Presents

FHA IntroductionJuly 20, 2011

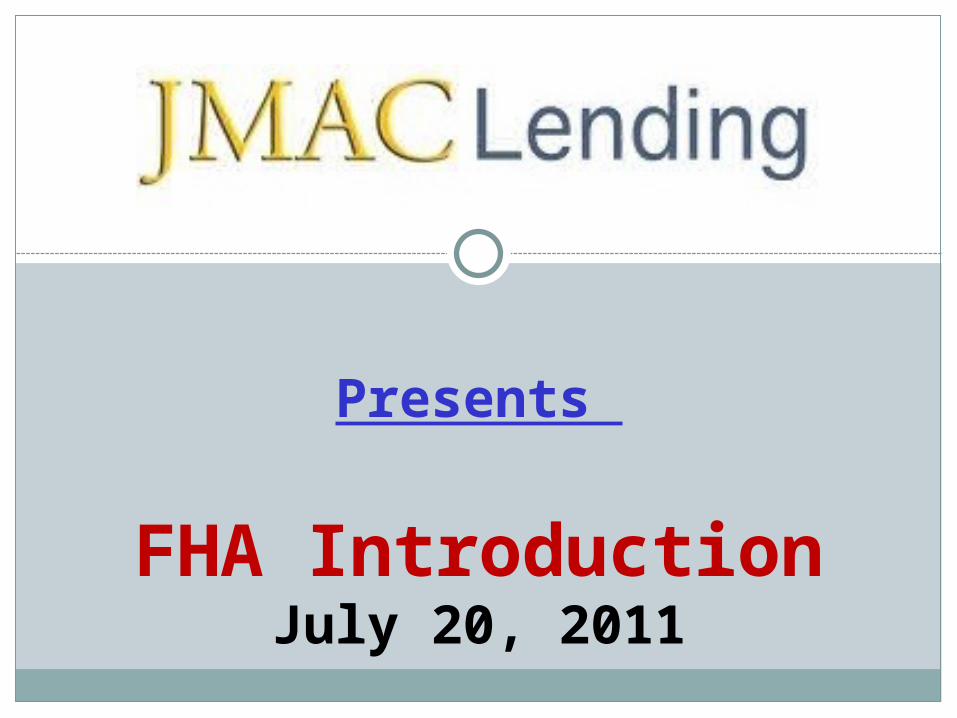

FHA Features

3.5% minimum down payment on purchase (96.5% LTV) Refinance rate and term max LTV is 97.75% Up to 85% LTV for cash out refinance. No $$ max for cash out. ALL down payment/cost can be gifted by family Can refinance from conventional to FHA FHA High Balance: max loan amount $729,750 subject to county

limits. FHA to FHA refi (Streamline): no appraisal nor income qualification. **6% seller credit includes recurring and non-recurring closing costs. More lenient on foreclosure (3 year) or BK history (2 yr on CH 7,

Chapter 13 BK must be 1 yr from filing, can remain open).** No need to worry about qualifying for mortgage insurance separately Available for BOTH first time homebuyers and CURRENT

homeowners Low credit score pricing adjustments more attractive than

conventional

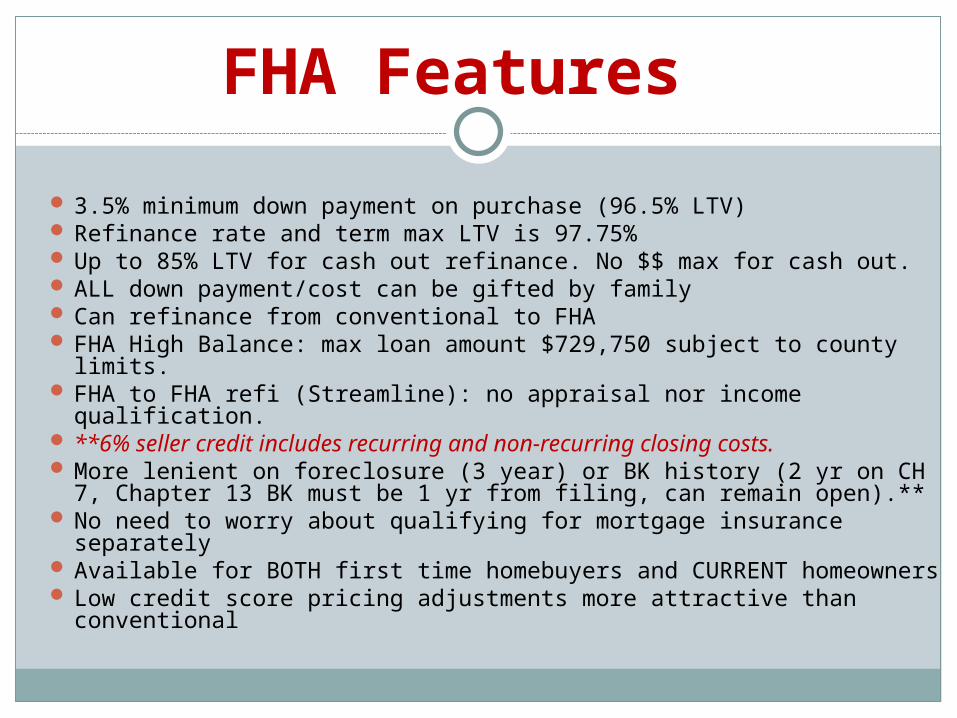

A Perfect FHA Loan

Borrower has limited funds for a down paymentLoan has a high LTVBorrower has less than perfect creditLoan requires MI but borrower’s fico is too low

for MIWhen DTI is over 41% (when MI is required)Source of down payment is a gift or community

2nd and borrower has less than 5% of own funds

Non-occupying co-borrower qualifications are less restrictive than conventional

85% cash out

FHA may not be right when…

Your loan is a second home or non-owner occupied

Your condo is not FHA approved The LTV is below 80% The buyer already has an FHA loan (Unless met

exceptions indicated in HUD Handbook)There is a non-borrowing spouse with a lot of

debts (FHA requires debts be included in DTI in community property states)

FHA vs. Conventional

Lower minimum down-payment of 3.5%.No appraisal required for FHA to FHA

streamline refinanceFHA Loss Mitigation OptionsStudent loan deferment

FHA vs. Conventional

High DTI compared to conventional loan. Fannie Mae now requires max DTI of 45% (back end). FHA can insure up to 45%(front)/55%(back) depending on AUS .

Max DTI doesn’t change even on High Balance loans (may go up to 45%/50% depending on AUS).

Family member can gift everything, including 3.5% down-payment requirement and ALL closing costs.

Down-Payment Assistant Programs (DAP)

FHA vs. Conventional

Seller can credit up to 6%** of ALL closing cost (recurring and non-recurring). That means seller can pay hazard insurance and tax impounds.

Non-occupying co-borrower transactions do not have separate LTV/DTI restrictions on the occupying borrowers. (Unless the borrower has no credit history)

Some Basic Credit Guidelines You May Want To

Know

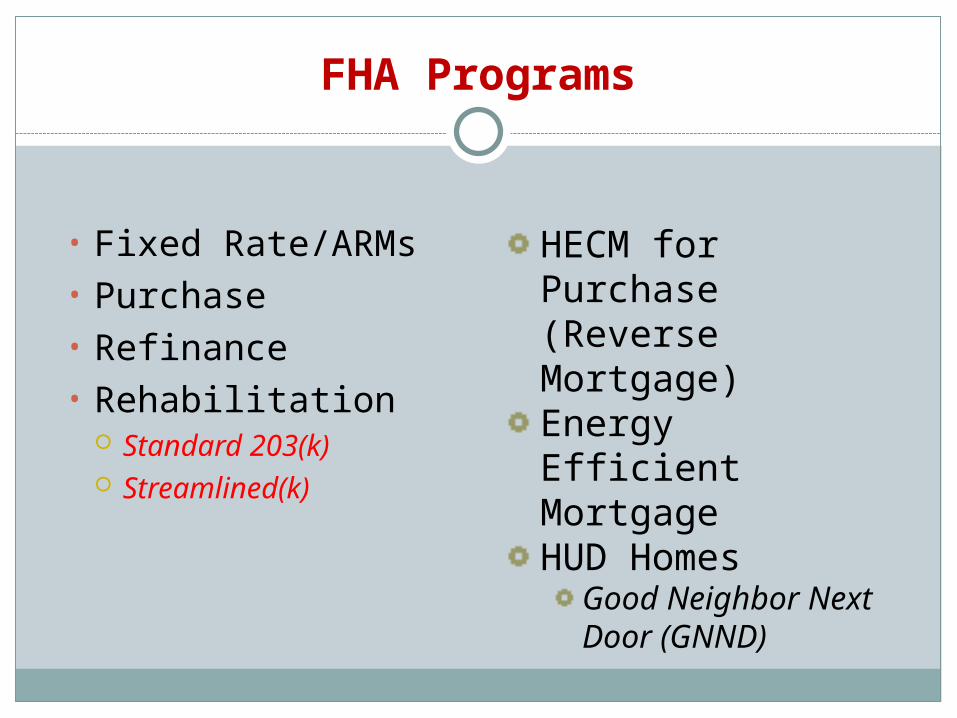

FHA Programs

• Fixed Rate/ARMs• Purchase• Refinance• Rehabilitation

Standard 203(k) Streamlined(k)

HECM for Purchase (Reverse Mortgage)Energy Efficient MortgageHUD Homes

Good Neighbor Next Door (GNND)

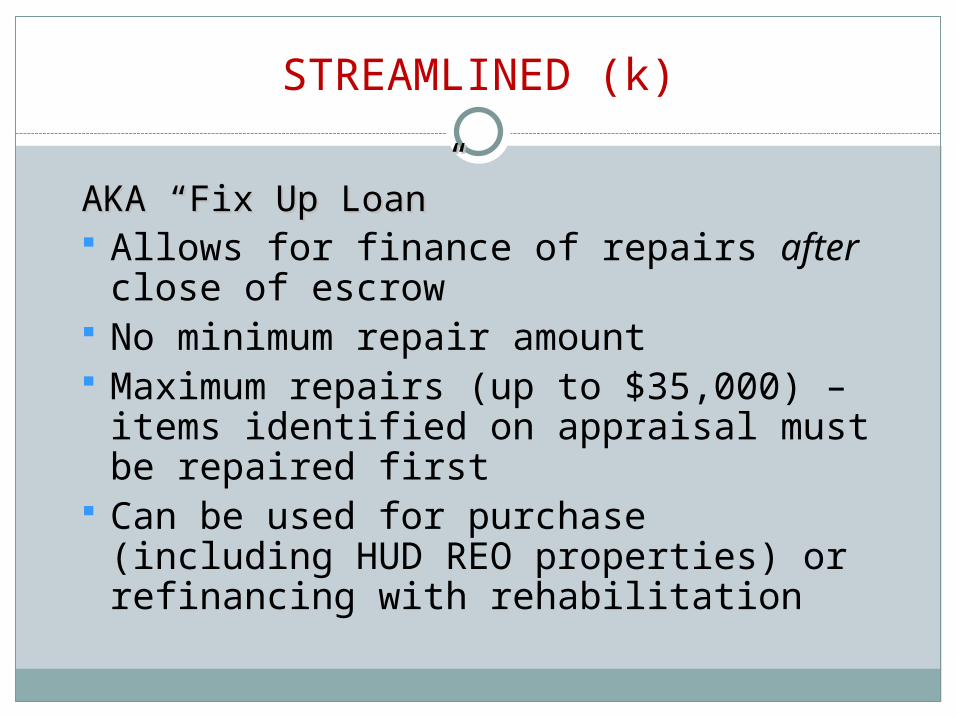

STREAMLINED (k)

AKA “Fix Up Loan”AKA “Fix Up Loan” Allows for finance of repairs after close

of escrow No minimum repair amount Maximum repairs (up to $35,000) –

items identified on appraisal must be repaired first

Can be used for purchase (including HUD REO properties) or refinancing with rehabilitation

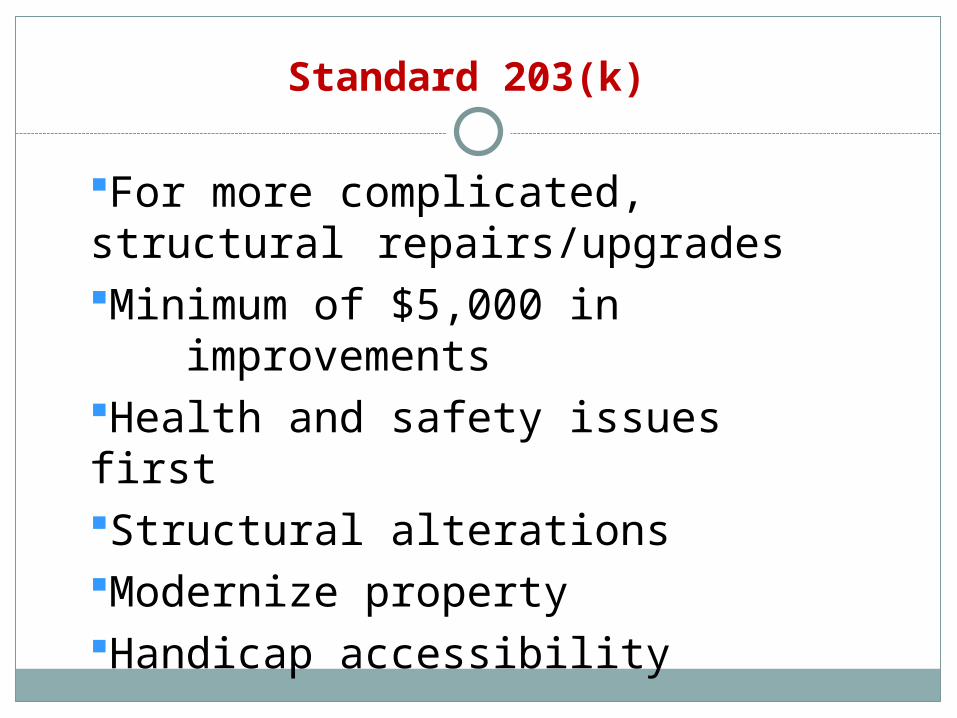

Standard 203(k)

For more complicated, structural repairs/upgradesMinimum of $5,000 in

improvementsHealth and safety issues firstStructural alterationsModernize propertyHandicap accessibility

Standard 203(k) – Cont.Standard 203(k) – Cont.

Up to 6 months mortgage payments can be financed as part of the mortgage

Lender escrows funds and pays to homeowner/contractor in up to 5 draws

Requires 203(k) consultant As repaired appraisal must support loan

amount for repaired property

Social Security Number Requirements

Borrower’s social security number will be verified & validated through FHAC - No T.I.N’s allowed.

Verify social security number on paystubs / W-2’s / 1040’s match.

Credit obtained must be under SSN that the Social Security Administration has on record for borrower

Employment

No time requirement for current job 2 year inclusive history required on 1003 Less than 2 years is acceptable if borrower

can document recently graduated student Acceptable explanations are required if

sporadic job history and changes in profession - must make sense - decision based on verifying capacity to repay

Probability of continued employment is very important

Recently returned to work - requires current job for 6 mos + and document min 2 year work history prior to the gap of employment

DOWNPAYMENT SOURCES

▪ Savings

▪ Secured funds

▪ Gifts - from relative or significant other

▪ Cash - if borrower meets profile

▪ Sale of personal property (must document value and sale)

▪ Sale proceeds

▪ 401K (use 60% of value)- must provide evidence the funds can be accessed.

▪ Investments

▪ Community Seconds

Bankruptcies

Chapter 7 Must document the BK was caused by extenuating

circumstances beyond the borrowers control and must document financial responsibility for exception if underwriter recommends approval Must be discharged for at least 2 years (AUS)

Chapter 13 Must be discharged for at least 2 years (AUS)

For both - Provide full BK docs and discharge papers.

Foreclosure & Del. Federal Debts

Foreclosure - must to be more than 3 years from end of foreclosure to date of application

Delinquent Federal Debts

Delinquent student loans and unpaid federal tax liens will be verified through FHA Connection

Borrower not eligible unless account is current, paid or otherwise satisfied prior to close of escrow

Liabilities

• Recurring obligations

• Revolving Credit

• Installment Debt - include student loans unless deferred > 12 mos

• Check the paystubs! Check for Credit Union payments, other payments not reflected on credit. Note: 401K payments are not counted as debt.

• Child Support/Alimony payments

• “Buy and Bail” policy in effect , similar to Agency. To use rental income on departure property requires minimum 25% equity evidenced by a FNMA appraisal (2055 for SFR, Full appraisal 1073 for condos)

• In community property states, any debt of the non-borrowing spouse must be included in debt ratio!!

Citizenship and Immigration Status

U.S. Citizenship not required

Lawful Permanent Resident Aliens are acceptable - document with copy of entire valid Resident Alien Card

Document evidence of permanent residency issued by Bureau of Citizenship and Immigration Services (BCIS)- part of Dept of Homeland Security

Non-permanent Resident Aliens acceptable with the following stipulations: property being purchased is the borrower’s principal residence. Will require:

* Valid Social Security number * Borrower must have Employment Authorization

Document issued by the BCIS * Temporary residency status that expires within one year AND there is a history of residency status renewals- assume the continuation will be granted

Eligible PropertiesEligible Properties

▪ 1-4 Units

▪ Townhouses

▪ FHA approved Condos

▪ PUDs

Required Disclosures and Forms

FHA Addendum & Real Estate Cert -(Amendatory Clause) signed at time of purchase contract by all borrower(s), seller(s), realtor(s).

92900A- FHA Addendum to Loan Application- Borrower(s) to sign page 2 at application- then sign page 4 at closing

Informed Consumer Choice - to be signed within 3 days of application

For Your Protection Get a Home Inspection (form 92564-CN)

Standard State and Federal required disclosures - signed & dated within compliance

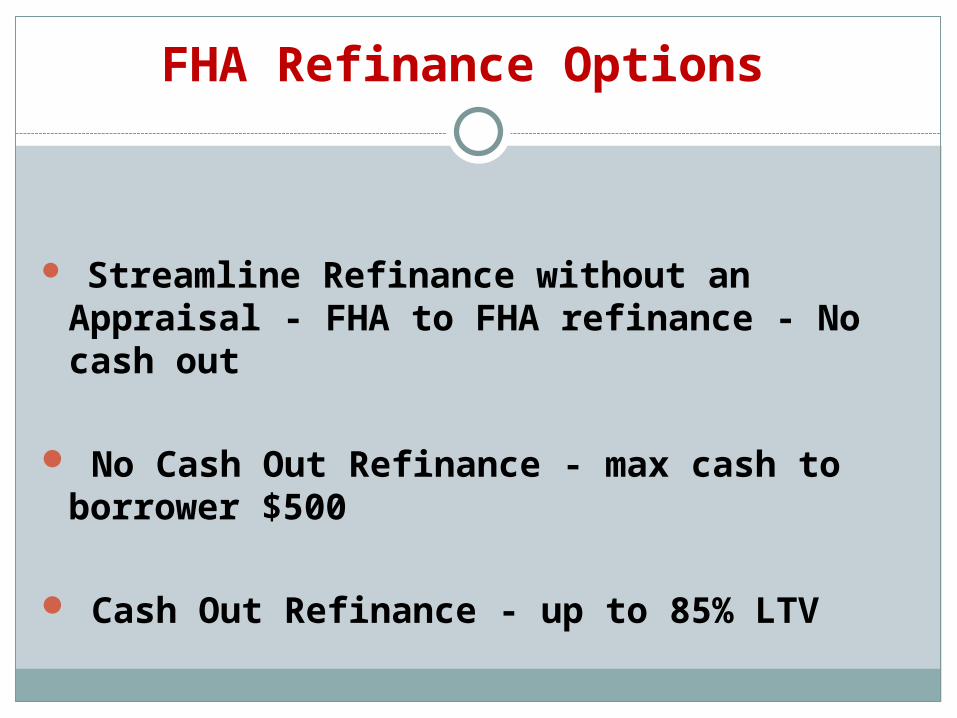

FHA Refinance Options

Streamline Refinance without an Appraisal - FHA to FHA refinance - No cash out

No Cash Out Refinance - max cash to borrower $500

Cash Out Refinance - up to 85% LTV

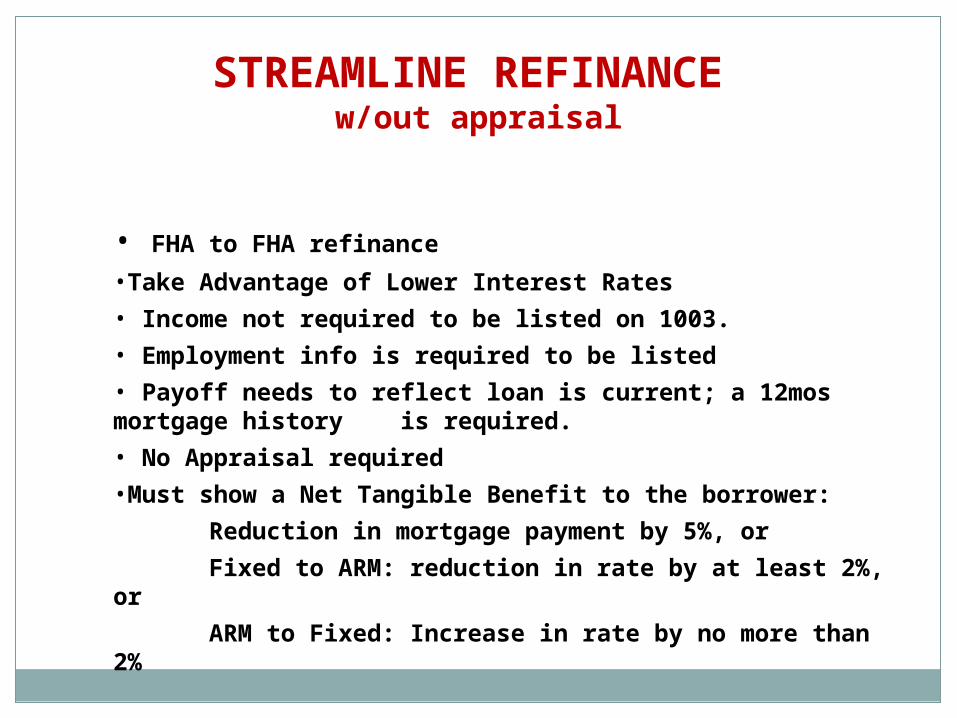

STREAMLINE REFINANCE w/out appraisal

• FHA to FHA refinance

•Take Advantage of Lower Interest Rates

• Income not required to be listed on 1003.

• Employment info is required to be listed

• Payoff needs to reflect loan is current; a 12mos mortgage history is required.

• No Appraisal required

•Must show a Net Tangible Benefit to the borrower:

Reduction in mortgage payment by 5%, or

Fixed to ARM: reduction in rate by at least 2%, or

ARM to Fixed: Increase in rate by no more than 2%

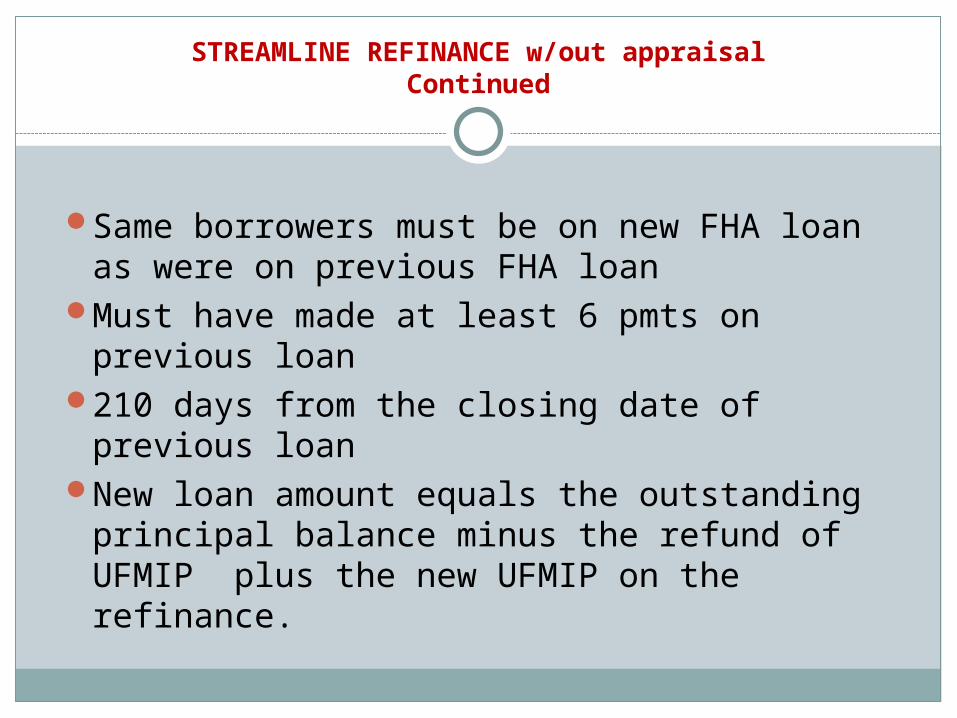

STREAMLINE REFINANCE w/out appraisalContinued

Same borrowers must be on new FHA loan as were on previous FHA loan

Must have made at least 6 pmts on previous loan

210 days from the closing date of previous loan

New loan amount equals the outstanding principal balance minus the refund of UFMIP plus the new UFMIP on the refinance.

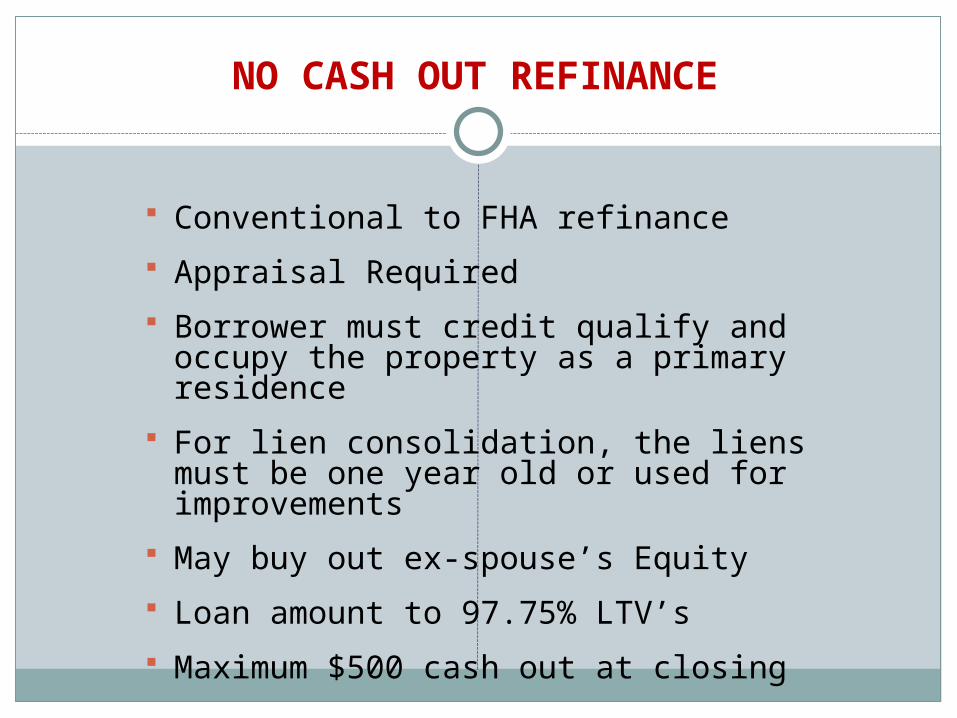

NO CASH OUT REFINANCE

Conventional to FHA refinance

Appraisal Required

Borrower must credit qualify and occupy the property as a primary residence

For lien consolidation, the liens must be one year old or used for improvements

May buy out ex-spouse’s Equity

Loan amount to 97.75% LTV’s

Maximum $500 cash out at closing

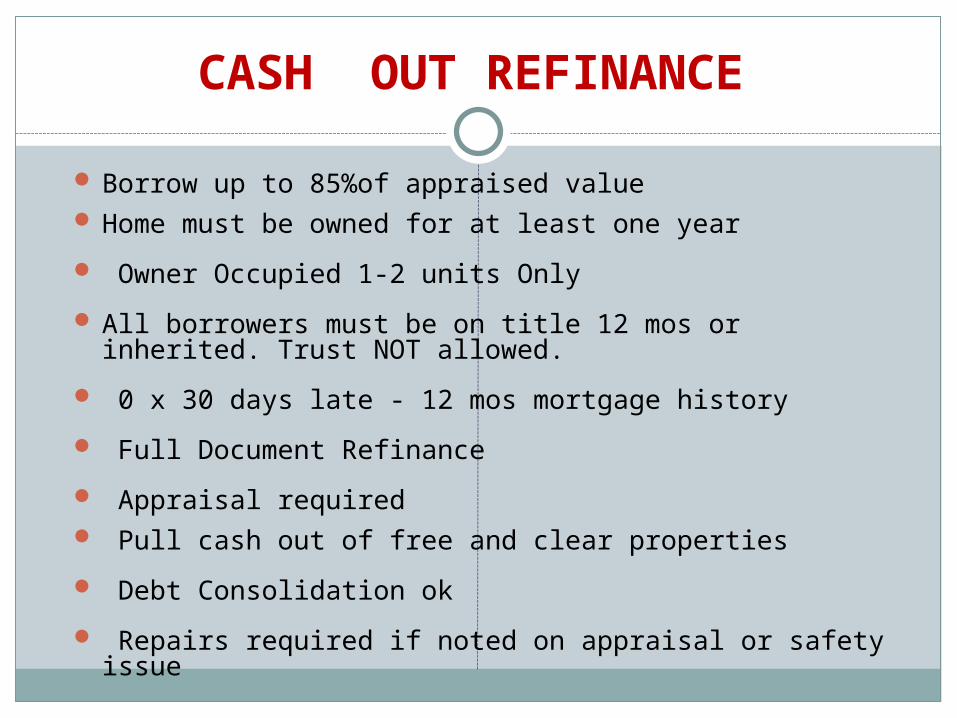

CASH OUT REFINANCE

Borrow up to 85%of appraised value Home must be owned for at least one year

Owner Occupied 1-2 units Only

All borrowers must be on title 12 mos or inherited. Trust NOT allowed.

0 x 30 days late - 12 mos mortgage history

Full Document Refinance

Appraisal required Pull cash out of free and clear properties

Debt Consolidation ok

Repairs required if noted on appraisal or safety issue

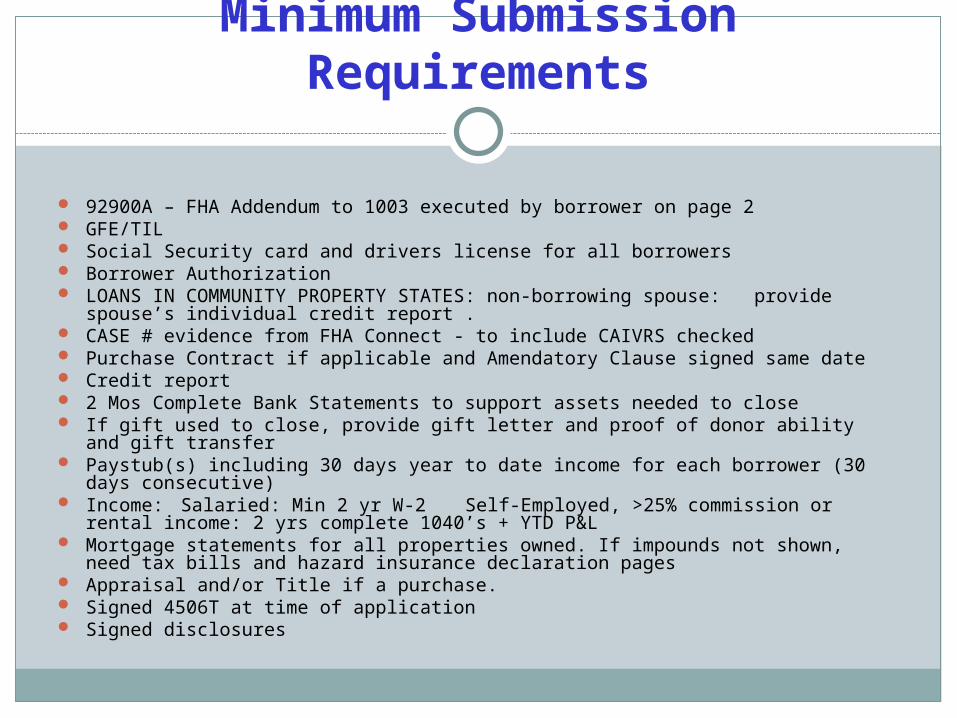

Minimum Submission Requirements

92900A – FHA Addendum to 1003 executed by borrower on page 2 GFE/TIL Social Security card and drivers license for all borrowers Borrower Authorization LOANS IN COMMUNITY PROPERTY STATES: non-borrowing spouse: provide

spouse’s individual credit report . CASE # evidence from FHA Connect - to include CAIVRS checked Purchase Contract if applicable and Amendatory Clause signed same date Credit report 2 Mos Complete Bank Statements to support assets needed to close If gift used to close, provide gift letter and proof of donor ability and gift transfer Paystub(s) including 30 days year to date income for each borrower (30 days

consecutive) Income:

Salaried: Min 2 yr W-2Self-Employed, >25% commission or rental income: 2 yrs complete 1040’s

+ YTD P&L Mortgage statements for all properties owned. If impounds not shown, need tax bills

and hazard insurance declaration pages Appraisal and/or Title if a purchase. Signed 4506T at time of application Signed disclosures

Mortgage Insurance

All FHA loans have mortgage insuranceFHA loan approval also approves the

insurance. No separate approval required.Insurance is paid both up front (UFMIP) and

monthly (MIP).Insurance is in effect until LTV reaches 78%

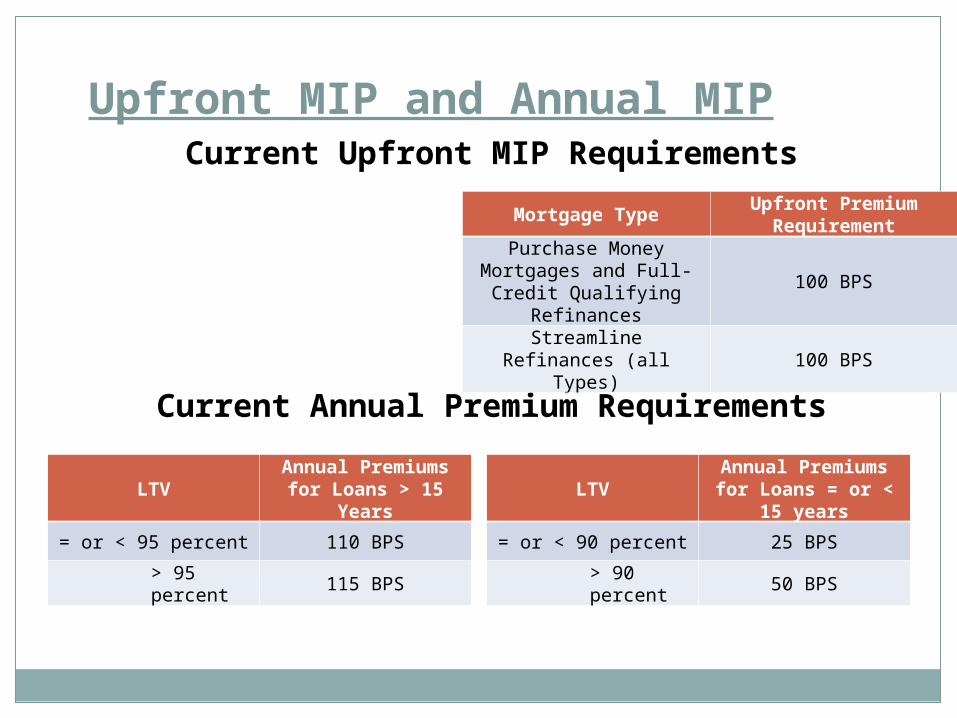

Upfront MIP and Annual MIPCurrent Upfront MIP Requirements

Current Annual Premium Requirements

Mortgage TypeUpfront Premium

RequirementPurchase Money Mortgages and Full-Credit Qualifying

Refinances100 BPS

Streamline Refinances (all Types)

100 BPS

LTVAnnual Premiums for Loans = or < 15 years

= or < 90 percent 25 BPS

> 90 percent 50 BPS

LTVAnnual Premiums for

Loans > 15 Years

= or < 95 percent 110 BPS

> 95 percent 115 BPS

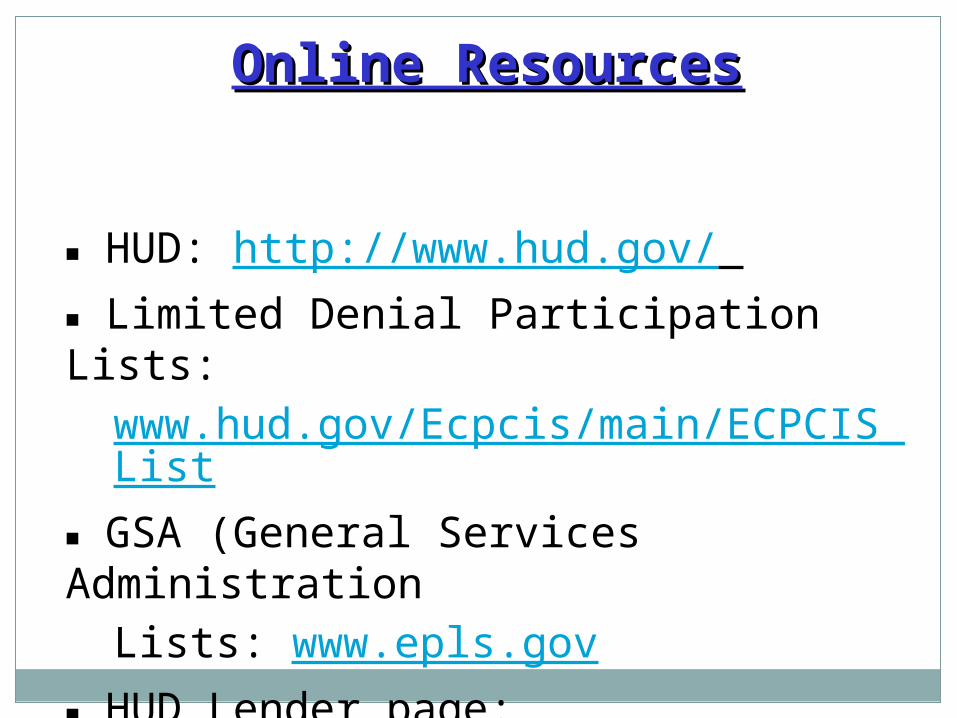

Online ResourcesOnline Resources

■ HUD: http://www.hud.gov/ ■ Limited Denial Participation Lists:

www.hud.gov/Ecpcis/main/ECPCIS_List

■ GSA (General Services AdministrationLists: www.epls.gov

■ HUD Lender page:www.hud.gov/groups/lenders.cfm

Recommended