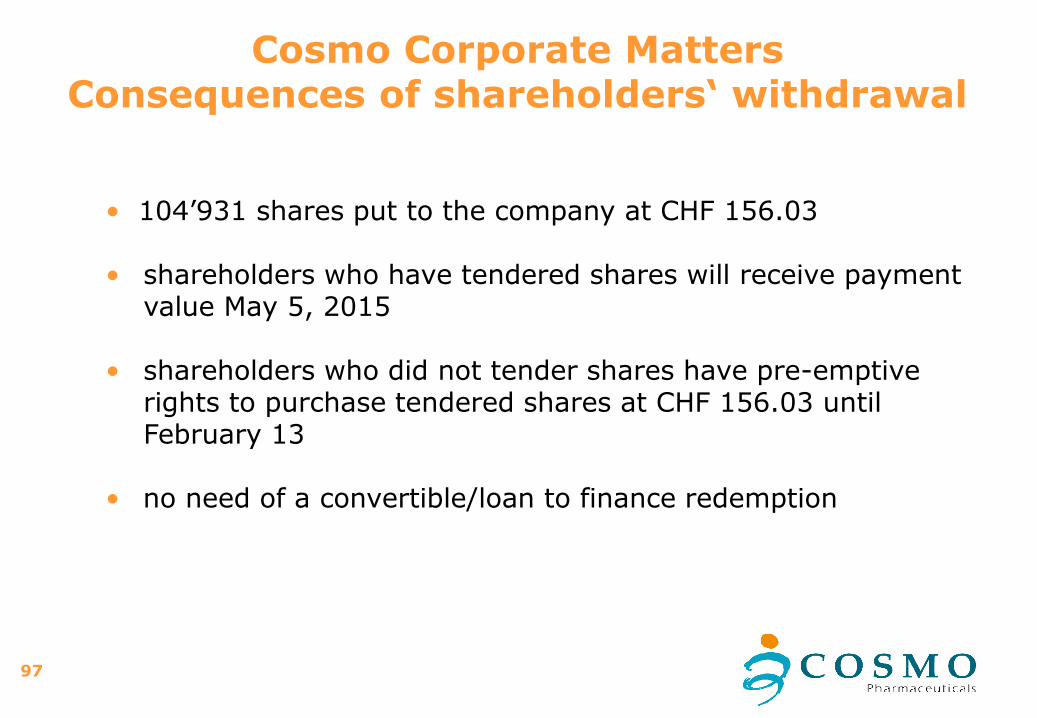

Cosmo Corporate MattersConsequences of shareholders‘ withdrawal

• 104’931 shares put to the company at CHF 156.03

• shareholders who have tendered shares will receive payment value May 5, 2015

• shareholders who did not tender shares have pre-emptive rights to purchase tendered shares at CHF 156.03 until February 13

• no need of a convertible/loan to finance redemption

98

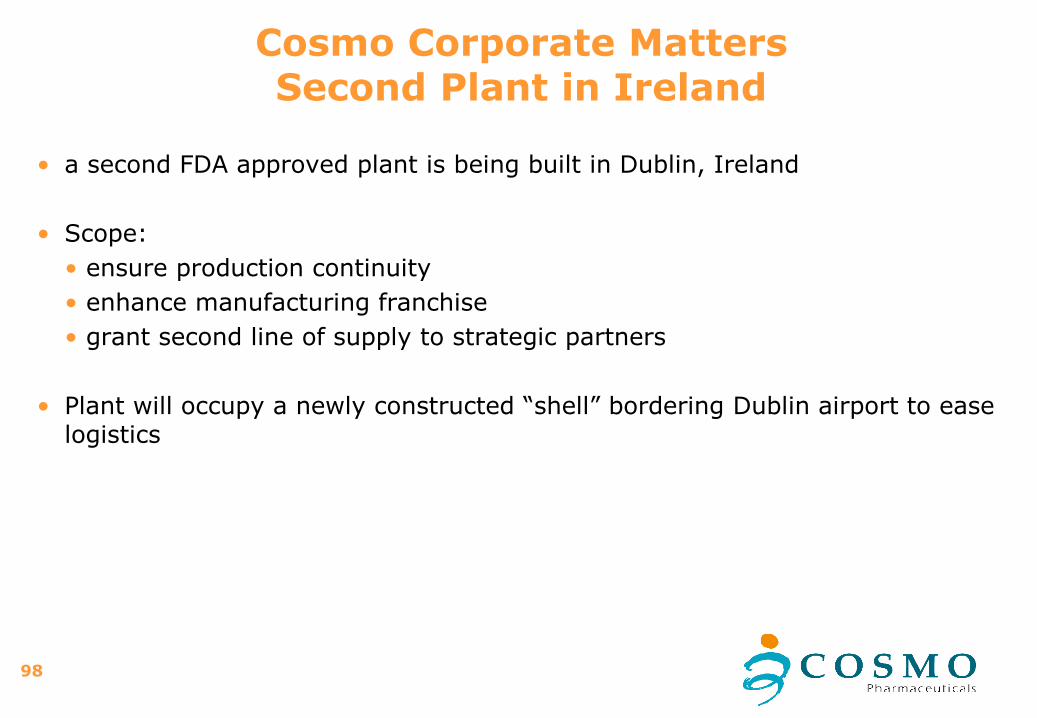

• a second FDA approved plant is being built in Dublin, Ireland

• Scope:

• ensure production continuity

• enhance manufacturing franchise

• grant second line of supply to strategic partners

• Plant will occupy a newly constructed “shell” bordering Dublin airport to ease logistics

Cosmo Corporate MattersSecond Plant in Ireland

99

• 3’000 sqm surface, 12m height

• MMX tablets production line (500k batch size) + bottle and blister packaging lines

• expected timeline:

• Q1 2015 planning permission filing

• Q4 2015 fit-out works start, around 12 months duration

• H2 2017 FDA inspection

• total investment: approx EUR 15m in 2016-2017

Cosmo Corporate MattersSecond Plant in Ireland - Features

100

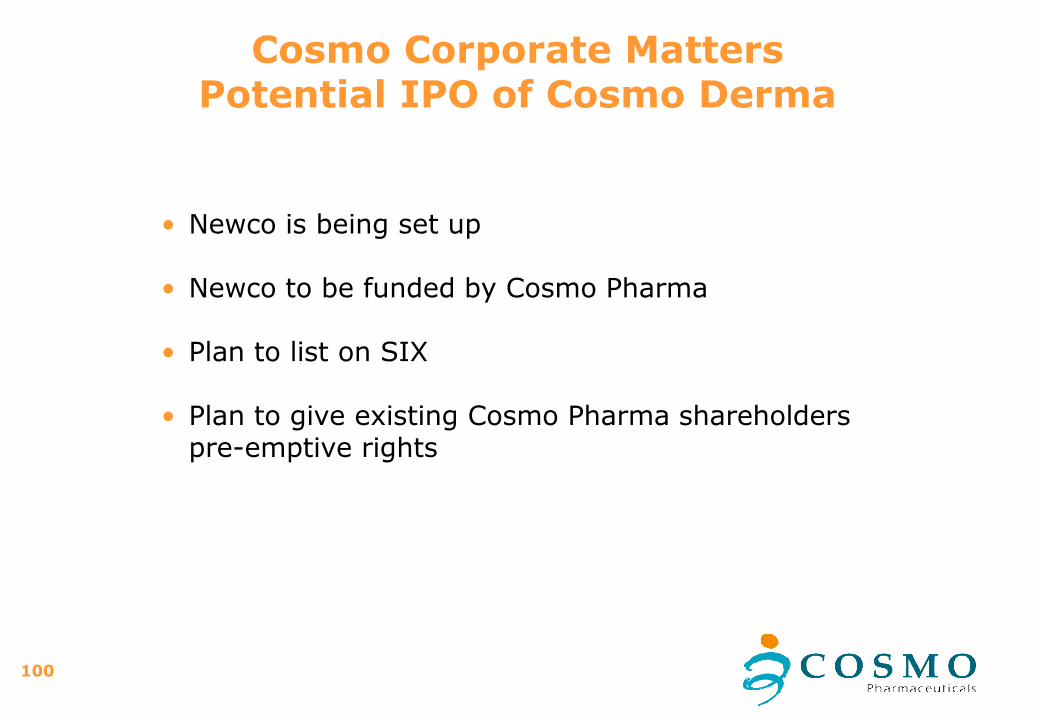

Cosmo Corporate MattersPotential IPO of Cosmo Derma

• Newco is being set up

• Newco to be funded by Cosmo Pharma

• Plan to list on SIX

• Plan to give existing Cosmo Pharma shareholderspre-emptive rights

101

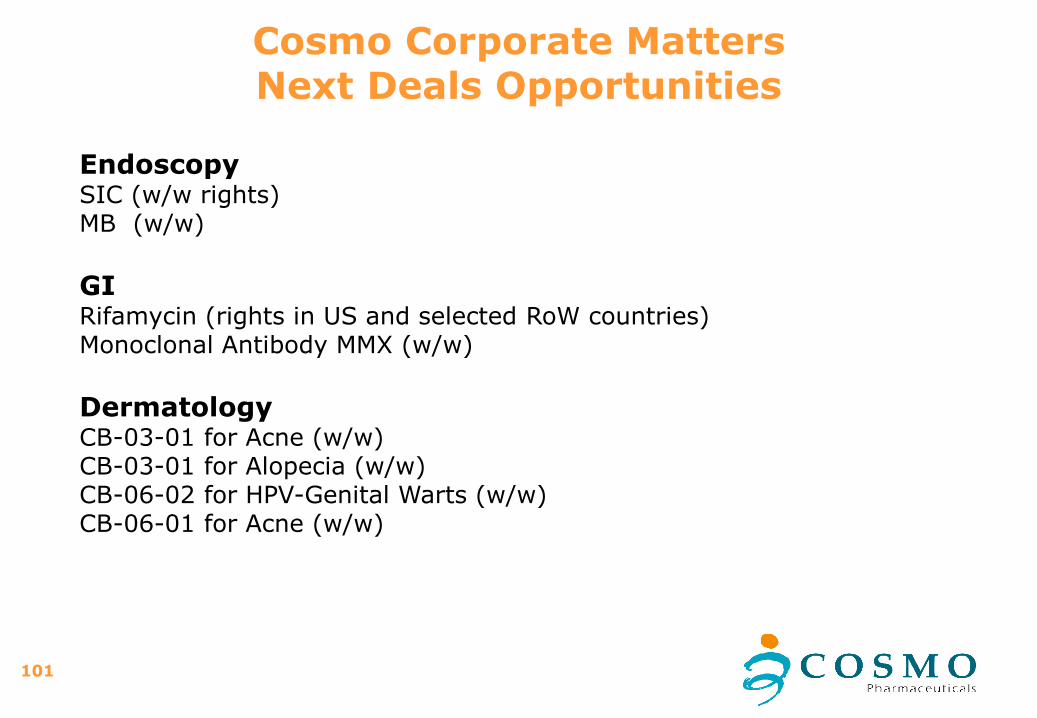

Cosmo Corporate MattersNext Deals Opportunities

EndoscopySIC (w/w rights) MB (w/w)

GIRifamycin (rights in US and selected RoW countries)Monoclonal Antibody MMX (w/w)

DermatologyCB-03-01 for Acne (w/w)CB-03-01 for Alopecia (w/w)CB-06-02 for HPV-Genital Warts (w/w)CB-06-01 for Acne (w/w)

102

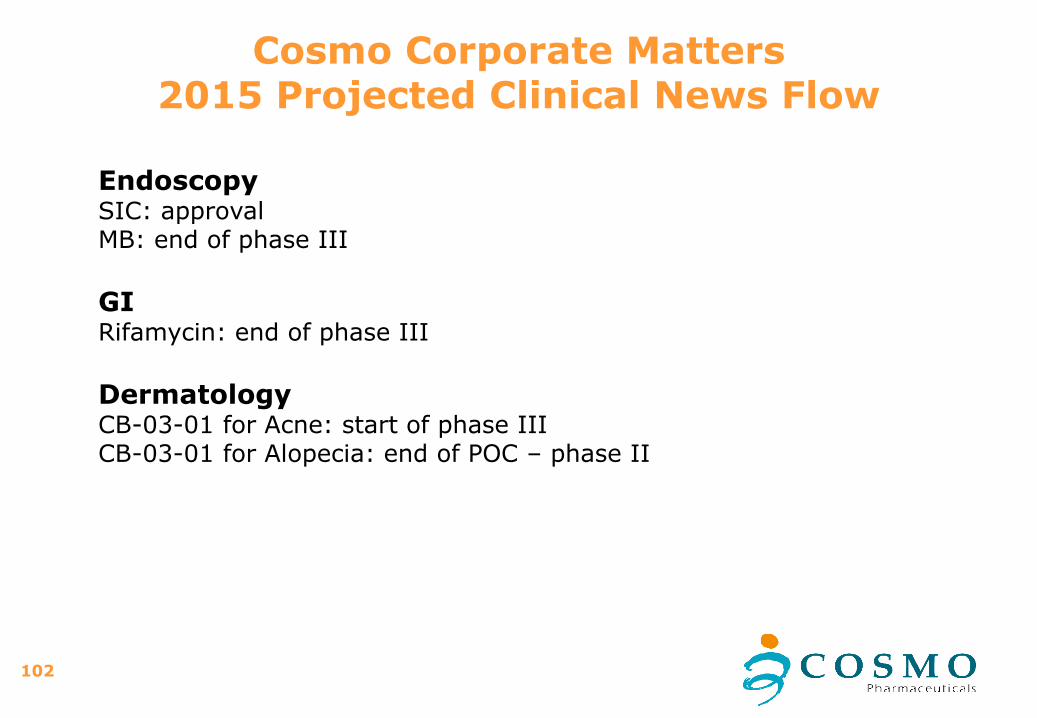

Cosmo Corporate Matters2015 Projected Clinical News Flow

EndoscopySIC: approvalMB: end of phase III

GIRifamycin: end of phase III

DermatologyCB-03-01 for Acne: start of phase IIICB-03-01 for Alopecia: end of POC – phase II

103

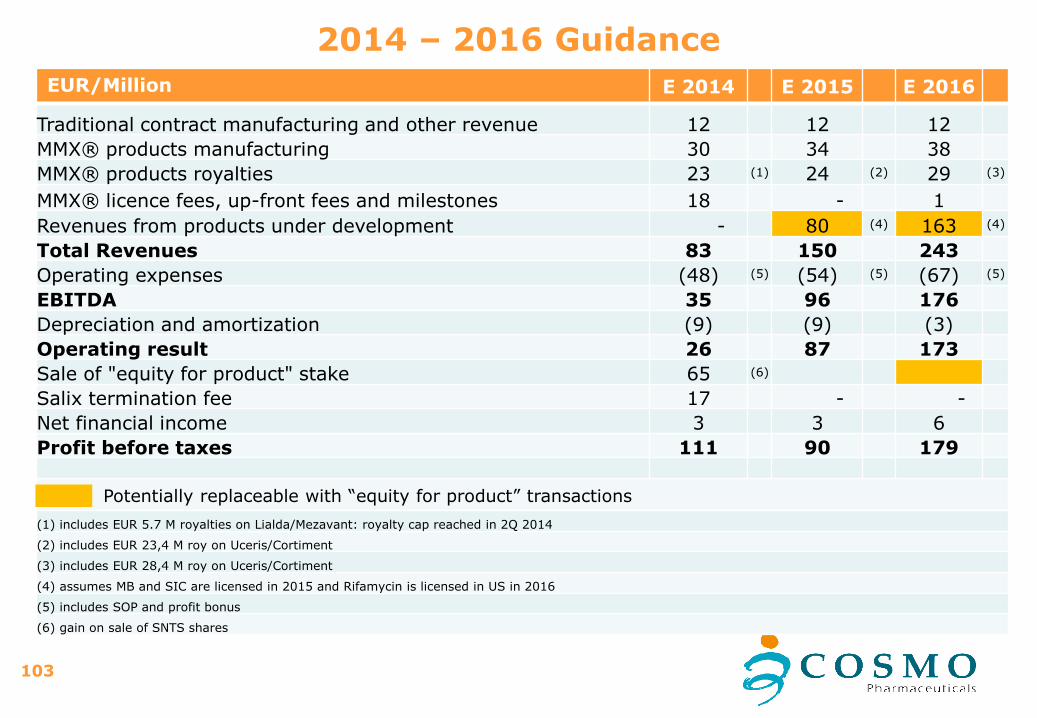

EUR/Million E 2014 E 2015 E 2016

Traditional contract manufacturing and other revenue 12 12 12

MMX® products manufacturing 30 34 38

MMX® products royalties 23 (1) 24 (2) 29 (3)

MMX® licence fees, up-front fees and milestones 18 - 1

Revenues from products under development - 80 (4) 163 (4)

Total Revenues 83 150 243

Operating expenses (48) (5) (54) (5) (67) (5)

EBITDA 35 96 176

Depreciation and amortization (9) (9) (3)

Operating result 26 87 173

Sale of "equity for product" stake 65 (6)

Salix termination fee 17 - -

Net financial income 3 3 6

Profit before taxes 111 90 179

Potentially replaceable with “equity for product” transactions

(1) includes EUR 5.7 M royalties on Lialda/Mezavant: royalty cap reached in 2Q 2014

(2) includes EUR 23,4 M roy on Uceris/Cortiment

(3) includes EUR 28,4 M roy on Uceris/Cortiment

(4) assumes MB and SIC are licensed in 2015 and Rifamycin is licensed in US in 2016

(5) includes SOP and profit bonus

(6) gain on sale of SNTS shares

2014 – 2016 Guidance

104

Cosmo Pharmaceuticals

Information Contacts

• Number of shares: 14,418,983

• Listing: SIX Swiss exchange, Main board

• ISIN: IT0004167463

• Alessandro Della Cha , [email protected]

• Chris Tanner, [email protected]: +39-02-9333’7276

• Giuseppe Cipriano, [email protected]

• Luigi Moro, [email protected]

Recommended